Investment styles - Marsh & McLennan Companies...Investment Guide . LifeStyle 35 Strategy. If you do...

12

INVESTMENT GUIDE July 2014 MMC UK Pensions Investment styles As a member of a Marsh & McLennan Companies (UK) defined contribution (DC) pension arrangement, your benefits at retirement will depend on how much has accumulated in your Individual Account as well as the type of benefits you choose at retirement. The size of your Individual Account will depend on the level of contributions paid and the growth on your investments. You can choose how your Individual Account is invested based on your personal circumstances and the degree of risk you wish to take. The information contained in this guide provides detail about the investment choices that are effective from August 2014. You will have two options for investing your Individual Account: Making your own selection (“FreeStyle”): you can select your own funds from the range of options on offer in whatever proportion and for however long you choose; or Following a pre-set strategy (“LifeStyle 35”): this option invests in higher risk, higher potential growth investments while you are some way (35 years or more) from retirement. From 35 years until 5 years from retirement, your individual account is automatically moved into a more diversified range of investments and then during the final years before your planned retirement date, your investments will be moved to lower risk, lower potential growth investments designed to protect the value of your Individual Account. COMPARE LEARN SAVE INVEST REVIEW

Transcript of Investment styles - Marsh & McLennan Companies...Investment Guide . LifeStyle 35 Strategy. If you do...

INVESTMENT GUIDE July 2014

MMC UK Pensions

Investment styles

As a member of a Marsh & McLennan Companies (UK) defined contribution (DC) pension arrangement, your benefits at retirement will depend on how much has accumulated in your Individual Account as well as the type of benefits you choose at retirement. The size of your Individual Account will depend on the level of contributions paid and the growth on your investments.

You can choose how your Individual Account is invested based on your personal circumstances and the degree of risk you wish to take. The information contained in this guide provides detail about the investment choices that are effective from August 2014.

You will have two options for investing your Individual Account:

Making your own selection (“FreeStyle”): you can select your own funds from the range of options on offer in whatever proportion and for however long you choose; or

Following a pre-set strategy (“LifeStyle 35”): this option invests in higher risk, higher potential growth investments while you are some way (35 years or more) from retirement. From 35 years until 5 years from retirement, your individual account is automatically moved into a more diversified range of investments and then during the final years before your planned retirement date, your investments will be moved to lower risk, lower potential growth investments designed to protect the value of your Individual Account.

COMPARE LEARN SAVE INVEST REVIEW

2

Investment Guide

LifeStyle 35 StrategyIf you do not wish to be actively involved in making investment decisions, you may wish to select the LifeStyle 35 strategy.

You should note that the LifeStyle 35 strategy is the default investment option for DC members. This means that if you do not make an investment selection, then any contributions to your Individual Account will be invested using the LifeStyle 35 strategy assuming a target retirement age of 65.

Please note that those members in MMC UK pension arrangements prior to 1 August 2014 and who are within ten years of their target retirement at that date will remain in the current lifestyle strategy, rather than be moved in to the LifeStyle 35 strategy.

The LifeStyle 35 strategy will not necessarily be the most appropriate option for you. For example, if you are intending to retire early, or you intend to keep your Individual Account invested after your target retirement age and defer retiring, it may be that investing using the lifestyle strategy set by the Trustee is not appropriate for you.

The LifeStyle 35 strategy is designed for saving for a level pension at retirement. This type of investment strategy is designed to reduce the level of risk and volatility of investment returns as you approach retirement, so it does have wider application too.

The chart below provides an overview as to the structure of the ‘LifeStyle 35’ option.

Your target retirement age is the age by which your funds will have been switched entirely out of the LifeStyle Equity Fund and Diversified Growth Fund into the Fixed Interest Bond Fund and Cash Fund. The default target retirement age is age 65, but you can choose a different age by contacting the MMC UK Pensions Administrator. More information about this is available at www.pensions.uk.mmc.com.

Invests in equities in earlier years seeking growth in a volatile

asset class

Equities then DGF phased out approaching retirement into traditionally less volatile funds in order to protect the value of

your Individual Account

Phases in to DGF to

help reduce expected

volatility

3

Investment Guide

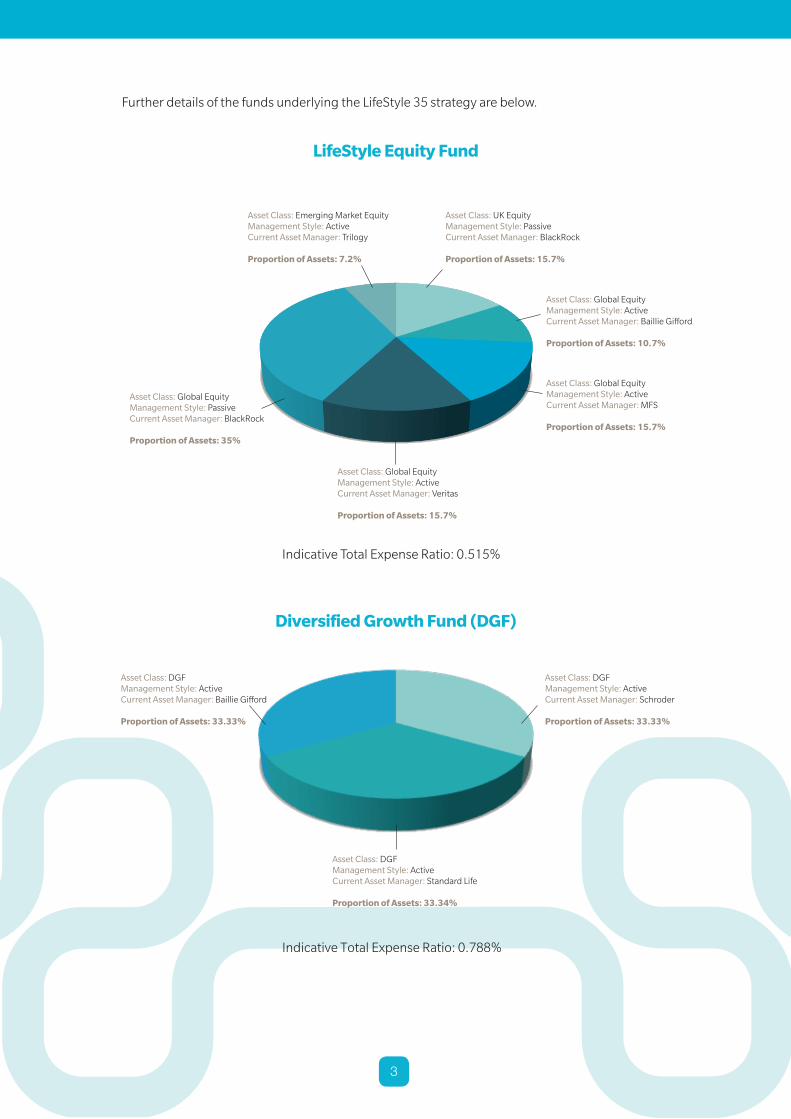

Further details of the funds underlying the LifeStyle 35 strategy are below.

LifeStyle Equity Fund

Diversified Growth Fund (DGF)

Asset Class: Emerging Market EquityManagement Style: ActiveCurrent Asset Manager: Trilogy

Proportion of Assets: 7.2%

Asset Class: UK EquityManagement Style: PassiveCurrent Asset Manager: BlackRock

Proportion of Assets: 15.7%

Asset Class: Global EquityManagement Style: ActiveCurrent Asset Manager: Baillie Gifford

Proportion of Assets: 10.7%

Asset Class: Global EquityManagement Style: ActiveCurrent Asset Manager: MFS

Proportion of Assets: 15.7%

Asset Class: Global EquityManagement Style: ActiveCurrent Asset Manager: Veritas

Proportion of Assets: 15.7%

Asset Class: Global EquityManagement Style: PassiveCurrent Asset Manager: BlackRock

Proportion of Assets: 35%

Asset Class: DGFManagement Style: ActiveCurrent Asset Manager: Schroder

Proportion of Assets: 33.33%

Asset Class: DGFManagement Style: ActiveCurrent Asset Manager: Baillie Gifford

Proportion of Assets: 33.33%

Asset Class: DGFManagement Style: ActiveCurrent Asset Manager: Standard Life

Proportion of Assets: 33.34%

Indicative Total Expense Ratio: 0.788%

Indicative Total Expense Ratio: 0.515%

Investment Guide

4

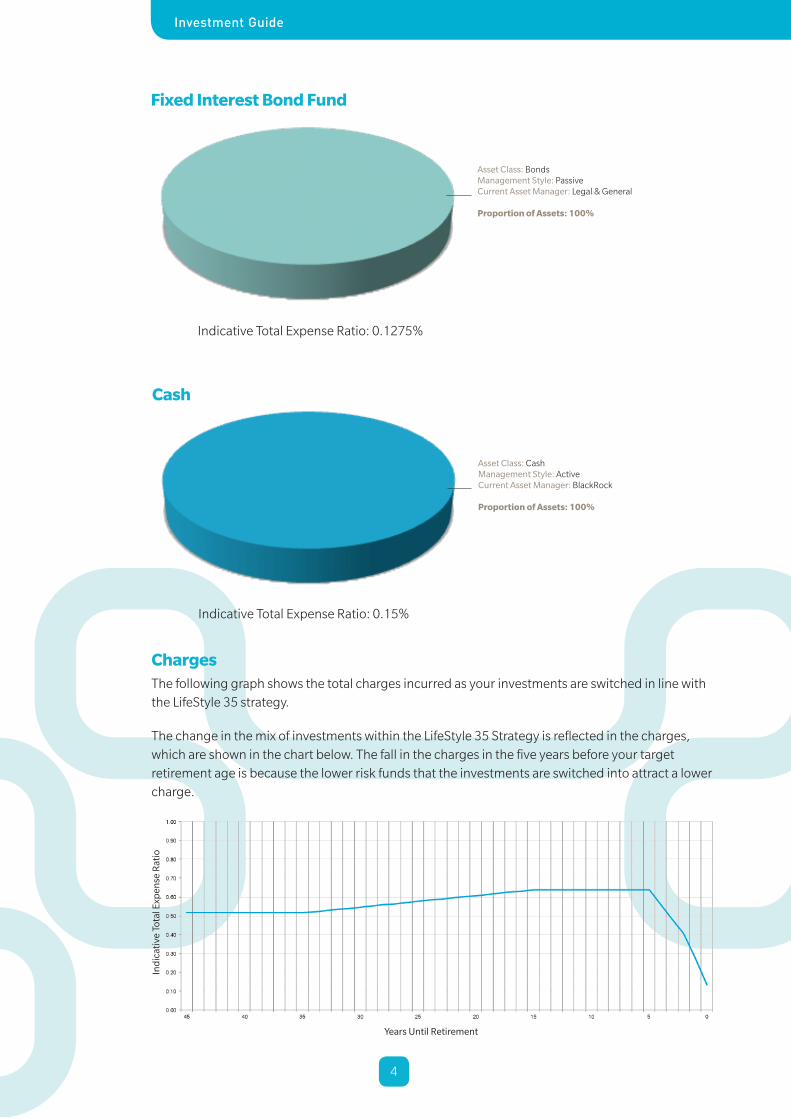

ChargesThe following graph shows the total charges incurred as your investments are switched in line with the LifeStyle 35 strategy.

The change in the mix of investments within the LifeStyle 35 Strategy is reflected in the charges, which are shown in the chart below. The fall in the charges in the five years before your target retirement age is because the lower risk funds that the investments are switched into attract a lower charge.

Ind

icat

ive

Tota

l Exp

ense

Rat

io

Years Until Retirement

Fixed Interest Bond Fund

Cash

Asset Class: BondsManagement Style: PassiveCurrent Asset Manager: Legal & General

Proportion of Assets: 100%

Asset Class: CashManagement Style: ActiveCurrent Asset Manager: BlackRock

Proportion of Assets: 100%

Indicative Total Expense Ratio: 0.1275%

Indicative Total Expense Ratio: 0.15%

5

If you prefer having the option to make your own investment choices, you can choose the FreeStyle option and will be able to select your own investment strategy from the range of funds detailed in the table below.

There will be nine fund options to choose from. The chart below provides an overview of the funds and highlights the level of capital risk / potential return associated with each.

FreeStyle funds

Fund Name Description Indicative Total

Expense Ratio

Capital Risk

Profile

Passive Equities Fund

Aims to achieve long-term capital growth by investing in a range of global equities which will track a chosen index.

0.2000% High

Long Term Growth Fund

Aims to achieve long-term capital growth by investing in a range of asset classes such as UK, overseas and emerging market equities and diversified growth funds.

0.5970% High

Shariah Fund Aims to provide long-term capital growth through investing primarily in a broad range of company shares from around the world, which meet the Islamic investment principles of the underlying fund/s.

0.3550% High / Specialist

Ethical Fund Aims to achieve long-term capital growth through investing primarily in the shares of companies that are selected based on the SRI (socially responsible investing) criteria of the underlying fund/s.

0.2550% High / Specialist

Diversified Growth Fund

Aims to achieve long-term capital growth by investing in a wide range of asset classes with the aim of providing a less volatile (but potentially lower return) than investing solely in equities.

0.7880% Medium

Moderate Growth Fund

Aims to achieve long-term capital growth by investing in a range of asset classes such as UK and overseas equities, diversified growth funds and bonds.

0.3720% Medium

Inflation-Linked Bond Fund

A diverse bond portfolio aiming to match the cashflows from a typical inflation linked annuity product in order to protect the purchasing power of a pension pot in the years up to retirement or to protect against times of stock market volatility.

0.1275% Low

Fixed Interest Bond Fund

A diverse bond portfolio aiming to match the cashflows from a typical traditional level annuity product in order to protect the purchasing power of a pension pot in the years up to retirement or to protect against times of stock market volatility.

0.1275% Low

Cash Fund Aims to achieve capital stability and long-term capital growth through investment primarily in a diversified range of money market instruments and near-cash instruments.

0.1500% Low

Those funds that have a higher potential for return over the long term may also have more volatility in their performance.

All investments carry a level of risk, but there are different types of risk including capital risk, inflation risk and pensions conversion risk (see the Glossary for definitions). You need to decide how much of each type of risk you are prepared to take.

Expected Capital Risk

Exp

ecte

d R

etur

n

Investment Guide

6

Each fund has a specific investment objective and performance target. The Trustee has selected one or more underlying fund manager(s) for each fund. Managers have been chosen for their abilities in a particular specialist area. The Trustee has the flexibility to change the underlying manager(s) at any time without significantly changing the objectives of the fund itself. The advantage of this is that you will be able to choose a fund that will always have the same investment objectives, irrespective of the underlying manager(s).

Further details of the underlying funds are below.

Long Term Growth Fund

The fund aims to achieve long-term capital growth by investing in a range of asset classes such as UK, overseas and emerging market equities and diversified growth funds.

Indicative Total Expense Ratio: 0.5970% LifeStyle Equity Fund(See page 3)

70%

Global Equity (30/70) Currency Hedged Fund

(BlackRock) 100%

Passive Equities Fund

The fund aims to achieve long-term capital growth by investing in a range of global equities which will track a chosen index.

Indicative Total Expense Ratio: 0.2000%

Ethical Fund

The fund aims to achieve long-term capital appreciation through investing primarily in the shares of companies that are selected based on the SRI (socially responsible investing) criteria of the underlying fund/s.

Indicative Total Expense Ratio: 0.2550%

Ethical Global Equity Index Fund

(Legal & General) 100%

Diversified Growth Fund (DGF)

The fund aims to achieve long-term capital growth by investing in diversified growth funds. A diversified growth fund invests across a range of asset classes with the aim of providing a less volatile (but potentially lower return) than investing solely in equities.

Indicative Total Expense Ratio: 0.7880%

Diversified Growth Fund

(Schroder) 33.33%

Diversified Growth Fund

(Baillie Gifford) 33.33%

Diversified Growth Fund

(Standard Life) 33.34%

Moderate Growth Fund

The fund aims to achieve long-term capital appreciation by investing in a range of asset classes such as UK and overseas equities, diversified growth funds and bonds.

Indicative Total Expense Ratio: 0.3720%

Fixed Interest Bond Fund 33.3%

Diversified Growth Fund

33.3%

Passive Equities Fund33.4%

Diversified Growth Fund (See page 3)

30%

7

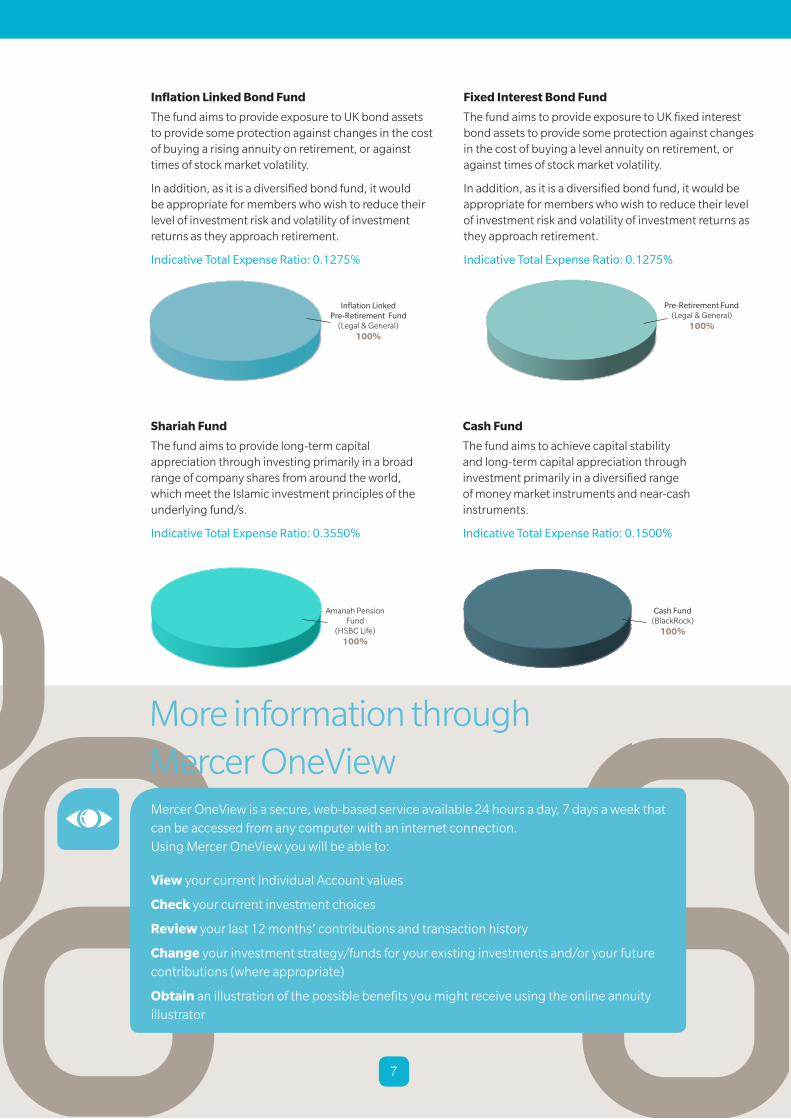

Inflation Linked Bond Fund

The fund aims to provide exposure to UK bond assets to provide some protection against changes in the cost of buying a rising annuity on retirement, or against times of stock market volatility.

In addition, as it is a diversified bond fund, it would be appropriate for members who wish to reduce their level of investment risk and volatility of investment returns as they approach retirement.

Indicative Total Expense Ratio: 0.1275%

Shariah Fund

The fund aims to provide long-term capital appreciation through investing primarily in a broad range of company shares from around the world, which meet the Islamic investment principles of the underlying fund/s.

Indicative Total Expense Ratio: 0.3550%

Cash Fund

The fund aims to achieve capital stability and long-term capital appreciation through investment primarily in a diversified range of money market instruments and near-cash instruments.

Indicative Total Expense Ratio: 0.1500%

Mercer OneView is a secure, web-based service available 24 hours a day, 7 days a week that can be accessed from any computer with an internet connection. Using Mercer OneView you will be able to:

View your current Individual Account values

Check your current investment choices

Review your last 12 months’ contributions and transaction history

Change your investment strategy/funds for your existing investments and/or your future contributions (where appropriate)

Obtain an illustration of the possible benefits you might receive using the online annuity illustrator

More information through Mercer OneView

Pre-Retirement Fund(Legal & General)

100%

Fixed Interest Bond Fund

The fund aims to provide exposure to UK fixed interest bond assets to provide some protection against changes in the cost of buying a level annuity on retirement, or against times of stock market volatility.

In addition, as it is a diversified bond fund, it would be appropriate for members who wish to reduce their level of investment risk and volatility of investment returns as they approach retirement.

Indicative Total Expense Ratio: 0.1275%

Inflation Linked Pre-Retirement Fund

(Legal & General) 100%

Amanah Pension Fund

(HSBC Life) 100%

Cash Fund(BlackRock)

100%

Diversified Growth Fund(See page 3)

30%

Investment Guide

8

PlanViewer The Trustee uses Fidelity Investments as its chosen DC investment platform provider through which members will be invested in the updated fund range and various underlying investment managers.

Members will be provided with access to PlanViewer, Fidelity’s secure online pension service via the MMC UK Pensions website.

PlanViewer gives access to a range of further information and services, including:

•Fidelity’s daily market news and updates

•Fund factsheets (with details of the fund objectives, performance benchmarks, any relevant charges and Fidelity’s risk profile)

•Fund unit price information

•Knowledge Centre giving access to an investment tutorial and guidance tools.

Please note: PlanViewer is provided by Fidelity, who is responsible for the content of the site. You should be aware that any opinions expressed are those of Fidelity and not the Trustee.

You are encouraged to regularly review the progress of your Individual Account and useful information can be found on choosing your investments on the sites mentioned earlier and on www.pensions.uk.mmc.com.

Whilst the Trustee and the Administrator can provide you with information about the current investment options available, they cannot offer you advice that is specific to your circumstances. Your choice of investment options will be based on a number of personal factors, including your attitude to taking risk and the length of time until your retirement. If you need advice based on your personal circumstances, you should speak to a Financial Adviser. For details of your nearest Financial Adviser, please visit www.unbiased.co.uk.

MMC UK Pension Fund Trustee Limited

Glossary of terms

9

Active managementAn active manager aims to outperform a specific target (for example a market index, or other fund managers). Although the potential returns from active investments (if successful) can be higher than passive investments over the long term, there is also a risk that they will be worse. Charges for actively managed funds tend to be higher than for corresponding passively managed funds.

Alternative investments“Alternative assets” is the term used for any form of investment which offers broadly similar potential for growth to equities over the longer term, but which doesn’t depend solely on the stockmarket going up to generate this return. Examples include property, some higher-risk bonds, commodities and currency. Like equities, these types of investments carry high “capital risk”. However, as the returns on these investments are not directly driven by the stockmarket, their value will rise and fall in a different way and at different times to equity funds. Therefore, investing in alternative assets alongside equities would ensure that you spread your risks.

BondsBonds are loans to a government, company or other organisation. The level of capital protection falls somewhere between cash and equities. Assuming the bond issuer does not default, the return on your investment over the lifetime of the bond is the interest you receive on the loan. This interest can either be “fixed” (for example 5%) or “index-linked” (which means that it varies in line with inflation). Bonds generally have a maturity date (when the loan is repaid) and bond funds usually hold a mix of bonds with different maturity dates. Bond prices usually fall when interest rates rise (and vice versa). Investing in bonds closer to retirement might help to protect the level of income you could secure with your Individual Account. This is because the cost of buying a pension depends partly on the price of bonds and gilts. Bonds and gilts are expected to provide lower returns, but they are generally less volatile i.e. they are not so prone to large short-term fluctuations in value.

CashCash funds hold various income producing investments and whilst they offer good capital protection they do not offer 100% capital protection due to the various risks inherent in the underlying securities – as such, the value of your investment can still go down as well as up. In addition to this risk, all cash funds are subject to the risk that returns may fail to outpace inflation, so the buying power of your investment may reduce. Cash funds can provide good security for your Individual Account if you are about to retire, but may not provide good enough long-term returns for younger members.

Diversified Growth Fund (DGF)A diversified growth fund invests across a range of asset classes with the aim of providing a less volatile (but potentially lower return) than investing solely in equities.

EquitiesEquities are shares in companies. In the past, they have grown in value more than bonds, gilts or cash over longer periods. However, they can go up and down in value, sometimes significantly. Equities are likely to carry the highest risk that they could fall in value, so you might want to choose a fund that invests mainly in equities if you are aiming for higher long-term returns, and are not too worried about losing value over shorter periods.

10

You may be more willing to invest mainly in equities if, for example, retirement is still some way off, or you have other secure investments, or your DC pension is only a small part of your retirement savings.

GiltsBonds issued by the UK Government.

Index fundAnother term for a passively managed fund.

Indicative Total Expense RatioThe measure of the total cost of investing in a fund, which may include various fees and other expenses and may vary from time to time.

Individual AccountAn investment account set up in your name as a member of the DC section of the MMC UK Pension Fund and/or the MMC UK Pension Savings Plan.

Passive managementA passive manager aims to match the performance of a chosen market index (sometimes known as index tracking). It follows the market whether it goes up or down and so returns do not depend on the success of the fund managers’ choices. Passive management takes away the possibility that your investments will do better than the market, but it also removes the risk that they will do worse. Charges for passively managed funds tend to be lower than for corresponding actively managed funds.

RiskAll investments carry a level of risk, but there are different types of risk which are detailed below. You need to decide how much of each type of risk you are prepared to take.

Capital RiskThe risk that your investments may fall in value and not recover. This could happen with equities, bonds, alternative assets and even cash funds.

Inflation RiskThe risk that your investments will not grow quickly enough to outpace the increase in the cost of living.

Pension Conversion RiskWhen you retire, you may choose to use part of your Individual Account to buy an annuity. The cost of buying an annuity varies and moves broadly in line with bonds and gilts and depends on whether you buy an increasing or non-increasing annuity.

By switching your investments into a fund that invests in bonds and /or gilts when you are closer to retirement can help protect against this risk.

Default RiskThe risk that the bond issuer will default so you will not get back the capital you have invested when the bond is due for repayment.

Investment Guide

Here to helpIf you have any questions about the information contained in this guide, please contact the Administrator at:

MMC UK Pension Fund/MMC UK Pension Savings Plan PO Box 476, Westgate House, 52 Westgate, Chichester PO19 3WZ Tel: 0845 6000293 Fax: 01243 522001 Email: [email protected]

This document is a summary description of investment options. MMC’s pension arrangements are governed by the rules

of the respective arrangements from time to time. If there is any discrepancy between the description of benefits in this

document and the rules of the MMC pension arrangements, the rules of the MMC pension arrangements will prevail.

Des

ign

ed &

pro

duc

ed b

y M

erce

r Li

mit

ed©

1020

4