Introduction to Auto Enrolment

27

An Introduction to An Introduction to Auto Enrolment Auto Enrolment

-

Upload

qtac-payroll-software -

Category

Business

-

view

40 -

download

0

Transcript of Introduction to Auto Enrolment

An Introduction toAn Introduction toAuto Enrolment Auto Enrolment

•Work Place Pensions•Auto Enrolment

•The Pensions Regulator•Pension Providers

•Auto Enrolment Functionality in QTAC Payroll•Planning for Success

By the end of this presentation you should be confident with the following concepts:

Contents of PresentationContents of Presentation

1. What is Auto Enrolment2. Contributions3. Staging Dates

4. Key Terms5. The Pensions Regulator

6. Pension Providers7. How can QTAC Payroll help

8. 7 Key Steps to Success9. Q&A’s

What is Auto EnrolmentWhat is Auto Enrolment

• ‘Workplace Pension Reform’ is the term used to describe the changes to pensions in the UK, where employees are automatically enrolled into an ‘Automatic Enrolment’ pension scheme, as long as they ‘qualify’.

• A workplace pension, which is arranged by the employer, is a way for employees to save for retirement. Some workplace pensions are also called ‘occupational’, ‘works’, ‘company’ or ‘work-based’ pensions.

• If a company already has a pension scheme they will need to check that it ‘qualifies’ if their plan is to use that scheme as their ‘Workplace Pension’.

• Companies who do not currently have a pension scheme setup will need to set up an ‘Auto Enrolment’ scheme. The pension scheme must ‘qualify’ - meaning the employee and employer contributions match or exceed the minimum contributions (detailed later in this document) and also that no restrictions are placed on membership.

• Every company will be required to offer employees the chance to join a pension scheme, which both the ‘employee’ and ‘employer’ will contribute in to. The employer has to contribute at least the minimum contribution into the scheme in order for the scheme to qualify.

• In most cases the government also add money into the pension scheme in the form of tax relief.

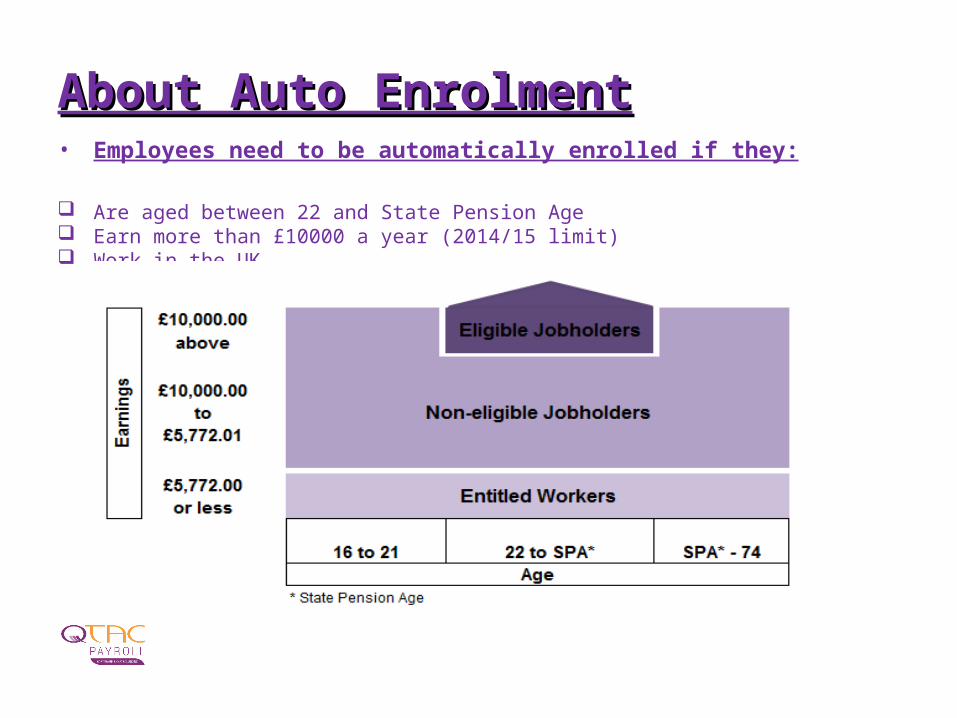

About Auto EnrolmentAbout Auto Enrolment• Employees need to be automatically enrolled if they:

Are aged between 22 and State Pension Age Earn more than £10000 a year (2014/15 limit) Work in the UK

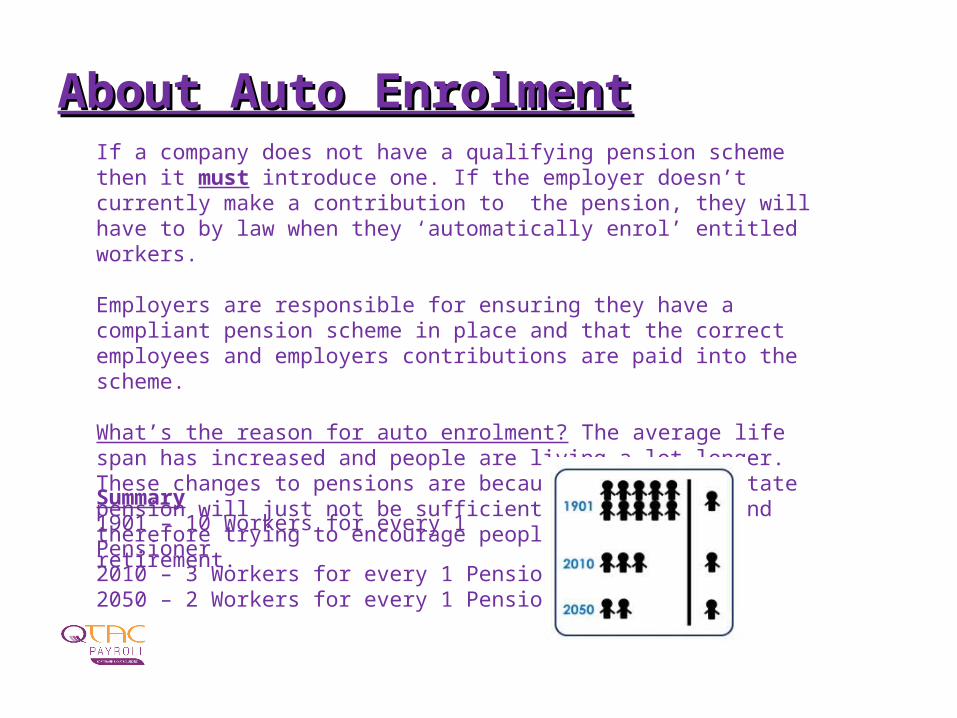

About Auto EnrolmentAbout Auto EnrolmentIf a company does not have a qualifying pension scheme then it must introduce one. If the employer doesn’t currently make a contribution to the pension, they will have to by law when they ‘automatically enrol’ entitled workers.

Employers are responsible for ensuring they have a compliant pension scheme in place and that the correct employees and employers contributions are paid into the scheme.

What’s the reason for auto enrolment? The average life span has increased and people are living a lot longer. These changes to pensions are because the current state pension will just not be sufficient when retiring and therefore trying to encourage people to save for retirement.

Summary1901 – 10 Workers for every 1 Pensioner2010 – 3 Workers for every 1 Pensioner2050 – 2 Workers for every 1 Pensioner

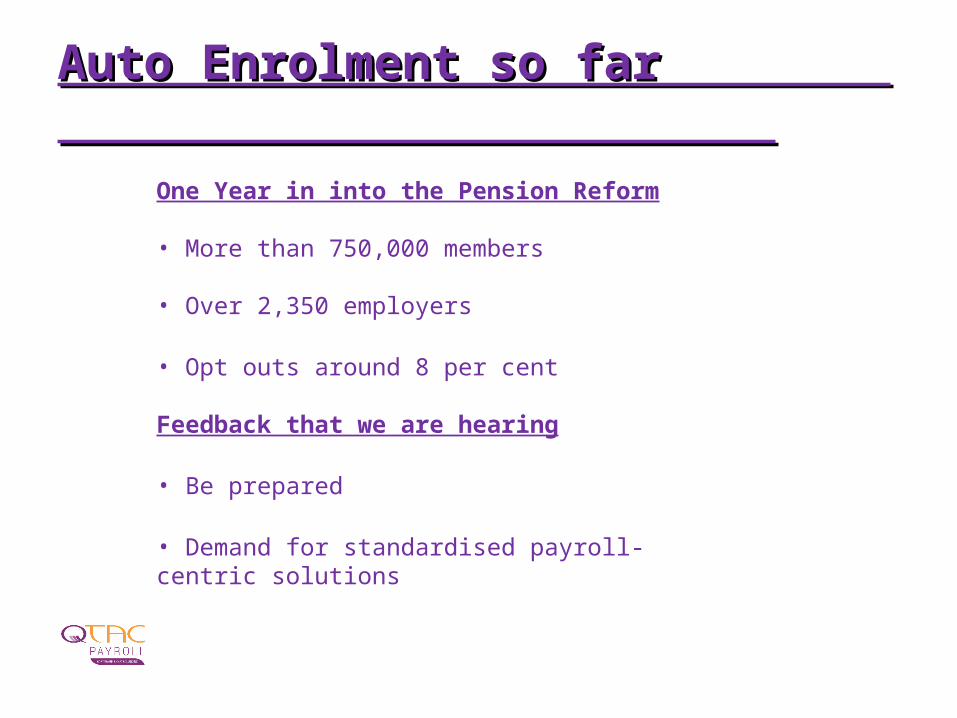

Auto Enrolment so far Auto Enrolment so far

One Year in into the Pension Reform

• More than 750,000 members

• Over 2,350 employers

• Opt outs around 8 per cent

Feedback that we are hearing

• Be prepared

• Demand for standardised payroll-centric solutions

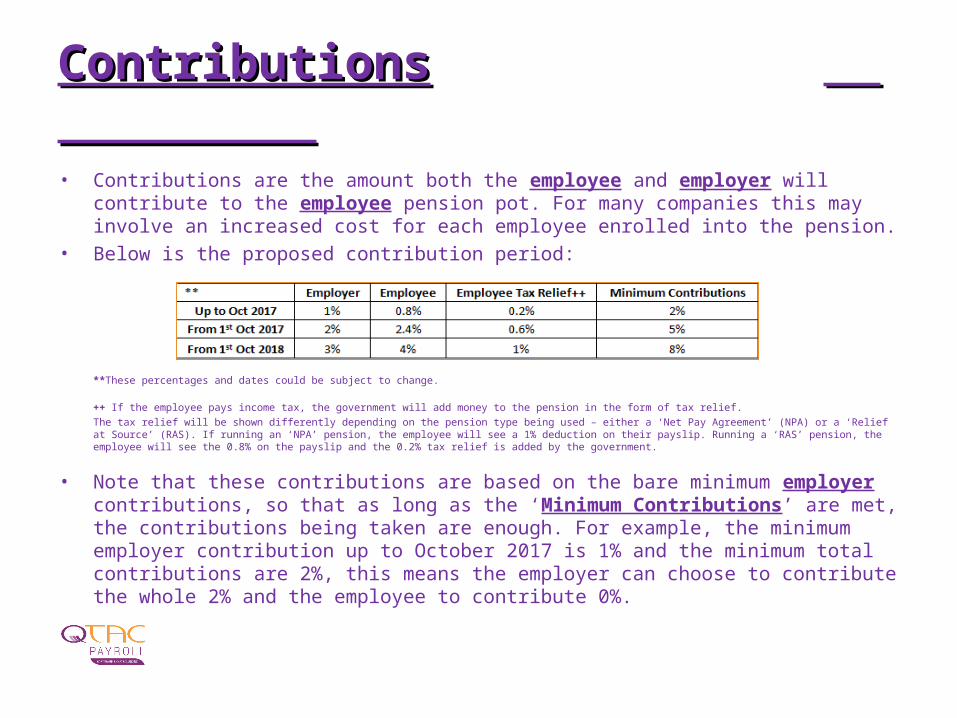

ContributionsContributions

• Contributions are the amount both the employee and employer will contribute to the employee pension pot. For many companies this may involve an increased cost for each employee enrolled into the pension.

• Below is the proposed contribution period:

**These percentages and dates could be subject to change.

++ If the employee pays income tax, the government will add money to the pension in the form of tax relief.The tax relief will be shown differently depending on the pension type being used – either a ‘Net Pay Agreement’ (NPA) or a ‘Relief at Source’ (RAS). If running an ‘NPA’ pension, the employee will see a 1% deduction on their payslip. Running a ‘RAS’ pension, the employee will see the 0.8% on the payslip and the 0.2% tax relief is added by the government.

• Note that these contributions are based on the bare minimum employer contributions, so that as long as the ‘Minimum Contributions’ are met, the contributions being taken are enough. For example, the minimum employer contribution up to October 2017 is 1% and the minimum total contributions are 2%, this means the employer can choose to contribute the whole 2% and the employee to contribute 0%.

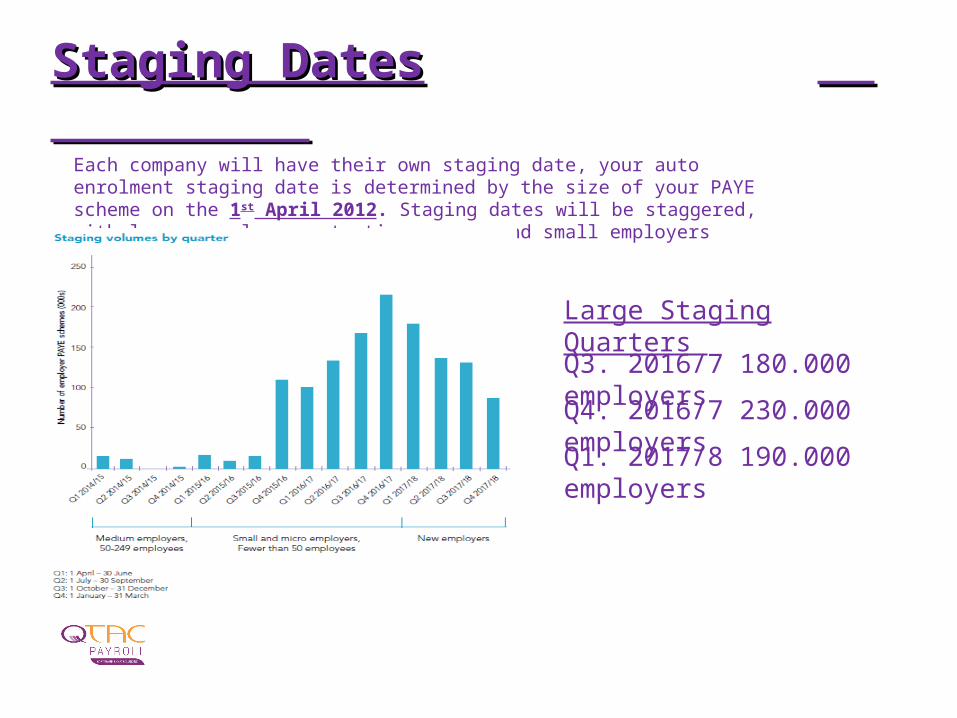

Staging DatesStaging Dates Each company will have their own staging date, your auto enrolment staging date is determined by the size of your PAYE scheme on the 1st April 2012. Staging dates will be staggered, with larger employers starting sooner and small employers starting later.

Q3. 2016/7 180.000 employers

Q4. 2016/7 230.000 employers

Q1. 2017/8 190.000 employers

Large Staging Quarters

Staging DatesStaging Dates • What is my staging date? The date you need to Automatically Enroll all eligible workers

• How do I find it out? Visit The Pensions Regulators website• Use the Staging Date Calculator

www.thepensionsregulator.gov.uk/

• A company can choose to move it’s staging date to an earlier date but it cannot be moved to a later one.

• A pension scheme can be setup for employees at any time. You do not have to wait until auto enrolment is introduced.

• We recommend that you give yourself plenty of time to prepare

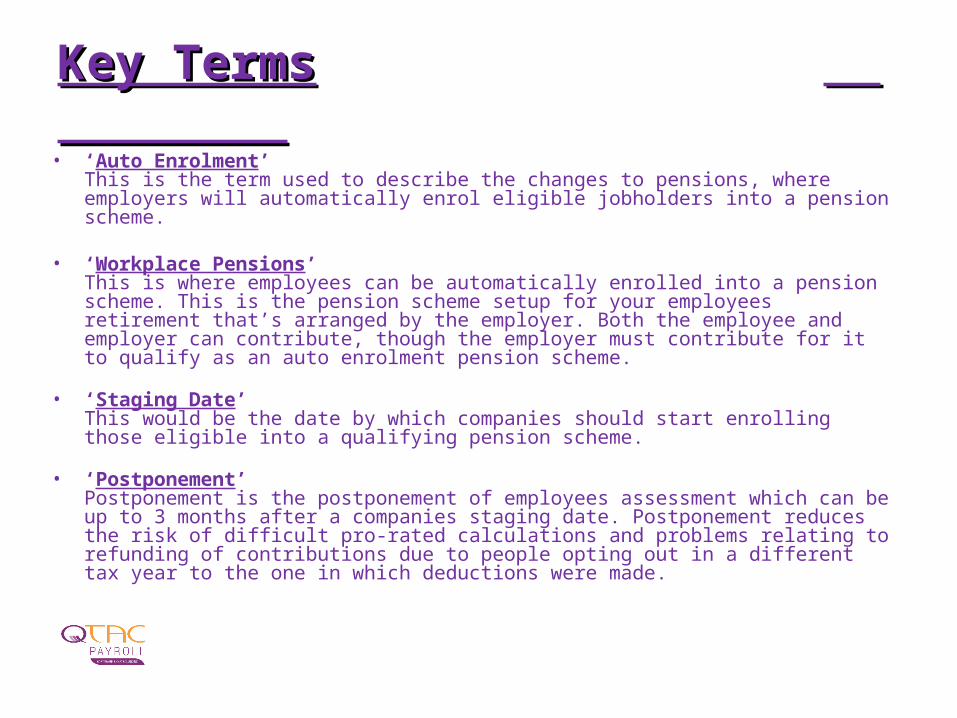

Key TermsKey Terms • ‘Auto Enrolment’

This is the term used to describe the changes to pensions, where employers will automatically enrol eligible jobholders into a pension scheme.

• ‘Workplace Pensions’ This is where employees can be automatically enrolled into a pension scheme. This is the pension scheme setup for your employees retirement that’s arranged by the employer. Both the employee and employer can contribute, though the employer must contribute for it to qualify as an auto enrolment pension scheme.

• ‘Staging Date’This would be the date by which companies should start enrolling those eligible into a qualifying pension scheme.

• ‘Postponement’Postponement is the postponement of employees assessment which can be up to 3 months after a companies staging date. Postponement reduces the risk of difficult pro-rated calculations and problems relating to refunding of contributions due to people opting out in a different tax year to the one in which deductions were made.

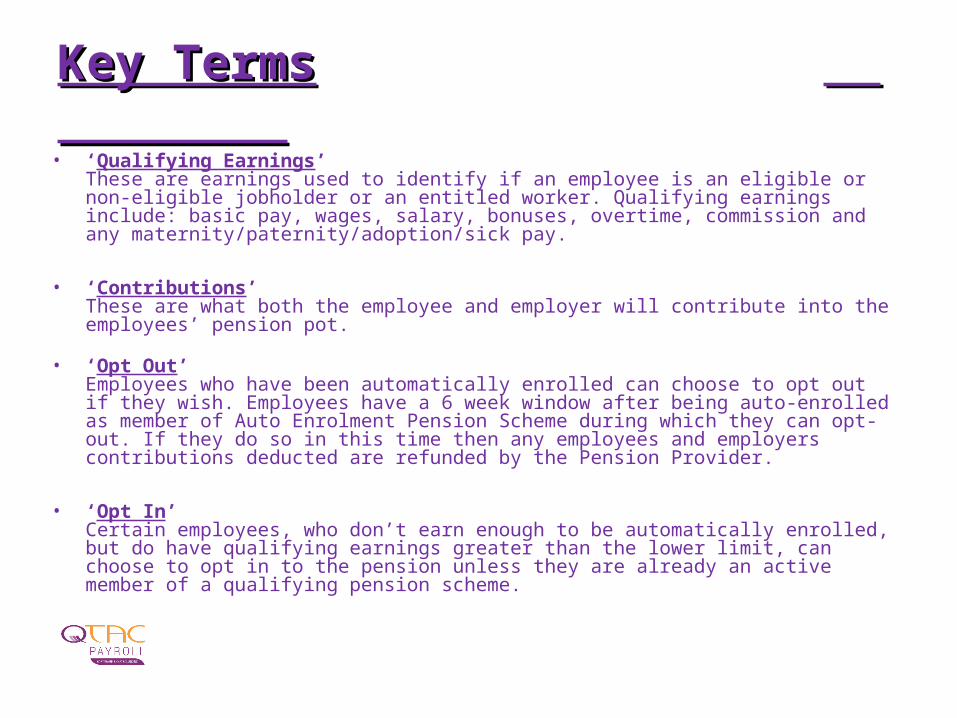

Key TermsKey Terms • ‘Qualifying Earnings’

These are earnings used to identify if an employee is an eligible or non-eligible jobholder or an entitled worker. Qualifying earnings include: basic pay, wages, salary, bonuses, overtime, commission and any maternity/paternity/adoption/sick pay.

• ‘Contributions’These are what both the employee and employer will contribute into the employees’ pension pot.

• ‘Opt Out’Employees who have been automatically enrolled can choose to opt out if they wish. Employees have a 6 week window after being auto-enrolled as member of Auto Enrolment Pension Scheme during which they can opt-out. If they do so in this time then any employees and employers contributions deducted are refunded by the Pension Provider.

• ‘Opt In’Certain employees, who don’t earn enough to be automatically enrolled, but do have qualifying earnings greater than the lower limit, can choose to opt in to the pension unless they are already an active member of a qualifying pension scheme.

Key TermsKey Terms

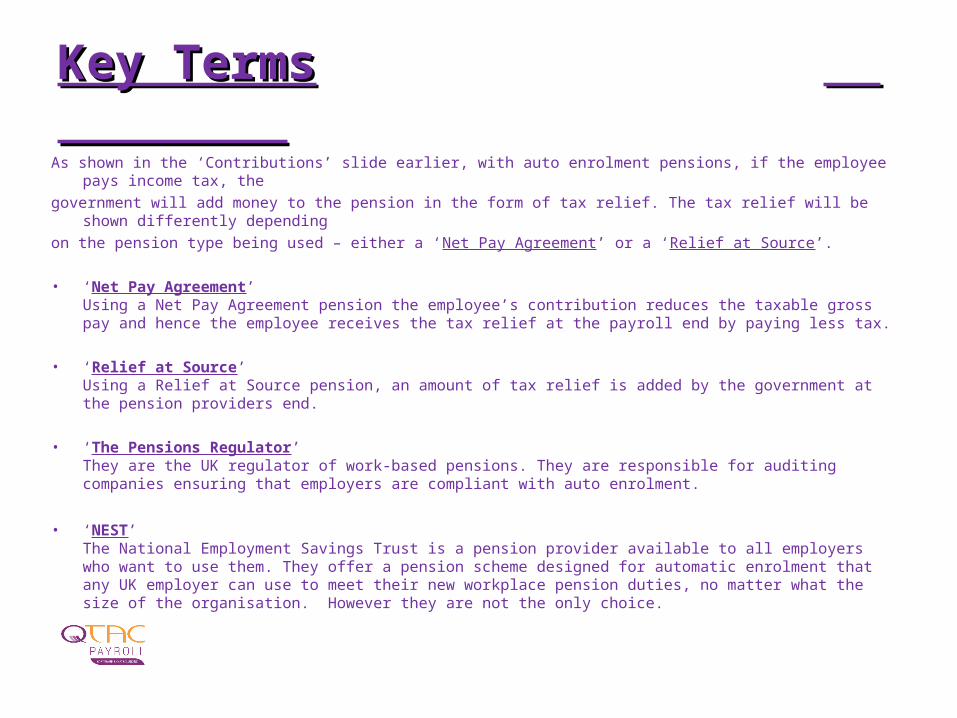

As shown in the ‘Contributions’ slide earlier, with auto enrolment pensions, if the employee pays income tax, thegovernment will add money to the pension in the form of tax relief. The tax relief will be shown differently dependingon the pension type being used – either a ‘Net Pay Agreement’ or a ‘Relief at Source’.

• ‘Net Pay Agreement’ Using a Net Pay Agreement pension the employee’s contribution reduces the taxable gross pay and hence the employee receives the tax relief at the payroll end by paying less tax.

• ‘Relief at Source’Using a Relief at Source pension, an amount of tax relief is added by the government at the pension providers end.

• ‘The Pensions Regulator’They are the UK regulator of work-based pensions. They are responsible for auditing companies ensuring that employers are compliant with auto enrolment.

• ‘NEST’The National Employment Savings Trust is a pension provider available to all employers who want to use them. They offer a pension scheme designed for automatic enrolment that any UK employer can use to meet their new workplace pension duties, no matter what the size of the organisation. However they are not the only choice.

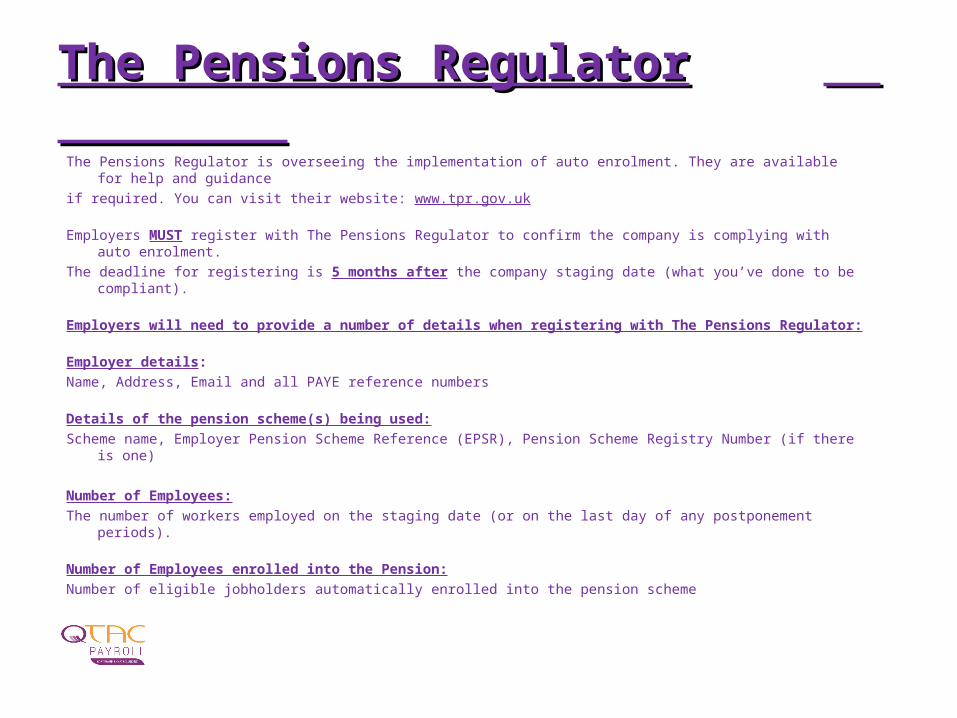

The Pensions RegulatorThe Pensions Regulator The Pensions Regulator is overseeing the implementation of auto enrolment. They are available for help and guidanceif required. You can visit their website: www.tpr.gov.uk

Employers MUST register with The Pensions Regulator to confirm the company is complying with auto enrolment.The deadline for registering is 5 months after the company staging date (what you’ve done to be compliant).

Employers will need to provide a number of details when registering with The Pensions Regulator:

Employer details: Name, Address, Email and all PAYE reference numbers

Details of the pension scheme(s) being used: Scheme name, Employer Pension Scheme Reference (EPSR), Pension Scheme Registry Number (if there is one)

Number of Employees:The number of workers employed on the staging date (or on the last day of any postponement periods).

Number of Employees enrolled into the Pension:Number of eligible jobholders automatically enrolled into the pension scheme

The Pensions RegulatorThe Pensions Regulator

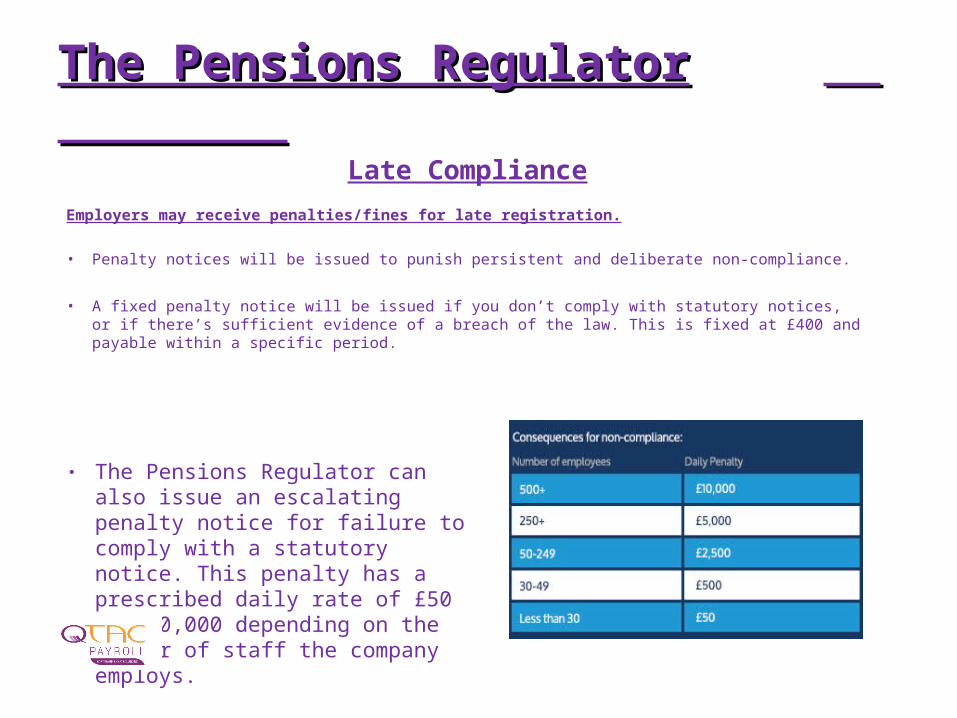

Late Compliance

Employers may receive penalties/fines for late registration.

• Penalty notices will be issued to punish persistent and deliberate non-compliance.

• A fixed penalty notice will be issued if you don’t comply with statutory notices, or if there’s sufficient evidence of a breach of the law. This is fixed at £400 and payable within a specific period.

The Pensions Regulator can also issue an escalating penalty notice for failure to comply with a statutory notice. This penalty has a prescribed daily rate of £50 to £10,000 depending on the number of staff the company employs.

Pension ProvidersPension Providers

Companies will want to look into which pension provider to use, as when offering a workplace pension scheme each will have their own positives and negatives. We suggest you consult an IFA in order to identify a pension that suits your business.

At QTAC we have been working closely with both Nest & NOW pension schemes to provide the necessary interfaces.

NOW Pensions are a pension provider that we will link with. Unlike NEST, NOW Pensions have the ability to pick and choose who they provide pension schemes to.

The ‘National Employment Savings Trust’ has been created as part of the government’s pension reforms to help employers meet their new duties. NEST is just one of the options available to employers when offering a pension scheme. Where as other pension providers can pick and choose who they provide schemes to, NEST must accept anyone who wants to use them.

Please Note:If you decide to use a different pension provider you will still be able to fulfil your

requirements by using QTAC with Auto Enrolment

How Can QTAC Help How Can QTAC Help Features included in the Auto Enrolment edition are:

Workforce Assessment Understand who in your workforce will be eligible for Auto Enrolment prior to stagingAssessment and Automatic Enrolment of eligible employees*Continual Assessment of your workforce*

Configure postponementAllow postponement on staging dates*Allow postponement on start of employment*Allow postponement when an employee becomes eligible*

Day to Day Auto Enrolment Management Allow employee opt in/opt outsTermination of automatic enrolment pensionsBulk amendments (phased contribution levels & pension provider movement)

* can be configured to run automatically as you run your payroll

How Can QTAC Help How Can QTAC Help

Employee Communications Create the correct, personalised communications for each of your employees*Automatically prepare communications to all of your employees

Pension Provider CommunicationsAutomatically manage Pensions data and paymentsPension file templates for new members and contributions A user friendly configurable pension provider communications tool that will allow you to create the correct data files in the correct file format, allowing you to securely upload to your Pensions portal or send to your Pensions Provider

Auto Enrolment Audit Allows you to view history of Auto Enrolment activity by employee

* can be configured to run automatically as you run your payroll

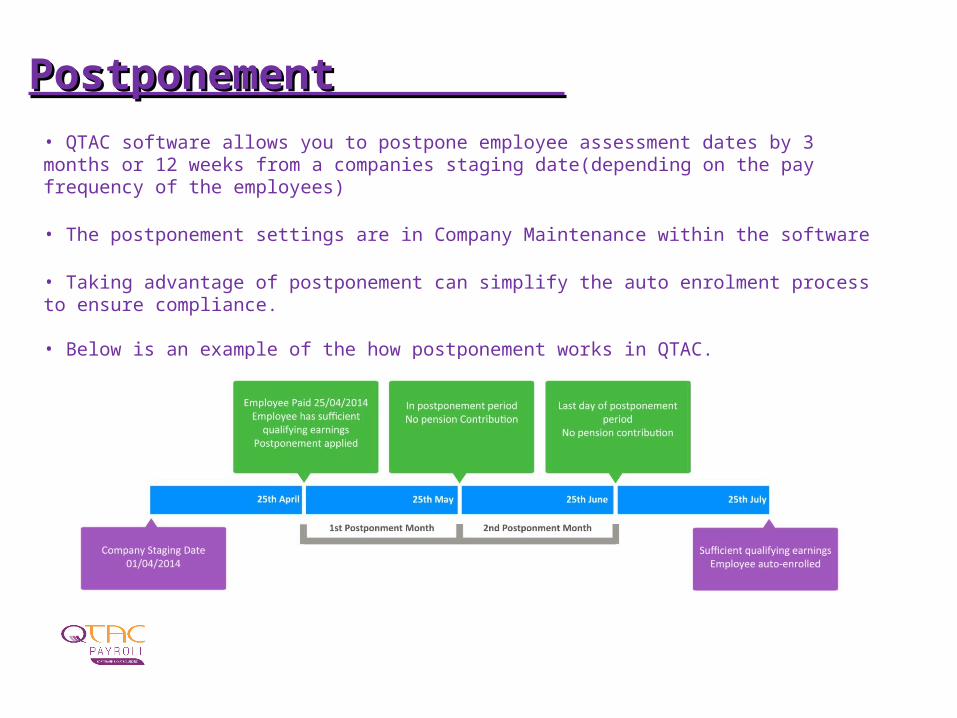

Postponement Postponement • QTAC software allows you to postpone employee assessment dates by 3 months or 12 weeks from a companies staging date(depending on the pay frequency of the employees)

• The postponement settings are in Company Maintenance within the software

• Taking advantage of postponement can simplify the auto enrolment process to ensure compliance. • Below is an example of the how postponement works in QTAC.

FAQ’s around postponement FAQ’s around postponement

Q – Toby is a new employee. His probation is 3 months. Can postponement be used for the new employees?A – Yes postponement can be used in this situation as long as it is communicated to the employee.

Q – I take on seasonal workers. Can I use postponement?A – Yes postponement can be used in this situation as long as it is communicated.

Q – I have already used postponement for Toby. But I have extended his probation period. Can I postpone him for a further 3 months?A – Toby must be reassessed on the last day of postponement, and if he meets the criteria of an eligible jobholder he must be automatically enrolled.

7 Key Steps to Success 7 Key Steps to Success 1. Know your staging date - when you ActThe date that the new law applies to your company is known as your staging date. This date is determined by the size of your largest PAYE scheme as at 1st April 2012. Companies that have PAYE schemes that are shared by multiple employers will have the same staging date in most cases. For multiple companies within one organisation, it is the largest employer that will dictate the staging date and this date will apply to all companies of that PAYE scheme.For more information about staging dates, please visit http://www.thepensionsregulator.gov.uk/employers/what-is-my-staging-date.aspx 2. Assess your workforceWorkers who will need to be automatically enrolled in a pension scheme are called ‘eligible jobholders’. An eligible jobholder is:• Aged between 22 and state pension age• Working or ordinarily working in the UK• Earning above £9,440 (currently) or £10,000 (from April 2014) 3. Review your pension arrangementsReview your existing pension scheme: If you have an existing pension scheme for your workers, you may wish to consider enrolling all eligible jobholders into this scheme. To do this, your existing scheme will need to qualify as an automatic enrolment scheme.To be a qualifying scheme, minimum contributions must be made or it must provide a minimum rate at which benefits will build up. A scheme suitable for automatic enrolment must also not:• Impose barriers to joining the scheme, such as probationary periods or age limits for members• Require staff to make an active choice to join or take other action prior to joining• Require the provision of extra information in order to stay in the scheme

4. Communicate the changes to all your workersYou must inform all your workers in writing about the changes detailing how they are affected by the changes. This communication must be provided in writing (which can include being sent by email) and must be specific to the individual.The duty is on the employer to provide the right information to the right individual, at the right time. 5. Automatically enrol your eligible job holdersThere is a process that you will need to follow in order to make an eligible jobholder a member of an automatic enrolment pension scheme. Certain information about your eligible jobholders will also need to be supplied to pension scheme managers for example at specific points in the process. 6. Register with The Pensions Regulator and Keep recordsYou are required to inform The Pension Regulator how you have fulfilled your new automatic enrolment duties by registering this information online shortly after your staging date. You will also need to maintain specified records about enrolled workers, their status within the scheme, the payment of contributions and the qualifying scheme itself. 7. Contribute to your workers’ pensionsStarting on your staging date, you must contribute to your chosen pension scheme on behalf of your workers. The minimum contribution rates that an employer must pay into their workers’ pension scheme will be introduced gradually over a 6 year period (from 2012 to 2018). This is known as ‘phasing’. The minimum overall contribution will be 2% rising to 8%. Where your employee doesn’t contribute towards the pension, the employer will be expected to contribute the full minimum amount.Phasing will apply to most, though not all, types of pension scheme (your work place pension scheme provider will be able to tell you if phasing applies to you).

7 Key Steps - continued7 Key Steps - continued

Questions and AnswersQuestions and Answers

Our next webinar’s will cover:Our next webinar’s will cover:

Managing Auto Enrolment with QTAC software Managing Auto Enrolment with QTAC software on 14on 14thth August August

Auto Enrolment for Accountants & Payroll Bureaux Auto Enrolment for Accountants & Payroll Bureaux on 28on 28thth August August

Stay up to date with the latest newsStay up to date with the latest newson Auto Enrolment on Auto Enrolment

You will be emailed a copy of the these slides & You will be emailed a copy of the these slides & thank you for listening thank you for listening