Introduction to Micro Finance

46

A Project Study Report On MICRIFINANCE TRENDS & FUTURE IN INDIA Submitted in partial fulfilment for the award of degree of Bachelor of Business Administration University of Rajasthan SUBMITTED TO: SUBMITTED BY: University of Rajasthan Anuj Jangid BBA 4 th Sem. Enroll.No. : 13/961 Page | 1

-

Upload

rahulsogani123 -

Category

Documents

-

view

229 -

download

1

description

report on micro finance

Transcript of Introduction to Micro Finance

AProject Study Report

On

MICRIFINANCE TRENDS & FUTURE IN INDIA

Submitted in partial fulfilment for the award of degree of

Bachelor of Business Administration

University of Rajasthan

SUBMITTED TO: SUBMITTED BY:

University of Rajasthan Anuj JangidBBA 4th Sem.Enroll.No. : 13/961

Apex Institute of Management and Science, Jaipur(Approved by AICTE, New Delhi & Affiliated to University of Rajasthan, Jaipur)

(2013-2016)

Page | 1

DECLARATION

I hereby declare that the Project entitled BRAND EXTENTION AND REPOSITIONING

submitted in University of Rajasthan in partial fulfillment for the award of the

Degree of BACHLOR OF BUSINESS ADMINISTRATION under the guidance of

Ms.Sonal Udeshi AIMS is my original material collected by myself. The project has not

previously formed the basis of the award of any other degree , diploma, associate ship,

Fellowship Or other title

Place: Jaipur Anuj Jangid

Date:

Page | 2

ACKNOWLEDGEMENT

I express my gratitude to the APEX INSTITUE for giving me the opportunity to work on the project during our fourth semester of our graduation degree . There are many who helped me during the project work , and I want to thank them all . My special thanks to Mrs.Sonal udeshi for their invalueable guidance throughout my project work and endeavor period has provided me the requisite motivation to complete my project work successfully. I specially appreciate the help and guidance of all those teachers who have directly or indirectly helped me making my project a success.

I would like to thank DR. Joytsana Khandelwal ( Deans AIMS ) Jaipur whose constant guidance and support has led me to complete the project.

Page | 3

Executive Summary

“True Learning Is Born Out Of Experiences And Observations.”

Theoretical Study Gives Us The Conceptual Clarity While Practical Study States About It And How It Can Be Performed In Real Life. Theoretical Study Does Give Us The Knowledge About Marketing, But Without The Practical Exposure One Cannot Be Total In The Same Field.

In The Competitive Economy The Quality And The Performance Of The Management Determines The Success Of The Organization. However The Art And Practice Of Management Is Quite Different Environment. I Got The Chance To Learn The Various Aspects Of The World Outside Book That Is So Wide And Expanded. As We Go Deeper Into, We Find More And More Of It.

The Main Objective Of The Project Is To Develop Knowledge About Succession Planning And Its Implementation In Business Organizations.

Page | 4

PREFACE

These projects are necessary part for the fulfilment of BBA Degree course. It helps the

students to gain knowledge about various practical aspects of the Industry or Organization.

In fact, it is the implementation of theory in practice, which is life force of management.I had

privileged of implementing the theory in practice during my project.This project exposed me

to a number of function and activities, which helped me in getting a practical touch of

knowledge.

The main objective of this project is to learn about the concept of “MICROFINANCE

TRENDS & FUTURE IN INDIA”, and to get the knowledge of change management and

this study helped in providing change management information that can be beneficial both

personally and professionally.

Page | 5

INTRODUCTION TO MICRO FINANCE

“Microfinance is the provision of financial services to low-income clients or

solidarity lending groups including consumers and the self-employed, who

traditionally lack access to banking and related services.”

Microfinance is not just about giving micro credit to the poor rather it is an

economic development tool whose objective is to assist poor to work their way out

of poverty. It covers a wide range of services like credit, savings, insurance,

remittance and also non-financial services like training, counselling etc.

Salient features of Microfinance:

Borrowers are from the low income group

Loans are of small amount – micro loans

Short duration loans

Loans are offered without collaterals

High frequency of repayment

Loans are generally taken for income generation purpose

Gaps in Financial system and Need for Microfinance

Microfinance is a source of financial services for entrepreneurs and small businesses

lacking access to banking and related services. The two main mechanisms for the

delivery of financial services to such clients are:

(1) relationship-based banking for individual entrepreneurs and small businesses;

and

(2) group-based models, where several entrepreneurs come together to apply for

loans and other services as a group.

In some regions, for example Southern Africa, microfinance is used to describe the

supply of financial services to low-income employees, which is closer to the retail

finance model prevalent in mainstream banking.

Page | 6

For some, microfinance is a movement whose object is "a world in which as many

poor and near-poor households as possible have permanent access to an appropriate

range of high quality financial services, including not just credit but also savings,

insurance, and fund transfers." Many of those who promote microfinance generally

believe that such access will help poor people out of poverty, including participants

in the Microcredit Summit Campaign. For others, microfinance is a way to promote

economic development, employment and growth through the support of micro-

entrepreneurs and small businesses.

Microfinance is a broad category of services, which includes microcredit.

Microcredit is provision of credit services to poor clients. Microcredit is one of the

aspects of microfinance and the two are often confused. Critics may attack

microcredit while referring to it indiscriminately as either 'microcredit' or

'microfinance'. Due to the broad range of microfinance services, it is difficult to

assess impact, and very few studies have tried to assess its full impact. Proponents

often claim that microfinance lifts people out of poverty, but the evidence is mixed.

What it does do, however, is to enhance financial inclusion.

Microfinance and poverty

Financial needs and financial services

In developing economies and particularly in rural areas, many activities that would

be classified in the developed world as financial are not monetized: that is, money is

not used to carry them out. This is often the case when people need the services

money can provide but do not have dispensable funds required for those services,

forcing them to revert to other means of acquiring them. In their book The Poor and

Their Money, Stuart Rutherford and Sukhwinder Arora cite several types of needs:

Lifecycle Needs: such as weddings, funerals, childbirth, education,

homebuilding, widowhood and old age.

Personal Emergencies: such as sickness, injury, unemployment, theft,

harassment or death.

Page | 7

Disasters: such as fires, floods, cyclones and man-made events like war or

bulldozing of dwellings.

Investment Opportunities: expanding a business, buying land or equipment,

improving housing, securing a job (which often requires paying a large

bribe), etc.

People find creative and often collaborative ways to meet these needs, primarily

through creating and exchanging different forms of non-cash value. Common

substitutes for cash vary from country to country but typically include livestock,

grains, jewellery and precious metals. As Marguerite Robinson describes in The

Microfinance Revolution, the 1980s demonstrated that "microfinance could provide

large-scale outreach profitably," and in the 1990s, "microfinance began to develop

as an industry".

In the 2000s, the microfinance industry's objective is to satisfy the unmet demand on

a much larger scale, and to play a role in reducing poverty. While much progress has

been made in developing a viable, commercial microfinance sector in the last few

decades, several issues remain that need to be addressed before the industry will be

able to satisfy massive worldwide demand.

The obstacles or challenges to building a sound commercial microfinance industry

include:

Inappropriate donor subsidies

Poor regulation and supervision of deposit-taking MFIs

Few MFIs that meet the needs for savings, remittances or insurance

Limited management capacity in MFIs

Institutional inefficiencies

Need for more dissemination and adoption of rural, agricultural microfinance

methodologies

Page | 8

A BRIEF ABOUT MFIs

Micro Finance Institutions (MFIs)

Those institutions which have microfinance as their main operation are known as micro

finance institutions. A number of organizations with varied size and legal forms offer

microfinance service. These institutions lend through the concept of Joint Liability

Group (JLG). A JLG is an informal group comprising of 5 to 10 individual members

who come together for the purpose of availing bank loans either individually or through

the group mechanism against a mutual guarantee. The reason for existence of separate

institutions i.e. MFIs for offering microfinance are as follows:

High transaction cost – generally micro credits fall below the break-even

point of providing loans by banks

Absence of collaterals – the poor usually are not in a state to offer collaterals

to secure the credit

Loans are generally taken for very short duration periods

Higher frequency of repayment of installments and higher rate of Default

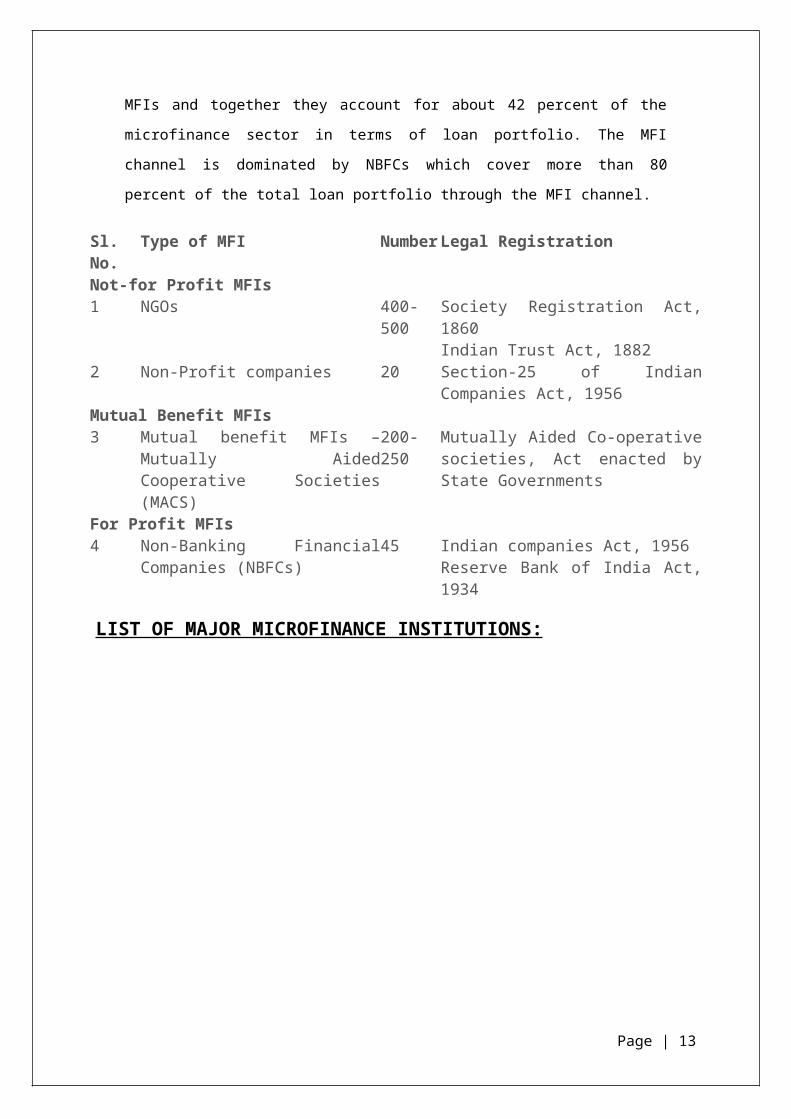

Non-Banking Financial Companies (NBFCs), Co-operative societies, Section-25 companies,

Societies and Trusts, all such institutions operating in microfinance sector constitute MFIs

and together they account for about 42 percent of the microfinance sector in terms of loan

portfolio. The MFI channel is dominated by NBFCs which cover more than 80 percent of

the total loan portfolio through the MFI channel.

Sl. No. Type of MFI Number Legal RegistrationNot-for Profit MFIs1 NGOs 400-500 Society Registration Act, 1860

Indian Trust Act, 18822 Non-Profit companies 20 Section-25 of Indian Companies Act,

1956Mutual Benefit MFIs3 Mutual benefit MFIs – Mutually

Aided Cooperative Societies (MACS)

200-250 Mutually Aided Co-operative societies, Act enacted by State Governments

For Profit MFIs4 Non-Banking Financial Companies

(NBFCs)45 Indian companies Act, 1956

Reserve Bank of India Act, 1934

Page | 9

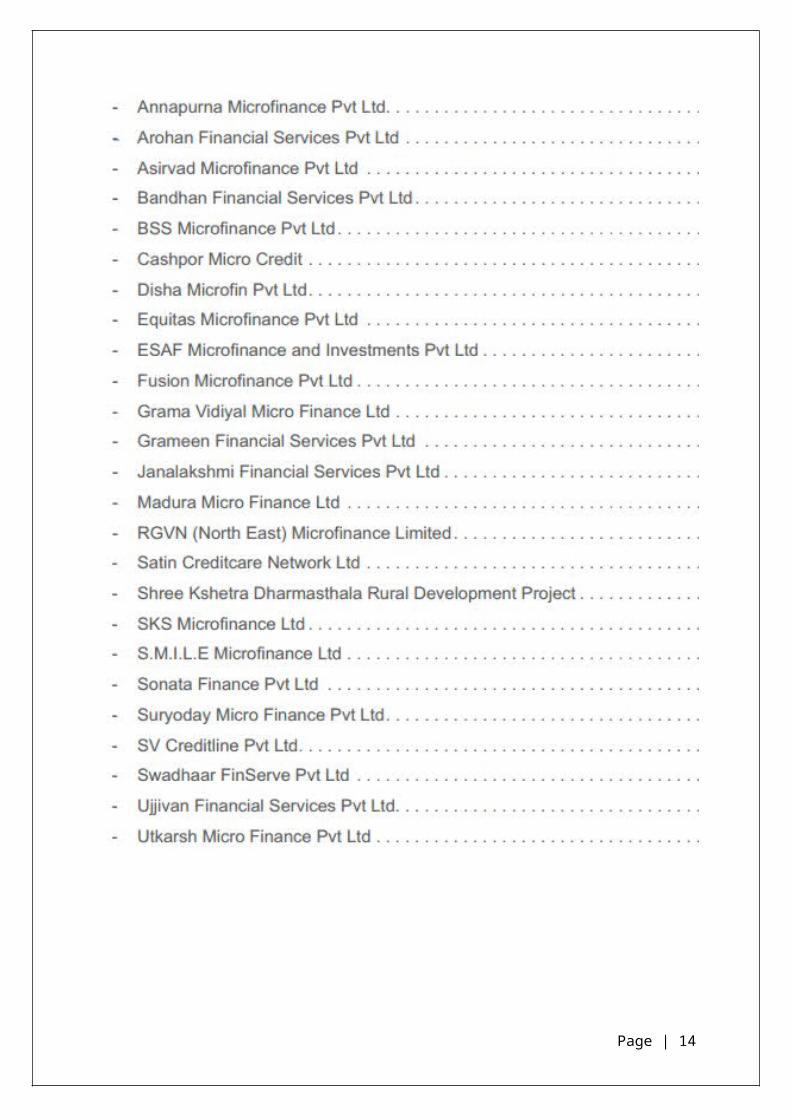

LIST OF MAJOR MICROFINANCE INSTITUTIONS:

Page | 10

MAJOR SCHEMES OFFERED BY MFIs:

1. GIDKA (Group Insurance Scheme for Khadi Artisan)With a view to provide safe

and secured life to Khadi Artisan a Group Insurance Scheme forKhadi Artisans has

been introduced. The Scheme covers all the spinners, weavers, pre-spinning artisans

and postweaving artisans engaged in Khadi activity, associated with

KhadiInstitutions (NGO‟s) throughout the Country.

2. DRDA (The District Rural Development Agency)The district Rural Development

Agency is visualized as specialized and professional agency capable of managing

the antipoverty Programmes of the Ministry of Rural Development onthe one hand

and to effectively relate these to the overall effort of poverty eradication in the

district.

3. NIRD (National Institute of Rural Development) National Institute of Rural

Development (NIRD) facilitates rural development through government and non-

governmental initiatives. NIRD is the country’s apex body for undertaking training,

research, action and consultancy functions in the rural development sector. It works

as an autonomous organization supported by the Ministry of Rural Development,

Government of India.

4. NRRDA (National Rural Road Development) Construction of rural roads brings

multifaceted benefits to the hitherto deprived rural areas and also an effective

poverty reduction strategy. Pradhan Mantri Gram SadakYojana Awareness of

Schemes and Services of Micro Finance Institutes (PMGSY) were taken up by the

Government of India with an objective to provide connectivity to the unconnected

Habitations in the rural areas.

5. CAPART (Council for Advancement of people’s Action and Rural Technology)

Council for Advancement of People’s Action and Rural Technology (CAPART) is

an autonomous body registered under the Societies Registration Act, 1860 and is

functioning under the aegis of the Ministry of Rural Development. CAPART is

involved in catalyzing and coordinating the emerging partnership between

Page | 11

Voluntary Organizations and the Government of India for sustainable development

of Rural Areas.

DRAWBACKS OF MICRO FINANCE

Ills of Micro Finance:

Financial illiteracy

One of the major hindrances in the growth of the microfinance sector is the financial

illiteracy of the people. This makes it difficult in creating awareness of microfinance

and even more difficult to serve them as microfinance clients. Though most of the

microfinance institutions claim to have educational trainings and programmes for

the benefit of the people, according to some of the experts the first thing these SHG

and JLG members are taught is to do their own signature.

The worst part is that many MFIs think that this is what financial literacy means. We

all know how dangerous it can be when one doesn’t know how to read but he/she

knows how to accept or approve it (by signing it).

Inability to generate sufficient funds

Inability of MFIs to raise sufficient fund remains one of the important concern in the

microfinance sector. Though NBFCs are able to raise funds through private equity

investments because of the for-profit motive, such MFIs are restricted from taking

public deposits. Not-for-profit companies which constitute a major chunk of the MFI

sector have to primarily rely on donations and grants from Government and apex

institutions like NABARD and SIDBI.

In absence of adequate funding from the equity market, the major source of funds

for MFIs are the bank loans, which is the reason for high Debt to Equity ratio of

most MFIs. MFIs receive debt from banks against their equity and in order to

increase their portfolio size they need to increase their debts for which they further

need to increase their equity. After the Andhra crisis, it is reported that banks have

stopped issuing fresh loans and even though currently few banks have resumed, they

want MFIs to increase their equity to get fresh loans. So the only mode for the MFIs

to increase their portfolio size is to increase their equity.

Page | 12

Dropouts and Migration of group members

Majority of the microfinance loans are disbursed on group lending concept and a

past record of the group plays an important role in getting new loans either through

SHG-Bank linkage or through MFIs. The two major problems with the group

concept are dropouts (when one or more members leave the group) and migration

(when one or more members move to another group). Most MFIs lend on the basis

of the past record of the group i.e. SHG or JLG and also on the individuals

repayment performance. In absence of a decent past record, members are deprived

of getting bigger loan amounts and additional services.

Transparent Pricing

Though the concern about the transparent pricing in the microfinance sector has

been an older one, it is gaining significance with the growing size and the increasing

competition in the sector. Non-transparent pricing by MFIs confines the bargaining

power of the borrowers and their ability to compare different loan products, because

they don’t know the actual price. In absence of the proper understanding of the

pricing, clients end up borrowing more than their ability to payback which results in

over-indebtedness of the borrower. Ambiguity in the pricing by MFIs is inviting

regulatory bodies to implement strict measures like interest rate caps. But simply

putting an interest rate cap may encourage MFIs to look for clients with larger loan

requirements. This may deprive the clients with smaller loan requirements who are

supposed to be the actual beneficiary of microfinance.

Cluster formation – fight to grab established market

MFIs’ drive to grab an established market and reduce their costs is resulting in

formation of clusters in some areas leaving the others out of the microfinance

outreach. By getting an established microfinance market, MFIs reduce their initial

cost in group formation of clients, educating them and creating awareness about

microfinance. This is one of the reasons for the dominance of the microfinance

sector in the southern states. Now the problem is that a similar trend is being

Page | 13

followed in the northern states as well. We have already seen what happened in A.P

and it seems that most of the MFIs have not taken a lesson from the Andhra crisis.

Multiple Lending and Over-Indebtedness

Both of these are outcome of the competition among the MFIs. Microfinance is one

such sector where the Neo-liberal theory of free market operation fails, at least to

some extent. Though competition is good for many sectors but in this case it is going

against both the parties. In order to eat away each other’s’ market share, MFIs are

ending up giving multiple loans to same borrowers which in some cases is leading to

over-indebtedness (a situation where the borrower has taken loans more than her/his

repaying capacity) of the borrower. MFIs are getting affected because borrowers are

failing to make payments and hence their recovery rates are falling, while over-

indebtedness is making the borrower go to depression and in some cases forcing

them to commit suicide.

Page | 14

SCOPE AND TRENDS IN INDIA

Microfinance sector has grown rapidly over the past few decades. Nobel Laureate

Muhammad Yunus is credited with laying the foundation of the modern MFIs with

establishment of Grameen Bank, Bangladesh in 1976. Today it has evolved into a

vibrant industry exhibiting a variety of business models. Microfinance Institutions

(MFIs) in India exist as NGOs (registered as societies or trusts), Section 25

companies and Non-Banking Financial Companies (NBFCs). Commercial Banks,

Regional Rural Banks (RRBs), cooperative societies and other large lenders have

played an important role in providing refinance facility to MFIs. Banks have also

leveraged the Self-Help Group (SHGs) channel to provide direct credit to group

borrowers.

With financial inclusion emerging as a major policy objective in the country,

Microfinance has occupied centre stage as a promising conduit for extending

financial services to unbanked sections of population. At the same time, practices

followed by certain lenders have subjected the sector to greater scrutiny and need for

stricter regulation.

This report, which contains only a part of the actual report is based on the research

work done as a part of the summer internship project at Reserve Bank of India,

Kanpur. The research involved study of the past literatures about the microfinance

sector, related online research papers and journals. The study also involved survey

of all MFIs in the state of Uttar Pradesh through field visits and online survey. The

annual reports and the sector reports published by regulatory bodies, MFI

associations and major microfinance players facilitated the study, especially in

understanding the size, growth and past trends. Interactions with some of the

industry experts helped in understanding and analysing the emerging concerns in the

microfinance sector and also to look for some possible solutions.

Although the microfinance sector is having a healthy growth rate, there have been a

number of concerns related to the sector, like grey areas in regulation, transparent

pricing, low financial literacy etc.

Page | 15

On a national level there has been a spate of actions taken to strengthen the

regulation of MF sector including, enactment of microfinance regulation bill by the

Government of Andhra Pradesh, implementation of sector-specific regulation by

Reserve Bank of India and most recently, release of Draft Microfinance Institutions

(development and regulation) Bill, 2014 for comments.

Based on the research work, a few major recommendations made in the report

include field supervision of MFIs to check ground realities and the operational

efficiency of such institutions. Offer incentives to MFIs for opening branches in

unbanked villages, so as to increase rural penetration. Also MFIs be encouraged to

offer complete range of products to their clients. Transparent pricing and technology

implementation to maintain uniformity and efficiency are among the others which

these institutions should adopt. Inability of MFIs in getting sufficient funds is a

major hindrance in the microfinance growth and so these institutions should look for

alternative sources of funds. Some of the alternative fund sources include outside

equity investment, portfolio buyouts and securitization of loans which only a few

large MFIs are currently availing.

According to the latest research done by the World Bank, India is home to almost

one third of the world’s poor (surviving on an equivalent of one dollar a day).

Though many central government and state government poverty alleviation

programs are currently active in India, microfinance plays a major contributor to

financial inclusion. In the past few decades it has helped out remarkably in

eradicating poverty. Reports show that people who have taken microfinance have

been able to increase their income and hence the standard of living.

About half of the Indian population still doesn’t have a savings bank account and

they are deprived of all banking services. Poor also need financial services to fulfill

their needs like consumption, building of assets and protection against risk.

Microfinance institutions serve as a supplement to banks and in some sense a better

one too. These institutions not only offer micro credit but they also provide other

financial services like savings, insurance, remittance and non-financial services like

individual counselling, training and support to start own business and the most

importantly in a convenient way. The borrower receives all these services at her/his

door step and in most cases with a repayment schedule of borrower’s convenience.

Page | 16

But all this comes at a cost and the interest rates charged by these institutions are

higher than commercial banks and vary widely from 10 to 30 percent. Some claim

that the interest rates charged by some of these institutions are very high while

others feel that considering the cost of capital and the cost incurred in giving the

service, the high interest rates are justified

Channels of Micro finance

In India microfinance operates through two channels:

1. SHG – Bank Linkage Programme (SBLP)

2. Micro Finance Institutions (MFIs)

SHG – Bank Linkage Programme

This is the bank-led microfinance channel which was initiated by NABARD in

1992. Under the SHG model the members, usually women in villages are

encouraged to form groups of around 10-15. The members contribute their savings

in the group periodically and from these savings small loans are provided to the

members. In the later period these SHGs are provided with bank loans generally for

income generation purpose. The group’s members meet periodically when the new

savings come in, recovery of past loans are made from the members and also new

loans are disbursed. This model has been very much successful in the past and with

time it is becoming more popular. The SHGs are self-sustaining and once the group

becomes stable it starts working on its own with some support from NGOs

SHG model – How it works and institutions like NABARD and SIDBI.

Legal structure and regulation

Although the SHG-Bank linkage model is well managed in India by NABARD, currently

there is no proper regulatory body for the supervision of MFIs. The presence of

institutions with a variety of legal forms makes it difficult for the regulation of all such

institutions by a single regulatory body in the current Indian legal structure. Though

NBFCs, which cover the major part of the outstanding loan portfolio by the microfinance

channel, are regulated by Reserve Bank of India, other MFIs like societies, trusts,

Page | 17

Section-25 companies and cooperative societies fall outside the purview of RBI’s

regulation. The acceptance of the Malegam committee recommendations by the RBI is a

big step forward in addressing the above concern but again it will cover only a section of

the MFIs i.e. NBFCs. The microfinance bill which was introduced in the year 2007 is

still pending. The most recent and the strongest step taken by the government, The Micro

Finance Institutions (Development and regulation) Bill, 2014 is a major step in the

microfinance sector. The proposed bill clarifies all doubts pertaining to regulation of the

MFIs by appointing RBI as the sole regulator for all MFIs.

Financial illiteracy

One of the major hindrances in the growth of the microfinance sector is the financial

illiteracy of the people. This makes it difficult in creating awareness of microfinance and

even more difficult to serve them as microfinance clients. Though most of the

microfinance institutions claim to have educational trainings and programmes for the

benefit of the people, according to some of the experts the first thing these SHG and JLG

members are taught is to do their own signature. The worst part is that many MFIs think

that this is what financial literacy means. We all know how dangerous it can be when one

doesn’t know how to read but he/she knows how to accept or approve it (by signing it).

Inability to generate sufficient funds

Inability of MFIs to raise sufficient fund remains one of the important concern in the

microfinance sector. Though NBFCs are able to raise funds through private equity

investments because of the for-profit motive, such MFIs are restricted from taking public

deposits. Not-for-profit companies which constitute a major chunk of the MFI sector

have to primarily rely on donations and grants from Government and apex institutions

like NABARD and SIDBI. In absence of adequate funding from the equity market, the

major source of funds for MFIs are the bank loans, which is the reason for high Debt to

Equity ratio of most MFIs.

MFIs receive debt from banks against their equity and in order to increase their portfolio

size they need to increase their debts for which they further need to increase their equity.

After the Andhra crisis, it is reported that banks have stopped issuing fresh loans and

even though currently few banks have resumed, they want MFIs to increase their equity

to get fresh loans. So the only mode for the MFIs to increase their portfolio size is to

Page | 18

increase their equity. The problem of inadequate funds is even bigger for small and

nascent MFIs as they find it very difficult to get bank loans because of their small

portfolio size and so they have to look for other costlier sources of fund.

Dropouts and Migration of group members

Majority of the microfinance loans are disbursed on group lending concept and a past

record of the group plays an important role in getting new loans either through SHG-

Bank linkage or through MFIs. The two major problems with the group concept are

dropouts (when one or more members leave the group) and migration (when one or more

members move to another group). Most MFIs lend on the basis of the past record of the

group i.e. SHG or JLG and also on the individuals repayment performance. In absence of

a decent past record, members are deprived of getting bigger loan amounts and

additional services.

Transparent Pricing

Though the concern about the transparent pricing in the microfinance sector has been an

older one, it is gaining significance with the growing size and the increasing competition

in the sector. Non-transparent pricing by MFIs confines the bargaining power of the

borrowers and their ability to compare different loan products, because they don’t know

the actual price. In absence of the proper understanding of the pricing, clients end up

borrowing more than their ability to payback which results in over-indebtedness of the

borrower.

MFIs, in order to make their products look less expensive and more attractive, are

disguising their actual/effective interest rates (better known as the Annualized

Percentage Rates – APR) by including other charges like service charge, processing fee

etc. Some MFIs even take interest free deposits for lending microloans. There have been

cases where the interest rates are linked with the loan amount, which means a higher

interest rate for smaller loans (because of higher transaction cost). This is resulting in

highest interest rate being charged to the poorest clients, which contradicts with the

social aspect of microfinance.

Ambiguity in the pricing by MFIs is inviting regulatory bodies to implement strict

measures like interest rate caps. But simply putting an interest rate cap may encourage

Page | 19

MFIs to look for clients with larger loan requirements. This may deprive the clients with

smaller loan requirements who are supposed to be the actual beneficiary of microfinance.

Cluster formation – fight to grab established market

MFIs’ drive to grab an established market and reduce their costs is resulting in formation

of clusters in some areas leaving the others out of the microfinance outreach. By getting

an established microfinance market, MFIs reduce their initial cost in group formation of

clients, educating them and creating awareness about microfinance. This is one of the

reasons for the dominance of the microfinance sector in the southern states. Now the

problem is that a similar trend is being followed in the northern states as well. We have

already seen what happened in A.P and it seems that most of the MFIs have not taken a

lesson from the Andhra crisis.

This cluster formation is restricting MFIs from reaching to rural areas where there is the

actual need for microfinance. People in urban and semi-urban areas are already having

access to microfinance through SHG-bank linkage or individual lending, but in rural

areas people don’t have access to banks and so SBLP is not much active in such areas.

Because of the initial cost involved in serving a new location, MFIs are not willing to go

to such remote locations. This is the reason most of the MFIs have their branches in

urban and semi-urban areas only resulting in a very low rural penetration of

microfinance.

It is high time for the MFIs to understand that though microfinance is a resalable

product, increasing the outreach of the microfinance sector by including new clients and

serving new locations is what which is needed the most at the moment.

Multiple Lending and Over-Indebtedness

Both of these are outcome of the competition among the MFIs. Microfinance is one such

sector where the Neo-liberal theory of free market operation fails, at least to some extent.

Though competition is good for many sectors but in this case it is going against both the

parties. In order to eat away each other’s market share, MFIs are ending up giving

multiple loans to same borrowers which in some cases is leading to over-indebtedness (a

situation where the borrower has taken loans more than her/his repaying capacity) of the

borrower

Page | 20

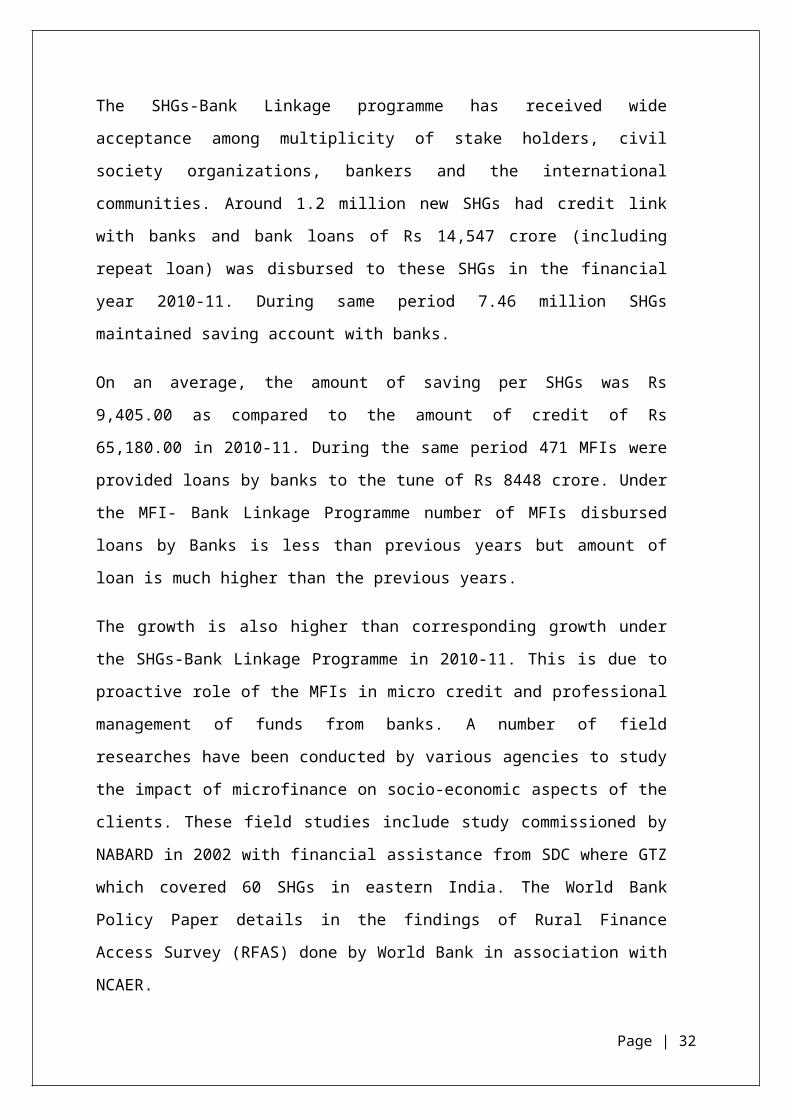

PRESENT STATUS OF MICROFINANCE IN INDIA

PRESENT STATUS OF MICROFINANCE IN INDIA Microfinance sector has

traversed a long journey from micro savings to microcredit and then to microenterprises

and now entered the field of micro insurance, micro pension. Financial institutions in the

country continue to play a leading role in the microfinance program for nearly two

decades now. They have joined hands proactively with informal delivery channels to

give microfinance sector the necessary momentum. The data for the year 2010-11 along

with a few preceding year have been presented and reviewed under two models of

microfinance (i) SHGBank Linkage model (ii)MFI-Bank Linkage model.

The SHGs-Bank Linkage programme has received wide acceptance among multiplicity

of stake holders, civil society organizations, bankers and the international communities.

Around 1.2 million new SHGs had credit link with banks and bank loans of Rs 14,547

crore (including repeat loan) was disbursed to these SHGs in the financial year 2010-11.

During same period 7.46 million SHGs maintained saving account with banks.

Page | 21

On an average, the amount of saving per SHGs was Rs 9,405.00 as compared to the

amount of credit of Rs 65,180.00 in 2010-11. During the same period 471 MFIs were

provided loans by banks to the tune of Rs 8448 crore. Under the MFI- Bank Linkage

Programme number of MFIs disbursed loans by Banks is less than previous years but

amount of loan is much higher than the previous years.

The growth is also higher than corresponding growth under the SHGs-Bank Linkage

Programme in 2010-11. This is due to proactive role of the MFIs in micro credit and

professional management of funds from banks. A number of field researches have been

conducted by various agencies to study the impact of microfinance on socio-economic

aspects of the clients. These field studies include study commissioned by NABARD in

2002 with financial assistance from SDC where GTZ which covered 60 SHGs in eastern

India. The World Bank Policy Paper details in the findings of Rural Finance Access

Survey (RFAS) done by World Bank in association with NCAER.

The RFAS covered 736 SHGs in the state of Andhra Pradesh and Uttar Pradesh. These

field studies reveal divergent research findings. But the common findings are of the

opinion that there is some increase in income levels and household assets in real terms

among the clients. These studies also brought out the fact that major occupation of group

members was agriculture along with other activities like farm labour and poultry. Being

rain fed area, lack of irrigation facility; declining agricultural outputs and fragmentation

of land have accentuated their vulnerabilities over a period of time.

The growth of microfinance organizations in India has also to be seen in the light of

financial sector reforms in India. Under the new approach, institutional viability is of

prime concern and instruments of directed credit and interest rate directives have been

totally diluted or done away with. As a consequence, banks are increasingly shying away

from rural lending as well as rationalizing their branch network in rural area.

Burgess and Pandey (2004) have brought out this fact in their study by stating that while

between 1977 and 1990 (Pre reform period) more bank branches were opened in

financially less developed states, but the pattern was reversed in post reform period. Thus

the access of the rural poor to credit through traditional bank lending has been reduced in

post reform era. The policy recommendation is to fill up this gap through microfinance.

Page | 22

FUTURE OF MICROFINANCE IN INDIA

An oft-neglected aspect of emerging economies is the severe poverty that still remains,

and there have been many strategies designed to provide the necessary financial

assistance that can help eradicate third-world living conditions. Originally hailed as a

means of enabling the poor to climb out of poverty, microfinance has come in for

criticism for sucking people into an uncompromising debt market.

In its latest report on the state of the microfinance industry, the Microcredit Summit

Campaign says the goals of funding poor people should be to prevent the vulnerabilities

they are accustomed to. It says: “If we want to provide financial services in a way that

helps people move out of poverty, then we need to provide things that cannot be stolen.

We need to provide products and services that help people living in poverty to address

the many areas of vulnerability that they face, so that their hard-earned gains are not

taken away by disaster and disease.”

Principles or profiteering

Although the concept of microfinance is rooted in a desire to help provide financial

services to people who would otherwise not be able to access them – thereby

empowering them to get out of poverty, as well as promoting better employment,

economic development and growth – there has been a debate over whether some

institutions are profiteering from the ignorance of the poor.

Originally developed during the 1970s by Bangladeshi economist Muhammad Yunus

and his Grameen Bank, microfinance was used to help struggling entrepreneurs from the

poorest parts of the world fund projects that would otherwise not get financing from

traditional sources. Yunus received the Nobel Peace Prize for his work, but questions

have been raised in recent years about the rates of interest on loans, a lack of

transparency and the aggressive recovery methods used by providers.

For a country expected to be a global economic powerhouse during the current century,

India is still saddled with a serious disparity in wealth between those at the bottom of

society and the phenomenally wealthy at the top. During the past decade, India’s

microfinance industry was held up as a shining example of how best to help the needy,

but has also been linked to a spate of suicides.

Page | 23

India is still saddled with a serious disparity in wealth

SKS, at the time India’s largest microfinance company, had a loan book worth $1.2bn. In

July 2014, it went public and, according to The Economist, was ’13 times

oversubscribed’. In the aftermath of the suicides, the company had to scale back its

operations in the region, cutting 1,200 jobs and shutting 78 branches. As a result, access

to microfinance declined in 2014; the first time this had happened since the Microcredit

Summit Campaign began recording how many clients the industry has.

The group’s report said: “Most of these reductions come from Andhra Pradesh, where

fast growth led to over lending, cases of harsh collection practices, and heavy regulation

from state government. Many [microfinance institutions] and banks stopped lending to

microfinance clients and self-help groups as a result.”

Tighter controls

One of the most contentious areas of microfinance is the level of interest on the loans

borrowers must pay back. During the industry’s most bullish period, some providers

charged borrowers as much as 40 percent. In 2014, new regulations were put in place to

prevent these extreme terms, with a cap of 26 percent interest on loans offered by

microfinance institutions.

There is also a limit of 10 percent on the amount lenders can place on top of the rate at

which customers have borrowed the money. KC Chakraborty, Deputy Governor of the

Reserve Bank of India, said the cap was necessary to prevent profiteering: “Charging an

interest rate beyond 26 percent from poor people is exploitation.”

Another area in which microfinance firms have been criticized is their alleged

application of a one-size-fits-all approach on a national level. Many argue that, for

microfinance schemes to be successful, lenders need to work on a local level, training up

borrowers and helping them understand how best to use their new capital.

Chakraborty believes the country’s microfinance institutions must take this route, saying

they “should develop local expertise and scale up locally. They should not scale up

nationally”. The Reserve Bank also introduced a licensing system for microfinance

organizations and placed restrictions on lending to people already had outstanding loans.

Page | 24

Growth prospects

Although the market took a considerable hit from the scandal, as well as 2009’s

economic downturn, there are signs it is starting to bounce back. In January, Yunus

Grameen Capital said it had secured $144m of equity for microfinance groups during

2012, “more than double the amount in the preceding year.”

Even SKS, with a reduced loan book of $325m, managed to raise $47.5m in equity in

2012. The total loan book for India’s microfinance industry is now said to be between

$2bn and $3bn; down on the $5bn before its downturn, but still a considerable amount.

Ultimately, how the industry survives the coming years depends on what strategies are

put in place by regulators to ensure that people are protected from predatory commercial

lenders. Providing the poor with an opportunity to break themselves out of poverty is a

noble ideal, but it must be achieved through proper training, a localised and flexible

strategy, and underpinned by meaningful and tight regulations.

How much longer India will need such a form of lending for the poor is also debateable.

While the country enjoys its newfound status as one of the economic engines of the East,

the disparity between rich and poor is both vast and shameful.

Bringing the poor into the tax system through employment will enhance the country’s

growth prospects, but it should be done in a realistic and sustainable way. It should also

avoid allowing an industry to develop collection tactics that bear worrying similarities to

those of loan sharks.

The caps placed on interest rates implemented in 2014 were necessary, and although

many firms have said the caps are stifling the industry’s ability to profit, they should be

maintained to ensure borrowers are not over-extended. Microfinance should be less

about profit and more about helping the poorest in society get on the first step to

prosperity.

Page | 25

RECOMMENDATIONS

1. Proper Regulation:

The regulation was not a major concern when the microfinance was in its

nascent stage and individual institutions were free to bring in innovative

operational models. However, as the sector completes almost two decades of age

with a high growth trajectory, an enabling regulatory environment that protects

interest of stakeholders as well as promotes growth, is needed.

2. Field Supervision:

In addition to proper regulation of the microfinance sector, field visits can be

adopted as a medium for monitoring the conditions on ground and initiating

corrective action if needed. This will keep a check on the performance of ground

staff of various MFIs and their recovery practices. This will also encourage

MFIs to abide by proper code of conduct and work more efficiently. However,

the problem of feasibility and cost involved in physical monitoring of this vast

sector remains an issue in this regard.

3. Encourage rural penetration:

It has been seen that in lieu of reducing the initial cost, MFIs are opening their

branches in places which already have a few MFIs operating. Encouraging MFIs

for opening new branches in areas of low microfinance penetration by providing

financial assistance will increase the outreach of the microfinance in the state

and check multiple lending. This will also increase rural penetration of

microfinance in the state.

4. Complete range of Products:

MFIs should provide complete range of products including credit, savings,

remittance, financial advice and also non-financial services like training and

support. As MFIs are acting as a substitute to banks in areas where people don’t

have access to banks, providing a complete range of products will enable the

poor to avail all services.

5. Transparency of Interest rates:

As it has been observed that, MFIs are employing different patterns of charging

interest rates and a few are also charging additional charges and interest free

deposits (a part of the loan amount is kept as deposit on which no interest is

paid).

Page | 26

All this make the pricing very confusing and hence the borrower feels incompetent

in terms of bargaining power. So a common practice for charging interest should be

followed by all MFIs so that it makes the sector more competitive and the

beneficiary gets the freedom to compare different financial products before buying.

6. Technology to reduce Operating Cost:

MFIs should use new technologies and IT tools & applications to reduce their

operating costs. Though most NBFCs are adopting such cost cutting measures,

which is clearly evident from the low cost per unit money lent (9%-10%) of such

institutions. NGOs and Section 25 companies are having a very high value of

cost per unit money lent i.e. 15-35 percent and hence such institutions should be

encouraged to adopt cost-cutting measures to reduce their operating costs. Also

initiatives like development of common MIS and other software for all MFIs can

be taken to make the operation more transparent and efficient.

7. Alternative sources of Fund:

In absence of adequate funds the growth and the reach of MFIs become

restricted and to overcome this problem MFIs should look for other sources for

funding their loan portfolio. Some of the ways through which MFIs can raise

their fund are:

a) By getting converted to for-profit company i.e. NBFC: Without investment by

outside investors, MFIs are limited to what they can borrow to a multiple of total

profits and equity investment. To increase their borrowings further, MFIs need

to raise their Equity through outside investors. The first and the most crucial step

to receive equity investment are getting converted to for-profit NBFC. Along

with the change in status the MFI should also develop strong board, a quality

management information system (MIS) and obtain a credit rating to attract

potential investors.

b) Portfolio Buyout: It is when banks or other institutions purchase the rights to future

payment stream from a set of outstanding loans granted by MFIs. In such

transactions MFIs are responsible for making up any loss in repayment up to a

certain percentage of the portfolio and this clause is known as “first loss default

guarantee”. The above clause ensures that the MFI retains the correct incentive to

collect these loans.

Page | 27

c) Securitization of Loans: This refers to a transaction in which the repayments from a

set of microloans from one or more MFIs are packaged into a special purpose

vehicle, from which tradable securities are issued. As the loans from multiple MFIs

can be pooled together the risk gets diversified. Though securitization of loans and

portfolio buyout are similar in many ways like first loss default guarantee clause,

limit to the amount of loans that can be sold off etc. The major difference between

the two is that securitizations require a rating from a credit rating agency and that it

can be re-sold, which makes securitized loans attract more potential buyers. Also

unlike portfolio buyout, there can be multiple buyers and sellers for each transaction

in case of securitization of loans as compared to single buyer and single seller in

portfolio buyout. Through securitization, MFIs can tap new sources of investments

because fund of certain types like mutual funds, which are barred from directly

investing in MFIs, can invest through securitized loans.

Page | 28

A FRESH START FOR THE MICROFINANCE IN INDIA

It has been a quiet period for the microfinance sector. While there was much hype about

the microfinance bill, it seems to have fallen by the wayside, at least from legislative

business. The oppressive Andhra Pradesh law continues to be in existence. Microfinance

institutions have reconciled themselves to the “new normal”, which is reporting their

performance in two parts — overall performance and performance outside Andhra

Pradesh.

Some institutions which were deeply invested in Andhra Pradesh have encountered

trouble and are facing bankruptcy. But the bloodbath seems to be over and we may be

ready for a new beginning. That several genuine institutions became collateral damage is

the bad news.

However, there is much good news for the sector. The new governor of the RBI is a

known liberal among conservatives. He signed a letter to the media when the crisis was

at its peak. The letter, signed by many Indian academics teaching at American

universities, called for saving the microfinance sector from the oppressive Andhra act.

Raghu ram Rajan has made his inclinations on the expected roadmap for financial

inclusion clear. This is a significant departure from the traditional position of the RBI,

which has always believed that financial inclusion has to be bank-led.

Rajan believes in the multiplicity of institutions. He argues for specialised institutions to

do specialised jobs. While he does not argue against the obligations to be placed on

banks for priority sector lending targets (which include microfinance as a category), he

does argue for giving them a choice on how to achieve this.

This includes the purchase of priority sector lending notes — a tradable paper that

represents the portfolio achieved by somebody beyond their obligations. These notes

could originate from non-banks as well, and is an attractive proposition for MFIs that are

non-banks.

Page | 29

Rajan has also argued for specialised and regional banks. While these two MFI applicants for a bank licence might find favour with the RBI if they pass all the other criteria, others can seek solace in the fact that there could be more regulatory easing to incorporate financial institutions in a more centrally regulated banking framework. The recent report by the Nachiket Mor committee provides a framework for microfinance institutions to morph into consumer banks with limited deposit taking ability.

The committee also argues for removing all caps on the spreads that the intermediaries

might have in order to be a portfolio that qualifies for the priority sector tag. If this report

is accepted, it will eliminate the oppressive clauses under the Male gam committee

report. This is good news for both banks and financial institutions.

Page | 30

CONCLUSION

The journey so far has never been a bed of roses for the MFIs. The usurious interest

rates, limited products, lack of accessibility have always won them brickbats from

the critics and sceptics.

The emergence of regulatory body for MFIs, enactment of legislation, performance

rating by industry bodies, increased funding, increasing spends on technology and

innovative products indemnify the potential of MFI industry.

Only 28 percent of the total demand for microfinance services would be covered by

the MFI globally by 2014 with the World Bank estimation of microfinance

requirement at USD 300 billion.

The world leaders at UN Summit 2005 have set the goal of reducing the extreme

poverty in the world by half by the year 2015, as one of the Millennium

Development Goals.

In that all-encompassing journey undoubtedly MFIs play a pivotal role. The

producers of software, hardware and associated infrastructure required by the MFIs

should by then acknowledge the undeniable prospects of MFIs and prepare

themselves accordingly. And by doing so they are also contributing to a larger social

cause; of course with business objective!

Page | 31

BIBLIOGRAPHY

WEBSITES:

a) http://indianresearchjournals.com/pdf/IJMFSMR/2012/November/13.pdf

b) indianresearchjournals.com/pdf/IJMFSMR/2012/

c) www.iitk.ac.in/ime/MBA_IITK/avantgarde/?p=475d) indianexpress.come) www.crisil.com/pdf/ratings/indias-25-leading-mfis.pdf

f) www.infosys.com/.../Emerging-Trends-in-the-Microfinance-Industry.pdfg) www.indiatimes.com

NEWSPAPERS & MAGAZINES: -

a) BUSINESS WORLD

b) INDIA TODAY

c) THE HINDU

d) THE FINANCIAL EXPRESS

e) THE TIMES OF INDIA

Page | 32