Intro to Derivatives - Finance

54

1 Introduction To Introduction To Derivatives Derivatives

-

Upload

darlingjunior -

Category

Documents

-

view

1.415 -

download

4

description

Transcript of Intro to Derivatives - Finance

11

Introduction To DerivativesIntroduction To Derivatives

22

This first lecture has four main goals:This first lecture has four main goals:1.1. Introduce you to the notion of risk and the role of derivatives in Introduce you to the notion of risk and the role of derivatives in

managing risk.managing risk.Discuss some of the general terms – such as short/long positions, bid-Discuss some of the general terms – such as short/long positions, bid-ask spread – from finance that we need.ask spread – from finance that we need.

2.2. Introduce you to three major classes of derivative securities.Introduce you to three major classes of derivative securities.ForwardsForwards

FuturesFutures

OptionsOptions

3.3. Introduce you to the basic viewpoint needed to analyze these Introduce you to the basic viewpoint needed to analyze these securities.securities.

4.4. Introduce you to the major traders of these instruments.Introduce you to the major traders of these instruments.

BasicsBasics

33

BasicsBasicsFinance is the study of risk.Finance is the study of risk.– How to measure itHow to measure it– How to reduce itHow to reduce it– How to allocate itHow to allocate it

All finance problems ultimately boil down to three main questions:All finance problems ultimately boil down to three main questions:– What are the cash flows, and when do they occur?What are the cash flows, and when do they occur?– Who gets the cash flows?Who gets the cash flows?– What is the appropriate discount rate for those cash flows?What is the appropriate discount rate for those cash flows?

The difficulty, of course, is that normally none of those questions have an The difficulty, of course, is that normally none of those questions have an easy answer.easy answer.

44

BasicsBasicsAs you know from other classes, we can generally classify risk as being As you know from other classes, we can generally classify risk as being diversifiable or non-diversifiable:diversifiable or non-diversifiable:

– Diversifiable – risk that is specific to a specific investment – i.e. the risk Diversifiable – risk that is specific to a specific investment – i.e. the risk that a single company’s stock may go down (i.e. Enron). This is that a single company’s stock may go down (i.e. Enron). This is frequently called frequently called idiosyncratic risk.idiosyncratic risk.

– Non-diversifiable – risk that is common to all investing in general and Non-diversifiable – risk that is common to all investing in general and that cannot be reduced – i.e. the risk that the entire stock market (or that cannot be reduced – i.e. the risk that the entire stock market (or bond market, or real estate market) will crash. This is frequently called bond market, or real estate market) will crash. This is frequently called systematic risksystematic risk..

The market “pays” you for bearing non-diversifiable risk only – not for The market “pays” you for bearing non-diversifiable risk only – not for bearing diversifiable risk.bearing diversifiable risk.

– In general the more non-diversifiable risk that you bear, the greater the In general the more non-diversifiable risk that you bear, the greater the expected return to your investment(s).expected return to your investment(s).

– Many investors fail to properly diversify, and as a result bear more risk Many investors fail to properly diversify, and as a result bear more risk than they have to in order to earn a given level of expected return.than they have to in order to earn a given level of expected return.

55

BasicsBasics

In this sense, we can view the field of finance as being about two issues:In this sense, we can view the field of finance as being about two issues:

– The elimination of diversifiable risk in portfolios;The elimination of diversifiable risk in portfolios;

– The The allocationallocation of systematic (non-diversifiable) risk to those members of systematic (non-diversifiable) risk to those members of society that are most willing to bear it.of society that are most willing to bear it.

Indeed, it is really this second function – the allocation of systematic risk – Indeed, it is really this second function – the allocation of systematic risk – that drives rates of return.that drives rates of return.

– The expected rate of return is the “price” that The expected rate of return is the “price” that the market pays investors for bearing the market pays investors for bearing systematic risk.systematic risk.

66

BasicsBasicsA A derivativederivative (or derivative security) is a financial instrument whose value (or derivative security) is a financial instrument whose value depends upon the value of other, more basic, underlying variables.depends upon the value of other, more basic, underlying variables.

Some common examples include things such as stock options, futures, Some common examples include things such as stock options, futures, and forwards. and forwards.

It can also extend to something like a reimbursement program for college It can also extend to something like a reimbursement program for college credit. Consider that if your firm reimburses 100% of costs for an “A”, 75% credit. Consider that if your firm reimburses 100% of costs for an “A”, 75% of costs for a “B”, 50% for a “C” and 0% for anything less. of costs for a “B”, 50% for a “C” and 0% for anything less.

77

Your “right” to claim this reimbursement, then is Your “right” to claim this reimbursement, then is tied to the grade you earn. The value of that tied to the grade you earn. The value of that reimbursement plan, therefore, is reimbursement plan, therefore, is derivedderived from the from the grade you earn. grade you earn.

We also say that the value is We also say that the value is contingentcontingent upon the upon the grade you earn. Thus, your claim for grade you earn. Thus, your claim for reimbursement is a “contingent” claim. reimbursement is a “contingent” claim.

The terms contingent claims and derivatives are The terms contingent claims and derivatives are used interchangeably.used interchangeably.

BasicsBasics

88

BasicsBasics

So why do we have derivatives and So why do we have derivatives and derivatives markets?derivatives markets?– Because they somehow allow investors to Because they somehow allow investors to

better control the level of risk that they bear.better control the level of risk that they bear.– They can help eliminate idiosyncratic risk.They can help eliminate idiosyncratic risk.– They can decrease or increase the level of They can decrease or increase the level of

systematic risk.systematic risk.

99

A First ExampleA First ExampleThere is a neat example from the bond-world of a derivative that is used to There is a neat example from the bond-world of a derivative that is used to move non-diversifiable risk from one set of investors to another set that are, move non-diversifiable risk from one set of investors to another set that are, presumably, more willing to bear that risk.presumably, more willing to bear that risk.

Disney wanted to open a theme park in Tokyo, but did not want to have the Disney wanted to open a theme park in Tokyo, but did not want to have the shareholders bear the risk of an earthquake destroying the park.shareholders bear the risk of an earthquake destroying the park.– They financed the park through the issuance of earthquake bonds.They financed the park through the issuance of earthquake bonds.– If an earthquake of at least 7.5 hit within 10 km of the park, the bonds If an earthquake of at least 7.5 hit within 10 km of the park, the bonds

did not have to be repaid, and there was a sliding scale for smaller did not have to be repaid, and there was a sliding scale for smaller quakes and for larger ones that were located further away from the quakes and for larger ones that were located further away from the park.park.

1010

A First ExampleA First Example

Normally this could have been handled in the insurance (and re-insurance) Normally this could have been handled in the insurance (and re-insurance) markets, but there would have been transaction costs involved. By placing markets, but there would have been transaction costs involved. By placing the risk directly upon the bondholders Disney was able to avoid those the risk directly upon the bondholders Disney was able to avoid those transactions costs. transactions costs. – Presumably the bondholders of the Disney bonds are basically the Presumably the bondholders of the Disney bonds are basically the

same investors that would have been holding the stock or bonds of the same investors that would have been holding the stock or bonds of the insurance/reinsurance companies.insurance/reinsurance companies.

– Although the risk of earthquake is not diversifiable to the park, it could Although the risk of earthquake is not diversifiable to the park, it could be to Disney shareholders, so this does beg the question of why buy the be to Disney shareholders, so this does beg the question of why buy the insurance at all.insurance at all.

This was not a “free” insurance. Disney paid LIBOR+310 on the bond. If the This was not a “free” insurance. Disney paid LIBOR+310 on the bond. If the earthquake provision was not it there, they would have paid a lower rate.earthquake provision was not it there, they would have paid a lower rate.

1111

A First ExampleA First Example

This example illustrates an interesting This example illustrates an interesting notion – that insurance contracts (for notion – that insurance contracts (for property insurance) are really derivatives!property insurance) are really derivatives!

They allow the owner of the asset to “sell” They allow the owner of the asset to “sell” the insured asset to the insurer in the the insured asset to the insurer in the event of a disaster.event of a disaster.

They are like put options (more on this They are like put options (more on this later.)later.)

1212

BasicsBasicsPositions – In general if you are buying an asset – be it a physical stock or Positions – In general if you are buying an asset – be it a physical stock or bond, or the right to determine whether or not you will acquire the asset in bond, or the right to determine whether or not you will acquire the asset in the future (such as through an option or futures contract) you are said to be the future (such as through an option or futures contract) you are said to be “LONG” the instrument.“LONG” the instrument.If you are giving up the asset, or giving up the right to determine whether or If you are giving up the asset, or giving up the right to determine whether or not you will own the asset in the future, you are said to be “SHORT” the not you will own the asset in the future, you are said to be “SHORT” the instrument.instrument.– In the stock and bond markets, if you “short” an asset, it means that you In the stock and bond markets, if you “short” an asset, it means that you

borrow it, sell the asset, and then later buy it back.borrow it, sell the asset, and then later buy it back.– In derivatives markets you generally do not have to borrow the In derivatives markets you generally do not have to borrow the

instrument – you can simply take a position (such as writing an option) instrument – you can simply take a position (such as writing an option) that will require you to give up the asset or determination of ownership that will require you to give up the asset or determination of ownership of the asset.of the asset.

– Usually in derivatives markets the “short” is just the negative of the Usually in derivatives markets the “short” is just the negative of the “long” position“long” position

1313

BasicsBasics

Commissions – Virtually all transactions in the financial markets requires Commissions – Virtually all transactions in the financial markets requires some form of commission payment. some form of commission payment.

– The size of the commission depends upon the relative position of the The size of the commission depends upon the relative position of the trader: retail traders pay the most, institutional traders pay less, market trader: retail traders pay the most, institutional traders pay less, market makers pay the least (but still pay to the exchanges.)makers pay the least (but still pay to the exchanges.)

– The larger the trade, the smaller the commission is in percentage terms.The larger the trade, the smaller the commission is in percentage terms.

Bid-Ask spread – Depending upon whether you are buying or selling an Bid-Ask spread – Depending upon whether you are buying or selling an instrument, you will get different prices. If you wish to sell, you will get a instrument, you will get different prices. If you wish to sell, you will get a “BID” quote, and if you wish to buy you will get an “ASK” quote.“BID” quote, and if you wish to buy you will get an “ASK” quote.

1414

BasicsBasics

The difference between the bid and the ask can vary depending upon The difference between the bid and the ask can vary depending upon whether you are a retail, institutional, or broker trader; it can also vary if you whether you are a retail, institutional, or broker trader; it can also vary if you are placing very large trades.are placing very large trades.

In general, however, the bid-ask spread is relatively constant for a given In general, however, the bid-ask spread is relatively constant for a given customer/position.customer/position.

The spread is roughly a constant percentage of the transaction, regardless The spread is roughly a constant percentage of the transaction, regardless of the scale – unlike the commission.of the scale – unlike the commission.

Especially in options trading, the bid-ask spread is a much bigger Especially in options trading, the bid-ask spread is a much bigger transaction cost than the commission.transaction cost than the commission.

1515

BasicsBasics

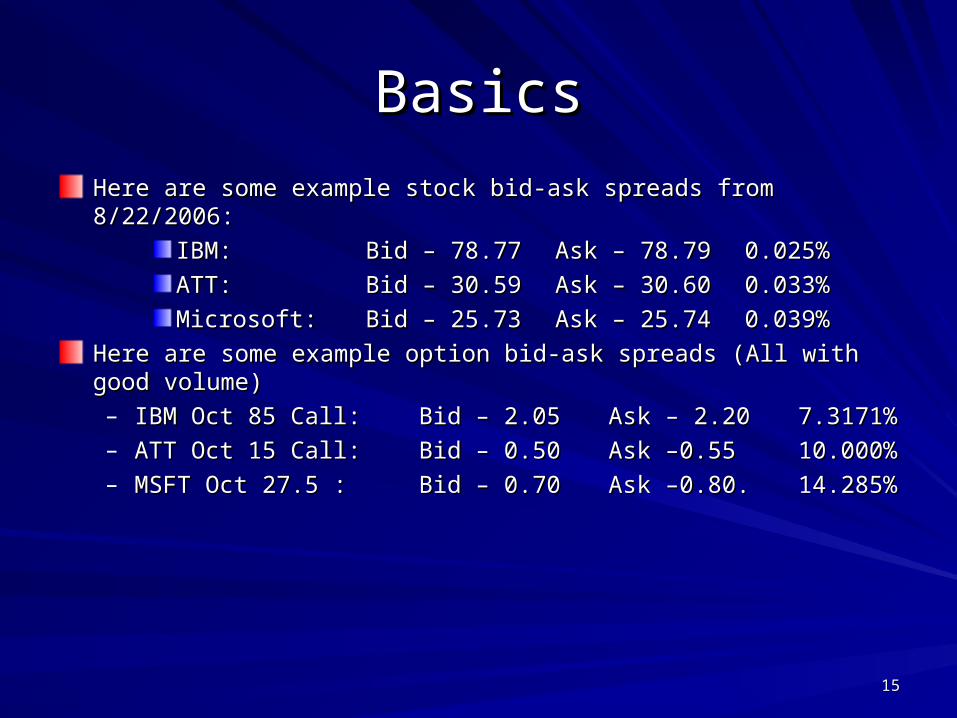

Here are some example stock bid-ask spreads from 8/22/2006:Here are some example stock bid-ask spreads from 8/22/2006:

IBM: IBM: Bid – 78.77 Bid – 78.77 Ask – 78.79Ask – 78.790.025%0.025%

ATT: ATT: Bid – 30.59Bid – 30.59 Ask – 30.60Ask – 30.600.033%0.033%

Microsoft:Microsoft: Bid – 25.73 Bid – 25.73 Ask – 25.74Ask – 25.74 0.039%0.039%

Here are some example option bid-ask spreads (All with good volume)Here are some example option bid-ask spreads (All with good volume)

– IBM Oct 85 Call: IBM Oct 85 Call: Bid – 2.05Bid – 2.05 Ask – 2.20Ask – 2.20 7.3171%7.3171%

– ATT Oct 15 Call:ATT Oct 15 Call: Bid – 0.50Bid – 0.50 Ask –0.55Ask –0.55 10.000%10.000%

– MSFT Oct 27.5 : MSFT Oct 27.5 : Bid – 0.70Bid – 0.70 Ask –0.80.Ask –0.80. 14.285%14.285%

1616

BasicsBasics

The point of the preceding slide is to demonstrate that the bid-ask spread The point of the preceding slide is to demonstrate that the bid-ask spread can be a huge factor in determining the profitability of a trade. can be a huge factor in determining the profitability of a trade.

– Many of those option positions require at least a 10% price movement Many of those option positions require at least a 10% price movement before the trade is profitable.before the trade is profitable.

Many “trading strategies” that you see people propose (and that are Many “trading strategies” that you see people propose (and that are frequently demonstrated using “real” data) are based upon using the frequently demonstrated using “real” data) are based upon using the average of the bid-ask spread. They usually lose their effectiveness when average of the bid-ask spread. They usually lose their effectiveness when the bid-ask spread is considered.the bid-ask spread is considered.

1717

BasicsBasics

Market Efficiency – We normally talk about financial markets as being Market Efficiency – We normally talk about financial markets as being efficient information processors.efficient information processors.

– Markets efficiently incorporate all publicly available information into Markets efficiently incorporate all publicly available information into financial asset prices.financial asset prices.

– The mechanism through which this is done is by investors buying/selling The mechanism through which this is done is by investors buying/selling based upon their discovery and analysis of new information.based upon their discovery and analysis of new information.

– The limiting factor in this is the transaction costs associated with the The limiting factor in this is the transaction costs associated with the market.market.

– For this reason, it is better to say that financial markets are efficient For this reason, it is better to say that financial markets are efficient to to within transactions costswithin transactions costs. Some financial economists say that . Some financial economists say that financial markets are efficient to within the bid-ask spread.financial markets are efficient to within the bid-ask spread.

– Now, to a large degree for this class we can ignore the bid-ask spread, Now, to a large degree for this class we can ignore the bid-ask spread, but there are some points where it will be particularly relevant, and we but there are some points where it will be particularly relevant, and we will consider it then.will consider it then.

1818

BasicsBasics

Before we begin to examine specific contracts, we need to consider two Before we begin to examine specific contracts, we need to consider two additional risks in the market:additional risks in the market:

– Credit risk – the risk that your trading partner might not honor their Credit risk – the risk that your trading partner might not honor their obligations.obligations.

Familiar risk to anybody that has traded on ebay!Familiar risk to anybody that has traded on ebay!

Generally exchanges serve to mitigate this risk.Generally exchanges serve to mitigate this risk.

Can also be mitigated by escrow accounts.Can also be mitigated by escrow accounts.

– Margin requirements are a form of escrow account.Margin requirements are a form of escrow account.

– Liquidity risk – the risk that when you need to buy or sell an instrument Liquidity risk – the risk that when you need to buy or sell an instrument you may not be able to find a counterparty.you may not be able to find a counterparty.

Can be very common for “outsiders” in commodities markets.Can be very common for “outsiders” in commodities markets.

1919

BasicsBasics

So now we are going to begin examining the So now we are going to begin examining the basic instruments of derivatives. In particular basic instruments of derivatives. In particular we will look at :we will look at :– ForwardsForwards– FuturesFutures– OptionsOptions

The purpose of our discussion is to simply The purpose of our discussion is to simply provide a basic understanding of the structure provide a basic understanding of the structure of the instruments and the basic reasons they of the instruments and the basic reasons they might exist. might exist.

2020

A A forward contractforward contract is an agreement between two parties to buy or sell an asset is an agreement between two parties to buy or sell an asset at a certain future time for a certain future price.at a certain future time for a certain future price.

– Forward contracts are normally not exchange traded.Forward contracts are normally not exchange traded.

– The party that agrees to buy the asset in the future is said to have the The party that agrees to buy the asset in the future is said to have the longlong position. position.

– The party that agrees to sell the asset in the future is said to have the The party that agrees to sell the asset in the future is said to have the shortshort position. position.

– The specified future date for the exchange is known as the delivery The specified future date for the exchange is known as the delivery ((maturitymaturity) date.) date.

Forward ContractsForward Contracts

2121

The specified price for the sale is known as the The specified price for the sale is known as the deliverydelivery price, we will denote price, we will denote this as K. this as K. – Note that K is set such that at initiation of the contract the value of the Note that K is set such that at initiation of the contract the value of the

forward contract is 0. Thus, by design, no cash changes hands at time forward contract is 0. Thus, by design, no cash changes hands at time 0. The mechanics of how to do this we cover in later lectures.0. The mechanics of how to do this we cover in later lectures.

As time progresses the delivery price doesn’t change, but the current spot As time progresses the delivery price doesn’t change, but the current spot (market) rate does. Thus, the contract gains (or loses) value over time. (market) rate does. Thus, the contract gains (or loses) value over time. – Consider the situation at the maturity date of the contract. If the spot Consider the situation at the maturity date of the contract. If the spot

price is higher than the delivery price, the long party can buy at K and price is higher than the delivery price, the long party can buy at K and immediately sell at the spot price Simmediately sell at the spot price STT, making a profit of (S, making a profit of (STT-K), whereas -K), whereas the short position could have sold the asset for Sthe short position could have sold the asset for STT, but is obligated to , but is obligated to sell for K, earning a profit (negative) of (K-Ssell for K, earning a profit (negative) of (K-STT).).

Forward ContractsForward Contracts

2222

Example:Example:– Let’s say that you entered into a forward contract to buy wheat at Let’s say that you entered into a forward contract to buy wheat at

$4.00/bushel, with delivery in December .$4.00/bushel, with delivery in December .– Let’s say that the delivery date was December 14 and that on Let’s say that the delivery date was December 14 and that on

December 14December 14thth the market price of wheat is unlikely to be exactly the market price of wheat is unlikely to be exactly $4.00/bushel, but that is the price at which you have agreed (via the $4.00/bushel, but that is the price at which you have agreed (via the forward contract) to buy your wheat.forward contract) to buy your wheat.

– If the market price is greater than $4.00/bushel, you are pleased, If the market price is greater than $4.00/bushel, you are pleased, because you are able to buy an asset for less than its market price.because you are able to buy an asset for less than its market price.

– If, however, the market price is less than $4.00/bushel, you are not If, however, the market price is less than $4.00/bushel, you are not pleased because you are paying more than the market price for the pleased because you are paying more than the market price for the wheat.wheat.

– Indeed, we can determine your net payoff to the trade by applying the Indeed, we can determine your net payoff to the trade by applying the formula: payoff = Sformula: payoff = STT – K, since you gain an asset worth S – K, since you gain an asset worth STT, but you have , but you have to pay $K for it. to pay $K for it.

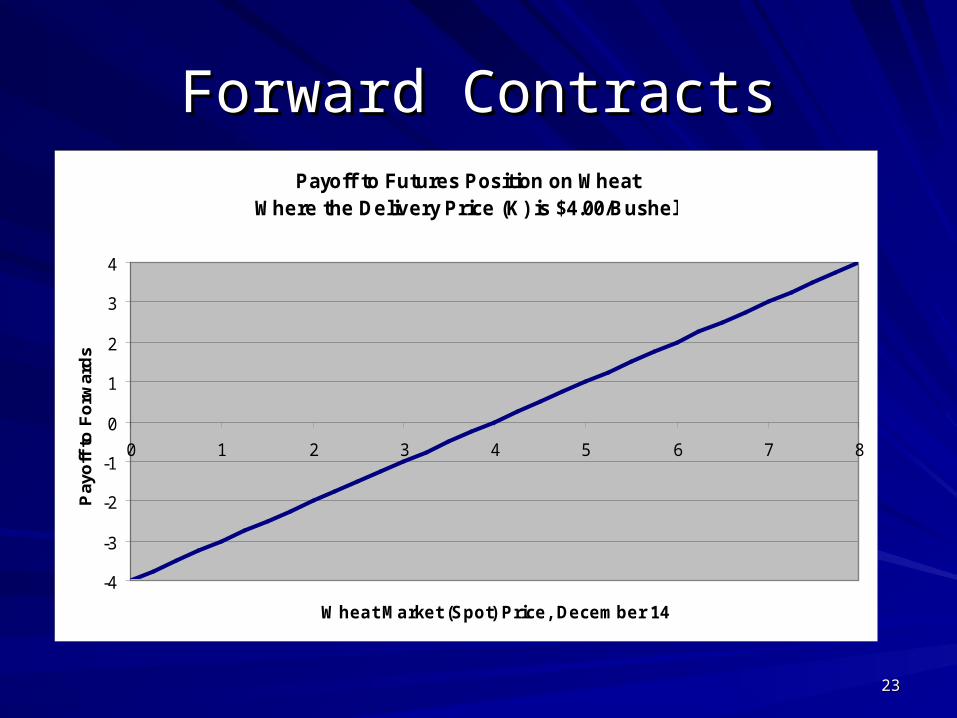

– We can graph the payoff function:We can graph the payoff function:

Forward ContractsForward Contracts

2323

Forward ContractsForward ContractsPayoff to Futures Position on Wheat

Where the Delivery Price (K) is $4.00/Bushel

-4

-3

-2

-1

0

1

2

3

4

0 1 2 3 4 5 6 7 8

Wheat Market (Spot) Price, December 14

Pay

off

to

Fo

rwar

ds

2424

Example:Example:– In this example you were the long party, but what about the short party?In this example you were the long party, but what about the short party?– They have agreed to sell wheat to you for $4.00/bushel on December They have agreed to sell wheat to you for $4.00/bushel on December

14.14.– Their payoff is positive if the market price of wheat is less than Their payoff is positive if the market price of wheat is less than

$4.00/bushel – they force you to pay more for the wheat than they could $4.00/bushel – they force you to pay more for the wheat than they could sell it for on the open market.sell it for on the open market.

Indeed, you could assume that what they do is buy it on the open Indeed, you could assume that what they do is buy it on the open market and then immediately deliver it to you in the forward market and then immediately deliver it to you in the forward contract.contract.

– Their payoff is negative, however, if the market price of wheat is greater Their payoff is negative, however, if the market price of wheat is greater than $4.00/bushel.than $4.00/bushel.

They could have sold the wheat for more than $4.00/bushel had They could have sold the wheat for more than $4.00/bushel had they not agreed to sell it to you.they not agreed to sell it to you.

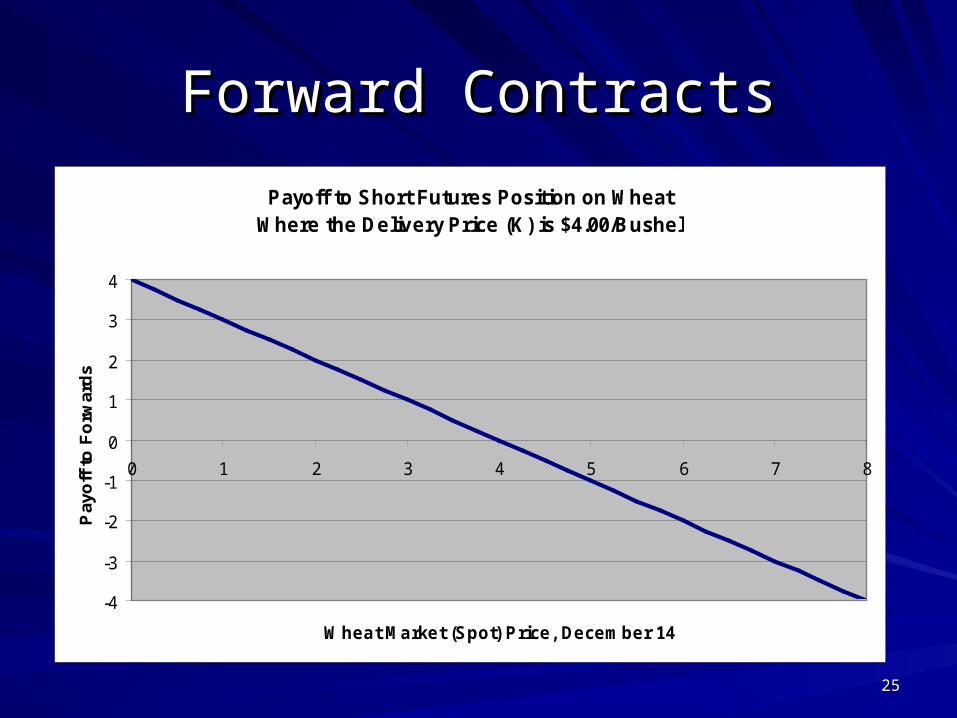

– So their payoff function is the mirror image of your payoff function:So their payoff function is the mirror image of your payoff function:

Forward ContractsForward Contracts

2525

Forward ContractsForward Contracts

Payoff to Short Futures Position on WheatWhere the Delivery Price (K) is $4.00/Bushel

-4

-3

-2

-1

0

1

2

3

4

0 1 2 3 4 5 6 7 8

Wheat Market (Spot) Price, December 14

Pay

off

to

Fo

rwar

ds

2626

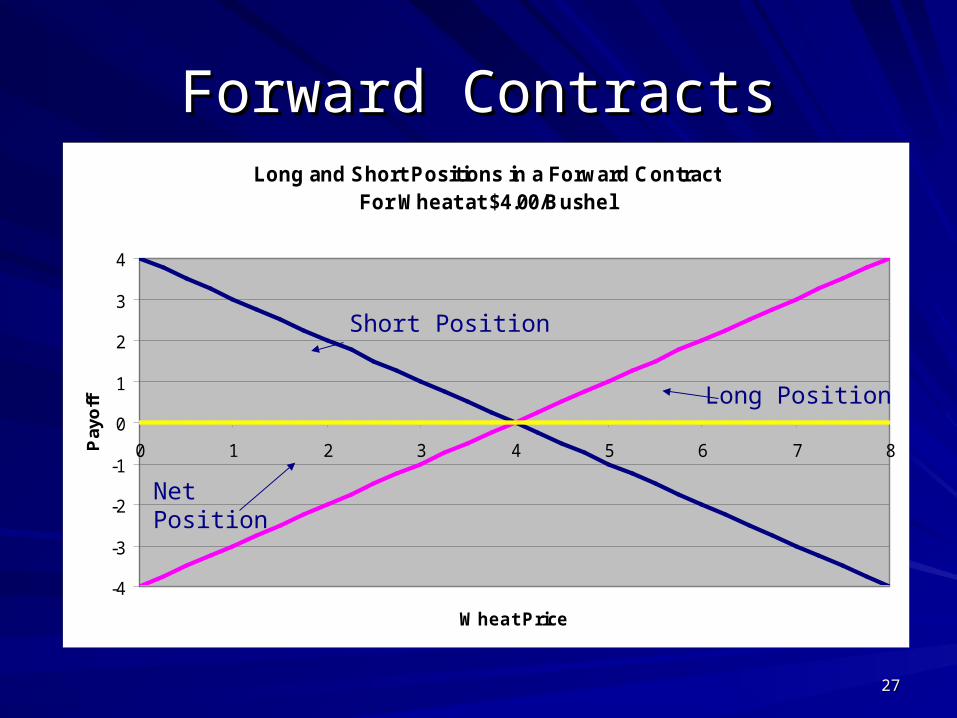

Forward ContractsForward Contracts

Clearly the short position is just the mirror Clearly the short position is just the mirror image of the long position, and, taken image of the long position, and, taken together the two positions cancel each together the two positions cancel each other out:other out:

2727

Forward ContractsForward ContractsLong and Short Positions in a Forward Contract

For Wheat at $4.00/Bushel

-4

-3

-2

-1

0

1

2

3

4

0 1 2 3 4 5 6 7 8

Wheat Price

Pay

off Long Position

Net Position

Short Position

2828

Futures ContractsFutures Contracts A futures contract is similar to a forward contract in that it is an agreement A futures contract is similar to a forward contract in that it is an agreement between two parties to buy or sell an asset at a certain time for a certain price. between two parties to buy or sell an asset at a certain time for a certain price. Futures, however, are usually exchange traded and, to facilitate trading, are Futures, however, are usually exchange traded and, to facilitate trading, are usually standardized contracts. This results in more institutional detail than is usually standardized contracts. This results in more institutional detail than is the case with forwards.the case with forwards.

The long and short party usually do not deal with each other directly or even The long and short party usually do not deal with each other directly or even know each other for that matter. The exchange acts as a clearinghouse. As far know each other for that matter. The exchange acts as a clearinghouse. As far as the two sides are concerned they are entering into contracts with the as the two sides are concerned they are entering into contracts with the exchange. In fact, the exchange guarantees performance of the contract exchange. In fact, the exchange guarantees performance of the contract regardless of whether the other party fails.regardless of whether the other party fails.

2929

Futures ContractsFutures ContractsThe largest futures exchanges are the Chicago Board of Trade (CBOT) and The largest futures exchanges are the Chicago Board of Trade (CBOT) and the Chicago Mercantile Exchange (CME).the Chicago Mercantile Exchange (CME).

Futures are traded on a wide range of commodities and financial assets.Futures are traded on a wide range of commodities and financial assets.

Usually an exact delivery date is not specified, but rather a delivery range is Usually an exact delivery date is not specified, but rather a delivery range is specified. The short position has the option to choose when delivery is made. specified. The short position has the option to choose when delivery is made. This is done to accommodate physical delivery issues. This is done to accommodate physical delivery issues.– Harvest dates vary from year to year, transportation schedules change, Harvest dates vary from year to year, transportation schedules change,

etc.etc.

3030

Futures ContractsFutures Contracts

The exchange will usually place restrictions The exchange will usually place restrictions and conditions on futures. These include:and conditions on futures. These include:– Daily price (change) limits.Daily price (change) limits.– For commodities, grade requirements.For commodities, grade requirements.– Delivery method and place.Delivery method and place.– How the contract is quoted.How the contract is quoted.

Note however, that the basic payoffs are the Note however, that the basic payoffs are the same as for a forward contract.same as for a forward contract.

3131

Options ContractsOptions Contracts Options on stocks were first traded in 1973. That was the year the famous Options on stocks were first traded in 1973. That was the year the famous Black-Scholes formula was published, along with Merton’s paper - a set of Black-Scholes formula was published, along with Merton’s paper - a set of academic papers that literally started an industry.academic papers that literally started an industry.Options exist on virtually anything. Tonight we are going to focus on Options exist on virtually anything. Tonight we are going to focus on general options terminology for stocks. We will get into other types of general options terminology for stocks. We will get into other types of options later in the class.options later in the class.There are two basic types of options:There are two basic types of options:– A A Call optionCall option is the right, but not the obligation, to buy the underlying is the right, but not the obligation, to buy the underlying

asset by a certain date for a certain price.asset by a certain date for a certain price.– A A Put optionPut option is the right, but not the obligation, to sell the underlying is the right, but not the obligation, to sell the underlying

asset by a certain date for a certain price.asset by a certain date for a certain price.Note that unlike a forward or futures contract, the holder of the Note that unlike a forward or futures contract, the holder of the options contract does not have to do anything - they have the options contract does not have to do anything - they have the option to do it or not.option to do it or not.

3232

Options ContractsOptions ContractsThe date when the option expires is known as the exercise date, the The date when the option expires is known as the exercise date, the expiration date, or the maturity date.expiration date, or the maturity date.The price at which the asset can be purchased or sold is known as the strike The price at which the asset can be purchased or sold is known as the strike price.price.If an option is said to be European, it means that the holder of the option can If an option is said to be European, it means that the holder of the option can buy or sell (depending on if it is a call or a put) only on the maturity date. If buy or sell (depending on if it is a call or a put) only on the maturity date. If the option is said to be an American style option, the holder can exercise on the option is said to be an American style option, the holder can exercise on any date up to and including the exercise date.any date up to and including the exercise date.An options contract is always costly to enter as the long party. The short An options contract is always costly to enter as the long party. The short party always is always paid to enter into the contractparty always is always paid to enter into the contract– Looking at the payoff diagrams you can see why…Looking at the payoff diagrams you can see why…

3333

Options ContractsOptions Contracts

Let’s say that you entered into a call option on IBM stock:Let’s say that you entered into a call option on IBM stock:– Today IBM is selling for roughly $78.80/share, so let’s say you entered Today IBM is selling for roughly $78.80/share, so let’s say you entered

into a call option that would let you buy IBM stock in December at a into a call option that would let you buy IBM stock in December at a price of $80/share.price of $80/share.

– If in December the market price of IBM were greater than $80, you If in December the market price of IBM were greater than $80, you would exercise your option, and purchase the IBM share for $80.would exercise your option, and purchase the IBM share for $80.

– If, in December IBM stock were selling for less than $80/share, you If, in December IBM stock were selling for less than $80/share, you could buy the stock for less by buying it in the open market, so you could buy the stock for less by buying it in the open market, so you would not exercise your option.would not exercise your option.

– Thus your payoff to the option is $0 if the IBM stock is less than Thus your payoff to the option is $0 if the IBM stock is less than $80$80

– It is (SIt is (STT-K) if IBM stock is worth more than $80-K) if IBM stock is worth more than $80– Thus, your payoff diagram is:Thus, your payoff diagram is:

3434

Options ContractsOptions ContractsLong Call on IBM

with Strike Price (K) = $80

-20

0

20

40

60

80

0 20 40 60 80 100 120 140 160

IBM Terminal Stock Price

Pa

yo

ff

K =

T

3535

Options ContractsOptions Contracts– What if you had the short position?What if you had the short position?– Well, after you enter into the contract, you have Well, after you enter into the contract, you have grantedgranted the option to the option to

the long-party.the long-party.– If they want to exercise the option, you have to do so.If they want to exercise the option, you have to do so.– Of course, they will only exercise the option when it is in there best Of course, they will only exercise the option when it is in there best

interest to do so – that is, when the strike price is lower than the market interest to do so – that is, when the strike price is lower than the market price of the stock. price of the stock.

So if the stock price is less than the strike price (SSo if the stock price is less than the strike price (STT<K), then the <K), then the long party will just buy the stock in the market, and so the option will long party will just buy the stock in the market, and so the option will expire, and you will receive $0 at maturity.expire, and you will receive $0 at maturity.

If the stock price is more than the strike price (SIf the stock price is more than the strike price (STT>K), however, then >K), however, then the long party will exercise their option and you will have to sell the long party will exercise their option and you will have to sell them an asset that is worth Sthem an asset that is worth STT for $K. for $K.

– We can thus write your payoff as: We can thus write your payoff as:

payoff = min(0,Spayoff = min(0,STT-K), -K),

which has a graph that looks like:which has a graph that looks like:

3636

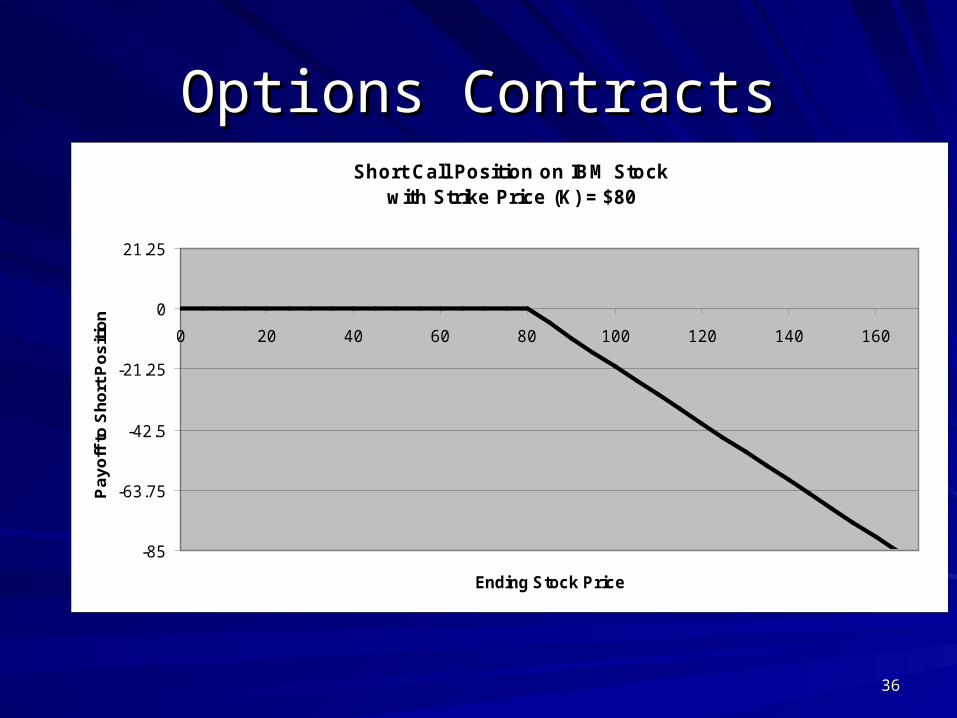

Options ContractsOptions ContractsShort Call Position on IBM Stock

with Strike Price (K) = $80

-85

-63.75

-42.5

-21.25

0

21.25

0 20 40 60 80 100 120 140 160

Ending Stock Price

Pa

yo

ff t

o S

ho

rt P

os

itio

n

3737

Options ContractsOptions Contracts

This is obviously the mirror image of the long position.This is obviously the mirror image of the long position.

Notice, however, that at maturity, the short option position can NEVER have Notice, however, that at maturity, the short option position can NEVER have a positive payout – the best that can happen is that they get $0.a positive payout – the best that can happen is that they get $0.

– This is why the short option party always demands an up-front payment This is why the short option party always demands an up-front payment – it’s the only payment they are going to receive. This payment is called – it’s the only payment they are going to receive. This payment is called the option the option premiumpremium or price. or price.

Once again, the two positions “net out” to zero: Once again, the two positions “net out” to zero:

3838

Options ContractsOptions ContractsLong and Short Call Options on IBM

with Strike Prices of $80

-100

-80

-60

-40

-20

0

20

40

60

80

100

0 20 40 60 80 100 120 140 160

Ending Stock Price

Pay

off

Long Call

Short Call

Net Position

3939

Options ContractsOptions Contracts

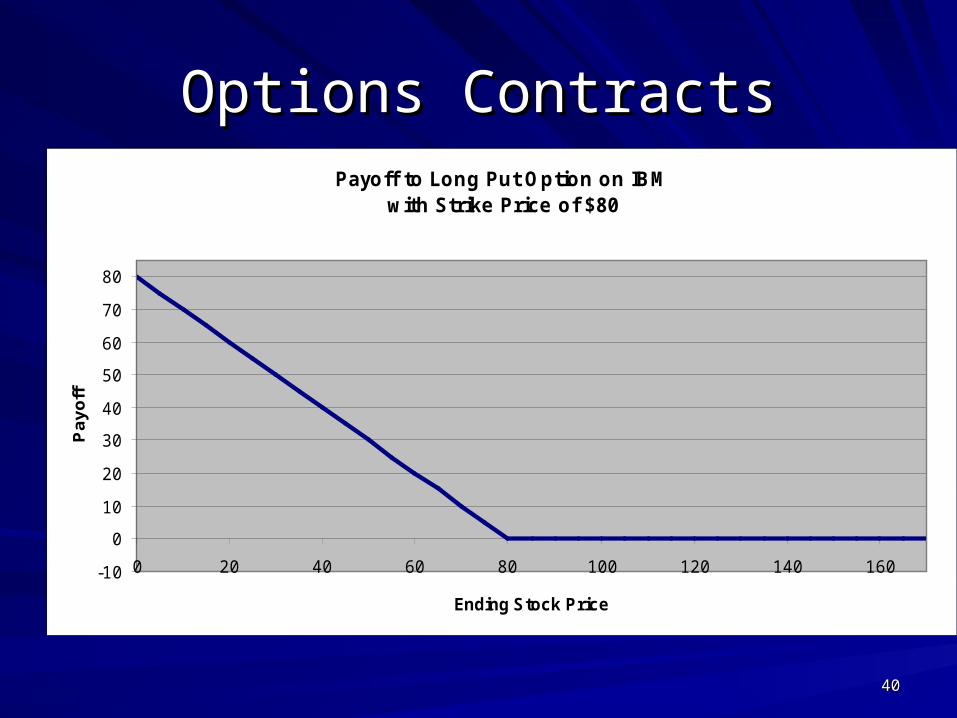

Recall that a put option grants the long party the right to sell the underlying Recall that a put option grants the long party the right to sell the underlying at price K.at price K.

Returning to our IBM example, if K=80, the long party will only elect to Returning to our IBM example, if K=80, the long party will only elect to exercise the option if the price of the stock in the market is less than $80, exercise the option if the price of the stock in the market is less than $80, otherwise they would just sell it in the market.otherwise they would just sell it in the market.

The payoff to the holder of the long put position, therefore is simplyThe payoff to the holder of the long put position, therefore is simply

payoff = max(0, K-Spayoff = max(0, K-STT))

4040

Options ContractsOptions ContractsPayoff to Long Put Option on IBM

with Strike Price of $80

-10

0

10

20

30

40

50

60

70

80

0 20 40 60 80 100 120 140 160

Ending Stock Price

Pa

yo

ff

4141

Options ContractsOptions Contracts

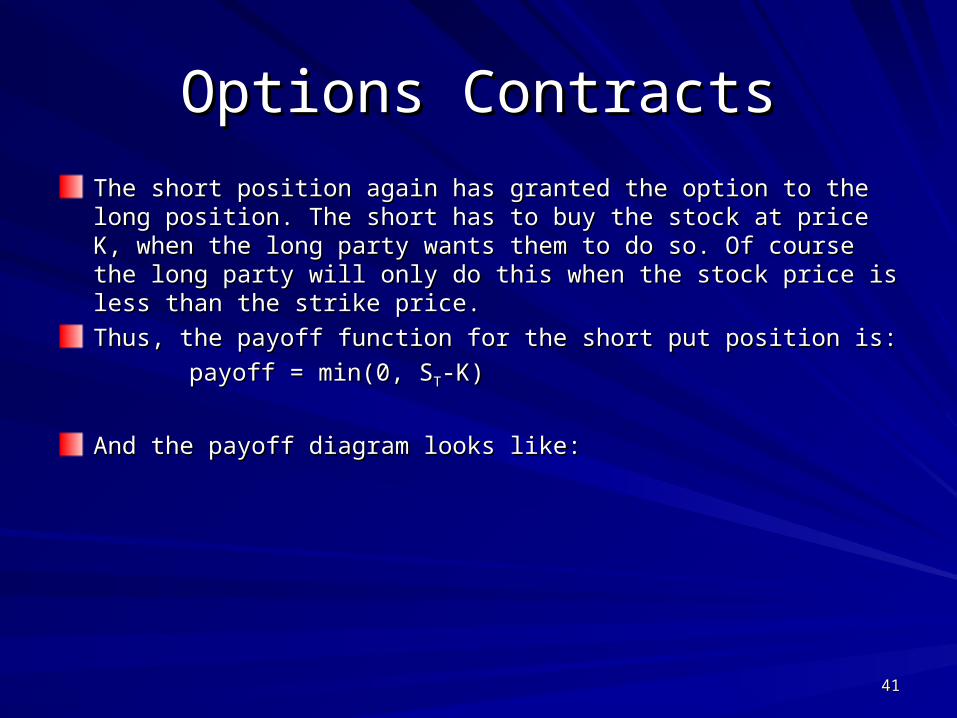

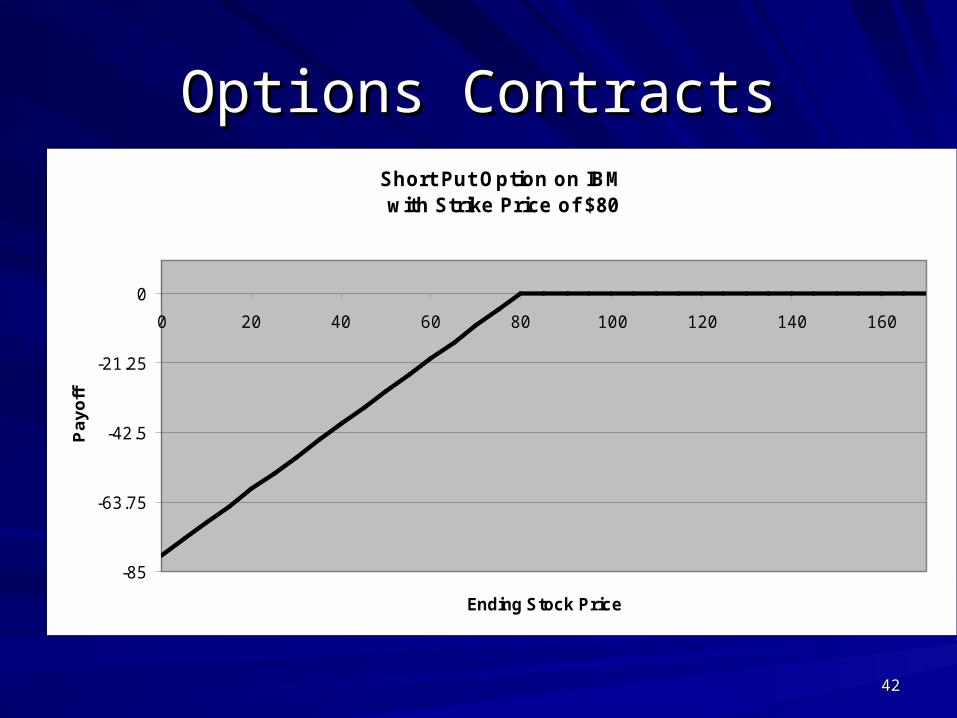

The short position again has granted the option to the long position. The The short position again has granted the option to the long position. The short has to buy the stock at price K, when the long party wants them to do short has to buy the stock at price K, when the long party wants them to do so. Of course the long party will only do this when the stock price is less so. Of course the long party will only do this when the stock price is less than the strike price.than the strike price.

Thus, the payoff function for the short put position is:Thus, the payoff function for the short put position is:

payoff = min(0, Spayoff = min(0, STT-K)-K)

And the payoff diagram looks like:And the payoff diagram looks like:

4242

Options ContractsOptions ContractsShort Put Option on IBMwith Strike Price of $80

-85

-63.75

-42.5

-21.25

0

0 20 40 60 80 100 120 140 160

Ending Stock Price

Pa

yo

ff

4343

Options ContractsOptions Contracts

Since the short put party can never receive a positive payout at maturity, Since the short put party can never receive a positive payout at maturity, they demand a payment up-front from the long party – that is, they demand they demand a payment up-front from the long party – that is, they demand that the long party pay a that the long party pay a premiumpremium to induce them to enter into the contract. to induce them to enter into the contract.

Once again, the short and long positions net out to zero: when one party Once again, the short and long positions net out to zero: when one party wins, the other loses.wins, the other loses.

4444

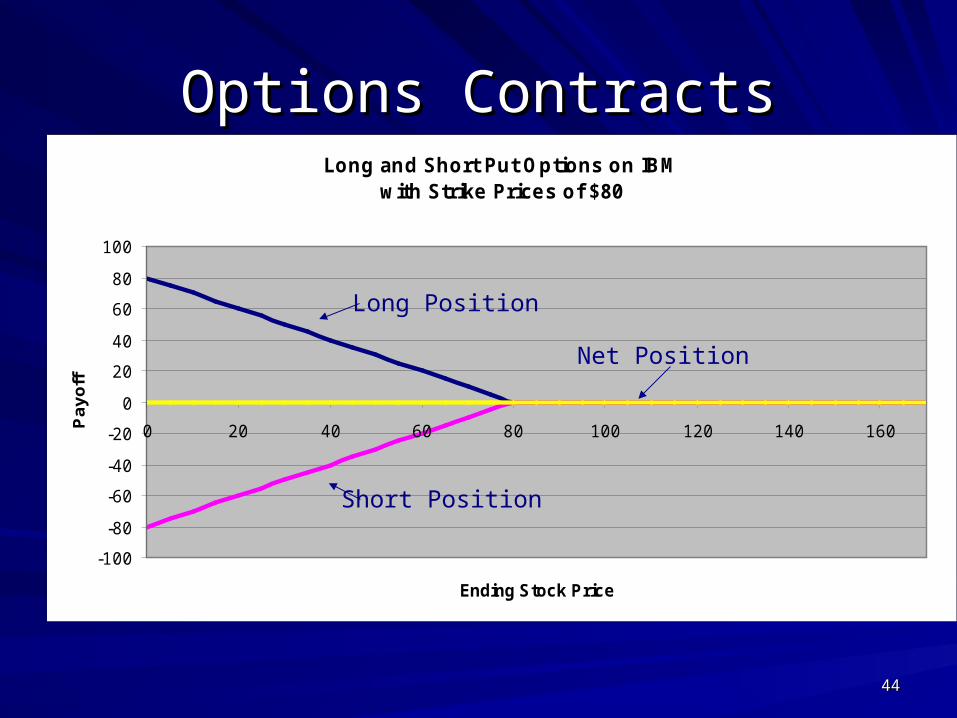

Options ContractsOptions ContractsLong and Short Put Options on IBM

with Strike Prices of $80

-100

-80

-60

-40

-20

0

20

40

60

80

100

0 20 40 60 80 100 120 140 160

Ending Stock Price

Pa

yo

ff

Long Position

Short Position

Net Position

4545

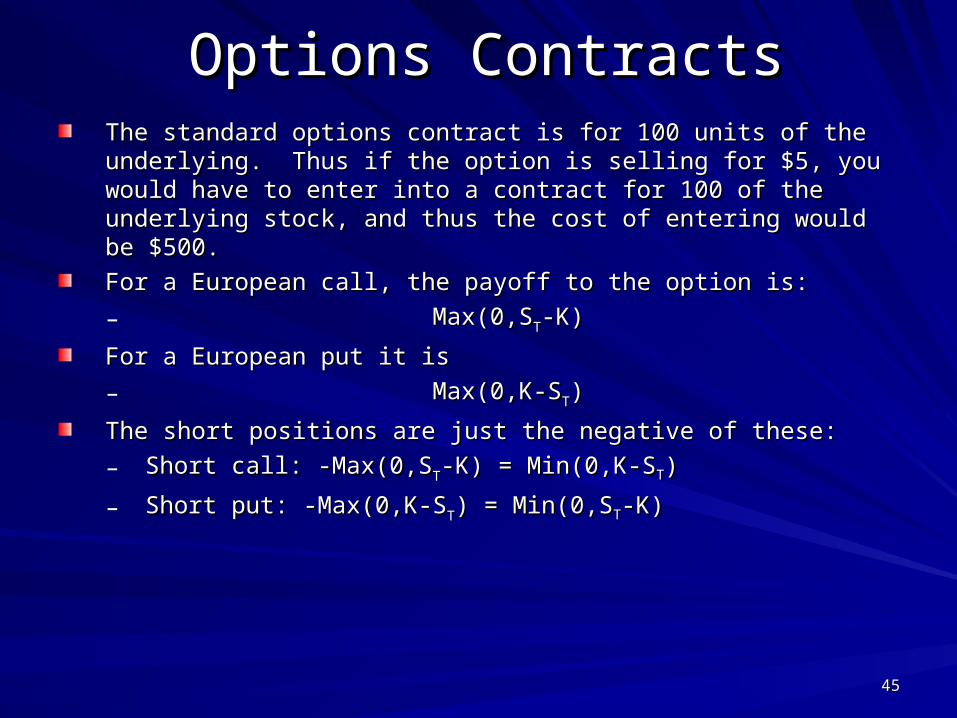

Options ContractsOptions ContractsThe standard options contract is for 100 units of the underlying. Thus if the The standard options contract is for 100 units of the underlying. Thus if the option is selling for $5, you would have to enter into a contract for 100 of option is selling for $5, you would have to enter into a contract for 100 of the underlying stock, and thus the cost of entering would be $500.the underlying stock, and thus the cost of entering would be $500.

For a European call, the payoff to the option is:For a European call, the payoff to the option is:

– Max(0,SMax(0,STT-K)-K)

For a European put it is For a European put it is

– Max(0,K-SMax(0,K-STT))

The short positions are just the negative of these:The short positions are just the negative of these:

– Short call: -Max(0,SShort call: -Max(0,STT-K) = Min(0,K-S-K) = Min(0,K-STT))

– Short put: -Max(0,K-SShort put: -Max(0,K-STT)) = Min(0,S = Min(0,STT-K)-K)

4646

Options ContractsOptions Contracts

Traders frequently refer to an option as being “in the money”, “out of the Traders frequently refer to an option as being “in the money”, “out of the money” or “at the money”. money” or “at the money”. – An “in the money” option means one where the price of the underlying is An “in the money” option means one where the price of the underlying is

such that if the option were exercised immediately, the option holder such that if the option were exercised immediately, the option holder would receive a payout.would receive a payout.

For a call option this means that SFor a call option this means that Stt>K>K

For a put option this means that SFor a put option this means that Stt<K<K– An “at the money” option means one where the strike and exercise An “at the money” option means one where the strike and exercise

prices are the same.prices are the same.– An “out of the money” option means one where the price of the An “out of the money” option means one where the price of the

underlying is such that if the option were exercised immediately, the underlying is such that if the option were exercised immediately, the option holder would NOT receive a payout.option holder would NOT receive a payout.

For a call option this means that SFor a call option this means that Stt<K<K

For a put option this means that SFor a put option this means that Stt>K.>K.

4747

Options ContractsOptions ContractsLong Call on IBM

with Strike Price (K) = $80

-20

0

20

40

60

80

0 20 40 60 80 100 120 140 160

IBM Terminal Stock Price

Pa

yo

ff

K =

T

Out of the money In the money

At the money

4848

Options ContractsOptions Contracts

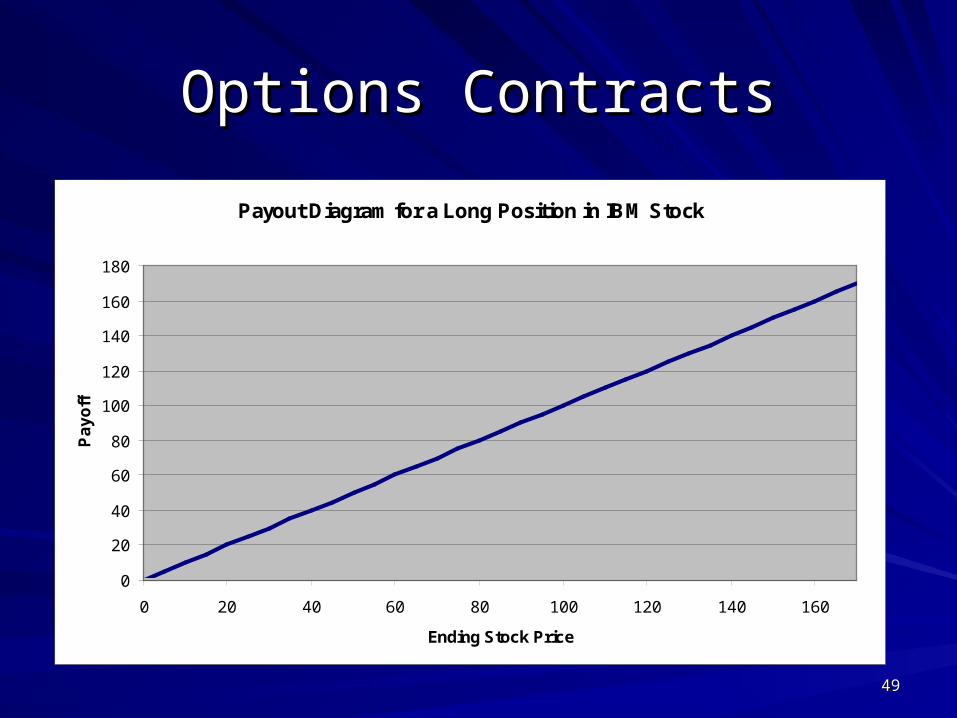

One interesting notion is to look at the One interesting notion is to look at the payoff from just owning the stock – its payoff from just owning the stock – its value is simply the value of the stock:value is simply the value of the stock:

4949

Options ContractsOptions Contracts

Payout Diagram for a Long Position in IBM Stock

0

20

40

60

80

100

120

140

160

180

0 20 40 60 80 100 120 140 160

Ending Stock Price

Pa

yo

ff

5050

Options ContractsOptions Contracts

What is interesting is if we compare the What is interesting is if we compare the payout from a portfolio containing a short payout from a portfolio containing a short put and a long call with the payout from put and a long call with the payout from just owning the stock:just owning the stock:

5151

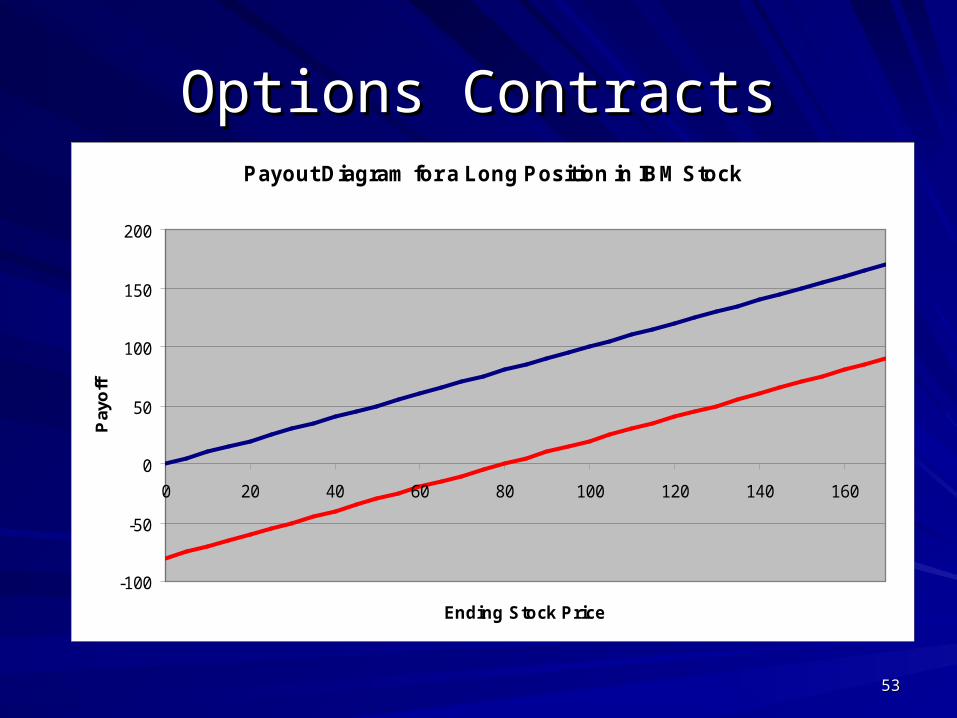

Options ContractsOptions ContractsPayout Diagram for a Long Position in IBM Stock

-100

-50

0

50

100

150

200

0 20 40 60 80 100 120 140 160

Ending Stock Price

Pay

off

Long Call

Short Put

Stock

5252

Options ContractsOptions Contracts

Notice how the payoff to the options portfolio has the same shape and slope Notice how the payoff to the options portfolio has the same shape and slope as the stock position – just offset by some amount?as the stock position – just offset by some amount?

This is hinting at one of the most important relationships in options theory – This is hinting at one of the most important relationships in options theory – Put-Call parity.Put-Call parity.

It may be easier to see this if we examine the aggregate position of the It may be easier to see this if we examine the aggregate position of the options portfolio:options portfolio:

5353

Options ContractsOptions ContractsPayout Diagram for a Long Position in IBM Stock

-100

-50

0

50

100

150

200

0 20 40 60 80 100 120 140 160

Ending Stock Price

Pay

off

5454

Options ContractsOptions Contracts

So who trades options contracts? Generally there are three types of options So who trades options contracts? Generally there are three types of options traders:traders:– HedgersHedgers - these are firms that face a business risk. They wish to get rid - these are firms that face a business risk. They wish to get rid

of this uncertainty using a derivative. For example, an airline might use of this uncertainty using a derivative. For example, an airline might use a derivatives contract to hedge the risk that jet fuel prices might a derivatives contract to hedge the risk that jet fuel prices might change. change.

– Speculators Speculators - They want to take a bet (position) in the market and - They want to take a bet (position) in the market and simply want to be in place to capture expected up or down movements.simply want to be in place to capture expected up or down movements.

– ArbitrageursArbitrageurs - They are looking for imperfections in the capital market. - They are looking for imperfections in the capital market.

![[JP Morgan] Intro to Credit Derivatives](https://static.fdocuments.net/doc/165x107/577d36821a28ab3a6b9348dd/jp-morgan-intro-to-credit-derivatives.jpg)