International Corporate Finance Atty. Jose Cochingyan...

60

International Corporate Finance Atty. Jose Cochingyan III Carlo Agdamag, A2015 1 INTERNATIONAL CORPORATE FINANCE Based on the Modules for Second Semester, AY 2013-2014 MODULE 1: THE WORLD AROUND US & THE CORPORATE ENTERPRISE 1. The Economic World Around Us 1.1. The Fiscal Climate and Development World Bank, World Development Report 2005: A Better Investment Climate for Everyone, Chapter 5: “Regulation and Taxation” The way governments regulate and tax firms and transactions play a big role in shaping the investment climate. o Sound regulation – addresses market failures that inhibit productive investment and reconciles the interest of firms with those of society o Sound taxation – generates the revenues to finance public services that improve the investment climate and meet other social goals o The challenge how to meet these objectives without undermining the opportunities an incentives for firms to invest productively REGULATING FIRMS Why regulate to restrict who may participate, where firms may locate, production process used, quality of products. Etc Regulatory problems o Partial enforcement evident in the huge informal sectors o Extraordinary requirements causes long delays o Creates monopolies and cartels o Imposes costs on consumers and stifles incentives for firms Studies show that developing countries tend to regulate more than richer countries. How then can govts make progress? o Strike a better balance between market failures and govt failures o Ensure good institutional fit Balancing market and gov’t failures & achieving good institutional fit Market failure – usual rationale for regulation. 3 most common types: o Externalities – arise when producing or consuming a product imposes costs (negative externatlities) or confers benefits (positive externalites) on others. Ex: pollution o Information Problems – arise when contracting parties have unequal access to information o Monopoly – arise when a firm has enough market power to raise prices above the competitive level and thereby extract higher profits at the expense of consumers and economic efficiency Government failure – Even market failure exists, it makes sense to intervene only when the expected benefits exceed the likely cost o Information and capacity problems – governments will never have as much information as firms about the impact of interventions on their costs or incentives o Rent-seeking – firms may seek regulation to protect themselves from competition. Officials accept bribes o Rigidity – regulation tends to be rigid, making it hard to keep up with changes in technology or way business is conducted The “institutional fit” challenge o Interventions that work well in one country may lead to very different results in others o Local conditions should be taken into account How to solve these? Addressing regulatory costs and informality o All regulations can impose costs on firms o A good investment climate does not seek to eliminate those costs o Instead, it seeks to ensure they are no higher than necessary to meet social interests. o Goal better regulation, not no regulation o Both investment and the productivity of the investment are lower in countries where he regulatory burden is greater o When compliance costs are the same for firms of different sizes, they impose a disproportionate burden on smaller firms o Informality – results when it is costly to comply with regulations By staying informal, firms can reduce costs Widespread in developing countries, accounting for more than half of GDP o Governments should streamline regulatory approval processes Online processing One-stop shops Reducing regulatory uncertainty and risk o Regulations can increase the risks firm face when they change frequently, vaguely drafted or enforced inconsistently

Transcript of International Corporate Finance Atty. Jose Cochingyan...

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 1

INTERNATIONAL CORPORATE FINANCE Based on the Modules for Second Semester, AY 2013-2014

MODULE 1: THE WORLD AROUND US & THE CORPORATE ENTERPRISE

1. The Economic World Around Us

1.1. The Fiscal Climate and Development

World Bank, World Development Report 2005: A

Better Investment Climate for Everyone, Chapter

5: “Regulation and Taxation”

The way governments regulate and tax firms and transactions play a big role in shaping the investment climate. o Sound regulation – addresses market failures that inhibit productive

investment and reconciles the interest of firms with those of society

o Sound taxation – generates the revenues to finance public services that improve the investment climate and meet other social goals

o The challenge how to meet these objectives without undermining

the opportunities an incentives for firms to invest productively REGULATING FIRMS

Why regulate to restrict who may participate, where firms may locate,

production process used, quality of products. Etc Regulatory problems

o Partial enforcement evident in the huge informal sectors o Extraordinary requirements causes long delays

o Creates monopolies and cartels o Imposes costs on consumers and stifles incentives for firms

Studies show that developing countries tend to regulate more than richer

countries. How then can govts make progress?

o Strike a better balance between market failures and govt failures o Ensure good institutional fit

Balancing market and gov’t failures & achieving good institutional fit

Market failure – usual rationale for regulation. 3 most common types: o Externalities – arise when producing or consuming a product

imposes costs (negative externatlities) or confers benefits (positive externalites) on others.

Ex: pollution

o Information Problems – arise when contracting parties have unequal access to information

o Monopoly – arise when a firm has enough market power to raise

prices above the competitive level and thereby extract higher profits at the expense of consumers and economic efficiency

Government failure – Even market failure exists, it makes sense to intervene only when the expected benefits exceed the likely cost

o Information and capacity problems – governments will never have as much information as firms about the impact of

interventions on their costs or incentives o Rent-seeking – firms may seek regulation to protect themselves

from competition. Officials accept bribes o Rigidity – regulation tends to be rigid, making it hard to keep up

with changes in technology or way business is conducted The “institutional fit” challenge

o Interventions that work well in one country may lead to very

different results in others o Local conditions should be taken into account

How to solve these?

Addressing regulatory costs and informality o All regulations can impose costs on firms o A good investment climate does not seek to eliminate those costs

o Instead, it seeks to ensure they are no higher than necessary to meet social interests.

o Goal better regulation, not no regulation

o Both investment and the productivity of the investment are lower in countries where he regulatory burden is greater

o When compliance costs are the same for firms of different sizes,

they impose a disproportionate burden on smaller firms o Informality – results when it is costly to comply with regulations

By staying informal, firms can reduce costs Widespread in developing countries, accounting for more

than half of GDP o Governments should streamline regulatory approval processes

Online processing One-stop shops

Reducing regulatory uncertainty and risk o Regulations can increase the risks firm face when they change

frequently, vaguely drafted or enforced inconsistently

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 2

o Managing regulatory risks Does not mean that regulations should never change

Instead, to minimize the adverse impact of uncertainty Firms should be consulted on proposed changes Transitions periods should also be provided

o Promoting certainty in the interpretation and application of existing regulations

Laws and regulations must be drafted with as much clarity and precision as possible

Timely publication of decisions precedents

Removing unjustified barriers to competition

o Competition creates opportunities for new firms and provides incentives for existing firms to innovate

o Regulation can create barriers to market entry or exit o Regulatory barriers to market entry

Requirements to set up new business Can open opportunities for individual entrepreneurs

o Regulatory barriers to market exit Ex: When bankruptcy regulations are long costly,

distressed firms are less willing to use them and the market becomes cluttered with failed firms

These block opportunities for new entrants

o Addressing competitive behavior by firms Firms can curb competition by colluding or forming cartels States should enact competition or antitrust laws Predatory pricing should be prevented Proposed mergers should be reviewed by an agency

TAXING FIRMS

Taxes represent a cost to firms and reduce their incentives to invest Taxation problems

o Benefit favored groups distorts competition o Tax administration burdensome

Increasing compliance costs

Reducing revenues Opening corruption

Taxes and the Investment Climate – taxes affect the incentives for firms to invest productively by weakening the link between effort and reward and by increasing the costs of inputs in the production process

o Tax rates A function of the size of government and the way the

burden is allocated among alternative sources Affected by the narrowness of the tax base and problems

of tax administration The tax burden of firms vary along several dimensions

The actual burden can differ from the statutory burden firms can pass them to consumers

Firms benefit from tax exemptions or privileges Firms that are in the informal economy (no tax)

o Tax administration Red tape and corruption in tax administration weaken the

incentive to comply with taxes and contribute to leakages o Taxes and competition

Taxes can affect the level of competition

Developing countries rely on trade taxes (tariffs) because of ease of collection, reducing pressure on local firms

Differential treatment of local firms in the same market How to improve taxation?

Broadening the tax base

o Reducing impediments to emergence of new firms o Addressing informality of existing firms o More vigorous tax enforcement action

Confronting informality o Caveat: forcing them to comply might result to them closing down o Even a big increase in formality may not lead to significant

increase in revenue, but would increase the cost of collecting

Simplifying tax structures o Tax systems riddled with exemptions are not transparent and can

act as magnets for rent-seeking behavior o Such system provides significant opportunities for corruption o Complicated systems increase costs of administration

Increasing the autonomy of tax agencies o Autonomy improves performance of revenue agencies

o Autonomy has to be balanced with accountability Tackling corruption in tax administration

o Minimize direct contact between tax officials and taxpayers, by automating and computerization procedures

o Organize the agency along functional lines rather than by tax type

Improving compliance through computerization

o Public satisfaction with tax service improves Regulating and taxing at the border

Regulatory barriers to foreign investments o Seeks to encourage FDI to promote spillover to local economy o Seeks to control foreign participation in ―sensitive‖ industries o Control the destabilizing effects of large, short-term capital flows

Regulatory barriers to foreign trade o Trade protection o Improving customs administration

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 3

Friedrich Schneider, Size and Measurement of the

Informal Economy in 110 Countries Around the

World (July 2002) Informal Economy

Definition all currently unregistered economic activities which

contribute to the official calculated Gross National Product o Smith: market-based production of goods and services, whether legal

or illegal that escapes detection in official GDP estimates o Includes unreported income from the production of legal goods and

services, either from monetary or barter transactions Principle of running water the informal economy adjusts to changes

in taxes, to sanctions from the tax authorities and to general moral attitudes, etc.

A large burden of taxation and social security contributions combined with government regulations are the main determinant of the size of the informal economy

Average size of informal economy as a percent of official GNI in 2000 o Developing countries 41%

o Transition countries 38% o OECD countries 18%

Indicators in the change of size of informal economy o Development of monetary indicators if activities in the informal

economy rise, additional monetary transactions are required o Development of the labor market increasing participation of

workers in the hidden sector results in a decrease in participation in the official economy. Similarly, increase activities in the hidden sector may be expected to be reflected in shorter working hours in the official economy

o Development of the production market an increase in the informal

economy means that inputs (especially labor) move out of the official economy (at least partly); this displacement might have a depressing effect on the official growth rate of the economy

Various methods used: the currency demand, the physical input measure, discrepancy method and the model approach

General impression: for all countries, the informal economy (labor force)

has reached a remarkably large size over the recent decade An increasing burden of taxation Informal economies are a complex phenomenon, present to an omportant

extent even in the industrialized and developed economies. People engage in informal in informal economic activity because of

government action, most notable taxation and regulation A government aiming to decrease informal economic activity has to

analyze the complex and frequently contradictory relationships among the

consequences of its own policy decisions

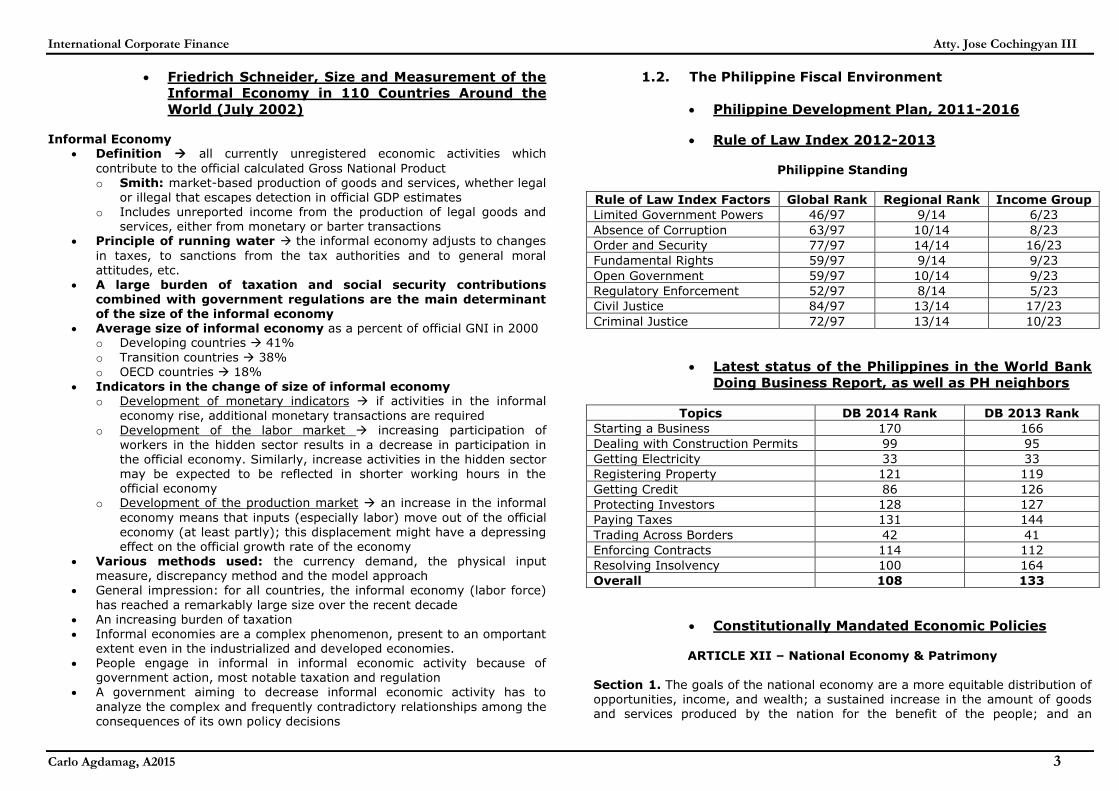

1.2. The Philippine Fiscal Environment

Philippine Development Plan, 2011-2016

Rule of Law Index 2012-2013

Philippine Standing

Rule of Law Index Factors Global Rank Regional Rank Income Group

Limited Government Powers 46/97 9/14 6/23

Absence of Corruption 63/97 10/14 8/23

Order and Security 77/97 14/14 16/23

Fundamental Rights 59/97 9/14 9/23

Open Government 59/97 10/14 9/23

Regulatory Enforcement 52/97 8/14 5/23

Civil Justice 84/97 13/14 17/23

Criminal Justice 72/97 13/14 10/23

Latest status of the Philippines in the World Bank

Doing Business Report, as well as PH neighbors

Topics DB 2014 Rank DB 2013 Rank

Starting a Business 170 166

Dealing with Construction Permits 99 95

Getting Electricity 33 33

Registering Property 121 119

Getting Credit 86 126

Protecting Investors 128 127

Paying Taxes 131 144

Trading Across Borders 42 41

Enforcing Contracts 114 112

Resolving Insolvency 100 164

Overall 108 133

Constitutionally Mandated Economic Policies

ARTICLE XII – National Economy & Patrimony Section 1. The goals of the national economy are a more equitable distribution of opportunities, income, and wealth; a sustained increase in the amount of goods and services produced by the nation for the benefit of the people; and an

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 4

expanding productivity as the key to raising the quality of life for all, especially the under- privileged.

The State shall promote industrialization and full employment based on sound agricultural development and agrarian reform, through industries that make full and efficient use of human and natural resources, and which are competitive in both domestic and foreign markets. However, the State shall protect Filipino enterprises against unfair foreign competition and trade practices. In the pursuit of these goals, all sectors of the economy and all regions of the

country shall be given optimum opportunity to develop. Private enterprises, including corporations, cooperatives, and similar collective organizations, shall be

encouraged to broaden the base of their ownership. Section 6. The use of property bears a social function, and all economic agents shall contribute to the common good. Individuals and private groups, including corporations, cooperatives, and similar collective organizations, shall have the

right to own, establish, and operate economic enterprises, subject to the duty of the State to promote distributive justice and to intervene when the common good so demands. Section 12. The State shall promote the preferential use of Filipino labor, domestic materials and locally produced goods, and adopt measures that help

make them competitive. Section 16. The Congress shall not, except by general law, provide for the formation, organization, or regulation of private corporations. Government-owned or controlled corporations may be created or established by special charters in the interest of the common good and subject to the test of economic viability.

Section 19. The State shall regulate or prohibit monopolies when the public interest so requires. No combinations in restraint of trade or unfair competition shall be allowed.

Taxation Policy: RA No. 8424, §2 (1997) Section 2. State Policy. - It is hereby declared the policy of the State to promote sustainable economic growth through the rationalization of the Philippine internal revenue tax system, including tax administration; to provide, as much as possible, an equitable relief to a greater number of taxpayers in order to improve levels of disposable income and increase economic activity; and to create a robust environment for business to enable firms to compete better in the regional as well

as the global market, at the same time that the State ensures that Government is able to provide for the needs of those under its jurisdiction and care.

2. General Principles of Corporate Finance

2.1. Managerial Finance and the Business Organization

LAWRENCE J. GITMAN, PRINCIPLES OF MANAGERIAL

FINANCE, 10th Edition; Chapter 1, “The Role and

Environment of Managerial Finance,” pp. 2-39

(2003) Finance and Business

Finance – art and science of managing money

Major Areas and Opportunities in Finance o Financial Services – area of finance concerned with the design and

delivery of advice and financial products to individuals, businesses and governments

o Managerial Finance – concerns the duties of the financial manager

in the business firm Financial Manager – actively manages the financial affairs of

any type of business, whether financial or nonfinancial, private or public, large or small profit-seeking or not-for-profit

Legal Forms of Business Organization o Sole Proprietorship – a business owned by one person who

operates it for his own profit; has unlimited liability

Unlimited Liability – the condition of sole proprietorship (or general partnership) allowing the owner‘s total wealth to be taken to satisfy creditors

o Partnership – a business owned by two or more people and operated for profit; has unlimited liability for general partners

o Corporation – artificial being created by law Stockholders – owners of a corporation, whose ownership, or

equity, is evidenced by either common or preferred stock Common Stock – purest and most basic form of corporate

ownership

Dividends – periodic distributions of earnings to the stockholders of a firm

Board of Directors – group elected by the firm‘s stockholders

and having ultimate authority to guide corporate affairs and make general policy

President or CEO – corporate official responsible for managing the firm‘s day-to-day operations and carrying out the policies established by the board of directors

o Other Limited Liability Organizations Limited Partnership – a partnership in which one of the

partners have limited liability as long as at least one partner (the

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 5

general partner) has unlimited liability. The limited partners cannot take an active role in the firm‘s management; they are

passive investors S corporation – (only in US) Limited liability corporation – gives its owners limited liability

and taxation as a partnership. LLCs work well for corporate joint ventures or projects developed through a subsidiary

Limited liability partnership – all partners have limited liability. They are liable for their own acts of malpractice, not for

those of other partners. The LLP is taxed as a partnership.

The Managerial Finance Function Organization of the Finance Function

o Depends on the size of the firm o Treasurer – the firm‘s chief financial manager, who is responsible for

the firm‘s financial activities, such as financial planning and fund

raising, making capital expenditure decisions, and managing cash, credit, the pension fund an foreign exchange (finance)

o Controller – the firm‘s chief accountant, who is responsible for the firm‘s accounting activities, such as corporate accounting, tax management, financial accounting and cost accounting (accounting)

o Foreign Exchange Manager – responsible for monitoring and

managing the firm‘s exposure to loss from currency flcutuations Relationship to Economics

o Marginal Analysis – economic principle that states that financial decisions should be made and actions taken only when the added benefits exceed the added costs

Relationship to Accounting o Accrual Basis – in preparation of financial statements, recognizes

revenue at the time of the sale and recognizes expenses when they are incurred

o Cash Basis – recognizes revenues and expenses only with respect to actual inflows and outflows of cash

Primary Activities of the Financial Manager

o Involvement in financial analysis and planning o Making investment decisions

o Making financing decisions Goal of the Firm

Maximize Profit o Earnings per share – the amount earned during the period on behalf

of each outstanding share of stock, calculated by dividing the period‘s

total earnings available for the firm‘s common stockholders by the number of shares of common stock outstanding

o Timing – the receipt of funds sooner rather than later is preferred

o Cash Flows – only when earnings increases are accompanied by increased future cash flows would a higher stock price be expected

o Risk – the chance that actual outcomes may differ from those expected

o A trade-off exists between cash flows and risk. Maximize Shareholder Wealth

o Goal of the firm maximize the wealth of the owners o Wealth measured by the share price of the stock, which is based on

timing of returns (cash flows), magnitude and risk o Return and risk are in fact the key determinants of share price, which

represents the wealth of the owners in the firm

Stakeholders – groups such as employees, customers, suppliers, creditors, owners and others who have a direct economic link to the firm

Ethics – standards of conduct or moral judgment

The Agency Issue In theory, most financial managers would agree with the goal of owner

wealth maximization. In practice however natures are also concerned with their personal wealth, job security and fringe benefits.

The result is a less-than-maximum return and a potential loss of wealth for the owners.

Agency Problem – likelihood that managers may place personal goals

ahead of corporate goals How to prevent agency problems?

o Market forces – major shareholders – exert pressure on management to perform threat of takeover – takeover of another firm that believes it can

enhance the target firm‘s value

o Agency Costs – costs borne by stockholders to minimize agency problems and contribute to the maximization of owner‘s wealth Structure management compensation – give managers

incentives to act in the best interest of the corporation Incentive Plans – management compensation pans that

tend to tie compensation to share price; e.g. stock options

Performance Plans - plans that tie management

compensation to measures such as EPS and other rates in return, e.g., performance shares, cash bonuses

Financial Institutions and Markets

Financial Institutions – an intermediary the channels this savings of individuals, businesses and governments into loans or investments

Financial Markets – forums in which suppliers of funds and demanders of funds can transact business directly o Private Placement – the sale of new security issue, typically bonds

or preferred stock, directly to an investor or group of investors

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 6

o Public Offering – the nonexclusive sale of either bonds or stock to the general public

o Primary Market – financial market in which securities are initially issued, the only market in which the issuer is directly involved in the transaction

o Secondary Market – financial market in which pre-owned securities (those that are not new issues) are traded

Money Market - a financial relationship created between suppliers and demanders of short-term funds

o Marketable securities – short-term debt instruments, such as US Treasury bills, commercial paper, and negotiable certificates of

deposit issued by government, business and financial institutions, respectively.

Capital Market – a market that enables suppliers and demanders of long-term funds to make transactions. E.g., bonds and stocks o Bond - long-term debt instrument used by business and government

to raise large sums of money, generally from a diverse group of lenders

o Preferred Stock – special form of ownership having a fixed periodic dividend that must be paid prior to payment of any common stock dividend

o Securities Exchanges – organizations that provide the marketplace

in which firms can raise funds through the sale of new securities and purchasers can resell securities

o Over-the-counter Exchange – an intangible market for the purchase and sale of securities not listed by the organized exchanges

o Efficient market – a market that allocates funds to their most productive uses as a result of competition among wealth-maximizing investors that determines and publicizes prices that are believed to be

close to their true value Business Taxes

Ordinary income – income earned through the sale of a firm‘s goods or services

Double taxation – occurs when the already once-taxed earnings of a corporation are distributed as cash dividends to stockholders, who must

pay taxes on them Intercorporate dividends – dividends received by one corporation on

common and preferred stock held in other corporations Capital Gain – the amount by which the sale price of an asset exceeds

the asset‘s initial purchase price Tax loss carryback/carryforward – a tax benefit that allows

corporations experiencing operating losses to carry tax losses o In PH, this is called the NOLCO

DIANE BEAL AND MICHELE GOYEN, INTRODUCING

CORPORATE FINANCE – “Introducing the Firm and Its

Goals,” pp. 3-30 (2005) Goals of Firms

Profit maximization – implies a business is managed to maximize the difference between revenues and expenses any period.

Wealth maximization – implies that the business is managed so that the present and future cash flows discounted at an appropriate value will get a present value which is maximized

Time value of money – is the concept that a dollar is worth more the

sooner it is received Discounting – is the process of calculating the present value of the

future amount. The discount factor incorporates the possible or required earning rate for the funds

Market capitalization – is the total value of the corporation as measured be the price of each issued share multiplied by the number of issued shares

Market value – is the price that the willing buyers are prepared to pay and willing sellers are prepared to accept

Roles of Financial Managers

Financial Derivatives – contracts that are derived from the value of some underlying assets and are used to manage risk

Financial Governance and financial decisions

Financial Governance – comprises all the financial and management

accounting systems and other financial processes that are put in place to achieve the objectives of the firm

Principal-Agent Problem

Principal agent problem – the scope for conflict or division between principals (owners) and agents (managers) over the goals of the firm

which are being pursued by its policy and management decisions Agency Costs – are the losses borne by the owners of the firm that can

be attributed to the agent having different objectives from the owners or principals

Ethics in Business

Ethics – are moral principles or rules of conduct which indicate the

acceptability of behavior within the community Whistleblowing – means informing (usually the employees of the

perpetrators) the relevant authorities of malpractice or dangers to the public or the environment

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 7

Corporate Social Responsibility - means that the firm has wider responsibilities in relation to objectives and people apart from the owners

or shareholders Corporate Governance – means the management of corporations

Dividend Imputation

Dividend Imputation – the system where dividends carry an additional benefit in the form of an attached tax credit for the relevant amount of tax paid by the company on its profits

Franked dividend – dividend carrying an attached franking or tax credit Fully franked dividend – carries a tax credit equal to the full 30%

company tax paid on the underlying profit Partly franked dividend – carries a tax credit less than the full 30%

company tax paid on the underlying profit Unfranked dividend – carries no tax credit

PASCAL QUIRY, MARIZIO DALLACCHIO, YANN LE FUR AND

ANTONIO SALVI, CORPORATE FINANCE, THEORY AND

PRACTICE, pp. 1-11 (2005)

The Financial Manager Primary Role to ensure that his company has a sufficient supply of

capital o Traditional view A buyer of capital who seeks to minimize its cost o Financial view A seller of financial securities who tries to

maximize their value The cost of capital and the value of securities vary in opposite directions

minimizing financial cost is synonymous with maximizing the

value of the underlying securities Financial Instrument

Defined as a schedule of future cash flows Types of Financial Securities

o Debt Instruments – contract that ties a lender (investor) to a borrower (the company)

o Equity Securities – represents the capital injected into a company by an investor who bears the full risk of the company‘s industrial undertakings

o Other Securities – holds characteristics of the two above Secondary Markets

The market for ―used‖ financial products Function to ensure that securities are properly priced and traded Liquidity refers to the ability to convert an instrument into cash

quickly and without loss of value

2.2. Corporate Governance

JILL SOLOMON AND ARIS SOLOMON, CORPORATE

GOVERNANCE AND ACCOUNTABILITY, pp. 1-43 (2004) Corporate Governance

Definition – the system of checks and balances, both internal and

external to companies, which ensures the companies discharge their accountability to all their stakeholders and act in a socially responsible way in all areas of their business activity

Theoretical Frameworks Agency Theory – the problem that arises as a result of this system of

corporate ownership is that the agents do not necessarily make decisions in the best in interest of the principal o Managers prefer to pursue their own personal objectives o Ex: managers are likely to display a tendency towards egoism

resulting in a tendency to focus on project and company investments that provide high short-term profits rather dandy maximization of long-term shareholder wealth through investment in projects that are

long-term in nature o Short-termism – tendency to foreshorten the time horizon applied to

investment decisions or raise the discount date above that appropriate to the firms fortune at the cost of capital

o Residual Loss – reduction in shareholders‘ welfare o Expensive and difficult for principal to verify what the agent is doing o This presents shareholders with a need to control company

management Transaction Cost Theory – based on the fact that firms have become so

large that be, in effect, substitute for the market in determining the allocation of resources o It is in the interests of the company management to internalize

transactions as much as possible. The main reason for this is that

such internalization removes risks and uncertainties about future product prices and quality.

Stakeholder Theory - companies are so large, and their impact on society so pervasive that they should discharge an accountability to many more sectors of society then solely their shareholders o Stakeholders – include shareholders, employees, suppliers,

customers, creditors, communities in the vicinity of the company‘s

operations and the general public o Some also advocate that the environment, animals and future

generations be included in the term

Enron Case Study

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 8

MARTIN FAHY, JEREMY ROCHE AND ANASTASIA WEINER,

CHAPTER 10, BEYOND CORPORATE GOVERNANCE, pp. 225-

259 (2004) Key Influenced Behind the Corporate Responsibility Movement

Technology Transparency

Sustainability Globalization Borderless Governance Stakeholder Pressure

Mega-Risk

Benefits of Corporate Responsibility Improved Risk Management Ensuring Compliance Improved Financial Performance Institutional Investment Accountability Employee Attraction and Retention

Innovation

Ajit Singh, “The New International Financial

Architecture, Corp. Governance and Competition &

Emerging Markets: Empirical Anomalies & Policy

Issues” in HA-JOON CHANG, RETHINKING DEVELOPMENT

ECONOMICS, pp. 377-403 (2003) Corporate Governance in Developing Countries

Asian Financial Crisis a more credible explanation of the crisis is that

afflicted economies dismantled their controls over the borrowing of the private sector and embraced financial liberalization. o As a consequence, the private sector built up short-term foreign

currency debt, which often found its way into the non-tradable sector and into speculative real estate ventures

Crony Capitalism results in poor corporate governance

o In Asia, firms controlled by families are most likely to have a separation between cash flow and control rights, that its to say,a greater degree of corporate ‗pyramiding‘

o Concentration of economic power in a set of families is not necessarily antithetical to the efficient functioning, transparency and democratic

accountability of the industrial system o Crony Capitalism is not strictly a corporate governance problem, since

family owners are likely to have the right incentives in firms

o Crony capitalism is rather a product of the complex of relations between the business and political elites and could in principle arise in

systems with widely dispersed ownership. o Overall, the experience of Asian countries with family-controlled firms

and strong economic growth suggests that they are an effective vehicle of late development and industrialization.

DEAN CESAR VILLANUEVA, PHILIPPINE CORPORATE

GOVERNANCE pp. 1-46 (2011)

Significance of the term “Corporate Governance” Corporate feature of ―centralized management‖ under Sec. 23 of the

Corp. Code fiduciary relationship between the Board of Directors and

the stockholders Good corporate citizen corporations must behave in a socially-

acceptable way Board of Directors are vested with public interest, and therefore, have a

heightened set of duties and responsibilities to society

Covered Corporations under the Revised CG Code This Revised Code of Corporate Governance… shall apply to registered

corporations and to branches or subsidiaries of foreign corporations operating in the Philippines that:

a. Sell equity and/or debt securities to the public that are required to be registered to the Commission

b. Have assets in excess of Fifty Million Pesos and at least two hundred (200) stockholders who own at least one hundred (100) shares each of equity securities

c. Whose securities are listed on the Exchange d. Grantees of secondary licenses from the Commission

Theories on Corporate Governance

Maximization of Shareholder Value o The primary obligation of the Board of Directors of a stock corporation

is to seek the maximum amount of profits for the corporation o Prevailing theory under the PH Corporation Code

Corporate Social Responsibility o The continuing commitment by business to behave ethically and

contribute to economic development while improving the quality of life

of the workforce and their families as well as the society at large Stakeholder Theory

o The obligation of business was not merely to seek profit for its stockholders but to coordinate stakeholder interests.

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 9

Trust Fund Doctrine The recognition of liability to other persons other than the stockholder or

members of the corporation has not been recognized or even operationalized, except in the application of the trust fund doctrine.

Under the trust fund doctrine, the capital stock, property and other assets of the corporation are regarded as equity in trust for the payment of the corporate creditors

The ―trust fund‖ doctrine considers the subscribed capital stock as a trust fund for the payment of the debts of the corporation, to which the

creditors may look for satisfaction. Until the liquidation of the corporation, no part of the subscribed capital stock may be turned over or released to

the stockholder (except in the redemption of the redeemable shares) without violating this principle. Thus dividends must never impair the subscribed capital stock; subscription commitments cannot be condoned or remitted; nor can the corporation buy its own shares using the subscribed capital as the consideration therefore

The requirement of unrestricted retained earnings to cover the shares is based on the trust fund doctrine which means that the capital stock, property and other assets of a corporation are regarded as equtiy in trust for the payment of corporate creditors. The reason is that creditors of a corporation are preferred over the stockholders in the distribution of corporate assets. There can be no distribution of assets among the

stockholders without first paying corporate creditors. Hence, any disposition of corporate funds to the prejudice of creditors is null and void

SEC Memorandum Circular No. 6, Series of 2009:

“Revised Code of Corporate Governance”

2.3. The Business Organization in the Philippine Context

Single Proprietorship

Excellent Quality Apparel Inc. v. Win Multi Rich

Builders Inc., 578 SCRA 272 (2009)

A sole proprietorship does not possess a juridical personality separate and distinct from the personality of the owner of the enterprise. The law merely recognizes the existence of a sole proprietorship as a form of business organization conducted for profit by a single individual and requires its proprietor or owner to secure licenses and permits, register its business name, and pay taxes to the

national government. The law does not vest a separate legal personality on the sole proprietorship or empower it to file or defend an action in court.

Partnership

Heirs of Jose Lim v. Lim, 614 SCRA 141 (2010)

Joint Venture

Philex Mining Corp. v. CIR, 551 SCRA 428 (2008)

Single Proprietorship

Excellent Quality Apparel Inc. v. Win Multi Rich

Builders Inc., 578 SCRA 272 (2009)

Corporation

Pioneer Insurance v. CA, 175 SCRA 668 (1989)

Lim Tong Lim v. Philippine Fishing Gear

Industries, Inc., 317 SCRA 728 (1999)

Koji Yasuma v. Heirs of Cecilio S. De Villa, 499

SCRA 466 (2006) If a corporation fails to register:

Pioneer case passive investors are not liable Lim Tong case passive investors may still be liable, if they benefitted

Publicly Listed Corporation

Securities Regulations Code §2, 3.1, 3.7, 8 SEC. 2. Declaration of State Policy. - The State shall establish a socially

conscious, free market that regulates itself, encourage the widest participation of ownership in enterprises, enhance the democratization of wealth, promote the development of the capital market, protect investors, ensure full and fair disclosure about securities, minimize if not totally eliminate insider trading and other fraudulent or manipulative devices and practices which create distortions in the free market.

To achieve these ends, this Securities Regulation Code is hereby enacted.

SEC. 3. Definition of Terms 3.1. "Securities" are shares, participation or interests in a corporation or in a commercial enterprise or profit-making venture and evidenced by a certificate, contract, instrument, whether written or electronic in character. It includes:

a) Shares of stock, bonds, debentures, notes, evidences of indebtedness,

asset-backed securities b) Investment contracts, certificates of interest or participation in a profit

sharing agreement, certificates of deposit for a future subscription; c) Fractional undivided interests in oil, gas or other mineral rights;

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 10

d) Derivatives like option and warrants; e) Certificates of assignments, certificates of participation, trust certificates,

voting trust certificates or similar instruments; f) Proprietary or non proprietary membership certificates in corporations; g) Other instruments as may in the future be determined by the

Commission. 3.7. "Exchange" is an organized marketplace or facility that brings together buyers and sellers and executes trades of securities and/or commodities.

SEC. 8. Requirement of Registration of Securities. –

8.1. Securities shall not be sold or offered for sale or distribution within the Philippines, without a registration statement duly filed with and approved by the Commission. Prior to such sale, information on the securities, in such form and with such substance as the Commission may prescribe, shall be made available to each prospective purchaser.

8.2. The Commission may conditionally approve the registration statement under such terms as it may deem necessary. 8.3. The Commission may specify the terms and conditions under which any written communication, including any summary prospectus, shall be deemed not to constitute an offer for sale under this Section. 8.4. A record of the registration of securities shall be kept in a Register of

Securities in which shall be recorded orders entered by the Commission with respect to such securities. Such register and all documents or information with respect to the securities registered therein shall be open to public inspection at reasonable hours on business days. 8.5. The Commission may audit tie financial statements, assets and other information of a firm applying for registration of its securities whenever it deems the same necessary to insure full disclosure or to protect the interest of the

investors and the public in general.

THOMAS LEE HAZEN, JERRY W. MARKHAM, CORPORATIONS

AND OTHER BUSINESS ENTERPRISES, pp. 1-26 (2009)

ADVANTAGES AND DISADVANTAGES OF PARTICULAR ENTERPRISES Sole Proprietorship

Advantages o Control – the owner of proprietorship directly controls and operates

the business o Simplicity – lack of a separate legal structure; more flexible

o Expenses – less operating expenses; no need for reporting o Taxes – the proprietorship is not taxed separately

Disadvantages

o Unlimited Liability – sole proprietor is subject to unlimited liability for any contractual or tort damage caused by the business or agents

o Management – usually dependent on the management of the owner o Transferability – cannot be readily sold

Partnerships

Advantages o Control – the partnership does not separate ownership and control o Simplicity – has a separate legal structure, but the partners may

agree to conduct business in almost any manner; flexibility o Expenses – less operating expenses than a corporation

o Taxes – the partnership is not taxed separately Disadvantages

o Unlimited Liability – the partners are subject to unlimited liability for any contractual or tort damage caused by partners or agents

o Transferability – a partner cannot sell his ownership interest

Limited Partnership

Advantages o Limited Liability – the liability of the limited partners is limited to

the amount of their investment; the general partner remains subject to unlimited liability

o Separation of ownership and control – limited partners may invest capital in an enterprise without becoming involved in management

o Expenses – simplicity in management is still available since the business may be structured freely under the agreement

Disadvantages o Unlimited Liability – the general partner is subject to unlimited

liability for any contractual or tort damages incurred by partnership o Transferability – a limited partner cannot usually readily sell his or

her owenership Corporations

Advantages o Limited Liability – the liability of investors (stockholders) is limited

to the amount of their investment o Separation of ownership and control – the corporate structure

separate ownership and control. Stockholders may invest capital without becoming involved in management

o Transferability - stockholdings in a corporation may be transferred o Perpetual Life – the corporation continues in existence until it is

dissolved. Survives the death of the owner Disadvantages

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 11

o Double Taxation – the corporation is separately taxed for any profits it may receive. The shareholders are then taxed again if the

remaining income is distributed to them o Management – managers of a corporation may mange for their own

interests rather than seeking to maximize shareholder wealth o Expenses – the corporation will encounter more expense in its

operations than required for other business enterprises

Large Taxpayer

NIRC §245(j) Sec. 245(j) The manner in which internal revenue taxes, such as income tax, including withholding tax, estate and donor's taxes, value-added tax, other

percentage taxes, excise taxes and documentary stamp taxes shall be paid through the collection officers of the Bureau of Internal Revenue or through duly authorized agent banks which are hereby deputized to receive payments of such taxes and the returns, papers and statements that may be filed by the taxpayers in connection with the payment of the tax: Provided, however, That notwithstanding the other provisions of this Code prescribing the place of filing of returns and payment of taxes, the Commissioner may, by rules and regulations,

require that the tax returns, papers and statements that may be filed by the

taxpayers in connection with the payment of the tax. Provided, however, That notwithstanding the other provisions of this Code prescribing the place of filing of returns and payment of taxes, the Commissioner may, by rules and regulations require that the tax returns, papers and statements and taxes of large taxpayers be filed and paid, respectively, through collection officers or through duly

authorized agent banks: Provided, further, That the Commissioner can exercise this power within six (6) years from the approval of Republic Act No. 7646 or the completion of its comprehensive computerization program, whichever comes earlier: Provided, finally, That separate venues for the Luzon, Visayas and Mindanao areas may be designated for the filing of tax returns and payment of taxes by said large taxpayers.

For the purpose of this Section, "large taxpayer" means a taxpayer who satisfies any of the following criteria; (1) Value-Added Tax (VAT). - Business establishment with VAT paid or payable of at least One hundred thousand pesos (P100,000) for any quarter of the preceding taxable year; (2) Excise Tax. - Business establishment with excise tax paid or payable of at least One million pesos (P1,000,000) for the preceding taxable year;

(3) Corporate Income Tax. - Business establishment with annual income tax paid or payable of at least One million pesos (P1,000,000) for the preceding taxable year; and

(4) Withholding Tax. - Business establishment with withholding tax payment or

remittance of at least One million pesos (P1,000,000) for the preceding taxable year.

Provided, however, That the Secretary of Finance, upon recommendation of the Commissioner, may modify or add to the above criteria for determining a large taxpayer after considering such factors as inflation, volume of business, wage and employment levels, and similar economic factors. The penalties prescribed under Section 248 of this Code shall be imposed on any violation of the rules and regulations issued by the Secretary of Finance, upon

recommendation of the Commissioner, prescribing the place of filing of returns and payments of taxes by large taxpayers.

Revenue Regulation 02-98 §2.57.2(M) & (W), as

amended by RR 06-09 Creditable Withholding Tax. — Under the creditable withholding tax system, taxes withheld on certain income payments are intended to equal or at least approximate the tax due of the payee on said income. The income recipient is still required to file an income tax return, as prescribed in Sec. 51 and Sec. 52 of the NIRC, as amended, to report the income and/or pay the difference between the

tax withheld and the tax due on the income. Taxes withheld on income payments covered by the expanded withholding tax (referred to in Sec. 2.57.2 of these

regulations) and compensation income (referred to in Sec. 2.78 also of these regulations) are creditable in nature. SECTION 2.57.2. Income Payment Subject to Creditable Withholding Tax and Rates Prescribed Thereon. — Except as herein otherwise provided, there shall be

withheld a creditable income tax at the rates herein specified for each class of payee from the following items of income payments to persons residing in the Philippines: (M) Income payments made by the top twenty thousand (20,000) private corporations to their local/resident supplier of goods and local/resident

supplier of services other than those covered by other rates of withholding tax. — Income payments made by any of the 20,000 corporations, as determined by the Commissioner, to their local/resident supplier of goods and local/resident supplier of services, including non-resident aliens engaged in trade or business in the Philippines. Provided, however that for purchases involving agricultural products in their original state, the tax required to be withheld under this sub-section shall only apply to purchases in excess of the cumulative amount

of P300,000 within the same taxable year. For this purpose, agricultural products in their original state as used in these regulations, shall only include corn, coconut, copra, palay, rice, cassava, sugar cane, coffee, fruits, vegetables, marine food products, poultry and livestocks.

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 12

Supplier of goods 1% Supplier of services 2%

Top 20,000 private corporations shall include a corporate taxpayer who has been determined and notified by the BIR as having satisfied any of the following criteria:

a. Classified and duly notified by the Commissioner as a large taxpayer under RR No. 1-98, as amended, or belonging to the Top 5,000 private

corporations under RR 12-94, or to the Top 10,000 private corporations under RR 17-2003, unless previously declassified as such or had already ceased business operations (automatic inclusion)

b. VAT payment or payable, whichever is higher, of at least P100,000 for the preceding year

c. Annual income tax due of at least P200,000 for the preceding year d. Total percentage tax paid of at least P100,000 for the preceding year

e. Gross sales of P10,000,000 and above for the preceding year f. Gross purchases of P5,000,000 and above for the preceding year g. Total excise tax payment of at least P100,000 for the preceding year

Revenue Regulation 16-2005 §4.114-3 SEC.4.114-3. Submission of Quarterly Summary List of Sales and

Purchases. — a. Persons Required to Submit Summary Lists of Sales/Purchases. —

(1) Persons Required to Submit Summary Lists of Sales. — All persons

liable for VAT such as manufacturers, wholesalers, service-providers, among others, with quarterly total sales/receipts (net of VAT) exceeding Two Million Five Hundred Thousand Pesos (P2,500,000.00).

(2) Persons Required to Submit Summary Lists of Purchases. — All persons liable for VAT such as manufacturers, service-providers, among others, with quarterly total purchases (net of VAT) exceeding One Million Pesos (P 1,000,000.00).

b. When and Where to File the Summary Lists of Sales/Purchases. — The quarterly summary list of sales or purchases, whichever is applicable, shall be submitted in diskette form to the RDO or LTDO or LTAD having jurisdiction over the taxpayer, on or before the twenty-fifth (25th) day of the month following the close of the taxable quarter (VAT quarter)-calendar quarter or fiscal quarter. However, taxpayers under the jurisdiction of the LTS, and those enrolled under

the EFPS, shall, through electronic filing facility submit their Summary List of Sales/Purchases to the RDO/LTDO/LTAD on or before the 30th day of the month following the close of the taxable quarter.

c. Information that Must be Contained in the Quarterly Summary List of Sales to be Submitted. — The quarterly summary list must contain the monthly

total sales generated from regular buyers/customers, regardless of the amount of sale per buyer/customer, as well as from casual buyers/customers with individual sales amounting to P100,000.00 or more. For this purpose, the term "regular buyers/customers" shall refer to buyers/customers who are engaged in business or exercise of profession and those with whom the taxpayer has transacted at least six (6) transactions regardless of amount per transaction either in the previous year or current year. The term "casual buyers/customers", on the other

hand, shall refer to buyers/customers who are engaged in business or exercise of profession but did not qualify as regular buyers/customers as defined in the

preceding statement. The foregoing paragraph, notwithstanding, information pertaining to sales made to buyers not engaged in business or practice of profession (e.g., foreign embassies) may still be required from the seller. The Quarterly Summary List of Sales to Regular Buyers/Customers and Casual

Buyers/Customers and Output Tax shall reflect the following: (1) BIR-registered name of the buyer who is engaged in business/exercise of

profession; (2) TIN of the buyer (Only for sales that are subject to VAT); (3) Exempt

Sales; (3) Zero-rated Sales;

(4) Sales Subject to VAT (exclusive of VAT); (5) Sales Subject to Final VAT Withheld; and (7) Output Tax (VAT on sales

subject to 10%). (The total amount of sales shall be system-generated) d. Information that must be Contained in the Quarterly Summary List of Purchases. (omitted)

e. Rules in the Presentation of the Required Information in the Summary Schedules. (omitted) f. The threshold amounts as herein set for sales and purchases may be

increased/modified by the Commissioner of Internal Revenue if it is necessary for the improvement in tax administration.

g. Required Procedure and Format in the Submission of Quarterly List of Sales/Purchases. (omitted) h. Issuance of Certificate of VAT Withheld at Source The certificate or statement to be issued is the Certificate of Final Tax Withheld at

Source (BIR Form No. 2306), a copy of which should be issued to the payee. i. Penalty Clause (omitted)

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 13

Speech of Mr. John Gokongwei before Ateneo 2004

Graduates

3. Capital Structure

Kenneth H. Marks, Larry E. Robbins, Gonzalo Fernandez

and John P. Funkhouser, The Handbook of Financing

Growth, 22-43 (2005) Capital Structure – refers to the amount of debt and equity and the types of debt and equity used to fund the operations of the company

Optimal Capital Structure

Balances the risk of bankruptcy with the tax savings of debt A company should use both equity and debt to fund its operations This provides greater returns to stockholders than what they would

receive in an all-equity firm By reducing the amount of equity and increasing the amount of debt, the

overall cost of capital is reduced The pool of financing alternatives grows as the critical mass of the

company grows The desired capital structure will change as the company moves from one

business stage to another Debt-to-equity ratio – compares the total liabilities on a company‘s

balance sheet to the company‘s equity Factors Shaping Capital Structure

Company Characteristics Company Stage

Use of Funds Capital Markets‘ Favor of the Industry

Base Assumptions Industry Leverage Norms Industry Dynamics Shareholder Objectives and Preferences

4. Players in Corporate Finance

4.1. In General

o KENNETH H. MARKS, LARRY E. ROBBINS, GONZALO

FERNANDEZ AND JOHN P. FUNKHOUSER, THE HANDBOOK OF

FINANCING GROWTH, 262-278 (2005) The Players and their Roles

Counsel – advocate I negotiations with counsel for third parties Board of Directors – composed of individuals who can help the company

through a rich network of potential customers, investors, vendors and partners

Investment Bankers – financial intermediaries (not investors) that act as an underwriter or agent for corporations raising capital or seeking

strategic transactions Accountants - compilation, review or audit of the financial statements of

the company and preparation of tax returns Consultants/Advisers

4.2. In Strategic Transactions

o MICHAEL E. S. FRANKEL, MERGERS AND ACQUISITIONS

BASICS 1-49 (2005) Strategic Transactions

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 14

MODULE 2: THE DEBT AND EQUITY DICHOTOMY

1. Examining the Firm as an Enterprise

William A. Klein & John C. Coffee, Jr.: Business

Organization and Finance, 1-50 (2007) Introduction

Participants / central figures

o Owner has equity or residual interest in the business

has control – right to decide on how operated o Employees o Lenders / creditors

The relationship among the participants involves a joint economic enterprise – there is a communality of interest

Bargain Elements (deal points) o Risk of loss – allocation among the participants of losses o Return – salaries, interest and other fixed claims and to

shares of the residual (the profit) o Control – determines who has the right to make decisions o Duration – determines how long the relationships among

participants will last and is intended to include the conditions on which the relationship can be terminated and on which a claim may be transferred.

Constraints o Conflict of interest – arises from the fact that people tend to

pursue their own self-interest o Government regulation – may limit the freedom of

participants in a business venture to adopt chosen rules o Limits on complete specificity – complete specificity of all

outcomes in all possible situations is not possible and even to the degree it is possible, may not be worth the cost

Sole Proprietorship

Definition a business owned directly by one individual (sole proprietor)

Ownership and management may be separated. Creditors

o Liability for debts – unlimited liability (personal in nature) o Secured creditor – one whose claim is secured by specific

property, and who has first claim to the proceeds of the sale of such property

o General creditor – all other creditors except a secured one o It is possible to avoid personal liability through a nonrecourse loan

Nonrecourse loan – loan secured by specific property o In the event of bankruptcy, no distinction is made between

business and personal debts, except for exempt personal assets o Leverage – used to describe the financial consequences of the

use of debt and equity. Debt creates financial leverage for the equity The greater the debt, the greater the leverage The greater the leverage, the greater the potential gains

and losses for the equity and the greater the risk of loss

for the debt o Effects of leverage result from the facts that:

the lender has a fixed claim the return on the investment is uncertain the borrower has a residual claim (right to whatever is

left after the debt holder‘s claim is satisfied) o Leverage creates risk. Greater leverage, greater risk

o Equity attributes of debt Creditors are subject to varying degrees of risk of default Degree of risk depends on total value of business as

compared to the amount of the debt As risk rises, creditors will become more concerned with

how the business is run and likely want increasing levels

of control As risk rises, higher interest rate may also be demanded—

a higher return on its investment in the business

Employees o A principal-agency relationship is created o The agent has power to bind the principal

o Agents owe a duty of loyalty or fiduciary obligation to their principal

2. Capital Structure

KENNETH H. MARKS, LARRY E. ROBBINS, GONZALO FERNANDEZ

AND JOHN P. FUNKHOUSER, THE HANDBOOK OF FINANCING

GROWTH, 22-43 (2005) Capital Structure – refers to the amount of debt and equity and the types of debt and equity used to fund the operations of the company Optimal Capital Structure

Balances the risk of bankruptcy with the tax savings of debt

A company should use both equity and debt to fund its operations

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 15

This provides greater returns to stockholders than what they would receive in an all-equity firm

By reducing the amount of equity and increasing the amount of debt, the overall cost of capital is reduced

The pool of financing alternatives grows as the critical mass of the company grows

The desired capital structure will change as the company moves from one business stage to another

Debt-to-equity ratio – compares the total liabilities on a company‘s

balance sheet to the company‘s equity

Factors Shaping Capital Structure Company Characteristics Company Stage Use of Funds Capital Markets‘ Favor of the Industry

Base Assumptions Industry Leverage Norms Industry Dynamics

Shareholder Objectives and Preferences

3. Debt v. Equity

KENNETH H. MARKS, LARRY E. ROBBINS, GONZALO FERNANDEZ

AND JOHN P. FUNKHOUSER, THE HANDBOOK OF FINANCING

GROWTH, 161-163 (2005)

4. The Balance Sheet

MARTIN FRIDSON & FERNANDO ALVAREZ, FINANCIAL STATEMENT

ANALYSIS, 29-48 (2002)

SRC Rule 68, as amended, Rules and Regulations

Covering Form and Content of Financial Statements

(October 25, 2005) – 4d *Superseded by 2011 amendment (see below); But this gives a complete picture of the parts of a financial statement that is currently required.

Basic Financial Statements and Minimum Presentation

(i) Balance Sheet (now called Statements of Assets and Liabilities)

As a minimum, the face of the balance sheet should include the following line items:

1. Cash and Cash Equivalents 2. Financial Assets 3. Trade and Other Receivables 4. Inventories 5. Property Plant and Equipment

6. Investments accounted for using the equity method 7. Intangible Assets

8. Trade and Other Payables 9. Tax Liabilities and assets 10. Provisions 11. Non-current interest-bearing liabilities 12. Minority Interest

13. Issues Capital and Reserves Except as otherwise required by the Commission, the various line items

and disclosures set forth for this form of statement shall be in accordance with the Philippine Financial Reporting Standards (PFRS) enumerated under paragraph (2)(a) of this Rule.

(ii) Income Statement

As a minimum, the face of the balance sheet should include the following line items:

1. Revenue 2. The results of operating activities

3. Finance costs 4. Shares of income and losses of associates and joint ventures

accounted for using the equity method 5. Tax expenses 6. Income or loss from ordinary activities

7. Extraordinary items 8. Minority interest

9. Net income or loss for the period

Except as otherwise required by the Commission, the various line items and disclosures set forth for this form of statement shall be in accordance with the Philippine Financial Reporting Standards (PFRS) enumerated under paragraph (2)(a) of this Rule.

(iii) Statement of Changes in Equity

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 16

Except as otherwise required by the Commission, Statements of Changes in Equity shall be prepared in accordance with the generally accepted accounting

principles in the Philippines [See definition in paragraph 1(b)(v) of Rule 68]. This Annex merely emphasizes some requirements as to presentation and disclosures on the Statements of Changes in Equity.

1. A corporation shall present, as a separate component of its financial statements, a statement showing: a. The net income or loss for the period; b. Each item of income and expense, gain or loss which, as required

by other Statements of Financial Accounting Standards, is recognized directly in equity, and the total of these items; and

c. The cumulative effect of changes in accounting policy dealt with under the Benchmark treatment, and the correction of fundamental errors as required by PFRS.

2. In addition, a corporation shall present, either within this statement or

in the notes: a. Capital transactions with owners and distributions to owners; b. The Balance of accumulated income or loss at the beginning of the

period and at the balance sheet date, and the movements for the period; and

c. A reconciliation between the carrying amount of each class of capital stock, additional paid in capital and each reserve at the beginning and the end of the period, separately disclosing each movement.

3. The requirements above may be met in a number of ways. The

approach adopted shall follow a columnar format which reconciles

between the opening and closing balances of each element within shareholders‘ equity, including items (a) to (f). An alternative is to present a separate component of the financial statements which presents only items (a) to (c). Under this approach, the items described in (d) to (f) are shown in the notes to the financial

statements. Whichever approach is adopted, a sub-total of the items in (b) to enable users to derive the total gains and losses arising from

the registrant‘s activities during the period, is required.

(iv) Cash Flow Statement

Except as otherwise announced by the Commission, the various line items and disclosures set forth for this form of statement shall be in accordance with

the PRFS under paragraph (2)(a) of this Rule.

(v) Notes to Financial Statement

(Accounting Policies and Explanatory Notes)

Except as otherwise announced by the Commission, the various disclosures for this part of the financial statement shall be in accordance with the PFRS enumerated under paragraph (2)(a) of this Rule.

SEC Memorandum Circular No. 16-09 (December 10,

2009) II 2(a) Preparation of Financial Statements

2. In relation to the audit of said financial statements, the management should provide its auditor with the following: a. Complete set of financial statements consisting of

(1) Statement of Financial Position; (2) Either a single statement of comprehensive income, or a separate

income statements and a separate statement of comprehensive income;

(3) Statement of changes in equity; (4) Statement of cash flows; (5) Notes including a summary of significant accounting policies;

(6) If applicable, schedules and reconciliation forming part of the financial

statements required under the existing rules of the Commission.

SRC Rule 68, as amended, Rules and Regulations

Covering Form and Content of Financial Statements

(October 20, 2011) – Part 2. B(vi)(a) & 5 I.2.B(vi) In the audit of the company‘s financial statements, the management shall provide the external auditor with the following documents:

(a) Complete set of financial statements as prescribed under the

applicable financial reporting framework of the entity, and If applicable,

schedules and reconciliation forming part of the financial statements required under the existing rules of the Commission;

I.5. Comparative Financial Statements

A. The financial statements to be filed with the Commission shall be presented in comparative form. The figures for the most recently ended fiscal year may be presented at the right portion immediately after the accounts name, followed by the figures for the last preceding year.

B. Balance Sheet or Statement of Financial Position

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 17

The audited balance sheets or statements of financial position shall be as of the end of each of the two most recently completed fiscal years.

C. Statement of Comprehensive Income, Statement of Cash Flows and

Statement of Changes in Equity If practicable, these statements shall be for each of the two most recent completed fiscal years or such shorter period as the company (including predecessors) has been in existence.

D. An explanation through a note or otherwise shall be made explaining the

reasons for filing a single-period statement, e.g. it is the first period of a new company.

E. When financial statements are presented on a comparative basis for more than the periods required, the auditor's report need not extend to prior

periods for which the financial statements are not required to be audited. i. If the financial statements of the prior year were not audited, such

statements shall be marked prominently as "UNAUDITED." In addition, the auditor shall disclose this in an ―other matter‖ paragraph in the auditor‘s report.

ii. If the financial statements of a prior-period have been examined by

another independent certified public accountant whose report is not presented, the statements shall be marked to disclose prominently that they are not being reported upon by the current auditor. If the auditor of the financial statements for such periods did not give an unqualified opinion on such statements, the auditor for the current year shall indicate in an ―other matter‖ paragraph of his report (I) that the financial statements of the prior-period were examined by

other auditors, (II) the date of their report (III) the type of opinion expressed by the predecessor auditor and (IV) the substantive reasons it was qualified.

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 18

MODULE 3: DEBT

1. Interpretation of Contracts

Civil Code, Arts. 1370-1379 Article 1370. If the terms of a contract are clear and leave no doubt upon the intention of the contracting parties, the literal meaning of its stipulations shall control. If the words appear to be contrary to the evident intention of the parties, the latter shall prevail over the former. (1281) Article 1371. In order to judge the intention of the contracting parties, their contemporaneous and subsequent acts shall be principally considered. (1282) Article 1372. However general the terms of a contract may be, they shall not be understood to comprehend things that are distinct and cases that are different

from those upon which the parties intended to agree. (1283) Article 1373. If some stipulation of any contract should admit of several meanings, it shall be understood as bearing that import which is most adequate to render it effectual. (1284) Article 1374. The various stipulations of a contract shall be interpreted together,

attributing to the doubtful ones that sense which may result from all of them taken jointly. (1285) Article 1375. Words which may have different significations shall be understood in that which is most in keeping with the nature and object of the contract. (1286)

Article 1376. The usage or custom of the place shall be borne in mind in the interpretation of the ambiguities of a contract, and shall fill the omission of

stipulations which are ordinarily established. (1287) Article 1377. The interpretation of obscure words or stipulations in a contract shall not favor the party who caused the obscurity. (1288) Article 1378. When it is absolutely impossible to settle doubts by the rules established in the preceding articles, and the doubts refer to incidental circumstances of a gratuitous contract, the least transmission of rights and interests shall prevail. If the contract is onerous, the doubt shall be settled in favor of the greatest reciprocity of interests. If the doubts are cast upon the principal object of the contract in such a way that

it cannot be known what may have been the intention or will of the parties, the

contract shall be null and void. (1289)

Article 1379. The principles of interpretation stated in Rule 123 of the Rules of Court shall likewise be observed in the construction of contracts. (n)

Rules of Court, Rule 130 §§10-19

4. Interpretation Of Documents Section 10. Interpretation of a writing according to its legal meaning. — The language of a writing is to be interpreted according to the legal meaning it bears

in the place of its execution, unless the parties intended otherwise. (8) Section 11. Instrument construed so as to give effect to all provisions. — In the construction of an instrument, where there are several provisions or particulars,

such a construction is, if possible, to be adopted as will give effect to all. (9) Section 12. Interpretation according to intention; general and particular provisions. — In the construction of an instrument, the intention of the parties is to be pursued; and when a general and a particular provision are inconsistent, the latter is paramount to the former. So a particular intent will control a general one that is inconsistent with it. (10)

Section 13. Interpretation according to circumstances. — For the proper construction of an instrument, the circumstances under which it was made, including the situation of the subject thereof and of the parties to it, may be shown, so that the judge may be placed in the position of those who language he is to interpret. (11)

Section 14. Peculiar signification of terms. — The terms of a writing are presumed to have been used in their primary and general acceptation, but evidence is admissible to show that they have a local, technical, or otherwise peculiar signification, and were so used and understood in the particular instance,

in which case the agreement must be construed accordingly. (12)

Section 15. Written words control printed. — When an instrument consists partly of written words and partly of a printed form, and the two are inconsistent, the former controls the latter. (13) Section 16. Experts and interpreters to be used in explaining certain writings. — When the characters in which an instrument is written are difficult to be deciphered, or the language is not understood by the court, the evidence of

persons skilled in deciphering the characters, or who understand the language, is admissible to declare the characters or the meaning of the language. (14)

International Corporate Finance Atty. Jose Cochingyan III

Carlo Agdamag, A2015 19

Section 17. Of Two constructions, which preferred. — When the terms of an agreement have been intended in a different sense by the different parties to it,

that sense is to prevail against either party in which he supposed the other understood it, and when different constructions of a provision are otherwise equally proper, that is to be taken which is the most favorable to the party in whose favor the provision was made. (15) Section 18. Construction in favor of natural right. — When an instrument is equally susceptible of two interpretations, one in favor of natural right and the

other against it, the former is to be adopted. (16)