International Technology Transfer Case Study Dec. 15 2008.

22

International Technology Transfer Case Study Dec. 15 2008

-

Upload

noah-singleton -

Category

Documents

-

view

213 -

download

0

Transcript of International Technology Transfer Case Study Dec. 15 2008.

International Technology Transfer Case Study

Dec. 15 2008

Definition and Channels• International technology transfer (ITT) is a comprehensive term covering

mechanisms for shifting information across borders and its effective diffusion into recipient economies.

• it refers to numerous complex processes, ranging from innovation and international marketing of technology to its absorption and imitation. Included in these processes are technology, trade, and investment policies that can affect the terms of access to knowledge.

• Channels– One major channel is trade in goods, especially capital goods and

technological inputs.– A second is foreign direct investment (FDI)– A third is technology licensing– non-market channels of ITT: the process of imitation through product

inspection, reverse engineering– temporary migration of students, scientists, and managerial and technical

personnel

Policies impacting ITT• Host country policies

– Absorption of ITT and its translation into greater competition depend on having an adequate supply of engineering and management skills.

– Backward spillovers from ITT appear to be strongest in countries where multinational firms are capable of working with competitive suppliers in order to increase their productivity and standards. Reducing entry barriers in supplier industries can assist ITT.

– Important factors include, among others, an effective infrastructure, transparency and stability in government, and a reasonably open trade and investment regime.

– Governments may reduce the "technological distance" between their firms and foreign firms in order to encourage ITT.

– attention should be paid to selecting IP standards that recognize the rights of inventors but encourage dynamic competition.

Policies (cont)• Source country policies

– Governments in developed countries could increase their technical and financial assistance for improving the ability of poor countries to absorb technology and trade.

– Governments could agree to offer identical fiscal benefits to firms transferring technologies to developing countries as to developing home regions.

– Developed countries could offer the same tax advantages for R&D performed abroad as for R&D done at home.

– Governments could ensure that tax deductions are available for contributions of technology to non-profit entities engaged in ITT.

– Fiscal incentives could be offered to encourage enterprises to employ, at least– temporarily, recent scientific and engineering and management graduates

from developing countries. – Universities could be encouraged to recruit and train students from LDCs in

science, technology, and management.

Case: Auto Industry in Chinese Economy

• 1.6 million Chinese were directly employed by this industry as of 2003 (not counting the employees of industries that supply the auto industry (i.e. steel, rubber), which are estimated at approximately 36.4 million workers). Auto industry is 3 percent of total manufacturing employment.

• The value added by the Chinese auto industry represented 6.3% of the total value added of manufacturing in China in 2003, a tripling of this percentage from its level in 1990 (CATARC 2004).

History of Chinese Auto Industry• Little to no manufacturing experience prior to WWII• Tech transfer from Soviets before Sino-Soviet split in 1960• After Cultural Revolution, no technological capabilities in this sector• Decision to “make or buy” – forced to buy because of weak technological

capabilities• Formation of many joint ventures with foreign firms and licensing of

technology from them as well, but without formal industrial policy• 1994 Auto Industry Policy – intention to create national industry• Consolidation of industry, but currently 118 manufacturers; all the major

ones have formed joint ventures with foreign auto companies• Joining WTO in 2001 effectively reversed many previous policies, but

increased competition• 2004 Auto Industry Policy – auto industry as “pillar” industry; create better

technological capabilities and consolidate industry

Chinese Automakers• Currently 116 automakers in China• Vast majority of output comes from the firms that

have formed joint ventures with foreign companies (quasi-exceptions are Chery and Geely)

• High profitability• Skills in manufacturing, parts and components, and

business development• Weak design and innovation capabilities, especially

for advanced engines and system integration

Terms of WTO for Chinese Auto Industry• Import tariffs for complete vehicles are to be reduced from the current 80

to 100 percent to 25 percent by July 1, 2006 • Import tariffs for parts and components are to be reduced from 35 percent

to 10 percent by the same date • Import quotas on vehicles will be decreased 15 percent per year until they

are cancelled in 2005 • Import licenses will also be phased out by 2005. • Majority ownership limits on foreign manufacturers for engines will also be

eliminated • Also, provincial governments will be given the authority to approve foreign

direct investment projects up to $150 million by 2005 (used to be $30 million)

• All of the Chinese government’s requirements regarding technology transfer, maintaining a foreign exchange balance, maintaining a trade balance, and meeting localization standards were eliminated upon China’s entry to the WTO in 2001.

2004 Auto Industry Policy

• 10-year update to 1994 policy• Emphasizes need for consolidation of industry

(i.e. FAW-Tianjin-Toyota)• Urges more capacity-building and innovation• First articulation of concern about environment

and oil imports• More emphasis on (and incentives for) exports

11th 5-Year Plan for Auto Industry

• 依托现有基础加快产业自主发展。– Speed up autonomous development based on the

current conditions (Chinese branding)• 依靠技术进步推动产业可持续发展。

– Promote sustainable development by using advanced technologies

• 利用市场机制促进产业结构优化升级。– Optimize and upgrade the industrial structure

using market mechanisms

Background Data

Comparisons

United States China

Total Oil Consumption, 2005

20 million bbls/day 6.5 million bbls/day

Percent Oil Consumed by Motor Vehicles

50 percent 40 percent

Percent Oil Imported, 2005

60 percent (12 million bbls/day)

43 percent (3 million bbls/day)

Total Number of Passenger Cars

228 million (approx.) 20 million (approx.)

Passenger Car Production in China (1991-2005)Data Sources: CATARC, 2005 Auto Industry of China; China Auto (Jan. 2006)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Production Mix is Changing

64 59 60 5850 47 42 41 41 36 34 34 28 30 27

2526 23 23

2827

28 28 28 34 36 33

27 2422

11 15 18 19 22 27 31 31 31 29 30 3446 46 51

0%

20%

40%

60%

80%

100%

1991 1993 1995 1997 1999 2001 2003 2005truck bus car

Source: CATARC, 2006

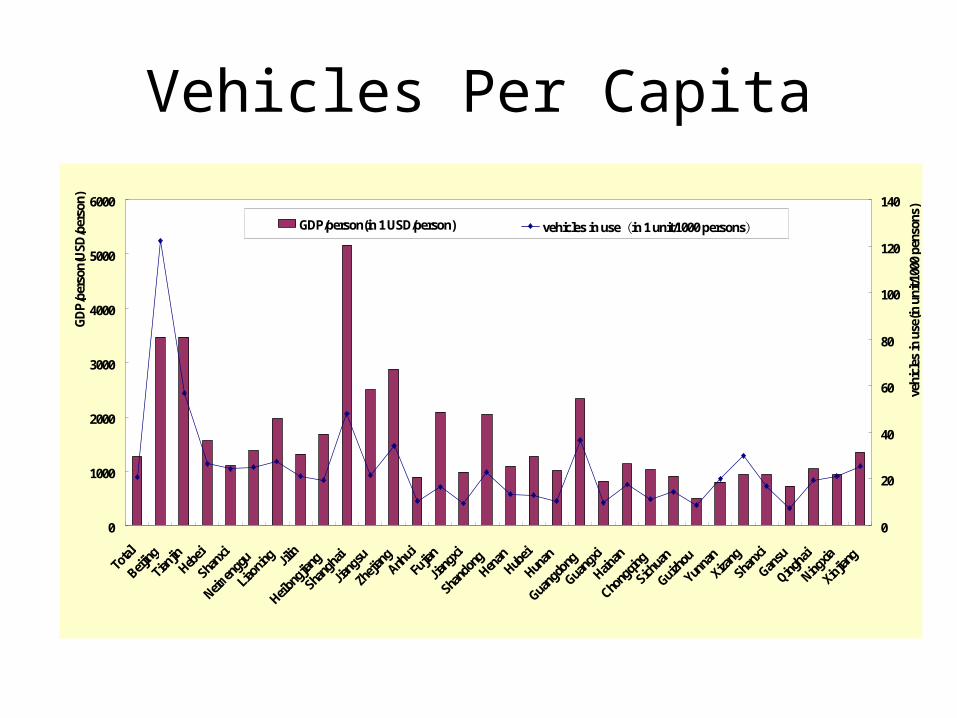

Vehicles Per Capita

0

1000

2000

3000

4000

5000

6000

Total

Beijing

Tianji

nHeb

ei

Shan

xi

Neimen

ggu

Liaon

ing Jilin

Heilon

gjian

g

Shan

ghai

Jiang

su

Zheji

angAnh

ui

Fujia

n

Jiang

xi

Shan

dong

Henan

Hubei

Hunan

Guang

dong

Guang

xi

Hainan

Chong

qing

Sichu

an

Guizho

u

Yunn

an

Xizan

g

Shan

xi

Gansu

Qingha

i

Ningxia

Xinjia

ng

GD

P/p

erso

n(U

SD

/per

son)

0

20

40

60

80

100

120

140

vehi

cles

in u

se(in

uni

t/100

0 pe

nson

s)

GDP/person(in 1 USD/person) vehicles in use(in 1 unit/1000 persons)

EIA Projections of Motor Vehicles in China 1999-2020

Data: EIA, "International Gross Domestic Product, Population, and General Conversion Factors Information," 2002 and EIA, "International Total Primary Energy and Related Information," 2002.

0

10

20

30

40

50

60

70

80

1990 1998 1999 2005 2010 2015 2020

Nu

mb

er

of

Ve

hic

les (

mill

ion

s)

Historical

Chinese Oil Reserves, 2003

21%

2%

77%Rest of WorldChinaOPEC

BP Statistical Review of World Energy, 2004

The Sino-U.S. Joint Ventures

Shanghai Auto Industry Corp.

First Auto Works

Tianjin Auto Works

Guangzhou Auto Works

Dongfeng Auto Works (former

SAW)

Beijing Auto Industry

Holding Co.

General Motors

VW

Toyota

DaimlerChrysler Hyundai

Nissan

Honda

Geely

CheryChang’An

Ford

Citroen

Suzuki

Foreign Investment in China’s Auto Industry: A Complicated Network

?

Shenyang Brilliance

BMW

Kia

Comparative Analysis

Beijing Jeep Shanghai GM Chang’An Ford

Technology or R&D Center?

Internal, but no joint work (all Chinese engineers)

Yes (PATAC) Internal, but very small for product adaptation

Capability level of Chinese partner accord. to US firm

product adaptation, localization

product adaptation, localization

Too new to characterize

U.S. firm funds other research in Chinese univ. or institutes?

No Yes Yes – In coordination with National Science Foundation of China

Number of Chinese vs. U.S. engineers

200 Chinese

1 U.S.

400 Chinese

>20 U.S.

n/a

Management of Tech Centers

1 Chinese,

1 U.S.

7 of 11 dept’s managed by U.S. engineers

n/a

Funding 30,000 RMB per year ($3,600)

For PATAC, GM put $25 million in cash and SAIC put $22 million (“in kind”)

n/a

Seven Main Findings• U.S. FDI did not substantially contribute to improving

Chinese vehicle technological capabilities because little knowledge was transferred along with the product.

• Chinese government failed to design and implement an aggressive, consistent strategy for the acquisition of technological capabilities from foreigners in the automobile industry.

• U.S. companies in JV’s are purely profit-motivated – Chinese also seek profits in short term, but most want skills for long term.

Findings (cont.)• Chinese firms have acquired good manufacturing skills and

also acquired some product adaptation capabilities. Parts suppliers appear to have more advanced capabilities due to local content requirements.

• Technologies that were transferred by U.S. firms in the period studied were rarely, if ever, updated once a model was in production, with the emerging exception of SGM. This is now changing due to competitiveness.

• Even though technology transfer was purely product, the FDI has contributed to the growth of the industry, which has benefited the Chinese economy in terms of jobs and spillovers.

• U.S. firms did not transfer pollution-control technology until required to do so by the Chinese government.