Invest North 2013investnorth.in/Editor/ckfinder/core/connector/userfiles/files... · Capital city:...

30

Confederation of Indian Industry Invest North 2013 A CII-KPMG study Rajasthan State Profile August 2013

Transcript of Invest North 2013investnorth.in/Editor/ckfinder/core/connector/userfiles/files... · Capital city:...

Confederation of Indian Industry

Invest North 2013

A CII-KPMG study

Rajasthan State Profile

August 2013

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 1

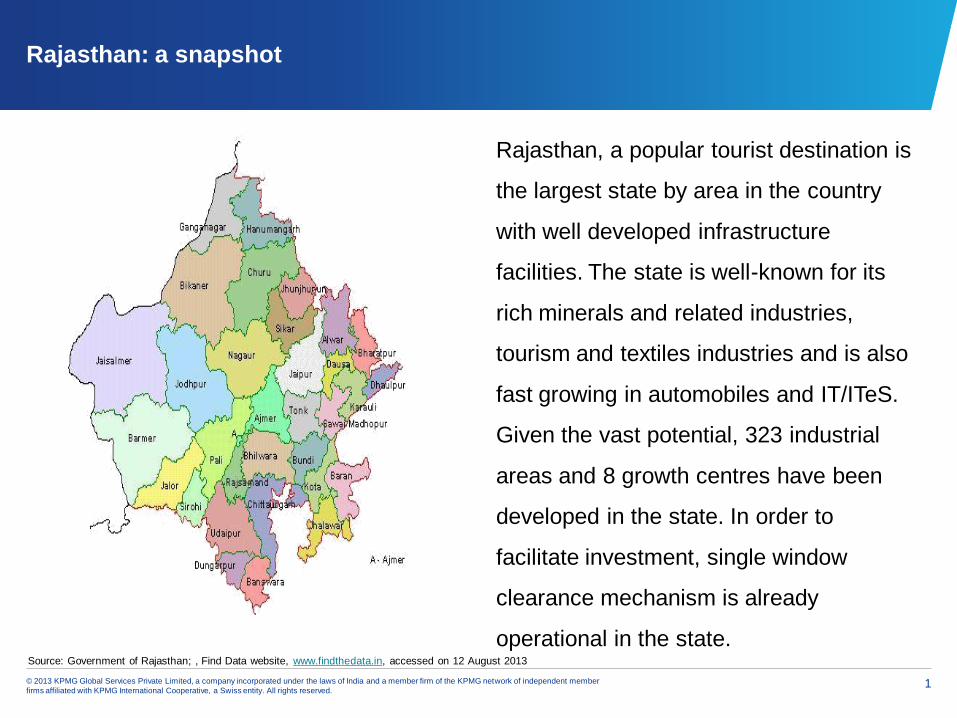

Rajasthan: a snapshot

Rajasthan, a popular tourist destination is

the largest state by area in the country

with well developed infrastructure

facilities. The state is well-known for its

rich minerals and related industries,

tourism and textiles industries and is also

fast growing in automobiles and IT/ITeS.

Given the vast potential, 323 industrial

areas and 8 growth centres have been

developed in the state. In order to

facilitate investment, single window

clearance mechanism is already

operational in the state. Source: Government of Rajasthan; , Find Data website, www.findthedata.in, accessed on 12 August 2013

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 2

Rajasthan: a snapshot

Overview

Economic indicators*

■ GSDP: State GDP recorded a CAGR of 9.2 percent during FY08-

FY12

■ GSDP composition: This has marginally shifted in favor of

Services

■ Sector-wise CAGR: Agriculture (7.9 percent), Industry (8.4

percent), Services (10.4 percent)

■ Per capita income: INR28,851 (USD602) in FY12 (latest available)

Notes: 1 USD = INR 47.9

*At constant FY05 prices (data as of February 2013)

Source: MOSPI

1,600 1,745 1,862

2,147 2,278

0

500

1,000

1,500

2,000

2,500

FY08 FY09 FY10 FY11 FY12

GSDP (INR billion)*

22.4 21.4 19.5 22.6 21.4

32.0 31.4 32.6 30.9 31.1

45.6 47.2 47.9 46.5 47.5

0

20

40

60

80

100

FY08 FY09 FY10 FY11 FY12

Agriculture Industry Services

GSDP composition (percent)*

Geographic and demographic indicators

■ Geographical area (sq km): 342,239

■ No. of districts: 33

■ Capital city: Jaipur

■ Key cities: Jaipur, Udaipur, Kota, Jodhpur, Ajmer and Alwar

■ Total population, 2011 census (million): 68.6

■ Population density, 2011 census (persons per sq km): 201

■ Literacy rate, 2011 census (percent): 67.1

Source: Census 2011 (http://www.census2011.co.in/census/state/rajasthan.html)

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 3

Rajasthan: a snapshot (cont.)

■ Installed power capacity, June 2013 (MW)

■ Road length, March 2011 (Km)

■ No. of airports, August 2013

■ Wireless subscribers, April 2013 (million)

■ Wireline subscribers, April 2013 (million)

Units

12,156

241,318

6

49

1

Investment

■ FDI: INR33.3 billion (USD685

million) during April 2000 to

April 2013

Physical infrastructure

343

31 51 33

132

0

100

200

300

400

FY09 FY10 FY11 FY12 FY13 Note: 1 USD = 48.6 during April 2000-April 2013

2 main airports at Jaipur and Udaipur ; Two civil enclaves at Jodhpur and Jaisalmer

Sources: CEA; TRAI; Ministry of Commerce and Industry; Ministry of Road Transport and Highways; Airports Authority of India; Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 4

State’s sector specific strengths

Auto and Auto Components Glass and Ceramics

Textiles

Solar power Petrochemicals

Agro processing

Source: Government of Rajasthan

IT/ITeS

Other sectors

Priority sectors

■ Tourism

■ Mineral processing

■ Renewable energy

■ Cement

■ Education

■ Gems and Jewellery

■ Infrastructure and Logistics

■ Handicrafts

■ Biotechnology and Health

■ Financial Services

■ Real estate

■ Retail

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 5

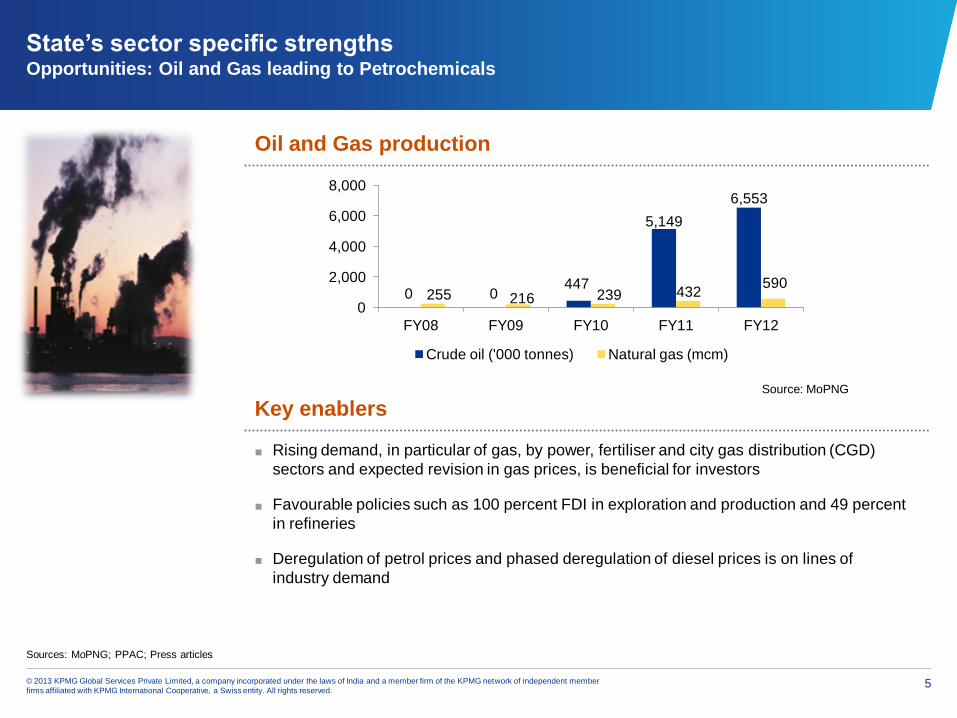

State’s sector specific strengths Opportunities: Oil and Gas leading to Petrochemicals

Oil and Gas production

■ Rising demand, in particular of gas, by power, fertiliser and city gas distribution (CGD)

sectors and expected revision in gas prices, is beneficial for investors

■ Favourable policies such as 100 percent FDI in exploration and production and 49 percent

in refineries

■ Deregulation of petrol prices and phased deregulation of diesel prices is on lines of

industry demand

Key enablers Source: MoPNG

0 0 447

5,149

6,553

255 216 239 432 590

0

2,000

4,000

6,000

8,000

FY08 FY09 FY10 FY11 FY12

Crude oil ('000 tonnes) Natural gas (mcm)

Sources: MoPNG; PPAC; Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 6

State’s sector specific strengths Opportunities: Oil and Gas leading to Petrochemicals (cont.)

■ Large reserves of oil and gas represent significant opportunity in view of the increased

potential for development

■ Share of oil and gas production from the state has increased from NIL to 17.2 percent in

case of crude and from 0.8 percent to 1.2 percent in case of gas during FY08-FY12

■ With increased oil and gas production, opportunities also exist in oil and gas transmission

and distribution, underground lignite gasification and coal to liquid conversion plants

■ Throughput of transmission pipelines (product) grew at a CAGR of 8.5 percent during

FY08-FY12

■ The state’s 2,572 retail outlets are the 7th highest in India

■ City Gas Distribution (CGD) network is under operation at Kota that is being carried out

through over 90 km of distribution pipelines

■ Rajasthan State Refinery formed joint venture with Hindustan Petroleum Corporation

Limited (HPCL) for setting a 9 million tonnes refinery cum petrochemicals units at Barmer

at an investment of INR372 billion. It is the second biggest project in the state and will

generate 3,00,000 jobs. It is expected to be completed by December 2017 and bring in

INR86 trillion of investment

Sector opportunities

■ Oil and Natural Gas Corporation, Cairn India, Indian Oil Corporation, HPCL, GAIL (India)

and GAIL Gas among others

Existing companies

Sources: MoPNG; PPAC; Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 7

State’s sector specific strengths Opportunities ‒ Oil and Gas leading to Petrochemicals (cont.)

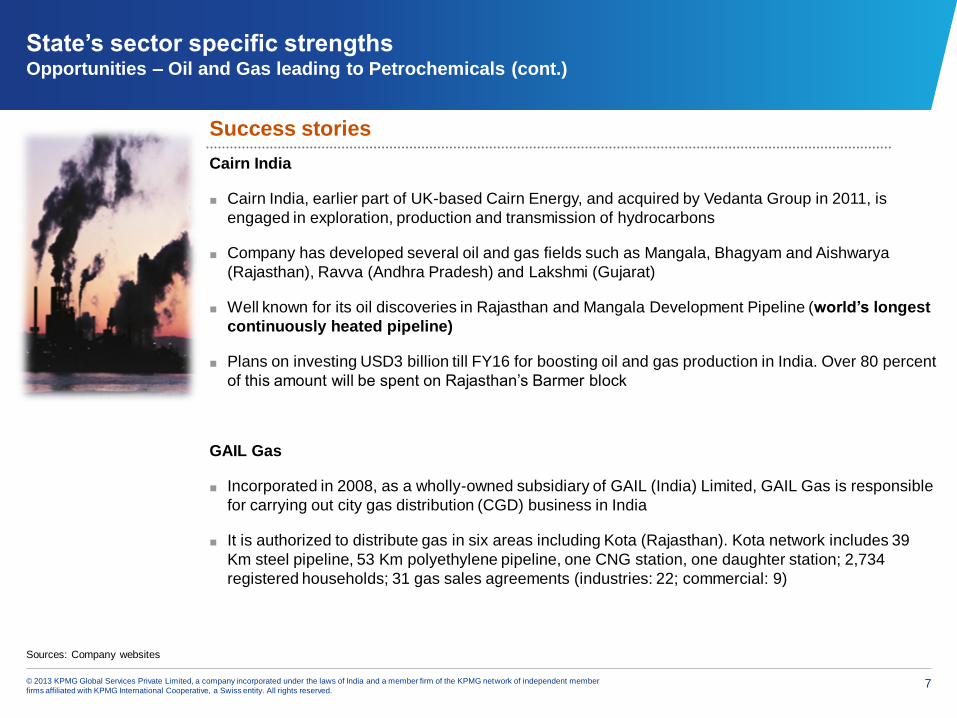

Cairn India

■ Cairn India, earlier part of UK-based Cairn Energy, and acquired by Vedanta Group in 2011, is

engaged in exploration, production and transmission of hydrocarbons

■ Company has developed several oil and gas fields such as Mangala, Bhagyam and Aishwarya

(Rajasthan), Ravva (Andhra Pradesh) and Lakshmi (Gujarat)

■ Well known for its oil discoveries in Rajasthan and Mangala Development Pipeline (world’s longest

continuously heated pipeline)

■ Plans on investing USD3 billion till FY16 for boosting oil and gas production in India. Over 80 percent

of this amount will be spent on Rajasthan’s Barmer block

GAIL Gas

■ Incorporated in 2008, as a wholly-owned subsidiary of GAIL (India) Limited, GAIL Gas is responsible

for carrying out city gas distribution (CGD) business in India

■ It is authorized to distribute gas in six areas including Kota (Rajasthan). Kota network includes 39

Km steel pipeline, 53 Km polyethylene pipeline, one CNG station, one daughter station; 2,734

registered households; 31 gas sales agreements (industries: 22; commercial: 9)

Success stories

Sources: Company websites

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 8

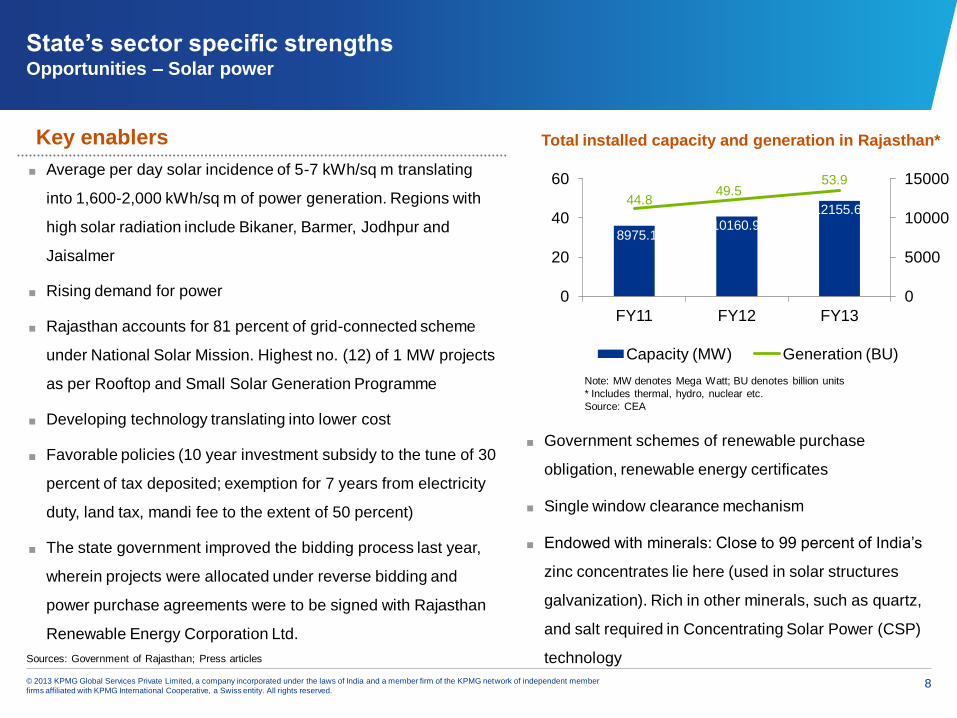

State’s sector specific strengths Opportunities ‒ Solar power

■ Average per day solar incidence of 5-7 kWh/sq m translating

into 1,600-2,000 kWh/sq m of power generation. Regions with

high solar radiation include Bikaner, Barmer, Jodhpur and

Jaisalmer

■ Rising demand for power

■ Rajasthan accounts for 81 percent of grid-connected scheme

under National Solar Mission. Highest no. (12) of 1 MW projects

as per Rooftop and Small Solar Generation Programme

■ Developing technology translating into lower cost

■ Favorable policies (10 year investment subsidy to the tune of 30

percent of tax deposited; exemption for 7 years from electricity

duty, land tax, mandi fee to the extent of 50 percent)

■ The state government improved the bidding process last year,

wherein projects were allocated under reverse bidding and

power purchase agreements were to be signed with Rajasthan

Renewable Energy Corporation Ltd.

Key enablers

Sources: Government of Rajasthan; Press articles

Total installed capacity and generation in Rajasthan*

Note: MW denotes Mega Watt; BU denotes billion units

* Includes thermal, hydro, nuclear etc.

Source: CEA

8975.1 10160.9

12155.6 44.8

49.5 53.9

0

5000

10000

15000

0

20

40

60

FY11 FY12 FY13

Capacity (MW) Generation (BU)

■ Government schemes of renewable purchase

obligation, renewable energy certificates

■ Single window clearance mechanism

■ Endowed with minerals: Close to 99 percent of India’s

zinc concentrates lie here (used in solar structures

galvanization). Rich in other minerals, such as quartz,

and salt required in Concentrating Solar Power (CSP)

technology

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 9

State’s sector specific strengths Opportunities ‒ Solar power (cont.)

■ Rajasthan has the highest installed solar power capacity in the northern region of 442

MW. This capacity accounts for a share of 92.3 percent in northern region’s solar power

capacity and of 31 percent of total installed solar power capacity in India, as of March 2013

■ Immense solar power potential presents opportunities for:

‒ Generation companies

‒ Transmission and distribution companies

‒ Equipment manufacturing or leasing companies

‒ Engineering, procurement and construction (EPC) companies

‒ Solar wafer manufacturers

■ Opportunities also exist for solar-based appliances manufacturers, such as water heaters,

solar-based desalination plants and solar pumps

■ State government plans on establishing Solar Energy Enterprise Zones (SEEZ) in Barmer,

Jaisalmer and Jodhpur districts and is offering incentives for the same

■ Upcoming solar parks in Jodhpur, Bikaner, Jaisalmer

Sector opportunities

Sources: IREDA, NVVN, State agencies, Project developers; Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 10

State’s sector specific strengths Opportunities ‒ Solar power (cont.)

Lanco

■ Lanco is a diversified business entity with operations ranging from power, solar,

infrastructure, natural resources and EPC

■ The company has four solar power plants in India at Rajasthan (Jaisalmer), Chhattisgarh

(Rajnandgaon) and two in Gujarat (Bhadrada and Chadiyana)

■ The company has signed several Power Purchase Agreements for these projects in

Rajasthan, Gujarat, Chhattisgarh etc. In Rajasthan, the PPA is for 100 MW

■ Besides, Lanco also has operations overseas in Asia-Pacific (China, Singapore, Indonesia)

and Europe (Italy, Netherlands)

■ Total income grew from INR33.4 billion in FY08 to INR47.4 billion in FY13

Success stories

Sources: Press articles; Company website

Existing companies

■ Reliance Power, Suzlon, Lanco, Welspun Energy, Azure Power, Fortum, Jakson Power

Solutions, Ajit Solar, Enercon, Vistas etc.

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 11

State’s sector specific strengths

Priority sectors

■ More than 100 companies operating in Alwar (Bhiwadi, Neemrana and Pathredi)

■ Original equipment manufacturer (OEM) specific zone created at Kushkhera

■ Several auto units operating in Japanese investment Zone at Neemrana

■ Training centre to be set up by Ministry of Micro, Small and Medium Enterprises

■ 57 percent of auto sales in India take place in northern and western regions, which are in close proximity to Rajasthan

■ Success stories: Ashok Leyland, Honda, Eicher, and Bosch

Auto and Auto Components

Source: Government of Rajasthan

Glass and Ceramics ■ State accounts for 40 percent of clay production and 70 percent of bone China production in India

■ Bikaner, Ganganagar, Nagaur, Bhilwara, Alwar, Udaipur are rich in various minerals such as gypsum, clay and limestone

■ As per Bureau of Investment Promotion, investment proposals >INR50 billion have been received recently in the sector

■ Upcoming Ceramics and Glass zone in Ghiloth of 752 acres with provisions being made for a gas pipeline

■ Opportunities: Industrial ceramics, potteryware, tiles, sanitaryware

■ Success stories: Saint Gobain, Kajaria and JCPL Ceramics

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 12

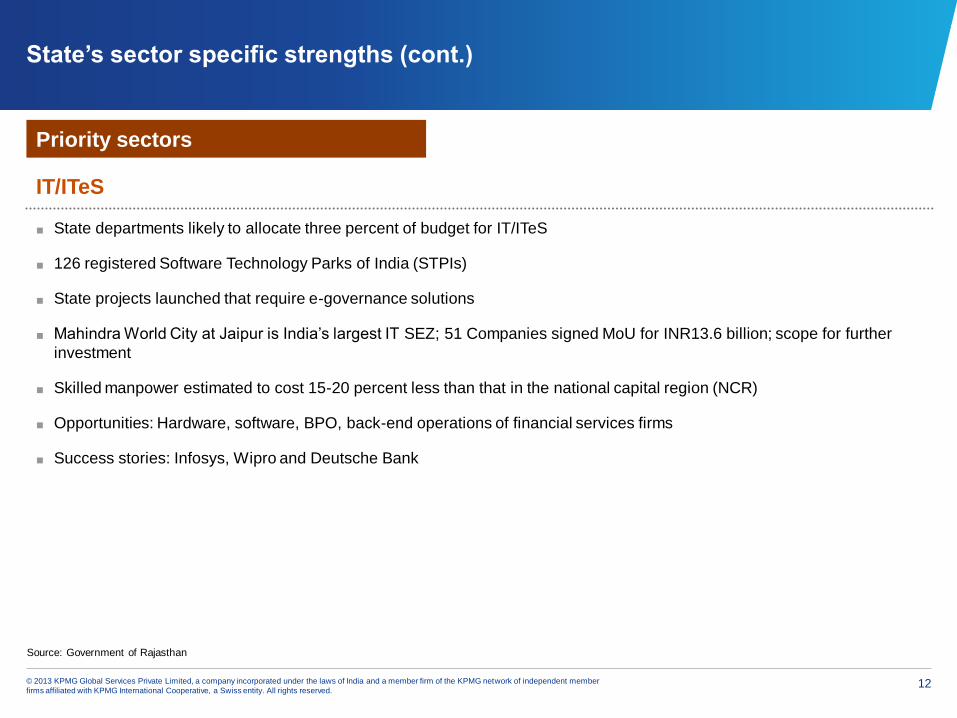

State’s sector specific strengths (cont.)

Priority sectors

■ State departments likely to allocate three percent of budget for IT/ITeS

■ 126 registered Software Technology Parks of India (STPIs)

■ State projects launched that require e-governance solutions

■ Mahindra World City at Jaipur is India’s largest IT SEZ; 51 Companies signed MoU for INR13.6 billion; scope for further

investment

■ Skilled manpower estimated to cost 15-20 percent less than that in the national capital region (NCR)

■ Opportunities: Hardware, software, BPO, back-end operations of financial services firms

■ Success stories: Infosys, Wipro and Deutsche Bank

IT/ITeS

Source: Government of Rajasthan

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 13

State’s sector specific strengths (cont.)

Priority sectors

■ Largest producer of polyester viscose yarn and synthetic

■ Industry hubs: Balotra, Bhiwadi, Bhilwara, Pali

■ Ministry of Textiles approved 9 parks costing INR15 billion and another INR4 billion as grant under Scheme for Integrated

Textile Parks (SITP)

■ Special customized package as approved by Cabinet

■ 10 Smart centers to be developed under Integrated Skill Development Scheme to train and employ 12,000 people

■ Success stories: Shriram Rayons and Ginni International

Textiles

■ Largest producer of oilseeds (rapeseed, mustard). High production of coriander, soybean, groundnut, pulses etc.

■ International Horticulture Innovation and Training Centre established at Jaipur

■ Opportunities: Organic farming, contract farming, cold chains, warehouses, testing and certification facilities

■ Success stories: Australian Wheat Board, ITC, Reliance

Agro processing

Source: Government of Rajasthan

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 14

Government identified areas/zones present immense investment opportunities

■ Behror

■ Bhiwadi

■ Ghiloth

■ Neemrana

■ Shahjhanpur

Industrial areas

■ Khushkhera ext.

■ Tapukara ext.

■ Soniyana (Chittor)

■ Kunjbiharipura (Jaipur)

■ Karni ext. (Bikaner)

■ Gajaner (Bikaner)

■ Borananda (Jodhpur)

Upcoming industrial areas

■ Automobile: Bhiwadi

■ Glass and ceramic (upcoming): Ghiloth

■ Textiles (upcoming on PPP mode): Jodhpur,

Bhilwara

Clusters/hubs

■ IT: Sitapura, Kota, Jodhpur, Udaipur

■ Textiles: Pali, Bagru, Kishangarh

■ Agro: Alwar, Jodhpur, Sriganganagar, Kota

Parks

Sources: Government of Rajasthan; Press articles

Growth centres

■ Abu Road

■ Bhilwara

■ Bikaner

■ Nagaur

■ Sikar

Mini growth centres

■ Baran

■ Bharatpur

■ Bhiwadi

■ Jodhpur

■ Karauli

■ Pali

■ Tonk

■ Udaipur

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 15

Government identified areas/zones present immense investment opportunities

(cont.)

Sources: Government of Rajasthan; Press articles

■ MoU: Neemrana Industrial Estate developed as per MoU between RIICO and Japan External Trade Organization

(JETRO)

■ Delhi-Mumbai Industrial Corridor (DMIC): This region to be part of much-talked about DMIC project

■ Investment: INR42 billion invested; expected employment: 9,120

■ Area: 1,167 acres, of this, close to 494 acres allotted to more than 25 companies (expected investment and

employment: more than INR25 billion and 3,000 respectively)

■ Sector presence: Most companies belong to automobile sector

■ Key investments: Daikin (INR6 billion), Mitsui Chemicals (INR4 billion), Mikuni India (INR1.5 billion), NYK Logistics

(INR1 billion) ; Nippon Steel (INR3 billion exp)

■ Units in production: 24 (Nissin Brake, Daikin Airconditioning, Mikuni, Nippon, Mytex Polymer etc.)

■ Proposed infrastructure development: Cargo airport between Ajarka and Kotkasim, and super express highway

through Neemrana

■ Gaining international attention: African delegation of 25 members from 15 countries and a delegation from Taiwan

Electrical and Electronic Manufacturers’ Association visited Neemrana

Neemrana: Japanese Investment Zone I

Rajasthan is the only state in the country to have three international investment zones

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 16

Government identified areas/zones present immense investment opportunities

(cont.)

Sources: Government of Rajasthan; Press articles

■ The investment zone being developed as per MoU signed between the RIICO and Korea Trade Investment

Promotion Agency (KOTRA)

■ Approximately 250 acres of land earmarked

■ Automobile and electronic sector companies have evinced greater interest

■ It will house a ceramic and glass hub, solar equipment manufacturing etc.

■ Gas supply being considered by GAIL

■ Area to be operational by 2014

Ghiloth: South Korean Investment Zone

Rajasthan is the only state in the country to have three international investment zones

■ The success of Japanese Investment Zone I laid the foundation for Japanese Investment Zone II

■ For the new phase, 500 acres of land will be made available

■ Central sales tax concession being offered to Japanese investors

Ghiloth: Japanese Investment Zone

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 17

Project-wise opportunities

Delhi-Mumbai Industrial Corridor

■ Length: 1,483 km

■ States: UP, Delhi, Haryana, Rajasthan, Gujarat and Maharashtra

■ Project implementation: Special Purpose Vehicle, Delhi Mumbai

Industrial Corridor Development Corporation

■ Around 40 percent of project areas falls in Rajasthan

■ Objectives: Provide high speed connectivity for high axle load wagons

(25 tonnes) of double stacked container trains; create at a global

manufacturing and trading hub

Project details

■ Government of India (49 percent)

■ Japan Bank for International Cooperation (26 percent)

■ Housing and Urban Development Corporation (19.9 percent)

■ Others include India Infrastructure Finance Company (4.1 percent) and

Life Insurance Corporation of India (1 percent)

Investors

Sources: Government of Rajasthan; DMIC; Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 18

Project-wise opportunities (cont.)

Delhi-Mumbai Industrial Corridor (cont.)

■ First phase of development: Six investment regions and six

industrial areas identified for investment

■ Second phase of development: Five investment regions and

seven industrial areas identified for investment

■ Expected investment in project’s cities: USD90-100 billion

■ Development of airports

■ Development of townships: 25-50 sq km in cities by 2019

■ Germany has evinced interest for investing in the project

Sources: Government of Rajasthan; DMIC; Press articles

■ Government approved financial assistance of INR25 billion per city

for development of Dadri, Noida, Ghaziabad, Manesar, Bawal,

Khushkhera, Bhiwadi, Neemrana, Ahmedabad, Dholera

First phase of development (2008-12)

Second phase of development (2013-17)

Core project areas

Industrial areas Investment regions

Jaipur-Dausa Khushkhera-Bhiwadi-

Neemrana

Rajsamand-Bhilwara Ajmer-Kishangarh

Jodhpur-Pali-Marwar

DMIC’s major junctions in Rajasthan

Phulera, Marwar, Bangurgram

Other areas for development

■ Industrial townships being planned in

Khushkhera-Bhiwadi-Neemrana and in

Jodhpur-Pali-Marwar regions

■ Greenfield airport, 24 sq km

■ Road corridor to connect Bhiwadi-Tapukara

industrial complex with Shahjahanpur-

Neemrana-Behror urban complex

■ Jodhpur-Pali-Marwar region to have an airport,

multi-modal logistics hub and mass rapid transit

system

■ Knowledge city Khushkhera-Bhiwadi-Neemrana

12.3 sq km

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 19

Project-wise opportunities (cont.)

Gyanodaya Schools Project

■ Objective: To provide equitable quality education in rural

areas

■ Project: Building secondary schools (Class VI-XII) in

areas where there is no such school in a 5 km radius

■ Estimated cost: INR6 billion

■ Project bid criterion: Viability Gap Funding (VGF)

■ Project type: PPP on design, build, finance, operate and

transfer (DBFOT) basis for 30 years after which, the

assets would be transferred to the Government

Project details

■ Government of Rajasthan (GoR) plans to build 165 new

senior secondary schools, of which five schools are

proposed to be built in each district of Rajasthan on

PPP basis

Source: Press articles

Phase-1

■ Phase-1 aims at constructing 50 schools in Ajmer (four

districts) and Udaipur (six districts)

■ Total investment in Phase-1, comprising 50 schools, has

been estimated to be INR2,074 million

Background

Project status

■ As of 31 March 2013, for Phase-1, the applicants have

been shortlisted and VGF has been sanctioned by the

Government of India (GoI) for the following areas:

‒ Ajmer

‒ Bhilwara

‒ Banswara

‒ Chittorgarh

‒ Dungarpur

‒ Nagaur

‒ Pratapgarh

‒ Rajsamand

‒ Tonk

‒ Udaipur

■ The applicants for the remaining schools would be

shortlisted in the upcoming phases of the project

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 20

Project-wise opportunities (cont.)

Gyanodaya Schools Project (cont.)

■ Project cost: INR6,000 million (Phase-1: INR2,074 million)

■ Internal rate of return (IRR): 14-16 percent

■ Average debt service coverage ratio: 2.1

Indicative project financials State Government

■ PPP school land to be provided on a 30 year lease

basis to the private partner at nominal lease rent

■ Construction subsidy with a ceiling of INR5 million

per school

Centre

■ VGF of 20 percent of the project cost

■ GoI approved financial assistance for the project

under the India Infrastructure Project Development

Fund (IIPDF)

■ Project development entails structuring, financial

modelling, bid documents preparation and bidding

process assistance. But, no financing support would

be provided during the operations

■ Asian Development Bank (ADB) has also provided

partial financial support for project development

activities

Fiscal support

Revenue model

■ Fee from private/open market students would be market-

based

■ Fees of Government-nominated voucher students would be

reimbursed by GoR

■ Voucher amounts would be calculated by GoR based on

Public Sector Comparator, linked to consumer price index

■ Additional revenues from any supplementary activities

undertaken by the school to the operator

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 21

Project-wise opportunities (cont.)

Water supply and sewerage system plants

Ajmer and Pushkar

■ Estimated cost: INR7 billion

■ Project type: PPP on DBFOT basis

■ Objective: Rehabilitation, augmentation and operation

of the water supply and sewerage system

Udaipur

■ Estimated cost: INR10 billion

■ Project type: PPP on DBFOT basis

■ Objective: Rehabilitation, augmentation and

operation of the water supply and sewerage system

Both projects are currently in the pipeline stage and are being managed by Public Health Engineering Department,

Government of Rajasthan

Status of the projects:

As of 31 March 2013, consultants submitted respective feasibility reports for both projects. Observations on the same

communicated. Modified reports are still awaited

Source: Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 22

Project-wise opportunities (cont.)

Nine textile parks under SITP

■ Scheme for Integrated Textile Parks (SITP): Aims at facilitating development of Integrated Textiles Parks (ITPs) in India

under PPP model

■ In March 2013, Ministry of Textiles started forming a panel of Project Management Consultants for implementing the

projects sanctioned under the 12th Five Year Plan

■ Scheme would be implemented through project specific Special Purpose Vehicle (SPV) of the user industry with one

project SPV for one park. Each ITP expected to have 50 units

■ GoI’s support under the scheme by way of grant or equity would be limited to 40 percent of project cost, which cannot

exceed INR400 million. Also, the grant cannot be used to purchase land for the ITP

■ The following textile parks have been approved in Rajasthan under SITP:

‒ Jaipur Texweaving Park, Kishangarh

‒ Kishangarh Hi-Tech Textile Park,

‒ Next Gen Textile Park Pvt. Ltd., Pali

‒ Jaipur Integrated Texcraft Park Pvt , Bagru

‒ Bharat Fabtex and Corporate Park, Pali

‒ Jaipur Kaleen Integrated Textiles Park, Dausa

‒ Mewar Industrial Textile Park, Pali

‒ Himmanda Integrated Textile Park, Baltora

‒ Rajasthan Integrated Apparel City, Tapukara

Source: Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 23

Government initiatives

Policies, schemes and reforms

Policies

■ There are more than 18 important policies and schemes in the

state

■ Textiles Policy 2013: Recently announced policy aims at

attracting investment of INR100 billion in five years and

generate 100,000 new jobs

■ Agro: State has an Agri-business policy and is already

working as per National Food Security Mission

■ Petrochemicals policy: The policy is being discussed in the

state

■ RIICO offers more than 20 schemes to investors in hotel and

tourism, complex building (commercial and residential),

interest rebates, equipment and project finance etc.

Reforms

■ State government issued several notifications to amend its

Factories Act, key being increase in renewal period to 10 years

from five years

■ Power tariffs increased by Rajasthan Electricity Regulatory

Commission

Incentives, single window clearance and

institutions

Incentives

■ Incentives provided under Rajasthan Investment Promotion

Scheme, 2010 to either new organizations or to existing ones

for expansion and modernization during April 2013 to March

2020

■ Customized packages to improved cost-economics of entities

■ Aims at getting new investment of INR105 billion in seven

years; generate 1,00,000 new jobs

Single Window System

■ Rajasthan, only state to have an Act on Single Window,

Rajasthan Enterprises Single Window Enabling and Clearance

Act, 2011

■ An online application, Single Point Electronic Monitoring and

Clearance System has also been introduced

■ Approvals provided in time bound manner

■ Mandatory approval for project investment of >INR10

Institutions

■ Bureau of Investment Promotion

■ Rajasthan State Industrial Development and Investment

Corporation (RIICO)

■ Office of the Commissioner of Industries

Sources: Government of Rajasthan; RIICO; Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 24

Government initiatives (cont.)

Land availability, identification of investment

zones and infrastructure development

Land availability

■ Land bank available: Land may be acquired or requested for

allotment

■ Conversion of land for industrial use: Revenue Department

and Urban Authorities to be approached for rural and urban

land

■ Land can also be procured from RIICO Industrial areas where

land acquisition in advanced stages: Karoli, Salarpur, Manda,

Prahaladpura, Baggad. Land also on offer at Bandapur, Kolila

Joga, Dhoomera, Haldina, Devnagar and others

Identification of investment zones and bilateral dialogues

■ RIICO has been identifying and developing industrial areas. So

far, 323 industrial areas have been developed

■ International Investment Zones have been identified for

Japanese and South Korean investors. Discussions being

carried with investors from Taiwan, Thailand and Israel

Infrastructure development

■ Second highest network of National Highways and still

developing

■ Three existing airports and plan for four additional airports

■ Several inland container depots at Bhiwadi, Kota, Jaipur and

more

Sources: Government of Rajasthan; Press articles

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 25

■ Power deficit: The state claims to be power surplus by FY14 end

■ Connectivity to hinterland: Few flights operate from the capital city, while

most other cities lack airports. Four new airports to be built by Airports Authority

of India. In addition, road and rail network being constructed

■ Diverse investment opportunities in sectors

■ Proven track record of present companies

■ Access to large market (Population of border

states, Gujarat, Madhya Pradesh, Uttar Pradesh,

Haryana, Punjab is 402 million)

■ Proximity to Country’s capital city

■ Facilitative policies being formed

■ Strong industrial base

■ Abundant mineral resources that lead to huge export

earnings (esp. marble, granite)

■ Land availability is not an issue as land bank is

available

■ Excellent road infrastructure with further scope for

expansion; a metro link underway at Jaipur

■ Presence of 466 higher educational

institutions/polytechnics with intake of 1,21,381

■ Availability of skilled labor backed by almost

negligible strikes, lock-outs etc. Labor cost is 20-30

percent lower Challenges

Sources: Press search

Growth agenda

Annexure

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 27

Special Incentive Package for Ceramic & Glass Sector, 2011

I

III

IV

V Rajasthan Solar Energy Policy, 2011

Rajasthan Investment Promotion Scheme, 2010 (RIPS)

II Rajasthan Industrial and Investment Promotion Policy, 2010 Focused on improving business environment, infrastructure, skills, employment

generation, land availability and supporting MSMEs

Package to be granted for minimum investment of INR500 million

Subsidy to the extent of 75 percent of tax paid

Exemption from electricity duty to power producers for own consumption; solar park

development of more than 100 MW; utility grid power projects for captive use to third party;

land for solar power to be allotted at concession of 10 percent to District Level

Committee rate

Policies and schemes for priority sectors

Sources: Government of Rajasthan; Bureau of Investment Promotion

Rajasthan Textile Policy, 2013

Customized package offered to new/existing units (undergoing modernization/

expansion/diversification upto 31 March 2020

Minimum investment: INR2.5 million

Direct employment: Atleast 10 people; atleast 25 percent in case of expansion/

diversification with minimum cap of 10 people

Interest subsidy at the rate of 5 percent per annum: Additional subsidy at the rate of 1

percent for fixed capital investment of more than INR250 million; Exemption at the rate of

7 percent for textiles

Reimbursement of VAT: Reimbursement of 60 percent on yarn purchase

Exemptions: 100 percent on luxury tax for seven years; 50 percent on electricity duty,

land tax, mandi fee for seven years; 50 percent on stamp duty and land use

conversion charge

Investment subsidy: Upto 50 percent of VAT, GST, CST for seven years

Exemptions: 50 percent on electricity duty, land tax and land use conversion charge

© 2013 KPMG Global Services Private Limited, a company incorporated under the laws of India and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 28

Policy for Promotion of Agro-processing & Agri-business, 2010

IX

VI

IT & ITeS Policy, 2007

VII

Rajasthan Incentive Scheme for BPO Centres & KPO Centres, 2011 VIII

Benefits as per RIPS. In addition, employment incentive at the rate of INR4,000

per employee for 3 years; stamp duty concession for food parks; subsidy on tariffs

for exports

Scheme applicable from issuance date to March 2018; 50 percent subsidy on capital

investment for projects upto INR2 million per BPO/KPO centre

Policies and schemes for priority sectors (cont.)

Source: Government of Rajasthan

Rajasthan Mineral Policy, 2011 Mining lease will be mortgaged in favor of financial institution

Procedures pertaining to transfer of leases, period or transfer of lease simplified

Incentives as per RIPS; VAT at the rate of 4 percent; mega projects and MSMEs to

get special package of incentives; rebate in government land; development of IT

Parks; Mega projects defined as direct employment of 500 in IT and 1,000 in ITeS

The information contained herein is of a general nature and is not intended to

address the circumstances of any particular individual or entity. Although we

endeavor to provide accurate and timely information, there can be no guarantee

that such information is accurate as of the date it is received or that it will continue

to be accurate in the future. The views and opinions expressed herein are those

of the interviewees and do not necessarily represent the views and opinions of

KPMG in India. No one should act on such information without appropriate

professional advice after a thorough examination of the particular situation.

© 2013 KPMG Global Services Private Limited, a company incorporated under

the laws of India and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative, a Swiss entity. All

rights reserved.

The KPMG name, logo and “cutting through complexity” are registered

trademarks or trademarks of KPMG International.