International Comparison Antea november 2014

24

1 internationalcomparison UPDATED INFORMATION. NOVEMBER 2014 “The content of this newsletter has been written or gathered by ANTEA and its representatives, for informational purposes only. It is not intended to be and is not considered to be legal advice, nor as a proposal for any type of legal transaction. Legal advice of any nature should be sought from legal counsel. For further advice please contact local office.” ÍNDEX internationalcomparison UPDATED INFORMATION. NOVEMBER 2014 • ITALY • MEXICO • PAKISTAN • ARGENTINA • ANDORRA • AUSTRIA • GREECE • ISRAEL • LUXEMBOURG • SPAIN • THE NETHERLANDS • VENEZUELA • GERMANY • ROMANIA • SERBIA • UK • SINGAPORE • TURKEY • HUNGARY • AUSTRALIA • COLOMBIA • URUGUAY • CYPRUS • PORTUGAL • REGISTRATION FOR VALUE-ADDED TAX (VAT) ITALY Who is required to register for VAT? Non-established taxable persons: Non-established taxable persons have to register for VAT in Italy if they intend to make taxable supplies or services in Italy. In case of a permanent establishment in Italy further particular rules are applicable (e.g. inscription of the Italian branch into the Italian register of companies) When is VAT registration required? The registration is required before carrying out taxable supplies or services in Italy. Are there penalties for not registering or late registration? Yes (basically 100 – 200% of the output VAT, further sanctions and interests for late payments), reductions can be obtained, but every case has to be verified. In some cases, criminal law rules are applicable. Is voluntary VAT registration possible for foreign entities? If a non-established taxable person applies for an Italian VAT number, the Italian Tax Authority asks for the reasons of the VAT registration. If there is no need for registration, the Italian tax authority might reject the application form. Are there any simplifications that could avoid the need for registration for foreign entities? There are specific reverse charge rules in the Italian VAT Law which can avoid the need for VAT registration for foreign entities in some cases. Andorra, Argentine, Australia, Austria, Bolivia, Brazil, Bulgaria, Colombia, Costa Rica, Cyprus, Chile, China, Ecuador, Egypt, El Salvador, France, Germany, Greece, Guatemala, Honduras, Hungary, India, Israel, Italy, Luxembourg, Malta, Mexico, Morocco, Pakistan, Peru, Poland, Portugal, Republic of Singapore, Romania, Serbia, Spain, Switzerland, The Netherlands, Tunisia, Turkey, UAE, United Kingdom, Uruguay, USA,Venezuela

description

Registration for TAX VAT

Transcript of International Comparison Antea november 2014

1internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

“The content of this newsletter has been written or gathered by ANTEA and its representatives, for informational purposes only. It is not intended to be and is not considered to be legal advice, nor as a proposal for any type of legal transaction. Legal advice of any nature should be sought from legal counsel. For further advice please contact local office.”

ÍND

EX

internationalcomparisonUPDATED INFORMATION. NOVEMBER 2014

• ITALY• MEXICO• PAKISTAN• ARGENTINA• ANDORRA• AUSTRIA

• GREECE• ISRAEL• LUXEMBOURG• SPAIN• THENETHERLANDS• VENEZUELA

• GERMANY• ROMANIA• SERBIA• UK• SINGAPORE• TURKEY

• HUNGARY• AUSTRALIA• COLOMBIA• URUGUAY• CYPRUS• PORTUGAL

•REGISTRATIONFORVALUE-ADDEDTAX(VAT)

ITALYWhoisrequiredtoregisterforVAT?

Non-establishedtaxablepersons:Non-establishedtaxablepersonshavetoregisterforVATinItalyiftheyintendtomaketaxablesuppliesorservicesinItaly.IncaseofapermanentestablishmentinItalyfurtherparticularrulesareapplicable(e.g.inscriptionoftheItalianbranchintotheItalianregisterofcompanies)

WhenisVATregistrationrequired?

Theregistration is requiredbeforecarryingout taxablesuppliesorservices inItaly.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes(basically100–200%oftheoutputVAT,furthersanctionsandinterestsforlatepayments),reductionscanbeobtained,buteverycasehastobeverified.Insomecases,criminallawrulesareapplicable.

IsvoluntaryVATregistrationpossibleforforeignentities?

Ifanon-establishedtaxablepersonappliesforanItalianVATnumber,theItalianTaxAuthorityasksforthereasonsoftheVATregistration.Ifthereisnoneedforregistration,theItaliantaxauthoritymightrejecttheapplicationform.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

TherearespecificreversechargerulesintheItalianVATLawwhichcanavoidtheneedforVATregistrationforforeignentitiesinsomecases.

Andorra, Argentine, Australia, Austria, Bolivia, Brazil, Bulgaria, Colombia, Costa Rica, Cyprus, Chile, China, Ecuador, Egypt, El Salvador, France, Germany, Greece, Guatemala, Honduras, Hungary, India, Israel, Italy, Luxembourg, Malta, Mexico, Morocco, Pakistan, Peru, Poland, Portugal, Republic of Singapore, Romania, Serbia, Spain, Switzerland, The Netherlands, Tunisia, Turkey, UAE, United Kingdom, Uruguay, USA, Venezuela

2internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Fornon-establishedtaxablepersonsfromotherMemberStates:• Applicationform;• Certificateoftheforeigncompaniesregister;• Certificateoftheforeigntaxauthority;• DescriptionoftheactivityperformedabroadandtobeperformedinItalyand

thereasonsfortheVATregistrationinItaly;• Copyoftheidentitycardofthelegalrepresentative;• Italianfiscalcode(codicefiscale)ofthelegalrepresentative.Forthetranslationoftheforeigncertificatesitisusuallynotnecessarytodothiswiththeapostille.For non-established taxable persons from outside the European Union a taxrepresentativehastobeappointed.InthiscasetheItaliantaxauthoritymayrequesttheapostilleonthecertificatesoftheforeignAuthorities.

HowfrequentlyareVATreturnstobesubmitted?

• AnnualVATreturn(dichiarazioneIVA);• AnnualcommunicationofVATdata(comunicazioneannualedatiIVA).

Arethereanyotherreturnstobesubmitted?

• Annualreturnofdata(comunicazionepolivalente)foreachclientandsupplier(i.g.FiscalCode,taxablebase,VAT);

• Intrastat(montlyorquarterly)tothecustomsauthorityregardingtheintra-communityacquisitionsandsalesofgoodsandserviceswithotherMemberStates;

• Blacklist(monthlyorquarterly)foroperationswithclientsandsuppliersinsocalled“blacklist”States,accordingtoItalianlaw.

OtherpointstobeconsideredforVATregistration?

IncaseofdistancesellingfromotherMemberStatestononVAT-registeredItaliancustomers,intheapplicationdocumentstheItaliantaxauthorityaskstodeclaretheamountsinvoicedsofarinthecurrentyearandtheprevioustwoyearswithdistancesellinginItalytonon-VATregisteredcustomers.

MEXICOWhoisrequiredtoregisterforVAT?

AllentitiesandpeoplethatdobusinessinMexico(ForinstancePE).

WhenisVATregistrationrequired?

BeforetheystarttodobusinessinMexico.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes, and in some cases (And very important) the invoices issued can not bedeductiblebytheclientsresidentsinMexico.

IsvoluntaryVATregistrationpossibleforforeignentities?

No,It iseithertheyneed itornot, if theyneed it theyhavetohavetheVATregistration.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

Notatthemoment.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Several documents, Among them articles of incorporation, birth certicate,documentsrelatedtotaxdomicileetc.translationwithapostilleismandatory.

HowfrequentlyareVATreturnstobesubmitted?

Onmonthlybasis,thereisanannualreturntoo.

Arethereanyotherreturnstobesubmitted?

Severalotherrelatedtoincometaxandinformativeonestoo.

OtherpointstobeconsideredforVATregistration?

IngeneralalltaxresidentsinMexiconeedsVATregistration,forforeignentitiesisveryimportanttoanalize,beforetheyhaveoperationswithMexico,iftheyneedsuchregistrationornot.

3internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

PAKISTANWhoisrequiredtoregisterforVAT?

ForSupplies:• A manufacture whose taxable annual turnover exceeds Rs. 5,000,000 or

whoseannualutilitybillsexceedRs.700,000duringpreceding12months.• AretailerwhosevalueofsuppliesexceedsRs.5,000,000duringpreceding

12months.• Animporterimportingtaxablegoods.• Awholesaler,dealeranddistributor.• Acommercialexporterforclaimingrefund.• Taxableserviceprovidersliabletoregisterunderprovincialsalestax.ForServices:Registrationwillberequiredforallthepersonswhoare:• Residents• Provideanyoftheserviceslistedintherelevantprovincialacts.• FulfillanyothercriteriawhichtherelevantAuthority/Board(thegoverning

body)mayprescribe.Everyprovincehasitsownauthority/board.WhenisVATregistrationrequired?

VAT(SalesTax)registrationisrequiredwhen:• Theabovecriteriaisachieved;• Apersonwhoisnotrequiredtoberegisteredandcarriesonaneconomic

activity,canapplyforVoluntaryregistrationatanytime.• TheBoard/Authority is satisfied thataperson is required tobe registered

buthasnotappliedforregistrationtheofficermaybyorderregisterthesaidperson.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes,therearepenaltiesforbothnotregisteringandlateregistration.Any personwho is required to be registered fails tomake an application forregistrationbeforemakingtaxablesuppliesshallbeliabletopayapenaltyofRs.10,000or5%oftheamountoftaxinvolved,whicheverishigher.Further, ifsuchaperson fails to registerwithin60daysofcommencementoftaxableactivity,heshallfurtherbeliabletoimprisonmentforatermwhichmayextendto3yearsorwithafineequaltoanamountoftaxinvolvedorboth.Providedfurther,ifsuchapersonfailstogetregisteredwithin90daysofprovidingtaxableservices,heshallfurtherbeliabletoimprisonmentforatermwhichmayextendto1yearorwithafineequaltoanamountoftaxinvolvedorboth.

IsvoluntaryVATregistrationpossibleforforeignentities?

No,avoluntaryVATregistrationisnotpossibleforforeignentities.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

No

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Followingdocumentsare required for registrationdependingupon the typeofentity:• OriginalNTN(nationaltaxnumber)certificate• CopyofCNIC(IDcards)ofdirectors,copyofpassport,incaseofforeigners• CopyofNTNofdirectors• Applicationformdulysignedbythedirectorswiththumbimpression• Incorporationcertificate(incaseoflimitedcompany)• CertifiedcopiesofForm-A,21,29(incaseoflimitedcompany)• Bankcertificate• CopyofrentagreementwiththecopyofCNICoftheowner/rentdeedalong

withthecopyofCNICoflandlord• Businessletterhead• Copyofelectricitybill,telephonebillandgasbillofthepremises• Copyofmobilebillofcurrentmonthofdirectors• Natureofbusinessindetail• GPRSviewofthemanufacturingsite

HowfrequentlyareVATreturnstobesubmitted?

Monthlyreturnsarerequiredtofile.

Arethereanyotherreturnstobesubmitted?

Withholding tax statements are required to file in case of withholding agent.Followingreturnsaretobefiledotherthanmonthlyreturns:• Specialreturn(ontheorderofcommissioner)• Finalreturn(forde-registrationsuchreturnshallbesubmitted)

4internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

OtherpointstobeconsideredforVATregistration?

• Apersonwhoreceivesataxableservicebutisnotaregisteredpersonshallbedeemedtobearegisteredpersonforthepurposesoftaxperiodinwhichsuchaperson:a)Receivestheservices;b)Aninvoiceforthevalueoftheserviceissenttotheperson;orc)Considerationfortheserviceispaidbytheperson;whicheverisearlier.

• Theboardshallpublishalistofregisteredpersonsonitswebsite.

ARGENTINAWhoisrequiredtoregisterforVAT?

Everypersonorentitiethatwantsto:• sellchattellocatedwithinthecountry’sterritory• work,leaseorprovideaserviceinArgentina.• Importagood• Provideaserviceoutsideofthecountry,whicheconomicusage isdone in

Argentina

WhenisVATregistrationrequired?

Registrationisrequiredtoeveryentitiethatwantstooperateaccordingtotheconditionssetabove.Thereisnominimuminvoicingorearningsestablishedtomakeitcompulsory.

Aretherepenaltiesfornotregisteringorlateregistration?

Thepenaltyisestablishedfrom50%toa100%oftheVATthatwasomitted.

IsvoluntaryVATregistrationpossibleforforeignentities?

Argentina’sVATlawdoesnotforeseeanylegalentitysimilartothevoluntaryVATregistration,notevenforlocalentities.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

No.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Forregistration,itisrequiredtofilladocumentcalledF.420/Jwithinformationabout the entitie, a copy of the companies statute with its correspondingtranslation(ifnotinSpanish)withapostilleaccordingtotheHagueConvention(if the entitie is established in a country that agreeswith theConvention) orcertifiedbyapublicnotaryandvalidatedbyArgetineconsulate(iftheentitieisestablishedinacountrythatdoesnotagreewiththeConvention),andacopyoftheregistrationatIGJ(thegovernmentalorganizationthatrulescommercialentities).

HowfrequentlyareVATreturnstobesubmitted?

Theyaretobesubmittedonceamonth.

Arethereanyotherreturnstobesubmitted?

Therearemonthlyinformationreturnsthatneedtobefulfilled.

OtherpointstobeconsideredforVATregistration?

TheVATpayedforexportscanberecoveredortransferredtoathirdpartyifitsurpassestheVATgeneratedbytheirtaxedoperations.

5internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

ANDORRAWhoisrequiredtoregisterforVAT?

All the individuals and the companies with an annual turnover higher than€40.000whichperformdeliveryofgoodsorrenderserviceslocatedinAndorra.

WhenisVATregistrationrequired?

NospecificVATregistrationisnecessaryforthetaxpayersestablishedinAndorra.Nevertheless, a specific registration is required to entrepreneurs qualified astaxpayerswhicharenotestablishedinAndorraandperformactivitieslocatedinsuchterritory.Inthisregard,theAndorranVATLawforeseesthesituationswhereforeignentrepreneursareconsideredasVATtaxpayers.

Aretherepenaltiesfornotregisteringorlateregistration?

TheyarenotspecificallyforeseenintheVATLaw,neverthelesstheAndorrantaxAuthoritiesareabletolevyageneralpenaltyasnotfulfillingwithallthelegalrequirements.

IsvoluntaryVATregistrationpossibleforforeignentities?

ForeignentitiesshouldberegisteredinAndorraforVATpurposesincasetheyperforminsuchterritoryunderapermanentestablishmentortheyareconsideredastaxpayerofactivitieslocatedinAndorra.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

N/A

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

N/A

HowfrequentlyareVATreturnstobesubmitted?

12monthly forms(dependingontheannualturnoverofthetaxpayer, thetaxrecordsmustbequarterlyorbiannual)

Arethereanyotherreturnstobesubmitted?

ThereisnootherreturnstobesubmittedinrelationtotheVAT

OtherpointstobeconsideredforVATregistration?

No

6internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

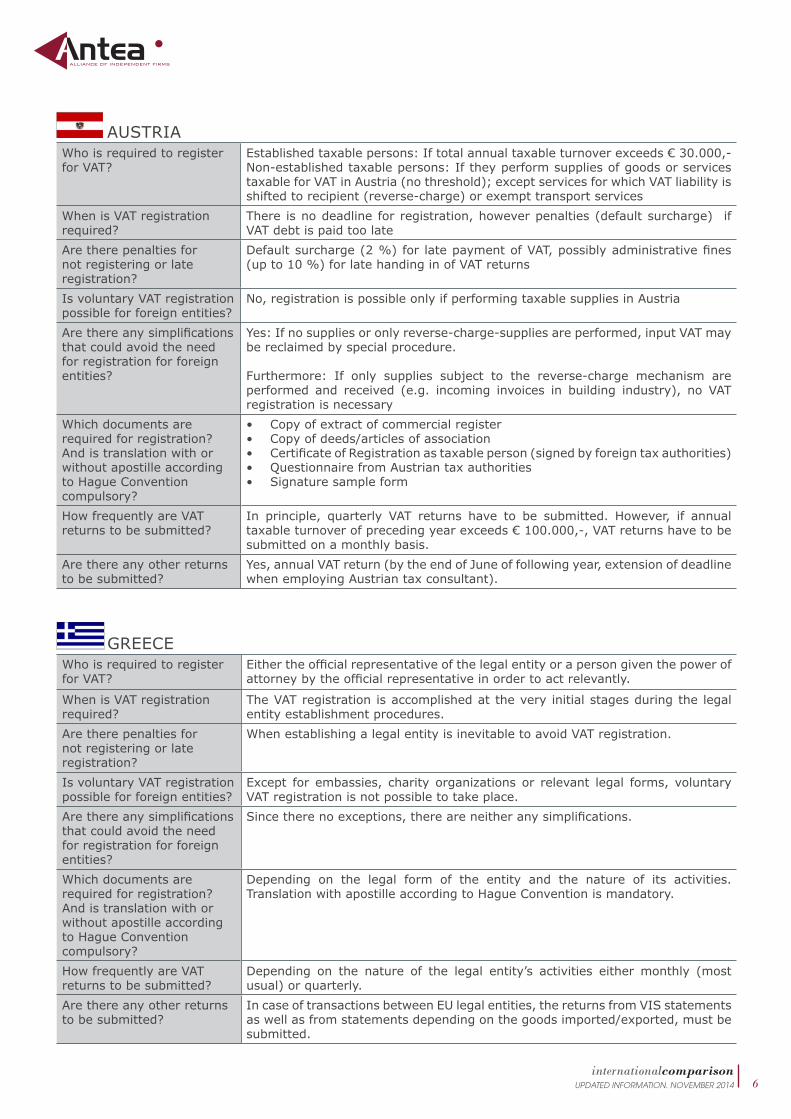

AUSTRIAWhoisrequiredtoregisterforVAT?

Establishedtaxablepersons:Iftotalannualtaxableturnoverexceeds€30.000,-Non-establishedtaxablepersons:IftheyperformsuppliesofgoodsorservicestaxableforVATinAustria(nothreshold);exceptservicesforwhichVATliabilityisshiftedtorecipient(reverse-charge)orexempttransportservices

WhenisVATregistrationrequired?

There isnodeadlineforregistration,howeverpenalties(defaultsurcharge) ifVATdebtispaidtoolate

Aretherepenaltiesfornotregisteringorlateregistration?

Defaultsurcharge(2%)for latepaymentofVAT,possiblyadministrativefines(upto10%)forlatehandinginofVATreturns

IsvoluntaryVATregistrationpossibleforforeignentities?

No,registrationispossibleonlyifperformingtaxablesuppliesinAustria

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

Yes:Ifnosuppliesoronlyreverse-charge-suppliesareperformed,inputVATmaybereclaimedbyspecialprocedure.

Furthermore: If only supplies subject to the reverse-charge mechanism areperformed and received (e.g. incoming invoices in building industry), no VATregistrationisnecessary

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

• Copyofextractofcommercialregister• Copyofdeeds/articlesofassociation• CertificateofRegistrationastaxableperson(signedbyforeigntaxauthorities)• QuestionnairefromAustriantaxauthorities• Signaturesampleform

HowfrequentlyareVATreturnstobesubmitted?

In principle, quarterly VAT returns have to be submitted. However, if annualtaxableturnoverofprecedingyearexceeds€100.000,-,VATreturnshavetobesubmittedonamonthlybasis.

Arethereanyotherreturnstobesubmitted?

Yes,annualVATreturn(bytheendofJuneoffollowingyear,extensionofdeadlinewhenemployingAustriantaxconsultant).

GREECEWhoisrequiredtoregisterforVAT?

Eithertheofficialrepresentativeofthelegalentityorapersongiventhepowerofattorneybytheofficialrepresentativeinordertoactrelevantly.

WhenisVATregistrationrequired?

TheVATregistrationisaccomplishedattheveryinitialstagesduringthelegalentityestablishmentprocedures.

Aretherepenaltiesfornotregisteringorlateregistration?

WhenestablishingalegalentityisinevitabletoavoidVATregistration.

IsvoluntaryVATregistrationpossibleforforeignentities?

Except for embassies, charity organizationsor relevant legal forms, voluntaryVATregistrationisnotpossibletotakeplace.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

Sincetherenoexceptions,thereareneitheranysimplifications.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Depending on the legal form of the entity and the nature of its activities.TranslationwithapostilleaccordingtoHagueConventionismandatory.

HowfrequentlyareVATreturnstobesubmitted?

Depending on the nature of the legal entity’s activities eithermonthly (mostusual)orquarterly.

Arethereanyotherreturnstobesubmitted?

IncaseoftransactionsbetweenEUlegalentities,thereturnsfromVISstatementsaswellasfromstatementsdependingonthegoodsimported/exported,mustbesubmitted.

7internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

ISRAELWhoisrequiredtoregisterforVAT?

VATisimposedforbusinessaction,andimportofgoods,inIsrael.

WhenisVATregistrationrequired?

• Israeliresident:immediately.• Foreign resident: foreign resident with taxable business activity in Israel

mustberegisteredwithin30days,andupdateauthoritieswithregardstohisfiscalrepresentativeinIsrael.

Aretherepenaltiesfornotregisteringorlateregistration?

• TaxcanbedeterminedbydecisionofVATauthorities.• Booksdisqualification.• Fines,interestandlinkage.• Etc.

IsvoluntaryVATregistrationpossibleforforeignentities?

No.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

• Thepayercanpayvatonoutputonbehalfoftheserviceprovider,andtheservice provider is not obligated to be registered, butwill not be able todemandvatoninput.

• Thepayercanissuetaxinvoiceonbehalfoftheserviceprovider,andpaythevatonhisbehalf.Theserviceprovidercandemandvatoninput.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Forforeignresident• CompanyincorporationdocumentinIsraelandabroad.• Personaldetailsofauthorizedsignatories.• Passportofcompanymanagers.• Writtenrequest:detailsregardingtheactivityinIsrael.• AgreementwithIsraeliclients.• OfficialapproveofopeningbankaccountinIsrael.• PersonaldetailsoffiscalrepresentativeinIsrael.• Allabove–translatedtoHebrewandApostille.

HowfrequentlyareVATreturnstobesubmitted?

• 30days/90days/180days,ormore.

Arethereanyotherreturnstobesubmitted?

No.

OtherpointstobeconsideredforVATregistration?

Foreignresidentmustestablishafiscalrepresentative,andactivatehisbusinessactivityasbyforeigncompanyorIndependenty.

8internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

LUXEMBOURGWhoisrequiredtoregisterforVAT?

In principle, any business entity or individual established in Luxembourg thatcarriesouteconomicactivities independentlyandregularly isdeemedtobeataxablepersonforVATpurposesandshouldberegisteredforVATpurposesinLuxembourg.

Morespecifically,thefollowingmustregisterforVAT:• any person established in Luxembourg who starts a taxable activity and

expectsannualturnovertoexceedEUR25,000;• any person who is not established or domiciled in Luxembourg, but who

carriesouttransactionssubjecttoVATinLuxembourgsuchastheoccasionalandtemporaryprovisionofserviceswhatevertheturnover;

• anypersonwho is taxable inprinciplebutexempted fromregistration forVATaswellasany legalpersonnotsubject toVATwhocarriesout intra-Community acquisitions of goods, for an annual amount exceeding EUR10,000;

• any taxable person, established in Luxembourg, who only carries outeconomicoperationsthatdonotgiverisetoarightofdeductionandwhopurchasesservicesfromataxablepersonestablishedabroad,forwhichtheservicebuyerisliablefortax;

• any taxable person, established in Luxembourg, who only carries outeconomicoperationsthatdonotgiverisetoarightofdeductionandwhoprovidestaxableservices,inanotherEUMemberState,forwhichtheservicebuyerisliableforthetax;

• anypersonestablishedinLuxembourg,subjecttotheagriculturalandforestryflat-ratetaxationandwhodeliversalcoholicbeveragesorwoodforanannualamountexceedingEUR25,000;

• anypersonestablishedandregisteredforVATinanotherEUMemberStatewhocarriesoutdeliveriesofgoods, includingthedispatchortransport,topersonsnotregisteredforVATandestablishedordomiciledinLuxembourg,foranannualamountexceedingEUR100,000.

WhenisVATregistrationrequired?

VATregistrationmusttakeplace:• within15daysofthestartoftheactivityfortaxablepersonsthatarenot

exemptfromregistration;• beforethefirstdayofthemonthfollowingthemonthwherethetaxexemption

limitisexceeded(duringthesamecalendaryear);• fortaxablepersonsexemptfromregistrationandforlegalpersonsnotliable

forVAT,beforethefollowingoperationsarecarriedout:• provisionofservicesinanotherEUMemberStateforwhichonlythebuyeris

liableforVAT;• intra-CommunitypurchaseofgoodssubjecttoVATinLuxembourg;• purchase of services from providers established outside Luxembourg and

wherethebuyerisliableforVAT.Aretherepenaltiesfornotregisteringorlateregistration?

A penalty of between EUR 50 and EUR 5,000may be assessed for late VATregistration.Besides,absenceorlatepaymentoftheVATduemaygiverisetoanadditionalpenaltyamountingto10%oftheentireVATdue.ThispenaltyshallalsoapplytoanyotherinfringementofLuxembourgVATrequirements.Moreover,anypersonwhohasfraudulentlytriedtoavoidthepaymentofVATorhasillegitimatelyrecoveredVATispunishablebyapenaltyof10%ofthesumoftheevadedVAT.

IsvoluntaryVATregistrationpossibleforforeignentities?

No.

9internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

VAT representative.TaxablepersonsperformingimportsofgoodsinLuxembourgandsubsequentsales/processingwhichareneitherestablishednorregisteredforVATpurposesinLuxembourgmayappointaVATrepresentativeinLuxembourg.

VATregistrationisnotrequiredinthecaseofcertainsupplies.• Triangulation. If a business is an intermediate supplier to a Luxembourg

buyer of goods which it purchases from a business registered for VAT inanotherEUMemberStateandthegoodsaredelivereddirectlyfromtheretoLuxembourg,VATduecanbeaccountedforbytheLuxembourgcustomer.

• Reverse charge for services.ThesupplyofservicesbyaforeignsuppliertoaLuxembourgtaxablepersonthatfallsunderthereversechargemechanism.Assuch,therecipientofthesupplymustaccountforthetax.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

InordertoregisterforVAT,thetaxablepersonhastosubmitaninitialdeclarationoradeclarationofoption(ifregistrationisoptional)correspondingtohissituationtothecompetenttaxoffice.

Forlegalpersons(companies),theinitialdeclarationmustbeaccompaniedby:• acopyoftheconstitutionaldocumentsinFrenchorGerman;• a copyof the identity card (orpassport)of thepartnersappearing in the

constitutional documents and/or the business managers/directors of thecompany.

Fornaturalpersons,thedeclarationmustbeaccompaniedby:• acopyoftheidentitycard/passportofthetaxableperson.

HowfrequentlyareVATreturnstobesubmitted?

Each taxable personmust submit periodic returns with regard to the annualturnoverachievedoverthepreviousyear:• IftheturnoverisbelowEUR112,000,anannualreturnisrequired.• IftheturnoverisbetweenEUR112,000andEUR620,000,quarterlyreturns

andanannualreturnarerequired.• IftheturnoverishigherthanEUR620,000,monthlyreturnsandanannual

returnarerequired.

AllbusinesseswhicharerequiredtosubmitVATreturnsonamonthlyorquarterlybasismustsubmitanannualsummaryVATreturnaswell.Theduedatefortheperiodicreturnsisthe15thdayofthemonthfollowingtheendofthereturnperiod.Theduedatefortheannualreturnis1stMayofthefollowingyear.

Arethereanyotherreturnstobesubmitted?

• Intrastat Declarations

VATregisteredbusinesseswithavalueofdispatchesorarrivalstoorfromotherEUMemberStates,whichexceedathreshold(EUR150,000percalendaryearfor thedispatches, EUR200,000per calendar year for the acquisitions)mustcomplete Intrastat declarations each month. Separate reports are requiredfor intra-Community acquisitions (Intrastat Arrivals) and for intra-Communitysupplies(IntrastatDispatches).

• EU Sales Lists (ESL) for goods and/or services

Inprinciple,VATregisteredbusinessesperformingintra-CommunitysuppliesofgoodsmustsubmitanESLforgoodsonamonthlybasisbythe15thdayofthemonthfollowingtheendofthemonth.However,ESLsforgoodsmaybesubmittedquarterlyifthethresholdofEUR50,000ofintra-CommunitysuppliesofgoodstootherEUmemberstatesisnotexceededduringtheconcernedquarterorduringthe fourpreviousquarters.Foraquarterlyfiling, theESLs forgoodsmustbesubmittedbythe15thdayofthemonthfollowingtheconcernedquarter.

ESLs are also mandatory for the supply of services which are rendered byLuxembourgtaxablepersonstoVATregisteredbusinesscustomersestablishedinotherEUMemberStatesandwhicharenotVATexemptinthoseMemberStates.Thetaxablepersoncanmakesubmissionsonamonthlyorquarterlybasis(nothreshold).ThefrequencyforESLforservicesisnotlinkedtotheperiodforfilingESLforgoods.

OtherpointstobeconsideredforVATregistration?

Beforeregistering forVAT,businessesmusthaveopenedabankaccountoradirectdepositaccount(CCP)ataLuxembourgorforeignbank.

10internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

SPAINWhoisrequiredtoregisterforVAT?

1.BusinessorprofessionalwhodelivergoodsorprovideservicesorcarryoutintracommunityacquisitionssubjecttoVAT.

2.Businessrecipientofgoodsincaseofreversecharge.3.EntitiesnotnecessarybusinessorprofessionalthatcarryoutintracommunityacquisitionssubjecttoVAT.

WhenisVATregistrationrequired?

Within30daysofthedatefromwhichtheactivitystarts.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes,sanctionscanbeimposed.

IsvoluntaryVATregistrationpossibleforforeignentities?

No,itiscompulsory.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

No.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

1.Spanishindividuals:• DNIcopy(identitycard).• Abroadresident:-Passportcopy.-Documentthatjustifyabroadresidence.

2.Foreignerindividuals:• NIEcopy(identitynumberofforeignercard).

3.Entitiesorcompanies• Incorporationpublicdeed.• Legalstatutesorequivalentdocument.• Certificateofinscriptioninapublicregister.

4.-Iftheapplicationisthroughalegalrepresentant:• NIFoftherepresentant.• Justificationoftherepresentationdulysworntranslatedandapostilled.

HowfrequentlyareVATreturnstobesubmitted?

• Quarterly303return:(April,July,OctoberandJanuary).• Monthly 303 return: compulsory for companieswhich turnover exceeds 6

millionEurosandcompaniessubjectedtothespecialregime(REDEME)thatallowstotheentitiesregisteredinittoperceivetheVATrefundsmonthly.

• Yearly390return:summarize

11internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

THENETHERLANDSWhoisrequiredtoregisterforVAT?

EverybodythatperformsVATtaxableactivities(import,export,supplyofgoodsorservices)intheNetherlandsorisdeemedtoperformtheseactivitiesintheNetherlands.

WhenisVATregistrationrequired?

• ForDutchresidents,immediatelyuponincorporationorstartofanenterprise.• For permanent establishments, upon the start of the business in the

Netherlands.• ForcompaniesinEUcountriesthatsellgoodstoDutchcustomers(individuals),

whenathresholdof€100,000inayearisexceededforthefirsttime.• InallothercasesassoonasthefirstVATtaxablehasbeenperformed.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes

IsvoluntaryVATregistrationpossibleforforeignentities?

Yes,forcompaniesfromnonEUcountrieswhowanttoreclaiminputVAT.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

IfVATiscorrectlychargedinreversetoaDutchcompany,aforeigncompanydoesnothavetoregisterintheNetherlands

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

• Copyofapassport(incaseofindividuals)• Copyofthearticlesofincorporation(inDutch,GermanorEnglish)• Atranslationofthearticlesofincorporationincaseofotherlanguages;no

apostillerequired• Completedregistrationform

Inadditionforforeigncompanieswithoutapermanentestablishment:• DeclarationofforeigntaxauthoritiesthatthecompanyisregisteredforVAT

purposes

HowfrequentlyareVATreturnstobesubmitted?

VATreturnsneedtobefiledonaquarterlybasis.Onecanchoosetofileonamonthlybasis,forinstanceiftheinputVATregularlyexceedstheVATpayable.

Arethereanyotherreturnstobesubmitted?

• DeclarationsofIntraCommunitysuppliesmayneedtobefiled.• Intrastatreturnsmayneedtobefiled,ifthethresholdof€900,000ineither

importorexportisexceeded.• Ifapermanentestablishment isrecognized intheNetherlands,an income

taxreturnhastobefiled.• Incaseofimporting,acustomsdeclarationmayberequired

12internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

VENEZUELAWhoisrequiredtoregisterforVAT?

Thosewhosellgoodsinthecountry;importers;independentprovidersofservicesperformedorusedinthecountry;exportersofgoods;andserviceexportersarerequiredtodeclaretheVAT,butdoesnotexistaVATregistry.ThereisjusttheRegisterTaxInformation(RIF).

WhenisVATregistrationrequired?

Statementsshallbesubmittedmonthly.Inthecaseofspecialtaxpayers(thoserankedbytheTaxAdministration)mustfulfillatimetable.

Aretherepenaltiesfornotregisteringorlateregistration?

Maximum200U.T.=Bs.34.000,00=US$5.400,00

IsvoluntaryVATregistrationpossibleforforeignentities?

Shall register in theRegisterTax Information (RIF),not residentordomiciledin the Bolivarian Republic of Venezuela entities, which have no permanentestablishmentorfixedbasewhenconductingeconomicactivitiesinthecountryorholdingsensitivegoodstobetaxedinVenezuela.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

Notparticularly,butfortheRIF,theregistrationprocessissimple.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Documents: The charter of organization, translated into Spanish by publicinterpreter,andwiththeHagueApostille.Copiesofpassportsoftheshareholders(allthepages).

HowfrequentlyareVATreturnstobesubmitted?

Monthly

Arethereanyotherreturnstobesubmitted?

Theincometax(ISLR)

13internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

GERMANYWhoisrequiredtoregisterforVAT?

Germanentities• All German entities, except for non-taxable legal entities and small

entrepreneurs(totalofsupplies in thepreviousyearnotexceeded17,500EURandinthecurrentyearpresumablynotexceeding50,000EUR)

• Exemptionof theexemption: If theseentitiesacquiredgoods inotherEUMemberStates(withtransporttoGermany)intheprecedingyearinexcessof12,500EURor if thisamountwillbeexceededduringthecurrentyear,registrationisrequiredandVATreturnmustbesubmitted.

Non-Germanentities• SameregistrationrulesasforGermanentities,• buttheexemptionforsmallentrepreneursdoesnotapplyfornon-resident

taxpayers.• Registration becomes mandatory, if a foreign business sells and delivers

goodstonon-registeredcustomersinGermany,andthevalueofthosegoodsexceedsathresholdof100,000EURintheprecedingorcurrentyear

WhenisVATregistrationrequired?

Thereisnodeadlineforregistration,butpromptnessshouldbeconsidered.

Aretherepenaltiesfornotregisteringorlateregistration?

TherearenopenaltiesforfailingtoregisterforVATintime.Ontheotherhandlatepayment(1%ofoutstandingVATmultipliedbythemonthsoverdue)orlatefiling(upto10%ofthenetVATliability,butnomorethan25,000EUR)mayleadtopenaltiesandinterestonoutstandingVAT.Repeateddelaysinfilingandpaymentaretreatedasfiscalfraud.

IsvoluntaryVATregistrationpossibleforforeignentities?

ThereisnoconceptofvoluntaryregistrationinGermanVATlaw.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

• Reversechargeservices• TriangulationwithanEU-memberasanintermediatesuppliertoaGerman

purchaser, and the goods are carried from another EU Member State toGermany.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

• Articleofassociation• Questionnaire for fiscal registration (includes information, such as: bank

details, estimated fee income, legal status of the company, place ofregistration,fulladdressoftheheadoffice)

• Associate(s)withaddress• DocumentsneedtobefilledinGermanorEnglish.• TranslationwithapostilleaccordingtoHagueConventionisnotnecessary.

HowfrequentlyareVATreturnstobesubmitted?

• Newbusinessmonthly(fortwoyearsmaximum)• Annual,ifthetaxliabilityforthepriorcalendaryeardidnotexceed1,000EUR• Quarterly,ifthetaxliabilityforthepriorcalendaryeardidnotexceed7,500EUR• Monthlyinallothercases

Arethereanyotherreturnstobesubmitted?

• EuropeanSales List (ESL)also statingany intermediate suppliers sales incontextofintra-CommunitytradeaswellasanytaxablesuppliesofservicesexecutedinotherEUMemberStates,iftheB2Bruleisapplicable.

• IntrastatSupplementaryDeclarationswithavalueofdispatchesordeliveriestoorfromotherEUMemberStates,whichexceed500,000EURpercalendaryear:monthlyrequired

OtherpointstobeconsideredforVATregistration?

VATreturnsandotherdeclarationshavetobetransmittedelectronically.

14internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

ROMANIAWhoisrequiredtoregisterforVAT?

Allentitieslocal&foreignwithtaxableactivities

WhenisVATregistrationrequired?

Whenthresholdexceed€65000

Aretherepenaltiesfornotregisteringorlateregistration?

Yes, approx. 120 Euro for delay of each tax declaration+interest for delayedpayments

IsvoluntaryVATregistrationpossibleforforeignentities?

Yes

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

No

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

vatregistrationformsignedoriginallybydirectorsorsecretaryIncorporationcertificateShareholders&directorsCertificateRegisteredofficecertificateAgreement

HowfrequentlyareVATreturnstobesubmitted?

VATreturnsarequarterlysubmittediftheturnoverislessthan100.000Euroandnointra-communityacquisitionsofgoods;otherwise,monthlyVATreturns

Arethereanyotherreturnstobesubmitted?

Vies&intrastatforarrival&despatchgoodswithineusubmittedmonthly

SERBIAWhoisrequiredtoregisterforVAT?

Ataxpayerwhointhepast12monthshasatotalturnoverinexcessof8,000,000dinars

WhenisVATregistrationrequired?

Nolaterthantheexpiryofthefirstdeadlineforthesubmissionofperiodictaxreturn

Aretherepenaltiesfornotregisteringorlateregistration?

Yes,penaltiesforlateregistrationarefrom100,000to1milliondinars

IsvoluntaryVATregistrationpossibleforforeignentities?

VoluntaryVATregistrationispossibleonlyforregisteredforeignentitiesundersamerulesthatapplytodomesticentities.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

No

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Forall:registrationformEPPDVForturnoverabove8mil-documentwhichclearlycandeterminetheamountoftherealizedtotalturnoverinthepreceding12monthsFornewentities:copyofdecisiononregistrationintheRegisterofCompanies

HowfrequentlyareVATreturnstobesubmitted?

DeadlinesforsubmittingVATtaxformsinSerbiaaremonthlyandquarterly.Fornewtaxpayerstaxperiodinfirsttwoyearsisonemonth.Changetoquarterlytaxperiodispossibleafterthatperiod.Taxpayerswithmorethan50milrsdturnoverinlast/following12monthsalsosubmittaxreturnformsmonthly.

Arethereanyotherreturnstobesubmitted?

ExceptobligationtosubmitIEPDVformforchangeofimportantdata(nameofcompany,address,phonenumber,activitycodeetc)therearenootherobligationfortaxreturn.Still,insomecases(i.e.“mostlyexporters”etc)somesupplementaryformscanbeneeded.

15internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

UKWhoisrequiredtoregisterforVAT?

Anyentitywhohas(orintendstohave)trading/taxableactivity.

WhenisVATregistrationrequired?

WheretaxablesuppliesmadeexceedthecurrentVATregistrationthresholdof£81,000forbusinessestablishedintheUK.Distanceselling–oncesalesexceed£70,000Acquisitions–oncevalueexceedscurrentthreshold,£81,000Reversecharge–oncevalueexceedscurrentthreshold£81,000Fornon-UKestablishedbusinessassoonastradingstartsintheUK.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes,apenaltyisimposedforlateregistration.Thisisagradedpenaltyappliedtothenetliabilitydueatthedateofregistration(calculatedfromwhenregistrationwasrequired)andisasfollows:Upto9monthslate–5%9-18months–10%Over18months–15%

IsvoluntaryVATregistrationpossibleforforeignentities?

IfnotestablishedintheUKcompulsoryregistrationisrequiredassoonastradingactivityintheUKstarts.Thiswasarulechangeboughtintoeffectfrom01/12/12.If established in the UK compulsory registration once threshold exceeded.VoluntaryregistrationavailableiftaxablesuppliesarebeingmadeoranintentiontomaketaxablesuppliesintheUK.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

Yesforgoodsandservices:a)GoodsTriangulationwhereintermediaryisEUbased&issupplyingUKcustomerwithgoodsfromEUsupplier.Calloffstock–UKcustomercontrolsstockforthemselvesfromEUsupplierandtreatsasacquisition.Supply&Install–EUVATregisteredsupplierwhoisnototherwiserequiredtoberegisteredforVATintheUK.UKcustomertreatsasanacquisition.b)ServicesPlaceofsupply–extensiontoreversechargeforserviceswherethePOSistheUKielandrelatedtransactions.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

OtherdocumentationisnotrequiredtobesubmittedwithanapplicationhoweverHMRCmayrequestfurtherinformationaspartoftheregistrationprocess.Adetailedapplicationisrequiredwhichrequeststhefollowing:CompanyinformationAuthorisedsignatorypersonaldetailsUKbusinessbankdetailsBusinesscontact/addressdetailsTradingactivitydescriptionDetailofrelatedUKbusiness/VATregisteredentitiesEstimatedfeeincomeandEUtradingfigures.

HowfrequentlyareVATreturnstobesubmitted?

Usually quarterly. If in a regular repaymentpositionmonthly returns canberequested.Annualaccountingisavailableforthosewithaturnoverbelow£1,350,000.Thisallowsthesubmissionofanannualreturn(10paymentsaremadeonaccountthroughouttheyear).

Arethereanyotherreturnstobesubmitted?

ECSaleslistsforgoodsandservicesIntrastatSupplementaryDeclarations

OtherpointstobeconsideredforVATregistration?

VATreturnsarerequiredtobesubmittedonlinethroughHMRC’swebsite. Anonlineaccountisrequiredtobesetup.AtaxrepresentativeisabletosetuptheaccountandsubmitreturnsontheVATregisteredentitiesbehalfiftheywish.

16internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

SINGAPOREWhoisrequiredtoregisterforVAT?

• Businesseswhosetaxableturnoverforthepast4quartersexceed$1milperyear;

• Businessesthatintendtomaketaxablesuppliesandcanresonablyexpecttheirtaxableturnovertobemorethan$1milinthenextyear(12months)

WhenisVATregistrationrequired?

Within30daysofthedatefromwhichregistrationliabilityarises

Aretherepenaltiesfornotregisteringorlateregistration?

Yes.Thebusinesswouldbeliabletoafineofupto$10,000andapenaltyequalto10%ofthetaxduefromthedateonwhichthebusinessisrequiredtoapplyforGSTregistration

IsvoluntaryVATregistrationpossibleforforeignentities?

An overseas entity is one that is not a resident in Singapore and/or does not have an established place of business in Singapore.

Yes.ForeignentitiesmaychoosetoregisterforGSTvoluntarilysoastoclaimGSTpaidonimports.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

AnyemployeesorthirdpartieswhohasbeendulyauthorisedtouseotherIRASe-ServicescanapplyforGSTregistrationonlineviamyTaxPortal.Processingofapplicationtakes2workingdays.ForeignentitiesmayappointaGST-registeredSingaporeagentwhowill importandsupplygoodsontheirbehalf.Thisagentisresponsibleforthegoodsasifheistheprincipal.Hewill importgoodsintoSingapore inhisname.Subsequentsupplyof thegoodswillbetreatedashistaxablesupplies.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Documentstobesubmittedaccordingtothetypeofbusiness.

Online-myTaxPortal

Paperform

HowfrequentlyareVATreturnstobesubmitted?

Monthly/Quarterly/HalfYearly

Arethereanyotherreturnstobesubmitted?

No.

OtherpointstobeconsideredforVATregistration?

• Sole-Proprietor/ Partner/ Director/ Trustee of a business is required tocompletethee-learningcourse“GST-BeforeIRegister”anditsquizbeforeapplyingforvoluntaryregistration

• Youmaybe required toprovideasecuritydepositwhenapplying forGSTregistration

17internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

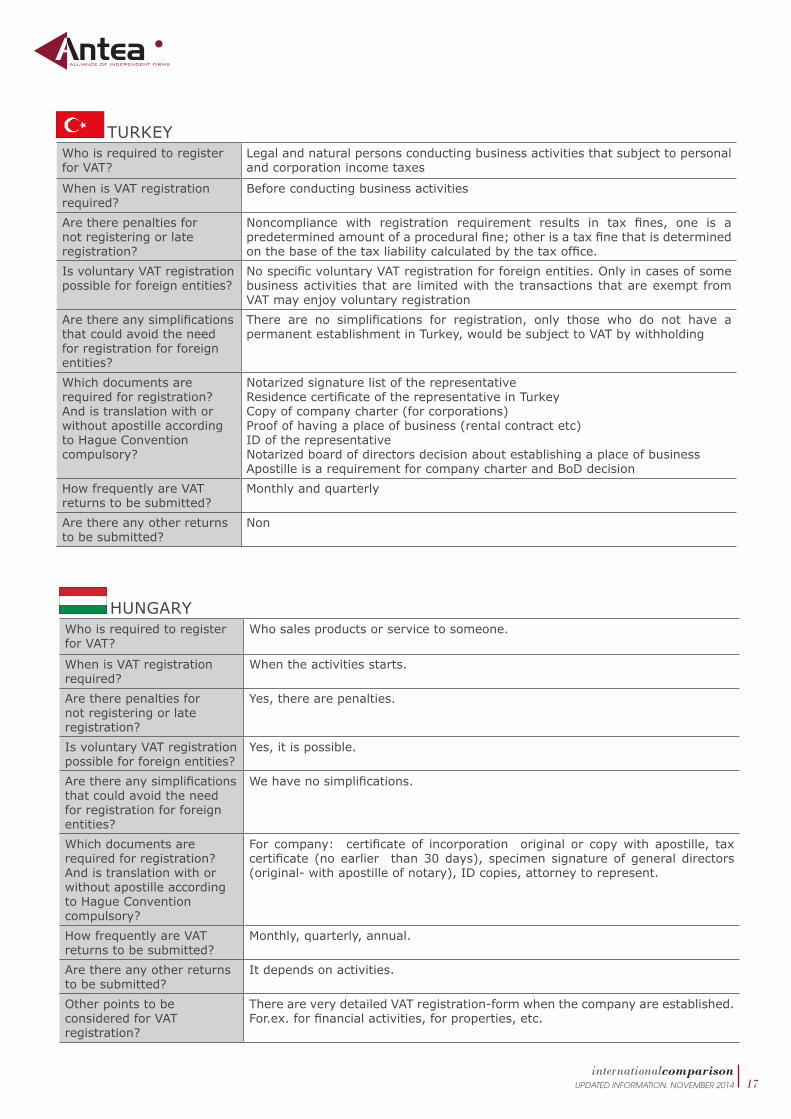

TURKEYWhoisrequiredtoregisterforVAT?

Legalandnaturalpersonsconductingbusinessactivitiesthatsubjecttopersonalandcorporationincometaxes

WhenisVATregistrationrequired?

Beforeconductingbusinessactivities

Aretherepenaltiesfornotregisteringorlateregistration?

Noncompliance with registration requirement results in tax fines, one is apredeterminedamountofaproceduralfine;otherisataxfinethatisdeterminedonthebaseofthetaxliabilitycalculatedbythetaxoffice.

IsvoluntaryVATregistrationpossibleforforeignentities?

NospecificvoluntaryVATregistrationforforeignentities.Onlyincasesofsomebusinessactivitiesthatare limitedwiththetransactionsthatareexemptfromVATmayenjoyvoluntaryregistration

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

There are no simplifications for registration, only those who do not have apermanentestablishmentinTurkey,wouldbesubjecttoVATbywithholding

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

NotarizedsignaturelistoftherepresentativeResidencecertificateoftherepresentativeinTurkeyCopyofcompanycharter(forcorporations)Proofofhavingaplaceofbusiness(rentalcontractetc)IDoftherepresentativeNotarizedboardofdirectorsdecisionaboutestablishingaplaceofbusinessApostilleisarequirementforcompanycharterandBoDdecision

HowfrequentlyareVATreturnstobesubmitted?

Monthlyandquarterly

Arethereanyotherreturnstobesubmitted?

Non

HUNGARYWhoisrequiredtoregisterforVAT?

Whosalesproductsorservicetosomeone.

WhenisVATregistrationrequired?

Whentheactivitiesstarts.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes,therearepenalties.

IsvoluntaryVATregistrationpossibleforforeignentities?

Yes,itispossible.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

Wehavenosimplifications.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

For company: certificateof incorporation original or copywith apostille, taxcertificate (noearlier than30days), specimensignatureofgeneraldirectors(original-withapostilleofnotary),IDcopies,attorneytorepresent.

HowfrequentlyareVATreturnstobesubmitted?

Monthly,quarterly,annual.

Arethereanyotherreturnstobesubmitted?

Itdependsonactivities.

OtherpointstobeconsideredforVATregistration?

ThereareverydetailedVATregistration-formwhenthecompanyareestablished.For.ex.forfinancialactivities,forproperties,etc.

18internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

AUSTRALIAWhoisrequiredtoregisterforVAT?

Youarerequiredtoregisterifyou:• runabusinessorenterprise(s9-20oftheGSTAct1999);and• yourcurrentorprojectedGSTTurnover(s188-15)is$75,000ormore(the

notforprofitorganizationthresholdis$150,000ormore).

Youmustalsoregister(regardlessofturnover)ifyouwishtoclaimfueltaxcreditsorprovidetaxitravel.

WhenisVATregistrationrequired?

Youneedtoregister ifyourturnoverexceedsthethresholdoryoureasonablyexpect it too. You are required to register within 21 days after reaching thethreshold.

Aretherepenaltiesfornotregisteringorlateregistration?

FailuretoregisterforGSTcanincurapenaltyof20penaltyunits.Currentvalueofpenaltyunitsasdefinedbysection4AAoftheCrimesAct1914.Currentlythepenaltyis$3,400.IfanyGSTispayabletheAustralianTaxationOffice(ATO)mayimposefurtherpenaltiesandinterestchargesinaccordancewiththelengthoftheperiodofnon/latepayment.

IsvoluntaryVATregistrationpossibleforforeignentities?

VoluntaryregistrationcanbeelectedbyanyentitycarryingonanenterpriseandmakingsaleofgoodsorservicesthatareconnectedwithAustralia,whetherinoroutsideofAustralia.

IfyouregisterforGSTyouarealsorequiredtopayGSTonyourtaxablesales.Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

IfyouarecarryingonanenterpriseandmakingsaleofgoodsorservicesthatareconnectedwithAustraliaandyoumeetthepreviouslymentionedcriteriayoumustregisterforGST.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

YoucanregisterforGSTby:• callingthe(ATO);• completingtheapplicablepaperform;or• onlineifyouhaveaBusinessportalaccountwithanAdministratorAUSkey.

YoucanalsoaskaregisteredtaxagentorBASagenttoundertakeyourregistration.

Thepaperformsrequireddependontheentitytype:• ABNregistrationforindividuals(soletraders)(NAT2938)• ABNregistrationforcompanies,partnerships,trustandotherorganisations

(NAT2939)• Addanewbusinessaccount(NAT2954)

Non-residentsarerequiredtoprovideevidenceof:• Identity;and• Carryingontheenterpriseforwhichtheyareseekingregistration.

Thefollowinglinkprovidesfurtherdetailofthedocumentationrequired-https://www.ato.gov.au/Business/International-tax-for-businesses/Indetail/Doing-business-in-Australia/Proof-of-identity---for-individualsand-businesses-resident-outside-Australia/

DocumentsmustbeinEnglishortranslatedintoEnglish.Thetranslationmustbecertifiedastrueandcorrectbyanauthorisedtranslationservice.

19internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

HowfrequentlyareVATreturnstobesubmitted?

LodgmentfrequencyvariesdependinguponGSTturnoverandotherrequirementsasdeterminedbytheATO(e.g.thoseparticipatinginadeferredGSTscheme)asfollows:

Monthly–GSTturnover>$20million

Quarterly–GSTturnover<$20million

Annually– Ifyouvoluntarily registerandyouhavenoelected topaybyGSTinstallments

Anentitymayelecttoreportonamorefrequentbasisbuttheycannotelecttoreducethefrequencyoftheirlodgments.

Arethereanyotherreturnstobesubmitted?

No.

COLOMBIAWhoisrequiredtoregisterforVAT?

All those individualsorcorporationsbelonging to thecommontaxsystemareobligatedtoenrollintheSingleTaxRegistry(RUT)wheretheywillbeassignedtheobligationtobill,recover,collect,reportandpayVATtotheNationalTaxandCustomsDirection(DIAN).

WhenisVATregistrationrequired?

Theregistrationisrequiredwhenindividualsorcorporationsmeettherequirementsforinvoicing,andareengagedinsellingtangiblegoodsorservices,andalsoallthoseengagedinexports,importsorcustoms.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes,theyareofeconomicnature,aswellastheclosureofestablishments,officesorclinics.

IsvoluntaryVATregistrationpossibleforforeignentities?

Branches, or foreign entities established in the country to develop operationsmustenrolltoavoidsanctions.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

If the foreign companyhasno operations in the country it is not required toregister

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

TocomplywithallformaldutiesforthecreationofacompanybeforeaChamberofCommerce,anditsrequirementsareasfollows:• SingleTaxRegistry(RUT)• To process the Unique Business Registration (RUE) in the commercial

registrationoftheChamberofCommerce• CommercialRegister• Contractorunilateralactthatconsistofaprivatedocument• Openingofbankaccounts• Draftingbylawsandsigningofarticlesofincorporation

HowfrequentlyareVATreturnstobesubmitted?

• If the companybeganoperations in the samefiscal year it is required todeclareandfileVATbimonthly.

• Startingon thesecondyear,andbasedongross revenues itwouldbeas

follows:

• Files annually with advances every four months, if income is below15,000TaxValueUnits(UVT)

• Files every fourmonths, if income is above 15,000UVT and below92,000UVT

• Fileseverytwomonthswhenincomeisabove92,000UVT• UVT is a Taxable Unit that changes every year. UVT 2014: 1 UVT =

27.485COP

20internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

URUGUAYWhoisrequiredtoregisterforVAT?

Alltaxpayers(companies, individualsprovidersofpersonalservices,etc),arerequiredtoregisterandpaythebalanceresultingfromthesettlementofVAT.

WhenisVATregistrationrequired?

AtthebeginningofthetaxableactivitiesbyVAT.

Aretherepenaltiesfornotregisteringorlateregistration?

Yes,therearelateforlateregistration.

IsvoluntaryVATregistrationpossibleforforeignentities?

Yes,foreignentitiescanregistervoluntarily.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

Iftheforeignentityistaxpayer,thereisnosimplification.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Alldocumentswhichbackuptheformationoftheentityanditisrepresentativesarerequired.

HowfrequentlyareVATreturnstobesubmitted?

VATreturnsarepresentedonceayearoreverymonth,dependingonthetaxpayer.

Arethereanyotherreturnstobesubmitted?

Intheorytherearenotothers.

OtherpointstobeconsideredforVATregistration?

Exceptinspecialcases,noother

Arethereanyotherreturnstobesubmitted?

For the sales tax there is only adeclarationofVAT, and it has threeperiodicpresentationsasalreadystatedinthepreviousitem.

ArethereotherpointstobeconsideredforVATregistration?

Besidesthosementionedaboveitmustbetakenintoaccount,thatthecompanybecomesaVATwithholdingagentforpeopleofthesimplifiedregime.

21internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

CYPRUSWhoisrequiredtoregisterforVAT?

Allentitieslocal&foreignwithtaxableactivities

WhenisVATregistrationrequired?

Whenthresholdexceed€15600

Aretherepenaltiesfornotregisteringorlateregistration?

Yes€85permonth

IsvoluntaryVATregistrationpossibleforforeignentities?

Yes

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

No

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

vatregistrationformsignedoriginallybydirectorsorsecretaryIncorporationcertificateShareholders&directorsCertificateRegisteredofficecertificateAgreement

HowfrequentlyareVATreturnstobesubmitted?

VATreturnsarequarterlysubmitted

Arethereanyotherreturnstobesubmitted?

Vies&intrastatforarrival&despatchgoodswithineusubmittedmonthly

OtherpointstobeconsideredforVATregistration?

N/A

22internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

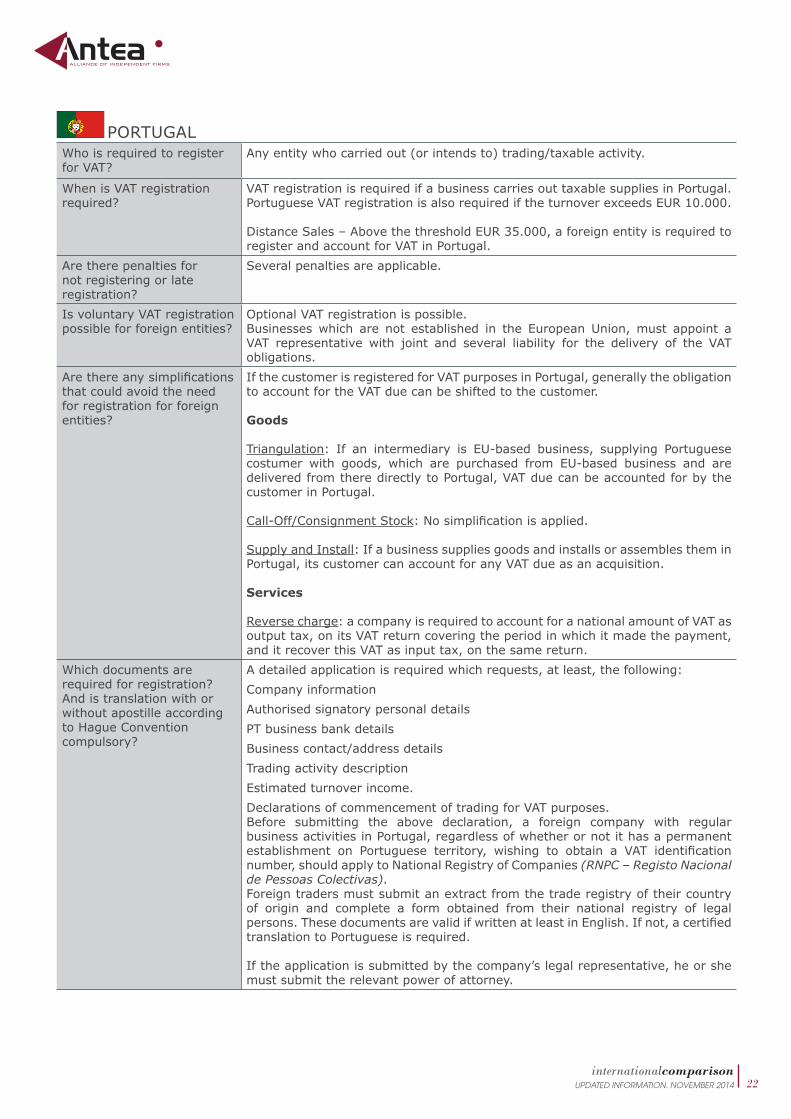

PORTUGALWhoisrequiredtoregisterforVAT?

Anyentitywhocarriedout(orintendsto)trading/taxableactivity.

WhenisVATregistrationrequired?

VATregistrationisrequiredifabusinesscarriesouttaxablesuppliesinPortugal.PortugueseVATregistrationisalsorequirediftheturnoverexceedsEUR10.000.

DistanceSales–AbovethethresholdEUR35.000,aforeignentityisrequiredtoregisterandaccountforVATinPortugal.

Aretherepenaltiesfornotregisteringorlateregistration?

Severalpenaltiesareapplicable.

IsvoluntaryVATregistrationpossibleforforeignentities?

OptionalVATregistrationispossible.Businesseswhich are not established in the EuropeanUnion,must appoint aVAT representative with joint and several liability for the delivery of the VATobligations.

Arethereanysimplificationsthatcouldavoidtheneedforregistrationforforeignentities?

IfthecustomerisregisteredforVATpurposesinPortugal,generallytheobligationtoaccountfortheVATduecanbeshiftedtothecustomer.

Goods

Triangulation: If an intermediary is EU-based business, supplying Portuguesecostumer with goods, which are purchased from EU-based business and aredeliveredfromtheredirectlytoPortugal,VATduecanbeaccountedforbythecustomerinPortugal.

Call-Off/ConsignmentStock:Nosimplificationisapplied.

SupplyandInstall:IfabusinesssuppliesgoodsandinstallsorassemblestheminPortugal,itscustomercanaccountforanyVATdueasanacquisition.

Services

Reversecharge:acompanyisrequiredtoaccountforanationalamountofVATasoutputtax,onitsVATreturncoveringtheperiodinwhichitmadethepayment,anditrecoverthisVATasinputtax,onthesamereturn.

Whichdocumentsarerequiredforregistration?AndistranslationwithorwithoutapostilleaccordingtoHagueConventioncompulsory?

Adetailedapplicationisrequiredwhichrequests,atleast,thefollowing:CompanyinformationAuthorisedsignatorypersonaldetailsPTbusinessbankdetailsBusinesscontact/addressdetailsTradingactivitydescriptionEstimatedturnoverincome.DeclarationsofcommencementoftradingforVATpurposes.Before submitting the above declaration, a foreign company with regularbusinessactivitiesinPortugal,regardlessofwhetherornotithasapermanentestablishment on Portuguese territory, wishing to obtain a VAT identificationnumber,shouldapplytoNationalRegistryofCompanies(RNPC – Registo Nacional de Pessoas Colectivas).Foreigntradersmustsubmitanextractfromthetraderegistryoftheircountryof origin and complete a form obtained from their national registry of legalpersons.ThesedocumentsarevalidifwrittenatleastinEnglish.Ifnot,acertifiedtranslationtoPortugueseisrequired.

Iftheapplicationissubmittedbythecompany’slegalrepresentative,heorshemustsubmittherelevantpowerofattorney.

23internationalcomparison

UPDATED INFORMATION. NOVEMBER 2014

HowfrequentlyareVATreturnstobesubmitted?

UsuallybusinessesarerequiredtosubmitVATreturnsonamonthlybasis.

IftheestimatedannualturnoverislowerthanEUR650,000,ataxableentitymayopttosubmitquarterlyVATreturns.

AnannualsummaryVATreturnshallbealsosubmittedandanannuallistingofnationalclientsandsupplierswithwhichthetotaltransactionsintheyearexceedEUR25.000.

Arethereanyotherreturnstobesubmitted?

EuropeanSalesList–recapitulativestatements:onamonthlyorquarterlybasis.

DeclarationonSuppliesinAutonomousRegions-MadeiraandAzores:MainlandVAT registered tax payerswho supply goods and/or serviceswithin the fiscalboundariesofMadeiraandAzoresmustdeclaretheseonaseparatereturntobeattachedtotheordinaryperiodicVATreturn.

IntrastatSupplementaryDeclarationsOtherpointstobeconsideredforVATregistration?

VATreturnsarerequiredtobesubmittedonlinethroughTaxAuthority’swebsite.Anonlineaccountisrequiredtobesetup.Ataxrepresentativeorthecharteredaccountant(internaloroutsourcing)isabletosetuptheaccountandsubmitreturnsontheVATregisteredentitiesbehalfiftheywish.

ANDORRAARGENTINEAUSTRALIA

AUSTRIABOLIVIABRAZIL

BULGARIACOLOMBIA

COSTA RICACYPRUSCHILECHINA

ECUADOREGYPT

EL SALVADORFRANCE

GERMANYGREECE

GUATEMALAHONDURASHUNGARY

INDIAISRAELITALY

LUXEMBOURGMALTA

MEXICOMOROCCO

THE NETHERLANDSPAKISTAN

PERUPOLAND

PORTUGALREPUBLIC OF SINGAPORE

ROMANIASERBIASPAIN

SWITZERLANDTUNISIATURKEY

UAEUNITED KINGDOM

URUGUAYUSA

VENEZUELA