Internal audit strategy for non-profits

41

Internal Audit Strategy and Risk Approach for Not for Profit Organizations A practical model Debashis Gupta India April 2, 2015 Debashis Gupta

-

Upload

debashis-gupta -

Category

Documents

-

view

52 -

download

0

Transcript of Internal audit strategy for non-profits

Internal Audit Strategy and Risk Approachfor Not for Profit OrganizationsA practical model

Debashis GuptaIndia

April 2, 2015Debashis Gupta

Discussion Points

Internal Audit Context Conceptual framework Model Resourcing Process Risk

Debashis Gupta

Internal Audit

Context & challenges

Debashis Gupta

Context

1. Wide geographical distribution of project/program sites/units

2. Range of programs/themes – research, publication, participatory action research, community capacity building…

3. Range of program delivery mechanisms4. Range of network, collaborations and

funding mechanisms, with associated stakeholder demands

5. Volunteers, partners (with/without formalized arrangements)Debashis Gupta

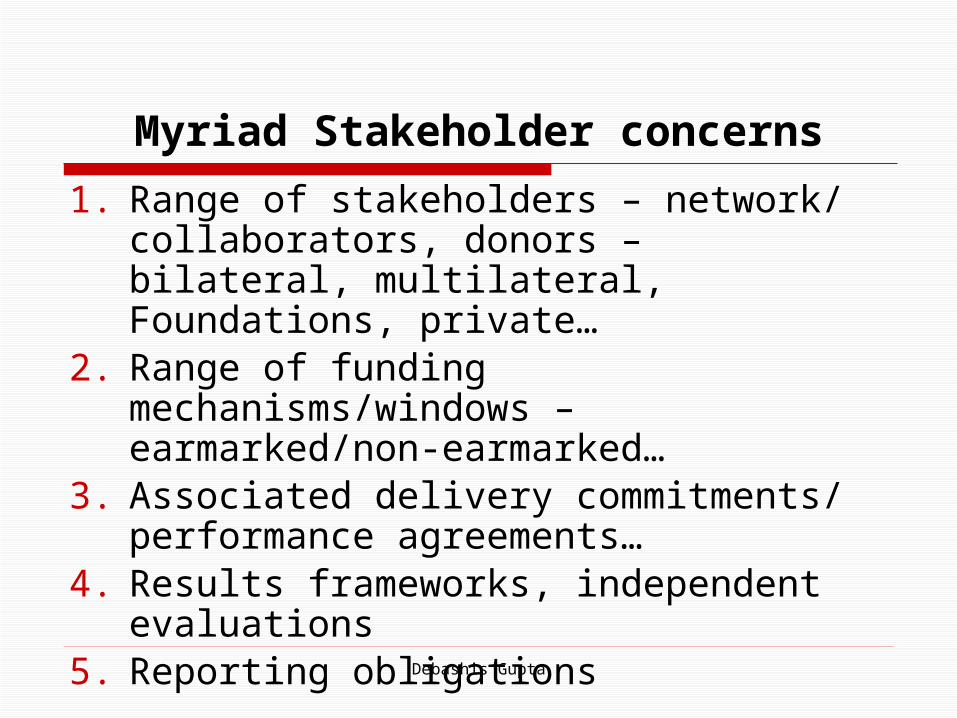

Myriad Stakeholder concerns

1. Range of stakeholders – network/ collaborators, donors – bilateral, multilateral, Foundations, private…

2. Range of funding mechanisms/windows – earmarked/non-earmarked…

3. Associated delivery commitments/ performance agreements…

4. Results frameworks, independent evaluations

5. Reporting obligations

Debashis Gupta

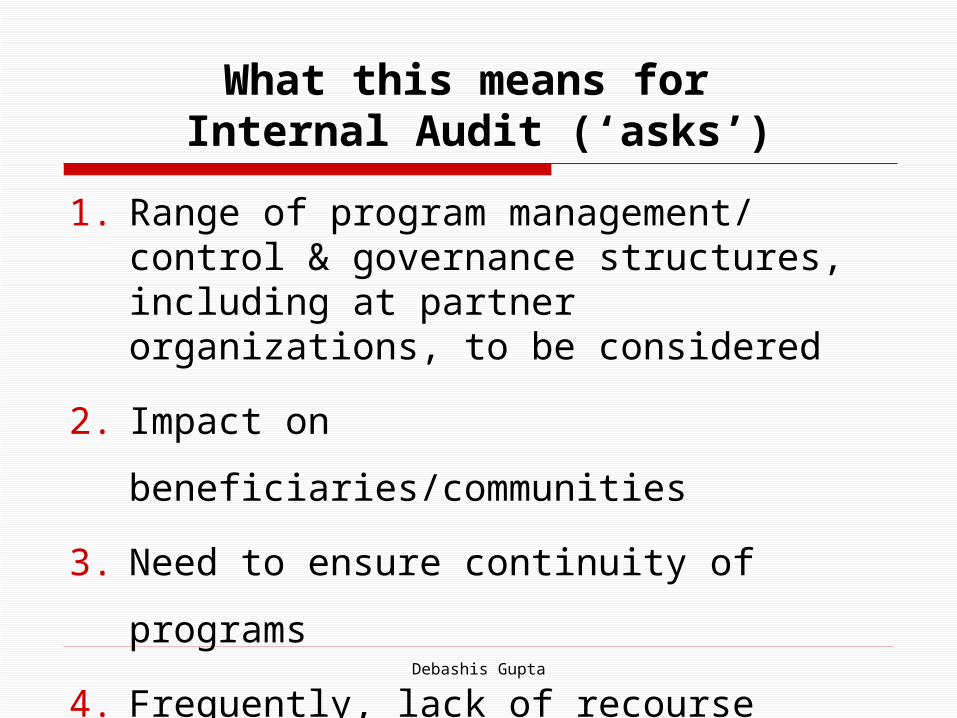

What this means for Internal Audit (‘asks’)

1. Range of program management/ control & governance structures, including at partner organizations, to be considered

2. Impact on beneficiaries/communities

3. Need to ensure continuity of programs

4. Frequently, lack of recourse

(legal/other) e.g. reg. volunteers

Debashis Gupta

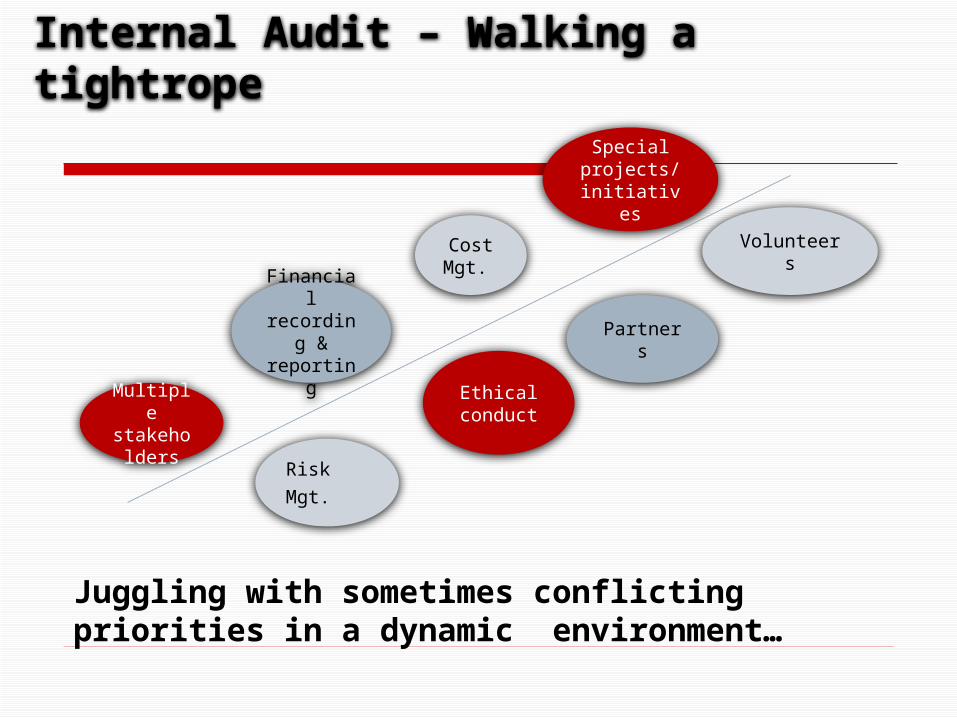

Internal Audit – Walking a tightrope

Multiple stakehol

ders

Financial recording

& reporting

Cost Mgt.

Special projects/ initiatives

Risk

Mgt.

Ethical conduct

Partners

Volunteers

Juggling with sometimes conflicting priorities in a dynamic environment…

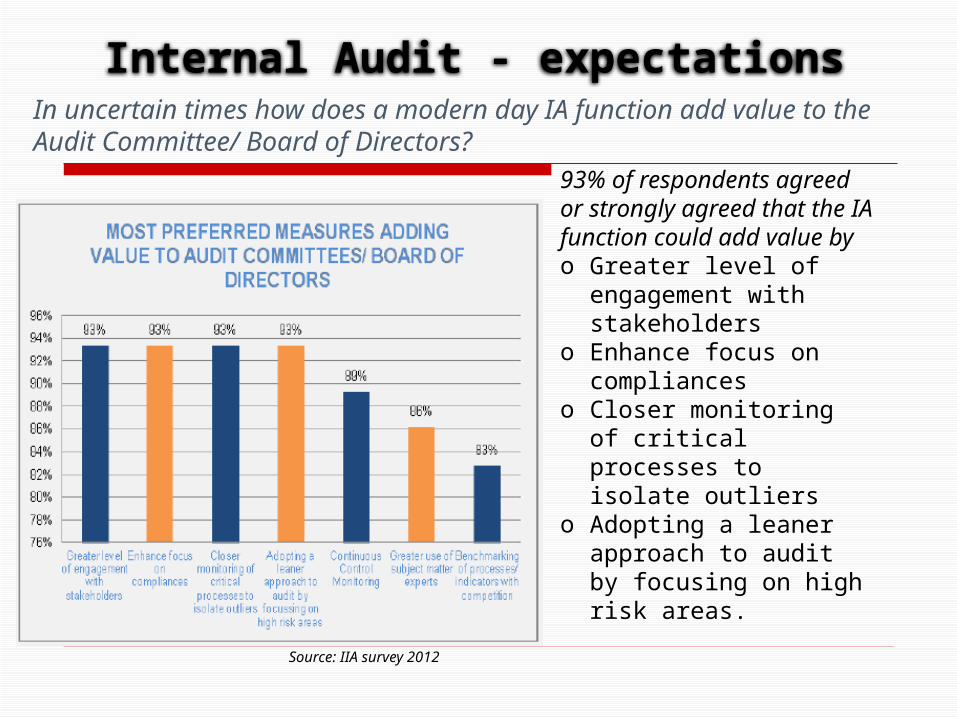

Internal Audit - expectationsIn uncertain times how does a modern day IA function add value to the Audit Committee/ Board of Directors?

93% of respondents agreed or strongly agreed that the IA function could add value by o Greater level of

engagement with stakeholders

o Enhance focus on compliances

o Closer monitoring of critical processes to isolate outliers

o Adopting a leaner approach to audit by focusing on high risk areas.

Source: IIA survey 2012

How Internal Audit copes (response)

1. Put beneficiaries/communities first2. Substance over form 3. Intent & transparency vs. procedure4. Assurance strategy – convergence/

synergies (IA, Monitoring, Evaluation,…)5. Capacity building (consulting role)

Debashis Gupta

Internal Audit

Conceptual Framework/s

Debashis Gupta

Internal Control & Governance Frameworks & models

1. COSO Internal Control Framework (now COSO 2013 ver.) – endorsed for SoX

2. CoCo (Canada)3. Continuous Control Monitoring (CCM) &

Continuous Audit (CA) models/systems4. Risk Management & Governance f/ws:

ISO:31000 Kings (IOD SA) COSO ERM Cadbury 3 Lines of Defence

Debashis Gupta

Internal Audit

A Practical Model

Debashis Gupta

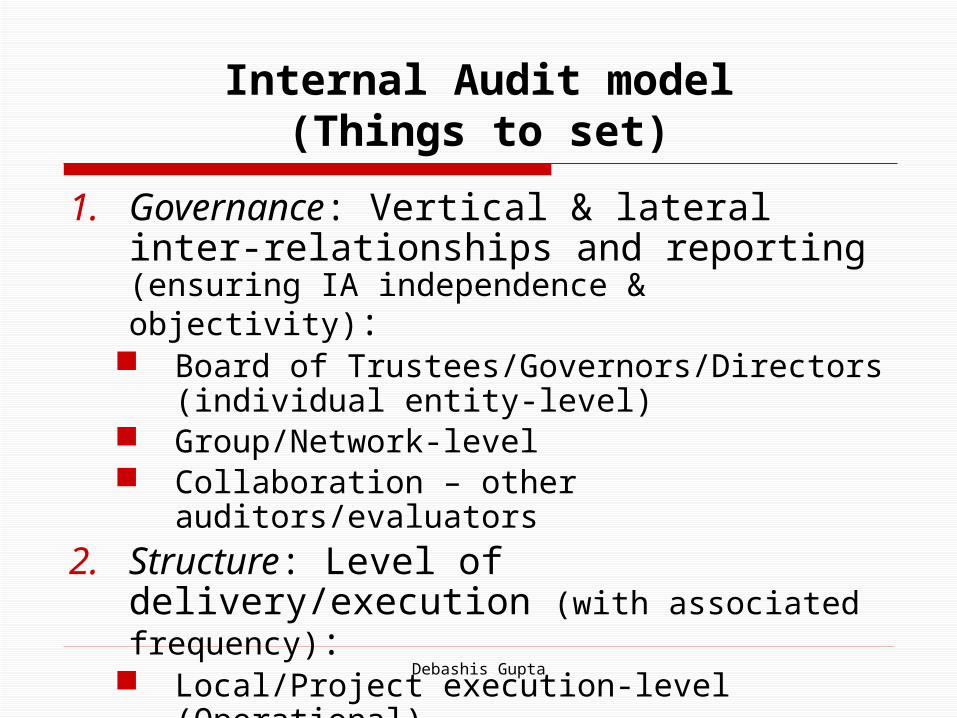

Internal Audit model(Things to set)

1. Governance: Vertical & lateral inter-relationships and reporting (ensuring IA independence & objectivity):

Board of Trustees/Governors/Directors (individual entity-level)

Group/Network-level Collaboration – other auditors/evaluators

2. Structure: Level of delivery/execution (with associated frequency):

Local/Project execution-level (Operational) Regional and/or HQ (often Strategic)

(IIA IPPF-sensitive)Cont’d…

Debashis Gupta

Internal Audit model(Things to set)

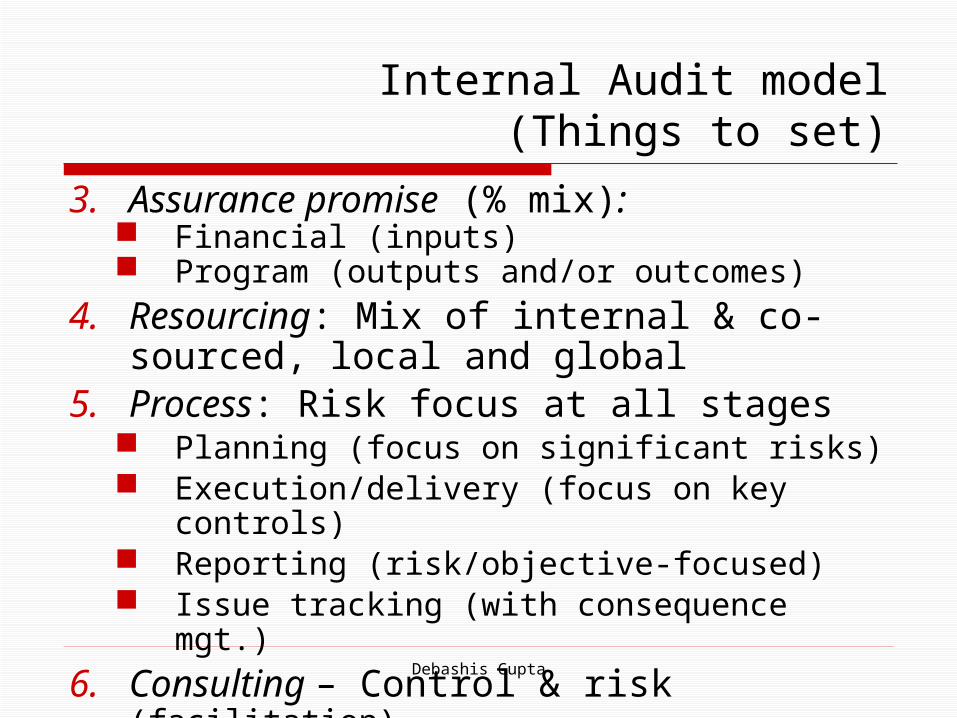

3. Assurance promise (% mix): Financial (inputs) Program (outputs and/or outcomes)

4. Resourcing: Mix of internal & co-sourced, local and global

5. Process: Risk focus at all stages Planning (focus on significant risks) Execution/delivery (focus on key controls) Reporting (risk/objective-focused) Issue tracking (with consequence mgt.)

6. Consulting – Control & risk (facilitation)

Debashis Gupta

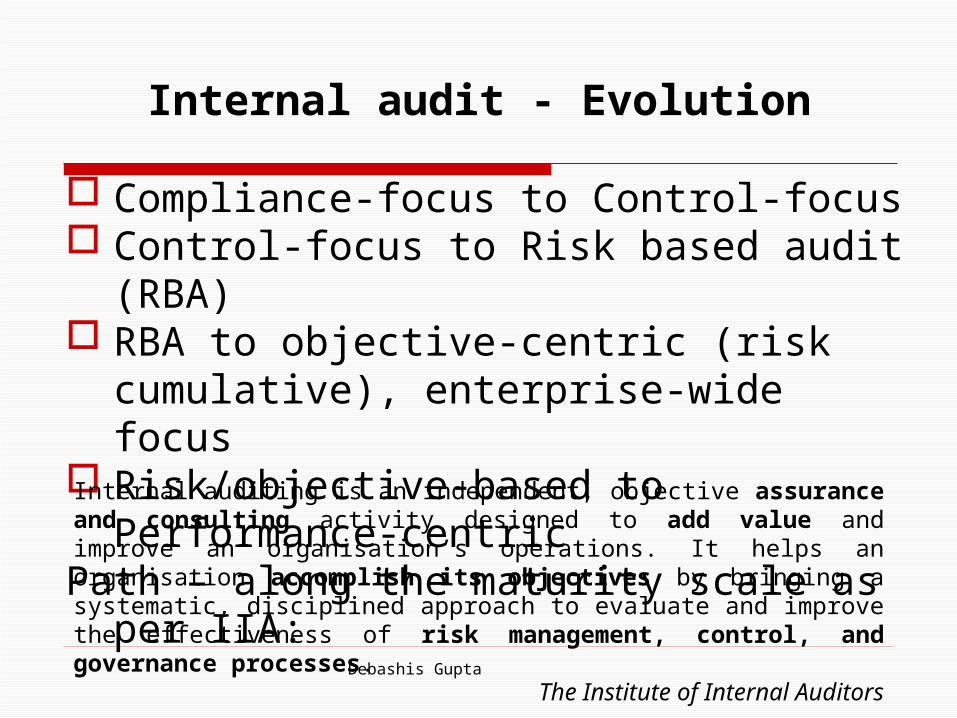

Internal audit - Evolution

Compliance-focus to Control-focus Control-focus to Risk based audit (RBA) RBA to objective-centric (risk cumulative),

enterprise-wide focus Risk/objective-based to Performance-centricPath – along the maturity scale as per IIA:Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organisation’s operations. It helps an organisation accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes.

The Institute of Internal AuditorsDebashis Gupta

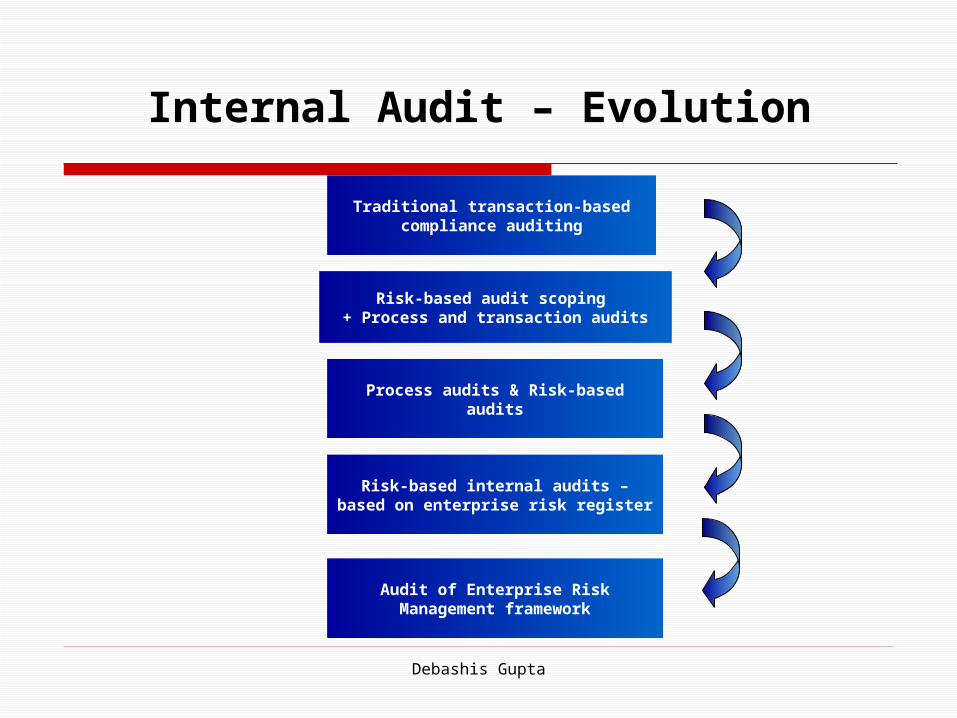

Internal Audit – Evolution

Traditional transaction-based compliance auditing

Risk-based audit scoping + Process and transaction audits

Process audits & Risk-based audits

Risk-based internal audits – based on enterprise risk register

Audit of Enterprise Risk Management framework

Debashis Gupta

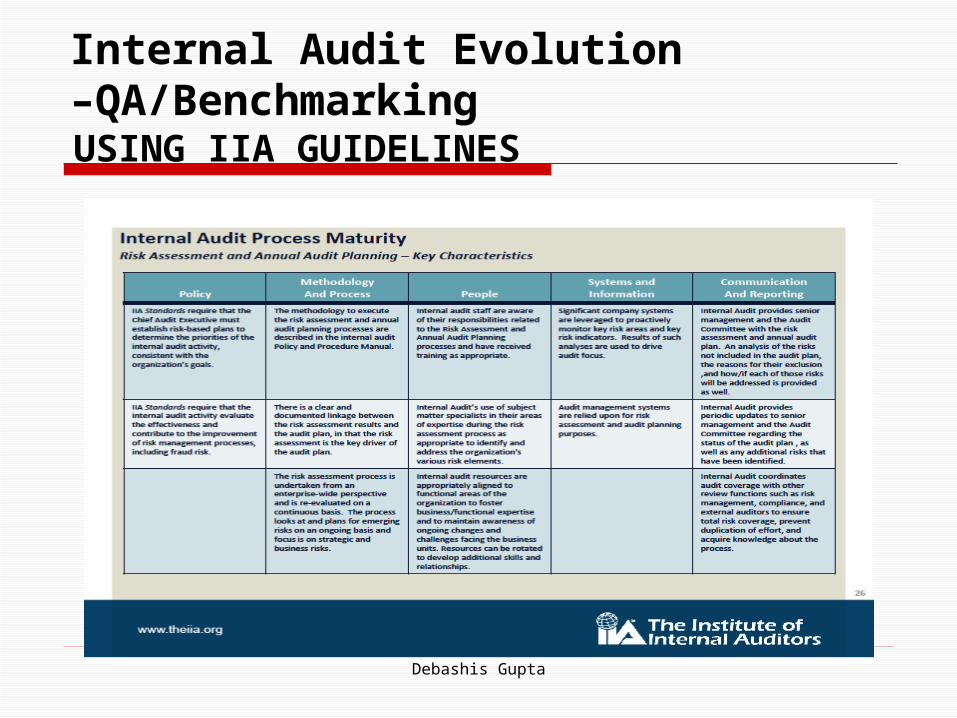

Internal Audit Evolution –QA/BenchmarkingUSING IIA GUIDELINES

Debashis Gupta

Internal Audit

Resourcing

Debashis Gupta

Internal Audit

Resourcing Strategy – Possible model1. Local – outsourced on ‘Co-sourcing’ model

(where appropriate resources available)

2. Centralised unit capacities to be built up for:A. Review of strategic & sensitive functions/projectsB. Improved monitoring of co-sourced auditorsC. Review of policies & processesD. Facilitating new initiatives e.g. control self

assessment, risk management

3. Explore potential to involve ‘guest’ auditors across regions/functions.

Debashis Gupta

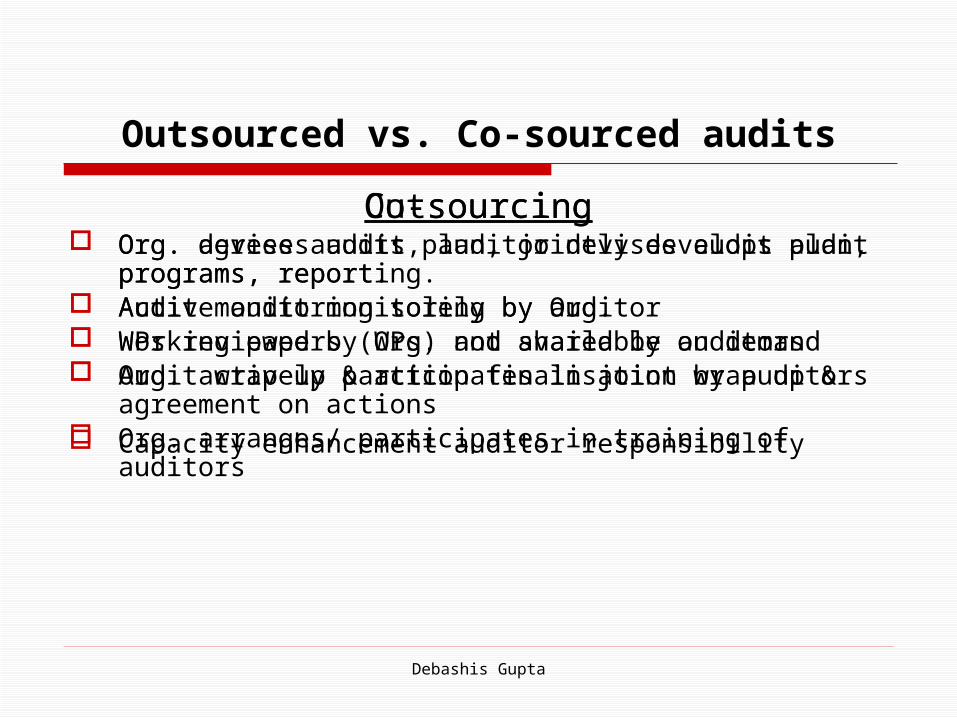

Outsourced vs. Co-sourced audits

Outsourcing Org. agrees audits, auditor devises audit plan, programs,

report. Audit monitoring solely by auditor Working papers (WPs) not shared by auditors Audit wrap up & action finalisation by auditors

Capacity enhancement auditor responsibility

Co-sourcing Org. devises audit plan, jointly develops audit programs,

reporting. Active audit monitoring by Org. WPs reviewed by Org. and available on demand Org. actively participates in joint wrap up & agreement

on actions Org. arranges/ participates in training of auditors

Debashis Gupta

Internal Audit

Process

Debashis Gupta

Internal Audit process

Planning1. Wide coverage – aim to cover all

significant locations and processes in multi-year cycle (e.g. once every 3 yrs)

2. Focus on fostering efficiencies/cost savings & best practices.

3. Project /program audits at various stages – planning, execution, closure

4. Supporting functions coverageKey: Risk weightage

Debashis Gupta

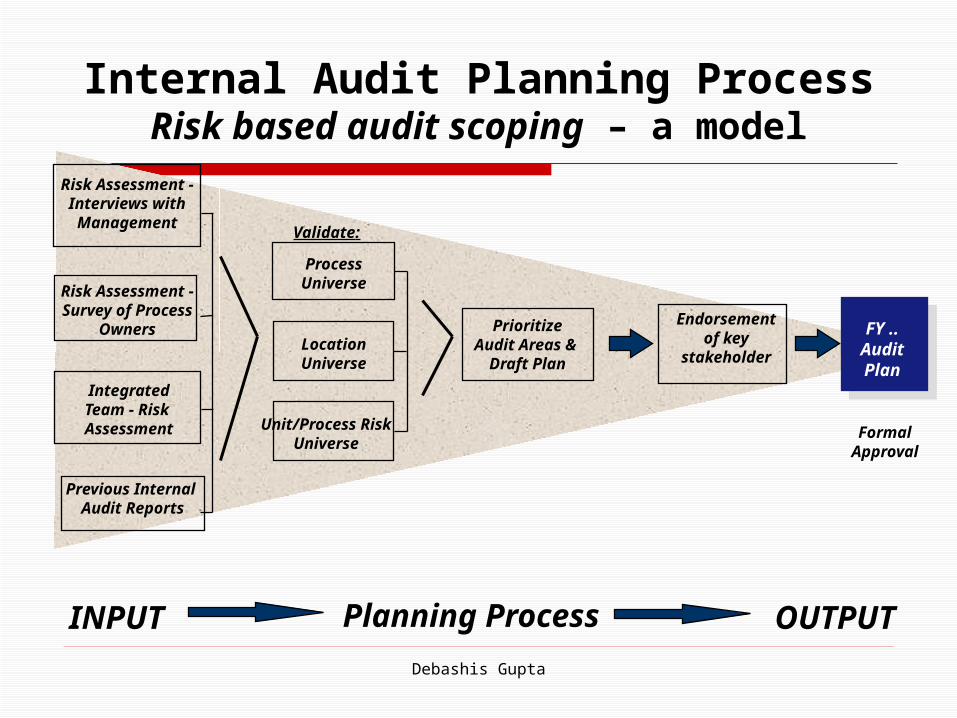

FY ..AuditPlan

Risk Assessment -Interviews with Management

Risk Assessment - Survey of Process

Owners

IntegratedTeam - Risk Assessment

ProcessUniverse

PrioritizeAudit Areas &

Draft Plan

Endorsement of key

stakeholder

Previous Internal Audit Reports

INPUT OUTPUTPlanning Process

LocationUniverse

Unit/Process RiskUniverse

Validate:

FormalApproval

Internal Audit Planning ProcessRisk based audit scoping – a model

Debashis Gupta

CO

MM

UN

ICATIO

N

PROCESS / PROCEDURAL CONTROLS

MONITORINGCONTROLS

Control environment

Con

trol e

nviro

nmen

t

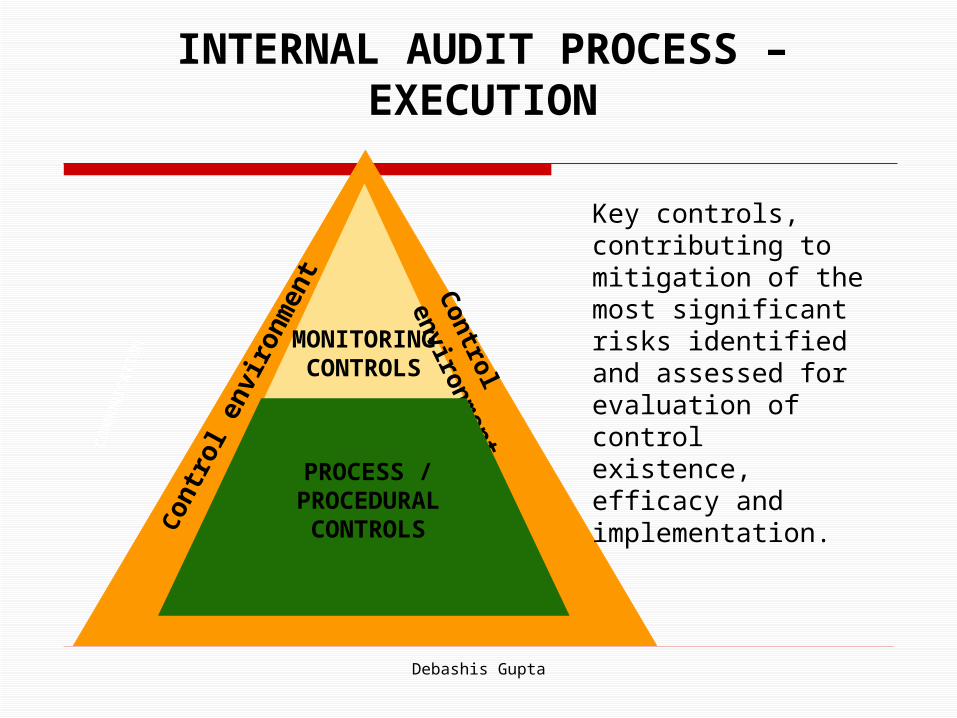

INTERNAL AUDIT PROCESS – EXECUTION

PROCESS / PROCEDURAL

CONTROLS

Key controls, contributing to mitigation of the most significant risks identified and assessed for evaluation of control existence, efficacy and implementation.

Debashis Gupta

Risk

Context – Internal Audit & Risk Status Conceptual frameworks Possible roadmap

Debashis Gupta

RISK BASED INTERNAL AUDIT – Purpose

Purpose of risk based internal audit is:

• To provide assurance on the effectiveness of controls and the management of risks to assist the company in achieving its objectives.

• To improve the company’s operations by adding value, supporting management and providing a platform for learning.

Debashis Gupta

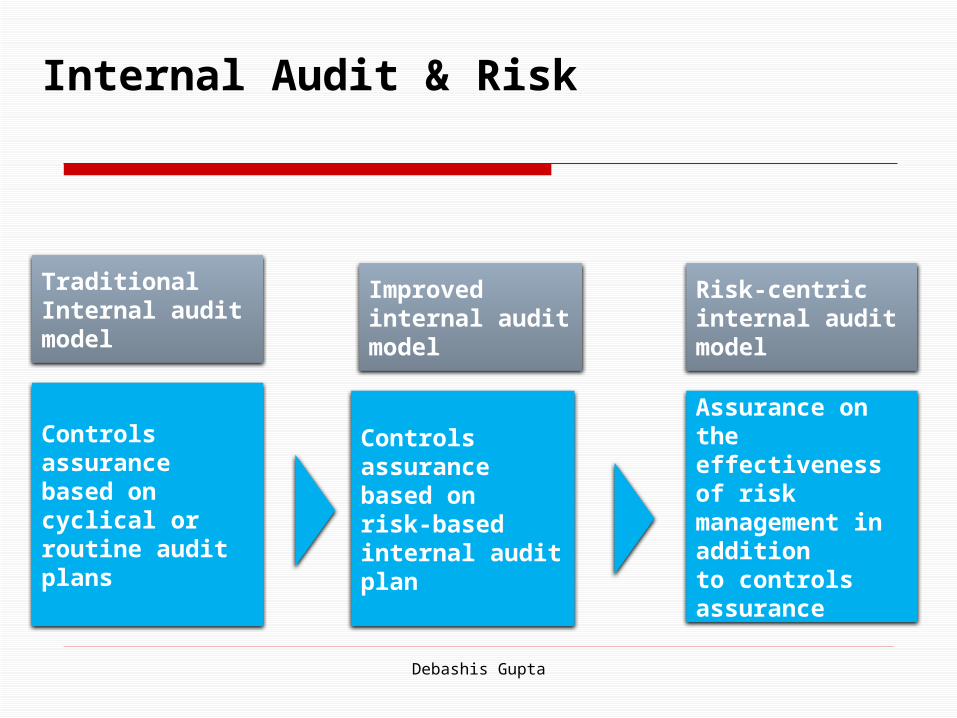

Internal Audit & Risk

Traditional Internal audit model

Controls assurance based on cyclical or routine audit plans

Improvedinternal audit model

Controls assurance based onrisk-based internal audit plan

Risk-centricinternal audit model

Assurance on the effectivenessof risk management in additionto controls assurance

Debashis Gupta

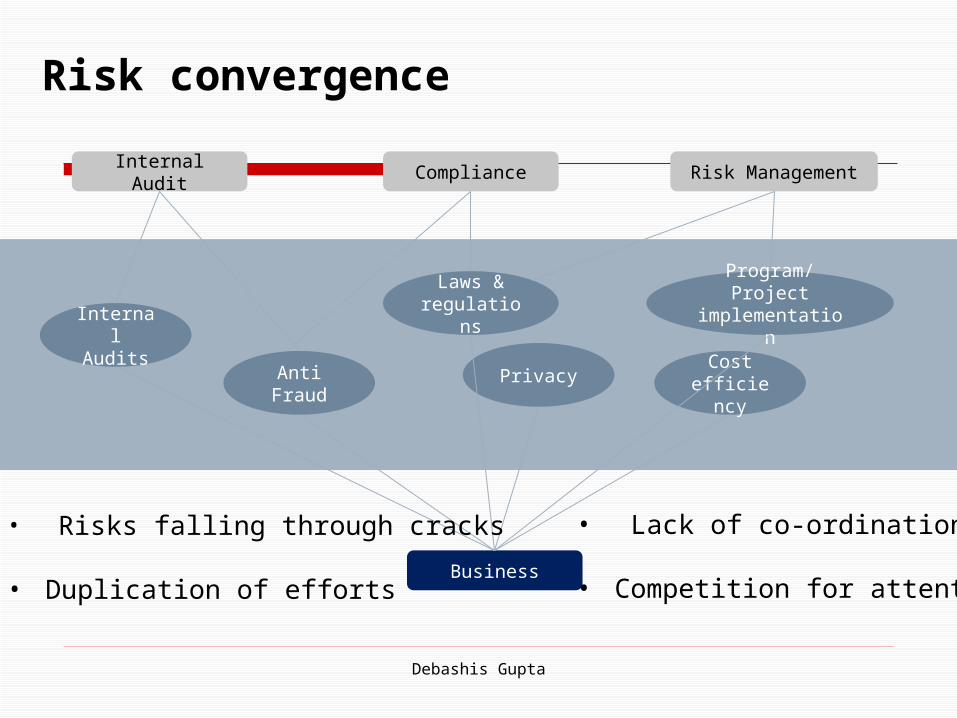

Risk convergence

Internal Audit Compliance Risk Management

Internal Audits

Cost efficienc

y

Laws & regulations

Anti Fraud

Privacy

Program/Project implementation

Business

• Lack of co-ordination • Competition for attention

• Risks falling through cracks • Duplication of efforts

Debashis Gupta

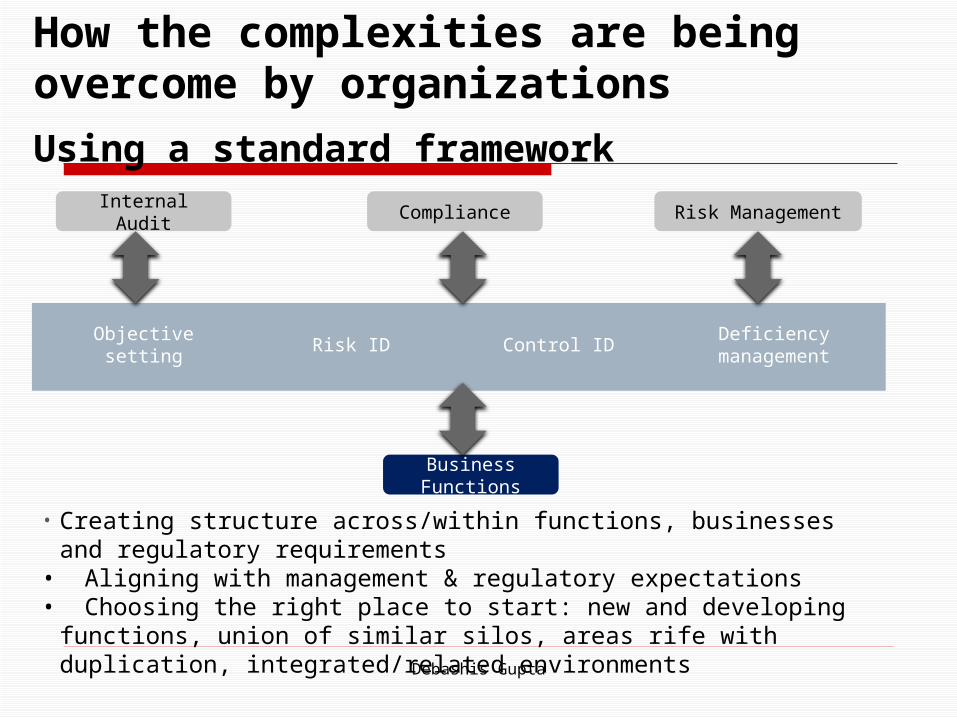

Using a standard framework

How the complexities are being overcome by organizations

Internal Audit Compliance Risk Management

Objective setting Risk ID Control IDDeficiency

management

Business Functions

• Creating structure across/within functions, businesses and regulatory requirements

• Aligning with management & regulatory expectations• Choosing the right place to start: new and developing functions, union of

similar silos, areas rife with duplication, integrated/related environmentsDebashis Gupta

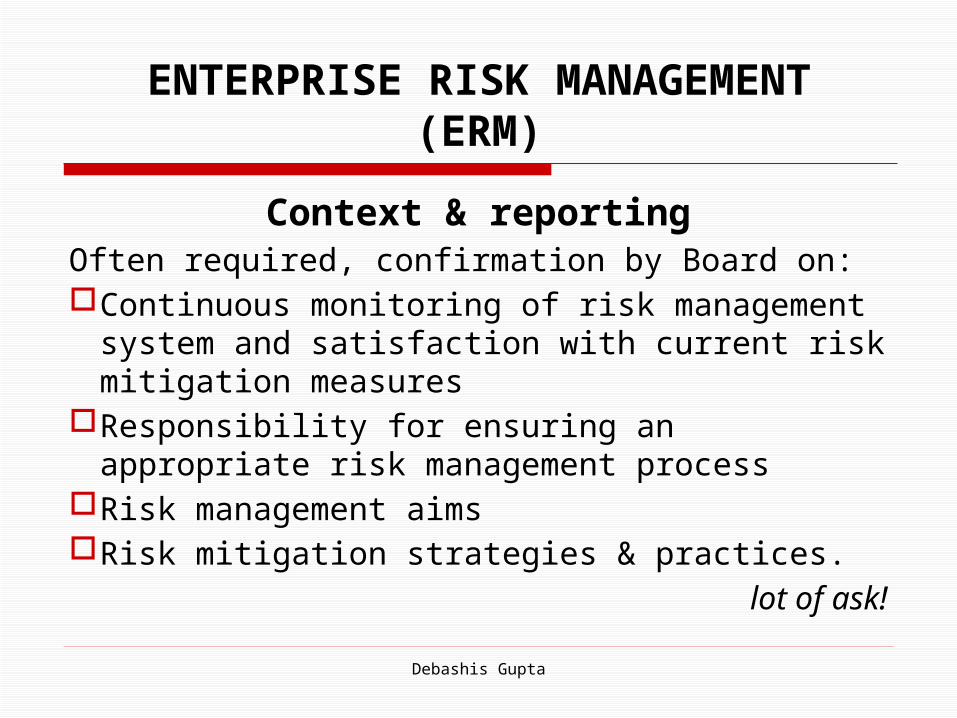

ENTERPRISE RISK MANAGEMENT(ERM)

Context & reportingOften required, confirmation by Board on:Continuous monitoring of risk management

system and satisfaction with current risk mitigation measures

Responsibility for ensuring an appropriate risk management process

Risk management aimsRisk mitigation strategies & practices.

lot of ask!

Debashis Gupta

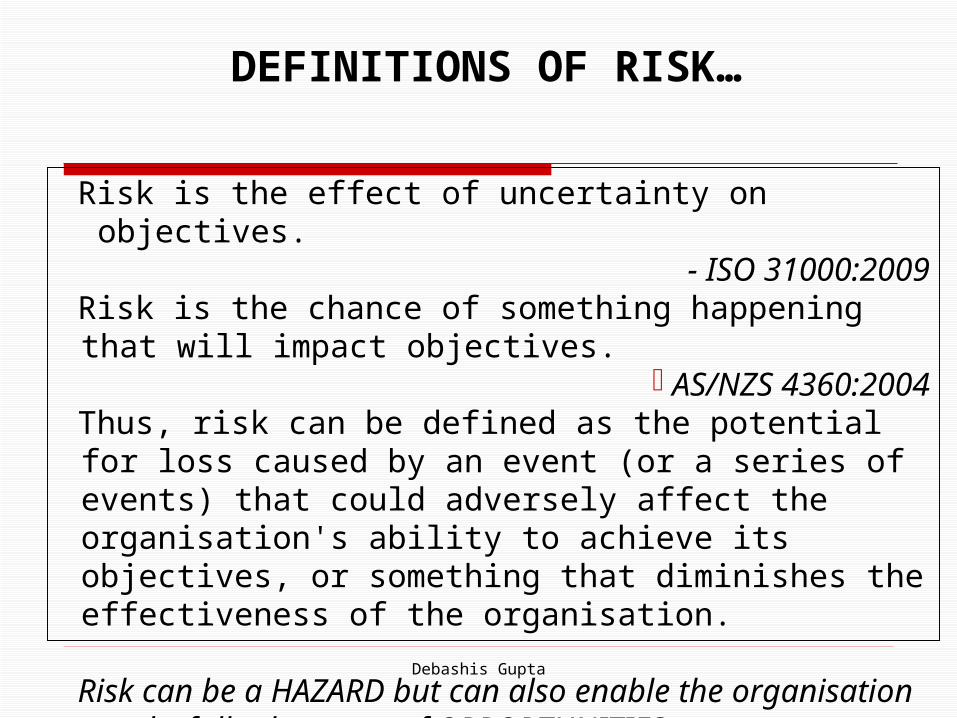

Risk is the effect of uncertainty on objectives.- ISO 31000:2009

Risk is the chance of something happening that will impact objectives.

- AS/NZS 4360:2004Thus, risk can be defined as the potential for loss caused by an event (or a series of events) that could adversely affect the organisation's ability to achieve its objectives, or something that diminishes the effectiveness of the organisation.

Risk can be a HAZARD but can also enable the organisation to take full advantage of OPPORTUNITIES.

DEFINITIONS OF RISK…

Debashis Gupta

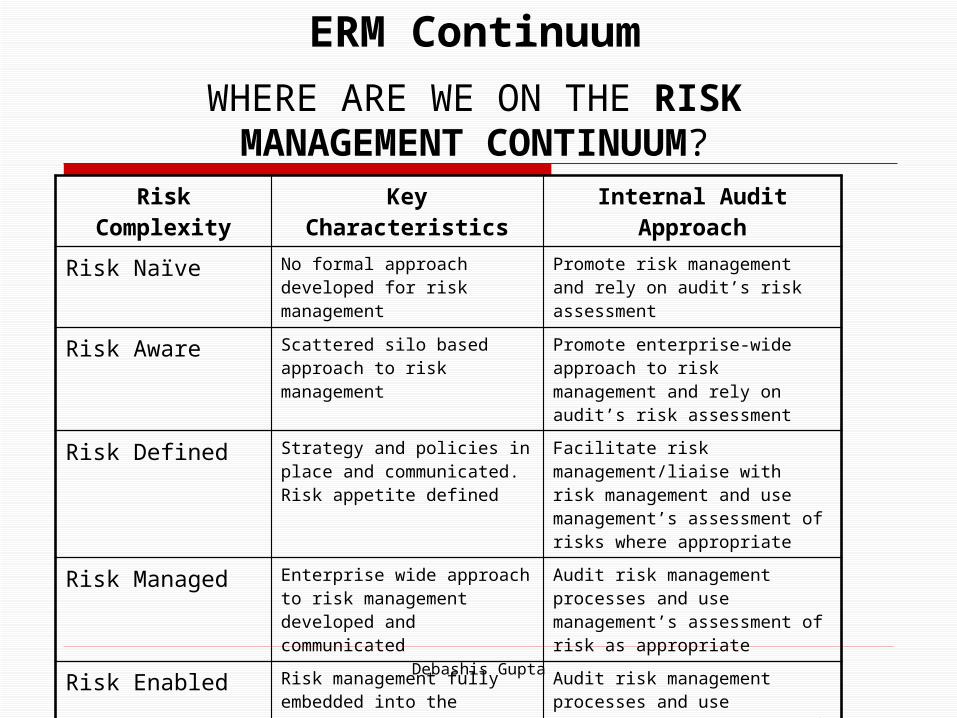

Risk Complexity

Key Characteristics Internal Audit Approach

Risk Naïve No formal approach developed for risk management

Promote risk management and rely on audit’s risk assessment

Risk Aware Scattered silo based approach to risk management

Promote enterprise-wide approach to risk management and rely on audit’s risk assessment

Risk Defined Strategy and policies in place and communicated. Risk appetite defined

Facilitate risk management/liaise with risk management and use management’s assessment of risks where appropriate

Risk Managed Enterprise wide approach to risk management developed and communicated

Audit risk management processes and use management’s assessment of risk as appropriate

Risk Enabled Risk management fully embedded into the operations

Audit risk management processes and use management’s assessment of risks

ERM Continuum

WHERE ARE WE ON THE RISK MANAGEMENT CONTINUUM?

Debashis Gupta

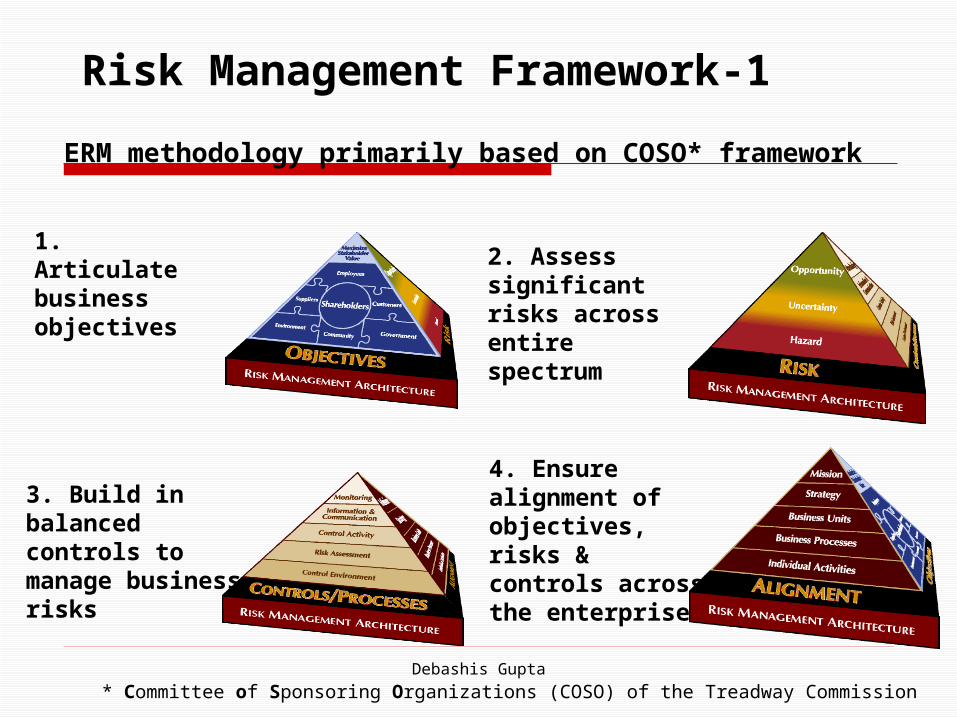

Risk Management Framework-1

1. Articulate business objectives

2. Assess significant risks across entire spectrum

4. Ensure alignment of objectives, risks & controls across the enterprise

3. Build in balanced controls to manage business risks

ERM methodology primarily based on COSO* framework

* Committee of Sponsoring Organizations (COSO) of the Treadway CommissionDebashis Gupta

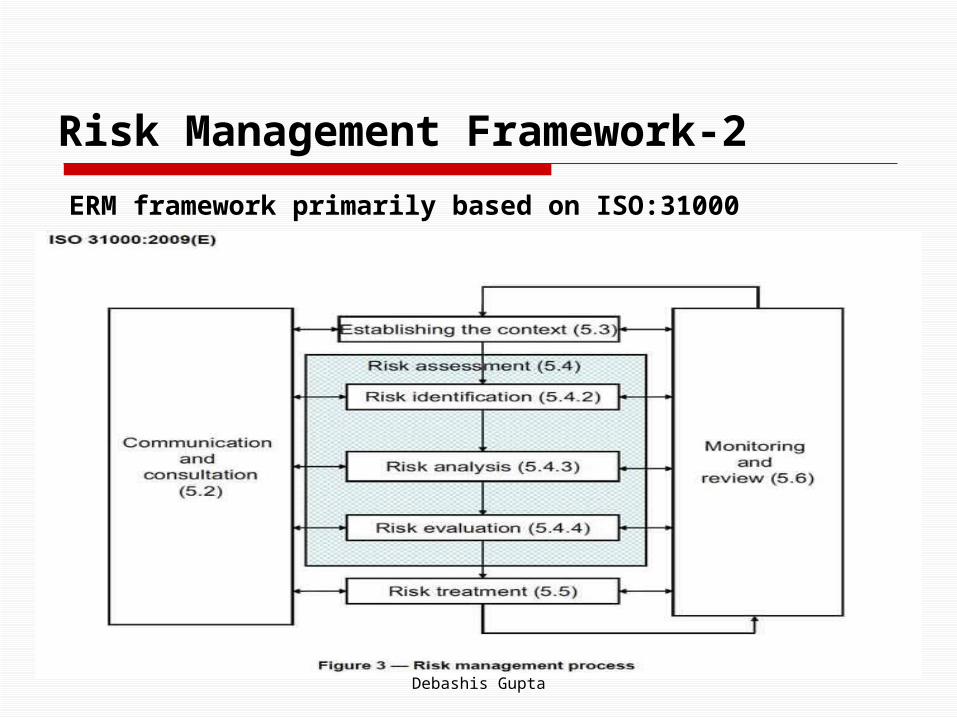

Risk Management Framework-2

ERM framework primarily based on ISO:31000

Debashis Gupta

ERM – Possible Roadmap

1. Developing a Risk Management Policy2. Developing a Risk Management

Framework covering:Structure, roles & responsibilitiesMethodologies, systems & toolsProcesses of risk identification, assessment,

prioritization, monitoring & reporting (in line with preferred framework e.g. ISO:31000 or COSO-ERM)

Cont’d…

Debashis Gupta

ERM – Possible Roadmap…3. Formal enterprise risk management

strategy can follow a two-pronged approach:

Risk management by process owners Risk identification, assessment & reporting

by ‘risk officers’ & ‘coordinators’ (existing functionaries co-opted in an ‘embedded’ role) facilitated by a nodal dept. (IA/ERM?) Identify the critical risks that the organisation is

facing, current or recommended actions to address these

Devise plans to continuously monitor and report on the most critical risks.

Cont’d…Debashis Gupta

ERM – Possible Roadmap…

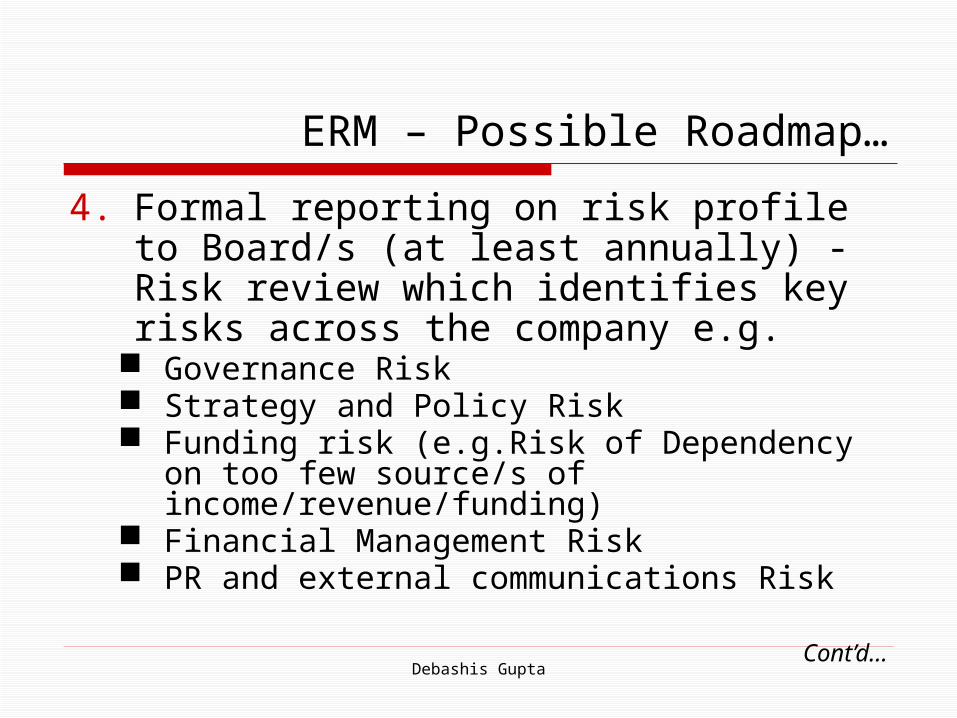

4. Formal reporting on risk profile to Board/s (at least annually) - Risk review which identifies key risks across the company e.g.

Governance Risk Strategy and Policy Risk Funding risk (e.g.Risk of Dependency on too

few source/s of income/revenue/funding) Financial Management Risk PR and external communications Risk

Cont’d…

Debashis Gupta

ERM – Possible Roadmap…

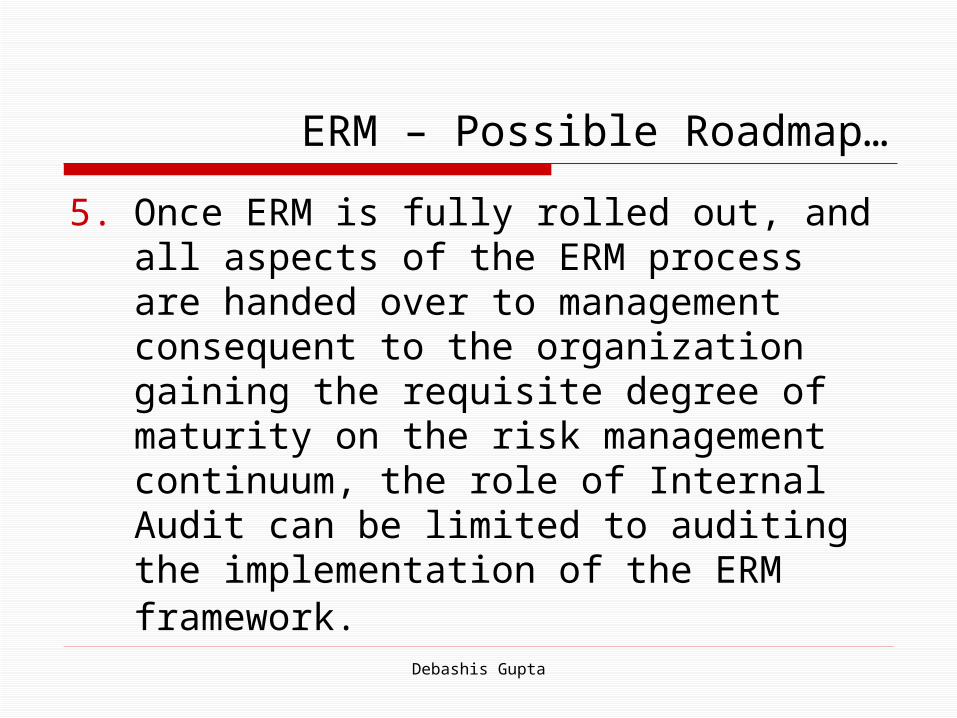

5. Once ERM is fully rolled out, and all aspects of the ERM process are handed over to management consequent to the organization gaining the requisite degree of maturity on the risk management continuum, the role of Internal Audit can be limited to auditing the implementation of the ERM framework.

Debashis Gupta

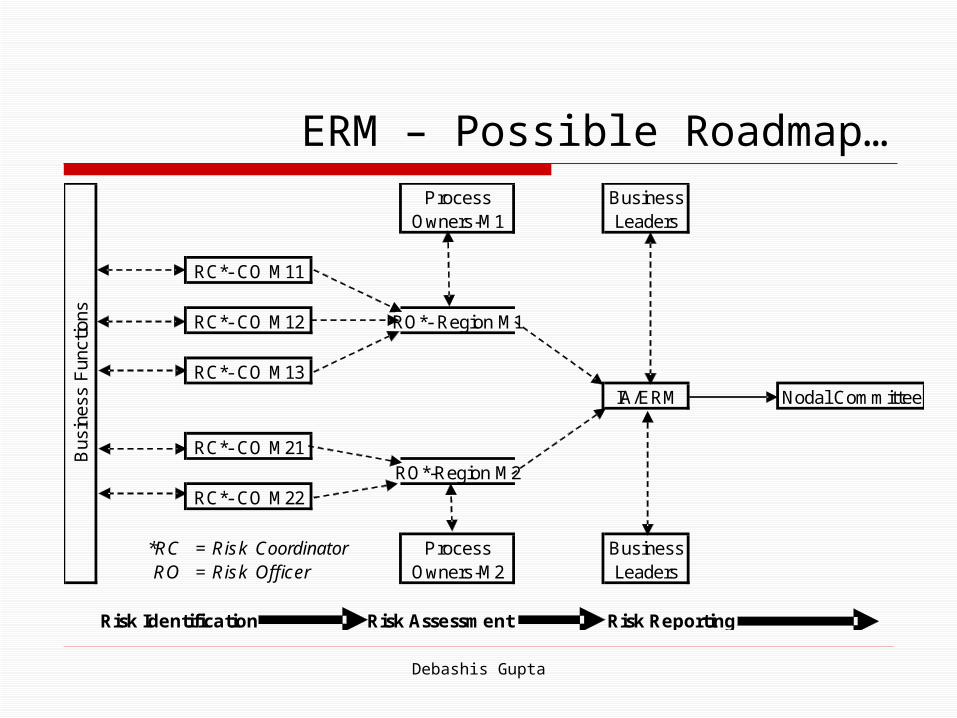

ERM – Possible Roadmap…Process Business

Owners-M1 Leaders

RC*- CO M11

RC*- CO M12 RO*- Region M1

RC*- CO M13IA/ERM Nodal Committee

RC*- CO M21RO*-Region M2

RC*- CO M22

*RC = Risk Coordinator Process BusinessRO = Risk Officer Owners-M2 Leaders

Risk Identification Risk Assessment Risk Reporting

Bus

ines

s F

unct

ions

Debashis Gupta

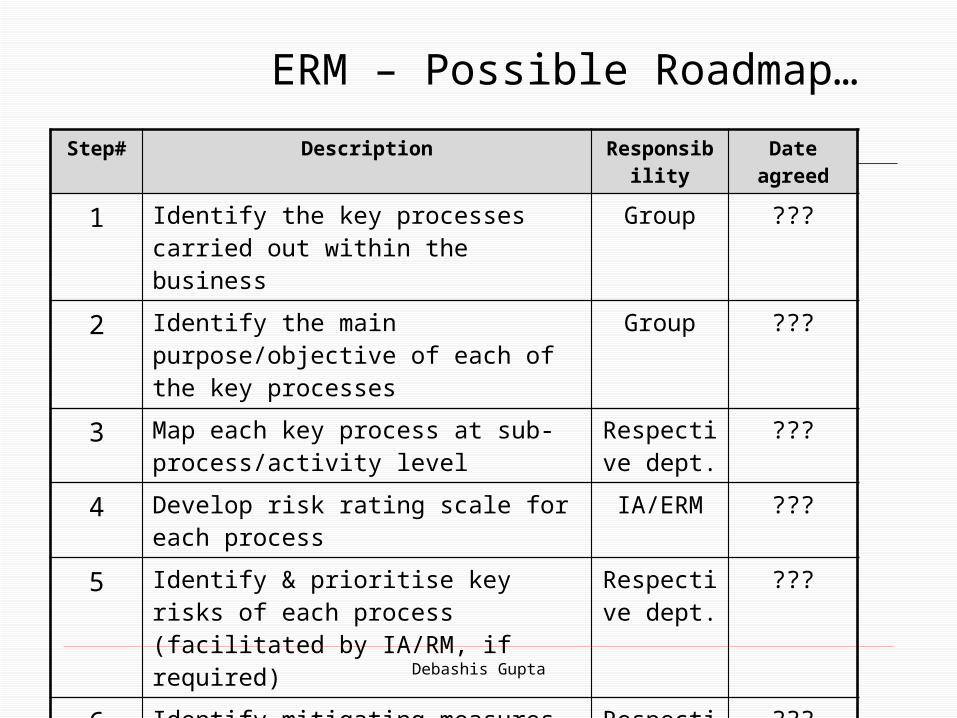

Step# Description Responsibility Date agreed

1 Identify the key processes carried out within the business

Group ???

2 Identify the main purpose/objective of each of the key processes

Group ???

3 Map each key process at sub-process/activity level

Respective dept.

???

4 Develop risk rating scale for each process IA/ERM ???

5 Identify & prioritise key risks of each process (facilitated by IA/RM, if required)

Respective dept.

???

6 Identify mitigating measures in place/ proposed for each key risk

Respective dept.

???

7 Presentation of key risks and associated mitigating measures to MCT

Respective dept.

???

ERM – Possible Roadmap…

Debashis Gupta

Thank You

Debashis Gupta