International Corporate Finance (ICF)

34

International International Corporate Finance Corporate Finance (ICF) (ICF) Jim Cook Cook-Hauptman Associates, Inc. (USA)

-

Upload

cooper-kirk -

Category

Documents

-

view

21 -

download

0

description

International Corporate Finance (ICF). Jim Cook Cook-Hauptman Associates, Inc. (USA). Agenda. Thursday – ( Sessions am: 8:30-12:00, pm: 1:30-5:00 ) am: Structures, Statements, Value, Analysis, Currency pm: Time & Currency Discounting/Trading of Money - PowerPoint PPT Presentation

Transcript of International Corporate Finance (ICF)

InternationalInternationalCorporate Finance (ICF)Corporate Finance (ICF)

Jim Cook

Cook-Hauptman Associates, Inc. (USA)

Day 2 in the pm # 2 / 34International Corporate Finance

AgendaAgenda Thursday – (Sessions am: 8:30-12:00, pm: 1:30-5:00)

am: Structures, Statements, Value, Analysis, Currency pm: Time & Currency Discounting/Trading of Money

Friday – (Sessions am: 8:30-12:00, pm: 1:30-5:00) am: Workshop on Evaluating Financials. Discussion of the RMB pm: Internal Operations: Cash Management & Project Evaluation

Saturday – (Sessions am: 8:30-12:00, pm: 1:30-5:00) am: Workshop on Financial Projections and Raising Capital pm: External Operations: Markets’ instruments and practices

Sunday – (Sessions am: 8:30-12:00, pm: 1:30-5:00) am: Workshop on Mini-Cases: Process, Discrete, Software, eBay pm: Reviewing important points. Final Exam.

On the Internet at: http://cha4mot.com/ICF0411

Day 2 in the pm # 3 / 34International Corporate Finance

The Operating CycleThe Operating Cycle Operating cycle – time between purchasing the

inventory and collecting the cash

Inventory period – time required to purchase and sell the inventory

Accounts receivable period – time to collect on credit sales

Operating cycle = inventory period + accounts receivable period

Day 2 in the pm # 4 / 34International Corporate Finance

Cash CycleCash Cycle

Cash cycle time period for which we need to finance our inventory Difference between when we receive cash from the sale and

when we have to pay for the inventory

Accounts payable period – time between purchase of inventory and payment for the inventory

Cash cycle = Operating cycle – accounts payable period

Day 2 in the pm # 5 / 34International Corporate Finance

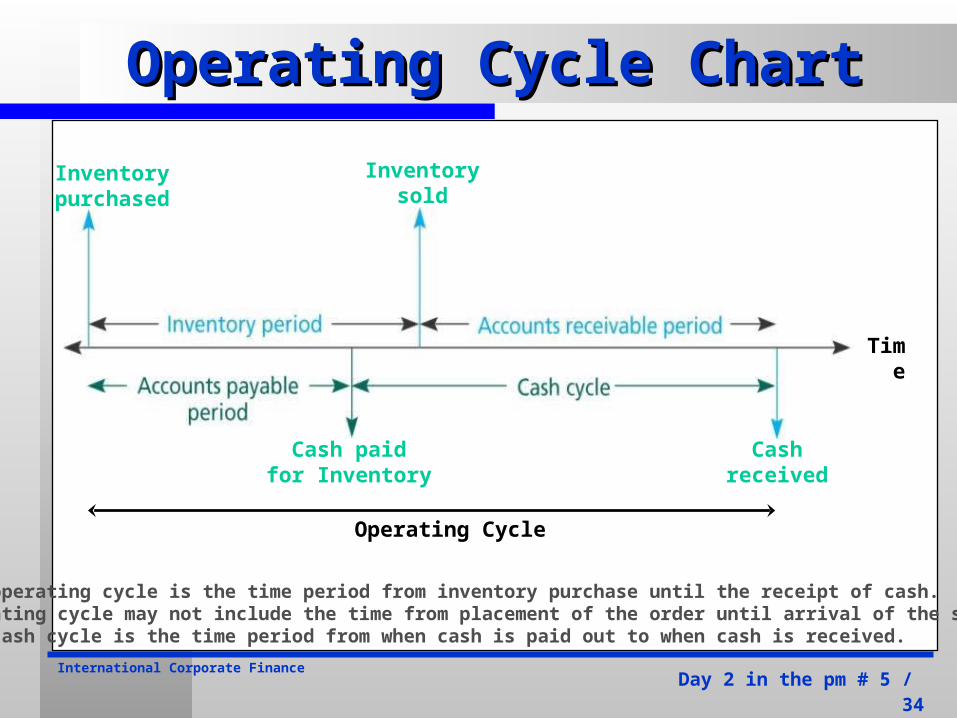

Operating Cycle ChartOperating Cycle Chart

Inventorypurchased

Inventorysold

Time

Cash paidfor Inventory

Cashreceived

Operating Cycle

The operating cycle is the time period from inventory purchase until the receipt of cash. (TheOperating cycle may not include the time from placement of the order until arrival of the stock.The cash cycle is the time period from when cash is paid out to when cash is received.

Day 2 in the pm # 6 / 34International Corporate Finance

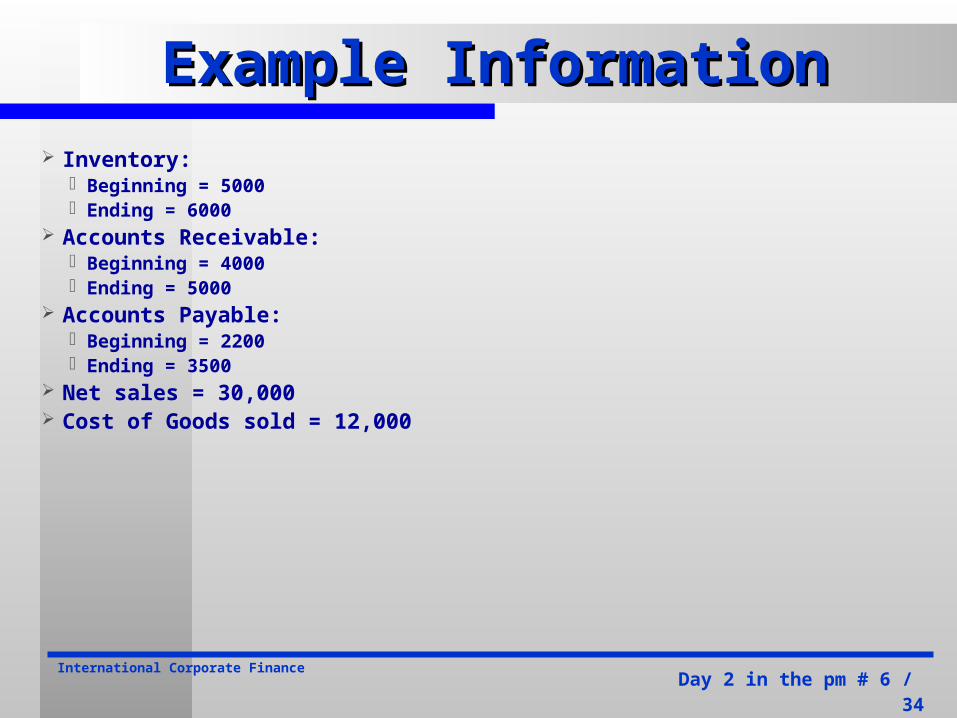

Example InformationExample Information Inventory:

Beginning = 5000 Ending = 6000

Accounts Receivable: Beginning = 4000 Ending = 5000

Accounts Payable: Beginning = 2200 Ending = 3500

Net sales = 30,000 Cost of Goods sold = 12,000

Day 2 in the pm # 7 / 34International Corporate Finance

Example – Operating CycleExample – Operating Cycle

Inventory period Average inventory = (5000 + 6000)/2 = 5500 Inventory turnover = 12,000 / 5500 = 2.18 times Inventory period = 365 / 2.18 = 167 days\

Receivables period Average receivables = (4000 + 5000)/2 = 4500 Receivables turnover = 30,000/4500 = 6.67 times Receivables period = 365 / 6.67 = 55 day

Operating cycle = 167 + 55 = 222 days

Day 2 in the pm # 8 / 34International Corporate Finance

Example – Cash CycleExample – Cash Cycle

Payables Period Average payables = (2200 + 3500)/2 = 2850 Payables turnover = 12,000/2850 = 4.21 Payables period = 365 / 4.21 = 87 days

Cash Cycle = 222 – 87 = 135 days

We have to finance our inventory for 135 days

We need to be looking more carefully at our receivables and our payables periods – they both seem extensive

Day 2 in the pm # 9 / 34International Corporate Finance

Credit Management: Key IssuesCredit Management: Key Issues

Granting credit increases sales

Costs of granting credit Chance that customers won’t pay Financing receivables

Credit management examines the trade-off between increased sales and the costs of granting credit

Day 2 in the pm # 10 / 34International Corporate Finance

Components of Credit PolicyComponents of Credit Policy

Terms of sale Credit period Cash discount and discount period Type of credit instrument

Credit analysis – distinguishing between “good” customers that will pay and “bad” customers that will default

Collection policy – effort expended on collecting on receivables

Day 2 in the pm # 11 / 34International Corporate Finance

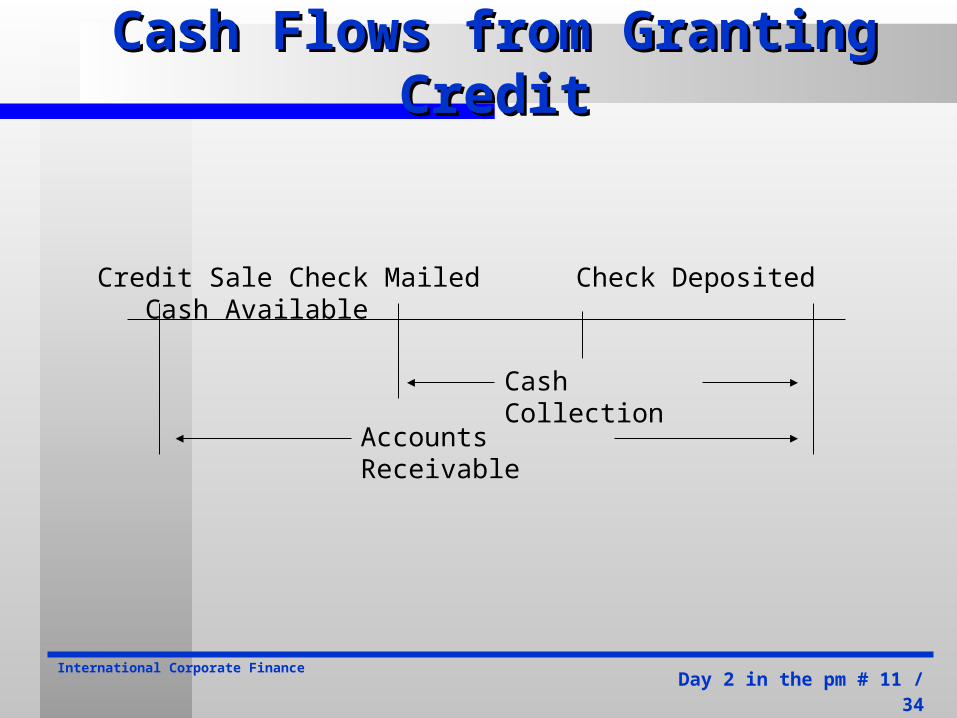

Cash Flows from Granting CreditCash Flows from Granting Credit

Credit Sale Check Mailed Check Deposited Cash Available

Cash Collection

Accounts Receivable

Day 2 in the pm # 12 / 34International Corporate Finance

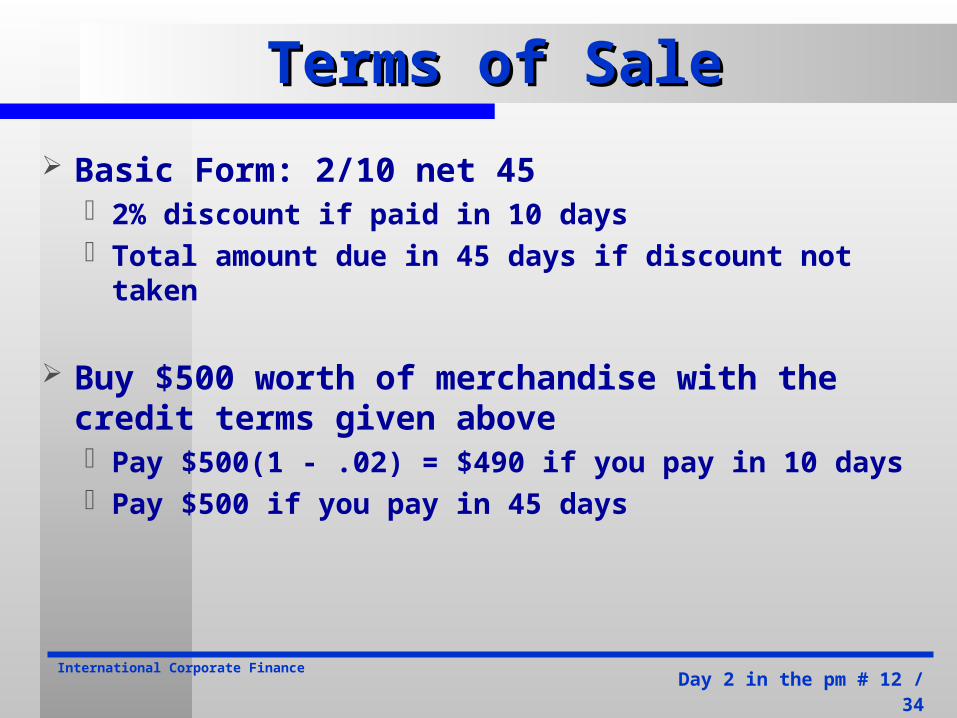

Terms of SaleTerms of Sale

Basic Form: 2/10 net 45 2% discount if paid in 10 days Total amount due in 45 days if discount not taken

Buy $500 worth of merchandise with the credit terms given above Pay $500(1 - .02) = $490 if you pay in 10 days Pay $500 if you pay in 45 days

Day 2 in the pm # 13 / 34International Corporate Finance

Example: Cash DiscountsExample: Cash Discounts

Finding the implied interest rate when customers do not take the discount

Credit terms of 2/10 net 45 and $500 loan $10 interest (.02*500) Period rate = 10 / 490 = 2.0408% Period = (45 – 10) = 35 days 365 / 35 = 10.4286 periods per year

EAR = (1.020408)10.4286 – 1 = 23.45%

The company benefits when customers choose to forego discounts

Day 2 in the pm # 14 / 34International Corporate Finance

Credit Policy EffectsCredit Policy Effects

Revenue Effects Delay in receiving cash from sale May be able to increase price May increase total sales

Cost Effects Cost of sale is still incurred even though the cash from the sale

has not been received Cost of debt – must finance receivables Probability of nonpayment – some percentage customers will

not pay for products purchased Cash discount – some customers will pay early and pay less

than the full sales price

Day 2 in the pm # 15 / 34International Corporate Finance

Short-Term Financial PolicyShort-Term Financial Policy

Size of investments in current assets Flexible policy – maintain a high ratio of current

assets to sales Restrictive policy – maintain a low ratio of current

assets to sales

Financing of current assets Flexible policy – less short-term debt and more

long-term debt Restrictive policy – more short-term debt and less

long-term debt

Day 2 in the pm # 16 / 34International Corporate Finance

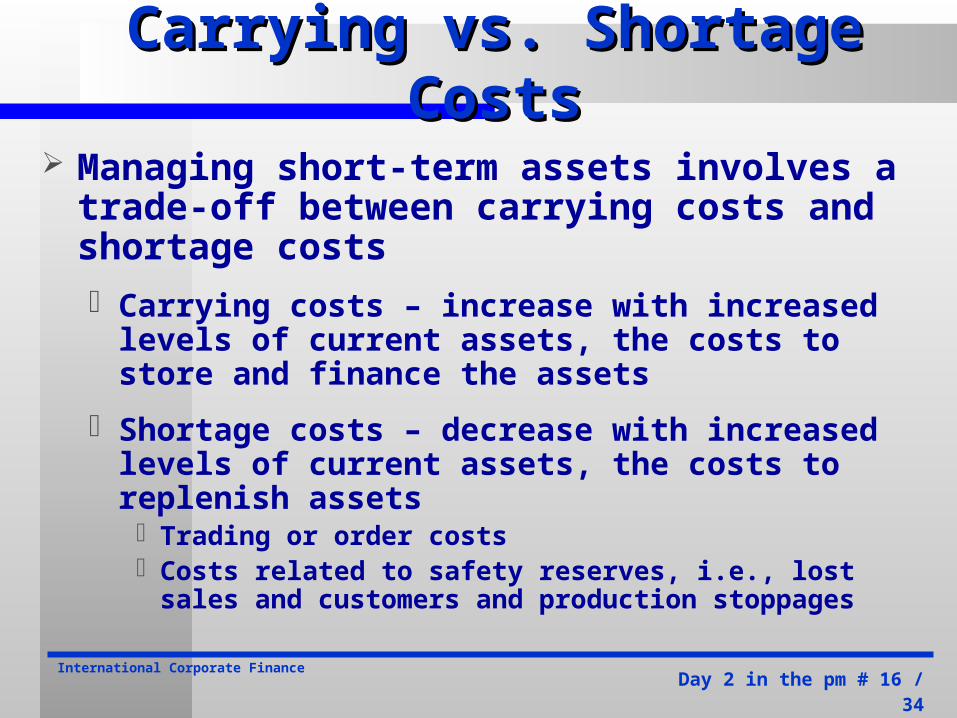

Carrying vs. Shortage CostsCarrying vs. Shortage Costs

Managing short-term assets involves a trade-off between carrying costs and shortage costs

Carrying costs – increase with increased levels of current assets, the costs to store and finance the assets

Shortage costs – decrease with increased levels of current assets, the costs to replenish assets Trading or order costs Costs related to safety reserves, i.e., lost sales and

customers and production stoppages

Day 2 in the pm # 17 / 34International Corporate Finance

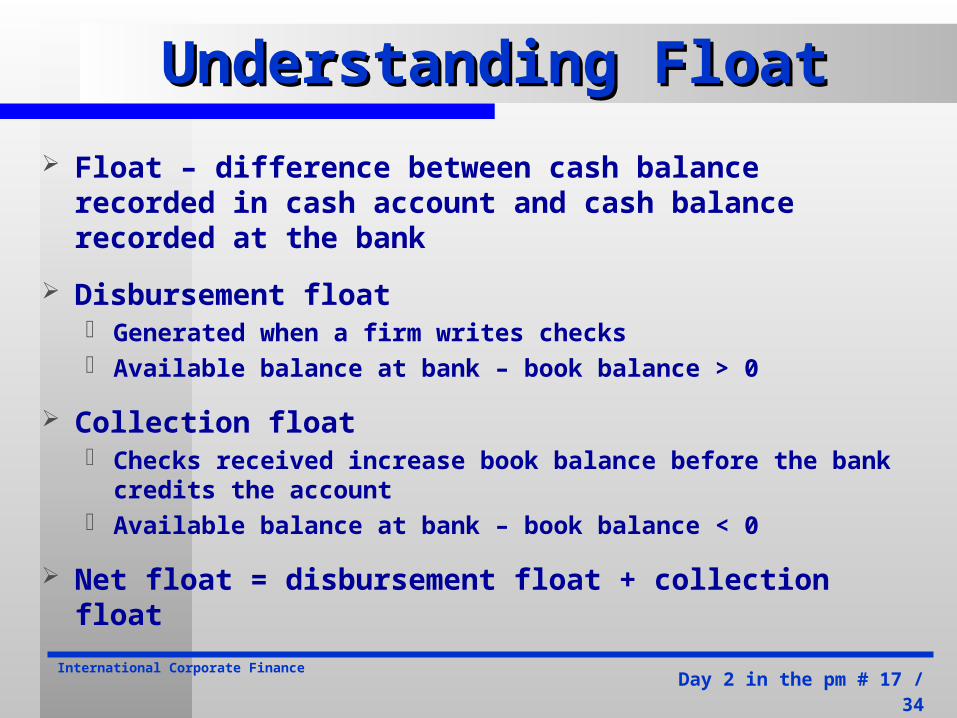

Understanding FloatUnderstanding Float

Float – difference between cash balance recorded in cash account and cash balance recorded at the bank

Disbursement float Generated when a firm writes checks Available balance at bank – book balance > 0

Collection float Checks received increase book balance before the bank

credits the account Available balance at bank – book balance < 0

Net float = disbursement float + collection float

Day 2 in the pm # 18 / 34International Corporate Finance

Example: Types of FloatExample: Types of Float

You have $3000 in your checking account. You just deposited $2000 and wrote a check for $2500. What is the disbursement float? What is the collection float? What is the net float? What is your book balance? What is your available balance?

Day 2 in the pm # 19 / 34International Corporate Finance

Example: Measuring FloatExample: Measuring Float

Size of float depends on the dollar amount and the time delay

Delay = mailing time + processing delay + availability delay

Suppose you mail a check for $1000 and it takes 3 days to reach its destination, 1 day to process and 1 day before the bank will make the cash available

What is the average daily float (assuming 30 day months)?

Method 1: (3+1+1)(1000)/30 = 166.67 Method 2: (5/30)(1000) + (25/30)(0) = 166.67

Day 2 in the pm # 20 / 34International Corporate Finance

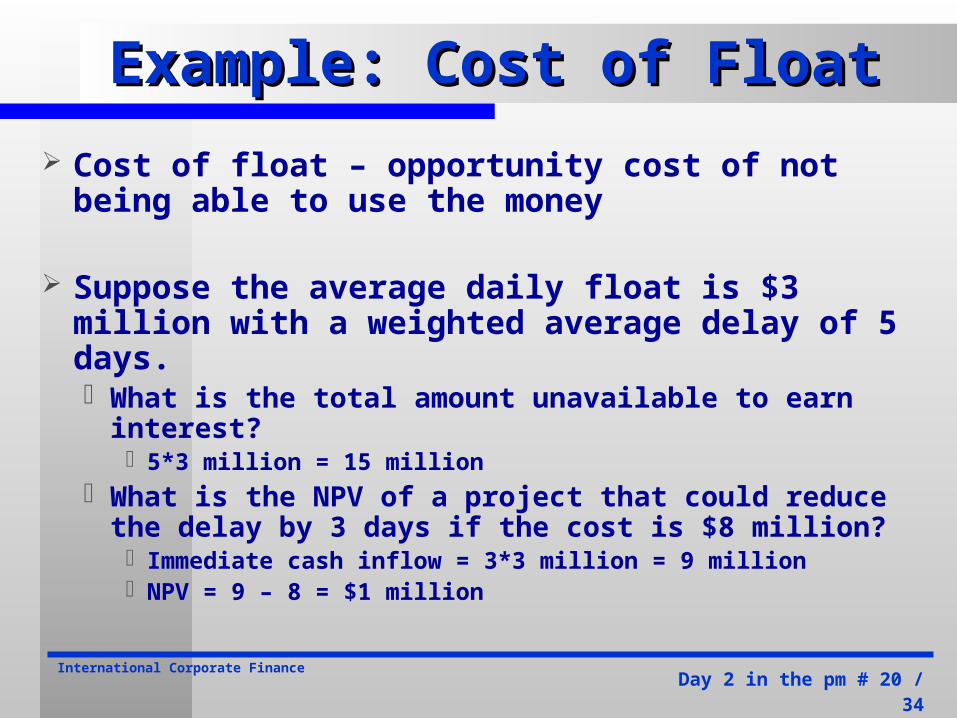

Example: Cost of FloatExample: Cost of Float

Cost of float – opportunity cost of not being able to use the money

Suppose the average daily float is $3 million with a weighted average delay of 5 days. What is the total amount unavailable to earn

interest? 5*3 million = 15 million

What is the NPV of a project that could reduce the delay by 3 days if the cost is $8 million? Immediate cash inflow = 3*3 million = 9 million NPV = 9 – 8 = $1 million

Day 2 in the pm # 21 / 34International Corporate Finance

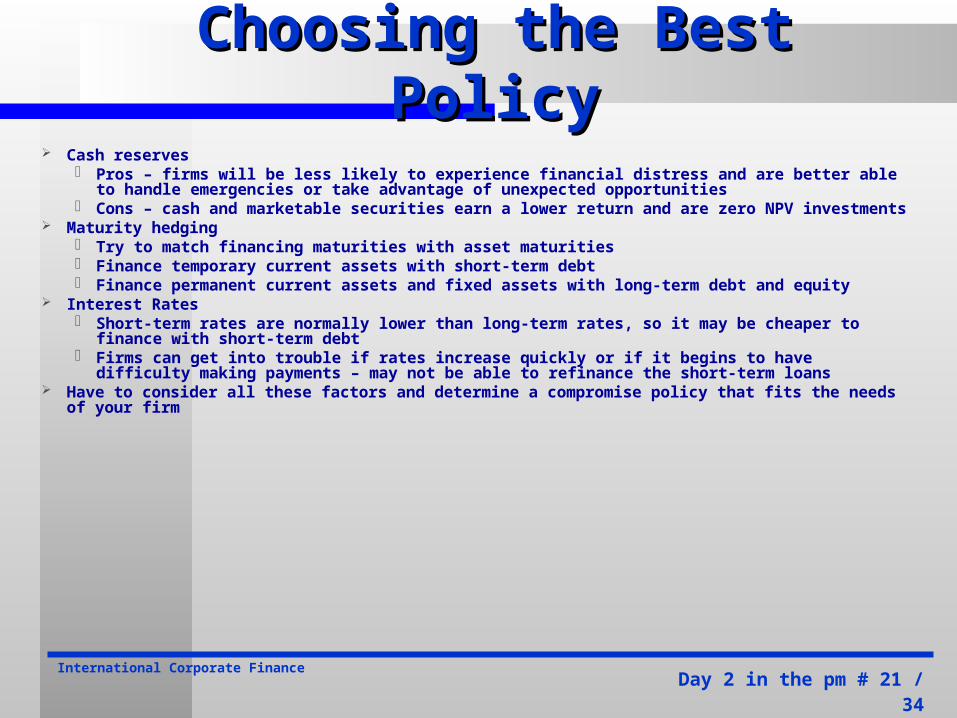

Choosing the Best PolicyChoosing the Best Policy Cash reserves

Pros – firms will be less likely to experience financial distress and are better able to handle emergencies or take advantage of unexpected opportunities

Cons – cash and marketable securities earn a lower return and are zero NPV investments Maturity hedging

Try to match financing maturities with asset maturities Finance temporary current assets with short-term debt Finance permanent current assets and fixed assets with long-term debt and equity

Interest Rates Short-term rates are normally lower than long-term rates, so it may be cheaper to finance with

short-term debt Firms can get into trouble if rates increase quickly or if it begins to have difficulty making

payments – may not be able to refinance the short-term loans Have to consider all these factors and determine a compromise policy that fits the needs of your firm

Day 2 in the pm # 22 / 34International Corporate Finance

Capital Budgeting FoundationsCapital Budgeting Foundations

For good selections, there must be good possibilities Have clear long term goals and specific direction Engage everyone to contribute ideas and improvements Research the emerging markets, competition, and technologies

For good outcomes, there must be clear structures Divide Capital Budgeting into Acquisitions and Projects Be sure that Buy versus Make is always considered Appoint a Process Master for Acquisitions and one for Projects Acquisitions may be centered in Purchasing or Finance, whereas Projects may be centered in Engineering or Manufacturing. Have an Investment Decision Council for integrating approvals

For Project Priortization, consider the Gartner Program (which follows immediately) as a starting reference

Day 2 in the pm # 23 / 34International Corporate Finance

Classification of ProjectsClassification of Projects

1. New products or expansion of existing products

2. Purchase or Renovation of equipment or buildings

3. Research and Development

4. Exploration

5. Other

6. Mandated key requirement: greater than one year!

Day 2 in the pm # 24 / 34International Corporate Finance

Prioritization Success FactorsPrioritization Success Factors

1. Establish governance and clear accountabilities

2. Allocate sufficient resources to support the process

3. Ensure the process is disciplined and sustained

4. Develop an objective prioritization framework

5. Support decision-making with tools

6. Maintain communication and education programs

Source: Getting Priorities Straight, Gartner Group, 2002.10

Day 2 in the pm # 25 / 34International Corporate Finance

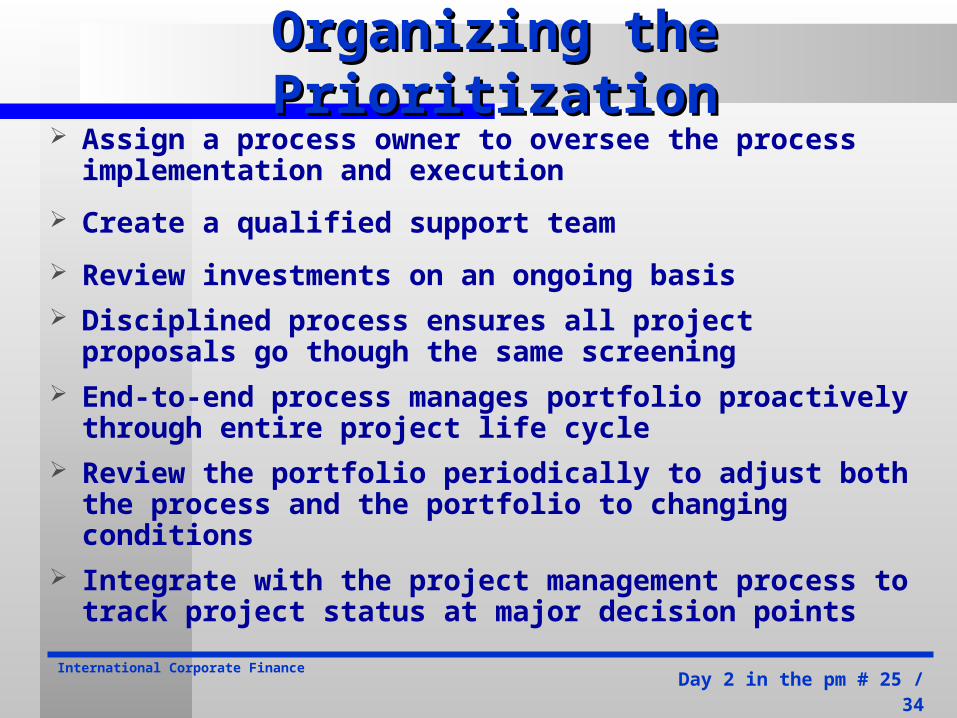

Organizing the PrioritizationOrganizing the Prioritization Assign a process owner to oversee the process

implementation and execution

Create a qualified support team

Review investments on an ongoing basis Disciplined process ensures all project proposals go

though the same screening End-to-end process manages portfolio proactively

through entire project life cycle Review the portfolio periodically to adjust both the

process and the portfolio to changing conditions Integrate with the project management process to

track project status at major decision points

Day 2 in the pm # 26 / 34International Corporate Finance

Project Portfolio ManagementProject Portfolio Management

Leading enterprises are adopting portfolio management techniques to gain benefits

Project portfolio management (PPM) is a 5-step process for prioritizing and managing initiatives

Process is not sequential, but has feedback loops

Manage portfolio

Match resources

Evaluate initiatives

Define initiatives

Prioritize &

balance

Day 2 in the pm # 27 / 34International Corporate Finance

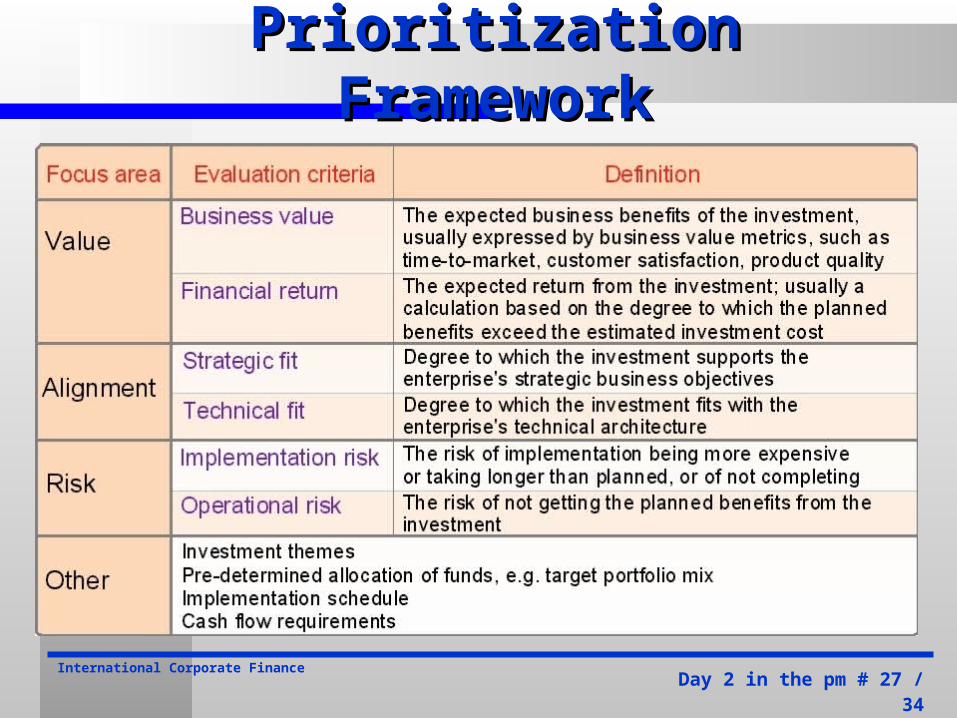

Prioritization FrameworkPrioritization Framework

Day 2 in the pm # 28 / 34International Corporate Finance

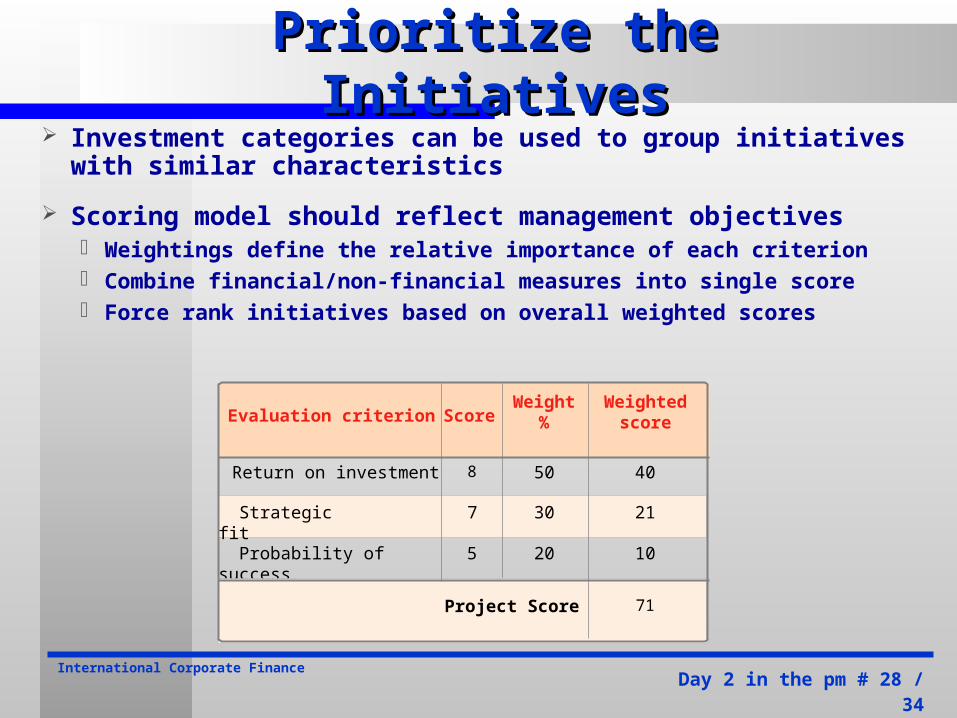

Prioritize the InitiativesPrioritize the Initiatives Investment categories can be used to group initiatives

with similar characteristics

Scoring model should reflect management objectives Weightings define the relative importance of each criterion Combine financial/non-financial measures into single score Force rank initiatives based on overall weighted scores

Probability of success

Return on investment 8 50 40

Strategic fit 7 30 21

5 20 10

Project Score 71

Evaluation criterion ScoreWeighted

scoreWeight

%

Day 2 in the pm # 29 / 34International Corporate Finance

Notes on the Scoring ModelNotes on the Scoring Model

1) Should closely match the Prioritization Framework2) No need for weightings to sum to 100, for example, a fantastic

flexibility capability should not lose out, nor should something of significant possibilities

3) Fatal items should be multiplied, not summed, for example, confidence (if near zero, don’t do it!)

4) Some visibility should be given to buy versus make5) ALL, projects are interdependent; they constitute the company!6) Maps can be a great help to justifying the right projects; maps of

technology, of capability, and of opportunity – often, in the real world, you must do three (or so) suboptimal projects to have a platform of substantial consequence.

7) Some provision should be made for learning from and improving the management processes

8) Ask often, what do I wish we had funded and why didn’t we?

Day 2 in the pm # 30 / 34International Corporate Finance

Financial AnalysisFinancial Analysis

But, how to do the Financial Analysis? Every Capital Budget Request must have a projected Cash

Flow of revenue recognition and direct costs (Finance can put in the overhead, taxes, but not interest or depreciation!)

The revenue recognition should be “signed off” by someone responsible for getting those revenues (or savings)

The resolution should be by month and should be CASH, not bookings, or even sales.

Key events and key contingencies should be highlighted

There must be a “champion” who will go as the project goes

Day 2 in the pm # 31 / 34International Corporate Finance

Incremental Cash FlowsIncremental Cash Flows

Initial cash outflow Initial cash outflow -- the initial net cash investment.

Interim incremental net cash flows Interim incremental net cash flows -- those net cash flows occurring after the initial cash investment but not including the final period’s cash flow.

Terminal-year incremental net cash flows Terminal-year incremental net cash flows -- the final period’s net cash flow.

Day 2 in the pm # 32 / 34International Corporate Finance

Cash Flow RulesCash Flow Rules

1) Include Cash, but not accounting income (don’t include depreciation, for example)

2) Operating flows, but not financing flows (no interest charges)

3) Include all other cash flows (that includes tax effects)

4) Just the incremental flows (attributable to project)

5) Include opportunity costs & side effects

6) Ignore sunk costs and allocated overhead costs (neither are incremental)

7) Include project-driven changes in working capital net of spontaneous changes in current liabilities

8) Include effects of inflation/deflation as can best be determined

Day 2 in the pm # 33 / 34International Corporate Finance

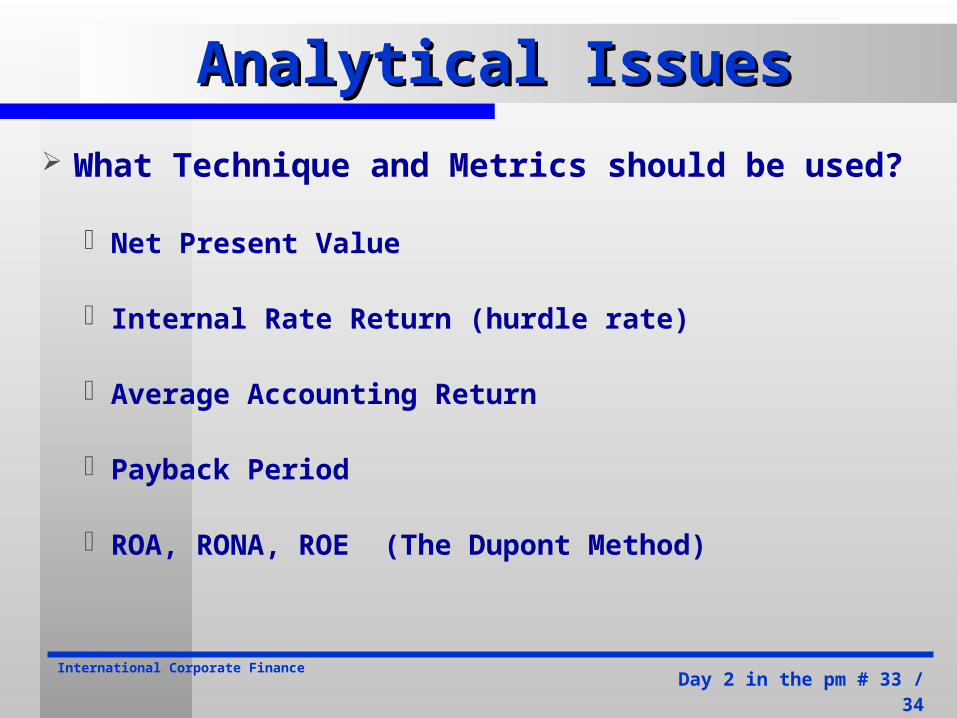

Analytical IssuesAnalytical Issues

What Technique and Metrics should be used?

Net Present Value

Internal Rate Return (hurdle rate)

Average Accounting Return

Payback Period

ROA, RONA, ROE (The Dupont Method)

Day 2 in the pm # 34 / 34International Corporate Finance

Concluding RemarksConcluding Remarks

Questions and Answers

Thank you, again.

You can find a copy of this lecture (450 KB) on the Internet at:

http://cha4mot.com/ICF0411