Investor Behavior - Actuarial Research Foundation

46

Risks In Investment Accumulation Products: Insights From Investor Behavior Foundation Symposium New York City January 14, 1999 by Nino Boezio

-

Upload

nino-boezio -

Category

Documents

-

view

155 -

download

0

Transcript of Investor Behavior - Actuarial Research Foundation

Risks In Investment Accumulation Products: Insights From Investor

BehaviorFoundation Symposium

New York CityJanuary 14, 1999by Nino Boezio

AgendaI - Why Study Investor Behavior?

– Current Investment Theory– Behavioral Finance

II - Framework Of StudyIII - General FindingsIV - ApplicationsV - Conclusions - Future Direction

Why Study Investor Behavior?“Without due recognition of crowd-thinking

(which often seems crowd madness) our theory of economics leave much to be desired.”

- Bernard M. Baruch (1932)

Why Study Investor Behavior?• “History repeats itself” - Phillip Guedalla• “If past history was all there was to the

game, the richest people would be librarians” - Warren Buffett

• History does not repeat itself but it does rhyme - Mark Twain

• Financial markets, unlike other areas, have been least studied for disaster prevention -Dr. Ron Dembo, Algorithmics

Why Study Investor Behavior?• Fundamental analysis is deficient in

explaining market activity completely, especially in shorter-term

• Certain events cannot be explained satisfactorily on a rational basis alone e.g. market undervaluation before 1980s, severe market corrections

• Understanding behavior will help us understand anomalies, booms & panics

Why Study Investor Behavior?Knowledge of how investors make decisions

help us understand:• What can go wrong with the current

investment management process• What errors and misjudgements do

investors make• When will consumers/investors buy

more/less of a product or decide to sell?

Prevailing Investment Theory

Current Investment TheoryCapital Asset Pricing Model (CAPM)• Rp = Rf + b (Rm - Rf)• investors risk averse - prefer smaller

variance for comparable levels of return• control risk via diversification• similar investment horizons• similar views on variance (not necessarily

the mean)

Current Investment TheoryCAPM Continued:• investors able to lend or borrow at

prevailing risk free rate and can sell short without restriction

• able to commit virtually any desired amount of funds without affecting price or return of any investment

(William Sharpe, “Capital Asset Pricing In A Theory Of Market Equilibrium Under Conditions Of Risk”, The Journal Of Finance, 1964)

Current Investment TheoryWhy do investors trade?• Risk/ return preferences are constantly

changing• Investors are also responding to new events• Events occur in random fashion, and are

independent of each other

Current Investment TheoryRandom Walk Hypothesis• the efficient marketplace is dominated by a

large number of rational, profit seeking, risk-averting investors

• information is quickly available & incorporated in prices

Current Investment Theory• Semistrong form of market efficiency

suggested - market reflects historical trading activity and public information (not private)

• “Market starts anew each day”- Adam Smith

Assuming investors are rational means that all behavior is reduced to a mathematical optimization problem (DeBondt)

Behavioral Finance• Identification of mistaken analyses and

biases made by investors• Investors not perfectly rational, as

foundations of modern finance assume• Does not reject fundamental analysis &

consumer behavior, but adding investor psychology to the list of factors

Investment Industry• Increasingly quantitative & short-term• Harder to beat the benchmarks - loser’s

game/ indexing?• Pressure building on management fees• Giving investors/ consumers what they want• Always looking for the winning “edge”• Industry changes mainly when necessary

The Investor Behavior Study -Research Of Literature

Investor Behavior StudyStudy Parameters - General Emphasis• Long-term rather than short-term behavior• Observed instead of hypothetical/

theoretical• Research which not mathematically driven

or based on technical analysisNot always exclusive since some inclusions

could stimulate further interest or discussion

Investor Behavior StudyRelatively easy to venture into other areas due

to an overlap but mostly avoided:• “mainstream” psychology• marketing/ advertising & consumer

behavior• general investment theory & portfolio

management• economics

Investor Behavior Study - Results• Most comprehensive study we are aware of• Retained experienced research consultant

(Teresa Croscup)– seven months of full-time research– approximately 1,000 article citations & 85-90%

collected– insights into copyright and legal issues– cataloging system incorporated, also by subject– software advice - for subject search, additions

Study - Investor Behavior Content

• A good synopsis of investor behavior research to the present

• Annotated bibliography completed & availability of articles indicated

• On Society of Actuaries website• Still some stones unturned -- areas for

further research• Includes some material on other areas (next

slide) for purposes of discussion

Study - Content Other Than Investor Behavior

Tax Effects Speculation MarketVolatility

EarningsForecasts

RiskAversion

DividendPolicy

FinancialReporting

HerdingMutualFunds

OpportunityCost

PensionFunds

TimeConstraints

PortfolioMix

CapitalBudgeting

SocialInvesting

IPOs

Investor Behavior -Observations Of Interest

Prospect Theory(Kahnehan & Tversky)

• Emotion destroys self-control which is required for rational decision making

• Investor frequently unable to fully comprehend what dealing with

• Asymmetry in taking risk, which is contrary to rational behavior

• Risk averse in gains, risk seeking in losses (next example)

Prospect Theory - Example (Tversky)

• Decision I– A. a sure gain of $240– B. a 25% chance to gain $1,000

• Decision II– C. a sure loss of $750– D. a 75% chance to lose $1,000

Prospect Theory - Example (Tversky)

• Given choice between A & B, 84% of participants choose A

• Given choice between C & D, 87% of participants choose D

• In combination, 73% chose A & D, 3% chose B & C

Prospect Theory - Example (Tversky)

• But in aggregating:– A & D = 25% chance of gaining $240 and a

75% chance of losing $760– B & C = 25% chance of gaining $250 and a

75% chance of losing $750• A & D inferior to B & C• People pay a premium for a sure gain, and

pay a premium to avoid a sure loss

Other Select Behavioral Traits• Mental accounting, overconfidence (Tversky)• Loss aversion, endowment theory, status

quo bias, pain of regret (Tversky, Kahneman, Knetsch)

• Regret aversion (Larrick, Boles)• Barn door closing, herd migration (Patel,

Zeckhauser, Hendricks)• Representativeness heuristic - a good stock

is a stock of a good company (Statman)

Investor Choice• Even though equities outperform bonds in

long-run, investors still include bonds in portfolio since:– care what happens in short-term– dislike loss in value more than like rise in value(Bernartzi, Thaler)

• More frequent valuations require more bonds (Bernartzi, Thaler)

Investor Choice• Evaluate stocks as if one year horizon,

otherwise equity premium too high based on risk averseness alone (Bernartzi, Thaler)

• More willing to accept risk if evaluate risks less often (Thaler, Tversky, Kahneman, Schwartz)

• Prefer less ambiguity (Curley, Yates, Frank, Abrams)

Investor Choice• Most important factor influencing investor

behavior is the recent past e.g. news, earnings, trends (Pennar)

• Average person is psychologically predisposed to lose money (Green)

• Nature of human behavior is to try to escape discipline (Epstein)

General Market Behavior• Serial market correlation i.e. trend• Stock prices have a memory (DeBondt)• US & Canadian equity markets - 1000 day

(4 year) memory, German equity markets 6 year memory (Ed Peters, PanAgora Asset Mgmt.)

• Investors think linearly, so fail to respond to trend change (Dreman)

• Market, like other areas, move in cycles

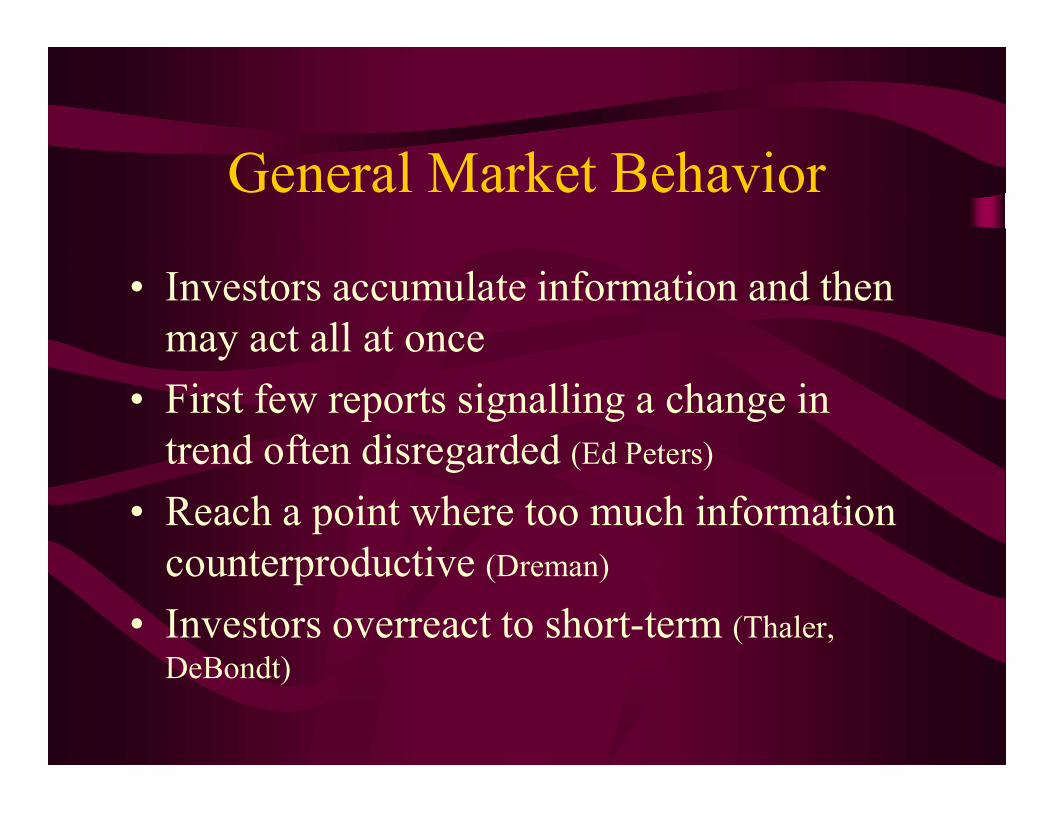

General Market Behavior• Investors accumulate information and then

may act all at once • First few reports signalling a change in

trend often disregarded (Ed Peters)• Reach a point where too much information

counterproductive (Dreman)• Investors overreact to short-term (Thaler,

DeBondt)

General Market Behavior• The longer that investors sustained to a

trend, the more vulnerable to an adverse, large, unanticipated trend reversal

• Markets highly correlated in panics• Circuit breakers may work opposite effect • Foreigners can unnecessarily incite a crisis,

since less informed• Under fear, liquidity diminishes

General Market Behavior• Investors believe what want to believe, and

hard to change • Private investors trade mutual funds like

they used to trade stocks and hold less than 3 years (John Bogle, Vanguard)

• Future cash flows into equity & mutual funds contingent on recent past performance

The Learning Process• Students bid up prices to bubbles the first

time around, but learned from the mistake (Gallant)

• Experienced commodity and stock traders much less biased (Anderson, Sunder)

Bubbles, Panics, Crises & Catastrophes

• Investors see hazards where do not exist, and overlook hazards that do exist (Curran)

• Base risk on events which most available to memory, fear and seduction (Curran)

• Examples of manias, panics: tulipmania, German hyper-inflation of 1920s, stock market crashes, bank runs, internet?

• Bubbles created by uninformed investors entering the market (Rappaport, White, Renshaw)

Bubbles, Panics, Crises & Catastrophes

• Behavioral trends can continue for quite some time

• Identifying manias can be subjective• Herd creates opportunities, but can be

dangerous & lonely (Norton)

Speculation• Gamblers are biased - see sequences e.g.

roulette wheel, dice (Keren, Lewis)• Stocks, futures & options offer same fast-

paced action & potential for high payoffs as do casinos & racetracks (Williams)

• Many aggressive traders are really gamblers (Williams)

• Gamblers of higher income & social class enter financial markets instead (Williams)

Applications &Areas For Further Study

ApplicationsCorporate Governance - immediate & direct

application. Examples:– Assist in review of corporate governance

guidelines– Assist in clarifying a Board’s role as overseer– Apply to investment managers - identify biases– Re-evaluate paradigms e.g. $US vs. Yen, small

vs. large cap (horizon)

Applications• Better product design

– risk management features– marketing approach (framing)– change product perceptions of risk/ reward

(mental accounting, compartmentalization)– perception of safety of institution– corporate response to each product’s investors

may need to be different, and re-evaluated periodically

Current Limitations• Current uses may be more defensive than

offensive - the loser’s game• Uses may still be subjective, and need to

move from observed to practical application• May need further developments, otherwise

may go the way of chaos theory• Statistical studies on expected performance

enhancement lacking

Areas For Further Study• Require a framework such as a behavioral

CAPM (Thaler)– Traditional CAPM: Rp = Rf + b (Rm - Rf) – Use a model such as Arbitrage Pricing Theory?

Involved multiple b in an equation which included: (1) inflation (2) industrial production (3) risk premium (4) interest rate term structure.

(Stephen Ross, “The Arbitrage Theory Of Capital Asset Pricing” Journal of Economic Theory, Dec. 1976)

Areas For Further Study• Need a benchmark of rationality (Brock)

– Use traditional “fundamental” valuation measures e.g. P/B, P/E, interest rates, dividend policy?

– “Greenspan” model (i.e. E/P vs 10 year bond yield)?

• Behavior research may highlight what people do, not always why (i.e. motives)

Conclusions• Understanding prior biases can lead to

improved product design and increased sales, higher customer retention

• Investor past experience with a product will improperly bias attitude towards the product going-forward

• Investor’s past market experience important in determining level of speculative attitude

Conclusions• Institutional attitude towards a product’s

investors may need to be more fluid• Application of principles a deviation from

current industry thinking• Current environment will determine what

investors want - may require frequent changes in products offered

• There may be multiple behavioral elements at work

Risks In Investment Accumulation Products: Insights From Investor

BehaviorFoundation Symposium

New York CityJanuary 14, 1999by Nino Boezio