Investment Procss of Unicon (Tufail)

of 55

-

Upload

tufail-khan -

Category

Documents

-

view

224 -

download

0

Transcript of Investment Procss of Unicon (Tufail)

-

7/29/2019 Investment Procss of Unicon (Tufail)

1/55

A

SUMMER TRAINING REPORT

ON

INVESTMENT SERVICES AND INVESTMENT PROCESSOF UNICON INVESTMENT SOLUTION

AT

UNICON INVESTMENT SOLUTION DELHI

Submitted In Partial Fulfillment for Requirements of the Award of

Degree of BUSINESS ADMINISTRATION To

KURUKSHETRA UNIVERSITY

(Session 2011-2013)

STUDENT DECLARATION

1

SUBMITTED BY:

Tufail Ahmad Khan

ROLL NO. 73117102

MBA (3rd SEM)

Batch: 2011-2013

Under The Supervision Of:

(Sales Manager)

-

7/29/2019 Investment Procss of Unicon (Tufail)

2/55

I TUFAIL AHMAD KHAN student of MBA here by declared that the research report entitled

INVESTMENT SERVICES AND INVESTMENT PROCESS OF UNICON

INVESTMENT SOLUTION is completed and submitted under the guidance of (Sales

Manager unicon investment solution) is my original work. The imperial finding in this report

is based on the data collected by me. I have not submitted this project report to Kurukshetra

University, Kurukshetra or any other University for the purpose of compliance of any

requirement of any examination or degree.

DATE: TUFAIL AHMAD KHAN

PLACE: MBA (2011-2013)

ROLL NO. 73117102

2

-

7/29/2019 Investment Procss of Unicon (Tufail)

3/55

ACKNOWLEDGEMENT

At the very beginning, I wish to render my deep sense of gratitude with special thanks and due

regard to (Sales Manager, Unicon Investment Solution) whom I required the privilege of

working. His invaluable guidance and thoughtful consideration had been the key motivatingfactor throughout my project, which enabled me to complete my project so efficiently and

effectively.

I wish to express my respectable thanks and gratitude to Mr. Madhur Raj Jain (HOD of

Management)theoretical knowledge about the subject.

I feel immense pleasure to offer my thanks to faculty members, who co-operated in analysis of

data and helped me to understand some behavioral aspects of consumers. I am very thankful to

my friends who directly and indirectly helped me in collection of data and material related to the

research topic.

TUFAIL AHMAD KHAN

3

-

7/29/2019 Investment Procss of Unicon (Tufail)

4/55

Contents

Chapter Topic name Page No.

Chapter-1 Executive Summary 5

Chapter-2

Financial Sector 6

Industry Profile 10

Chapter-3 Company Profile 28

Chapter-4

Object of this Study 37

Research Methology 38

Chapter-5 Data Analysis 39

Chapter-6

Conclusion 48

Recommendation 51

Limitation 52

Chapter-7

Questionnaire 53

Bibliography 55

4

-

7/29/2019 Investment Procss of Unicon (Tufail)

5/55

EXECUTIVE SUMMARY

To get initial success in this field is very difficult. Although the business generation becomes

easier with time as they serve more people who then get added up in the loyal clientage. Thus

time and service are two most factors to get in this field.

Also the corporate remains a very important segment which gets business in bulk but retail

cannot be ignored which makes your business ticking.

Customer remains in the pivotal position.

The financial sector is in a process of rapid transformation. Reforms are continuing as part of the

overall structural reforms aimed at improving the productivity and efficiency of the economy.

The role of an integrated financial infrastructure is to stimulate and sustain economic growth.

5

-

7/29/2019 Investment Procss of Unicon (Tufail)

6/55

FINANCIAL SECTOR

The financial sector is in a process of rapid transformation. Reforms are continuing as part of the

overall structural reforms aimed at improving the productivity and efficiency of the economy.

The role of an integrated financial infrastructure is to stimulate and sustain economic growth.

The US$ 28 billion Indian financial sector has grown at around 15 per cent and has displayed

stability for the last several years, even when other markets in the Asian region were facing a

crisis. This stability was ensured through the resilience that has been built into the system over

time. The financial sector has kept pace with the growing needs of corporate and other

borrowers. Banks, capital market participants and insurers have developed a wide range of

products and services to suit varied customer requirements. The Reserve Bank of India (RBI) has

successfully introduced a regime where interest rates are more in line with market forces.

Financial institutions have combated the reduction in interest rates and pressure on their margins

by constantly innovating and targeting attractive consumer segments. Banks and trade financiers

have also played an important role in promoting foreign trade of the country.

Banks

The Indian banking system has a large geographic and functional coverage. Presently the total

asset size of the Indian banking sector is US$ 270 billion while the total deposits amount to US$

220 billion with a branch network exceeding 66,000 branches across the country. Revenues of

the banking sector have grown at 6 per cent CAGR over the past few years to reach a size of US$

15 billion. While commercial banks cater to short and medium term financing requirements,

national level and state level financial institutions meet longer-term requirements. This

distinction is getting blurred with commercial banks extending project finance. The total

disbursements of the financial institutions in 2011 were 87963cr.

Banking today has transformed into a technology intensive and customer friendly model with afocus on convenience. The sector is set to witness the emergence of financial supermarkets in the

form of universal banks providing a suite of services from retail to corporate banking and

industrial lending to investment banking. While corporate banking is clearly the largest segment,

personal financial services is the highest growth segment.

6

-

7/29/2019 Investment Procss of Unicon (Tufail)

7/55

The recent favourable government policies for enhancing limits of foreign investments to 49 per

cent among other key initiatives have encouraged such activity. Larger banks will be able to

mobilise sufficient capital to finance asset expansion and fund investments in technology.

Capital Market

The Indian capital markets have witnessed a transformation over the last decade. India is now

placed among the mature markets of the world. Key progressive initiatives in recent years

include:

The depository and share dematerialisation systems that have enhanced the efficiency of the

transaction cycle

Replacing the flexible, but often exploited, forward trading mechanism with rolling settlement,

to bring about transparency

The InfoTech-driven National Stock Exchange (NSE) with a national presence (for the benefit

of investors across locations) and other initiatives to enhance the quality of financial disclosures.

Corporatisation of stock exchanges.

The Securities and Exchange Board of India (SEBI) has effectively been functioning as an

independent regulator with statutory powers.

Indian capital markets have rewarded Foreign Institutional Investors (FIIs) with attractive

valuations and increasing returns. The Mumbai Stock Exchange continues to be the premierexchange in the country with an increase in market capitalization from US$ 40 billion in 1990-

1991 to US$ 203 billion in 1999-2000. The stock exchange has about 5,133 listed companies

and an average daily volume of about a billion dollars

Many new instruments have been introduced in the markets, including index futures, index

options, derivatives and options and futures in select stocks.

Insurance

With the opening of the market, foreign and private Indian players are keen to convert untapped

market potential into opportunities by providing tailor-made products:

With competition, the erstwhile state sector companies have become aggressive in terms of

product offerings, marketing and distribution.

7

-

7/29/2019 Investment Procss of Unicon (Tufail)

8/55

The Insurance Regulatory and Development Authority (IRDA) has played a proactive role as a

regulator and a facilitator in the sectors development.

The size of the market presents immense opportunities to new players with only 20 per cent of

the countrys insurable population currently insured.

The state sector Life Insurance Corporation (LIC), the largest life insurer in 2000, sold close to

20 million new policies with a turnover of US$ 5 billion.

The gross premia for the insurance sector2,91,605 crore for 2010-11.

There are four public sector and 15 private sector insurance companies operating in

general/non-life insurance business with a premium income of over (Rs 23.13 billion) in

January 2012

The markets potential has been estimated to have a premium income of US$ 80 billion with a

potential size of over 300 million people. The General Insurance Corporation (GIC) (which

covers the non-life sector) had a total premium income of US$ 2 billion in 2001-02. This has the

potential to reach US$ 9 billion in the next five years.

Venture Capital

Technology and knowledge have been and continue to drive the global economy. Given the

inherent strength by way of its human capital, technical skills, cost competitive workforce,research and entrepreneurship, India is positioned for rapid economic growth in a sustainable

manner. To realise the potential, there is a need for risk finance and venture capital (VC) funding

to leverage innovation, promote technology and harness knowledge based ideas.

The Indian venture capital sector has been active despite facing a challenging external

environment in 2001 and a competitive market scenario.

There were 34 VCFs and 2 Foreign VCFs registered with SEBI in March 2008.

According to a survey conducted by Thomson Financial and Prime Database, India ranked as

the third most active venture capital market in Asia Pacific (excluding Japan). It recorded 115

deals in 2001 with average investment per deal amounting to US$ 7.9 million. 57 VCFs invested

US$ 908 million in 101 Indian companies during 2001.

Disbursements for 2008 are expected to be US$ 2 billion and are estimated to reach US$ 10

billion by 2009.

8

-

7/29/2019 Investment Procss of Unicon (Tufail)

9/55

There is an increased interest in India: 70 VC funds operate in India with the total assets under

management worth about US$ 6 billion.

The amount has grown nearly twenty fold in the past five years. Most VCs believe that 2008-09

will be driven by a relatively stable economy and new initiatives that will boost the e-commerce

sector, particularly on-line trading and e-banking sectors.

9

-

7/29/2019 Investment Procss of Unicon (Tufail)

10/55

INDUSTRY PROFILE

A. Origin and Development of the industry

The Bombay Stock Exchange (BSE) is known as the oldest exchange in Asia. It traces its historyto the 1850s, when stockbrokers would gather under banyan trees in front of Mumbais Town

Hall. The location of these meetings changed many times, as the number of brokers constantly

increased. The group eventually moved to Dalal Street in 1874 and in 1875 became an official

organization known as The Native Share & Stock Brokers Association. In 1956, the BSE

became the first stock exchange to be recognized by the Indian Government under the Securities

Contracts Regulation Act.

The Bombay Stock Exchange developed the BSE Sensex in 1986, giving the BSE a means to

measure overall performance of the exchange. In 2000 the BSE used this index to open its

derivatives market, trading Sensex futures contracts. The development of Sensex options along

with equity derivatives followed in 2001 and 2008, expanding the BSEs trading platform.

Historically an open-cry floor trading exchange, the Bombay Stock Exchange switched to an

electronic trading system in 1995. It took the exchange only fifty days to make this transition.

Capital market reforms in India and the launch of the Securities and Exchange Board of India

(SEBI) accelerated the integration of the second Indian stock exchange called the National Stock

Exchange (NSE) in 1992. After a few years of operations, the NSE has become the largest stock

exchange in India.

Three segments of the NSE trading platform were established one after another. The Wholesale

Debt Market (WDM) commenced operations in June 1994 and the Capital Market (CM) segment

was opened at the end of 1994. Finally, the Futures and Options segment began operating in

2000. Today the NSE takes the 14th position in the top 40 futures exchanges in the world.

In 1996, the National Stock Exchange of India launched S&P CNX Nifty and CNX Junior

Indices that make up 100 most liquid stocks in India. CNX Nifty is a diversified index of 50

stocks from 25 different economy sectors. The Indices are owned and managed by India Index

Services and Products Ltd (IISL) that has a consulting and licensing agreement with Standard &

Poors.

10

-

7/29/2019 Investment Procss of Unicon (Tufail)

11/55

In 1998, the National Stock Exchange of India launched its web-site and was the first exchange

in India that started trading stock on the Internet in 2000. The NSE has also proved its leadership

in the Indian financial market by gaining many awards such as Best IT Usage Award by

Computer Society in India (in 1996 and 1997) and CHIP Web Award by CHIP magazine (1999).

The National Stock Exchange of India was promoted by leading financial institutions at the

behest of the Government of India, and was incorporated in November 1992 as a tax-paying

company. In April 1993, it was recognized as a stock exchange under the Securities Contracts

(Regulation) Act, 1956. NSE commenced operations in the Wholesale Debt Market (WDM)

segment in June 1994. The Capital Market (Equities) segment of the NSE commenced operations

in November 1994, while operations in the Derivatives segment commenced in June 2000.

Since the early 1950s till the early 1990s, Indian policy makers had been nourishing the goal of

Socialist pattern of society. They had been following the development planning strategy of the

former Soviet Russia in a mixed economic framework. From July 1991, in the face of an

unprecedented foreign exchange crisis, Indian economy started experiencing an IMF-World

Bank dictated regime of liberalization.

One aspect of this is financial liberalization. There is a move towards privatization of

nationalized banks these banks are selling their shares in the stock market. Transnational banks

are encouraged to operate in the Indian banking sector. Attempts are made to attract foreign

direct investment in different sectors. There is an increasing entry of foreign portfolio capital due

to stock market liberalization.

People are encouraged to invest in stocks through income tax benefits and abolition of capital

gains tax. There is a move to develop a national pension fund which will be invested in different

stocks to get returns out of which pension will be provided to retired people. It is expected that

boosting up of stock market will accelerate the process of capital accumulation and growth.

Stock market development has been an important part of financial liberalization in the less

developed countries (LDCs). In the pro-liberalization circle, stock market is assigned to play an

important role in the capitalist development of LDCs.

There are many studies supporting the positive link between stock market development and

growth. Let us mention some of the recent studies. One important study was undertaken by

Levine and Zervos (1998). Their cross-country study found that the Development of banks and

stock markets has a positive effect on growth. In another study Levine (2003) argued that

11

-

7/29/2019 Investment Procss of Unicon (Tufail)

12/55

although theory provides ambiguous relationship between stock market liquidity and economic

growth, the cross-country data for 49 countries over the period 1976-93 suggest a strong and

positive relationship (see also Levine, 2001). Henry (2000) studied a sample of 11 LDCs and

observed that stock market liberalizations lead to private investment boom. Recently, Bekaert et

al (2005) analyzed data of a large number of countries and observed that the stock market

liberalization leads to an approximate 1 % increase in annual real per capita GDP growth.

There are some economists who are skeptical. Long time back Keynes (1936) compared the

stock market with casino and commented: when the capital development of a country becomes

the by-product of the activities of a casino, the job is likely to be ill-done.

Referring to the study of World Bank (1993) Singh (1997) pointed out that stock markets have

played little role in the post-war industrialization of Japan, Korea and Taiwan. He argued that the

recent move towards stock market liberalization is unlikely to help in achieving quicker

industrialization and faster long-term economic growth in most of the LDCs.

In this perspective this study examines the nature of relationship between stock market and

growth through capital accumulation in India.

Growth and present status of the industry

The ever-growing and fast-maturing 'India Market' is a lucrative business destination for

developed countries. With 7-8% of GDP growth, huge analytical, young and English speaking

work forces the pull for opportunities are luring. The bandwidth of 'India Market' is enviably

wide and very deep.

'Markets in India' are well protected by legal guidelines and efficient administrators. With a

liberal and proactive government at the center the road ahead for 'Markets of India' is very rosy.

'Market India' has witnessed exponential growth over past one and half decade. A liberal and

transparent financial policy has affected free-in-flow of FII and as a result of which 'India

Market' has grown to a colossal monster in the international market. Foreseeing sure and

substantial returns on investments (ROI) companies are pro- actively listing on the stock market

indexes. Government agencies once much hated for red tape and bribes has shed its image.

Professionalism is their new mantra. Public Enterprises like IOC, ONGC, BHEL, NTPC, SAIL,

MTNL, BPCL, HPCL and GAIL, SBI, LIC, Hindustan Antibiotics Limited, Air India etc. to

name a few, are giving Private Indian companies a good run for their money. Private giants like

12

-

7/29/2019 Investment Procss of Unicon (Tufail)

13/55

Reliance Industries Limited, Infosys, Tata, Birla Corporation, Jet Airways, Ranbaxy, Biocon,

Bajaj Auto, and ICICI are breaking their own records every financial year.

Future of the industry

The stock market is booming in spite of the low agriculture output. The monsoon is good in an

overall sense but still the question remains who take the credit? The answer is the karma of the

people. I appreciate the Indian politicians and the industrialists who being pawns of destiny are

doing things positive and productive. India, as a country is running a very good period and the

position of planets in the transit are giving wonderful results.

Less than one percent of populations own stocks and less than 1000 individuals control the

market, the majority being the FIIS, the promoters of the company. The credit should go to

media for making stock market headlines.

The question many people in the market ask:

Will the Bull Run continue? What heights we can reach?

First of all, mark my words Indian bourses in the future will be one of the best investments in the

world. There will be a time when it can even reach 3000 points in the nifty. India will begin one

of the best dasas of the Sun, which will work in its favour. So before 2009 Indian bourses should

see an all time high.

Now this Bull Run will continue. There can be some correction in the BSE sensex in the 7500 points level.

The market will hover between the 6000- 7000 till mid august.

There will be huge fluctuations.

Investors and new entrants to the market to cool down a bit and come well below 7000.

In any case if you are long terms players then step-in and buy now and forget for another 10

years. You will make a killing in the Indian markets.

Most of the tech companies and the main index will do well but slightly in the lower side of

expectations.

13

-

7/29/2019 Investment Procss of Unicon (Tufail)

14/55

AN OVERVIEW OF FINANCIAL SERVICES

Since 1990s, there has been an upsurge in the financial services provided by various banks and

financial institutions. Efficiency of emerging financial system largely depends upon the quality

and variety of financial; services provided by the banking and non-banking financial companies.

The term Financial Services can be defined as, activities, benefits and satisfactions,

connected with sale of money, that offer to users and customers, financial related value.

Suppliers of financial services include the following types of institutions:

Banks and financial Institutions.

House building societies.

Insurances companies.

Credit card issuer companies.

Investment trust and Mutual funds.

Stock exchanges.

Leasing companies.

Unit trusts.

Finance Companies, and so on.

Financial service organizations render services to industrial enterprises and ultimate consumer

markets. This can be further subdivided to include Government/ public sector/ private sector, the

commercial sector, industry and international markets. Within the financial services industry the

main sectors are banks, financial institutions and non-banking financial companies.

Characteristics of financial services:

The financial have the following characteristics.

Intangible: An organization engaged in providing financial services is largely dependent on the

feedback from the public as to effectiveness, quality and attractiveness of the services rendered.

Direct sale: Direct sale is the only possible channel of distribution. There are no middlemen in

between. In order to insure that services are available at the right time and at the right place,

simultaneous production and distribution of financial services is undertaken by the service

organizations.

14

-

7/29/2019 Investment Procss of Unicon (Tufail)

15/55

Heterogeneity. In order to cater a variety financial and related needs of different customers in

different areas, financial service organization have to offer a wide range of products and services.

Fluctuation in demand: The demand for certain categories of financial services e.g., life

insurance; do fluctuate significantly, according to the level of general economic activity. This

factor puts extra pressures on the roles and functions of marketing in insurance organizations.

Project customers interest: The responsibility of any financial services organization to protect

consumers interest is important not just in banking and insurance, but also in other sectors of the

financial services.

Labour intensive: Personalized service versus automation, in fact, is an important issue in

financial services. The financial services sector is highly Labour intensive. It leads to increase in

the costs of production and consequently affects the price of financial product.

Geographical dispersion: Financial services must have both apple and wider application. To

insure this, the service providing organizations must have massive branch network so that

international, national and local customers enjoy benefits of convenience.

Lack of special identity. Customers usually approach a nearby branch of bank or financial

institution, because it is convenient to them. As the competing products offered by various

service organizations are similar, the emphasis is more on the package then the product. The

package consists of branch location, staff, services, reputation, advertising and new services

offered from time to time.

Information based. Financial services industry is an information-based industry. It involves

creation, dissemination, and use of information. Information is an essential component in the

production of financial services. Cost of processing information is quite relevant in the profitable

production of financial services.

Require quality Labour. Financial services require huge amounts of high quality Labour to

deal with information and communication with the market. The types of Labour rage from

workers performing simple tasks to those undertaking complex analysis and negotiation require

years of training and experience.

15

-

7/29/2019 Investment Procss of Unicon (Tufail)

16/55

Kinds of financial services:

Financial services provided by various financial institutions, commercial banks and merchant

bankers can be broadly classified into 2 categories:

(1) Asset based / Fund based services.

(2) Fee based / Advisory services.

The important fund based services include:

Equipment Leasing /Finance.

Hire- Purchase and Consumer Credit.

Bill Discounting.

Venture capital.

Housing Finance.

Insurance Services.

Factoring etc.

The fee based/ advisory services include:

Issue Management.

Portfolio Management.

Corporate Counseling.

Loan Syndication.

Merger and Acquisition.

Capital Restructuring.

Credit Rating.

Stock Broking and so on.

16

-

7/29/2019 Investment Procss of Unicon (Tufail)

17/55

INSURANCE IN INDIA

The insurance sector in India has come a full circle from being an open competitive market

to nationalization and back to a liberalized market again. Tracing the developments in the Indian

insurance sector reveals the 360-degree turn witnessed over a period of almost two centuries.

A brief history of the Insurance sector

The business of life insurance in India in its existing form started in India in the year 1818 with

the establishment of the Oriental Life Insurance Company in Calcutta. Some of the important

milestones in the life insurance business in India are:

1912: The Indian Life Assurance Companies Act enacted as the first statute to regulate the life

insurance business.

1928: The Indian Insurance Companies Act enacted to enable the government to collect

statistical information about both life and non-life insurance businesses.

1938: Earlier legislation consolidated and amended to by the Insurance Act with the objective of

protecting the interests of the insuring public.

1956: 245 Indian and foreign insurers and provident societies taken over by the central

government and nationalized. LIC formed by an Act of Parliament, viz. LIC Act,

1956, with a capital contribution of Rs. 5 crore from the Government of India.

17

-

7/29/2019 Investment Procss of Unicon (Tufail)

18/55

General Insurance

The General insurance business in India, on the other hand, can trace its roots to the Triton

Insurance Company Ltd., the first general insurance company established in the year 1850 in

Calcutta by the British. Some of the important milestones in the general insurance business in

India are:

1907: The Indian Mercantile Insurance Ltd. set up, the first company to transact all classes of

general insurance business.

1957: General Insurance Council, a wing of the Insurance Association of India, frames a code of

conduct for ensuring fair conduct and sound business practices.

1968: The Insurance Act amended to regulate investments and set minimum solvency margins

and the Tariff Advisory Committee set up.

1972: The General Insurance Business (Nationalization) Act, 1972 nationalized the general

insurance business in India with effect from 1st January 1973. 107 insurers amalgamated and

grouped into four companies viz. the National Insurance Company Ltd., the New India

Assurance Company Ltd., the Oriental Insurance Company Ltd. and the United India Insurance

Company Ltd. GIC incorporated as a company.

Insurance sector reforms

In 1993, Malhotra Committee, headed by former Finance Secretary and RBI Governor R. N.

Malhotra, was formed to evaluate the Indian insurance industry and recommend its future

direction. The Malhotra committee was set up with the objective of complementing the reforms

initiated in the financial sector.

The reforms were aimed at creating a more efficient and competitive financial system

suitable for the requirements of the economy keeping in mind the structural changes currently

underway and recognizing that insurance is an important part of the overall financial system

where it was necessary to address the need for similar reforms

In 1994, the committee submitted the report and some of the key recommendations included:

I) Structure

Government stake in the insurance Companies to be brought down to 50%

Government should take over the holdings of GIC and its subsidiaries so that these

subsidiaries can act as independent corporations

18

-

7/29/2019 Investment Procss of Unicon (Tufail)

19/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

20/55

Reforms in the Insurance sector were initiated with the passage of the IRDA Bill in Parliament in

December 1999. The IRDA since its incorporation as a statutory body in April 2000 has

fastidiously stuck to its schedule of framing regulations and registering the private sector

insurance companies.

The other decision taken simultaneously to provide the supporting systems to the insurance

sector and in particular the life insurance companies was the launch of the IRDAs online service

for issue and renewal of licenses to agents.

The approval of institutions for imparting training to agents has also ensured that the insurance

companies would have a trained workforce of insurance agents in place to sell their products,

which are expected to be introduced by early next year.

Since being set up as an independent statutory body the IRDA has put in a framework of globally

compatible regulations. In the private sector 12 life insurance and 6 general insurance companies

have been registered.

MAJOR DEVELOPMENTS DURING THE YEAR

The year 2008-09 witnessed the commercial banks becoming aggressive players in the home

loans market and a dramatic fall in interest rates across all maturities. This fall in interest rates

was driven by the decreasing bank rate and the increased competition with in the banks

themselves and between the Banks and HFCs. There was a growing emphasis on the adjustable

rate loans due to the decreasing interest rate scenario.

In presenting the Union Budget for 2008-09 the Honble finance minister announced that

National Housing Bank would launch a Mortgage Credit Guarantee Scheme, which would be

provided to all housing loans thereby fully protecting lenders against default. Towards this end

the Asian Development Bank (ADB) approved an investment of up to US$10 million

Equivalent in November 2008 to help pioneer the first mortgage guarantee company for India.

Mortgage financing through the India Mortgage Guarantee Company (IMGC) will help narrow

the housing shortfall. The India Mortgage Guarantee Company will improve the efficiency of

housing finance and protect mortgage lenders such as banks and housing finance

Companies in cases of borrower default.

The creation of IMGC will:

20

-

7/29/2019 Investment Procss of Unicon (Tufail)

21/55

Generate a greater volume of mortgage lending in the Indian market

Lower down payment requirements to as low as 5%

Broaden the eligibility for mortgages, and

Extend mortgage repayment periods by up to 25 years these changes will, in turn, support

capital market development by promoting securitization and increasing home ownership. The

incremental direct disbursement market share for the years 2001-02 and 2008-09 shows that the

HFCs have lost

Significant market share to the Banks.

Organized as a public limited company, IMGC is sponsored by the National Housing Bank

(NHB) of India and the Canadian Mortgage and Housing Corporation. Other main shareholders

are the International Finance Corporation, and ADB. The total project cost is estimated at US$40

million in paid-up capital. Finishing touches are being given to IMGC, which is expected to

formally come in to existence in September of this year. The schemes from IMGC are expected

to be launched by January 04 with the enactment of The Securitisation and Reconstruction of

Financial Assets and Enforcement of Security Interest Act 2008 (The Securitisation Act), banks

have been empowered to attach assets of the defaulters without intervention of lengthy and time

consuming court procedures.

This would help the banks for speedier foreclosure of home loan accounts in default. NHB is

also operational zing the foreclosure laws, which will enable the HFCs to foreclose the

defaulting account and apply to the recovery officer for sale of mortgaged property. Easier

foreclosure laws coupled with the proposed mortgage credit guarantee scheme of the NHB are

expected to release nonperforming funds of HFCs for lending.

Products and Services

The housing finance industry is getting increasingly commodities. Competition within the sector

is ensuring that in case of inadequate credit appraisal or recovery systems. The defense strategies

for managing increasing default rates fall into three basic categories: borrower strength,

collateral strength, lender techniques and various forms of insurance.

The first line of defense against loss is making good loan decisions; the second is managing the

asset effectively, with risk sharing entities coming last. Credit risk insurance is only activated

after the lender has done everything possible to avoid a loss on the loan.

21

-

7/29/2019 Investment Procss of Unicon (Tufail)

22/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

23/55

Transfer the assets to a larger player (commercial bank or general public) in the form of portfolio

sell out or a MBS. However, only HFCs with the ability to raise good quality assets and having

adequate distribution channels are likely to survive the competition.

MUTUAL FUNDS:

Mutual funds are companies that pool funds from a large number of investors and invest them on

their behalf for a financial return by buying, holding and selling securities. Funds managed by

institutional investors are huge and growing rapidly, particularly as part of the resolution of

pension pressures in various parts of the world. Global Assets under Management (AUM) rose 6

per cent to US $ 38.2 trillion in the first half of 2003, according to Cerulli Associates' latestGlobal Update report. Cerulli predicts the global compound annual growth rate for the industry

to be 8 per cent between 2011 and 2012

INDIAN MUTUAL FUND INDUSTRY

The history of Indian mutual fund industry can be distinctly divided into two phases - the period

before liberalization when only public sector players existed with one dominant player Unit

Trust of India and the post-liberalization era where the industry was opened up to private players.

Unit Trust of India (UTI) was established in 1963 and launched its legendary first scheme 'US-

64' in 1964. UTI witnessed a slow and steady growth over seventies and eighties and by end of

1988 it had an AUM of Rs. 67,000 million. From 1987, non-UTI, public sector mutual funds

were allowed and a series of mutual fund companies were set up by public sector banks and

financial institutions. At the end of 1993, the overall AUM of mutual fund industry was Rs.

470,004 million.

The mutual fund industry was opened up for private participation 1993 and a new era was

ushered in, paving the way for an unprecedented choice of products and services to Indian

investors. Detailed guidelines were established and the mutual fund industry (except UTI) came

under the regulation of Securities Exchange Board of India (SEBI). Many reputed foreign mutual

23

-

7/29/2019 Investment Procss of Unicon (Tufail)

24/55

funds such as Templeton, Alliance, Prudential group etc. set up operations in India. As at the end

of January 2003, there were 33 mutual funds with total assets of Rs. 1,218,050 million.

In February 2003, the Unit Trust of India Act 1963 was repealed and UTI was broken into two

separate entities. One is the Specified Undertaking of the Unit Trust of India, still under thecontrol of Government of India with AUM of Rs. 298,350 million as at the end of January 2003.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is registered

with SEBI and functions under the Mutual Fund Regulations. As at the end of October 31, 2003,

there were totally 31 funds in India, with assets under management of about Rs. 1,267,260

million.

TRENDS IN MARKETING OF MUTUAL FUNDS IN INDIA

The changing marketing trends in the mutual fund industry in India can be easily linked and

traced to its history of growth. The changes in marketing strategies can be characterized by 4

stages which have evolved along with the growth and evolution of the industry.

Product Focus

For the first three decades of the industry, from the setting up of UTI till the entry of private

sector players, the only focus of the marketing strategy was different product offerings. UTI and

various other public sector mutual funds focused on introducing an array of products falling in

different categories. The categorization was primarily based on two factors: one was the way the

schemes were traded and the other through different composition of debt and equity securities in

the scheme.

By the way Schemes were traded:

>Open-ended Schemes

>Close-ended Schemes

In an open-ended scheme there are no limits on the total size of the corpus. Investors are

permitted to enter and exit the open-ended scheme at any point of time at a price that is linked tothe net asset value (NAV). In case of close-ended schemes, the total size of the corpus is limited

by the size of the initial offer. The entry and exit of investors is possible by only trading on the

stock exchanges. Due to liquidity constraints posed by close-ended funds, they were soon

rendered obsolete and most of the prevailing schemes today are open-ended schemes.

24

-

7/29/2019 Investment Procss of Unicon (Tufail)

25/55

By Composition of Debt and Equity in the Scheme:

> Growth Schemes

>Income Schemes

>Balanced Schemes

>Money Market Schemes

The products were also differentiated by the composition of equity and debt in various schemes.

Growth schemes invest predominantly in equities whereas Income schemes invest only in fixed

income debt securities. Balanced schemes try to derive the benefits of both equity and debt by

investing in both. Money market schemes invest in short term liquid securities like money

market instruments so that they serve as appropriate products for investing short term funds.

There were other niche schemes to fulfill specific needs, such as Tax Saving Schemes, Sector

Specific Schemes, Index Schemes (which are passively invested in a benchmark Index) and so

on. In the Product Focus stage, the aim of the mutual fund companies was to introduce a wide

variety of products and due to oligopolistic competition.

Customer Ownership Focus

Mutual fund companies began to segment their target customers and position their various

products based on the target segment they proposed to address. The target segment was broadly

divided into institutional segment and individual investor segment. The institutional segment

consisted of treasury departments of Corporate, Trusts etc and suitable products such as

Institutional Income schemes and Money Market schemes were targeted at them. The individual

investor was in turn divided into various segments such as Young Families with small or no

children, Middle-aged People saving for retirement and Retired People looking for steady

income. Suitable products such as Growth and Balanced schemes for young families and Income

schemes for retired people were marketed.

By proper segmentation and by targeting the right product to the right customer, Mutual Fund

companies hoped to win the confidence of their customers and 'own' them for a lifetime.

Specialized Product & Service Focus

25

-

7/29/2019 Investment Procss of Unicon (Tufail)

26/55

If one observes the trends in the recent past, Companies have been taking the above customer

focus further by designing and launching specialized products and services. As awareness levels

of individual investors go up, focus is on identifying one's investment needs depending on one's

financial goals, risk taking ability and tim e horizon. Investors chose companies, which help

them in the above through specialized products and services.

For example, a common financial goal is to save and invest for meeting the education needs of

children. A number of mutual funds such as Pru-ICICI Mutual Fund and UTI Mutual Fund have

launched products that are designed to serve this specific need. A similar such need is planning

for a comfortable retirement.

Non Banking Financial Companies

Non-Banking Financial Companies (NBFCs) are a set of financial service companies that are

quite unique to India in terms of their size and the range of services provided by them. The

services provided by NBFCs range from retail service such as loans, leasing and hire purchase

financing, brokerage and distribution services; to bill discounting and syndication services to

corporate customers. Till early 1990s, when NBFCs were at their peak, most retail customers

would approach an NBFC rather than a bank for all their financial service needs. However, since

its peak in the mid-1990s when public deposits held by NBFCs increased to 9.5 per cent of bank

deposits, this sector saw a steep decline. Aggregate public deposits of NBFCs as a percentage of

bank deposits came down to 1.5 per cent by March 2012.

Till 1990s, NBFCs constituted a significant part of the Indian financial services industry and

complemented the services provided by a bank. They were a heterogeneous group of

intermediaries of varying size and provided a range of services. They were characterized by their

ability to provide niche financial services and due to their relative organizational flexibility; they

were often able to provide tailor-made services relatively faster than banks and financial

institutions. This enabled them to build up a wide-ranging clientele from small borrowers to

establish corporate.

26

-

7/29/2019 Investment Procss of Unicon (Tufail)

27/55

Based on the principal activity carried out by the company, NBFCs were classified by RBI

under five main categories - Equipment leasing company (EL), Hire Purchase finance company

(HP), Investment company (IC), Loan company (LC) and Residuary non-banking company

(RNBCs - large companies not coming under any one particular category). NBFCs achieved their

zenith in early 1990s. Their accelerated expansion in 90s was driven by the opportunities created

by the process of financial liberalization. However, their rapid growth resulted in unhealthy

practices and certain disconcerting developments. In response to this, RBI considerably tightened

its supervisory and regulatory framework over NBFCs in 1998. Some of the new measures of

Hire purchase finance, mostly consisting of retail funding of cars, commercial vehicles and

consumer durables were the primary activity, followed by loans and inter-corporate deposits.

27

-

7/29/2019 Investment Procss of Unicon (Tufail)

28/55

COMPANY PROFILE

UNICON INVESTMENT SOLUTIONS

UNICON is a financial services company which has emerged as a one-stop investment solutionsprovider. It was founded in 2004 by two visionary and flamboyant entrepreneurs, Mr. Gajendra

Nagpal and Mr. Ram M. Gupta, who possess expertise in the field of Finance. The company is

headquartered in New Delhi, and has its corporate office in Mumbai with regional offices in

Kolkata, Chennai, Hyderabad and Noida

UNICON is a professionally managed company, lead by a team with outstanding managerial

acumen and cumulative experience of more than 200 years in the financial markets. The

company is supported by more than 3500 Uniconians and has an extensive network of over 100

branches, 600 plus business partner locations & 2500 remisers providing it with a national

footprint.

With a customer base of over 200,000, the UNICON Group has an eye for the intricate financial

needs of its clients and caters to both their short term and long term financial needs through a

comprehensive bouquet of investment services. These services range from offline & online

trading in equity, commodities and currency derivatives to debt markets to corporate finance and

portfolio management services. The company has a sizable presence in the distribution of 3rd

party financial products like mutual funds, insurance products and property broking. It also

provides expert Advisory on Life Insurance, General Insurance, Mutual Funds and IPOs. The

distribution network is backed by in-house back office support to provide prompt and efficient

customer service

The Equity broking arm UNICON Securities Pvt. Ltd offers personalized premium services on

the NSE, BSE & Derivatives market. The Commodity broking arm Unicon Commodities Pvt.

Ltd offers services in Commodity trading on NCDEX and MCX. The UNICON group also has a

PCG division providing investments solutions for High Net worth Individuals. The Corporate

Advisory Services arm Unicon Capital Services (P) Ltd offers entire gamut of Investment

Banking services to corporate.

UNICON can boast of some of the most respected names in the Private Equity space like

Sequoia Capital and Nexus India Capital as its share holders.

28

-

7/29/2019 Investment Procss of Unicon (Tufail)

29/55

Mission & Vision

Mission:

To create long term value by empowering individual investors through superior financial

services supported by culture based on highest level of teamwork, efficiency and integrity.

Vision:

To provide the most useful and ethical Investment Solutions - guided by values driven approach

to growth, client service and employee development.

29

-

7/29/2019 Investment Procss of Unicon (Tufail)

30/55

MANAGEMENT TEAM

Mr. Gajendra Nagpal

Founder & CEO

Mr. Ram M Gupta

Co-Founder & President

Mr. Y.P. Narang

Head - Fixed Income Group

Mr. Sandeep Arora

Chief Operating Officer

Mr. Vikas Mallan

Chief Financial Officer,

Head Distribution

Mr. Trinadh Kiran

National Head (E-Broking)

Mr. Subhash Nagpal

Director - Strategic

Planning & Distribution

Ms. Anjali MukhijaChief Compliance Officer

Mr. Vijay Chopra

National Head (Business Alliances)

Mr. Anurag Nayar

Chief Technology Officer

Mr. Ashish Kukreja

Head HNI Client Relations

Ms. Divya Varma Kaur

Head -HR & Training

Mr. Sandeep Mahajan

Head (Equity Broking-Offline

30

-

7/29/2019 Investment Procss of Unicon (Tufail)

31/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

32/55

Facilities Offered by Unicon

* De-materialization:

You can submit your physical shares at the Unicon branch for dematerialization into

electronic form.

* Re-materialization:

You can also request for Re-materialization which enables you to convert the

dematerialized shares into physical form.

* Transfer:

Inter and intra depository services are available through which you can transfer shares.

* IPO:

You can apply for IPO using your demat account details and on allotment the securities

are transferred directly to your demat account.

* Corporate Actions:

While holding your stock in demat account, in case you are eligible for any bonus and

rights issues the allotment would be transferred to your demat account.

* Easi:

You can view your demat account over the Internet and avail a host of services. This facilityempowers our clients to view, download, and print updated holdings with respective valuations.

32

-

7/29/2019 Investment Procss of Unicon (Tufail)

33/55

IPO

At Unicon you can invest in the Primary markets (Initial Public Offerings) online without

going through the hassles of filling up any IPO application forms or any other paperwork.

We shall make sure that you do not miss the opportunity to subscribe/invest in a good IPO issue

by providing you an online IPO application form, transfer of funds online through secured

payment Gateways of leading banks like ICICI, HDFC, and AXIS bank.

In addition to the above we shall provide you with the In-Depth analysis of the IPO issues which

shall be hitting the Indian Markets in near future, IPO Calendar, analysis on the recent IPO

listings, prospectus, offer documents and other IPO research reports so as to help you take an

informed decision to invest in the IPO issues.

Online IPO facility is open to all our registered clients at no cost whatsoever. All you need is the

following to subscribe online to the IPO issues:

A trading account with Unicon

A Demat account with Unicon

An access to the net banking facility with the Banks through which Unicon has operational

Gateway facility (ICICI, HDFC and AXIS Bank).

You must have signed a Power of Attorney (POA) agreement for applying in IPOs online.

Mutual Fund

Unicon Provides expert advice to its clients for their investments in equity & debt markets

through Mutual Funds.

Our experts advice you the best investment solutions that suit you and help you to reach your

financial goals.

33

-

7/29/2019 Investment Procss of Unicon (Tufail)

34/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

35/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

36/55

firm ensures that clients requirements are met at optimum cost. By constantly improving our

knowledge capital and remaining focused on client needs, we aim to create significant value for

our clients by helping them execute the right capitalization strategy. We also intend to initiate

merchant banking services (Capital Markets Fundraising) in the short term (Merchant Banking

License pending)

Offerings

Private Equity (PE) Syndication

They specialize in the syndication of the private equity for the Indian companies in high-growth

markets on their capitalization/re-capitalization strategies, which helps them to achieve their

growth targets. Our team of professionals ensures complete confidentiality, strong focus on

implementation and quick turnaround time. Access to key decision makers at PE funds gives us

an edge in optimal structuring and efficient closure of transactions. They service their clients

through various stages of the PE deal namely collateral preparation, investor short listing,

commercial term sheet, due diligence and final closure.

Mergers & Acquisitions (M&A) Advisory

They provide both buy-side and sell-side advisory services as part of their M&A advisory

offering. They advise clients during the entire transaction process right from target identification

to deal closure. They have an experienced and highly qualified team with more than 40+ man-

years of experience which specializes in identification and short listing of potential targets,

strategic planning of an acquisition and arranging capital for the transaction, if needed.

Debt Syndication

Our offerings include:

Project Finance / Term Loans for Expansion - Arranging Long-term loans for setting up

new projects from Financial Institutions and Banks

External Commercial Borrowings (ECBs) - Arranging LIBOR-linked loans

Foreign Currency Convertible Bonds (FCCB)-Arranging FCCB Loans

Working Capital Facilities - Arranging fund-based and non-fund based limits for clients

from Banks at competitive rates

36

-

7/29/2019 Investment Procss of Unicon (Tufail)

37/55

Trade Finance - Arrangement of trade finance (Buyer's / Suppliers Credit)

Inter-Corporate Deposits Borrowing and Placement

OBJECTIVES OF THE STUDY

To find the market potential and market penetration of UNICON INVESTMENT

SOLUTION product offerings in New Delhi. To collect the real time information about preference level of customers using Demat

account and their inclination towards various other brokerage firms e.g. India bulls,

Share khan, Indiainfoline, Religare, Alan kit, Unicon.

To expand the market penetration of UNICON INVESTMENT SOLUTION.

To provide pricing strategy of competitors to fight cut throat competition. To increase

the product awareness of UNICON INVESTMENT SOLUTION as single window

shop for investment solutions

37

-

7/29/2019 Investment Procss of Unicon (Tufail)

38/55

RESEARCH METHODOLOGY

Research design and methodology

It was important to collect detailed information on various aspects for effective analysis. As

Marketing today is becoming more of a battle based on information based society companies

with superior information enjoys a competitive advantage.

Methodology Adopted

The information was collected through person interview and interview was conducted through

the mode of questionnaire.

Analysis of Data

Data collection

The data collection was collected through primary as well as secondary source.

PRIMARY DATA:

Primary data was collected from 150 respondents using a schedule of question and a survey was

conducted. The tabular and graphical data was Microsoft excel.SECONDARY DATA:

Secondary data was collected mainly from internet, printed journals on the capital markets of

India, newspaper articles and books written on the Indian stock markets.

SAMPLING:Judgment, non-random sampling was used. Respondents were request to help with the

schedule at their offices, homes or at the UNICON INVESTMENT SOLUTION office.

38

-

7/29/2019 Investment Procss of Unicon (Tufail)

39/55

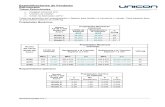

DATA ANALYSIS

1. Preference of investment

Fig. Result of preference of investment

Interpretation: This data shows that the mutual fund market is on the rise yet, so the most

favored investment continues to be in the share market.so with the more transparent system,

investment in the market can definitely be increased.

Preference of investment Respondents In %

Derivatives 9 6%

Share 12 8%

Mutual Fund 105 70%

Bond 24 16%

Total 150 100%

2 Awareness on Online Share Trading

39

-

7/29/2019 Investment Procss of Unicon (Tufail)

40/55

Fig. Result of Awareness of Online Share Trading

Interpretation: With the increase in cyber education, the awareness towards online share trading

has increased by leaps and bounds. This awareness is expected to increase further with the

increase in Internet education.

Result of Awareness of Online Share Trading

Online Share Trading Respondents In%

Yes 108 72%

No 42 28%

Total 150 100%

3. Awareness of unicon investment solutions

Fig. Result 0f Awareness of unicon as a brand

40

-

7/29/2019 Investment Procss of Unicon (Tufail)

41/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

42/55

Awareness of unicon facilities

Awareness of unicon facilities Respondents In%

Yes 120 80

No 30 20

Total 150 100%

5. Satisfaction Level among Customers with current broker

Fig. Result of satisfaction level among customers with current broker

Interpretation: This pie-chart corroborate the fact that Strategic marketing, today, has gone

beyond only meeting Sales targets and generating profit volumes. It shows that all the

competitors are striving hard not only to woo the customers but also to make them Brand loyal

by generating customer satisfaction.

satisfaction level among customers with current broker:

Satisfaction level Respondents In%

Yes 108 72

No 42 28

Total 150 100%

6. Frequency of Trading

42

-

7/29/2019 Investment Procss of Unicon (Tufail)

43/55

Monthly 52%Yearly 12%

Daily 10%

Weekly 26%

Fig. Result of Frequency of Trading

Interpretation: Inspite of the huge returns that the share market promises, we see that there is

still a dearth of active traders and investors. This is because of the non transparent structure of

the Indian share market and the skepticism of the target audience that is generated by the

volatility of the stock market. It requires efficient bureaucratic intervention on the part of the

Government.

In Table Result of Frequency of TradingFrequency of Trading In % Respondents

Daily 10% 15

Weekly 26% 39

Monthly 52% 78

Yearly 12% 18

Total 100% 150

7.Percentage of earnings invested in Share Trading

43

-

7/29/2019 Investment Procss of Unicon (Tufail)

44/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

45/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

46/55

Yes 80%

No 20%

AnalysisThe above table clearly show that from a sample size of 150 respondents, 120 individuals wereaware of demat account.

The basic purpose of this Question is to know about awareness of demat account amongrespondents.

Aware of DEMAT Account:Responses Number of Responses % of Responses

Yes 120 80

No 30 20

Total 150 100%

11. Are You Satisfied with your demat service provider?

46

-

7/29/2019 Investment Procss of Unicon (Tufail)

47/55

This graph shows that most of the people were satisfied with demat service provider.

Responses Number of Responses % of Responses

Yes 135 90%

No 15 10%

Total 150 100%

CONCLUSIONS

47

-

7/29/2019 Investment Procss of Unicon (Tufail)

48/55

To get initial success in this field is very difficult. Although the business generation becomes

easier with time as we serve more people who then get added up in the loyal clientage. Thus time

and service are two most factors to get in this field.

Also the corporate remains a very important segment which gets business in bulk but retail

cannot be ignored which makes your business ticking.

Customer remains in the pivotal position.

Based on the findings of our project we would like to suggest the following:-

1. After sales services and follow up calls are important for getting new references so

trained telesales should be appointed for this purpose whose sole work should be to make

feedback calls.

2. Investment is having too many financial products right from Demat account to General

Insurance and not all the salespeople are familiar with each and every product so the

work force should be segregated each group dealing in a specific product and the sales

target should be given likewise.

3. While interacting with the investors I found that most of the customers are unaware about

the Mutual fund. Some of the people look upon mutual funds and equity trading as

gambling. Thus a mutual fund awareness program can help to increase the penetration of

mutual funds in the market.

4. UNICON INVESTMENT should declare in black ink that they will charge just 1 paisa

per transaction. People tend to think that there must be some hidden charges.

5. Rs 750 account opening charges are too high when targeting a corporate so the company

should be flexible on this amount.

6. UNICON INVESTMENT should provide periodic training for updating the product

knowledge of various financial advisors.

7. Company should have a scheme of rewards and recognition to employees and the field

persons to boost their motivation.

KEY ISSUES AND CONCLUSIONS

48

-

7/29/2019 Investment Procss of Unicon (Tufail)

49/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

50/55

-

7/29/2019 Investment Procss of Unicon (Tufail)

51/55

RECOMMENDATIONS

The company should effectively focus on advertising.

The company should make more aware to the customer about their investment process.

Company must provide full information to their employee about sector and there product and

services in which its deals.

Company basically deals in customer relationships it must provide more and more training and

development programme to their relationship manager.

Company must focus on the need and wants of the customer as well as after sales services, to

make the customer more loyal.

Company must give reliable and full information to their customer about their product and

services, and also there benefits.

Company should take care of their employee by giving them cash incentive or taking those

people abroad who have achieve their target or make a large-volume of sales. And also give

catered meals to staff that work long hours or those working during peak hours.

Lastly taking the feedback from customer so as to better tune its services with the customer

needs.

51

-

7/29/2019 Investment Procss of Unicon (Tufail)

52/55

LIMITATIONS

Limitations and Constraints

Time Constraints:

Time is that factor which cannot be hold by anyone, ones it goes never comes back.

The researcher found lack of time and done a precise in-dept study and bring out the available

data and information.

Resource Constraints:

Earlier there was not that much researches had been conduct on this topic, so the researcher find

it difficult to group the information and get the best output.

As the researcher had only used the secondary data the lack or impropriety in the secondary data

will also present in the research project

52

-

7/29/2019 Investment Procss of Unicon (Tufail)

53/55

APPENDIX

QUESTIONNAIRE

Q1. In which of these Financial Instruments do you Preference of investment into?

Shares Mutual Funds Bonds Derivatives

Q2. Are you aware of online Share trading?

Yes No

Q3. Heard about UNICON INVESTMENT SOLUTION ? Yes No

Q4. Do you know about the facilities provided by UNICON INVESTMENT SOLUTION?

Yes No

Q5. Are you currently satisfied with your Share trading company?

Yes No

Q6. How often do you trade?

Daily Weekly Monthly Yearly

Q7. What percentage of your earnings do you invest in share trading?

Up to 10% Up to 25% Up to 50% Above 50%

Q8. How do you rate these share trading companies?

1. 2. 3

53

a. Reliance moneyb. ICICI Directc. India Bullsd. IL&FS INVESTSMARTe. Others (Please

-

7/29/2019 Investment Procss of Unicon (Tufail)

54/55

Q9. With which company do you have your DEMAT account?

Reliance money ICICI Direct UNICON India Bulls

Others

Q10.Are you aware of DEMAT?

Yes No

Q11. Are You Satisfied with your demat service provider?

Yes No

54

-

7/29/2019 Investment Procss of Unicon (Tufail)

55/55

BIBLIOGRAPHY

Books

Financial Management Prashanna Chandra,6thedition

Financial Management Khan & Jain ,13th edition

Securities Analysis and Portfolio Management ,Fischer & Jordon

Research Methodology, David .R. Cooper and Schindler

Websites

www.unicon.co.in

www.icicidirect.com www.UNICON INVESTMENT.com

www.nseindia.com

www.economicstimes.com

http://www.unicon.co.in/http://www.icicidirect.com/http://www.investsmart.com/http://www.nseindia.com/http://www.economicstimes.com/http://www.unicon.co.in/http://www.icicidirect.com/http://www.investsmart.com/http://www.nseindia.com/http://www.economicstimes.com/