INVESTMENT ADVISER’S LETTER TO … ADVISER’S LETTER TO SHAREHOLDERS SEMI-ANNUAL REPORT ......

48

TWEEDY, BROWNE FUND INC. This booklet consists of two separate documents: INVESTMENT ADVISER’S LETTER TO SHAREHOLDERS SEMI-ANNUAL REPORT Tweedy, Browne Global Value Fund Tweedy, Browne Global Value Fund II – Currency Unhedged Tweedy, Browne Value Fund Tweedy, Browne Worldwide High Dividend Yield Value Fund September 30, 2012

Transcript of INVESTMENT ADVISER’S LETTER TO … ADVISER’S LETTER TO SHAREHOLDERS SEMI-ANNUAL REPORT ......

TWEEDY, BROWNE FUND INC.

This booklet consists of two separate documents:

INVESTMENT ADVISER’S LETTERTO SHAREHOLDERS

SEMI-ANNUAL REPORT

Tweedy, Browne Global Value FundTweedy, Browne Global Value Fund II – Currency Unhedged

Tweedy, Browne Value FundTweedy, Browne Worldwide High Dividend Yield Value Fund

September 30, 2012

TWEEDY, BROWNE FUND INC.

Investment Adviser’s Letter to Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I-1

Semi-Annual Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-1

Tweedy, Browne Fund Inc.Expense Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-2

Tweedy, Browne Global Value FundPortfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-3Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-5Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-5Schedule of Forward Exchange Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-5

Tweedy, Browne Global Value Fund II – Currency UnhedgedPortfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-7Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-9Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-9

Tweedy, Browne Value FundPortfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-10Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-11Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-11Schedule of Forward Exchange Contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-11

Tweedy, Browne Worldwide High Dividend Yield Value FundPortfolio of Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-12Sector Diversification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-13Portfolio Composition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-13

Tweedy, Browne Fund Inc.Statements of Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-14Statements of Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-15Statements of Changes in Net Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-16Financial Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-18Notes to Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-20Investment in the Fund by the Investment Adviser and Related Parties . . . . . . . . . . . . . . . . . . . . II-23Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-27

TWEEDY, BROWNE FUND INC.

Our Investment Team

This page left blank intentionally.

TWEEDY, BROWNE FUND INC.

Investment Adviser’s Letter to Shareholders (Unaudited)

… the riskiness of an investment is not measured by beta (aWall Street term encompassing volatility and often used inmeasuring risk) but rather by the probability – the reasonedprobability – of that investment causing its owner a loss ofpurchasing power over his contemplated holding period. Assetscan fluctuate greatly in price and not be risky as long as they arereasonably certain to deliver increased purchasing power overtheir holding period. And as we will see, a nonfluctating assetcan be laden with risk.

– Warren Buffett, Why Stocks Beat Gold and Bonds,Fortune Magazine, February 27, 2012

Since we last wrote to you in early May, the net change inmost developed market equity indices has been relativelyminor, but the ride between then and now measured by theswings in these indices has been anything but dull. Manymarket indices around the world declined as much as 15% to20% between late March and early June and then seeminglythrew off concerns about a worrisome world and ran back upto the levels seen in late Spring. If you had just returned froma six-month sabbatical to the South Pole, no doubt you wouldhave concluded that you had not missed much, and thereturns year-to-date are probably better than a cursoryassessment of the world’s financial health would havesuggested last December. In fact, aside from a modestlyencouraging flow of news in the past few months fromEuropean capitals, in our estimation not much has happenedthat will dramatically change the uncertain outlook in thecoming months. Wall Street “physicians” have diagnosed thepast several months as a “traditional” summer rally althoughwe don’t know how “traditional” those rallies are. Oddly, atthe same time, we have an environment that Grant’s InterestRate Observer described as one in which “safety” is in abubble. Shorter term interest rates (up to 2 years) in manycountries are negative, meaning you have to pay the borrowerfor the privilege of holding their paper. Our ten year treasurybond, which is a bellwether measure for the cost of money,currently yields about 1.8%. Surely not much of a return ifheld to maturity, and that leaves aside any discussion aboutthe purchasing power of those dollars in ten years if youdecide to hang on until maturity. Despite these yields, moneycontinues to flow into government securities, money marketfunds and many bond funds. Further evidence of this “safetybubble” is the increased issuance of corporate debt,presumably to “lock in” low interest rates. Finally, in anexample of unintended consequences, private equity firmshave been able to increase their issuance of debt to paythemselves and their investors large dividends driven in partby the low returns available elsewhere in the fixed incomemarkets. Our hunch again is the cost of money must be a keydriver of their decision since the case for a “robust” macroenvironment is weak. We are sure it comes as no surprise toyou that we believe there are better opportunities in theequity markets.

When it comes to the year ahead, those in the business ofpredicting market movements are seemingly looking atdifferent facts since there is not much agreement amongthem. We are reminded in some ways of the presidentialcandidates’ discussion over taxes and the budget. Can theypossibly be looking at the same data? Now we certainly arenot going to burden you with our politics and we are in noway trying to be smug in our comments about market“forecasting.” As we have said before, we believe the task oftrying to get the “market direction” right over a limited timeperiod is not the best way to evaluate the merits of anyparticular investment. Put simply, we operate with a differentinvestment horizon and a different perspective. As investors,we own businesses and we like the productive capital-building nature of their assets. Our job is to try and determinewhat that business will look like in three to five years and buyit at a discount from our estimate of business value. If we canget these variables about right, our expectation is we willmake out very well over time.

So what has changed from our perspective since our lastletter other than some halting steps in the right direction inEurope? The answer has to be “Not a lot.” Certainly, at themacroeconomic level, the U.S. economy continues to grow ata rate insufficient to make much of a dent in theunemployment rate and provide employment opportunitiesfor our college graduates and unemployed. The solutionobviously requires an end to political gridlock and a plan/compromise which puts us back on a sustainable fiscal path.There is little disagreement over the view that the currentpath is not sustainable. To get to a sustainable path willrequire more deal makers and fewer ideologues. A credibleplan could very likely have a significant impact on theeconomy since the critical missing ingredient is confidence.Interest rates and the cost of money is not standing in the wayof a pickup in economic activity. On a positive note, at themicroeconomic level corporations are generally faring quitewell. Balance sheets are strong, costs are under control and inthe case of businesses that operate on a global basis (many ofwhich we own), they are doing well in those markets whereyou would expect them to do well. What they are also doingis sitting on their liquidity for the most part rather thaninvesting, which is rational given the circumstances. An endto political brinkmanship would no doubt have a realbeneficial impact on markets. Very much the same can besaid about Europe as about the U.S. Europe faces the samedemographic/entitlement problems but has the addedproblem of much more rigid labor markets and a need tomove toward a more federal political structure, certainly withregard to banking regulation as a first step. Recent discussionsin Europe, at the policy level, have taken on a more hopefultone. A common currency will ultimately be difficult tomaintain without further fiscal and financial integration andpoliticians seem to be inching in the direction of furtherintegration. At the end of what is likely to be a bumpy ride,we think it would be wrong to bet that the “political class”will drive the rest of us off the economic cliff. In the

I-1

meantime, we want to own the most resilient and financiallysound businesses we can find when the market puts them upfor sale at a discount.

As we have mentioned many times in past reports, ourreturns over time in individual stocks are derived from theclosing of the discount between our original purchase priceand our estimate of intrinsic value, and from the futurecompounding of the businesses’ underlying value. Given therise in equity prices, it should come as no surprise that thediscount in many of our holdings has narrowed, with futurereturns in some of our holdings becoming more reliant on thecompounding of intrinsic value. Nonetheless, we still havenumerous stocks that are priced at a discount from ourestimates of intrinsic value. What does all this mean for ourinvestors? First, valuation informs our outlook and theadvance in global equity prices over the last six months hasmade our job of finding attractive entry points into new stockideas much more difficult, and new opportunities are certainlyturning up with less frequency. Secondly, we have beentrimming and, in a few instances selling, securities that havereached our estimates of intrinsic value. This includes manyof our steady consumer products companies such as Nestle,Heineken, Diageo, Philip Morris International and the likewhere we have enjoyed very satisfactory returns. We willcontinue to hold several of these companies as their prospectsfor future compounding of intrinsic value remain high, butsome will have to go. Some of the proceeds from these trimsand sales have found their way into industrial companies thatare a bit more economically sensitive where we have foundpricing opportunities as investors have begun to discount aslowing global economy. The rest has gone into cash reserves.If equity markets continue to march forward in the weeks andmonths ahead, cash reserves will likely build at the margin inour Funds.

Performance Results

We are pleased to report that the performance of all fourof our Funds has been quite good on both an absolute andrelative basis over the last six months. Three of our Fundshave achieved double-digit rates of return year-to-datethrough September 30, 2012. Worldwide High DividendYield Value Fund is up over 9% for the same period. Whilethis is really good news, as we mentioned, we have also had tosell and trim back a number of positions that traded up to ourestimates of intrinsic value resulting in a modest level ofrealized gains in our portfolios. This means that the tax manthis year will be sharing in small part in our good fortune.Over the longer term, in all of our Funds, the tax man’s takehas typically been de minimus. We are very proud of the factthat all four Funds, since their respective inceptions, have notonly outperformed their respective benchmarks net of feesand expenses, but they have also outperformed these samebenchmarks net of estimated taxes on distributions andassuming a sale at the end of the period. Since its inceptionover 19 years ago, our flagship Fund, the Tweedy, BrowneGlobal Value Fund, has outperformed the hedged andunhedged MSCI EAFE Index by over 365 basis points on anannualized basis net of fees, expenses and taxes, and this iswithout applying a fee against, or tax effecting, the Index.This is in large part related to the Fund’s longer term

investment horizon and associated low levels of annualportfolio turnover, which have averaged approximately 13%annually since the Fund’s inception (through fiscal year-endMarch 31, 2012).

Presented below are investment results of the fourTweedy, Browne Funds, through September 30, 2012, withcomparisons to the indices we consider relevant.*

Tweedy, Browne Global Value Fund

Period Ended9/30/12

Returnbefore

Taxes**

Returnafter

Taxes onDistributions**

Return afterTaxes on

Distributions &Sale of Fund

Shares**

MSCIEAFE

Index(1)(2)

(Hedgedto US$)

MSCIEAFE

Index(1)(2)

(in US$)

3 Months 5.12% 5.12% 3.33% 4.67% 6.92%

6 Months 3.57 3.57 2.32 -0.69 -0.70

1 Year 19.23 18.70 13.59 14.15 13.75

3 Years 9.92 9.82 8.76 1.50 2.12

5 Years 0.46 -0.23 0.47 -5.70 -5.24

10 Years 9.36 8.87 8.37 5.43 8.20

15 Years 7.69 6.65 6.40 2.47 3.37

Since Inception(6/15/93)(3) 9.77 8.75 8.41 4.62 4.73

Total Annual Fund Operating Expense Ratio as of 3/31/12: 1.40%†

Tweedy, Browne Global Value Fund II –Currency Unhedged

Period Ended9/30/12

Returnbefore

Taxes**

Returnafter

Taxes onDistributions**

Return afterTaxes on

Distributions &Sale of Fund

Shares**

MSCIEAFE

Index(1)(2)

(in US$)

MSCIEAFE

Index(1)(2)

(Hedgedto US$)

3 Months 6.48% 6.48% 4.21% 6.92% 4.67%

6 Months 2.57 2.57 1.67 -0.70 -0.69

1 Year 16.21 16.05 10.81 13.75 14.15

Since Inception(10/26/09)(3) 7.11 7.02 6.10 1.62 1.44

Gross Annual Fund Operating Expense Ratio as of 3/31/12: 1.44%†‡

Net Annual Fund Operating Expense Ratio as of 3/31/12: 1.41%†‡

Tweedy, Browne Value Fund

Period Ended9/30/12

Returnbefore

Taxes**

Returnafter

Taxes onDistributions**

Return afterTaxes on

Distributions &Sale of Fund

Shares**

S&P 500/MSCIWorldIndex

(Hedged toUS$)(1)(4)(5)(6)¶

MSCIWorldIndex

(Hedged toUS$)(1)(6)

S&P500(1)(5)

3 Months 4.98% 4.98% 3.24% 5.59% 5.59% 6.35%

6 Months 3.52 3.52 2.29 1.22 1.22 3.43

1 Year 21.79 21.11 14.92 21.40 21.40 30.20

3 Years 9.50 8.91 8.11 7.03 7.03 13.20

5 Years 2.06 1.01 1.57 -2.37 -2.37 1.05

10 Years 6.75 5.82 5.75 6.13 - 8.01

15 Years§ 4.92 3.98 4.01 3.48 - 4.70

Since Inception§(12/8/93)(3) 8.35 7.47 7.24 7.23 - 8.24

Total Annual Fund Operating Expense Ratio as of 3/31/12: 1.41%†

¶ S&P 500 (12/8/93-12/31/06)/MSCI World Index (Hedged to US$) (1/1/07-present).

I-2

Tweedy, Browne WorldwideHigh Dividend Yield Value Fund

Period Ended9/30/12

Returnbefore

Taxes**

Returnafter

Taxes onDistributions**

Return afterTaxes on

Distributions &Sale of Fund

Shares**

MSCIWorld

Index(1)(6)

(in US$)

3 Months 5.66% 5.66% 3.68% 6.71%

6 Months 2.88 2.38 1.85 1.30

1 Year 15.76 15.08 10.34 21.59

3 Years 9.64 9.25 8.22 7.48

5 Years 1.87 1.34 1.37 -2.15

Since Inception(9/5/07)(3) 2.08 1.56 1.55 -1.15

30-Day Standardized Yield (Subsidized) as of 9/30/12: 1.80%

30-Day Standardized Yield (Unsubsidized) as of 9/30/12: 1.81%

Gross Annual Fund Operating Expense Ratio as of 3/31/12: 1.39%†‡

Net Annual Fund Operating Expense Ratio as of 3/31/12: 1.39%†‡

* The preceding performance data represent past performance andis not a guarantee of future results. Total return and principalvalue of an investment will fluctuate so that an investor’s shares,when redeemed, may be worth more or less than their original cost.The returns shown do not reflect the deduction of taxes that ashareholder would pay on Fund distributions or the redemption ofFund shares. Current performance may be lower or higher than theperformance data shown. Please visit www.tweedy.com to obtainperformance data, which is current to the most recent month end.See page I-8 for footnotes 1 through 6, which describe the indicesand inception dates of the Funds. Results are annualized for allperiods greater than one year.

** After-tax returns are calculated using the historical highestindividual federal marginal income tax rates, and do not reflect theimpact of state and local taxes. Returns after taxes on distributionsare adjusted for federal income taxes associated with funddistributions, but do not reflect the federal income tax impact of gainsor losses recognized when fund shares are sold. Returns after taxeson distributions and sale of fund shares are adjusted for federalincome taxes associated with fund distributions and reflect the federalincome tax impact of gains or losses recognized when fund shares aresold. Actual after-tax returns depend on an investor’s tax situationand may differ from those shown. Additionally, the after-tax returnsshown are not relevant to investors who hold their Fund sharesthrough tax-deferred arrangements such as 401(k) plans orindividual retirement accounts.

† The Funds do not impose any front-end or deferred sales charge.However, the Tweedy, Browne Global Value Fund, Tweedy,Browne Global Value Fund II – Currency Unhedged and Tweedy,Browne Worldwide High Dividend Yield Value Fund impose a 2%redemption fee on redemption proceeds for redemptions or exchangesmade within 60 days of purchase. Performance data does not reflectthe deduction of the redemption fee, and if reflected, the redemptionfee would reduce the performance data quoted for periods of 60 daysor less. The expense ratios shown above reflect the inclusion ofacquired fund fees and expenses (i.e., the fees and expensesattributable to investing cash balances in money market funds) andmay differ from those shown in the Funds’ financial statements.

‡ Tweedy, Browne Company LLC (the “Adviser”) hascontractually agreed to waive its investment advisory fee and/or to reimburse expenses of the Worldwide High Dividend

Yield Value Fund and Global Value Fund II — CurrencyUnhedged to the extent necessary to maintain the totalannual fund operating expenses (excluding fees and expensesfrom investments in other investment companies, brokerage,interest, taxes and extraordinary expenses) at no more than1.37%. This arrangement will continue at least throughDecember 31, 2013. In this arrangement the Worldwide HighDividend Yield Value Fund and Global Value Fund II —Currency Unhedged have agreed, during the two-year periodfollowing any waiver or reimbursement by the Adviser, torepay such amount to the extent that after giving effect tosuch repayment such adjusted total annual fund operatingexpenses would not exceed 1.37% on an annualized basis.The performance data shown above would be lower had feesand expenses not been waived and/or reimbursed.

§ The Value Fund’s performance data shown above wouldhave been lower had certain fees and expenses not beenwaived from December 8, 1993 through March 31, 1999.

/ /

We have written in past letters that it is not only thereturns that an investment advisor earns that determines hisor her effectiveness. Of equal, if not more importance, is howthose returns were achieved. We have always felt that buyingat large discounts from estimated intrinsic value; diversifyingby issue, industry, country and market cap; taking aconservative approach to business appraisal; and avoidinghighly leveraged businesses helped to limit the risks we havetaken with our shareholders’ and our own money. We wouldagree wholeheartedly with the Oracle of Omaha, WarrenBuffett, that volatility, or the day-to-day movement of stockprices, is not real risk. That said, some of our clients andfinancial advisors do use statistical tools to try to measure therisks that investment advisors take while investing theirclients’ capital. While we do not pay much, if any, attentionto such statistical measures, we thought we would share withyou just how the Tweedy, Browne Global Value Fund stacksup when viewed through such a lens.

For example, one measure that consultants and financialadvisors use to evaluate an advisor’s performance is upside anddownside capture. This compares how much of the upside anadvisor generally captures in strong market environments tothe amount of the downside the advisor captures in downmarkets. Evaluating our Global Value Fund’s performancewith this measure, we found that over the last ten yearsthrough September 30, 2012, the Fund capturedapproximately 94% of the return of its benchmark (MSCIEAFE Index (Hedged to US $))in up markets while capturingonly 72% of the return of that benchmark in down markets.This compares to a downside capture of 111% and an upsidecapture of 119% for the average Foreign Large Value fund atMorningstar.7 By limiting our losses in down markets, andparticipating fairly aggressively in up markets, we have beenable to beat our benchmark by roughly 395 basis points on anannualized basis over the last ten years. Now this outcome hasnot been produced by a secret formula on our part. Nor is itan outcome for which we have a statistical explanation.Moreover, we have no idea what next year will bring. Whatwe do know is the process has worked well most of the timeover long periods of time and in many markets.

I-3

Another measure that financial consultants use toevaluate the risks that an advisor takes is the manager’s“volatility” of returns, or how a fund’s returns vary around itsaverage return over time compared to the same measure ofvariance applied to its benchmark. A lower standarddeviation of returns or variance for the fund relative to itsbenchmark is considered by those consultants to be anindication that the fund is achieving its returns at a lowerlevel of risk than the benchmark. With respect to thismeasure, the Tweedy, Browne Global Value Fund’s returnsover the last ten years were earned with a level of volatilitythat was 87% that of its benchmark’s. Again, our commentson this matter are the same as our comments on the conceptof upside/downside capture.

Another measure some financial consultants use is“alpha.” A high and positive “alpha” in excess of aninvestment manager’s benchmark suggests the investmentmanager is producing attractive returns on a risk adjustedbasis. Here again, the Tweedy, Browne Global Value Fundhas achieved an “alpha,” which is 190% greater than that ofthe average Foreign Large Value fund at Morningstar for theten years ending September 30, 2012. Again, we wouldreiterate that measures of volatility and alpha assume that riskis “variance” and this is not something with which we wouldagree. Whether one’s perception of risk is grounded instatistics, or as is the case with us, in Benjamin Graham’sfundamental price-to-value relationship, the Tweedy, BrowneGlobal Value Fund has produced returns over the longer termthat are more than commensurate with the risks taken.

Our Fund Portfolios

Please note that individual companies discussed herein representholdings in our Funds, but are not necessarily held in all four of ourFunds. Refer to footnote 8 at the end of the letter for the individualweightings of these companies in the respective Funds.

A cursory review of our Funds’ portfolios’ top twenty-fivepositions might lead one to conclude that our portfolios aredominated by the stocks of branded consumer productscompanies. To be sure, our Fund portfolios have had asignificant exposure to food, beverage and tobacco companiesfor quite some time relative to benchmark indices, and thesecompanies have served us very well in an environment whereinvestors have often preferred steadier, underleveragedbusinesses that pay an attractive dividend. However, a closerexamination of our Funds’ portfolios would reveal a morediversified structure with significant exposure to oil & gascompanies, healthcare companies, financials and industrialcompanies in addition to our consumer stocks. This is simplya result of where we have uncovered undervalued securitiesover time.

Over the last couple of years, securities’ markets havebeen in a rather frenetic “risk on, risk off” state of mind asthey react almost daily to the ebb and flow of various“headline” macro risks, not the least of which has been theSouthern European crisis. We would suspect this marketcondition and the frequent trading it implies is welcomed bythe IRS, as most gains are likely to be short term, giving thegovernment a bigger bite of the profits. When the risk trade ison and investors are feeling more confident, the more

economically sensitive stocks, i.e., financials, industrials, mediaand oil & gas holdings, have tended to perform well. Incontrast, when the risk trade is off and investors are worried,the steadier, consumer products companies provided muchneeded ballast for our Funds. For the most part, in 2011 the risktrade was off, and our consumer stocks held up better than moststocks, and helped to propel our Funds to a strong relativeoutperformance of their respective benchmarks. On the otherhand, thus far, 2012 has been a good year for global equities.With the exception of April and May of this year when theSouthern European issue heated up, the markets have been“risk on.” While our consumer stocks for the most partcontinued to perform well, many of our more economicallysensitive issues, became leaders in our portfolios during theyear. This would include certain of our bank and insurancestocks as well as some of our media and industrial holdings.

In general, most stocks in our Funds’ portfolios are upnicely this year, and as we mentioned, caused us to trim, andin some instances sell stocks whose market prices are nowtrading at or near our estimate of their underlying intrinsicvalues. This list includes companies such as Diageo, Nestle,Philip Morris International, Kone, Henkel, Wal-Mart, ArcaContinental, and Fraser & Neave, among others. Some of theresulting cash from this pruning has found its way intocompanies outside the consumer sector, including industrial,energy and financial companies, but a growing portionremains unspent waiting for pricing opportunities. We wouldlike to highlight and share with you in more detail than weusually go into in these reports three companies in which wehave started to build a position. This should give you an ideaas to where value is showing up for us in today’s equitymarkets and remind you of the types of characteristics we liketo see in the companies in which we invest.

Safran

The first is a French aerospace company called Safran thatderives the majority of its earnings and value from its civil jetengine business. At our initial purchase price, we believed wewere paying approximately 9 x 2012 Earnings Before Interestand Taxes and Amortization (EBITA), and a much lowermultiple of prospective 2013 and 2014 EBITA.

The civil jet engine industry is an oligopolistic industrywith large barriers to entry, stable market shares, and longproduct cycles. The engine that comprises the majority ofSafran’s engine business is called the CFM56, which isproduced through a 50/50 joint venture with General Electriccalled CFMI. The CFM56 is the dominant engine on narrowbody aircraft where it has a 100% share on the Boeing 737and a 50% share on the A320 where it competes against aconsortium controlled by Pratt & Whitney called IAE. Boththe Airbus A320 and 737 have substantial backlogs anddeliveries should grow nicely over the next several years.Moreover, CFMI (Safran) has secured its status as the solesupplier on the new version of the 737 (737 Max) and as adual supplier on the new version of the A320 (A320 Neo),which ensures that CFMI will retain its dominant share onnarrow body planes well into the 2020s.

The jet engine business model is a “razor/razor blade”business. Jet engines are sold around cost, but the real money

I-4

is made on high margin (60%) spare parts, which areeffectively captive to the original equipment manaufacturer(OEM), giving Safran substantial pricing power. Generic(PMA) parts represent approximately 3% of the market andhave struggled to gain share for a variety of reasons, including:an expensive and time consuming certification process;leasing companies’ preference for OEM parts which betterpreserve residual aircraft values; airline concerns related tothe reputational risks associated with the failure of an engineequipped with PMA parts; and the increasing penetration of“power by the hour” contracts, whereby the OEM alsoperforms the overhaul work. As such, once an engine is sold,it is very likely guaranteed to generate a long-term stream ofspare parts revenue for the OEM. Each engine will have tovisit the shop for an overhaul 3 to 5 times over its life andwhile there is uncertainty regarding the exact timing of thevisit there is strong visibility and stability over multi-yearperiods.

Our research suggests that spare parts revenue for theCFM56 will experience significant growth over the next 3 to5 years driven by an increase in shop visits, price increases,mix shift benefits, and a catch-up from deferred maintenance.

Shop visits – On average the current generation ofengines stay on the wing for approximately eight to nine yearsbefore coming into the shop for an overhaul. This means thatcurrent shop visits are being driven in large part by deliveriesin 2004 and 1996, which were both trough years for CFM56deliveries. However, from 1996 to 2000 and 2004 to 2008engine deliveries grew by more than 100% and 70%,respectively, which should drive an increase in shop visitsover the next 3 to 5 years. It is also worth mentioning that asof December 2011, approximately 9,500 of the roughly 18,000engines in the active fleet had never been to the shop.

Price and Mix – Our research indicates that OEMs areable to raise prices on most spare parts by approximately5% per annum. Moreover, there is an ongoing mix shift fromfirst generation engine shop visits to second generationengine shop visits, which generate significantly higherrevenue per shop visit. We estimate that by 2015, secondgeneration engines will account for approximately 66% of allshop visits as compared to 52% in 2011.

Deferred maintenance – During industry downturnsairlines defer maintenance and reduce the scope of shop visitsto preserve cash. Historically this has resulted in very steeprecoveries in spare parts revenue when the cycle turns.Discussions with industry participants suggest that the airlinesare pushing up against the limits of these deferral strategiesand at some point these strategies will result in a substantialcatch-up.

We don’t believe the positive aspects of the civil jetengine business are reflected in Safran’s current valuation.Given the quality of the business, the stability of the industry,as well as strong growth prospects for the aftermarket, wethink Safran is conservatively worth 12 to 13 x forwardEBITA. It is also encouraging that comparable transactionshave occurred at significantly higher multiples. In October of2011, Pratt & Whitney purchased Rolls Royce’s 32.5% shareof IAE (the only competitor to CFMI in the narrow body

space) at an estimated high teens multiple of operatingincome bringing Pratt’s total ownership of IAE to 65%. Whilewe have never used a high teens comparable to value aprospective investment, always preferring to use moreconservative multiples, we were delighted to see that a veryhigh price had been paid by a knowledgeable acquirer for abusiness directly comparable to Safran.

As we have mentioned in past letters, value investors suchas ourselves often have a difficult time investing in hightechnology companies largely due to their frequent highvaluations, rapid rates of change in technology, and thepotential for obsolescence. The last thing in the world wewant to do is pay a high price for a rapidly growing businessthat gets leapfrogged by technological change shortly after webuy it. With this in mind, you might be surprised to knowthat we began building a position in Google back in Februaryof this year when the stock dipped down to around $565 pershare. At this price, we felt we were getting a bargain, payingroughly 12.5 x 2012 estimated earnings net of the cash on itsbalance sheet. And this was for a business that grows its topline at greater than 20% per year.

Google principally provides paid search, which is aneffective, measurable, and high return on investment form ofadvertising. Google provides paid search on desktopcomputers, tablets, and mobile phones and has market sharesthat range from 65% to 85% throughout much of the world.Additionally, Google has one of the largest Displayadvertising networks in the industry, which is growingextremely fast and is quickly becoming a more meaningfulpart of the business.

Paid search is more mature today than it was in 2005 andwe think that future growth will slow. Nevertheless, Googlegrew revenue roughly 24% in the first half of 2012 on acurrency exchange rate neutral basis and our research suggeststhat paid search is still relatively underpenetrated.Advertising dollars have not yet caught up with the ongoingshift to ecommerce and digital media consumption, whichwill continue to drive dollars to paid search as well asGoogle’s fast growing global display network. Display has thepotential to be a large business as it is driven in large part bybrand based ad spending which accounts for the vast majorityof global ad spending.

With market shares in the search business that range from65% to 85% in most countries throughout the world, it isreasonable to conclude that Google has a strong competitiveposition. Google’s revenue is roughly 15 times higher than itsnearest competitor, which has enabled them to putsignificantly more money into R&D, distribution, and thedevelopment of products and eco-systems that furtherpromote and protect the use of Google’s search. Moreover, asMicrosoft’s investment in search can attest, the searchbusiness is expensive to enter. However, like everyinvestment we make, Google is not without risks. Verticalsearch, uncertainty regarding future growth rates, and risksrelated to Apple’s strong share in smartphones and tablets allneed to be monitored closely. Nevertheless, we feel thatGoogle is well positioned to protect its interests and, perhaps

I-5

most importantly, we paid a price that we felt more thandiscounted these potential risks.

We bought Google at roughly 12.5 x 2012 estimatedearnings net of the cash on the balance sheet. We think thisis a very low valuation as companies with market leadingpositions secured by strong competitive advantages in seculargrowth markets typically do not trade at market multiples.Unlike most companies growing revenue over 20% perannum, Google is also able to generate significant free cashflow due to the phenomenal economics of paid search. Forthese reasons we believe Google is undervalued and deserves asignificantly above average multiple.

Vallourec

Vallourec is a vertically integrated producer of brandedpremium seamless steel pipes and connections that have avariety of industrial purposes, the most important of which isfor use in drilling for oil & gas, an application where the useof a strong, reliable pipe is critical. Although the company isheadquartered and listed in France, it is truly a globalenterprise with more than 70% of revenue generated outsideof Europe. Revenue from oil and gas operations accounted for61% of its total revenue in the last quarter. Vallourec’s oil &gas segment sells seamless steel pipes and connectionsprimarily for use in unconventional oil & gas plays in the U.S.,as well as in deepwater projects throughout the world. Thesetypes of wells use considerably more seamless pipes andconnections than traditional wells. More importantly, as newsources of oil and gas are in more difficult to drill locations,like deepwater offshore and unconventional shale, there isgrowth in demand for Vallourec’s capabilities. For example, in1990, deepwater offshore drilling was zero percent of global oilproduction. Today deepwater drilling produces roughly 5.5million barrels of oil per day, and is projected to produceroughly 9 million barrels per day by 2020. Also,unconventional gas (shale) has grown rapidly in recent years,and today represents 23% of annual U.S. gas production.

Vallourec has been in business for 100 years, and has alimited number of competitors in this niche business of highquality seamless pipes and connections. These products aredesigned to withstand the extreme temperature, pressure, andother factors related to more complex oil & gas drillingconditions and are protected by a multitude of patents andtechnical know-how. Vallourec’s customers are keenly awareof the environmental risks and safety requirements fordrilling, particularly offshore, and thus have a preference forhigh quality pipes and connections. The cost of these pipesand connections relative to the overall price to drill a well isvery low. The price of the pipes provided by Vallourec is 5%to 10% of the total cost of an oil\gas well, so there is little tobe gained by switching to a cheaper pipe, but a lot to lose.Given the potential for catastrophic environmental disasters(and significant fines), it would not be rational for a drillingcustomer to scrimp on price for this most important, yetrelatively inexpensive component of his or her well.

Facing higher costs in Europe, and with the potential tolower its production costs abroad, Vallourec recentlyembarked on a major expansion of its production facilities,adding new capacity in the U.S. and in Brazil. These facilities

will allow Vallourec to produce its products locally, instead ofproducing and exporting from Europe. In May 2012,Vallourec’s management made a number of announcements,including delays in qualification for the Brazilian plant andhigher than expected capital expenditures to bring the U.S.plant on line. The stock sold off significantly and reachedwhat we thought were quite attractive levels over the nextmonth, eventually bottoming near two-thirds of book value.This caught our interest. We began building a position in ourFunds in Vallourec at around 28 to 29 Euros per share in lateJune. At this price, we felt we were paying roughly 69% of thecompany’s stated book value, 82% of tangible book value, andtwo-thirds of a conservative estimate of the company’sintrinsic value. Given the rather concentrated nature of theseamless pipe industry, there were not a lot of comparableM&A deals to examine. However, in 2007, Tenaris, one ofVallourec’s major competitors, acquired Hydril, a leadingNorth American manufacturer of premium connections andpressure control products for 15 x EBIT. Consistent with ourconservative appraisal policies, we used a lower multiple of10 x 2013 EBIT to value Vallourec, and purchased shares atapproximately two-thirds of that value.

Despite the delays in qualification and the higher thanexpected capital expenditures, we believe that both projectswill ultimately be successful, particularly given the favorableoutlook for unconventional shale plays and deepwater. Ourevaluation of the business, specifically the connectionsbusiness, leads us to believe that Vallourec’s intrinsic value isgreater than its stated book value. Although in the short termthe company’s legacy exposure to European manufacturingcould weigh on the stock, we believe the long term prospectsfor Vallourec’s oil & gas business are quite strong. It has asolid balance sheet with very little debt, which should allow itto weather near term disappointments that may arise. Forinvestors such as ourselves, who are willing to look further outon the investment horizon for our returns, we felt we werebeing presented with an unusual pricing opportunity.

Tweedy, Browne Worldwide High Dividend YieldValue Fund

Just a quick word about the approaching fiscal cliff andwhat, if anything, it might portend for high dividend stocks.As we have said in past letters, higher tax rates should not inour opinion materially alter the attractive fundamental casefor dividend paying equities. First, many political observersbelieve that a grand bargain will be struck after the electionthat for the most part preserves the tax advantaged status ofdividends. Secondly, even if a bargain is not achieved and taxrates on dividends rise, it is our understanding that a largepercentage of the investors who own dividend paying equitiesare tax exempt institutions and tax exempt accounts such asIRAs and 401(k)s. Thirdly, it is quite possible, if not likely,that of the remaining taxable investors who own dividendpaying equities, only the top earners (those making over$250,000) will pay higher rates on dividends. Finally,according to a recent research report from Fidelity, whendividend tax rates were brought down from high ordinaryrates to the low rates under the Bush tax cuts, there was verylittle reaction in equity markets in terms of new flows intohigher yielding equities.9 It is quite possible that we will have

I-6

the same kind of muted reaction if rates do indeed rise ondividends. In our view, this does not suggest a potentialstampede out of dividend paying equities, particularly thosethat are attractively priced, have conservative payout ratios,and pay a reasonable and growing dividend yield.

As with our other Funds, in the Worldwide HighDividend Yield Value Fund we have trimmed or sold of latenumerous consumer based companies that have served uswell, such as Kimberly-Clark and Philip Morris among othersas they approached fair value, and reinvested in moreindustrial based companies, such as Siemans, ABB and Tescoamong others. All three of these companies at originalpurchase traded at siginficant discounts from conservativeappraisals, and paid stable and growing dividends between3.8% and 4.6%.

While a good deal of money has flowed into dividendstocks over the last year or so, and for good reason given theirvaluations, the uncertain macro picture, and low yields onbonds, we believe that our holdings remain reasonably toattractively priced with a weighted average price earningsratio of 12.1 x 2012 estimated earnings, and a weightedaverage dividend yield of 4.2%. (Please note that the weightedaverage dividend yield shown above is not representative of theWorldwide High Dividend Yield Value Fund’s yield, nor does itrepresent the Fund’s performance. The figure solely represents theaverage dividend yield of the common stocks held in the Fund’sportfolio. Please refer to the 30-Day Standardized Yield in theperformance chart on page I-3 for the Fund’s yield.) That said,with the advance in global equity markets over the lastseveral months, mis-priced dividend stocks are becomingmore difficult to uncover.

Looking Forward

To say that markets have been driven lately by the actionsand comments of central bankers around the world is anunderstatement. Thanks in large part to their ratherexpansive monetary policies, global equity markets havesteamed ahead this year. Year-to-date, the MSCI WorldIndex, a proxy for developed equity markets around the globe,is up approximately 13% in U.S. dollars, and has compoundedat 22.5% per year since the bottom of the financial crisis overthree years ago (March 9, 2009 through September 30, 2012).Not bad for the so called “new normal,” which post-crisismarket prognosticators suggested called for more mutedreturns. However, in our humble opinion, fundamentally notmuch has changed, particularly on the macroeconomic frontwhere uncertainty still looms large. The global economicrecovery remains anemic; the eurozone continues to be miredin uncertainty; China appears to be slowing; tensions areescalating in the Middle East; and the U.S. has madelittle-to-no progress with respect to its own budget crisis. Evencorporate performance, which has been surprisingly good,now appears to be weakening somewhat. Despite bonds beingat historically low yields, investment capital, supported bymonetary ease, has only just begun to flow back into stocksever so modestly.

As always, our forward view is largely informed byvaluation. To that end, as of October 31, 2012, the weighted

average P/E multiple on our Funds was approximately13.2 x 2012 estimated earnings, which translates into anearnings yield of approximately 7.6%.* This compares veryfavorably to the yield on ten-year treasuries, which is less than2%, and the recent level of the Consumer Price Index, whichhas been running around 2.2%†. While some caution iscertainly warranted given higher stock prices and continuedmacroeconomic uncertainty, we think that value-orientedequities are still for the most part fairly priced today, and webelieve offer investors a better chance of preservingpurchasing power over time.

One final note. We will be moving our offices in lateFebruary of next year to Stamford Connecticut, a suburbancommunity about 40 miles up the road from New York City.In looking out over the next ten to twenty years in ourbusiness, we felt that there were meaningful cost savings to behad moving out of New York into Connecticut. As many ofyou may know, the Stamford/Greenwich Connecticut areahas become a financial center over the last 10 yearsparticularly for investment advisory firms and hedge funds.Our new offices will be in the Thomson Reuters building, apremier Stamford building located adjacent to the Stamfordtrain station, which is easily accessible to our employees andclients from New York City via trains out of Grand CentralStation. The transition should be seamless. Please come visitus if you find yourself in the New York area.

Thank you for investing with us, and for your continuedconfidence.

Sincerely,

TWEEDY, BROWNE COMPANY LLC

William H. BrowneThomas H. ShragerJohn D. SpearsRobert Q. Wyckoff, Jr.Managing Directors

October 2012

* P/E ratios based on estimated 2012 earnings.Source: Bloomberg.

† Stocks and bonds are subject to different risks. In general, stocksare subject to greater price fluctuations and volatility than bondsand can decline significantly in value in response to adverse issuer,political, regulatory, market, or economic developments. Unlikestocks, bonds, if held to maturity, generally offer to pay both a fixedrate of return and a fixed principal value. Bonds are subject tointerest rate risk (as interest rates rise bond prices generally fall),the risk of issuer default, issuer credit risk, and inflation risk,although U.S. Treasuries are backed by the full faith and credit ofthe U.S. government.

I-7

Footnotes:(1) Indexes are unmanaged, and the figures for the indexes

shown include reinvestment of dividends and capital gainsdistributions and do not reflect any fees or expenses.Investors cannot invest directly in an index. We stronglyrecommend that these factors be considered before aninvestment decision is made.

(2) MSCI EAFE Index US$ is an unmanaged capitalizationweighted index of companies representing the stock marketsof Europe, Australasia and the Far East. MSCI EAFEIndex Hedged consists of the results of the MSCI EAFEIndex hedged 100% back into US dollars and accounts forinterest rate differentials in forward currency exchangerates. Results for both indexes are inclusive of dividends andnet of foreign withholding taxes.

(3) Inception dates for the Global Value Fund, Global ValueFund II – Currency Unhedged, Value Fund andWorldwide High Dividend Yield Value Fund are June 15,1993, October 26, 2009, December 8, 1993, andSeptember 5, 2007, respectively. Prior to 2004,information with respect to MSCI EAFE indexes used wasavailable at month end only; therefore the closest month endto the Global Value Fund’s inception date, May 31, 1993,was used.

(4) S&P 500/MSCI World Index (Hedged to US$) is acombination of the S&P 500 Index and the MSCI WorldIndex (Hedged to US$), linked together by Tweedy,Browne Company, and represents the performance of theS&P 500 Index for the periods 12/8/93 – 12/31/06, andcontinuing with the performance of the MSCI World Index(Hedged to US$), beginning 1/01/07 and thereafter. Forthe period from the Fund’s inception through 2006, theInvestment Adviser chose the S&P 500 as the relevantmarket benchmark. Starting in mid-December 2006, theFund’s investment mandate changed from investing at least80% of its assets in US securities to investing no less thanapproximately 50% in U.S securities, and so the InvestmentAdviser chose the MSCI World Index (Hedged to US$) asthe most relevant benchmark for the Fund for periodsstarting January 1, 2007.

(5) S&P 500 Index is an unmanaged capitalization weightedindex composed of 500 widely held common stocks thatassumes the reinvestment of dividends. The index isgenerally considered representative of U.S. largecapitalization stocks.

(6) The MSCI World Index is a free float-adjusted unmanagedmarket capitalization weighted index that is designed tomeasure the equity market performance of developedmarkets. The MSCI World Index (US$) reflects the returnof this index for a US dollar investor. MSCI World Index(Hedged to US$) consists of the results of the MSCI WorldIndex with its foreign currency exposure hedged 100% backinto US dollars. The index accounts for interest ratedifferentials in forward currency exchange rates. Results forthis index are inclusive of dividends and net of foreignwithholding taxes.

(7) Morningstar’s Foreign Large Value category: Foreign large-value funds invest mainly in big international stocks that areless expensive than the market as a whole. Most of thesefunds divide their assets among a dozen or more developedmarkets, including Japan, United Kingdom, France, andGermany. They tend to invest the rest in emerging marketssuch as Hong Kong, Brazil, Mexico and Thailand. Thesefunds typically will have less than 20% of assets invested inU.S. stocks.

(8) As of September 30, 2012, Tweedy, Browne Global ValueFund, Tweedy, Browne Global Value Fund II- CurrencyUnhedged, Tweedy, Browne Value Fund and Tweedy,Browne Worldwide High Dividend Yield Value Fund hadinvested the following percentages of its net assets,respectively, in the following portfolio holdings: Diageo(3.5%, 3.3%, 3.4%, 2.3%); Nestle (3.5%, 2.9%, 3.6%,2.2%); Heineken (3.7%, 2.8%, 3.2%, 0.0%); PhilipMorris International (1.7%, 1.2%, 1.6%, 1.6%); Kone(1.0%, 0.4%, 0.0%, 0.0%); Henkel (2.5%, 1.7%,2.4%, 0.0%); Wal-Mart (0.0%, 0.0%, 2.3%, 0.0%);Arca Continental (1.6%, 0.5%, 0.6%, 0.5%); Fraser &Neave (0.0%, 0.0%, 0.0%, 0.0%); Safran (1.6%, 2.0%,0.0%, 0.0%); Google (1.1%, 0.0%, 1.7%, 0.0%);Vallourec (0.8%, 1.0%, 0.0%, 0.0%); Kimberly-Clark(0.0%, 0.0%, 0.0%, 0.7%); Siemans (0.0%, 1.6%,0.0%, 2.6%); ABB (0.0%, 0.9%, 0.0%, 2.0%); andTesco (0.0%, 0.9%, 0.0%, 1.4%).

(9) “Dividends and taxes: Why market forces may continue tosupport dividend-paying stocks”, James Morrow (PortfolioManager, Fidelity Equity-Income Fund), FidelityViewpoints, Fidelity.com, September 19, 2012.

Current and future portfolio holdings are subject to risk.Investing in foreign securities involves additional risks beyondthe risks of investing in US securities markets. These risksinclude currency fluctuations; political uncertainty; differentaccounting and financial standards; different regulatoryenvironments; and different market and economic factors invarious non-US countries. In addition, the securities of small,less well known companies may be more volatile than those oflarger companies. Value investing involves the risk that themarket will not recognize a security’s intrinsic value for a longtime, or that a security thought to be undervalued mayactually be appropriately priced when purchased. Please referto the Funds’ prospectus for a description of risk factorsassociated with investments in securities which may be heldby the Funds.

Although the practice of hedging against currency exchangerate changes utilized by the Tweedy, Browne Global ValueFund and Tweedy, Browne Value Fund reduces the risk of lossfrom exchange rate movements, it also reduces the ability ofthe Funds to gain from favorable exchange rate movementswhen the US dollar declines against the currencies in whichthe Funds’ investments are denominated and in some interestrate environments may impose out-of-pocket costs on theFunds.

I-8

This letter contains opinions and statements on investmenttechniques, economics, market conditions and other matters.Of course there is no guarantee that these opinions andstatements will prove to be correct, and some of them areinherently speculative. None of them should be relied upon asstatements of fact.©2012 Morningstar, Inc. All Rights Reserved. Theinformation contained herein: (1) is proprietary toMorningstar and/or its content providers; (2) may not becopied or distributed; and (3) is not warranted to be accurate,complete or timely. Neither Morningstar nor its content

providers are responsible for any damages or losses arisingfrom any use of this information. Past performance is noguarantee of future results.

Tweedy, Browne Global Value Fund, Tweedy, Browne GlobalValue Fund II – Currency Unhedged, Tweedy, Browne ValueFund, and Tweedy, Browne Worldwide High Dividend YieldValue Fund are distributed by Tweedy, Browne CompanyLLC.

This material must be preceded or accompanied by aprospectus for Tweedy, Browne Fund Inc.

I-9

This page left blank intentionally.

TWEEDY, BROWNE FUND INC.

Tweedy, Browne Global Value FundTweedy, Browne Global Value Fund II – Currency UnhedgedTweedy, Browne Value FundTweedy, Browne Worldwide High Dividend Yield Value Fund

SEMI-ANNUAL REPORT

September 30, 2012

II-1

TWEEDY, BROWNE FUND INC.

Expense Information (Unaudited)

A shareholder of the Global Value Fund, Global ValueFund II – Currency Unhedged, Value Fund or WorldwideHigh Dividend Yield Value Fund (collectively, the “Funds”)incurs two types of costs: (1) transaction costs and(2) ongoing costs, including management fees and otherFund expenses. The Example below is intended to help ashareholder understand their ongoing costs (in U.S. dollars)of investing in the Funds and to compare these costs withthe ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000invested at the beginning of the period and held for theentire period of April 1, 2012 to September 30, 2012.

Actual Expenses The first part of the table presentedbelow, under the heading “Actual Expenses”, providesinformation about actual account values and actualexpenses. The information in this line may be used with theamount a shareholder invested to estimate the expensesthat were paid by the shareholder over the period. Simplydivide the shareholder’s account value by $1,000 (forexample, an $8,600 account value divided by $1,000 = 8.6),then multiply the result by the number in the first lineunder the heading entitled “Expenses Paid during Period” toestimate the expenses paid during this period.

Hypothetical Example for Comparison Purposes Thesecond part of the table presented below, under the heading“Hypothetical Expenses”, provides information abouthypothetical account values and hypothetical expenses

based on each Fund’s actual expense ratio and an assumedrate of return of 5% per year before expenses, which is noteach Fund’s actual return. The hypothetical account valuesand expenses may not be used to estimate the actual endingaccount balance or expenses paid by the shareholder of theFunds for the period. This information may be used tocompare the ongoing costs of investing in the Funds toother funds. To do so, compare this 5% hypotheticalexample with the 5% hypothetical examples that appear inthe shareholder reports of the other funds.

Please note that the expenses shown in the table beloware meant to highlight a shareholder’s ongoing costs onlyand do not reflect redemption fees. Redemptions from theGlobal Value Fund, the Global Value Fund II – CurrencyUnhedged and the Worldwide High Dividend Yield ValueFund, including exchange redemptions, within 60 days ofpurchase are subject to a redemption fee equal to 2% of theredemption proceeds, which will be retained by the Funds.There are no other transactional expenses associated withthe purchase and sale of shares charged by any of the Funds,such as commissions, sales loads and/or redemption fees onshares held longer than 60 days. Other mutual funds mayhave such transactional charges. Therefore, the second partof the table is useful in comparing ongoing costs only, andwill not help a shareholder determine the relative total costsof owning different funds. In addition, if redemption feeswere included a shareholder’s costs would have been higher.

Actual ExpensesHypothetical Expenses

(5% Return before Expenses)

BeginningAccountValue4/1/12

EndingAccountValue

9/30/12

ExpensesPaid during

Period*4/1/12 –9/30/12

BeginningAccountValue4/1/12

EndingAccountValue

9/30/12

ExpensesPaid during

Period*4/1/12 –9/30/12

AnnualizedExpense

Ratio

Global Value Fund $1,000.00 $1,035.70 $7.04 $1,000.00 $1,018.15 $6.98 1.38%

Global Value Fund II –Currency Unhedged $1,000.00 $1,025.70 $6.96 $1,000.00 $1,018.20 $6.93 1.37%

Value Fund $1,000.00 $1,035.20 $7.09 $1,000.00 $1,018.10 $7.03 1.39%

Worldwide High DividendYield Value Fund $1,000.00 $1,028.80 $6.97 $1,000.00 $1,018.20 $6.93 1.37%

* Expenses are equal to each Fund’s annualized expense ratio, multiplied by the average account value over the period,multiplied by the number of days in the period, divided by 365 (to reflect the one-half year period).

II-2

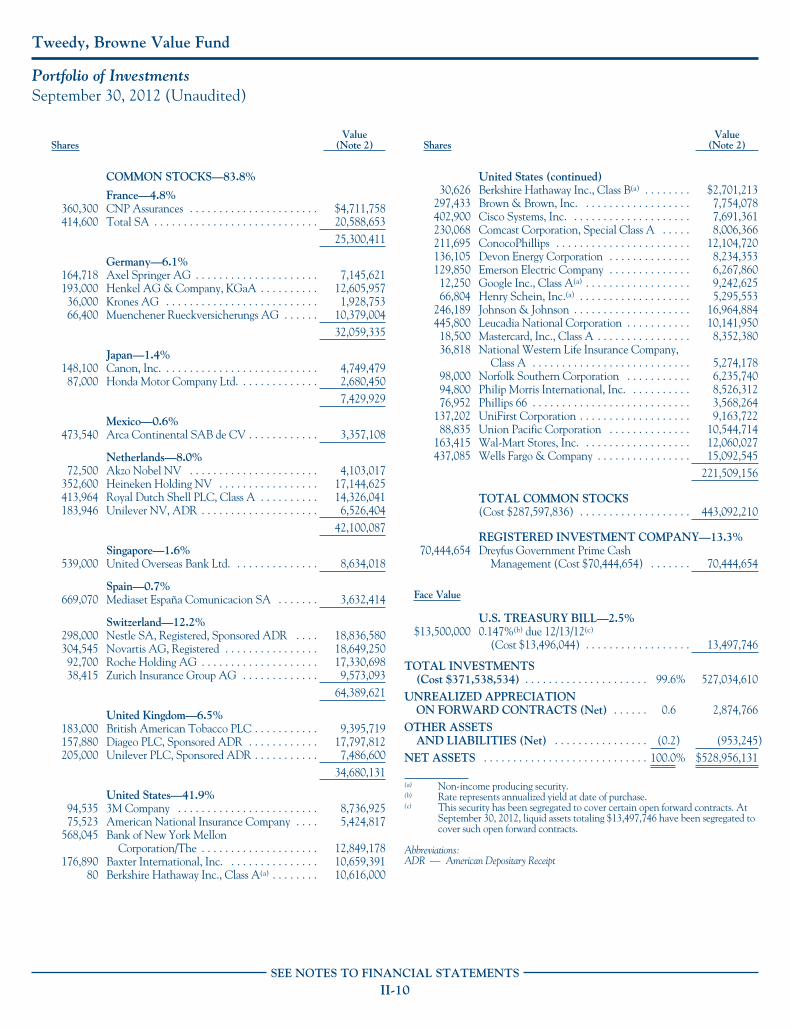

Tweedy, Browne Global Value Fund

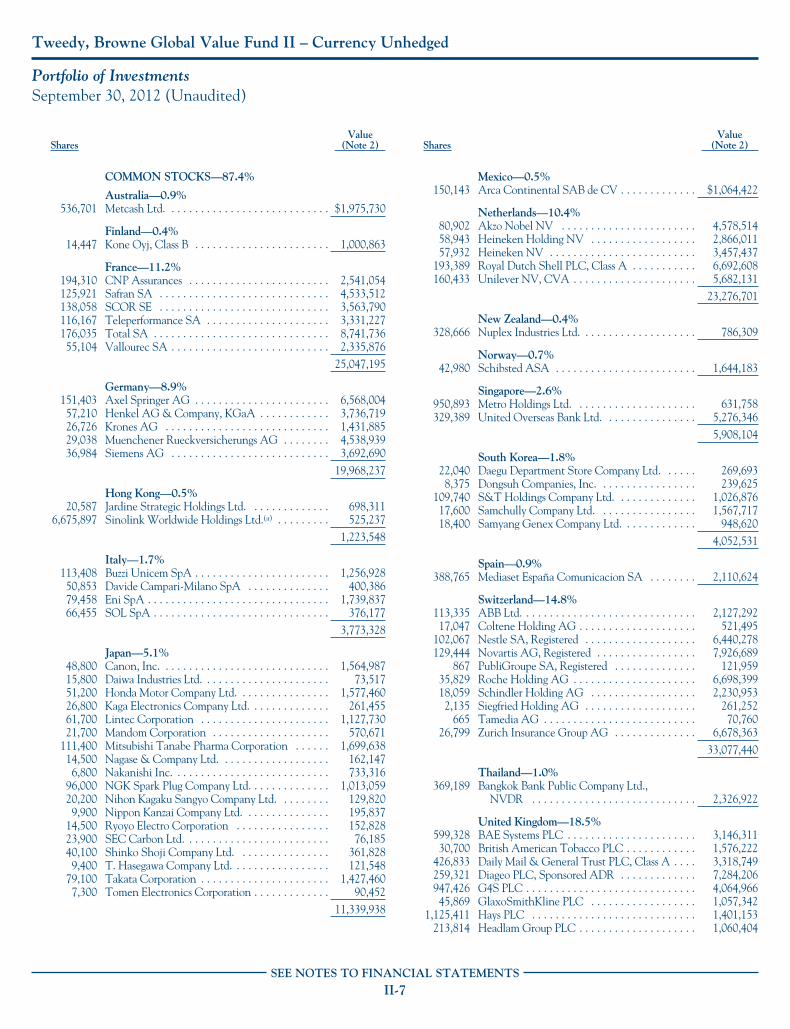

Portfolio of InvestmentsSeptember 30, 2012 (Unaudited)

SharesValue

(Note 2)

COMMON STOCKS—85.0%

Canada—1.1%750,000 National Bank of Canada . . . . . . . . . . . . . . . . . . . $56,710,199

Czech Republic—0.0%(a)

2,800 Philip Morris CR a.s. . . . . . . . . . . . . . . . . . . . . . . 1,620,626

Finland—1.0%756,800 Kone Oyj, Class B . . . . . . . . . . . . . . . . . . . . . . . . . 52,429,795

France—9.1%7,719,256 CNP Assurances . . . . . . . . . . . . . . . . . . . . . . . . . . 100,947,1732,181,535 Safran SA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78,541,434

651,820 SCOR SE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16,825,895712,949 Teleperformance SA . . . . . . . . . . . . . . . . . . . . . . 20,444,659

3,984,810 Total SA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 197,881,984988,950 Vallourec SA . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41,921,912

456,563,057

Germany—9.3%3,726,000 Axel Springer AG . . . . . . . . . . . . . . . . . . . . . . . . 161,637,3601,936,000 Henkel AG & Company, KGaA . . . . . . . . . . . . . 126,451,460

896,077 Krones AG . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48,008,65442,354 KSB AG . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22,097,858

699,000 Muenchener Rueckversicherungs AG . . . . . . . . . 109,260,903467,456,235

Hong Kong—0.4%271,000 Guoco Group Ltd. . . . . . . . . . . . . . . . . . . . . . . . . 2,439,725434,500 Jardine Strategic Holdings Ltd. . . . . . . . . . . . . . . . 14,738,240

2,104,000 Sinolink Worldwide Holdings Ltd.(b) . . . . . . . . . . 165,53617,343,501

Italy—0.7%3,645,000 Arnoldo Mondadori Editore SpA(b) . . . . . . . . . . . 4,661,173

144,268 Buzzi Unicem SpA . . . . . . . . . . . . . . . . . . . . . . . . 1,598,9564,795,392 SOL SpA(c) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27,144,892

33,405,021

Japan—5.2%191,000 Aica Kogyo Company Ltd. . . . . . . . . . . . . . . . . . . 3,277,442

1,594,700 Canon, Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51,141,086200,000 Daiwa Industries Ltd. . . . . . . . . . . . . . . . . . . . . . . 930,591

2,064,000 Fujitec Company Ltd. . . . . . . . . . . . . . . . . . . . . . . 12,177,069446,600 Fukuda Denshi Company Ltd. . . . . . . . . . . . . . . . 14,350,900

1,069,200 Hi-Lex Corporation . . . . . . . . . . . . . . . . . . . . . . . 15,598,2261,577,500 Honda Motor Company Ltd. . . . . . . . . . . . . . . . . 48,602,410

75,400 Kaga Electronics Company Ltd. . . . . . . . . . . . . . . 735,586125,000 Katsuragawa Electric Company Ltd.(b) . . . . . . . . . . 144,602133,000 Kawasumi Laboratories, Inc. . . . . . . . . . . . . . . . . . 776,118

1,329,500 Kuroda Electric Company Ltd. . . . . . . . . . . . . . . . 16,251,34373,800 Lintec Corporation . . . . . . . . . . . . . . . . . . . . . . . . 1,348,89069,100 Mandom Corporation . . . . . . . . . . . . . . . . . . . . . . 1,817,206

216,700 Medikit Company Ltd. . . . . . . . . . . . . . . . . . . . . . 7,241,902165,400 Mirai Industry Company Ltd. . . . . . . . . . . . . . . . . 1,913,36861,600 Mitsubishi Tanabe Pharma Corporation . . . . . . . . 939,835

2,116,000 NGK Spark Plug Company Ltd. . . . . . . . . . . . . . . 22,329,512162,780 Nippon Kanzai Company Ltd. . . . . . . . . . . . . . . . 3,220,03172,700 Ryoyo Electro Corporation . . . . . . . . . . . . . . . . . . 766,247

SharesValue

(Note 2)

Japan (continued)168,500 Sangetsu Company Ltd. . . . . . . . . . . . . . . . . . . . $4,656,491100,400 SEC Carbon Ltd. . . . . . . . . . . . . . . . . . . . . . . . . 320,041400,000 Shinko Shoji Company Ltd. . . . . . . . . . . . . . . . 3,609,254151,400 SK Kaken Company Ltd. . . . . . . . . . . . . . . . . . . 6,402,391375,300 T. Hasegawa Company Ltd. . . . . . . . . . . . . . . . . 4,852,851

1,787,400 Takata Corporation . . . . . . . . . . . . . . . . . . . . . . 32,255,907200,000 Tomen Electronics Corporation . . . . . . . . . . . . . 2,478,149

258,137,448

Mexico—3.0%11,580,000 Arca Continental SAB de CV . . . . . . . . . . . . . . 82,095,083

532,995 Coca-Cola Femsa SA de CV,Sponsored ADR(d) . . . . . . . . . . . . . . . . . . . . . 68,756,355

150,851,438

Netherlands—10.0%2,093,000 Akzo Nobel NV . . . . . . . . . . . . . . . . . . . . . . . . . 118,449,8523,835,000 Heineken Holding NV . . . . . . . . . . . . . . . . . . . 186,470,8933,950,188 Royal Dutch Shell PLC, Class A . . . . . . . . . . . . 136,704,049

967,460 Telegraaf Media Groep NV, CVA . . . . . . . . . . . 9,389,5771,368,000 Unilever NV, CVA . . . . . . . . . . . . . . . . . . . . . . 48,451,100

499,465,471

Norway—1.6%2,084,693 Schibsted ASA . . . . . . . . . . . . . . . . . . . . . . . . . 79,749,121

Singapore—1.4%4,428,800 United Overseas Bank Ltd. . . . . . . . . . . . . . . . . 70,943,116

South Korea—0.4%150,900 Daegu Department Store Company Ltd. . . . . . . 1,846,49490,974 Hanil Cement Company Ltd. . . . . . . . . . . . . . . 3,315,066

141,713 Samchully Company Ltd. . . . . . . . . . . . . . . . . . 12,623,06214,792 Samyang Genex Company Ltd. . . . . . . . . . . . . . 762,608

18,547,230

Spain—1.0%9,086,000 Mediaset España Comunicacion SA . . . . . . . . . 49,328,342

Sweden—0.0%(a)

63,360 Cloetta AB, B Shares(b) . . . . . . . . . . . . . . . . . . . 146,886

Switzerland—17.6%388,000 CIE Financiere Richemont AG . . . . . . . . . . . . . 23,284,954218,165 Coltene Holding AG(c) . . . . . . . . . . . . . . . . . . . 6,674,020343,783 Daetwyler Holding AG, Bearer . . . . . . . . . . . . . 28,660,77710,000 Loeb Holding AG . . . . . . . . . . . . . . . . . . . . . . . 2,041,924

2,781,120 Nestle SA, Registered . . . . . . . . . . . . . . . . . . . . 175,484,58880 Neue Zuercher Zeitung(b) . . . . . . . . . . . . . . . . . . 515,003

3,002,000 Novartis AG, Registered . . . . . . . . . . . . . . . . . . 183,831,77343,688 Phoenix Mecano AG . . . . . . . . . . . . . . . . . . . . . 21,035,135

185,918 PubliGroupe SA, Registered(c) . . . . . . . . . . . . . . 26,152,756984,000 Roche Holding AG . . . . . . . . . . . . . . . . . . . . . . 183,963,397248,117 Siegfried Holding AG(c) . . . . . . . . . . . . . . . . . . . 30,361,199

4,297 Sika AG, Bearer . . . . . . . . . . . . . . . . . . . . . . . . 8,769,574432,618 Tamedia AG . . . . . . . . . . . . . . . . . . . . . . . . . . . 46,032,986584,275 Zurich Insurance Group AG . . . . . . . . . . . . . . . 145,602,474

882,410,560

SEE NOTES TO FINANCIAL STATEMENTSII-3

Tweedy, Browne Global Value Fund

Portfolio of InvestmentsSeptember 30, 2012 (Unaudited)

SharesValue

(Note 2)

Thailand—1.1%9,089,500 Bangkok Bank Public Company Ltd., NVDR . . $57,289,246

United Kingdom—14.5%1,521,000 AGA Rangemaster Group PLC . . . . . . . . . . . . . 1,495,1621,782,000 BBA Aviation PLC . . . . . . . . . . . . . . . . . . . . . . 5,683,2261,882,980 British American Tobacco PLC . . . . . . . . . . . . . 96,677,3245,464,262 Daily Mail & General Trust PLC, Class A . . . . . 42,486,2006,289,000 Diageo PLC, Sponsored ADR . . . . . . . . . . . . . . 176,655,073

13,550,100 G4S PLC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58,137,2042,845,500 Hays PLC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,542,6891,397,625 Headlam Group PLC . . . . . . . . . . . . . . . . . . . . . 6,931,4796,648,155 HSBC Holdings PLC . . . . . . . . . . . . . . . . . . . . . 61,546,4721,026,408 Imperial Tobacco Group PLC . . . . . . . . . . . . . . 37,988,7263,346,355 Provident Financial PLC . . . . . . . . . . . . . . . . . . 74,192,9494,891,800 TT Electronics PLC . . . . . . . . . . . . . . . . . . . . . . 11,355,2482,700,000 Unilever PLC . . . . . . . . . . . . . . . . . . . . . . . . . . 98,186,603

17,721,661 Vodafone Group PLC . . . . . . . . . . . . . . . . . . . . 50,294,425725,172,780

United States—7.6%75,700 American National Insurance Company . . . . . . 5,437,531

1,094,821 Baxter International, Inc. . . . . . . . . . . . . . . . . . . 65,973,913436 Berkshire Hathaway Inc., Class A(b) . . . . . . . . . . 57,857,200301 Berkshire Hathaway Inc., Class B(b) . . . . . . . . . . 26,548

587,000 ConocoPhillips . . . . . . . . . . . . . . . . . . . . . . . . . 33,564,66049,250 Devon Energy Corporation . . . . . . . . . . . . . . . . 2,979,62576,000 Google Inc., Class A(b) . . . . . . . . . . . . . . . . . . . . 57,342,000

865,835 Johnson & Johnson . . . . . . . . . . . . . . . . . . . . . . 59,664,690918,700 Philip Morris International, Inc. . . . . . . . . . . . . 82,627,878293,500 Phillips 66 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,609,595

379,083,640

Miscellaneous—0.0%(a)

Undisclosed Securities(f) . . . . . . . . . . . . . . . . . . . 417,823

TOTAL COMMON STOCKS(Cost $2,768,311,281) . . . . . . . . . . . . . . . . . . . . 4,257,071,535

SharesValue

(Note 2)

PREFERRED STOCKS—0.2%

Croatia—0.1%166,388 Adris Grupa d.d. . . . . . . . . . . . . . . . . . . . $6,440,919

Germany—0.1%314,700 Villeroy & Boch AG . . . . . . . . . . . . . . . . 3,027,161

TOTAL PREFERRED STOCKS(Cost $12,253,786) . . . . . . . . . . . . . . . . . 9,468,080

REGISTERED INVESTMENT COMPANY—11.4%571,224,628 Dreyfus Government Prime Cash

Management (Cost $571,224,628) . . . . 571,224,628

Face Value

U.S. TREASURY BILL—2.5%$125,000,000 0.136%(e) due 11/01/12(d)

(Cost $124,985,523) . . . . . . . . . . . . . . 124,991,916

TOTAL INVESTMENTS(Cost $3,476,775,218) . . . . . . . . . . . . . . . . . . 99.1% 4,962,756,159

UNREALIZED APPRECIATIONON FORWARD CONTRACTS (Net) . . . . . 0.5 27,325,362

OTHER ASSETSAND LIABILITIES (Net) . . . . . . . . . . . . . . . 0.4 19,791,950

NET ASSETS . . . . . . . . . . . . . . . . . . . . . . . . . . . 100.0% $5,009,873,471

(a) Amount represents less than 0.1% of net assets.(b) Non-income producing security.(c) “Affiliated company” as defined by the Investment Company Act of 1940. See

Note 4.(d) All or a portion of this security has been segregated to cover certain open forward

contracts. At September 30, 2012, liquid assets totaling $168,749,888 have beensegregated to cover such open forward contracts.

(e) Rate represents annualized yield at date of purchase.(f) “Undisclosed Securities” represent issuers, generally smaller capitalization issuers,

where disclosure may be disadvantageous to the Fund’s accumulation or dispositionprogram.

Abbreviations:ADR — American Depositary ReceiptCVA — Certificaaten van aandelen (Share Certificates)

NVDR — Non Voting Depository Receipt

SEE NOTES TO FINANCIAL STATEMENTSII-4

Tweedy, Browne Global Value Fund

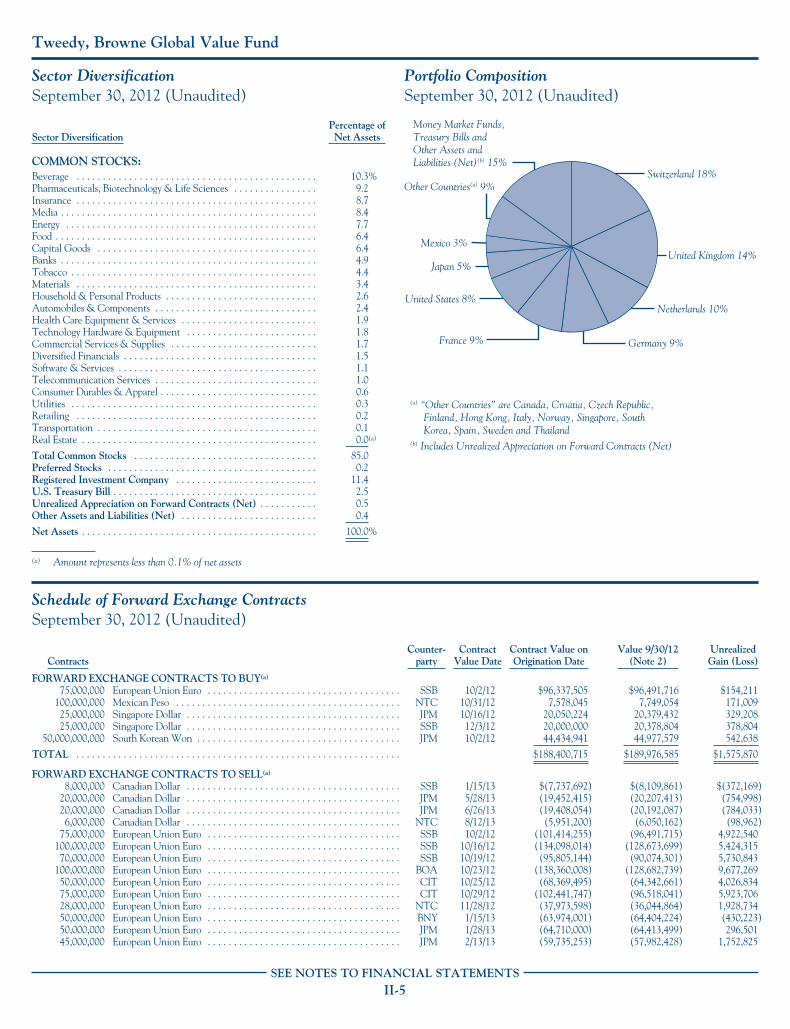

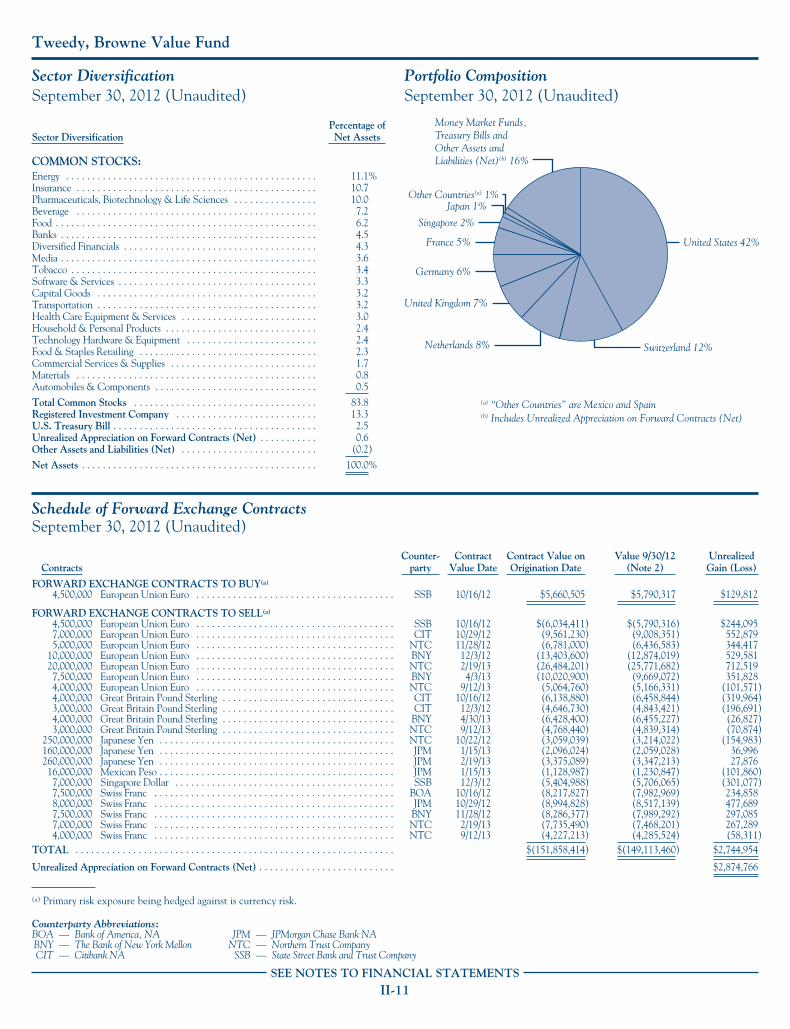

Sector DiversificationSeptember 30, 2012 (Unaudited)

Sector DiversificationPercentage ofNet Assets

COMMON STOCKS:Beverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10.3%Pharmaceuticals, Biotechnology & Life Sciences . . . . . . . . . . . . . . . . 9.2Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8.7Media . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8.4Energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7.7Food . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.4Capital Goods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.4Banks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.9Tobacco . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.4Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.4Household & Personal Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.6Automobiles & Components . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.4Health Care Equipment & Services . . . . . . . . . . . . . . . . . . . . . . . . . . 1.9Technology Hardware & Equipment . . . . . . . . . . . . . . . . . . . . . . . . . 1.8Commercial Services & Supplies . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.7Diversified Financials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.5Software & Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.1Telecommunication Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.0Consumer Durables & Apparel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.6Utilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.3Retailing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.2Transportation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.1Real Estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.0(a)

Total Common Stocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85.0Preferred Stocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.2Registered Investment Company . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.4U.S. Treasury Bill . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.5Unrealized Appreciation on Forward Contracts (Net) . . . . . . . . . . . 0.5Other Assets and Liabilities (Net) . . . . . . . . . . . . . . . . . . . . . . . . . . 0.4

Net Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100.0%

(a) Amount represents less than 0.1% of net assets

Portfolio CompositionSeptember 30, 2012 (Unaudited)

(a) “Other Countries” are Canada, Croatia, Czech Republic, Finland, Hong Kong, Italy, Norway, Singapore, South Korea, Spain, Sweden and Thailand(b) Includes Unrealized Appreciation on Forward Contracts (Net)

Money Market Funds, Treasury Bills and Other Assets and Liabilities (Net)(b) 15%

Switzerland 18%

United Kingdom 14%

Netherlands 10%

Germany 9%France 9%

Mexico 3%

Japan 5%

United States 8%

Other Countries(a) 9%

Schedule of Forward Exchange ContractsSeptember 30, 2012 (Unaudited)

ContractsCounter-

partyContract

Value DateContract Value onOrigination Date

Value 9/30/12(Note 2)

UnrealizedGain (Loss)

FORWARD EXCHANGE CONTRACTS TO BUY(a)

75,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . SSB 10/2/12 $96,337,505 $96,491,716 $154,211100,000,000 Mexican Peso . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . NTC 10/31/12 7,578,045 7,749,054 171,00925,000,000 Singapore Dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . JPM 10/16/12 20,050,224 20,379,432 329,20825,000,000 Singapore Dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . SSB 12/3/12 20,000,000 20,378,804 378,804

50,000,000,000 South Korean Won . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . JPM 10/2/12 44,434,941 44,977,579 542,638

TOTAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $188,400,715 $189,976,585 $1,575,870

FORWARD EXCHANGE CONTRACTS TO SELL(a)

8,000,000 Canadian Dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . SSB 1/15/13 $(7,737,692) $(8,109,861) $(372,169)20,000,000 Canadian Dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . JPM 5/28/13 (19,452,415) (20,207,413) (754,998)20,000,000 Canadian Dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . JPM 6/26/13 (19,408,054) (20,192,087) (784,033)6,000,000 Canadian Dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . NTC 8/12/13 (5,951,200) (6,050,162) (98,962)

75,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . SSB 10/2/12 (101,414,255) (96,491,715) 4,922,540100,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . SSB 10/16/12 (134,098,014) (128,673,699) 5,424,31570,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . SSB 10/19/12 (95,805,144) (90,074,301) 5,730,843

100,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . BOA 10/23/12 (138,360,008) (128,682,739) 9,677,26950,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CIT 10/25/12 (68,369,495) (64,342,661) 4,026,83475,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CIT 10/29/12 (102,441,747) (96,518,041) 5,923,70628,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . NTC 11/28/12 (37,973,598) (36,044,864) 1,928,73450,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . BNY 1/15/13 (63,974,001) (64,404,224) (430,223)50,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . JPM 1/28/13 (64,710,000) (64,413,499) 296,50145,000,000 European Union Euro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . JPM 2/13/13 (59,735,253) (57,982,428) 1,752,825

SEE NOTES TO FINANCIAL STATEMENTSII-5

Tweedy, Browne Global Value Fund

Schedule of Forward Exchange ContractsSeptember 30, 2012 (Unaudited)

ContractsCounter-

partyContract

Value DateContract Value onOrigination Date

Value 9/30/12(Note 2)

UnrealizedGain (Loss)