Invest Malaysia 2015 - maybank.com · Invest Malaysia 2015 ... Prime savers ratio rising Potential...

40

0 www.maybank.com Invest Malaysia 2015 Humanising Financial Services Mandarin Oriental, Kuala Lumpur 23 April 2015

Transcript of Invest Malaysia 2015 - maybank.com · Invest Malaysia 2015 ... Prime savers ratio rising Potential...

0www.maybank.com

Invest Malaysia 2015

Humanising Financial Services

Mandarin Oriental, Kuala Lumpur

23 April 2015

1

Invest Malaysia 2015

Financial Performance

Regional Achievements by Business Unit

Outlook and 2015 Strategic Priorities

Shareholder Returns

Maybank’s Future in the ASEAN Economic Community

22

We are guided by our Vision, Mission and Strategic Objectives

Vision

Strategic Objectives

Mission

To be a regional financial services leader

Humanising Financial Services

Community Financial

Services

1. Undisputed No. 1 Retail Financial Services provider in

Malaysia by 2015

2. Leading ASEAN wholesale bank eventually expanding to

Middle East, China & India

3. Undisputed Insurance & Takaful Leader in Malaysia and

Emerging Regional Player

4. Truly regional organisation with approximately 40% of pre-

tax profit derived from international operations by 2015

5. Global leader in Islamic Finance

Global Banking

Insurance and Takaful

International

Islamic Banking

33

Opportunities in the ASEAN Economic Community (1/3)

Favourable Demographics

We are positive about the future of ASEAN with the advent of the ASEAN Economic Community in 2015.

629 million

population

255 m6 m

31 m

69 m

16 m91 m

101 m

7 m

53 m

● 7th largest economy in the world, projected

to be 4th largest by 2030.

● Combined GDP of USD2.3 trillion, third

largest economy straddling China and India

● Average annual GDP growth of around 6%

over the past 15 years.

● More than 600 million people, third largest

in Asia after China and India. Larger than

EU (507 million) and NAFTA (474 million).

Economy

Increased Intra-Regional and China Trade

● Intra-ASEAN trade rose to USD520 billion in

2010 from just USD90 billion in 1993.

● China is ASEAN’s No. 1 trading partner, with

its share rising to 12% in 2011 from 2% in

1993.

● China-ASEAN bilateral trade is expected to

reach US$1 trillion by 2020 from USD500

billion in 2014.

44 4

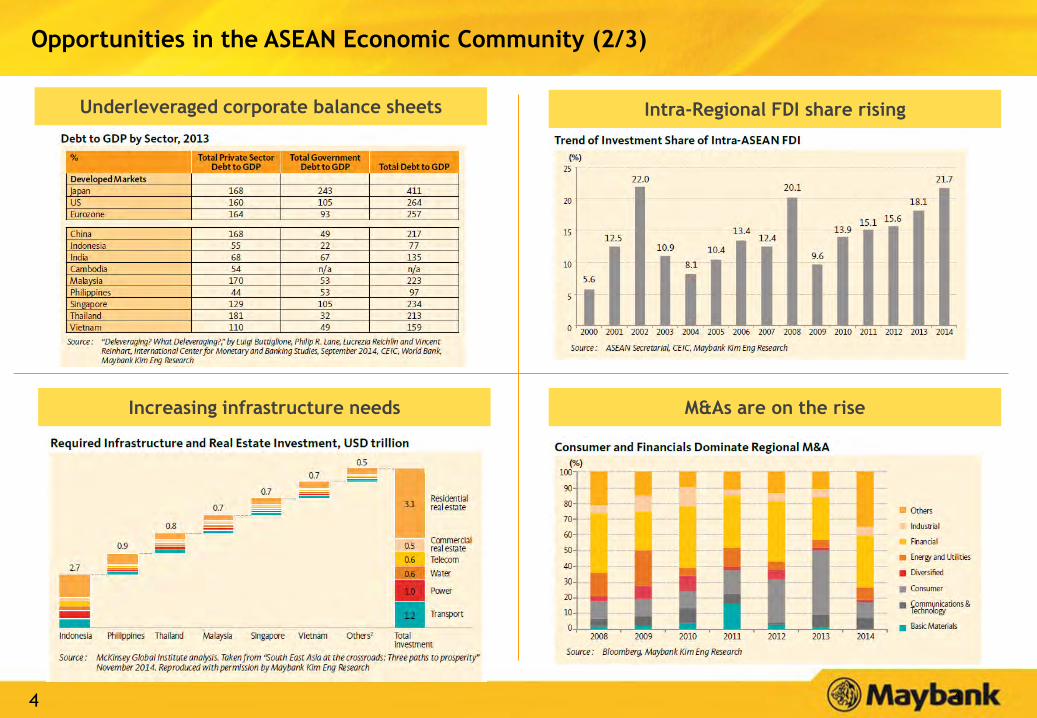

Opportunities in the ASEAN Economic Community (2/3)

Underleveraged corporate balance sheets Intra-Regional FDI share rising

M&As are on the riseIncreasing infrastructure needs

55 5

Opportunities in the ASEAN Economic Community (3/3)

5

Prime savers ratio rising Potential for higher financial inclusion

Significant upside for insurance Islamic banking set to expand

Source: Charts and data for slides 3-5 are from Big Ideas: The Charts of ASEAN,

produced by Maybank Kim Eng Research for the CAP10 ASEAN CEO Summit

6

Expanding ASEAN footprintMaybank is present in all ten ASEAN countries, making it a truly ASEAN franchise

BANK

MARKET

CAP

@

17 Apr 15

(USD Bil)

TOTAL

ASSETS

@

31 Dec 14

(USD Bil)

MALAYSIA

SIN

GAPO

RE

IND

ON

ESIA

TH

AIL

AN

D

PH

ILIP

PIN

ES

BRU

NEI

VIE

TN

AM

CAM

BO

DIA

LAO

S

MYA

NM

AR

1 DBS 39.0 333

2 OCBC 32.2 303

3 UOB 28.7 234

4 BCA 28.3 44

5 Maybank 24.3 183 *

6 Mandiri 21.8 69

7 Public 20.7 99

8 SCB 18.4 82

9 CIMB 14.1 118

10 Bangkok 11.1 84

11 BDO 9.6 42

12 Metrobank 6.9 36

Universal BankingRetail & Commercial

BankingInvestment Banking Affiliate/Representative Office * Wholesale Banking license only

7

44

65

69

82

99

118

183

232

303

333

Bank Central Asia

Bank Rakyat Indonesia

Bank Mandiri

Siam Commercial

Public Bank

CIMB

Maybank

UOB

OCBC

DBS

36.2

50.1

51.2

57.6

79.0

80.6

125.5

176.5

185.3

239.4

28.9

41.9

43.6

54.6

70.0

75.6

116.9

150.5

158.4

210.7

Bank Central Asia

Bank Rakyat Indonesia

Bank Mandiri

Siam Commercial

Public Bank

CIMB

Maybank

UOB

OCBC

DBS

Loans Deposits

950

1,381

1,390

1,642

1,676

2,045

2,053

2,565

3,034

3,194

CIMB

Public Bank

Bank Central Asia

Siam Commercial

Bank Mandiri

Bank Rakyat Indonesia

Maybank

UOB

OCBC

DBS

Strong Financial Position: Top 5 Bank in ASEANMaybank is a Top 5 ASEAN banking group in terms of assets, loans and deposits, and Net Profit

No.4 No.4

No.4

Total Assets (USD bil): 31 Dec 2014 Loans and Deposits (USD bil): 31 Dec 2014

Net Profit (USD mil): CY 31 Dec 2014 Market Capitalisation (USD bil): 17 April 2015

* Due to decline in Ringgit

*

39.0

32.2

28.7

28.3

25.0

24.3

21.8

20.7

18.4

14.1

DBS

OCBC

UOB

Bank Central Asia

Bank Rakyat Indonesia

Maybank

Bank Mandiri

Public Bank

Siam Commercial

CIMB

No.6

8 8

Emerging Regional LeaderPresence in all 10 ASEAN countries

■ No. 1 bank in Malaysia: Conventional and Islamic

■ Top 5 bank in ASEAN

■ No. 103 in The Banker’s Top 1000 World Banks

■ Most Valuable Company on Bursa Malaysia

■ 2,400 branches and offices in 20 countries,

serving more than 22 million customers

■ 1,185 branches in 10 ASEAN countries

■ 5 International Financial Centres

■ 48% owned by PNB and its funds and 13% by EPF

■ Foreign shareholding 21.5%

■ A- credit rating, on par with Malaysia sovereign

Wide Branch Network

Leadership Position

Strong Shareholders and Credit Ratings

99

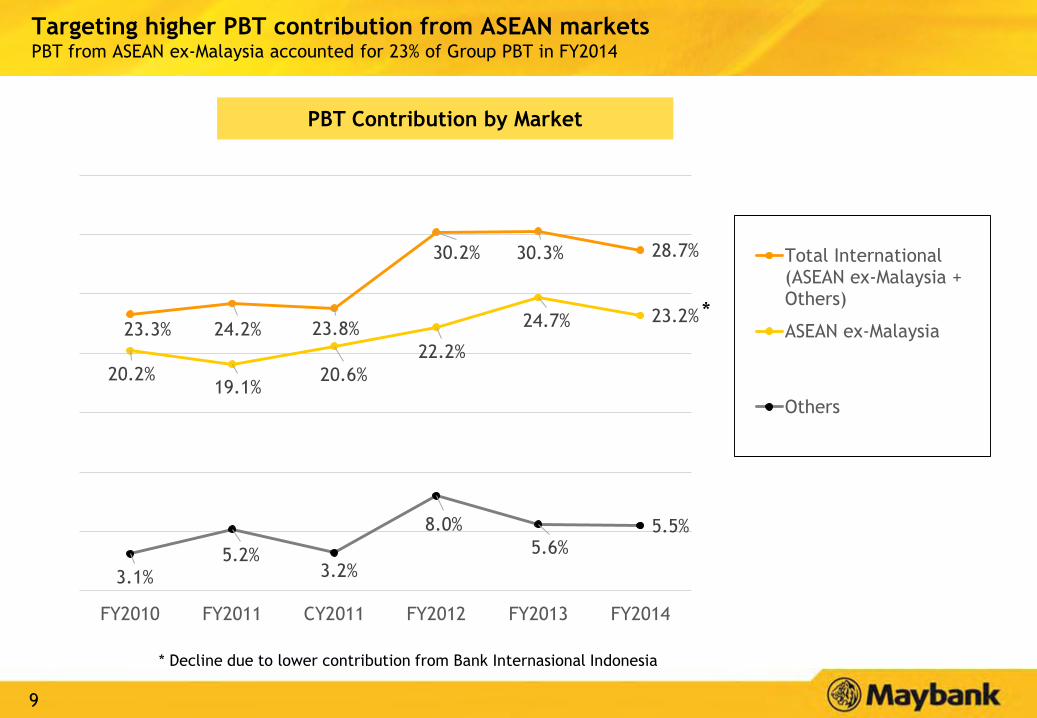

Targeting higher PBT contribution from ASEAN marketsPBT from ASEAN ex-Malaysia accounted for 23% of Group PBT in FY2014

PBT Contribution by Market

23.3% 24.2% 23.8%

30.2% 30.3% 28.7%

20.2%19.1%

20.6%

22.2%

24.7% 23.2%

3.1%

5.2%3.2%

8.0%

5.6%5.5%

FY2010 FY2011 CY2011 FY2012 FY2013 FY2014

Total International(ASEAN ex-Malaysia +Others)

ASEAN ex-Malaysia

Others

*

* Decline due to lower contribution from Bank Internasional Indonesia

10

Maybank’s Business UnitsRegionalisation is driving higher income contribution from international operations

11 11

New organisation structure from 2014

New organisation structure from 1st January 2014 resulted in greater Group synergies and better risk management.

Community Financial Services

Global Banking

Insurance & Takaful

Malaysia

Singapore

Indonesia

InternationalIslamic Banking

12

Invest Malaysia 2015

Financial Performance

Outlook and 2015 Strategic Priorities

Shareholder Returns

Maybank’s Future in the ASEAN Economic Community

Regional Achievements by Business Unit

13

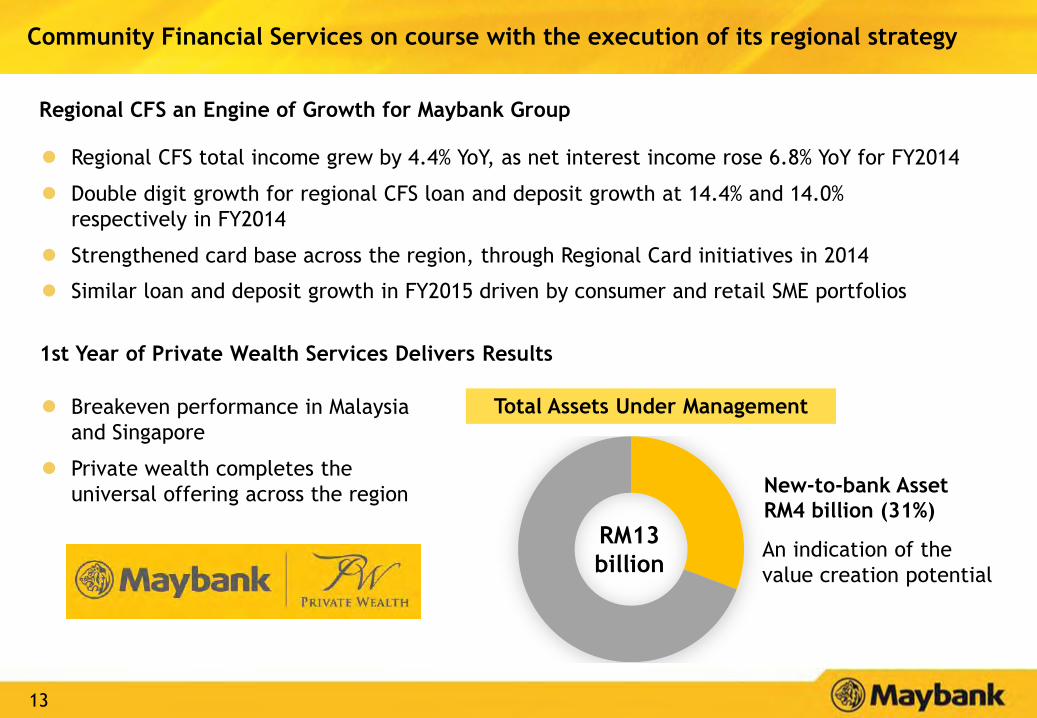

Community Financial Services on course with the execution of its regional strategy

Regional CFS total income grew by 4.4% YoY, as net interest income rose 6.8% YoY for FY2014

Double digit growth for regional CFS loan and deposit growth at 14.4% and 14.0%

respectively in FY2014

Strengthened card base across the region, through Regional Card initiatives in 2014

Similar loan and deposit growth in FY2015 driven by consumer and retail SME portfolios

Regional CFS an Engine of Growth for Maybank Group

1st Year of Private Wealth Services Delivers Results

Breakeven performance in Malaysia

and Singapore

Private wealth completes the

universal offering across the region

RM13

billion

Total Assets Under Management

New-to-bank Asset

RM4 billion (31%)

An indication of the

value creation potential

14

Global Banking strengthened its regional play through multiple product and service offerings

Global Banking key achievements in 2014

Established regional centres of excellence and operating model in

Singapore for Maybank Kim Eng, Global Markets, Transaction Banking

and Asset Management Group

Improved Coverage

Model Across the

Region

Regionalised

Business Models and

Platforms

Established Regional

Centres of

Excellence

Secured 16% more key regional deals or more than 500 new accounts

Received 55 regional awards

Maybank Kim Eng: Maintained position as ASEAN’s largest equities

franchise in 2014

Global Markets: Appointed Renminbi/Singapore dollar Market Maker and

completed first Award Winning Structured Note Issuance

Transaction Banking: Rolled out Maybank 2E Regional Cash in Cambodia,

completing footprint in ASEAN

Asset Management Group: Launched Maybank Global Sukuk fund and

received approval for distribution of two Maybank funds under the

ASEAN collective Investment Scheme

15

879

905

976

1,146

1,508

1,596

1,654

1,693

1,855

1,862

3.5%

3.6%

3.9%

4.6%

6.1%

6.4%

6.6%

6.8%

7.5%

7.5%

Bangkok Bank

HSBC

DBS

RHB Capital

BoA Merrill Lynch

UBS

JPMorgan

Credit Suisse

CIMB

Maybank

2,593

2,965

3,194

3,367

3,594

4,687

4,820

5,734

6,728

8,839

3.8%

4.3%

4.7%

4.9%

5.2%

6.8%

7.0%

8.4%

9.8%

12.9%

Krung Thai Bank

Kasikornbank

Siam Commercial Bank

RHB

AmInvestment

Standard Chartered

DBS

HSBC

Maybank

CIMB

Source: 1Dealogic, 2Bloomberg

Maybank Kim Eng (MKE) among the top investment banks in ASEAN

Equity Brokerage League Table by Country

Country Rank Market ShareTrading Value

(USD m)

Thailand 1 10.6% 67,310

Malaysia 4 9.2% 30,509

Indonesia 7 3.9% 9,782

Philippines 4 6.9% 6,743

Singapore N.A. 5.6% 22,380

Hong Kong Tier2 0.2% 10,479

Equity Capital Markets (USD mil)1

ASEAN Domestic Bonds (USD mil)2

MKE is ASEAN’s largest equity franchise with the

highest trade value in 2014

MKE secured the highest ASEAN ECM deal volume MKE’s PBT increased its contribution to Group’s

PBT from 1.5% in FY2011 to 4.3% in FY2014

MKE’s role in the largest China bond issuance by a

South East Asian issuer solidified its Top 2 position

(RM mil) 2011 2012 2013 2014

Total Income 888.1 1,279.0 1,536.3 1,515.3

Income contribution

to Maybank Group5.5% 6.8% 7.8% 7.4%

PBT 126.4 346.2 461.8 478.8

PBT contribution to

Maybank Group1.5% 3.5% 4.6% 4.3%

Note: Kim Eng was consolidated in May 2011 and PBT Contribution to Maybank Group is

calculated before elimination of Group head office cost

16

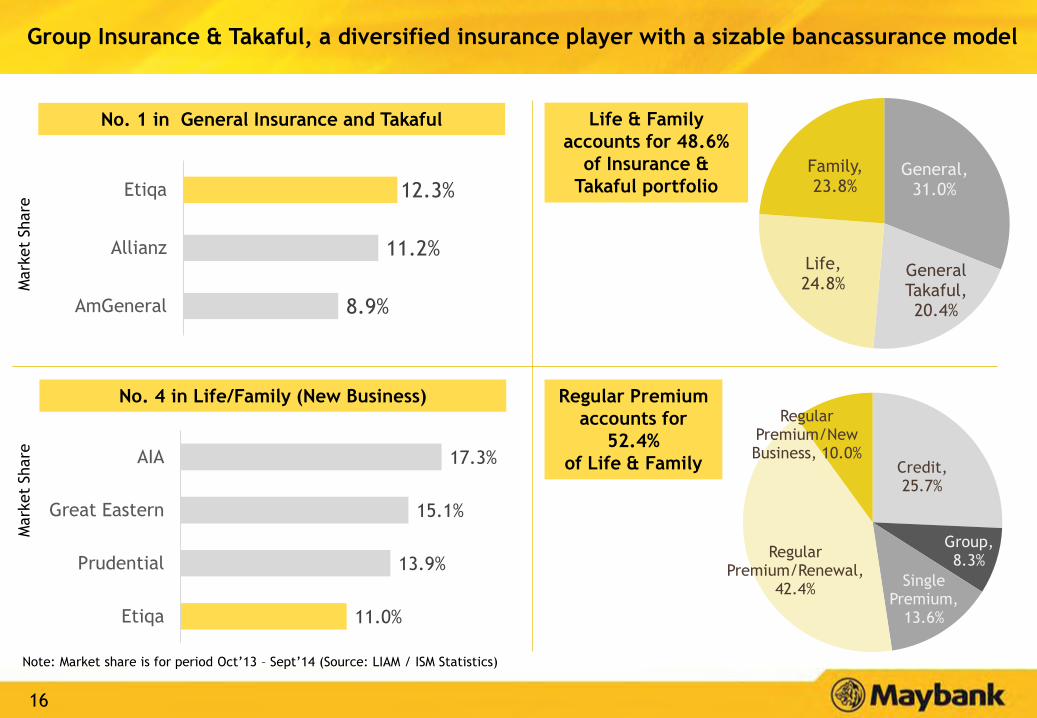

Group Insurance & Takaful, a diversified insurance player with a sizable bancassurance model

No. 1 in General Insurance and Takaful

Note: Market share is for period Oct’13 – Sept’14 (Source: LIAM / ISM Statistics)

8.9%

11.2%

12.3%

AmGeneral

Allianz

Etiqa

Mark

et

Share

Mark

et

Share

No. 4 in Life/Family (New Business)

11.0%

13.9%

15.1%

17.3%

Etiqa

Prudential

Great Eastern

AIA

Life & Family

accounts for 48.6%

of Insurance &

Takaful portfolio

Regular Premium

accounts for

52.4%

of Life & Family

General, 31.0%

General Takaful, 20.4%

Life, 24.8%

Family, 23.8%

Credit, 25.7%

Group, 8.3%

Single Premium,

13.6%

Regular Premium/Renewal,

42.4%

Regular Premium/New Business, 10.0%

17

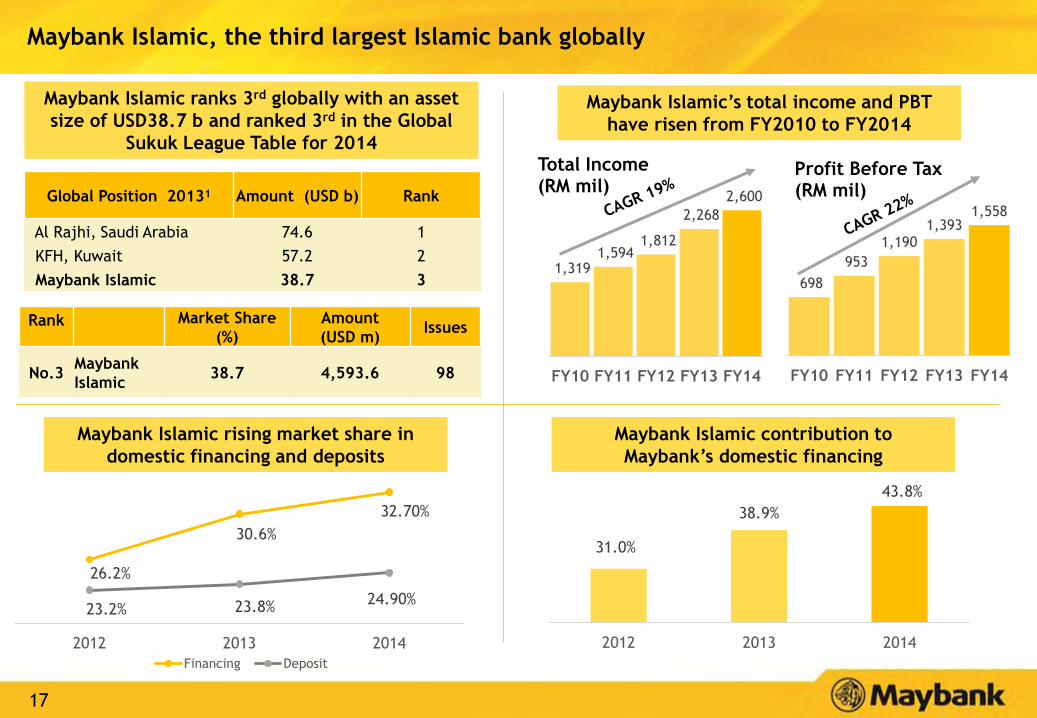

Maybank Islamic, the third largest Islamic bank globally

Source: The Banker November 2014, excludes Iran

26.2%

30.6%

32.70%

23.2% 23.8%24.90%

2012 2013 2014

Financing Deposit

31.0%

38.9%

43.8%

2012 2013 2014

Maybank Islamic ranks 3rd globally with an asset

size of USD38.7 b and ranked 3rd in the Global

Sukuk League Table for 2014

Maybank Islamic contribution to

Maybank’s domestic financing

Maybank Islamic’s total income and PBT

have risen from FY2010 to FY2014

1,319 1,594

1,812

2,268

2,600

FY10 FY11 FY12 FY13 FY14

Total Income (RM mil)

698

953

1,190 1,393

1,558

FY10 FY11 FY12 FY13 FY14

Profit Before Tax (RM mil)

Maybank Islamic rising market share in

domestic financing and deposits

Global Position 20131 Amount (USD b) Rank

Al Rajhi, Saudi Arabia 74.6 1

KFH, Kuwait 57.2 2

Maybank Islamic 38.7 3

Rank Market Share

(%)

Amount

(USD m)Issues

No.3Maybank

Islamic38.7 4,593.6 98

18

Invest Malaysia 2015

Regional Achievements by Business Unit

Outlook and 2015 Strategic Priorities

Shareholder Returns

Maybank’s Future in the ASEAN Economic Community

Financial Performance

19

FY2014 Headline Key Performance IndicatorsMaybank ROE at 13.8%, supported by a stronger performance in the second half of 2014

Notes:

1 Annualised

* Last revised ROE guidance announced on 26 November 2014

# in local currency terms.

Singapore’s industry loan growth average comprises domestic business unit (DBU) loans

FY2014

Guidance

Headline KPI

Return on Equity 13% - 14%* 13.50% 14.60% 13.8% -

Other targets

Group Loans Growth 13% 7.50% 18.70% 13.4% -

• Malaysia 9% - 10% 2.50% 15.20% 9.0% 8.7%

• Singapore # 13% 14.60% 11.20% 13.3% 5.9%

• Indonesia # 16% - 17% 9.00% 1.70% 5.4% 11.4%

• Community Financial Services 15.30% 14.80% 15.6% N.A

• Global Banking -10.60% -35.40% -22.0% N.A

Group Deposits Growth 10% - 12% 5.50% 16.30% 11.1% -

Industry

Average

Acheivement

FY2014Key Performance Indicators 1H FY2014¹ 2H FY2014¹

20 20

Summary Financial Performance for 2014

Increased fund based income through Group loans growth of

13.4% while managing margin compression of 12 bps …

… but lower fee based income due to slower capital market

activity and lower forex profit …

By kept overheads growth under controls through the

Strategic Cost Management Programme, and …

… with significantly lower impairment losses helped by higher

bad debt recovery,…

… we delivered profit to shareholders which was 2.5%

higher than the previous year.

EPS declined due to expanded capital base from DRP.

Net Fund Based Income

RM12.6b, +5.9%

Net Fee Based Income

RM5.9b, -10.7%

Net Income

RM18.5b, 0.0%

Overhead expenses

RM9.1b, +2.1%

Impairment losses

RM0.47b, -46.5%

Profit after Tax and

Minority Interest

RM6.7b, +2.5%

Earnings per Share

74.2 sen, -2.2%

… led to flat net income growth.

2121

2.80

2.70

2.72

2.80

2.56 2.53

2.48

2.43 2.31

FY07 FY08 FY09 FY10 FY11 PF11 FY12 FY13 FY14

42.8

44.4

52.2

46.5

49.2

49.7

48.6 47.8

48.9

FY07 FY08 FY09 FY10 FY11 PF11 FY12 FY13 FY14

86.1

88.0

87.6

86.9

90.2

87.8

89.8 89.9

91.8

FY07 FY08 FY09 FY10 FY11 PF11 FY12 FY13 FY14

17.6

15.2

3.1

14.5 14.5 15.2 16.0

15.1 13.8

FY07 FY08 FY09 FY10 FY11 PF11 FY12 FY13 FY14

Key Operating RatiosMaintained good performance amidst challenging environment

2015 guidance

13.0-14.0

90.0

threshold

2015 guidance

-10 bps (2.21)

2015 guidance

47-48

Return on Equity (%) Net Interest Margin (%)

Loan to Deposit Ratio (%) Cost to Income Ratio (%)

22

Asset QualitySlight uptick in Impaired Loans Ratios but still robust asset quality

82.3%86.9%

105.6% 107.5%

95.6%

3.34%

2.84%

1.78%

1.48% 1.52%

0%

1%

2%

3%

4%

5%

0%

20%

40%

60%

80%

100%

120%

FY11 PF11 FY12 FY13 FY14

Loan Loss Coverage

Group Gross Impaired Loans Ratio

3.93%3.51%

2.00% 1.69% 1.85%

FY11 PF11 FY12 FY13 FY14

0.46% 0.53% 0.42%

0.29%0.23%

FY11 PF11 FY12 FY13 FY14

4.15%

2.29% 2.18% 2.81%3.24%

FY11 PF11 FY12 FY13 FY14

Indonesia (BII Group)

Singapore

Malaysia

Gross Impaired Loans RatioGroup Gross Impaired Loans Ratio

and Loan Loss Coverage Ratio

*

* Inclusive of regulatory reserve is 100.0%

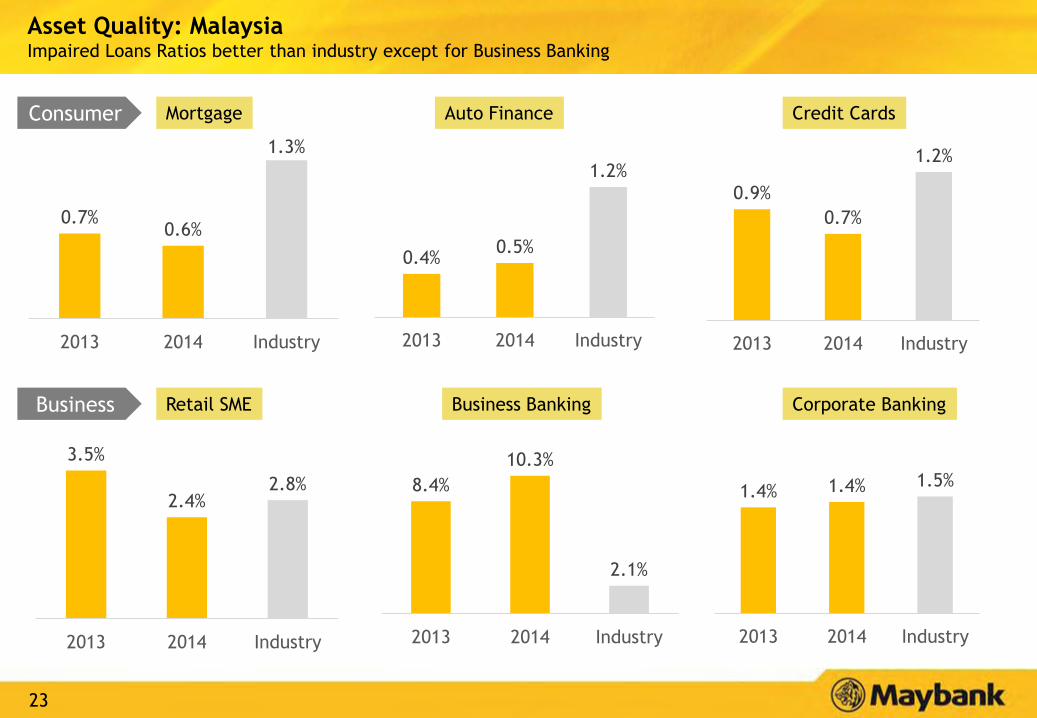

23

0.9%

0.7%

1.2%

2013 2014 Industry

Asset Quality: MalaysiaImpaired Loans Ratios better than industry except for Business Banking

0.7%0.6%

1.3%

2013 2014 Industry

Mortgage

0.4%0.5%

1.2%

2013 2014 Industry

Auto Finance Credit Cards

3.5%

2.4%2.8%

2013 2014 Industry

Retail SME Business Banking Corporate Banking

8.4%

10.3%

2.1%

2013 2014 Industry

1.4% 1.4% 1.5%

2013 2014 Industry

Consumer

Business

2424

Strong Capital Adequacy

11.57%

10.22%11.02% 11.39%

CY 2011 FY 2012 FY 2013 FY 2014

16.29% 15.85% 15.43% 15.88%

CY 2011 FY 2012 FY 2013 FY 2014

Note: The capital ratios for CY 2011 and FY2012 are adjusted for dividend payment and reinvestment made under the Dividend Reinvestment Plan

(DRP) and capital ratios for FY 2013 and FY 2014 are on the assumption of 85% reinvestment rate under the DRP

4%

BNM

Regulatory

Minimum

8%

BNM

Regulatory

Minimum

The Group is well capitalised and will continue to maintain sufficient levels of capital and an

optimum mix of different capital components to ensure sufficient support for the underlying

risks of the Group’s business, to optimise growth and to withstand capital demands under various

market conditions.

Common Equity Tier 1 (CET1) ratio Total Capital ratio

2525

Singapore

… balanced by higher deposits growth of

16.5%, also exceeding industry.

19.6%

9.2%

13.8% 13.4%

Dec 13 Dec 14

Business loans grew 12.3% to S$12.2 billion driven by syndicated, term and revolving

credit.

Consumer loans grew 15.4% to reach S$22.8 billion driven by housing and other personal

loans but car loans continued to decline due to the tighter regulatory financing limits

Expanded our Insurance and Takaful presence in Singapore through Etiqa

13.7%

7.1%8.5%

16.5%

Dec 13 Dec 14

Industry Growth Maybank Singapore Growth

Maybank Singapore loans growth of 13.4%

exceeded industry and …

Loans Growth Deposits Growth

2626

103.7

30.9 35.3 35.8

109.4

24.0

40.8 41.5

Total Global Banking Business Banking Consumer

2013 2014

Indonesia

1,545

699

2013 2014

Bank Internasional Indonesia’s net profit fell 55% to Rp 699 trillion mainly due to higher

loan loss provisions (+126%) for specific corporate accounts affected by adverse market

conditions.

To arrest asset quality deterioration, credit approval procedures were tightened resulting

in Global Banking loans declining 22% but Business Banking and Consumer loans grew

15.5% and 16.0%,

-55% -22.3% +16.0%+5.4% +15.5%

Net Profit (Rp trillion) Loans (Rp trillion)

2727

We secured a banking license in Myanmar and opened a representative

office

Myanmar will enable us to facilitate cross-border trade, not only in our

core markets but also the Greater Mekong Subregion.

International

International PBT contribution (excluding Singapore and Indonesia) increased by

32.8% YoY.

International providing cross-border solutions and capturing trade flow between the

ASEAN region and China

Provides wholesale and investment banking services to commercial

and corporate clients in Hong Kong and China.

Opened our latest China branch in Kunming, Yunnan.

Landmark achievement: Appointment of Maybank as a

Renminbi/Singapore dollar Market MakerGreater

China

Myanmar

2828

Invest Malaysia 2015

Financial Performance

Regional Achievements by Business Unit

Outlook and 2015 Strategic Priorities

Maybank’s Future in the ASEAN Economic Community

Shareholder Returns

2929

0.69

3.824.45

2.58

5.756.55 6.72

2.67#

FY 2009* FY 2010 FY 2011 6 months FP2011 ^ FY 2012 FY 2013 FY 2014

Net Profit

3.1%

14.5% 15.2%16.2% 16.0%

15.1%13.8%

ROE (%)

RM 6 billion

Rights Issue

Launched

House of

Maybank

Acquired

Kim Eng

RM 3.66 billion

Equity Private

Placement

Delivering on Shareholder Return Maybank has seen a steady rise in earnings as we stayed focused on our regional strategy and business growth

Summary of Analysts' Recommendations

as at 27 Feb 2015

Target Price RM10.15

Coverage 25 analysts

Recommendations 15 Buy, 7 Hold, 3 Sell

Analysts'

Consensus:

Net Profit

(RM mil)

FY2014 6,517

FY2015 6,916

* FY2009: Lower net profit due to impairment of investment in BII and MCB

# RM2.67 billion: FY2009 PATAMI before impairment of investment in BII and MCB

^ 6 months Financial Period ended 31 Dec 2011 due change in financial year end

FY2014 PATAMI of RM6.72

billion was 3.1% ahead of

consensus

3030

6.01

5.29 5.24

7.07

5.38

5.84

-

1

2

3

4

5

6

7

8

2009 2010 2011 2012 2013 2014

Maybank Public Bank CIMB DBS UOB OCBC Mandiri BCA Bank Rakyat Siam Comm Kasikorn Bank Bangkok Bank

Maybank provides superior dividend yield amongst most regional banks

Annual Dividend Yield 2009-2014

Source: Bloomberg

(%)

3131

High Dividend PayoutGross dividend for 2014 at 57 sen, 6.5% higher than the previous year

60.0% 61.0%

76.5% 74.9% 79.9% 74.7% 71.9%78.5%

26

11

28 3222.5 24

18

8

44

32

36

33

3133

FY08** FY09 FY10 FY11 FP11 FY12 FY13 FY14

Final

Interim

● Dividend payout ratio for 2014 at 78.5% continues to be above policy rate of 40% - 60%

* Reinvestment rate for the Dividend Reinvestment Plan

** Adjusted for 1:4 Bonus Issue in February 2008 and 9:20 Rights Issue at RM2.74 in March 2009

# The Net Dividend is 28.5 sen of which 15 sen is single-tier dividend.

85.9%*

85.7%*

88.2%* 85.9%*88.5%*

91.1%*

86.1%*

88.6%*

#

N.A.*

44.0

8.0

55.0

60.0

36.0

65.0

53.557.0

84.0%*

Dividend

Payout Ratio

Gross Dividend (sen) and Payout Ratio (%)

3232

Invest Malaysia 2015

Financial Performance

Regional Achievements by Business Unit

Shareholder Returns

Maybank’s future in the ASEAN Economic Community

Outlook and 2015 Strategic Priorities

33

Key Indicators

Malaysia

Consumer lending expected to moderate

Top line for banks to be challenging with

subdued capital markets and soft loan

demand

Competition for deposits to remain keen

amid on-going liquidity pressure

Cost and capital management will remain

key priorities

Market Outlook for 2015

GDP (f): 4.5% (2014: 6%)

System loan growth (f): 7-8%

System deposit growth: (f) 6-7%

OPR: 3.25% (2014: 3.25%)

USD/MYR (f): 3.61 (2014: 3.27)

Inflation (f): 4.0% (2014: 3.2%)

Outlook

34

Key Indicators

Singapore

Government expected to maintain

property cooling measures to prevent

speculative activity

Asset quality to remain stable

Market Outlook for 2015

GDP (f): 2.5% (2014: 2.9%)

System Loan growth (f): 8%-9%

System Deposit growth (f): 5%-6%

USD/SGD (f): 1.35 (2014: 1.28)

Inflation (f): 1.0% (2014: 1.0%)

Outlook

35

Key Indicators

Indonesia

Government infrastructure spending likely

to increase, supporting loan growth in 2H

FY2015

Funding to remain tight, leading to margin

pressure as LDR remains elevated

Weaker commodity prices could adversely

impact asset quality and domestic demand

Market Outlook for 2015

GDP (f): 5.5% (2014: 5.02%)

System Loan growth (f): 15%

System Deposit growth (f): 15%

Reference Rate (f): 8.0%

(2014: 7.75%)

USD/IDR average (f): 12514 (2014:

11885)

Inflation average (f): 7.25% (2014:

6.42%)

Outlook

3636 36

Revenue generation

Strengthen the Group’s revenue growth

Continue with international market performance

Solidify our position in ASEAN for AEC opportunities

e.g. Qualified ASEAN bank

Productivity and Efficiency

Continue focus on productivity Group-wide

Deploy capital efficient strategy

Group Strategic Priorities for 2015

3737

Focus on productivity Group-wide

Continue with Strategic Cost Management Programme to manage our

overheads growth in a comfortable range against income growth

Focus on IT expenses, marketing expenses and general and administrative

expenses.

Drive productivity improvements, measured by profitability over cost ratio

per employee.

Capital efficient strategy

Drive more productive use of capital over the medium to longer term since

additional capital buffer requirements will be introduced for domestic

systemically important banks.

Adopt right risk posture to balance our capital needs and provide an

optimum return for our shareholders.

Productivity and Efficiency

3838

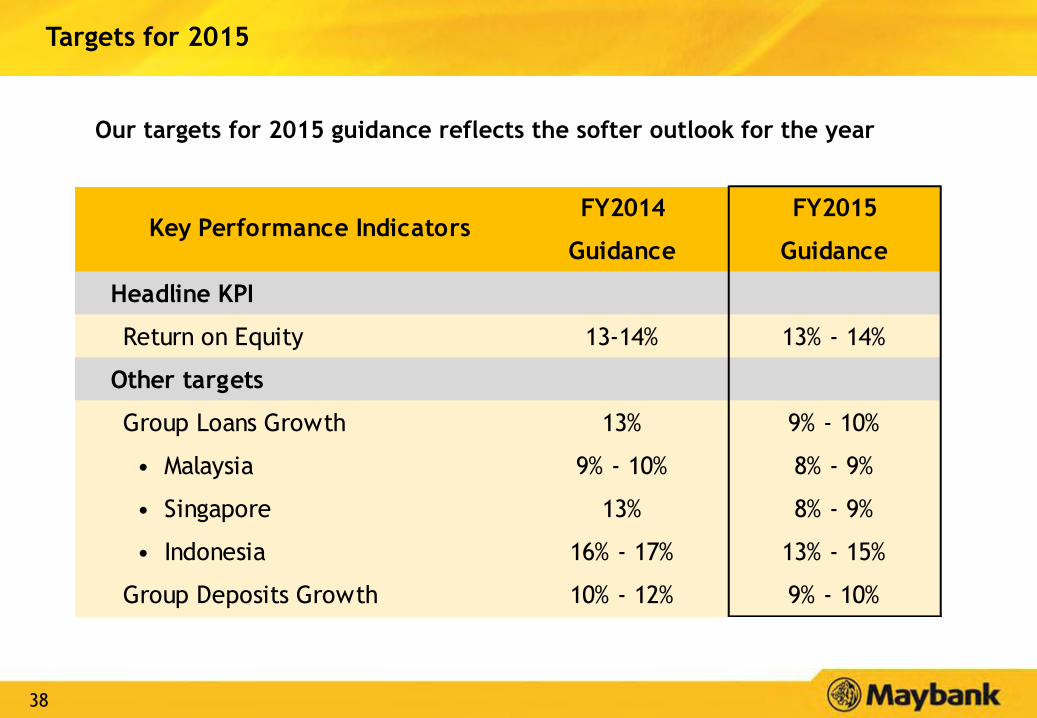

Targets for 2015

Our targets for 2015 guidance reflects the softer outlook for the year

FY2014 FY2015

Guidance Guidance

Headline KPI

Return on Equity 13-14% 13% - 14%

Other targets

Group Loans Growth 13% 9% - 10%

• Malaysia 9% - 10% 8% - 9%

• Singapore 13% 8% - 9%

• Indonesia 16% - 17% 13% - 15%

Group Deposits Growth 10% - 12% 9% - 10%

Key Performance Indicators

39

Mohamed Rafique Merican

Group Chief Financial Officer

Contact: (6)03-2074 7878

Email: [email protected]

MALAYAN BANKING BERHAD

14th Floor, Menara Maybank

100, Jalan Tun Perak

50050 Kuala Lumpur, Malaysia

Tel : (6)03-2070 8833

www.maybank.com

Narita Naziree

Head, Group Performance Reporting& Investor Relations

Contact: (6)03-2074 8017

Email: [email protected]

Disclaimer. This presentation has been prepared by Malayan Banking Berhad (the “Company”) for information purposes only and does not purport to contain all the

information that may be required to evaluate the Company or its financial position. No representation or warranty, express or implied, is given by or on behalf of the

Company as to the accuracy or completeness of the information or opinions contained in this presentation.

The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of

it form the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever.

The Company does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in

connection therewith.

Investor Relations Contact

Humanising Financial Services