Investor Sentiment and Seasoned Equity Offerings · PDF fileInvestor Sentiment and Seasoned...

62

1 Investor Sentiment and Seasoned Equity Offerings Xiaoying Deng a , Emir Hrnjić b and Seow Eng Ong c a,c Department of Real Estate, National University of Singapore, Singapore, 117566 b NUS Business School, National University of Singapore, Singapore, 119245 Preliminary draft: October 29, 2011 First draft: December 14, 2011 This draft: April 16, 2012 Abstract We document that investor sentiment is positively related with pre-SEO overpricing and plays an important role in managers’ equity issuance decisions. Further, we provide evidence that investor sentiment impacts the SEO discounting and underpricing. High sentiment periods are followed by low long run returns suggesting that sentiment does not proxy for unobservable fundamentals. Overall, our findings are consistent with market timing and behavioral explanations for equity offerings. Keywords: Investor Sentiment, Seasoned equity offerings, Market Timing, Behavioral finance, Underwriters, Real Estate Investment Trust Authors’ contact information: a Department of Real Estate, National University of Singapore, 4 Architecture Dr.,Singapore, 117566 E-mail: [email protected] b NUS Business School, National University of Singapore, 15 Kent Ridge Dr, Singapore, 119245 E-mail: [email protected] c Department of Real Estate, National University of Singapore, 4 Architecture Dr.,Singapore, 117566 E-mail: [email protected]

-

Upload

truonghuong -

Category

Documents

-

view

214 -

download

0

Transcript of Investor Sentiment and Seasoned Equity Offerings · PDF fileInvestor Sentiment and Seasoned...

1

Investor Sentiment and Seasoned Equity Offerings

Xiaoying Denga, Emir Hrnjićb and Seow Eng Ongc

a,c Department of Real Estate, National University of Singapore, Singapore, 117566

b NUS Business School, National University of Singapore, Singapore, 119245

Preliminary draft: October 29, 2011

First draft: December 14, 2011 This draft: April 16, 2012

Abstract

We document that investor sentiment is positively related with pre-SEO overpricing and plays an important role in managers’ equity issuance decisions. Further, we provide evidence that investor sentiment impacts the SEO discounting and underpricing. High sentiment periods are followed by low long run returns suggesting that sentiment does not proxy for unobservable fundamentals. Overall, our findings are consistent with market timing and behavioral explanations for equity offerings. Keywords: Investor Sentiment, Seasoned equity offerings, Market Timing, Behavioral finance,

Underwriters, Real Estate Investment Trust

Authors’ contact information: a Department of Real Estate, National University of Singapore, 4 Architecture Dr.,Singapore, 117566 E-mail: [email protected] b NUS Business School, National University of Singapore, 15 Kent Ridge Dr, Singapore, 119245 E-mail: [email protected] c Department of Real Estate, National University of Singapore, 4 Architecture Dr.,Singapore, 117566 E-mail: [email protected]

2

Abstract

We document that investor sentiment is positively related with pre-SEO

overpricing and plays an important role in managers’ equity issuance decisions.

Further, we provide evidence that investor sentiment impacts the SEO

discounting and underpricing. High sentiment periods are followed by low long

run returns suggesting that sentiment does not proxy for unobservable

fundamentals. Overall, our findings are consistent with market timing and

behavioral explanations for equity offerings.

Keywords: Investor Sentiment, Seasoned equity offerings, Market Timing,

Behavioral finance, Underwriters, Real Estate Investment Trust

3

Introduction

Firm’s decision to issue equity is sensitive to fundamental and behavioral market

conditions at the time of issuance. In this paper, we examine the relationship between

investor sentiment and the firm’s seasoned equity offerings (SEO, thereafter). More

specifically, we examine the probability of SEO issuance, SEO pricing, and market

reactions.

It is well documented that firms conduct equity issuance when the shares are

overvalued. In the Graham and Harvey (2001)’s survey, two-thirds public

corporations’ CFOs asserted that“the amount by which our stock is undervalued or

overvalued was an important or very important consideration” in equity issuance

decision. The positive relation between equity issuance and its ex ante indicators of

overvaluation is hard to reconcile with the predictions of trade-off theory and

pecking-order theory (Myers and Majluf 1984) of capital structure. Baker and

Wurgler (2002) propose a market timing theory that managers attempt to sell

overpriced shares to investors if market permits, but leave the question why shares

are mispriced at issuance unanswered. Our paper extends this strain of literature by

answering how firm managers time the market.

Recent advances in behavioral finance suggest that investor sentiment contributes to

stock mispricing. Brown and Cliff (2004) provide the evidence that market pricing

errors are positively related to sentiment. Lemmon and Portniaguina (2006) argue that

investor sentiment explains size premium. Studies in equity offerings document

positive relationship between investor sentiment and IPO underpricing , and negative

4

relationship between sentiment and long run returns (Cornelli, Goldreich and

Ljungqvist 2006; Derrien 2005). While these studies provide the evidence of the

sentiment’s impact on unseasoned equity issues, it remains an open question if these

effects could be generalized to seasoned equity markets since, unlike IPOs, seasoned

firms’ value is established and easily observable in the secondary market. Altinkiliç

and Hansen (2003) and Corwin (2003) empirically examine determinants of SEO

discounting and underpricing. Altinkiliç and Hansen (2003) find that unexpected

underpricing is related to information gathering and marketing activities, whereas

Corwin (2003) documents that underpricing is related to price pressure and

uncertainty. However, none of these papers examine the impact of investor sentiment

-- the main variable in our analysis.1 Finally, Baker and Wurgler (2006) document

that the aggregate fraction of equity issues is higher during high sentiment periods and

high sentiment periods are followed by lower long run returns. While Baker and

Wurgler (2006) focus on the equity issuance at the aggregate level, they do not

examine the impact of investor sentiment on seasoned issues at the individual level.

Our paper fills the gap in the literature.

As a laboratory for our analysis, we use seasoned equity issuance activities of Real

Estate Investment Trusts (REITs, thereafter), which are typically excluded in

corporate finance studies. Created in United States, REITs offer individuals the

opportunities to invest in real properties. REITs are ideal setting for our analysis for

several reasons. First, since REITs do not have to pay corporate tax, there is no tax

benefit for debt issuance. Second, the tax exempt feature requires REITs to distribute

a minimum 90% of their taxable income to investors as dividends, thus, limiting the 1 Corwin (2003) also reports that SEO underpricing is related to the concurrent level of underpricing in IPO market, recognizing that there is a common underlying factor influencing both markets. However, he does not pursue this enquiry further.

5

possibility of free cash flow. Restricted with investment options on real estate assets

and dividend pay-out regulation, REITs rely primarily on external financing to fund

investments and at a higher frequency than general firms. Third, REITs are highly

leveraged firms and as a result, REIT managers have enough incentives to monitor the

equity capital market to balance the costs of different capital. Thus REITs' seasoned

equity issuance decisions and pricing are more likely to be market driven. Fourth,

REITs capital structure is more consistent with market timing theory since the key

drivers behind the traditional capital structure theories are partially silent in REITs

(Ooi, Ong and Li 2010). Also, the similar leverage across REITs enables us to

circumvent capital structure issues that may contaminate equity issuance studies.

Finally, REITs provide us with a unique opportunity to separate sentiment into supply

and demand component.

To the best of our knowledge, this is the first paper to analyze the impact of investor

sentiment on seasoned equity activities and SEO pricing process. The study sample

covers all US listed REITs firms and spans a twenty-four-year period from 1986 to

2009. The empirical results suggest that the equity offerings are strongly influenced

by sentiment investors. Consistent with the market timing and behavioral finance

hypothesis, we observe a strong positive relation between the decision to issue equity

and the investor sentiment. By decomposing pre-SEO market-to-book ratio, we find

that pre-SEO mispricing is positively related with the level of investor sentiment.

Further, we document that investor sentiment is positively related with the SEO

discounting and underpricing, whereas it is negatively related with long run stock

returns. Overall, investor sentiment seems to play an important role in seasoned equity

offerings.

6

Our contributions are manifold. First, we provide evidence that equity offering

decision is influenced by market-wide sentiment. Second, we provide evidence that

sentiment is positively related to pre-SEO mispricing levels, supporting the market

timing setting with investor sentiment. Third, we document evidence that pricing of

SEOs is influenced by sentiment in the short run and the long run. Overall, we

contribute to the existing equity offering literature by providing evidence that

sentiment plays a nontrivial role in market timing and price formation.

This paper proceeds as follows. We review the relevant literature in Section II and

construct our hypotheses in Section III. Section IV describes the data. Section V

discusses the empirical results. Section VI presents the robustness test. Section VII

concludes.

Literature Review

1. investor sentiment and equity offering

Abundance of evidence suggests that overvaluation is a motive for equity issuance

(Graham and Harvey 2001). For example, equity issuance is positively associated

with ex ante indicators of overvaluation like market-to-book ratio and market indices.

(Loughran, Ritter and Rydqvist 1994) find that cumulative IPO volumes are highly

correlated with stock market valuations and this strong relationship is also identified

in seasoned equity issuance (Jung, Kim and Stulz 1996). The evidence of earning

management before equity issuance (Teoh, Welch and Wong 1997) and post-issue

7

long run underperformance (Loughran and Ritter 1997) indicate that managers

attempt to sell overpriced shares to investors if market permits (Baker and Wurgler

2002).

Stein (1996) suggests that managers try to 1) maximize fundamental value by

financing projects to increase the present value of future cash flow, 2) maximize the

current price of the firm’s securities by catering to sentiment investors to capture the

demand side surplus, and 3) exploit the current mispricing for the benefit of current

investors by allowing them to sell the overvalued stocks to over-confident investors.

The solution to this problem indicates that the marginal cost from issuing equity,

deviating from current capital structure, is balanced with marginal issuance benefit,

i.e. the direct market timing gains from over-confident investors and stock mispricing.

The impact of sentiment investors has been examined in the IPO market. (Ljungqvist,

Nanda and Singh 2006) propose that sentiment investors are over-optimistic about the

future prospects for the issuance firms. Rational managers are assumed to make

decisions responding to mispricing by sentiment investors. While their decisions may

maximize the short-run value of the firm, they may also result in lower long-run

values as prices correct. Using ‘grey market’ pre-IPO trading as proxies for investor

sentiment, Cornelli, Goldreich and Ljungqvist (2006) and Dorn (2009) find

correlation with high initial returns and low long-run returns (Derrien 2005).

In the context of REITs, empirical results show that target leverage plays a secondary

role in REITs corporate financing decisions. Ooi, Ong and Li (2010) examine the

public offerings timing attempts in REITs and targeted debt ratios. They point out that

8

REITs time market within a general targeted debt ratio environment. Boudry,

Kallberg and Liu (2010) also recorded strong evidence supporting the market timing

theory in explaining the issuance decisions of REITs.

However, there is no study examining whether investor sentiment influence

managers’ issuance decisions and market reaction to SEO decision. Our paper

provides a detailed examination on the effects of investor sentiment and equity

offerings on REITs.

2. Investor sentiment and equity pricing

In behavioral finance, sentiment investors who trade on “noisy” information drive

temporary price away from intrinsic values(De Long, Shleifer, Summers and

Waldmann 1990). Also, risk exposure and financing constraints limit rational

arbitrageurs’ ability to offsetting against sentiment investors, making price deviate

from fundamental value over time(Shleifer and Vishny 1997). Baker and Wurgler

(2007) interpret investor sentiment as a misguided belief about firm’s risks or future

cash flows growth based on the current information.

Prior literature utilizes several proxies for the investor sentiment. Direct measures of

investor sentiment are derived from surveys like Index of Consumer Sentiment

constructed by Thomson Reuters/University of Michigan, (henceforth, ICS) and

Conference Board Consumer Confidence Index constructed by the Conference Board

(henceforth, CBIND) and survey values from American Association of Individual

Investors. Michigan Consumer Sentiment Index and Conference Board Consumer

9

Confidence Index are used to represent the sentiment in overall market (Lemmon and

Portniaguina 2006), while survey values of American Association of Individual

Investors focus on the perception of retail traders, which are often viewed to be

sentiment investors (Brown and Cliff 2004). Qiu and Welch (2004) compare different

sentiment measures with small firm performance, suggesting that Conference Board

Consumer Confidence Index and Michigan Consumer Sentiment Index better

represent the behavior of sentiment investors. The most prominent indirect measure is

Baker and Wurgler (2006) index (B-W, thereafter) which utilizes several market

variables known to be indicative of sentiment. B-W is calculated as the principal

component from closed end fund discount, dividend premium, NYSE turnover, first

day IPO returns, number of IPOs, and proportion of equity offerings(Campbell, Rhee,

Du and Tang 2008; Sankaraguruswamy and Mian 2008).

Prior studies use different measures of investor sentiment to examine the role of

investor sentiment in asset pricing. Pronounced effect of investor sentiment has been

identified in public stock market over different horizons (Brown and Cliff 2004;

Baker and Wurgler 2007) and cross sectional stock returns (Baker and Wurgler 2006).

In real estate market, existing evidence indicates that investor sentiment also

influences acquisition prices in both private and public commercial real estate

market(Clayton, Ling and Naranjo 2009).

Empirical Implications

The existing behavioral models in literature (Cornelli, Goldreich and Ljungqvist

2006; Ljungqvist, Nanda and Singh 2006; Stein 1996) allow us to make predictions

10

about the relationship between the investor sentiment on one side and firms’ seasoned

equity offering activities, SEO price dynamics, and long run returns.

Managers issue equity in order to take advantage of the inflated share price. Investors

in the market realize that managers are opportunistic and revise firm’s valuation

downwards in response to SEO announcement which leads to the negative effect on

the share price; i.e., negative returns at the announcement day. During high sentiment

periods, which are dominated by overoptimistic sentiment investors, managers have

higher incentive to act opportunistically. Hence, we conjecture that above behavior is

more pronounced during high sentiment periods. So, during high sentiment, we expect

higher overpricing of SEO issuing firms and higher probability of SEO decision. At

the same time, investors adjust for this behavior and, therefore, during high sentiment

periods, SEO announcement is even more negative news. Hence, we conjecture that

this results in more negative returns at the announcement. In sum, this reasoning leads

to following hypotheses:

Hypothesis 1: Pre-SEO stock mispricing is positively related with investor sentiment.

Hypothesis 2: Probability of SEO issuance is positively related to investor sentiment.

Hypothesis 3: SEO announcement return is negatively related with investor

sentiment.

11

Investor sentiment contributes to the marginal benefits of equity issuance, hence

influencing the amount of equity issued. Firms tend to issue more equity at higher

investor sentiment periods. Hence:

Hypothesis 4: Investor sentiment is positively related to the amount issued.

Hypothesis 5: Investor sentiment is positively related to the offer price revision.

In the preceding discussion, we hypothesized that SEO firms act opportunistically and

issue equity when investor sentiment is high and shares are overpriced. However, it is

not obvious how this will influence pricing of the new issue. Managers and

underwriters are aware that market is dominated with sentiment investors and they

may take advantage of their overoptimism and set SEO offer price higher; i.e. at a

smaller discount from previous day closing price. At the same time, new SEO shares

are usually placed with regular investors and underwriter is interested in nurturing

long term relationship with these investors since they will have repeated interactions

in future issues. Since underwriters know that shares are overpriced and will revert to

the true value in the long run, underwriter may decide to protect their regular

investors from long run decline in share price. In that case, they will price SEO shares

lower; i.e. at a larger discount. Ultimately, the impact of investor sentiment on

discounting and first day return is an empirical issue. This reasoning leads us to

following hypotheses.

Hypothesis 6A: Investor sentiment is positively correlated with SEO discounting.

Hypothesis 6B: Investor sentiment is negatively correlated with SEO discounting.

12

Hypothesis 7A: Investor sentiment is positively correlated with SEO first day return.

Hypothesis 7B: Investor sentiment is negatively correlated with SEO first day return.

During high sentiment periods, markets are dominated with overoptimistic investors

and SEO firms are overpriced. Since sentiment investors arrive and leave market

together, valuations will revert to the fundamental value over the long run. This

implies that long run return will be negative. Hence:

Hypothesis 8: Long-run return is negatively correlated with investor sentiment.

Research Design

1. Sample Selection

We analyze the SEOs conducted by REITs firms (SIC code=6798) during January 1,

1986 and December 31, 2009, as reported in the Securities Data Company (SDC)

database. The study period begins from 1986, after the introduction of the Tax

Reform Act, which allows REITs to engage in a variety of real estate activities,

making REITs resort to external financing more frequently. Accounting information

and stock price data are retrieved from COMPUSTAT and the Center for Research in

Security Prices (CRSP). We further restrict the SEO sample to common shares. Our

final sample consists of 994 US REITs SEOs. As we impose other data availability

conditions on SDC, COMPUSTAT and CRSP, some of our findings are based on

samples fewer than 994 SEOs.

13

2. Pre-SEO valuation

To examine the impact of investor sentiment on misvaluation before SEO, we

decompose pre-issue market-to-book (m-b) ratios into misvaluation (m-v) and growth

opportunities (v-b) components following the methodology developed by Rhodes-

Kropf, Robinson and Viswanathan (2005) (RKRV, thereafter), and utilized in several

recent papers (Fu, Lin and Officer 2010; Hertzel, Hrnjić, Officer and Si 2011; Hertzel

and Li 2010).

According to behavioral theories, if investors do not have information that managers

have or sentiment investors overestimate the future cash flows, market-to-value will

capture the mispricing component of the market-to-book ratio. For estimation

purpose, RKRV(2005) methodology implement a vector of contemporaneous cross

sectional industrial level accounting multiples and long run firm accounting multiples

to estimate the firm value v.

itjitjitjtitjtitititit bvvvvmbm );();();();( (1)

The first component );( jtitit vm measures the difference between market value

and fundamental value estimated using firm-specific accounting data and the

contemporaneous industry accounting multiples, interpreted as the mispricing

component in market-to-book ratio. This component is the mispricing proxy we use in

this paper. The third component itjit bv );( captures the growth opportunities the

firms face contemporarily.

To empirically address the mispricing component, RKRV (2005) adopt three different

models to estimate firm value. In our paper, given REITs unique dividend payout

14

policy, we adjust RKRV’s 3rd model by adding dividend factor into the accounting

information vector. We therefore express market value as a linear model as follows.

ititjtitjtitjtitjtjtit LEVNIINIbm

4)0(3210 )ln()ln( (2)

Where )ln(NI is the positive net income in natural logarithm, LEV is leverage ratio,

To calculate the REITs industry wide accounting multiples, we run cross-sectional

regressions for the REITs industry to obtain the estimated REITs industry accounting

multiples jt̂ for each year t. Hence we estimate the firm value with following

equation.

itjtitjtitjtjt

jtjtjtjtititit

LEVNIIb

LEVNIbv

3)0(210

3210

ˆ)ln(ˆˆˆ

)ˆ,ˆ,ˆ,ˆ;,,(

(3)

The difference between market value itm at day prior to SEO issuance and

)ˆ,ˆ,ˆ,ˆ,ˆ;,,,( 43210 jtjtjtjtjtitititit DVCLEVNIbv is our proxy for mispricing in this

paper.

3. SEO discounting and underpricing variables

To analyze the price dynamics around SEOs, we define discounting as the (negative

of) percentage difference between the offer price and the closing price at the prior

trading day. Note that this variable is positive if offer price is lower than the previous

day closing price. Similarly, we define underpricing as the percentage change from

the offer price to the closing price on the first trading day after SEO.

4. Survey based proxies for investor sentiment

15

Researchers adopt both direct and indirect approaches to quantify investor sentiment.

In this paper, we adopt the survey based indices as proxies to capture the investor

sentiment. In robustness test, we implement indirect measure of investor sentiment to

verify the results.

Investor sentiment is addressed in the Survey of Consumers constructed by Thomson

Reuters/University of Michigan and Research Centre and Consumer Confidence

Survey constructed by the Conference Board, both of which are shown to be valid

measure of investor sentiment in Qiu and Welch (2004) and Lemmon and

Portniaguina (2006). The monthly surveys conducted by Thomson Reuters/University

of Michigan use around fifty core questions that reflect respondents’ attitudes and

expectations about overall economic conditions and personal finances. Based on the

interviews from at least 500 households across the States, the Index of Consumer

Sentiment is developed. Likewise, the Index of Consumer Confidence of the

Conference Board is constructed monthly based interviews about customers’

perceptions of economic conditions in the States. And the sample size is around five

thousand households, larger compared with the sample size used in the Index of

Consumer Sentiment.

As REITs bridge both financial market and real estate, it is plausible that REITs

equity issuance is influenced by real estate market sentiment as well. The survey data

allow us to further differentiate real estate market sentiment into investor sentiment of

real estate market (the demand side) and the supplier sentiment of the real estate

market (the supply side). Investor sentiment of real estate market (the demand side) is

also addressed in the buying condition survey conducted by Thomson

Reuters/University of Michigan. The survey is conducted on a sample of 500

households about their opinion to purchase a property: good, bad and uncertain, and

16

labels these responses with ten different reasons. The examples of reasons are that

prices will increase, it is a good investment and it is good time, etc. Those responses

are used to calculate the relative value of buyers’ perception of real estate market.

And to measure supplier sentiment of real estate market (the supply side), we use the

NAHB/Wells Fargo Housing Market Index constructed by the National Association

of Home Builders. The survey is conducted monthly on a sample of four hundred

builders about their attitudes toward house sales and potential buyers. The

NAHB/Wells Fargo Housing Market Index is developed as a weighted average of

those responses, reflecting builders’ perceptions of sales conditions in real estate

market.

We are aware that the sentiment survey values convey the information about the

sentiment as well as their opinions on the economy fundamentals. To capture the

excess optimism or pessimism, we remove the effect of economy fundamentals from

the raw survey values by regressing the values against a set of variables suggested in

Lemmon and Portniaguina (2006) and used in Hrnjić and Sankaraguruswamy (2011 ).

118117116115114

113112111110987

6543210

3

3

ttttt

ttttttt

tttttt

CAYCPIURATELABORCONS

GDPYLDDEFDIVCAYCPIURATE

LABORCONSGDPYLDDEFDIVICS

Where DIV is the dividend yields, DEF is the yield spread between Moody’s Aaa and

Baa-rated bonds, YLD3 is the three-month Treasury bill yield, GDP is GDP growth

deflated to 2005 dollars(in the natural logarithm), CONS is personal consumption

expenditures growth (in the natural logarithm), LABOR is the labor income growth (in

the natural logarithm) deflated by the PCE deflator, URATE is the adjusted

unemployment rate reported by the Bureau of Labor Statistics, CPI is the inflation

rate, CAY is consumption-to-wealth ratio. Since our sentiment is measured at a

17

monthly frequency, for some macro data which are reported on a quarterly basis, we

take the same value for all months in a certain quarter.

The residual from the above equation is labeled ICSR. If we use CBIND, BC, and

HMI as a proxy for sentiment residual are labeled CBINDR , BCR, and HMIR,

respectively. ICSR and CBINDR denote the excess optimism or pessimism of

consumers and is our proxy for investor sentiment. BCR denote the excess optimism

or pessimism of housing buyers and is our proxy for real estate sentiment from

demand side, while HMIR is our proxy for real estate sentiment from the supply side.

5. Control variables

To analyze the impact of investor sentiment on SEO price dynamics, we also control

for other determinants of price dynamics that have been documented in prior studies.

Offer size (Size) is the relative SEO offer size (number of shares offered multiplied by

offer price) scaled by market capitalization of the issuing firm (Altinkiliç and Hansen

2003; Brounen and Eichholtz 2001). Uranking is the underwriter

reputation(Safieddine and Wilhelm Jr 1996). We also add total assets (Asset) and sale

(Sale) to control for firm size. Leverage (Lev) and leverage change from the previous

period (Clev) allow us to further capture the impact of leverage as recorded in the

literature (Brounen and Eichholtz 2001). SeqREIT is constructed as the current SEO

sequence regarding the REIT itself to account for the clustering and frequency of SEO

(Ghosh, Nag and Sirmans 2000). Yearslisted is the number of years between the SEO

year and the IPO year to measure the growth level of the firm as suggested in

(DeAngelo, DeAngelo and Stulz 2010).

We are mindful that market conditions influence price dynamics around SEOs.

Specifically, instead of using past stock returns, we compute the risk premium

18

(Rpremia) over the past 1 month prior to issue date. Also we use the 6 month

government bond yield (Byield) to measure the attractiveness of the equity offering.

We are aware that the time-varying growth opportunities might also be responsible for

some of our analysis(Yung, Çolak and Wei 2008). Hence we use the third component

(Growth) of RKRV(2005) market-to-book decomposition as described previously to

control for the market reaction associated with growth/ investment opportunities. We

use the abnormal return around earning announcement releases (Infoas) as a measure

of information asymmetry suggested for stock mispricing (Lowry, 2003)

Dummy variables are also included. EQUI equals to one if the firm is an equity REIT,

zero otherwise. MORT equals to one if the firm is a mortgage REIT, zero otherwise.

NASDAQ equals to one if the firm is listed on NASDAQ, zero otherwise(Mola and

Loughran 2004).

Results Interpretation

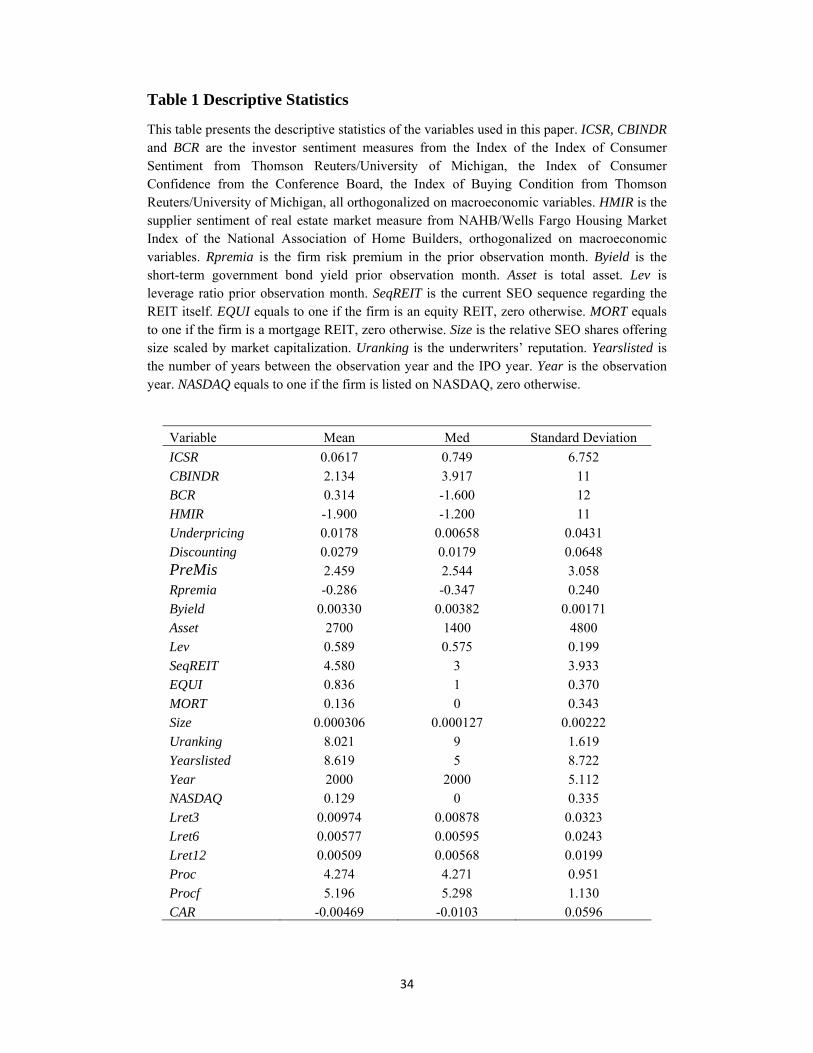

Descriptive Statistics

19

Table 1 shows the summary statistics for all the variables used in this paper. In

general, mean pre-SEO mispricing level is 2.459, which shows that SEO stocks are on

average overvalued before issuance compared to the peers. The median accumulative

abnormal return around announcements is -1.03%. In comparison, the average

abnormal return is -2% for SEOs by US general firms (Altinkiliç and Hansen 2003;

Asquith and Mullins Jr 1986; Eckbo and Masulis 1992). The mean Discounting and

Underpricing are 2.89% and 1.78% respectively. In comparison, the average

underpricing level is 2.92% in 1990s and 1.3% 1980s for SEOs by US general

firms(Corwin 2003). The mean past stock return is 1.56%, indicating a price run-up

prior issuance on average. Given the high payout ratio, it is not surprising that REITs

firms conduct equity offering at a higher frequency (mean SeqREIT is 4.58). Also,

SEOs firms have a relatively high leverage ratio (mean 58.9%). The mean Yearlisted

is 8.619 years, suggesting that SEO firms are on average in their pre-natural stage.

Equity offering tend to be made shortly after financial results are announced.

[Insert Table 1]

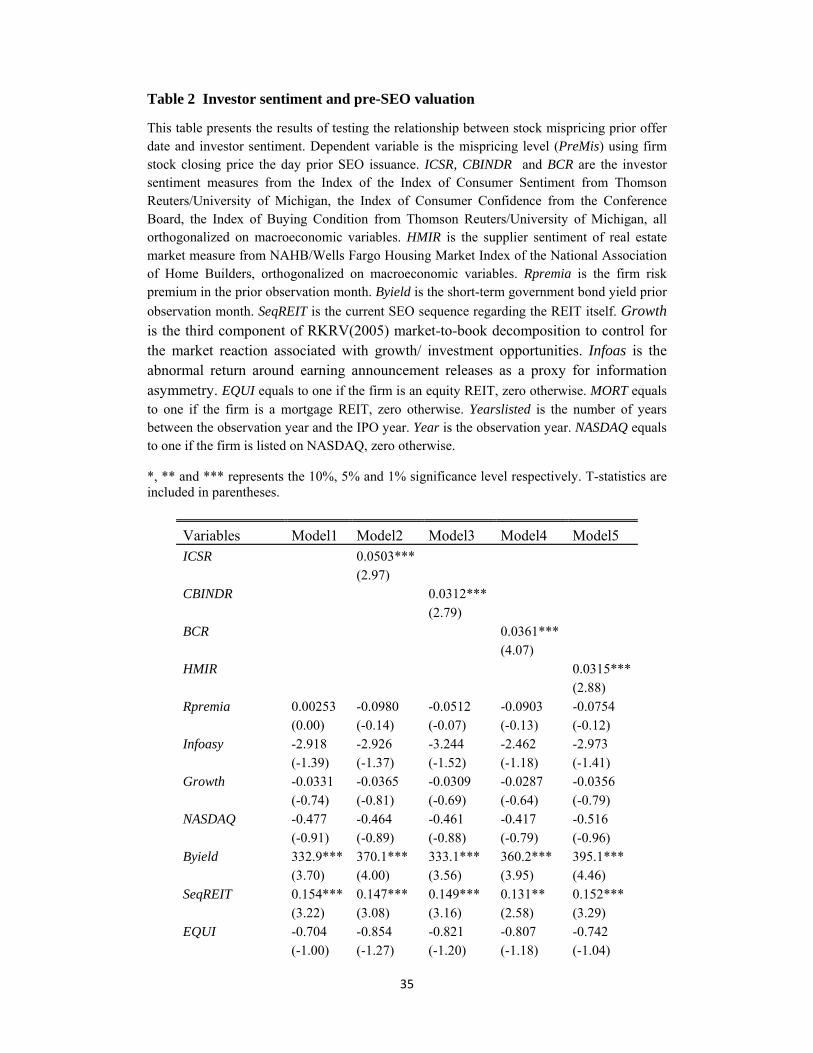

Sentiment and pre-SEO valuation

Theoretical models in behavioral finance assume that rational managers make

decisions in response to sentiment investors which suggests that pre-SEO

overvaluation or mispricing is increasing in sentiment. This enables us to test whether

managers take advantage of prevailing sentiment by examining the relation between

sentiment and market valuation prior to the SEO issuance.

As described in previous section, we adopt the RKRV(2005) methodology to

calculate the mispricing (PreMis) using firm stock closing price the day prior SEO

20

issuance. We analyze the relation between sentiment and pre-issuance mispricing of

SEO firms in the following multivariate model.

NASDAQYear

dYearslisteMORTEQUIInfoasSeqREIT

GrowthByieldRpremiaSentimenteMis

1101

98765

43210Pr

(4)

Where Sentiment are ICSR, CBINDR , BCR and HIMR.

Table 2 shows the results. The coefficients for investor sentiment proxies are

significant and positive (coefficient for ICSR=0.0503, t-stat=2.97). This shows that

mispricing magnifies as sentiment increases, indicating that managers tend to exploit

prevailing sentiment in equity issuance. We also notice that model’s explanatory

power (adjusted R square) substantially increases after incorporating sentiment

variables.

For other control variables, we see a negative relation between mispricing level and

past market return. Mispricing level is likely to be higher for older, more frequent

equity issuance firms, in crisis period when the whole market is in panic.

[Insert Table 2]

Sentiment and SEO probability

We specify a discrete choice probability model to analyze the impact of sentiment on

SEO timing. The probit model identifies an equity issuance for every REIT in our

sample on a monthly basis2. Dependent variable equals one if an SEO is observed,

zero otherwise. Accounting data are at a quarterly frequency retrieved from

COMPUSTAT FUNDAMENTAL QUARTERLY.

2 We also run the probit model quarterly and annually, and the results remain robust.

21

Table 3 reports the results from the probit model for SEO issuance. All coefficients

have predicted signs. The coefficients for investor sentiment proxies are positive. A

higher level of investor sentiment tends to increase the probability of SEO issuance,

consistent with prior market-timing analysis of SEO (Loughran and Ritter 1997).

And it is interesting to see that real estate sentiment of suppliers is negatively related

with SEO issuance probability.

Equity offerings are also more likely for young firms who are in their early stage of

growth. Yearslisted, which proxies for corporate life stage cycle, is significant and

negatively related with SEO issuance probability. This lends support to the lifecycle

theory that predicts young firms sell stock to fund investment (DeAngelo, DeAngelo

and Stulz 2010). And about the effect of growth opportunities, an increase in the

growth opportunities significantly increases the likelihood of SEO, in line with the

investment-based explanation for SEO issuance which argues that managers issue

equity by timing the investment(Carlson, Fisher and Giammarino 2006). Also, risk

premia is positively related to the equity issuance, supporting that managers time the

market by exploiting equity cost fluctuations.

[Insert Table 3]

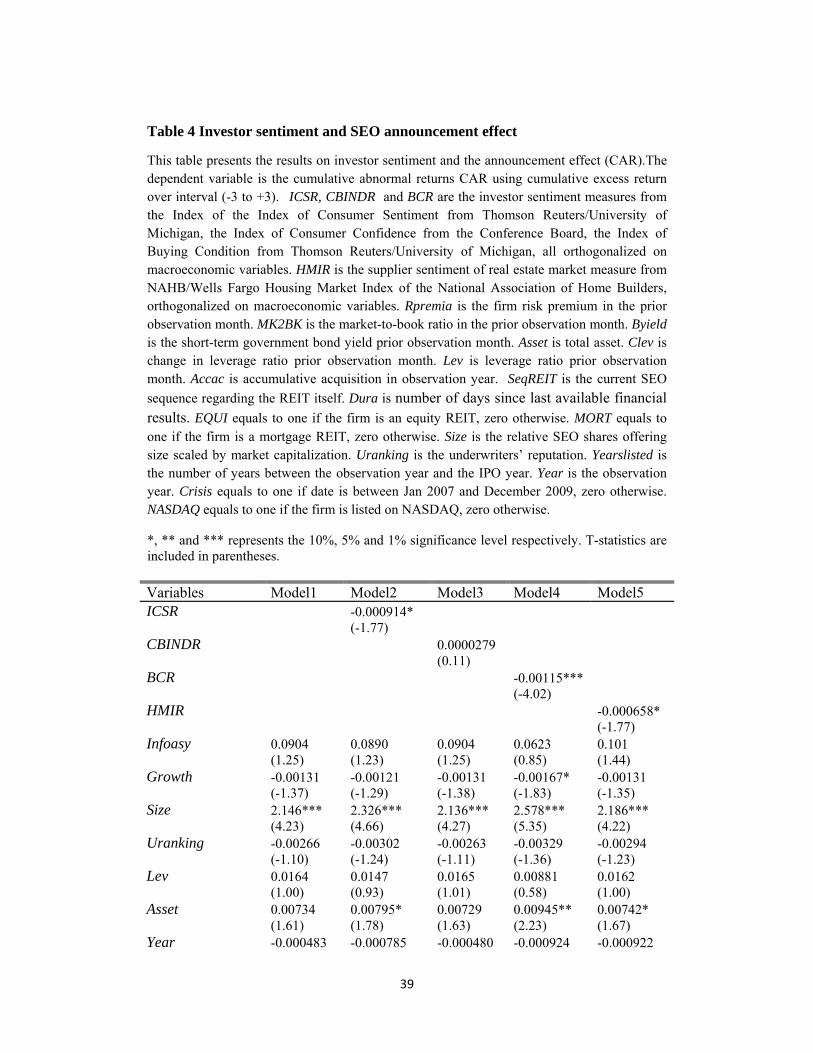

Sentiment and SEO announcement effect

Our SEO sample includes 814 events with announcement date reported in SDC. We

calculate the cumulative abnormal returns CAR using cumulative excess return over

interval (-3 to +3). We observe a statistically significant decline of 0.5% in the

22

cumulative abnormal returns (CAR) associated with the SEO announcements. This

evidence is consistent with the negative price reaction documented by previous

studies and Myers and Majluf (1984)’s pecking order hypothesis.

If the negative price reaction around announcement reflects the overvaluation, this

announcement effect tends to be affected by sentiment as sentiment contributes to

mispricing argued in prior literature. We examine the impact of investor sentiment on

the announcement effect (CAR) in a multivariate regression specified below.

Year

dYearslisteSeqREITMORTEQUIYearByield

LevSizeInfoasGrowthAssetSentimentCAR

31

121110987

6543210

(5)

Reported in Table 4 we note that sentiment proxies are all significantly negatively

related to cumulative abnormal return. Since investors interpret an equity issuance

announcement as an indicator of stock overvaluation, the stock price declines. Higher

level of investor sentiment exacerbates managers’ incentives and price decline is more

pronounced. For control variables, we observe SEO size have a positive impact on

abnormal return, which is quite different from general industry where to expect a

negative effect. And market tends to assign a positive effect on announcements of

REITs with higher leverage, which is in accordance with the prior findings in REITs.

Last, the yield of short-term bond has a negative effect on equity offering

announcements as expected.

[Insert Table 4]

Sentiment and SEO discounting

23

In order to examine the investor sentiment impact on SEO underpricing we estimate

the following regression.

NASDAQYeardYearsliste

SizeMORTEQUIInfoasSeqREITGrowthLev

UrankingAssetByieldRpremiaSentimentgDiscountin

514131

2111109876

543210

(6)

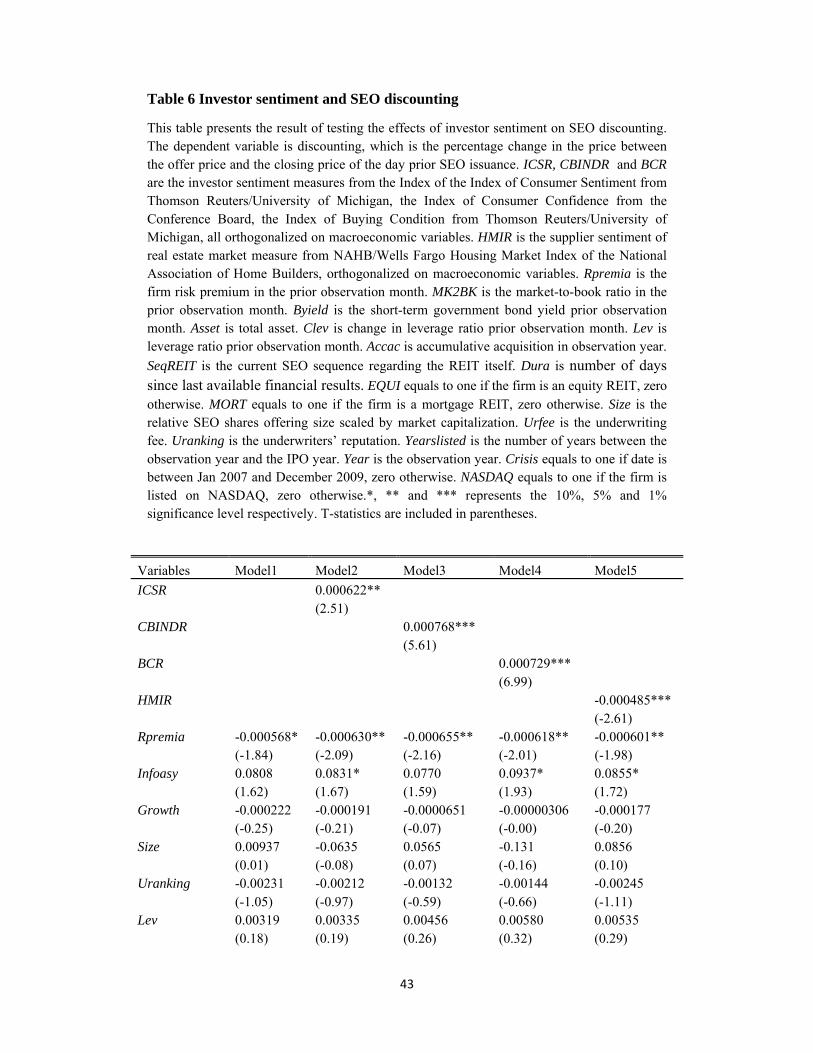

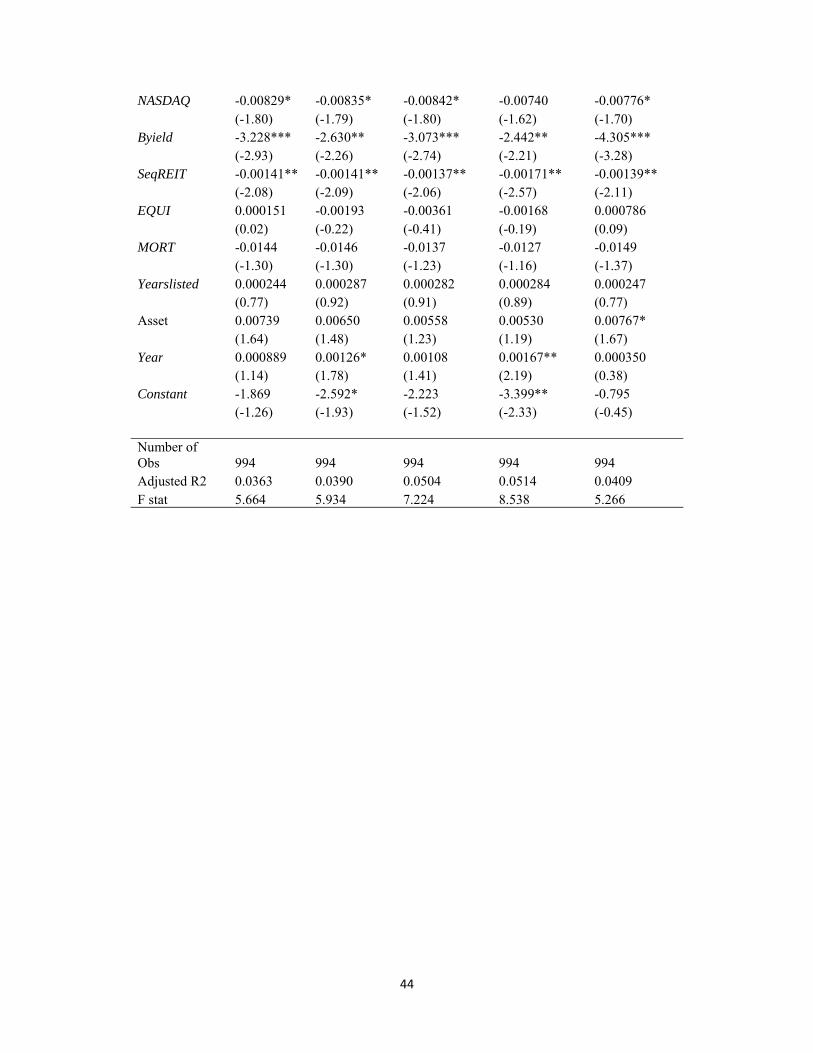

Table 6 reports the results of sentiment on SEO discounting. We note that ICSR and

CBINDR are all significant and positive indicating that investor sentiment positively

impacts the discounting level. This further suggests that firms do not fully incorporate

the effect of prevailing sentiment when setting the offer price. The interesting part is

that we observe a positive effect of BCR on discounting, but a negative effect of

HMIR. This difference indicates that investor sentiment from demand side of real

estate market influences the offer price.

For other control variables, discounting is likely to be lower for firms with higher risk

premia. Short-term bond yield has a negative effect on discounting level.

[Insert Table 6]

Sentiment and SEO underpricing

Next, we estimate the following regression to implement the investor sentiment

impact on SEO underpricing after controlling for other determinants of SEO

underpricing like what we do in discounting.

24

YeardYearslisteUrankingNASDAQ

SizeMORTEQUIInfoasSeqREITGrowthLev

ClevAssetByieldRpremiaSentimentngUnderprici

61514131

2111109876

543210

(7)

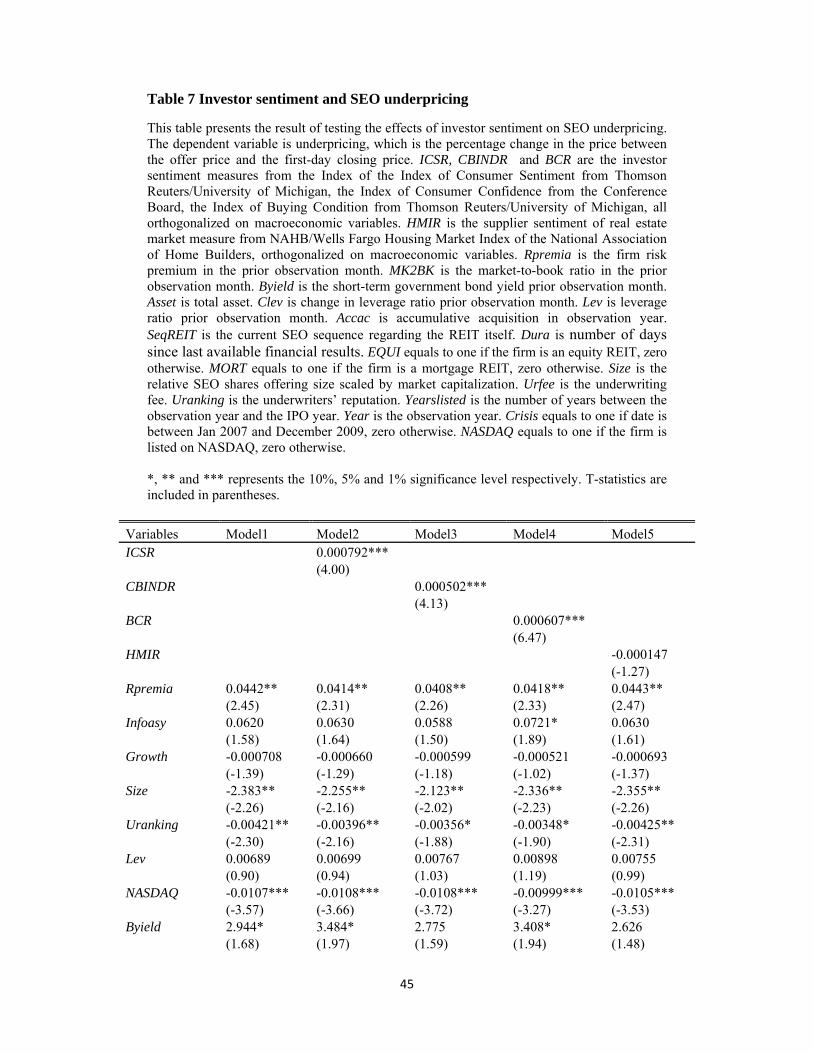

Table 7 shows the results from estimating a multivariate regression of SEO under-

pricing on investor sentiment. We observe that ICSR and CBINDR are significant and

positive, implying that an increase in investor sentiment leads to increase in the

underpricing. As sentiment investors would bid up the stock price, under-pricing is

positively related to the size of the sentiment investor, which is consistent with

previous finding in IPO market that interprets underpricing as a compensation to

regular investors(Ljungqvist, Nanda and Singh 2006). Also, we note that underpricing

is positively related with investor sentiment of real estate market, while there is no

effect on supplier sentiment.

For control variables, variables have a similar effect on underpricing like discounting.

Firms listed on NASDAQ, with a higher underwriting fee and higher past return seem

to have a lower underpricing. And firms tend to underprice more in a depressed

market.

[Insert Table 7]

Sentiment on REITs SEO activity

In the context of equity offerings, market timing theory implies that firms are more

likely to issue equity when managers perceive that the market condition is favorable.

As previous section argues, investor sentiment indicates whether the market condition

for equity issuance is good or bad. Further, for firms who conduct equity offerings in

25

a favorable market, they are likely to sell more equity than a depressed market(Alti

2006). If investor sentiment is the key determinants of market timing as proposed, the

amount of equity issued should be affected by the sentiment investors.

We measure the amount of equity issued by REITs firms at the SEO using the total

proceeds filed (Procf). We address the sentiment effect using following regression

that controls for various SEO determinants.

dYearslisteSeqREITMORT

EQUIByieldYearUrankingLevNASDAQInfoas

GrowthAssetBKMKRpremiaSentimentocf

121113

1211019876

543210 2Pr

(8)

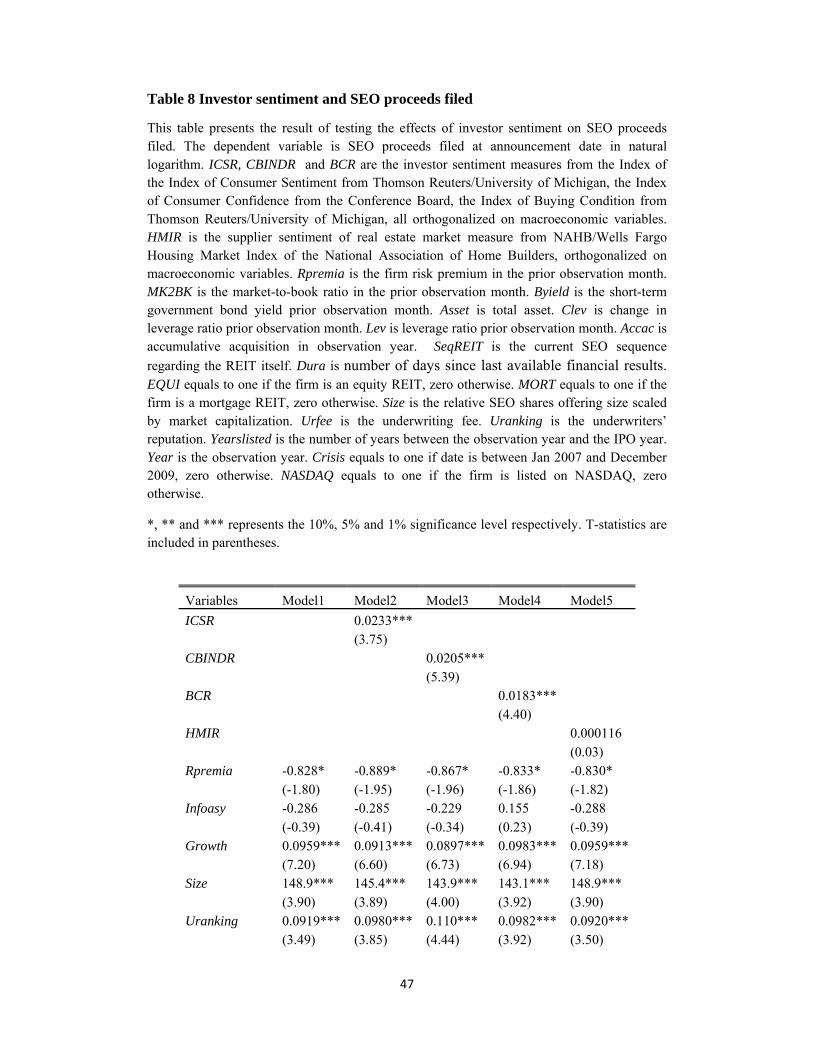

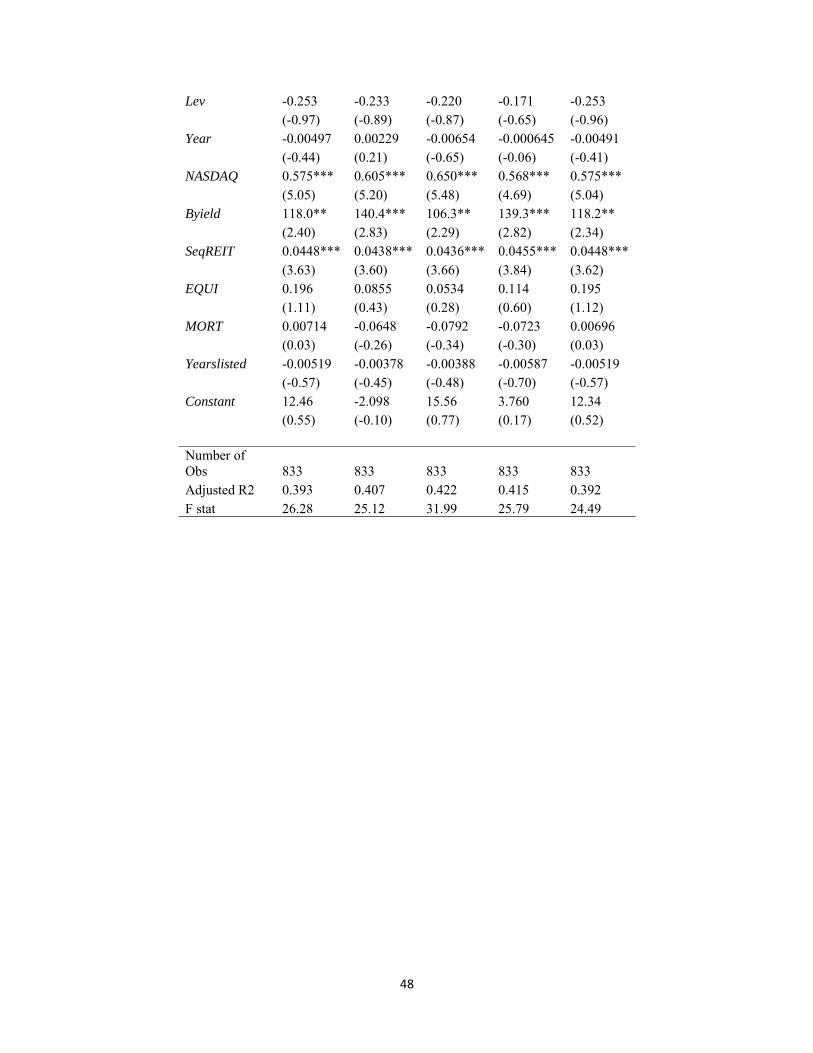

Table 8 reports the main results for sentiment on proceeds filed. The first column is

estimated without sentiment variables. Sentiment variables are added to regressions

respectively. All investor sentiment proxies are significantly positive, suggesting that

firms issue more equity at high sentiment period.

We are mindful that firms might revise their target proceeds to capture the time

varying sentiment investors.

It is possible that firms revise their target proceeds to account for the time variant

sentiment. We achieve this by analyzing the sentiment impact on proceeds generated

at issue date (Proc) with following regression.

26

dYearslisteSeqREITMORT

EQUIByieldYearUrankingLevNASDAQof

GrowthAssetInfoasRpremiaSentimentoc

121113

1211019876

543210

Pr

Pr

(9)

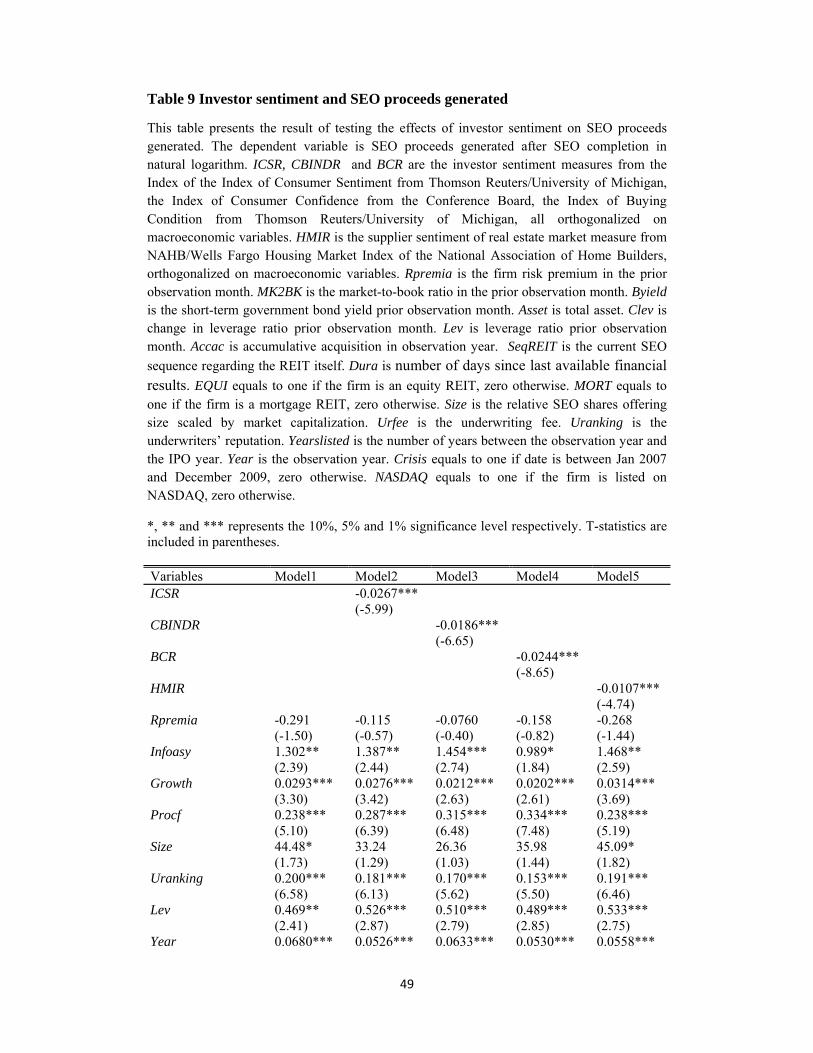

As reported in Table 9 , all sentiment variables are significantly negative related to

proceeds generated, suggesting that firms do not fully incorporate the impact of

sentiment at time of issuance(Cornelli, Goldreich and Ljungqvist 2006).

In general, SEO market volume is a significant indicator of firms’ market timing

attempts. Firms issue more stock in high sentiment periods in the market.

Sentiment and SEO long run return

Finally, we examine the impact of sentiment investors on long term stock

performance.

So far, although we have controlled for fundamentals in SEO decision and pricing, it

is not impossible that our sentiment variables may proxy for some underlying

unobservable fundamentals besides the behavioral component. If managers time the

market for mispricing, the long-run relative underperformance of stocks after

seasoned equity offerings should be identified (Loughran and Ritter 1995) as the

sentiment investors leave the market. If our sentiment proxies for the unobservable

fundamentals, SEO prices will stay at the new level and its future performance is

unrelated with the sentiment at issuance. Otherwise, if we observe long run

27

underperformance after SEO, i.e. SEO prices is mean-reverting, our proxies are

behavioral(Ljungqvist, Nanda and Singh 2006).

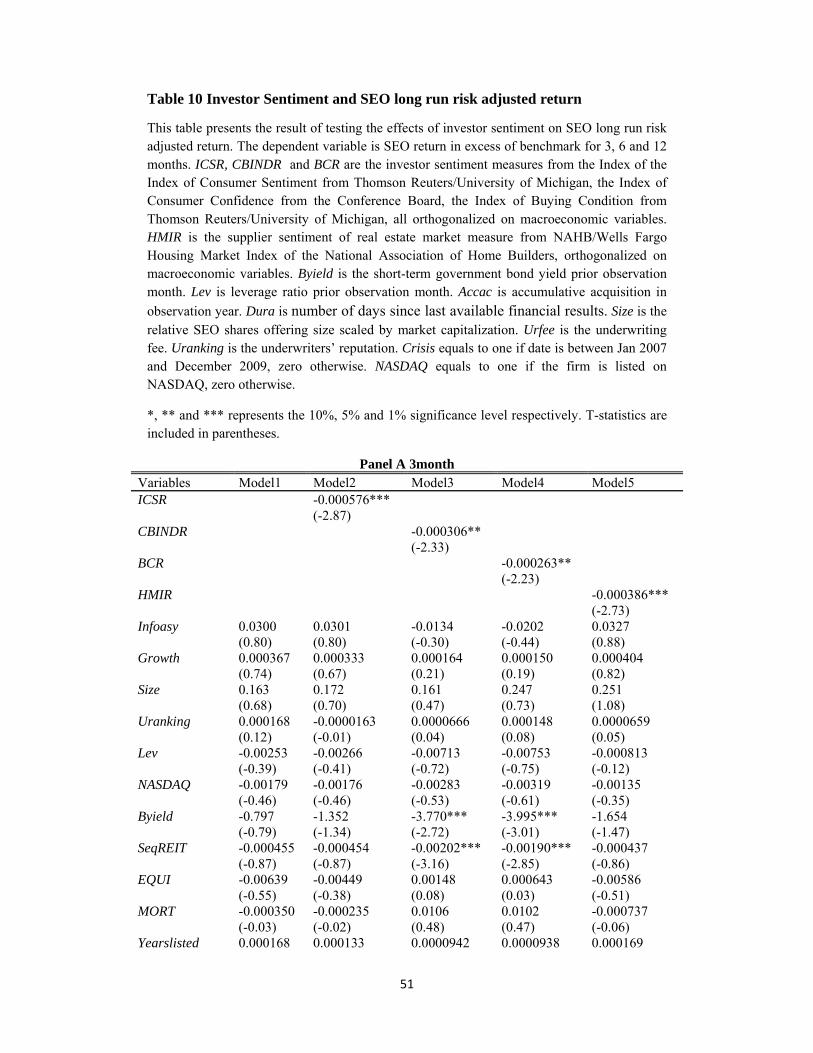

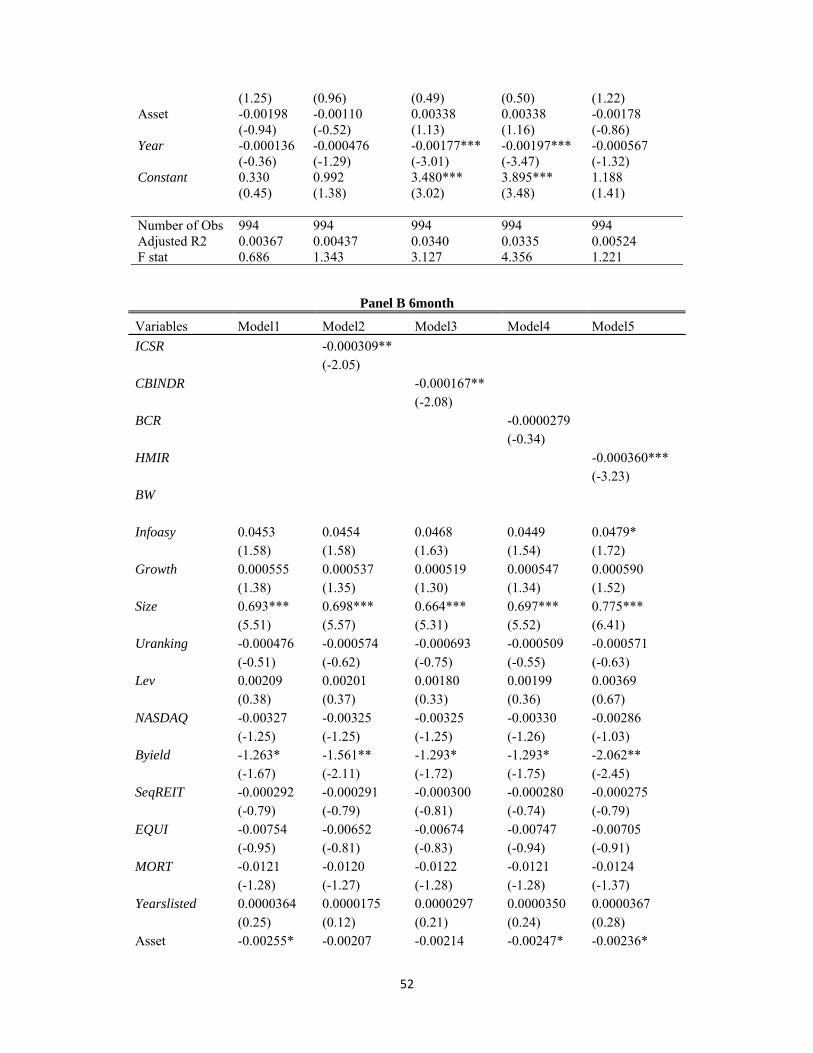

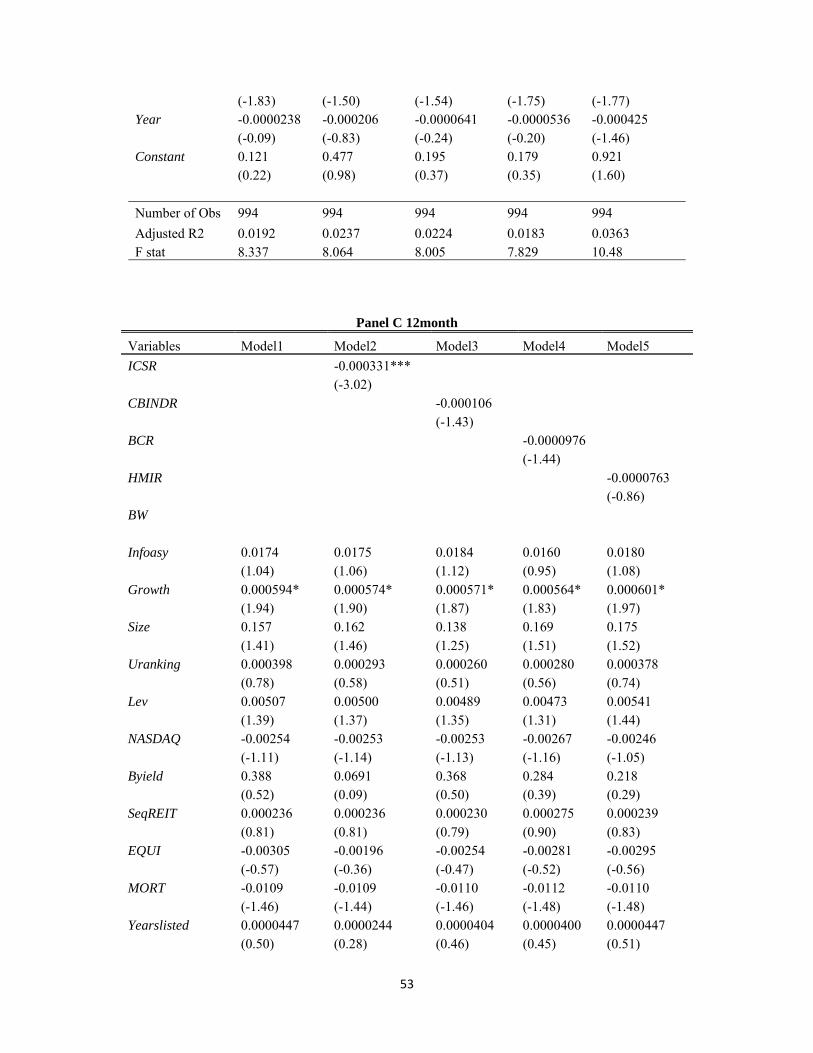

We calculate the SEO long-term risk adjusted return using Fama French four factor

model for 3, 6 and 12 months3. We specify a multivariate regression to test the impact

of investor sentiment as follows. The control variables are those shown to be

significant in explaining discounting and underpricing.

NASDAQCrisis

UrankingGrowthSizeInfoasLevSentimentLret

87

6543210

(10)

Reported in Table 10, all sentiment variables are significant at 5% level, supporting

that sentiment-oriented stock mispricing matters the equity performance in the long

run. We find that the SEO long-term risk adjusted return are negatively related to

sentiment, suggesting that SEOs revert to their fundamental values as market corrects

the misevaluation.

Robustness Test

In this section, we conduct the robustness tests of results by analyzing the SEO offer

price revision , the hot market effect, doing clustering analysis and using alternative

measure of investor sentiment.

1. Sentiment and SEO offer price revision

We further look at impact of investor sentiment on SEO offer price revision. If

managers perceive the prevailing sentiment investors, they are inclined to incorporate

3 We also calculated long run risk adjusted return applying Fama-French three factor model in the unreported regressions.

28

the sentiment effect through revising the offer price. We achieve this by analyzing the

following regression on price revision, which is defined as the price adjustment

between mid-file price and the SEO offer price.

SeqREITMORT

EQUIByieldYearUrankingLevNASDAQdYearsliste

GrowthAssetInfoasRpremiaSentimentvice

1113

1211019876

543210RePr

(11)

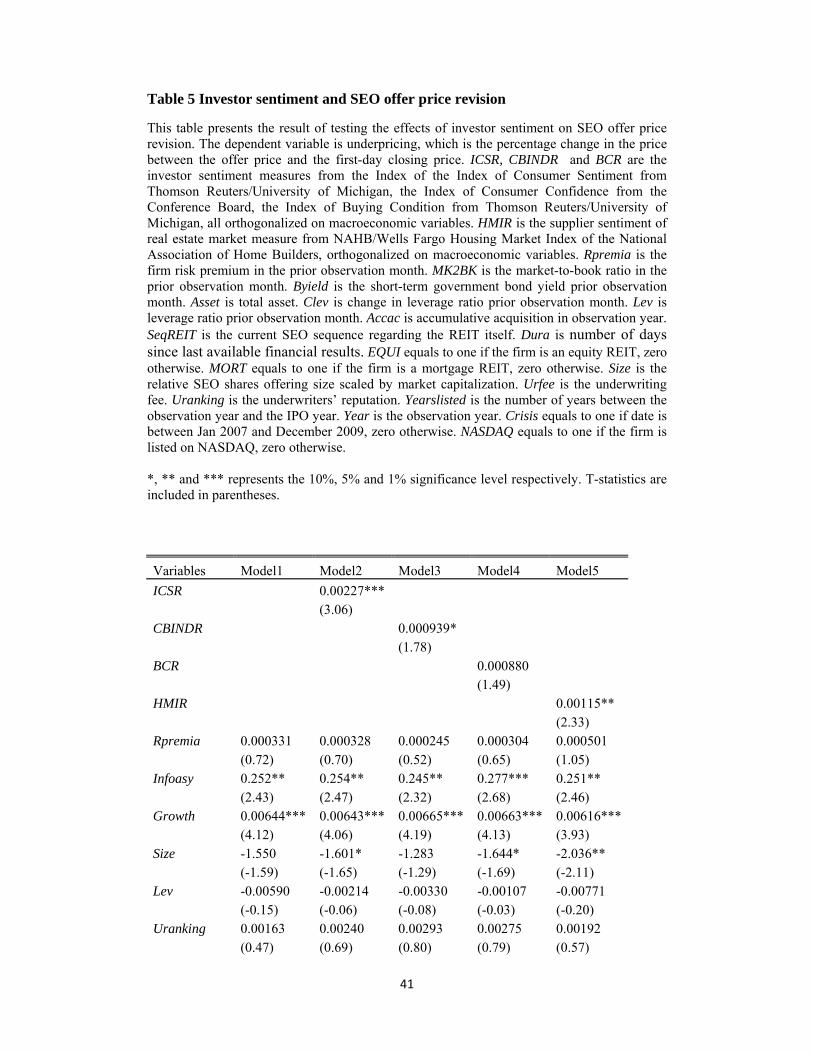

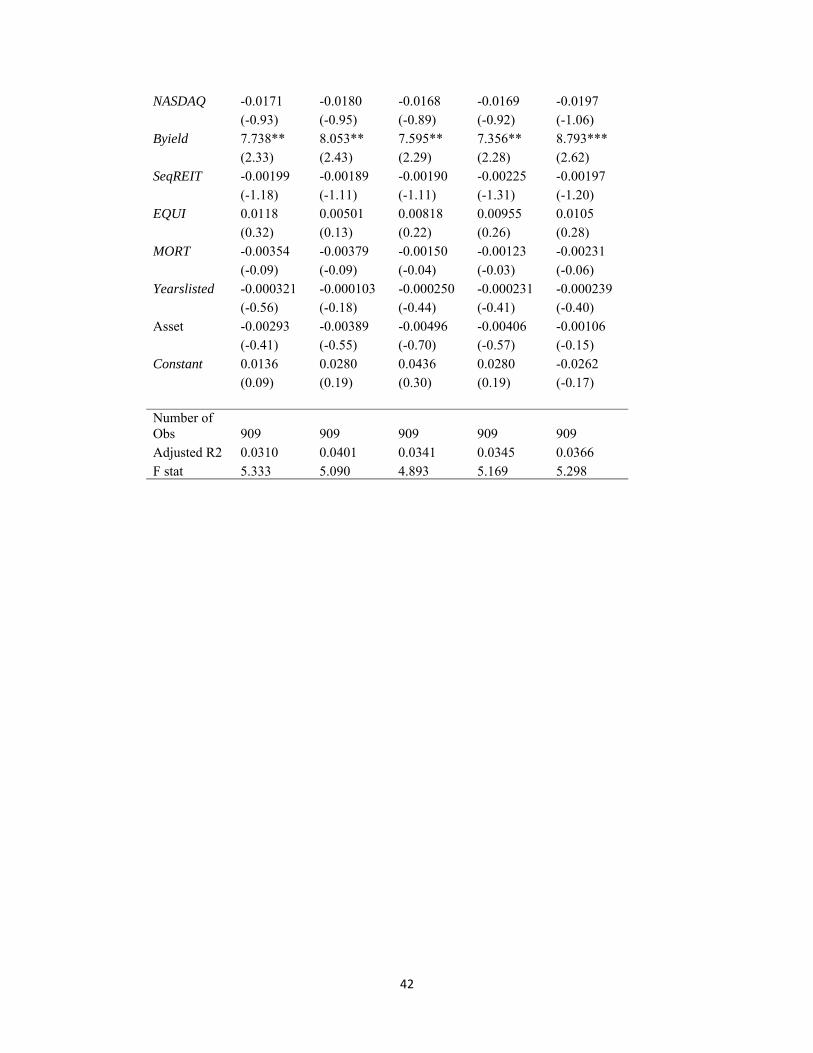

Table 5 reports the results. A higher level of investor sentiment tends to increase the

price revision magnitude, consistent with the hypothesis that that managers time the

prevailing sentiment investors in the market.

[Insert Table 5]

2. Hot market effect

IPO literature suggests that the impact of sentiment on stock price is asymmetric

between high and low sentiment periods(Hrnjić and Sankaraguruswamy 2011 ;

Ljungqvist, Nanda and Singh 2006). Firms discount more during the high sentiment

period. We further test the asymmetric relationship between sentiment and SEO

pricing by interacting CBINDR with CBINDR –AB66 and CBINDR –BL33, where

CBINDR –AB66 proxies for high sentiment periods and CBINDR –BL33 proxies for

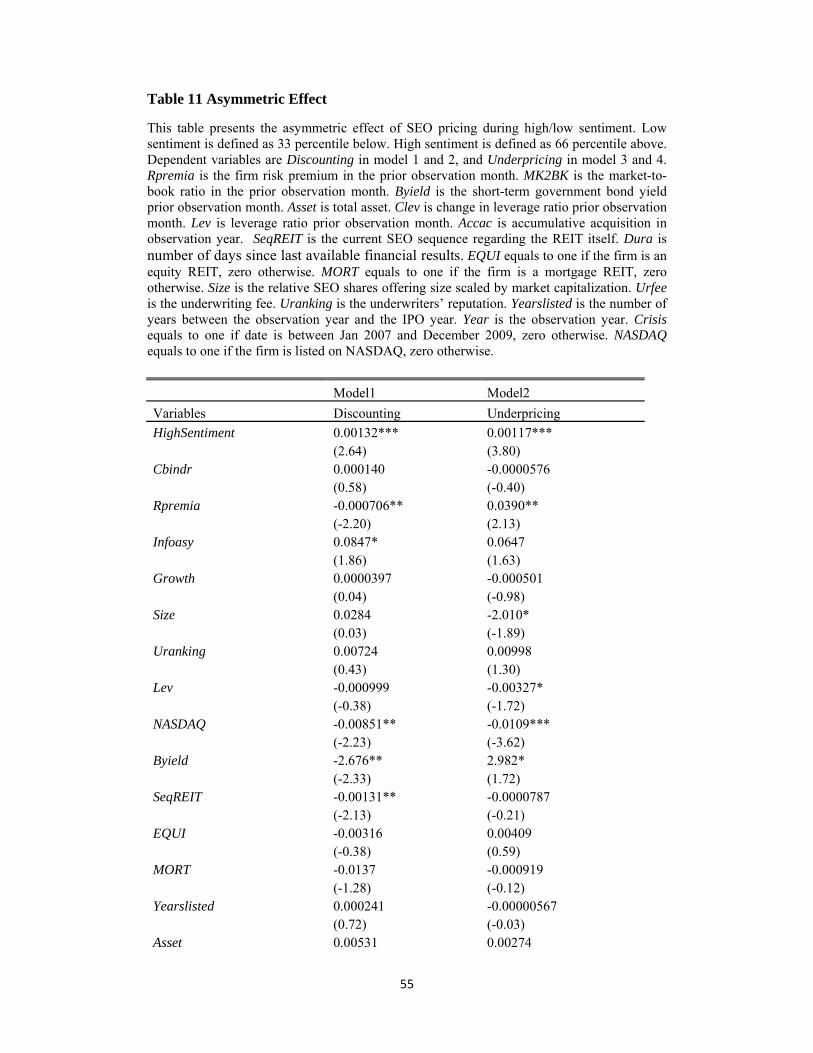

low sentiment periods . Reported in Table 111, the coefficient on interaction variable

HighSentiment is positive and significant for both discounting and underpricing,

suggesting that the relationship between sentiment and SEO pricing is asymmetric.

[Insert Table 11]

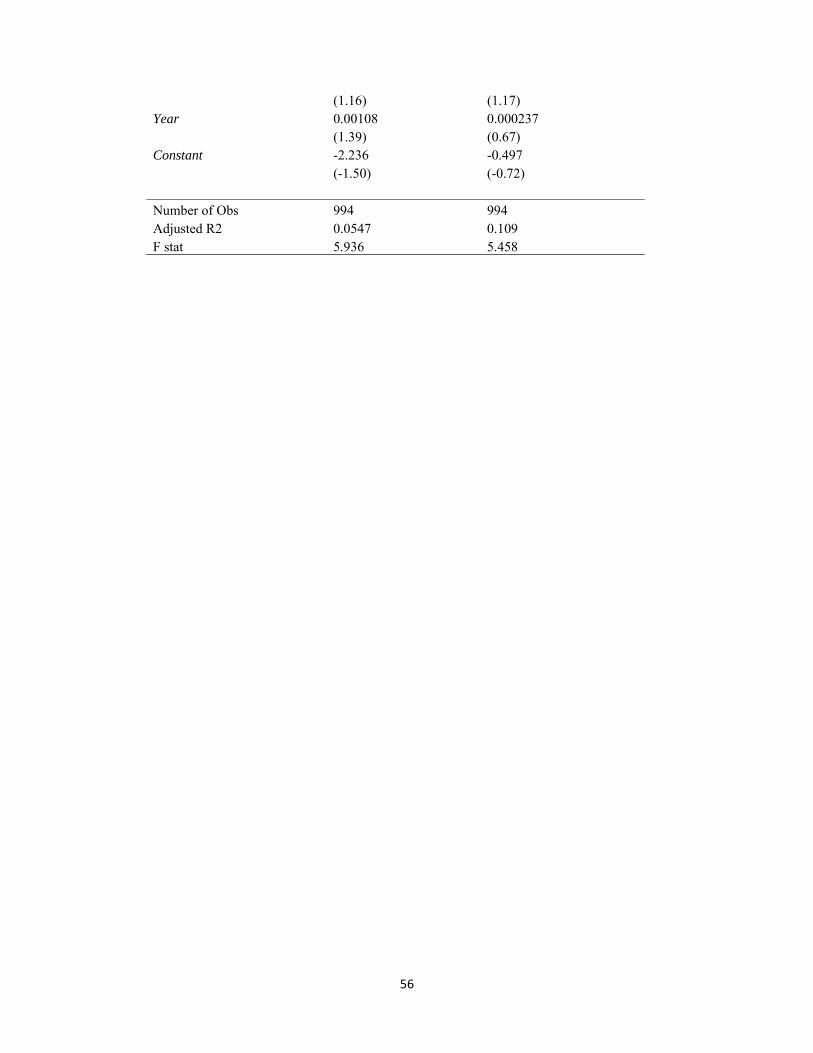

We also compare SEOs over high sentiment periods and low sentiment periods by

estimating the possibility that firms conduct SEOs during high or low sentiment

periods. From Table 12, we observe that high sentiment and low sentiment periods

do not differ in much in SEO activities, consistent with the findings in IPO market

cycles(Helwege and Liang 2004).

29

[Insert Table 12]

3. Clustering analysis

We are mindful that the equity issuance clustering effect might bias our estimates. We

address this issue by clustering error terms (Petersen 2009). We reestimate Eq. (4),

Eq. (5), Eq. (6), Eq. (7), Eq. (8), Eq. (9), and Eq. (10) after clustering standard errors

by month. The coefficients of our sentiment proxies remain significant and robust.

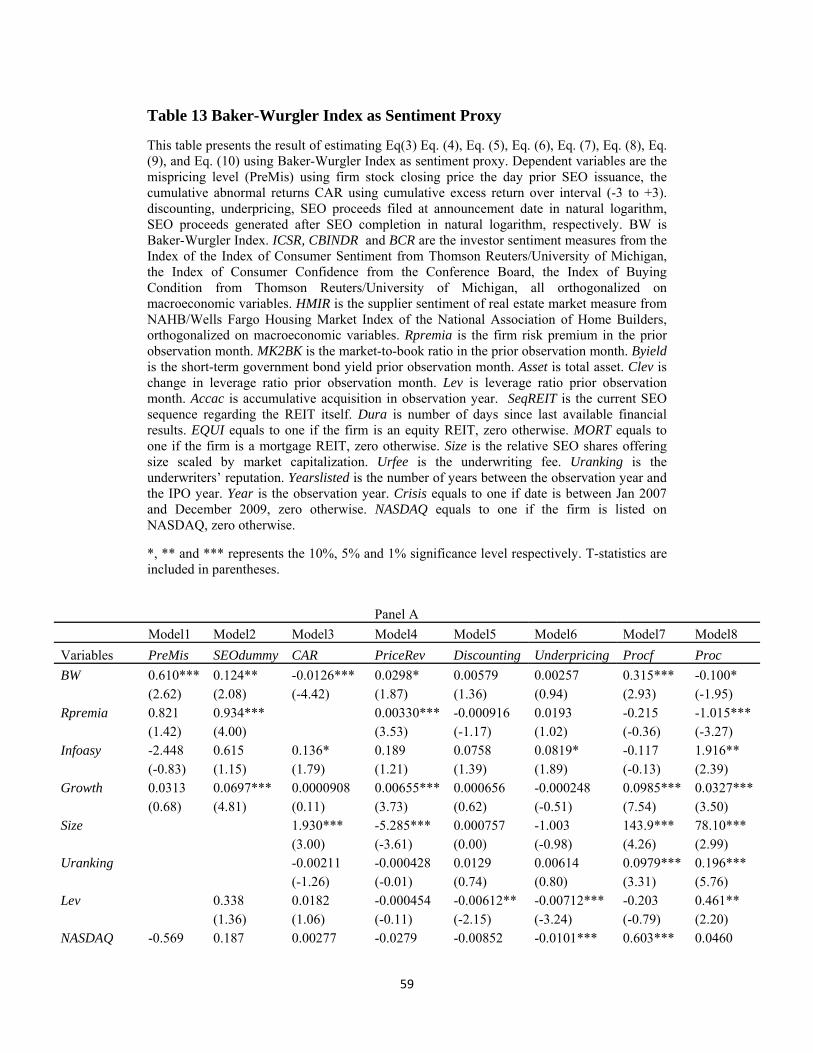

4. Alternative measure of sentiment

So far, we use direct measure of investor sentiment to quantify the effect of sentiment

on seasonal equity offerings. Another widely used measure of sentiment is Baker-

Wurgler investor sentiment index(Baker and Wurgler 2006; Baker and Wurgler 2007;

Campbell, Rhee, Du and Tang 2008; Sankaraguruswamy and Mian 2008). Baker-

Wurgler investor sentiment index is calculated by applying principle component

analysis to capture the principle component from closed end fund discount, dividend

premium, turnover, first day IPO returns, IPOs number and proportion of equity

offering.

We substitute the Baker-Wurgler index with our sentiment proxies and reestimate

Eq.(4), Eq. (5), Eq. (6), Eq. (7), Eq. (8), Eq. (9), and Eq. (10). Table 13 describes the

results. We see that most coefficients on Baker-Wurgler index are significant and all

the signs are consistent with our sentiment proxies in previous testing.

[Insert Table 13]

Conclusion

30

To the best of our knowledge, this is the first paper to analyze the impact of investor

sentiment on seasoned equity offerings. Our empirical results suggest that the level of

investor sentiment impacts pre-SEO mispricing and the decision to issue SEO.

Consistent with the notion that market interprets SEO announcement in high

sentiment periods as more negative signal, we find that announcement returns are

negatively related to sentiment. Further, we document that investor sentiment is

positively related with the SEO discounting; i.e., the higher the sentiment, the larger

the discount from the previous day closing price. Similarly, higher sentiment periods

are characterized with higher first day returns. Sentiment doesn’t seem to proxy for

unobservable risk characteristic as we find that post-SEO long run returns are more

negative in high sentiment periods.

Our paper contributes to several strands of literature. First, market timing theory

predicts that firms conduct equity issuance when the shares are overvalued. In this

paper, we examine the extent to which investors’ sentiment contributes to equity

decisions and SEO price dynamics and report that managers issue more often when

sentiment is high and shares are overpriced. Second, while empirical studies

document positive effect of investor sentiment on IPO underpricing and negative

effect on long run returns, this is the first paper to examine the impact of sentiment on

seasoned equity offerings. Third, our paper contributes to the determinants of SEO

discounting and underpricing. Altinkilic and Hansen (2003), Corwin (2003), and

Mola and Lughran (2004) empirically examine determinants of SEO discounting and

underpricing, but none of these papers examine the impact of investor sentiment. This

is the first paper to document significant impact of investor sentiment on SEO pricing

process.

31

Overall, investor sentiment seems to play an important role in seasoned equity

offerings. Our findings are consistent with market timing and behavioral explanations

for equity offering. .

Despite our best efforts to control for fundamentals like time-varying growth

opportunities and risk premia which can also explain SEO decision and pricing, it is

not impossible that there is other underlying unobservable fundamental factor

responsible for some of our results. Future work may focus on identifying these

factors and integrating them in the analysis.

32

References

Alti, A., 2006. How Persistent Is the Impact of Market Timing on Capital Structure?, Journal of Finance 61, 1681-1710.

Altinkiliç, O., and R. S. Hansen, 2003. Discounting and underpricing in seasoned equity offers, Journal of Financial Economics 69, 285-323.

Asquith, P., and D. W. Mullins Jr, 1986. Equity issues and offering dilution, Journal of Financial Economics 15, 61-89.

Baker, M., and J. Wurgler, 2002. Market Timing and Capital Structure, Journal of Finance 57, 1-32.

Baker, M., and J. Wurgler, 2006. Investor sentiment and the cross-section of stock returns, Journal of Finance 61, 1645-1680.

Baker, M., and J. Wurgler, 2007. Investor sentiment in the stock market, Journal of Economic Perspectives 21, 129-151.

Boudry, W. I., J. G. Kallberg, and C. H. Liu, 2010. An analysis of REIT security issuance decisions, Real Estate Economics 38, 91-120.

Brounen, D., and P. M. A. Eichholtz, 2001. Capital structure theory: Evidence from European property companies' capital offerings, Real Estate Economics 29, 615-632.

Brown, G. W., and M. T. Cliff, 2004. Investor sentiment and the near-term stock market, Journal of Empirical Finance 11, 1-27.

Campbell, C. J., S. G. Rhee, Y. Du, and N. Tang, 2008. Market Sentiment, IPO Underpricing, and Valuation, SSRN eLibrary.

Carlson, M., A. Fisher, and R. Giammarino, 2006. Corporate investment and asset price dynamics: Implications for SEO event studies and long-run performance, Journal of Finance 61, 1009-1034.

Clayton, J., D. C. Ling, and A. Naranjo, 2009. Commercial real estate valuation: Fundamentals versus investor sentiment, Journal of Real Estate Finance and Economics 38, 5-37.

Cornelli, F., D. Goldreich, and A. Ljungqvist, 2006. Investor Sentiment and Pre-IPO Markets, Journal of Finance 61, 1187-1216.

Corwin, S. A., 2003. The Determinants of Underpricing for Seasoned Equity Offers, Journal of Finance 58, 2249-2279.

De Long, J. B., A. Shleifer, L. H. Summers, and R. J. Waldmann, 1990. Noise Trader Risk in Financial Markets, Journal of Political Economy 98, 703.

DeAngelo, H., L. DeAngelo, and R. M. Stulz, 2010. Seasoned equity offerings, market timing, and the corporate lifecycle, Journal of Financial Economics 95, 275-295.

Derrien, F., 2005. IPO Pricing in“Hot” Market Conditions: Who Leaves Money on the Table?, Journal of Finance 60, 487-521.

Dorn, D., 2009. Does sentiment drive the retail demand for IPOs?, Journal of Financial and Quantitative Analysis 44, 85-108.

Eckbo, B. E., and R. W. Masulis, 1992. Adverse selection and the rights offer paradox, Journal of Financial Economics 32, 293-332.

Fu, F., L. Lin, and M. S. Officer, 2010. Acquisitions Driven by Stock Overvaluation: Are They Good Deals?, SSRN eLibrary.

Ghosh, C., R. Nag, and C. F. Sirmans, 2000. The pricing of seasoned equity offerings: Evidence from REITs, Real Estate Economics 28, 363-384.

Graham, J. R., and C. R. Harvey, 2001. The theory and practice of corporate finance: evidence from the field, Journal of Financial Economics 60, 187-243.

Helwege, J., and N. Liang, 2004. Initial public offerings in hot and cold markets, Journal of Financial and Quantitative Analysis 39, 541-569.

Hertzel, M., E. Hrnjić, M. Officer, and C. Si, 2011. Why Do Firms Go Public? Evidence from the Decomposition of M/B ratio, Working paper.

Hertzel, M. G., and Z. Li, 2010. Behavioral and rational explanations of stock price performance around SEOs: Evidence from a decomposition of market-to-book ratios, Journal of Financial and Quantitative Analysis 45, 935-958.

33

Hrnjić, E., and S. Sankaraguruswamy, 2011 Market-wide Sentiment, Firm-level Sentiment, and IPO Pricing Process, EFA.

Jung, K., Y. C. Kim, and R. M. Stulz, 1996. Timing, investment opportunities, managerial discretion, and the security issue decision, Journal of Financial Economics 42, 159-185.

Korajczyk, R., D. Lucas, and R. McDonald, 1991. The effect of information releases on the pricing and timing of equity issues, Review of Financial Studies 4, 685-708.

Lemmon, M., and E. Portniaguina, 2006. Consumer confidence and asset prices: Some empirical evidence, Review of Financial Studies 19, 1499-1529.

Ljungqvist, A., V. Nanda, and R. Singh, 2006. Hot markets, investor sentiment, and IPO pricing, Journal of Business 79, 1667-1702.

Loughran, T., and J. R. Ritter, 1995. The new issues puzzle, Journal of Finance 50, 23-51. Loughran, T., and J. R. Ritter, 1997. The operating performance of firms conducting seasoned

equity offerings, Journal of Finance 52, 1823-1850. Loughran, T., J. R. Ritter, and K. Rydqvist, 1994. Initial public offerings: International

insights, Pacific-Basin Finance Journal 2, 165-199. Mola, S., and T. Loughran, 2004. Discounting and Clustering in Seasoned Equity Offering

Prices, Journal of Financial and Quantitative Analysis 39, 1-23. Myers, S. C., and N. S. Majluf, 1984. Corporate financing and investment decisions when

firms have information that investors do not have, Journal of Financial Economics 13, 187-221.

Ong, S., J. Ooi, and Y. Kawaguichi, 2011. Seasoned Equity Issuance by Japan and Singapore REITs, The Journal of Real Estate Finance and Economics 43, 205-220.

Ooi, J., S.-E. Ong, and L. Li, 2010. An Analysis of the Financing Decisions of REITs: The Role of Market Timing and Target Leverage, The Journal of Real Estate Finance and Economics 40, 130-160.

Petersen, M., 2009. Estimating standard errors in finance panel data sets: Comparing approaches, Review of Financial Studies 22, 435-480.

Qiu, L. X., and I. Welch, 2004. Investor Sentiment Measures, SSRN eLibrary. Rhodes-Kropf, M., D. T. Robinson, and S. Viswanathan, 2005. Valuation waves and merger

activity: The empirical evidence, Journal of Financial Economics 77, 561-603. Safieddine, A., and W. J. Wilhelm Jr, 1996. An empirical investigation of short-selling

activity prior to seasoned equity offerings, Journal of Finance 51, 729-749. Sankaraguruswamy, S., and G. M. Mian, 2008. Investor Sentiment and Stock Market

Response to Corporate News, SSRN eLibrary. Shleifer, A., and R. W. Vishny, 1997. The limits of arbitrage, Journal of Finance 52, 35-55. Stein, J. C., 1996. Rational capital budgeting in an irrational world, Journal of Business 69,

429-455. Teoh, S. H., I. Welch, and T. J. Wong, 1997. Earnings management and the

underperformance of seasoned equity offerings, Journal of Financial Economics. Yung, C., G. Çolak, and W. Wei, 2008. Cycles in the IPO market, Journal of Financial

Economics 89, 192-208.

34

Table 1 Descriptive Statistics

This table presents the descriptive statistics of the variables used in this paper. ICSR, CBINDR and BCR are the investor sentiment measures from the Index of the Index of Consumer Sentiment from Thomson Reuters/University of Michigan, the Index of Consumer Confidence from the Conference Board, the Index of Buying Condition from Thomson Reuters/University of Michigan, all orthogonalized on macroeconomic variables. HMIR is the supplier sentiment of real estate market measure from NAHB/Wells Fargo Housing Market Index of the National Association of Home Builders, orthogonalized on macroeconomic variables. Rpremia is the firm risk premium in the prior observation month. Byield is the short-term government bond yield prior observation month. Asset is total asset. Lev is leverage ratio prior observation month. SeqREIT is the current SEO sequence regarding the REIT itself. EQUI equals to one if the firm is an equity REIT, zero otherwise. MORT equals to one if the firm is a mortgage REIT, zero otherwise. Size is the relative SEO shares offering size scaled by market capitalization. Uranking is the underwriters’ reputation. Yearslisted is the number of years between the observation year and the IPO year. Year is the observation year. NASDAQ equals to one if the firm is listed on NASDAQ, zero otherwise.

Variable Mean Med Standard Deviation

ICSR 0.0617 0.749 6.752 CBINDR 2.134 3.917 11 BCR 0.314 -1.600 12 HMIR -1.900 -1.200 11 Underpricing 0.0178 0.00658 0.0431 Discounting 0.0279 0.0179 0.0648 PreMis 2.459 2.544 3.058 Rpremia -0.286 -0.347 0.240 Byield 0.00330 0.00382 0.00171 Asset 2700 1400 4800 Lev 0.589 0.575 0.199 SeqREIT 4.580 3 3.933 EQUI 0.836 1 0.370 MORT 0.136 0 0.343 Size 0.000306 0.000127 0.00222 Uranking 8.021 9 1.619 Yearslisted 8.619 5 8.722 Year 2000 2000 5.112 NASDAQ 0.129 0 0.335 Lret3 0.00974 0.00878 0.0323 Lret6 0.00577 0.00595 0.0243 Lret12 0.00509 0.00568 0.0199 Proc 4.274 4.271 0.951 Procf 5.196 5.298 1.130 CAR -0.00469 -0.0103 0.0596

35

Table 2 Investor sentiment and pre-SEO valuation

This table presents the results of testing the relationship between stock mispricing prior offer date and investor sentiment. Dependent variable is the mispricing level (PreMis) using firm stock closing price the day prior SEO issuance. ICSR, CBINDR and BCR are the investor sentiment measures from the Index of the Index of Consumer Sentiment from Thomson Reuters/University of Michigan, the Index of Consumer Confidence from the Conference Board, the Index of Buying Condition from Thomson Reuters/University of Michigan, all orthogonalized on macroeconomic variables. HMIR is the supplier sentiment of real estate market measure from NAHB/Wells Fargo Housing Market Index of the National Association of Home Builders, orthogonalized on macroeconomic variables. Rpremia is the firm risk premium in the prior observation month. Byield is the short-term government bond yield prior

observation month. SeqREIT is the current SEO sequence regarding the REIT itself. Growth is the third component of RKRV(2005) market-to-book decomposition to control for the market reaction associated with growth/ investment opportunities. Infoas is the abnormal return around earning announcement releases as a proxy for information asymmetry. EQUI equals to one if the firm is an equity REIT, zero otherwise. MORT equals to one if the firm is a mortgage REIT, zero otherwise. Yearslisted is the number of years between the observation year and the IPO year. Year is the observation year. NASDAQ equals to one if the firm is listed on NASDAQ, zero otherwise.

*, ** and *** represents the 10%, 5% and 1% significance level respectively. T-statistics are included in parentheses.

Variables Model1 Model2 Model3 Model4 Model5 ICSR 0.0503***

(2.97) CBINDR 0.0312***

(2.79) BCR 0.0361***

(4.07) HMIR 0.0315***

(2.88) Rpremia 0.00253 -0.0980 -0.0512 -0.0903 -0.0754

(0.00) (-0.14) (-0.07) (-0.13) (-0.12) Infoasy -2.918 -2.926 -3.244 -2.462 -2.973

(-1.39) (-1.37) (-1.52) (-1.18) (-1.41) Growth -0.0331 -0.0365 -0.0309 -0.0287 -0.0356

(-0.74) (-0.81) (-0.69) (-0.64) (-0.79) NASDAQ -0.477 -0.464 -0.461 -0.417 -0.516

(-0.91) (-0.89) (-0.88) (-0.79) (-0.96) Byield 332.9*** 370.1*** 333.1*** 360.2*** 395.1***

(3.70) (4.00) (3.56) (3.95) (4.46) SeqREIT 0.154*** 0.147*** 0.149*** 0.131** 0.152***

(3.22) (3.08) (3.16) (2.58) (3.29) EQUI -0.704 -0.854 -0.821 -0.807 -0.742

(-1.00) (-1.27) (-1.20) (-1.18) (-1.04)

36

MORT -0.875 -0.959 -0.910 -0.896 -0.897 (-1.12) (-1.28) (-1.19) (-1.18) (-1.14)

Yearslisted 0.0288 0.0317* 0.0297* 0.0303* 0.0286 (1.60) (1.82) (1.67) (1.72) (1.63)

Year 0.0122 0.0350 0.0137 0.0402 0.0445 (0.33) (0.91) (0.37) (1.05) (1.17)

Constant -22.39 -67.96 -25.38 -78.35 -87.03 (-0.30) (-0.89) (-0.34) (-1.02) (-1.15)

Number of Obs 994 994 994 994 994 Adjusted R2 0.0650 0.0756 0.0761 0.0827 0.0750 F stat 3.955 5.809 6.001 6.330 5.022

37

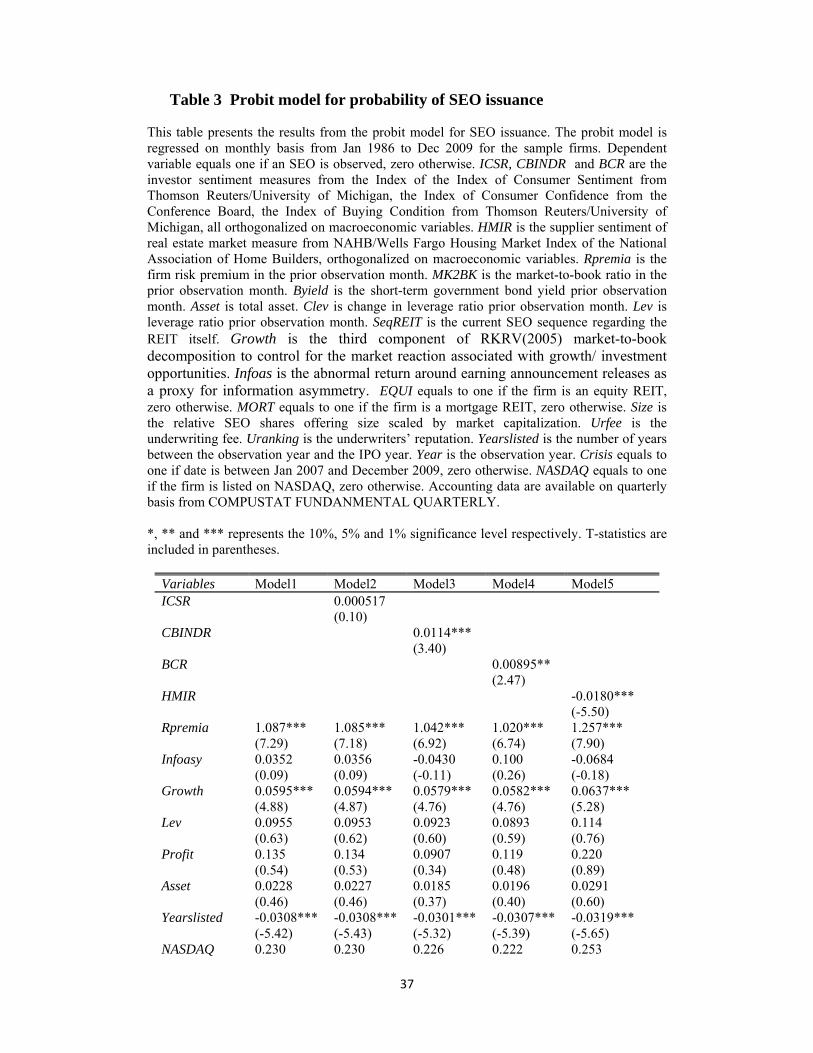

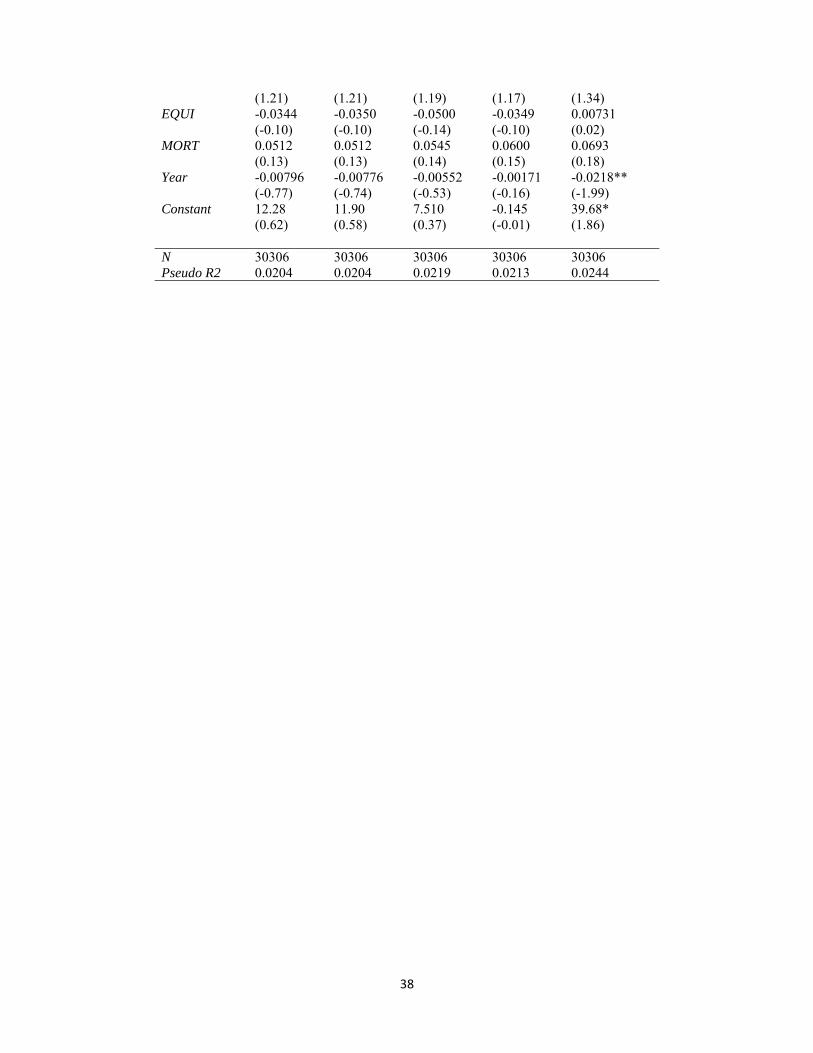

Table 3 Probit model for probability of SEO issuance

This table presents the results from the probit model for SEO issuance. The probit model is regressed on monthly basis from Jan 1986 to Dec 2009 for the sample firms. Dependent variable equals one if an SEO is observed, zero otherwise. ICSR, CBINDR and BCR are the investor sentiment measures from the Index of the Index of Consumer Sentiment from Thomson Reuters/University of Michigan, the Index of Consumer Confidence from the Conference Board, the Index of Buying Condition from Thomson Reuters/University of Michigan, all orthogonalized on macroeconomic variables. HMIR is the supplier sentiment of real estate market measure from NAHB/Wells Fargo Housing Market Index of the National Association of Home Builders, orthogonalized on macroeconomic variables. Rpremia is the firm risk premium in the prior observation month. MK2BK is the market-to-book ratio in the prior observation month. Byield is the short-term government bond yield prior observation month. Asset is total asset. Clev is change in leverage ratio prior observation month. Lev is leverage ratio prior observation month. SeqREIT is the current SEO sequence regarding the REIT itself. Growth is the third component of RKRV(2005) market-to-book decomposition to control for the market reaction associated with growth/ investment opportunities. Infoas is the abnormal return around earning announcement releases as a proxy for information asymmetry. EQUI equals to one if the firm is an equity REIT, zero otherwise. MORT equals to one if the firm is a mortgage REIT, zero otherwise. Size is the relative SEO shares offering size scaled by market capitalization. Urfee is the underwriting fee. Uranking is the underwriters’ reputation. Yearslisted is the number of years between the observation year and the IPO year. Year is the observation year. Crisis equals to one if date is between Jan 2007 and December 2009, zero otherwise. NASDAQ equals to one if the firm is listed on NASDAQ, zero otherwise. Accounting data are available on quarterly basis from COMPUSTAT FUNDANMENTAL QUARTERLY. *, ** and *** represents the 10%, 5% and 1% significance level respectively. T-statistics are included in parentheses.

Variables Model1 Model2 Model3 Model4 Model5 ICSR 0.000517

(0.10) CBINDR 0.0114***

(3.40) BCR 0.00895**

(2.47) HMIR -0.0180***

(-5.50) Rpremia 1.087*** 1.085*** 1.042*** 1.020*** 1.257***

(7.29) (7.18) (6.92) (6.74) (7.90) Infoasy 0.0352 0.0356 -0.0430 0.100 -0.0684

(0.09) (0.09) (-0.11) (0.26) (-0.18) Growth 0.0595*** 0.0594*** 0.0579*** 0.0582*** 0.0637***

(4.88) (4.87) (4.76) (4.76) (5.28) Lev 0.0955 0.0953 0.0923 0.0893 0.114

(0.63) (0.62) (0.60) (0.59) (0.76) Profit 0.135 0.134 0.0907 0.119 0.220

(0.54) (0.53) (0.34) (0.48) (0.89) Asset 0.0228 0.0227 0.0185 0.0196 0.0291

(0.46) (0.46) (0.37) (0.40) (0.60) Yearslisted -0.0308*** -0.0308*** -0.0301*** -0.0307*** -0.0319***

(-5.42) (-5.43) (-5.32) (-5.39) (-5.65) NASDAQ 0.230 0.230 0.226 0.222 0.253

38

(1.21) (1.21) (1.19) (1.17) (1.34) EQUI -0.0344 -0.0350 -0.0500 -0.0349 0.00731

(-0.10) (-0.10) (-0.14) (-0.10) (0.02) MORT 0.0512 0.0512 0.0545 0.0600 0.0693

(0.13) (0.13) (0.14) (0.15) (0.18) Year -0.00796 -0.00776 -0.00552 -0.00171 -0.0218**

(-0.77) (-0.74) (-0.53) (-0.16) (-1.99) Constant 12.28 11.90 7.510 -0.145 39.68*

(0.62) (0.58) (0.37) (-0.01) (1.86) N 30306 30306 30306 30306 30306 Pseudo R2 0.0204 0.0204 0.0219 0.0213 0.0244

39

Table 4 Investor sentiment and SEO announcement effect

This table presents the results on investor sentiment and the announcement effect (CAR).The dependent variable is the cumulative abnormal returns CAR using cumulative excess return over interval (-3 to +3). ICSR, CBINDR and BCR are the investor sentiment measures from the Index of the Index of Consumer Sentiment from Thomson Reuters/University of Michigan, the Index of Consumer Confidence from the Conference Board, the Index of Buying Condition from Thomson Reuters/University of Michigan, all orthogonalized on macroeconomic variables. HMIR is the supplier sentiment of real estate market measure from NAHB/Wells Fargo Housing Market Index of the National Association of Home Builders, orthogonalized on macroeconomic variables. Rpremia is the firm risk premium in the prior observation month. MK2BK is the market-to-book ratio in the prior observation month. Byield is the short-term government bond yield prior observation month. Asset is total asset. Clev is change in leverage ratio prior observation month. Lev is leverage ratio prior observation month. Accac is accumulative acquisition in observation year. SeqREIT is the current SEO

sequence regarding the REIT itself. Dura is number of days since last available financial results. EQUI equals to one if the firm is an equity REIT, zero otherwise. MORT equals to one if the firm is a mortgage REIT, zero otherwise. Size is the relative SEO shares offering size scaled by market capitalization. Uranking is the underwriters’ reputation. Yearslisted is the number of years between the observation year and the IPO year. Year is the observation year. Crisis equals to one if date is between Jan 2007 and December 2009, zero otherwise. NASDAQ equals to one if the firm is listed on NASDAQ, zero otherwise.

*, ** and *** represents the 10%, 5% and 1% significance level respectively. T-statistics are included in parentheses. Variables Model1 Model2 Model3 Model4 Model5 ICSR -0.000914*

(-1.77) CBINDR 0.0000279

(0.11) BCR -0.00115***

(-4.02) HMIR -0.000658*

(-1.77) Infoasy 0.0904 0.0890 0.0904 0.0623 0.101

(1.25) (1.23) (1.25) (0.85) (1.44) Growth -0.00131 -0.00121 -0.00131 -0.00167* -0.00131

(-1.37) (-1.29) (-1.38) (-1.83) (-1.35) Size 2.146*** 2.326*** 2.136*** 2.578*** 2.186***

(4.23) (4.66) (4.27) (5.35) (4.22) Uranking -0.00266 -0.00302 -0.00263 -0.00329 -0.00294

(-1.10) (-1.24) (-1.11) (-1.36) (-1.23) Lev 0.0164 0.0147 0.0165 0.00881 0.0162

(1.00) (0.93) (1.01) (0.58) (1.00) Asset 0.00734 0.00795* 0.00729 0.00945** 0.00742*

(1.61) (1.78) (1.63) (2.23) (1.67) Year -0.000483 -0.000785 -0.000480 -0.000924 -0.000922

40

(-0.46) (-0.79) (-0.46) (-0.91) (-0.95) NASDAQ 0.00440 0.00442 0.00436 0.00285 0.00438

(0.54) (0.54) (0.53) (0.39) (0.54) Byield -2.061 -2.926 -2.064 -3.318 -4.360*

(-0.99) (-1.48) (-0.98) (-1.62) (-1.97) SeqREIT 0.000603 0.000561 0.000606 0.000383 0.000566

(0.85) (0.82) (0.86) (0.58) (0.84) EQUI -0.00470 -0.000243 -0.00489 0.000623 -0.00373

(-0.49) (-0.02) (-0.50) (0.07) (-0.39) MORT -0.0130 -0.0100 -0.0131 -0.00890 -0.0123

(-0.80) (-0.61) (-0.80) (-0.57) (-0.77) Yearslisted 0.0000158 -0.0000420 0.0000183 0.0000453 0.00000150

(0.05) (-0.14) (0.06) (0.16) (0.01) Constant 0.785 1.375 0.780 1.618 1.669

(0.38) (0.71) (0.38) (0.82) (0.88) Number of Obs 832 832 832 832 832 Adjusted R2 0.0254 0.0323 0.0243 0.0560 0.0332 F stat 3.275 3.351 3.117 5.009 3.217

41

Table 5 Investor sentiment and SEO offer price revision

This table presents the result of testing the effects of investor sentiment on SEO offer price revision. The dependent variable is underpricing, which is the percentage change in the price between the offer price and the first-day closing price. ICSR, CBINDR and BCR are the investor sentiment measures from the Index of the Index of Consumer Sentiment from Thomson Reuters/University of Michigan, the Index of Consumer Confidence from the Conference Board, the Index of Buying Condition from Thomson Reuters/University of Michigan, all orthogonalized on macroeconomic variables. HMIR is the supplier sentiment of real estate market measure from NAHB/Wells Fargo Housing Market Index of the National Association of Home Builders, orthogonalized on macroeconomic variables. Rpremia is the firm risk premium in the prior observation month. MK2BK is the market-to-book ratio in the prior observation month. Byield is the short-term government bond yield prior observation month. Asset is total asset. Clev is change in leverage ratio prior observation month. Lev is leverage ratio prior observation month. Accac is accumulative acquisition in observation year. SeqREIT is the current SEO sequence regarding the REIT itself. Dura is number of days since last available financial results. EQUI equals to one if the firm is an equity REIT, zero otherwise. MORT equals to one if the firm is a mortgage REIT, zero otherwise. Size is the relative SEO shares offering size scaled by market capitalization. Urfee is the underwriting fee. Uranking is the underwriters’ reputation. Yearslisted is the number of years between the observation year and the IPO year. Year is the observation year. Crisis equals to one if date is between Jan 2007 and December 2009, zero otherwise. NASDAQ equals to one if the firm is listed on NASDAQ, zero otherwise. *, ** and *** represents the 10%, 5% and 1% significance level respectively. T-statistics are included in parentheses.

Variables Model1 Model2 Model3 Model4 Model5

ICSR 0.00227***(3.06)

CBINDR 0.000939* (1.78)

BCR 0.000880 (1.49)

HMIR 0.00115** (2.33)

Rpremia 0.000331 0.000328 0.000245 0.000304 0.000501 (0.72) (0.70) (0.52) (0.65) (1.05)

Infoasy 0.252** 0.254** 0.245** 0.277*** 0.251** (2.43) (2.47) (2.32) (2.68) (2.46)

Growth 0.00644*** 0.00643*** 0.00665*** 0.00663*** 0.00616*** (4.12) (4.06) (4.19) (4.13) (3.93)

Size -1.550 -1.601* -1.283 -1.644* -2.036** (-1.59) (-1.65) (-1.29) (-1.69) (-2.11)

Lev -0.00590 -0.00214 -0.00330 -0.00107 -0.00771 (-0.15) (-0.06) (-0.08) (-0.03) (-0.20)

Uranking 0.00163 0.00240 0.00293 0.00275 0.00192 (0.47) (0.69) (0.80) (0.79) (0.57)

42

NASDAQ -0.0171 -0.0180 -0.0168 -0.0169 -0.0197 (-0.93) (-0.95) (-0.89) (-0.92) (-1.06)

Byield 7.738** 8.053** 7.595** 7.356** 8.793*** (2.33) (2.43) (2.29) (2.28) (2.62)

SeqREIT -0.00199 -0.00189 -0.00190 -0.00225 -0.00197 (-1.18) (-1.11) (-1.11) (-1.31) (-1.20)

EQUI 0.0118 0.00501 0.00818 0.00955 0.0105 (0.32) (0.13) (0.22) (0.26) (0.28)

MORT -0.00354 -0.00379 -0.00150 -0.00123 -0.00231 (-0.09) (-0.09) (-0.04) (-0.03) (-0.06)

Yearslisted -0.000321 -0.000103 -0.000250 -0.000231 -0.000239 (-0.56) (-0.18) (-0.44) (-0.41) (-0.40)

Asset -0.00293 -0.00389 -0.00496 -0.00406 -0.00106 (-0.41) (-0.55) (-0.70) (-0.57) (-0.15)

Constant 0.0136 0.0280 0.0436 0.0280 -0.0262 (0.09) (0.19) (0.30) (0.19) (-0.17)

Number of Obs 909 909 909 909 909 Adjusted R2 0.0310 0.0401 0.0341 0.0345 0.0366 F stat 5.333 5.090 4.893 5.169 5.298

43

Table 6 Investor sentiment and SEO discounting

This table presents the result of testing the effects of investor sentiment on SEO discounting. The dependent variable is discounting, which is the percentage change in the price between the offer price and the closing price of the day prior SEO issuance. ICSR, CBINDR and BCR are the investor sentiment measures from the Index of the Index of Consumer Sentiment from Thomson Reuters/University of Michigan, the Index of Consumer Confidence from the Conference Board, the Index of Buying Condition from Thomson Reuters/University of Michigan, all orthogonalized on macroeconomic variables. HMIR is the supplier sentiment of real estate market measure from NAHB/Wells Fargo Housing Market Index of the National Association of Home Builders, orthogonalized on macroeconomic variables. Rpremia is the firm risk premium in the prior observation month. MK2BK is the market-to-book ratio in the prior observation month. Byield is the short-term government bond yield prior observation month. Asset is total asset. Clev is change in leverage ratio prior observation month. Lev is leverage ratio prior observation month. Accac is accumulative acquisition in observation year.

SeqREIT is the current SEO sequence regarding the REIT itself. Dura is number of days since last available financial results. EQUI equals to one if the firm is an equity REIT, zero otherwise. MORT equals to one if the firm is a mortgage REIT, zero otherwise. Size is the relative SEO shares offering size scaled by market capitalization. Urfee is the underwriting fee. Uranking is the underwriters’ reputation. Yearslisted is the number of years between the observation year and the IPO year. Year is the observation year. Crisis equals to one if date is between Jan 2007 and December 2009, zero otherwise. NASDAQ equals to one if the firm is listed on NASDAQ, zero otherwise.*, ** and *** represents the 10%, 5% and 1% significance level respectively. T-statistics are included in parentheses.

Variables Model1 Model2 Model3 Model4 Model5

ICSR 0.000622** (2.51)

CBINDR 0.000768*** (5.61)

BCR 0.000729*** (6.99)

HMIR -0.000485*** (-2.61)

Rpremia -0.000568* -0.000630** -0.000655** -0.000618** -0.000601** (-1.84) (-2.09) (-2.16) (-2.01) (-1.98)

Infoasy 0.0808 0.0831* 0.0770 0.0937* 0.0855* (1.62) (1.67) (1.59) (1.93) (1.72)

Growth -0.000222 -0.000191 -0.0000651 -0.00000306 -0.000177 (-0.25) (-0.21) (-0.07) (-0.00) (-0.20)

Size 0.00937 -0.0635 0.0565 -0.131 0.0856 (0.01) (-0.08) (0.07) (-0.16) (0.10)

Uranking -0.00231 -0.00212 -0.00132 -0.00144 -0.00245 (-1.05) (-0.97) (-0.59) (-0.66) (-1.11)

Lev 0.00319 0.00335 0.00456 0.00580 0.00535 (0.18) (0.19) (0.26) (0.32) (0.29)

44

NASDAQ -0.00829* -0.00835* -0.00842* -0.00740 -0.00776* (-1.80) (-1.79) (-1.80) (-1.62) (-1.70)

Byield -3.228*** -2.630** -3.073*** -2.442** -4.305*** (-2.93) (-2.26) (-2.74) (-2.21) (-3.28)

SeqREIT -0.00141** -0.00141** -0.00137** -0.00171** -0.00139** (-2.08) (-2.09) (-2.06) (-2.57) (-2.11)

EQUI 0.000151 -0.00193 -0.00361 -0.00168 0.000786 (0.02) (-0.22) (-0.41) (-0.19) (0.09)

MORT -0.0144 -0.0146 -0.0137 -0.0127 -0.0149 (-1.30) (-1.30) (-1.23) (-1.16) (-1.37)

Yearslisted 0.000244 0.000287 0.000282 0.000284 0.000247 (0.77) (0.92) (0.91) (0.89) (0.77)

Asset 0.00739 0.00650 0.00558 0.00530 0.00767* (1.64) (1.48) (1.23) (1.19) (1.67)

Year 0.000889 0.00126* 0.00108 0.00167** 0.000350 (1.14) (1.78) (1.41) (2.19) (0.38)

Constant -1.869 -2.592* -2.223 -3.399** -0.795 (-1.26) (-1.93) (-1.52) (-2.33) (-0.45)

Number of Obs 994 994 994 994 994 Adjusted R2 0.0363 0.0390 0.0504 0.0514 0.0409 F stat 5.664 5.934 7.224 8.538 5.266

45

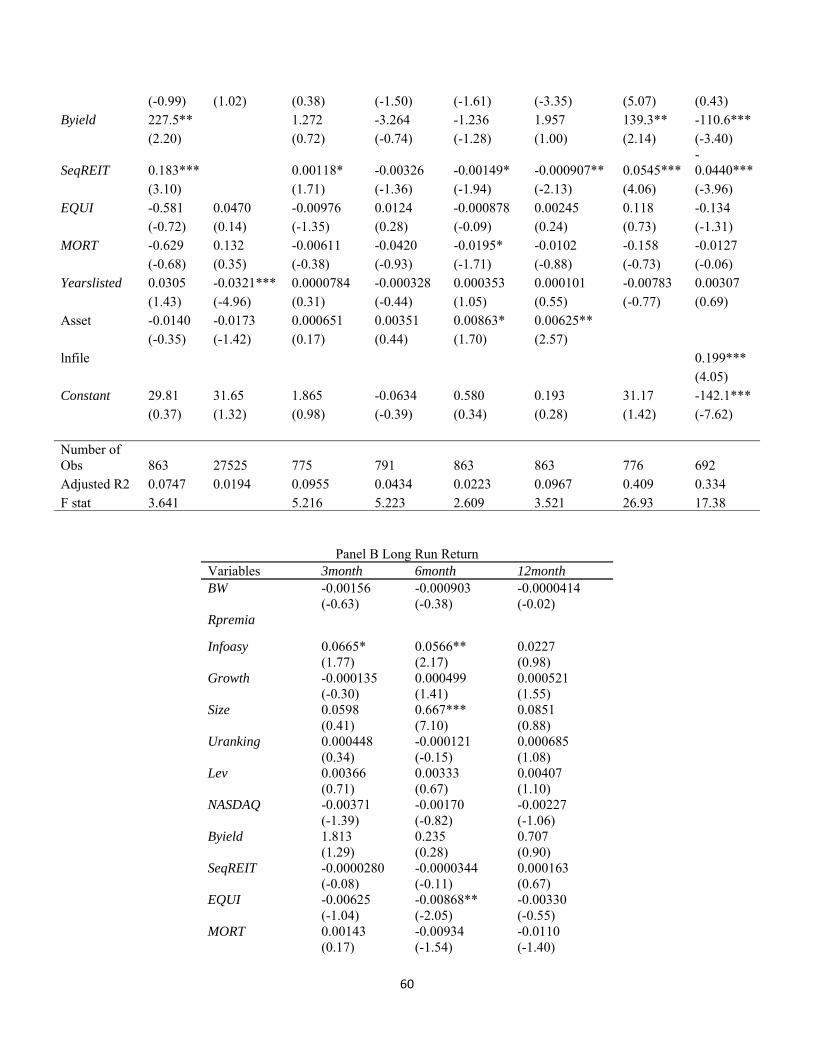

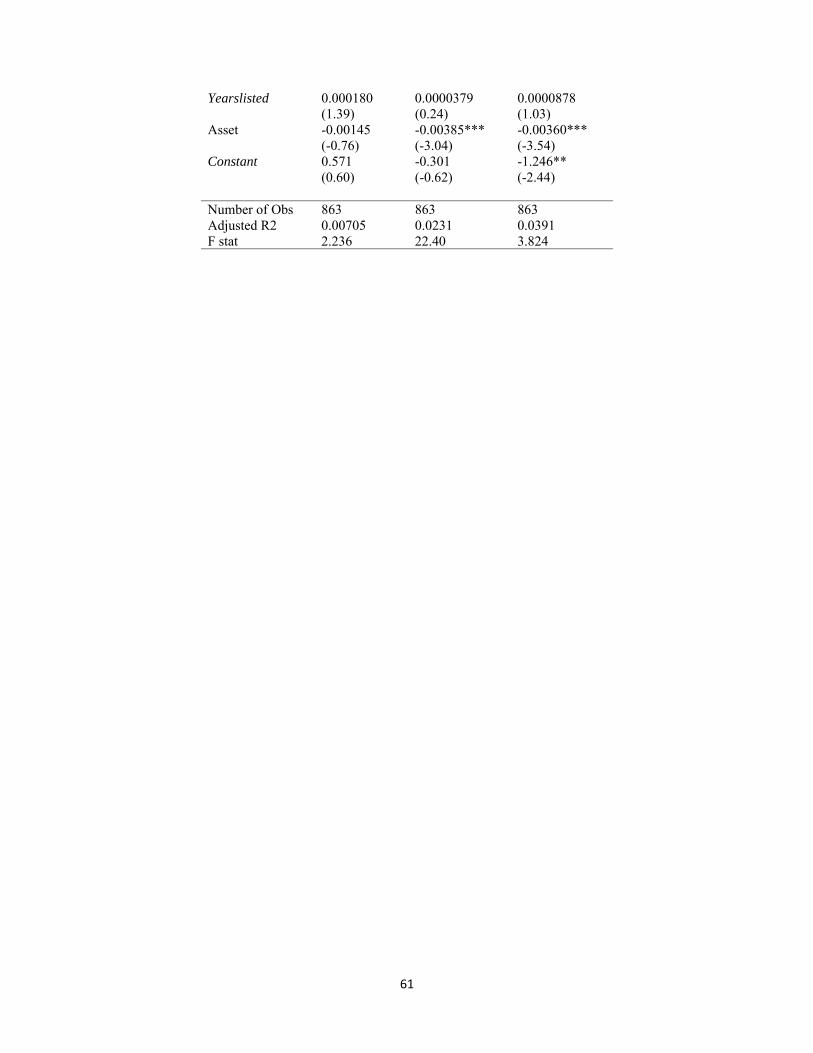

Table 7 Investor sentiment and SEO underpricing