Internal Analysis Lecture 4

25

1 Internal Analysis

-

Upload

anush-prasannan -

Category

Documents

-

view

227 -

download

0

Transcript of Internal Analysis Lecture 4

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 1/25

1

Internal Analysis

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 2/25

2

Lecture Topics

• Purpose of Internal Analysis

• Competitive Advantage and Core

Competence

• Value Chain

• Financial Analysis

• Combining Internal and External

Analyses

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 3/25

3

Purpose of Internal Analysis

• An organization’s future successdepends on its own internal conditions

as well as external conditions

• Managers need to be able to identify – Strengths that the company can relay on in

order to compete

– Weaknesses that need to be corrected or minimized as competitive factors

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 4/25

4

Competitive Advantage

• The collection of factors that sets a

company apart from its competitors

and gives it a unique position in themarket

• Means to add value for stakeholders

• Focus especially on adding value for customers

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 5/25

5

Core Competence

A unique set of lasting capabilities thata company relies on to achieve

competitive advantage and add value

• Innovation• Efficiency

• Customer Responsiveness

• Quality

• Special Expertise

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 6/25

6

Value Chain

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 7/25

7

Value Chain Interpretation

• Represents a company or any organization

• Simplified illustration of all activities that an

organization must perform

• Framework for analyzing a company’s

strengths and weaknesses

• Margin represents profit- expand margin by

– Being able to charge a higher price

– Operating at a lower cost within the Value Chain

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 8/25

8

Primary Activities in the

Value ChainActivities directly involved in producing,selling, distributing, and servicing productfor buyer.

• Inbound logistics: receiving, storing, and distributinginputs for production

• Operations: all activities involved in transforminginputs into final products

• Outbound logistics: collecting, storing, distributing

product to final buyer • Marketing and Sales: activities used to get customers

to buy company products

• Service: installation, repair, support, training for using

a product

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 9/25

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 10/25

10

Applying Value Chain Analysis

• Framework for identifying company’sstrengths and weaknesses

• Means to focus on where the

company’s core competencies exist andcan be used to achieve competitive

advantage and add value

• Comparison with competitors revealsopportunities for improving company’s

competitive position

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 11/25

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 12/25

12

Income StatementSales

Cost of Goods SoldGross Profit

Operating Expenses

Wages and Salaries

Rent

Advertising

Insurance

Research and Development

Depreciation

Total Operating Expenses

Operating Income (Earnings Before Interest and Taxes – EBIT)

Interest

Income Before Taxes

Taxes

Net Income

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 13/25

13

Balance Sheet Assets

Current Assets

CashMarketable Securities

Accounts Receivable

Inventory

Total Current Assets

Fixed AssetsProperty, Plant, Eqt.

Less: Accumulated

Depreciation

Net Fixed Assets

Other Assets

Patents, Trademarks

Goodwill

Total Other Assets

Total Assets

Liabilities and Owners’ Equity

Liabilities

Current Liabilities Accounts Payable

Wages Payable

Notes Payable

Taxes Payable

Total Current LiabilitiesLong Term Liabilities

Loans

Mortgages

Total Long Term Liabilities

Owners’ Equity

Stock

Retained Earnings

Total Owners’ Equity

Total Liabilities and Owners’ Equity

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 14/25

14

Types of Ratios

• Profitability• Activity – Efficiency

• Liquidity

• Debt - Leverage

• Growth

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 15/25

15

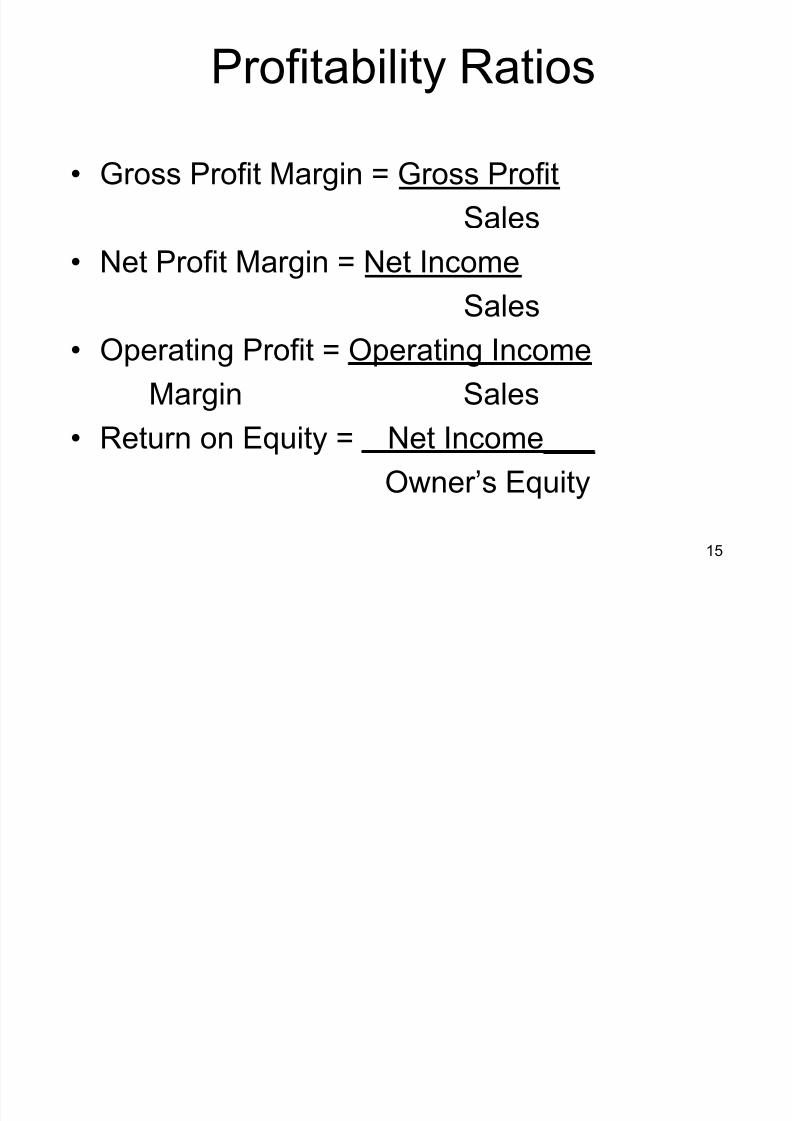

Profitability Ratios

• Gross Profit Margin = Gross Profit

Sales

• Net Profit Margin = Net IncomeSales

• Operating Profit = Operating Income

Margin Sales

• Return on Equity = Net Income___

Owner’s Equity

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 16/25

16

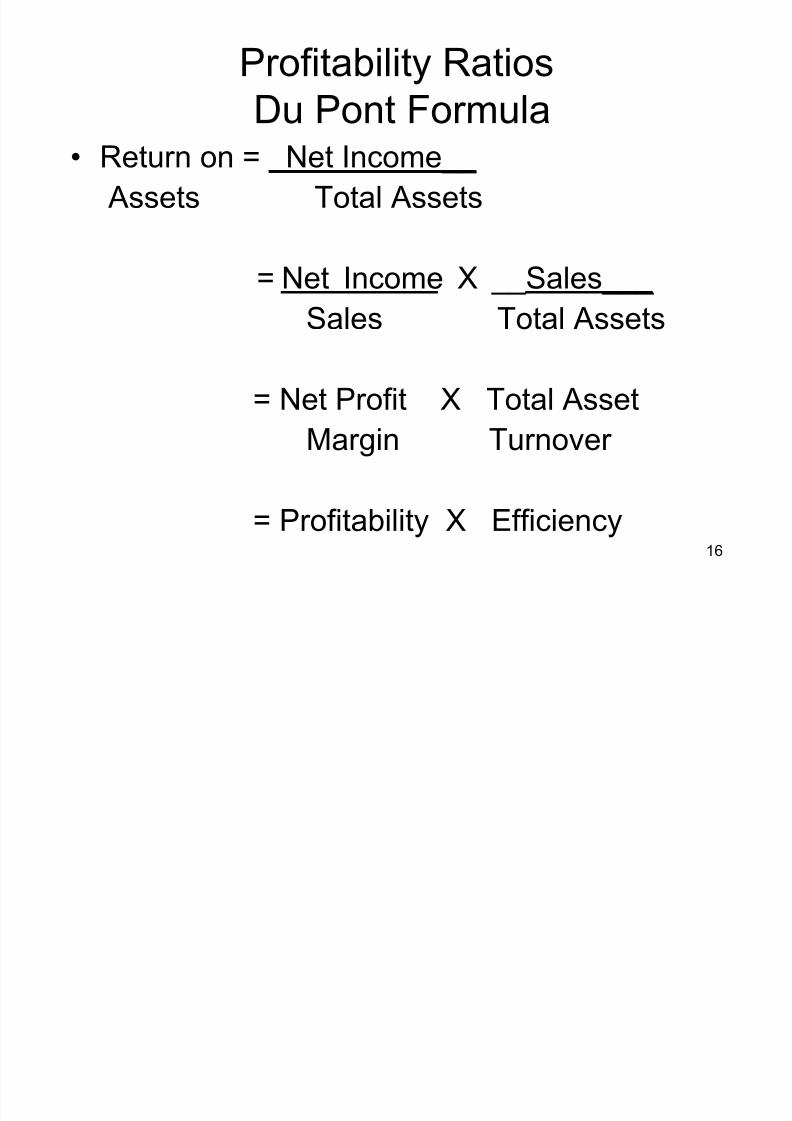

Profitability Ratios

Du Pont Formula• Return on = Net Income__

Assets Total Assets

= Net Income X __Sales___ Sales Total Assets

= Net Profit X Total Asset

Margin Turnover

= Profitability X Efficiency

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 17/25

17

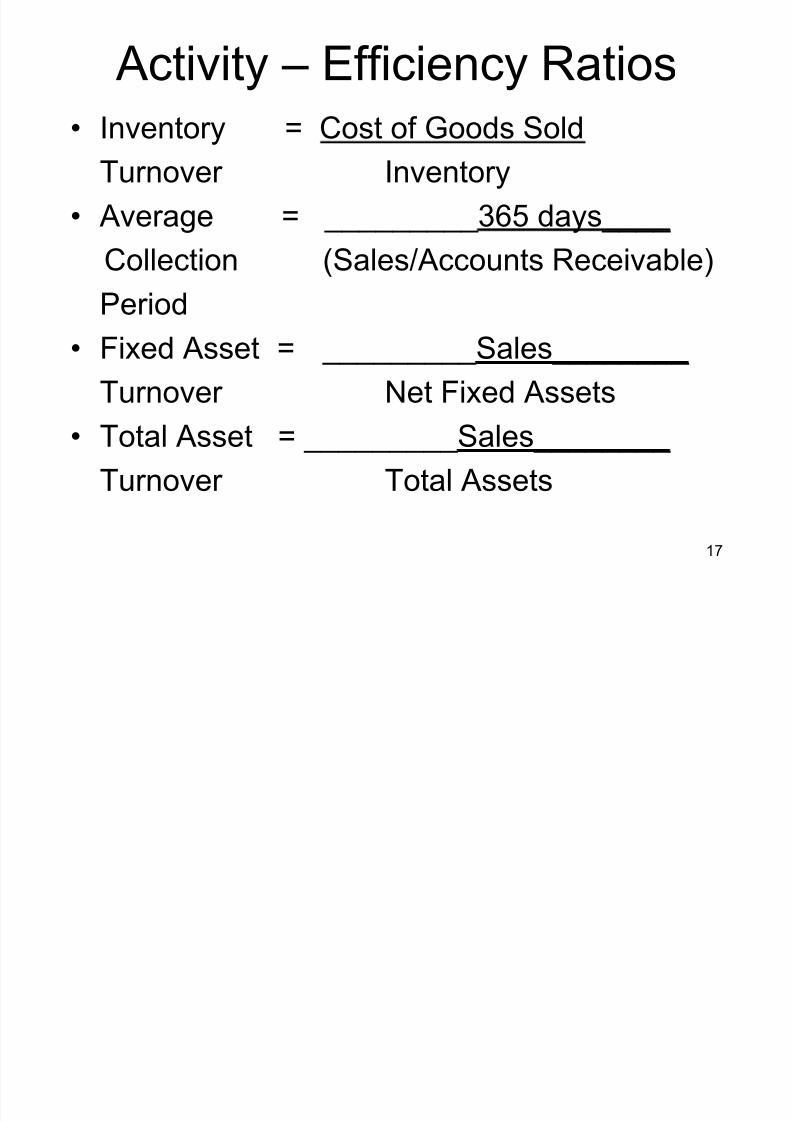

Activity – Efficiency Ratios

• Inventory = Cost of Goods SoldTurnover Inventory

• Average = _________365 days____

Collection (Sales/Accounts Receivable)

Period

• Fixed Asset = _________Sales________

Turnover Net Fixed Assets

• Total Asset = _________Sales________

Turnover Total Assets

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 18/25

18

Liquidity Ratios

• Current = __Current Assets___ Current Liabilities

• Quick = Current Assets – Inventories

Current Liabilities

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 19/25

19

Debt –Leverage Ratios

• Debt = Current + Long Term LiabilitiesTotal Assets

• Debt = Current + Long Term Liabilities

Total Owners’ Equity • Times = Operating Income (EBIT)

Interest Interest

Earned

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 20/25

20

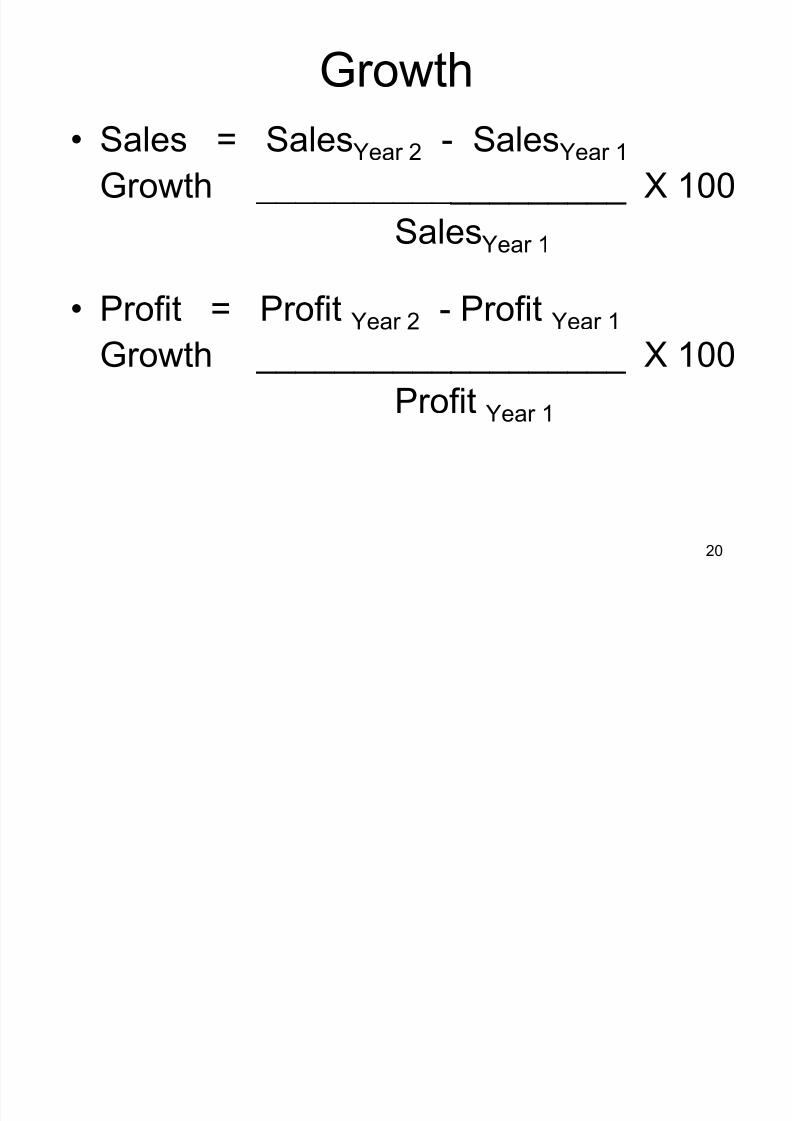

Growth

• Sales = SalesYear 2 - SalesYear 1 Growth ___________________ X 100

SalesYear 1

• Profit = Profit Year 2 - Profit Year 1

Growth ___________________ X 100

Profit Year 1

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 21/25

21

Combining Internal and

External Analyses• Internal and External Analyses commonly

referred to as SWOT:Strengths

Weaknesses

Opportunities

Threats

• Strengths and Weaknesses identified fromInternal Analysis

• Opportunities and Threats identified fromExternal Analyses

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 22/25

22

Internal Analysis

• Strengths and Weaknesses identified

through the use of tools such as:

– Core Competencies

– Stakeholder Analysis

– Value Chain

– Financial Analysis

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 23/25

23

External Analysis

• Opportunities and Threats identified through

the use of tools such as:

– General Environment Assessment – Five Force Analysis

– Key Success Factors in Industry

– Competitive Changes during Industry Evolution

– Strategic Groups

– National Competitive Advantage

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 24/25

24

Results of Internal and

External Analysis

• Requires creative interpretation

• Understanding of company’s competitiveposition in its industry

• Identification of strategic issues the companyfaces

• Strategic issues – Represent dangers to the company’s long-term

survival – Suggest areas where the company should

concentrate its efforts in order to grow

7/27/2019 Internal Analysis Lecture 4

http://slidepdf.com/reader/full/internal-analysis-lecture-4 25/25

25

Internal Analysis

•Strengths

•Weaknesses

External Analysis

•Opportunities

•Threats

Strategic

Issues

Strategic

AlternativesStrategy

Tools Tools