INVESTOR PRESENTATION November 2015 - Grupa...

30

INVESTOR PRESENTATION November 2015

Transcript of INVESTOR PRESENTATION November 2015 - Grupa...

INVESTOR PRESENTATION

November 2015

2

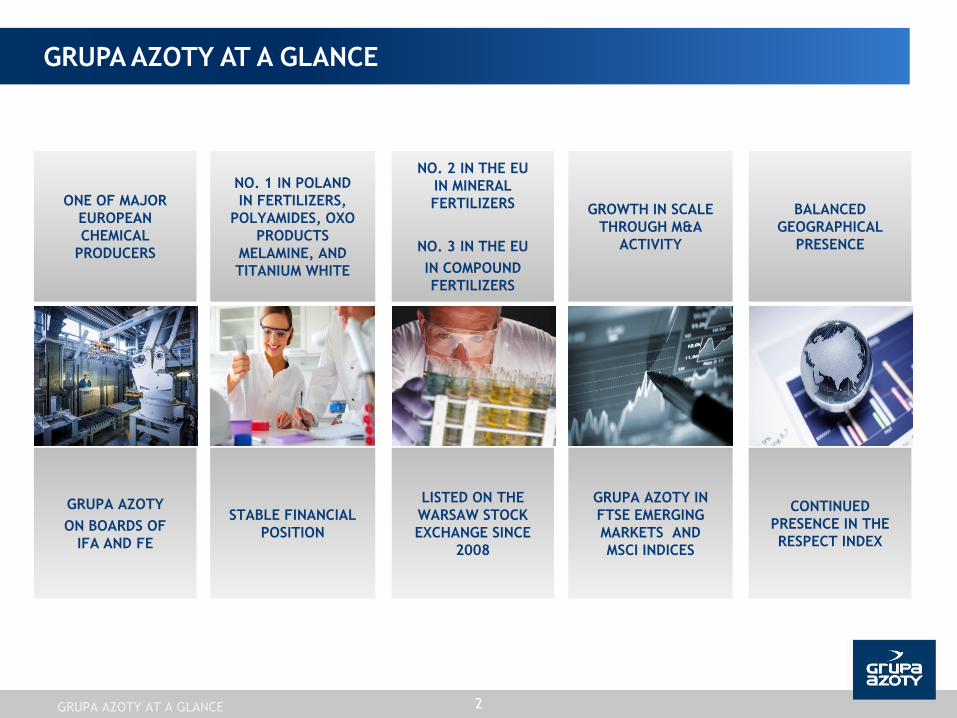

ONE OF MAJOR

EUROPEAN

CHEMICAL

PRODUCERS

NO. 1 IN POLAND

IN FERTILIZERS,

POLYAMIDES, OXO

PRODUCTS

MELAMINE, AND

TITANIUM WHITE

NO. 2 IN THE EU

IN MINERAL

FERTILIZERS

NO. 3 IN THE EU

IN COMPOUND

FERTILIZERS

GROWTH IN SCALE

THROUGH M&A

ACTIVITY

BALANCED

GEOGRAPHICAL

PRESENCE

GRUPA AZOTY

ON BOARDS OF

IFA AND FE

STABLE FINANCIAL

POSITION

LISTED ON THE

WARSAW STOCK

EXCHANGE SINCE

2008

GRUPA AZOTY IN

FTSE EMERGING

MARKETS AND

MSCI INDICES

CONTINUED

PRESENCE IN THE

RESPECT INDEX

GRUPA AZOTY AT A GLANCE

GRUPA AZOTY AT A GLANCE

3

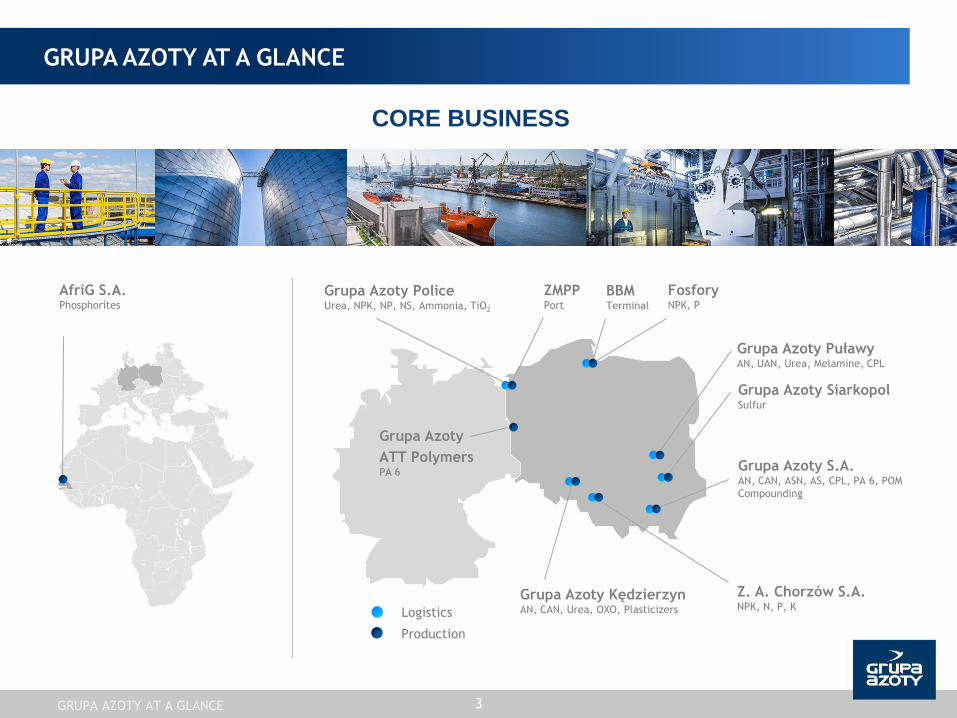

CORE BUSINESS

GRUPA AZOTY AT A GLANCE

Logistics

Production

ZMPP Port

Grupa Azoty Police Urea, NPK, NP, NS, Ammonia, TiO2

BBM Terminal

Fosfory NPK, P

Grupa Azoty

ATT Polymers PA 6

Grupa Azoty Puławy AN, UAN, Urea, Melamine, CPL

Grupa Azoty Siarkopol Sulfur

Grupa Azoty S.A. AN, CAN, ASN, AS, CPL, PA 6, POM

Compounding

AfriG S.A. Phosphorites

Grupa Azoty Kędzierzyn AN, CAN, Urea, OXO, Plasticizers

Z. A. Chorzów S.A. NPK, N, P, K

GRUPA AZOTY AT A GLANCE

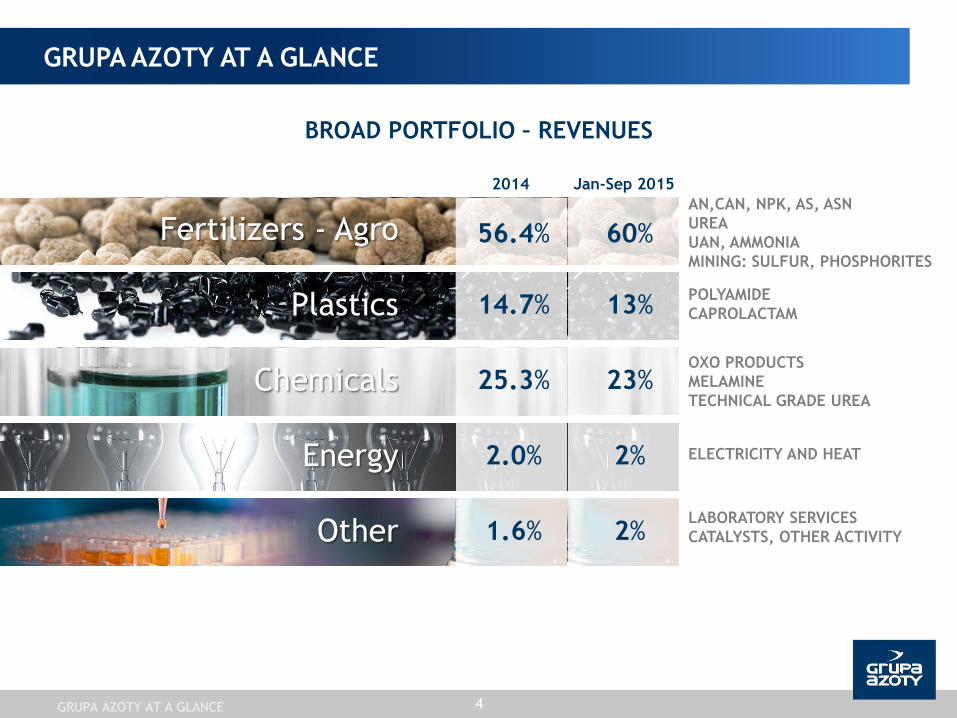

56.4% Fertilizers - Agro

4

BROAD PORTFOLIO – REVENUES

GRUPA AZOTY AT A GLANCE

AN,CAN, NPK, AS, ASN

UREA

UAN, AMMONIA

MINING: SULFUR, PHOSPHORITES

POLYAMIDE

CAPROLACTAM

OXO PRODUCTS

MELAMINE

TECHNICAL GRADE UREA

ELECTRICITY AND HEAT

LABORATORY SERVICES

CATALYSTS, OTHER ACTIVITY 1.6% Other

14.7% Plastics

25.3% Chemicals

2.0% Energy

GRUPA AZOTY AT A GLANCE

2014 Jan-Sep 2015

60%

13%

23%

2%

2%

90% of revenue derived from sales to EU markets

5

Poland

54%

+2%

Jan-Sep 2014

Jan-Sep 2015

South America

4%

+0.1%

Africa

2%

+0.1%

European Union 1

34%

-1% Asia

5%

-0.1%

Other Europe

1%

-1%

North America

0.3%

+0.1%

1 Excluding Poland

5

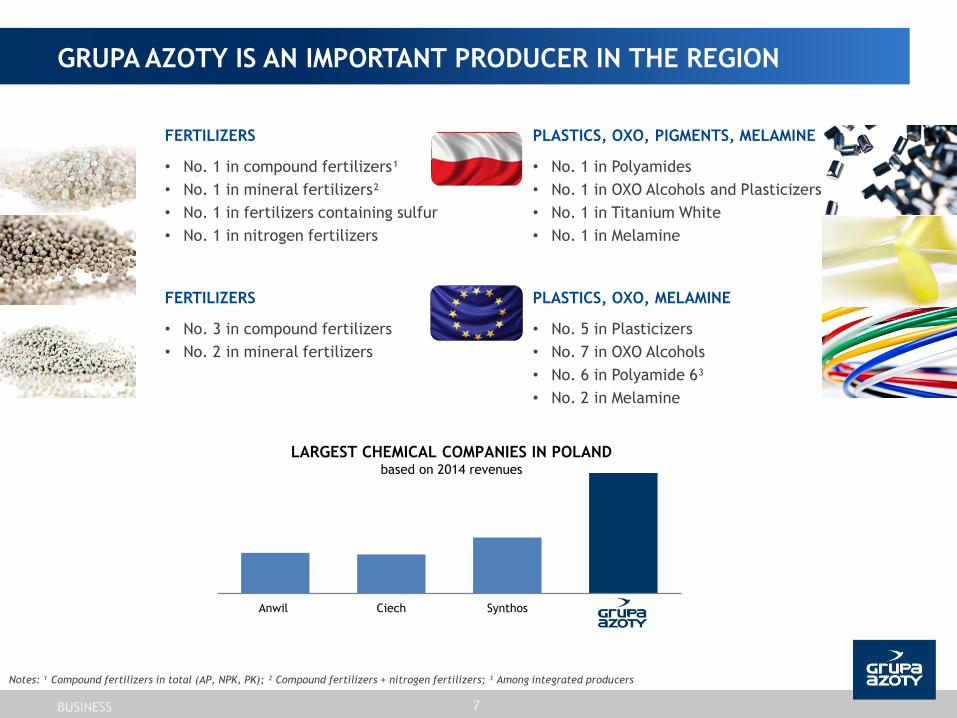

STRONG POSITION IN TARGET MARKETS

GRUPA AZOTY AT A GLANCE

BUSINESS

7

Notes: ¹ Compound fertilizers in total (AP, NPK, PK); ² Compound fertilizers + nitrogen fertilizers; ³ Among integrated producers

GRUPA AZOTY IS AN IMPORTANT PRODUCER IN THE REGION

Anwil Ciech Synthos

LARGEST CHEMICAL COMPANIES IN POLAND based on 2014 revenues

FERTILIZERS

• No. 1 in compound fertilizers¹

• No. 1 in mineral fertilizers²

• No. 1 in fertilizers containing sulfur

• No. 1 in nitrogen fertilizers

FERTILIZERS

• No. 3 in compound fertilizers

• No. 2 in mineral fertilizers

PLASTICS, OXO, PIGMENTS, MELAMINE

• No. 1 in Polyamides

• No. 1 in OXO Alcohols and Plasticizers

• No. 1 in Titanium White

• No. 1 in Melamine

PLASTICS, OXO, MELAMINE

• No. 5 in Plasticizers

• No. 7 in OXO Alcohols

• No. 6 in Polyamide 6³

• No. 2 in Melamine

BUSINESS

15

17

19

21

23

25

27

29

31

EUR/MWh

PGNiG tariff Average natural gas price paid by the Group TTF DA*

GAS PRICES (EUR/MWh)

NATURAL GAS DEMAND

(BCM)

2015 Q3 2015

2.1 0.4

FROM OUTSIDE THE SYSTEM

Q3 2014 Q3 2015

60% 47%

8

PGNIG'S NEW PRICING POLICY

The PGNiG Tariff sets a maximum gas price

The new discount scheme is linked to quoted

market prices of gas

Increased pricing differentiation, with prices

depending on the volumes and stability of gas

consumption over a gas year, reduces

diversification of gas sources

Source: ICIS.

* Day Ahead prices at Title Transfer Facility, a virtual trading point for natural gas in the Netherlands, no transfer costs.

GAS DIVERSIFICATION

BUSINESS

0 4 000 8 000 12 000 16 000 20 000

Azomures S.A.

Timac Agro (Groupe Roullier)

Achema JSC

Eurochem

Fertiberia

Borealis

Agrofert

Interagro*

(GK) Grupa Azoty

YARA

9

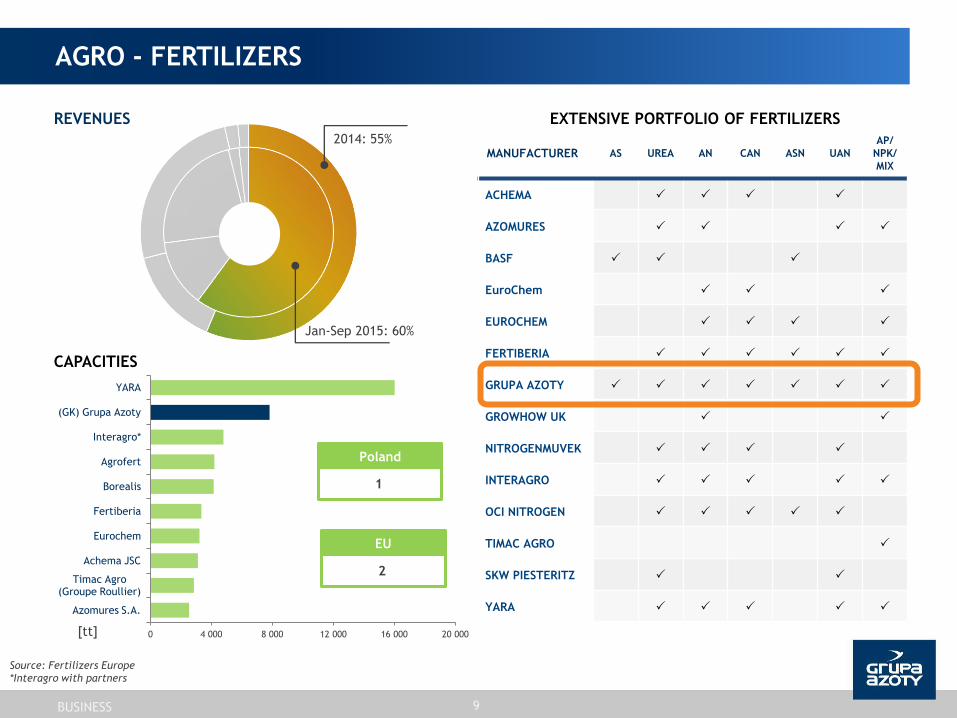

AGRO - FERTILIZERS

MANUFACTURER AS UREA AN CAN ASN UAN

AP/

NPK/

MIX

ACHEMA

AZOMURES

BASF

EuroChem

EUROCHEM

FERTIBERIA

GRUPA AZOTY

GROWHOW UK

NITROGENMUVEK

INTERAGRO

OCI NITROGEN

TIMAC AGRO

SKW PIESTERITZ

YARA

EXTENSIVE PORTFOLIO OF FERTILIZERS REVENUES

[tt]

CAPACITIES

EU

2

Poland

1

2014: 55%

Jan-Sep 2015: 60%

Source: Fertilizers Europe

*Interagro with partners

BUSINESS

10

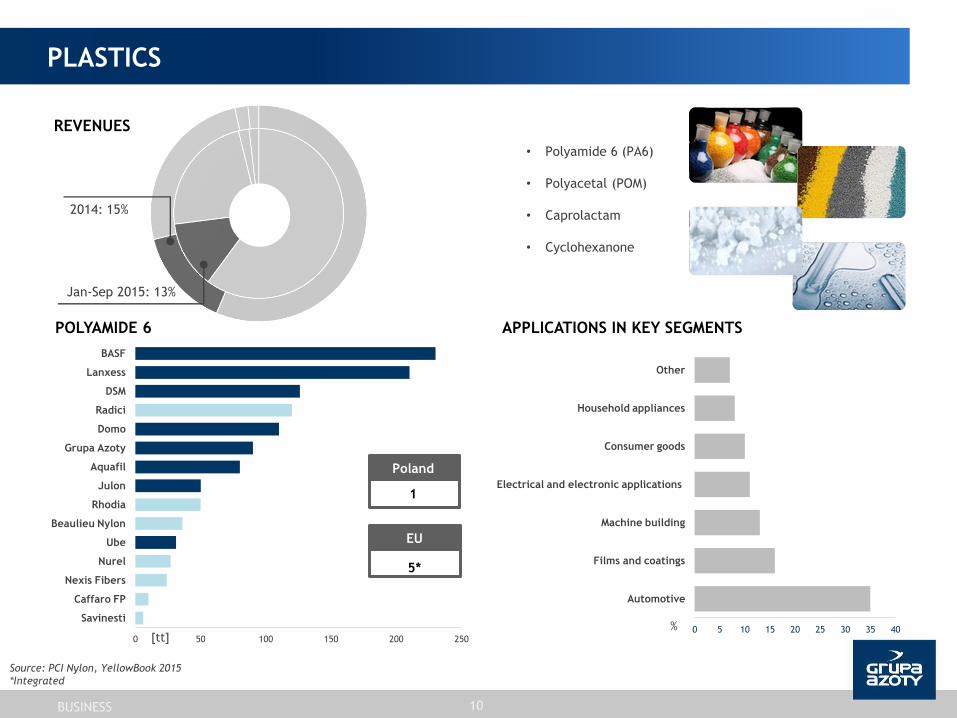

PLASTICS

REVENUES

Source: PCI Nylon, YellowBook 2015

*Integrated

[tt]

POLYAMIDE 6

Poland

1

EU

5*

APPLICATIONS IN KEY SEGMENTS

0 5 10 15 20 25 30 35 40

Automotive

Films and coatings

Machine building

Electrical and electronic applications

Consumer goods

Household appliances

Other

%

Jan-Sep 2015: 13%

2014: 15%

• Polyamide 6 (PA6)

• Polyacetal (POM)

• Caprolactam

• Cyclohexanone

BUSINESS

0 50 100 150 200 250

Savinesti

Caffaro FP

Nexis Fibers

Nurel

Ube

Beaulieu Nylon

Rhodia

Julon

Aquafil

Grupa Azoty

Domo

Radici

DSM

Lanxess

BASF

0 100 200 300 400 500

INEOS …

DEZA

Perstorp

Oltchim

OXEA

Grupa Azoty

Polynt

Evonik

BASF

Exxon Mobil

11

CHEMICALS

0 100 200 300 400 500

Oltchim

Grupa Azoty

Perstorp

Oxochimie (j.v. Arkema i INEOS)

OXEA

BASF

Melamine

0 20 40 60 80 100 120 140 160

Azomures S.A.

BASF SE

Grupa Azoty

Borealis Group

OCI Melamine

OXO** Plasticizers*

Poland

1

EU

3

Poland

1

EU

5

Poland

1

EU

5

REVENUES

2014: 25%

Jan-Sep 2015: 23%

[tt]

[tt]

[tt]

Source: Plasticizers Alkohols 2013 and Plasticizers (UE) 2013

* Production capacities for phthalate plasticizers and terephthalate plasticizers

** Production capacities for 2-EH, N-butanol, isobutanol

BUSINESS

Oxochimie (j.v. of Arkema

and INEOS)

12

Natural Gas Oxygen Nitrogen

Methanol

Phenol

Benzene Sulfur

Ammonia

Nitric Acid

AS

CAN

ASN

Ammonium

Sulfate

Mixed Acid

Caprolactam

PA 6

POM

Trioxane

Compounded

Polymers

C-none

Oleum

Dolomite Stone

Production of

Synthesis Gas

Formalin

Ilmenite Titanium Slag Titanium

White

Phosphorites

Potassium Salt

Phosphoric

Acid

NP

Fertilizers

NPK / PK

Fertilizers

Ortoxylene

Napthalene Maleic

Anhydride

Phtalic

Anhydride

Plasticizers

OXO

Alcohols

Urea Propylene

Aldehydes

Melamine

UAN

Sulfuric Acid

BUSINESS

RAW MATERIALS TO PRODUCTS - GRUPA AZOTY

STRATEGY

Grupa Azoty is a long-term investment

generating real profits – its share price has

moved up by more than 450% since the IPO

Continuous development through organic

growth, operational excellence and M&A

activities

We launch new and invest in existing product

lines to enhance their efficiency and improve

production quality

We constantly enhance our product mix We extend product chains, tailoring our

products to customer requirements

We actively diversify our sources of key raw

materials to increase security of supplies

14

WHY IS IT A GOOD IDEA TO INVEST IN GRUPA AZOTY?

STRATEGY

DIVIDEND POLICY

The Management Board will

recommend to the General Meeting

dividend distributions of 40%-60% of

the Company’s net profit.

Dividend

for the

year

Net profit

(PLN '000)

Dividend amount

(PLN '000)

Dividend

per share

Payout

ratio

2008 61,935 39,899 PLN 1.02 64%

2012 250,692 148,793 PLN 1.50 59%

2013 44,117 19,839 PLN 0.20 45%

The guiding principle behind Grupa Azoty’s dividend policy is to make

distributions proportionate to the Company’s earnings and financial

standing

Any decisions on dividend payment

will take account of a number of

factors concerning the Company and

the Grupa Azoty Group, including

business outlook, future profits, cash

requirements, financial standing,

growth plans, and legal

requirements.

15

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

STRATEGY

STRATEGY 16

REMITS OF THE GRUPA AZOTY MANAGEMENT BOARD MEMBERS

President of the Management

Board

P. Jarczewski

Vice-President of the Management

Board

A. Skolmowski

Vice-President of the Management

Board

W. Szczypiński

Vice-President of the Management

Board

K. Jałosiński

Vice-President of the Management

Board

M. Kapłucha

Vice-President of the Management

Board

M. Rybak

Member of the Management

Board

A. Kopeć

Corporate Affairs and HR

Finance Tarnów Police Supply Chain Puławy Social Dialogue

Audit, Risks and Compliance

Planning and Controlling Plastics

Feedstock Supply Integration and

Maritime Logistics

Investments Technical Safety

and Environmental Protection

Communication IT Organic Synthesis

Strategy and Development

Agro Business IR Production Integration

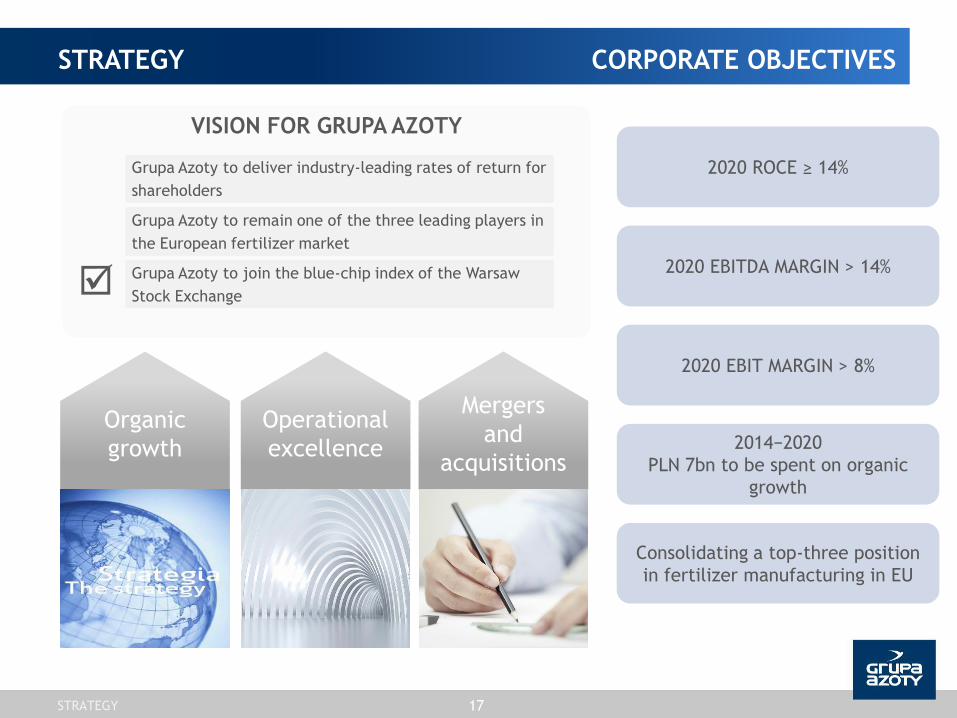

VISION FOR GRUPA AZOTY

Organic

growth

Operational

excellence

Mergers

and

acquisitions

Grupa Azoty to remain one of the three leading players in

the European fertilizer market

Grupa Azoty to deliver industry-leading rates of return for

shareholders

STRATEGY 17

Grupa Azoty to join the blue-chip index of the Warsaw

Stock Exchange

STRATEGY

2020 ROCE ≥ 14%

2014−2020

PLN 7bn to be spent on organic

growth

Consolidating a top-three position

in fertilizer manufacturing in EU

2020 EBIT MARGIN > 8%

2020 EBITDA MARGIN > 14%

CORPORATE OBJECTIVES

STRATEGY 18

32%

PLN 7bn

2014−2020

CORPORATE

PROJECTS

68 CAPEX PROJECTS

11% 19% 30% 4% 2% 2%

PLASTICS ENERGY FERTILIZERS OXOPLASTS MELAMINE PIGMENTS

ORGANIC GROWTH

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

PIPELINE OF STRATEGIC INVESTMENT PROJECTS

CHP Plant

PLN 600m (2019)

UAN production unit

PLN 29.5m (2015)

Polyamide plant

PLN 320m (2016)

Mineral fertilizer granulation plant

PLN 140m (2016)

Puławy Power Plant

PLN 1,125m (2019)

Extension of nitric acid unit

PLN 695m (2021)

Nitrate mechanical granulation plant

two lines – PLN 385m (line 1 by 2018, line 2 by 2020)

Propylene production plant

PLN 1.7bn (2019)

Upgrade of the ammonia unit

PLN 156m (by 2016)

Flue gas purification unit

and upgrade of the EC II CHP plant

PLN 164m (by 2016)

2014–2020 PLN 7bn 68 investment projects

19

GRUPA AZOTY POLICE

GRUPA AZOTY KĘDZIERZYN

GRUPA AZOTY PUŁAWY

GRUPA AZOTY S.A.

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

STRATEGY

STRATEGY 20

Commitment

building

programme

Periodic

evaluation

system

Objective-based

incentive

system

Flexible

working hours

Operational

control

Process

output − APC

Cost of

Quality

TOP 60

White Energy

Best

practices for

generation

and

transmission

Best

practices for

energy use in

production

processes

KPIs in

repair/

overhaul

contracts

TPM

Preventive

maintenance

Optimisation

of outbound

logistics

Best

procurement

practices

across

categories

PRODUKCJA ENERGY

INTENSITY

REPAIRS AND

OVERHAULS

PROCUREMENT

AND LOGISTICS

SUPPORT

FUNCTIONS

OPERATIONAL EXCELLENCE

Purpose of the

Azoty PRO

scheme:

PLN 300m plus

in annual

benefits after

completion of

the project

PRODUCTION

• 100% interest in ATT Polymers GmbH

• 53% interest in ZAK 2010

1.3 1.4 1.2 1.9

5.3

7.1

9.8 9.9

2007 2008 2009 2010 2011 2012 2013 2014

STRATEGY 21

MERGERS AND ACQUISITIONS

Consolidated revenues PLN bn

• controlling interest in ZA Puławy (up to 95.98%)

• 85% interest in Siarkopol

• 55% interest in AIG, Senegal (GA Police)

2013

• 10.4% interest in ZA Puławy in the first

tender offer

2012

2011 • 66% interest in ZCh Police

• 41% interest in ZAK

TARGET SELECTION PROCESS

Grupa Azoty

business tree

Start of analysis

1

ca. 2,000

entities

Long list of

potential targets

2

over 100 entities

Business segment

maps and matrices

3

over 50 entities

Short list of

potential targets

4

top 10 entities

Company profiles

5

ACQUISITIONS SINCE 2007

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

FINANCIAL HIGHLIGHTS

23

REPORTED FINANCIAL DATA

2013 2014 Jan-Sep 2014 Jan-Sep 2015

Revenues 9,821 9,898 7,342 7,521

EBIT 703 302 294 639

EBITDA 1,253 822 695 1 001

Net profit 714 265 250 540

Equity 6,271 6,488 6,488 6,998

Net debt 627 527 455 410

PLNm

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Grupa Azoty S.A. Grupa Azoty ZAK Group Grupa Azoty POLICE Group Grupa Azoty PUŁAWY Group Other

STRUCTURE OF THE GROUP'S CONSOLIDATED REVENUES IN 2014

FINANCIAL HIGHLIGHTS

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

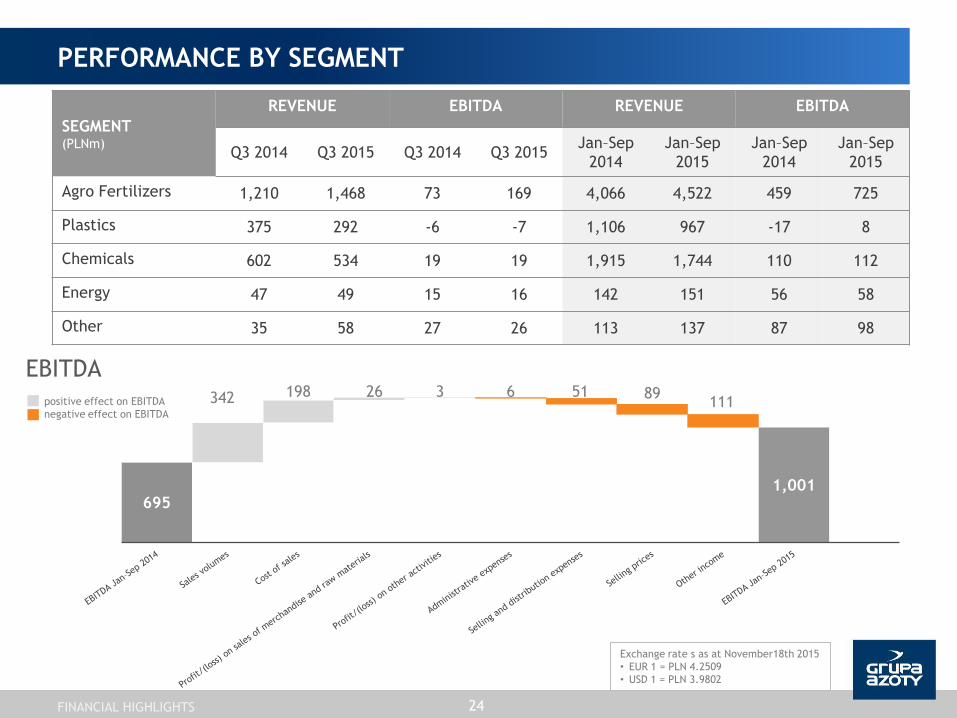

695 1,001

342 198 26 3 6 51 89 111

PERFORMANCE BY SEGMENT

24

EBITDA

FINANCIAL HIGHLIGHTS

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

SEGMENT (PLNm)

REVENUE EBITDA REVENUE EBITDA

Q3 2014 Q3 2015 Q3 2014 Q3 2015 Jan–Sep

2014

Jan–Sep

2015

Jan–Sep

2014

Jan–Sep

2015

Agro Fertilizers 1,210 1,468 73 169 4,066 4,522 459 725

Plastics 375 292 -6 -7 1,106 967 -17 8

Chemicals 602 534 19 19 1,915 1,744 110 112

Energy 47 49 15 16 142 151 56 58

Other 35 58 27 26 113 137 87 98

positive effect on EBITDA

negative effect on EBITDA

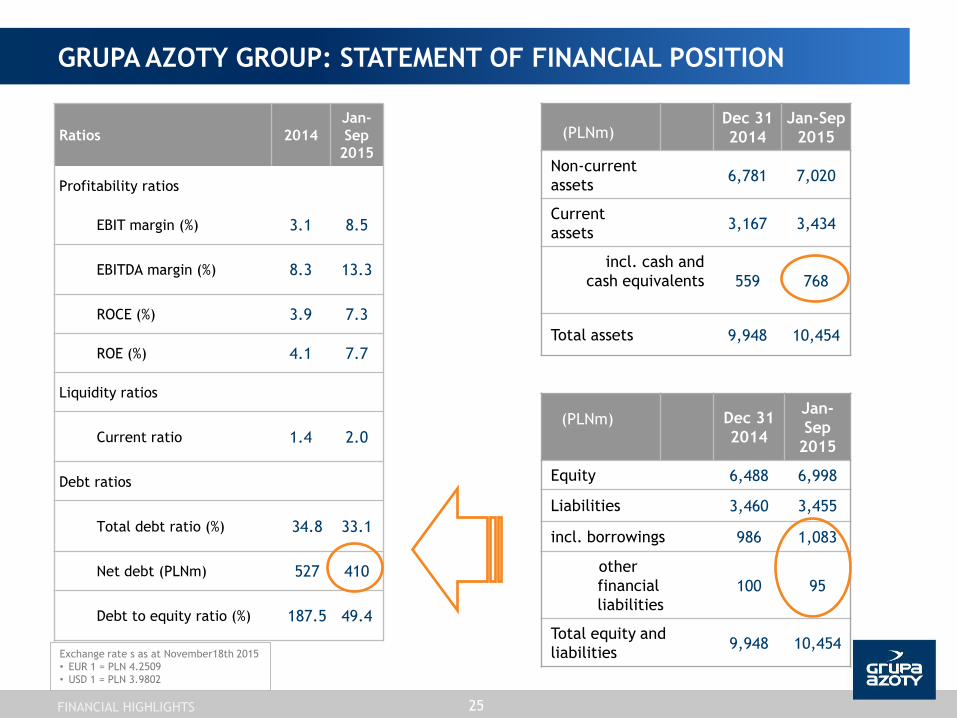

Ratios 2014

Jan-

Sep

2015

Profitability ratios

EBIT margin (%) 3.1 8.5

EBITDA margin (%) 8.3 13.3

ROCE (%) 3.9 7.3

ROE (%) 4.1 7.7

Liquidity ratios

Current ratio 1.4 2.0

Debt ratios

Total debt ratio (%) 34.8 33.1

Net debt (PLNm) 527 410

Debt to equity ratio (%) 187.5 49.4

Dec 31

2014

Jan-Sep

2015

Non-current

assets 6,781 7,020

Current

assets 3,167 3,434

incl. cash and

cash equivalents

559 768

Total assets 9,948 10,454

GRUPA AZOTY GROUP: STATEMENT OF FINANCIAL POSITION

Dec 31

2014

Jan-

Sep

2015

Equity 6,488 6,998

Liabilities 3,460 3,455

incl. borrowings 986 1,083

other

financial

liabilities

100 95

Total equity and

liabilities 9,948 10,454

(PLNm)

(PLNm)

25

FINANCIAL HIGHLIGHTS

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

26

COST STRUCTURE

Pro-forma data, including Grupa Azoty PUŁAWY and Grupa Azoty SIARKOPOL

RAW MATERIALS

0

2 000

4 000

6 000

8 000

10 000

12 000

2013* 2014 Raw material and consumables used Services

Labour costs Depreciation and amortisation

Other

-4%

40%

9% 4% 5%

5%

7%

7%

23%

Natural gas

Propylene

Phosphate

Potassium salt

Phenol

Coal

Electricity

Other

Lower costs of raw materials and consumables

attributable to lower prices of energy

resources and petroleum raw materials, as well

as procurement synergies

FINANCIAL HIGHLIGHTS

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

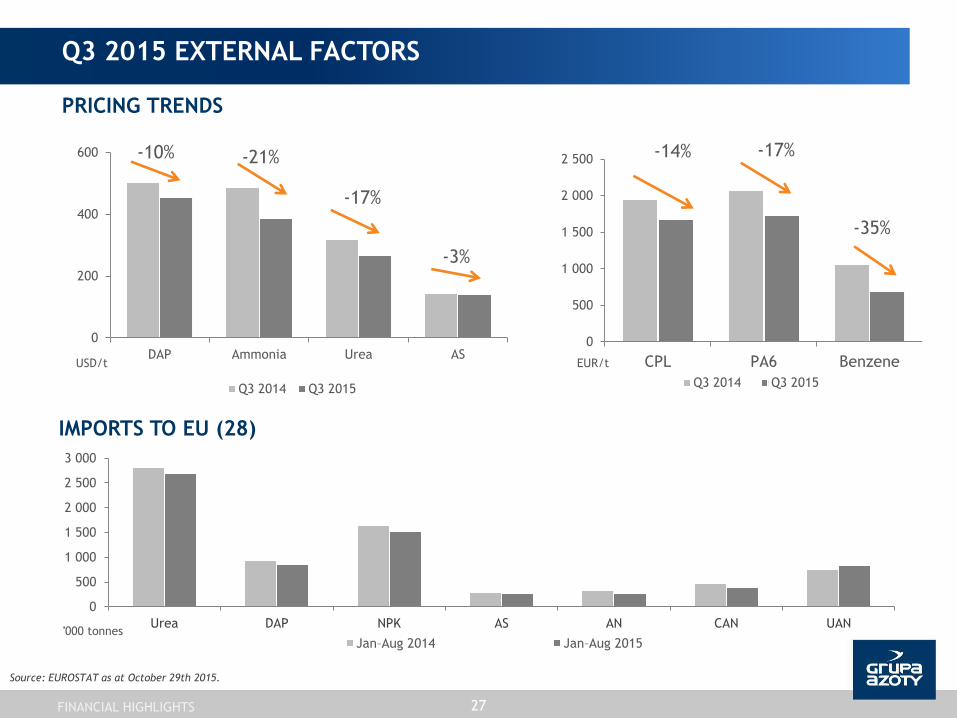

Q3 2015 EXTERNAL FACTORS

PRICING TRENDS

0

200

400

600

DAP Ammonia Urea AS USD/t

Q3 2014 Q3 2015

-10% -21%

-17%

-3%

0

500

1 000

1 500

2 000

2 500

CPL PA6 Benzene EUR/t

Q3 2014 Q3 2015

-14% -17%

-35%

Source: EUROSTAT as at October 29th 2015.

0

500

1 000

1 500

2 000

2 500

3 000

Urea DAP NPK AS AN CAN UAN '000 tonnes

Jan–Aug 2014 Jan–Aug 2015

IMPORTS TO EU (28)

27 FINANCIAL HIGHLIGHTS

-200

-100

0

100

200

300

400

500

600

700

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 2013

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Q1 2015

Q2 2015

Q3 2015

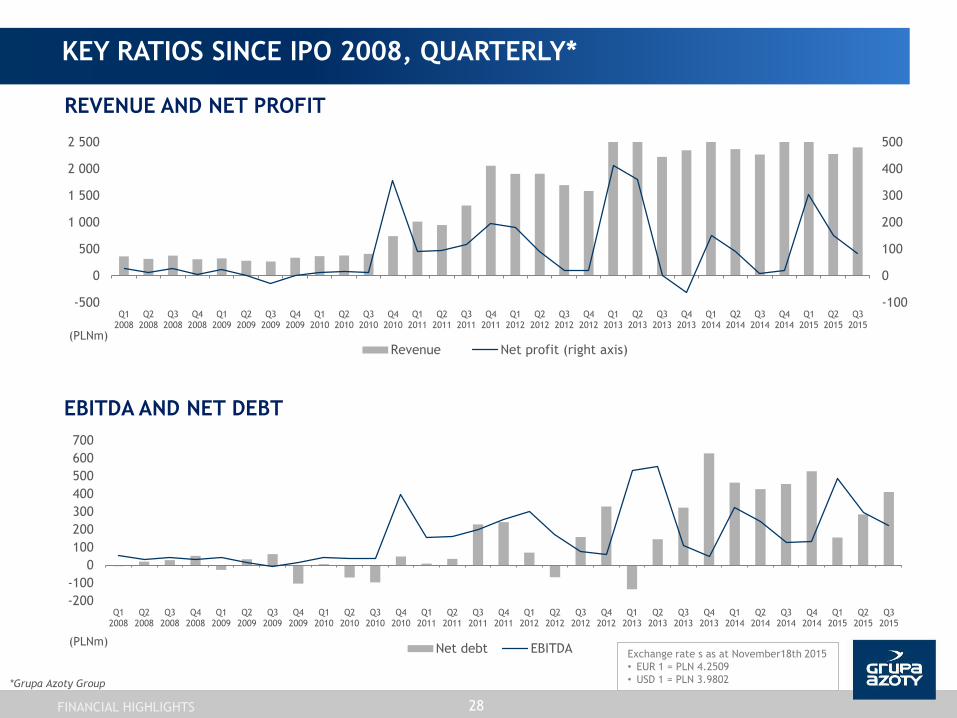

EBITDA AND NET DEBT

Net debt EBITDA

*Grupa Azoty Group

-100

0

100

200

300

400

500

-500

0

500

1 000

1 500

2 000

2 500

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 2013

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Q1 2015

Q2 2015

Q3 2015

REVENUE AND NET PROFIT

Revenue Net profit (right axis) (PLNm)

(PLNm)

28

KEY RATIOS SINCE IPO 2008, QUARTERLY*

FINANCIAL HIGHLIGHTS

Exchange rate s as at November18th 2015

• EUR 1 = PLN 4.2509

• USD 1 = PLN 3.9802

DISCLAIMER 29

DISCLAIMER

The information contained herein has been prepared by the Grupa Azoty Group (“the Group”) solely for the purpose of presentation to investors (“the

Presentation”). By participating in the meeting at which this Presentation is given or by referring to this Presentation you agree to the restrictions and

disclaimers presented below.

This Presentation does not constitute, or form any part of, and should not be considered as, an offer to sell or invitation to subscribe for, or as a guarantee

of purchase or other acquisition of any securities of any of the Group companies. Neither this presentation nor any part hereof may form the basis of, or be

relied upon in connection with, any subscription for or acquisition of any securities of the Group companies. Neither this Presentation nor any part hereof

may form the basis of, or be relied upon in connection with, any contract or commitment or investment decision relating to any securities of the Group

companies. This Presentation does not constitute a recommendation regarding any securities of the Group companies.

No statement or assurance, express or implied, has been made by or on behalf of the Group or any of its shareholders, members of its bodies, officers,

employees, agents or advisers or any other person as to the accuracy, completeness or reliability of the information or opinions contained in this

Presentation. The discussion of various subjects in this Presentation may include forward-looking statements. Forward-looking statements are different from

statements of historical fact. They can be identified by the use of such words as "expect", "intend", "plan", "believe", "anticipate", "will", "aim", "can",

"would", "could", "continue" or similar expressions. Forward-looking statements include statements about the financial performance, business strategy, plans

and objectives of the Group (including development plans relating to the Group). All forward-looking statements contained in this Presentation relate to

matters involving known and unknown risks, issues that are impossible to predict, and other factors. Actual results and achievements of the Group may

materially differ from those given in past declarations, and from the Company’s past performance and achievements. Forward-looking statements are made

based on various assumptions about future events, including assumptions regarding the current and future business strategies of the Group and its future

business environment. Although the Group believes that its estimates and assumptions are reasonable, they may prove to be incorrect. The information,

opinions and forward-looking statements contained herein are valid only on the date of this Presentation and are subject to change without notice. Unless

required by law, the Group and its advisors are not obliged to publish any updates or modify any information, data or statements contained in this

Presentation in the event of a change to the Group’s strategy or plans or the occurrence of any facts or circumstances that will have an effect on the

Group’s strategy or plans. Please note that the only reliable source of data on the Group's and Group companies’ financial performance, as well as

forecasts, events and indicators relating to the Group and the Group companies, are the current and periodic reports released by the Group companies to

comply with the applicable disclosure requirements under Polish law.

Neither the Group nor any of its shareholders, members of its bodies, officers, employees, agents or advisers nor any other person shall be liable for any

loss arising due to the use of this Presentation or its contents, or otherwise in connection with this Presentation.

Neither the Group nor any of its shareholders, members of its bodies, officers, employees, agents or advisers nor any other person is required to provide the

recipients of this Presentation with any additional information or to update this Presentation.

This Presentation contains information on the chemical industry in Poland and abroad, including information on the market share of the Company and some

of its competitors. In each case the source of such information is provided, and such information has not been subject to independent verification by or on

behalf of the Group.

This Presentation is not for distribution to or use by any person or entity in any jurisdiction where such distribution or use would be contrary to local law or

would oblige the Group or any of its affiliates to obtain an authorisation, license or exemption from the registration requirements under applicable laws.

Neither this Presentation nor any part hereof may be copied or transmitted into the United States, and cannot be disseminated, directly or indirectly in the

United States. Failure to comply with this restriction may constitute a violation of US securities laws. Persons who come into possession of this Presentation

should observe all the above limitations. Any securities referred to herein have not been and will not be registered under the US Securities Act of 1933. Any

such securities may not be offered or sold in the United States, except pursuant to an exemption or in a transaction not subject to the registration

requirements of the Act.

THANK YOU FOR YOUR ATTENTION For more information visit www.grupaazoty.com

Contact: [email protected]