Investments in Associates: IAS 28. JOIN KHALID AZIZ ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM. ...

26

Investments in Associates: IAS 28

-

Upload

randall-kennedy -

Category

Documents

-

view

224 -

download

3

Transcript of Investments in Associates: IAS 28. JOIN KHALID AZIZ ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM. ...

Investments in Associates: IAS 28

JOIN KHALID AZIZ

ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM.

FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA.

COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA.

CONTACT: 0322-3385752 0312-2302870 R-1173,ALNOOR SOCIETY, BLOCK 19,F.B.AREA,

KARACHI, PAKISTAN.

3

Investments in Associates

Related standards IAS 28 Current GAAP comparisons Looking ahead End-of-chapter practice

4

Related Standards

IAS 27 Consolidated and Separate Financial Statements IAS 36 Impairment of Assets IAS 39 Financial Instruments: Recognition and Measurement

5

IAS 28 – Overview

Objective and scope Application of the equity method Disclosure

6

IAS 28 – Objective and Scope

Accounting requirements for investments in associates unless entity is preparing separate financial statements under IAS 27

Associates an entity over which an investor has significant influence, but which is not a

subsidiary or an interest in a joint venture may be an unincorporated organization such as a partnership

Exclusions from complying with IFRS: investments in associates held by venture capital organizations, mutual funds,

unit trusts, similar organizations

These investments are accounted for at FVTPL under IAS 39

7

IAS 28 – Objective and Scope

Significant Influence power to take part in the financial and operating policy decisions of the investee but not to the extent

of having control or joint control usually when holding, directly or indirectly, 20% to 50% of the voting power of another entity equity method of accounting required for investments in associates

Control a higher level of power exists when an investor can govern the financial and operating policies of an investee and through this

obtain benefits from its activities

8

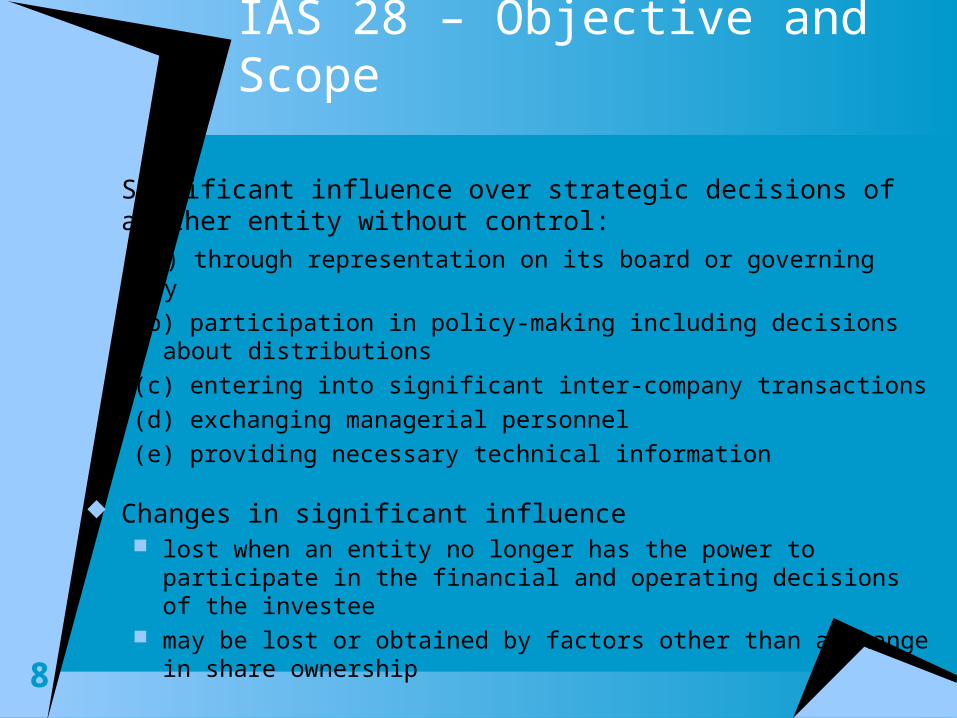

IAS 28 – Objective and Scope

Significant influence over strategic decisions of another entity without control:

(a) through representation on its board or governing body

(b) participation in policy-making including decisions about distributions

(c) entering into significant inter-company transactions

(d) exchanging managerial personnel

(e) providing necessary technical information

Changes in significant influence lost when an entity no longer has the power to participate in the financial and

operating decisions of the investee may be lost or obtained by factors other than a change in share ownership

9

IAS 28 – Objective and Scope

Equity Method of accounting for investments

investment originally recognized at cost adjusted after acquisition for the investor’s share of the post-acquisition changes in the investee’s book value

or net assets investor’s share of investee’s profit or loss is recognized in the profit or loss of the investor distributions from the investee reduce the carrying amount of the investment

Benefits of the equity method

better information in the statement of comprehensive income about the investor’s (and associate’s) performance than recognizing the dividend received

if investor exercises influence that is beneficial to the investee, it recognizes the positive effect on the investee’s profit in its own profit and loss

10

IAS 28 – Application of the Equity Method

Exceptions to applying the equity method for investments in associates

1. the investment is classified as held for sale

2. the investor’s parent company is exempt from preparing consolidated financial

statements

3. the investor itself meets all the same criteria in 2 above that exempt a parent

from preparing consolidated statements

The equity method is often called one-line consolidation procedures are similar to those used to account for acquisition of a subsidiary and for subsequent

consolidation procedures in IAS 27 both methods are concerned with accounting for the investments as part of the reporting entity rather

than as passive holdings

11

IAS 28 – Application of the Equity Method

At Acquisition investor prepares an analysis of the purchase cost investor identifies any difference between the investor’s cost and its share of the fair value of the associate’s

identifiable net assets at acquisition as goodwill

Goodwill not recognized separately from the investment itself represents a portion of the investment’s carrying amount is not amortized if negative, is recognized in the investor’s profit or loss in the year of acquisition

Associate's Fair Value Differences difference between fair values and carrying amounts on the investee’s books explains another portion of the purchase cost of the investment investor’s share of these differences are amortized as the underlying assets are realized and liabilities are settled by

the associate

12

IAS 28 – Application of the Equity Method

13

IAS 28 – Application of the Equity Method

After Acquisition As associate earns a profit -- its net assets increase

the investor recognizes its share of the profit and increases the carrying amount of the investment for its share of the increase in the associate’s net assets

Fair value differences not recognized in the associate’s records not amortized in the profit or loss that the associate reports are amortized by the investor as they are included in the investment account balance usually has the effect of reducing the investment income reported

14

IAS 28 – Application of the Equity Method

Dividends as associate declares/pays dividends, its net assets decrease investor recognizes its share of the reduction as the dividend is received

This entry reflects the conversion of the investment into cash by the investor

Adjustments needed each period elimination of profits and losses on intercompany transactions between the investor and the associate for upstream (associate to investor) and downstream (investor to associate) transactions

the investor’s share of any unrealized profits and losses are eliminated with adjustments to the investment and the investment income accounts

15

IAS 28 – Application of the Equity MethodOther Adjustments investor adjusts investment account and its OCI or other equity account for its share of

associate’s OCI and changes in other equity accounts investor’s share of associate’s losses is more than the carrying amount of the investment

continue to recognize losses and resulting liability to extent investor has legal or constructive obligations to make payments on behalf of associate

Other Issues associate’s accounting policies are required to be the same as those of the investor, otherwise

they are conformed before its financial statements are used in the equity method associate’s financials must be dated no more than three months from the investor’s reporting

date, adjusted for significant transactions and events that occurred in the intervening period

JOIN KHALID AZIZ

ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM.

FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA.

COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA.

CONTACT: 0322-3385752 0312-2302870 R-1173,ALNOOR SOCIETY, BLOCK 19,F.B.AREA,

KARACHI, PAKISTAN.

17

IAS 28 – Application of the Equity MethodImpairment Losses

investment account reduced by investor’s share of losses reported by associate

investor applies IAS 39 to determine whether an impairment loss carrying amount of investment as a whole is compared with its recoverable

amount the higher of value in use and fair value less selling costs

impairment loss is not allocated to specific assets underlying the investment investment tested for impairment as a single asset impairment loss may be reversed in the future

18

IAS 28 – Application of the Equity Method

Loss of Significant Influence

When investor ceases to have significant influence over an associate

Unless associate becomes a subsidiary or joint venture, the investment is accounted for under IAS 39 investment that remains is remeasured at its fair value proceeds on disposal are recognized difference between total of these two amounts and carrying value of investment when

significant influence is lost is recognized in profit or loss

Amounts remaining in entity’s OCI attributable to the associate account for as if associate had disposed of the related assets/liabilities

Amounts are reclassified to profit or loss if that is what associate would have done on disposal

IAS 28 – Disclosure

Investments in associates under equity method reported as non-current assets

Disclose

(a) carrying amount of investments

(b) investor’s share of profit or loss for the period

(c) investor’s share of any discontinued operations of associates, report separately in discontinued operations

(d) investor’s share of changes recognized in OCI by associate, report in OCI

(e) information about any related contingent liabilities

19

IAS 28 – Disclosure

Other information required info that provides reader with a better understanding of circumstances and

financial position of associates

Examples

• summarized financial information about associates

• reasons supporting use of equity method with holdings of < 20%

• reasons why any associates not accounted for using equity method

20

Current GAAP Comparisons

Main differences – impairment requirements- Under IFRS, impairment is when recoverable amount < carrying

amount; Canadian GAAP says when a significant/prolonged decline in value below carrying amount

- Under IFRS, loss = excess of carrying amount above recoverable amount (based on discounted present values); Canadian GAAP loss is excess of carrying amount above undiscounted future cash flows

- Under IFRS, loss is reversed when recoverable amount changes; Canadian GAAP does not allow reversal

22

Looking Ahead Early 2008

minor amendments made to IAS 28 to reduce choice and exemptions – no change to major concepts and how equity method is applied

Topic not listed on current IASB project agenda no significant changes expected in foreseeable future work on IAS 27 may have implications for IAS 28

New term being considered = significant involvement Not yet determined how this term is related to “significant influence”

23

End-of-Chapter Practice

24

End-of-Chapter Practice

25

End-of-Chapter Practice

JOIN KHALID AZIZ

ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM.

FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA.

COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA.

CONTACT: 0322-3385752 0312-2302870 R-1173,ALNOOR SOCIETY, BLOCK 19,F.B.AREA,

KARACHI, PAKISTAN.