internship report on IESCO Wapda final project 2014

174

ACKNOWLEDGEMENT ACKNOWLEDGEMENT I take this opportunity to express my profound gratitude and deep regards to my all guides for his exemplary guidance, monitoring and constant encouragement throughout the course of this project. The blessing, help and guidance given by him time to time shall carry me a long way in the journey of life on which I am about to embark. I am thankful to my professors and staff members of IESCO, especially Mr. Naveed Sabir (Assistant Engineer of IESCO for the valuable information provided by them in their respective fields. I am grateful for their cooperation during the period of my assignment. Lastly, I thank almighty, my parents, brother, sisters and friends for their constant encouragement without which this project would not be possible. 1

-

Upload

ilhaan-marwat -

Category

Education

-

view

232 -

download

14

Transcript of internship report on IESCO Wapda final project 2014

ACKNOWLEDGEMENTACKNOWLEDGEMENT

I take this opportunity to express my profound gratitude and deep regards to my all

guides for his exemplary guidance, monitoring and constant encouragement

throughout the course of this project. The blessing, help and guidance given by him

time to time shall carry me a long way in the journey of life on which I am about to

embark.

I am thankful to my professors and staff members of IESCO, especially Mr. Naveed

Sabir (Assistant Engineer of IESCO for the valuable information provided by them in

their respective fields.

I am grateful for their cooperation during the period of my assignment.

Lastly, I thank almighty, my parents, brother, sisters and friends for their constant

encouragement without which this project would not be possible.

1

TABLE OF CONTENT

1. Preface …………………………………………………..…03

2. Executive Summary…………………………………..……04

3. Objective ………………………………………………..…06

4. Overview of UBL ……………………………………..07

5. Vision, Mission…………………………………..…08

6. Nature of Organization……………………………………...09

7. Number of Employees ……………………..…………….…11

8. Board Of Directors …………………………………………15

9. Branches…………………………….…………………..…..19

10. Department………………………………………………….23

11. Structure of Finance/Accounts Department…………………25

12. Critical Analysis …………………………………………….27

13. Financial Analysis of UBL………………………………….29

14. Balance Sheet……………………………………………..… 30

15. Profit & Loss Statement…………………………….………..31

16. UBL Ratio Analysis ………………………………………....32

17. Horizontal Analyses …………………………………………45

18. Vertical Analyses……………………………………………..49

19. Organaizational Analysis……………………………………...51

20. Future Prospects for UBL…………..……………………......52

21. Weakness of Organaization……………………………….....54

22. Conclusion & Recommendations……………………………5423. References & Sources Used…………………………………5524. Annexure……………………………………………….……56

2

PREFACE

"Anything learnt by practice is worthy than by theory."

Our degree is a professional one, and a professional must has technical knowledge,

which is achieved through experiences.

It is the requirement for the completion of MBA degree that the students have to

spend time in an organization as internee after completing most part of his course.

Internship has specific purposes. It provides real life environment to students where

they can implement their knowledge practically, improve their analytic and leadership

skills and enhance their capabilities in different aspect of business field. At the end of

their course they have to write a report as the requirement of degree, which improve

their writing skills.

I did my internship in Wapda (IESCO) Islamabad.

I arranged the contents of this report during my internship and all facts present in this

report are true to my best knowledge.

3

1. Executive Summary:

In this internship report there are five major parts first part consist of

introduction of the organization and also discuss the business volume of the

organization. The second part of this report is organizational structures and discusses

the whole groups that are working in the organization and also describe decision-

making power in this organization. Third part of the report is the resources of the

organization if the resources of the organization are fully utilized than no organization

go to failure and also describe the resources of funds. The fourth part of the report is

very important part that is analysis of financial reports and balance sheet and ratio

analysis of the organization. The last part consists of future prospect, strength,

weakness, conclusion and recommendation for the organization. In last all annexure

are attached with the report.

IESCO was formed in 1998 to take over the assets, functions and responsibilities of

the erstwhile Islamabad Area Electricity Board, which was then a division of

WAPDA.

It services 2.1 million consumers directly, but touches the lives of more than 25 mln

people living in the 6 districts its services.

IESCO Strategic Vision 2012-2015

IESCO committed to providing leadership in sustainable development and

incorporating sustainability principles and identifying alternative and sustainable

courses of action to minimize its environmental impact.

4

IESCO is committed to creating and promoting an environmentally sustainable and

responsible culture and foster continuous improvement in its performance in terms of

its environmental footprint.

IESCO is committed to ensuring the health and wellbeing of its staff. It will put in

place a comprehensive package of wellbeing measures including occupational health

services, employee assistance programmed, a stress management policy and a rolling

programmed of wellbeing and healthy lifestyle events.

IESCO is committed to providing universal health coverage to its staff and their

families and ensuring financial risk protection for healthcare through the most cost

effective and transparent measures. IESCO upholds the principles of equity in doing

so.

5

2. O B J E C T I V E S:

Objective of the study was two pronged.

General Objective:

To get acquaintance to the IESCO operations.

To know what sort of changes management brings in managerial activities.

To see the application of our Professional studies especially.

Specific Objective:

Specific purpose of the study includes.

A partial fulfillment as a requirement for the completion of MBA Degree.

To objectively observe the operations of IESCO in general and the operations

of IESCO in specific.

To make recommendations or implementation plans for the improvement of

the operations of IESCO in the light of our professional studies.

6

3. Overview of Wapda IESCO:

3.1: History of IESCO:

WAPDA, the Pakistan Water and Power

Development Authority, was created in

1958 as a Semi-Autonomous Body for the

purpose of coordinating and giving a

unified direction to the development of

schemes in Water and Power Sectors,

which were previously being dealt with,

by the respective Electricity and Irrigation

Department of the Provinces.

Since October 2007, WAPDA has been bifurcated into two distinct entities i.e.

WAPDA and Pakistan Electric Power Company (PEPCO). WAPDA is responsible

for water and hydropower development whereas PEPCO is vested with the

responsibility of thermal power generation, transmission, distribution and billing.

There is an independent Chairman and MD (PEPCO) www.pepco.gov.pk replacing

Chairman WAPDA and Member (Power) who were previously holding the additional

charges of these posts.

7

We light your life…

8

I sl a m abad E l e c tr i c S u p pl y Co m pany Limited ( I E SCO)

Islamabad Electric Supply Company Limited (IESCO) is a public limited company

incorporated in Pakistan on 25th April 1998 under the Companies Ordinance, 1984.

The company was established to take over all the properties, rights, assets,

obligations and liabilities of Islamabad Area Electricity Board owned by WAPDA,

and such other assets and liabilities as agreed. The company has been granted

distribution license by NEPRA on 2nd November, 2001 for a term of 25 years for

electricity distribution.

IESCO has witnessed significant growth and development in the power sector during

the recent past. IECSO presently serves over 1.90 million customers. IESCO has

been operating at high levels of efficiencies and has been rated as the best

performing Distribution Company in the country as at the close of the financial year

on June 30, 2009 in terms of lowest Progressive Distribution losses with a level of

7.7%.

IESCO was formed as a public limited company, incorporated in Pakistan on 25th

April 1998 under the Companies Ordinance, 1984 to take over the assets, functions

and responsibilities of the erstwhile Islamabad Area Electricity Board, which was then

a division of WAPDA.

IESCO's core function is to supply, distribute and sell power (electricity) in the

licensed area from Attock to Jhelum, and from the river Indus to River Neelum in

Kashmir.

IESCO serves 2.2 million consumers directly, but touches the lives of more than 25

million people living in the 6 districts of its services.

“This business plan will become a road map to chart the course of this objective

explaining the number of areas as to how to achieve this target. It will define

&focus on objective by using appropriate information & analysis.”

9

Vision

To be the most admired public utility in Pakistan,

an undisputed leader in the power sector, efficient

and profitable.

Mission

To provide uninterrupted power supply to our

customers enabling trade and industry,

commerce, educational & social activities to

flourish and enrich the lives of our customers.

To be a socially responsible corporate citizen.

To be the most efficient public utility in

Pakistan.

To achieve the lowest line losses in the

distribution sector.

To be an employer of choice.

10

To generate profits for our stakeholders.

3.2) Nature of organization:

Area Electricity Board (AEB) Islamabad was one of the eight AEB's constituted

through amendments in WAPDA Act during 1981. Later Government of Pakistan

under the Power Sector Restructuring Program approved revamping of WAPDA

power sector, resultantly twelve corporate entities were formed. Eight Distribution

and Supply Companies (DISCOs), one National Transmission and Distribution

Company (NTDC) and three Generation Companies (GENCOs). All these companies

have been incorporated under Companies Ordinance 1984.

IESCO was incorporated on 25th April, 1998 vide company registration No. L09499

of 1997-98 under section 32 and certificate for commencement of business was

obtained on 1st June, 1998 under section 146(2) of Companies Ordinance 1984.

The main objective of the company was to acquire/take over those properties, rights

and liabilities of Pakistan, Water and Power Development Authority comprising of

administrative division formally known as the Islamabad Area Electricity Board

(AEB) and to carry on, expand and extend the business and activities.

11

To play and active role to make “Sar Sabz and Roshan Pakistan”

To facilitate agriculture and industrial sector

To ensure un-interrupted and stable power supply to all customers

State-of-the-art customer care for satisfaction of customers

To provide electricity to every village in jurisdiction of company

To establish, construct and operate reliable electricity distribution network.

IESCO’s Commitment

Improve customer satisfaction

Reduce Line Losses

Weed out corruption

Increase revenue generation

IESCO web site is launched to provide

the best

Customer services

12

Management Philosophy

Open door policy for all

Tackle all problems upfront

Merit, justice, fair play be the hallmark

Transparency in all fields

Accountability of everyone

Corporate Strategy

In the long run the company desires to

become a profit earning concern by

minimizing the line losses and maximizing

the recovery. The company would like to

ensure availability of uninterrupted power

supply to the people of the thirteen districts

under its jurisdiction. To ensure that the

company is well managed and deliver

efficient and quality service to the

electricity consumer at the minimum cost possible.

Culture

IESCO has its own strong culture. The employees own the company.

13

Cover Value:

Business Strategy:

The business strategy is to provide electricity to the consumers at affordable rates.

The domestic consumers using less energy are charge at very low rates. The

commercial, industrial and big domestic consumers are charged very high rates. In

order to develop agriculture sector, subsidies provided and they are charged less rates

as compared to commercial and industrial consumers.

14

Merit Team Work

Efficiency Transparency

Safety

3.3) Breakdown:

Islamabad Circle

Islamabad Division 1 Islamabad Division 2 Barakahu Division

City Circle Rawalpindi

Rawat Division City Division Cantt Division (Rawalpindi) Satellite Town Division Westridge Division Tariqabad Division

Attock Circle

Taxila Division Pindigheb Division Attock Division

Chakwal Circle

Chakwal Division Talagang Division Dhudial Division Pind Dadan Khan Division

Jhelum Circle

Jhelum Division 1 Jhelum Division 2 Gujar Khan Division

15

Organizational Setup

Chief Executive Officer is the executive head responsible for efficient and effective running of the company. His team includes eight executive Directors:

Finance Director/Company Secretary Chief Engineer/Technical Director Chief Engineer/Operation Director Chief Engineer (Development) PMU Chief Engineer (P&E) Human Resource and Administration Director / Director General Chief Engineer / Customer Service Director Chief Engineer (O&M) T&G GSO

Other Manage rates

Manager Customer Services

Manager Material Management

Manager L&L

Manager Construction, Maintenance and Operation

Manager Grid System Operation

Manager Public Relation

Manager Computer Operation

Project Manager Construction Operation

Regional Manager Metering and Testing

Operational Setup

To ensure uninterrupted supply of electricity and most intimate customer services

IESCO is divided into four Circles, 19 Divisions and 94 Subdivisions.

Circle is headed by Superintending Engineers (SEs), Divisions are managed by

Executive Engineers (XENs) and Subdivisions are run by Sub Divisional Officers

(SDOs). Each division has a Customer Services Officer (CSO).

16

Area of Operation

Looks after the electricity distribution network in the administrative districts of

Rawalpindi, Chakwal, Attock, Jhelum and Federal Capital Islamabad.

17

GSO Circle 01

Operations Divisions 19

Operations Sub Divisions 102

Project directors Const/GSC 1 each

GSO/GSC/Tech Services Divisions 04 each

Construction Division 05

Construction Sub Division 18

18

3.4) Number of Employees:

S.# Category Distribution GSO Total

01 Officers Gr-18 & above 151 10 161

02 Assist: Managers 256 31 287

03 Assist: Managers (C.S) 25 0 25

04 LS-I 479 23 502

05 LS-II 408 5 413

06 SSO-I 1 109 110

07 SSO-II 1 218 219

08 Foreman 3 21 24

09 LFM-I (Foreman) 35 0 35

10 LFM-II (Foreman) 37 1 38

11 Commercial Assistant 637 0 637

12 LM-I (Lineman) 1559 63 1622

13 LM-II (Lineman) 1497 83 1580

14 ALM (Asstt: Lineman) 4154 53 4207

15 Meter Reader 1637 0 1637

16 Bill Distributor 440 0 440

17 Chowkidar / NQ 850 40 890

18 Clerks all types 957 24 981

19 Other Staff 2016 1369 3385

Grand Total 15143 2050 17193

19

4.) Organizational Structure:

4.1) Head Office:

WAPDA, the Pakistan Water and Power Development Authority, was created

in 1958 as a Semi-Autonomous Body for the purpose of coordinating and giving a

unified direction to the development of schemes in Water and Power Sectors, which

were previously being dealt with, by the respective Electricity and Irrigation

Department of the Provinces.

Since October 2007, WAPDA has been bifurcated into two distinct entities i.e.

WAPDA and Pakistan Electric Power Company (PEPCO). WAPDA is responsible for

water and hydropower development whereas PEPCO is vested with the

responsibility of thermal power generation, transmission, distribution and billing.

There is an independent Chairman and MD (PEPCO) www.pepco.gov.pk replacing

Chairman WAPDA and Member (Power) who were previously holding the additional

charges of these posts.

20

4.2) Geographical Map:

21

5). Board of Directors

Prime Minister of Pakistan has been pleased to approve reconstitution of IESCO Board Members. IESCO BOD consists of a blend of very experienced persons from Government/WAPDA and private sector.

22

Board of Directors

23

5.1) Attendance of Board MeetingsThe Board met eight (08) times during the FY-2011-12 an average participation of 74% of its members. The members' participation of the Board Meetings is:

N a m e Meetings * Attendance

Mr. Mohsin Khalid, Chairman 8 8

Mr. Javed Parvez, CEO/Director 8 6

Mr. Tariq Sadiq, Director 8 8

Asjad Imtiaz Ali, Director 8 8

Lt. Gen (R) Muhammad Asghar, Director 8 4

Mr. Muhammad Khalid Qureshi, Director 8 4

Dr. Sania Nishtar, Director 8 5

Mr. Farid Rehman, Director 8 3

Mr. Jawed Akhtar Bhatti, Director 6 5

Mr. Yassar Sakhi Butt, Director 6 5

Mr.Amjad Ali Khan, Director 2 2

Mr. Shahid Hussain Raja, Director 6 3

Mr.Mehfooz Ellahi, Director 2 2

Syed Ali Raza Saeed Shah, Director 2 2

88 65

24

Board of Director

Board Operations and Finance Committee Board Human Resource

CommitteeBoard Audit Committee

Chief Executive Officer

Executive Management

25

5.2) Auditing Committee

The Auditing Committee supervises all the operations and accounts of the IESCO.

The Office of the Governor is obliged to furnish all the information and documents

requested by the Auditing Committee. The Auditing Committee, having no

administrative power, submits its opinions in writing to the Board and also presents a

copy thereof to the Prime Ministry. The Committee submits to the General Assembly

a report to be drawn up on the operations and accounts of the IESCO as at the end of

the year. Members of the Auditing Committee serve for a term of two years. Members

of the Auditing Committee may not share in the profits of the IESCO.

5.3) Risk Management Committee of Board

The department is responsible for assessing and controlling the financial and

operational risks associated with the financial and real-estate investments of the

IESCO's capital, foreign exchange reserves, supplementary pension fund and other

euro and foreign currency portfolios.

It monitors decisions regarding the strategic allocation and tactical management of the

IESCO's portfolios and the supplementary pension fund.

It examines the methods of assessing and controlling financial risks, measures the

degree of risk present in the IESCO's portfolios and checks compliance with the limits

imposed on their management.

It oversees the management of the IESCO's equity holdings, including their risk

profile.

It is also responsible for assessing the risks associated with assets provided as

collateral for financing transactions.

26

5.4) Human Resources Manager

1. HR manager and his department is responsible provides proposals to the top

management for setting the IESCO’s personnel policy and for its effective

application;

2. recruits the personnel suitable to the IESCO’s needs, determines their

employment conditions and employs them in the organization according to

their qualifications;

3. conducts and follows the matters of all kinds pertaining to personnel;

4. executes the preparatory works for determination and development of the

remuneration policy;

5. informs the employees of the regulation pertaining to personnel, personal

rights, and social security;

6. Makes arrangements in the organization of the IESCO in order to increase the

productivity of operations, to cut the costs, to enhance the service quality and

develops the appropriate methods to this end.

7. conducts job analysis, job and task descriptions and their standardization

works; develops and implements the ways that set the productivity standards

of the employees and conducts analysis on the training needs of the personnel;

8. develops an effective training system in accordance with the IESCO’s general

objective and policy as well as technological, economic and social

developments, conducts research in this area, prepares, implements and

evaluates the training plans and programs.

27

Billing & Collection Profile:

28

Transmission lines and grids:

29

T & D Line Losses:

Transmission Losses:

Distribution Losses:

30

6). Board Committees Formulation:

Various committees comprising of honorable Board Members preferably from the

relevant field of expertise have been formulated to accord necessary approvals and

have a keen look into the day to day affairs of the company.

6.1) Auditing Committee:

The present Auditors M/S Taseer Hadi & co. Chartered Accountants retired and have

completed 12th years as Auditor have offered themselves for re-appointment.

Auditors' Report to the Members:-

We have audited the annexed balance sheet of Islamabad Electric Supply Company

Limited the Company as at 30 June 2012 and the related profit and loss account,

statement of comprehensive income, cash flow statement and statement of changes in

equity together with the notes forming part thereof, for the year then ended and we

state that we have obtained all the information" and explanations which, to the best of

our knowledge and belief, were necessary for the purposes of our audit.

It is the responsibility of the Company's management to establish and maintain a

system of internal control, and prepare and present the above said statements in

conformity with the approved accounting standards and the requirements of

Companies Ordinance, 1984. Our responsibility is to express an opinion on these

statements based on our audit.

We conducted our audit in accordance with the auditing standards as applicable in

Pakistan. These standards require that we plan and perform the audit to obtain

reasonable assurance about whether the financial statements are free of any material

misstatement. An audit includes examining on a test basis, evidence supporting the

amounts and disclosures in the above said statements.

An audit also includes assessing the accounting policies and significant estimates

made by management, as well as, evaluating the overall presentation of the above said

statements.

31

We believe that our audit provides a reasonable basis for our opinion and, after due

verification, we report that:

a) The Company's management based on its interpretation of the short order of

Honorable Islamabad High Court dated 24 October 2012 has not reversed electricity

sales the revenue amounting to Rs.14, 554.34 million relating to the years from 30

June 2009 to 2012.

Had the electricity sales been reversed, loss for the year ended 30 June 2012 would

have increased by Rs.9, 634.28 million with the effect of reversal of electricity sales

for the year ended 30 June 2012 and Rs.4, 920.06 million with the effect of reversal of

electricity sales relating to prior years and accumulated loss as at 30 June 2012 would

have increased by Rs.14, 554.34 million.

b) In our opinion:

i) Except for the effect of the matter described in paragraph (a) above, the balance

sheet and profit and loss account together with the notes thereon have been drawn up

in conformity with the Companies Ordinance, 1984, and are in agreement with the

books of account and are further in accordance with the accounting policies

consistently applied.

ii) The expenditure incurred during the year was for the purpose of the Company's

business and

iii) The business conducted, investments made and the expenditure incurred during

the year were in accordance with the objects of the Company;

c) The balance sheet, profit and loss account, statement of comprehensive income,

cash flow statement and statement of changes in equity together with the notes

forming part thereof conform with the approved accounting standards as applicable

in Pakistan, and give the information required by the Companies Ordinance, 1984, in

the manner so required and respectively give a true and fair view of the state of the

Company's affairs as at 30 June 2012 and of the loss, its cash flows and changes in

equity for the year then ended.

32

Where it has been explained along with the other matters that the management has

taken up the matter of long outstanding receivable of Rs.10,076 million from the

Government of Azad Jammu and Kashmir (GoAJK) with the Ministry of Water and

Power, Government of Pakistan (MOW&P) and MOW&P has confirmed that the

matter is under deliberation with Ministry of Finance and GoAJK and early

settlement is expected.

Further MOW&P in a meeting with the Chief Executives of distribution companies

has instructed note to recognized provision against this receivable as there are bright

chances of recovery of this amount. Accordingly the management is confident of

complete recovery of this amount. Our opinion is not qualified in this regard.

4.4) Self Generation:

Keeping in view the worst Energy crisis prevailing in the country at present and due

to mounting public pressure on DISCO's dealing the end consumers, the management

of company may think to go for self-generation in the upcoming years.

4.5) Enterprise Resource Planning:

IESCO's Management is enthusiastically heading towards implementation of ERP and

all possible efforts are being carried out to implement ERP during 2012-2013.

33

4.6: Reports

1. Income Statement

Income statement or report of income, indicate the amount of revenue received and

expenses incurred over a specific period of time. Income statement is record of

financial flow over time. Actual income report is usually more complicated than this

simple statement because each item may have several component accounts. Its

major’s items are:

Interest IncomeInterest Expense Non Interest IncomeNon Interest Expense

So, the difference between all revenues and expenses is net income. Thus:

Net income = Total revenue items – Total expense items

IESCOs take deposits from savers and pay interest on some of these accounts. They

pass these funds on to borrowers and receive interest on the loans. Their profits are

derived from the spread between the rate they pay for funds and the rate they receive

from borrowers. This ability to pool deposits from many sources that can be lent to

many different borrowers creates the flow of funds inherent in the IESCO system. By

managing this flow of funds, IESCO generate profits, acting as the intermediary of

interest paid and interest received, and taking on the risks of offering credit.

2. Balance Sheet

IESCO’s balance sheet displays the yield generated from earning assets and interest

bearing deposits. IESCO provide first of all, the balance sheet a balance of Assets,

Liabilities and equity items balance at the end of the period. Balances provide for

better analytical framework to help understand the financial performance. Balance of

Assets, Liabilities and equity item there is a corresponding cash, loan, deposit,

advances reveres etc.

3.

34

3. Loan Report

Loan/Credit reports is prepare for mortgage rates, credit card approvals and apartment

requests. Reviewing credit reports helps management catch signs of identity theft

early. Loan report contain following information:

Which type of loan sanction

Volume of loan

Time line

Up to date on loans

4. Compliance Report

Statement of compliance of IESCO is prepared in accordance with the approved

accounting standards as applicable in Pakistan. Approved accounting standards

comprise of such International Financial Reporting Standards (I FRS) issued by the

International Accounting Standards Board and Islamic Financial Accounting

Standards issued by the Institute of Chartered Accountants of Pakistan as are notified

under the Companies Ordinance, 1984, provisions of and directives issued under the

Companies Ordinance, 1984.

5: FINANCIAL RISK MANAGEMENT

The Company has exposure to the following risks from its use of financial instruments:

Credit riskLiquidity riskMarket risk

This note presents information about the company's exposure to each of the above

risks, the Company's objectives, policies and processes for measuring and managing

risk and management of capital. Further quantitative disclosures are included

throughout these financial statements.

35

5.1. Risk management frame work:

The Board of Directors has overall responsibility for the establishment and oversight

of the Company's risk management framework. The Board is responsible for

developing and monitoring the Company's risk management policies.

The Company's risk management policies are established to identify and analyze the

risks faced by the Company, to set appropriate risk limits and controls, and to

monitor risks and adherence to limits. Risk management policies and systems are

reviewed regularly to reflect changes in market conditions and the Company's

activities. The Company, through its training and management standards and

procedures, aims to develop a disciplined and constructive control environment in

which all employees understand their roles and obligations.

The Company's Board oversees how management monitors compliance with the

company's risk management policies and procedures and reviews the adequacy of

the risk management framework in relation to the risks faced by the Company. The

Board is assisted in its oversight role by Internal Audit. Internal Audit undertakes

both regular and ad hoc reviews of risk management controls and procedures, the

results of which are reported to the Board.

5.2: Credit risk:

Credit risk is the risk of financial loss to the Company if a consumer or counterparty

to a financial instrument fails to meet its contractual obligations. The Company is

exposed to credit risk to the extent of loans, deposits and advances, trade debts,

interest accrued, other receivables and IESCO balances. The Company deals with

regular and permanent consumers who normally make payments on time.

36

The Company controls its credit risk by continuous monitoring of its receivables. The

management believes that there is no credit risk involved in respect of receivables

from the Government of Pakistan.

5.3: Market risk

Market risk is the risk that changes in market prices, such as foreign exchange rates,

interest rates and equity prices will affect the company's income or the value of its

holdings of financial instruments. The objective of market risk management is to

manage and control market risk exposures within acceptable parameters, while

optimizing the return. The Company is exposed to currency risk and interest rate risk

only.

37

5.4: Exposure to currency risk

The Company is exposed to currency risk on long term loans in a currency other than

the respective functional currency of the Company, primarily in U.S. Dollars. The

Company's exposure to foreign currency risk is as follows:

6: BRANCH:

6.1 : Account Officer

An account officer is responsible to look after the financial part of IESCO. He is also

given the responsibility of financial planning and record keeping of all the account.

Essential Duties:

The main purpose of an account officer is to analyze financial activities.

He is also responsible for promotion of all the products.

An account officer maintains the growth targets of finance in IESCO.

Helps in solving due accounts of the past.

The looks after managing financial risks.

He reviews all the necessary documents to avoid disputes.

If any financial problem arises, it is his duty to look after the matter and solve it.

He is responsible for all the client communications.

38

Account officers prepare the budget for the IESCO they are working under. He

compares previous year's budgets and tries to improve the drawbacks.

They should be prepared to lead during crisis.

An account officer must maintain payments and receipts.

He must ensure all the bills are paid properly.

He files of return in FBR.

Another important duty of an account officer is to look whether all the audit

objectives and audit statements are responded properly.

He should allocate works to staffs according to workload.

Look after weekly/monthly reports.

6.2: Clearing Officer

Compiles settlement data and submits checks, drafts, and other items to clearinghouse

association for exchange and settlement with other IESCOs: Sorts items into bundles,

lists items, and totals amounts, using adding machine or calculator. Clearing officer

posts totals to clearinghouse settlement sheet.

Mails or delivers items to clearinghouse. Accepts items from clearinghouse that have been drawn on own IESCO and posts totals on settlement sheet. Totals debit and credit columns and computes net balance. Clearing officer have submits sheet to clearinghouse for verification. May maintain telephone contact with IESCO personnel and others to locate missing checks, correct errors, and reconcile differences in records.

Essential Duties:

Outward clearing: Receive and verify outward cheques from branches and

process them for clearing

Inward clearing: Attend clearing house sessions to collect inward cheques and

thereafter post and distribute them to branches

On a daily basis balance Head Office clearing accounts

Processing EFTs: Collect and process EFT’s from inter IESCO and other WAPDA

branches by attending the clearing house sessions and thereafter credit the

corresponding beneficiary customer account.

Processing Telegraphic Transfers by assist customers in filling in Telegraphic

Transfers form instructions

Process Telegraphic Transfers instructions in SWIFT system

39

Prepare daily and monthly Exchange report to Head office

Process funds transfers (both internal and inter branch) as instructed by State

IESCO Pakistan

Reconcile cheques both inward and outward on head office clearing account

and IESCO clearing statement

Liaise with the reconciliation officer to point out outstanding transactions

6.3: Cashier

A teller is an employee of IESCO who deals directly with most customers. In some

places, this employee is known as a cashier. In IESCO teller jobs require cash

handling experience and a high school diploma. Most IESCO provide on the job

training.

Primary fun actions are:

Cashing cheques

Checking statements

Processing payments

Making money transfers

Updating account details

This is because they are the first people that a customer sees at the IESCO and are

also the people most likely to detect and stop fraudulent transactions in order to

prevent losses at IESCO (counterfeit currency and checks, identity theft, confidence

tricks, etc.). In IESCO also requires tellers to be friendly and interact with the

customers, providing them with information about customers' accounts and IESCO

services.

Tellers work from a station, usually located on a Teller Line. Most stations have:

A teller system, which includes cash drawers, receipt validate/printers, proof work

sorters, and paperwork used for completing IESCO transactions.

40

These transactions include:

Check cashing, depositing, transfers, wire transfers

Receive checking and savings deposits: verify cash and endorsements, receive

proper identification for cash back, and issue receipts of deposit.

Examine checks deposited and determine proper funds availability based on

regulation requirements and complete Hold Notices.

Answer basic customer inquiries regarding interest rates, service charges, and

account histories while complying with disclosure requirements, regulations

and consumer privacy policies.

Cross-sell IESCO products and services.

Issuing negotiable items (cashier's checks, traveler's cheques, money orders,

federal draft issuances, etc.)

Payment collecting

Savings bond purchase or redemption

Resolving customer issues

6.4 : Customer Service Officer

A Customer Service Officer at IESCO, often known as a new accounts representative,

helps customers set up new checking, savings, and investment accounts. Even though

they work with loan officers to meet client needs, they usually only help with

preliminary customer requests and general product offerings but don't perform

underwriting duties or finalize loans.

41

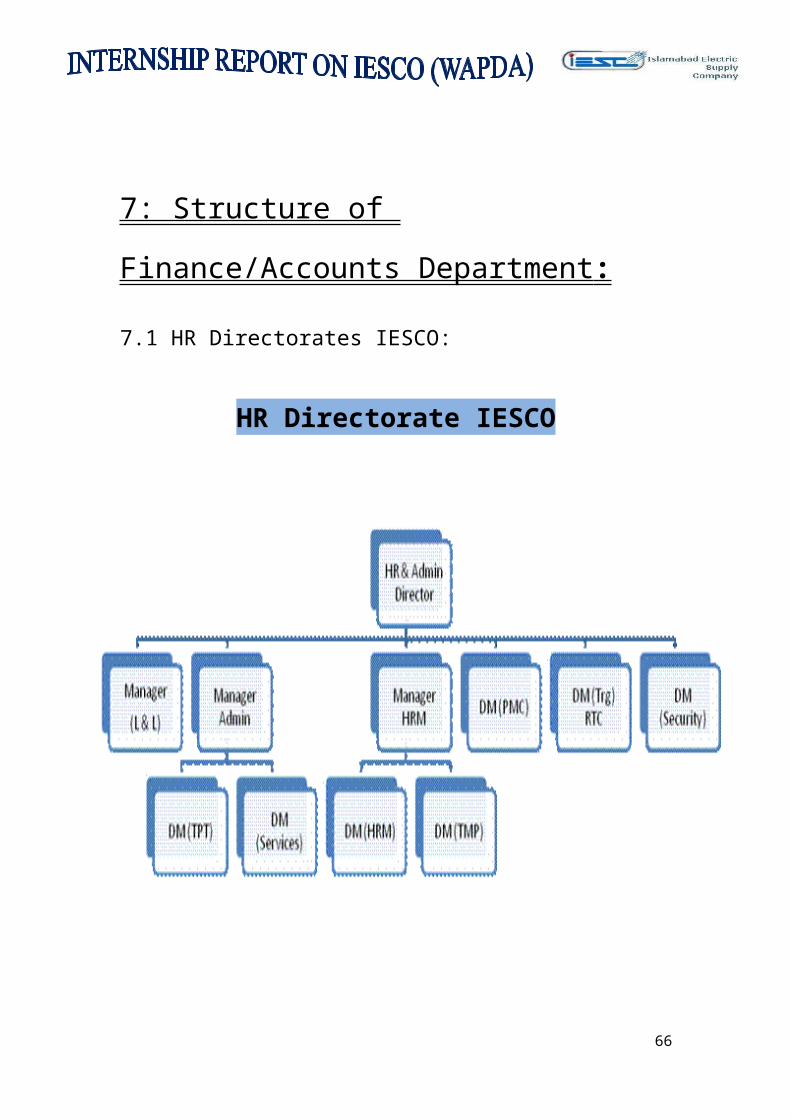

7: Structure of Finance/Accounts Department :

7.1 HR Directorates IESCO:

HR Directorate IESCO

42

Operation Directorate

The basic tasks performed by the operation directorate are:

Operation and maintenance of distribution system

Operation and maintenance of sub-transmission and grid systems

The Directorate consists of the following departments: -

O&M (T&Gs) Department

The Operation & Maintenance (Transmission and Grid Stations) - O&M (T&Gs)

department headed by a Senior Manager is responsible for the electrical network at

132KV and 66KV and has under its purview 67 132KV and 15 66KV Grid Stations

and 1515 KMs of 132KV and 628 KMs of 66KV lines. The department carries out its

functions in the field through the Superintending Engineer (Grid System Operation)

SE (GSO) by issuing guidelines, schedules and authorization for the preventive and

emergency maintenance programs, and carries out frequent inspection to ensure

compliance by the field organization.

O&M (Dist) Department

The Operation & Maintenance (Distribution) - O&M (Dist) department

headed by a Senior Manager, is responsible for the electrical system at 11KV and

400V. Policy guidelines, schedules and authorization for maintenance of feeders are

issued to the 6 operating circles in the field headed by then Superintending Engineers

and frequent inspections are carried out to ensure compliance. The department also

has a civil engineering division headed by an Executive Engineer for the design,

construction and maintenance of all the buildings of IESCO.

43

Technical Services Department

The Technical Services Department carries out the testing, calibration and

repair of all the energy meters, and also the installation of the maximum demand

meters. It is headed by 02 Managers who have 03 distribution circles each as their

areas of responsibility.

PDC Department

The Power Distribution Control Department headed by an Executive Engineer

has been set up to monitor the entire electrical network of IESCO round the clock.

Information about the supply breakdowns, major equipment damages and occurrences

of importance are received through telephone and fax from the field and are

transmitted to the highest level in IESCO and WAPDA, and then instructions are

passed for situation management.

Safety Department

The Safety Department headed by a Deputy Manager ensures that the system

is operated in compliance with the statutory provisions regarding safety for the

employees and the public. Frequent inspections are carried out and safety parades by

the employees are held to ensure that working practices are safe and the employees

are adequately trained in safety measures. Every accident occurring to an employee,

member of public or animal is investigated meticulously and lessons learnt and

disseminated.

In order to update the assets information and to monitor the efficacy of its

operation, maintenance and safety policies and programs related to the entire IESCO

electrical network, the following returns are prepared and issued.

44

Technical Services and Operations

M&T organization is one of the most important departments in IESCO, the

company revenue depends on accurate functioning of its cash box i.e., energy meter,

M&T deals with checking installation, testing and re-calibration of energy meters the

importance of M&T can’t be over emphasized. It also attends any fault in metering

equipment involving panels, MDI meter, C.Ts, P.Ts or cable and this ensures

continuity of supply to consumer using electricity in bulk. The low losses in B-2 & B-

3 units of IESCO speak volumes for efficiency of M&T department. It has dedicated

and devoted staff and ready for duty at call at any time. This department also enables

operation wing to reutilize defective T&P meters and thus saving a large amount of

revenue by repairing these meters.

Material Management Directorate

Pre qualification and Registration of firms for supply of distribution / GSO Material

Procurement of material through tender Disposal of unserviceable material / vehicles

through tender and auction Formation of rate contract for regular supply of material

with firms.

Arrangement of all kinds of material including T&P items from other DISCOs as per

requirement of field formations.

Maintaining of minimum and maximum level of material in stores

Issuance of material as per requirements of field formation

(A) Private New Connection & Extension of Load

(B) Government Connection

(C) Housing Schemes

(D) Others Works

45

Training Centers

IESCO also provides refresher courses to the employees for working in

computer based and modern systems. The newly induced employees are enrolled for

newly induction program and they are trained for IESCO environment and systems.

Since the situation of Law and Order is very spoil in our county therefore security

staff of the IESCO is also provided refresher courses to familiar with advance security

systems and arms. For this purpose a Training center is established in 220KV Grid

Station Bund Road Lahore. All the newly induced officials and officers are required

to pass their newly induction courses. The departmental promotion exams and training

is also performed in this center.

Customer Services Directorate

The tasks assigned to Customer Services Directorate in IESCO are:

Implementation of Commercial Policies

Monitoring and management of recovery process

Monitoring of line losses and preparation of accurate line losses statements

Settling consumer disputes involving technical, commercial and tariff issues

Processing and monitoring policies and procedures for Customer Services

Processing/sanctioning of various incentives for customers and employees

introduced from time to time.

Effective marketing of electricity

Tariff structuring and management of other tariff related matters

Compilation of statistical data and management returns

Co-ordination with Manager MIS for regulating effective billing program

Surveillance and detection of electricity theft

Taking effective measures for prevention of electricity theft

46

8: CRITICAL ANALYSIS:

Risk Framework of IESCO

Almost all of the IESCO explain their risk management framework in their annual

reports. Management of risk is a core function of IESCO. The reason is that it

performs vital activities of measuring, monitoring, controlling and reporting credit,

market, liquidity and operational risks. According to the Annual Report 2010 of

IESCO the economic and security situation witnessed by Pakistan during 2010

demanded further strengthening of the IESCO's internal risk and management

controls through a renewed focus on special asset and portfolio management. In order

to be in a better position to respond to all the challenges faced by the IESCO and to

effectively monitor and control the resulting shocks the Risk Management Framework

was revitalized through integrated risk management approach for managing credit

risk, market risk, liquidity risk and operational risk. A dedicated Risk Management

Division (RMD) is in place with the General Manager of RMD department reporting

directly to the Chief Executive Officer. Risk Management Division has been

structured to address credit, market, IT and operational risk. This division consists of

highly capable people. The IESCOs face a number of risk during their operations

however there are a certain number of risks that are considered to be the main types of

risks. IESCO is no exception to that as it also faces the same types of risk faced by

other commercial IESCOs in the market. These main risks are:

1- Credit Risk: Risk from the borrower as he fails to repay the money to the

IESCO.

2- Liquidity Risk: Risk than a security/asset cannot be traded in a quick time

frame in the market.

3- Market Risk: Risk of the reduction in value of a portfolio due to market

conditions.

4- Operational Risk: Risk due to the transactions of the business.

47

48

B A L A N C E S H E E TB A L A N C E S H E E T

ITEMS2011PKR in Min

2010PKR in Min

2009PKR in Min

2008PKR in Min

2007PKR in Min

ASSETS

Cash and Balance 8,959 7,248 6,471 5,647 5,861

Balances 879 1,400 1,497 3,909 4,350Lending to financial and Other Institutions

813 2,532 2,755 3,990 3,175

Investment 45,776 34,986 29,537 14,053 19,182

Advances 65,340 54,676 48,727 47,575 40,154

Operating fixed assets 3,834 3,469 3,334 3,127 2,151Deferred tax assets- net 362 385 108 126 --

Other assets 3,769 3,410 2,881 2,550 1,981Total Assets 129,732 108,106 95,310 80,977 76,854

LIABILITIES

Deposits and other accounts 99,734 82,017 73,548 61,634 60,150Borrowings 14,557 12,371 9,386 8,441 5,865Bills payable 1,571 1,858 1,763 1,255 1,641Other liabilities 1,995 1,745 1,612 1,336 964Deferred tax liabilities – net -- -- -- -- 425

Sub-ordinate loans 898 1,197 1,198 1,198 1,199

Total Liabilities 118,755 99,188 87,507 73,864 70,244

REPRESENTED BY:

Share Capital 8,028 6,023 5,019 4,114 4,114

Reserves 1,183 2,029 2,004 2,017 1,877

Inappropriate profit 1,026 329 158 835 239Surplus on revaluation of assets (net of tax)

740 537 622 147 380

Total Equity 10,977 8,918 7,803 7,113 6,610Net worth (assets=liabilities + equity )

129,732 108,106 95,310 80,977 76,854

49

P R O F I T & L O S S S T A T E M E N TP R O F I T & L O S S S T A T E M E N T

ITEMS

2011

Rs.in Min

2010

Rs.in Min

2009

Rs.in Min

2008

Rs.in Min

2007

Rs.in Min

Profit 12,895 10,250 9,337 7,823 6,272

Fee, commission, brokerage and exchange income

915 603 673 638 472

Capital gain and dividend income 428 175 120 268 331

Other income 612 450 375 320 263

TOTAL INCOME 14,850 11,478 10,505 9,049 7,338

Profit 8,997 7,203 6,603 4,878 4,334

Operating expenses 3,503 2,683 2,079 1,952 1,293

Provisions 1,272 1,452 1,633 1,266 235

Taxation 294 15 45 252 476

TOTAL EXPENSES (14,066) (11,353) (10,360) (8,348) (6,338)

PROFIT AFTER TAXATION 784 125 145 701 1,000

50

9: Ratio Analysis

A ratio is simple arithmetical expression of the relationship of one number to another.

It may be defined as the indicated quotient of two mathematical expressions.

According to Accountant’s Handbook by Wixon, Kell and Bedford, “a ratio is an

expression of the quantitative relationship between two numbers”.

Ratio analysis is the process of determining and presenting the relationship of items

and group of items in the statements. According to Batty J. Management Accounting,

“Ratio can assist management in its basic functions of forecasting, planning

coordination, control and communication”.

It is helpful to know about the liquidity, solvency, capital structure and profitability

of an organization. It is helpful tool to aid in applying judgments, otherwise complex

situations. Ratio analysis can represent following three methods and can say, may be

expressed in the following three ways:

1. Pure Ratio or Simple Ratio: - It is expressed by the simple division of one

number by another

2. ‘Rate’ or ‘so Many Times: - In this type, it is calculated how many times a

figure is, in comparison to another figure.

3. Percentage: - In this type, the relation between two figures is expressed in

hundredth.

ADVANTAGE OF RATIO ANALYSIS

1. Helpful in locating the weak spots of the business.

2. Helpful in forecasting and estimate about the trend of the business.

3. Fixation of ideal standards.

4. Study of financial soundness and effective control

Limitations of Ratio Analysis

1. Comparison not possible if different firms adopt different accounting policies.

2. Ratio analysis becomes less effective due to price level changes.

3. Ratio may be misleading in the absence of absolute data.

4. Limited use of a single data.

5. Lack of proper standards.

6. False accounting data gives false ratio.

51

10: IESCO RATIO ANALYSIS

A. PERFORMANCE

1. Return On Equity

2. Return On Assets

3. Provision Expense / Pre Provision Profit

4. Cost To Income Ratio:

5. Other Operating Income / Total Net Revenue

6. Internal Growth Rate

7. Capital Gearing Ratio

8. Working Capital Turnover Ratio

B. CAPITAL ADEQUACY

9. Capital Ratio

10. Capital Formation Rate (Internal Capital Generation)

11. Leverage Ratio = Total Assets Equity Capital

12. Leverage Ratio (2) =Loan Loss Reserve Tot Loans

13. Weighted Average Cost Of Capital (WACC)

14. Working Capital

15. Employed Capital

16. Fixed Assets To Proprietor’s Fund Ratio

C. LIQUIDITY

17. Current Ratio

18. Liquid Assets / Deposits And Borrowings

19. Loans / Deposits

20. Loans / Deposits And Borrowing

21. Loans / Total Assets

22. Cash & Due From BanksTotal Assets

23. CASA Ratio

D. OPERATING EFFICIENCY

24. Total Operating Expense Operating Income

25. Operating Income/ Assets

26. Net Profit Margin =Net Profit Gross Operating Income

27. Net Interest Margin =Total Non-Interest IncomeTotal Assets

28. Interest Expense/ Operating Income

29. Interest Expense/ Total Income

30. Total Interest ExpTotal Assets

31. Internal Fund = Retaining Earning +Deprecation

52

E. CREDIT PERFORMANCE

32. Provisions/ Gross Advance

33. Liquid Asset To Deposits And Short Term Loan (LADST)

34. Interest Coverage Ratio

F.INTERMEDIATION EFFICIENCY

35. NIMR (Net Interest/Mark-Up Revenue) / Avg. Assets Investments)]

36. Yield On Asset =[Interest Earned/Average (Earning Assets-Equity)]

37. Yield On Assets(2) = Total Interest IncomeTotal Assets

38. Yield On Assets (4)= Total Interest Expense Total Assets

39. Yield On Assets(3) = Interest Expense/Gross Operating Income

40. [Cost Of Interest Expensed / Average (Deposits + Borrowings)]

41. Spread

G. TAX MANAGEMENT MEASURES

42. Tax Exempt Position =Loan Loss Provision Total Income

43. Provision Expense / Pre Provision Profit

44. Interest Paid / Pre- Interest And Tax Profit

45. Deprecation /Pre- Depreciation, Interest And Tax Profit

10.1 : IESCO RATIO ANALYSIS

A. PERFORMANCE

Return On Equity

Return On Assets

Provision Expense / Pre Provision Profit

Cost To Income Ratio:

Other Operating Income / Total Net Revenue

Internal Growth Rate

Capital Gearing Ratio

Working Capital Turnover Ratio

53

1. Return on Equity:

Return on Equity / Return on Assets

Returns on equity and assets are well-established metrics long used in fundamental analysis

across a wide range of industries. Return on equity is especially useful in the valuation of banks,

as traditional cash flow models can be very difficult to construct for IESCO, and return-on-

equity models can offer similar information.

Return on Equity 2011

%

2010

%

2009

%

2008

%

2007

%

6.18814 5.57138 5.26597 5.080455 5.353007

Comment

By dividing profit after tax on share capital for 5 years I come to know that IESCO return on

equity is lie between the ranges of 5-6 in increasing trend. IESCO is raising capital and profit

side by side.

54

2. Return on Assets

Return on Assets 2011

%

2010

%

2009

%

2008

%

2007

%

0.604323 0.115627

0.152135 0.865678 1.301168

Comments

IESCO ROA overall decrease which show IESCO management not properly deploy asset into

earning 2007 it was 1.3% but afterward it decrease. But in 2011 ROA restart to improve.

55

3. Provision Expense / Pre Provision Profit

Provision Expense / Pre Provision Profit

2011 2010 2009 2008 2007

ITEMS Rs.in Min Rs.in MinRs.in Min

Rs.in Min

Rs.in Min

Provisions Expense

1,272 1,452 1,633 1,266 235

Pre Provision Profit

2,350 1,592 1,823 2,219 1,711

Formula : Provision Expense / Pre Provision Profit

PERCENTAGE 54.12766 91.20603 89.57762 57.05273 13.73466

Comments

IESCO deducts provision form Total income to know actual profit. This act can save bank form huge

amount of Tax and a good indicator of bank performance.

56

PRE PROVISION PROFIT

(Working 1)

a) Profit after taxation

784 125 145 701 1,000

b) Provisions Expense

1,272 1,452 1,633 1,266 235

c) Taxation 294 15 45 252 476

Pre Provision Profit = a +b + c

Pre Provision Profit 2,350 1,592 1,823 2,219 1,711

4. Other Operating Income / Total Net Revenue

Operating Income / Total Net Revenue

ITEMS 2011 2010 2009 2008 2007

Rs.in Min Rs.in Min Rs.in Min Rs.in MinRs.in Min

Operating Income 1343 778 793 906 803

Total Net Revenue 784 125 145 701 1000

Formula: Operating Income / Total Net Revenue

% % % % %

Operating Income /Total Net Revenue

1.71301 6.224 5.4689 1.2924 0.803

Working 2

ITEMS

2011 2010 2009 2008 2007

Rs.in Min

Rs.in Min

Rs.in Min

Rs.in Min

Rs.in Min

Fee, commission, brokerage and exchange income

915 603 673 638 472

Capital gain and dividend income

428 175 120 268 331

Total Operating Income 1343 778 793 906 803

Comments

57

Here, I use the ratio of” Operating Income / Total Net Revenue” to analysis how much IESCO

earns other then interest income to measure the performance.

In 2007 Operating Income / Total Net Revenue was less than 1 % in 2008-2010 it increase but in

2011 Operating Income / Total Net Revenue ratio again decrease.

Reason behind it is that management mostly relay on interest income.

5. Internal Growth Rate

Internal growth rate is measure by divide retain earning on net assets. Internal growth is use to

evaluate the management performances.

Internal Growth Rate

2011 2010 2009 2008 2007

ITEMS Rs.in Min Rs.in Min Rs.in Min Rs.in Min Rs.in Min

Retain Earning

588 93.75 108.75 525.75 750

Net Assets

129,732 108,106 95,310 80,977 76,854

Internal Growth Rate = Retain earning/ net assets

IG Rate 0.45% 0.09% 0.11% 0.65% 0.98%

IESCO deploy retain earning into assets at the ratio of .98% while 1% is benchmark which IESCO fail to achieve. From 2007 to 2010 it decrease and in 2011 it increase at .45%.

6. Capital Gearing Ratio

Capital Gearing ratio establishes a relationship between equity capital (including all reserves

and undistributed profits) and fixed cost bearing capital. If the amount of fixed cost bearing

capital is more than the equity share capital including reserves an undistributed profits), it will be

called high capital gearing and if it is less, it will be called low capital gearing.

58

59

Formula:

Capital Gearing Ratio = [Equity Share Capital+ Reserves + P&L Balance/ Fixed Cost

Bearing Capital]

Capital Gearing Ratio

2011 2010 2009 2008 2007

Items PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

1. Share Capital 8,028 6,023 5,019 4,114 4,114

2. Reserves 1,183 2,029 2,004 2,017 1,877

3. P&L Balance 784 125 145 701 1,000

Total (1+2+3) 9,995 8,177 7,168 6,832 6,991

Fixed Cost Bearing Capital

14557 12371 9386 8441 5865

[Equity Share Capital+ Reserves + P&L Balance/ Fixed Cost Bearing Capital]

Capital Gearing Ratio 69% 66% 76% 81% 119%

Whereas, Fixed Cost Bearing Capital = Preference Share Capital + Debentures + Long Term

Loan (IESCO neither issue preference stock nor debentures) so long term loan only consider as

fixed cost bearing capital.

Comments

IESCO Capital Gearing ratio is too high like 119% in 2007 and 69-81% in 2008-11 and high

gearing will be beneficial to equity shareholders when the rate of interest/dividend payable on

fixed cost bearing capital is lower than the rate of return on investment in business.

60

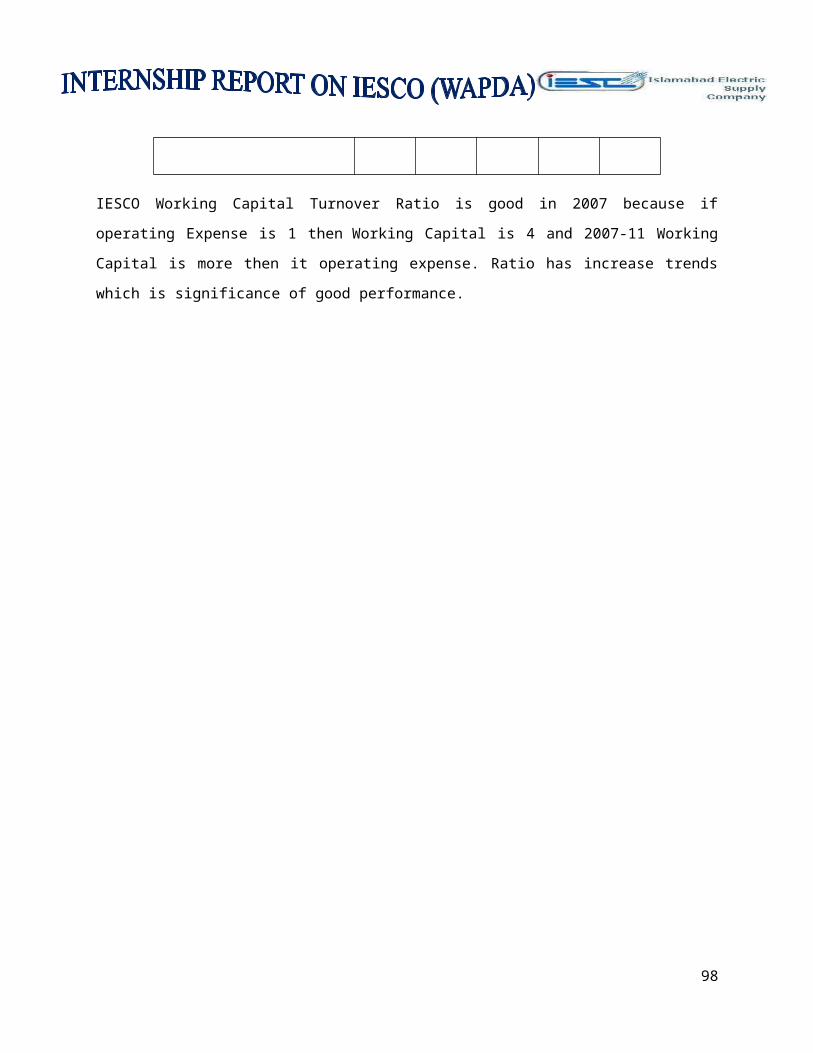

7. Working Capital Turnover Ratio

This ratio reveals how efficiently working capital has been utilized in making income.

Formula: - Working Capital Turnover Ratio = operating Expense / Working Capital

This ratio is of particular importance in banks where current assets play a major role in generating income. It shows the number of times working capital has been rotated in producing sales.

A high working capital turnover ratio shows efficient use of working capital and quick turnover of current assets like stock and debtors. A low working capital turnover ratio indicates under-utilization of working capital.

Working Capital Turnover Ratio

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in MinPKR in Min

PKR in Min

Operating expenses 3,503 2,683 2,079 1,952 1,293

Working Capital 5,905 4,596 4,290 3,844 5,066

Formula: - Operating Expense / Working Capital

Working Capital Turnover Ratio

59% 58% 48% 51% 26%

Times Times Times Times Times

3:5 3:5 1:2 1:2 1:4

IESCO Working Capital Turnover Ratio is good in 2007 because if operating Expense is 1 then Working

Capital is 4 and 2007-11 Working Capital is more then it operating expense. Ratio has increase trends

which is significance of good performance.

61

8. Capital Ratio

CAPITAL RATIO

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Share Capital 10,977 8,918 7,803 7,113 6,610

Total assets 129,732 108,106 95,310 80,977 76,854

Formula: Capital Ratio=Equity / Total Assets

% % % % %

Equity / Total Assets

8.4612894 8.24931086 8.1869688 8.7839757 8.600723

Formula = Retained Earnings / Capital Equity

Comments: IESCO ICGR in 2007 was good as 11% but 7% in 2008 in 2009-10 it decrease at its lower level

as 1%. Because IESCO income was low in these period. 2001 it increase at 5% due to increase in income.

62

Internal Capital Generation Rate (ICGR) 2011 2010 2009 2008 2007

ITEMS Rs.in Min Rs.in Min Rs.in Min

Rs.in Min

Rs.in Min

Retained Earnings

588 93.75 108.75 525.75 750

Total Equity

10,977 8,918 7,803 7,113 6,610

Formula = Retained Earnings / Capital Equity ICGR 5.36% 1.05% 1.39% 7.39% 11.35%

9. Leverage Ratio = Total Assets Equity Capital

Leverage Ratio

2011 2010 2009 2008 2007

ITEMS PKR in MinPKR in Min

PKR in Min

PKR in Min

PKR in Min

Total assets

129,732 108,106 95,310 80,977 76,854

Total equity

10,977 8,918 7,803 7,113 6,610

Leverage Ratio = Total Assets Equity Capital

Leverage Ratio

11.8185297 12.12222 12.21453 11.38437 11.62693

Comments

IESCO leverage ratio is 11-12 times in five years management maintain assets and increasing

trend. IESCO have enough leverage to meet liquidity crunch.

63

10. Working Capital

Working Capital

Items 2011 2010 2009 2008 2007

PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Current Assets 121,767 100,842 88,987 75,174 72,722

Current Liabilities 115,862 96,246 84,697 71,330 67,656

Formula= Current Assets – Current Liabilities

Working Capital 5,905 4,596 4,290 3,844 5,066

Comment IESCO enjoy working capital in 2007 good but decrease in 2008 -9 in 2010-11 almost get back

their sustain able situation. Decreasing (reason - raison d'être) is increase in current liabilities.

Current Ratio

This ratio explains the relationship between current assets and current liabilities of IESCO.

Current Assets:-‘Current assets’ includes those assets which can be converted into cash with in a year’s

time.

Current Assets = Cash in Hand + Cash at Bank + B/R + Short Term Investment + Debtors (Debtors –

Provision) + Prepaid Expenses.

Current Liabilities: - ‘Current liabilities’ include those liabilities which are repayable in a year’s time.

Current Liabilities = Bank Overdraft + B/P + Creditors + Provision for Taxation + Proposed Dividend +

Unclaimed Dividends + Outstanding Expenses + Loans Payable within a Year.

64

Comments

According to accounting principles, a current ratio of 2:1 is supposed to be an ideal ratio. It means that

current assets of a business should, at least, be twice of its current liabilities. IESCO higher ratio indicates

the better liquidity position; the firm will be able to pay its current liabilities more easily. If the ratio is

less than 2:1, it indicates lack of liquidity and shortage of working capital.

65

working

Current Assets2011 2010 2009 2008 2007

PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Cash and Balance 8,959 7,248 6,471 5,647 5,861

Balances with Other WAPDA branches

879 1,400 1,497 3,909 4,350

Lending to financial and Other Institutions

813 2,532 2,755 3,990 3,175

Investment 45,776 34,986 29,537 14,053 19,182

Advances 65,340 54,676 48,727 47,575 40,154

TOTAL 121,767 100,842 88,987 75,174 72,722

Current Liabilities2011 2010 2009 2008 2007

PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Deposits and other accounts

99,734 82,017 73,548 61,634 60,150

Borrowings 14,557 12,371 9,386 8,441 5,865

Bills payable 1,571 1,858 1,763 1,255 1,641

TOTAL 115,862 96,246 84,697 71,330 67,656

The biggest drawback of the current ratio is that it is susceptible to “window dressing”. This ratio can be

improved by an equal decrease in both current assets and current liabilities.

11. Liquid Assets / Deposits And Borrowings

Liquid Assets / Deposits And Borrowings

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min

PKR in Min PKR in Min

PKR in Min

Liquid Assets 125601 104311 92321 78301 74873

Deposits + Borrowings 114,291 94,388 82,934 70,075 66,015

Liquid Assets / Deposits And Borrowings

Liquid Assets / Deposits And Borrowings

1.098958 1.1051298 1.113186 1.117389 1.134182

Comments

IESCO liquid assets to deposits and borrowings ratio is 1 over 5 years. And it has no big change.

Because IESCO keep equal liquid asset equal to Deposit and browning.

66

12. Loans / Deposits

Loans / Deposits

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Loans 65,340 54,676 48,727 47,575 40,154

Deposits 99,734 82,017 73,548 61,634 60,150

Formula: Loans / Deposits

% % % % %

Loans / Deposits 65.51427 66.6642366.2519

7 77.189538 66.75644

Comments:

The loan/deposit ratio helps assess IESCO’s liquidity, and by extension, the aggressiveness of the bank's

management. IESCO the loan/deposit ratio is too high; the bank could be vulnerable to any sudden

adverse changes in its deposit base. 2007-11 Loans / Deposits ratio is 66 %.

67

13. Loans / Deposits And Borrowing

Loans / Deposits And Borrowing

2011 2010 2009 2008 2007

ITEMS PKR in Min

PKR in Min

PKR in Min

PKR in Min PKR in Min

Loans 65,340 54,676 48,727 47,575 40,154

Deposits + Borrowings 114,291 94,388 82,934 70,075 66,015

Formula: Loans / Deposits And Borrowing

% % % % %

Loans /Deposits And Borrowing 57.169 57.926 58.753 67.8915 60.825

Comments:

IESCO should keep loans / deposits and borrowing ratio 45% but their ratio is 57-60% which can create

liquidity crunch.

68

14. Loans / Total Assets

Loans / Total Assets

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Loans 65,340 54,676 48,727 47,575 40,154

Total assets 129,732 108,106 95,310 80,977 76,854

Formula: Loans / Deposits And Borrowing

% % % % %

Loans / Total Assets 50.36537 50.57629

51.12475 58.75125 52.24712

Comments:

IESCO loan to total asset is about 50% over 2007-11 which is satisfactory. IESCO follow time matching

police which improve it liquidity ratio.

69

15. Cash & Due From Banks to Total Assets

Cash & Due From Banks /Total Assets

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Balances with Other Banks

879 1,400 1,497 3,909 4,350

Total assets 129,732 108,106 95,310 80,977 76,854

Formula: Cash & Due From Banks/Total Assets

% % % % %

Cash & Due From Banks Total Assets

0.677551 1.2950251.570664

4.8272966

5.660083

Comments:

In 2007 IESCO cash & due from banks /total assets ratio is higher but 2008-11 it decrease the reason is

that IESCO decrease balance in banks and advance money into market because in these day’s interest

rate was high.

70

16. Total Operating Expense Operating Income

Total Operating Expense Operating Income

ITEMS2011 2010 2009 2008 2007

Rs.in Min Rs.in Min Rs.in Min Rs.in Min Rs.in Min

Operating expenses

3,503 2,683 2,079 1,952 1,293

Total Operating Income

1343 778 793 906 803

Total Operating Expense Operating Income

Times 2.60834 3.44859 2.62169 2.15453 1.61021

Comments:

For IESCO these ratios indicate the relationship between expenses and income. The operating ratio

reveals the ratio of total operating expenses in relation to income but some of the expenses include in

operating ratio may be increasing while some may be decreasing. Hence, specific expenses ratio are

computed by dividing each type of expense with the net sales to analyze the causes of variation in each

type of expense. 2077-11 operating income lies in 1-2 time of operating expense.

71

working

ITEMS2011 2010 2009 2008 2007

Rs.in Min Rs.in Min Rs.in Min Rs.in Min Rs.in Min

Fee, commission, brokerage and exchange income

915 603 673 638 472

Capital gain and dividend income

428 175 120 268 331

Total Operating Income 1343 778 793 906 803

72

17. Operating Income/ Assets

Operating Income/ Assets

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Total Operating Income 1343 778 793 906 803

Total assets 129,732 108,106 95,310 80,977 76,854

Formula = Operating Income/ Assets

Ratio 1.035% 0.720% 0.832% 1.119% 1.045%

Comments: IESCO has 1% operating income over total assets in 2007 and same in2008 but in

2009-10 it decrease to less than one percent and 2011 it ratio again 1%.

18. Net Interest Margin =Total Interest IncomeTotal Assets

Net Interest Margin =Total Interest Income/Total Assets

2011 2010 2009 2008 2007

ITEMS PKR in MinPKR in Min

PKR in Min PKR in Min PKR in Min

Interest Earned

12,895 10,250 9,337 7,823 6,272

Total Assets 129,732 108,106 95,310 80,977 76,854

Formula=Total Interest Income/Total Assets

Ratio 9.94% 9.48% 9.80% 9.66% 8.16%

Comments

73

IESCO net interest margin is good in 2007-11 it show increasing treads. Reason is that rate of interest is

high in Pakistan.

19. Interest Expense/ Operating Income

Interest Expense/ Operating Income

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in MinPKR in

MinPKR in Min PKR in Min

Interest Expensed 8,997 7,203 6,603 4,878 4,334

Total Operating Income w2 1343 778 793 906 803

Formula= Interest Expense/ Operating Income

6.70 9.26 8.33 5.38 5.40

Comments

IESCO interest expense ratio is increase in 2007-10 and decrease in 2011 because 2007-10 interest

expense is low in compare to total income and in 2011 interest expense is high than operating income.

74

20. Interest Expense/ Total Income

Interest Expense/ Total Income

2011 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in Min

PKR in Min PKR in Min

Interest Expensed

8,997 7,203 6,603 4,878 4,334

Total Income 14,850 11,478 10,505 9,049 7,338

Formula= Interest Expense/ Total Income

61% 63% 63% 54% 59%

Comments

Interest expense of IESCO is increase 2007-10 because it directly relate to deposits. In 2007-10 interest

expense is increase because interest rate is high and decrease in 2011 because interest rates decrease.

21. Total Interest ExpTotal Assets

Total Interest ExpTotal Asset

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Interest Expensed

8,997 7,203 6,603 4,878 4,334

Total assets 129,732 108,106 95,310 80,977 76,854

Total Interest ExpTotal Assets

7% 7% 7% 6% 6%

75

76

Comments:

IESCO interest expense over total asset is 6% which is so good form 2007-08 and increase in 2009-11 at 7% the valid reason is increase in interest rate hike this ratio.

22. Internal fund = retaining earning +deprecation

Internal Fund

2011 2010 2009 2008 2007

ITEMS PKR in Min PKR in Min PKR in Min PKR in Min PKR in Min

Retaining Earning

588 93.75 108.75 525.75 750

Depreciation 541,733 470,131 450,120 430,550 401,077

Internal Fund = Retaining Earning +Deprecation

Internal Fund 542,321.00 470,224.75 450,228.75 431,075.75 401,827.00

Comment

IESCO has handsome internal finance and can face liquidities crunch by itself internal fund is

continuously increasing from 2007 to 2011 which indicate IESCO is financially too strong.

77

10.2: Horizontal Analyses

orizontal analysis (also known as trend analysis) is a financial statement analysis technique that shows changes in the amounts of corresponding financial statement items over a period of time. It is a useful tool to evaluate the trend situations. Here, statements

for five year periods are used in horizontal analysis. The earliest period is usually used as the base period and the items on the statements for all later periods are compared with items on the statements of the base period. The changes are generally shown in percentage.

H

A procedure in fundamental analysis in which an analyst compares ratios or line items in IESCO financial statements over a certain period of time. The analyst will use his or her discretion when choosing a particular timeline; however, the decision is often based on the investing time horizon under consideration.

In meanwhile, a Horizontal analysis is the comparison of historical financial information over a series of reporting periods, or of the ratios derived from this financial information. The analysis is most commonly a simple grouping of information that is sorted by period, but the numbers in each succeeding period can also be expressed as a percentage of the amount in the baseline year, with the baseline amount being listed as 100%.

A common problem with horizontal analysis is that the aggregation of information in the financial may have changed over time, due to ongoing changes in the chart of accounts, so that revenues, expenses, assets, or liabilities may shift between different accounts and therefore appear to cause variances when comparing account balances from one period to the next.

78

When conducting a horizontal analysis of IESCO, it is useful to conduct the analysis for all of the financial statements at the same time, so the complete impact of operational results on IESCO's financial condition over the review 5 years period.

10.3: Horizontal Analysis of the Balance Sheet

Horizontal analysis of the balance sheet is also usually in a two-year format, such as the one shown below, with a variance showing the difference between the two years for each line item. An alternative format is to add as many years as will fit on the page, without showing a variance, so that you can see general changes by account over multiple years. A less-used format is to include a vertical analysis of each year in the report, so that each year shows each line item as a percentage of the total assets in that year.

79

B A L A N C E S H E E TB A L A N C E S H E E T

I T E M S

2011

%

2010 2009

%

2008

%

2007

%

ASSETS

Cash and Balance 123.6065

B A

S E

Y

E A

R

B A

S E

Y

E A

R

89.2798 77.91115 80.86369

Balances 62.78571 106.9286 279.2143 310.7143

Lending to financial 32.109 108.8073 157.5829 125.3949

Investment 130.8409 84.4252 40.1675 54.82765Advances 119.504 89.11954 87.01258 73.4399

Operating fixed assets 110.5218 96.10839 90.14125 62.00634Deferred tax assets- net 94.02597 28.05195 32.72727 --

Other assets 110.5279 84.4868 74.78006 58.09384

Total assets 120.0044 84.4868 74.90519 71.09134

LIABILITIES

Deposits and other accounts 121.6016 88.16347 75.14784 73.33845Borrowings 117.6704 89.67409 68.23216 47.40926Bills payable 84.55328 94.88698 67.54575 88.32078Other liabilities 114.3266 92.37822 76.5616 55.24355Deferred tax liabilities – net -- -- -- 00Sub-ordinate loans 75.02089 100.0835 100.0835 100.1671

Total liabilities 119.7272 88.22337 74.46869 70.81905REPRESENTED BY:Share Capital 133.2891 83.33057 68.30483 68.30483

Reserves 58.30458 98.76787 99.40858 92.50862

Inappropriate profit 311.8541 48.02432 253.7994 72.64438

Surplus on revaluation of assets (net of tax)

137.8026 115.8287 27.3743 70.7635

123.0881 100 88.22337 74.46869 70.81905

80

Cash and Balance

Cash is current asset of IESCO and in horizontal analysis 2010 is taken as base year “cash and balance with treasury banks” trend is increase over the time. In 2008 cash and balance with treasury banks was decrease because in this year IESCO Demand was high otherwise 2009 to 2011 its trend show growth.

Balances

81

IESCO has huge amount in bank balance in 2007 but it starts decrease in 2008-11 because management uses this asset in investments.

Lending to financial and Other Institutions