IR presentation Q1-Q3 2016 - Outotec · • General Manager, Atlas Copco CMT Sweden AB 2008-2011...

61

Sustainable use of Earth’s natural resources IR presentation Q1-Q3 2016

Transcript of IR presentation Q1-Q3 2016 - Outotec · • General Manager, Atlas Copco CMT Sweden AB 2008-2011...

Sustainable use ofEarth’s natural resources

IR presentationQ1-Q3 2016

© Outotec – All rights reserved

Safety performance in Q1-Q3/2016

OUTOTEC IR presentation2 Q1-Q3 2016

0

1.4(2015: 2.8)

1,232

Fatal accidents

Lost-Time Injury Rateper million hoursincl. employees andsubcontractors

13 Lost time injuries reported Reported near misses

© Outotec – All rights reserved

Markku Teräsvasara, Outotec’s CEO since October 1, 2016

Q1-Q3 2016 OUTOTEC IR presentation3

Work experience• President, Atlas Copco Mining and Rock Excavation

Service Division, Sweden 2014-9/2016• President, Atlas Copco Surface Drilling Equipment

Division, China 8/2011-2013• General Manager, Atlas Copco CMT Sweden AB 2008-2011• Vice President, Marketing Atlas Copco, Surface

Drilling Equipment (SDE) division 2004-2008• Product Manager, Atlas Copco Rock Drilling

Equipment division, Underground Equipment 2001-2004• Product Manager, Atlas Copco CMT Finland

(Customer Center) 1997-2001• Project Manager and Senior designer, Insinööritoimisto

Pitkälä Oy & Pitla Oy 1994-1997(Partner & Member of the Board 1994 - 2001)

• Designer, Insinööritoimisto Lauri Pitkälä Oy, Finland 1990-1993• Designer, Nord-engineering Oy, Turku, Finland 1988-1990

Born 1965B.Sc. Civil engineeringFinnish citizen

© Outotec – All rights reserved

Interaction

Speed

Clear visionand strategy Transparency

I believe in

Q1-Q3 2016 OUTOTEC IR presentation4

© Outotec – All rights reserved

First impressions on Outotec

Q1-Q3 2016 OUTOTEC IR presentation5

Clear vision andstrategy

Good technologicalexpertise

70 M€ savings planprogressing as planned,

work with internalefficiency will continue

Large installed baseto build service

business on

© Outotec – All rights reserved

Based on my first impressions, these are our opportunities

Q1-Q3 2016 OUTOTEC IR presentation6

We can take Outotec back to profitable growth!Stability

Profitability

Growth

• Achieve profitable service growth throughimproved service offering

• Increase profitability by modularization andsourcing

• Establish mid-and high-tier product andservice portfolio

• Engaged, clear and sustainable organization• Customer driven sales and delivery

capabilities

© Outotec – All rights reserved

Outotec at a glance

Q1-Q3 2016 OUTOTEC IR presentation7

Key figures

Financial performance

Geographic coverage

Business overview

740

1,0001,218

878 970

1,386

2,0871,912

1,4031,201

0

2

4

6

8

10

12

0

400

800

1200

1600

2000

2400

2006 *) 2007 2008 2009 2010 2011 2012 2013 2014 2015

Sales Operating profit margin

*) Combined basis 2010 onwards adj. EBIT, excl. restructuring and acquisition-related costs as well as purchase price allocation amortizations.

EUR million %

FY 2015 FY 2014

Net Sales, EUR million 1,201 1,403

Share of services in sales, % 43 37

Gross Margin, % 28 23Adjusted EBIT, % (excl. one-time items) 4.7 4.0Gearing, % 9.9 -1.3

Equity ratio, % 31.1 36.1Balance sheet total, EUR million 1,531 1,442

• Outotec is a global leader in minerals and metals processingtechnology, deliveries to more than 80 countries

• Outotec designs and delivers tailored solutions for minerals andmetals processing, water treatment, and producing energy frombiomass and wastes

• Company develops technologies which utilize natural resources,raw materials, energy and water efficiently, and minimize the plant’slifetime costs

• HQ in Finland, some 4,200 employees (Q3/2016) in 34 countries

Outotec R&D, sales and service centersOutotec manufacturing/assembly

© Outotec – All rights reserved

A century of accumulated expertise 1/2

October 28, 2016 OUTOTEC IR presentation8

© Outotec – All rights reserved

A century of accumulated expertise 2/2

October 28, 2016 OUTOTEC IR presentation9

© Outotec – All rights reserved

10

Minerals Processing segment’s offering

A complete portfolio of leading process solutions and services with full plant delivery capability

WaterTechnology

FLSmidth, CITIC,Metso,ThyssenKrupp

FLSmidth, Metso,BGRIMM, Tenova,Woodgrove

FLSmidth, Tenova-Delcor, WesTech

Aqseptence-Diemme, Metso,Andritz, FLSmidth

Thermo Fisher,BGRIMM, Blue Cube

APC: Metso,Woodgrove, SGSMinerals

DCS: Major DCSsuppliers

FLSmidth, Golder,GR Engineering,AMC

Customers ownmaintenance,Major tech.suppliers, Localcompanies

Thickening AnalyzersGrinding Flotation AutomationFiltering ServicesTailings management

1,100 grindingmills delivered,strong in S/Msize mills andprocesstechnology

10,000 flotationunits deliveredsince 1960s,bigcell technologyreferences,automation

1,800 thickenersdelivered, globalprojectexecutioncapability,feedwell design

Full analyserportfolio, lowestmin detectionlimits, only Xrayused

Uniquecombination ofautomation &analysers,important for riskmanagement

Full processand equipmentportfolio,effluenttreatment andbackfill plants

Prop equipmentand totalprocessknowhow,global servicenetwork

3,500 filtersdelivered, mostefficientconcentratefiltering, provenperformance

Competition fragmented, a number of players competing in part of the portfolio

Q1-Q3 2016 OUTOTEC IR presentation

© Outotec – All rights reserved

Q1-Q3 2016 OUTOTEC IR presentation11

Industry-leading technologies, process solutions and services

Metals, Energy & Water segment’s offering

Ferrous metals Sulfuric acid/Off-gas/Roasting

Fives, FLSmidth,Metso,Aqseptence-Diemme

Kobelco, Metso,Primetals, Jemeco

SMS Siemag,Tenova, Jemeco

GEA Bischoff,MECS

Alumina,Aluminum Base metals (Cu, Ni,

Zn, Au, Ag, PGM)Ferroalloys

GlencoreTechnology, Tenova

Leader in CFBAluminiumCalcination andHOT TubeDigestion

Over 60% of theworld’s pelletsmade withtravelling gratetechnology

650 acid plantsand 270 non-ferrous roastingplants

Leader in Cusmelting, anodecasting, SX and Znleaching, strong inNi smelting andEW

Energy Water

Alumina calciner,Green anode plants,

Rod Hop

Sintering, Pelletizing,Direct Smelting

Sulfuric acid plant,Roasting

Smelting, Converting,Leaching, SX/EW,

electrorefining

Smelting,Preheating, Steel

Belt Sintering

Waste-to-energy,Sludge incineration,Oil shale processing

Industrial watertreatment, municipal

water systems

Competition fragmented, a number of players competing in part of the portfolio

Services

Advisory, maintenance,operations & remoteservices, upgrades

Valmet, Andritz,Babcock&Wilcox

Veolia, GE Water,Suez

FLSmidth, Metso,major tech suppliers,locals and customers

Leader in FerroChrome, 20pelletizing andsinter plants and9 smelters forferroalloys

Versatile waste-to-energysolution, over250 materialsused

Effluenttreatment plants,backfill plants,water recycling

Shutdownservices, bestsuited to provideservices for owntechnologies

© Outotec – All rights reserved

Long-term customer relationships with the industry’s topcompanies

Q1-Q3 2016 OUTOTEC IR presentation12

In history, top ten customers have accounted for some 35% of sales.

Major global mining companies Local mining and metallurgicalcompanies in emerging regionsIntermediate sized companies

Selected reference customers of Outotec

© Outotec – All rights reserved

Offering industry’s most sustainable processing technologies

Q1-Q3 2016 OUTOTEC IR presentation13

343545

2015

6,600

2014

5,900

2013

5,400

Our handprint is bigger than our footprintThousands of tons of CO2-equivalent

Footprint: Outotec’s greenhouse gas emissions

Handprint: Greenhouse gas emissions avoidedthrough use of Outotec’s technologies

The 3rdmost

sustainablecompany in the

world (2016)

EnvironmentalGoods and

Services equals

to 90% oforders (2014-15)

© Outotec – All rights reserved

Metals demand is forecasted to grow 2-4%

Q1-Q3 2016 OUTOTEC IR presentation14

SUPPLY DEMAND2016F

Production, Mt2016F

Consumption, MtCAGR%

2015-25EIncrease,

Kt/aAluminium 57,8 57,6 2,7 % 1692

Copper 22,5 22,3 1,8 % 419Zinc 14,0 14,5 2,4 % 367

Nickel 2,0 1,9 1,4 % 29

Source: Wood Mackenzie, Morgan Stanley, Outotec analysis

Share of Outotec sales byend product

* Incl. water, sulfuric acid and off-gas

6%4%4%

8%

8%

4%7%

11%

17%

32%

Others

Copper

Precious Metals

Zinc

Aluminium

Ferroalloys

Iron

Nickel

Other Metals

2015

Energy and environmentalsolutions*

© Outotec – All rights reserved

Deep downcycle expected to turn into a decent growth

Q1-Q3 2016 OUTOTEC IR presentation15

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

110 000

120 000

130 000

140 000

150 000

2019 2020201820172016201520142013201220112010

30 000

+8%

-51%

Sustaining capex

Including greenfieldand brownfield expansion

Total Capex per type, MUSD

Project visibility gap

Source: Woodmac, June 2016

© Outotec – All rights reserved

Maintenance Capex to remain flat, expansion Capexexpected to grow esp. in copper, gold, zinc and nickel

Q1-Q3 2016 OUTOTEC IR presentation16

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

0%-25%

Copper

Gold

Iron Ore

NickelZincAluminiumAluminaLead

202020192018201720162015201420132012201120100

5 000

10 00015 00020 000

25 00030 000

35 00040 00045 000

50 00055 00060 000

65 00070 00075 000

80 00085 000

90 00095 000

100 000

105 000110 000

20152014201320122011 201820172010 2016

+14%

-63%

Copper

GoldIron OreAluminiumNickelZincAluminaLead

20202019

Sustaining capexper metal

Expansion capexper metal

Project visibility gap

Source: Woodmac, June 2016

© Outotec – All rights reserved

Mining and metals production country ranking – Cu, Zn, Ni

Q1-Q3 2016 OUTOTEC IR presentation17

© Outotec – All rights reserved

Mining and metals production country ranking – Al, Au, Fe

Q1-Q3 2016 OUTOTEC IR presentation18

© Outotec – All rights reserved

Long-term financial targets - Road map to 2020

Q1-Q3 2016 OUTOTEC IR presentation19

10%2020

2-3%2016

aEBIT* aEBIT*

ServicesR&D,Design-to-cost

Bestcostcountrysourcing

Efficiency

Annual averageservice sales growth5-15% (incl. M&A)

Gearing at max 50%

* Excluding restructuring and acquisition-related costs as well as purchase price allocation amortizations.

© Outotec – All rights reserved

Service sales target

Q1-Q3 2016 OUTOTEC IR presentation20

Grow performance services

Grow spare & wear parts business

Strengthen service capabilities and intensity

Customers need services that improve productivity and reduce opex

Average growth 5-15%(June 7, 2016)

31% 40%+O

VE

RTH

EC

YCLE

Services % of sales

currenttarget

Spare parts

Technical services

Modernizations

Shutdown services

O&M (incl. spare parts)

Split in services, 2015

© Outotec – All rights reserved

Q1-Q3 2016 financial information

Q1-Q3 2016 OUTOTEC IR presentation21

© Outotec – All rights reserved

Signs of recovery in minerals processing market,environment challenging for metals refining market

Q1-Q3 2016 OUTOTEC IR presentation22

MinMetcompaniescontinued toinvest intheir existingplants withfast returns.

Smallerequipmentorderspicked up

Interest intechnologiesthat minimizeenvironmentalimpacts

Customersfocus onefficientinventory andcash flowmanagement.

Gold,copper,nickel andzinc projectswere mostactive.

© Outotec – All rights reserved

Q3 in a nutshell

Q1-Q3 2016 OUTOTEC IR presentation23

• Customers’ large investmentsare still developing slowly.

• Weak performance in certainprojects in the Metals, Energy &Water impacted profitability andcash flow.

• Savings program proceeds asplanned, fixed costs reduced by26%.

• Order intake increased in theMinerals Processing segment.

+

_

© Outotec – All rights reserved

Order intake in the Minerals Processing picked up

Q1-Q3 2016 OUTOTEC IR presentation24

EMEA

51%APAC

20%

535389

387

336

0

100

200

300

400

500

600

700

800

900

Q1-Q3/2015 Q1-Q3/2016

Serviceorders

Capexorders

AMERICAS

29%

Process equipment forGoldcorp,MexicoApprox. 23 M€

2 mine backfill plants,Philippines andAustraliaApprox. 20 M€

Process equipment forgreenfield gold project,SenegalApprox. 10 M€

Flotation anddewatering technology,RussiaApprox. 30 M€

Modular flotation cPlantfor Ma’aden Gold,Saudi Arabia< 10 M€

2 modular solventextraction plants,Macedonia and Egypt25 M€

© Outotec – All rights reserved

Stable order backlog

Q1-Q3 2016 OUTOTEC IR presentation25

€ million

Iranian projectsnot included in

Q3 end backlog:EUR 200 (230)

million

240

371

235168

493418

384299

475

260

120139 106202

111

419 350269

357 344

532

803

327425

736

452 471 491366

230

426

210

380266 322

260

395

268 267

170

281 274

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

Q2/

2006

Q3/

2006

Q4/

2006

Q1/

2007

Q2/

2007

Q3/

2007

Q4/

2007

Q1/

2008

Q2/

2008

Q3/

2008

Q4/

2008

Q1/

2009

Q2/

2009

Q3/

2009

Q4/

2009

Q1/

2010

Q2/

2010

Q3/

2010

Q4/

2010

Q1/

2011

Q2/

2011

Q3/

2011

Q4/

2011

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Q1/

2015

Q2/

2015

Q3/

2015

Q4/

2015

Q1/

2016

Q2/

2016

Q3/

2016

Order backlog at the end of the period Share of unannounced orders Order intake by quarter

RoughlyEUR 300

million of theQ3 end backlogto be delivered

in 2016

EUR 1,030

million, -8%

© Outotec – All rights reserved

Weak performance in certain projects impacted profitability

Q1-Q3 2016 OUTOTEC IR presentation26

EUR million Q32016

Q32015

Q1-Q32016

Q1-Q32015

Change,%

Incomparablecurrencies

Sales 245 307 753 895 -16% -12%Service sales 105 129 320 373 -14% -8%Share of services in sales, % 43 42 42 42Gross Margin, % 24 28 25 28Adjusted EBIT* 2 15 2 38Adjusted EBIT*, % 1 5 0 4- Restructuring and acquistion-related costs -1 -6 -10 -13- PPA amortization -2 -2 -6 -7EBIT -1 7 -14 18EBIT, % -0 2 -2 2Profit for the period -3 2 -17 6* Excl. restructuring and acquisition-related costs and PPA amortizations.

© Outotec – All rights reserved

Profitability impacted by additional project provisionsbooked in Q3

Q1-Q3 2016 OUTOTEC IR presentation27

Adjusted EBITQ1-Q3 2016

2 M€

OtherFixed costdecrease*

Provision impact2015 & 2016

Sales decreaseAdjusted EBITQ1-Q3 2015

38 M€

*Decline yoy 21% (in comparable currencies 20%)

© Outotec – All rights reserved

Minerals Processing

Q1-Q3 2016 OUTOTEC IR presentation28

0%2%4%6%8%10%12%14%16%18%20%

050

100150200250

300350

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Q1/

2015

Q2/

2015

Q3/

2015

Q4/

2015

Q1/

2016

Q2/

2016

Q3/

2016

Sales EBIT*, %

Sales and adjusted EBIT development

• Order intake grew 18%• Sales decreased 10% mainly due to decline in

spare part orders and low order intake in thelatter part of 2015 and H1/2016

• Achieved fixed cost savings balanced out thelower sales

Minerals ProcessingEUR million

Q1-Q32016

Q1-Q32015

Change,%

Change incomp

currency, %Order intake 462 393 18 26Sales 361 402 -10 -5Service sales 197 229 -14 -7Adjusted EBIT*) 22 19Adjusted EBIT*), % 6 5Unrealized and realized lossesrelated to valuation of FXforward agreements

-1 -3

* Excl. restructuring and acquisition-related costs and PPA amortizations

© Outotec – All rights reserved

-10%

-5%

0%

5%

10%

15%

050

100150200250300350400

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Q1/

2015

Q2/

2015

Q3/

2015

Q4/

2015

Q1/

2016

Q2/

2016

Q3/

2016

Sales EBIT*, %

Metals, Energy & Water

• Customers’ large investments develop slowly• Decline in plant orders and low service volumes• Lower sales and weak performance in certain

projects weakened the segment’s profitability• More saving actions ongoing

Q1-Q3 2016 OUTOTEC IR presentation29

Metals, Energy & WaterEUR million

Q1-Q32016

Q1-Q32015

Change,%

Change incomp

currency, %Order intake 263 530 -50 -49Sales 392 494 -21 -18Service sales 122 145 -15 -10Adjusted EBIT*) -17 24Adjusted EBIT*), % -4 5Unrealized and realized lossesrelated to valuation of FXforward agreements

-3 -1

* Excl. restructuring and acquisition-related costs and PPA amortizations

Sales and adjusted EBIT development

© Outotec – All rights reserved

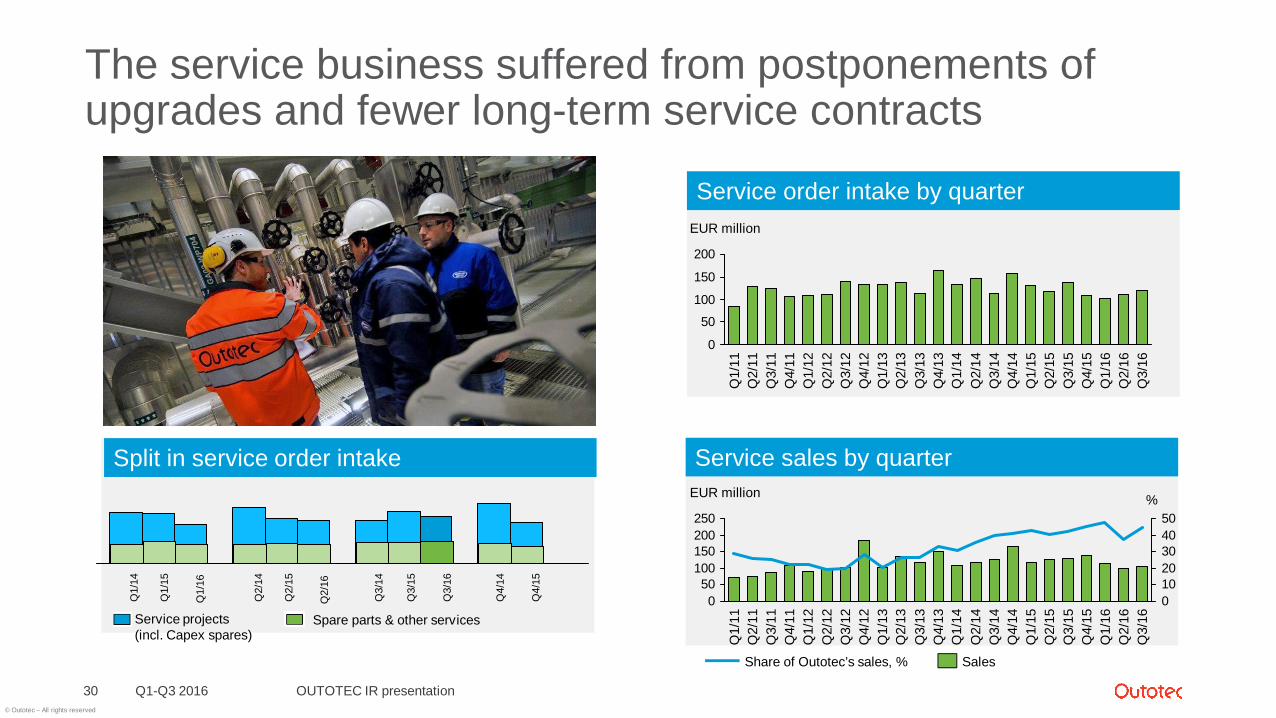

Service order intake by quarter

0

50

100

150

200

Q4/

13Q

3/13

Q2/

13Q

1/13

Q4/

12Q

3/12

Q2/

12Q

1/12

Q4/

11Q

3/11

Q2/

11Q

1/11

Q3/

16Q

2/16

Q1/

16Q

4/15

Q3/

15Q

2/15

Q1/

15Q

4/14

Q3/

14Q

2/14

Q1/

14

EUR million

The service business suffered from postponements ofupgrades and fewer long-term service contracts

Q1-Q3 2016 OUTOTEC IR presentation30

Service sales by quarterSplit in service order intake

050

100150200250

01020304050

EUR million %

Q3/

16Q

2/16

Q1/

16Q

4/15

Q3/

15Q

2/15

Q1/

15Q

4/14

Q3/

14Q

2/14

Q1/

14Q

4/13

Q3/

13Q

2/13

Q1/

13Q

4/12

Q3/

12Q

2/12

Q1/

12Q

4/11

Q3/

11Q

2/11

Q1/

11

SalesShare of Outotec’s sales, %

Spare parts & other servicesService projects(incl. Capex spares)

Q1/

14

Q1/

15

Q2/

14

Q2/

15

Q3/

14

Q3/

15

Q4/

14

Q4/

15

Q1/

16

Q2/

16

Q3/

16

© Outotec – All rights reserved

Change in cash flow due to projects under execution tying up morecapital, lack of large advance payments, restructuring-related costs

Q1-Q3 2016 OUTOTEC IR presentation31

EUR million Q1-Q32016

Q1-Q32015

Cash from operations 31 43Change in working capital -94 -10Interest -5 -3Taxes -4 -8

NET CASH FROM OPERATING ACTIVITIES -73 22

Capital expenditure -16 -43Acquisitions -3 -28Other investing activities 2 0

CASH FLOW AFTER INVESTING ACTIVITIES -90 -49

Cash and cash equivalents 265 267

© Outotec – All rights reserved

Liquidity and equity remained solid

Q1-Q3 2016 OUTOTEC IR presentation32

Q32016

Q32015

Q42015

Net interest-bearing debt, EUR million -21* 74 40

Gearing, % -4* 17 10

Equity-to-assets ratio, % 42* 32 31

Return on investment, %, LTM -6 4 -1

Return on equity, %, LTM -8 1 -4

Working capital at the end of the period, EUR million -10 -12 -89

Advances received 207 205 232

Equity, EUR million 534 426 405

Balance sheet total, EUR million 1,482 1,527 1,531* If the hybrid bond (EUR 150 million) were treated as a liability equity-to-assets ratio would be 30%, gearing34%, and net interest-bearing debt EUR 129 million.

© Outotec – All rights reserved

Fixed cost savings achieved as planned

33 Q1-Q3 2016 OUTOTEC IR presentation

• Target is EUR 70million annual fixedcost reductioncompared to Q1-Q3/2015 run rate.

• Of this, EUR 56million was reachedin Q1-Q3/2016.

Fixed cost Fixed cost2015 2016

278

348

84

95

82

Q2

Q1

Q3

Total Q1-Q3Annualized

Target fixed cost level

62

69

74

Cumulativesavings

8

34

56

We are actively working on improving our performance, especially inthe Metals, Energy & Water segment.

© Outotec – All rights reserved

Key events after September 30, 2016

Q1-Q3 2016 OUTOTEC IR presentation34

October 4Outotec announced representatives forOutotec's Nomination Board fromSolidium, Varma and Ilmarinen, and theChairman of the Board.

October 1New CEO Markku Teräsvasarastarted to work at Outotec.

October 24

Kalle Härkki, D.Sc. (Tech.), wasappointed President of Metals,Energy & Water business unit.

October 10

Outotec celebrated its 10th

anniversary and launched historybook "150 years' evolution toward agreener future - the Outotec story“.

© Outotec – All rights reserved

We expect increased activity in minerals processing tocontinue, metals refining markets to remain weak

Q1-Q3 2016 OUTOTEC IR presentation35

Increased interest in technologies thatminimize environmental impacts.

Customers’ need for productivityimprovement creates opportunities forOutotec’s performance solutions.

Markets in the Middle East, Southand Central America, and Russiaare expected to continue active.

The scarcity andcost of water aswell as need toimproveemission controldrive processmodernizations.

Development of gold, copper, nickel,and zinc projects are expected tocontinue more active than aluminumand iron.

Waste-to-energy solutionsmarket is volatile, asdecisions depend onsubsidies andenvironmental regulations.

© Outotec – All rights reserved

Sales guidance is narrowed and due to the continued challenges in the Metals, Energy &Water segment adjusted EBIT is expected to be at the lower end of the guidance range:

Financial guidance for 2016 narrowed

Q1-Q3 2016 OUTOTEC IR presentation36

Expected salesfrom Q3

order backlog(incl. services)

~EUR 300 million

Salesfrom new

order intake(incl. services)

+=Sales will be

approx.EUR 1.0 - 1.1 bn

(previously 1.0-1.2)

Adjusted EBIT*

will be approximately 2 – 3% (previously 2 – 4%)

* Excluding restructuring and acquisition-related costs as well as purchase price allocation amortizations.

+Sales from Q1-Q3EUR 753 million

© Outotec – All rights reserved

Profitability roadmap from 2015 to 2016

Q1-Q3 2016 OUTOTEC IR presentation37

DepreciationProvisionimpact

Savings* Sales reduction,market risk

aEBIT 2015 aEBIT 2016e

*Incl. cost structure program and other actions

Guidance upperboundary 3%

Guidance lowerboundary 2%

© Outotec – All rights reserved

Interest bearing loans and hybrid bond, repayment profile

Q1-Q3 2016 OUTOTEC IR presentation38

© Outotec – All rights reserved

More mature backlog ties more capital

Q1-Q3 2016 OUTOTEC IR presentation39

• Working capital is driven by OrderIntake due to advance payments

• Capex is expected to decreasefrom past years

• Cash flow typically stronger in H2than in H1

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

-300

-200

-100

0

100

200

300

Dec2009

Dec2010

Dec2011

Dec2012

Dec2013

Dec2014

Dec2015

Sep2016

Working Capital CAPEX Free cash flow Book-to-bill

© Outotec – All rights reserved

POC and cashflow profile example

Q1-Q3 2016 OUTOTEC IR presentation40

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27POC Cumulative cashflow

MEUR

Month

Total order backlogstructure in 2012

Total order backlogstructure in 2015

0% 100%

Percentage of Completion, %

Timing of large projectcompletions, andpossible release ofprovisions, affectsquarterly earnings.

Advancepayment~10-30%

NOTE: The figures are illustrative and vary project by project

Timing of large project completions affects quarterly earnings

© Outotec – All rights reserved

Equity to assets ratio, gearing and liquidity at healthylevels

Q1-Q3 2016 OUTOTEC IR presentation41

171 291 318 258 280 403 359 324 282 301Cash at hand

Equity toassets

Gearing

265

-160

-140

-120

-100

-80

-60

-40

-20

0

20

0

5

10

15

20

25

30

35

40

45

50

Dec2006

Dec2007

Dec2008

Dec2009

Dec2010

Dec2011

Dec2012

Dec2013

Dec2014

Dec2015

Sep2016

© Outotec – All rights reserved

Customer solutions

Q1-Q3 2016 OUTOTEC IR presentation42

© Outotec – All rights reserved

Laiva Gold mine in FinlandCustomer case, ore sorting

Q1-Q3 2016 OUTOTEC IR presentation43

Outotec solution• Outotec sensor-based ore

sorting solution removingwaste rock and improving thehead grade.

• When waste rock is removedthere is less ore feed to thecrushing and grinding circuit,reducing energy and waterconsumption

Customer challenge• Mine is closed because of low head

grade ore• Study completed around Outotec ore

sorting solution considering reopeningthe mine

Study indicates that the Outotec ore sorting solutionenables reopening the mine:

“The economic assessment for the Laiva Gold Mineindicated the potential for restarting the site, whichcan be operated on a long-term basis at a broadrange of commodity prices. Base-case net presentvalue of €77 million, producing 529,000 troy ouncesof gold over a seven-year mine life.”

© Outotec – All rights reserved

Reducing mill downtime at a gold mineCustomer case, comminution

Q1-Q3 2016 OUTOTEC IR presentation44

Customer challenge• Excessive grinding mill downtime during the year

leading to decreased yearly production• Unplanned mill downtime due to liner failure• Inadequate tooling• Limited reline shutdown planning• Coordination between different maintenance

vendors• In total of over 340 hours downtime

due to mill maintenance

Outotec solution• Pre shutdown planning• Liner redesign – to reduce the number of pieces• Tooling improvements – liner handler, skid steers & hand tooling• Changes to liner fixtures & fittings• Continuous Improvement Program• Optimizing liner life time through Outotec patented MillMapper™ software

Customer benefits• 50% less downtime due to mill

maintenance• In total a reduction of 170 hours

of reline incurred downtime• Safer, less labor intensive relines• Circa 12-14 million USD in

additional production revenue

© Outotec – All rights reserved

HIGmillTM fine grinding for FQM KevitsaCustomer case, comminution

Customer challenges• Fine valuable minerals

and difficult to recover• 12% copper not

recovered in coppercircuit due to poorliberation

• If liberation poor,copper-nickelseparation insufficient

• Existing plant in arcticcircle with limitedfootprints

Q1-Q3 2016 OUTOTEC IR presentation45

Outotec solution• Mineral analysis showed very fine grind < 20 micron required for

copper & nickel liberation• Outotec conducted laboratory HIGmill fine grinding and mineral

recovery (flotation) tests• HIGmill chosen as most energy efficient and smallest footprint

technology on market today which would improve mineral recoveryand grade

• Installation & commissioning only 2 weeks in Feb 2015• Outotec provided ramp-up and operation support

Customer benefits• HIGmill improved overall plant performance• Copper loss to nickel circuit improved from 12% to 8%• Overall copper recovery increased by up to 1.5%

• 1.5% increase represents around $1million increase in finalcopper value, after smelting and refining to produce LME gradecopper

• Improved concentrate grades• Less nickel in final copper concentrate• Less copper in final nickel concentrate

• Installed & commissioned without effecting production• HIGmill allowed coarser primary grind and hence higher plant

throughput• More metal out of same ton of ore < 2 year payback

© Outotec – All rights reserved

Turn-key flotation retrofit with fast turnaroundCustomer case, flotationCustomer challenge• Poor flotation performance in terms of copper and gold recovery• Flotation circuit had poor availability• Substantial maintenance requirements• Limited time available for shutdown

Q1-Q3 2016 OUTOTEC IR presentation46

Customer benefits• Greater stability and control of flotation cells• Significantly decreased energy consumption

with Outotec cells (40%)• Minimized production losses during

installation and commissioning• Increased flotation circuit availability, leading

to increased production• Improved recovery of coarse particles

Outotec solution• In-depth metallurgical assessment identified large improvement potential in the

flotation plant• Retrofit of 10 x 160 m3 flotation cells• A full turn-key delivery• Advanced operator training with Outotec´s Virtual Experience training

© Outotec – All rights reserved

Digitalization creating new growth and opportunities -managing water balance and quality at mine sites

Q1-Q3 2016 OUTOTEC IR presentation47

Solution: Intelligent digital solution for monitoring and managing dataon the mine site’s water balance and quality.

Value: Sustainable balance of water supply and consumption,while stabilizing production and reducing business risks.

Onlinemonitoring

Digitalplatform

Modeling &simulation

Predictability& reliability

Accessto water

Alternativewater

sources

Stableprocess

Mitigationof risks

Licenseto

operate

© Outotec – All rights reserved

Holistic process water management reducesoperational risks, OPEX and effluents

Q1-Q3 201648

With higher closure rate• Reducing raw water need• Reducing process variations to improve yield• Process water doesn’t need to be potable water grade• At full closure basically no effluents• Less socio-political risk related to fresh water

OUTOTEC IR presentation

* Example of 20 Mt/a Cu concentrator water balancein Chilean climate using paste tailings, price of rawwater 4 USD / m3.

© Outotec – All rights reserved

Holistic tailings management can bring significant costsavings and reduces safety risks

• Holistic tailings management covers bothsurface and underground operations.

• Paste and dry stacking technologiescombined with closed water loops arethe best available technologies forconserving water within the concentratorenvironment.

• The short and long term risks can besignificantly reduced by reducing theamount of water in the surface tailingsstorage facility.

Q1-Q3 2016 OUTOTEC IR presentation49

PASTEBACKFILL

DRYSTACKING

Footprint= 12%OPEX= 37%

PASTE

Footprint= 53%OPEX= 58%

THICKENEDTAILINGS

Footprint= 72%OPEX= 75%

WETTAILINGS

Footprint= 100%OPEX

= 100%

© Outotec – All rights reserved

Codelco Ministro Hales 1/2Customer case, full solution

Q1-Q3 201650

Customer challenges• Ore with very high content of impurities, primarily

arsenic causing challenge in processing

• Commercial terms for the concentrate notfavourable for selling

OUTOTEC IR presentation

Outotec solution• Several studies and test campaigns over the years to identify

best metallurgical solution

• Complete, integrated process which is based on patentedOutotec solutions and technologies and proven Outotecproprietary equipment

• Arsenic levels of the concentrate lowered without loosing sulphur

• Sustainable water and effluent treatment in challengingenvironment

1991

•Codelco and Outotecstart working togetheron solving thechallenges

2010

•Investment decisionmade

2014

•Commissioningcompleted

2016•Official inauguration

© Outotec – All rights reserved

Codelco Ministro Hales 2/2Customer case, full solution

Q1-Q3 2016 OUTOTEC IR presentation51

Partial roasting• Patented Outotec solution which

removes over 90% of the arsenic inthe ore concentrate

• Exceeding 605,000 tpa concentrate(110%)

Gas Cleaning• Outotec’s proprietary gas cleaning

and sulfuric acid productiontechnology eliminates over 99.9% ofthe gaseous emission of the facility.

Effluent Treatment• Outotec’s proprietary effluent treatment technology cleans the process

effluents and recirculates clean water back to the process.

Outotec delivers a complete, integrated solution from a broad portfolio of patented andproprietary solutions, and a long history of process technology

© Outotec – All rights reserved

Norilsk Nickel, Nadezhda Flash Smelting Furnace No.1modernizationCustomer case, modernization

Q1-Q3 201652 OUTOTEC IR presentation

Customer challenge• Changing raw material base requires dealing with low-heat value

and more complex concentrates• Very tight implementation schedule• Supplier responsible for providing Russian Safety Approvals

which is normally out of scope

Outotec solution• Higher capacity feeder and concentrate burner and new furnace

cooling elements and cooling monitoring system based on Outotecproprietary technologies

• Pre-planning and experienced personnel• Extensive performance guarantees combined with a long-term service

contract• Using internal and external resources to obtain Russian Safety

Approvals• Short implementation and down time and fast ramp up after start up

© Outotec – All rights reserved

Pelletizing Segregation SolutionCustomer case, profitability improvement

OUTOTEC IR presentationQ1-Q3 201653

Customer challengeCustomer had a profitability challenge in an iron-orepelletizing plant in Brazil

FuelConsumption

FuelConsumption

ProductivityProductivityProductQualityProductQuality

Outotec solution• Assess to identify improvement potential

• Plant Performance Assessment• CFD Study• Pot Grate Tests

• Design a tailored solution• 3D area scanning• Double Deck Roller Screen basic design• Shutdown planning

• Deliver a holistic, safe & efficient implementation• Detail design for modernization• Retrofit new Outotec Double Deck Roller Screen• Shutdown execution

• Verify & support performance results• Segregation verification test• Energy efficiency test

Delivered Value*

10.5% fuel savingsImproved productivity2,8 M€ annual OPEX savings*6 month payback*

*Value Assumptions: Natural Gas: € 0.37/Nm3, Antracite: € 0.12/kgOnly estimates based on pot grate tests.

© Outotec – All rights reserved

ERZ Zürich, sludge incineration plantCustomer case, waste to energy

Q1-Q3 201654

Customer challenge• Sustainable solution required to treat sewage sludge from the entire canton of Zürich,

Switzerland covering over 70 waste water treatment plants!• March 2013 – public must approve such an investment in a referendum. 96% vote in favor,

project goes ahead• Summer 2015 – commissioning complete and plant goes into operation. October 2015 –

official inauguration.• Limitations for sewage sludge disposal in landfill and as fertilizer• High transport and logistics costs for sludge containing > 70% water• Strict emissions limits with plant location in the heart of Zürich

OUTOTEC IR presentation

Outotec solution• Self-sustaining thermal treatment of sewage sludge without additional fuel.

• Thermal incineration of sewage sludge using Outotec fluidized bed technology• Thermal dryer using heat from the process.

• State-of-the-art flue gas cleaning system• Phosphorus recovery possible from ash

© Outotec – All rights reserved

UK moving to a new renewable energy subsidy scheme

Q1-Q3 2016 OUTOTEC IR presentation55

Ending of the previous subsidyscheme resulted in record highorder intake for Outotec Wasteto Energy solutions for Advancedstaged gasification usingrenewable fuels

6 plants &4 O&M (12-years)

New subsidy scheme continued tobe good for Outotec Waste toEnergy technologies

1 plant,next CFD auction

expected late2016

© Outotec – All rights reserved

Levenseat Renewable ltdCustomer case, waste to energy

Q1-Q3 201656

Customer challenge• UK is exporting high amounts of RDF

to be incinerated in Europe• High landfill cost in the UK

OUTOTEC IR presentation

Outotec solution• Waste to Energy plant in UK• Gasification of waste is an environmentally friendly way of

efficiently converting waste to energy• Reliable and tested solution based on the Outotec Fluidized

bed technology with over 100 references• 2015 Contract signing, 2017 expected start up

© Outotec – All rights reserved

Service offeringbuilding blocks

Performance services

Q1-Q3 2016 OUTOTEC IR presentation57

OperationsServices

AdvisoryServices

MaintenanceServices

RemoteServices

TrainingServices

Spare andWear Parts Upgrades

Decreasedoperating cost

Improved health andsafety

Improvedenvironmental

efficiency

Improved capitalefficiency

Improved equipmentand process

efficiency

Our solutionstarget toaddresscustomer

challengesand improve

theirperformanceand efficiency

© Outotec – All rights reserved

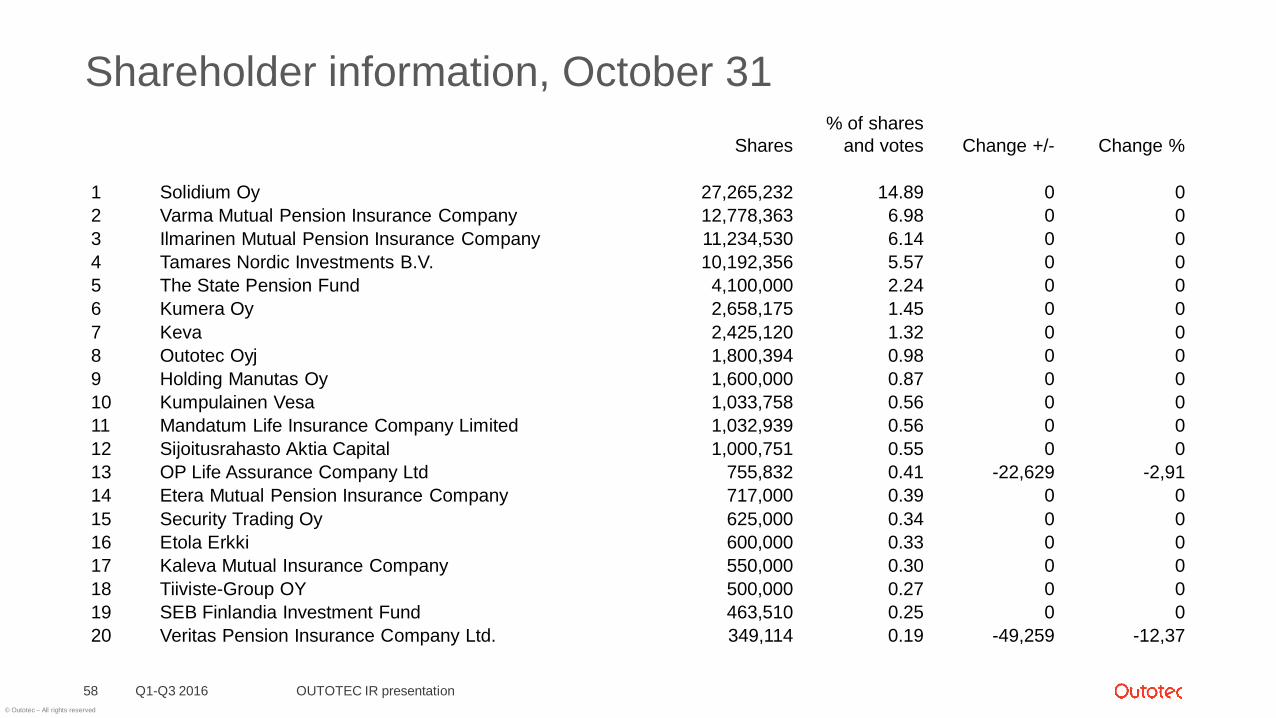

Shareholder information, October 31

Q1-Q3 2016 OUTOTEC IR presentation58

Shares% of shares

and votes Change +/- Change %

1 Solidium Oy 27,265,232 14.89 0 02 Varma Mutual Pension Insurance Company 12,778,363 6.98 0 03 Ilmarinen Mutual Pension Insurance Company 11,234,530 6.14 0 04 Tamares Nordic Investments B.V. 10,192,356 5.57 0 05 The State Pension Fund 4,100,000 2.24 0 06 Kumera Oy 2,658,175 1.45 0 07 Keva 2,425,120 1.32 0 08 Outotec Oyj 1,800,394 0.98 0 09 Holding Manutas Oy 1,600,000 0.87 0 010 Kumpulainen Vesa 1,033,758 0.56 0 011 Mandatum Life Insurance Company Limited 1,032,939 0.56 0 012 Sijoitusrahasto Aktia Capital 1,000,751 0.55 0 013 OP Life Assurance Company Ltd 755,832 0.41 -22,629 -2,9114 Etera Mutual Pension Insurance Company 717,000 0.39 0 015 Security Trading Oy 625,000 0.34 0 016 Etola Erkki 600,000 0.33 0 017 Kaleva Mutual Insurance Company 550,000 0.30 0 018 Tiiviste-Group OY 500,000 0.27 0 019 SEB Finlandia Investment Fund 463,510 0.25 0 020 Veritas Pension Insurance Company Ltd. 349,114 0.19 -49,259 -12,37

© Outotec – All rights reserved

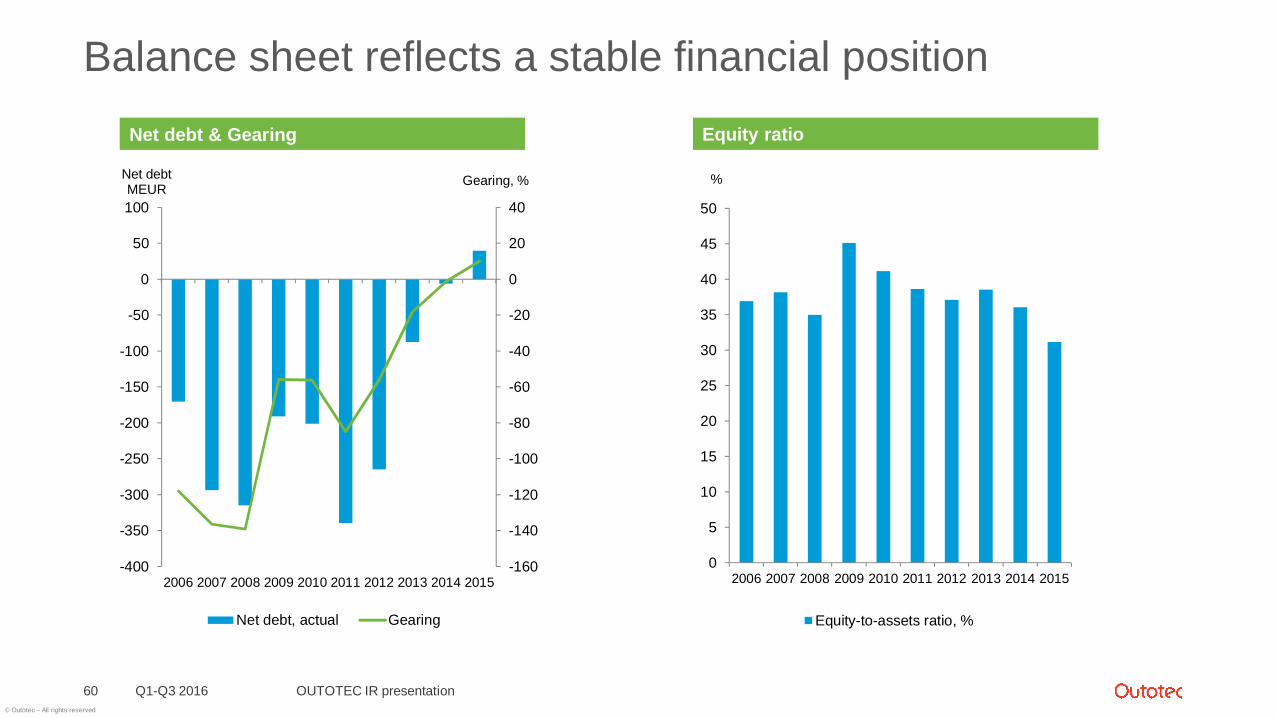

Balance sheet reflects a stable financial position

Q1-Q3 2016 OUTOTEC IR presentation60

-160

-140

-120

-100

-80

-60

-40

-20

0

20

40

-400

-350

-300

-250

-200

-150

-100

-50

0

50

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Gearing, %Net debtMEUR

Net debt, actual Gearing

0

5

10

15

20

25

30

35

40

45

50

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

%

Equity-to-assets ratio, %

Net debt & Gearing Equity ratio

© Outotec – All rights reserved

Q1-Q3 2016 OUTOTEC IR presentation61