Investor Presentation - Microsoft · Investor Presentation 23 •Tüpraş generated 29.8 million...

51

Investor Presentation January 2020

Transcript of Investor Presentation - Microsoft · Investor Presentation 23 •Tüpraş generated 29.8 million...

Hizmete Özel / Confidential

Investor Presentation

January 2020

Hizmete Özel / Confidential

This presentation contains forward-looking statements that reflect the Company management’s current views with respect to certain future events. Although it is believed that the expectations reflected in these statements are reasonable, they may be affected by variables and changes in

underlying assumptions that could cause actual results to differ materially.

Neither Tüpraş nor any of its directors, managers or employees nor any other person shall have any liability whatsoever for any loss arising from use of this presentation.

www.tupras.com.trJanuary 20Investor Presentation 2

Disclaimer

Disclaimer

Hizmete Özel / Confidential

Refining Market

Hizmete Özel / Confidential

Brent Crude Prices

www.tupras.com.trJanuary 20Investor Presentation 4Refining Market

$/bbl

+ OPEC and its allies increasing output cuts+ Impact of Iran & Venezuela sanctions+ Escalating regional tension

- Concerns on global economic development- China's purchases to slow as approaching long-term

reserve targets

2016 ave.43.7 $/bbl

2017 ave.54.3 $/bbl

2018 ave.71.0 $/bbl

2019 ave.64.3 $/bbl

All waivers expired on Iran

OPEC Production Cut Decision

Iran Sanctions

DroneAttack toSaudiFields30.7

81.2

67.0

20

26

32

38

44

50

56

62

68

74

80

86

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-16

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-17

Dec

-17

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Jun

-18

Jul-

18

Au

g-1

8

Sep

-18

Oct

-18

No

v-18

Dec

-18

Jan

-19

Feb

-19

Mar

-19

Ap

r-1

9

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-19

Dec

-19

Jan

-20

Hizmete Özel / Confidential

Refinery Capacity Changes

www.tupras.com.trJanuary 20Investor Presentation 5Refining Market

Expectations until 2024:

• ~80% of net capacity additions will come from Asia & Middle East

• Net capacity and demand in Europe will remain roughly unchanged

2.10

0.98

1.68

0.49

1.30

-0.95

0.22

-1.41

-2 -1 0 1 2 3

China

India

Middle East

Other Asia

Other

Japan

N. America

Europe

2012-2018 Net Capacity Additions by Region

2.0

0.9

1.71.3

0.9

0.2

1.97

0.89

1.93 1.96

1.50

0.51

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2019 2020 2021 2022 2023 2024

2019-2024 Net Capacity Additions

Asia & Middle East Other Total

Hizmete Özel / Confidential

Middle Distillate Cracks

www.tupras.com.trJanuary 20Investor Presentation 6Refining Market

14.9

16.2

15.0

12.2

12.9

11.4

14.1

16.216.6

17.9

13.9

11.3

13.7

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Diesel

5yr range 2019 2020 5 yr ave

14.4 13.8

13.2

10.3

10.9 11.2

14.8

16.4

17.0 17.4

12.5

9.3

12.0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Jet Fuel

5yr range 5 yr ave 2019 2020

5 yr between 2015-2019, data as of 6 Jan 2020

$/bbl

Hizmete Özel / Confidential

Gasoline and High Sulphur Fuel Oil Cracks

www.tupras.com.trJanuary 20Investor Presentation 7Refining Market

$/bbl

7.0

1.72.9

9.0

12.1

10.09.4

14.7

12.010.6

11.0

9.9

4.3

0

5

10

15

20

25

1 2 3 4 5 6 7 8 9 10 11 12

Gasoline

5yr range 2020 2019 5 yr ave

-26.6

-7.0

-5.0 -5.5

-8.6

-11.3-9.8

-6.9

-13.4-16.9

-22.5

-31.6

-32.9-35

0

1 2 3 4 5 6 7 8 9 10 11 12

High Sulphur Fuel Oil

5yr range 2020 2019 5 yr ave

5 yr between 2015-2019, data as of 6 Jan 2020

Hizmete Özel / Confidential

-12

-10

-8

-6

-4

-2

0

2Q

1 2

016

Q2

20

16

Q3

20

16

Q4

20

16

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

17

Q1

20

18

Q2

20

18

Q3

20

18

Q4

20

18

Q1

20

19

Q2

20

19

Q3

20

19

Q4

20

19

ArabHeavy

BasrahHeavy

Kirkuk

Kuwait

Ural

¹Average

Crude Price Differentials to Brent

www.tupras.com.trJanuary 20Investor Presentation 8Refining Market

¹Simple average of listed differentials

•Iran Sanctions

•Venezuela Sanctions

•OPEC+ Cut decision and over-compliance

•Druzhba contamination

•Drone attack to Saudi fields

Supply Shocks on Heavy Crude

A total of ~4 mbd is missing from heavy crude pool since December

2018, leading to price increases and narrowing differentials

Hizmete Özel / Confidential

Taking a Look at 2019…

www.tupras.com.trJanuary 20Investor Presentation 9Refining Market

January February March April May June July August September October November December

Weak Crack Margin Environment in 1HDiesel +5% Jet -9% Gasoline -36% HSFO -37% IMO Impact on Cracks

Elevated Concerns on Global Slowdown

Sanctions on Iran crude

OPEC Supply Cut <100% Compliance

Venezuela Crude Exports

Drone Attack to Aramco Oil Fields

Druzba Pipeline Contamination

OPEC Supply Cut >%120 Compliance

All waivers expired on Iran

IMO Impact on Differentials

Cra

cks

Dif

fere

nti

als

OPEC Supply Cut 100-120% Compliance

Hizmete Özel / Confidential

Turkish Market

Hizmete Özel / Confidential

Turkish Consumption 2015-2018

www.tupras.com.trJanuary 20Investor Presentation 11Turkish Market

Source: Tüpraş and EMRA ¹Bunker excluded

20.60

22.30

24.2023.60

2015 2016 2017 2018

DieselMillionTons

+8.5%

+8.5%

-2.4%

4.58

4.404.52

4.99

2015 2016 2017 2018

Jet Fuel

+10.4%

+2.7%-3.9%

2.10

2.23

2.302.34

2015 2016 2017 2018

Gasoline

+1.8%

+3.1%

+6.5%

0.6 0.58

0.49

0.39

2015 2016 2017 2018

Fuel Oil¹

-20.1%

-15.7%

-3.5%

Hizmete Özel / Confidential

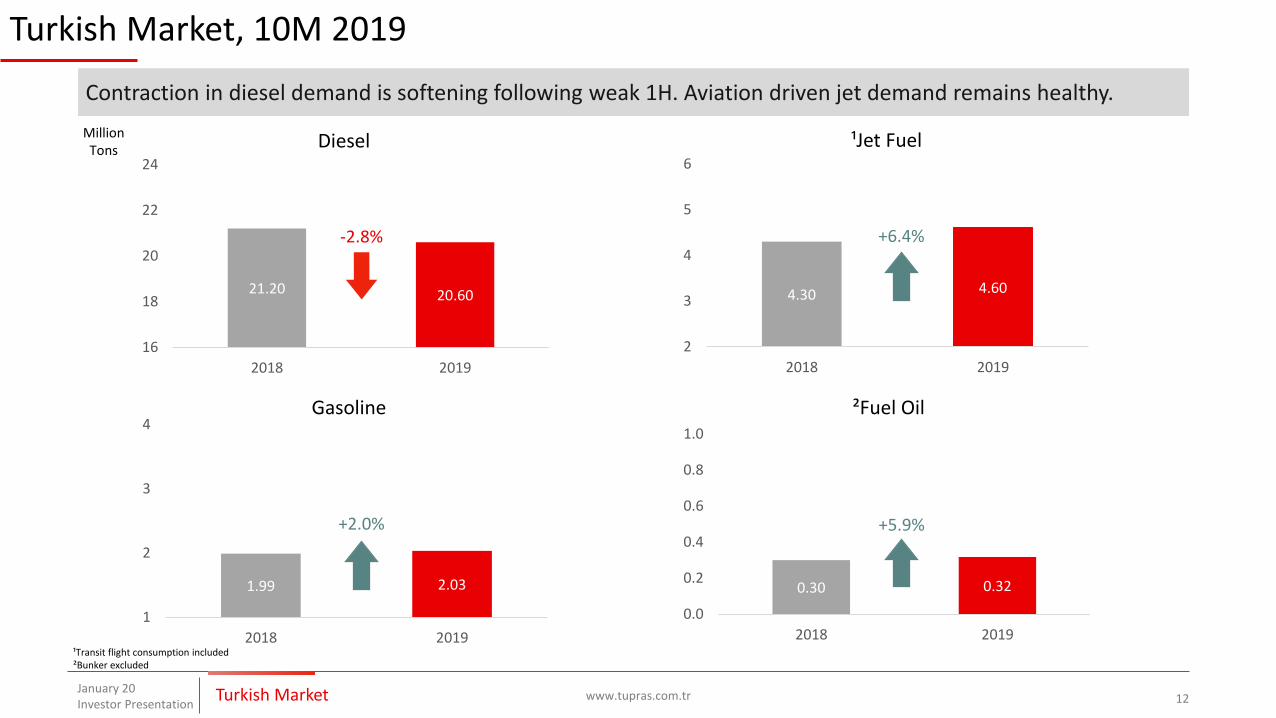

0.30 0.32

0.0

0.2

0.4

0.6

0.8

1.0

2018 2019

²Fuel Oil

1.99 2.03

1

2

3

4

2018 2019

Gasoline

4.30 4.60

2

3

4

5

6

2018 2019

¹Jet Fuel

21.20 20.60

16

18

20

22

24

2018 2019

Diesel

Turkish Market, 10M 2019

www.tupras.com.trJanuary 20Investor Presentation 12Turkish Market

MillionTons

Contraction in diesel demand is softening following weak 1H. Aviation driven jet demand remains healthy.

¹Transit flight consumption included²Bunker excluded

-2.8% +6.4%

+5.9%+2.0%

Hizmete Özel / Confidential

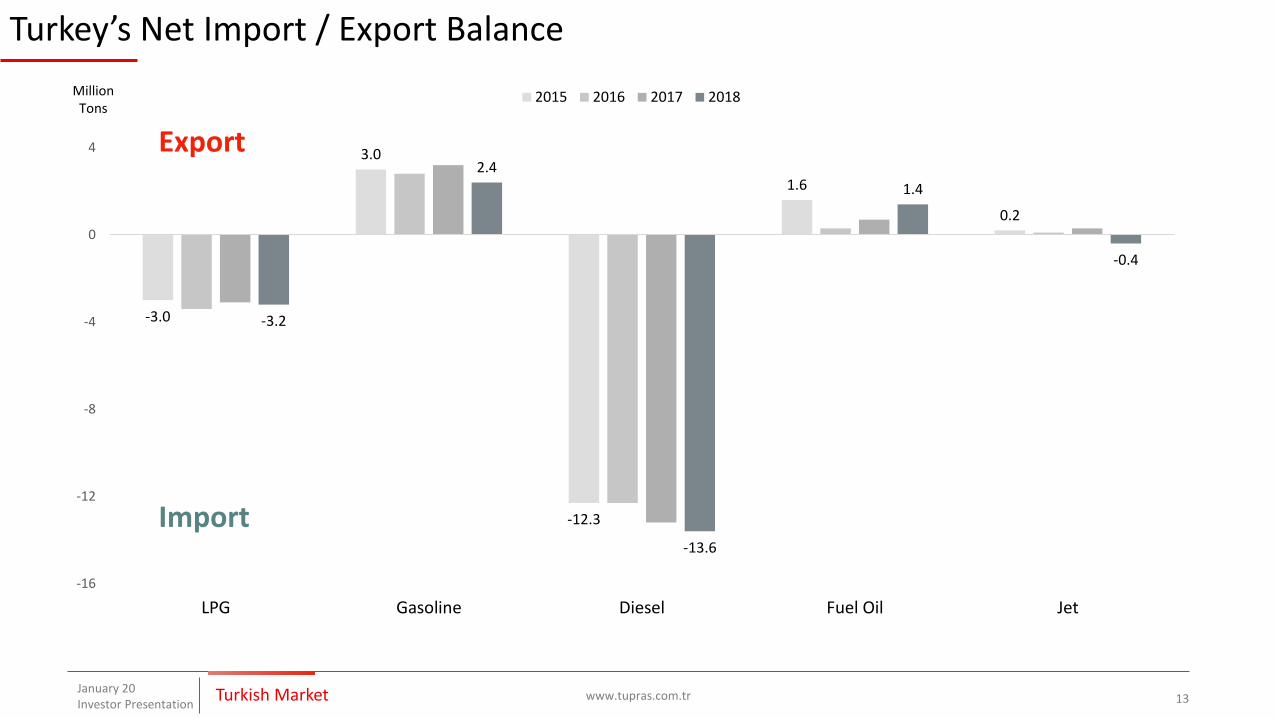

Turkey’s Net Import / Export Balance

www.tupras.com.trJanuary 20Investor Presentation 13Turkish Market

-3.0

3.0

-12.3

1.6

0.2

-3.2

2.4

-13.6

1.4

-0.4

-16

-12

-8

-4

0

4

LPG Gasoline Diesel Fuel Oil Jet

2015 2016 2017 2018

Export

Import

MillionTons

Hizmete Özel / Confidential

Company Overview

Hizmete Özel / Confidential

Domestic Ownership

17%

Foreign Ownership

83%

Tüpraş Shareholder Structure

www.tupras.com.trJanuary 20Investor Presentation 15Company Overview

¹As of September 30th,2019

Koç Holding77%

Aygaz20%

Opet3%

Ditaş79.98%

Opet40%

Körfez Ulaştırma100%

Publicly Traded

¹Distribution of Domestic-Foreign Ownership of Tüpraş

Shares

Free Float49%

Tüpraş is Turkey’s biggest industrial company and leading refiner.

Energy Investments Inc. (SPV)51%

Hizmete Özel / Confidential

Tüpraş’s Refining Assets & Distribution Network

www.tupras.com.trJanuary 20Investor Presentation 16Company Overview

İzmit

• 11.3 MT Capacity• NC: 14.5• Storage Capacity: 2.99 mn m3

İzmir

• 11.9 MT Capacity• NC: 7.66• Storage Capacity:2.51 mn m3

Kırıkkale

• 5.4 MT Capacity• NC: 6.32• Storage Capacity: 1.27 mn m3

Batman

• 1.4 MT Capacity• NC: 1.83• Storage Capacity:0.27 mn m3

Turkey‘s Storage Capacity

Tüpraş & Opet

57%

Others 43%

Railway

Iraq-Turkey Oil Pipeline

Baku-Tbilisi-Ceyhan Oil Pipeline

+ Tüpraş supplies ~60% of Turkey’s petroleum product needs

+ Tüpraş benefits from an integrated system optimization with its high complexity, procurement and logistics flexibility

Total Capacity

30 mntons

Nelson Complexity

9.5

Tüpraş Storage Cap.

7 mnm3

Hizmete Özel / Confidential

Nelson Complexity of Refining Companies

www.tupras.com.trJanuary 20Investor Presentation 17Company Overview

Hizmete Özel / Confidential

Tüpraş Subsidiaries

www.tupras.com.trJanuary 20Investor Presentation 18Company Overview

OPET, Distribution, Tüpraş Share: 40%

• 1,640 stations as of 30 September 2019• As of August 2019 Market share: 18.9% in white products; 31.7% in

black products

DİTAŞ, Marine Transport, Tüpraş Share: 79.98%

• 3 Crude Oil Tanker: 479,765 DWT• 1 Crude Oil - Product Tanker: 51,532 DWT• 9 Product Tanker: 155,478 DWT“

Körfez Ulaştırma, Railway Transport, Tüpraş Share: 100%

• ~7% share in Turkish rail freight market• ~1.4 mn ton of product and semi-product carried in 9M 2019.• Operates with 10 diesel locomotives and over 600 cistern wagons

Tüpraş Trading UK, Trading, Tüpraş Share: 100%

• Trading Office in London will be an important step into wider integration with the global energy landscape by allowing to:

Closely monitor international market opportunities Support import and export operations Create additional value from supply chain and sales activities

Hizmete Özel / Confidential

Operations

Hizmete Özel / Confidential

6 610

2 2 33 3 1 0

12 13 1310 10 10

2

17 1511

14 14

7

14

65 6763

7176

7981

2012 2013 2014 2015 2016 2017 2018

Africa America Europe CIS Middle East

Main Crude Suppliers in 2018

Crude Suppliers of Tüpraş

www.tupras.com.trJanuary 20Investor Presentation 20

In 2018, Tüpraş purchased 20 different types of crude from 12 countries with gravities ranging between 19-47 API.

Operations

Crude Oil Imports by Region (%)

Hizmete Özel / Confidential

LPG4%

Gasoline19%

Naphtha1%

Jet18%

Gasoil37%

Other2%

Kok3%

Fuel Oil7%

Asphalt9%

LPG Gasoline Naphtha Jet Gasoil

Other Kok Fuel Oil Asphalt

Light Distil.20%

Mid. Distil.55%

Other White 4%

Black Prod.20%

Q3 Product Yields

www.tupras.com.trJanuary 20Investor Presentation 21

LPG4%

Gasoline19%

Naphtha1%

Jet19%

Gasoil32%

Other2%

Kok3%

Fuel Oil7%

Asphalt13%

LPG Gasoline Naphtha Jet Gasoil

Other Kok Fuel Oil Asphalt

Light Distil.21%

Mid. Distil.51%

Other white4%

Black Prod.24%

2018 Q3

White Product Yield (%) 75.8%

Production 7.7 mn tons

API 30.7

2019 Q3

White Product Yield (%) 79.5%

Production 7.5 mn tons

API 31.49

Operations

Hizmete Özel / Confidential

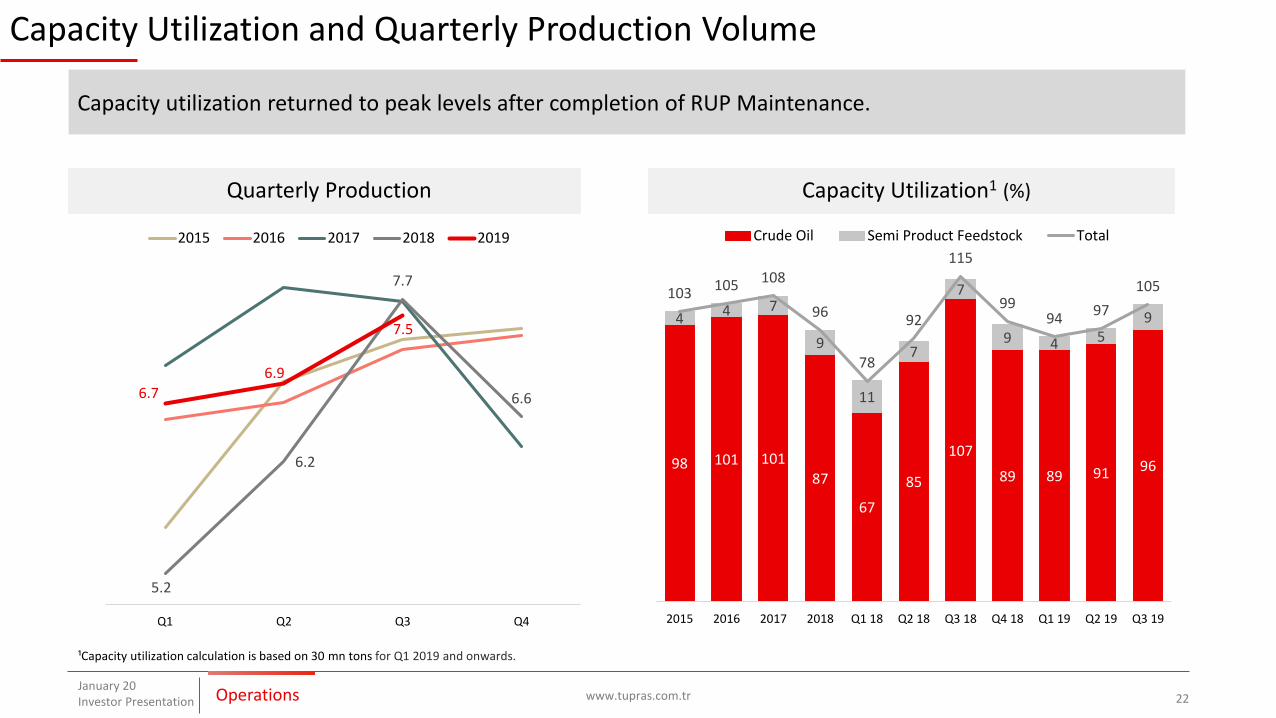

98 101 10187

67

85

107

89 89 91 96

4 4 7

9

11

7

7

9 4 59

103 105 108

96

78

92

115

9994

97

105

2015 2016 2017 2018 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19

Crude Oil Semi Product Feedstock Total

5.2

6.2

7.7

6.66.7

6.9

7.5

Q1 Q2 Q3 Q4

2015 2016 2017 2018 2019

Capacity Utilization1 (%)Quarterly Production

Capacity Utilization and Quarterly Production Volume

www.tupras.com.trJanuary 20Investor Presentation 22

¹Capacity utilization calculation is based on 30 mn tons for Q1 2019 and onwards.

Capacity utilization returned to peak levels after completion of RUP Maintenance.

Operations

Hizmete Özel / Confidential

Distributors, 50%

THY Opet, 10%

Jet, 6%

LPG, 3%

Other, 6% Export,

14%

Bitumen, 10%

Military, 1%

Sales

www.tupras.com.trJanuary 20Investor Presentation 23

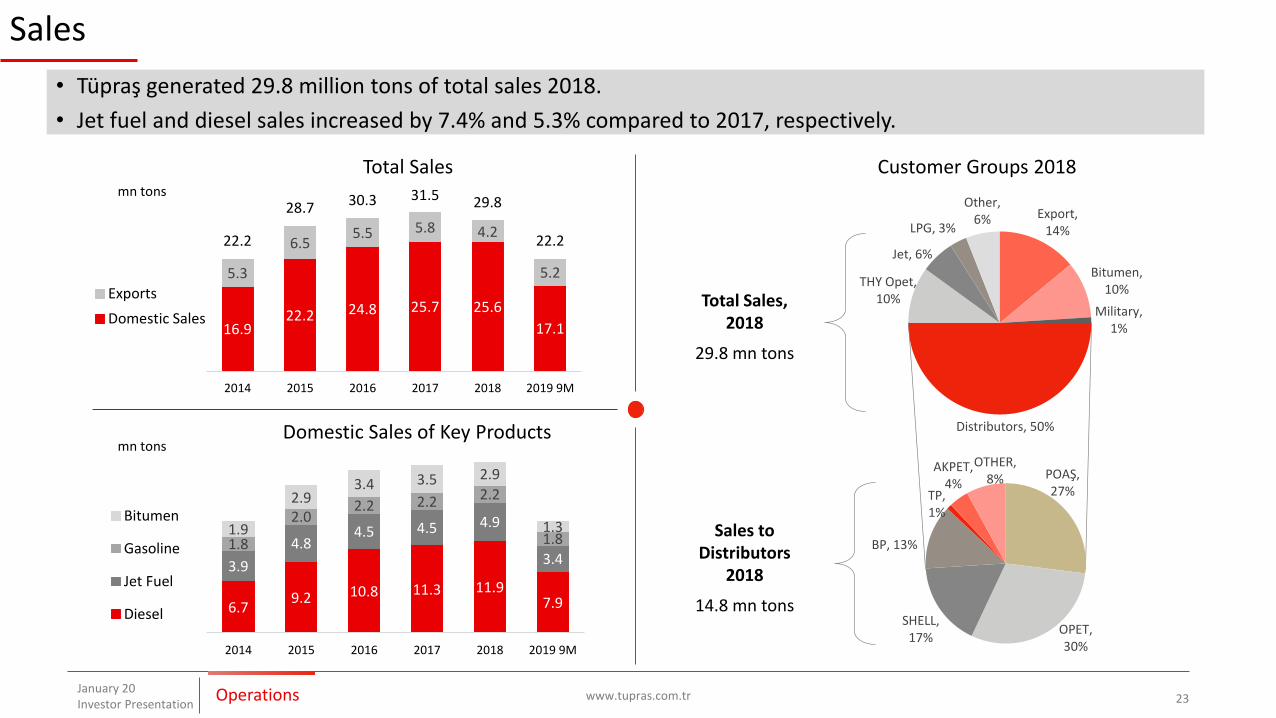

• Tüpraş generated 29.8 million tons of total sales 2018.

• Jet fuel and diesel sales increased by 7.4% and 5.3% compared to 2017, respectively.

16.922.2 24.8 25.7 25.6

17.1

5.3

6.55.5 5.8 4.2

5.2

22.2

28.7 30.3 31.5 29.8

22.2

2014 2015 2016 2017 2018 2019 9M

Exports

Domestic Sales

6.79.2 10.8 11.3 11.9

7.9

3.9

4.84.5 4.5 4.9

3.41.8

2.02.2 2.2 2.2

1.81.9

2.93.4 3.5 2.9

1.3

2014 2015 2016 2017 2018 2019 9M

Bitumen

Gasoline

Jet Fuel

Diesel

Total Sales

Domestic Sales of Key Products

Customer Groups 2018

POAŞ, 27%

OPET, 30%

SHELL, 17%

BP, 13%

TP, 1%

AKPET, 4%

OTHER, 8%

Operations

mn tons

mn tons

Sales to Distributors

2018

14.8 mn tons

Total Sales, 2018

29.8 mn tons

Hizmete Özel / Confidential

Key FinancialsFinancials

Hizmete Özel / Confidential

Margin Environment

www.tupras.com.trJanuary 20Investor Presentation 25

Tüpraş’ 3.7 $/bbl Net Refining Margin in 9M 2019 was higher than 2.9 $/bbl Med Complex margin.

2.53.2

6.56.0

8.1

9.3

3.7

1.71.9

4.84.0

5.34.6

2.9

2013 2014 2015 2016 2017 2018 9M 2019

Tüpraş Net Margin Mediterranean

Premium to the benchmark Mediterranean peers’ refining margin due to:

• Refined products deficit characteristic to the Turkish

market

• Access to cheaper sources of crude oil

• Ability to use heavier and sour crudes

• Close proximity to major suppliers reduces

transport costs

• Lower cost basis and more efficient energy usage

• Ability to produce higher value added range

of refined products

• Direct pipeline connections with domestic clients

• High export capability

5.5

2.02.9

1.2

4.2

1.7 2.0

4.84.0

5.44.6

2.9

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

Med Complex

Month Annual

Financials

$/bbl

$/bbl

Hizmete Özel / Confidential

Tüpraş and Med Margins

www.tupras.com.trJanuary 20Investor Presentation 26Financials

6.9

4.6

8.5

10.7

3.7

5.3

3.6

5.8

4.5

2.9

2015 2016 2017 2018 2019

9M Margins

Tüpraş Net Med Margin

($/bbl) Gross Margin Inventory Effect Clean Gross Margin Clean NET Margin Med Margin

2019 Q3 9.1 -1.4 10.6 5.4 3.3

2019 9M 9.0 -0.1 9.1 3.8 2.9

2018 Q3 17.6 3.1 14.5 10.4 5.1

2018 9M 16.0 2.5 13.6 8.3 4.5

$/b

bl

Hizmete Özel / Confidential

Income Statement

www.tupras.com.trJanuary 20Investor Presentation 27

Tüpraş recorded 956 mn TL EBITDA in Q3 2019.

*On CMB reports. EBIT includes extra items such as FX impacts of trade receivables and payables. In our EBITDA calculation. FX related items are excluded from EBIT as customary in international practices.

Million TLQ3 Q3

%9M 9M

%2019 2018 2019 2018

Net Sales 23,309 30,247 -23 67,970 63,749 7

COGS -22,152 -26,337 -16 -64,150 -56,549 13

Gross Profit 1,157 3,910 -70 3,820 7,200 -47

Operating Expenses -451 -324 39 -1,244 -870 43

Income/Loss from other operations -98 -2,783 -407 -3,771

Operating Profit 608 802 -24 2,169 2,559 -15

Income/Loss from equity investment 63 47 34 172 185 -7

Operating Profit Before Fin. Income/Loss 671 849 -21 2,341 2,743 -15

Financial Income /Expense -817 -171 -2,214 -668

Profit Before Tax -146 678 127 2,075

Net Profit (excluding minority interest) -155 542 340 1,947

EBITDA *(mn.TL) 956 3,778 -75 3,301 7,021 -53

Inventory Gain/Loss -692 1,667 283 2,950 -90

EBITDA* (mn. TL) CCS 1,648 2,111 -22 3,018 4,071 -26

Financials

Hizmete Özel / Confidential

Financial Highlights

www.tupras.com.trJanuary 20Investor Presentation 28

Tüpraş recorded 3,301 MTL EBITDA in 9M 2019.

367 3351,575 1,033 851

1,080 688

1,542 2,2101,4951,144

867

1,528

3,778

9561,2081,505

1,237

1,887

2015 2016 2017 2018 2019

EBITDAQ1 Q2 Q3 Q4

3,799 3,301

27579

869378

-375

710331

1,457

1,027870

750

581

992

542

-155

815

803

493

1,766

2015 2016 2017 2018 2019

¹Net Income

Q1 Q2 Q3 Q4

1.8 1.8

1.1

1.3

1.7

1.01.1 1.2

1.3

1.1

2015 2016 2017 2018 Sep. 2019

Current Ratio & Net Debt / R. EBITDA

Net Debt / R. EBITDA Current Ratio

35%

22%

41%37%

21%

2015 2016 2017 2018 Sep. 2019

²Return on Average Equity

1) Excluding minority interest 2) Calculation based on rolling net income

3,396

5,882

8,908

2,550

1,793

3,8123,713

340

Financials

Mn TL Mn TL

Hizmete Özel / Confidential

Balance Sheet Analysis

www.tupras.com.trJanuary 20Investor Presentation 29

Strong balance sheet maintained.

3.9

6.8

1.5 1.50.9

4.2

1 year 1-2 years 2-3 years 3-4 years 4-5 years Over 5 years

Redemption Schedule

Loan Eurobond TL bond Total

0.8

-0.2

2.1

4.7

1.6

-0.7

-2.3

Dec-15 Dec-16 Dec-17 Dec-18 Mar-19 Jun-19 Sep-19

Working Capital Requirement

6.96.1 6.2

12.010.6 10.1

8.7

Dec-15 Dec-16 Dec-17 Dec-18 Mar-19 Jun-19 Sep-19

Net Debt

Proactive Financial Management

• Delevering continues despite operational headwinds

• Dynamic liquidity management ensures optimal cash and receivables management

Billion TL Billion TL

Billion TL

Financials

Hizmete Özel / Confidential

Q3 Profit Before Tax Bridge (2018-2019)

www.tupras.com.trJanuary 20Investor Presentation 30

Decline in profit before tax was driven by narrow differentials and natural gas price hikes.

Million TL

FX

Inventory

+2,473

-2,384

Financials

Hizmete Özel / Confidential

Annual Profit Before Tax Bridge (2017-2018)

www.tupras.com.trJanuary 20Investor Presentation 31

2018 PBT was lower mainly due to Crude Oil Differential and Crack Margin impacts. With the help of FX based pricing, FX losses incurred from payables were recovered with Inventory Gains.

Million TL

Financials

Hizmete Özel / Confidential

Dividend (TL)

www.tupras.com.trJanuary 20Investor Presentation 32

3.2 2.9

5.05.8

4.85.8

10.2

7.2

15.2 14.8

2.5 3.03.9 3.9

1.6

6.5 6.2

13.615.2

77%

101%

79%

66%

33%

0%

64%

87%89%

102%

0%

40%

80%

120%

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Earnings per Share Gross Dividend Dividend Payout

Financials

Hizmete Özel / Confidential

Investments (Million $)

www.tupras.com.trJanuary 20Investor Presentation 33

274355

400

186 177

628

974

1213

959

344

213 185138 112

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 20199M

Ongoing Projects

• Revamp of Crude Units

• FCC Modernization

• New Sulphur Units

• Energy Saving Projects

• Optimization of conversion

units

• 6.5 bn USD investments since privatization

• Reached 9.5 Nelson Complexity

• Capability to process heavier and more sour crude

Avg. 278 Mn$

Avg. 943 Mn$

Avg. 220 Mn$

Financials

Hizmete Özel / Confidential

9M 2019 Results

www.tupras.com.trJanuary 20Investor Presentation 34

3.7

2.9

0 1 2 3 4 5 6

9M

Refining Margins ($/bbl)

Med Margin Tüpraş Net Margin

98.3% total capacity utilization in 9M 2019

21.2 22.228 30

Production Sales

Operationals9M 2019 Target

22.2 mn tons of sales and 21.2 m tons of production in 9M 2019

112150

9M 2019 Target

Capex (mn $)

112 mn$ refining CAPEX in 9M 2019

98.3

0 20 40 60 80 100

9M

Capacity Utilization (%)

3.7 $/bbl net refining margin in 9M 2019

Med FY Exp

Tüpraş FY Target

Financials

Hizmete Özel / Confidential

Tüpraş Balance Sheet (Million TL)

www.tupras.com.trJanuary 20Investor Presentation 35

30.09.2019 31.12.2018 Diff. Diff. (%)Current Assets 28,945 20,962 7,983 38

Cash & C. Equivalents 10,106 5,983 4,123 69Trade Receivables 6,063 5,429 635 12

Derivatives 350 176 174 99Inventories 9,489 6,765 2,724 40

Pre-paid expenses 231 109 122 113Other Current Assets 2,707 2,502 205 8

Long Term Assets 26,735 19,074 7,662 40Financial Assets & Subsidiaries 1,368 1,271 97 8

Fixed Assets 20,290 12,397 7,893 64Derivatives 122 168 -46 -28

Pre-paid expenses 349 378 -29 -8Deferred Tax 3,114 3,566 -452 -13

Other Long Term Assets 1,492 1,293 199 15

Total Assets 55,681 40,036 15,645 39Short Term Liabilities 27,358 15,950 11,408 72

Financial Loans 3,860 4,113 -253 -6Trade Payables 17,834 7,496 10,337 138

Derivatives 288 236 52 22Provisions 201 80 120 150

Other ST Liabilities 5,175 4,024 1,152 29Long Term Liabilities 15,323 14,140 4,237 8

Financial Loans 14,990 13,836 1,154 8Payables & Provisions 278 257 21 8

Derivatives 46 42 4 10Other LT Liabilities 8 5 4 84

Total equity attr. to equity holders of the parent 12,839 9,825 3,014 31Minority Interests 161 121 40 33

Total Liabilities & Equity 55,681 40,036 15,645 39

Financials

Hizmete Özel / Confidential

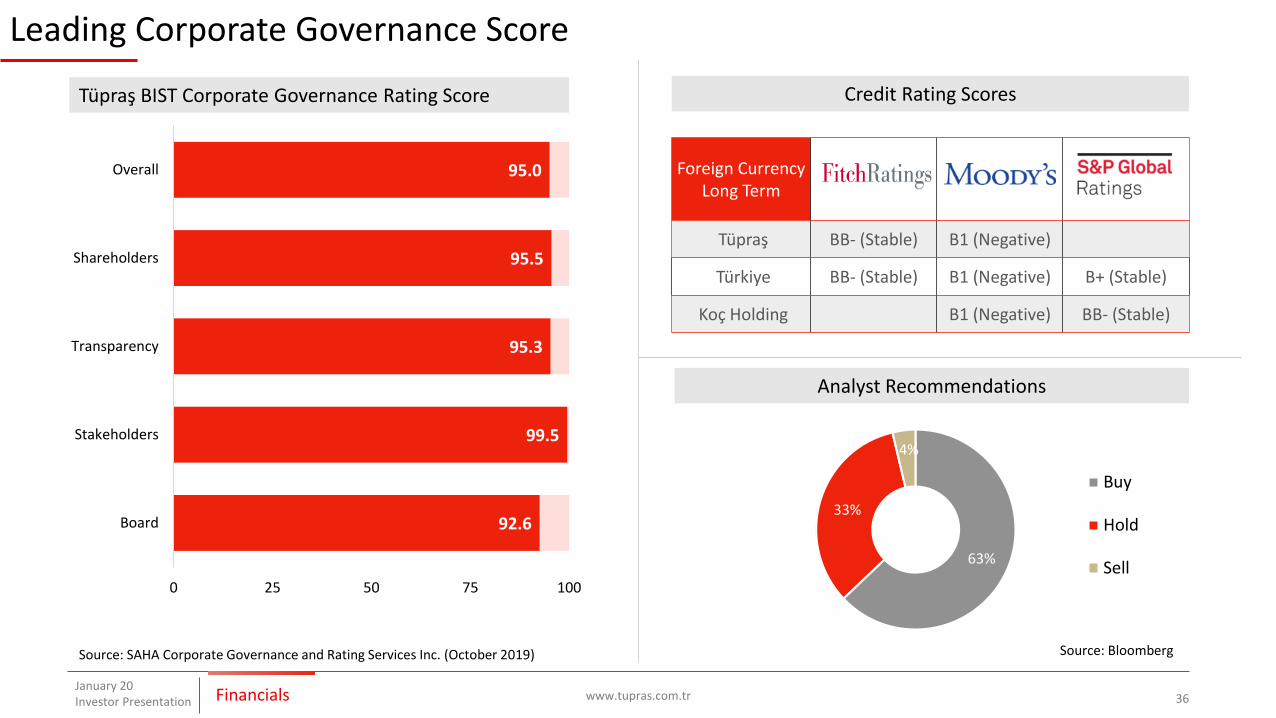

Foreign Currency Long Term

Tüpraş BB- (Stable) B1 (Negative)

Türkiye BB- (Stable) B1 (Negative) B+ (Stable)

Koç Holding B1 (Negative) BB- (Stable)

Leading Corporate Governance Score

www.tupras.com.trJanuary 20Investor Presentation 36

92.6

99.5

95.3

95.5

95.0

0 25 50 75 100

Board

Stakeholders

Transparency

Shareholders

Overall

Tüpraş BIST Corporate Governance Rating Score

Source: Bloomberg

63%

33%

4%

Buy

Hold

Sell

Analyst Recommendations

Credit Rating Scores

Source: SAHA Corporate Governance and Rating Services Inc. (October 2019)

Financials

Hizmete Özel / Confidential

Proactive in liquidity risk management & targets/limits for financial ratios:

• Net financial debt/EBITDA

• Net financial debt/Equity

Financial Policy

www.tupras.com.trJanuary 20Inestor Presentation 37

Financial Discipline: Risk management policies focusing on areas such as leverage, liquidity, counterparty risk, commodity, interest rate and currency exposure.

Leverage & Liquidity

• Current ratio

• Share of long term debt

Deposit is kept within bank-based limits:

• Credit rating assessment and strong capital base.

• Cap on the maximum deposit allocated to a single bank.

• Threshold for deposits subject to banks shareholders’ equity.

Counterparty Risk Policy

• The fixed/floating profile of financial debt.

• Proactive management of FX risk with derivative instruments

• Zero FX exposure target.

Interest Rate & Fx

Inventory Hedging Policy:• Operational hedge: Optimum stock policy & forward pricing mechanism.• Financial hedge: Expected inventory exposure for the year end is hedged by using derivatives.• Hedging ratio increasing throughout the year.

Crack Margin Hedging Policy:• Financial hedge: Crack margin (gasoline, diesel, jet fuel, fuel oil) risk mitigation by using derivatives.• Hedge ratio between %0-%50 with up to 1 year hedge tenor

CommodityHedging

Policy

Financials

Hizmete Özel / Confidential

FX Exposure Management (30 September 2019)

www.tupras.com.trJanuary 20Investor Presentation 38

Cash

342

Forward & CFH2,463

Stock1,682

Receivables & Other Assets

98

Payables2,252

ST Financial Loans533

• RUP: 191• Other: 342

LT Financial Loans1,789

• RUP: 707• Eurobond: 700• Other Loans: 382

Consolidated Hard Currency Assets

Consolidated Hard Currency Liabilities

Million $

+11 mn $

* Cash flow hedge accounting : 864 mn $

• A significant portion of the Group's crude oil and refined

product purchases are denominated in US Dollars. In

addition, the Group finances its capital expenditures

mostly through borrowings denominated in US Dollars.

• Natural Hedge: The Group is able to mitigate some of

the impact of volatility in exchange rates through

natural hedges: crude oil and refined product

inventories are US Dollar denominated assets.

• Cash flow Hedge: RUP Facility financing loans

designated as hedging instruments of highly probable

export revenues.

• As a general Koç Holding financial policy, Group

companies are allowed to keep foreign exchange

positions within certain limits.

Tüpraş continues to employ strict FX policies to mitigate currency risks stemming from volatility.

Financials

Hizmete Özel / Confidential

Appendix

Hizmete Özel / Confidential

2019 Refinery Maintenance Schedule

www.tupras.com.trJanuary 20Investor Presentation 40

Refinery Unit QuarterDuration(weeks)

Reason Status

İzmir

Plt 100 CDU Q4 2-3 Periodic

Plt-8200 Hydrocracker Q4 2-3 Periodic

Plt-8100 Vacuum Q4 2 Periodic

Plt 9200 CCR Q1 3 Completed

İzmit

RUP Q1&Q2 11 Completed

Plt 2 Crude Oil & Vacuum Q4 7-8 Periodic

Plt 7 FCC Q4 5-6 Periodic

Kırıkkale

Batman Plt 100/1100 Crude Oil & Vacuum Q1 10 Completed

Appendix

Hizmete Özel / Confidential

2019 Expectations

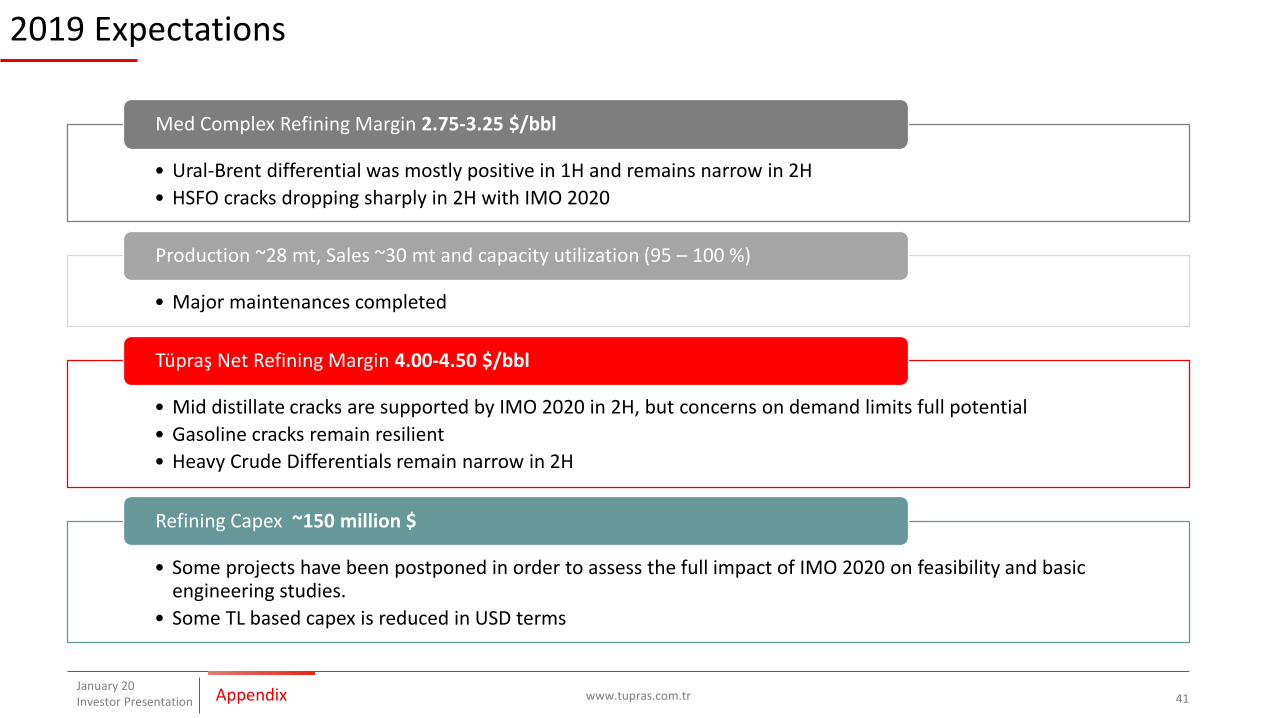

www.tupras.com.trJanuary 20Investor Presentation 41

• Ural-Brent differential was mostly positive in 1H and remains narrow in 2H

• HSFO cracks dropping sharply in 2H with IMO 2020

Med Complex Refining Margin 2.75-3.25 $/bbl

• Major maintenances completed

Production ~28 mt, Sales ~30 mt and capacity utilization (95 – 100 %)

• Mid distillate cracks are supported by IMO 2020 in 2H, but concerns on demand limits full potential

• Gasoline cracks remain resilient

• Heavy Crude Differentials remain narrow in 2H

Tüpraş Net Refining Margin 4.00-4.50 $/bbl

• Some projects have been postponed in order to assess the full impact of IMO 2020 on feasibility and basic engineering studies.

• Some TL based capex is reduced in USD terms

Refining Capex ~150 million $

Appendix

Hizmete Özel / Confidential

Competition - STAR Refinery

www.tupras.com.tr 42January 20Investor Presentation

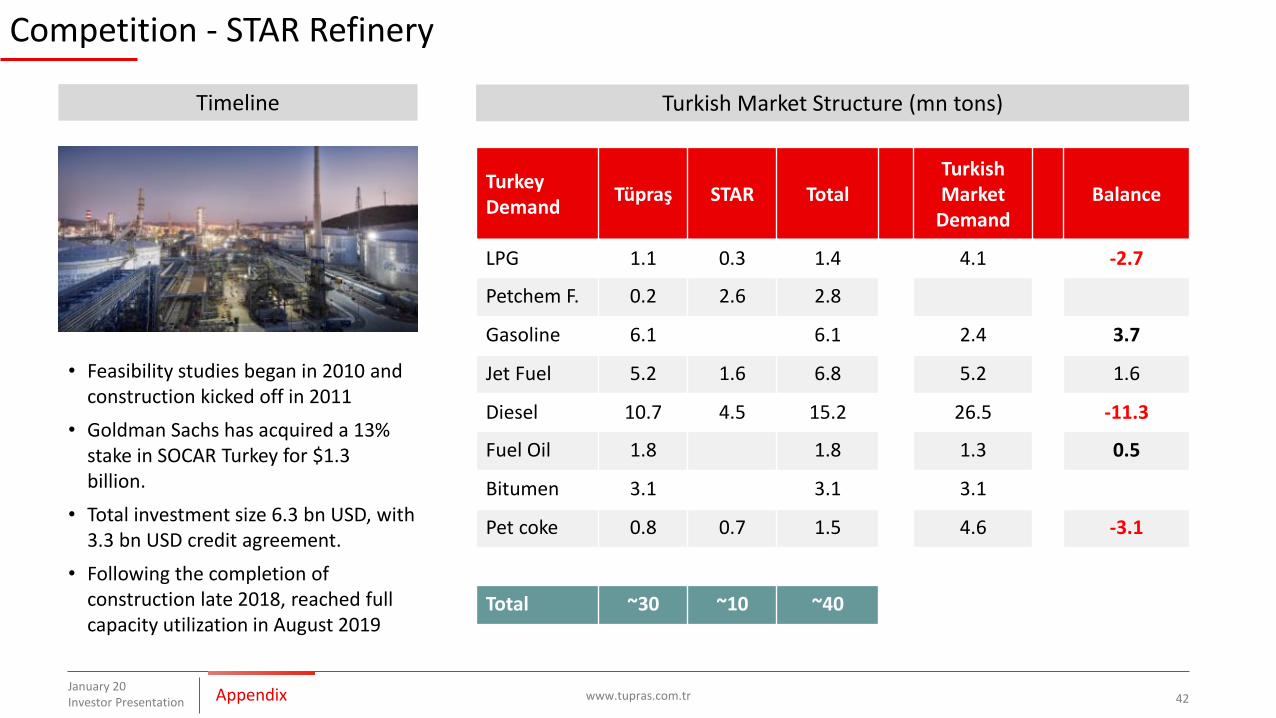

• Feasibility studies began in 2010 and construction kicked off in 2011

• Goldman Sachs has acquired a 13% stake in SOCAR Turkey for $1.3 billion.

• Total investment size 6.3 bn USD, with 3.3 bn USD credit agreement.

• Following the completion of construction late 2018, reached full capacity utilization in August 2019

Turkish Market Structure (mn tons)Timeline

Turkey Demand

Tüpraş STAR TotalTurkishMarket

DemandBalance

LPG 1.1 0.3 1.4 4.1 -2.7

Petchem F. 0.2 2.6 2.8

Gasoline 6.1 6.1 2.4 3.7

Jet Fuel 5.2 1.6 6.8 5.2 1.6

Diesel 10.7 4.5 15.2 26.5 -11.3

Fuel Oil 1.8 1.8 1.3 0.5

Bitumen 3.1 3.1 3.1

Pet coke 0.8 0.7 1.5 4.6 -3.1

Total ~30 ~10 ~40

Appendix

Hizmete Özel / Confidential

Competition - Regional Competition

www.tupras.com.tr 43January 20Investor Presentation

• Tüpraş competes with 71 refineries in the Mediterranean and Black Sea markets.• Mediterranean regional product balance is also affected from Middle East, North West Europe and Asia flows

17 Refineries ~1.8mbd

Mediterranean Black Sea

54 Refineries ~7.8mbd

Appendix

Hizmete Özel / Confidential

IMO 2020: Changes in Bunker Specification and Its Effects

www.tupras.com.trJanuary 20Investor Presentation 44

Current compliant fuels

Cu

rren

t O

utl

oo

kB

eyo

nd

20

20

Demand shift beyond 2020

HSFO replacement expectations

Long term outlook for marine fuels

• Marine Gasoil (Diesel): Easiest solution as it is already available

• Very Low Sulphur Fuel Oil (VLSFO): Either through FCC with sweet crudes or by blending

• Scrubbers: As of 01/11/19, ~2.8K vessels are either fitted or scheduled to be fitted and ~0.6K vessels are on order book to be delivered with scrubbers

• LNG: requires significant investments at ports

0

1

2

3

4

5

6

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Compliant HSFO Non-compliant HSFO ULSFO MGO LNG

• MGO is expected to be the initial choice in 2020• VLSFO becomes more widespread through the years as

availability & compatibility issues get resolved• Compliant HSFO use grows as scrubber numbers rise

from ~2K after Jan 1st, 2020 (some ports started bans on open-loop scrubbers thus this projection might change)

Source: Market Reports

Appendix

Hizmete Özel / Confidential

Tüpraş Production Flow and Yield Breakdown

www.tupras.com.trJanuary 20Investor Presentation 45

• Residuum Upgrade Plant (RUP) was completed in 2015 and it is the main conversion unit of Tüpraş.

• First periodic maintenance was completed in Q2 2019.

Appendix

Key Units# of

UnitsCapacity(m3/d)

CRUDE OIL 8 99,420

VACUUM DIST. 8 42,752

HYDROCRACKER 4 18,032

ISOMERATION 3 7,804

UNIFINER REFORMER

5 16,225

KERO/DIESEL (HDS)

9 37,265

FCC 2 4,650

COKER 1 9000

NAPHTASPLITTER

8

LPG MEROX 6

Flow Diagram

LPG MEROX

NAPHTHASPLITTER

ISOMER.

VACUUMDIST.

UNIFINERREFORMER

KERO/DIESEL (HDS)

FCC

HYDROCRACKER

COKER

Bitumen

Lube Oil

FCCGasolineHDS

BenzenSaturation

Multiple distillation

and production

units

Other, 3.8%

Bitumen & Fuel Oil, 19.9%

Lube Oil, 0.5%

Diesel,

33.9%

Jet Fueloil, 16.5%

GasolineNaphtha,

22.0%

LPG, 3.5%

Hizmete Özel / Confidential

RUP Feedstock and Production

www.tupras.com.trJanuary 20Investor Presentation 46

• Residium Upgrade Plant (RUP) was completed in 2015 and it is the main conversion unit of Tüpraş.

• First periodic maintenance was completed in Q2 2019.

Total Output ~4.25mn tonsTotal Processing ~4.50 mn tons

Appendix

Hizmete Özel / Confidential

European Pump Price Comparison

www.tupras.com.trJanuary 20Investor Presentation 47

2.833.93

2.373.02

3.562.79

3.722.73

0.70

0.00

0.870.54

0.000.96

0.000.95

3.45

4.55 5.696.14 5.86

6.15 6.64 6.60

0

2

4

6

8

10

12

TR Spa. Ger UK Eu19 Fra. Gre. Ita.

Gasoline (TL/Lt)

Refinery Price Dist. Margin Tax

3.174.10

2.893.94

4.52

3.02 3.05 3.18

0.760.00

0.910.00

0.00

0.92 0.80 0.73

2.58

3.85 4.374.78

4.49 5.55 5.756.21

0

2

4

6

8

10

12

TR Spa. Ger. EU19 Gre. Fra. Ita. UK

Diesel (TL/Lt)

Refinery Price Dist. Margin Tax

European prices as of 16th December - Turkeys prices as of 24th December

Turkish fuel prices are highly competitive with other European countries.

Appendix

Hizmete Özel / Confidential

Tüpraş - ESG - Over a Decade of Dedication

www.tupras.com.trJanuary 20Investor Presentation 48Appendix

Tüpraş kicked off its sustainability

program back in 2008 and achieved

many milestones in a decade

~480 energy efficiency

projects leading to

~35,000 TJ saving and

2.4 mt CO2 reduction

31%increase in solid waste recovery

20 points drop in Energy

Intensity

36% decrease in fresh

water usage

~205 MTL donations and sponsorships

75% increase in female

employee numbers

~1mn workhours dedicated to

OHS training

+1.3 points increase in Corporate

Governance rating

17% female representation in senior and mid-level

management

See our Sustainability Report for details

Hizmete Özel / Confidential

Tüpraş - ESG - 2018 Achievements

www.tupras.com.tr 49

• Kırıkkale Refinery won the first place, İzmit Refinery the second and Batman Refinery the third in the Industrial Energy Efficiency Project Competition.

• İzmit Refinery won the first prize in the Sustainable Business Awards -Water Management Category.

• Achieved 69.5% water recycle ratio

• Achieved 88.6% solid waste recovery

Environmental Responsibility

• Signed agreement to supportHeForShe (Global cooperation with UN Women and Fenerbahçe Sports Club)

• 62% of ex-crude procurement activities were conducted through local businesses.

Social Support

• 9.50 Corporate Governance Rating

• 13% Female Representation at the Board,

• 17% Female Representation in Upper and Mid-Level Management.

Governance Excellence

AppendixJanuary 20Investor Presentation

Hizmete Özel / Confidential

Koç Holding

www.tupras.com.tr 50

• Koç Holding is Turkey’s largest industrial and services group in terms of revenues, exports, employees, taxes paid and market capitalization

• The only Turkish company in Fortuna 5001.• 20% CAGR in consolidated profit2 the last five years

Turkey’s Leading Investment Holding Company

• Leading positions with clear competitive advantages in sectors with long-term growth potential such as energy, automotive, consumer durables and finance.

Pioneer in its Sectors

8%

Combined Revenues /

GDP

10%

Total Exports / Turkey’s Exports

16%

Total Market Cap in Borsa

Istanbul

Notes : Data as of YE18, 2018 GDP reflects the projection of Turkish government’s New Economic Program.(1) 2018 Report(2) In TL terms between 2014-18

AppendixJanuary 20Investor Presentation

Hizmete Özel / Confidential

Investor Presentation

Latest Webcast

Sustainability Report

contact us: [email protected]