Investments For Life

31

Investing For a Lifetime TM

Transcript of Investments For Life

Investing For a Lifetime

TM

TM

Principles from Behavioral Finance

Investors are over-confident(think they are better at making choices than they really are)

They believe in winning streaks and are impressed by short-term success

Confuse familiarity with real knowledge and over-react to both good & bad news

Most are trapped in a cycle of fear & greed

Where Investors go Wrong:

Source: The Economist, “Law of Averages” July 5, 2003

Typical Behavior

TM

Requires a focus/discipline

Risk Management

Financial Plan

Asset Allocation

Long term focus

Scenario approach

Customized portfolio

Rational expectations

Managing Money

Arbitrary

Focus on reward

No plan

Performance Driven

Responsive to noise

Betting on a single outcome

Follow the crowd

Adaptive expectations

Make Money

There is a difference

Financial Planning Discipline

TM

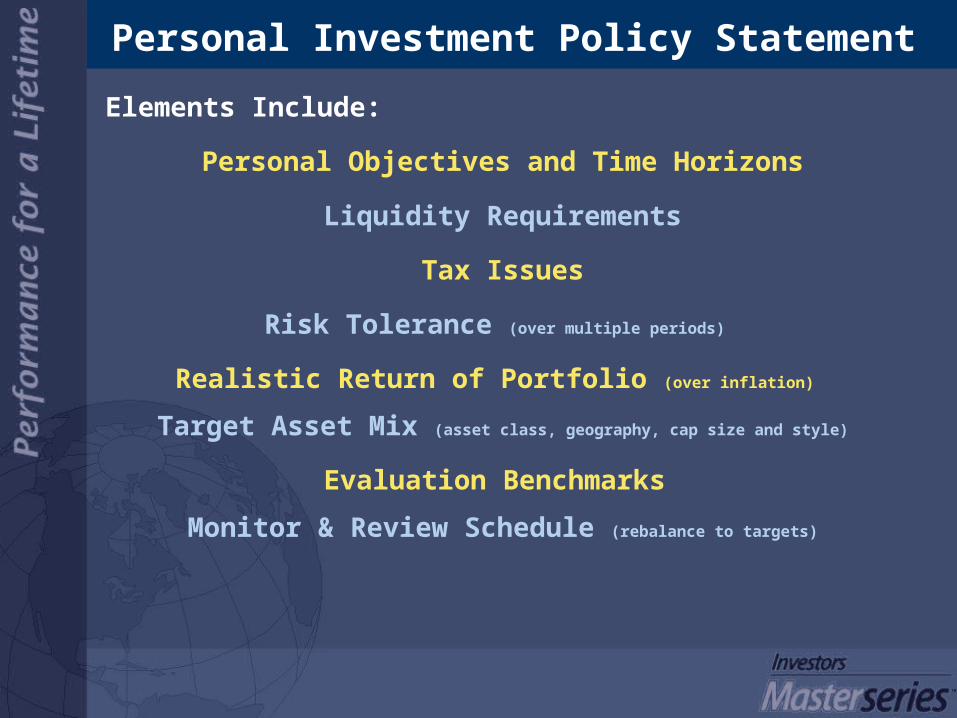

Personal Investment

Policy Statement

. . . your personal “roadmap” to successful

investing.

Step 1. The Foundation

Investing for a lifetime requires a...

TM

Elements Include:

Personal Objectives and Time Horizons

Liquidity Requirements

Tax Issues

Risk Tolerance (over multiple periods)

Realistic Return of Portfolio (over inflation)

Target Asset Mix (asset class, geography, cap size and style)

Evaluation Benchmarks

Monitor & Review Schedule (rebalance to targets)

Personal Investment Policy Statement

TM

Focus and Commitment

. . . to help with decision-making in all

market conditions

Step 2. The Discipline

Investing for a lifetime also requires...

TM

Focus OnFocus On

Asset Allocation

Staying Invested

Multi-Dimensional Diversification

Realistic Returns

AvoidAvoid

Performance ChasingConcentrating RiskShort Term NoiseThe Media Hype

Principles of Investing

TM

Asset Allocation is the Critical Factor

More than 90% of a portfolio’s variability

depends on asset mix

Market Timing

2.1%

Other Factors

1.8%

Stock Selection

4.6% Asset Allocation

91.5%

Long-term portfolio performance is most

influenced byasset allocation

and less influenced bymarket timing and

stock selection

Source: Brinson, Singer, Beebower Study;Financial Analysts Journal, Feb. 91

Focus on Portfolios

TM

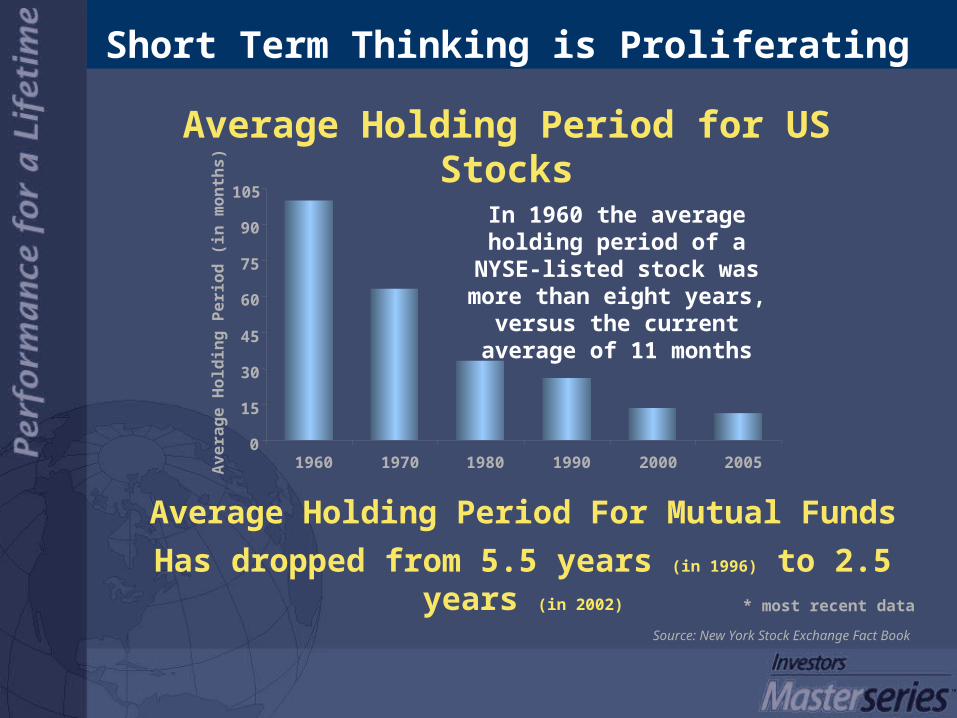

Average Holding Period for US Stocks

Source: New York Stock Exchange Fact Book

Short Term Thinking is Proliferating

In 1960 the average holding period of a NYSE-listed

stock was more than eight years, versus the current

average of 11 months

0

15

30

45

60

75

90

105

1960 1970 1980 1990 2000 2005

Av

era

ge

Ho

ldin

g P

eri

od

(in

mo

nth

s)

Average Holding Period For Mutual Funds

Has dropped from 5.5 years (in 1996) to 2.5 years (in 2002)

* most recent data

TM

1 208% 1413 -71%

2 115% 1408 -49%

3 105% 1406 -43%

4 93% 1401 -36%

5 93% 1395 -34%

6 92% 1402 -37%

7 90% 1341 -26%

8 87% 1309 -24%

9 84% 1370 -29%

10 79% 1347 -27%

The First Shall Be Last . . .

Reversion to the Mean in Fund Performance

Rank Ann.Ret. Rank Ann.Ret.

1998-99 2000-01

Source: Bogle Financial Center1,413 U.S. Equity funds with $100 million + in assets

TM

-5

0

5

10

15

20

25

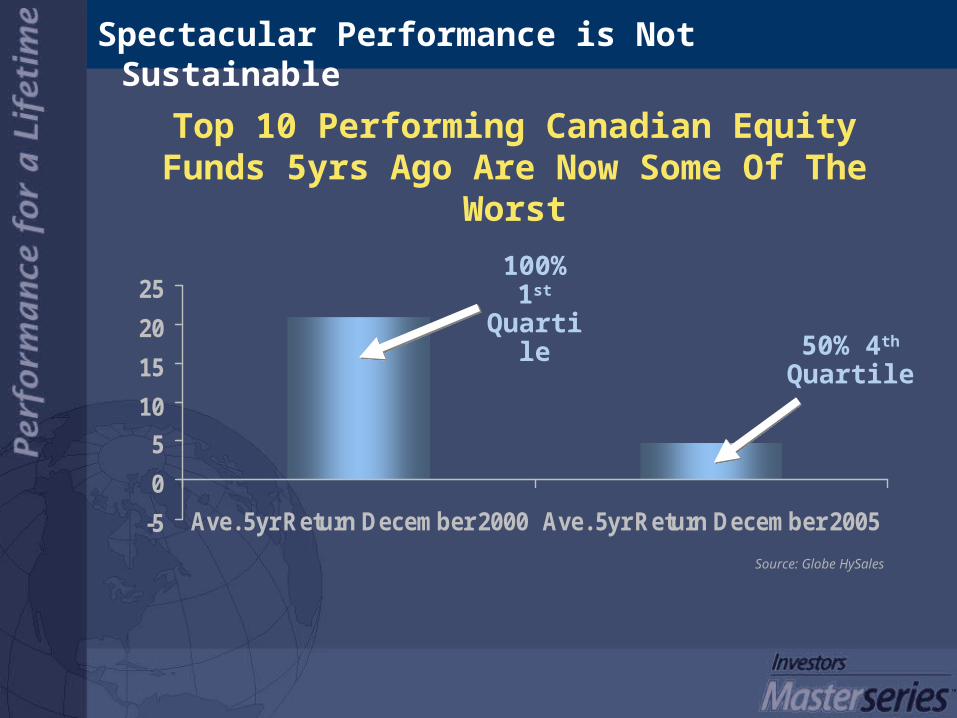

Ave. 5yr Return December 2000 Ave. 5yr Return December 2005

Top 10 Performing Canadian Equity Funds 5yrs Ago Are Now Some Of The Worst

Source: Globe HySales

100% 1st Quartile

50% 4th Quartile

Spectacular Performance is Not Sustainable

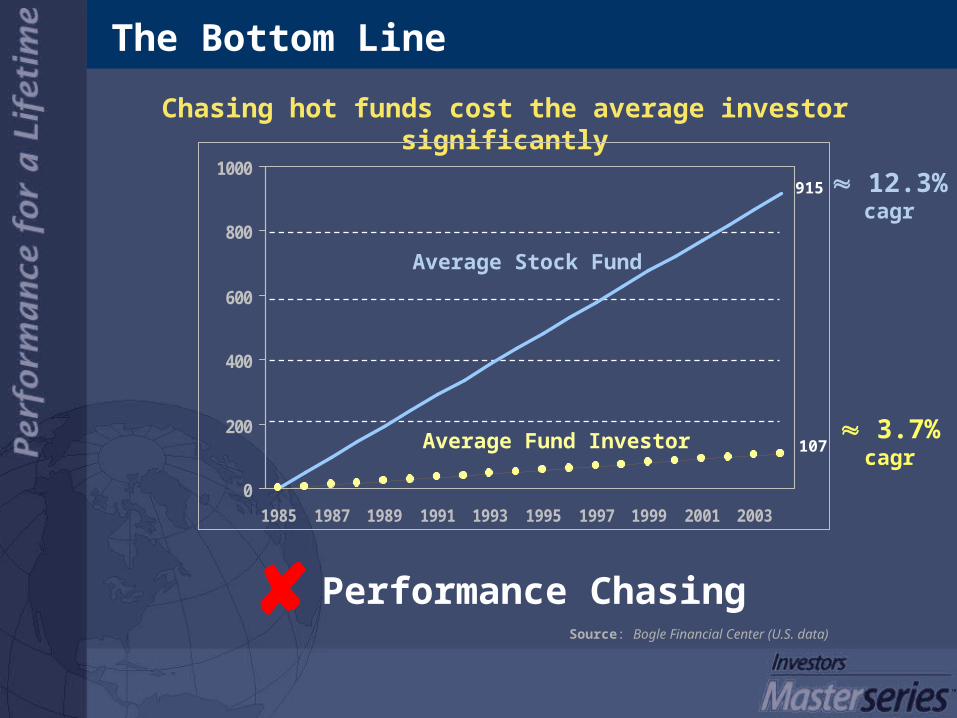

TM

Average Stock Fund

Average Fund Investor

The Bottom Line

3.7% cagr

12.3% cagr

Chasing hot funds cost the average investor significantly

Performance ChasingSource: Bogle Financial Center (U.S. data)

0

200

400

600

800

1000

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

915

107

TM

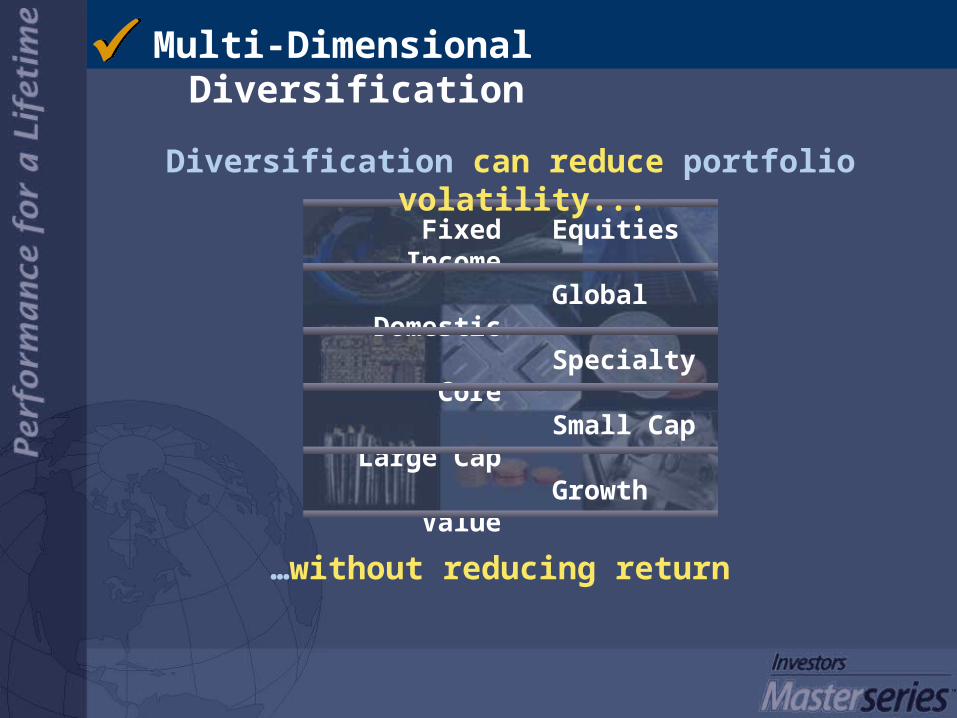

Multi-Dimensional Diversification

Equities

Global

Specialty

Small Cap

Growth

Fixed Income

Domestic

Core

Large Cap

Value

Diversification can reduce portfolio volatility...

…without reducing return

TM

0

1000

2000

3000

4000

Dec-94 Dec-95 Dec-96 Dec-97 Dec-98 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05

S&P/TSX Scotia Universe

Va

lue

of

Inv

es

tme

nt

($)

S&P/TSX vs. Sc.McL. Universe Bond Index

Fixed Income and Equities

Bonds can outperform EquitiesSource: I.G. Investment Management, Ltd.; Scotia Capital; TSE

Annual Returns

S&P/TSXSc.McL. Univ. Bond Index

2001

8.1

1995 1996 1997 1998 1999

14.5 28.3 15.0 -1.6 31.7

20.7 12.3 9.6 9.2 -1.1

2003

26.7

6.7

2000

7.4

10.2

-12.6 -12.4

8.7

2002 2004 14.5

7.2

2005 24.1

6.5

TM

Domestic and Global

Data to December 31, 2005

Performance of 5 Geographic Markets ($Cdn)

Different Markets Outperform Year-to-Year

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005S&P500 33.91 23.36 39.11 37.60 14.14 -5.51 -6.45 -22.72 5.28 3.26 1.62MSCI Europe 18.37 21.48 29.18 37.62 9.33 -4.78 -14.98 -19.03 13.36 12.58 5.98S&P/TSX 14.53 28.35 14.98 -1.58 31.71 7.41 -12.57 -12.44 26.72 14.48 24.13MSCI Emg Mkt -7.74 6.37 -7.74 -20.14 57.34 -27.97 3.63 -6.76 27.87 17.30 30.32MSCI Asia Pac -0.65 -7.91 -23.92 9.81 49.30 -25.61 -15.86 -15.86 15.29 10.44 19.88

Calendar Returns ($Cdn.)

Source: I.G. Investment Management, Ltd.; Bloomberg

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

S&P500$2,726

MSCI Emrg. Mkts. $1,548

MSCI Asia Pac Free $991

MSCI Europe $2,478

S&P/TSX $3,245

TM

Highest Return

1995 1996 1997 1998 1999 2000

Lowest Return

Large Cap and Small Cap

Cdn. Barra Large Cap Growth

Cdn. Barra Large Cap Value

Cdn. Barra Small Cap Growth

Cdn. Barra Small Cap Value

Cap Size Performance Changes Year-to-Year

Source: I.G. Investment Management, Ltd.; Barra

2001 2002 2003 2004 2005 LC

Value15.94

LC Value36.17

LC Value28.65

LC Value-1.58

LC Value2.76

LC Value31.69

LC Value5.06

LC Value-11.49

LC Value29.47

LC Value16.99

LC Value25.58

LC Growth

2.12

LC Growth42.81

LC Growth13.70

LC Growth22.01

LC Growth

3.99

LC Growth

-5.68

LC Growth-21.39

LC Growth-13.08

LC Growth24.07

LC Growth12.07

LC Growth23.44

SC Value23.48

SC Value30.03

SC Value6.91

SC Value12.18

SC Value-22.79

SC Value5.25

SC Value25.24

SC Value2.07

SC Value40.23

SC Value23.52

SC Value20.41

SC Growth13.78

SC Growth33.81

SC Growth39.21

SC Growth

4.62

SC Growth-19.25

SC Growth

3.43

SC Growth

-8.02

SC Growth-12.72

SC Growth47.79

SC Growth11.03

SC Growth15.58

TM

80.00

70.00

60.00

50.00

40.00

30.00

20.00

10.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

Dec-94 Dec-95 Dec-96 Dec-97 Dec-98 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05

Value and Growth

Value Can Outperform

Growth Can Outperform

Canadian Barra Rolling 12 Month Relative ReturnsAs of February 28, 2006

%

Source: I.G. Investment Management, Ltd.; Barra

TM

You Can’t Predict Next Year’s Winner

The Bottom Line

Concentrating Risk

TM

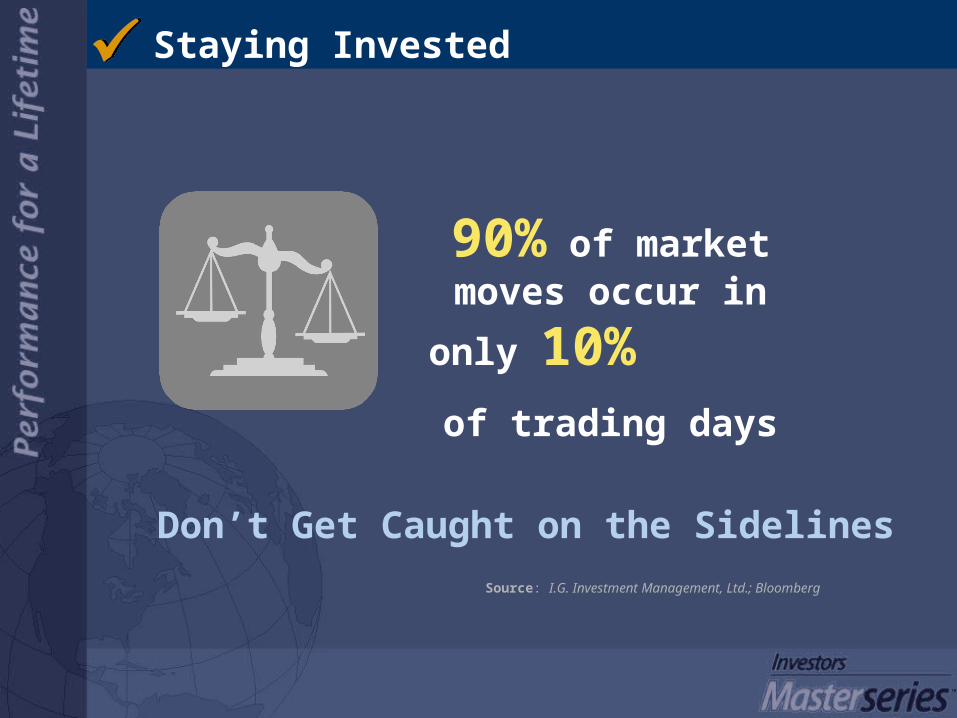

Staying Invested

Don’t Get Caught on the Sidelines

90% of market moves

occur in only 10%

of trading days

Source: I.G. Investment Management, Ltd.; Bloomberg

TM

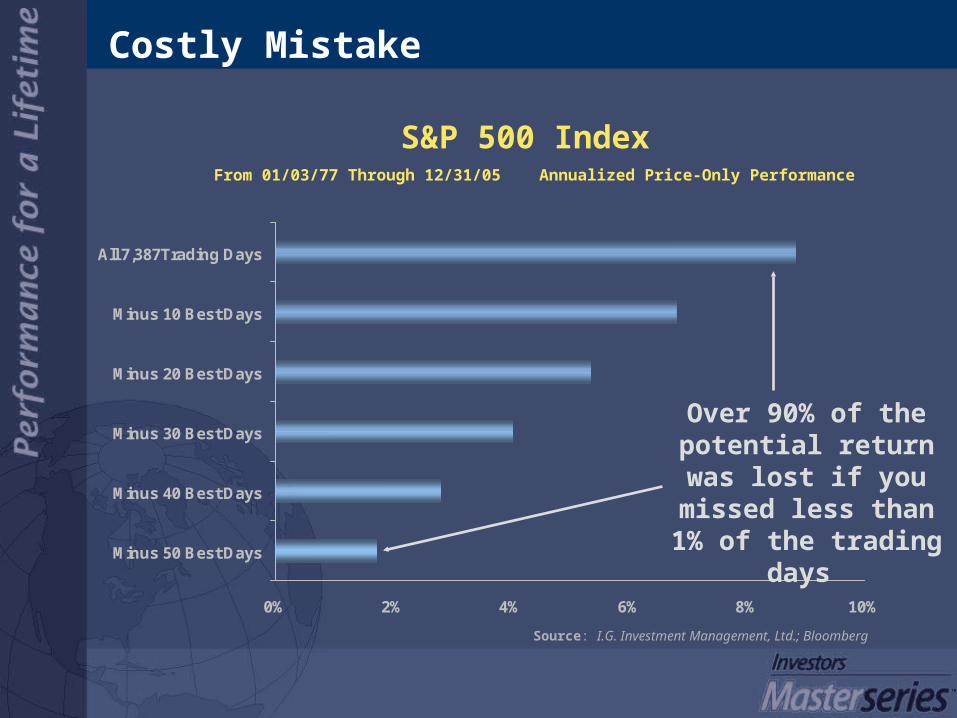

0% 2% 4% 6% 8% 10%

Minus 50 Best Days

Minus 40 Best Days

Minus 30 Best Days

Minus 20 Best Days

Minus 10 Best Days

All 7,387Trading Days

Costly Mistake

S&P 500 Index From 01/03/77 Through 12/31/05 Annualized Price-Only Performance

Over 90% of the potential return was lost if you missed

less than 1% of the trading days

Source: I.G. Investment Management, Ltd.; Bloomberg

TM

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

80

90

100

Average

TSE 300

75% Stocks / 25% L.T. Bonds

Range of Returns (1956 - 2005)

Time Reduces Volatility

1 Year 5 Years 10 Years 20 Years 30 Years3 Years

Holding period to minimize a negative return in the equity

market:

Just over 5 years

Source: I.G. Investment Management, Ltd.; Scotia Capital; TSE

TM

100%

100%

99%

91%

9%

73%

27%

Positive Returns

Negative Returns

707 One-month periods

696 One-Year periods

672 Three-Year periods

648 Five-Year periods

The likelihood of receiving a negative return diminishes as the investment term lengthens.

Since 1962, the TSX has had onlypositive 15 Year returns.

In comparison, since 1947,only 60% of the 673 monthlyreturns were positive.

39%

61%

528 Fifteen-Year periods

588 Ten-Year periods

*Past performance is not indicative of future performance

TSX Composite Total Return

Source: Portfolio Analytics

As of May 2006

TM

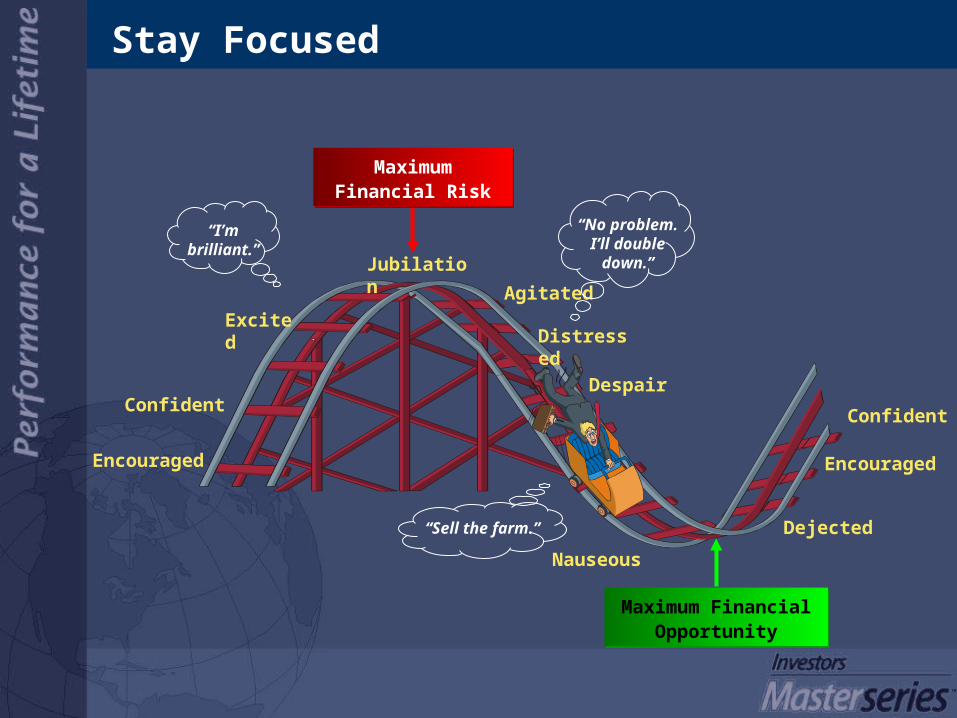

Encouraged

Confident

Excited

Jubilation

Agitated

Distressed

Despair

Nauseous

Dejected

Encouraged

Confident

Maximum Financial Opportunity

Maximum Financial Opportunity

Maximum Financial Risk

Maximum Financial Risk

“I’m brilliant.”

“Sell the farm.”

“No problem. I’ll double

down.”

Stay Focused

TM

Time in the Market creates Wealth

The Bottom Line

Short Term Noise

TM

Realistic Returns

However, we all have a different

propensity for risk

We all have the same propensity for

return

TM

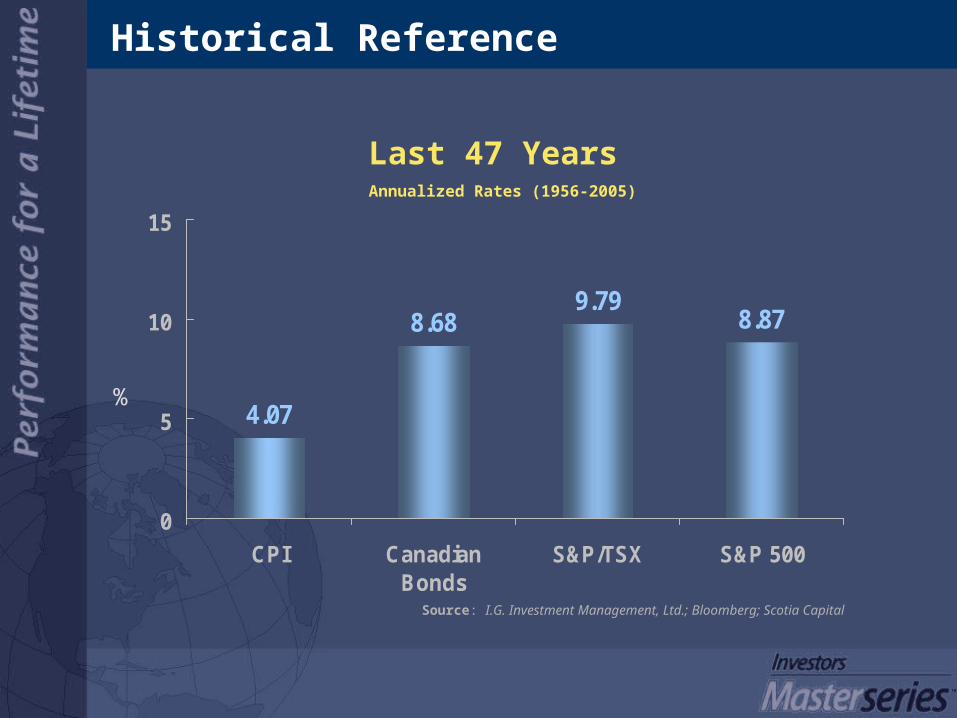

Historical Reference

Last 47 Years Annualized Rates (1956-2005)

Source: I.G. Investment Management, Ltd.; Bloomberg; Scotia Capital

4.07

8.689.79

8.87

0

5

10

15

CPI CanadianBonds

S&P/TSX S&P 500

%

TM

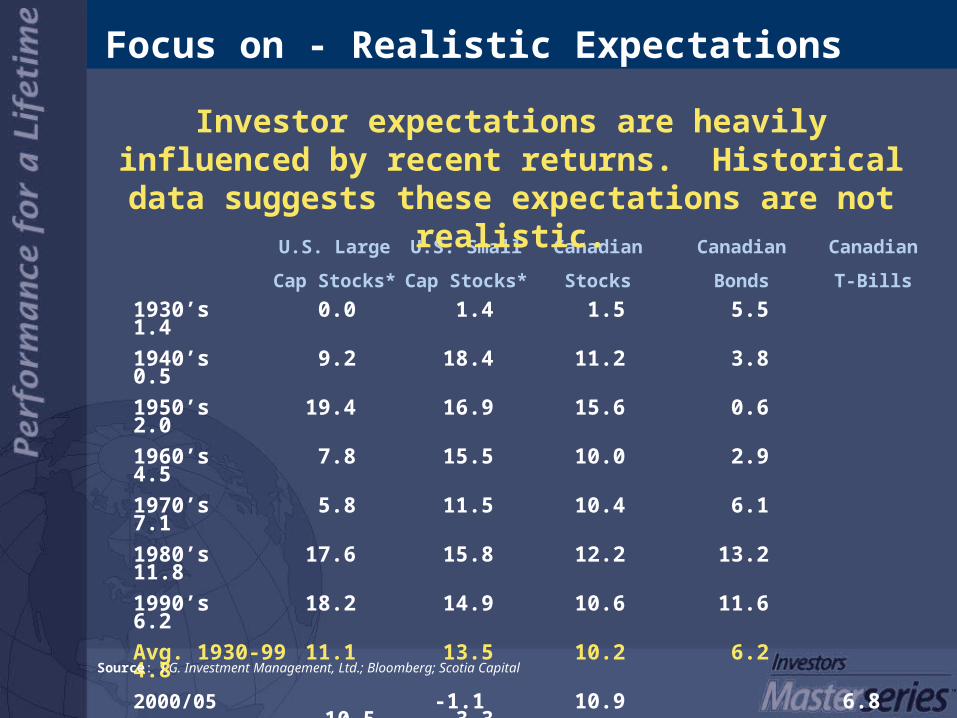

Focus on - Realistic Expectations

1930’s 0.0 1.4 1.5 5.5 1.4

1940’s 9.2 18.4 11.2 3.8 0.5

1950’s 19.4 16.9 15.6 0.6 2.0

1960’s 7.8 15.5 10.0 2.9 4.5

1970’s 5.8 11.5 10.4 6.1 7.1

1980’s 17.6 15.8 12.2 13.2 11.8

1990’s 18.2 14.9 10.6 11.6 6.2

Avg. 1930-99 11.1 13.5 10.2 6.2 4.8

2000/05 -1.1 10.9 6.8 10.5 3.3 *Returns based on U.S. $

U.S. Large U.S. Small Canadian Canadian Canadian

Cap Stocks* Cap Stocks* Stocks Bonds T-Bills

Investor expectations are heavily influenced by recent returns. Historical data suggests these expectations

are not realistic.

Source: I.G. Investment Management, Ltd.; Bloomberg; Scotia Capital

TM

Recap of Important Points

Have a plan and stick to it

Single best determinant of success is the appropriate asset mix

Diversification is a guiding principle

Time in the market…not market timing creates wealth

The challenges are many but none so great as removing the behaviors that negatively impact

the decision-making process

TM

January 1802 - December 2005

Source: “ Stocks for the Long Run”, by Jeremy J. Siegel

(U.S. $)

STOCKS $598,609

BONDS$1150

BILLS$296

GOLD$1.63

DOLLAR $0.06

$0.01

$0.1

$1.

$10.

$100.

$1,000.

$10,000.

$100,000.

$1,000,000.

1801

1811

1821

1831

1841

1851

1861

1871

1881

1891

1901

1911

1921

1931

1941

1951

1961

1971

1981

1991

2001

The “ REAL” Opportunity

TM

‘90% percent of the game is half mental.’

Yogi Berra

TM

Disclaimer

This presentation is published by Investors Group. It represents the views of the investment management team at I.G. Investment Management, Ltd. and is provided as a general source of information. It is not intended to provide investment advice or as an endorsement of any investment. Some of the securities mentioned may be owned by Investors Group or its mutual funds. Every effort has been made to ensure that the material contained in the commentary is accurate at the time of publication, however, Investors Group cannot guarantee the accuracy or the completeness of such material and accepts no responsibility for any loss arising from any use of or reliance on the information contained herein.

Please read the mutual fund's prospectus before investing. Commissions, trailing commissions, management fees and other expenses may be associated with mutual fund investments. There is no guarantee that the fund will maintain its net asset value or that the full amount of your investment will be returned to you. Past performance may not be repeated.

© Copyright 2006 IGM Financial Inc.

™ Trademarks owned by IGM Financial Inc. and licensed to its subsidiary Corporations.

Do not reproduce any part of this presentation without permission.