Introduction to Discounted Cash Flow Valuation

16

Introduction to Introduction to Discounted Cash Discounted Cash Flow Valuation Flow Valuation Nicholas Ramm Nicholas Ramm Finance Sector, Madison Finance Sector, Madison Investment Fund Investment Fund October 29, 2007 October 29, 2007

description

Introduction to Discounted Cash Flow Valuation. Nicholas Ramm Finance Sector, Madison Investment Fund October 29, 2007. What is DCF analysis?. Method of valuing a financial asset Focus on firms Uses cash flows Find present value of these cash flows. Present Value. - PowerPoint PPT Presentation

Transcript of Introduction to Discounted Cash Flow Valuation

Introduction to Introduction to Discounted Cash Flow Discounted Cash Flow

ValuationValuation

Nicholas RammNicholas Ramm

Finance Sector, Madison Investment Finance Sector, Madison Investment FundFund

October 29, 2007October 29, 2007

What is DCF analysis?What is DCF analysis?

Method of valuing a financial assetMethod of valuing a financial asset Focus on firmsFocus on firms

Uses Uses cash flowscash flows

Find Find present valuepresent value of these cash of these cash flowsflows

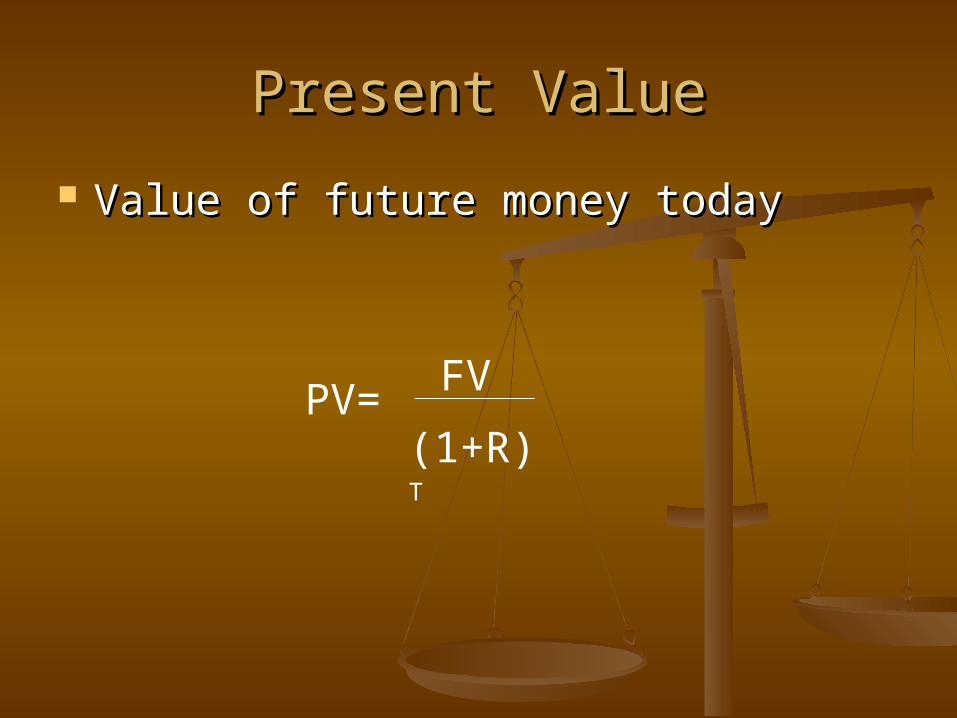

Present ValuePresent Value

Value of future money todayValue of future money today

PV=FV

(1+R)T

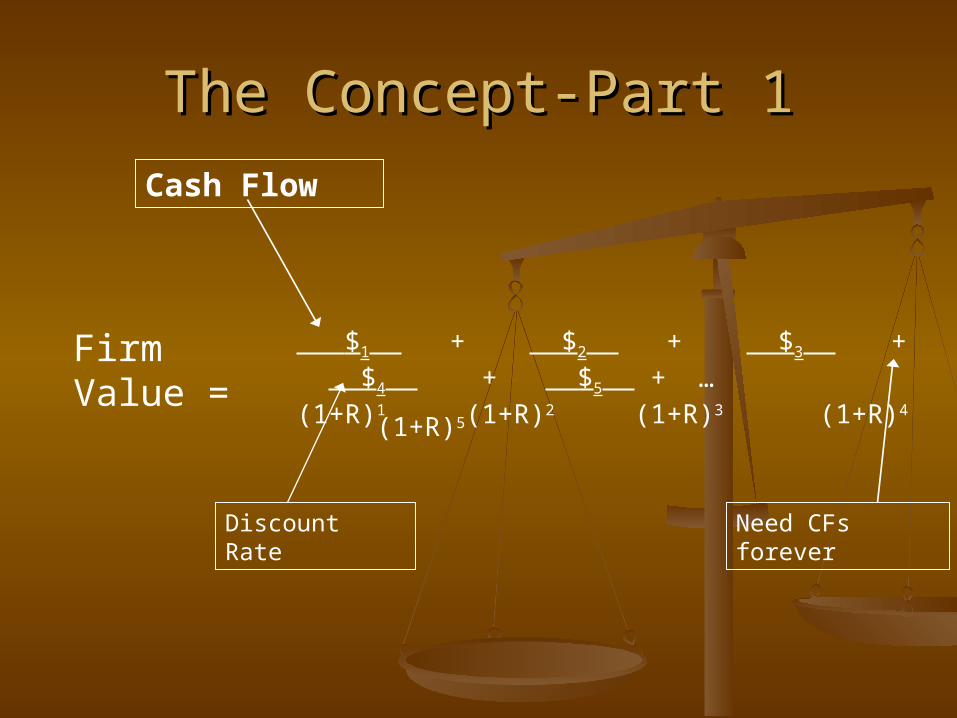

The Concept-Part 1The Concept-Part 1

Firm Value = $1 + $2 + $3 + $4 + $5 + …(1+R)1 (1+R)2 (1+R)3 (1+R)4 (1+R)5

Cash Flow

Discount Rate Need CFs forever

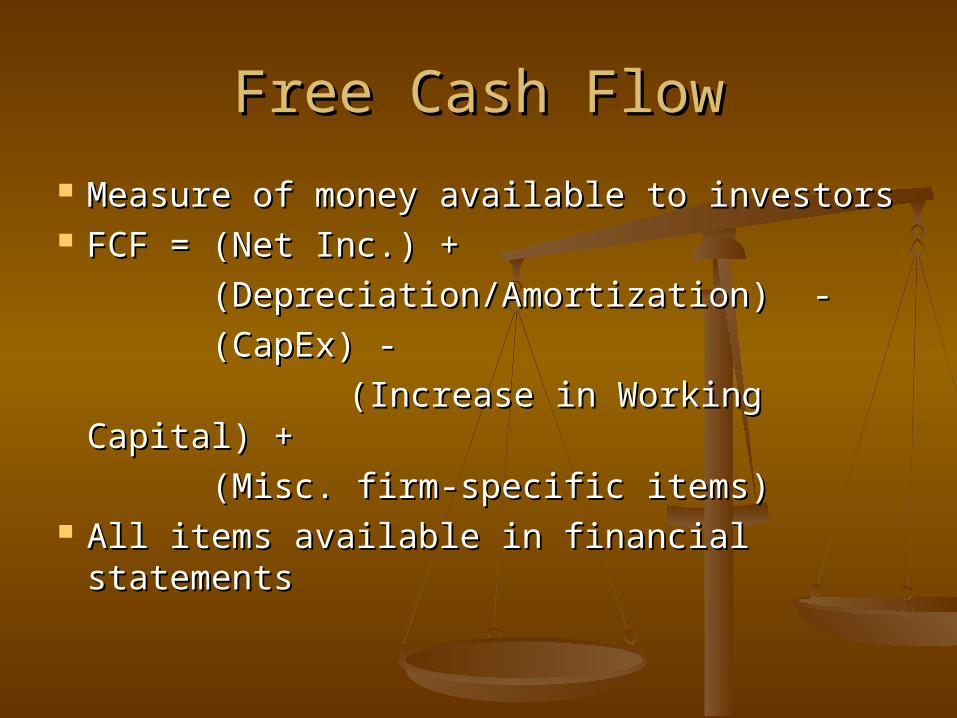

Free Cash FlowFree Cash Flow

Measure of money available to investorsMeasure of money available to investors FCF = (Net Inc.) +FCF = (Net Inc.) +

(Depreciation/Amortization) -(Depreciation/Amortization) -

(CapEx) -(CapEx) -

(Increase in Working Capital) +(Increase in Working Capital) +

(Misc. firm-specific items)(Misc. firm-specific items) All items available in financial All items available in financial

statementsstatements

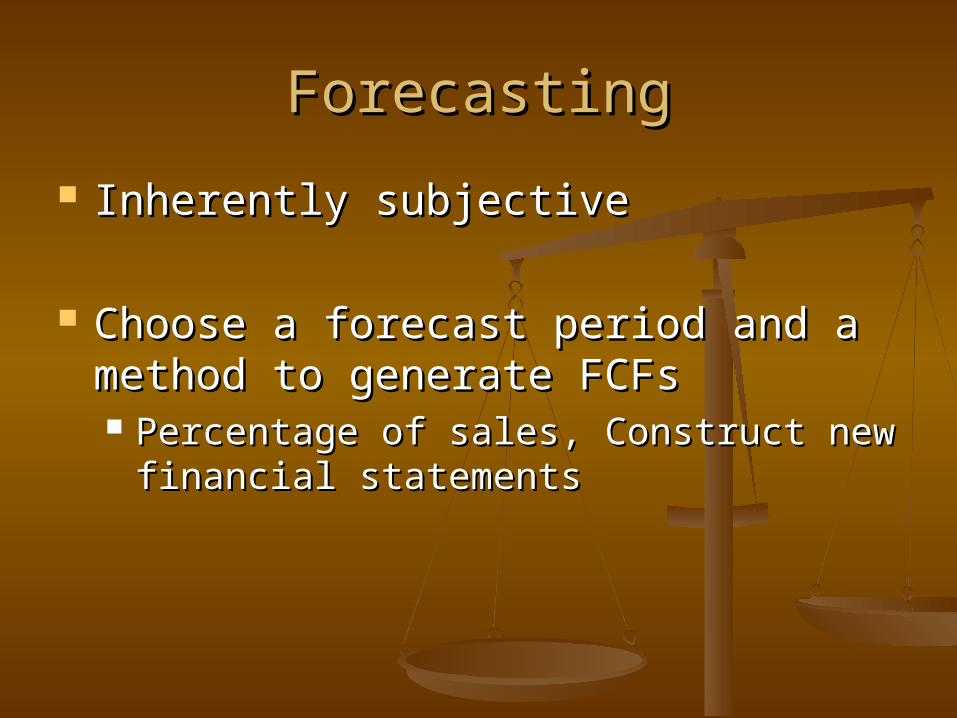

ForecastingForecasting

Inherently subjectiveInherently subjective

Choose a forecast period and a Choose a forecast period and a method to generate FCFsmethod to generate FCFs Percentage of sales, Construct new Percentage of sales, Construct new

financial statementsfinancial statements

The Concept-Part 2The Concept-Part 2

Firm Value = FCF1 + FCF2 + FCF3 + FCF4 + FCF5 + …(1+R)1 (1+R)2 (1+R)3 (1+R)4 (1+R)5

Discount Rate Need CFs forever

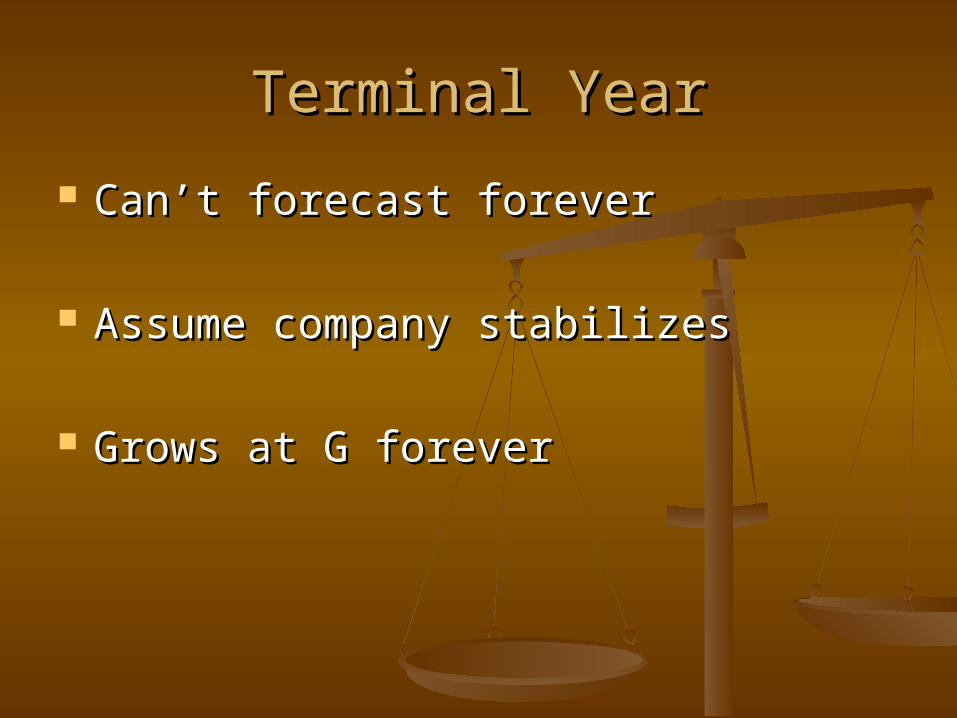

Terminal YearTerminal Year

Can’t forecast foreverCan’t forecast forever

Assume company stabilizes Assume company stabilizes

Grows at G foreverGrows at G forever

Terminal YearTerminal Year

TYV = FCFTY * (1 + G)

R - G

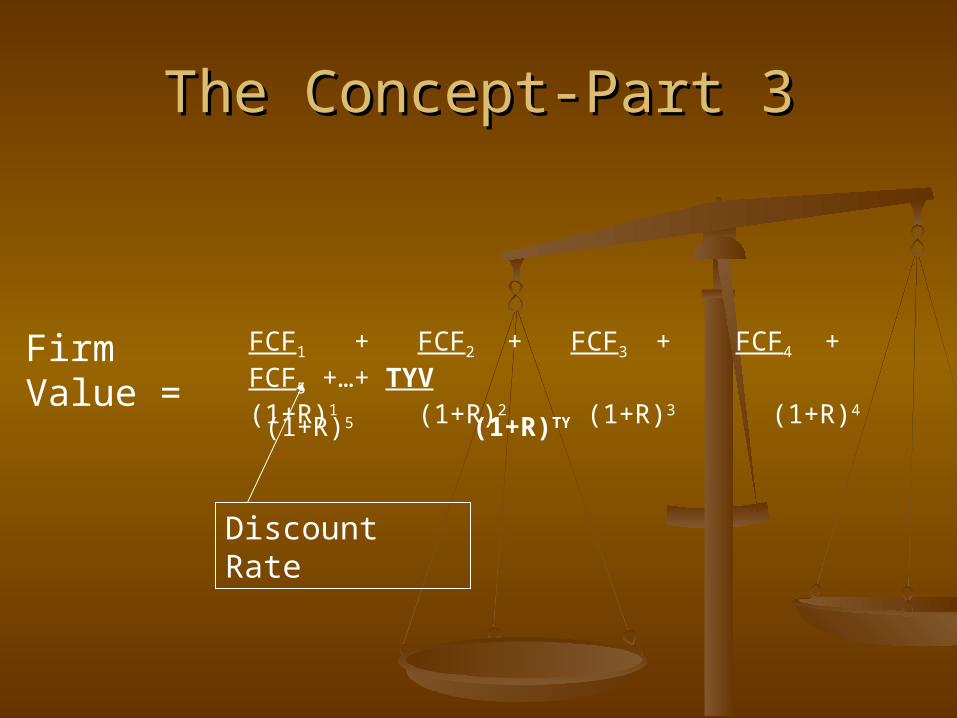

The Concept-Part 3The Concept-Part 3

Firm Value = FCF1 + FCF2 + FCF3 + FCF4 + FCF5 +…+ TYV(1+R)1 (1+R)2 (1+R)3 (1+R)4 (1+R)5 (1+R)TY

Discount Rate

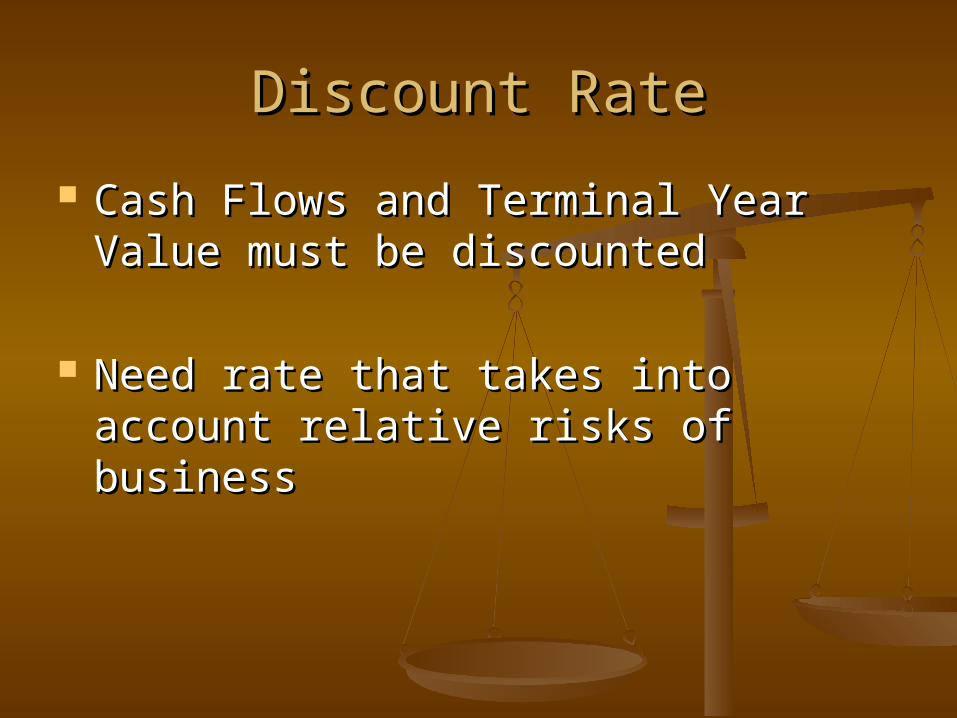

Discount RateDiscount Rate

Cash Flows and Terminal Year Value Cash Flows and Terminal Year Value must be discountedmust be discounted

Need rate that takes into account Need rate that takes into account relative risks of businessrelative risks of business

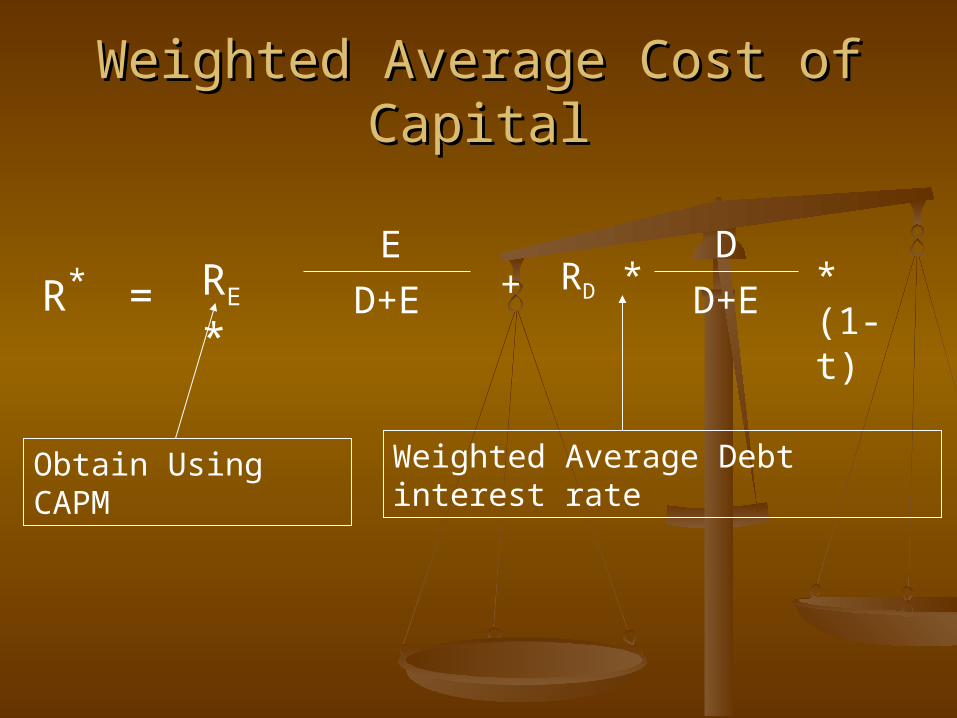

Weighted Average Cost of CapitalWeighted Average Cost of Capital

R* = RE *E

D+E + RD *D

D+E

Obtain Using CAPM Weighted Average Debt interest rate

* (1-t)

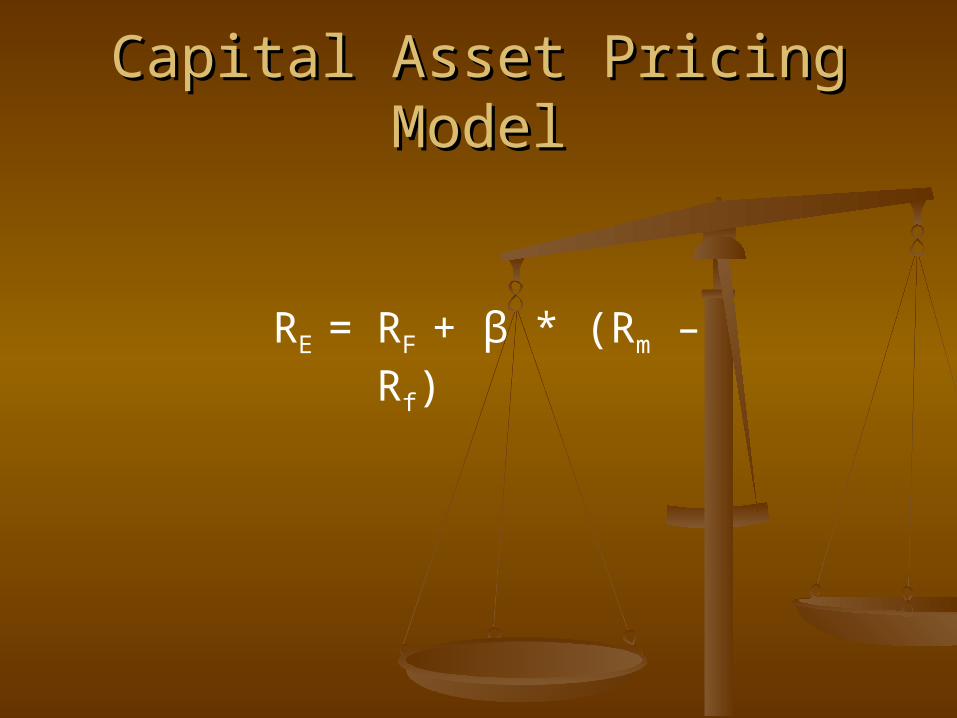

Capital Asset Pricing ModelCapital Asset Pricing Model

RE = RF + β * (Rm – Rf)

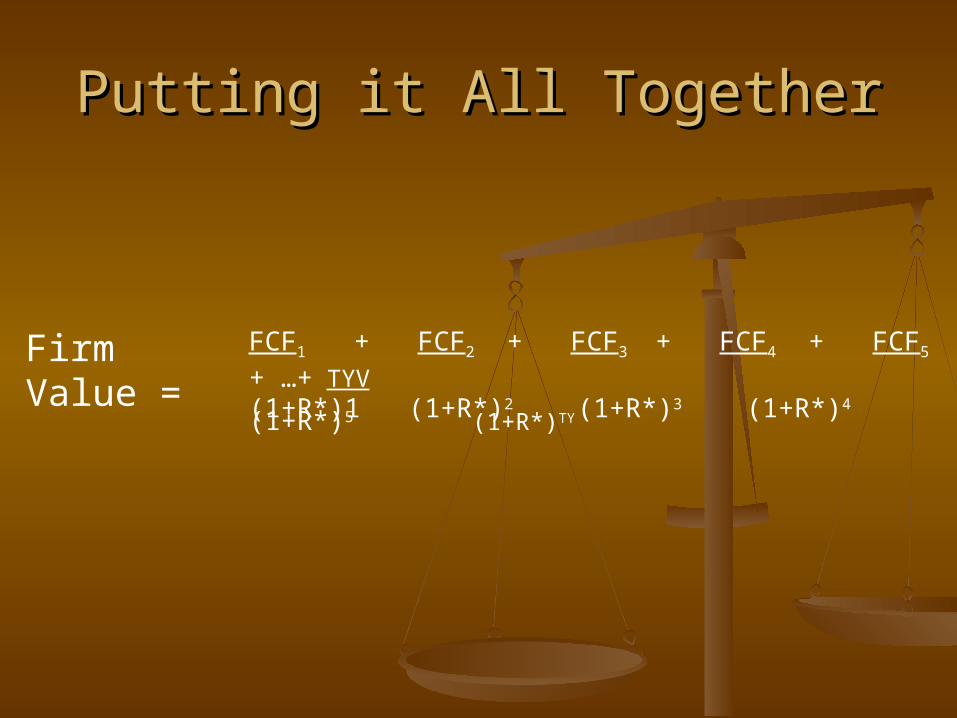

Putting it All TogetherPutting it All Together

Firm Value = FCF1 + FCF2 + FCF3 + FCF4 + FCF5 + …+ TYV

(1+R*)1 (1+R*)2 (1+R*)3 (1+R*)4 (1+R*)5 (1+R*)TY

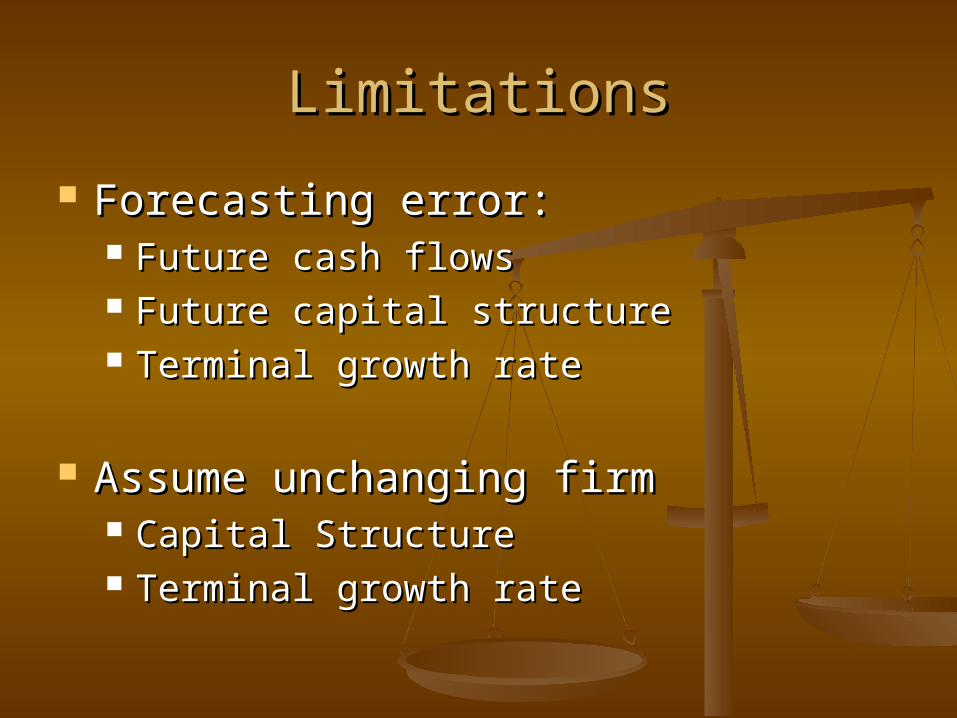

LimitationsLimitations

Forecasting error:Forecasting error: Future cash flowsFuture cash flows Future capital structureFuture capital structure Terminal growth rateTerminal growth rate

Assume unchanging firmAssume unchanging firm Capital StructureCapital Structure Terminal growth rateTerminal growth rate

Questions?Questions?