Internship Report on Askari Bank

181

Internship Report Askari Bank Limited Submitted To: Sir Raza Ali Submitted By: 1 University Of Sargodha

-

Upload

sajidobry847601844 -

Category

Documents

-

view

2.117 -

download

294

Transcript of Internship Report on Askari Bank

Internship Report

Askari Bank Limited

Submitted To:

Sir Raza AliSubmitted By:

Hasnain Manzoor

Session 2008-12

1

University Of Sargodha

Sumission Date: 23-09-2011

Preface

Now a day the business environment keeps on changing everywhere. New dimensions

of business are coming before us. These dramatic and dynamic changes in business world

require the specialties about the all aspect of business of today. Because of these

requirements business knowledge became important and business education becomes the

need of time. The person with latest knowledge can survive in this vast field.

But practical knowledge is also necessary along with the theoretical knowledge. This

made the internship an integral part of B.Com. One can see how the theories and

knowledge are being practically implemented. I completed my internship in Askari Bank

Limited. This report carried the information about history, organizational structure,

departments, strengths and weaknesses etc. Askari Bank Limited. In this report I tried my

level best efforts to encompass and elaborate the necessary information about the Askari

Bank Limited. This internship report includes a complete introduction, performance and

financial analysis of the statements of the Askari Bank Limited.

2

University Of Sargodha

To My Eminent

“MAAN JEE”

Who Spent Each And Every Moment of Her Life

Praying for me And for My Success

Praying for Me

And for My Success

To My Eminent

“MAAN JEE”

Who Spent Each And Every Moment of Her Life

Praying for me And for My Success

Praying for Me

And for My Success

To My

“ABBU JEE”

Who Supported Me through All My Life

TO My Friends

“And Respected Teachers”Who Always Helped Me In

Spare Of Life

DEDICATION

3

University Of Sargodha

ACKNOWLEDGEMENT

‘In the name of Allah, the most Gracious, the most merciful’

Writing an internship report appeared to be a great experience to me. It added a lot to my

knowledge while I was working on this report. If I say that this report is one of my

memorable experiences in student life, then it would not be wrong.

Completion of internship report is not an easy task. It requires continuous hard work and

zeal. Completion of this report would have not been possible with out the support of all

staff members at the bank, my respected teachers, my friends and my well wishers. I

would like to mention that Mr. Shakeel Ahmad Nadeem, who is presently serving the

bank as Manager Operations, has been very kind and supportive through out my stay at

the branch.

My gratitude will always remain due to the AIOU for expanding my knowledge and

experience. This prestigious institution will has a lasting impact on my life.

4

University Of Sargodha

May Allah Bestow His Blessings On All Of Us

EXECUTIVE SUMMARY

The Department of Commerce was established in 2007 and offers B.Com (Hons) in

2008. They are giving the best education and are offering for specialization, financial

management and Accounting. An important programmed is six to eight weeks internship

with any recognized institution.

I decided to take up Askari Commercial Bank Limited for my internship because it’s

competing bank nowadays and gives a good training to the internees. So in order to learn

more this was my choice.

This report is about my internship that I have undergone at Askari Bank Limited Jhang

Branch from 21st June 2011 to 2nd August 2011.

During my internship I am able to learn practical aspect of business, and get good working experience.

On the very first day of my internship I reported to Human Resource Manager / Operation Manager

5

University Of Sargodha

Shakeel Ahmad Nadeem. He gave me small introduction of the bank and introduced me to the staff of

the bank. Every internee is rotated among the bank’s departments and so was I. This rotation is done in

order to have general concept regarding bank’s functions, operations and policies. In this rotation the

stay in department is usually a week. I have learned more about the Bills and Foreign Trade department

and have given below the caption of activities I was involved in during the period of six weeks.

During my internship I found that Askari Bank is a best bank in Jhang because most of the Exports and

Imports in Jhang are done through this bank. Low profit rates are one of the major reasons for not

meeting the deposit targets. The profit rates on Askari deposit schemes are quite low when compared

with other banks especially with the National Saving Centers. In today every customers is the rational

customer he knows the value of money and wants a best return on his money.

Earlier Askari Commercial were able to attract customer due to their ancillary services like ATM

Cards, Credit Cards, Online Banking etc. but now all the banks are offering these services through their

own network or through third party contracting, so our plus points are no more our advantages. So the

only things through which ACBL can increase their deposits are profit rates, because the customers

only want maximum profit on their investment.

6

University Of Sargodha

BANKING IN PAKISTAN

Pakistan came into being on 14th August, 1947; sufficient banking services were

available in the areas forming Pakistan. Out of the total branches of the nearly 3,500 in

the undivided India, as many as about 1,500 branches were existing in these areas.It was

agreed between the two countries that reserve bank of India shall continue to function in

the Pakistan territory until 30th September 1948 and that Indian notes would continue to

be legal tender at Pakistan until 30th September 1948. Unfortunately, relationship

between the two countries became most strained immediately after independence;

banking was mostly in the lands of Hindus who immediately started transferring their

offices and assets into India. As a result most of the banks in Pakistan were closed down

and even those which were open were not doing any effective business.

The number of banking office in Pakistan came down to about 200 on 30th June 1948.

Branches of some European banks were also functioning in a limited manner, financing

in export of crops, and their number was limited to about 20. It was only the Habib bank,

which transferred its office from Bombay to Karachi Austral Asia bank was another

bank, which was in existence in the Pakistan territory at the time of independence.

Despite of best efforts on the part of government of Pakistan, no heady way could be

7

University Of Sargodha

made on this behalf and reserve bank of India was in no mood to help the new country.

Imperial bank of India, agent of the reserve bank of India also started closing down its

branches in Pakistan. to advance Reserve bank also refused money to Pakistan to make

essential payments such as salaries etc, also Pakistan’s share of Rs.75 billion in cash

balance was with held by bank, causing hardships to the newly born state. In view of

these hopeless state affairs it was agreed between the two countries that reserve bank

would serve as monetary authority in Pakistan only up to 30th June 1948.

Banking in fact is primitive as human society, forever since man came to realize the

importance of money as a medium of exchange, the necessity of a controlling or

regulating agency or institution was naturally felt. Perhaps it was the Babylonians who

developed banking system as early as 2000bc. It is evident that the temples of the

Babylon were used as ‘Banks’ because of the prevalent respect and confidence at the

clergy.

At the time of independence there were 631 offices of the scheduled banks in Pakistan, of

which 487 were located in West Pakistan alone. As a new country with resources it was

very difficult for Pakistan to run its own banking system immediately. Therefore the

expert committee recommended that the Reserve Bank of India should continue to

function in Pakistan until 30, September 1948, so that problems of time and demand

liability, coinage currencies, exchange etc, could be settled between India and Pakistan.

The non Muslims started transferring their funds and accounts to India. By the end of

June 1948, the number of officers of scheduled banks in Pakistan declined from 631 to

255. There were 19 foreign banks with the status of small branch offices that were

engaged solely in export crop from Pakistan, while there were only two Pakistani

institutions, Habib Bank, and Australasia Bank, the customers of the banks are not

satisfied with the uncertain condition of banking. Similarly the Reserve Bank of India

8

University Of Sargodha

was not in the favor of Govt. of Pakistan. The Govt. of Pakistan decided to establish a

full-fledge central bank. The governor general of Pakistan, Quaid-e-Azam Muhammad

Ali Jinnah, inaugurated the state bank of Pakistan on July 1, 1948.The first Pakistani

notes was issued in October 1948 in the state bank of Pakistan. After the establishment of

state bank, banking expansion got momentum. More Pakistan schedule bank continues to

be the established. The network of banking braches now covers a very large segment of

national economy.

Monetary policy and banking system play an important role in the development of all

economic fields of the country because necessary finances for completion of economic

plans are provided by them. Therefore an organized banking system and the financial

institutions play an active role in this matter. The stable an organize banking policy is

much effective to improve the level of saving and consequently the level of investment.

The monitory policy is adopted and controlled by the bank but its success depends upon

the cooperation of commercial banks. Availability of the credit is a big problem for

LDCs. The shortage of supply of capital can be improved better and organized banking

system because the banks can increasing the saving through launching the various

attractive schemes in various productive sectors banks also produce credit money and

through this way resources are supplied to productive sectors of the country.

KINDS OF BANKS:

In Pakistan following types of banks are operating in the business circle

like economics.

COMMERCIAL BANKS:

9

University Of Sargodha

These banks are set up on commercial basis. Therefore, their primary

objective is to earn profit and maximize it is far as possible. For this they received cash

deposits from the people in different accounts. They give loans to different business

enterprises and thereby create credit money.

The State Bank of Pakistan is the central bank of Pakistan, Commercial Banks, financial

institutions and cooperative banks are the other components of the banking system.

AGRICULTURAL BANK:

These banks are providing long term and short term credit facilities to

landlords and tenant farmers.

INDUSTRIAL BANK:

These banks are medium and long term loans to industrialists to set up

new industries for the extension of industries already in operation.

MORTGAGE BANKS:

These banks provide the loans to the people against their moveable and

immoveable property.

EXCHANGE BANKS:

10

University Of Sargodha

These banks deal in foreign exchange. They provide credit to importers

and exporters by discounting foreign bills of exchange.

SAVING BANKS:

These banks are set up to induce the people to accumulate their small

saving in these banks.

CENTRAL BANKS:

Each country in the world has its own central bank. This bank does not

deal with public directly. This means that it neither receives cash deposits from the

people nor it’s give them loans. Therefore it is not a profit making institution.

History Of Organization:

Askari Bank (formerly Askari Commercial Bank) was incorporated in Pakistan on

October 9, 1991, as a Public Limited Company. It started its operations on April 1,

1992. The bank principally deals with banking, as defined in the Banking Companies

Ordinance, 1962. The Bank is listed on the Karachi, Lahore & Islamabad Stock

Exchanges.

Askari Bank has expanded into a network of 226 branches, including 31 dedicated

Islamic banking branches, and a wholesale bank branch in Bahrain. A shared network of

4,173 online ATMs covering all major cities in Pakistan supports the delivery channels

for customer service. Askari Bank achieved planned growth in business and operations

during 2009. The total assets of the Bank amounted to Rs.254 billion as at December 31,

2009, registering an increase of 23 percent over December 31, 2008.Customer deposits

11

University Of Sargodha

reached Rs.206 billion by December 31, 2009, an increase of 23 percent over December

31, 2008.

Profit after taxation showed an increase of 187% at Rs.1.11 billion, when compared with

last year’s Rs.386 million. The banking spread registered slight improvement over last

year, despite absorbing the adverse impact on net mark-up income due to increased

nonperforming advances. The Bank’s NPLs stood at Rs.17.73 billion as of December 31,

2009 compared to Rs.11.69 billion at the end of previous year, an increase of 52 percent.

Askari Commercial Bank Limited (ACBL) works as a Unit of Army Welfare Trust was established

for the Welfare of Army Officials. The office of Army Welfare Trust is situated at AWT Plaza,

Rawalpindi. AWT offers the “AWT Saving Scheme” to the army officials only. AWT has its units as

under:

1. Askari Associates.

2. Askari Leasing.

3. Askari General.

4. Private Business.

5. Textile Mills.

6. Cement Industry.

7. Askari Commercial Bank.

12

University Of Sargodha

Incorporated in Pakistan on October 09, 1991. The bank obtained business commencement certificate

on February 26, 1992 and started operations form April 1, 1992, as public limited company, and has

since expanded into a nation-wide presence of 51 branches, supported by a network of online ATMs.

The Bank is listed on the Karachi, Lahore and Islamabad Stock Exchanges and the initial public

offering was over subscribed by 16 times. Askari Commercial Bank is scheduled Commercial Bank

and is principally engaged in the business of banking as defined in the Banking Companies Ordinance

1962.

Nature Of Organization

Vision Statement:-

“To be the Bank of First Choice in the Region”

13

University Of Sargodha

Mission Statement: -

The mission statement of the bank is

“To be the leading private sector bank in Pakistan

with an international presence, delivering quality

services through innovative technology and effective

resource management in a modern and progressive

organization culture of meritocracy, maintaining high

ethical and professional standards, while providing

enhanced value to all their stakeholders, and

contributing to society”

Features

Products & services of ACBL

14

University Of Sargodha

A product ACBL includes all those services which customer normally required for

effectively managing his business. ACBL offers the following financial services to its

customers.

Mahana Bachat Account

Roshan Mustaqbil Deposit

Deposit Multiplier Account

Personal Finance

Islamic banking services

Agricultural finance solution

Corporate & investment banking

Mortgage Finance

Debit/Visa Card

International banking services

DEMAND DEPOSIT

Current Account

15

University Of Sargodha

Call Deposit Receipt

TIME DEPOSIT

PLS saving Deposit

Askari special Deposit account

Askari FISDA Account

Askari FAIDA Account Finance

Value Plus Saving Deposit

Notice Deposit

Askari Advantage

Term Deposit

LOCKERS

Small Size Lockers

Medium Size Lockers

Large size lockers

Fund Based Loan

16

University Of Sargodha

Running Finance

Cash Finance

Term Finance

Staff Finance

Askari Personal Finance

Trade Finance

Non-Fund Based Loan

Letter of Credit (LC)

Letter of Guarantee (LG)

Import Related Finance

Payment Against document

Finance Against imported Merchandise

Finance against Trust receipt.

Export Related Finance

17

University Of Sargodha

Pre-shipment Finance

Post shipment

Finance Against Packing Credit

FUND BASED LOAN:

In this type of loan, funds are directly involved.

RUNNING FINANCE: (R/F):

It is popularly known as overdraft. It is offered for working capital requirement of the customer. It is

created in current account adjustment from time to time finally on expiry date. This facility is normally

issued against hypothecation of immovable property. It is allowed to the borrower under a pre-

sanctioned limit. A current account is opened and the conduct of this account is kept under review for a

period of three to six months. The borrower can draw cheque on his account maximally up to the

amount of limit sanctioned to him. The amount outstanding against the borrower is mark-up will be

changed on the basis of the amount outstanding. This facility is issued on revolving basis repayment

should be completed by the maturity date. Repayment in monthly installments is not required.

CASH FINANCE: (C/F):

18

University Of Sargodha

It is also offered for the working capital requirement of the customer. It is the type of loan in which

client is given cash in lump sum it is offered against the pledge of moveable property or stock of

borrower. In majority of the cases this finance is allowed against pledge of stock. The amount of

finance is credited to borrowers CD account and he/she utilizes it for business purposes. Repayment is

not made by monthly installments. Adjustments are linked with delivery of goods kept under bank’s

pledge. Goods are pledge when the payment is done on delivery order of the bank. Goods released are

equivalent in value to the repayment amount and remaining goods are stills kept in pledge with bank

for further recovery. Goods are released on the Delivery Order (DO) by the bank to the Go down

Officer.

TERM FINANCE: (T/F):

Term finance is offered to client for investment in any project or business. It is issued for fixed time

period. The amount of finance is credited to borrower’s personal account by debiting the Term Finance

Account. The amount of finance is credited to borrower’s personal account by debiting the Term

Finance Account. The amount of Finance is disbursed in lump sum. Partial transactions are not allowed

in the Term Finance account. The repayment of Term Finance is usually in installments and with other

documents a letter of installments is taken from the borrower at the time of disbursement. By that letter,

the borrower binds him to pay the installments at regular intervals. Monthly repayment amount is

calculated by dividing the principal amount by time period plus mark-up.

19

University Of Sargodha

FINANCE AGAINST IMPORTED MERCHANDISE:

This type of finance is offered to the importer to finance their needs for meeting the cost including

freight, insurance, and customs and excise duty payable on the imported merchandise. The lending

bank mostly pledges the imported goods. The merchandise is released for the use of the importer

(borrower) upon repayment of the bank’s finance and charges either fully or partially, on production of

the Delivery Order issued by the banker in favor of the borrower.

NON-FUND BASED FACILITIES:

These are those types of facilities in which funds are not directly involved.

LETTER OF CREDIT:

Letter of Credit issued by the bank can broadly be classified as under: -

Sight letter of credit.

Usance letter of credit.

The sights L/Cs call for the draft to be drawn ‘at sight’. Documents negotiated and received against

sight are held as security till their retirement. Drafts drawn under Usance are for a tenure specified in

the L/C and are payable by the customer on due date.

Credit line proposal must clearly state the type of letter of credit the branch is intended to issue.

20

University Of Sargodha

LETTER OF GUARANTEE:

Guarantees issued by the bank can be classified under two broad categories.

(1) FINANCIAL GUARANTEE:

Bank guarantees the fulfillment of a financial commitment on behalf of the customer. Under these

guarantees, the bank is called upon to pay in the event of a breach of terms on the part of the customer.

(2) PERFORMANCE GUARANTEE:

The bank guarantees the due fulfillment of a contract or other work as specified in the guarantee, by the

customer. The amount of guarantee is usually up to the extent of the value of the contract.

(3) SHIPPING GUARANTEE:

Bank issues guarantee in favor of the shipping company to enable the importer to obtain delivery of the

goods without production of the Bill of Lading.

Core Values:

21

University Of Sargodha

We understand that our commitment to satisfy customers’ needs must

be fulfilled within a professional and ethical framework. We subscribe to a culture of

high ethical standards, based on the development of right attitudes. We believe in our

'core values' as the essential and enduring tenets of our organization - the very small set

of guiding principles that have a profound impact on how everyone in the organization

thinks and acts. They have an intrinsic value for us and bear significant importance to all

our employees. They are the few extremely powerful guiding principles; the soul of the

organization - the values that guide all our actions.

The intrinsic values, which are the corner stones of our corporate behavior, are:

Commitment

Integrity

Fairness

Team-work

Service

CORPORATE PHILOSOPHY:

I n s p i r i n g R e l a t i o n s h i p sI n s p i r i n g R e l a t i o n s h i p s

From knowing our customers requirements to understanding employee needs, from

utilizing modern technology to making responsible social contributions, from enhancing

stake-holders value to practising corporate ethics.... We are continuously and consistently

Striving to address newer challenges with a single motivation: “the power to inspire

and be inspired”

22

University Of Sargodha

OBJECTIVES:

Deliver solutions that meet customer’ financial needs.

Build and sustain a high performance culture.

Build trusted relationships with all stakeholders.

Build and manage the Banks’ portfolio of business to achieve strong and

Sustainable shareholder return.

Create and leverage strategic assets and capabilities for competitive advantage.

To facilitate the bank with modern banking technique.

To accelerate commercial activities and capture large market share.

Inspiring Technological Innovation

Technology has played a pivotal role in meeting customer expectations, particularly with

respect to speed and quality of service. We have fully automated transaction-processing

systems for back-office support. Our branch network is connected online real time and

our customers have access to off site as well as on site ATMs, all over Pakistan. Our

Phone Banking Service and Internet Banking Facility allows customers to enjoy routine

banking services from anywhere anytime in the world.

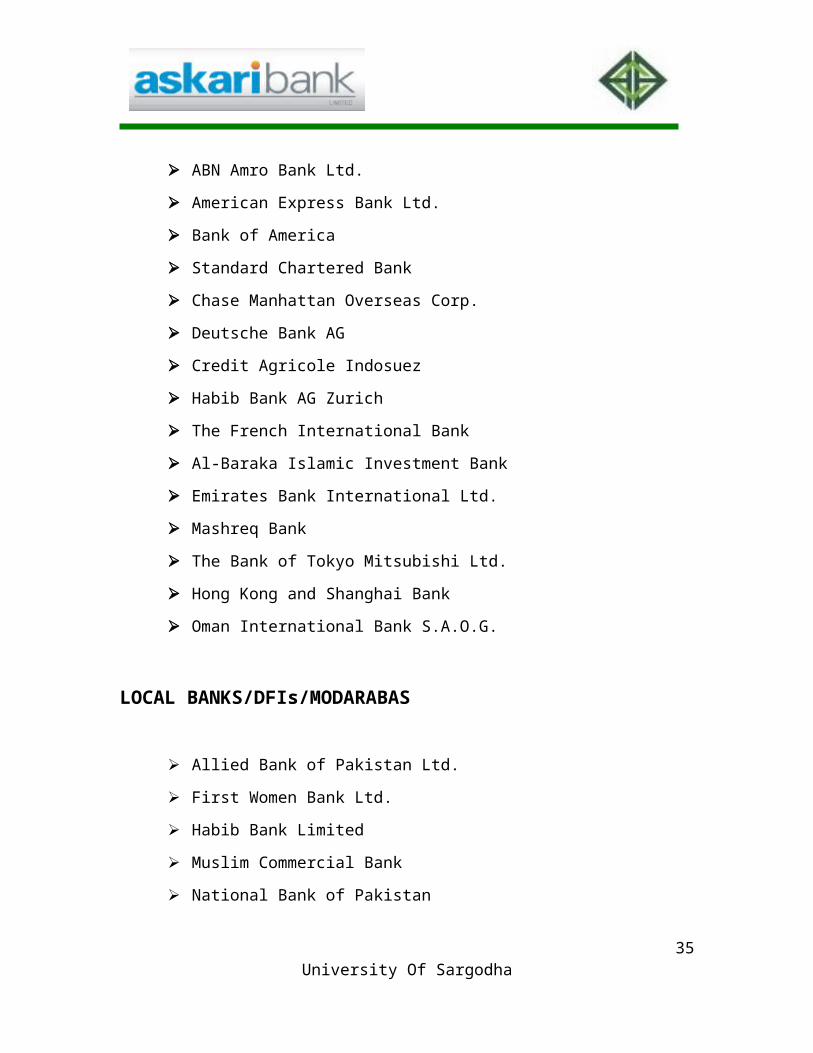

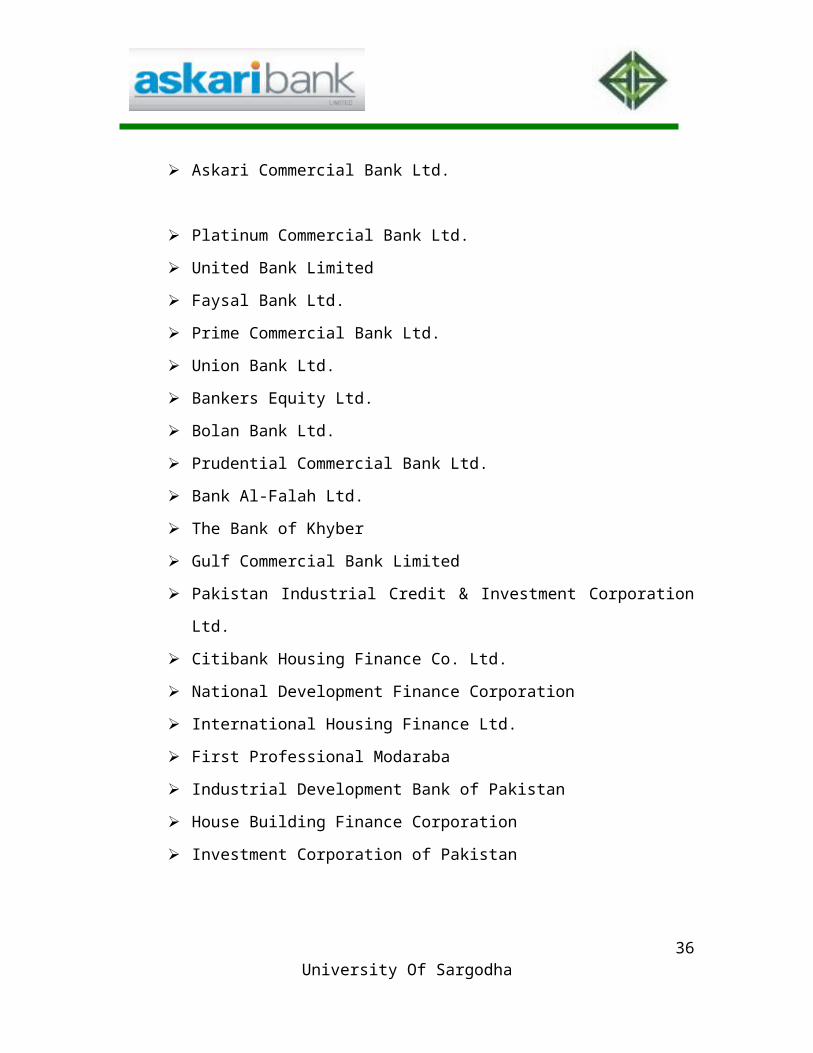

LIST OF THE COMPETITOR BANKS

23University Of Sargodha

FOREIGN BANKS

ABN Amro Bank Ltd.

American Express Bank Ltd.

Bank of America

Standard Chartered Bank

Chase Manhattan Overseas Corp.

Deutsche Bank AG

Credit Agricole Indosuez

Habib Bank AG Zurich

The French International Bank

Al-Baraka Islamic Investment Bank

Emirates Bank International Ltd.

Mashreq Bank

The Bank of Tokyo Mitsubishi Ltd.

Hong Kong and Shanghai Bank

Oman International Bank S.A.O.G.

LOCAL BANKS/DFIs/MODARABAS

Allied Bank of Pakistan Ltd.

First Women Bank Ltd.

Habib Bank Limited

Muslim Commercial Bank

National Bank of Pakistan

Askari Commercial Bank Ltd.

Platinum Commercial Bank Ltd.

24

University Of Sargodha

United Bank Limited

Faysal Bank Ltd.

Prime Commercial Bank Ltd.

Union Bank Ltd.

Bankers Equity Ltd.

Bolan Bank Ltd.

Prudential Commercial Bank Ltd.

Bank Al-Falah Ltd.

The Bank of Khyber

Gulf Commercial Bank Limited

Pakistan Industrial Credit & Investment Corporation Ltd.

Citibank Housing Finance Co. Ltd.

National Development Finance Corporation

International Housing Finance Ltd.

First Professional Modaraba

Industrial Development Bank of Pakistan

House Building Finance Corporation

Investment Corporation of Pakistan

25

University Of Sargodha

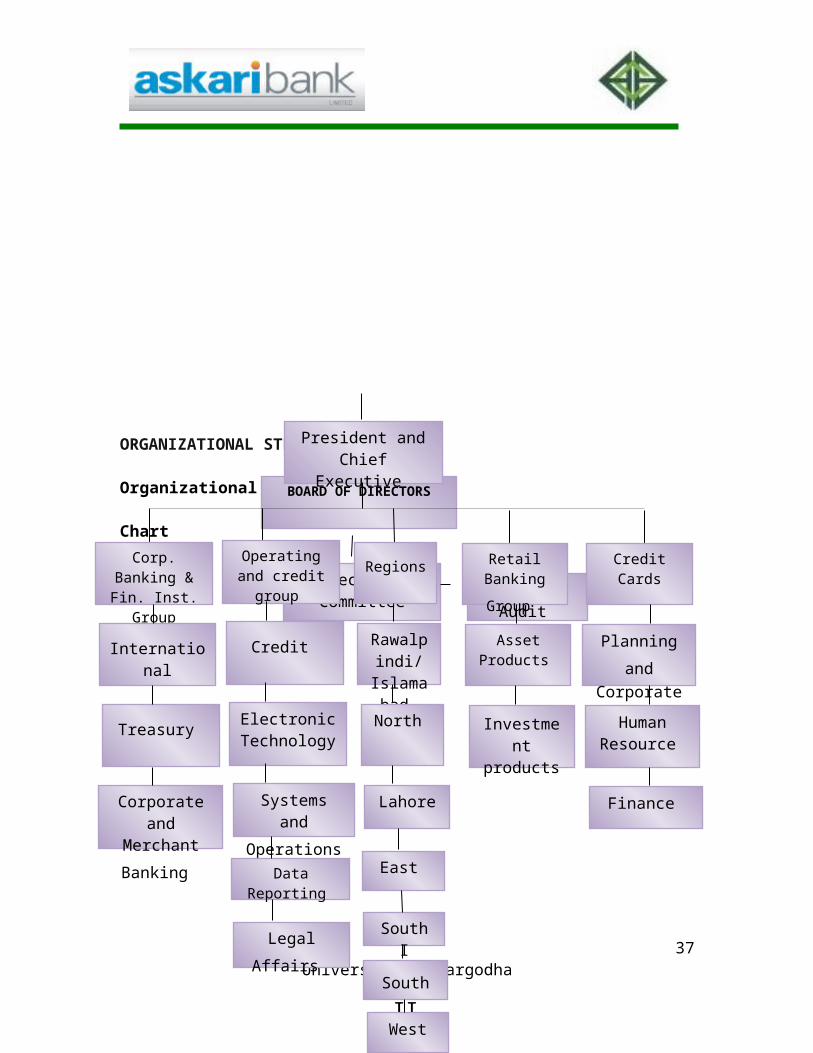

ORGANIZATIONAL STRUCTURE

Organizational

Chart

26

University Of Sargodha

BOARD OF DIRECTORS

Executive Committee Internal Audit

President and Chief Executive

Corp. Banking & Fin. Inst.

Group

Operating and credit group Regions Retail

Banking

Group

Credit Cards

International Credit Rawalpindi/

Islamabad

Asset Products

Planning and Corporate

affairs

Treasury Electronic

Technology North Investment

products Human

Resource

Corporate and Merchant

Banking

Systems and

Operations Lahore Finance

Data Reporting East

Legal Affairs South I

South II

West

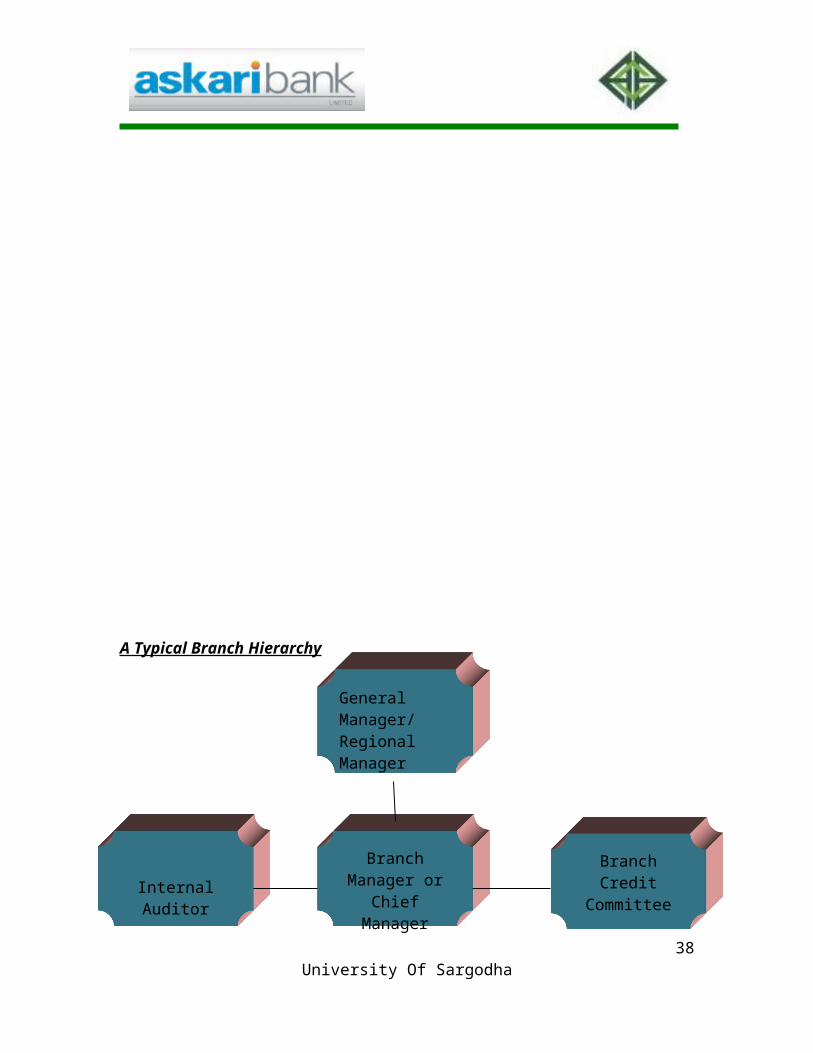

A Typical Branch Hierarchy

27

University Of Sargodha

General Manager/ Regional Manager

Branch Manager or Chief Manager

Branch Credit Committee

Internal Auditor

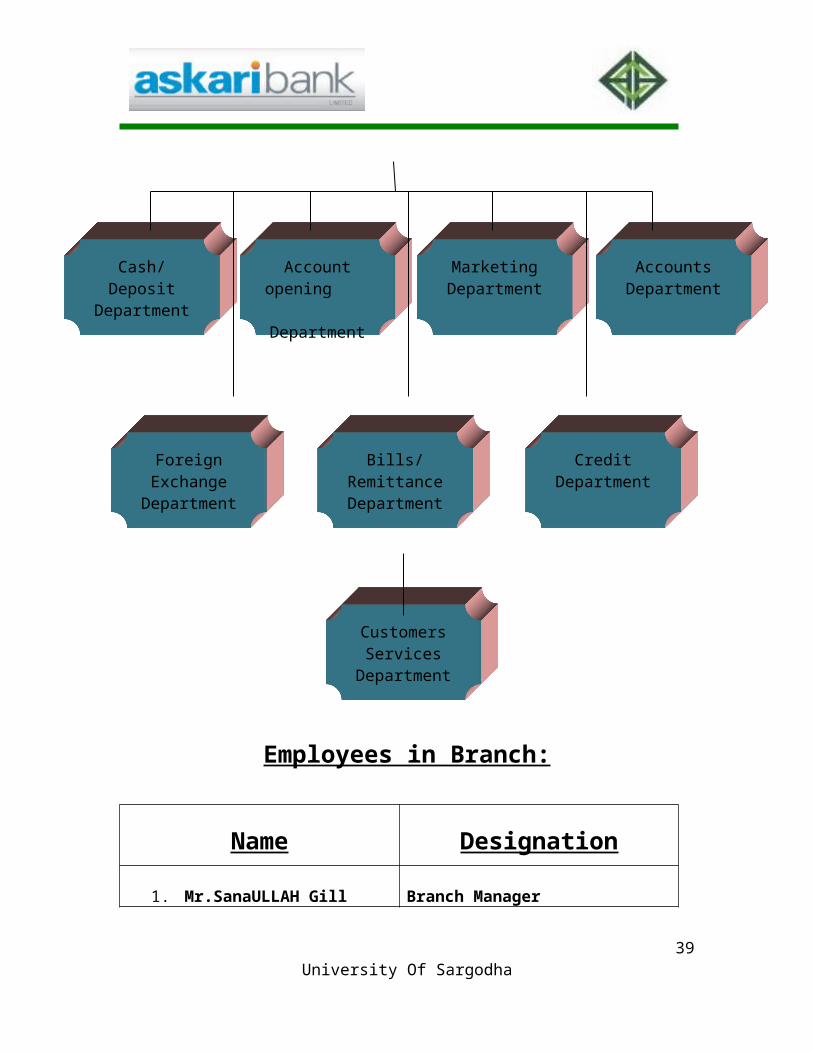

Cash/Deposit Department

Account opening Department

Marketing Department

Accounts Department

Foreign Exchange

Department

Bills/ Remittance Department

Credit Department

Customers Services

Department

Employees in Branch:

Name Designation

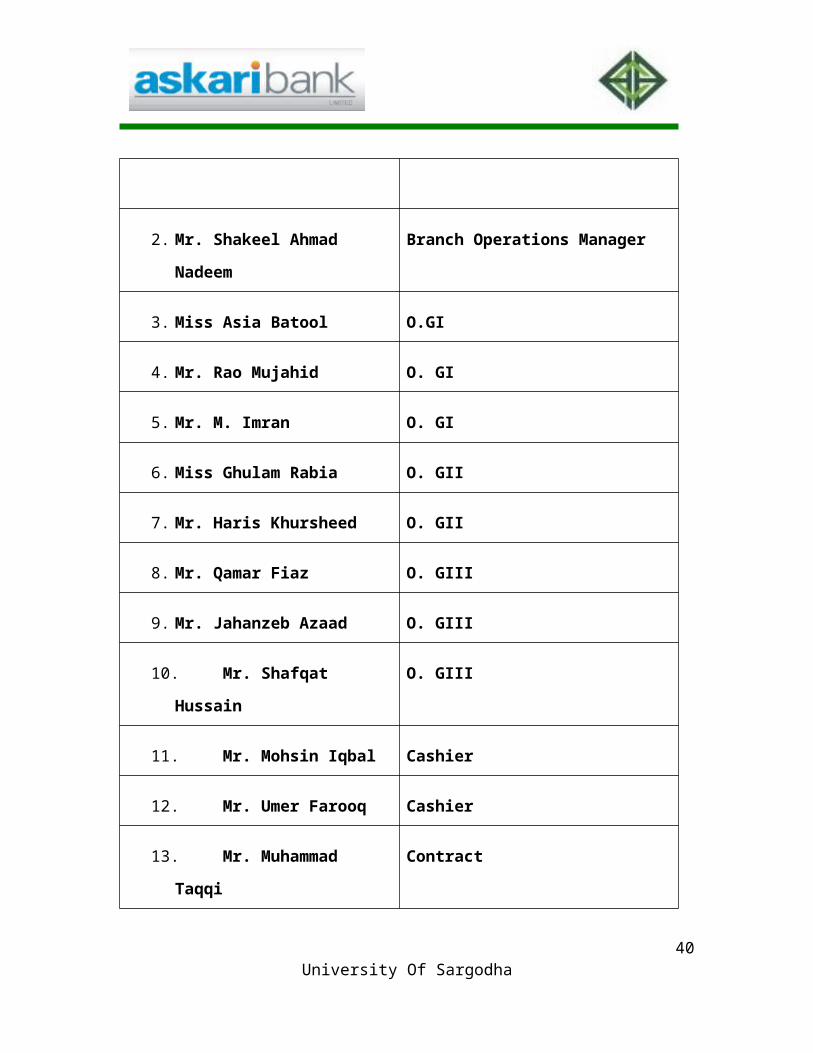

1. Mr.SanaULLAH Gill Branch Manager

2. Mr. Shakeel Ahmad Nadeem Branch Operations Manager

3. Miss Asia Batool O.GІ

4. Mr. Rao Mujahid O. GІ

5. Mr. M. Imran O. GІ

6. Miss Ghulam Rabia O. GІІ

7. Mr. Haris Khursheed O. GІІ

8. Mr. Qamar Fiaz O. GІІІ

9. Mr. Jahanzeb Azaad O. GІІІ

10. Mr. Shafqat Hussain O. GІІІ

11. Mr. Mohsin Iqbal Cashier

12. Mr. Umer Farooq Cashier

13. Mr. Muhammad Taqqi Contract

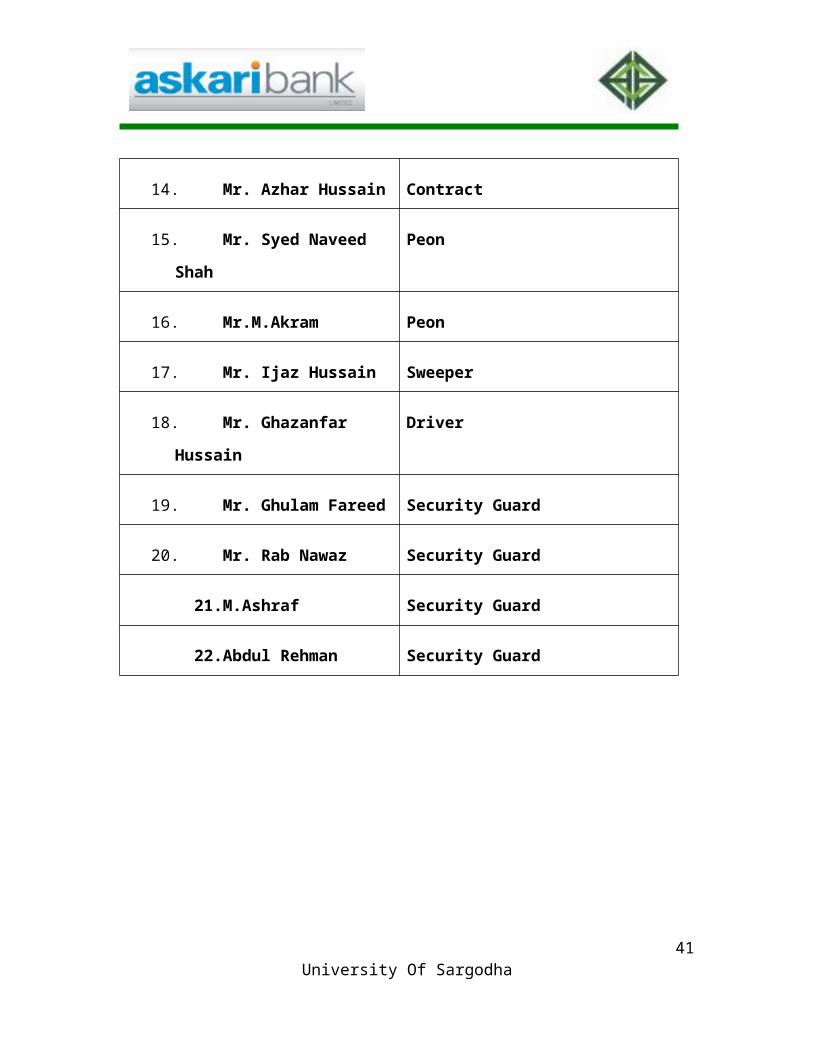

14. Mr. Azhar Hussain Contract

28

University Of Sargodha

15. Mr. Syed Naveed Shah Peon

16. Mr.M.Akram Peon

17. Mr. Ijaz Hussain Sweeper

18. Mr. Ghazanfar Hussain Driver

19. Mr. Ghulam Fareed Security Guard

20. Mr. Rab Nawaz Security Guard

21.M.Ashraf Security Guard

22.Abdul Rehman Security Guard

29

University Of Sargodha

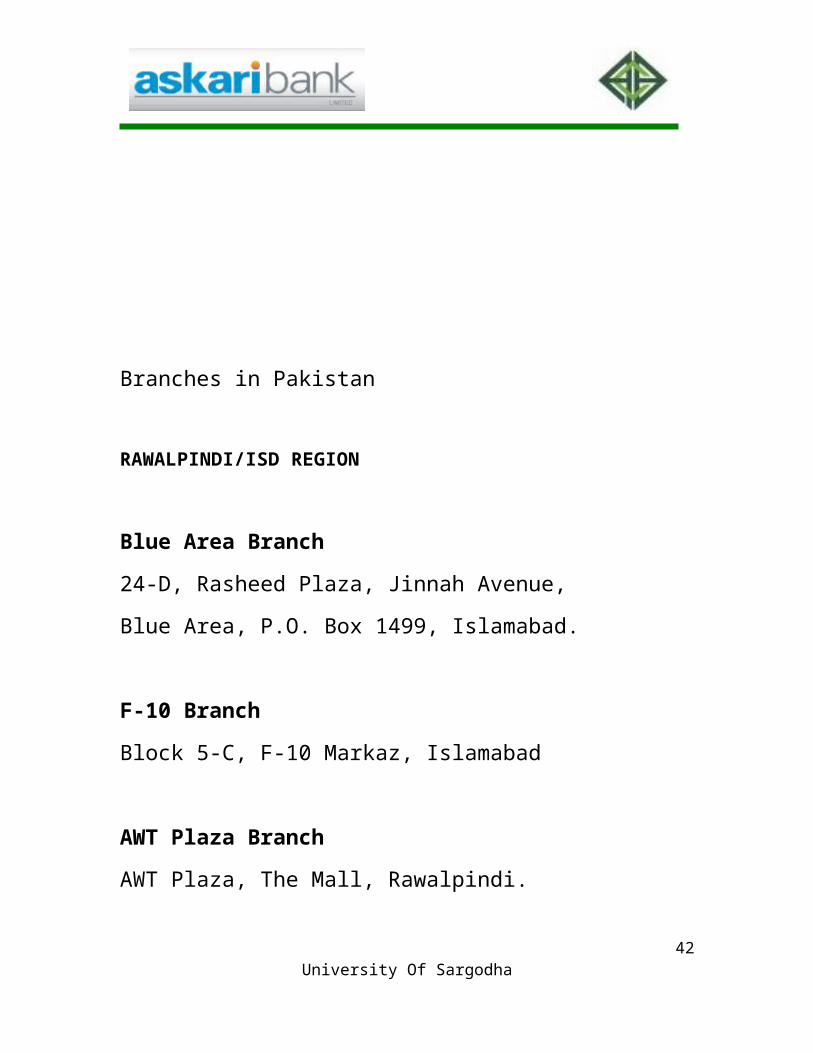

Branches in Pakistan

RAWALPINDI/ISD REGION

Blue Area Branch

24-D, Rasheed Plaza, Jinnah Avenue,

Blue Area, P.O. Box 1499, Islamabad.

F-10 Branch

Block 5-C, F-10 Markaz, Islamabad

AWT Plaza Branch

AWT Plaza, The Mall, Rawalpindi.

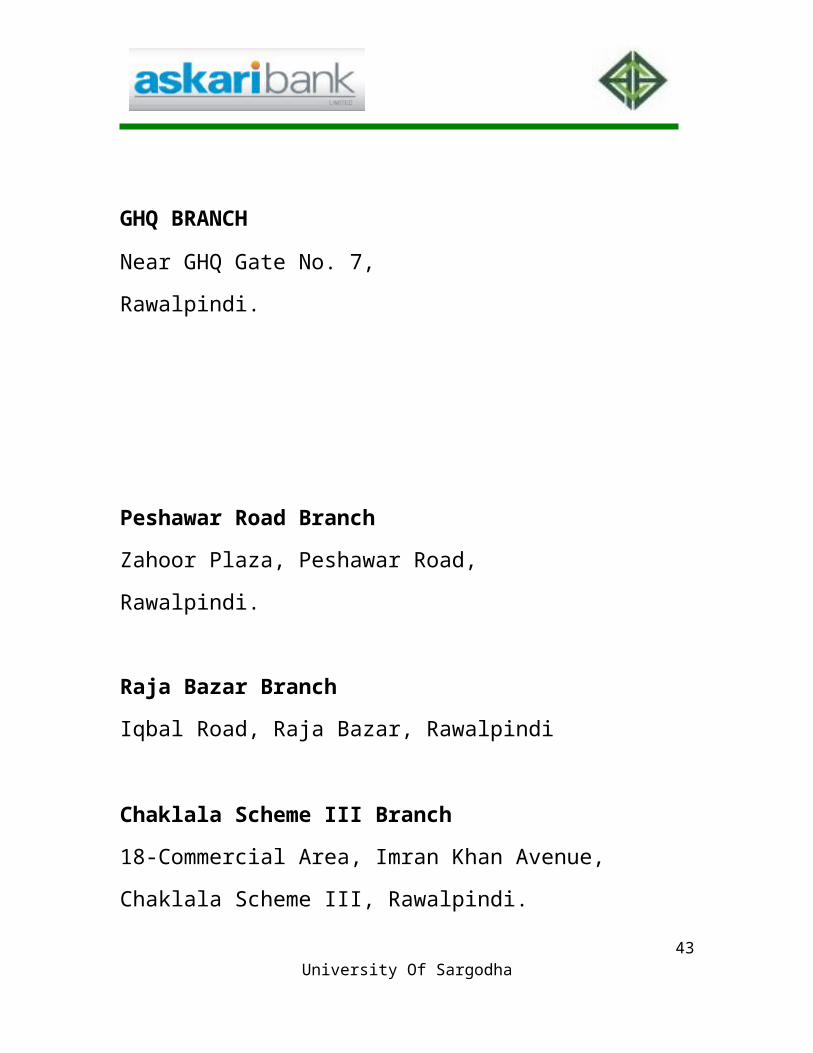

GHQ BRANCH

Near GHQ Gate No. 7,

Rawalpindi.

30

University Of Sargodha

Peshawar Road Branch

Zahoor Plaza, Peshawar Road,

Rawalpindi.

Raja Bazar Branch

Iqbal Road, Raja Bazar, Rawalpindi

Chaklala Scheme III Branch

18-Commercial Area, Imran Khan Avenue,

Chaklala Scheme III, Rawalpindi.

Hyder Road Rawalpindi Branch

Hyder Road Sadar Rawalpindi

Satellite Town Rawalpindi

313-T Commercial Market,

5th Road Satellite Town, Rawalpindi

31

University Of Sargodha

NORTH REGION

Peshawar Cantt Branch

Plaza Branch, 3-7, Fakhr-e-Alam Road,

Peshawar Cantt.

Chowk Yadgar Branch

Chowk Yadgar, Peshawar City.

Abbottabad Branch

Lala Rukh Plaza, Mansehra Road, Abbottabad.

Mardan Branch

The Mall, Mardan.

Mirpur Branch

Hanfi Building Branch,121 C/1, Sector C-2,

Chowk Shaheedan, Mirpur.

32

University Of Sargodha

LAHORE REGION

Badami Bagh Branch

165-B, Badami Bagh, Lahore

Tufail Road Branch

12-Tufail Road, Lahore Cantt.

Circular Road Branch

77-Circular Road, Lahore

Gulberg Branch

10-E/11, Main Boulevard

Gulberg-III, Lahore.

Lahore Main Branch

Shahrah-e-Aiwan-e-Tijarat, Lahore.

33

University Of Sargodha

LCCHS Branch

L.C.C.H.S Society Office

Sector Y, Commercial Area,

Phase-III, Lahore Cantt.

The Mall Branch

The Mall, Lahore

EAST REGION

Bahawalpur Branch

1-Noor Mahal Road, Bahawalpur.

Faisalabad Main Branch

University Road, Faisalabad

Gujranwala Branch

Trust Plaza, G.T. Road,

Gujranwala.

34University Of Sargodha

Multan Branch

Abdali Road, Multan.

Rahimyar Khan Branch

Ashraf Complex, Model Town,

Rahimyar Khan.

Phoolnagar Branch

Lahore-Multan Road, Distt. Kasur,

Sahiwal Branch

48/B & B1, High Street Branch, Sahiwal.

Sargodha Branch

80-Club Road, Old Civil Lines Sargodha.

Jhang Branch

35

University Of Sargodha

Church Road Jhang Sadar

Sialkot Branch

Paris Road, Sialkot.

Gujrat Branch

Hassan Plaza (Opposite Pak Fan Mosque),

GT Road, Gujrat.

Peoples Colony Branch

Peoples Colony,

Faisalabad.

SOUTH REGION-I

Cloth Market Branch

Laxmidas Street, Karachi

36

University Of Sargodha

Gulistan-e-Jauhar Branch

Asia Pacific Trade Centre,

Rashid Minhas Road, Karachi.

Jodia Bazar Branch

Qazi Usman Road, Near Lal Masjid,

P.O Box: 6831, Karachi.

Saima Trade Tower Branch

I.I. Chundrigar Road, Karachi.

Gawadar Branch

Airport Road, Postal Code 91200, Gawadar.

Hydri Branch Karachi

SF 14/18 Alburhan Arcade,

37University Of Sargodha

Block E Barkat-e-Hydri,

North Nazimabad Karachi 74700

Sukkur Branch

Sarafa Bazar, Sukkur

SOUTH REGION-II

Clifton Branch

Marine Trade Centre, Block-9,

Karachi.

Defense Branch

Jami Commercial Street No.11,

Off Khayaban-e-Ittehad,

Phase-VII, Defence Housing Authority, Karachi.

Sharah-e-Faisal Branch

38University Of Sargodha

11-A, Progressive Square, Block-6, P.E.C.H.S,

P.O. Box: 12696, Karachi.

Bahadurabad Branch

Zeenat Terrace,

265-Block 3,Bahaduryar Jang Society,

Bahadurabad, Karachi.

Dar-ul-Aman Branch

Dar-ul-Aman, Housing Society,

47-A, Block No. 7& 8, Shahrah-e-Faisal, Karachi.

Hyderabad Branch

332-333, Saddar Bazar

Quetta Cantt Branch

Chilton Road, Bolan Complex, Quetta Cantt.

39University Of Sargodha

Quetta Main Branch

M.A Jinnah Road, Quetta.

Chaman Branch

Trunk Road, Off Mall Road, Chaman.

Corporate Information

Lt. Gen. Imtiaz Hussain (HIM)

Lt. Gen. (R) Zarrar Azim

Chairman Executive Committee

Mr. Shaharyar Ahmad

President & Chief Executive

Brig (R) Muhammad Shiraz Baig

Company Secretary

Brig (R) Asmat Ullah Khan Niazi

40University Of Sargodha

Director

Brig (R) Muhammad Bashir Baz

Director

Brig (R) Shaukat Mahmood Chaudhari

Director

Mr. Zafar Alam Khan Sumb

Director

Mr. Kashif Mateen Ansari

Director

Mr. Muhammad Najam Ali

Director

Mr. Muhammad Afzal Munif

Director

Mr. Tariq lqbal Khan Director

Director

Mr. A.J.MubbasharDirector

(NIT Nominee)Director

41

University Of Sargodha

Audit Committ ee

Dr. Ziauddin Ahmad

Road, Karachi

Brig (R) Muhammad Shiraz Baig

Member

Mr. Kashif Mateen Ansari

Member

Auditors

A.F.Ferguson & Co.

Chartered Accountants

Legal Advisors

Rizvi, Isa, Afridi & Angell

Registrar & Share Transfer

M/s THK Associates

(Private) Limited,

Ground Floor, State Life Building # 3,

Brig (R) Asmat Ullah Khan Niazi

Chairman

42

University Of Sargodha

Executive Profiles

Mr. Agha Ali Imam- Senior Executive Vice President

M.R Mehkari - Senior Executive Vice President

Suhail Ahmad Rizvi- Executive Vice President

Mr. Nazimuddin A. Chaturbhai, Senior Executive Vice President

Mr. Tahir Aziz, Executive Vice President

Malik Asad Ali Noon, Executive Vice President

Introduction Of All Departments

Departments Of Askari Commerical Bank

Accounts Department

Cash Department

43

University Of Sargodha

Clearing Department

Credit Department

ACCOUNT OPENING

DEFINITION OF BANKERS:

As defined in section 3(b) of negotiable instrument act 1881,

‘”bankers” means the person transacting the business of accepting for the purpose of

lending on investment of deposits of money from the public, repayable on demand

or otherwise, and withdraw able by cheque, draft, or otherwise, and include the post

office savings the bank.

DEFINATION OF THE CUSTOMER:

A customer is the person who maintains a regular bank

accounts without taking in to consideration the duration and frequency of operation

of his accounts it means that the person becomes a customer of the bank as soon as

he open his accounts deposit money in the same and the bank accepts the said

deposit.

QUALIFICATION OF CUSTOMER:

He should not be a minor because a minor is not competent to contrect.according

to section (3) of the majority act 1875 a person is deemed to have attained the age of

majority when he has completed the age of (18) years.

44

University Of Sargodha

He should be a person of sound mind

Section (12) of the contract act says that “the person is said to be of sound mind for

entering into contract if at the time when he makes it he is capable of understanding

it and of forming a rational judgment as to its effects upon his interest.

He should have not been debarred from entering in to any contract under the law.

There is an offer by the customer and acceptance by the banker. The customer offer

the money to deposit and banker offers to accept it.

RIGHTS OF A CUSTOMER:

A customer has the following universally accepted rights.

To draw cheques against his credit balance in the account.

To receive pass book or statement of his account.

To sue the bank for the cost, loss and damages, when his cheque is wrongfully

dishonored by the banker.

To sue when the banker has not maintained the secrecy of his account, except when

it is done under compulsion of law in the interest of the bank or as the duty to

public.

DUTIES OF THE CUSTOMER:

Section (72) of negotiable instrument act 1881 lies down that the customer must

present the cheques for payment and collection with in the business hours of the

bank.

To keep his cheque book under lock and key

45

University Of Sargodha

To draw the cheques very carefully so that there is no room for any fraudulent

additions or alterations.

To see that the cheque issued by him presented to the bank for payment with in a

reasonable time.

OPENING OF ACCOUNT

The banking history is replete with various instances of fraud largely

due to incorrect opening of accounts. These fraud could have been avoided in if the

branch managers and other designated officers had taken due care and exercised

required precautions at the time of opening of accounts.

At the time of opening of accounts, officers should tactfully obtain as much

information as possible about the integrate and character of the person, his correct

name, address and occupation. This infect will be the only opportunity when they

will be able to talk to the prospective customers in a friendly and frank atmosphere.

This is the time when they have a slight edge over the customer. He or she at this

point of time is willing to divulge as much information about his personal status and

business etc to the bank manager. It is therefore necessary that due care and proper

procedure be followed for opening different types of accounts for various types of

customers.

Askari commercial bank limited has the following classifications of accounts,

INDIVIDUALS ACCOUNTS

PARTNERSHIP FIRM ACCOUNTS

JOINT STOCK COMPANY ACCOUNTS

AGENCY ACCOUNTS

46

University Of Sargodha

CLUBS, SOCIETIES & ASSOCIATIONS ACCOUNTS

EXECUTORS AND ADMINISTRATORS ACCOUNTS

TRUSTS

LOCAL BODIES ETC.

PROPERITORSHIP

JOINT ACCOUNTS

OTHER MISC ACCOUNTS

When a customer opens an account under the law he enters into a contractual

relationship with the bank.

At the time of opening the account, intended customer must have the following

characteristics:

A He must have reached the age of majority

In term of section 3 of the Indian majority act 1875 (as adopted in Pakistan) a person

is a major if he attain the age of 18 years. However, the age of majority shall be 21

years in case of European nationals and also where guardian is appointed under the

guardians and wards act.

A person who is under the age specified herein above is considered a minor. In term

of section 11 of the contract act, a minor is declared incompetent to enter into a

contract. As such, any contract with a minor is a void. However, the banks generally

allow the minor to open accounts with a view to inculcate in them the habits of

saving. Such account is opened jointly with their guardian and is allowed to be

operated by the guardian. The guardian for the purpose will sign the account

opening from and the specimen signature card.

A person is said to be of sane or sound mind it he understands the terms and the

47

University Of Sargodha

conditions of the contract and is capable enough to form rational judgment as the

effects of the contract upon his interest.

He must not be insolvent and bankrupt.

At the time of opening the account, he should not be adjudicated as insolvent.

Generally a person is considered as insolvent if his liabilities exceed the assets he is

possessing.

He must not be debarred under any law from entering into any contract.

It is the duty of the banker to make sure that all above criteria is satisfied before he

allows the opening of the account.

For general guidance of the officers, given below are the essential points that must

not escape their attention while opening the accounts.

WHO DEAL WITH OPENING OF ACCOUNT:

As for as possible the account opening job should be handled by the branch manager

himself. Only in exceptional cases in main branches, the job may be assigned to

other officers.

INFORMATION:

As much relevant information as possible must be elicited from the prospective

customer relating to his means, line and place of business etc.

FORMS TO BE FILLED IN CAREFULLY:

Each and every column of the account opening form should be neatly and correctly

filled in with necessary details.

48

University Of Sargodha

INTRODUCTION OF ACCOUNT:

Account must be properly introduced. In this concern, the following precautions are

to be observed.

I As for as possible, the person introducing the account should attend

the personally with the prospective customer. This would serve the dual purpose.

A branch manager shall have the opportunity of eliciting vital

information as to the standing, respectability and the means of the person he is

introducing.

B The identity of the customer must be properly established beyond any

doubt.

Introducing from person having doubtful dealing with the bank should be discretely

declined. The staff member generally should not introduce the account. They will

introduce accounts only for those persons who are personally known to them and

whose credentials are absolutely clean.

As for possible, the account opening form should be completed by the prospective

customer in presence of the introducer who is then aware of the particulars furnished

and can corroborate the same.

Specific information concerning the profession should be recorded in the account

opening form. The description private Service’ or ‘Businessman’ is insufficient.

Signature on the account opening form must be put by the customer will attest them

properly in presence of introducer.

No cheque book should be issued to the new accounts are properly introduced.

Account may be opened with cash or cheque. Initial deposits, it is incumbent upothe

49

University Of Sargodha

Branch Manager to satisfy themselves additionally that title of account holder is

genuine for the cheque deposited. Prudent bankers avoid opening new accounts with

Cheque. Letter of thanks should be sent to the introducer the day the account is

opened. This precaution would accomplish the purpose of intimating the introducer

that the account has been opened on strength of his introduction thereby inviting

disclaimer if untrue.

A letter of thanks should be sent to the new account holder, preferably through

registered mail, to verify his address.

In the evening, the officer of the branch should visit the customer’s area to establish

that the address given by the customer is correct and the commands respect and

honor in the neighborhoods/vicinity he is living.

Number of the customer’s national identity card should be correctly recorded in the

account opening form and copy of it should be kept on record.

No account should be opened in the name of an undercharged insolvent.

TYPES OF ACCOUNTS

Let us now turn to procedure to be followed in case of each type of accounts.

INDIVIDUAL ACCOUNTS:

Such account may be classified as follows:

Accounts of literate ladies and gentlemen.

Accounts of parade observing ladies.

Joints accounts.

Minor accounts.

1. In order to open the account for literate people an account opening form,

signature card, form “A”, and an ID copy are required with Rs. 2500 for opening

50

University Of Sargodha

account and he must fulfil all customer characteristics.

2. In case of illiterate ladies and gents, the following precautions are observed in

addition to those provided in the above guideline.

a) Two photographs are to be obtained one to be pasted on account opening form

and the other specimen signature card.

b) Instead of signature left hand thumbs impression to be obtained on the specimen

signature card from gents and right hand thumb impression from the ladies.

c) Each time such customers should attend the bank personally and will put their

thumb impressions on the cheque before the passing officer.

d) Such customers should be advised not to issue cheque payable to third parties.

e) Cheque should be marked payment in person to ensure even if the cheque is

presented through clearing that particular cheque can only be paid in person

3. When account is opened by more than one person but the relationship between

them is neither of trustees nor partners it would be termed as joint account.

Whenever such accounts are open-end, definite instruction regarding operations on

the account and payments of balance in cased of death of any one of them should be

obtained.

4. A person who is under the age as specified above is considered as minor, a

minor is declared incompetent to enter into a contract. However, the banks

generally allow the minor to open accounts with a view to the condition of saving

habits. Such account is opened jointly with their guardian and is allowed to operate

by the guardian.

ACCOUNTS OF PARTNERSHIP FIRMS:

51

University Of Sargodha

While opening accounts of the partnership firms, the

partnership deed from registered firms is required obtained in the addition to account

opening form and specimen signature card. The partnership letter is attached with

the

Accounts opening form, which must also be signed by all the partners of the firms

whether registered or unregistered.

In these accounts, the following points should be remembered.

1. All the partners must sign the account opening form.

2. The names of persons authorised to operate the account must be neatly and

correctly given in the account opening form.

3. For partnership concerns carrying on the business under impersonal name it is

generally described that the title of accounts should show name of the partners or

managing partner.

4. A cheque payable to the firm should not be accepted for credit to personal

accounts of the partners without the written authority of all the partners.

5. The maximum numbers of partners in general business 20 and the minimum is 2

for the banking firms the maximum numbers of the partners is 10 in Pakistan

however bank can not be opened by the partnership concern.

6. Since these are the business concern they will be allowed to open current

accounts. No saving s bank accounts be opened in partnership name.

Partnership account opening required following documents:

1) Account opening form (A.O.P)

2) A.O.P should be duly introduced

3) Copy of N.I.C Of all partners

4) Registration certificate (optional)

5) Partnership deed

52

University Of Sargodha

6) Rubber-stamp on letterhead of the firm

7) Letter Head

8) Official capacity (It means that all the partners will sign and choose the singe for

operation of account with the bank. And in account opening form the name of the

Official capacity is written in special instruction and recommended by all the

partners).

ACCOUNTS JOINT STOCK COMPANIES:

Joint stock companies include

Private limited companies and

Public limited companies

PRIVATE LIMITED COMPANIES:

Private limited companies are those where the share capital is not

offered to the general public instead the offer is restricted to particular class of

society or with in the family members. Generally their share is not transferable. The

minimum number of

Shareholder is 2 and maximum, is 50 private limited company are not listed on stock

exchanges and therefore their shares are not publicly quoted.

PUBLIC LIMITED COMPANIES:

In this case, the promoters and general public contribute share

capital. Any Pakistani who is authorised to enter into contract can purchase share.

Shares of these companies are transferable and brought and sold freely in stock

exchanges. The minimum number of shareholder is 10 whereas there is no upper

limit.

The following documents are required for joint stock company’s account

opening.

53

University Of Sargodha

a) Copy of resolution

While opening the company’s account, the manager must ensure that board of

directors of the company is properly constituted and request for opening the account

comes through resolution of the board of directors. The resolution for account

opening should bear company seal and signed by the chairman of the meeting where

Such resolution is passed and counter-signed by the company’s secretary or

authorised director must be submitted to the bank before an account can be opened.

b) A.O.F. duly signed.

c) Memorandum of Association & Articles of Association.

d) Certificate of Incorporation.

e) Certificate of Commencement of Business (only required for public limited

companies.

f) National identity cards of directors.

g) List of director with their shareholding.

h) Specimen signature card duly signed

ACOUNT OF PROPRIETOR:

1. A.O.F should be duly introduced

2. Copy of N.I.C of proprietor

3. Specimen signature card duly signed

4. Proprietorship declaration concerns on firm’s letterhead’s

ACCOUNTS OF CLUBS, SOCIETIES AND ASSOCIATION:

Clubs, societies and associations are non-profit and non-trading in nature. They have

their own rules and regulations and committees mention their affairs, which is called

Governing Bodies.

Documents that are required are:

i) Account opening form

54

University Of Sargodha

ii) Specimen signature card

iii) Resolution to be passed by their governing bodies

iv) Certified copy of rules and regulations or Bye-law

v) Letter of registration

Letter of undertaking to the effect that as and when change take place they will

inform the bank of such changes.

DEPOSITS:

Deposit is the lifeblood of a commercial bank. Main function of a commercial

bank is to enhance the savings from the savers to the ultimate user of funds. The

process of collecting savings is called Deposit Mobilization.

FORMS OF DEPOSITS:

Two broad forms of deposits with reference to time period are:

A)Demand deposit: These are payable on demand. They include current

account, sundry deposit (e.g. margin account) and deposit receipt. No profit is given

on demand deposits.

i) CURRENT ACCOUNT:

ii) This type of account is usually opened for businessman or such persons

who needs deposits and withdrawals facility without any restriction.

Introduction is necessary when opening a current account, the procedure

has already been explained else were in this book and account number is

allotted and for withdrawals cheque book is issued and a statement of

account is provided so that customer can reconcile his account with his

own record.

No interest return is paid on such account is Pakistan; This account can be

55

University Of Sargodha

opened with Rs. 500. Banks usually recover service/incidental charges on

current account if the required minimum balance is not maintained. Or when the

maintenance of the account becomes expenses e.g. For example too many

transactions take place on summing a large number of chequebooks and other

stationary not consistent with the average balance.

ii) CALL DEPOSIT RECEIPT:

It is a contract for a specific deposit transaction and is used as a security for

bidding etc. It is non-transferable and is payable only to beneficiary or purchaser.

iii) SUNDRY DEPOSIT -MARGIN ACCOUNT,

At the time of issuance of LG / LC or acceptance the party is supposed to deposit

is kept in an account called sundry deposit. Margin account Similarly, at the time of

allotment of locker the locker holder is supposed to deposit a certain sum as

security, which is kept in sundry deposit account.

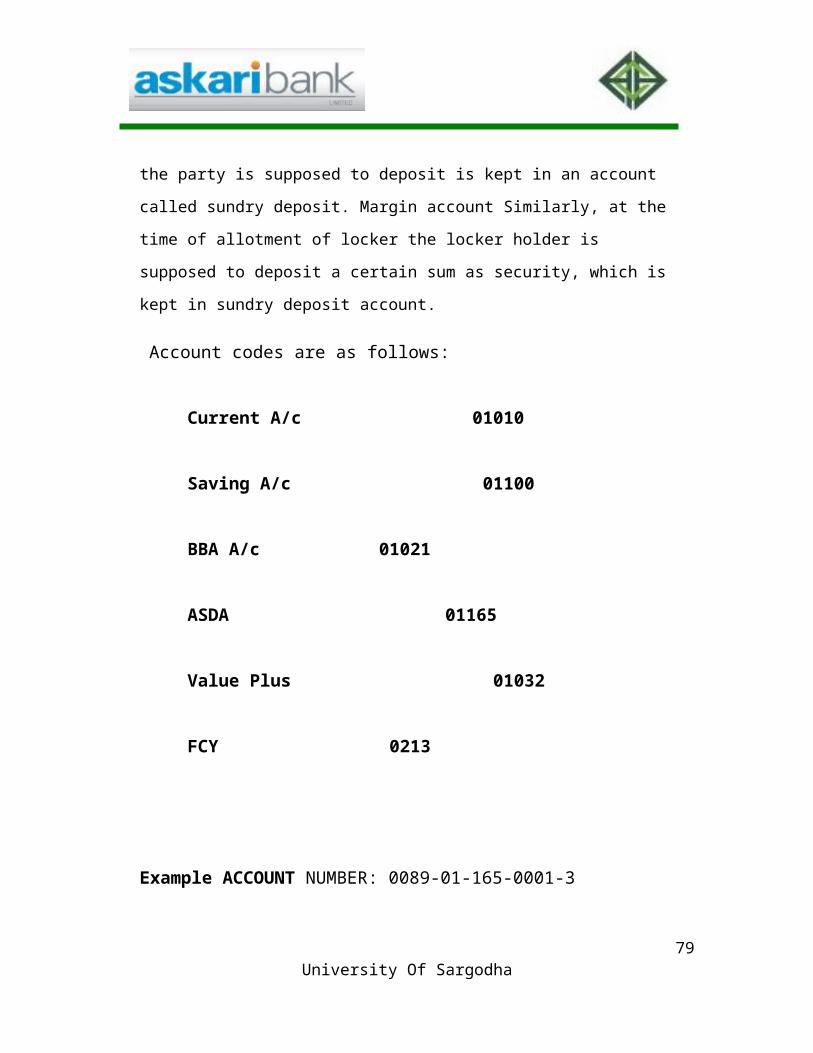

Account codes are as follows:

Current A/c 01010

Saving A/c 01100

BBA A/c 01021

ASDA 01165

56

University Of Sargodha

Value Plus 01032

FCY 0213

Example ACCOUNT NUMBER: 0089-01-165-0001-3

0089 = Branch Code

01 = Currency Code

165 = Asda Account

0001 = Account Number of the Asda Account Holder

There are three modes of posting in ledger balance

MODES OF POSTING

Cash

Clearing

Transfer

Cheque Book Issuance

Cheque book is issued for only, current account PLS account and ASDA,

57

University Of Sargodha

FISDA and FAIDA accounts. It is not issued for PLS Term Deposit and value plus

Saving Accounts, because in these accounts, amount cannot be withdrawn within a

fixed time period.

Procedure or Cheque Book Issue:

1. Signatures on cheque book requisition are verified by matching with the

Signatures on the SS card scanned into the computer.

2. The title of account and date of chequebook issuance is mentioned on the

chequebook requisition and the account opening officer signs the requisition

leaf.

3. The next chequebook number that was previously entered in the register is

allotted to the account holder.

4. The title of the account is entered in the chequebook issuance register.

5. The chequebook of that number is taken out and filled in with the title of

account, account number, etc and signed by the officer.

6. Each leaf of chequebook is stamped with account number stamp.

7. Cheque book charges are deducted from the account according to the leaves of

58

University Of Sargodha

the cheque books (Rs.6/- for each leaf.)

8. To deduct the chequebook charges, the debit voucher should be filled with that

amount and should be handed over to the account holder.

Categories of Cheque Books

1. Ten Leaves:

It is used for value Plus, PLS account and FADIA account.

2. Twenty-five Leaves:

It can also be used for current deposit, value plus, PLS and FADIA accounts.

3. Fifty Leaves:

It is used for current deposit and ASDA account.

4. Hundred Leaves:

It can also be used for current deposit, value plus, PLS and FADIA accounts.

59

University Of Sargodha

REMITTANCE DEPARTMENT

The need of remittance is commonly felt is commercial life particularly and in

everyday life generally. The main function of the remittance department is to transmit

money from one place to another. By providing this service to the customer, bank earns a

lot of income. Also customer is able to meet its day to day financial requirements.

Demand Draft

It is an instrument payable on demand for which value has been received, issued

by the branch of the bank drawn i.e. payable at some other place (branch) of the same

bank. If two banks are involved then the DD is sent to other bank but in other case it is

handed over to the applicant.

Issuance Procedure:

A demand draft application is given to the customer; he fills in relevant

information and signs it.

The officer checks the information form.

The bank charges such as commission, excise duty is charged as per effective

schedule of charges. If he fills the tax exemption form, tax is not charged.

60

University Of Sargodha

In case of cash deposit, the cashier counts the amount and signs the DD

application and enters it in the register.

Then the officer of remittance department signs it and operation manager counter

signs it.

The entry is made in the DD issuing register, DD is given to the customer.

Vouchers are prepared and posted.

DD advises are printed and mailed to the respective branch.

Payment Procedure:

DD is received by the bank.

The DD credit advice is received through mail. The numbers are checked and

signatures are verified.

An entry is made on the DD payable register and the vouchers are made.

DD credit is attached with the vouchers and given for posting to the computer.

When DD is received the test numbers are checked and the payment is made.

61

University Of Sargodha

Vouchers are given for posting and the entry that was made in the register is

closed i.e. DD payable is Nil.

Telegraphic Transfer (TT)

It is the quickest way of transfer of funds from one place (Branch) to other place

(Branch) of the same bank. Generally, a mail transfer advice reaches the drawer branch

the next day through courier services. But sometimes, a customer demands that his funds

should be transferred through the quickest means. In such cases, transfer of funds

message is passed through telephone or telegram.

This mode of transfer was used before online. Online system is very effective for

this purpose now-a-days. In Askari Commercial Bank online system is used.

Issuance Procedure:

The request of issuing TT is taken on the standard printed form.

The customer fills the form properly and signs it.

The Head of Remittance Department checks it, the charges such as commission,

tax and telex as per effective schedule and signs it.

If he fills the tax exemption form then no tax is deducted.

62

University Of Sargodha

Then a TT is made on white slip. There are 3 copies, the original one is faxed to

the Branch, one to the Head Office and one is kept for record.

The entry is made in the TT issuing register.

When commission bill is received, it is attached to the TT office copy in the file.

Payment Procedure:

When a TT arrives, the test numbers are checked and the signatures are verified.

The entry is made in the TT payable register.

If there is no account then the TT received needs revenue stamp and then payment

is made. TT receipt is strictly non-negotiable.

Pay Order

It is an instrument issued for payment in same city. Pay order issued from on e

branch can only be payable from the same branch. It is normally referred to as banker’s

cheque. It is also called confirmed cheque, because bank issues this on it own guarantee.

Issuance Procedure:

The standard form is given to the customer. He fills in the details and signs it.

The concerned officer checks the form.

63

University Of Sargodha

Bank charges (or commission) as per the schedule of charges and the withholding

tax of 0.3% are applied.

The cash amount of the pay order is received.

A cash memo is signed, stamped and handed over to the applicant as a receipt.

Then the pay order receipt is filled accordingly.

Counter foil is also filled.

An entry is made in the pay order issue register.

Then the authorized officer signs it after checking the pay order.

The order is then handed over to the applicant after obtaining his signature on the

PO Form.

A voucher is also made and posted at the computer.

Payment Procedure:

On presentation of the pay order receipt, two authorized officers of the branch

sign the receipt.

PO entry is made in the PO issue register.

Then the amount is credited to the account of the customer or pain in cash.

PO is posted at the computer.

64

University Of Sargodha

Pay Slip

It is an instrument issued by the bank for the settlement of its own payment. It is

used for payment by the bank to anyone (may be employees) in this case only one bank is

involved. He is the issuer as well as the payer.

No Excise Duty

No Commission

Issuance:

A credit voucher is sent from the account department to the remittance

department.

Pay Slip book is taken out and filled according to the credit voucher.

It is entered in the pay slip register.

It is signed by authorized Officer.

A voucher is prepared and posted.

Pay Slip is then handed over to the customer.

Payment Procedure:

Pay Slip is just like a cheque and bank is liable to pay against pay slip.

After that when the pay slip is received by the bank for payment, it is again

transferred in the register.

Then payment is made and it is posted in the computer.

Outward Bills for Collection

The bills, which are received by the bank and sent to other cities (branches) for

the local clearing in that city, are called Outward Bills for Collection.

65

University Of Sargodha

Procedure:

The cheques that are of other cities are separated.

They are entered in the OBC Register and OBC numbers are given to them.

The OBC forwarding schedules are prepared for different branches.

The respective cheques are attached with the schedule.

The office copy is filled and original schedule is mailed.

On clearing, the respective banks send back the OBCs along with the IBCA (Inter

Branch Credit Advice).

The OBC numbers are checked from the OBC register, after that entries are made.

Commission charges are deducted from the account.

Inward Bills for Collection

The bills, which are received by the bank from other branches out of the city for

local clearing, are called Inward Bills for Collection.

Procedure:

The OBC of other branches will be the IBC of this branch. So an OBC forwarding

schedule is received by mail.

The cheques are entered in the IBC register. The IBC numbers are allotted to

them.

The cheques are lodged for clearing.

After realization, an IBCA is prepared and mailed to the branch from where the

cheque was received.

At the end of the day, two vouchers are prepared and posted.

66University Of Sargodha

CLEARING

Meaning of clearing:

The word clearing has been derived from the word “Clear” and is defined as “a

system by which banks exchange cheques and other negotiable instruments draw on each

other within a specified area and thereby secure payment for their client through the

clearing house at specified time” in an efficient way.

Advantages of Clearing:

1. Since clearing does not involve any cash etc and all the transaction take place

through book entries, the number of transactions can be unlimited.

2. No cash is needed as such the risks of robbery, embezzlements and pilferage are

totally eliminated.

67

University Of Sargodha

3. As major payments are made through clearing, the banks can manage cash

payment at the counters with a minimum amount of cash in vaults.

4. A lot of time, cost and labour are saved.

5. Since it provides an extra service to the customers of banks without any service

charger or costs, more and more people are inclined and attracted towards

banking.

Clearing House:

It is a place where representatives of all scheduled banks sit together and

interchange their claims against each other with the help of controlling staff of State Bank

of Pakistan and where there is no branch of State Bank of Pakistan the designated branch

of National Bank of Pakistan acts as controlling member instead of State Bank of

Pakistan.

Working of clearing house:

All the bank which are the member of clearing house maintain accounts with

State Bank of Pakistan by debit and credit to which the clearing settlements are made. If

on a particular day, a bank delivers cheques and other negotiable instruments worth more

than the total amount of Cheque received by it that banks accounts with State Bank of

Pakistan will be credited with the differential amount. If on the other hand the total

amount of cheques and other negotiable instruments draw on a certain bank by other bank

is more than the total amount receivable by it from other banks, then this bank’s account

will be debited on that day.

68

University Of Sargodha

The cheque delivered to the representatives of other banks for clearing are called

outward clearing, whereas cheques received from the representatives of other banks for

payment are called inward clearing.

Procedure of Settlement:

Presume that ACBL got the cheques which are drawn on HBL, NBP and MCB

for amounts Rs. 50,000/-, Rs. 15,000/- respectively, its total being amounts Rs.95,000/-,

it means that this amount is to be credited to ACBL A/C with S.B.P. on the other hand

the cheques drawn on ACBL are from HBL, NBP and MCB of Rs.15,000/-, Rs.75,000/-

and Rs.30,000/- respectively, its total being Rs.1,20,000/-, it means that this amount is to

be debited from ACBL account. The difference between Rs.95,000/- credit and debit

Rs.1,20,000/- debit is Rs.25,000/- debit which means the house is against ACBL for

Rs.25,000/-.

If we separately show it them.

1. ACBL has t receive Rs.50, 000/- from HBL and to pay Rs.15, 000/- to HBL so

difference is Rs.35, 000/- credit.

2. ACBL has to receive Rs.30, 000/- from NBP and to pay Rs.75, 000/- to NBP so

difference is Rs.45, 000/- debit.

3. ACBL has to receive from MCB Rs.15, 000/- and to pay Rs.30, 000/- to MCB so

difference is Rs.15, 000/- debit.

GRAND TOTAL:

69

University Of Sargodha

35000-45000-15000 = -25000

i.e. Rs.25000 debit.

Hence ACBL A/C with State Bank of Pakistan will be debited with Rs.25, 000/-

and the contra will be other banks accounts respectively. This called as “Debit and Credit

Rule”.

Outward Clearing At The Branch

The following points are to be taken into consideration while an instrument is

accepted at the counter to be presented in outward clearing:

1. The name of the branch appears on its face where it is drawn on

It should not be stale or post dated or without date

2. Amount in words and figures does not differ

3. Signature of the drawer appears on the face of instrument

4. Instruments is not mutilated

5. There should be no material alteration if so, it should be properly authenticated

6. If order instrument, suitably endorsed and last endorsee’s account being credited

7. Endorsement is in accordance with the crossings if any

8. The amount of the instrument is same as mentioned on the paying-in-slip and

counterfoil

9. The title of account on the paying-in-slip is that of payee or endorsee (with the

exception of bearer cheque).

If an instrument is in order then out bank’s special crossing stamp is affixed

across the face of the instrument. Clearing stamps is affixed on the face of the

70

University Of Sargodha

instruments, paying-in-slip and counterfoil (The stamp is affixed in such a manner

that half appears on paying-in-slip and half on counterfoil). The instrument is suitably

discharged, where a bearer cheque does not required any discharge and also an

instrument in favour of a bank need not be discharged. The instrument along with

paying-in-slip is retained while the counterfoil is given to the customer duly signed.

Then the following steps are to be taken:-

1. The particulars of the instruments and the and the pay-in-slip or credit

vouchers are entered in the Outward Clearing Register.

2. Serial number is given to each voucher

3. The register is balanced, the credit voucher are separated form the instrument

and are released to respective departments against instrument and are released

to respective departments against acknowledgement in the register

4. The schedules are arranged bank-wise

5. The schedules are prepared in triplicate, two copies of which are attached with

the relevant instrument and the third is kept as office copy

6. The house page is prepared from schedules in triplicate

7. The schedules and house pages are signed by the officer incharge with branch

stamp

8. The grand total of the house page is taken and agreed with that of the outward

clearing register

9. The instruments along with duplicate and house page are sent to the Main

Office

Inward Clearing Of The Branch

1. The particulars of the instruments are compared with the list

71

University Of Sargodha

2. The instruments are detached and sort out department wise

3. The entry is made in the Inward Clearing Register (serial number, instrument

number, account number, amount of the instrument is written).

4. The instruments are sent to the respective departments against acknowledgement

in the Inward Clearing Register.

5. The instruments are scrutinized in each respect before honoring the same.

FOREIGN EXCHANGE DEPARTMENT

Foreign Exchange Department works like the general bank departments with the

difference that it deals in foreign currency. This department deals with the following:-

Import

Export

Foreign Currency Accounts

Foreign Remittance

Submission of Monthly Reports to SBP

IMPORT

72

University Of Sargodha

The international trade transaction, in which one country buys goods from other

country, is called import.

The import trade in Pakistan is governed by import and export Act of 1950.

Previously, the regulating body of imports was controller of Import and Export. But this

function has been shifted to Export Promotion Bureau.

Foreign Exchange Departments of all banks are restricted to word under the rules

and regulations of government.

Import License and Registration:

The individuals and firms who desire to import goods from the foreign countries

are required to obtain import license. Import licenses are a type of artificial restraint on

the import trade of a country. To acquire import license, the importer has to submit

applications to the licensing authority. The importers can only get their merchandize

cleared from the custom authorities if they have the import license duly issued in their

names. The import licenses issued by the Import Trade Controller are required to be

registered with the State Bank of Pakistan.

Contract of sale:

After getting the license, the importer then negotiates with the exporter. When

they reach to an agreement on all terms of sale, they sign a contract. Thus contract

includes all information of terms and condition of sale.

Letter of credit:

Foreign trade payment problems are mainly solved by a letter of credit. A letter of

credit is issued by the importer’s bank. If guarantees payment to the exporter up to

specified amount of money provided the terms and conditions laid down the L/C are

fulfilled.

73

University Of Sargodha

A letter of credit is a commitment on the part of buyer’s bank to pay or accept

draft drawn upon it, provided drafts do not exceed a specified amount.

A letter of credit thus is a (I) written undertaking by an importer’s bank to

exporter’s bank. (II) That it will pay or accept draft drawn upon it up to a stated amount

with a specified time. (III) The payment will only be made to the exporter if he compliers

with the terms of credit.

Parties to a letter of credit:

There are four parties involved in letter of credit.

1. Account party: The buyer or the importer on whose account and request the

letter of credit is opened is known as account party or opener.

2. Issuing bank: The bank which issues or opens a letter of credit at the request of

importer is called issuing bank.

3. Exporter or seller: The seller or the party in whose favor L/C is drawn is the

exporter. He is also called beneficiary.

4. Negotiating bank: The paying bank in the exporter’s country, on which the draft

is drawn, is called negotiating bank or paying bank.

Opening of letter of credit:

The main steps involved in the opening of the letter of creditor as follows:

Application for letter of credit:

The importer will request his own bank or any other bank, which deals in foreign

trade transactions to issue a letter of credit in favor of the exporter. He will prepare an

application on the prescribed form available from the bank. The information, which are

supplied in the application are based on the contract of sale and include only the

important feature of contract, such as value of merchandise, port of shipment, documents

to be presented, port of unloading, brief description of goods, import license etc.

74

University Of Sargodha

Scrutiny of application:

Before issuing a letter of credit, the bank will scrutinize whether the importer is of

good financial standing, possesses the import license issued by import control.

Authorities, the amount available covers the letter of credit applied for, market demand of

goods, collateral offered to cover the credit etc.

Cash margin:

The bank asks the importer to deposit cash or securities with the bank. The proper

margin of cash or securities to be deposited is decided by the bank depending upon the

credit worthiness of the importer.

Issue of the letter of credit:

The importer bank after being fully satisfied will issue a letter of credit in favor of

the exporter. The L/C may be sent directly to the exporter or the advising bank in the

exporter’s county. In such a case, the advising bank will inform the exporter about

opening a letter of credit.

Shipment of goods:

When the exporter receives L/C, he examines it to ensure that it conforms to the

terms of contract of sales. He then shifts the goods and presents all required documents

along with the bill to negotiating bank.

Role of negotiating bank:

The negotiating bank after receiving all the documents and the bill from the

exporter will scrutinize them whether these conform with the terms of letter of credit. If

75

University Of Sargodha

the documents of title accompanying the bill are in order, these will be sent to the

importers bank for payment.

Liability of the issuing bank:

On receipt of documents and the bill, the issuing bank will examine them. If the

documents on the face appear to be in order, the payment would be released by the bank.

In case any defect is found in the documents and the draft is honored by the issuing bank

the importer can claim damages on the issuing bank. The issuing bank is only

accountable for the completeness of documents, not to see whether goods conform to the

contract of sale.

Payment by importer to the bank:

First the importer pays all his obligations the bank then bank releases the

documents. In case of sight draft, the importer’s bank pays the amount on the same day

charging the importing customer’s account. In case of a time draft, the importer

discharges his obligations to the accepting bank on or before the maturity date of

acceptance. The accepting bank will then release all the shipping documents to the

importer.

Payment to the exporter:

The exporter can obtain payment from the negotiating bank by discounting the

draft (L/C) immediately after shipping the goods and obtaining shipping documents.

EXPORT

76

University Of Sargodha

The international trade transaction in which one country sells its goods to other

country is called Export.

The controlling body of export in Pakistan is Export Promotion Bureau, it gives

different incentives to the businessmen for enhancing the exports and reducing the

Balance of payment deficit. It restricts the export of some goods and reinforces export of

other.

The steps involved in import are described earlier from the importer’s point of

view. The procedure of export is same, as it can be described from exporters point of

view. The activities, which are different, described here.

Foreign bill purchased (FBP):

Following requirements must be fulfilled before the purchase of Foreign Export

Bills.

Exporter should be account holder of the bank. Bank issues the Form-E. Form-E

should be filled correctly and then bank authenticates the E-Form. Exporter goes to the

custom authorities for custom clearance. Shipping Company issues Bill of Lading or

Airway Bill. Exporter should bring other documents like certificates of Origin,

commercial invoice, packing list etc. Bank scrutinizes the documents.

After fulfilling these requirements, bank purchases the export bill and makes

payment for the value of goods in Pak Rupee to the Exporter.

Lodgment:

Lodgment means making the payment to exporter by bank against the purchase of

bill. Two types of rates are used in evaluating the amount:

1. OD Buying rate/At sight rate:

It is the rate of export bill, payment of which is to be received within 12 days

from the date of lodgment.

77

University Of Sargodha