Investing in liquid alternative...

37

For professional investors or advisers only. Andrew Dreaneen Head of Schroder GAIA Product & Business Development Investing in liquid alternative strategies Trends & Morningstar Investment Summit 9 March 2016

Transcript of Investing in liquid alternative...

For professional investors or advisers only.

Andrew Dreaneen Head of Schroder GAIA Product & Business Development

Investing in liquid alternative strategies

Trends & Morningstar Investment Summit 9 March 2016

Agenda

Trends in Alternatives

Introducing Schroders capabilities in liquid alternatives

Leading blue-chip hedge fund managers

Main reservations and dispelling the myths

The power of diversifying returns streams

Conclusions

1

Trends in Alternatives

Why liquid alternatives now?

3

Source: MSCI December 2015

Global stress points/ downside risks for investors 2016

US Election Rate

Increases

Oil Glut

Commodities EM Hangover

Brexit

QE Effectivenes

s

EU Integration

Middle East Tensions

Russia Expansion

China Growth

Yuan Devaluation

South China Sea tension

Oil Has Really Collapsed

4

Source: Bloomberg January 2016

Wow, US oil is really cheap

China’s slowing growth has crushed shipping rates

5

Source: Bloomberg, Baltic Exchange, Supercarexperiences.com January 2016

It is now cheaper to rent a 1,100 foot dry bulk tanker than a Ferrari

($5,597)

($1,563)

KKR

Why liquid alternatives now? Liquid alternatives have mitigated losses in recent sell-offs

6

Source: Bloomberg as at 31 January 2016. Performance shown from 31 December 2014 to 31 January 2016. All GAIA performance is shown for the C Acc share class in base currency. Performance is calculated on an NAV to NAV basis.

Egerton Sirios

BSP

85

90

95

100

105

Jun-15 Aug-15 Oct-15 Dec-15

Schroder GAIA BSP Credit Merrill Lynch HY Index

3.63%

85

90

95

100

105

110

115

Dec-14 Feb-15 Apr-15 Jun-15 Aug-15 Oct-15 Dec-15

Schroder GAIA Egerton Equity MSCI World

-8.63% 90

95

100

105

110

Dec-14 Feb-15 Apr-15 Jun-15 Aug-15 Oct-15 Dec-15

Schroder GAIA Sirios US Equity

S&P 500 Net Total Return

-1.01%

-4.29%

85

90

95

100

105

110

Dec-14 Feb-15 Apr-15 Jun-15 Aug-15 Oct-15 Dec-15

Schroder GAIA KKR Credit Credit Suisse HY Index

-2.51%

-6.51%

-1.25%

-8.79%

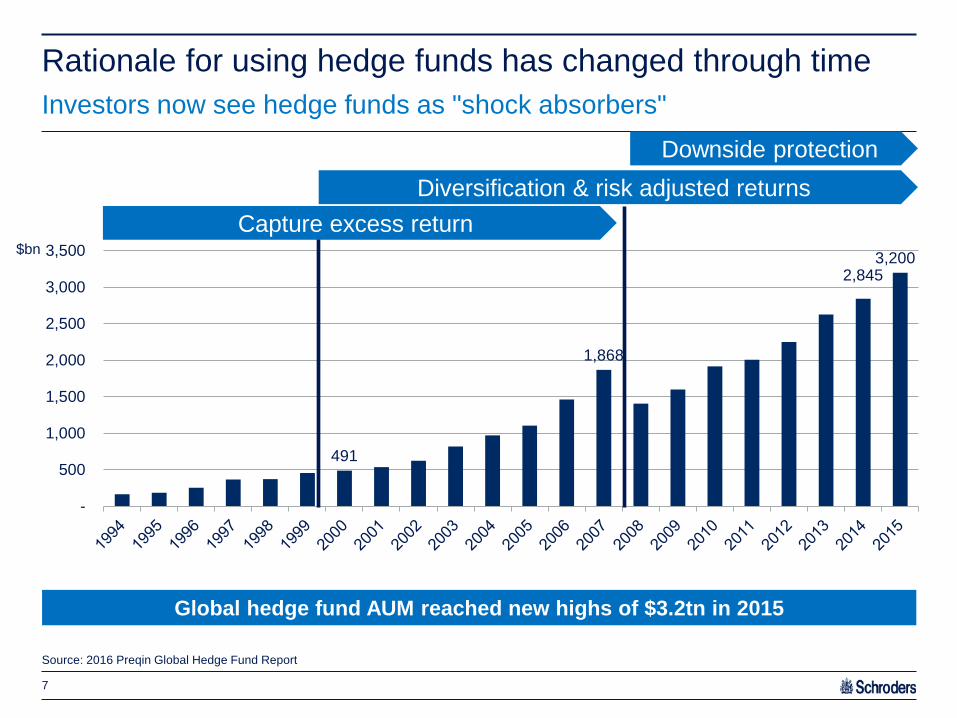

Rationale for using hedge funds has changed through time Investors now see hedge funds as "shock absorbers"

Source: 2016 Preqin Global Hedge Fund Report

Global hedge fund AUM reached new highs of $3.2tn in 2015

$bn

491

1,868

2,845 3,200

-

500

1,000

1,500

2,000

2,500

3,000

3,500

7

Capture excess return Diversification & risk adjusted returns

Downside protection

European Investors have > $800bn invested in hedge funds Investor sentiment now strongly in favour of UCITS and non UCITS AIFs

8

UCITS Liquid Alternatives

Liquid, regulated European onshore fund structure that can be used for alternatives

Harmonised format that can be ‘passported’ across Europe for distribution purposes

Suitable for sale to retail as well as professional investors

3.

2.

Non-UCITS Onshore Fund

New onshore structures post-AIFMD implementation; less stringent regulation than UCITS funds

Structures include QIAIF, RIAIF, PIF (Ireland); Part II, SIF, SICAR (Lux); some formats (e.g. RIAIF) may be suitable for sale to retail investors

Still largely unproven as a concept for HF managers

$204bn

$60bn (est.)

$2.9tn

Hedge Fund Vehicles Total AUM AUM from European Investors

1.

Offshore Hedge Fund

Offshore, unregulated HF vehicle

Most popular pre-2008/9, but comparatively low demand in Europe in recent years

AIFMD regulations have made the marketing of offshore HFs more challenging

$164bn

Source: HFR, HFI, Central Bank of Ireland, McKinsey “The Mainstreaming of Alternative Investments” (2011), Barclays Strategic Consulting estimates and analysis

$60bn (est.)

$600bn

Who are the buyers of liquid alternatives today? The main buyers are private banks/ wealth managers with demand broad-based

9

Source: Estimates based on data from Lipper, ICI, Mercer, Towers Watson, Insurance Europe, The Consulting Partnership AG, BCG, PWC, Strategic Consulting Proprietary Market Sizing Model. Individual numbers may not match sums due to rounding. AUM on a ‘look-through’ basis – i.e. disregarding FOFs, consultants and advisers. As at September 2015.

6 3 3

1 1

3

3

1

1

1 1

1

1 8

2

5 1

1

22

6 11

25

5

1

8

3

5

5

6

1

2

2

8

7

3 3 1

1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

UK France Germany / Austria Switzerland Italy / Spain Nordics Benelux

Mass Affluent E&F Family Office Private Banks Pension Insurance

41 18 27 40 17 7 14 $bn

Future expected investor behaviour Where is the growth expected to come from?

Source: Barclays, October 2015. Barclays Strategic Consulting estimates and analysis. 1. For offshore buyers includes amount of continued allocation to offshore funds as well as UCITS funds. Estimated long-term potential based on analysis of total investable assets and likely appetite for HFs/UCITS going forwards

There are three main constituencies of buyers for HF strategies in Europe; we estimate that those that only invest in UCITS could become the majority of AUM over time

10

‘Crossover’ Current

Offshore HF Buyers

Investors

$200bn

$600bn1

$750bn

‘Migration’ Former

Offshore HF Buyers

‘Entrant’ New

Alternatives Buyers

Comments Key Channels Est. Potential Asset Pool1

Investors with no prior HF investments getting exposure to alternatives through UCITS

Includes retail investors as well as some institutions

Potentially the largest asset pool but growth still uncertain

Investors with prior offshore HF exposure now using UCITS structures

Driven by mixture of preference for the format and regulatory pressures

Significant regional skew towards certain countries, particularly Southern Europe

Market for offshore HFs in Europe is stagnant, with limited growth potential

However, many of the buyers of offshore HFs in Europe also invest in UCITS funds

UCITS vehicle may be chosen if it is the only available option or offers superior terms to offshore vehicle

Local/retail banks Financial advisors/IFAs Distribution platforms Small institutional investors Wealth managers

Private banks Wealth managers/multi-family offices Certain institutions (e.g. insurance) FOFs

Family offices Institutions Private banks FOFs

Exam

ples

93.2 60.1 50.6

58 207 185

45.7% 29.5% 24.8%

Who are the main providers of liquid alternatives today?

Hedge Fund Managers Long Only Asset Managers Convergence Asset Managers

# Pr

oduc

ts

Source: HFR, HFI, Strategic Consulting analysis

AUM

(USD

bn)

11

Using distribution capabilities to build alternatives businesses Marketing HF expertise to UCITS investor base

AUM dominated by Asset Managers 75%: but Hedge Fund Managers now 25%

% A

UM

Introducing Schroders capabilities in liquid alternatives

Schroders AUM breakdown Broad liquid alternatives capability within the firm

13

Source: Schroders, as at 30 June 2015

GAIA

Liquid Alternatives

UCITS Funds

Firm AUM

$6bn

$18bn

$156bn

$487bn

Internally managed • Schroder ISF European Equity

Absolute Return • Schroder ISF European Alpha

Absolute Return* • Schroder ISF European Total Return • Schroder ISF Asian Total Return* Externally managed • Schroder GAIA Egerton Equity* • Schroder GAIA Sirios US Equity • Schroder GAIA Paulson Merger

Arbitrage

Schroders’ liquid alternatives capabilities Total AUM of Schroders liquid alternatives is $18.2bn

14

Source: Schroders as at 30 June 2015. * Fund is hard closed. Schroder ISF: Schroder International Selection Fund. Schroder IF: Schroder Investment Fund

Internally managed • Schroder ISF Strategic Bond • Schroder ISF Asian Bond Absolute

Return • Schroder ISF Emerging Marlets Debt

Absolute Return Externally managed • Schroder GAIA BSP Credit • Schroder GAIA KKR Credit

Internally managed • Schroder ISF Global Property

Securities • Schroder ISF Asia Pacific Property

Securities • Schroder IF Flexible Cat Bond

UCITS hedge fund platforms

15

Source: Kepler Partners LLP as at December 2015

Investment Bank Platforms Asset Manager Platforms Independent/Boutique Platforms

Deutsche Bank Banor Alceda UCITS Platform

Goldman Sachs E.I. Sturdza Strategic Management Ltd Alpha UCITS

Merrill Lynch Investment Solutions Guggenheim Altex UCITS

Morgan Stanley FundLogic Hedge Invest Bryan Garnier

SEB Prime Solutions UCITS HDF Rothschild Dexion

Lyxor Asset Management Independent UCITS

Schroder GAIA Gateway

Tages Milltrust EMMA Platform

Montlake UCITS Platform

SIG Global

Trium

Universal Investments

Source: Schroders as at 30 September 2015. *Hard closed.

Schroder GAIA Overview of sub-funds

Launch date

Manager Fund Strategy Geographic focus AUM (USD)

25 Nov 2009 Schroder GAIA Egerton Equity* Equity long short Global 1,399m

27 Feb 2013 Schroder GAIA Sirios US Equity Equity long short Predominantly US 2,003m

6 Nov 2013 Schroder GAIA KKR Credit Credit long short Predominantly Europe 293m

25 Jun 2014 Schroder GAIA Paulson Merger Arbitrage Merger Arbitrage US, Canada and

Western Europe 950m

17 Jun 2015 Schroder GAIA BSP Credit Credit long short Predominantly US 34m

9 Dec 2015 Schroder GAIA BlueTrend Trend Following Global 96m

16

Total AUM 5,533m

Source: Schroders as at 31 January 2016 *Hard closed.

Alternative UCITS platforms GAIA compares favourably against its competitors

Number of

external funds on platform

AUM (USD m)

Average AUM per

fund (USD m)

Schroders 6 4,775 795

BAML 16 6,276 392

HDF Rothschild 3 1,286 429

Deutsche Bank 11 3,686 335

Lyxor 8 1,533 192

Morgan Stanley 18 2,419 134

Goldman Sachs 4 524 131

Guggenheim 1 175 175

Alpha UCITS 5 384 77

Montlake 9 546 61

17

Source: Kepler. As at 31 January 2016. Data refers to external managers for each platform. This is collected on a best efforts basis and there could be omissions

“When trying to identify the quality of each platform we believe that AuM per fund is one of the most telling statistics. Schroder GAIA once again takes the leading spot by a significant margin with $795m invested in the average fund on its platform, reflecting the quality of the hosted funds and their impressive distribution capabilities.” Kepler

Schroders

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

0 5 10 15 20

Number of Funds

AUM (USD)

Leading blue-chip hedge fund managers

0%

500%

1000%

1500%

2000%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2014

2015

Schroder GAIA Egerton Equity Strategy MSCI World

Independent money management firm based in London, founded in 1994 by John Armitage

Experienced investment team of 16 professionals Employee investments account for c. 7% of total firm assets Key to success is research-intensive stock picking. ‘Bottom-up’

approach to stock selection creates a portfolio that is dynamic, eclectic, and uncorrelated

The strategy aims to deliver equity type returns with less volatility than the market over the medium to long term

Egerton Capital Limited: AUM $13.7bn Performance objective

Schroder GAIA Egerton Equity Equity long short fund with significant outperformance over time

19

Source: Schroders and Egerton as at 31 January 2016. *Performance shown for chain-linked track record of Egerton long short Equity B1 USD since its inception on 31 December 1994. Egerton’s offshore fund has been used from December 1994 to November 2009. From December 2009 onwards Schroder GAIA Egerton Equity C Acc USD Hedged has been used. The MSCI Europe Index has been used from December 1994-January 2012, from February 2012-onwards the MSCI World Index is used. . Performance is shown net of fees, NAV to NAV.

Performance analysis (Egerton’s equity long short strategy*)

Fundamental long short equity fund, typically long-biased Straightforward, liquid strategy investing predominantly in large cap

equities Opportunistically invest in corporate bonds Uses little or no leverage Reduces volatility through the use of alpha shorts, hedges (e.g. index

put options) and cash Avoids large drawdowns

Fund key features

Strategy* Index

Annualised return 13.7% 7.4%

Annualised volatility 9.6% 15.4%

Sharpe ratio 1.1 0.3

Maximum drawdown -28.3% -50.9%

Portfolio Manager John Armitage, Egerton

Inception date 25 November 2009

Base currency EUR

Institutional share class fee 1.25%/20%

Liquidity Weekly (on Wed) and month end

-100%

0%

100%

200%

300%

400%

1999 2001 2003 2005 2007 2009 2011 2013 2015

Schroder GAIA Sirios US Equity Strategy S&P 500

Boston based US focused firm co-founded by John Brennan in 1999 Experienced team of 15 investment professionals Employee investments account for a significant percentage of total

firm assets Ability to analyse and invest across the capital structure for best risk-

adjusted returns

The strategy aims to deliver equity type returns with less volatility than the market over the medium to long term

Sirios Capital Management: AUM $3.5bn Performance objective

Schroder GAIA Sirios US Equity US equity long short fund with demonstrated downside protection

20

Source: Schroders and Sirios as at 31 January 2016. *Performance shown for Sirios Overseas Fund Limited in USD. Sirios’ offshore fund has been used from July 1999 to February 2013 . From March 2013 onwards Schroder GAIA Sirios US Equity C Acc USD has been used. . Performance is shown net of fees, NAV to NAV.

Performance analysis (Sirios equity long short strategy*)

Fundamental long short equity fund, typically long-biased Invests primarily in US mid/large-cap companies with material

exposure in Asia and Europe Opportunistic exposure to fixed income for equity-like returns with

lower risk Identifies attractively valued, growth-oriented companies for longs;

shorts in companies with deteriorating fundamentals and poor balance sheets

Moderate use of leverage Low correlation to equity markets Low downside participation

Fund key features

Strategy* Index

Annualised return 8.6% 3.9%

Annualised volatility 9.0% 15.1%

Sharpe ratio 0.71 0.11

Maximum drawdown -19.3% -50.9%

Portfolio Manager John Brennan, Sirios

Inception date 27 February 2013

Base currency USD

Institutional share class fee 1.50%/20%

Liquidity Daily

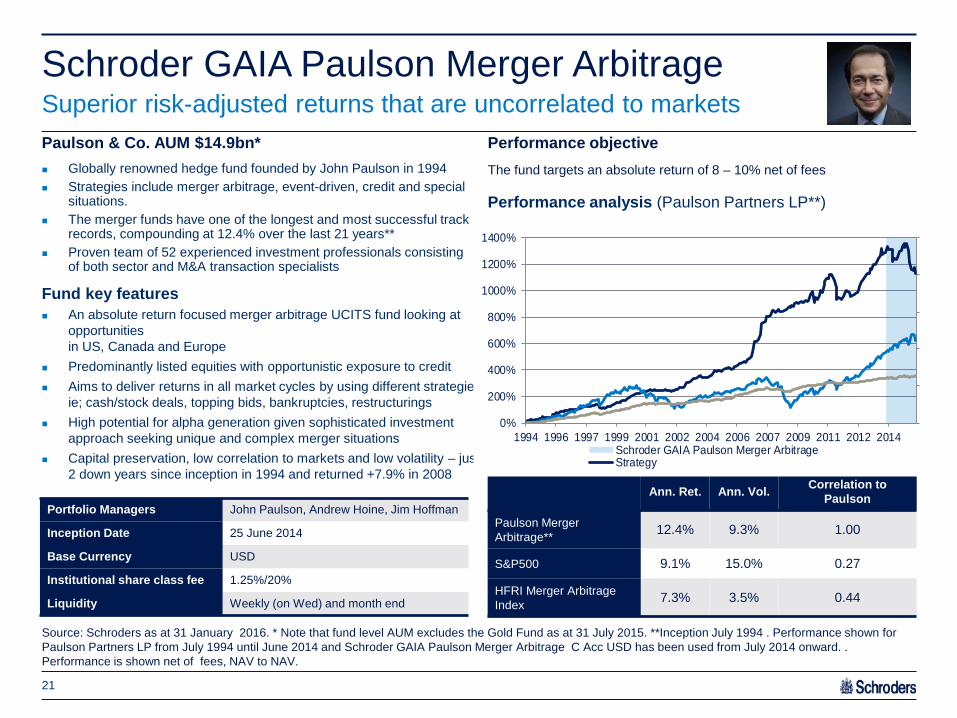

Globally renowned hedge fund founded by John Paulson in 1994 Strategies include merger arbitrage, event-driven, credit and special

situations. The merger funds have one of the longest and most successful track

records, compounding at 12.4% over the last 21 years** Proven team of 52 experienced investment professionals consisting

of both sector and M&A transaction specialists

The fund targets an absolute return of 8 – 10% net of fees

Paulson & Co. AUM $14.9bn* Performance objective

Schroder GAIA Paulson Merger Arbitrage Superior risk-adjusted returns that are uncorrelated to markets

21

Source: Schroders as at 31 January 2016. * Note that fund level AUM excludes the Gold Fund as at 31 July 2015. **Inception July 1994 . Performance shown for Paulson Partners LP from July 1994 until June 2014 and Schroder GAIA Paulson Merger Arbitrage C Acc USD has been used from July 2014 onward. . Performance is shown net of fees, NAV to NAV.

Performance analysis (Paulson Partners LP**)

An absolute return focused merger arbitrage UCITS fund looking at opportunities in US, Canada and Europe

Predominantly listed equities with opportunistic exposure to credit Aims to deliver returns in all market cycles by using different strategies.

ie; cash/stock deals, topping bids, bankruptcies, restructurings High potential for alpha generation given sophisticated investment

approach seeking unique and complex merger situations Capital preservation, low correlation to markets and low volatility – just

2 down years since inception in 1994 and returned +7.9% in 2008

Portfolio Managers John Paulson, Andrew Hoine, Jim Hoffman

Inception Date 25 June 2014

Base Currency USD

Institutional share class fee 1.25%/20%

Liquidity Weekly (on Wed) and month end

Ann. Ret. Ann. Vol. Correlation to Paulson

Paulson Merger Arbitrage** 12.4% 9.3% 1.00

S&P500 9.1% 15.0% 0.27

HFRI Merger Arbitrage Index 7.3% 3.5% 0.44

Fund key features

0%

200%

400%

600%

800%

1000%

1200%

1400%

1994 1996 1997 1999 2001 2002 2004 2006 2007 2009 2011 2012 2014Schroder GAIA Paulson Merger ArbitrageStrategy

Portfolio Manager Simon Thorp and James Sclater, KKR

Inception date 06 November 2013

Base currency EUR

Institutional share class fee 1.25%/15%

Liquidity Weekly (on Wed) and month end

The KKR Credit Alpha strategy is a directional long/short liquid European credit strategy.

It invests primarily in liquid high yield and low investment grade fixed income securities and derivatives (bonds, CDS, credit indices and credit options).

KKR Credit Long Short team is one of the most established in Europe Dedicated team of 6 experienced investment professionals

The fund targets an absolute return of 7-10% net of fees KKR Credit Advisors (UK) AUM: c.$26.4bn* Performance objective

Schroder GAIA KKR Credit Low net credit long short fund investing predominately in Europe

22

Source: Schroders as at 31 January 2016. KKR & Co. L.P. acquired Avoca Capital on 19 February 2014. * AUM as at 31 December 2015 **Performance shown for KKR’s credit long short strategy: From 11 November 2000 until 31 October 2013 the KKR Credit Alpha Fund has been used. From 1 November 2013 to 6 November 2013 a net estimate of the KKR Credit Alpha fund has been used. From 7 November 2013 onwards performance is for Schroder GAIA KKR Credit C Acc EUR. . Performance is shown net of fees, NAV to NAV.

Performance analysis (KKR credit long short strategy**)

An absolute return focused credit long short UCITS fund Investment grade and high yield exposure predominately in Europe Aims to identify companies with improving or deteriorating capacity to

service their debt, where that change is not reflected in their current pricing

Deep dive credit research and value investing approach Best-in-class technology at the centre of the credit process “All weather” positive returns through the cycle, the strategy has had

no down years in last decade

Fund key features

Ann. Ret. Ann. Vol. Sharpe ratio

Strategy** 7.1% 6.9% 0.8

IBOXX Liquid HY 5.0% 10.3% 0.3

Barclays Gbl. Agg. 5.0% 2.7% 1.1

MSCI World 2.7% 14.5% 0.1

-50%

0%

50%

100%

150%

200%

250%

2000200120022003200420052006200720082009201020112012201320142015

Schroder GAIA KKR Credit

Benefit Street Partners (BSP) was established in 2008 and manages over $10 billion in assets

Multi-strategy credit specialist including high yield, levered loans, private/opportunistic debt, liquid credit, structured credit and commercial real estate debt

Team of 59 investment professionals BSP is the debt investment arm of Providence Equity with AUM of

$45bn

The fund targets an absolute return of 5 – 7% net of fees

Investment Manager: AUM $11.0bn* Performance objective

Schroder GAIA BSP Credit Low net credit long short fund investing predominately in US

23

The BSP Credit Long Short Strategy includes BSP Credit Alpha Fund and a separately managed account (SMA) following a similar strategy. Performance is shown net of fees. From 7 February 2011 to 1 March 2012, the performance is for SMA, from 1 March 2012 until June 2015 for the BSP Credit Alpha Fund, and from July 2015 onwards for Schroder GAIA BSP Credit C Acc USD. *As at 31 September 2015. Source: Schroders, BSP, Bloomberg, Merrill Lynch as at 31 October 2015. . Performance is shown net of fees, NAV to NAV.

Performance analysis (Cayman hedge fund)

Based on an existing Cayman hedge fund with $1.4 billion AUM, which includes ~$110 million from employees

Targets 5-7% net return with low volatility, low correlation Aims to provide capital growth through investment worldwide, with at

least 51% of the Fund invested in US companies Absolute return approach combining fundamental credit analysis Sophisticated trade structuring and active trading to maximize

expected return while limiting downside risk across market cycles Strategies employed include fundamental longs/shorts, relative

value pair trades and capital structure arbitrage

Portfolio Manager Thomas Gahan

Inception date 17 June 2015

Base currency USD

Institutional share class fee 1.50%/20% over Libor capped at 2% 1.00%/15% over Libor capped at 2% (early bird up to $80m)

Liquidity Weekly (on Wed) and month end

Fund key features

Annualised return 4.7%

Annualised volatility 3.4%

Max drawdown -5.3%

0%

5%

10%

15%

20%

25%

30%

35%

Feb-

11M

ay-1

1A

ug-1

1N

ov-1

1Fe

b-12

May

-12

Aug

-12

Nov

-12

Feb-

13M

ay-1

3A

ug-1

3N

ov-1

3Fe

b-14

May

-14

Aug

-14

Nov

-14

Feb-

15M

ay-1

5A

ug-1

5N

ov-1

5

-50%

0%

50%

100%

150%

200%

250%

300%

Jan-

04A

ug-0

4M

ar-0

5O

ct-0

5M

ay-0

6D

ec-0

6Ju

l-07

Feb-

08S

ep-0

8A

pr-0

9N

ov-0

9Ju

n-10

Jan-

11A

ug-1

1M

ar-1

2O

ct-1

2M

ay-1

3D

ec-1

3Ju

l-14

Feb-

15S

ep-1

5

BlueTrend Barclays Global Aggregate Bond Index

HFRI Fund Weighted Composite Index MSCI World

Systematica founded in January 2015 after a decade of experience within BlueCrest Capital Management

Systematica manage total assets of $9.0bn, with $7.2bn in their trend-following strategy

Investment team headed by Leda Braga, former President and Head of Systematic Trading at BlueCrest Capital Management

The fund aims to provide capital growth by adopting a pure systematic trend following strategy, across global markets, based on quantitative signals with multiple time horizons. It targets returns of 10-15%.

Investment Manager: AUM $9.0bn Performance objective

Schroder GAIA BlueTrend Diversified Systematic Macro Trend Following Strategy

24

Source: Systematica Investments and Schroders, as at 31 January 2016. Managed by BlueCrest Capital Management Group from inception to 1 January 2015 when Systematica Investments Limited (acting in its capacity as general partner of Systematica Investments LP) became the investment manager. *BlueTrend strategy refers to an SMA from January 2004 to March 2004 and BlueTrend Fund Limited (Class A USD) from 1 April 2004 to 31 December 2015. From 1 January 2016 onwards performance is provided for Schroder GAIA BlueTrend C Acc USD. Performance for Barclays Global Aggregate Bond Index and HFRI Fund Weighted Composite Index as at 31 December 2015. Performance is shown net of fees, NAV to NAV.

Performance analysis (BlueTrend strategy*)

Diversified systematic trend following fund, launched in April 2004 Extremely competitive track record with average annualised return

of 11%, with 14% annualised volatility Positive in 9 out of the past 10 years Uncorrelated returns over time/delivered positive returns in both up

and down markets Performed well in periods of prolonged market downturns like 2008 Trades the most liquid assets among equity, currency, commodity

and fixed income

Strategy

Annualised return 11.2%

Annualised volatility 14.1%

Maximum drawdown -22.1%

Investment team Head Leda Braga

Inception date 9 December 2015

Base currency USD

Institutional share class fee 1.50%/20%

Liquidity Weekly (on Wed) and month end

Fund key features

Main reservations and dispelling the myths

0

5

10

15

20

25

Institutional Retail

Main reservations and typical alternative allocations Fees, liquidity, education

26

Source: Goldman Sachs, Morningstar/Barron’s, McKinsey, Simfund, November 2013

Can retail allocations to alternatives increase with the introduction of Liquid Alternatives?

0

0.1

0.2

0.3

0.4

0.5

0.6

Fees Lack ofliquidity

Lack oftransparency

Benefitsuncertain

Unclear howstrategy works

in portfolioframework

Institutional Retail

‘Knowledge

% of advisors Alternatives allocation

Top reasons to hesitate on alternatives

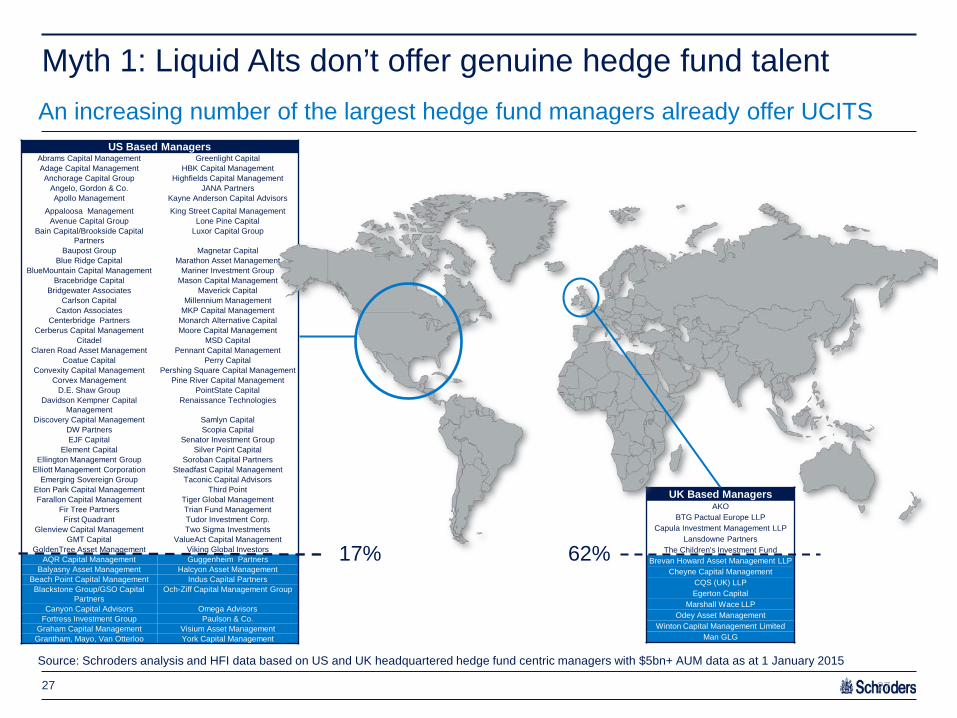

UK Based Managers AKO

BTG Pactual Europe LLP Capula Investment Management LLP

Lansdowne Partners The Children's Investment Fund

Brevan Howard Asset Management LLP Cheyne Capital Management

CQS (UK) LLP Egerton Capital

Marshall Wace LLP Odey Asset Management

Winton Capital Management Limited Man GLG

US Based Managers Abrams Capital Management Greenlight Capital Adage Capital Management HBK Capital Management Anchorage Capital Group Highfields Capital Management

Angelo, Gordon & Co. JANA Partners Apollo Management Kayne Anderson Capital Advisors

Appaloosa Management King Street Capital Management Avenue Capital Group Lone Pine Capital

Bain Capital/Brookside Capital Partners

Luxor Capital Group

Baupost Group Magnetar Capital Blue Ridge Capital Marathon Asset Management

BlueMountain Capital Management Mariner Investment Group Bracebridge Capital Mason Capital Management

Bridgewater Associates Maverick Capital Carlson Capital Millennium Management

Caxton Associates MKP Capital Management Centerbridge Partners Monarch Alternative Capital

Cerberus Capital Management Moore Capital Management Citadel MSD Capital

Claren Road Asset Management Pennant Capital Management Coatue Capital Perry Capital

Convexity Capital Management Pershing Square Capital Management Corvex Management Pine River Capital Management

D.E. Shaw Group PointState Capital Davidson Kempner Capital

Management Renaissance Technologies

Discovery Capital Management Samlyn Capital DW Partners Scopia Capital EJF Capital Senator Investment Group

Element Capital Silver Point Capital Ellington Management Group Soroban Capital Partners

Elliott Management Corporation Steadfast Capital Management Emerging Sovereign Group Taconic Capital Advisors

Eton Park Capital Management Third Point Farallon Capital Management Tiger Global Management

Fir Tree Partners Trian Fund Management First Quadrant Tudor Investment Corp.

Glenview Capital Management Two Sigma Investments GMT Capital ValueAct Capital Management

GoldenTree Asset Management Viking Global Investors AQR Capital Management Guggenheim Partners

Balyasny Asset Management Halcyon Asset Management Beach Point Capital Management Indus Capital Partners Blackstone Group/GSO Capital

Partners Och-Ziff Capital Management Group

Canyon Capital Advisors Omega Advisors Fortress Investment Group Paulson & Co.

Graham Capital Management Visium Asset Management Grantham, Mayo, Van Otterloo York Capital Management

Myth 1: Liquid Alts don’t offer genuine hedge fund talent

Source: Schroders analysis and HFI data based on US and UK headquartered hedge fund centric managers with $5bn+ AUM data as at 1 January 2015

27

An increasing number of the largest hedge fund managers already offer UCITS

62% 17%

27

80

85

90

95

100

105

Jun-14 Dec-14 Jun-15 Dec-15Schroder GAIA Paulson Merger Arbitrage C Acc USDPauslon Partners LP

90

100

110

120

130

140

Feb-13 Aug-13 Feb-14 Aug-14 Feb-15 Aug-15Schroder GAIA Sirios US Equity - C Acc USD SiriosReference fund

90

110

130

150

170

190

Nov-09 Nov-10 Nov-11 Nov-12 Nov-13 Nov-14 Nov-15Schroder GAIA Egerton Equity C Acc EUREgerton European Equity Fund Ltd - Class B20

KKR

Egerton Sirios

Myth 2: All liquid alternatives are hedge fund lite Schroder GAIA strategies represent core capabilities with low tracking error

28

Source: Schroders, Egerton, Sirios and KKR. As at 31 January 2016. *Paulson as at 31 December 2015 Performance data is net of all fees and charges. The GAIA C share class has been used for all GAIA funds. For Egerton European Equity from November 2009 to 31 December 2011 the B16 share class has been used. Please note, Egerton’s offshore hedge fund included a provision for potential tax liabilities at the end of March 2010 resulting in a 5.1% decrease in the NAV. These tax liabilities did not impact Schroder GAIA Egerton Equity. For illustrative purposes the data here ignores this provision and therefore shows the two strategies on a more like for like basis. No indicative weekly NAVs were produced for Egerton’s B16 share class during April 2010, therefore the B1 share class has been used as a proxy over this period. From 1 January 2012 to 31 December 2012 the B29 share class was used. From 1 January 2013 onwards the B20 share class is used

Paulson*

90

95

100

105

Oct-13 Apr-14 Oct-14 Apr-15 Oct-15Schroder GAIA KKR Credit - Class C Acc EURKKR Credit Alpha

Performance comparison UCITS vs. offshore hedge funds

Myth 3: Liquid alternatives are inferior to hedge funds Despite limitations, liquid alts can provide similar benefits to hedge funds

29

Source: HFR as of 31 January 2016

Industry performance

HFRI HFRU

Number of funds 2,200 500

Regulatory regime Flexible UCITS

Opportunity set

-30%

-20%

-10%

0%

10%

20%

30%

2008 2009 2010 2011 2012 2013 2014 2015

HFRI Fund Weighted Composite Index HFRU Hedge Fund Composite Index

Index YTD 2016 F/Y2015 F/Y 2014 Annualised Return

Annualised Volatility Drawdown Months to Recover

Correlation to S&P 500

(5 years)

Traditional Hedge Fund HFRI Offshore Hedge Fund Weighted Composite Index

-1.7% -1.1% 3.0% 2.1% 6.6% -20.1% 14 0.84

Liquid Alternatives HFRU UCITS Hedge Fund Composite Index

-3.0% 1.7% 4.5% 1.7% 3.5% -6.7% 10 0.63

Typical Fee Structures Cumulative performance

Myth 4: All liquid alts are expensive What is most important price or performance?

30

Source: Morningstar, Schroders, as at 31 December 2015. Common inception date taken of September 1994. Egerton performance shows Egerton offshore fund from December 1994 until November 2009. From December 2009 onwards Schroder GAIA Egerton Equity C Acc EUR is used. Performance shown is net of any fees and calculated on an NAV to NAV basis.

Typical Fees Variable Fees

Cumulative return since

1994

MSCI World ETF 10bps None 158%

Global Equity long only

0.50-1.00% None 197%

HFRI 1.25-1.75% 15-20% 431%

Schroder GAIA Egerton Equity

1.25% 20% 1,523%

0%

200%

400%

600%

800%

1000%

1200%

1400%

1600%

1800%

1994

1995

1996

1997

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2012

2013

2014

2015

Global Equity Large Caps BlendEgertonMSCI WorldHFRI

The power of diversifying return streams

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Egerton KKR Paulson Sirios BSP MSCI World BlueTrend

Paulson

Egerton

KKRSirios

MSCI WorldBSP

BlueTrend

Schroder External Hedge Fund Manager Partnerships Cumulative performance

32

Source: Schroders. Analysis shown from November 2000 (common inception date) to 31 January 2016. The data shown for ‘Schroders External Hedge Fund Manager Partnerships’ is shown for the relevant flagship hedge fund strategy from November 2000 until inception of the Schroder GAIA fund. From each inception, performance is shown for Schroder GAIA Egerton Equity, Schroder GAIA Sirios US Equity, Schroder GAIA KKR Credit and Schroder GAIA Paulson Merger Arbitrage. From 7 February 2011 to 1 March 2012, BSP performance is shown for SMA, and from 1 March 2012 onwards for the BSP Credit Alpha Fund. . Performance is shown net of fees, NAV to NAV.

Schroder External Hedge Fund Manager Partnerships All strategies have outperformed equity markets on a risk adjusted basis

33

Return Std dev Sharpe ratio Schroder GAIA BlueTrend** 11.2% 14.1% 0.7 Schroder GAIA Egerton Equity 8.4% 8.5% 0.8 Schroder GAIA Paulson Merger Arbitrage 9.2% 8.3% 0.9 Schroder GAIA KKR Credit 7.1% 6.9% 0.8 Schroder GAIA Sirios US Equity 6.7% 8.5% 0.6 Schroder GAIA BSP Credit* 4.7% 3.4% 1.3 MSCI World 2.7% 14.5% 0.1

0%

2%

4%

6%

8%

10%

12%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0%

Schroder GAIA Paulson Merger Arbitrage Schroder GAIA KKR Credit Schroder GAIA Egerton Equity Schroder GAIA Sirios US EquitySchroder GAIA BSP Credit BlueTrend MSCI World

Return

Volatility

Source: Schroders. Analysis shown from November 2000 (common inception date) to 31 January 2016. *Please note that BSP and BlueTrend have an inception date since November 2000 and performance is included from inception of the strategy. For BSP, from 7 February 2011 to 1 March 2012, the performance is for SMA, from 1 March 2012 until June 2015 for the BSP Credit Alpha Fund, and from July 2015 onwards for Schroder GAIA BSP Credit. The data shown for ‘Schroders External Hedge Fund Manager Partnerships’ is shown for the relevant flagship hedge fund strategy from November 2000 until inception of the Schroder GAIA fund. From each inception, performance is shown for Schroder GAIA Egerton Equity, Schroder GAIA Sirios US Equity, Schroder GAIA KKR Credit, Schroder GAIA Paulson Merger Arbitrage and Schroder GAIA BSP Credit. Schroder GAIA BlueTrend strategy performance from January 2004. From January 2004 until March 2004 a SMA is used and BlueTrend Fund Limited (Class A USD) from 1 April 2004 onwards.

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

2000 2002 2004 2006 2008 2010 2012 2014

Schroders External Hedge Fund Manager Partnerships

MSCI World NR LCL

Schroder External Hedge Fund Manager Partnerships Performance simulation with equal allocation to each external manager

34

Source: Schroders. Analysis shown from November 2000 (common inception date) to 31 January 2016. *Please note that BSP and BlueTrend have an inception date since November 2000 and performance is included from inception of the strategy. For BSP, from 7 February 2011 to 1 March 2012, the performance is for SMA, from 1 March 2012 until June 2015 for the BSP Credit Alpha Fund, and from July 2015 onwards for Schroder GAIA BSP Credit. The data shown for ‘Schroders External Hedge Fund Manager Partnerships’ is shown for the relevant flagship hedge fund strategy from November 2000 until inception of the Schroder GAIA fund. From each inception, performance is shown for Schroder GAIA Egerton Equity, Schroder GAIA Sirios US Equity, Schroder GAIA KKR Credit, Schroder GAIA Paulson Merger Arbitrage and Schroder GAIA BSP Credit. Schroder GAIA BlueTrend strategy performance from January 2004. From January 2004 until March 2004 a SMA is used and BlueTrend Fund Limited (Class A USD) from 1 April 2004 onwards.

Return Std Dev Sharpe ratio Schroders External Hedge Fund Manager Partnerships* 8.9% 5.4% 1.3

MSCI World NR LCL 3.1% 14.5% 0.1

Combining alternative funds provides superior risk adjusted returns

0.0% 5.0% 10.0% 15.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

0%1%2%3%4%5%6%7%8%9%

10%

0% 2% 4% 6% 8% 10% 12% 14% 16%

Schroders External Hedge Fund Manager Partnerships* MSCI World

Hedge fund AUM continues to grow with strong demand for liquid alternatives as portfolio diversifiers given expected heightened volatility

Growth has been fuelled by sophisticated private banks and wealth managers, looking forward we expect this client base to expand to include broader UCITS investors with growing demand

The UCITS hedge fund industry is now >$200bn of AUM with 25% managed by hedge fund managers** and a number of high profile launches expected in 2016

Total UCITS hedge fund platform assets grew in 2015 from $24.1bn* to $32.4bn* and represents c10% of total market share

Fees are an important consideration for liquid alternatives and each strategy should be assessed based on numerous criteria such as manager skill, unique alpha generation, consistent risk adjusted returns, proven downside protection and volatility management

Schroders offers a broad range of liquid alternative funds including a leading platform of external managers

Conclusions

35

Source: Schroders January 2016 *Kepler as at 30 September 2015. **Barclays strategic consulting analysis as at 30 September 2015

Important Information: This presentation does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of Schroder GAIA (the “Company”). Nothing in this presentation should be construed as advice and is therefore not a recommendation to buy or sell shares.

Subscriptions for shares of the Company can only be made on the basis of its latest Key Investor Information Document and prospectus, together with the latest audited annual report (and subsequent unaudited semi-annual report, if published), copies of which can be obtained, free of charge, from Schroder Investment Management (Luxembourg) S.A.

An investment in the Company entails risks, which are fully described in the prospectus.

Past performance is not a reliable indicator of future results, prices of shares and the income from them may fall as well as rise and investors may not get the amount originally invested. Schroders have expressed their own views and opinions in this presentation and these may change. This presentation is issued by Schroder Investment Management Limited, 31, Gresham Street, EC2V 7QA, who is authorised and regulated by the Financial Conduct Authority. Registration No 1893220, England.

For your security, communications may be taped or monitored.

Third party data is owned or licensed by the data provider and may not be reproduced or extracted and used for any other purpose without the data provider's consent. Third party data is provided without any warranties of any kind. The data provider and issuer of the document shall have no liability in connection with the third party data. The Prospectus and/or www.schroders.com contains additional disclaimers which apply to the third party data.

Important Information

36

![Malonamide, phosphine oxide and calix[4]arene ... · the future use of volatile organic compounds in nowadays liquid–liquid extraction systems. One possible alternative to these](https://static.fdocuments.net/doc/165x107/5f368d51b7a9a60b987899ee/malonamide-phosphine-oxide-and-calix4arene-the-future-use-of-volatile-organic.jpg)