Investment Climate Statement - Indonesia · Singapore 32% Japan 18% Malaysia 4% ... treaty, the tax...

16

Copyright (c) Mizuho Bank, Ltd. All Rights Reserved. Investment Climate Statement - Indonesia October 2018 Mizuho Bank, Ltd. Global Strategic Advisory Department

Transcript of Investment Climate Statement - Indonesia · Singapore 32% Japan 18% Malaysia 4% ... treaty, the tax...

Copyright (c) Mizuho Bank, Ltd. All Rights Reserved.

Investment Climate Statement - Indonesia

October 2018

Mizuho Bank, Ltd.

Global Strategic Advisory Department

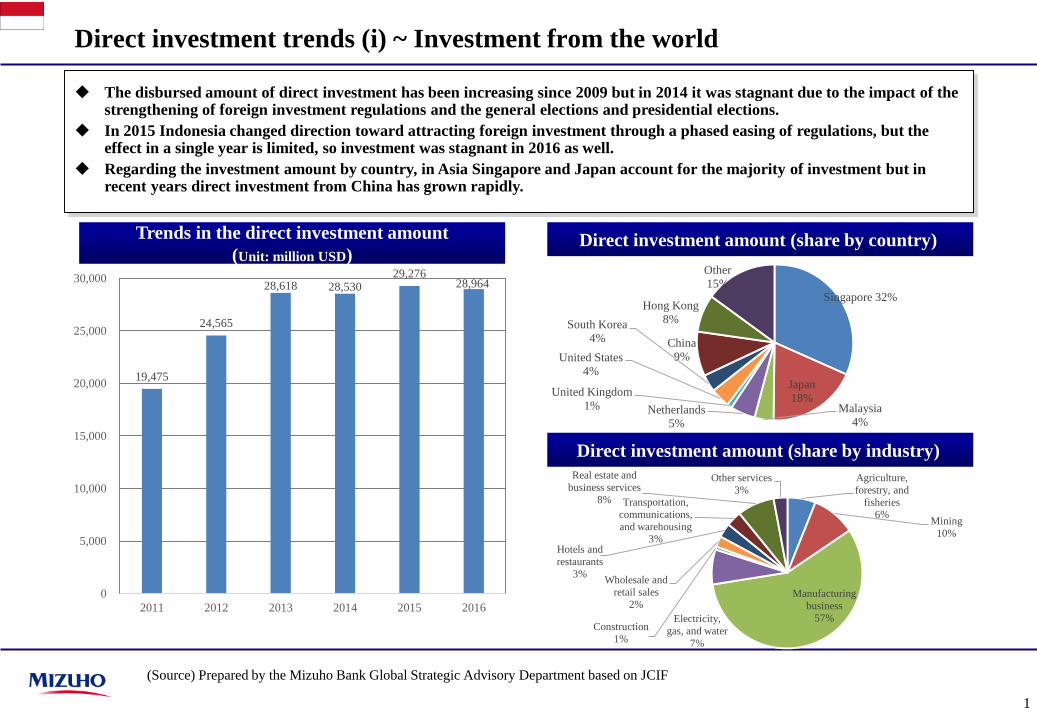

Direct investment trends (i) ~ Investment from the world

1

The disbursed amount of direct investment has been increasing since 2009 but in 2014 it was stagnant due to the impact of thestrengthening of foreign investment regulations and the general elections and presidential elections.

In 2015 Indonesia changed direction toward attracting foreign investment through a phased easing of regulations, but the effect in a single year is limited, so investment was stagnant in 2016 as well.

Regarding the investment amount by country, in Asia Singapore and Japan account for the majority of investment but in recent years direct investment from China has grown rapidly.

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on JCIF

Trends in the direct investment amount

(Unit: million USD)

19,475

24,565

28,618 28,530 29,276

28,964

0

5,000

10,000

15,000

20,000

25,000

30,000

2011 2012 2013 2014 2015 2016

Singapore 32%

Japan

18%Malaysia

4%Netherlands

5%

United Kingdom

1%

United States

4%

South Korea

4% China

9%

Hong Kong

8%

Other

15%

Direct investment amount (share by country)

Direct investment amount (share by industry)

Agriculture,

forestry, and

fisheries6%

Mining

10%

Manufacturing

business

57%Electricity,

gas, and water

7%

Construction

1%

Wholesale and

retail sales

2%

Hotels and

restaurants

3%

Transportation,

communications,

and warehousing3%

Real estate and

business services

8%

Other services

3%

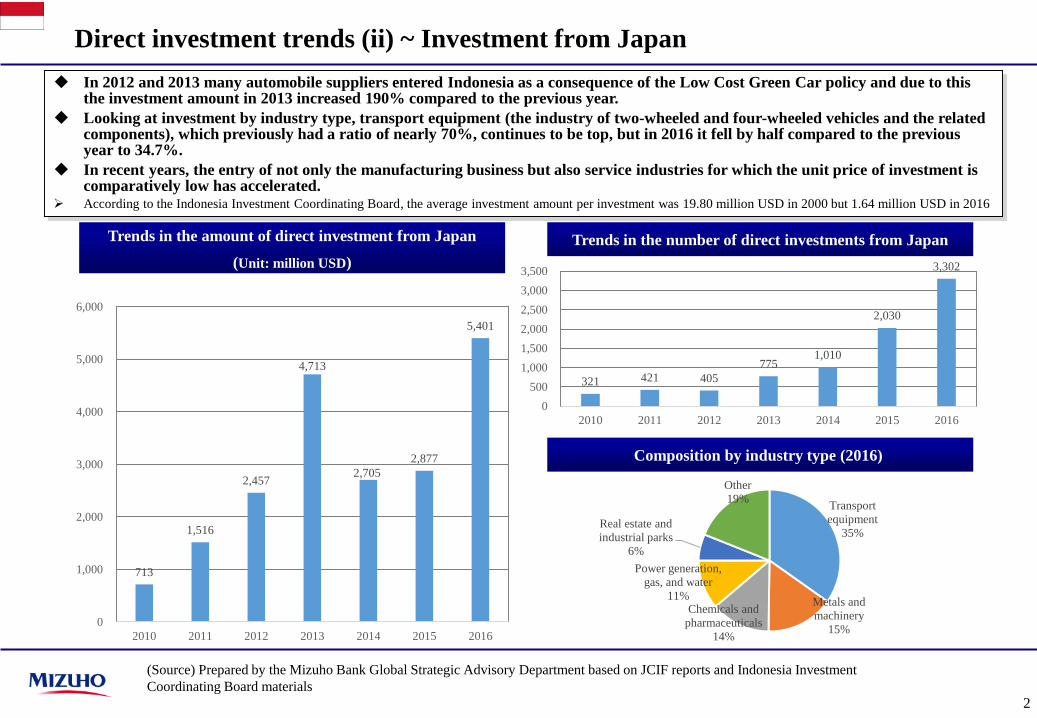

Direct investment trends (ii) ~ Investment from Japan

2

In 2012 and 2013 many automobile suppliers entered Indonesia as a consequence of the Low Cost Green Car policy and due to this the investment amount in 2013 increased 190% compared to the previous year.

Looking at investment by industry type, transport equipment (the industry of two-wheeled and four-wheeled vehicles and the related components), which previously had a ratio of nearly 70%, continues to be top, but in 2016 it fell by half compared to the previous year to 34.7%.

In recent years, the entry of not only the manufacturing business but also service industries for which the unit price of investment is comparatively low has accelerated.

According to the Indonesia Investment Coordinating Board, the average investment amount per investment was 19.80 million USD in 2000 but 1.64 million USD in 2016

Trends in the amount of direct investment from Japan

(Unit: million USD)

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on JCIF reports and Indonesia Investment

Coordinating Board materials

Trends in the number of direct investments from Japan

Composition by industry type (2016)

713

1,516

2,457

4,713

2,705

2,877

5,401

0

1,000

2,000

3,000

4,000

5,000

6,000

2010 2011 2012 2013 2014 2015 2016

321 421 405

775 1,010

2,030

3,302

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014 2015 2016

Transport

equipment

35%

Metals and

machinery

15%

Chemicals and

pharmaceuticals

14%

Power generation,

gas, and water

11%

Real estate and

industrial parks

6%

Other

19%

Major industrial parks and special economic zones

3

Approximately 80% of Japanese enterprises have offices or factories in the districts surrounding Jakarta.

Many industrial parks are dotted along the expressway heading east from Jakarta.

Batam Industrial Park

There are approximately 40 companies

including Kyocera, etc.

(12) Karawang International Industrial City

There are approximately 50 companies including

Daihatsu Motor, Yamaha, etc.

(8) MM2100 Industrial Town

There are approximately 60 companies

including Toyota Motor Corporation, etc.

(11) East Jakarta Industrial Park

There are approximately 70 companies

including Seiko Epson, etc.

1 Jakarta Industrial Estate Pulogadung

2 Nusantara Bonded Zone

3 Marunda Industrial Park

4 Krakatau Industrial Estate - Cilegon

5 Modern Cikande Industrial Estate

6 Pasar Kemis Industrial Estate

7 Cikarang Industrial Estate

8 MM2100 Industrial Town

9 Bekasi International Industrial Estate (BIIE)

10 Bekasi International Industrial Estate

11 East Jakarta Industrial Park (EJIP)

12 Karawang International Industrial City

13 Suryacipta City of Industry

14 Bukit Indah Industrial Park

15 Cirebon Industrial Estate

16 Cirebon Industrial Estate

17 Cilacap Industrial Estate

18 Turboyo Industrial Estate

19 Tanjung Emas Export Processing Zone

20 Guna Mekar Industrial Estate

21 Ngoro Industrial Park

22 Gresik Industrial Estate

23 Kabil Industrial Estate

24 Batam Industrial Park

25 Bintang Industrial Park

26 Spinindo Mitradaya Batam Industrial Estate

27 Batamasia Industrial Park

28 Bintan Industrial Estate

29 Medan Industrial Estate

30 Makassar Industrial Estate

31 PIER (Pasuruan Industrial Estate Rembang)

32 Greenland International Industrial Center

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on the Indonesia Investment Coordinating

Board (BKPM)

Medan

Sumatra

Batam

Jakarta

Bandung

Kalimantan(Borneo)

Ujung Pandang

Sulawesi(Celebes)

Surabaya

Denpasar

Bali

Irian Jaya

Batam

Hang Nadim

International Airport

Jakarta area

Soekarno–Hatta International Airport

Jakarta

Accounting and taxation-related information (i) ~ Accounting

4

It is necessary for the Board of Directors to prepare the annual reports, including the financial statements, and after completion

of the audit of the Komisaris Board, to receive the approval of a shareholders' meeting within 6 months of the end of the fiscal

year.

In the case that any of the following are applicable, it is necessary to present the annual financial statements to a certified public

accountant to receive an audit.

In the case that the business field is related to the raising of funds for the general public

In the case of issuing debt approval forms, etc.

In the case that the company is a publicly-traded company

Major accounting systems

Status of compliance with

international accounting standards

Accounting currency

The standard is accounting principles (PSAK) in compliance with the international financial reporting standards (IFRS)(Accounting principles for small and medium-sized enterprises: ETAP is also available)

Indonesia rupiah-denominated or US dollar-denominated (in the case that this is permitted by

the Ministry of Finance)

Related laws and regulations Company Law, Capital Market Law, etc.

Booking language Indonesian or a foreign language (in the case that this is permitted by the Ministry of Finance)

Accounting period 12 months (establishment of the fiscal year is optional but mainly December settlement of

accounts)

Books maintenance period As a general rule, 10 years

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on "Investment, M&As, Company Law,

Accounting and Taxation, and Labor in Indonesia,” etc.

Accounting and taxation-related information (ii) ~ Taxation

5

The major taxes in Indonesia are as follows.

Note should be made of the prepaid import tax (PPH 22) and domestic income tax withheld at source (PPH 23), etc. which are distinctive tax systems in Indonesia.

Corporate

income tax

Individual

income tax (PPH

21)

Value added tax

Export and

import duty

Land and

building tax

Overseas income

tax withheld at

source (PPH 26)

Luxury-goods

sales tax

Stamp duty

25%

The following taxes are stipulated based on taxable income.

50 million rupiahs or less: 5%; more than 250 million rupiahs to 500 million rupiahs or less: 25%

More than 50 million rupiahs to 250 million rupiahs or less: 15%; more than 500 million rupiahs: 30%

10% with respect to the sale of goods and the provision of servicesIn the case of exports the tax is exemptedAnimal feed, agricultural goods, mining products, medical health services, public transportation, educational services, social welfare services, mail services, etc. are non-taxable

The import duty is taxable at the tax rate of 0% to 150% of the appraised customs value of the imported goods.

(Japan and Indonesia concluded a bilateral free trade agreement in 2008. Exports from Japan: 90% tax reduction. Exports from Indonesia: 93% tax reduction)

This is based on the government construction sales price decided by the Ministry of Finance every three years and applies a uniform 0.5% of the following taxable amountsIn the case of less than 1, billion rupiahs: 20% of the government construction sales price In the case of 1, billion rupiahs or more: 40% of the government construction sales price

Withholding tax with respect to foreign services: basic tax rate of 20% (dividends, interest, royalties, etc. remitted overseas. In the case that there is a tax treaty, the tax is in accordance with that treaty.) Based on the tax treaty, the rate for Japan is 10% (in the case of dividends to Japan, if the investment ratio is 25% or more: 10%; if the investment ratio is less than 25%: 15%)

The tax rate of the luxury-goods sales tax is 10% to 75%, and the items subject to the tax are classified into seven taxable categories based on their degree of luxury.They are taxable only once, either when a manufacturer of luxury goods delivers the luxury goods or when the luxury goods are imported. Dairy products, juices, carbonated drinks, cosmetics, photographic film, carpets, rugs and mats, etc. are outside the scope of the taxation

For notarial deeds, contracts, receipts, checks, etc. the stamp duty is 6,000 rupiahs when the money value stated in the document is more than 1 million

rupiahs and 3,000 rupiahs when the money value stated in the document is 1 million rupiahs or less.

(Source) Prepared by the Mizuho Bank Global Strategic Advisory

Department based on JBIC materials and JCIF materials

Prepaid import

tax (PPH 22)

Importers that possess an import license (API): (general consumer goods): 2.5%

Importers that do not possess an import license (API) and consumer goods other than the above: 7.5%

Domestic income

tax withheld at

source (PPH 23)

Withholding tax with respect to domestic services: basic tax rate of 15% (dividends, interest (bank interest is separate), royalties, etc. that are generated inside

Indonesia)

Tax rate with respect to other domestic service-related fees: 2%

Entry format (i) ~ Overview

6

The basic investment and entry format in Indonesia is as follows.

In the majority of industry types entry using the branch format is not permitted, so the general approach is entry as a local

corporation

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on a full range of information

The basic investment and entry format in Indonesia

Direct investment (local subsidiaries: PT)

Entry using a branch is not permitted except

for some industry types such as financial

institutions, etc.

Establishment of a branch

Commercial activities are not permitted

Establishment of a representative office

100% foreign

investment

Joint ventures

Other

Investment by a single or

multiple foreign enterprises

Joint ventures with Indonesian

enterprises (state-run and private

sector) and individuals

Investment on the basis of

individual private sector and

government-affiliated projects

In the case of direct investment, there are the

following three basic formats.

1 2 3

Period necessary for formation: about 3~6

months Period necessary for formation: about 1.5

months

Foreign representative

office

Foreign representative

trading office

Foreign construction

company representative

office

Gathering of a full range of

information, formation of a local

corporation, preparation, etc.

Promotion, information

gathering, and buying and selling

agents are possible.

Construction service activities

through joint ventures with local

construction companies are

possible

In the case that activities for profit are included in

the content of the activities in Indonesia, formation

of a local corporation becomes an option

In the majority of industry types the branch format

is not permitted

If only auxiliary operations (mediation for the

overseas parent company, sales promotion, and

information gathering) are to be carried out, the

representative office format also becomes an

option. (In the case of a construction business,

partial operations are possible.)

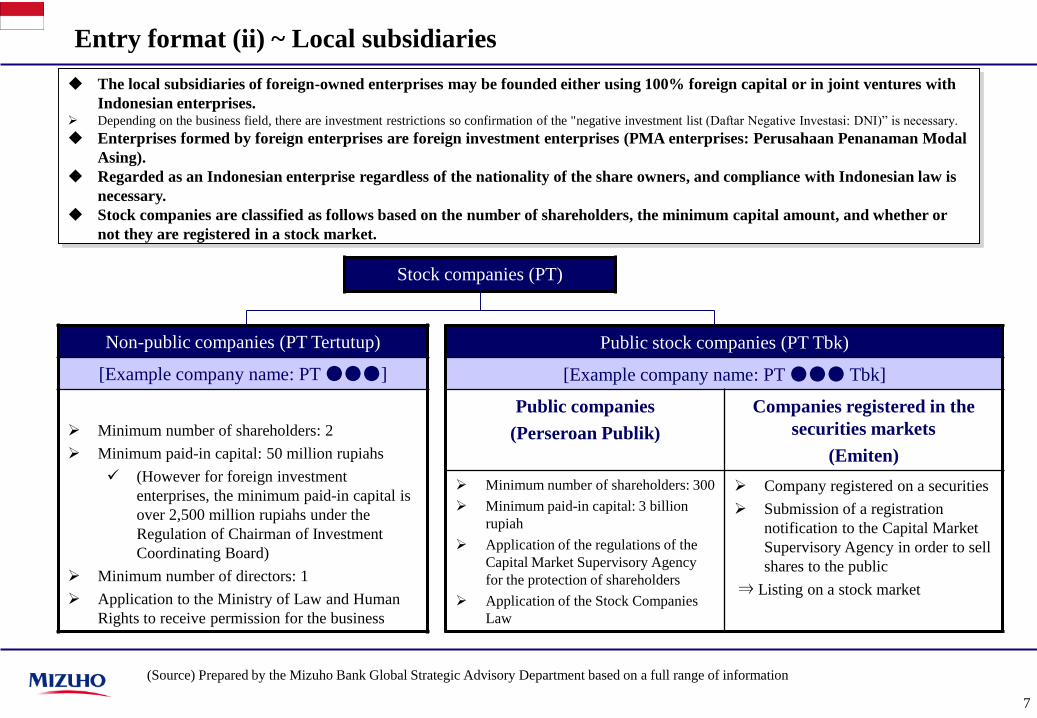

Entry format (ii) ~ Local subsidiaries

7

The local subsidiaries of foreign-owned enterprises may be founded either using 100% foreign capital or in joint ventures with

Indonesian enterprises. Depending on the business field, there are investment restrictions so confirmation of the "negative investment list (Daftar Negative Investasi: DNI)” is necessary.

Enterprises formed by foreign enterprises are foreign investment enterprises (PMA enterprises: Perusahaan Penanaman Modal

Asing).

Regarded as an Indonesian enterprise regardless of the nationality of the share owners, and compliance with Indonesian law is

necessary.

Stock companies are classified as follows based on the number of shareholders, the minimum capital amount, and whether or

not they are registered in a stock market.

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on a full range of information

Non-public companies (PT Tertutup)

[Example company name: PT●●●]

Minimum number of shareholders: 2

Minimum paid-in capital: 50 million rupiahs

(However for foreign investment

enterprises, the minimum paid-in capital is

over 2,500 million rupiahs under the

Regulation of Chairman of Investment

Coordinating Board)

Minimum number of directors: 1

Application to the Ministry of Law and Human

Rights to receive permission for the business

Public stock companies (PT Tbk)

[Example company name: PT●●● Tbk]

Public companies

(Perseroan Publik)

Companies registered in the

securities markets

(Emiten)

Minimum number of shareholders: 300

Minimum paid-in capital: 3 billion

rupiah

Application of the regulations of the

Capital Market Supervisory Agency

for the protection of shareholders

Application of the Stock Companies

Law

Company registered on a securities

Submission of a registration

notification to the Capital Market

Supervisory Agency in order to sell

shares to the public

⇒ Listing on a stock market

Stock companies (PT)

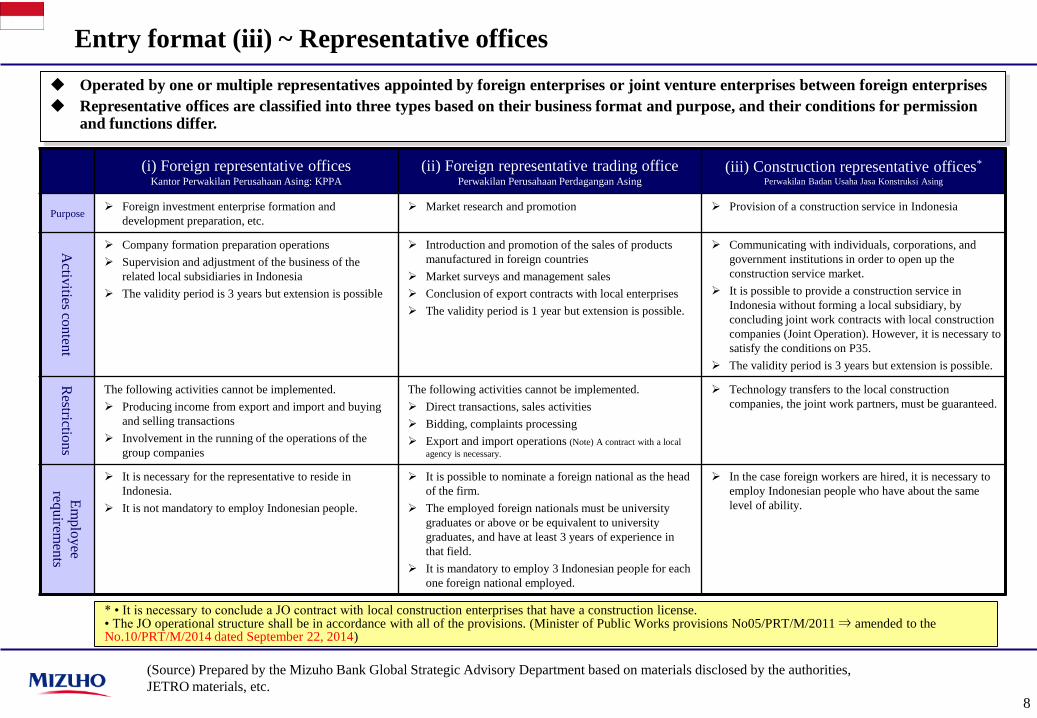

Entry format (iii) ~ Representative offices

8

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on materials disclosed by the authorities,

JETRO materials, etc.

Operated by one or multiple representatives appointed by foreign enterprises or joint venture enterprises between foreign enterprises

Representative offices are classified into three types based on their business format and purpose, and their conditions for permission and functions differ.

(i) Foreign representative offices Kantor Perwakilan Perusahaan Asing: KPPA

(ii) Foreign representative trading office Perwakilan Perusahaan Perdagangan Asing

(iii) Construction representative offices*

Perwakilan Badan Usaha Jasa Konstruksi Asing

Purpose Foreign investment enterprise formation and

development preparation, etc.

Market research and promotion Provision of a construction service in Indonesia

Activ

ities conten

t

Company formation preparation operations

Supervision and adjustment of the business of the

related local subsidiaries in Indonesia

The validity period is 3 years but extension is possible

Introduction and promotion of the sales of products

manufactured in foreign countries

Market surveys and management sales

Conclusion of export contracts with local enterprises

The validity period is 1 year but extension is possible.

Communicating with individuals, corporations, and

government institutions in order to open up the

construction service market.

It is possible to provide a construction service in

Indonesia without forming a local subsidiary, by

concluding joint work contracts with local construction

companies (Joint Operation). However, it is necessary to

satisfy the conditions on P35.

The validity period is 3 years but extension is possible.

Restrictio

ns

The following activities cannot be implemented.

Producing income from export and import and buying

and selling transactions

Involvement in the running of the operations of the

group companies

The following activities cannot be implemented.

Direct transactions, sales activities

Bidding, complaints processing

Export and import operations (Note) A contract with a local

agency is necessary.

Technology transfers to the local construction

companies, the joint work partners, must be guaranteed.

Em

plo

yee

requ

iremen

ts

It is necessary for the representative to reside in

Indonesia.

It is not mandatory to employ Indonesian people.

It is possible to nominate a foreign national as the head

of the firm.

The employed foreign nationals must be university

graduates or above or be equivalent to university

graduates, and have at least 3 years of experience in

that field.

It is mandatory to employ 3 Indonesian people for each

one foreign national employed.

In the case foreign workers are hired, it is necessary to

employ Indonesian people who have about the same

level of ability.

* • It is necessary to conclude a JO contract with local construction enterprises that have a construction license.• The JO operational structure shall be in accordance with all of the provisions. (Minister of Public Works provisions No05/PRT/M/2011 ⇒ amended to the No.10/PRT/M/2014 dated September 22, 2014)

Investment promotion

Indonesia has 32 industrial parks that offer the following preferential treatment systems for companies expanding into Indonesia

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on JETRO and JCIF materials, etc.

Encouraged investment

Preferential

treatments by

industry type

Preferential treatment

systems for foreign capital

Preferential

treatments by

region

Other preferential

treatments

Preferential treatment

systems in the Eastern

Region of Indonesia

(KTI)

Preferential treatment

systems in bonded

zones (KB)

Preferential treatment

systems in free trade

zones (FTZ)

Exemptions from

import duties

Tax allowances

Corporate tax allowances

Tax holidays

Temporary exemptions from

corporate tax

Preferential treatment

systems in Integrated

Economic Development

Zones (KAPET)

9

Regulations related to the Company Law

10

The current Company Law of Indonesia was established in 2007 and is comprised of a total of 161 articles.

The commercial law of Indonesia has been greatly influenced by the law of the Netherlands, and even in the modern era when the Company Law was established systems derived from the law of the Netherlands such as the system of the Komisaris Board, etc. survive.

The highest law regulating investment activities by foreign enterprises with respect to Indonesia is the Investment Law.

The first legal procedures when forming PMA (foreign capital) enterprises are application to the Investment Coordinating Board (BKPM) for basic investment permission and acquisition of the basic investment permission.

The positioning of the Company Law

(Source) Prepared by the Mizuho Bank Global Strategic Advisory Department based on JETRO materials, Ministry of Justice materials, etc.

Major points of difference from the stock companies of Japan

“Company” under the Company Law means a stock company (Perseroan

Terbatas), and the liability of the stockholders is limited liability in the same

way as for stock companies in Japanese law.

Stock companies are classed as “non-public companies” and “public

companies (Perseroan Terbuka)" and the latter are classed as "major

companies (Perseroan Publik)" and "companies which make public share

offerings." (Most Japanese enterprises take the format of non-public

companies.)

In Indonesia, unlike Japan, stock companies with one shareholder are not

permitted, and a minimum of 2 shareholders is necessary even in business

fields in which foreign capital with a 100% stake is possible.

If 2 shareholders are formally in place, for example the parent company in

Japan and its representative director, etc., then the requirement under the

Company Law is satisfied regardless of the relationship between the

minimum 2 shareholders.

The matters that it is necessary to state in the Articles of Incorporation

(Anggaran Dasar), the fundamental principles of a stock company, are

largely similar to the Articles of Incorporation in Japanese law, and as long

as the provisions of the Company Law are not violated the stipulation of

optional provisions in the Articles of Incorporation is permitted.

Permissiveness regarding formation Stock companies are formed when 2 or more individuals or corporations

(hereinafter referred to as “incorporators”) prepare a formation notarial deed and obtain the permission of the Minister of Law and Human Rights.

Each of the incorporators must subscribe to some of the shares of the company; therefore a minimum of 2 shareholders exist in stock companiesfrom the time of their formation.

Stipulation of the minimum capital amount Under the Company Law, authorized stated capital must be a minimum of 50

million rupiahs Under the Investment Coordinating Board Chairman rules, PMA (foreign

capital) enterprises are required to have an investment amount (the stated capital and the business funds procured through borrowings) of over 10 billion rupiahs and paid-in stated capital of 2.5 billion rupiahs or more, and the minimum paid-in capital under the Company Law is not applied. (There are minimum paid-in capital requirements under the Commerce Law forspecific industry types.)

Komisaris Boards These are institutions that supervise the company management by the Board

of Directors and offer advise regarding management to the Board of Directors (institutions similar to the board of company auditors in Japan).

Under the Company Law, each Komisaris bears the duty of care of a good manager with respect to companies in the same way as the directors, and in the case that the company incurs damages due to a violation by a Komisaris, said Komisaris bears liability as an individual to pay compensation for thedamages to the company.

11

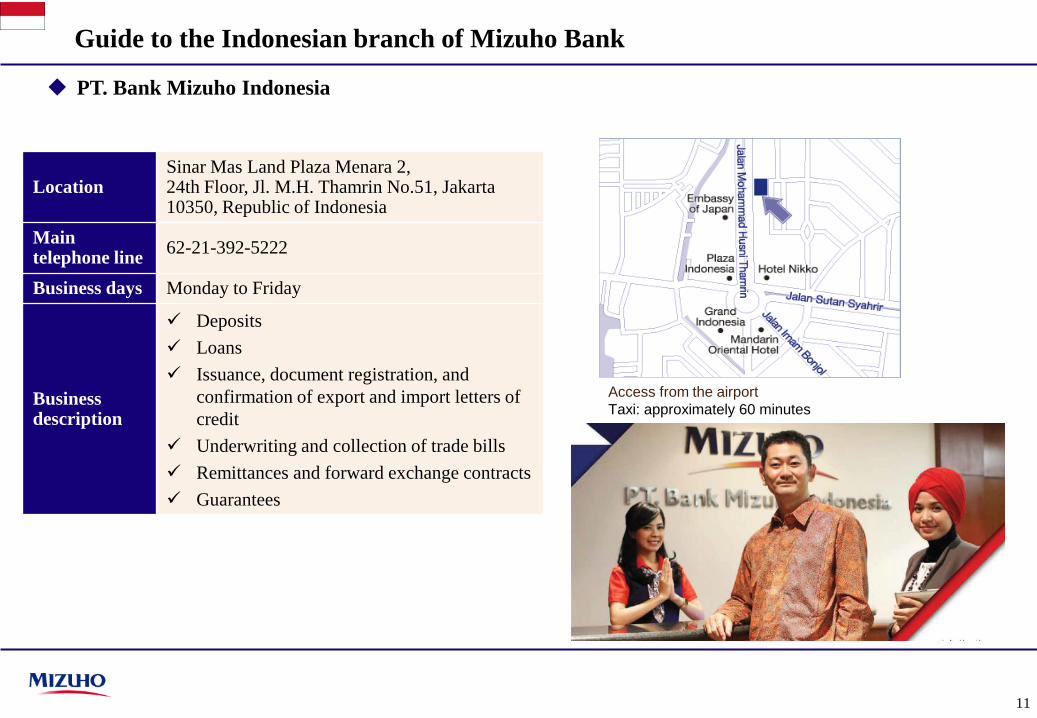

Guide to the Indonesian branch of Mizuho Bank

LocationSinar Mas Land Plaza Menara 2, 24th Floor, Jl. M.H. Thamrin No.51, Jakarta 10350, Republic of Indonesia

Main telephone line

62-21-392-5222

Business days Monday to Friday

Business description

Deposits

Loans

Issuance, document registration, and

confirmation of export and import letters of

credit

Underwriting and collection of trade bills

Remittances and forward exchange contracts

Guarantees

PT. Bank Mizuho Indonesia

Access from the airport

Taxi: approximately 60 minutes

約30km/60分

タクシー利用:通常時

スカルノハッタ国際空港

ジャカルタ市内中心部

当社オフィス

日本大使館

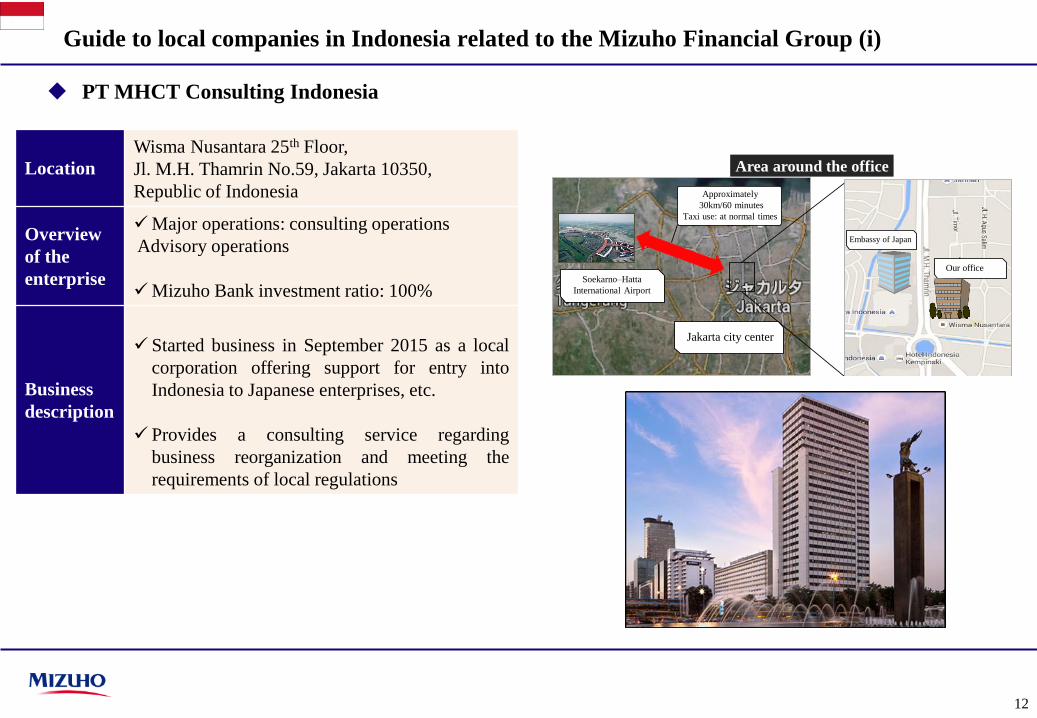

PT MHCT Consulting Indonesia

12

Guide to local companies in Indonesia related to the Mizuho Financial Group (i)

Area around the officeLocation

Wisma Nusantara 25th Floor,

Jl. M.H. Thamrin No.59, Jakarta 10350,

Republic of Indonesia

Overview

of the

enterprise

Major operations: consulting operations

Advisory operations

Mizuho Bank investment ratio: 100%

Business

description

Started business in September 2015 as a local

corporation offering support for entry into

Indonesia to Japanese enterprises, etc.

Provides a consulting service regarding

business reorganization and meeting the

requirements of local regulations

Approximately

30km/60 minutes

Taxi use: at normal times

Embassy of Japan

Our office

Jakarta city center

Soekarno–Hatta

International Airport

PT Mizuho Balimor Finance

13

Guide to local companies in Indonesia related to the Mizuho Financial Group (ii)

Location

Grha 137 Building, 7th Floor,

Jl. Pangeran Jayakarta No.137, Jakarta 10730,

Republic of Indonesia

Overview

of the

enterprise

Major operations: automobile loan and lease

operations

Mizuho Bank investment ratio: 51%

Business

description

In 2011 Mizuho acquired 51% of the shares

issued by Balimor Finance, converting said

company into a consolidated subsidiary of the

Bank.

Provides an automobile-related finance

business in Indonesia (centered on the

automobile loan and lease business)

14

Business alliance ~ Bank Negara Indonesia

(i) Collaboration regarding liquidity

⇒Mutual exchange of the dollars possessed by Mizuho and the rupiahs possessed by BNI

(ii) Collaboration in the funds management service

⇒ Provision of a cash management service utilizingthe broad network of BNI

(iii) Collaboration regarding the retail business for

clients

⇒ Provision of a retail banking service including accounts for receiving salaries, credit cards, etc.

(iv) Collaboration regarding cross-border

M&As/business matching

⇒Mashing the investment needs of Mizuho clients with the investment acceptance needs of BNI clients

(v) Support for the provision of information to BNI

clients

⇒ BNI will be able to provide information to its clients utilizing Mizuho’s global network

In February 2013 Mizuho Bank concluded an MOU (memorandum of understanding) regarding a business alliance with Bank

Negara Indonesia (BNI). This makes working together in a wide range of fields possible, including utilizing the network

covering all of Indonesia possessed by BNI for our customers, the introduction of business mashing destinations, the use of the

retail banking service, etc.

• Bank Negara Indonesia (BNI) is the fourth-largest state-run bank in Indonesia by asset size. In 1996 it

became the first state-run bank to achieve listing on a

stock market. Its domestic branch network consists of

approximately 920 branches. Its distinguishing feature

is that it has a client base of blue-chip local enterprises,

centered on state-run enterprises. It is the only state-run

bank of Indonesia that has a branch in Tokyo.

[Main prizes, etc. won by BNI]

• Best Local Cash Management Award

⇒Won an award at Asia Money (2010, 2011, 2012, and 2015)

• Best Cash Management Solution Provider in

Southeast Asia

⇒Won an award at Alpha South East Asia (2011) • Became a funds management bank for leading oil and

gas enterprises

⇒ PT. Medco E&P Indonesia, Total EP Indonesia etc.

Content of the alliance Overview of Bank Negara Indonesia (BNI)

Disclaimer

15

© 2018 Mizuho Bank, Ltd.

These materials have been prepared solely for the purpose of providing information relating to financial solutions, and are not intended to induce

or introduce readers to engage in any particular financial transaction. Nor do they assume any transaction with any Mizuho Financial Group

company.

These materials have been prepared based on information adjudged to be reliable and accurate, but Mizuho Bank, Ltd., does not guarantee its

reliability or accuracy. Readers are requested to exercise their own judgment when using these materials and, if necessary, to consult with

lawyers, certified public accountants, tax accountants, and other experts in this regard.

The entire content of these materials is subject to the copyright of Mizuho Bank, Ltd., with all rights reserved. Accordingly, these materials, in

whole or in part, may not be (i) copied, photo copied, or reproduced in any other means, or (ii) redistributed without written consent of Mizuho

Bank, Ltd.

![BENEFICIAL OWNERSHIP, TAX TREATIES AND INTERNATIONAL TAX ... · Article 11 - Interest - 2002 Indonesia/NL Tax Treaty: 1. Interest arising in [Indonesia] and paid to a resident of](https://static.fdocuments.net/doc/165x107/5ccd654d88c993b2538e1911/beneficial-ownership-tax-treaties-and-international-tax-article-11-interest.jpg)