Ipsen 2015 Full Year Financial Results - Homepage - … pour nom de la société - 07/04/2011 / page...

34

Full Year Results Roadshow - London, March 9, 2016 Ipsen 2015 Full Year Financial Results

Transcript of Ipsen 2015 Full Year Financial Results - Homepage - … pour nom de la société - 07/04/2011 / page...

IPSEN pour nom de la société - 07/04/2011 / page 1

Full Year Results Roadshow - London, March 9, 2016

Ipsen 2015 Full Year Financial Results

2 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 2 2

Disclaimer This presentation includes only summary information and does not purport to be comprehensive. Forward-looking statements, targets and estimates contained herein are for illustrative purposes only and are based on management’s current views and assumptions. Such statements involve known and unknown risks and uncertainties that may cause actual results, performance or events to differ materially from those anticipated in the summary information. Actual results may depart significantly from these targets given the occurrence of certain risks and uncertainties, notably given that a new product can appear to be promising at a preparatory stage of development or after clinical trials but never be launched on the market or be launched on the market but fail to sell notably for regulatory or competitive reasons. The Group must deal with or may have to deal with competition from generic that may result in market share losses, which could affect its current level of growth in sales or profitability. The Company expressly disclaims any obligation or undertaking to update or revise any forward-looking statements, targets or estimates contained in this presentation to reflect any change in events, conditions, assumptions or circumstances on which any such statements are based unless so required by applicable law. All product names listed in this document are either licensed to the Ipsen Group or are registered trademarks of the Ipsen Group or its partners. The implementation of the strategy has to be submitted to the relevant staff representation authorities in each country concerned, in compliance with the specific procedures, terms and conditions set forth by each national legislation.

Safe Harbor The Group operates in certain geographical regions whose governmental finances, local currencies or inflation rates could be affected by the current crisis, which could in turn erode the local competitiveness of the Group’s products relative to competitors operating in local currency, and/or could be detrimental to the Group’s margins in those regions where the Group’s drugs are billed in local currencies. In a number of countries, the Group markets its drugs via distributors or agents: some of these partners’ financial strength could be impacted by the crisis, potentially subjecting the Group to difficulties in recovering its receivables. Furthermore, in certain countries whose financial equilibrium is threatened by the crisis and where the Group sells its drugs directly to hospitals, the Group could be forced to lengthen its payment terms or could experience difficulties in recovering its receivables in full. Finally, in those countries in which public or private health cover is provided, the impact of the financial crisis could cause medical insurance agencies to place added pressure on drug prices, increase financial contributions by patients or adopt a more selective approach to reimbursement criteria. All of the above risks could affect the Group’s future ability to achieve its financial targets, which were set assuming reasonable macroeconomic conditions based on the information available today.

3 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 3 3

Agenda

1 2015 overview

3 Cabozantinib in-licensing and outlook

2 2015 financial performance

2015 overview

5 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 5 5

Ipsen, an international specialty pharma company

~77%

~23%

FY 2015 sales by segment

Primary care

FY 2015 sales by geography

38% 37%

11% 14%

Europe G5

Developed RoW

Emerging markets

US

Specialty care

Building a credible and profitable footprint in the US

1 France

2 China

4 Germany

3 US

5 Italy

Top 5 affiliates

Note: ROW: Rest of World

One of the largest emerging market presence in the industry

6 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 6 6

Implementation of a refocused strategy in specialty and primary care

Strong operational performance driven by US turnaround

Key execution milestones

1

2

New corporate governance model with search for new Chief Executive Officer 3

7 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 7 7

A refocused strategy to sustain high sales and profit growth

Note: GI:Gastrointestinal; OTx:Dual channel approach (Rx/OTC); NET: Neuroendocrine tumors

Lead

Reinforce

Explore

Specialty care

NET Spasticity Dysport®

aesthetics

Urology-oncology

Adult endocrinology

GI/orphan cancers

Niche strategy

Optimize

Diversify

Expand

Primary care

Smecta® Forlax® Tanakan®

Adjacent GI Probiotics

Geographies

Move to OTx commercial model

8 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 8 8

Specialty Care - Drug sales(2)

Core Operating margin ≥ 22.0%

Primary Care - Drug sales(2)

≥ 14.0%

[-3.0% ; 0.0%]

22.3%

+14.4%

-1.1%

2015 guidance(1)

2015 actuals

2015 sales and Core Operating Income strong performance in line with market guidance

(1) Revised on 31 July 2015 – (2) Year-on-year sales growth at constant currency

9 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 9 9

Turnaround of the US platform, with high potential for growth

(1) Restated for Increlex® supply interruption Note: All growth rates at constant currency; AUL: Adult Upper Limbs; NET: Neuroendocrine tumors;

US affiliate sales growth(1) Somatuline® US sales growth

2013 2014 2015

11.5%

31.2%

64.9%

2013 2014 2015

18.6% 28.6%

111.9%

Business update

Renewed management and Salesforce (NET & spasticity)

Successful Somatuline® NET launch and preparation of Dysport® AUL spasticity launch

Strong Dysport® aesthetics performance from Galderma

US operations profitable in 2015, ahead of plan

2015 financial performance

11 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 11 11

40

52

115

17

20

60

280

334

402

Forlax

Tanakan

Smecta

Hexvix

Increlex

Nutropin

Dysport

Decapeptyl

Somatuline®

®

®

®

®

®

®

+1.4%

(10.2%)

+34.2%

+9.7%

(11.2%)

®

+42.2%

+6.6%

Excellent 2015 sales growth with strong Q4

Drug sales – FY 2015 in million euros – % excluding foreign exchange impact

French Primary care: (7.7%)

International Primary care: +1.2% 1.4%

Group sales €1,443.9m

+10.4%

Primary care €329.7m(1)

(1.1%)

(1) Includes €24.3m of Drug-related sales

Spec

ialty

car

e Pr

imar

y ca

re

® Specialty care €1,114.2m

+14.4%

+1.3%

Positive Primary care international growth despite headwinds in China/Russia

Somatuline® NET and Dysport ® aesthetics driving specialty care growth

12 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 12 12

FY sales in million euros

1,275

1,444

102

25 4 9 (7) 3 33

FX

Primary care

FY 2015 FY 2014

Decapeptyl®

Other Primary

care

Group sales growth: +10.4% (€136m) at constant currency

French PC

Specialty care

93% of FY15 sales growth(1) stemming from Somatuline® and Dysport®

Dysport®

Somatuline®

Other Specialty

care

€33m positive FX impact on 2015 sales

(1) Excluding FX

13 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 13 13

Strong Somatuline® 2015 performance, driven by successful NET launch

247 288

402

2013 2014 2015

+16.8%

Business update

3-year growth 2015 performance

Geographic distribution (2015)

Overall acceleration of growth due to NET global launch

Strong growth in North America, up 112% with positive price impact

Double digit growth in Europe, notably in Germany, the UK, Poland and France

42% 28% 18% 12%

G5(1)

Emerging markets(2) United States

Developed RoW

(1) France, Germany, UK, Italy, Spain – (2) Notably includes China, Russia and Brazil Note: all variations at constant exchange rate; NET: Neuroendocrine tumors;

+34.2%

US: Ipsen present in >1 000 accounts, including all 25 major reference centers

Europe: GEP NET approval granted by all European countries

Increased penetration across geographies

14 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 14 14

Somatuline® accelerated NET penetration in the US and Europe

Source: IMS MIDAS + Symphony Healthcare. (1) G5: France, Germany, UK, Spain, Italy; (2) Market share in volume Note: Market definition = long-acting SSAs; NET: Neuroendocrine tumors;

Somatuline® US quarterly data, all indications

0

2

4

6

8

10

12

14

0

10

20

30

40

Q4 2013 Q2 2014 Q4 2014 Q2 2015 Q4 2015

Somatuline® Europe G5(1) quarterly data, all indications

20

25

30

35

40

45

0

10

20

30

40

Q4 2013 Q2 2014 Q4 2014 Q2 2015 Q4 2015

Ipsen reported sales ($m) Market share(2) (%) Ipsen reported sales (€m) Market share(2) (%)

Somatuline® capturing majority of new patients in US and Europe

Increased number of switched patients

12.8% 44.2%

15 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 15 15

Dysport® 2015 performance driven by aesthetics

242 255

280

2013 2014 2015

+8.6%

Business update

3-year growth 2015 performance

Geographic distribution (2015)

Strong Galderma performance in aesthetics in a solid underlying market growth

Solid performance in emerging markets, notably in Russia, Brazil and Australia

Strong US Q4 driven by aesthetics & spasticity launch

G5(2)

Developed RoW United States

Emerging markets(3)

18% 12% 25% 45%

+9.7%

(1) China, India, South Korea (and Indonesia under certain conditions) – (2) France, Germany, UK, Italy, Spain – (3) Notably includes China, Russia and Brazil

Note : all variations at constant exchange rate; AUL: Adult Upper Limbs

Q3 US launch of Dysport® in AUL spasticity and sales force build-up

Setup of European business unit for therapeutics

Galderma partnership expanded to key Asia Pacific territories(1)

16 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 16 16

Dysport® US market share in aesthetics increasing since Galderma takeover

Botox® market

share (%)

Source: GuidePoint - Filler & Toxin Panel

Dysport® US market share in excess of 20% thanks to Galderma’s commercial push

30%

40%

50%

60%

70%

80%

90%

0%

5%

10%

15%

20%

25%

30%

35%

Feb 10 Jun 10 Oct 10 Feb 11 Jun 11 Oct 11 Feb 12 Jun 12 Oct 12 Feb 13 Jun 13 Oct 13 Feb 14 Jun 14 Oct 14 Feb-15 Jun-15 Oct-15

~73%

~22%

~5%

Botox®

Dysport ®

Xeomin®

Dysport® / Xeomin® market share (%)

17 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 17 17

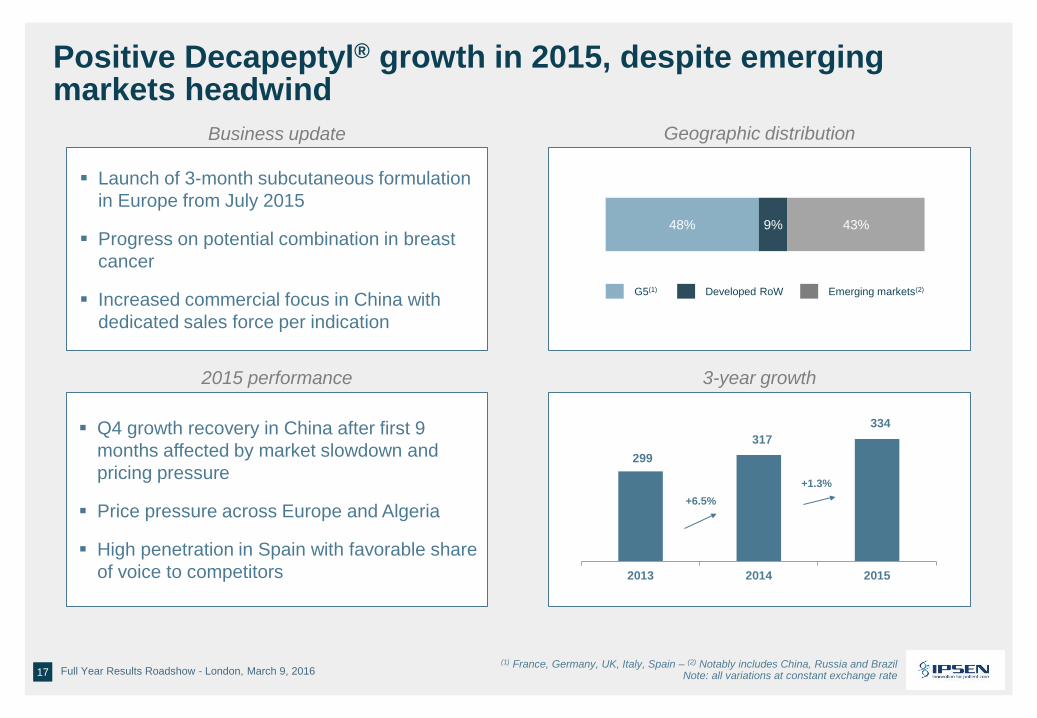

Positive Decapeptyl® growth in 2015, despite emerging markets headwind

299 317

334

2013 2014 2015

+6.5%

3-year growth

Business update

2015 performance

Geographic distribution

Q4 growth recovery in China after first 9 months affected by market slowdown and pricing pressure

Price pressure across Europe and Algeria

High penetration in Spain with favorable share of voice to competitors

G5(1) Developed RoW Emerging markets(2)

48% 9% 43%

+1.3%

(1) France, Germany, UK, Italy, Spain – (2) Notably includes China, Russia and Brazil Note: all variations at constant exchange rate

Launch of 3-month subcutaneous formulation in Europe from July 2015

Progress on potential combination in breast cancer

Increased commercial focus in China with dedicated sales force per indication

18 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 18 18

Primary care resilient thanks to international market growth

354 328 330

2013 2014 2015

(4,8)%

Business update

3-year growth 2015 performance

Geographic distribution

Smecta® sales impacted by new manufacturing setup in Algeria and destocking in distribution and price pressure in China

Tanakan® facing out of pocket market slowdown and tough competition in Russia and France

Solid performance of Etiasa® in China and Fortrans® notably in Russia

30% 5% 65%

(1) France, Germany, UK, Italy, Spain – (2) Notably includes China, Russia and Brazi Note: all variations at constant exchange rate; OTx:Dual channel approach (Rx/OTC)

G5(1) Developed RoW Emerging markets(2)

(1.1)%

Start of Tanakan® local production in Russia

Launch of Smecta® ready-to-use (liquid) and Strawberry taste in Q4 2015 in France

Accelerated switch of China primary care model to OTx with recruitment of 100 additional reps in 2016

19 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 19 19

in m€ FY 2015 FY 2014 Change % Change

Change at constant FX

Net sales 1,443.9 1,274.8 +169.1 +13.3% +10.4%

Other revenues 76.3 57.6 +18.7 +32.5%

Revenue 1,520.2 1,332.4 +187.8 +14.1%

Cost of goods sold (336.8) (310.0) -26.8 +8.7%

R&D expenses (192.6) (186.9) -5.7 +3.0%

Selling expenses (541.4) (464.1) -77.3 +16.7%

G&A expenses (122.9) (111.2) -11.7 +10.4%

Other core (4.1) 0.3 -4.4 NA

Core Operating income 322.5 260.6 +61.9 +23.8%

Core Operating margin 22.3% 20.4% +1.9 pt

P&L - From sales to Core Operating Income

Operating leverage driving margin expansion

20 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 20 20

50%

17%

10%

5%

18%

Ipsen exposure to foreign currencies

EUR

USD

GBP

CNY

Other(1)

(1) Includes RUB, BRL, AUD, PLN and other currencies

Evolution of major currencies vs. EUR 2015 sales exposure by currency

2015 sales growth benefited from strong USD, CNY and GBP appreciation versus euro

2016 sales to be impacted by depreciation of emerging countries currencies (BRL, CNY, RUB)

€1,443.9 million

…

Foreign Currency policy

Average rates change (2015vs. 2014)

19.9% 17.6% 11.1%

-25.3%

-15.4%

USD CNY GBP RUB BRL

Global FX exposure mitigated by cost base in local currency and hedging of key currencies

21 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 21 21

FY 2014 FY 2015

COGS (€m)

24.4% 23.6%

R&D (€m)

Selling expenses (€m)

FY 2014 FY 2015

+16.7%

G&A (€m)

+8.7%

541.4

464.1

336.8

+3.0%

192.6 186.9

+10.4%

8.7% 8.5%

122.9

111.2

Drivers for operating cost evolution

Note: All ratios in percentage of sales; NET: Neuroendocrine tumors

36.4% 37.5%

Positive mix effect, manufacturing efficiencies Impact of TasQ studies discontinuation

Support functions, variable compensation Impact of US investment (NET, spasticity)

FY 2014 FY 2015

24.3% 23.3%

310.0

FY 2014 FY 2015

14.7% 13.3%

22 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 22 22

in m€ FY 2015 FY 2014 Change % Change

Net sales 1,443.9 1,274.8 +169.1 +13.3%

Core Operating income 322.5 260.6 +61.9 +23.8%

Core Operating income margin 22.3% 20.4% +1.9 pt

Other non core (7.2) (9.2) +2.0

Restructuring costs (6.7) (21.9) +15.2

Impairment gain / (losses) (64.6) (8.0) -56.6

Operating income 244.0 221.4 +22.6 +10.2%

Financial result (6.4) (15.1) +8.7

Income taxes (49.8) (53.8) +4.0

Share of profit from JV 2.5 1.9 +0.6

Discontinued operations 0.5 (0.5) +1.0

Consolidated net profit 190.7 154.0 +36.7 +23.8% Consolidated profit margin 13.2% 12.1% +1.1 pt

EPS – fully diluted (€) 2.30 1.87 +0.43 +23.0%

Core EPS – fully diluted (€) 2.78 2.22 +0.56 25.2%

P&L - From Core Operating Income to EPS

Consolidated net profit up 24% after TASQ impairment charge and exceptionally low tax rate

23 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 23 23

180 214

+290

-61

-58

-15 -70

-29 -39

+16

In million euros

Operating cash

flow(1)

31 Dec 2015 31 Dec 2014

Change in working capital(1)

Solid cash generation to finance capex, BD and return to shareholders through dividend & share buy-back

Dividends

BD & milestones Closing

cash

Capex

Opening cash

Other

Closing cash up €34m vs 2014

Strong cash generation to self-finance acquisitions

Free cash flow: €156m

(1) Excluding milestone amortization

Restructuring

Share Buyback

24 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 24 24

Proposal to maintain a dividend of €0.85 per share to support BD investment

Group sales up 10.4% at constant currency

Strong Core Operating Income margin of 22.3%(1)

Consolidated net profit of €190.7m, up 23.8% year-on-year

Fully diluted core EPS of €2.78, up 25.2% year-on-year

Closing cash balance of €214m, up 19%

Key financial takeaways

(1) In percentage of sales

Cabozantinib in-licensing and outlook

26 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 26 26

Exclusive license agreement with Exelixis for Cabozantinib, with key indication in Renal Cell Carcinoma (RCC)

Potential development in further indications

Medullary Thyroid

Cancer

Exclusive global licensing and commercialization rights (ex North America & Japan)

Renal Cell Carcinoma

Filed in 2nd line

Hepatocellular Carcinoma

Ph3 in 2nd line

Key indications

Marketed

110 000 patients 60 000 patients 1500 patients European incidence

27 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 27 27

Cabozantinib, a best in class showing positive PFS and OS data

Standard of care: TKI(1)s

RCC

2nd line treatments

(1)Tyrosine Kinase Inhibitors OS: Overall survival, PFS: Progression Free Survival, ORR: Objective Response Rate

Approved therapies

1st line treatments

TKI(1)s and mTOR inhibitors

Potential entrants

Cabozantinib Immunomodulators

RCC 2nd line treatment paradigm shift from PFS to OS

PFS OS ORR PFS OS ORR

PFS OS ORR

28 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 28 28

Accelerate specialty care growth in the next 5 years with a 4th pillar added to Ipsen Specialty portfolio

Acquire a potential best in class derisked asset in attractive niche RCC with solid scientific data triggering treatment paradigm shift

RCC: Renal Cell Carcinoma

Completion of a global oncology therapeutic footprint (US and Europe)

Reinforce Ipsen portfolio in niche oncology with potential for further development in other indications

Strong rationale for Cabozantinib in-licensing

29 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 29 29 MTC: Medullary Thyroid Cancer, RCC: Renal Cell Carcinoma

Cabozantinib, deal terms and impact on Ipsen operations

Operations

Upfront: $200m

Regulatory: up to $110m ($60m for RCC and $50m for HCC indications)

Commercial: up to $545m

Milestones

Royalties Tiered up to 26% on net sales

Transfer of MTC Market Authorization in H2 2016 and RCC launch starting

in 2017

Significant commercial investment

Cost containment and project prioritization initiatives to minimize impact of

2016 - 2018 investment period

30 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 30 30

Specialty care sales

Core Operating margin Around 21% of sales

Growth > 10.0%, year-on-year

Primary care sales Slight growth, year-on-year

2016 financial objectives

Including a negative impact of: • ~150 basis points resulting from the investment required to

prepare the commercial launch of Cabozantinib for the treatment of Renal Cell Carcinoma in Europe

• ~100 basis points from foreign exchange rates

At constant currency

At constant currency

31 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 31 31

Update of 2020 financial outlook

2015 2020E

Group sales Core Operating margin

> 7%

22.3%

> 26%

2015 2020E

>+370bps

€1.4bn

> €2.0bn

Specialty care

Specialty care

Primary care

>8%

[2% to 4%]

CAGR

Primary care

2020 Sales target increased to reflect Cabozantinib sales contribution

2020 Profitability target confirmed

32 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 32 32

2016 roadmap

Note: OTx:Dual channel approach (Rx/OTC); NET: Neuroendocrine tumors

Position Somatuline® as a leader in NET and secure Dysport® spasticity launch

Prepare the commercial launch of Cabozantinib for the treatment of Renal Cell Carcinoma in Europe

Implement new Primary Care OTx model, notably in China

Ipsen to deliver top tier growth and superior value creation to shareholders

Continue Business development to replenish pipeline and complement marketed product portfolio

Appendix

34 Goldman Sachs 35th Annual Global Healthcare Conference – June 2014 Full Year Results Roadshow - London, March 9, 2016 34 34

R&D

Regulatory/ Commercial

H1 2016 H2 2016 2017

Major R&D and regulatory milestones to come

Note: ALL: Adult Lower Limb; GEP NETs: Gastroenteropancreatic neuroendocrine tumors; PLL: Pediatric Lower Limb; PUL: Pediatric Upper Limb, RCC : Renal Cell Carcinoma), HCC : Hepatocellular carcinoma

Syntaxin compound PhI initiation

OPS201 – Lu Satoreotide PhI initiation

Dysport® PLL US launch

Telotristat etiprate

EU filing

Dysport® PUL PhIII results

Dysport® ALL US filing

OPS202 – Ga Satoreotide PhIII initiation

Dysport® Solution PhIII results in Glabellar lines

Dysport® PLL US filing

Cabozantinib RCC EU approval

Cabozantinib HCC phIII results

Telotristat etiprate

EU launch

Cabozantinib RCC launch