INTRODUCTION - Bangladesh Bank · Dutch Bangla Bank Ltd. 14. Mercantile Bank Ltd. ... bills mainly...

31

i INTRODUCTION After liberation, the banks operating in Bangladesh (except those incorporated abroad) were nationalised. These banks were merged and grouped into six commercial banks. Of the total six commercial banks, Pubali Bank Ltd. and Uttara Bank Ltd. were subsequently transferred to the private sector with effect from January 1985. Rupali Bank was transferred as public limited company from December1986. The rest three State Owned Banks were operating as public limited company from the quarter October- Govt. owned specialised banks were renamed as Bangladesh Krishi Bank and Bangladesh Shilpa Bank. In March 1987 Bangladesh Krishi Bank was bifurcated and another specialised bank emerged as Rajshahi Krishi Unnayan Bank (RAKUB) for Rajshahi Division. Bank of Small Industries & Commerce Bangladesh Ltd. (BASIC) started its operation as a private bank from September 1988. Later on BASIC was brought under direct control of the Government and was reckoned to as a specialised bank with effect from June 1993. From July 1995 again the BASIC was categorised as a private bank. In 1997, Government decided to treat this bank as a Specialised bank again. So in this booklet, the BASIC has been treated as a Specialised bank. Bangladesh Shilpa Bank(BSB) & Bangladesh Shilpa Rin Sangstha(BSRS) merged and renamed as Bangladesh development Bank Limited(BDBL) from the quarter January- Standard Chartered Grindlays Bank was merged with Standard Chartered Bank during the Quarter (January-March, 2003). American Express Bank also merged with Standard Chartered Bank during the quarter (October-December, 2005).The Oriental Bank Ltd. an Islamic private bank was renamed as ICB Islamic Bank Ltd. from the quarter (April-June, 2008). Credit Agricole Indosuez, a foreign private bank is renamed as Commercial Bank of Ceylon Ltd. from the quarter (October- December, 2003). Shamil Bank is renamed as Bank Al-Falah Ltd. from the quarter (April- June, 2005). Arab Bangladesh Bank Ltd is renamed as AB Bank Ltd from the quarter (January-March, 2008) and Social Investment Bank Ltd is renamed as Social Islami Bank Ltd from the quarter (April-June, 2009). It is mentioned that First Security Bank Ltd has started its operation according to Islamic Sariah from the quarter (January- Shahjalal Bank Ltd. has started its operation according to Islamic Sariah from the quarter April-June - and EXIM Bank Ltd has also started its operation according to Islamic Sariah from the quarter (July-September, 2004). The branches of foreign banks operating in Bangladesh are being treated as foreign private banks. Among all fourth generation Scheduled ICULTURE AND started their operation from the quarter April- June, 2013. MODHUMOTI BANK om the quarter July-September, 2013 have started their operation from the quarter October-December, 2013. It is mentioned that Union Bank Ltd. based on Islamic Sariah. All such banks operating in Bangladesh with different paid-up capital and reserves having a minimum of an aggregate value of Tk. 50 lacs and conducting their affairs to the satisfaction of the Bangladesh Bank have been declared as scheduled banks in terms of section 37(2) of Bangladesh Bank Order 1972. In terms of section 13 of Bank Company Act, 1991, the minimum aggregate value was Tk. 20 crores. From 30 th 2003 it was Tk 100 crores. From 8 th 2007 it was Tk. 200 crores . From 11 th 2011, it has been raised at the minimum of Tk. 400 crores ( as per Circular Letter No. BRPD (R-1) 717/ 2008 - 511 dated August 12, 2008).

Transcript of INTRODUCTION - Bangladesh Bank · Dutch Bangla Bank Ltd. 14. Mercantile Bank Ltd. ... bills mainly...

i

INTRODUCTION

After liberation, the banks operating in

Bangladesh (except those incorporated abroad)

were nationalised. These banks were merged

and grouped into six commercial banks. Of the

total six commercial banks, Pubali Bank Ltd.

and Uttara Bank Ltd. were subsequently

transferred to the private sector with effect from

January 1985. Rupali Bank was transferred as

public limited company from December1986.

The rest three State Owned Banks were

operating as public limited company from the

quarter October-

Govt. owned specialised banks were renamed as

Bangladesh Krishi Bank and Bangladesh Shilpa

Bank. In March 1987 Bangladesh Krishi Bank

was bifurcated and another specialised bank

emerged as Rajshahi Krishi Unnayan Bank

(RAKUB) for Rajshahi Division. Bank of Small

Industries & Commerce Bangladesh Ltd.

(BASIC) started its operation as a private bank

from September 1988. Later on BASIC was

brought under direct control of the Government

and was reckoned to as a specialised bank with

effect from June 1993. From July 1995 again

the BASIC was categorised as a private bank. In

1997, Government decided to treat this bank as

a Specialised bank again. So in this booklet, the

BASIC has been treated as a Specialised bank.

Bangladesh Shilpa Bank(BSB) & Bangladesh

Shilpa Rin Sangstha(BSRS) merged and

renamed as Bangladesh development Bank

Limited(BDBL) from the quarter January-

Standard Chartered Grindlays

Bank was merged with Standard Chartered

Bank during the Quarter (January-March,

2003). American Express Bank also merged

with Standard Chartered Bank during the

quarter (October-December, 2005).The Oriental

Bank Ltd. an Islamic private bank was renamed

as ICB Islamic Bank Ltd. from the quarter

(April-June, 2008). Credit Agricole Indosuez, a

foreign private bank is renamed as Commercial

Bank of Ceylon Ltd. from the quarter (October-

December, 2003). Shamil Bank is renamed as

Bank Al-Falah Ltd. from the quarter (April-

June, 2005). Arab Bangladesh Bank Ltd is

renamed as AB Bank Ltd from the quarter

(January-March, 2008) and Social Investment

Bank Ltd is renamed as Social Islami Bank Ltd

from the quarter (April-June, 2009). It is

mentioned that First Security Bank Ltd has

started its operation according to Islamic Sariah

from the quarter (January-

Shahjalal Bank Ltd. has started its operation

according to Islamic Sariah from the quarter

April-June

-

and EXIM Bank Ltd has also started

its operation according to Islamic Sariah from

the quarter (July-September, 2004). The

branches of foreign banks operating in

Bangladesh are being treated as foreign private

banks.

Among all fourth generation Scheduled

ICULTURE AND

started their operation from the quarter April-

June, 2013.

MODHUMOTI BANK

om the

quarter July-September, 2013

have started their

operation from the quarter October-December,

2013. It is mentioned that Union Bank Ltd.

based on Islamic Sariah.

All such banks operating in Bangladesh

with different paid-up capital and reserves

having a minimum of an aggregate value of Tk.

50 lacs and conducting their affairs to the

satisfaction of the Bangladesh Bank have been

declared as scheduled banks in terms of section

37(2) of Bangladesh Bank Order 1972. In terms

of section 13 of Bank Company Act, 1991, the

minimum aggregate value was Tk. 20 crores.

From 30th 2003 it was Tk 100 crores.

From 8th 2007 it was Tk. 200 crores .

From 11th 2011, it has been raised at

the minimum of Tk. 400 crores ( as per Circular Letter No. BRPD (R-1) 717/ 2008 - 511 dated

August 12, 2008).

ii

The names of the scheduled banks

whose operations are recorded in this

volume are as below:

A. STATE OWNED BANKS:

1. Agrani Bank Limited.

2. Janata Bank Limited.

3. Rupali Bank Limited.

4. Sonali Bank Limited.

B. SPECIALSED BANKS:

1. Bangladesh Krishi Bank.

2. Rajshahi Krishi Unnayan Bank.

3. Bank of Small Industries and

Commerce Bangladesh Ltd.

4. Bangladesh Development

Bank Limited.

C. PRIVATE BANKS:

a) Foreign Banks:

1. Standard Chartered Bank

2. State Bank of India

3. Habib Bank Ltd.

4. Citi Bank, N.A.

5. Commercial Bank of Ceylon Ltd.

6. National Bank of Pakistan

7. Woori Bank

8. The Hong Kong & Shanghai Banking

Corporation Ltd.

9. Bank Al-Falah Ltd.

b) Private Banks (Incorporated in

Bangladesh excluding Islamic

Banks):

1. AB Bank Ltd.

2. National Bank Ltd.

3. The City Bank Ltd.

4. International Finance Investment and

Commerce Bank Ltd.

5. United Commercial Bank Ltd.

6. Pubali Bank Ltd.

7. Uttara Bank Ltd.

8. Eastern Bank Ltd.

9. National Credit and Commerce Bank

Ltd.

10. Prime Bank Ltd.

11. Southeast Bank Ltd.

12. Dhaka Bank Ltd.

13. Dutch Bangla Bank Ltd.

14. Mercantile Bank Ltd.

15. Standard Bank Ltd.

16. One Bank Ltd.

17. Bangladesh Commerce Bank Ltd.

18. Mutual Trust Bank Ltd.

19. Premier Bank Ltd.

20. Bank Asia Ltd.

21. Trust Bank Ltd.

22. Jamuna Bank Ltd.

23. BRAC Bank Ltd.

24. NRB Commercial Bank Ltd.

25. South Bangla Agriculture and

Commerce Bank Ltd.

26. Meghna Bank Ltd.

27. Midland Bank Ltd.

28. The Farmers Bank Ltd.

29. NRB Bank Ltd.

30. Modhumoti Bank Ltd.

31. NRB Global Bank Ltd.

c) Islamic Banks

1. Islami Bank Bangladesh Ltd.

2. ICB Islamic Bank Ltd.

3. Al-Arafah Islami Bank Ltd.

4. Social Islami Bank Ltd.

5. EXIM Bank Ltd.

6. First Security Islami Bank Ltd.

7. Shahjalal Islami Bank Ltd.

8. Union Bank Ltd.

iii

The banks play an important role in the

economy of the country. Bangladesh Bank

has been collecting, compiling and publishing

statistics on scheduled banks for the use of

researchers, planners and policy makers.

The statistical tables contained in this

issue have been prepared from the returns

submitted by the individual bank branches of

scheduled banks as on the last day of the

quarter ending 30th

June 2014. At the end of

the period under study the total number of

reported bank branches including Head

Offices, Islamic Windows and SME service

centers stood at 8886, which contains only 76

branches of foreign banks.

For useful presentation of data, banks

have been classified into several groups viz.

All Banks

Specialised Banks Foreign Banks

(Including Islamic Banks). A

has been introduced consisting of seven banks

(Incorporated in Bangladesh), run on the basis

of Islamic Sariah with effect from quarter

January-March 1998. These banks are 1)

Islami Bank Bangladesh Ltd. 2) ICB Islamic

Bank Ltd. 3) Al-Arafah Islami Bank Ltd. 4)

Social Islami Bank Ltd. 5) EXIM Bank Ltd.

6) Shahjalal Islami Bank Ltd. 7) First Security

Islami Bank Ltd. and 8) Union Bank Ltd. The

publication provides a detailed analysis of

bank deposits (excluding inter-bank)

by Rates of Interest & Types ,

; outstanding advances

(excluding inter-bank transactions) mainly

by Rates of Interest &

Securities by Size of

Account etc. and

bills mainly in the form of by .

From the very inception, the

were being

collected and published on quarterly basis.

Later on since December, 1988 the data had

been collected on half yearly basis and

published on annual basis ending December

every year. Subsequently, from December

1990 the data were collected on quarterly

basis but published on annual basis. Then it

was decided to publish again on quarterly

basis from June 1992 and the present

publication follows as a sequel to the change

in the policy decision.

The role of agricultural credit in

fostering the economy of the country has

gained importance nowadays. To this end in

mind agricultural credit statistics time series

data were collected and presented pertaining

to the period from 1984-85 to 2013-14.

The figures published in this booklet

may differ from those contained in the

statement of position of Scheduled Banks

released each week by the Bangladesh Bank

due to difference in timing and coverage.

From the quarter July-September,

2013, the Scheduled Banks were instructed

to follow the Guidelines to Fill in the

Banking Statistics Returns SBS-1, SBS-2 &

SBS-3 fifth edition, published in July 2013.

In this brochure, all statistical tables have

been prepared on the basis of returns,

submitted by the scheduled banks as per the

booklet, published in July 2013.

For taking into account, the

remittances (in Foreign Currency) by the

Wage earners abroad, two types of deposits:

Foreign Currency Deposits have been

introduced from the quarter ending on

December, 2001.

iv

EXPLANATORY NOTES TO THE TABLES

Table-1: Divisions/Districts wise

distribution of per capita

Deposits/Advances on the basis of

population: The table furnishes the

division/district wise distribution of

population, number of reporting bank

branches, per capita deposits and per capita

advances.

Table-2 to 7: Deposits Distributed by Types

of Accounts: These tables show the

classification of total demand and time

liabilities of scheduled banks (excluding inter-

bank) into fourteen broad types such as (a)

Current and Cash Credit Account (credit

balances) Deposits, (b) Deposits

withdrawable on Sight, (c) Savings Deposits,

(d) Convertible Taka Accounts of Foreigners,

(e) Foreign Currency Accounts, (f) Wage

Currency Deposits, (h) Special Notice

Deposits, (i) Fixed Deposits, (j) Recurring

Deposits, (k) Margin Deposits (Foreign

Currency/Taka), (l) Special Purpose Deposits,

(m) Negotiable Certificates of Deposits &

Promissory Notes and (n) Restricted

(Blocked) Deposits.

a) Current and Cash Credit Accounts

Deposits: These are of the nature of

demand deposits and comprise current

accounts and credit balances of cash

credit accounts. Generally no interest is

allowed on these deposits. These deposits

are to be reported in code no.-100 as

usual but from the quarter, October-

December, 2005 some banks have started

paying interest on this type of account.

This later type is to be reported in code

no.-105. These accounts have chequing

facilities and balances are transferable.

b) Deposits Withdrawable on Sight: This

item includes all deposits which cannot

be transferred through cheques but are

withdrawable on demand such as

overdue Fixed Deposits Accounts,

unclaimed balances, payment orders,

telephonic transfers, mail transfers,

demand drafts, unclaimed dividends and

draft payable accounts, Earnest Money of

Tenders/Quotations etc.

c) Saving Deposits Account: Deposit on

these accounts is self-explanatory and

generally emanates from the individuals.

A portion, varying from time to time, of

savings deposits constitutes demand

deposits. From 1st July, 1996 11% of

savings deposits was regarded as demand

deposits and from 1st July 1997, it was

10%. At present from 24th

June, 2007,

9% of savings deposits has been being

regarded as demand deposits.

d) Convertible Taka Account of

Foreigners: Convertible Taka account of

foreigners is deposits of foreign

individuals, embassies, foreign

Governments and international agencies,

all of which have non-resident status

under foreign exchange regulations.

e) Foreign Currency Accounts: Foreign

currency accounts consist of the deposits

(in foreign currency) of the foreigners

(residing abroad or in Bangladesh) and

foreign missions & their expatriate

employees.

f) The

depositors of these accounts are the

Bangladeshi nationals, who work abroad.

These accounts are fed by the remittances

(in foreign currency) from these persons.

Deposits in NFCD accounts along with

interest thereon are also reported in these

accounts. .

g) Resident Foreign Currency Deposits: Persons ordinarily residing in Bangladesh

may open this account with foreign

v

exchanges brought in at the time of their

return from travel abroad. Deposits or

remittances from persons, working in

Bangladesh missions abroad and

Retention quota deposits by the exporters

are also included in these deposits.

h) Special Notice Deposits: This item

includes the deposits that are deposited

for a period ranging from 7 days to 89

days. These types of liabilities are

payable on Special notice or after a

specified period other than the fixed

deposits. Some of these types of deposits

are of the nature of time deposits.

i) Fixed Deposits: These are reclassified

by period of maturity and are exclusively

time deposits.

j) Recurring Deposits: According to this

scheme the investors would be required

to deposit their money limited to

maximum of Tk. 500 per month for a

period of 10 years and 20 years. Interest

on the invested amount will be

compounded at the rate of 15% and

calculated on yearly basis. Deposits

Pension schemes are of the nature of time

deposits and it was introduced in 1983.

Later on Deposits Scheme e.g. APS,

SDPS, SPS, PDS, PSS etc. and Hajj

Deposits Schemes have been introduced

by the various Banks with various

interest.

k) Margin Deposits (Foreign

Currency/Taka): Equivalent Taka of

margin on letters of Credit and margins

on guarantee (in Taka & Foreign

Currency) are included in this item.

l) Special Purpose Deposits: This item

comprises employee

funds/pension Accounts, contribution

towards insurance funds, Hajj Deposits,

Staff guarantee/Security funds, Security

Deposits, Gift Certificate Deposits,

Sundry deposits, Surcharge and

Development charge etc.

m) Negotiable Certificates of Deposits and

Promissory Notes:

Negotiable certificates of deposits are

bearer certificate deposits and are of

nature of time deposits.

n) Restricted (Blocked) Deposits: The

balances of restricted (blocked) deposits

are reported in this item against Private

Sector. According to Special Law, the

competent authority blocks these

accounts. In blocked period, the

depositors cannot withdraw their

deposits.

Table 8 to 13. Deposits Distributed by

Divisions/Districts and Areas (Urban &

Rural): These tables show the district-wise

distribution of deposits of urban and rural

regions of the country. It is mentioned that the

transaction of the branches in municipal area

is treated as urban area transaction (deposits

or advances as the case may be) while the

transaction of the branches located out-side

the municipal area is regarded as rural area

transaction (deposits or advances).

Table 14 to 19: Deposits Distributed by

Sectors and Types: These Tables provide a

break up of deposits by different sectors of

deposits mentioned in the paragraph number

two.

vi

Table 20 to 25: Deposits Distributed by

Rates of Interest/Profit and Types: These

tables show the rates of interest allowed by

the scheduled banks on different types of

deposits. No interest is allowed on current

deposits (without interest, Code no.-100) and

deposits withdrawable on sight while interest

is allowed on current deposits (with interest,

Code no.-105), savings deposits, fixed

deposits, pension scheme deposits and foreign

currency accounts of non-residents and

residents. The rate of interest varies from time

to time. The amount of deposits against

bills payables such as MT, DD, TT,

outstanding drafts etc. Depositors will have

the option for withdrawing interest

accumulated every twelve months or can have

the interest with the principal to be

compounded in case of maturity exceeding

one year. Profit/Loss is applicable in the cases

of Islamic Banks (Islami Bank Bangladesh

Ltd., ICB Islamic Bank Ltd., Al-Arafah

Islami Bank Ltd., Social Islami Bank Ltd.,

EXIM Bank Ltd, First Security Islami Bank

Ltd., Shahjalal Islami Bank Ltd. and Union

Bank Ltd.).

Table 26 to 31: Deposits Distributed by

Size of Accounts: The Statistics of number of

Accounts and corresponding amount falling

within specified groups are not based

exclusively on individual accounts. As the

number of accounts is considerably large, the

respondents have the option to combine the

accounts and amount in such cases when the

types of deposits, the category of depositors

and the rates of interest allowed thereon are

the same. In such cases it is not the actual size

of components but the average size of the

group that determines the class to which it

belongs. Notwithstanding the existence of an

element of statistical errors, it is believed that

the estimates would not differ significantly

from the actual position.

Table 32: Deposits Distributed by Size of

Accounts and Sectors: The Tables provide a

break up of deposits by size of accounts and

sector.

Table 33: Deposits Distributed by Selected

Thanas: The statistics show the distribution

of deposits in the leading thanas of the

country and those have been presented in the

descending order of magnitude of deposits.

Table 34: Debits to Deposits Accounts and

Turnover: The table shows debits to various

types of deposit accounts during the period

under review. This also includes co-efficient

of turnover by relating debits to average

amounts of deposits.

Table 35 to 40: Advances Classified by

Securities: These tables show the break-up of

scheduled banks advances (excluding

interbank) by types of securities pledged or

hypothecated.

Table 41 to 46: Advances Classified by

Economic Purposes: These tables show the

advances made by scheduled banks to

different economic purposes for which the

borrowers borrow. If a borrower pursues more

than one profession the classification is done

in accordance with his major calling.

Table 47 to 52: Advances Classified by

Rates of Interest and Securities: These

tables give the rates of interest charged by the

scheduled banks on various types of securities

as well as clean advances. Advances to

Classified advances (Bad/ Loss) (c) Advances

associated with clearing disputes etc.

Table 53: Advances Classified by Selected

Thanas: This table shows the classification of

advances in the leading thanas of the country

and those have been presented in the

descending order of magnitude of advances.

vii

Table 54: Advances Classified by Size of

Accounts and Economic Groups: The table

provides statistics on advances classified by

size of accounts and economic groups. The

respondents can group those accounts

together where the securities, the economic

purpose, the category of borrowers and the

rates of interest are the same. As a result the

size of distribution suffers from a similar

limitation as its analogy in deposits.

Table 55 to 60: Advances Classified by Size

of Accounts: These tables provides statistics

on advances classified by size of accounts.

Table 61: Advances Classified by Major

Economic Purposes and Sectors: The table

provides a break-up of advances classified by

major economic purposes to public and

private sectors.

Table 62 to 67: Advances Classified by

Division / Districts and Areas (Urban /

Rural): These tables show the district-wise

classification of advances of urban and rural

regions of the country.

Table 68: Advances Classified by Size of

Accounts and Sectors: The table provides

statistics on advances classified by size of

accounts and sector.

Table 69 to 74: Advances Classified by

Rates of Interest and Major Economic

Purposes: These tables provide rates of

interest charged by the scheduled banks on

advances for different economic purposes.

Table 75 to 80: Agricultural Credits

Statistics.

Table 81 to 86: Classification of Bills

purchased and discounted: The statement

provides an account of bills purchased and

discounted by major economic purposes of

drawees. Along with the corresponding

statement on advances the statistics provide

information on the structure of bank credit.

Table 87: Classification of Bills by sectors.

viii

A REVIEW ON DEPOSITS AND ADVANCES OF SCHEDULED BANKS

(AS ON END JUNE, 2014)

Total deposit liabilities (excluding

interbank items) of the scheduled banks increased

by Tk.27172.79 crores or 4.37% to Tk. 649440.02

crores during the quarter April-June, 2014 as

compared to increases of Tk. 11736.69 crores or

1.92% and Tk. 27220.01 crores or 5.00 % in the

previous quarter (January-March, 2014) and the

corresponding quarter (April-June, 2013) of the

last year respectively. The increase in deposits

during the quarter was due to increases in urban

deposits by Tk. 19346.91 crores or 3.80% to Tk.

528490.05 crores and in rural deposits by

Tk. 7825.88 crores or 6.92% to Tk. 120949.97

crores. The share of urban deposits to total

deposits at the end of the quarter April-June, 2014

was 81.38% as compared to 81.82% at the end of

the preceding quarter (January-March, 2014) and

81.98% at the end of the corresponding quarter

(April-June, 2013) of the last year. Bank deposits

registered an increase of Tk. 77332.34 crores or

13.52% from end June, 2013 to June, 2014 as

compared to an increase of Tk. 85700.47 crores or

17.62% from end June, 2012 to end June, 2013.

Banks' Advances:

advances increased by Tk.

18686.71crores or 4.14% to Tk. 469583.21 crores

during the quarter April-June, 2014 as compared

to increases of Tk. 7052.09 crores or 1.59% and

Tk. 10755.89 crores or 2.60% respectively during

the preceding quarter (January-March, 2014) and

the corresponding quarter (April-June, 2013) of

the last year. Bank advances in urban areas

increased by Tk. 17001.41 crores or 4.19%

to Tk. 423226.68 crores and in rural areas

increased by Tk. 1685.30 crores or 3.77% to Tk

46356.53 crores during the quarter under review.

Bank advances exhibited an increase by Tk.

44778.74 crores or 10.54% from end June, 2013

to end June, 2014 as compared to an increase of

Tk. 38871.33 crores or 10.07% from end June,

2012 to end June, 2013.

ix

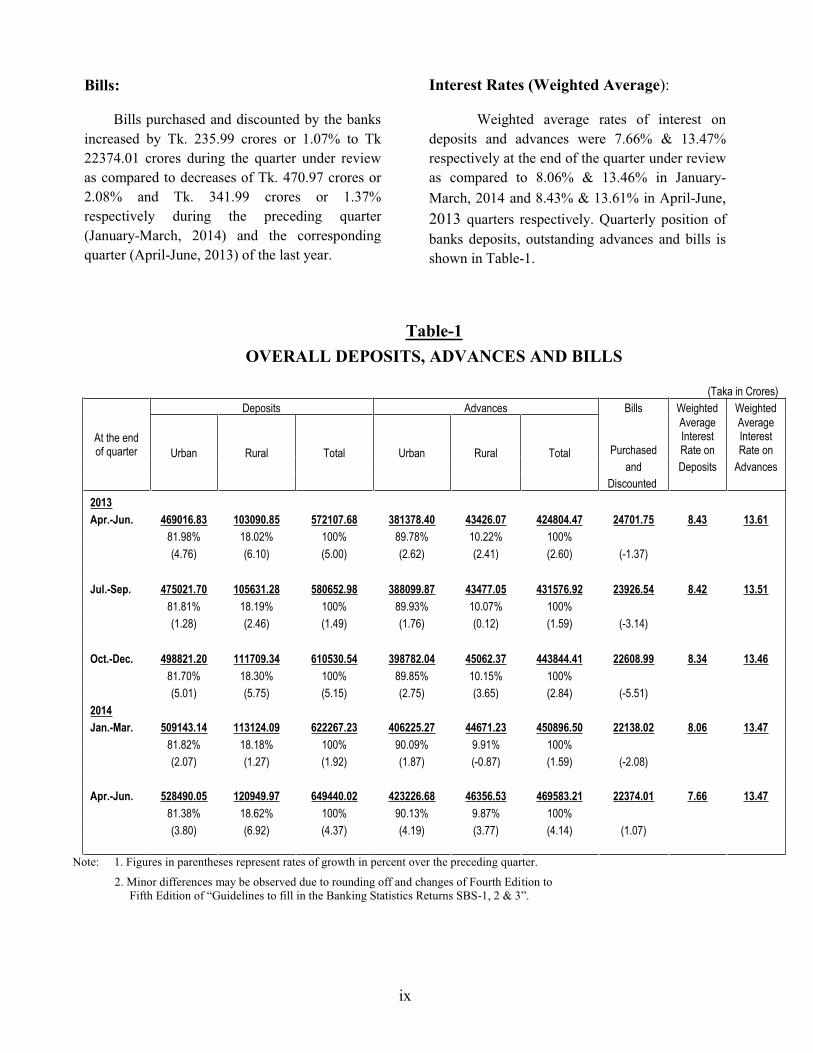

Bills:

Bills purchased and discounted by the banks

increased by Tk. 235.99 crores or 1.07% to Tk

22374.01 crores during the quarter under review

as compared to decreases of Tk. 470.97 crores or

2.08% and Tk. 341.99 crores or 1.37%

respectively during the preceding quarter

(January-March, 2014) and the corresponding

quarter (April-June, 2013) of the last year.

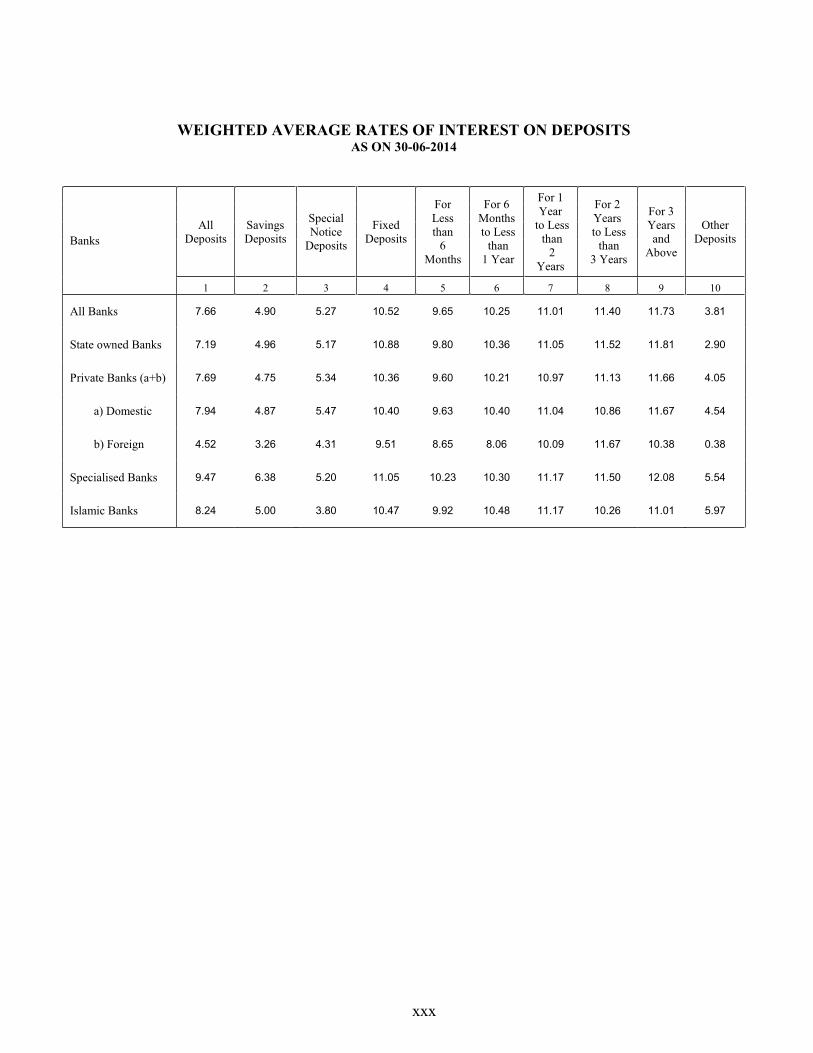

Interest Rates (Weighted Average):

Weighted average rates of interest on

deposits and advances were 7.66% & 13.47%

respectively at the end of the quarter under review

as compared to 8.06% & 13.46% in January-

March, 2014 and 8.43% & 13.61% in April-June,

2013 quarters respectively. Quarterly position of

banks deposits, outstanding advances and bills is

shown in Table-1.

Table-1

OVERALL DEPOSITS, ADVANCES AND BILLS

(Taka in Crores)

At the end of quarter

Deposits Advances Bills Weighted Weighted

Urban Rural Total Urban Rural Total Purchased

Average Interest Rate on

Average Interest Rate on

and Deposits Advances

Discounted

2013

Apr.-Jun. 469016.83 103090.85 572107.68 381378.40 43426.07 424804.47 24701.75 8.43 13.61

81.98% 18.02% 100% 89.78% 10.22% 100%

(4.76) (6.10) (5.00) (2.62) (2.41) (2.60) (-1.37)

Jul.-Sep. 475021.70 105631.28 580652.98 388099.87 43477.05 431576.92 23926.54 8.42 13.51

81.81% 18.19% 100% 89.93% 10.07% 100%

(1.28) (2.46) (1.49) (1.76) (0.12) (1.59) (-3.14)

Oct.-Dec. 498821.20 111709.34 610530.54 398782.04 45062.37 443844.41 22608.99 8.34 13.46

81.70% 18.30% 100% 89.85% 10.15% 100%

(5.01) (5.75) (5.15) (2.75) (3.65) (2.84) (-5.51)

2014

Jan.-Mar. 509143.14 113124.09 622267.23 406225.27 44671.23 450896.50 22138.02 8.06 13.47

81.82% 18.18% 100% 90.09% 9.91% 100%

(2.07) (1.27) (1.92) (1.87) (-0.87) (1.59) (-2.08)

Apr.-Jun. 528490.05 120949.97 649440.02 423226.68 46356.53 469583.21 22374.01 7.66 13.47

81.38% 18.62% 100% 90.13% 9.87% 100%

(3.80) (6.92) (4.37) (4.19) (3.77) (4.14) (1.07)

Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter.

2. Minor differences may be observed due to rounding off and changes of Fourth Edition to

-

x

Banks' Credit:

Total credit of the Scheduled banks

increased by Tk 18922.72 crores or 4.00% to Tk.

491957.22 crores during the quarter under review

as compared to increases of Tk. 6581.10 crores or

1.41% and Tk. 10413.90 crores or 2.37%

respectively during the preceding quarter

(January-March, 2014) and the corresponding

quarter (April-June, 2013) of the last year.

Banks' Investment:

The Scheduled banks' investment

increased by Tk. 8940.34 crores or 5.36% to Tk.

175707.05 crores at the end of the quarter April-

June, 2014 as compared to increases of Tk.

5049.41 crores or 3.12% and Tk. 21156.59 crores

or 17.44% respectively during the

Preceding quarter (January-March, 2014) and

the corresponding quarter (April-June, 2013) of

the last year.

Borrowings from the Bangladesh Bank:

The Scheduled Banks' borrowings from

the Bangladesh Bank at the end of the quarter

under review decreased by Tk. 1059.25 crores or

16.09% to Tk. 5523.19 crores as compared to a

decrease of Tk. 62.47 crores or 0.94% and a

decrease of Tk. 369.20 crores or 3.77%

respectively during the preceding quarter

(January-March, 2014) and the corresponding

quarter (April-June, 2013) of the last year.

Quarterly position of the scheduled banks' credit,

investment and borrowings from the Bangladesh

Bank is shown in Table-2.

TABLE-2

BORROWING FROM BANGLADESH BANK

(Taka in Crores)

At the end Scheduled Banks' Credit Scheduled Banks' Investment Borrowings from

of quarter Advances Bills Total Govt. Others Total Bangladesh

Investment Bank

2013

Apr.-Jun 424804.47 24701.75 449506.22 120808.55 21651.34 142459.89 9436.81

94.50% 5.63% 100% 84.80% 15.20% 100%

(2.60) (-1.37) (2.37) (16.75) (21.44) (17.44) (-3.77)

Jul.-Sep. 431576.92 23926.54 455503.46 124799.82 22629.18 147429.00 8569.40

94.75% 5.25% 100% 84.65% 15.35% 100%

(1.59) (-3.14) (1.33) (3.30) (4.52) (3.49) (-9.19)

Oct.-Dec. 443844.41 22608.99 466453.40 133433.83 28283.47 161717.30 6644.91

95.15% 4.85% 100% 82.51% 17.49% 100%

(2.84) (-5.51) (2.40) (6.92) (24.99) (9.69) (-22.46)

2014

Jan.-Mar. 450896.50 22138.02 473034.50 142942.39 23824.32 166766.71 6582.44

95.32% 4.68% 100% 85.71% 14.29% 100%

(1.59) (-2.08) (1.41) (7.13) (-15.77) (3.12) (-0.94)

Apr.-Jun. 469583.21 22374.01 491957.22 149325.16 26381.89 175707.05 5523.19

95.45% 4.55% 100% 84.99% 15.01% 100%

(4.14) (1.07) (4.00) (4.47) (10.74) (5.36) (-16.09)

Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter.

2. Minor differences may be observed due to rounding off.

xi

Deposits by Category of Banks:

The increase of Tk. 27172.79 crores

or 4.37% in total deposit liabilities during the

quarter April-June, 2014 over the preceding

quarter January-March, 2014 was shared by

increases in Private banks by Tk. 18722.90 crores

or 4.76%, Specialised banks by Tk. 692.81 crores

or 2.03%, Islamic banks by Tk. 7033.55 crores or

6.20%, State Owned banks by Tk. 10392.48

crores or 6.53% and decrease in Foreign banks by

Tk.2635.40 crores or 7.35%. The net accretion in

deposits during the quarter under review over the

same quarter (April-June, 2013) of the last year

amounting to Tk. 77332.34 crores or 14.19% was

due to increase in deposits of State Owned banks

by Tk. 16920.80 crores or 11.95%, in

Private banks by 54642.05 crores or 15.93%, in

Specialised banks by Tk. 4487.30 crores or

16.38%, in Islamic banks by Tk. 19275.78 crores

or 20.11% and in Foreign banks by Tk. 1282.19

crores or 3.89%. Of the total deposits of Tk.

649440.02 crores at the end of the quarter under

review, the shares of State Owned banks,

Specialised banks, Foreign banks, Private banks

and Islamic banks were Tk. 169487.81 crores

(26.10%), Tk. 34873.63 crores (5.37%), Tk.

33198.09 crores (5.11%), Tk. 411880.49 crores

(63.42%) and Tk. 120477.36 crores (6.20%)

respectively. The position in respect of deposit

liabilities by category of banks is shown in Table-

3.

TABLE-3

DEPOSITS DISTRIBUTED BY CATEGORY OF BANKS

(Taka in Crores)

At the end State Specialised Foreign Private Banks Islamic All

of quarter owned Banks Banks (Including Banks Banks

Banks (Islamic Banks)

2013

Apr.-Jun. 152567.01 30386.33 31915.90 357238.44 101201.58 572107.68

26.67% 5.31% 5.58% 62.44% 17.69% 100%

(7.77) (10.94) (-3.25) (4.17) (5.60) (5.00)

Jul.-Sep. 153915.71 31206.72 33632.02 361898.53 102296.84 580652.98

26.51% 5.37% 5.79% 62.33% 17.62% 100%

(0.88) (2.70) (5.38) (1.30) (1.08) (1.49)

Oct.-Dec. 161039.92 33961.60 33997.10 381531.92 107821.65 610530.54

26.38% 5.56% 5.57% 62.49% 17.66% 100%

(4.63) (8.83) (1.09) (5.43) (5.40) (5.15)

2014

Jan.-Mar. 159095.33 34180.82 35833.49 393157.59 113443.81 622267.23

25.57% 5.49% 5.76% 63.18% 17.66% 100%

(-1.21) (0.65) (5.40) (3.05) (5.21) (1.92)

Apr.-Jun. 169487.81 34873.63 33198.09 411880.49 120477.36 649440.02

6.53% 2.03% -7.35% 63.42% 18.55% 100%

(26.10) (5.37) (5.11) (4.76) (6.20) (4.37)

Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter.

2. Minor differences may be observed due to rounding off.

xii

Deposits by Types of Accounts:

Breakdown by types of deposits

accounts revealed that the share of fixed

deposits decreased from 54.30% at the end of

the quarter January-March, 2014 to 53.81% at

the end of quarter April-June, 2014. The

amount of fixed deposits increased by Tk.

11567.57 crores or 3.42% to Tk. 349474.28

crores at the end of the quarter under review

as or compared to increases of Tk. 11738.55

crores or 3.60% and Tk. 14212.80 crores or

5.01% at the end of the preceding quarter

(January-March, 2014) and the corresponding

quarter (April-June, 2013) of the last year

respectively. The share of savings deposits to

total deposits increased from 16.28% on the

31st March, 2014 to 16.66% on the 30

th June,

2014. Deposits distributed by types of

accounts are shown in Table-4.

x

iii

TA

BL

E-4

DE

PO

SIT

S D

IST

RIB

UT

ED

BY

TY

PE

S O

F A

CC

OU

NT

S

(T

aka in

Cro

res)

At th

e end

C

urren

t S

avin

gs

Co

nvertib

le

Tak

a

Acco

unt o

f

Fo

reigners

Fo

reign

Curren

cy

Acco

unts

Wag

e

Earn

ers'

Dep

osits

Resid

ent

Fo

reign

Curren

cy

Dep

osits

Sp

ecial

No

tice

Dep

osits

Fix

ed

Recu

rring

O

ther

To

tal

of q

uarter

and

Cash

D

epo

sits D

epo

sits D

epo

sits D

epo

sits D

epo

sits

C

redit

Acco

unt

D

epo

sits

20

13

Ap

r.-J

un

. 4

54

68

.39

99

316

.22

12

43

.13

30

91

.41

13

56

.48

56

51

.48

45

796

.84

29

806

1.8

1

40

941

.78

3

11

80

.14

57

210

7.6

8

7

.95

%

17

.36

%

0.2

2%

0

.54

%

0.2

4%

0

.99

%

8.0

0%

5

2.1

0%

7

.16

%

5.4

5%

1

00

%

(8

.78)

(-0.9

1)

(10

.93

) (1

7.3

6)

(-16

.34

) (2

7.0

6)

(13

.04

) (5

.01)

(9.9

3)

(-0.7

9)

(5.0

0)

Ju

l.-Sep

. 4

26

18

.89

97

899

.42

10

63

.90

31

91

.14

95

9.9

2

52

04

.98

46

359

.41

31

158

0.3

7

39

380

.93

32

394

.02

58

065

2.9

8

7

.34

%

16

.86

%

0.1

8%

0

.55

%

0.1

7%

0

.90

%

7.9

8%

5

3.6

6%

6

.78

%

5.5

8%

1

00

%

(-6

.27

) (-1

.43

) (-1

4.4

2)

(3.2

3)

(-29

.23

) (-7

.90

) (1

.23)

(4.5

4)

(-3.8

1)

(3.8

9)

(1.4

9)

Oct.-D

ec.

46

315

.71

10

052

3.8

0

10

46

.16

38

74

.19

14

43

.38

51

73

.91

49

991

.07

32

616

8.1

6

43

133

.17

3

28

60

.99

61

053

0.5

4

7

.59

%

16

.46

%

0.1

7%

0

.63

%

0.2

4%

0

.85

%

8.1

9%

5

3.4

2%

7

.06

%

5.3

8%

1

00

%

(8

.67)

(2.6

8)

(-1.6

7)

(21

.40

) (5

0.3

6)

(-0.6

0)

(7.8

3)

(4.6

8)

(9.5

3)

(1.4

4)

(5.1

5)

20

14

Ja

n.-M

ar.

47

854

.05

10

130

3.7

2

10

99

.04

46

56

.93

20

32

.58

54

53

.34

45

772

.69

33

790

6.7

1

42

857

.67

3

33

30

.50

62

226

7.2

3

7

.69

%

16

.28

%

0.1

8%

0

.75

%

0.3

3%

0

.88

%

7.3

6%

5

4.3

0%

6

.89

%

5.3

6%

1

00

%

(3

.32)

(0.7

8)

(5.0

5)

(20

.20

) (4

0.8

2)

(5.4

0)

(-8.4

4)

(3.6

0)

(-0.6

4)

(1.4

3)

(1.9

2)

Ap

r.-J

un

. 5

04

17

.80

10

820

3.9

3

13

24

.76

25

67

.99

18

69

.85

49

88

.00

51

157

.00

34

947

4.2

8

42

714

.55

3

67

21

.86

64

944

0.0

2

7

.76

%

16

.66

%

0.2

0%

0

.40

%

0.2

9%

0

.77

%

7.8

8%

5

3.8

1%

6

.58

%

5.6

5%

1

00

%

(5

.36)

(6.8

1)

(20

.54

) (-4

4.8

6)

(-8.0

1)

(-8.5

3)

(11

.76

) (3

.42)

(-0.3

3)

(10

.17

) (4

.37)

No

te: 1. F

igu

res in p

arenth

eses represen

t rates of g

row

th in

percen

t over th

e preced

ing q

uarter.

2. M

ino

r differen

ces may

be o

bserv

ed d

ue to

roun

din

g o

ff and

chan

ges o

f Fou

rth E

ditio

n to

Fift

-

3. O

ther d

epo

sits inclu

de D

epo

sits With

draw

able o

n S

igh

t, Marg

in D

epo

sits, Sp

ecial Pu

rpo

se Dep

osits, N

ego

tiable C

ertificates of D

epo

sits & R

estricted D

epo

sits.

xiv

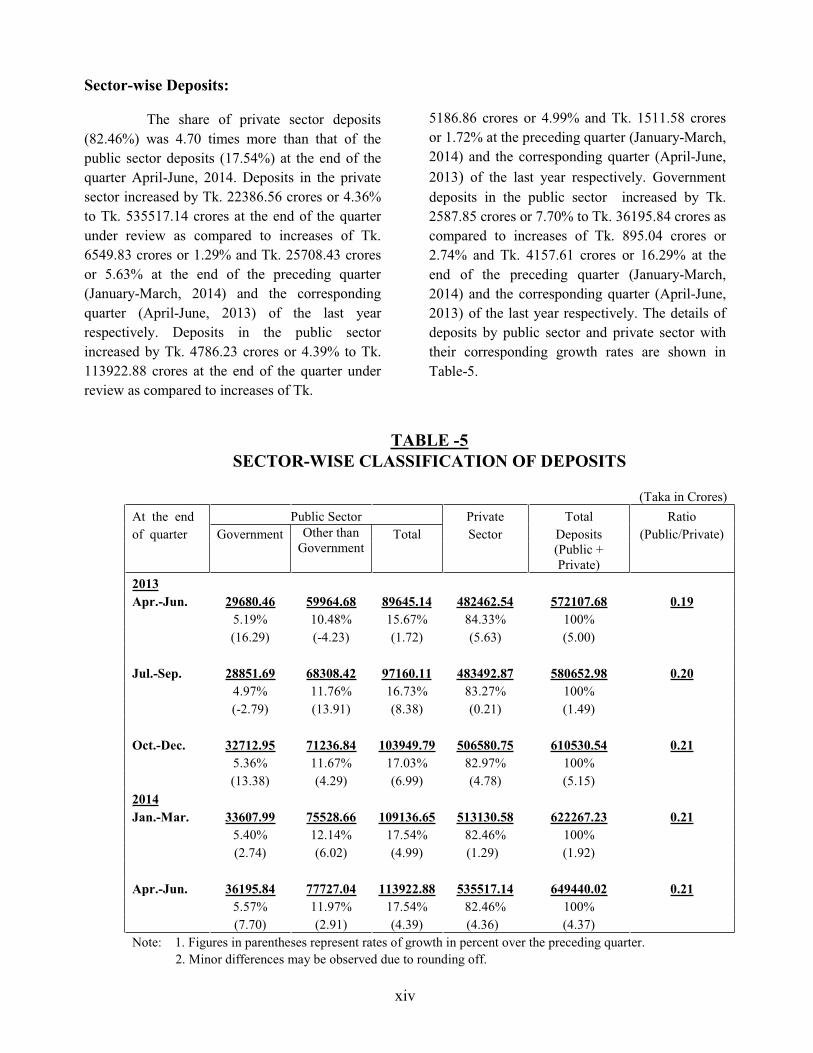

Sector-wise Deposits:

The share of private sector deposits

(82.46%) was 4.70 times more than that of the

public sector deposits (17.54%) at the end of the

quarter April-June, 2014. Deposits in the private

sector increased by Tk. 22386.56 crores or 4.36%

to Tk. 535517.14 crores at the end of the quarter

under review as compared to increases of Tk.

6549.83 crores or 1.29% and Tk. 25708.43 crores

or 5.63% at the end of the preceding quarter

(January-March, 2014) and the corresponding

quarter (April-June, 2013) of the last year

respectively. Deposits in the public sector

increased by Tk. 4786.23 crores or 4.39% to Tk.

113922.88 crores at the end of the quarter under

review as compared to increases of Tk.

5186.86 crores or 4.99% and Tk. 1511.58 crores

or 1.72% at the preceding quarter (January-March,

2014) and the corresponding quarter (April-June,

2013) of the last year respectively. Government

deposits in the public sector increased by Tk.

2587.85 crores or 7.70% to Tk. 36195.84 crores as

compared to increases of Tk. 895.04 crores or

2.74% and Tk. 4157.61 crores or 16.29% at the

end of the preceding quarter (January-March,

2014) and the corresponding quarter (April-June,

2013) of the last year respectively. The details of

deposits by public sector and private sector with

their corresponding growth rates are shown in

Table-5.

TABLE -5

SECTOR-WISE CLASSIFICATION OF DEPOSITS

(Taka in Crores)

At the end Public Sector Private Total Ratio

of quarter Government Other than

Government Total Sector Deposits (Public/Private)

(Public +

Private)

2013

Apr.-Jun. 29680.46 59964.68 89645.14 482462.54 572107.68 0.19

5.19% 10.48% 15.67% 84.33% 100%

(16.29) (-4.23) (1.72) (5.63) (5.00)

Jul.-Sep. 28851.69 68308.42 97160.11 483492.87 580652.98 0.20

4.97% 11.76% 16.73% 83.27% 100%

(-2.79) (13.91) (8.38) (0.21) (1.49)

Oct.-Dec. 32712.95 71236.84 103949.79 506580.75 610530.54 0.21

5.36% 11.67% 17.03% 82.97% 100%

(13.38) (4.29) (6.99) (4.78) (5.15)

2014

Jan.-Mar. 33607.99 75528.66 109136.65 513130.58 622267.23 0.21

5.40% 12.14% 17.54% 82.46% 100%

(2.74) (6.02) (4.99) (1.29) (1.92)

Apr.-Jun. 36195.84 77727.04 113922.88 535517.14 649440.02 0.21

5.57% 11.97% 17.54% 82.46% 100%

(7.70) (2.91) (4.39) (4.36) (4.37)

Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter.

2. Minor differences may be observed due to rounding off.

x

v

Div

ision

-wise U

rba

n/R

ura

l Dep

osits:

Distrib

utio

n of

dep

osits

by ad

min

istrative

areas rev

ealed th

at

Dh

aka

Div

ision

co

ntrib

uted

m

ore

than

h

alf (6

4.0

2%

) of

the

total

dep

osits an

d th

e share o

f urb

an d

eposits in

this d

ivisio

n w

as 54

.98%

at

the

end

o

f th

e q

uarter

un

der

review

. T

he

dep

osits

in

this

div

ision

increased

by 3

.91%

to T

k. 4

15

79

7.1

5 cro

res at the en

d o

f the q

uarter

Ap

ril-Jun

e, 20

14

as com

pared

to in

creases of 1

.81

% an

d 6

.25%

at the

end

of p

recedin

g q

uarter Jan

uary

-March

, 201

4 an

d th

e corresp

on

din

g

qu

arter of th

e last year (A

pril-Ju

ne, 2

01

3) resp

ectively

. Th

e share o

f

dep

osits

in R

angp

ur

Div

ision

(1

.78%

) an

d B

arisal D

ivisio

n (1

.78

%)

were

the

low

est. D

ivisio

n w

ise d

istributio

n o

f dep

osits

in urb

an an

d

rural areas is sh

ow

n in

Tab

le-6.

TA

BL

E-6

(Con

td.)

DIV

ISIO

N-W

ISE

UR

BA

N/R

UR

AL

DIS

TR

IBU

TIO

N O

F D

EP

OS

ITS

(T

aka in

Cro

res)

At th

e end

C

hittag

ong D

ivisio

n

Dh

aka D

ivisio

n

Kh

uln

a Div

ision

R

ajshah

i Div

ision

of q

uarter

Urb

an

Rural

To

tal U

rban

R

ural

To

tal U

rban

R

ural

To

tal U

rban

R

ural

To

tal

20

13

Ap

r.-J

un

. 8

45

67

.22

26

560

.48

11

112

7.7

0

31

884

8.4

6

50

028

.23

36

887

6.6

9

17

581

.55

61

51

.11

23

732

.66

16

639

.73

5

43

6.2

2

22

075

.95

1

4.7

8%

4

.64

%

19

.42

%

55

.73

%

8.7

4%

6

4.4

8%

3

.07

%

1.0

8%

4

.15

%

2.9

1%

0

.95

%

3.8

6%

(0

.87

) (5

.59

) (1

.96

) (6

.30

) (5

.90

) (6

.25

) (6

.51

) (7

.80

) (6

.84

) (6

.54

) (8

.11

) (6

.92

)

Ju

l.-Sep

. 8

69

92

.24

28

167

.36

11

515

9.6

0

32

342

1.5

6

51

195

.53

37

461

7.0

9

17

038

.92

58

78

.12

22

917

.04

16

450

.85

5

60

0.9

1

22

051

.76

1

4.9

8%

4

.85

%

19

.83

%

55

.70

%

8.8

2%

6

4.5

2%

2

.93

%

1.0

1%

3

.95

%

2.8

3%

0

.96

%

3.8

0%

(2

.87

) (6

.05

) (3

.63

) (1

.43

) (2

.33

) (1

.56

) (-3

.09

) (-4

.44

) (-3

.44

) (-1

.14

) (3

.03

) (-0

.11

)

Oct.-D

ec.

91

839

.44

28

571

.80

12

041

1.2

4

33

787

9.2

7

55

167

.82

39

304

7.0

9

18

565

.90

64

13

.70

24

979

.60

17

437

.84

5

87

1.6

2

23

309

.46

1

5.0

4%

4

.68

%

19

.72

%

55

.34

%

9.0

4%

6

4.3

8%

3

.04

%

1.0

5%

4

.09

%

2.8

6%

0

.96

%

3.8

2%

(5

.57

) (1

.44

) (4

.56

) (4

.47

) (7

.76

) (4

.92

) (8

.96

) (9

.11

) (9

.00

) (6

.00

) (4

.83

) (5

.70

)

20

14

Ja

n.-M

ar.

94

421

.82

29

169

.50

12

359

1.3

2

34

470

6.6

7

55

435

.28

40

014

1.9

5

18

752

.47

66

65

.69

25

418

.16

17

462

.52

5

82

8.5

6

23

291

.08

1

5.1

7%

4

.69

%

19

.86

%

55

.40

%

8.9

1%

6

4.3

1%

3

.01

%

1.0

7%

4

.08

%

2.8

1%

0

.94

%

3.7

5%

(2

.81)

(2.0

9)

(2.6

4)

(2.0

2)

(0.4

8)

(1.8

1)

(1.0

0)

(3.9

3)

(1.7

6)

(0.1

6)

(-0.7

3)

(-0.0

7)

Ap

r.-J

un

. 9

72

06

.04

31

226

.20

12

843

2.2

4

35

707

2.2

2

58

724

.93

41

579

7.1

5

19

778

.03

76

94

.94

27

472

.97

18

727

.99

6

26

2.5

1

24

990

.50

1

4.9

7%

4

.81

%

19

.78

%

54

.98

%

9.0

4%

6

4.0

2%

3

.05

%

1.1

8%

4

.23

%

2.8

8%

0

.96

%

3.8

5%

(2

.95)

(7.0

5)

(3.9

2)

(3.5

9)

(5.9

3)

(3.9

1)

(5.4

7)

(15

.44

) (8

.08

) (7

.23

) (7

.45)

(7.2

8)

Note: 1

. Fig

ures in

paren

theses rep

resent rates o

f gro

wth

in p

ercent o

ver th

e preced

ing q

uarter.

2. M

inor d

ifferences m

ay b

e show

n d

ue to

roun

din

g o

ff.

x

vi

TA

BL

E-6

(Con

cld

.)

DIV

ISIO

N-W

ISE

UR

BA

N/R

UR

AL

DIS

TR

IBU

TIO

N O

F D

EP

OS

ITS

(Tak

a in C

rores)

At th

e end

B

arisal Div

ision

S

ylh

et Div

ision

R

angp

ur D

ivisio

n

All D

ivisio

ns

of q

uarter

Urb

an

Rural

To

tal U

rban

R

ural

To

tal U

rban

R

ural

To

tal U

rban

R

ural

To

tal

20

13

Ap

r.-J

un

. 6

94

2.7

9

31

05

.95

10

048

.74

1

69

33

.76

89

37

.20

25

870

.96

75

03

.32

2

87

1.6

6

10

374

.98

46

901

6.8

3

10

309

0.8

5

57

210

7.6

8

1

.21

%

0.5

4%

1

.76

%

2.9

6%

1

.56

%

4.5

2%

1

.31

%

0.5

0%

1

.81

%

81

.98

%

18

.02

%

10

0%

(7

.99)

(6.8

1)

(7.6

2)

(3.6

9)

(4.4

9)

(3.9

6)

(-17

.03

) (1

1.5

4)

(-10

.70

) (4

.76)

(6.1

0)

(5.0

0)

Ju

l.-Sep

. 6

80

7.7

3

31

58

.50

99

66

.23

1

71

58

.72

89

19

.58

26

078

.30

71

51

.68

2

71

1.2

8

98

62

.96

47

502

1.7

0

10

563

1.2

8

58

065

2.9

8

1

.17

%

0.5

4%

1

.72

%

2.9

6%

1

.54

%

4.4

9%

1

.23

%

0.4

7%

1

.70

%

81

.81

%

18

.19

%

10

0%

(-1

.95

) (1

.69)

(-0.8

2)

(1.3

3)

(-0.2

0)

(0.8

0)

(-4.6

9)

(-5.5

8)

(-4.9

4)

(1.2

8)

(2.4

6)

(1.4

9)

Oct.-D

ec.

73

36

.36

33

40

.93

10

677

.29

1

80

45

.92

93

87

.72

27

433

.64

77

16

.47

2

95

5.7

5

10

672

.22

49

882

1.2

0

11

170

9.3

4

61

053

0.5

4

1

.20

%

0.5

5%

1

.75

%

2.9

6%

1

.54

%

4.4

9%

1

.26

%

0.4

8%

1

.75

%

81

.70

%

18

.30

%

10

0%

(7

.77)

(5.7

8)

(7.1

3)

(5.1

7)

(5.2

5)

(5.2

0)

(7.9

0)

(9.0

2)

(8.2

1)

(5.0

1)

(5.7

5)

(5.1

5)

20

14

Ja

n.-M

ar.

73

80

.56

34

55

.80

10

836

.36

1

86

05

.49

96

12

.55

28

218

.04

78

13

.61

2

95

6.7

1

10

770

.32

50

914

3.1

4

11

312

4.0

9

62

226

7.2

3

1

.19

%

0.5

6%

1

.74

%

2.9

9%

1

.54

%

4.5

3%

1

.26

%

0.4

8%

1

.73

%

81

.82

%

18

.18

%

10

0%

(0

.60)

(3.4

4)

(1.4

9)

(3.1

0)

(2.3

9)

(2.8

6)

(1.2

6)

(0.0

3)

(0.9

2)

(2.0

7)

(1.2

7)

(1.9

2)

Ap

r.-J

un

. 7

91

8.9

9

36

62

.05

11

581

.04

1

94

67

.08

10

110

.23

29

577

.31

83

19

.70

3

26

9.1

1

11

588

.81

52

849

0.0

5

12

094

9.9

7

64

944

0.0

2

1

.22

%

0.5

6%

1

.78

%

3.0

0%

1

.56

%

4.5

5%

1

.28

%

0.5

0%

1

.78

%

81

.38

%

18

.62

%

10

0%

(7

.30)

(5.9

7)

(6.8

7)

(4.6

3)

(5.1

8)

(4.8

2)

(6.4

8)

(10

.57

) (7

.60)

(3.8

0)

(6.9

2)

(4.3

7)

No

te: 1. F

igures in

paren

theses rep

resent rates o

f gro

wth

in p

ercent o

ver th

e preced

ing q

uarter.

2. M

ino

r differen

ces m

ay b

e sho

wn d

ue to

separate ro

und

ing o

ff.

xvii

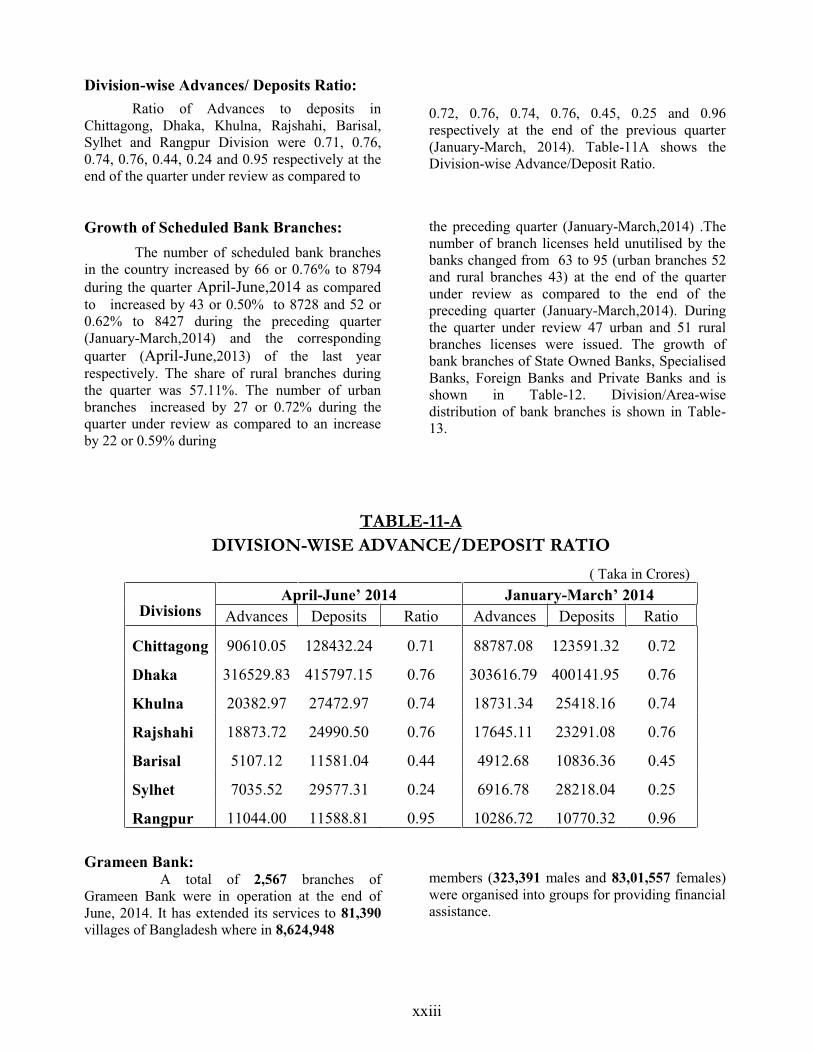

Advances by Category of Banks: The State owned Banks accounted

for 17.86% of the total advances at the end of the

quarter under review. Advances made by State

owned banks decreased by 0.55% to Tk.83851.57

crores at the end of the quarter under review as

compared to an increase of 1.21% and a decrease

(January-March, 2014) and the corresponding

quarter (April-June, 2013) of the last year

advances increased to 7.11% on the 30th

from 7.04% on the 31st March 2014.

Advances classified by category of banks are

shown in Table-7.

of 1.23% at the end of the preceding quarter

TABLE -7 ADVANCES CLASSIFIED BY CATEGORY OF BANKS

(Taka in Crores) At the end State Specialised Foreign Private Banks Islamic All

of quarter Owned Banks Banks (including Banks Banks

Banks Islamic Banks)

2013

Apr.-Jun. 86166.38 29685.57 21302.08 287650.44 89217.98 424804.47

20.28% 6.99% 5.01% 67.71% 21.00% 100%

(-1.23) (6.19) (3.36) (3.38) (1.05) (2.60)

Jul.-Sep. 82093.56 29987.02 22301.43 297194.91 91984.17 431576.92

19.02% 6.95% 5.17% 68.86% 21.31% 100%

(-4.73) (1.02) (4.69) (3.32) (3.10) (1.59)

Oct.-Dec. 83303.22 31424.94 22185.89 306930.36 94649.88 443844.41

18.77% 7.08% 5.00% 69.15% 21.33% 100%

(1.47) (4.80) (-0.52) (3.28) (2.90) (2.84)

2014

Jan.-Mar. 84312.69 31726.29 21774.69 313082.83 99112.59 450896.50

18.70% 7.04% 4.83% 69.44% 21.98% 100.00%

(1.21) (0.96) (-1.85) (2.00) (4.71) (1.59)

Apr.-Jun. 83851.57 33410.80 21787.86 330532.98 103848.25 469583.21

17.86% 7.11% 4.64% 70.39% 22.11% 100.00%

(-0.55) (5.31) (0.06) (5.57) (4.78) (4.14)

Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter.

2. Minor differences may be observed due to rounding off.

xviii

Sector-wise Advances: Advances in the private sector increased by

Tk. 19748.52 crores or 4.47% to Tk. 461201.77

crores at end of the quarter (April-June, 2014) as

compared to increases of Tk. 6107.00 crores or

1.40% and Tk. 11320.43 crores or 2.81% at the

preceding quarter (January-March, 2014) and the

corresponding quarter (April-June, 2013) of the last

year respectively. Loans to the public sector

decreased by Tk. 1061.81 crores or 11.24% to

Tk.8381.44 crores as compared to an increase of

Tk. 945.09 crores or 11.12% and a decrease of

Tk. 564.54 crores or 4.79% during the preceding

quarter (January-March, 2014) and corresponding

quarter of the last year respectively. The decrease

in advances to public sector was due to decrease

in 'Government' sector by Tk. 713.76 crores or

29.95% to Tk. 1669.39 than

Government' sector loans decreased by Tk. 348.05

crores or 4.93% to Tk. 6712.05 crores at the end

of the quarter under review. The sector-wise

position of advances is shown in Table-8.

TABLE- 8 SECTOR-WISE CLASSIFICATION OF ADVANCES

(Taka in Crores)

At the end Public Sector Private Total Ratio

of quarter Government Other than Total Sector Advances (Public/Private)

Government (Public + Private)

2013

Apr.-Jun. 2892.29 8339.23 11231.52 413572.95 424804.47 0.03

0.68% 1.96% 2.64% 97.36% 100%

(-13.65) (-1.27) (-4.79) (2.81) (2.60)

Jul.-Sep. 2117.43 5639.96 7757.39 423819.53 431576.92 0.02

0.49% 1.31% 1.80% 98.20% 100%

(-26.79) (-32.37) (-30.93) (2.48) (1.59)

Oct.-Dec. 1613.62 6884.54 8498.16 435346.25 443844.41 0.02

0.36% 1.55% 1.91% 98.09% 100%

(-23.79) (22.07) (9.55) (2.72) (2.84)

2014

Jan.-Mar. 2383.15 7060.10 9443.25 441453.25 450896.50 0.02

0.53% 1.57% 2.09% 97.91% 100.00%

(47.69) (2.55) (11.12) (1.40) (1.59)

Apr.-Jun. 1669.39 6712.05 8381.44 461201.77 469583.21 0.02

0.36% 1.43% 1.78% 98.22% 100.00%

(-29.95) (-4.93) (-11.24) (4.47) (4.14)

Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter.

2. Minor differences may be observed due to rounding off.

xix

Economic Purpose-wise Advances:

Bulk of Advances (39.38%) was used

f the April-June,

2014. Trade loans increased by Tk. 2224.73 crores

or 1.22% to Tk. 184921.74 crores and 'Term Loan'

increased by Tk. 6605.46 crores or 9.08% to Tk.

79392.81 crores at the end of the quarter under

review as compared to an increase of 4.88% and a

decrease of 4.77% respectively at the end of the

preceding quarter (January-March, 2014) and

increases of 1.19% & 7.25% respectively at the

corresponding quarter (April-June, 2013) of the

Tk. 5312.

increased by 3.09% to Tk. 25951.90 crores as

compared to increases of 2.64% & 1.44% at the

end of the preceding quarter (January-March,

2014) and a decrease of 4.42% & an increase

3.03% at the corresponding quarter (April-June,

2013) of the last year respectively. 'Construction'

loan decreased by 1.00% to Tk. 40728.98 crores

28731.00 crores respectively at the end of the

quarter under review. 'Others' loans showed an

increase of Tk. 890.45 crores to Tk. 18571.62

crores at the end of the quarter under review as

compared to the preceding quarter. Table-9 shows

economic purpose-wise classification of advances.

TABLE -9 ECONOMIC PURPOSE-WISE CLASSIFICATION OF ADVANCES

(Taka in Crores)

At the end

of quarter

Agriculture,

Fishing &

Forestry

Industry Constru-

ction Transport Trade &

Commerce

Consumer

Finance Others Total

Term

Loan

Working

Capital

Financing

2013

Apr.-Jun. 22971.10 96137.10 57047.66 38705.45 5852.84 156336.84 28021.55 19731.93 424804.47

5.41% 22.63% 13.43% 9.11% 1.38% 36.80% 6.60% 4.64% 100%

(3.03) (7.25) (3.41) (1.23) (-4.42) (1.19) (10.48) (-13.21) (2.60)

Jul.-Sep. 24656.89 84941.63 62419.86 36299.08 5297.35 165991.69 33140.78 18829.64 431576.92

5.71% 19.68% 14.46% 8.41% 1.23% 38.46% 7.68% 4.36% 100%

(7.34) (-11.65) (9.42) (-6.22) (-9.49) (6.18) (18.27) (-4.57) (1.59)

Oct.-Dec. 24817.19 76433.39 72889.24 39657.89 5101.02 174201.72 29595.58 21148.38 443844.41

5.59% 17.22% 16.42% 8.94% 1.15% 39.35% 6.67% 4.76% 100%

(0.65) (-10.02) (16.77) (9.25) (-3.71) (4.95) (-10.70) (12.31) (2.84)

2014

Jan.-Mar. 25174.18 72787.35 78669.85 41139.24 5235.81 182697.01 27511.89 17681.17 450896.50

5.58% 16.14% 17.45% 9.12% 1.16% 40.52% 6.10% 3.92% 100.00%

(1.44) (-4.77) (7.93) (3.74) (2.64) (4.88) (-7.04) (-16.39) (1.59)

Apr.-Jun. 25951.90 79392.81 85973.11 40728.98 5312.05 184921.74 28731.00 18571.62 469583.21

5.53% 16.91% 18.31% 8.67% 1.13% 39.38% 6.12% 3.95% 100.00%

(3.09) (9.08) (9.28) (-1.00) (1.46) (1.22) (4.43) (5.04) (4.14)

Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter. Minor differences may be observed due to

-1,2 & 3 .

2. Other purposes include Other Institutional Loan & miscellaneous.

xx

Security-wise Advances: An analysis of advances classified by

securities revealed that 56.67% of the total loans

Rea

port Documents/

the end of the quarter under review. Advances

266102.62 crores y

increased by 6.34% to Tk. 35935.80 crores at the

end of the quarter April-June, 2014. Other

Items' which includes (i) Gold & Gold Ornaments,

(ii)Vehicles, (iii) Hypothecation of Crops, (iv)

Assignment of Bills Receivable, (v) Parri Passu

Charge, (vi) Other secured and unsecured

advances recorded an decrease of 15.39% to Tk.

36303.28 crores at the end of the quarter April-

June, 2014 as compared to an increase of 2.62%

and a decrease of 10.39% at the end of the

preceding quarter (January-March, 2014)) and the

corresponding quarter April-June, 2013 of the last

year respectively. Security wise classification of

advances is shown in Table-10.

TABLE - 10

SECURITY-WISE CLASSIFICATION OF ADVANCES

(Taka in Crores)

At the end

of quarter

Shares &

Securities

Export

Documents/

Commodities

Machinery

/

Fixed

Assets

Real

Estate

Financial

Obligations

Only

Guarantee of

Individuals/

Institutions

Other

Items

Total

2013

Apr.-Jun. 2100.09 34330.06 30566.87 227427.18 30131.40 55198.69 45050.18 424804.47

0.49% 8.08% 7.20% 53.54% 7.09% 12.99% 10.60% 100%

(30.59) (-16.20) (-0.64) (9.23) (26.83) (-5.58) (-10.39) (2.60)

Jul.-Sep. 1817.58 31201.18 32716.87 235516.95 33080.80 64375.93 32867.61 431576.92

0.42% 7.23% 7.58% 54.57% 7.67% 14.92% 7.62% 100%

(-13.45) (-9.11) (7.03) (3.56) (9.79) (16.63) (-27.04) (1.59)

Oct.-Dec. 1942.17 34707.42 31923.45 240499.04 30061.24 62901.05 41810.04 443844.41

0.44% 7.82% 7.19% 54.19% 6.77% 14.17% 9.42% 100%

(6.85) (11.24) (-2.43) (2.12) (-9.13) (-2.29) (27.21) (2.84)

2014

Jan.-Mar. 2565.75 36399.15 33792.73 256498.42 31352.61 47382.45 42905.39 450896.50

0.57% 8.07% 7.49% 56.89% 6.95% 10.51% 9.52% 100.00%

(32.11) (4.87) (5.86) (6.65) (4.30) (-24.67) (2.62) (1.59)

Apr.-Jun. 3074.42 35458.93 35935.80 266102.62 39765.79 52942.37 36303.28 469583.21

0.65% 7.55% 7.65% 56.67% 8.47% 11.27% 7.73% 100.00%

(19.83) (-2.58) (6.34) (3.74) (26.83) (11.73) (-15.39) (4.14)

Note: 1. Figures in parentheses represent rates of growth in percent over the preceding quarter.

2. Minor differences may be observed due to rounding off and changes of Fourth Edition to

n the Banking Statistics Returns SBS-1,

xx

i

Div

ision

-wise U

rba

n/R

ura

l Ad

va

nces:

Div

ision

-wise b

reak-u

p o

f advan

ces revealed

that D

hak

a Div

ision

con

sum

ed 6

7.4

1%

of to

tal advan

ces of w

hich

the sh

are of u

rban

and

rural sto

od

at 62

.88%

and

4.5

2%

respectiv

ely at th

e end

of th

e qu

arter

Ap

ril- Jun

e, 201

4. T

he lo

ans in

Dhak

a Div

ision

increased

by 4

.25%

to

Tk. 3

16

52

9.8

3 cro

res and

in C

hittag

on

g D

ivisio

n in

creased b

y 2

.05

% to

Tk. 9

06

10

.05

crores an

d in

Kh

uln

a Div

ision

increased

by 8

.82

% to

Tk.

20382.9

7

crores

durin

g

the

qu

arter un

der

review

. T

he

loan

s in

Sylh

et Div

ision

increased

by 1

.72

% to

Tk. 7

03

5.5

2 cro

res, in B

arisal

Div

ision in

creased b

y 3

.96%

to T

k. 5

10

7.1

2cro

res, in R

ajshah

i Div

ision

increased

by 6

.96

% to

Tk. 1

88

73

.72 cro

res and

that in

Ran

gp

ur D

ivisio

n

increased

by 7

.36%

to T

k. 1

10

44

.00

Div

ision

-wise d

istribu

tion

of u

rban

and

rural lo

ans is sh

ow

n in

Tab

le-11

.

TA

BL

E-11(C

on

td.)

DIV

ISIO

N-W

ISE

UR

BA

N/

RU

RA

L C

LA

SS

IFIC

AT

ION

OF

AD

VA

NC

ES

(Tak

a in C

rores)

At th

e end

of q

uarter

Chittag

on

g D

ivisio

n

Dh

aka D

ivisio

n

Kh

uln

a Div

ision

R

ajshah

i Div

ision

Urb

an

Rural

To

tal U

rban

R

ural

To

tal U

rban

R

ural

To

tal U

rban

R

ural

To

tal

20

13

Ap

r.-Ju

n.

75

661

.36

89

69

.41

84

630

.77

2

65

09

7.3

4

19

938

.45

28

503

5.7

9

13

648

.28

44

79

.58

18

127

.86

13

046

.08

3

36

3.3

4

16

409

.42

1

7.8

1%

2

.11

%

19

.92

%

62

.40

%

4.6

9%

6

7.1

0%

3

.21

%

1.0

5%

4

.27

%

3.0

7%

0

.79

%

3.8

6%

(2

.38)

(1.3

0)

(2.2

6)

(2.8

3)

(2.6

1)

(2.8

2)

(-1.6

7)

(1.7

6)

(-0.8

4)

(3.7

0)

(5.8

5)

(4.1

3)

Ju

l.-Sep

. 7

79

35

.07

88

38

.38

86

773

.45

2

68

81

9.3

4

20

066

.32

28

888

5.6

6

13

913

.89

46

53

.31

18

567

.20

13

303

.40

3

26

4.1

1

16

567

.51

1

8.0

6%

2

.05

%

20

.11

%

62

.29

%

4.6

5%

6

6.9

4%

3

.22

%

1.0

8%

4

.30

%

3.0

8%

0

.76

%

3.8

4%

(3

.01)

(-1.4

6)

(2.5

3)

(1.4

0)

(0.6

4)

(1.3

5)

(1.9

5)

(3.8

8)

(2.4

2)

(1.9

7)

(-2.9

5)

(0.9

6)

Oct.-D

ec. 7

84

68

.23

94

28

.89

87

897

.12

2

77

90

0.4

4

20

507

.46

29

840

7.9

0

14

042

.94

45

94

.61

18

637

.55

13

529

.34

3

55

4.3

6

17

083

.70

1

7.6

8%

2

.12

%

19

.80

%

62

.61

%

4.6

2%

6

7.2

3%

3

.16

%

1.0

4%

4

.20

%

3.0

5%

0

.80

%

3.8

5%

(0

.68)

(6.6

8)

(1.2

9)

(3.3

8)

(2.2

0)

(3.3

0)

(0.9

3)

(-1.2

6)

(0.3

8)

(1.7

0)

(8.8

9)

(3.1

2)

20

14

Ja

n.-M

ar.

80

122

.08

86

65

.00

88

787

.08

2

82

84

2.7

1

20

774

.08

30

361

6.7

9

14

143

.25

45

88

.09

18

731

.34

14

054

.30

3

59

0.8

1

17

645

.11

1

7.7

7%

1

.92

%

19

.69

%

62

.73

%

4.6

1%

6

7.3

4%

3

.14

%

1.0

2%

4

.15

%

3.1

2%

0

.80

%

3.9

1%

(2

.11)

(-8.1

0)

(1.0

1)

(1.7

8)

(1.3

0)

(1.7

5)

(0.7

1)

(-0.1

4)

(0.5

0)

(3.8

8)

(1.0

3)

(3.2

9)

Ap

r.-Ju

n.

81

783

.10

88

26

.95

90

610

.05

2

95

28

3.6

6

21

246

.17

31

652

9.8

3

15

250

.69

51

32

.28

20

382

.97

15

073

.04

3

80

0.6

8

18

873

.72

1

7.4

2%

1

.88

%

19

.30

%

62

.88

%

4.5

2%

6

7.4

1%

3

.25

%

1.0

9%

4

.34

%

3.2

1%

0

.81

%

4.0

2%

(2

.07)

(1.8

7)

(2.0

5)

(4.4

0)

(2.2

7)

(4.2

5)

(7.8

3)

(11

.86

) (8

.82

) (7

.25

) (5

.84

) (6

.96

)

No

te: 1. F

igu

res in p

arenth

eses represen

t rates of g

row

th in

percen

t over th

e preced

ing q

uarter.

2. M

ino

r differen

ces may

be o

bserv

ed d

ue to

rou

nd

ing o

ff.

xx

ii TA

BL

E-11(C

on

cld

.)

DIV

ISIO

N-W

ISE

UR

BA

N/

RU

RA

L C