IRDA 474 Qset 15th Nov 11

123

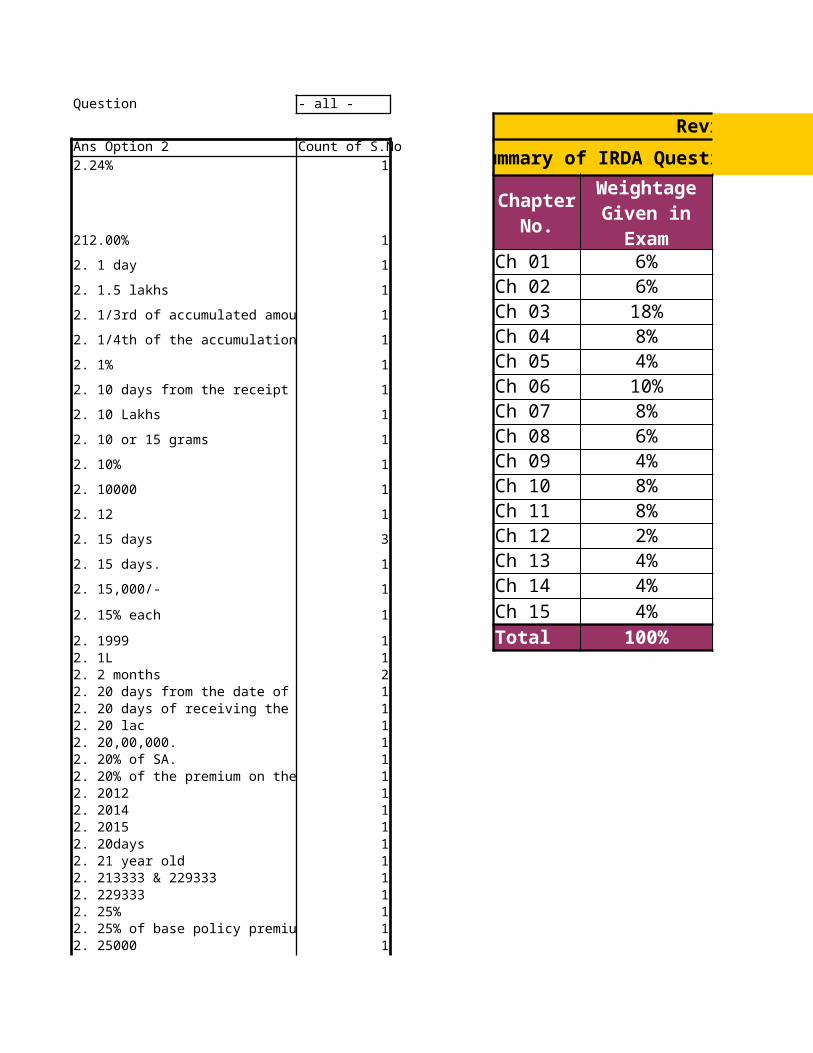

Question - all - Revi Ans Option 2 Count of S.No ummary of IRDA Questi 2.24% 1 212.00% 1 2. 1 day 1 Ch 01 6% 2. 1.5 lakhs 1 Ch 02 6% 2. 1/3rd of accumulated amou 1 Ch 03 18% 2. 1/4th of the accumulation 1 Ch 04 8% 2. 1% 1 Ch 05 4% 2. 10 days from the receipt 1 Ch 06 10% 2. 10 Lakhs 1 Ch 07 8% 2. 10 or 15 grams 1 Ch 08 6% 2. 10% 1 Ch 09 4% 2. 10000 1 Ch 10 8% 2. 12 1 Ch 11 8% 2. 15 days 3 Ch 12 2% 2. 15 days. 1 Ch 13 4% 2. 15,000/- 1 Ch 14 4% 2. 15% each 1 Ch 15 4% 2. 1999 1 Total 100% 2. 1L 1 2. 2 months 2 2. 20 days from the date of 1 2. 20 days of receiving the 1 2. 20 lac 1 2. 20,00,000. 1 2. 20% of SA. 1 2. 20% of the premium on the 1 2. 2012 1 2. 2014 1 2. 2015 1 2. 20days 1 2. 21 year old 1 2. 213333 & 229333 1 2. 229333 1 2. 25% 1 2. 25% of base policy premiu 1 2. 25000 1 Chapter No. Weightage Given in Exam

-

Upload

nithyananda-patel -

Category

Documents

-

view

220 -

download

1

description

hii

Transcript of IRDA 474 Qset 15th Nov 11

Question - all -

Revised IC 33 QuestionsAns Option 2 Count of S.No Summary of IRDA Question Set contributed by Regulatory Team2.24% 1

212.00% 1

2. 1 day 1 Ch 01 6%2. 1.5 lakhs 1 Ch 02 6%2. 1/3rd of accumulated amount. 1 Ch 03 18%2. 1/4th of the accumulation fund 1 Ch 04 8%2. 1% 1 Ch 05 4%2. 10 days from the receipt 1 Ch 06 10%2. 10 Lakhs 1 Ch 07 8%2. 10 or 15 grams 1 Ch 08 6%2. 10% 1 Ch 09 4%2. 10000 1 Ch 10 8%2. 12 1 Ch 11 8%2. 15 days 3 Ch 12 2%2. 15 days. 1 Ch 13 4%2. 15,000/- 1 Ch 14 4%2. 15% each 1 Ch 15 4%2. 1999 1 Total 100%2. 1L 12. 2 months 22. 20 days from the date of receipt 12. 20 days of receiving the proposa 12. 20 lac 12. 20,00,000. 12. 20% of SA. 12. 20% of the premium on the base 12. 2012 12. 2014 12. 2015 12. 20days 12. 21 year old 12. 213333 & 229333 12. 229333 12. 25% 12. 25% of base policy premium 12. 25000 1

Chapter No.

Weightage Given in Exam

2. 26% 12. 3 lacs 22. 3.0% 12. 30 Days 12. 30 Days 12. 30 lakhs 12. 35% 12. 5 years 12. 50,000 12. 50% 12. 50% of basic premium. 22. 500000 12. 6 years 12. 75000 12. 8320 12. 90 days 12. 9320 12. A demand to fulfill the insurer’s o 12. A Lien 12. a person working in a chemical f 12. A policy document has been stam 12. a term life policy 12. Accumulation Phase 12. Advisor confidential report 12. Advisor Confidential Sheet 12. Advisors confidential report 12. After the fact finding process 12. Age of both the candidate are dif 12. Agents 12. All death claims 12. All similar risks are pooled toget 12. All types of insurance except Mo 12. An Identity Proof 12. an impression of the left thumb is 12. Annuity part 12. Annuity Plan 12. annuity will be continued for nex 12. Assignment. 12. At an early age 12. At the time of a claim 12. At the time of claim 12. Attestation 12. Audit by Finance Ministry 12. B. Moral hazard, as he is 52 yea 12. B.A legal person to act on behalf 12. B.KYC document 12. bad 12. bancassurance 12. Bancassurance. 12. Bank fixed deposits. 1

2. Banks 12. Behavior that is based upon the 12. Benefit illustration documents 12. Benefit illustration of unit linked 12. Bombay Stock exchange 12. Both life insurance 12. Brochure 12. Capacity to contract 12. Capacity to pay the premiums in 12. Capital Profit 12. Captial Appreciation 12. Certificate of Baptism 12. Charges 12. Child Plan 12. Churning 12. Churning. 12. CI benefit reduced from existing 12. Claim experiences. 12. claim of hospital charge Rs 20,00 12. Claim will be settled as Cancer 12. Classification of Risk Departmen 12. Client’s Expense statement 12. clients personal problems 12. Compound Revisionary bonus 12. Concealment of a material fact 12. Conditional and Absolute Assign 12. Conditional Assignment 12. Consulting the client’s parents 12. Consumer Forum 12. Consumer insurance council 12. Contract comes to an end. 12. Control 12. Convertible plan 22. Convertible Term plan 12. Converting the policy to Paid up 12. COPA 12. Corporate agent 12. Critical illness (CI) 12. Current assets. 12. Customer Grievance Departmen 12. Date of commencement of last 12. death is uncertain 12. Decrease 22. Decreases 12. Denny and his wife 12. Designated Person. 12. District Level 12. Doing a financial planning 12. Domicile status 12. Early death claim 1

2. economic values of assets 12. employee-employer 12. Employees 12. Employer & Employee 12. Endorsements 12. Endowment plan 22. Endowment plan. 12. Entire charges less bed charges w 12. Equal to base cover 12. Equity Linked Saving Schemes. 12. Every individual’s income and exp 12. Facts of law 12. Family floater 12. Family health insurance plan 12. Financial risk 12. Find out the reasons for refusal 12. First Premium Receipt is issued. 12. First Two years of policy 12. Five years. 12. Fixed income 12. Flexibility of Premium payment t 12. Fluctuating income 12. Fraudulent 12. Fraudulent misrepresentation. 12. Fraudulent representation 12. Gathering client data 12. Give a joint decision with the c 12. Grievance call center 12. Group Insurance 12. Habits and Hobbies of Proposer. 12. Has the power to supersede the I 12. Hazard 12. Hazard 12. He can file a complaint against 12. He can surrender whole life poli 12. He can take Business Partner in 12. He has breached the company by 12. He has opted for Settlement opti 12. He will get tax benefit up to 25% 12. High client satisfaction 12. Higher profits 12. His future aspiration 12. Hospitalization Care Rider 12. Husband and Wife only 12. husband-wife 12. Identify only the client’s needs. 12. Identify, Quantify & Prioritize Ne 12. If the agent has worked with th 12. If the policy has lapsed and it ha 12. Imagined to be important by Advi 1

2. Increase in Sum Assured next ye 12. Increase in the agents earning 12. Increase in the range 12. Increase the profitability 12. Indemnity 12. Indemnity contract. 12. Indian Contract Act 12. Indisputability clause 12. Individuals have same financial ne 12. Inflation 12. Inflation only. 12. Infrastructure Bond 12. Insist with the client to take a te 12. Insurance 12. Insurance agent 12. Insurance broker is represents 12. Insurance Company 32. Insurance Company and IRDA 12. Insurance Council 12. insurance institute of India 12. Insurance is taken out by an ind 12. Insurance should not taken by hi 12. Insured 12. Interact with the government 12. Interest Benefit and Bonus Benefi 12. Interest. 12. Internal Grievance Redressal Cell 12. Invalid 22. Investment 12. Investment and Protection 12. IRDA 42. IRDA Acts code of conduct. 12. IRDA claim protection regulation 12. It falls 12. It was paid up. 22. Keyman Insurance 12. Lack of insurable interest 12. Legal heir of life Assured 12. Legal heir of the life assured 12. Legality of an object. 12. Legality of object or purpose 12. Less renewal income. 12. Level 12. Level Premium 12. Life and General (non-life) Insur 12. life annuity 22. Life Insurance 12. Life Insurance Company 12. Life Insurance Corporation 22. Life, Non Life, Miscellaneous 1

2. Likely to decrease. 12. Listening skills. 12. low 12. Low Returns 12. Low Risk. 12. Lump Sum with no fixed term 12. Main Underwriter 12. Maintaining insurable interest 12. Major Double Rupees Tag 12. Major Possible Loss. 12. Making false insurance claims. 12. Marriage 12. Married Man 12. Matching the product with Rames 12. Maturity benefit 12. Medical examinations 12. Middle class. 12. Money Back Plan. 12. Moral 12. Moral Hazard 32. Moral peril. 12. More gold in value 12. More than 10000 12. Mortality. 12. Mr. Shanth can take loan which s 12. Mr. Shanth cannot renew the pol 12. Mutual fund 12. Mutual Fund Management Syste 12. National Insurance Academy. 12. Necessary to pay premium until 12. Need to add that hospital as TPA 12. Need to complete 50 hours of pra 12. need to disclose the amount of 12. Net Premium. 12. Nishu has to sign an indemnity b 12. No, customers needs are differen 12. Nomination can be done either at 12. Nomination transfers the title wh 12. Not a specific plan 12. Not eligible for Claim settlement 12. Not needed 12. Not Possible 12. Not possible as life has many risk 12. Not standard but accept 12. Number of days admitted in hospi 12. Number of premiums payable. 12. One party makes an offer which t 12. Only by non life 12. Only half of the fund can be wit 12. Only lung is affected so health i 1

2. Only Maturity Benefit. 12. only proposer 12. Only self and spouse can be cove 12. Open Ended Questions. 12. Open Market 12. Opertaive Clause 12. Opportunity of new business for 12. Paraplegia 12. Particular Risk. 12. Particular. 12. past data 12. Perceived need 12. Perils are risks that policyholder 12. Person receives an amount equal 12. Physical 12. physical hazard 12. Placement 12. Policy holder 12. Policy will be surrendered by th 12. Policyholder’s Protection regulat 12. Pooling of Risk 12. Post retirement stage 12. Pre- retirement 12. Preamble. 12. Premium cheque and health decl 12. Present value of future earnings. 12. Principle amount 12. Priorities Clients Need 12. Private sector employees 12. Product – Based Selling 12. Product Design. 12. Proof of identity 12. Proposal form. 12. Proposing 12. Provide Benefit illustration docum 12. Proviso of policy. 12. Public Provident Fund 12. Purchasing House 12. Quarterly 12. Raghav will be terminated 12. Real needs are actual needs and 12. recommend to wait some days to 12. Recurring deposits 12. Redressal 12. Reduction in costs 12. Regular Income 12. Renewal Commission. 12. renewal receipt 12. Representation of facts by the pol 12. Representatives from all govern 1

2. Reputation of the company will b 12. Reserve bank of India 12. Reserve Bank of India. 12. reviewed 12. Reviewing financial needs and p 12. revival 12. rider is like a clause 12. Risk avoid 12. Risk Diversified Insurance 12. Risk Grading 12. Risk of death 12. Risk premium plus interest earni 12. Risk transfer 12. ROP plan 12. Rs. 1, 10,000 12. Rs. 24000 per month 12. Rs. 25000/- 12. Rs. 4, 50,000/- 12. Rs. 50,000 12. Rs.25000 12. Same for all policies sold by the 12. Satish should outline the reasons 12. Savings 12. Savings. 12. Schedule 12. SEBI 12. Section 42 of the insurance act 12. Section 42 of the Insurance Act 12. Selling insurance policies throu 12. Selling what adviser wish to sell. 12. Semi Annually 12. Shailesh’s income is more than A 12. shareholders 12. Shares 12. Shares will be less attractive. 12. Should ask for reference who migh 12. Should ask for the reason for n 12. Smoking is a hazard and lung can 12. Some percentage of the expense 12. Specialized inspection agencies 12. Specified amount multiplied by t 12. Speculative risk 12. Standard Age proof 12. Suggest an alternative plan 12. Sum Assured 12. Surrendering the policy 12. Tables of details of various proba 12. Taking Health Plan, Insurance Pl 12. Tariff Advisory Committee 12. Tax planning need. 1

2. Taxation 12. Term 12. Term Plan 22. Term Plan with return of premiu 12. the amount that can be paid tow 12. The assignor need not be major a 12. The beneficiaries. 12. The client represent the broker 12. The company is acquiring more 12. The financial history of his family 12. the higher 12. The insurable interest between th 12. The insurance company makes enq 12. The insurance company may pay an 12. The nominee makes a demand. 12. The policy may be pledged. 12. The premium remains constant wi 12. the process is initiated by the c 12. the risk associated might decrea 12. The risk retained person 's family 12. This condition is excluded in the 12. This plan is ideal for brother & sis 12. This rider is ideal for helping t 12. Those Insurer who did not cre 12. through internet 12. To be an active link between Glo 12. to his nominee 12. To purchase a health plan along 12. Top Level 12. Total 4 lakhs will be paid as de 12. Total Protection Policies. 12. Transfer 12. Two persons 12. Two years 12. ULIP 12. Under conditions of the reinsurer 12. Under selling of Insurance policie 12. Under the category of peril risk 12. Understand about company 12. Underwriter 12. unethical 12. Unit linked Insurance plans 12. Up to 99990 12. Using different pool for paying cl 12. Value contract. 12. Vishal is older than Sandeep 12. When a client is holding a produ 12. When both the life partners are 12. When cheque amount is deposited 12. when he survives the term 1

2. When Mr. Ranga is diagnosed a cr 12. When the client’s needs have be 12. Will be considered as non stand 12. X with wife 12. Yearly 12. Yes, as it is within 1 year 12. Young married 12. Young married with children. 12.1/2th of Accumulated Fund 12.20 Days 12.Bank 12.Cumlative deposit 12.Family floater Insurance Plan [email protected] 12.Principal of Indemnity apply 12.Return of Premium on maturity 12.Sum Assured + Bonus 1(empty) 1Total Result 474

Revised IC 33 Questions

Summary of IRDA Question Set contributed by Regulatory Team

3 223 299 634 492 425 314 573 292 194 164 321 172 232 262 19

50 474

Questions/chapter Expected

Questions Available in Qbank

Question Ans Option 1 Ans Option 2 Ans Option 3 Ans Option 4

Ch 2 2

Ch 8 2

Ch 8 1. Young unmarr 2. Young marr 3. Young married 4. Pre retirem 4

Ch 2 1. Regulation 2. Redressal 3. Research 4. Repository 3

Ch 10 2

Correct option

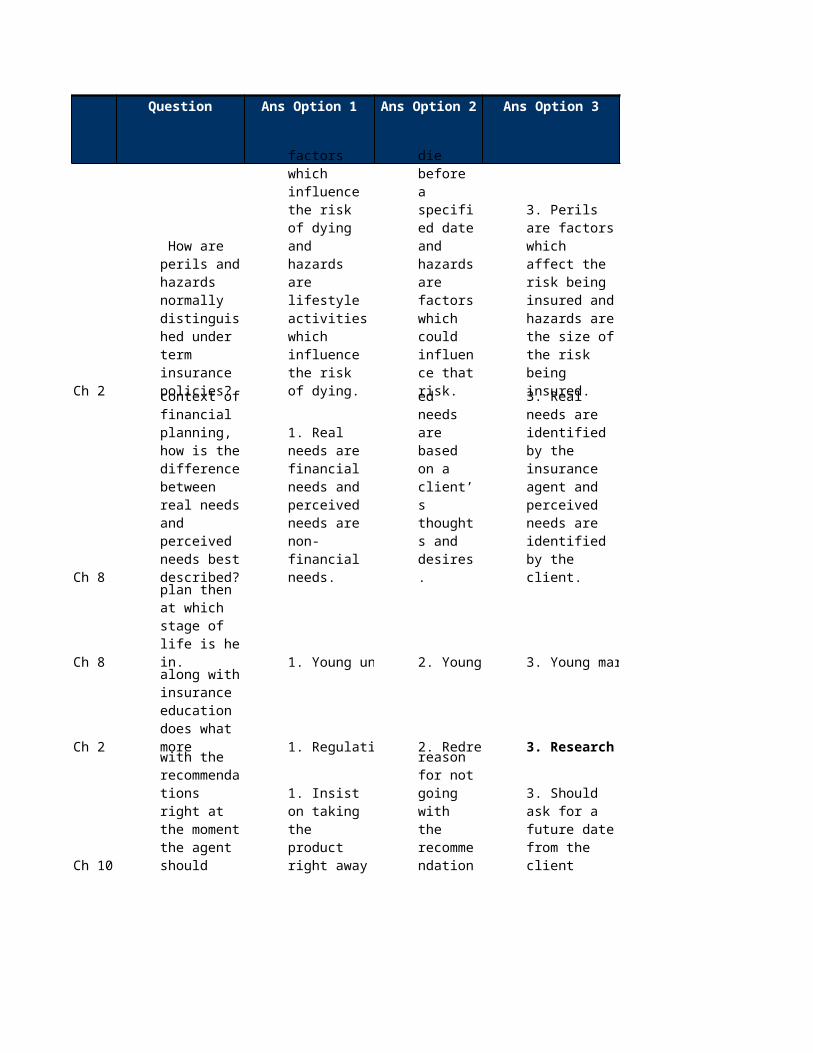

How are perils and hazards normally distinguished under term insurance policies?

1. Perils are medical factors which influence the risk of dying and hazards are lifestyle activities which influence the risk of dying.

2. Perils are risks that policyholders will die before a specified date and hazards are factors which could influence that risk.

3. Perils are factors which affect the risk being insured and hazards are the size of the risk being insured.

4. Perils are factors which could influence an insured event occurring and hazards are the actual events which will trigger a payout

In the context of financial planning, how is the difference between real needs and perceived needs best described?

1. Real needs are financial needs and perceived needs are non-financial needs.

2. Real needs are actual needs and perceived needs are based on a client’s thoughts and desires.

3. Real needs are identified by the insurance agent and perceived needs are identified by the client.

4. Real needs are needs which satisfy an objective and perceived needs are needs which do not satisfy an objective.more on health

plan and retirement plan then at which stage of life is he in.and risk management along with insurance education does what more If the client does not wish to proceed with the recommendations right at the moment the agent should

1. Insist on taking the product right away

2. Should ask for the reason for not going with the recommendation

3. Should ask for a future date from the client

4. Should review once again

Ch 8 4. Pension plan 3

Ch 11 3. It was lost. 3

Ch 11 1. It was lost. 3. It was lapsed. 1

Ch 8 1. Marriage. 2. Savings. 3. Education. 4. Protection. 1

Ch 4 1. Inflation. 2. Interest. 3. Discount rate 3

Ch 6 2

Ch 4 2

Ch 9 1

moreover he feels that if he does not die then he would need the amount. What type of plan should he opt for?

1. Term Insurance Plan

2. Endowment plan

3. Return of premium plan

paid in a policy and it was advertised in the newspaper also. This indicates that the policy was.

1. It was assigned.

2. It was paid up.

4. It was surrendered.signed in a

policy when the claim was paid. This indicates that the policy was.

2. It was paid up.

4. It was surrendered.

They want to plan for savings, child education/marriage and their retirement and protection of income. Which should be their lowest priority?no of years of work, increments in salary what is also to be taken in to account?

4. Compounding.interest rates

then what will be the effect on share prices.

1. Shares will be more attractive.

2. Shares will be less attractive.

3. Fixed deposits will be more attractive.

4. Fixed deposits will be less attractive.

Company. Vishal is asked to undergo a medical checkup but Sandeep is not asked to do so. What will be most possible reason?

1. Sandeep has taken another policy from XYZ Life Insurance Company

2. Vishal is older than Sandeep

3. Sandeep is earning more then Vishal

4. Vishal is working in a MNCwill be the next

step after Identifying clients need

1. Quantify clients need

2. Priorities Clients Need

3. Recommending Product

4. Fill up the proposal form

Ch 6 1. Easy access 3. Tax Benefits 4. Liquidity 4

ch 3 1. 213333 2. 229333 3. 273333 4. 293333 3

Ch 6 1. Guarantees 2. Taxation 3. Tenure 1

Ch 8 1. Savings 2. Insurance 3

Ch 2 3. Moral hazard 4. Peril 1

Ch 11 3. Fraud 1

Ch 2 4. Randomness 1

Ch 1 3. Bank 4. Broker 4

Ch 6 2. ULIP 4. FD 3

purpose of investing money in debt mutual fund?

2. Fixed income

years. The sum assured Rs.8,00,000/- and accumulated bonus Rs.60,000/-. What is the paid up value? Recurring Deposits & cumulative deposits in a bank

4. Lock in periodsher husband’s

death. In such a situation what will be her prime focus?

3. Investment management

4. Planning for pension

While taking up the Insurance policy he disclosed this information. What kind of hazard does it refers to

1. Physical hazard

2. Fraudulent representation Which of the

following falls under voidable contract?

1. Misrepresentation

2. Lack of insurable interest

4. None of the above Law of large

numbers is worked out by which of the following?

1. Pooling of risk

2. Maintaining insurable interest

3. With utmost good faithbetween all

financial products then the best person he can approach is

1. Individual agent

2. Corporate agentmaintain

emergency funds the best place is a bank or

1. Equity market

3. Debt mutual fund

Ch 9 3

Ch 12 3

Ch 3 1. It rises 2. It falls 3

Ch 6 1. Liquidity 3. Purity 1

Ch 4 3. SA is too high 4. Pure Risk 3

Ch 15 1

Ch 11 2

and children’s education. But the customer insists on only a child plan for the time being and asks the agent to give him a child plan. The agent should.

1. Do the fact finding exercise again

2. Insist with the client to take a term plan

3. Give a child plan and revisit the client on a later date

4. Give the lead to another agent

If a case is already before the consumer forum, then the ombudsman should

1. Give a recommendation

2. Give a joint decision with the consumer forum

3. Dismiss the case

4. Give an award.same, what will

be impact of net premium if the age of the policyholder increases

3. It remains constant

4. Gross premiums increasesconverting

physical gold assets to gold ETFs.

2. More gold in value

4. More conversion valueunderwriter

should ask beyond agent’s confidential report.

1. Physical Hazard

2. Moral Hazard

TROP product. But the client refused. According to ethical business practices what will the agent do ?

1. Enquire about the refusal from the client

2. Suggest an alternative plan

3. Pass on to the superior

4. Pass on to the other agent

or misrepresentation. However, due to which of the following circumstances the insurer can retain the premium of the policyholder

1. Fraudulent claim

2. Indisputability clause

3. Redressal procedure

4. Pending decision from Ombudsman

Ch 15 2. Brochure 1

Ch 2 1

Ch 3 1

Ch 7 2

Ch 14 1

Ch 6 2. Decrease 3. Increase 2

is the best method of showing the amount of commission earned by the advisor

1. Signed copy of sales illustration

3.Hand written declaration by agent

4.Verbal communication to customer

insure them against similar risks. At what circumstances will the insurance companies pool the risk of a life insurance and health insurance together?

1. Under no circumstances

2. Under conditions of the reinsurer

3. As directed by actuary

4. As per company policy

the policy. What are the two most important things required in order to reinstate the policy?

1. Reinstatement Fee and Proof of continuing good health

2. Premium cheque and health declaration

3. Only health certificate

4. Premium cheque with arrears

pension plan from company A and buys an annuity from company B, what is the nature of transaction?

1. Life Long Annuity

2. Open Market

3. Reinsuring Annuity

4. deferred Annuity

If a policy holder buys a policy from the advisor and lodges a complaint, it should be treated as :

1. Same for all policies sold by advisor

2. Same for all policies sold by the advisor except corporate clients

3.Only for policy for which complaint has been given

4.None applicable

of India announces a series of significant interest rate increases, the prices of these shares are most likely to

1. Become volatile

4. Remain unchanged

Ch 1 1

Ch 3 1. expired 2. reviewed 3. Void 4. Valid 4

Ch 4 4

Ch 6 1

Ch 5 1

Ch 2 2

Ch 5 4

Ch 7 2

calculating premium rates of insurance products, then he is mostly likely a member of

1. institutes of actuaries of India

2. insurance institute of India

3. Charted institute of insurance

4. Insurance institute of risk managementfound that the

person doesn’t have insurable interest then the contract is died in their thirties due to heart attack what is the kind of peril or hazard the proposer has?

1. Insurable hazard

2. moral hazard

3. non insurable hazard

4. Physical hazard

500000. What will be the maximum amount of EMI that can be charged by the Bank to recover the loan amount?

1. Rs. 32000 per month

2. Rs. 24000 per month

3. Rs. 40000 per month

4. Rs. 48000 per monthadvisable in

ULIP plan because it increase

1. Investment Risk

2. Risk of death

3. Uncertainty of return

4. Chances of lapse

According to insurance terminology which of the following is correct?

1. Lung cancer is a hazard whereas smoking is a peril

2. Smoking is a hazard and lung cancer is a peril

3. Lung cancer is a peril and smoking is a moral hazard

4. Smoking is a moral hazard whereas lung cancer is a peril.

policy term. He declares the commission to each of them. The commission of one of the policy is more than the other. What should be the reasons for this difference?

1. Risk profile of both the policyholder are different

2. Age of both the candidate are different

3. One has chosen Single premium policy and other has chosen regular premium policy

4. Both have chosen different kind of policies.Annuity policy

would extend which of the following benefit?

1. Ensure Better annuity rate

2. Increase in the range

3. Increase in return

4. Switch of Funds

Ch 9 1. Money Back 2. Term Plan 4. ULIP 4

Ch 9 1. Fact finding 1

Ch 3 3Ch 2

ch 3 2

ch 3 2

ch 3 4. Acceptance. 3

Ch 6 1

Ch 7 3

Ch 7 3

and drawing a handsome salary. He has no liabilities. What kind of plan can be suggested to him?

3. Endowment Plan

understand the mental state of client in respect to his investments in saving products

2. Consulting the client’s parents

3. Consulting the family of the client

4. Reviewing his existing investments

Net premium is equal to

1. Premium plus interest earning

2. Risk premium plus interest earning

3. Premium minus interest earning

4. Risk premium minus interest earning

Pooling of risk in insurance means

1. The premium collected & deposited in a pool

2. All similar risks are pooled together

3. Premium is pool to make claims

4. Contribution of insurance company

Principle of utmost good faith will operate in existing policy

1. Every time premium is paid

2. If the policy has lapsed and it has to be revived.

3. If the insured person falls sick and is admitted to hospital.

4. If the insured person changes his job.agree and

understand the same thing and in the same sense which is called

1. Consideration.

2. Legality of an object.

3. Consensus ad idem.insurance,

Insurable interest must exist

1. At inception of policy

2. Not needed

3. At the time of claim

4. Any time during the contractbank pays the

principal and the total interest at the end of the term.

1. Traditional deposits

2. Recurring deposits

3. Cumulative deposits

4. Term Deposits

The Premium on all riders put together should not exceed

1. 10% of the premium on the base policy

2. 20% of the premium on the base policy

3. 30% of the premium on the base policy

4. 40% of the premium on the base policy

Ch 7 1

Ch 7 1

Ch 7 1

Ch 7 3. till he die 2

ch 1 1

Ch 2 1. Tax benefit 2. Savings 3. Investment 4. Protection 4

Ch 5 1. Moral 2. Physical 3.Ethical 2

Ch 14 1

How riders will help the customer in life insurance?

1. allows policyholders to customize their insurance cover with additional benefits

2. rider is like a clause

3. Operative clause.

4. Rider is like Preamble.

In Daily hospitalization cash benefit scheme,

1. The daily amount paid is fixed and will never be more or less than the cost of actual treatment.

2. The insurance company may pay an additional amount on a daily basis if the insured is admitted to the Intensive Care Unit (ICU).

3. The insurance company will pay for doctor consultation fees incurred prior to hospitalization

4. Only surgery expenses are included in daily hospitalization benefit

withdrawal allowed as commutation in pension plans is

1. 1/3rd of the accumulation fund

2. 1/4th of the accumulation fund

3. 1/2nd of the accumulation fund

4. Full withdrawal is allowed

happen to annuity, if the customer survives for 5 years after the end of guarantee period?

1. paid up to 75 Yrs

2. annuity will be continued for next 5 Years

4. not remembered

In term insurance if Critical illness rider claim happens then what will happen to existing policy

1. CI benefit will cease

2. CI benefit reduced from existing sum assured

3. CI benefit continues

4. No change in policy.main objective

of taking the life insurance policy?consumes alcohol- what is the type of hazard?

4.Ethical & Moral bothInsurance can

be taken in following relationship

1. employee- employer

2. husband-wife

3. family members

4. society members

Ch 8 1. IRDA 3. Distric Forum 2

Ch 3 1. Young 3. Retirement 4. children 2

Ch 5 1. 2.5% 2. 3.0% 3. 5.0% 4. 7.5% 3

Ch 4 1. 1 lacs 2. 3 lacs 3. 2 lacs 4. 1.50 lacs 2

Ch 7 1

Ch 11 3. Parents only 1

Ch 7 1. 30 days 2. 90 days 3. 120 days 4. 180 days 4

Ch 13 3

Ch 11 1. IRDA 2. SEBI 3. RBI 4. SBI 3

Ch 12 3. Claim 2

Where one can approach in case of dispute?

2. Consumer Forum

4. National Forumis the most

important for which age group

2. Pre- retirement

operate under a life insurance policy, what rate of increase will generally apply?annum for his ULIP policy. What should be the SA in case he wants to avail the tax benefits?that the decision on the proposal must be conveyed to the proposer within

1. 15 days of receiving the proposal

2. 20 days of receiving the proposal

3. 25 days of receiving the proposal

4. 30 days of receiving the proposal Family floater

health Insurance plan covers

1. All members of a Family

2. Husband and Wife only

4. Children Onlylong does an

insurance company have to complete its investigation of a claim?

How the Daily hospitalization cash benefit will provide benefits to policyholder who is hospitalized?

1. Entire charges are refunded.

2. Entire charges less bed charges will be paid

3. A fixed amount on a daily basis is paid irrespective of the actual cost of treatment

4. Only Hospital bill will be paidmonetary

authority of the financial system in India?clause can be enforced by the insurance company during the

1. First five years of policy

2. First Two years of policy

4. Inception of the policy

Ch 7 1. Up to 50000 3. Up to 100000 1

Ch 13 3. Loans facility 4. No benefit 1

Ch 11 1. 18 year old 3. 23 year old 4. 25 year old 1

Ch 14 1. 1 month 2. 2 months 3. 3 months 4. 6 months 4

Ch 14 1. 50 lakhs 2. 30 lakhs 3. 25 lakhs 4. 20 lakhs 4

Ch 6 3

Ch 7 1. Monthly 2. Quarterly 3. Half Yearly 4. Annually 2

Ch 3 3

ch 3 1. 8000 2. 8320 3. 9456 4. 9240 2

Ch 14 1. 20,000 2. 50,000 4. Unlimited 4

Ch 13 1. 1 month 2. 2 months 3. 3 months 4. 6 months 1

Ch 7 1. 2013 2. 2015 3. 2017 4. 2020 2

are paid out of a legitimate source of funds cash is accepted

2. Up to 99990

4. Without any limitbe the benefit

to the customer as NO CLAIM BONUS

1. Discount in next year premium

2. Increase in Sum Assured next yearcompetent to

enter into a contract if they are

2. 21 year oldfor

investigation in disputed claim?restricted to insurance contracts of value not exceeding?Information about the location of the insurance Ombudsman had written?

1. Operative clause

2. Attestation

3. Information statement

4. Endorsementsthe interest

that in normally compounded on what basis.for accidental death benefit rider must not exceed

1. 15% of base policy premium

2. 25% of base policy premium

3. 30% of base policy premium

4. 40% of base policy premium

frequency loading of 4% is added in a quarterly premium what is the amount that needs to be paid.of insurable interest does an individual have in his own life?

3. Up to the sum assured taken in the planpasses an

award within which timea designated authority in 2010 then the person can apply for a license in which year.

Ch 15 2

Ch 7 1. Switching 3. Churning 4. Fact Finding 3

Ch 6 1. Denny 4

Ch 3 1

Ch 3 1. Loading 3. Frequency 4. Interest 1

Ch 5 1. One person 3. Three persons 4

Ch 2 3.50:50 1

Ch 4 4

Under the hospital care rider what is the payout made

1. 10% of the sum assured

2. Specified amount multiplied by the number of days the policyholder is hospitalized

3. expenses incurred per day multiplied by no. of days stay in the hospital

4. 100% of Sum Assured

endowment plan and take a whole life in order to earn higher commission its termed as

2. Doing a financial planning

are alive. He has taken a family floater plan. Under the plan who all will be covered.

2. Denny and his wife

3. Denny, his wife and children

4. Denny, his wife, his children and his parents

with it mid way as he required the money with the intention of not getting the interest. What will he get?

1. Discounted Value

2. Principle amount

3. Discounted Value with persistency bonus

4. Principle with persistency bonusplan the

additional premium added is known as

2. Investment Nomination

can be in favor of how many people?

2. Two persons

4. It can be any number

the policy is been done on joint life basis and the need for nomination under the plan will be as

1. Joint life policy

2. Not Possible

4.Not Applicable

What key impact will the agent have in low persistency

1. Increase more business

2. Increase in the agents earning

3. Will improve reputation

4. Will have impact in his commission.

Ch 4 1. 10 days 2. 15 days 3. 30 days 4. 45 days 2

Ch 7 2

Ch 2 1. 10000 2. 25000 3. 50000 4. 100000 3

Ch 6 1. Actuary 4. Accounts 1

Ch 5 1. 2 lacs 2. 3 lacs 3. 5 lacs 4. 6 lacs 2

Ch 12 1. Term plan 1

Ch 4 1. IRDA 4. LIC 2

Ch 5 3

Ch 14 1. Term plan. 3

needs to inform the policyholder regarding the status of the policy.

Certificate from the village panchayat

1. Will be considered as standard age proof

2. Will be considered as non standard age proof

3. Will not be accepted

4. Will be verified firstmaximum sum

assured under a micro insurancewishes to be in a department which calculates the level of premium. In which department should he join?

2. Underwriter

3. Claim Department

premium paid which is 60000, what amount of sum assured should he avail in a ULIP plan.of insurance for protection at the lowest premium. Which is the best plan for him?

2. Endowment plan

3. Whole life plan

4. Money back plan. The insurance

act of 1938 created which of these.

2. Tariff Advisory Committee

3. National Insurance Academy

was filled by Nishu, then what is the additional requirement to be taken along with the documents.

1. The policy needs to be advertised in the newspaper.

2. Nishu has to sign an indemnity bond.

3. Thumb impression of Ashu has to be taken.

4. Ashu needs to be medically examined.

25% of the sum insured in spite of all his premiums been paid on time. This indicates that his policy is a

2. Endowment plan.

3. Money back plan.

4. Wholelife plan.

Ch 7 1. 10,00,000. 3. 50,00,000 4. 1,00,00,000. 3

Ch 7 3

Ch 3 3

Ch 4 3

Ch 5 3

Ch 4 1. High income. 3

ch 3 1. Charges. 2. Mortality. 3. Interest. 4. Inflation. 1

Ch 4 1. Voidable 2. Invalid 3. Valid 2

Ch 4 1. Null and void 2. Invalid 3. Voidable 4. Valid 2

Ch 3 1. Proviso 2. Schedule 4. Endorsement 2

Ch 2 3

Ch 14 1. Rises 4

of COPA is limited to what amount at the district level.

2. 20,00,000.term plan the

maximum premium of the accidental rider can be.

1. 100% of basic premium.

2. 50% of basic premium.

3. 30% of basic premium.

4. 35% of basic premium.term plan the

maximum premium of the accidental rider can be.

1. 100% of basic premium.

2. 50% of basic premium.

3. 30% of basic premium.

4. 35% of basic premium.to the principle

of indemnity a life insurance policy is a.

1. Insurance contract.

2. Indemnity contract.

3. Value contract.

4. Major life contract.Harish declares

that he consumes alcohol twice every week. This is a

1. Moral hazard.

2. Moral peril.

3. Physical hazard.

4. Physical peril.insurance is

made specifically for people from.

2. Middle class. 3. Low income.

4. Affluent class. The reduction

in the benefit illustration shows what.inception of the life insurance policy then, life insurance contract is

4. Null & voidablesigned by a 15

years old boy, this contract will bepolicy is issued with a lien, it will be mention in

3. Terms & conditionsamount under

a life Insurance policy is generally based on

1. Total paid premium

2. Sum Assured

3. Surrender value

4. Paid up value

De- tarrification is a process by which pricing of Insurance

2. Decreases

3. Reaches at a level as per industry trends

4. Insurance can price their product on their self past experiences.

Ch 14 3. All insurer 4. It is optional 3

Ch 13 2. IRDA 2

Ch 5 3

Ch 6 2

Ch 5 1. Bank 3. Post Office 4. Share Market 3

Ch 9 2. Inflation 3. Interest rate 4. Market Risk 2

Ch 5 1

Ch 5 1. Term Plan 1

protection of Policyholder’s interest 2002 (IRDA), Which insurer will have a grievance redressal System

1. Some Specific Insurer

2. Those Insurer who did not created Insurance Ombudsman Systemhas created a

call center for logging a complaint

1. Life Insurance Council

3. Insurance Association

4. Insurance Institute of India

What is the key function of NIA

1. Provide suggestion for Premium calculation

2. To be an active link between Global market & Indian Life Insurance Industry

3. Design, implement and operate an insurance training

4. Regulate the investment of funds by Life Insurance company

received Maturity in a lump sum. What is the possibility of receiving it in installments if it is not a annuity plan

1. He has switched his fund

2. He has opted for Settlement option

3. He has he has redirected his past premium.

4. Policy was lapsed on the time of maturityto purchase a

Kisan Vikas Patra. What is the most suitable place to purchase it

2. Insurance Companyreturn on his

fixed deposit in a bank. If his net return is 3%, what can be the reason

1. Administrative chargefinding, rating

is mentioned ‘3’. This Indicates

1. Risk apatite of client

2. His future aspiration

3. Commitment to need

4. Willingness to pay

provide financial security to his dependent. Which plan should be offered

2. Term Plan with return of premium

3. Pure Endowment plan

4. Unit Linked Plan

Ch 11 1. 3 years 2. 5 years 3. 7 years 4. 2 years 2

Ch 5 2

ch 1 3. Term plan 1

Ch 7 1

Ch 4 1

Ch 14 1. It is higher 2. Decrease 2

Ch 5 1. One year 2. Two years 3. Three years 4. Five years 2

Ch 7 3

Ch 13 2

wants to fixed deposit in bank. What duration is required for it?

Incase of presumption of death

1. Not necessary to pay premium until court decree

2. Necessary to pay premium until court decree

3. Claim not admissible

4. Depends on case to case

payment in the 5yrs and in the maturity he gets rest of sum assured. What type of policy it is

1. Money back policy

2. Convertible plan

4. Endowment policy

Which is correct in relation to Insurance Broker?

1. Insurance broker is represents insurance buyer and remunerated by the insurance company

2. Insurance broker is represents insurance buyer and remunerated by the Client

3.Insurance Broker gets money from both Insurance company as well as from Client fo selling Insurance

4. None are correct

But shailesh pays more monthly payment than ankit for same amount of policy. Why?

1. Shailesh is older than ankit.

2. Shailesh’s income is more than Ankit’s income

3. Shailesh & Ankit want it that way

4. Option 1 & 3 are correct3rd year as

compared to the 4th year of lien.

3. Slightly higher

4. Slightly lowercomplaint can

be made through consumer protection act.weekly premium payments are accepted.

1. Health Insurance

2. Group Insurance

3. Micro Insurance

4. Macro Insurance

wants to take ADB rider, he is not sure of how much sum assured he needs to take for ADB rider. What is your suggestion?

1. Needs to take expert’s suggestion

2. Equal to base cover

3. Any Amount he can take if he is ready to pay premium

4. 50% of SA max.

Ch 5 2

Ch 15 1. Nil 2. 10% 3. 20% 4. 30% 1

Ch 6 1. 2011 2. 2012 3. 2013 4. 2014 1

Ch 3 4

Ch 2 1

Ch 14 1

Ch 13 1. 10 days 2. 15 days 3. 20 days 4. 25 days 2

Ch 5 1

Ch 7 4

the qualification of Agent is determined?

1. Address of the agent

2. Domicile status

3. Qualification of Agent

4. DOB of Agentpays the

premium of 5000/- and suffers illness before maturity?2010 As per Agents code of conduct, an agent can get a new policy from this customer from Feb which year units in gold ETF, It means that how much grams we have in physical

1. 5 or 10 grams

2. 10 or 15 grams

3. 15 or 25 grams

4. 50 or 100 gramsinsurance, the

insurable interest should exist

1. At the time of taking the policy

2. At the time of claim

3. At the time policy matures

4. At the time of taking the policy & claim

Pooling of insurance applies to

1. all types insurance

2. All types of insurance except Motor insurance

3. Only life insurance

4. Only Non-life insuranceawards passed

by the Insurance Ombudsman within how may days

If IRDA is unable to discharge its functions or duties, Central Government

1. Has the power to supersede the IRDA by issuing notification.

2. Has the power to supersede the IRDA by issuing a bill in parliament

3. Has the power to supersede the IRDA by issuing draft

4. Can make changes in IRDA law

efficient investment and invests in senior citizen saving scheme. Its the impact in his taxation

1. He will get tax benefit up to 5000

2. He will get tax benefit up to 25%

3. He will get a reduction in tax slab

4. His investment would be deducted from taxable income

Ch 7 3

Ch 8 1

Ch 13 2. Marriage 4

Ch 7 3. Training 3

Ch 2 2

Ch 11 3. Financial risk 4

Ch 13 1. 10 days 2. 20days 3. 30 days 4. 60 days 3

Ch 4 4

Ch 5 1. Provisio 2

What are the benefits to the policyholder Under Surgical care rider?

1. Number of days admitted in hospital & surgery expenses in full

2. Number of days admitted in hospital & surgery expenses in partial

3. Treatment cost of surgery subject to terms & conditions

4. Lump sum amount what he has incurred

hospital which doesn’t have cashless facility. How the policy holder will get benefited

1. Need to spend and Get claim from the insurer

2. Need to add that hospital as TPA

3. Need not to claim

4. Need to switch to the another insurer

given the top priority. Needs: Income protection, Childs education, marriage and emergency funds.

1. Childs education

3. Emergency funds

4. Income protection National

insurance academy has the following main functions

1. Calculating premium

2. Interact with the government

4. Mortality assumptionsand critical

illness rider in classified under

1. Life and non life respectively

2. Both life insurance

3. Both non life insurance

4. Nonlife and life respectively.

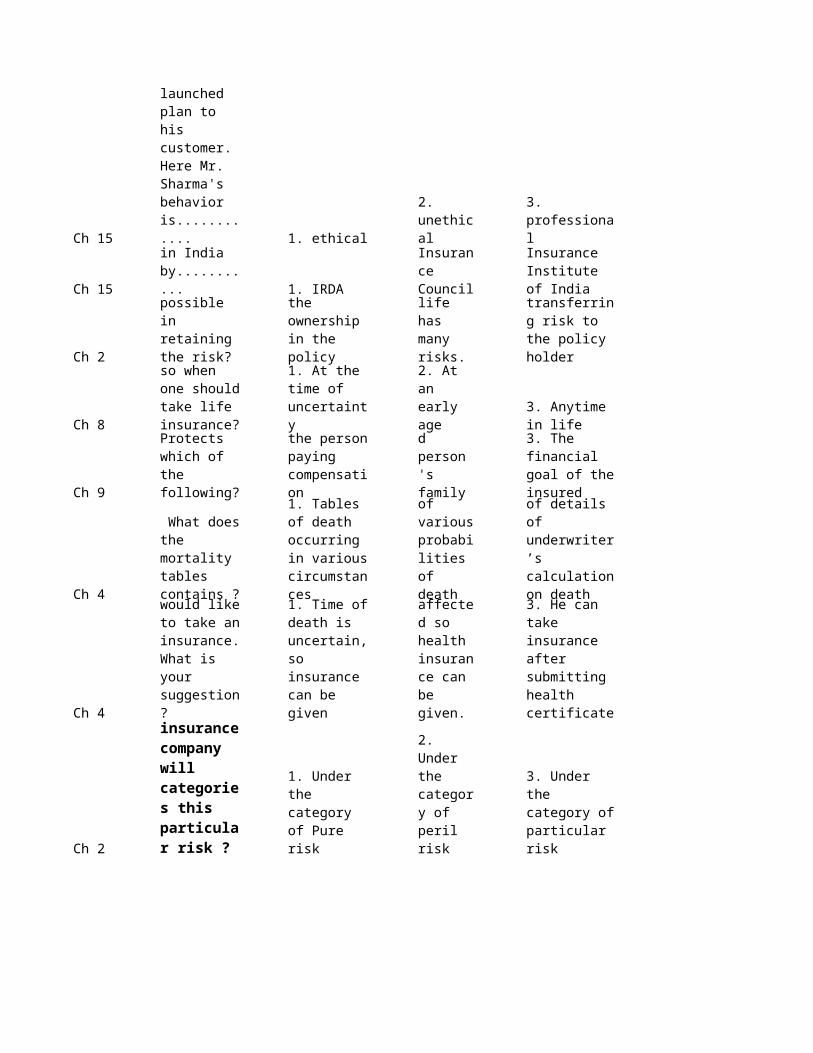

Pure risk is classified under

1. Economic risk

2. Speculative risk

4. Insurable risk

same will have to be paid by the insurance after how many days from the date of admission of the claim?regulations IGMS should be mandatory set up by

1. Only by few selected insurers

2. Only by non life

3. Some life and non life

4. By all insurers.

insurance company can exclude this hazard and mention it in which part of the policy document?

2. Endorsements

3. Operative clause

4. Terms and Conditions

Ch 15 1

Ch 7 1

Ch 3 4. Vesting age 3

Ch 2 1

Ch 10 1. Pure risk 3. Particular risk 3

Ch 14 1. Lower profits 1

Ch 11 2. COPA 3. Sebi 1

Ch 6 1. Nil 2. 1% 3. 5% 4. 10% 1

When can an insurance company give more than 35% first year commission?

1. When the insurance company is in the first 10 years of operation

2. If the agent has worked with the company for more than 5 years

3. If the agent has worked with the company for more than 10 years

4. If the agent is doing more than 3 policies in a month.commission

which he will earn from the product which he is going to sell

1. When the customer asks him

2. After the fact finding process

3. After quantifying the need

4. After the product is recommended to the clientwhat are the

parts which shows the benefit for an annuitant.

1. Insurance coverage

2. Annuity part

3. Guaranteed and non guaranteed part

and accumulated bonus Rs.60,000/-. What is the paid up value if bonus accumulated and if not bonus accumulated?

1. 213333 & 273333

2. 213333 & 229333

3. 229333 & 273333

4. 229333 & 293333affect specific

individuals or local communities in nature is called as

2. Financial risk

4. Physical hazardto the insurer

in case the persistency falls

2. Higher profits

3. Increased Liability

4. Decreased Life fund

where he/she should follow up are – Ombudsman, IRDA Customer Grievance Cell and ………………………..

1. Consumer Forum

4. Life Insurance Council5000 has

matured, how much will be deducted when the maturity claim arises

Ch 5 3. Safety 4. Liquidity 4

Ch 3 2

Ch 3 1. Commission 2. Charges 2

Ch 1 4

Ch 5 2. Banks 4. Brokers 1

Ch 7 1. Endowment 2. Term 3. Money Back 4. Whole of Life 3

ch 1 3

Ch 10 1

Ch 7 3

investing in Debt Mutual Fund, what is the primary objective

1. Good Returns

2. Regular Incomeinterest in the

life of an employee, what kind of policy is this?

1. Surety insurance

2. Keyman Insurance

3. Partnership Insurance

4. Debtor Insuranceillustration, the

reduction of the actual benefit amount is mainly due to deduction of

3. Non guaranteed benefits

4. Reversionary Bonusbased on the

key principle that policyholders should be prevented from

1. Insuring existing losses.

2. Making false insurance claims.

3. Paying excessively for insurance cover.

4. Profiting from insurance.

The client of reinsurer are

1. Insurance companies

3. Asset Management Companies

during the term of the policy, his nominees gets the sum insured. What type of policy is this ?insurance policy, which of the following information is the most critical

1. Group lifestyle

2. Employees

3. Age of the group

4. Medical history of group

Brokers Association of India, what is the most appropriate relationship between Insurer and Broker?

1. Insurance broker represent the client and the insurer remunerate the broker

2. The client represent the broker and the insurer remunerate the broker

3. Insurer represent both client and broker remuneration

4. Broker only service the client

A low persistency ratio for the insurance company means that:

1. The customers are satisfied with the products

2. The company is acquiring more business and new customers

3. A large numbers of policies have lapsed / surrendered resulting in loss of profit

4. The company will not declare bonus

Ch 14 3

Ch 10 1. 24 hours 2. 1 day 3. 10 days 4. 30 days 3

Ch 4 2

ch 3 1

Ch 5 1

Ch 5 4. Term Plan 3

Ch 6 2. ROP plan 4. Ulip 2

Ch 5 3

withdrawal. This is known as commutation. Up to what proportion of the accumulated fund can be withdrawn?

1. The entire fund can be withdrawn

2. Only half of the fund can be withdrawn

3. Only one third of the fund can be withdrawn

4. Only one fourth of the fund can be withdrawn

insurer is supposed to respond after receiving any communication from its policyholders? For an insurance agent, a low persistency ratio means :

1. Loss of renewal commission

2. High client satisfaction

3. Higher reputation

4. More earning of First Year Commission

contract, if they disagree with the terms and conditions of the Policy, within a ‘free look-in period’ of

1. 15 days from the date of receipt of the policy document

2. 20 days from the date of receipt of the policy document

3. 25 days from the date of receipt of the policy document

4. 30 days from the date of receipt of the policy document

In the case of life insurance, insurable interest should exist

1. At the inception of the policy

2. At the time of a claim

3. At the time of every renewal premium payment

4. All the above occasionfollowing plan

remaining part of the Sum Assured is paid on maturity?

1. Endowment Plan

2. Convertible Plan

3. Money Back plan

at the end of the term he wants to get at least some return. Under which policy he will get these benefits

1. Endowment plan

3. Whole life planKishan Vikash

Patra under post office schemes is done

1. Regularly with no fixed term

2. Lump Sum with no fixed term

3. Lump Sum for fixed period of time

4. Regularly for fixed period of time

Ch 11 3

Ch 2 3

Ch 4 3

Ch 5 1. Physical 2. Moral 3. Occupation 2

Ch 5 1. Agent 4. Proposer 3

Ch 8 1. 1 lakh 2. 1.5 lakhs 3. 2 lakhs 4. 3 lakhs 1

Ch 8 1. 75K 2. 1L 3. 1.5 L 4. 50K 2

Ch 2 1. Health plan 2. Child Plan 3. Life Insurance 4

Ch 8 3. Life Insurance 4. Retirement 2

Ch 9 1. Retain 2. Transfer 3. Avoid 4. None 2

Ch 3 1. Save Tax 3. High Returns 4. Protection 4

Ch 12 1

and wants to make use of tax benefit under the policy for whole SA. How much premium would help him avail this benefit

1. Less than 10000

2. More than 10000

3. Less than 20000

4. More than 20000settlement,

any queries or additional documents can asked from the claimant within

1. 5 days from the receipt

2. 10 days from the receipt

3. 15 days from the receipt

4. 20 days from the receipt

Law of Large number helps the insures to

1. Calculate the premium

2. Increase the profitability

3. Ascertain the death ratio

4. Declare the bonusdue to

Financial fraud would come under which hazard

4. Not applicablesignature is

required on attestation of the policy?

2. Policy holder

3. Authorized officials of insurerceiling of tax

exemption under 80 c.limit of tax benefit that can be availed of under Section 80C.?having 9 year old child. Which product is not to be given priority?

4. Retirement Planchildren. Which

plan can he take that can cover his whole family?

1. Health Insurance

2. Family floater Which is the

best option to manage risk?major reason for self employed to take insurance.

2. Fluctuating income What is the

major reason for conducting fact finding exercise?

1. Need analysis

2. Understand about company

3. Introduction of agent

4. Understanding the Customer

Ch 1 1. 60000 2. 75000 3. 100000 4. 5000 2

Ch 12 2. IRDA 3. Actuaries 4. Underwriter 2

Ch 12 1. IRDA 4. CII 2

Ch 14 4

Ch 5 1. Rs. 1, 00,000 3. Rs. 25,000 4. Rs. 60,000 2

Ch 3 3. State Level 4. Mandal Level 2

Ch 8 1. Rs. 75,000 3. Rs. 1, 20,000 4. Rs. 1, 00,000 4

Ch 2 1

Ch 10 4. Health Plan 1

SA of 1 lakh, what will be the payout after 15 years in a simple revisionary bonus system?for annual assumed growth rate are given by

1. Life Insurance Council

Pricing element is done by

2. Insurance Company

3. Life Insurance Councilinclude

_______________, apart from Procedure, Training and audit.

1. Inspection by IRDA

2. Audit by Finance Ministry

3. Appointment of Principal Compliance Officer

4. Inspection by Auditor Generalpremiums by

cash cannot exceed ____________ .

2. Rs. 50,000

insurer. But it was rejected. He feels that it is repudiated on wrong reasons. Which consumer forum can he approach?

1. National Commission

2. District Leveldeduction that

can be gained for premium paid is _______ in a financial year.

2. Rs. 1, 10,000

some personal problems he has decided to cancel the policy on 8th July, 201 Can he cancel or return the policy?

1. No, as 15 days period is over

2. Yes, as it is within 1 year

3. No, as 20 days period is over

4. Yes, as it is within 3 monthshis daughter

Sneha is 3 years old. Which plan can he take?

1. Term & Children Plan

2. Annuity Plan

3. Whole Life Plan

Ch 11 1. Transfer 2. Control 3. Retaining 4. Avoidance 3

Ch 9 2

Ch 5 1. Normal 3. Early 4. General. 3

Ch 3 1. Middle Level 2. Top Level 3. Low Level 4. High Level 4

Ch 14 1. 5000 2. 10000 3. 15000 4. 20000 1

Ch 1 1. 15 days 2. 30 Days 3. 45 days 4. 60 Days 1

Ch 1 1. 1Lakh 2. 10 Lakhs 3. 15Lakhs 4. 20 Lakhs 4

Ch 6 1. 48% 2. 50% 3. 60% 4. 26% 4

the funds available in the bank and monthly rentals received from village. This comes under Risk ______ Naveen referred Prasad to Ram. Prasad is also teacher. Ram who is an agent advised Prasad to take money back plan as he is of same age (33 years). Is it the right advice? Why?

1. Yes, as Naveen and Ram are of same age.

2. No, customers needs are different

3. Yes, as both are teachers

4. No, as there is an age difference.

for a term of 15 years. Ajay died after 4 years. Insurance company will not treat this claim as ________ claim.

2. Fraudulent

having 2 sons, Vineeth and Sumith. The level of risk appetite, Rajesh belongs is _______. Assured allowed for Micro Insurance?days does the Free Look Period last?powers are restricted to insurance contracts of what value?what is the maximum stake that the Foreign Partner in Insurance Company hold?

Ch 5 1

Ch 14 3. Post Office 3

Ch 4 1. 50,000/- 2. 15,000/- 3. 10,000/- 4. 100,000/- 4

Ch 2 1. 15 Days 2. 30 Days 3. 2 Months 4. 3 Months 2

Ch 4 1. A clause 2. A Lien 3. A Loading 2

Ch 15 1. Peril 2. Hazard 3. Risk 4. Uncertainty 3

Ch 15 1. PAN Card 3

Ch 7 1. Churning 3. Underwriting 4. Switching 1

Ch 7 2

What does MDRT Stand for?

1. Million Dollar Round Table

2. Major Double Rupees Tag

3. Major Dollar Round Tag

4. Mean Disposition Residence Time you have to go

if you wanted to buy a Kisan Vikas Patra?

1. Any Nationalized Bank

2. Insurance Company

4. Mutual Fund Companylimit of tax

benefit that can be availed of under Section 80C?has to give his decision within how many days?associated with the person would decrease with time, then he would accept the case with

4. Level Premiumsuffering from

lung cancer is a smoker. Here smoking can be termed as Which of the following is a Non Standard Age Proof

2. Certificate of Baptism

3. Certificate from Village Panchayat

4. Certificate from School or College

analysis and told him that his Insurance need is higher than 10, 00,000 and suggested that he surrenders the existing policy and buys a new one. This is an example of 2. Proposing If the recommendation of the agent has been rejected by the client, the agent should:

1. Ask the client to fill the proposal form

2. Find out the reasons for refusal

3. Must try to convince the client to follow his recommendation

4. Must try to force the client to follow his recommendation

Ch 9 4

Ch 6 1. 25% each 3. 50% each 4

Ch 7 1. Agent 2. Insured 3. Policy Holder 1

Ch 4 1. Annually 3. Quarterly 4. Monthly 1

Ch 7 2

Ch 4 2

Ch 7 1. X only 4. X with all 4

Ch 4 2. 500000 3. 1500000 4. 4000000. 1

Ch 12 1. Rs.20000 2. Rs.25000 3. Rs.5000 4. Rs.50000 4

Ch 6 1. Monthly 2. Yearly 3. Quarterly 2

Ch 13 1. RBI 2. IRDA 3. SEBI 4. Constitution 1

Ch 7 1

Which of the following is true regarding Family Floater Health Insurance Plan?

1. A Family Floater Plan is the same as a Individual Plan

2. Only self and spouse can be covered in this plan

3. Any number of people may be covered in this plan.

4. The insurance cover is shared amongst the family members in no fixed Proportion.proportion is

the cover in a Family Floater Plan shared? 2. 15% each

4. No Proportionproducts their

main features and their tax treatments is the role of:

4. Insured personinterest is

normally compounded in a

2. Semi Annually

company pays for the treatment costs in the event of hospitalization of the insured person is called

1. Critical Illness Rider

2. Hospitalization Care Rider

3. Accidental Benefit Rider

4. Surgical Care Rider Age proof

submitted from Village Panchayat is:

1. Standard and accepted

2. Not standard but accept

3. Not at all accepted

4. Accepted with SSLC book/mark listwife, 2 children

and aged parents Health premium is allowed for

2. X with wife

3. X with wife and kids

Maximum Life cover

1. 20 times annual salaryregulation, it

allows cash premium not over than Bank interest is accumulated

4. Once in 6 months _____ controls

monetary system in India

Hospitalization rider has the following benefit:

1. Person receives fixed amt daily for no of days in hospital

2. Person receives an amount equal to the expense.

3. Person receives a fixed amount of 1000 daily.

4. Person receives benefit only if he is hospitalized for 3 days minimum.

Ch 3 1. 7680 2. 9320 3. 8320 4. 6600 3

Ch 15 1. 2015 2. 2014 3. 2013 4. 2017 1

Ch 8 1

ch 1 2

ch 1 2

Ch 2 2. Level 3. Uncertainty 4

Ch 2 4

Ch 2 1. Risk Transfer 2. Risk avoid 1

ch 1 1

Ch 4 2

%. Hence actual quarterly premium will be withdrawn in June 2010 due to malpractice. He can reapply for his license in A Professional insurance market carries…..

1. Need – Based Selling

2. Product – Based Selling

3. Commission – Based Selling

4. Company – Based Selling.

Insurance Market divided into

1. Endowment and Money Back Insurance

2. Life and General (non-life) Insurance

3. Government and Private Insurance Markets

4. Health and Saving Insurance Markets

What is Bancassurance?

1. Giving insurance policies to Banks.

2. Selling insurance policies through Banks.

3. Giving guarantee to policies by Banks.

4. None of the above.

The “Risk” contains….

1. Peril and Hazard

4. All of the above.similar risks by

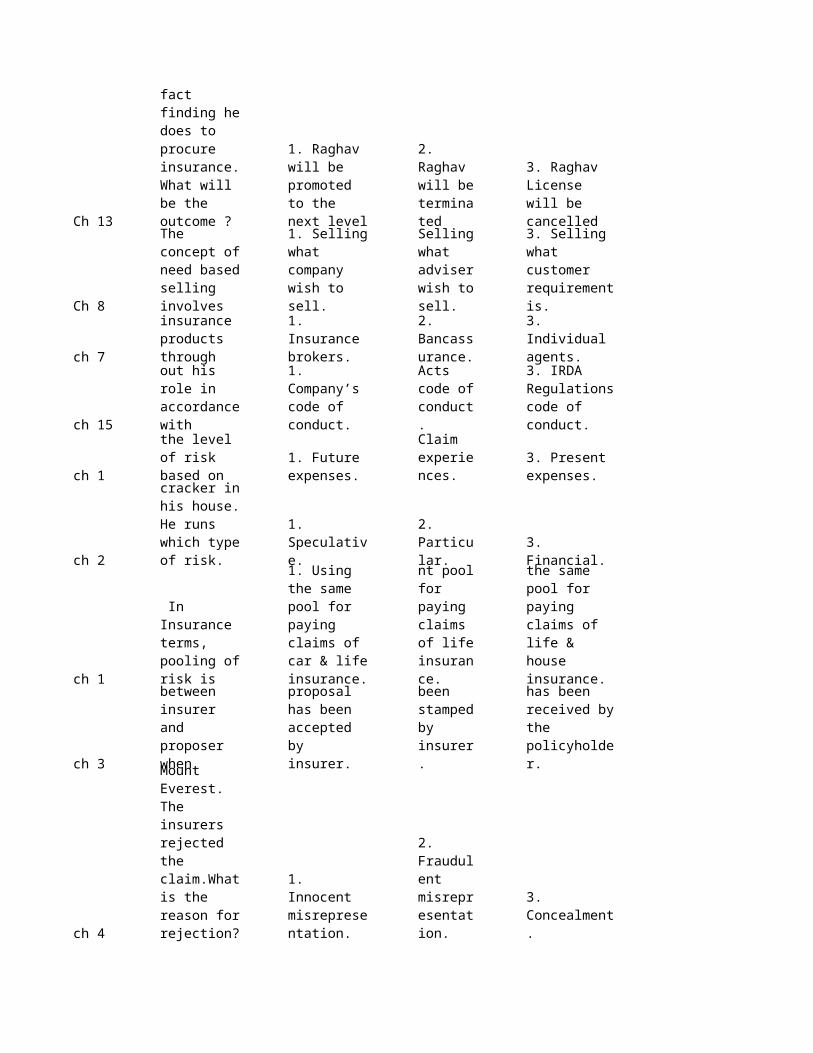

Insurance Company is called as….

1. Grouping of Risk

2. Risk Grading

3. Risk Assessment

4. Pooling of Risk The function

of Insurance works on…..

3. Risk retention.

4. All of the above.

A contract comes into existence when………

1. One party makes an offer which the other party accepts unconditionally.

2. One party makes an offer which the other party put extra conditions.

3. One party makes an offer where other party gives counter offer.

4. One party makes an offer which the other party receives the offer.

Kumar would like to take Life Insurance policy on wife’s name in order to get monitory benefit. Insurance company rejects this proposal on the grounds of…….

1. Anti Money Laundry

2. Legality of object or purpose

3. Capacity of paying future premiums.

4. All of the above

Ch 3 4

Ch 3 1

Ch 3 4

Ch 4 2

Ch 3 3. Sum Assured 4

Ch 3 2

Ch 5 3

Ch 4 1

Ch 4 2

Ch 4 1

Under this situation may leads to breach of the duty of utmost good faith.

1. Non disclosure of material facts.

2. Concealment of a material fact

3. Fraudulent misrepresentation of facts.

4. All of the above.

Principle of Indemnity denotes…..

1. Insurance can not be used to make a profit

2. Insurance should not taken by high risk people.

3. Insurance can not taken by politicians.

4. All of the above. The principle

of utmost good faith is not applicable to

1. Facts of common knowledge

2. Facts of law

3. Facts those are not material.

4. All of the above.main source

for insurance company to get information of proposer?

1. Advertisements.

2. Proposal form.

3. Conducting interviews.

4. Telephonic conversations.involved in

calculating Surrender Value of the Policy?

1. Number of year’s premium paid.

2. Number of premiums payable.

4. All of the above.

What are the different types of Assignments?

1. Full Assignment and Partial Assignment

2. Conditional and Absolute Assignment.

3. Life Assignment and General Assignment.

4. Standard Assignment and Non-Standard Assignment.

insurance policy with ABC Company. But he is not satisfied with the policy benefits. What Mr. Kumar can do under this situation?

1. He can not do any thing, because be received the policy bond.

2. He can file a complaint against insurance company in court.

3. He can send back the policy document to insurance company with in 15 days from policy receiving date.

4. Serve notice to insurance company on policy benefits.

Moral Hazard reflects the …….

1. Intentions and attitude of Proposer.

2. Habits and Hobbies of Proposer.

3. Occupation and Residence of Proposer.

4. Medical and Personal History of Proposer.replacement

methods equates Human Life Value (HLV) to

1. Future value of Present earnings.

2. Present value of future earnings.

3. Present value of previous earnings.

4. Future value of previous earnings.

Agent will be called as…..

1. Primary Underwriter

2. Main Underwriter

3. Chief Underwriter.

4. Information Underwriter.

Ch 3 1. Rs. 2500/- 3. Rs. 250000/- 4. Rs. 5000/- 2

Ch 5 3

Ch 5 1

Ch 5 1. High Returns 2

Ch 6 3

Ch 6 1. Insurance 3. Investment. 4

Ch 6 1. Insurance 2. Shares 3

Ch 5 4

Sum Assured by paying Rs. 50,000 premium per year. Company declared 5% Simple Reversionary bonus, what is bonus amount?

2. Rs. 25000/-

The two basic elements of most life insurance plans are

1. Guaranteed Benefit and Non-guaranteed Benefit.

2. Interest Benefit and Bonus Benefit.

3. Death Benefit and Maturity Benefit.

4. Bonus Benefit and Tax Benefit.

Term Insurance Plan will give….

1. Only Death Benefit.

2. Only Maturity Benefit.

3. Only Bonus Benefit.

4. Only Tax Benefit. Low risk

products give…..

2. Low Returns

3. Moderate Returns

4. Good Returns

Who will maintain Mutual Fund Schemes?

1. Mutual Fund Management Societies

2. Mutual Fund Management Systems.

3. Asset Management Companies.

4. Asset Maintenance Company Limite4.

Which is the primary saving need among all saving needs?

2. Purchasing House

4. Contingency/ Emergency Fun4.

is going to happen with in Nine months. He would like to get some returns from this money in these 9 months period. What is the best option to park his money?

3. Fixed Deposit in Bank

4. Mutual Funds.following

product not comes under Section 80 ( C ), income tax act 196

1. National Saving Certificates.

2. Equity Linked Saving Schemes.

3. Principle component of home loan.

4. Premium paid for Health Insurance Plan.

Ch 7 3. Rs. 90,000/- 1

Ch 7 2

Ch 7 3

Ch 7 1

Ch 9 3. Retirement. 4. Children. 3

Ch 9 2

Ch 8 3

Ch 8 1

pension fund. He would like to utilize commutation benefit before taking pension. What is amount Mr. Suresh can withdraw as commutation?

1. Rs. 3, 00,000/-

2. Rs. 4, 50,000/-

4. Rs, 4, 85, 468/-create

purchase price or Pension Fund. We call this phase as…..

1. Collection Phase.

2. Accumulation Phase

3. Pension Phase.

4. Primary Phase.family

members also. We will call these plans as…..

1. Family Health Insurance Plans

2. Total Protection Policies.

3. Family Floater Health Insurance Plans.

4. Family Rakshak Health Plans.

Insurance. What are the options available to Mr. Hitesh to fulfill his need with a little cost?

1. Taking Life Insurance plan with Critical Illness Rider.

2. Taking Health Plan, Insurance Plan separately.

3. Taking Medi-claim plan with Life Insurance.

4. Taking Hospital Benefit Plan with Endowment Plan.

solutions for health care and inheritance planning. Which main life stage he most likely to fall into?

1. Young Unmarried.

2. Young married with children.questioning is

very useful to gather information from clients?

1. Closed Ended Questions

2. Open Ended Questions.

3. Interrogative Questions.

4. Clarification Questions.

Perceived needs are those….

1. Short term needs.

2. Imagined to be important by Advisor.

3. Imagined to be important by client.

4. Long term needs.

Need analysis involves identifying………

1. Financial provision to meet predictable and unpredictable needs.

2. Capacity to pay the premiums in future.

3. Existing insurance plans.

4. Family and Employment details.

Ch 12 1. Photographs 4

Ch 12 3

Ch 15 1. Switching 2. Churning 3. Redirecting. 4. Shifting. 2

Ch 1 1

Ch 10 4

Ch 11 2

Ch 11 1. Client 2. IRDA 3. Advisor 4

Ch 11 1

Ch 11 1. Three years 3. Seven years. 4. Nine years. 3

Ch 12 1. Layering 3. Integration 1

Ch 13 1. 74% 2. 26% 3. 24% 4. 76% 2

Which is the not part of KYC norms?

2. Proof of identity

3. Proof of address.

4. Lapsed policy details.

Remuneration to Agents includes

1. First Year Commission

2. Renewal Commission.

3. Both of the above.

4. Salary and Reimbursement.

new one. But new policy does not have any extra benefits but it will give more commission to Mr. Gayaram. This is called as……

An insurance agent is intermediary between….

1. Client and Insurance Company

2. Insurance Company and IRDA

3. Client and IRDA

4. Insurance and Re-insurance company. factor which

has influence on persistency?

1. Role of Agent

2. Product Design.

3. Policy Servicing

4. All of the above.

What is meant by a claim under insurance policy?

1. A demand to fulfill the policyholder’s obligations.

2. A demand to fulfill the insurer’s obligations.

3. Any demand made by the policyholder on the insurer.

4. All of the above.the initiation to

settle the maturity claim process?

4. Insurance company

Which is the right statement regarding claim enquiry?

1. The insurance company makes enquire only on death claims.

2. The insurance company makes enquire on maturity claims only.

3. Enquiry will be done on both Maturity and Death Claims.

4. Enquiry will be done if death happens before one year from policy inception date. person will be

presumed to be dead only after….

2. Five years.

2nd stage in Money Laundering?

2. Placement

4. Amalgamation.foreign

company has in one insurance company in India?

Ch 13 3

Ch 14 1. 10 2. 12 3. 14 4. 15 2

Ch 14 3

Ch 15 4

Ch 15 4. Churning. 3

Ch 2 2

Ch 1 3

Ch 3 1. claim 2. revival 3. inception 4. surrender 3

Ch 2 3

Ch 1 2

Ch 1 3

terms and conditions that may be offered by insurers in the respect of general insurance business.

1. Insurance Regulatory and Development Authority.

2. Reserve Bank of India.

3. Tariff Advisory Committee.

4. Insurance Institute of India.ombudsmen

offices located in India?department that is established by IRDA to deal with customer complaints?

1. Customer Complaint Department (CCD)

2. Customer Grievance Department (CGD)

3. Consumer Affairs Department (CAD)

4. Consumer Protection Department (CPD)

Ethics can be defined as…

1. Those values we commonly hold to be “good” and “right”.

2. Behavior that is based upon the moral judgments of an individual

3. A study of what makes one’s own actions right or wrong.

4. All of the above.Which is not

unethical behavior in below statements?

1. Over selling of Insurance policies.

2. Under selling of Insurance policies.

3. Explaining all details of the policy to customer.

has taken a term insurance for Rs. 30,000,00/- for 30 years. This is an example for-----------------

1. Risk retention

2. Risk transfer

3. Risk avoidance

4. Risk tolerancenot include the

channel of indirect marketing?

1. individual agents

2. bancassurance

3. insurance brokers

4. through internetcontract the

insurable interest needs to be at the time of ....Which of the following can be an example of moral hazard?

1. a family history of heart disease

2. a person working in a chemical factory

3. a person consuming alcohol

4. A teacher working in a primary school.

The business of Insurance is connected with................

1. physical values of assets

2. economic values of assets

3. metaphysical values of assets

4. market values of assetsneed life

insurance because..................

1. death is certain

2. death is uncertain

3. the timing of death is uncertain

4. Death is the solution.

ch 3 3. premium 4. claim 3

Ch 1 1. future data 2. past data 2

ch 3 3. husband-wife 4

ch 3 1. only insurers 3

Ch 4 1

Ch 3 3

Ch 3 3

Ch 3 1

insurance contract 'consideraton' means........

1. proposal form

2. Advisors confidential reportthe risk is

determined on the basis of ..........

3. statistical data

4. mathematical datainsurable

interest in the following options.........

1. surety-co surety

2. employee-employer

4. brother-sisterThe principle of

utmost good faith applies to...........

2. only proposer

3. both insurers and proposer

4. neither insures nor proposer

When an illiterate person wants to have a policy.....

1. an impression of the left thumb is taken and third party has to attest it

2. an impression of the left thumb is taken and the advisor has to attest it

3. an impression of the left thumb is sufficient and need not be attested

4. A relative of the illiterate person has to sign on behalf of that illiterate person.

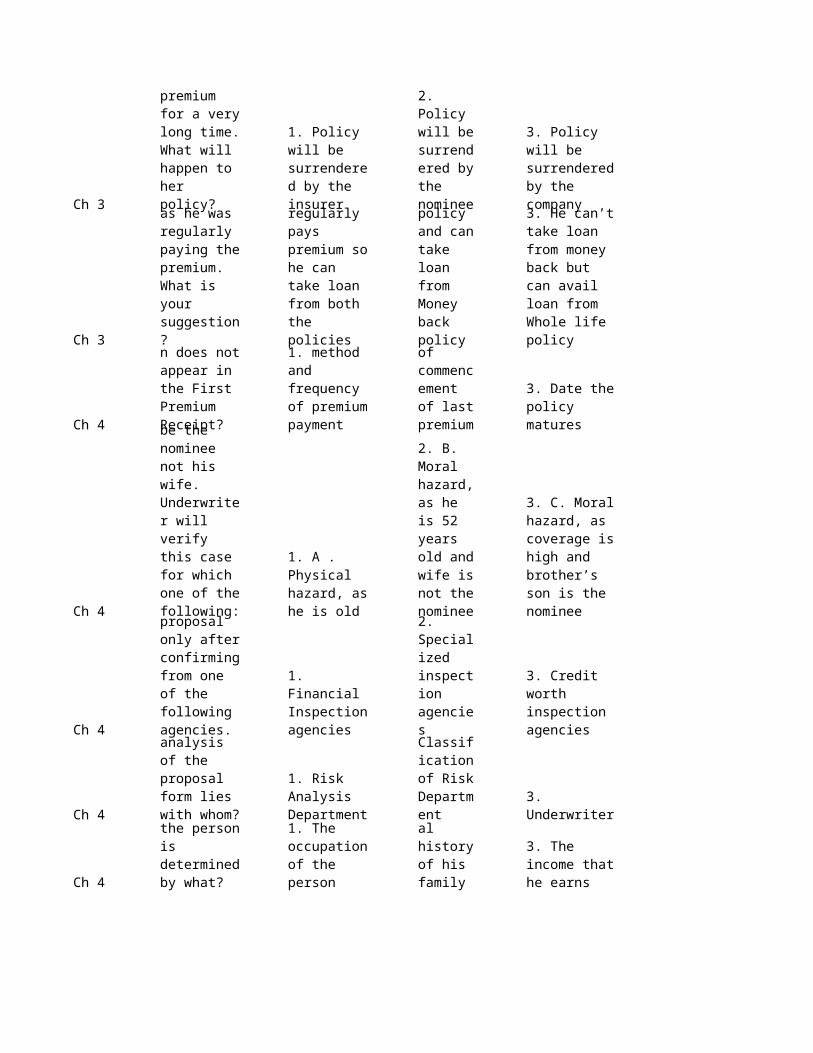

could not pay premium for 5th and 6th year. In the 7th year he approaches the company to renew the policy. Now which of the following options will apply to him?

1. The policy will be renewed on the existing terms and conditions.

2. Mr. Shanth cannot renew the policy

3. the policy may be renewed on different terms and conditions

4. Mr. Shanth can renew the policy only on the approval of the insurer

Which of the following statement is not true in connection with nomination?

1. The life insured can nominate one or more than one person as nominees.

2. Nomination can be done either at the time the policy is bought or later.

3. A person having a policy on the life of another should make a nomination.

4. The section 39 of the Insurance Act 1938 speaks about the nomination.

Which of the following statements in correct in connection with assignment?

1. Assignee cannot make fresh nomination in the policy

2. The assignor need not be major at the time of assignment.

3. Section 45 of the insurance act speaks about assignment.

4. Conditional assignment and absolute assignment are one and the same.

Ch 3 2

Ch 4 1. 10 days 2. 15 days 3. 20 days 4. 25 days 2

Ch 4 3. brochure 1

Ch 4 1. moral hazard 2

Ch 4 2

Ch 5 2

Ch 5 1. when he dies 2

Ch 8 1

Ch 8 1. high 2. low 3. normal 4. Neutral. 2

Ch 6 4. call centers 2

taken an endowment policy of 20 years. He has paid premium for 10 years and now the policy is in force. At this point of time can Shanth take loan?

1. Mr. Shanth will not be granted any loan

2. Mr. Shanth can take loan which should be certain percentage of the surrender value of the policy.

3. There is no concept of loan in insurance policy

4. loans are allowed only in term plansregulations the

decisions on the proposal must to convey to the proposer within......required information about the proposer in.....

1. Proposal form.

2. renewal receipt

4. annual reportmining

company. So he is exposed to..............

2. physical hazard

3. mental hazard

4. Ethical hazard. Lien is

imposed on a policy when underwriter feels that......

1. the risk associated might increase

2. the risk associated might decrease

3. the risk associated might not be harmful

4. the risk associated might be generalan individual

can be protected with the help of.........

1. a unit linked policy

2. a term life policy

3. an endowment policy

4. a money back policyyears for the

sum assured of Rs. 75,000,00/-. It can be paid to him......

2. when he survives the term

3. when he is hospitalized

4. when he loses his job

The disposable income means......

1. the surplus amount that can be invested

2. the amount that can be paid towards one's EMIs

3. the annual bonus amount

4. the sum of one's all investmentstarted

earning. His risk appetite is expected to be.....following ways is easier for a person to take a saving product?

1. through individual agents

2. through internet

3. corporate agents

Ch 5 2

Ch 6 3. Shares 4

Ch 7 3

Ch 7 4

Ch 7 3

Ch 7 2

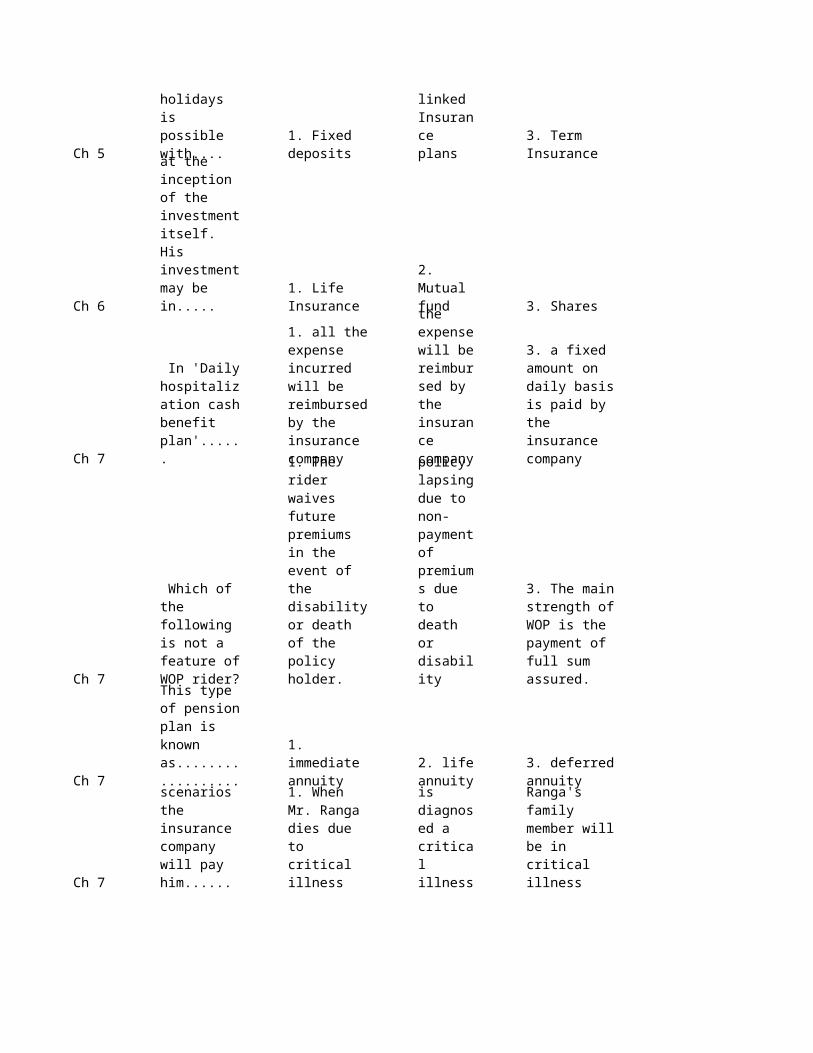

withdrawal and taking premium holidays is possible with....

1. Fixed deposits

2. Unit linked Insurance plans

3. Term Insurance

4. Endowment plans

the tenure, interest rate and method of payment of interest at the inception of the investment itself. His investment may be in.....

1. Life Insurance

2. Mutual fund

4. Bank deposits

In 'Daily hospitalization cash benefit plan'......

1. all the expense incurred will be reimbursed by the insurance company

2. Some percentage of the expense will be reimbursed by the insurance company

3. a fixed amount on daily basis is paid by the insurance company

4. The insurance company will pay all the expense only after consulting hospital authority.

Which of the following is not a feature of WOP rider?

1. The rider waives future premiums in the event of the disability or death of the policy holder.

2. This rider is ideal for helping to prevent a policy lapsing due to non-payment of premiums due to death or disability

3. The main strength of WOP is the payment of full sum assured.

4. WOP rider can be offered with all plans

He has bought retirement plan for 20 years. This type of pension plan is known as..................

1. immediate annuity

2. life annuity

3. deferred annuity

4. joint life annuity

Illness Rider. In which of the following scenarios the insurance company will pay him......

1. When Mr. Ranga dies due to critical illness

2. When Mr. Ranga is diagnosed a critical illness

3. When Mr. Ranga's family member will be in critical illness

4. When Mr. Ranga dies due to severe road accident.

Ch 8 1. the lower 2. the higher 3. the smarter 4. the superior 1

Ch 8 1

Ch 8 1. Real need 2

Ch 8 1

Ch 9 1

Ch 12 3

Ch 15 1. good 2. bad 3. compulsory 4. appreciable 2

Ch 13 1. 30 % 2. 35% 3. 40% 4. 45% 2

Ch 12 1

the age of an individual..............their liabilities will be.daughter Anusha has got married. Now Mr. Ramachandra is free from his burden. So Mr. Ramachandra is now in the ...................stage.

1. Pre-retirement stage

2. Post retirement stage

3. Married with older children stage

4. Employment stage

every day. So he wants to buy an expensive car when he will have sufficient fund. Here Mr. Vinodh's need is.............

2. Perceived need

3. Imaginary need

4. Important needinsurance

advisor to identify the.............

1. clients financial need

2. clients personal problems

3. clients hereditary diseases

4. Clients’ social background.

During the recommendation stage the advisor needs to......

1. recommend the products that best meet the client's needs

2. recommend to wait some days to invest

3. recommend the new product the company has recently launched

4. Recommend to take his own time to take a decision.

As per the IRDA circular an insurance agent.......

1. need not disclose the amount of commission

2. need to disclose the amount of commission

3. need to disclose the amount of commission on demand

4. Should not disclose.advisor

churning is.............practicepercentage of first year commission to be paid to an insurance advisor is.............agent's death, the commission payable will be paid to.........

1. his legal heirs

2. to his nominee

3. will stop automatically

4. Paid in lump sum to the survivors.

Ch 11 2

Ch 11 3

Ch 11 1. 5 years 2. 6 years 3. 7 years 4. 8 years 3

Ch 11 2

Ch 13 2

Ch 13 1. 50% 2. 25% 3. 26% 4. 27% 3

Ch 13 1. 1956 2. 1999 3. 1955 4. 1947 3

Ch 14 1. policyholders 3. insurers 1

Ch 14 1. IRDA 2. Agents 3. Shareholders 4. Underwriters 2

2010, but unfortunately he died on 18th August 201 His death claim is considered as..........

1. Normal death claim

2. Early death claim

3. Abnormal death claim

4. Unnatural death claimInvestigation

will be triggered in case of......

1. Maturity claims

2. All death claims

3. Early death claims

4. Rider benefit claims.heard

for .......years his is presumed to be dead.

In the process of settling maturity claims....

1. the company will wait until the claimant comes to office to demand the claim

2. the process is initiated by the company well in advance of the maturity date

3. it is the responsibility of the claimant to approach the company

4. If the claimant does not come within a month the entire maturity amount will be forfeited. Issuance of a

license to a person has been stipulated in................Act

1. Section 43 of the Insurance Act 1939

2. Section 42 of the Insurance Act 1938

3. Section 12 of the Insurance Act 1922

4. Section 34 of the Insurance Act 1932(FDI) in Indian