INVESTOR PRESENTATION Q1:2019 - Saia Corporation · FORWARD LOOKING STATEMENT During this...

23

INVESTOR PRESENTATION Q1:2019

Transcript of INVESTOR PRESENTATION Q1:2019 - Saia Corporation · FORWARD LOOKING STATEMENT During this...

INVESTOR PRESENTATION Q1:2019

FORWARD LOOKING STATEMENT

During this presentation, some "forward-looking statements" within the meaning of

the Private Securities Litigation Reform Act of 1995, may be made. These "forward-

looking statements" and all other statements that may be made in this presentation

that are not historical facts are subject to a number of risks and uncertainties;

therefore, actual results may differ materially. Please refer to our recent SEC filings

for more information on the factors that could cause actual results to differ.

2

• Saia competes in the domestic less-than-truckload (LTL) market with estimated annual industry revenue of $40 billion

• In the LTL industry, the top 5, 10 and 25 carriers have approximately 50%, 75% and 90% total share of revenue respectively

OUR INDUSTRY

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

FEDEXFREIGHT

OLDDOMINION

XPOFREIGHT

UPSFREIGHT

YRCFREIGHT

ABFFREIGHT

ESTESEXPRESSLINE

YRCREGIONAL

R+LCARRIERS

SAIA

Top 10 LTL Carriers – Revenue* (M)

3

* Most recent annual reported revenue

OUR COMPANY

NON-UNIONEMPLOYEES

~10k ~18kTRACTORS, TRAILERS & FORKLIFTS

160TERMINALS

~5/7AVERAGE AGE OF TRACTORS/TRAILERS

SHIPMENTS DELIVERED DAILY

~29K

AND WE’RE STILL GROWING . . .

4

OUR CUSTOMERS

No single customer represents greater than 4% of sales5

SOURCE: CUSTOMER SATISFACTION

SURVEY, MASTIO & COMPANY, DEC 2015

PEOPLE

PROCESS

TOOLS99.1%+

INVOICEACCURACY

99.5%+CLAIMS-FREE

98%+ON-TIMEDELIVERY

99%+ON-TIMEPICKUP

98%+EXCEPTION-

FREE

CUSTOMER SATISFACTION

IS OUR #1 GOAL

WE OFFER A SUPERIOREXPERIENCE AS A TRUSTED CARRIER

CUSTOMER SERVICE INDICATORS

6

OUR SERVICE

• 40-state coverage

• Average LTL shipment weighs 1,322 pounds

• Average length of haul 837 miles

• ~75% of our shipments are delivered within 48 hours

• 2018 Cargo claims ratio of 0.79%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

2013 2014 2015 2016 2017 2018

Claims Ratio

7

• 40+ hours onboarding for dockworkers/drivers

• 20 days training for Customer Service

Representatives

• Dock-to-driver program

• Ongoing training meetings for all employees

• Actively recruiting top talent

• Safety recognition program

DEDICATED NON-UNION

WORK FORCE

RIGHT ROLESRIGHT

EQUIPMENTRIGHT

APPROACH

The industry’s first Chief Customer Officer

Logistics posts and trailer rails for locked-in stability

Proactive customer service

Customer Connectivity Specialists (EDI)

Arms-reach access to straps and airbags for secure bracing

Quality Matters More campaign, including documented load-closing process

Regional claims prevention managers

Leading-edge technology

60+ day onboarding / monitoring process for new customersALL

OPTIMIZED FOR THE BEST LTL SHIPPING

INVESTING IN & LEVERAGING OUR PEOPLE

8

AS REPORTED BY AN INDEPENDENT THIRD-PARTY SURVEY

1 Hire experienced drivers

2 300+ driver trainers on staff

3Annually certify all drivers in Smith System Defensive Driving

4 Weekly pre-shift safety meetings

5 100% of drivers are HazMat certified

6Tractors equipped with advanced collision avoidance technology

7 Bendix and Lytx – video training

8 Fleet Safety Gap Analysis

PEOPLE

PROCESS

TECHNOLOGY

OUR SAFETY CULTURE

9

IMPROVED RESULTS

• Pricing discipline has led to improved financial results

• Revenue – 7-year CAGR of 7%

• Operating Income – 7-year CAGR of 26%

$1

$21

$41

$61

$81

$101

$121

$141

$161

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2011 2012 2013 2014 2015 2016 2017 2018

Revenue vs Operating Income

Revenue (mil) Operating Income (mil)

10

• Average tractor age has improved to 5 years from 8 years

• Average trailer age has improved to 7 years from 12 years

• Fuel mileage benefit as well as lower emissions across the fleet

• Buying tractors with automatic transmissions to potentially attract new entrants to driver workforce

INVESTMENTS

11

$68$83

$122$112 $113

$152

$217

$252

$(10)

$40

$90

$140

$190

$240

$290

2011 2012 2013 2014 2015 2016 2017 2018

Equipment Properties Technology Maintenance Replacement Level

NORTHEAST EXPANSION

Opened 10 new terminals since May 2017 to serve new markets in the Northeast, with 4-6 additional terminal openings slated for 2019.

TST Partnership to serve Canadian customers

Annual LTL industry revenue in the northeastern US is approximately $8 billion of the total domestic LTL industry estimated at $40 billion

$6 billion

12

GEOGRAPHIC EXPANSION

1 Northeast market expansion was initiated in May 2017

2Saia has looked to supplement existing geographic footprint

3 Building 48 state coverage and density

4Northeastern presence to provide access to Canadian customers – TST Overland Express

5 Leverage infrastructure

6 Attain operating efficiencies “less fringe in network”

7 Supports Yield initiatives

13

4Q18 FINANCIAL RESULTS

• LTL Shipments per workday decreased 0.2%

• LTL Tonnage per workday decreased 0.6%

• LTL Yield increased 12.0%

• Record Revenue and Operating Income

4Q2018 4Q2017 Change

Revenue $407 $360 13%

Operating Income $33.3 $22.9 45%

Operating Ratio (%) 91.8 93.6 180 bps

Diluted Earnings Per Share $0.97 $1.82 NM

Net Debt / Capital (%) 14.8 18.0 NM

EBITDA* $60.2 $45.6 32%*non-GAAP Financial Metric reconcilliation included in Appendix

In $ U.S. millions except per share amounts and %

14

2018 FINANCIAL RESULTS

• LTL Shipments per workday increased 4.4%

• LTL Tonnage per workday increased 6.6%

• LTL Yield increased 10.2%

• Record Revenue and Operating Income

2018 2017 Change

Revenue $1,654 $1,405 18%

Operating Income $141.2 $94.7 49%

Operating Ratio (%) 91.5 93.3 180 bps

Diluted Earnings Per Share $3.99 $3.49 NM

Net Debt / Capital (%) 14.8 18.0 NM

EBITDA* $243.3 $181.8 34%*non-GAAP Financial Metric reconcilliation included in Appendix

In $ U.S. millions except per share amounts and %

15

INVESTMENT SUMMARY

• Unique story in that we are a 90+ year old company, with above-market growth potential

• Investments in our network have us well positioned for volume growth and share gains

• Significant Revenue Growth Opportunities:

On-going yield improvement opportunities

Geographic expansion into additional U.S. markets and Canada

Market penetration opportunities in legacy geography

• Significant operating leverage as 100 basis points of operating margin improvement results in $0.47 per share in earnings

16

APPENDIX

Thank you for your continued interest in Saia!

For more information see our website www.saia.comor contact [email protected]

17

FINANCIAL POSITION

• Solid liquidity position

• Capacity to fund growth

(millions)Borrowings Liquidity

Cash $ - $ 2.2

Capitalized Leases 102.9 -

Senior Fixed Notes - -

Revolving Credit Facility 20.0 202.3

Total $ 122.9 $204.5

Revolving Credit Facility $250.0

Borrowings (20.0)

Letters of Credit Outstanding

(27.7)

Available on Facility $202.3

$157$148

$127$133

$143

$155

$121 $123

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

3/31/17 6/30/17 9/30/17 12/31/17 3/31/18 6/30/18 9/30/18 12/31/18

Total Debt

18

RECONCILIATION OF NON-GAAP MEASURES

In thousands, except per share amounts

2018 4Q TTM Net debt / total capital: 31-Dec-18Revenue from continuing operations $1,653,849 Total debt $122,859Increase in operating income resulting

from 1% operating ratio improvement $16,538 Less: Cash and cash equivalents $2,194

Marginal tax rate 25.00% Net debt $120,665Increase in net income resulting from 1%

operating ratio improvement $12,404

Shareholders' equity $695,864

Common shares outstanding - Diluted 26,289 Total capital $816,529Increase in earnings per share resulting

from 1% operating ratio improvement $0.47 Net debt / Total capital 14.8%

2018 4Q EBITDA

Income Before Income Taxes $31,698

Interest Expense $1,328

Depreciation and amortization $27,188

EBITDA $60,214

2018 EBITDA

Income Before Income Taxes $135,833

Interest Expense $5,418

Depreciation and amortization $102,153

EBITDA $243,404 19

2019 PLANNED CAPEX

20

($ in thousands) Count Cost

Tractors ~1000 114,000$

Trailers ~1700 61,000

Forklifts 9,000

Net Revenue Equipment 184,000

Properties 72,000

Technology Equipment 19,000

Net Capital Expenditures 275,000$

HISTORICAL TRENDS

Operating Income ($mil) EPS ($)

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2013 2014 2015 2016 2017 2018 -

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

2013 2014 2015 2016 2017* 2018

*Adjusted EPS – see slide 18 for Reconciliation of this Non-GAAP Measure

21

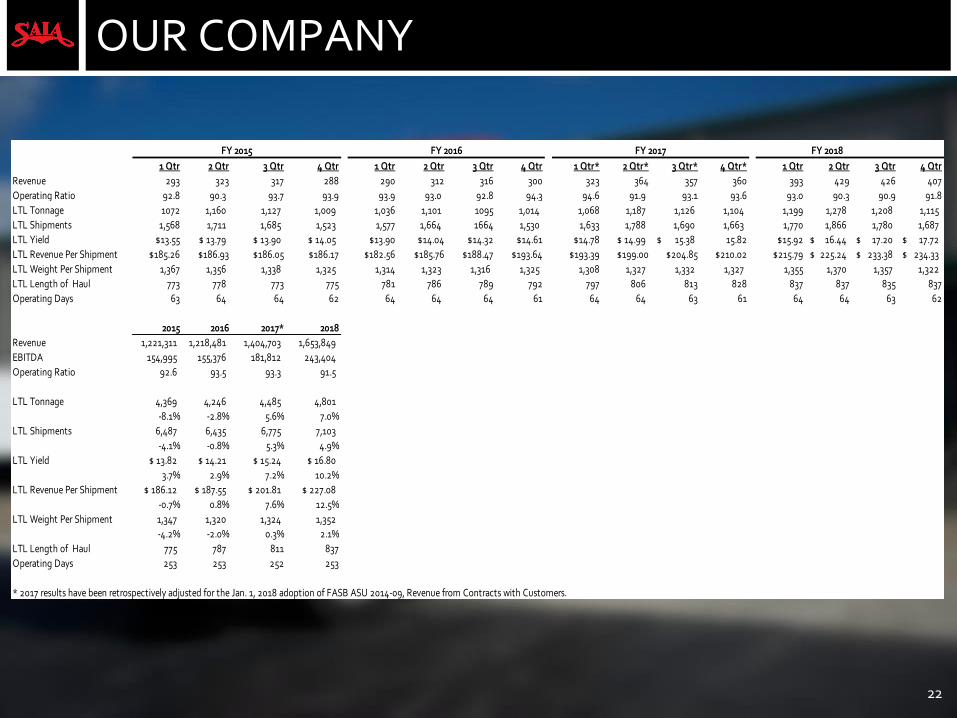

OUR COMPANY

FY 2015 FY 2016 FY 2017

1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr* 2 Qtr* 3 Qtr* 4 Qtr* 1 Qtr 2 Qtr 3 Qtr 4 Qtr

Revenue 293 323 317 288 290 312 316 300 323 364 357 360 393 429 426 407

Operating Ratio 92.8 90.3 93.7 93.9 93.9 93.0 92.8 94.3 94.6 91.9 93.1 93.6 93.0 90.3 90.9 91.8

LTL Tonnage 1072 1,160 1,127 1,009 1,036 1,101 1095 1,014 1,068 1,187 1,126 1,104 1,199 1,278 1,208 1,115

LTL Shipments 1,568 1,711 1,685 1,523 1,577 1,664 1664 1,530 1,633 1,788 1,690 1,663 1,770 1,866 1,780 1,687

LTL Yield $13.55 $ 13.79 $ 13.90 $ 14.05 $13.90 $14.04 $14.32 $14.61 $14.78 $ 14.99 15.38$ 15.82 $15.92 16.44$ 17.20$ 17.72$

LTL Revenue Per Shipment $185.26 $186.93 $186.05 $186.17 $182.56 $185.76 $188.47 $193.64 $193.39 $199.00 $204.85 $210.02 $215.79 225.24$ 233.38$ 234.33$

LTL Weight Per Shipment 1,367 1,356 1,338 1,325 1,314 1,323 1,316 1,325 1,308 1,327 1,332 1,327 1,355 1,370 1,357 1,322

LTL Length of Haul 773 778 773 775 781 786 789 792 797 806 813 828 837 837 835 837

Operating Days 63 64 64 62 64 64 64 61 64 64 63 61 64 64 63 62

2015 2016 2017* 2018

Revenue 1,221,311 1,218,481 1,404,703 1,653,849

EBITDA 154,995 155,376 181,812 243,404

Operating Ratio 92.6 93.5 93.3 91.5

LTL Tonnage 4,369 4,246 4,485 4,801

-8.1% -2.8% 5.6% 7.0%

LTL Shipments 6,487 6,435 6,775 7,103

-4.1% -0.8% 5.3% 4.9%

LTL Yield $ 13.82 $ 14.21 $ 15.24 $ 16.80

3.7% 2.9% 7.2% 10.2%

LTL Revenue Per Shipment $ 186.12 $ 187.55 $ 201.81 $ 227.08

-0.7% 0.8% 7.6% 12.5%

LTL Weight Per Shipment 1,347 1,320 1,324 1,352

-4.2% -2.0% 0.3% 2.1%

LTL Length of Haul 775 787 811 837

Operating Days 253 253 252 253

* 2017 results have been retrospectively adjusted for the Jan. 1, 2018 adoption of FASB ASU 2014-09, Revenue from Contracts with Customers.

FY 2018 FY 2019

22

MANAGEMENT OVERVIEW

Management Team

Saia

Tenure

Industry

Experience

Chief Executive Officer 22 33

President,Chief Operating Officer 5 10

EVP, Chief Customer Officer 21 30

EVP, Operations 42 42

V.P. Human Resources 5 17

23