Investor Call Presentation - Diamond Bankdiamondbank.com/images/banners/linkcreation/IR/2013... ·...

40

Investor Call Presentation Full Year 2013 & Q1 2014 Results

Transcript of Investor Call Presentation - Diamond Bankdiamondbank.com/images/banners/linkcreation/IR/2013... ·...

14 APRIL 2014

Investor Call Presentation

Full Year 2013

&

Q1 2014 Results

2

Forward looking statements

This presentation contains or incorporates by reference ‘forward-looking statements’ regarding the belief or current expectations of Diamond

Bank, the Directors and other members of its senior management about the Group’s businesses and the transactions described in this

presentation. Generally, words such as ‘‘could’’, ‘‘will’’, ‘‘expect’’, ‘‘intend’’, ‘‘anticipate’’, ‘‘believe’’, ‘‘plan’’, ‘‘seek’’ or similar expressions identify

forward-looking statements.

These forward-looking statements are not guarantees of future performance. Rather, they are based on current views and assumptions and

involve known and unknown risks, uncertainties and other factors, many of which are outside the control of the Company and/or its Group and

are difficult to predict, that may cause actual results to differ materially from any future results or developments expressed or implied from the

forward-looking statements. Such risks and uncertainties include, but are not limited to, regulatory developments, competitive conditions,

technological developments and general economic conditions. The Bank assumes no responsibility to update any of the forward looking

statements contained in this presentation.

Any forward-looking statement contained in this presentation based on past or current trends and/or activities of Diamond Bank should not be

taken as a representation that such trends or activities will continue in the future. No statement in this presentation is intended to be a profit

forecast or to imply that the earnings of the Company for the current year or future years will necessarily match or exceed the historical or

published earnings of the Company. Each forward-looking statement speaks only as of the date of the particular statement. Diamond Bank

expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein

to reflect any change in Diamond Bank’s expectations with regard thereto or any change in events, conditions or circumstances on which any

such statement is based.

3

Outline

• Executive Summary (by Dr. Alex Otti, GMD)

• Strategy & Business Update (by Dr. Alex Otti, GMD)

• FY 2013 Financial Performance (by Abdulrahman Yinusa, CFO)

• Q1 2014 Financial Performance (by Abdulrahman Yinusa, CFO)

• Concluding Remarks (by Dr. Alex Otti, GMD)

4

Overview

The global economic recovery remained weak despite the US Federal Reserve tapering which further

depressed economic activities in emerging markets.

Global economy grew 3.0% in 2013, and forecast to grow by 3.7% in 2014; driven by recovery in

advanced economies.

The World Economy

The Nigerian Economy

Our Strategy

Outlook

The Nigerian economy grew by approximately 6.8% in 2013. Nigeria remains an attractive investment

destination as the on-going transformation in the real sector is poised to deliver sustainable growth in

the mid to long term.

The recent rebasing of the GDP (to $510bn) offers fresh imperatives for investment opportunities.

The Bank’s full year 2013 and Q1 2014 results point to a healthy and sustainable growth. Our strategy

remains to consolidate our dominance in the Retail/SME space while remaining relevant in the

Corporate space.

We will continue to offer unequalled customer experience within the financial inclusion framework.

Despite the challenging operating environment, we will continue to explore all opportunities to grow

our business and market share as we leverage on our growing customer relationships.

We remain positive on our retail banking strategy, even though our business and corporate banking

segments remain significant business drivers.

5

Operating Environment

Average GDP growth rate of 6.8% in 2013 (7.7% in Q4 2013)

Agriculture, Wholesale & Retail trades and Services remain key drivers of GDP

Average Headline Inflation of 8.5% in 2013 year-on-year (8.0% in Dec. 2013)

Stable official exchange rate – N155/N160; albeit the Naira came under pressure at the parallel

market segment.

Reduction in Commission on Turnover (COT) from N5/mille to N3/mille (April 2013); N2/mille (Year

2014); N1/mille (Year 2015); and N0/mille (year 2016)

Increase in the savings interest rate to 30% of Monetary Policy Rate (MPR) – 3.6%

Increase in Cash Reserve Requirement (CRR) charge on Public Sector funds to 50% ( August 2013),

and 75% (February 2014)

Increase in CRR charge on Private Sector funds to 15% from 12% (April 2014)

Cashlite policy – Lagos (April 2012); 6 States (Oct. 2013); Nationwide (to commence in July 2014)

Sound and Stable Macroeconomic Environment

Regulatory Environment

6

Nigerian Economy – Key Trends

0

2

4

6

8

10

12

14

16

2008 2009 2010 2011 2012 2013

Monetary policy rate Standing lending rate Standing deposit rate

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

14

2008 2009 2010 2011 2012 2013

Interest Rates, %

Private Sector Credit Growth, % YoY

2010 2011 2012 2013

7.9% 7.4%

6.6% 6.8%

GDP Growth Rates, % YoY

Inflation Rate, % YoY

13.9%

10.9% 12.2%

8.5%

2010 2011 2012 2013

7

Diamond Bank at a glance

Diamond Bank

Diamond Bank Togo

Diamond Bank Senegal

Diamond Bank Cote d’Ivoire

Current Group Structure

Diamond Pension Fund

Custodian

Diamond Bank Benin S.A.

Diamond Bank

UK

Diamond Bank commenced operations in March 1991; assumed the

universal banking status in Feb. 2001; and was listed on the NSE in

May 2005.

The Bank acquired Lion Bank in October 2005 and listed its GDRs on

the Professional Securities Market of the London Stock Exchange in

January 2008.

The Group has 286 branches across Nigeria, Benin Republic, Cote

d’Ivoire, Senegal, Togo and the United Kingdom.

In line with the new CBN banking model, Diamond divested from its

subsidiaries and obtained licence to operate as a commercial bank

with international authorization.

Background

Countries with Banking Presence

Nigeria (255 branches), Benin (19), Cote d’Ivoire (3), Senegal (4), Togo (4) and UK (1)

Listings Nigeria Stock Exchange – 2005 London PSE – 2008

Market Capitalisation*

N91.9 billion (As of 31 March 2014)

Ratings Fitch: BBB+ (B, Stable - Int’l), GCR: A-

Number of accounts

3.4 million

ATMs/POS 689 / 10,500

Staff Head Count (Group)

4,366

Alternative Delivery Channels

ATMs, POS, Internet, mobile

Direct Sales Force 1,567

Strategic Partners IFC, USAID, WWB, EFINA, MTN

Recognitions Appointed by DFID as one of the four African banks to manage $7.1 million financial inclusion project

Awards

IFC’s Award for Best Issuing Bank in Su—Saharan Africa (under IFC Global Trade Finance Program); Best Credit card in Nigeria; Best Bank in Oil & Gas investment

Key Highlights

8

Gross earnings grew 30% to N181 billion, driven by the growth in

balance sheet and other transactional activities.

PBT grew by 19% to N32bn from N27bn in December 2012.

Customer deposits continued to drive balance sheet growth.

Comments

FY 2013 Group Performance Summary

P & L (N’Bn) FY 2013 FY 2012 % Growth

Gross Earnings 181 139 30

Operating Income 140 113 24

Profit Before Tax 32 27 19

Balance Sheet FY 2013 FY 2012 % Growth

Total Assets 1,519 1,178 29

Loans to customers 689 585 18

Deposits 1,206 910 33

9

Forecast for 2014 Profitability

Impact on P&L (N’Bn)

Operating Profit 55

Provision for Losses

- Direct Provision (Circa) ~ (20)

Profit/(Loss) Before Tax 35

45 55

28 32

2012 2013 2014 est

Operating Profit PBT

Deposits (N’Bn) Operating Profit and PBT (N’Bn)

ROE of 23% achieved in 2013 financial year

ROE of above 20% expected in 2014 (excl. impact of any increase in

equity capital)

Comments

35

55

-11.4%

22.7% 23.0%

> 20%

2011 2012 2014 est.

ROAE

2013

10

Outline

• Executive Summary (by Dr. Alex Otti, GMD)

• Strategy & Business Update (by Dr. Alex Otti, GMD)

• FY 2013 Financial Performance (by Abdulrahman Yinusa, CFO)

• Q1 2014 Financial Performance (by Abdulrahman Yinusa, CFO)

• Concluding Remarks (by Dr. Alex Otti, GMD)

11

Business Segments

79

222

109

309

1

Gross Risk Assets (N'bn)

Retail Banking

Business Banking

Subsidiaries

Corporate Banking

Treasury

6.2

6.2 5.3

7.7

0

NPLs (N'bn)

Retail Banking

Business Banking

Subsidiaries

Corporate Banking

Treasury

393

542

189

53 29

Deposits (N'bn)

Retail Banking

Business Banking

Subsidiaries

Corporate Banking

Treasury

7.8 2.8

4.9

2.5 0

NPL (%)

Retail Banking

Business Banking

Subsidiaries

Corporate Banking

Treasury

12

Retail Banking

More Efficient Balance Sheet

Strategic Partnerships

Continue to drive low-cost deposits by deploying cost effective delivery channels.

Continue to reach out to the under-banked and underserved population through:

(i) Full roll out of the BETA proposition in partnership

with Women’s World Banking (WWB)

(ii) Launched the youth & mass market proposition in

partnership with MTN (Diamond Y’ello Account)

Retail Banking Growth Strategy Retail Banking Loan Portfolio

New Segments Launched the school banking proposition to capture the

entire value chain of the educational sector.

16% 13% 12% 12% 11%

4% 4% 6% 5% 5%

11% 11% 10% 10% 9%

53% 54% 51% 51% 50%

16% 18% 21% 22% 25%

Dec. 12 Mar. 13 Jun. 13 Sep. 13 Dec. 13

Personal Loan Auto Loan & Lease Mortgages MSME Credit Card

Critical target markets include:

– MSMEs (with annual turnover of < N500 million)

– Individuals and Sole Proprietors

– Mass Market

Recognition

Only Nigerian Bank appointed alongside three other African banks by UK’s DFID to manage $7.1 million dedicated to bringing 1.3 million people in sub-Saharan Africa into the formal financial services sector.

Ranked among the four most customer-centric banks in the Retail segment – 2013 Retail Banking Survey

Awards

Best Credit Card product of the year by Coalition for e-payments (2nd year running)

Best co-branded program of the year by Coalition for e-payments

13

Our Retail Footprint: Diverse Channel Options

Number of Customer Accounts (million)

Number of Online Banking Customers

Number of ATMs

240

408

671

Dec. 2011 Dec. 2012 Dec. 2013

180%

1.5

2.1

3.4

Dec. 2011 Dec. 2012 Dec. 2013

69,789

356,907

1,120,671

Dec. 2011 Dec. 2012 Dec. 2013

15,058%

127%

1,053 1,092

1,567

Dec. 2011 Dec. 2012 Dec. 2013

Number of Direct Sales Agents No. of Mobile Banking Customers (million)

49%

Number of Telephone Banking customers

2,933

828,155

1,185,729

Dec. 2011 Dec. 2012 Dec. 2013

1.4

1.9

2.8

Dec. 2011 Dec. 2012 Dec. 2013

100%

403,272%

14

24% Savings & Demand

Deposits 85% (86%)

Time deposits 15% (14%)

Dec 2013 (Dec 2012)

86% 85% 84% 86% 85%

14% 15% 16% 14% 15%

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

Low Cost Deposits Fixed Deposits

Retail Deposits (N’Bn)

N393bn

29%

N305bn N316bn N334bn

Retail Banking – Trend in Deposits & Loans

15%

N343bn

16%

4%

11%

53%

16%

Dec. 12

Personal Loan

Auto Loan & Lease

Mortgages

MSME

Credit Card

11%

5%

9%

50%

25%

Dec. 13

Personal Loan

Auto Loan & Lease

Mortgages

MSME

Credit Card

15

Business Banking

Middle Market 66%

(67%)

Public Sector 34%

(33%)

Deposits N542bn (Dec 2012: N415bn)

Middle Market 96%

(96%)

Public Sector 4%

(4%)

Risk Assets N222bn (Dec 2012: N213bn)

Business Banking Growth Strategy

SMEs

Strategic Partnerships

Continue to provide flexible access to credits – provision of on-lending facilities

Continue to work with DFIs to support SMEs

Partnering with IFC to build capacity and increase access to agric. finance for SMEs

International Trade

Leverage on our UK subsidiary in providing trade finance support

Risk Assets

Deposits

16

Corporate Banking

Loan Portfolio

Deposits

28% 21% 22% 21%

16% 17% 18% 18%

56% 62% 60% 61%

Dec. 2012 Jun. 2013 Sep. 2013 Dec. 2013

Institutional banking Infrastructure & Transport Energy Business

47% 38% 35% 31% 38%

22% 22% 33% 27%

30%

31% 40%

32%

42%

32%

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

Institutional banking Infrastructure & Transport Energy Business

More Efficient Balance Sheet

Strategic Partnerships

Continue to leverage on e-payment and cash management services.

Continue to work with DFIs and multilateral agencies to provide funding

Corporate Banking Growth Strategy

Recognitions & Awards

Received the World Finance Group award for the best Oil & Gas Investment in 2013 (2nd year running)

Appointed as one of the lending institutions to disburse the Cabotage Vessel Financing Fund (CVFF)

17

Outline

• Executive Summary (by Dr. Alex Otti, GMD)

• Strategy & Business Update (by Dr. Alex Otti, GMD)

• FY 2013 Financial Performance (by Abdulrahman Yinusa, CFO)

• Q1 2014 Financial Performance (by Abdulrahman Yinusa, CFO)

• Concluding Remarks (by Dr. Alex Otti, GMD)

18

Strong Balance Sheet Growth (Dec. 2012 to

Dec. 2013)

+29%

Assets

+18%

Loans (net)

+33%

Deposits

ROAE of 23.0% (Dec. 2012: 22.7%); ROAA of 2.1% (Dec. 2012: 2.0%)

EPS of 197k (Dec. 2012: 153k)

Profit before tax (PBT) up 19% to N32.0 billion (Dec. 2012: N27.0 billion)

Efficiency and

Profitability

Capital ratios – 17.3% risk adjusted capital ratio in FY 2013 against 15% statutory limit

Liquidity ratios of 41.8% (Dec. 2012: 42.3%, Sept. 2013: 36.7%)

Liquidity was adversely impacted by the new CRR on government funds

Capital and

Liquidity

Strong net interest margin of 8.1% - one of the best in the industry

30% growth in gross earnings to N181 billion (Dec. 2012: N139 billion)

Low cost of funds – 3.4% driven by the continuous growth in retail deposits

Revenue Mix

Financial Highlights

Improving NPL – 3.5% in FY 2013; 4.7% in Dec. 2012

Coverage ratio – 116.1% in FY 2013 from 88.9% in Dec. 2012 Assets Quality

19

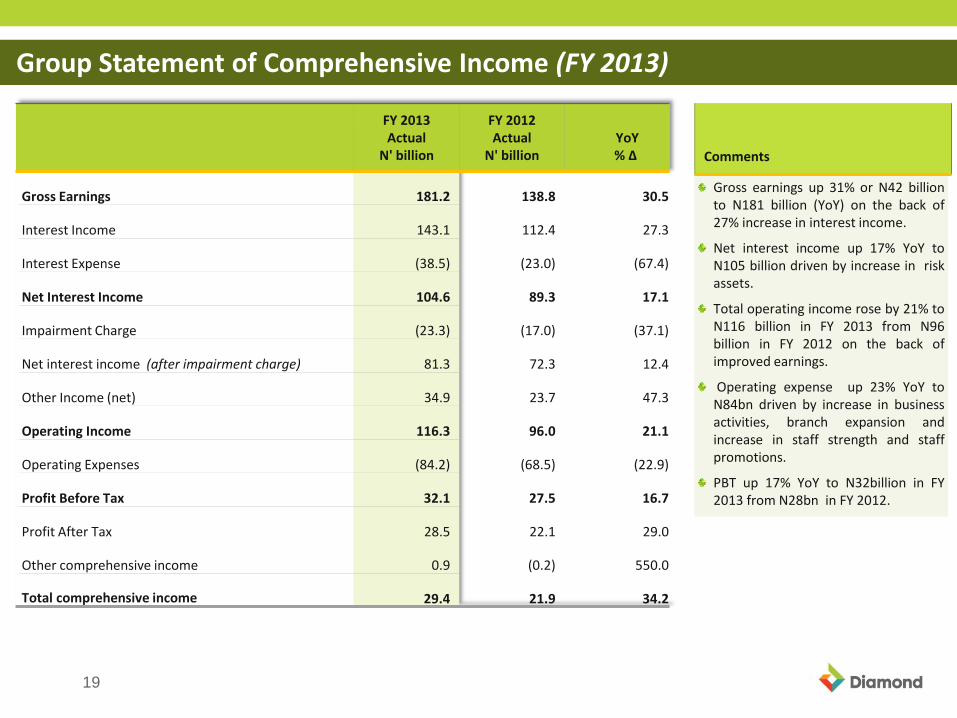

Group Statement of Comprehensive Income (FY 2013)

Gross earnings up 31% or N42 billion to N181 billion (YoY) on the back of 27% increase in interest income.

Net interest income up 17% YoY to N105 billion driven by increase in risk assets.

Total operating income rose by 21% to N116 billion in FY 2013 from N96 billion in FY 2012 on the back of improved earnings.

Operating expense up 23% YoY to N84bn driven by increase in business activities, branch expansion and increase in staff strength and staff promotions.

PBT up 17% YoY to N32billion in FY 2013 from N28bn in FY 2012.

Comments

FY 2013 Actual

N' billion

FY 2012 Actual

N' billion YoY % Δ

Gross Earnings 181.2 138.8 30.5

Interest Income 143.1 112.4 27.3

Interest Expense (38.5) (23.0) (67.4)

Net Interest Income 104.6 89.3 17.1

Impairment Charge (23.3) (17.0) (37.1)

Net interest income (after impairment charge) 81.3 72.3 12.4

Other Income (net) 34.9 23.7 47.3

Operating Income 116.3 96.0 21.1

Operating Expenses (84.2) (68.5) (22.9)

Profit Before Tax 32.1 27.5 16.7

Profit After Tax 28.5 22.1 29.0

Other comprehensive income 0.9 (0.2) 550.0

Total comprehensive income 29.4 21.9 34.2

20

Loans to banks

7% (8%)

Loans and advances to customers 71% (79%)

Investment securities 22% (13%)

Interest Income

Commission on turnover 17% (18%)

Letter of credit

commission 11% (9%)

Service fees & charges 35%

(54%)

Others 37% (19%)

Net Fee and Commission Income

Group Profit Drivers – Strong Revenue Generation

Gross earnings up 30.5% to N181.2 billion YoY.

Interest income accounted for 79.0% of gross earnings (80.9% in

2012) while 18.2% was derived from non-interest income (19.4% in

2012).

Revenue growth was driven by sustained risk assets volume and fee

generating transactions.

However, this was partially offset by the impact of margin

compression.

Dec 2013 (Dec 2012) Dec 2013 (Dec 2012)

112.4 143.1

26.4

38.1

Dec. 2012 Dec. 2013

Int Income Non int. Income

Revenue Mix (YoY : +31%)

N181.2bn

N138.8bn

Comments

21

Group Profit Drivers – Moderate Operating Expenses

N’Billion

17.0 23.3

Dec. 2012 Dec. 2013

Impairment Charge (YoY: -37%)

60.6% 60.3%

Dec. 2012 Dec. 2013

Cost to Income Ratio (excludes provisions)

Operating expenses increased 23% year-on-year to N84.2 billion,

due mainly to investment in new branches and work force.

Staff strength in the Bank increased to 3,805 in Dec 2013 from

2,912 in Dec. 2012.

Impairments went up due principally to significant reduction in

collateral valuations.

Comments

N’Billion

42.5 54.8

26.0

29.4

Dec. 2012 Dec. 2013

Operating expenses Employee benefit expenses

Expense Summary (YoY: +23%)

22

2

2

Group Statement of Financial Position

Net loan book of N689 billion, up 18% from

December 2012 (N585 billion) primarily

reflecting growth in volume of business.

Deposit base continues to grow above the N1

trillion mark closing at N1.206 trillion, up 33%

from December 2012 (N910 billion).

Total assets up 29% to N1.5 trillion from N1.2

trillion as at December 2012.

Effect of new CRR Policy led to increase in cash

and balances sterilized at the CBN by 73% in FY

2013 from N132bn in Dec 2012.

Comments

FY 2013 Actual

N' billion

FY 2012 Actual

N' billion

YoY % Δ

Cash & Balances with Central Banks 228.3 132.2 72.7

Loans & Advances to Banks 129.4 139.8 (7.4)

Loans & Advances to Customers 689.2 585.2 17.8

Investments 294.0 173.7 69.3

Pledged Assets 96.5 79.3 21.7

Other Assets 22.1 13.8 60.1

Fixed Assets & Intangibles 52.7 45.8 15.1

Deferred Tax Asset 6.7 8.3 (19.3)

Total Assets 1,518.9 1,178.1 28.9

Deposits from Banks 54.6 31.2 75.0

Deposits from Customers 1,206.0 910.2 32.5

Derivative Liability 14.7 13.2 11.4

Other Liabilities 36.3 45.2 (19.7)

Borrowings 47.5 50.0 (5.0)

Long Term debt 20.9 19.4 7.7

Equity 138.9 108.9 27.5 Total Equity & Liabilities 1,518.9 1,178.1 28.9

23

Group Risk Management Metrics – FY 2013

FY 2013 N’ billion

9-M 2013 N’ billion

H1 2013 N’ billion

Q1 2013 N’ billion

FY 2012 N’ billion

Gross Risk Assets 718.7 715.4 652.1 625.0 610.7

NPL 25.4 31.0 26.7 28.9 28.7

Provisions 29.5 33.6 27.6 32.4 25.5

NPL Ratio 3.5% 4.3% 4.1% 4.6% 4.7%

NPL Coverage Ratio 116.1% 108.4% 103.1% 112.1% 88.9%

NPL ratio stood at 3.5% in FY 2013. This is an improvement compared to 4.7% in Dec. 2012

Coverage Ratio improved to 116.1% in FY 2013 from 88.9% in FY 2012

Comments

24

Group Key Performance Metrics – FY 2013

FY 2013

9-M 2013

H1 2013

Q1 2013

FY 2012

Net Interest Margin (NIM) 8.1% 8.6% 8.8% 8.8% 9.9%

Cost of Risk 3.5% 3.4% 3.1% 2.1% 3.3%

Cost of Funds 3.4% 3.4% 3.5% 3.6% 2.9%

Loan-to-Deposit Ratio 59.6% 67.4% 64.0% 63.2% 67.1%

Capital Adequacy Ratio (CAR) 17.3% 17.1% 16.5% 16.3% 17.3%

Liquidity Ratio 41.8% 36.7% 48.2% 46.9% 42.3%

Cost to Income Ratio 60.3% 58.9% 59.1% 60.7% 60.6%

Earnings per share 197K 185k 175k 174k 153k

ROE 23.0% 22.4% 22.1% 22.5% 22.7%

The Group Net Interest Margin (NIM) decreased to 8.1% in FY 2013 from 8.6% in Q3 2013 due principally to impact of 50% CRR charge on public sector funds.

Comments

25

Group Balance Sheet Structure

1,178 1,273 1,334 1,377

1,519

910 989

1,032 1,062 1,206

585 593 625 682 689

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

Total Assets Deposits Loans & Advances

Balance Sheet Trend (N’Bn)

Total assets stood at N1.5 trillion as at FY 2013, up N339 billion or 29%,

from N1.2 trillion at the end of Dec 2012.

Growth in balance sheet driven by growth in deposits (N1.2 trillion as at

Dec. 2013, from N910 billion in Dec. 2012).

Net Risk Assets up by N104 billion or 18% to N689 billion (Dec. 2012: N585

billion).

Comments

1,519 358

689

294

97 59 22

Total assets LiquidAssets

Risk Assets Investments PledgedAssets

Fixed Assets OtherAssets

Total Assets (N’Bn) Dec. 2013 (Dec. 2012)

1,519 55 1,206

48 36 36 139

TotalLiabilities

Dep. FromBanks

Depositsfrom

Customers

Borrowings OtherLiabilities

Tier 2Capital

Equity

Total Liabilities (N’Bn) Dec. 2013 (Dec. 2012)

1,178 272

585

174

54 14

79

1,178 910

45 33 109

50

31

26

Group Funding Mix & Deposits Composition

2010 2011 2012 2013

73% 78% 76% 74%

27% 22% 24% 26%

Demand & Savings Deposits Time Deposits

Sustaining Stable Low-Cost Funding Base

18% 11% 9% 9%

70% 76% 77% 79%

2010 2011 2012 2013

Equity Tier 2 Capital Borrowings

Other Liabilities Deposits Dep. From Banks

Funding Structure

2012

49% 57% 59% 57%

24% 21% 17% 17%

27% 22% 24% 26%

2010 2011 2012 2013

Demand Savings Time

Deposit Mix by Type

34%

45%

22%

Corporate

Deposit Mix by Business Segment

31%

24%

43%

2%

Retail Business

2013

27

Group Loan Growth

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

611 625

652

715 719

Gross Loans Gross Risk Assets (N’Bn)

Dec. 2012 Mar. 2013 Jun. 2013 Sep.2013 Dec. 2013

29 29 27

31

25 26

32

28

34

29

Non Performing Loans Provisions

Non Performing Loans & Provisions (N’Bn)

Loans and advances (gross) went up by 18% to N719 billion year-on-year (Dec

2012: N611 billion).

The growth in loan portfolio is driven by our growing customer relationships

especially in the business and corporate banking segments.

Loan to deposit ratio stood at 60% as at 31St Dec 2013 from 67% in Dec 2012.

Comments Loan to Deposit Ratio

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

67.1%

63.2% 63.2%

67.4%

59.6%

28

26%

18%

8%

10% 9%

7%

4%

5%

3%

1%

2%

2%

1%

4%

Oil & Gas 26%

General Comm 18%

Manufacturing 8%

Others 10%

Real Est & Const 9%

Power & Energy 7%

Government 4%

ICT 5%

Consumer Credit 3%

Transportation 1%

Agriculture 2%

Mortgage 2%

Education 1%

Financial and insurance 4%

Gross Loan Breakdown – Dec 2013

(N611bn) N719bn N719bn

Group Lending

26%

18%

8%

10% 9%

7%

4%

5%

3%

1%

2%

2%

1%

4%

Oil & Gas (26%) 26%

General Comm (20%) 18%

Manufacturing (13%) 8%

Others (8%) 10%

Real Est & Const (7%) 9%

Power & Energy (6%) 7%

Government (6%) 4%

ICT (4%) 5%

Consumer Credit (3%) 3%

Transportation (3%) 1%

Agriculture (2%) 2%

Mortgage (2%) 2%

Education (0%) 1%

Financial and insurance (0%)4%

Gross Loan Breakdown – (Dec 2012) Dec 2013

29

Group NPL Analysis

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

23% 20% 21% 15% 33%

52% 52% 57% 73% 51%

25% 28% 22% 12% 16%

Substandard Doubtful Lost

NPL by Category

N28.9bn

General Commerce and Oil & Gas accounted for about 65% of total NPLs.

The Group has managed its credit risk more effectively through its

improved risk management practices as demonstrated by < 5% NPL ratio.

Comments

General Comm 34%

Oil & Gas 31%

Consumer Credit 9%

Others 4%

Agriculture 6%

Real Estate & Constr. 7%

Manufacturing 1%

Power 1%

Communication 4%

Mortgage 3%

NPL by Sector (Dec. 2009) NPL by Sector (Dec 2013)

General Commerce 34%

Oil & Gas 27%

Consumer Credit 12%

Communication 9%

Others 8%

Agriculture 4%

Real Estate & Constr. 3%

Manufacturing 3%

Power 0%

NPL by Sector (Dec 2012)

N28.7Bn

N25.4Bn

N26.7bn N28.7bn N31.0bn N25.4bn

30

Group Asset Quality

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

4.7% 4.6% 4.1% 4.3%

3.5%

NPL Ratio

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

88.9% 112.1% 103.1% 108.4% 116.1%

Coverage Ratio

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

3.3%

2.1%

3.1% 3.4% 3.5%

Cost of Risk

Cost of risk remained within 5% in Dec 2013.

Coverage ratio improved to 116.1% in Dec 2013 from 88.9% in Dec 2012.

NPL ratio of sub 5% achieved through out 2013.

Comments

31

Group Net Interest Margin

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

9.9%

8.8% 8.8% 8.6% 8.1%

Strong Net Interest Margin (NIM)

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

13.8% 13.4% 13.4% 12.0%

11.1%

Yield on Earning Assets

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

2.9% 3.6% 3.5% 3.4% 3.4%

Low Cost of Funds Comments

Reduction in NIM by 50 bps due to the impact of CRR on public sector

funds as additional funds were sterilized thereby constraining earnings.

Despite the impact of the new CRR policy, the bank will continue to

protect its margin by leveraging on its Retail Banking strategy to maintain

cost of funds below industry average.

Cost of funds remained stable in FY 2013.

32

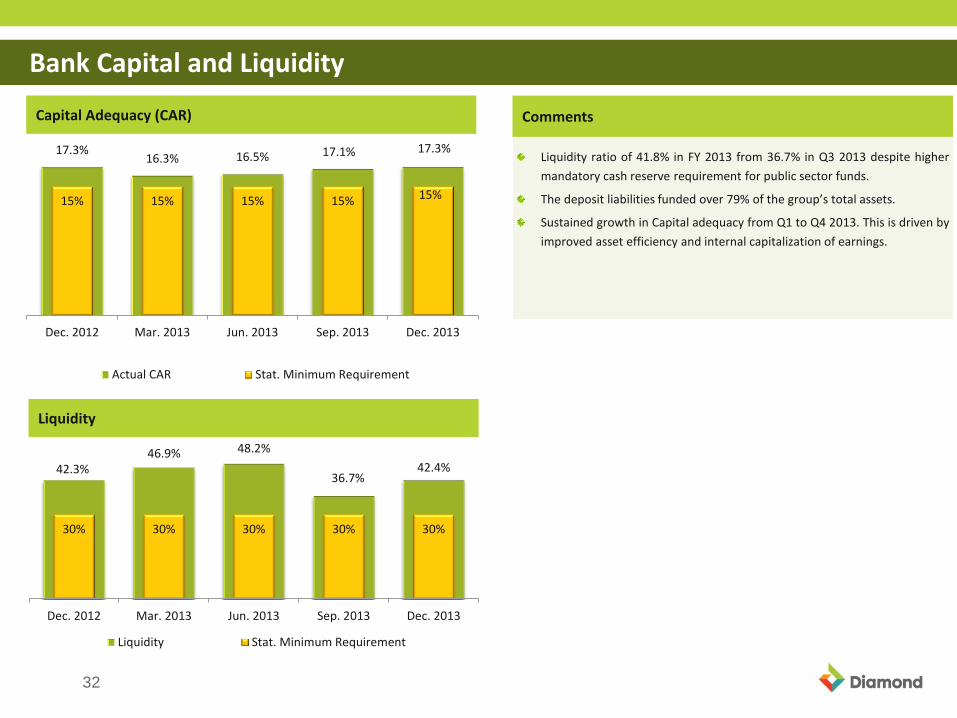

Bank Capital and Liquidity

42.3% 46.9% 48.2%

36.7% 42.4%

30% 30% 30% 30% 30%

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

Liquidity Stat. Minimum Requirement

Liquidity

Liquidity ratio of 41.8% in FY 2013 from 36.7% in Q3 2013 despite higher

mandatory cash reserve requirement for public sector funds.

The deposit liabilities funded over 79% of the group’s total assets.

Sustained growth in Capital adequacy from Q1 to Q4 2013. This is driven by

improved asset efficiency and internal capitalization of earnings.

Comments

17.3% 16.3% 16.5% 17.1% 17.3%

15% 15% 15% 15% 15%

Dec. 2012 Mar. 2013 Jun. 2013 Sep. 2013 Dec. 2013

Actual CAR Stat. Minimum Requirement

Capital Adequacy (CAR)

33

Outline

• Executive Summary (by Dr. Alex Otti, GMD)

• Strategy & Business Update (by Dr. Alex Otti, GMD)

• FY 2013 Financial Performance (by Abdulrahman Yinusa, CFO)

• Q1 2014 Financial Performance (by Abdulrahman Yinusa, CFO)

• Concluding Remarks (by Dr. Alex Otti, GMD)

34

Group Statement of Comprehensive Income (Q1 2014)

Gross earnings up 22% or N9 billion to N49 billion (YoY) on the back of 13% increase in interest income.

Net interest income up 12% YoY to N28 billion driven by increase in risk assets

Total operating income rose by 19% to N32 billion in Q1 2014 from N27 billion in Q1 2013 on the back of improved earnings.

Operating expense up 23% YoY to N23bn driven by branch expansion and increase in business activities.

PBT up 6% YoY to N9billion in Q1 2014.

Comments

Q1 2014 Actual

N' billion

Q1 2013 Actual

N' billion YoY % Δ

Gross Earnings 49.0 40.3 21.6

Interest Income 38.2 33.8 13.0

Interest Expense (10.8) (9.3) (16.1)

Net Interest Income 27.5 24.5 12.2

Impairment Charge (5.0) (3.2) (56.3)

Net interest income (after impairment charge) 22.5 21.3 5.6

Other Income (net) 9.9 6.0 65.0

Operating Income 32.4 27.3 18.7

Operating Expenses (23.2) (18.6) (24.7)

Profit Before Tax 9.2 8.7 5.7

Profit After Tax 8.4 6.3 33.3

Other comprehensive income (0.2) (0.3) 33.3

Total comprehensive income 8.2 6.0 36.7

35

3

5

Group Statement of Financial Position (Q1 2014)

Net loan book of N712 billion, up 4% from

December 2013 (N689 billion) primarily

reflecting growth in volume of business.

Deposit base up 2% to N1.233 trillion

from December 2013 (N1,206 trillion),

and up 25% from March 2013 (N989

billion).

Total assets up 4% to N1.6 trillion from

N1.5 trillion as at December 2013.

Effect of new CRR Policy led to increased

Cash & Balances sterilized at the CBN.

Comments

Q1 2014 Actual

N' billion

Q1 2013 Actual

N' billion

YoY % Δ

FY 2013 Actual

N' billion

QoQ % Δ

Cash & Balances with Central Banks 245.1 128.9 90.1 228.3 7.4

Loans & Advances to Banks 140.9 125.9 11.9 129.4 8.9

Loans & Advances to Customers 712.2 592.5 20.2 689.2 3.3

Investments 296.7 259.8 14.2 294.0 0.9

Pledged Assets 94.6 82.8 14.3 96.5 (2.0)

Other Assets 34.5 28.4 21.5 22.1 56.1

Fixed Assets & Intangibles 53.4 46.2 15.6 52.7 1.3

Deferred Tax Asset 6.7 9.2 (27.2) 6.7 0.0

Total Assets 1,584.1 1,273.7 24.4 1,518.9 4.3

Deposits from Banks 51.3 31.4 63.4 54.6 (6.0)

Deposits from Customers 1,233.2 989.0 24.7 1,206.0 2.3

Derivative Liability 14.7 13.2 11.4 14.7 0.0

Other Liabilities 69.8 55.8 25.1 36.3 92.3

Borrowings 47.0 49.8 (5.6) 47.5 (1.1)

Long Term debt 21.0 19.6 7.1 20.9 0.5

Equity 147.1 114.9 28.0 138.9 5.9

Total Equity & Liabilities 1,584.1 1,273.7 24.4 1,518.9 4.3

36

Group Risk Management Metrics – Q1 2014

Q1 2014 N’ billion

FY 2013 N’ billion

9-M 2013 N’ billion

H1 2013 N’ billion

Q1 2013 N’ billion

Gross Risk Assets 747.8 718.7 715.4 652.1 625.0

NPL 33.0 25.4 31.0 26.7 28.9

Provisions 34.3 29.5 33.6 27.6 32.4

NPL Ratio 4.4% 3.5% 4.3% 4.1% 4.6%

NPL Coverage Ratio 103.9% 116.1% 108.4% 103.1% 112.1%

NPL ratio stood at 4.4% in Q1 2014 against 3.5% recorded as at 31st December 2013.

Coverage Ratio of 103.9% in Q1 2014 from 116.1% in FY 2013.

Comments

37

Group Key Performance Metrics – Q1 2014

Q1 2014

FY 2013

9-M 2013

H1 2013

Q1 2013

Net Interest Margin (NIM) 7.4% 8.1% 8.6% 8.8% 8.8%

Cost of Risk 2.7% 3.5% 3.4% 3.1% 2.1%

Cost of Funds 3.3% 3.4% 3.4% 3.5% 3.6%

Loan-to-Deposit Ratio 60.6% 59.6% 67.4% 64.0% 63.2%

Capital Adequacy Ratio (CAR) 17.4% 17.3% 17.1% 16.5% 16.3%

Liquidity Ratio 37.3% 41.8% 36.7% 48.2% 46.9%

Cost to Income Ratio 62.0% 60.3% 58.9% 59.1% 60.7%

Earnings per share (annualized) 232K 197K 185k 175k 174k

ROE 23.6% 23.0% 22.4% 22.1% 22.5%

The Group Net Interest Margin (NIM) decreased to 7.4% in Q1 2014 from 8.1% in FY 2013 due to impact of 75% CRR charge on public sector funds.

Comments

38

Outline

• Executive Summary (by Dr. Alex Otti, GMD)

• Strategy & Business Update (by Dr. Alex Otti, GMD)

• FY 2013 Financial Performance (by Abdulrahman Yinusa, CFO)

• Q1 2014 Financial Performance (by Abdulrahman Yinusa, CFO)

• Concluding Remarks (by Dr. Alex Otti, GMD)

39

Concluding remarks

The tight monetary policy stance of the Central Bank is expected to continue in 2014. This should

restrain the earnings capability of Banks. However, we are determined to deliver on our profit

guidance in 2014.

The recent rebasing of Nigeria’s GDP has revealed more sectors with compelling growth dynamics

and opportunities. We will continue to leverage on our existing relationships to explore these

opportunities in 2014 and beyond.

The Group’s financial performance for FY 2013 and Q1 2014 is a reflection of our unfettered

commitment to growing shareholder value through technology driven banking solutions.

We will sustain our retail banking leadership as we continue to offer unparalleled customer

experience through safe and convenient delivery channels.

We remain on course towards deploying additional capital from the debt/equity market to

support our rapidly expanding businesses. In this regard, we are currently assessing the pulse of

the international debt market as well as the local equity market or possible raising of

debt/equity capital at the appropriate time.

40

Thank You