Successful Intern Management: A Guide for Intern Managers ...

Upload

kripa-adhikaryCategory

view

349download

0

An Internship Report on

DCBL Bank Ltd

Prepared by:

Kripa Adhikary

PU Registration No: 2009-2-22-0014

Submitted to:

Ace Institute of Management

Faculty of Management

Pokhara University

In partial fulfillment of the requirements for the degree of

Masters of Business Administration

Kathmandu

Date: 26/11/2010

LETTER OF ACCREDITATION

It is hereby certified that this report, entitled “Internship Report On Laxmi bank”

prepared by M/S Kripa Adhikary is an outcome of the eight weeks internship undergone

at “DCBL”.

The facts and ideas presented in this report are an outcome of the student’s hard work and

dedication to the project, undertaken as a partial fulfillment for the requirements for

degree of Masters of Business Administration.

The outcome of this project has been highly appreciated.

…………………….. ………………………

Mr. Sushil Manandhar External Evaluator

Assistant Manager Pokhara University

DCBL

2

ACKNOWLEDGEMENT

It is difficult to draw up a list of persons to be thanked because several people

have helped in preparation of this report in diverse ways. Knowledge itself is cumulative

so it is difficult to acknowledge intellectual ideas. It is impossible to acknowledge all

those who contributed to this study. But still some persons need to be publicly

acknowledged.

I would like to first of all thank our faculty supervisor and Program director Mr.

Bishal Shrestha of Ace Institute of Management for his guidance and support in the

organization selection and on the on the preparation of this report. I am also thankful to

our college management for providing us computer and internet facility without which I

would be unable to prepare my report.

I would especially like to thank Ms Sabina Nakarmi of Human Resource

Department of DCBL Bank for selecting me as an intern. I would like to thank Mr.

Sushil Manandhar Head of Treasury Department and Ms Deena Chitrakar Head of

Division Operations Risk Management and all the staffs of respective departments for

being so kind and co-operative towards me during my internship period. I would also like

to thank them for giving their valuable time in explaining various activities and

terminologies. Their response has certainly made me know about the general operation of

the bank's system and procedure.

Finally, I like to present my sincere thanks to my family members and my friends

for their co-operation, guidance and support while the preparing this report. Thanks all

for your encouragement, support and warm co-operation.

Kripa Adhikary

3

LIST OF ACRONYMS

LCY Local Currency

FCY Foreign Currency

NRB Nepal Rastra Bank

CRR Cash Reserve Ratio

IDT Inter Department Ticket

IBT Inter Branch Transaction

MT Message Type

SWIFT Society for Worldwide Interbank Financial Telecommunication

ATM Automated Tailor Machine

4

EXECUTIVE SUMMARYThis report entailed an internship report on "DCBL Bank ltd" has been prepared for the

partial fulfillment of MBA program on the basis of eight week internship experience at

DCBL Bank limited.

In DCBL Bank I was placed in two departments namely treasury department and

remittance department. In treasury department I was involved in activities related to

purchase and sell of foreign currency and borrowing and lending of currency. Similarly in

remittance department I was involved in making draft, swift transfers, traveler’s cheque

and purchase and sell of foreign currency.

During my internship I learned about operations related two department and I also found

interrelation between two departments. As an outsider people may not find the fact that

these two departments were correlated. For instance remittance department was involved

in foreign currency transaction but exchange rate that they would use would be borrowed

from treasury department. I could find out many features of professional world such as

working under deadlines, using specific procedures while performing, working in teams,

listing to what others are saying, become focused and so on.

I could find close relationship between subjects that we studied in MBA and working

environment. I found that concepts borrowed from books related to Emerging Concept of

Management, Financial Institution and Markets, Financial Management, Financial

Accounting, Business Development Plan, Principle of Marketing, Business

Communication, Managing information System etc were actually used in the working

environment.

Lastly, during my internship was good as I learned about the banking operations and

activities related to two departments. Apart from this I got chance learn about real

working environment and the difference and similarities between the corporate world and

the academic world in terms of working procedure, value system, and organizational

culture and so on.

5

CONNTENTSLetter of accreditation..........................................................................................................2

ACKNOWLEDGEMENT...................................................................................................3

Executive Summary.............................................................................................................5

Chapter One.........................................................................................................................7

1. INTRODUCTION........................................................................................................7

1.1 BACKGROUND..................................................................................................7

1.2 OBJECTIVE OF THE INTERNSHIP...................................................................8

1.3 Limitations of the Study.............................................................................................9

1.4 DETAILS OF INTERNSHIP AT DCBL BANK LTD..........................................9

1.5 INTRODUCTION OF DCBL BANK LTD...........................................................9

Chapter Two......................................................................................................................15

2. Assignments/ Activities/ Projects Undertaken.......................................................15

2.1 Assignments Undertaken During the Internship..................................................15

2.2. INTRODCTION..................................................................................................19

Chapter Three....................................................................................................................30

3. PROGRAM AND WORKPLACE RELATIONSHIP...........................................30

Chapter Four......................................................................................................................35

4. CONCLUSION.......................................................................................................35

Appendix............................................................................................................................36

6

CHAPTER ONE

1. INTRODUCTION

1.1 BACKGROUND

The bank is a financial institution, which deals with money. Its primary activity is to

accept deposits from the surplus unit and provide loans to the deficit unit. It allows

interest on the deposits received and charges interest on the loans granted. The difference

between the interest charged on the loan and interest provided on the deposit is the major

source of income for the bank. The other source of income for any banks is the fees,

commission and charges that bank takes for various other types of services it provides.

The evolution of banking industry had started a long time back, during ancient times.

There was reference to the activities of moneychangers in the temple of Jerusalem in the

New Testament. In ancient Greece the famous temples if Delphi and Olympia served as

the great depositories for peoples’ surplus funds and these were the centers of money

lending transaction. Indeed the traces of “rudimentary banking” were found in the

Chaldean, Egyptian, and Phoenician history. The development of banking in ancient

Rome roughly followed the Greek pattern. Banking suffered oblivion after the fall of the

Roman roughly followed the Greek pattern. Banking suffered oblivion after the fall of the

Roman Empire after the death of Emperor Justinian in 565 AD, and it was not until the

revival of trade and commerce in the Middle Ages that the lessons of finance were learnt

a new from the beginning. Money lending in the middle ages was, however, largely

confined to the Jews since the Christians were forbidden by the Canon law to indulge in

the sinful act of lending money to other on interest. However, as the hold of church

loosened with the development of trade and commerce about the thirteenth century

Christians also took to the lucrative business of money lending, thereby entering into

keen competition with the Jews who had hitherto monopolized the business.

7

As a public enterprise, banking made its first beginning around the middle of the twelfth

century in Italy and the Bank of Venice, founded in 1157 was the first public banking

institution. Subsequently, the Bank of Barcelona and the Bank of Genoa in 1401 and

1407 respectively were established. The Bank of Venice and Bank of Genoa continued to

operate until the eighteenth century. With the expansion of commercial activities in

Northern Europe there sprang up a number of private banking houses in Europe and

slowly it spread throughout the world.

The development of banks in case of Nepal is quite recent. In 1933 B.S, an institution

called "Tejarath Adda" was established during the tenure of the Prime Minister Randip

Singh. It was the first step towards the institution development of banking in Nepal.

However, "Nepal Bank Limited (NBL)" is the real and the first commercial bank in

Nepal, which was established in 30th of Kartik, 1994B.S.The establishment of NBL

paved the path for development of banking in Nepal. Though this bank was given the

authority and responsibility of Central Bank, "Nepal Rastra Bank" was established in

14th of Baishakh, 2012 B.S (1995A.D) as Central Bank due to non-satisfactory banking

activities and political instability. Nepal Rastra Bank issued Nepali notes on 7th Falgun

for the first time.

After the liberalization of the financial sector, financial sector has made a hall- mark

progress both in terms of the number of financial institutions and beneficiaries of

financial services. By November 2010, NRB licensed bank and financial institution

totaled 156. Out of them, 29 are commercial banks, 30 development banks, 70 finance

companies, 11 micro- credit development banks and 16 saving and credit cooperatives.

1.2 OBJECTIVE OF THE INTERNSHIPThis report has been prepared for the partial fulfillment of the requirement of the Masters

of Business Administration (MBA) Pokhara University. This report is based upon

internship experience of eight weeks in DCBL Bank Limited. This report gives

information about working environment and activities performed in two different

departments of DCBL Bank. The main objectives of internship are:

To understand the working environment of banking sector through experience

8

To understand operations of the bank

To know the functioning of various departments

To know about the application of theoretical knowledge in practical world

1.3 LIMITATIONS OF THE STUDYThere are few limitations while doing study such as:

Due to the limited time treasury department and Remittance department is

concentrated for the purpose of study.

The outcome of the report is based on the observation, experience and interaction

during eight week internship and this may not cover all the details of the

department.

1.4 DETAILS OF INTERNSHIP AT DCBL BANK LTDAddress: Kathmandu Plaza, Kamaladi, Kathmandu

Position: Intern

Working Duration: 15th August to 7th October

Working Hours:

Sunday to Thursday: 11:30a.m. - 5: 30 p.m.

Friday: 11:30 a.m. to 1:30 p.m.

Name and Designation of Internship Supervisor at DCBL Bank:

Sushil Manandhar- Assistant Manager- Treasury Department-DCBL Bank,

Deena Chitrakar- Assistant Manger-Operations Risk Management Division-DCBL Bank

Name and Designation of Internship Supervisor at AIM:

Bishal Shrestha- Associate Director- Ace Institute of Management

1.5 INTRODUCTION OF DCBL BANK LTD

1.5.1 Background to DCBL Bank

9

DCBL Bank Limited started its operation in 2001 as development bank and was backed

by the expertise of the professional bankers, prominent industrialists, entrepreneurs,

bureaucrats and career diplomats.

The policy of the Bank is to create a relationship with the customer based on shared

vision and mutual understanding for mutual benefit. It focuses in providing qualitative

and diversified banking services backed by efficient personal approach at desired

level. The Bank has been providing diversified services to its clientele by offering its

products in the form of Loans, Guarantees and Venture Capital etc.

The bank started its operation as an 'A' class commercial bank since last year during May

2008. At present, it has total 13 branches including the Head Office at Kamaladi. Further

the bank is planning to have 20 branches within two months period.

1.5.2Vision of DCBL Bank“To be the most trusted bank."

1.5.3 Mission Statement of DCBL Bank "We are committed to provide high quality financial services in ways that create

sustainable added value to all our stakeholders on the basis of superior service, effective

quality management system, innovation, highest level of professionalism based team

works and operational excellence, while maintaining high level of ethical standards as a

socially responsible corporate citizen."

1.5.4 Future plan of DCBL Bank Establish at least new 8 branches within this year to reach 20 branches including 2

branches in remote area as per NRB policy.

Extend the ATM services by increasing its number inside and outside Kathmandu

valley.

Introduce new type of plans and products in deposit and loans

To increase the loan amount by twice in industries like small and cottage industry,

tourism, agriculture and so on.

Increase the quality of risky assets

10

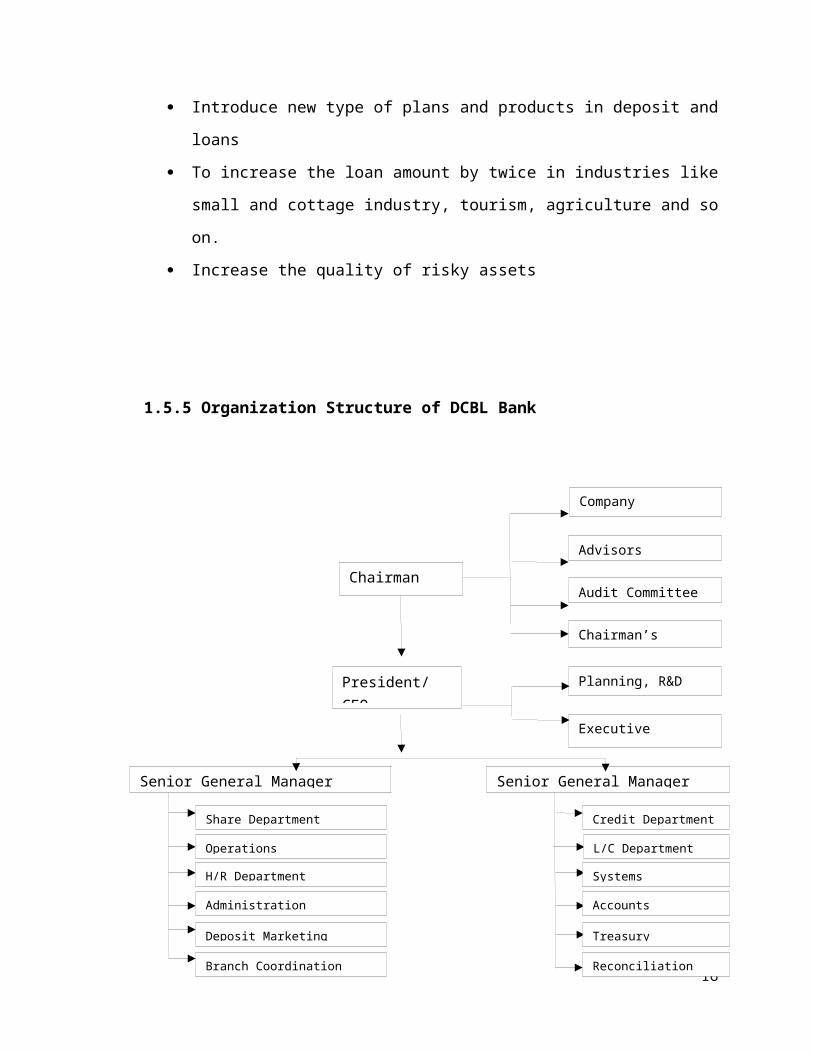

1.5.5 Organization Structure of DCBL Bank

1.5.6 Products and Services of DCBL Bank Banking

Fixed Deposit:

Investment Banking:

o Bonds

o Merchant Banking

Saving Deposit:

11

Chairman /BOD

President/ CEO

Senior General Manager (Operations) Senior General Manager (Credit)

Company Secretary

Advisors

Audit Committee

Chairman’s Secretariat

Planning, R&D

Executive Secretariat

Credit Department

L/C Department

Systems

Treasury

Accounts

Reconciliation

Share Department

Branch Coordination

H/R Department

Administration

Deposit Marketing

Operations

Shuva Lav Bachat

Premium Shuva Lav Bachat

Special Saving Deposit

Nari Saving Deposit

Shareholders Saving Deposit

Current/call account:

Lending

Project financing:

Working capital loan:

Financing Inventory

Financing Receivables

Financing Import Bills

Financing Export Bills

Financing Bill Purchases

Financing Overheads

Term loan

Retail loan

Venture Capital

Other Services

Foreign Exchange Business

Guarantee Business

Advisory and consulting

Services

Letter of Credit

DCBL cash credit

ATM

DCBL prepaid cards

Remittance

12

1.5.7 Areas of Operation at DCBL BankAs an intern I got chance to work in two departments of DCBL Bank. These departments

are:

Treasury Department: The treasury department manages the sources and uses of funds in

case of banks as well as of other organization. So the scope of treasury department is very

wide. In banks treasury department is responsible for the market risk management,

foreign exchange risk management, liquidity management and investment portfolio

management.

The objective of treasury management is to plan, mobilize, monitor and manage the

liquid resources of the Bank to generate income at minimal risk in a manner that is

consistent with the objectives of the Bank which must be drawn up by clearly defining

the responsibilities of each department.

The major functions of Treasury department are as follows:

Manages overall liquidity of the bank.

Ensures that the Cash Reserve Ratio (CRR) is maintained within Central Bank’s

guidelines.

Lending/Borrowing of Currency (Local/Foreign) at local and international market

Deals in Government securities

Deals in Forward Contracts

Manage the Bank’s Investment portfolio.

Advise Foreign Exchange (FX) Rate

Manage Foreign Currency (FCY) position of the Bank

Funding Nostro accounts

Prepare Exchange Rate

Earn from Speculation and interest arbitrage

Documenting all deals

13

Remittance Department: I was placed in the Remittance department for the last five

weeks of my internship. The remittance department is responsible for transferring the

funds from one place to another as required by the customer for different purposes like

household expenses, tuition fee payment, payment for goods or services purchased, loan

repayment, travel expenses, etc. The customers of this department may demand the

transfer of their funds using different modes depending upon their requirement and this

department is responsible to make such transfers.

The major functions of this department are:

Issuance of Bank draft

Fund transfer through swift

Buying and selling foreign currencies

Selling traveler’s cheque

Bills purchasing i.e. purchasing the traveler’s cheque originally sold by the bank

14

Chapter Two

2. ASSIGNMENTS/ ACTIVITIES/ PROJECTS UNDERTAKEN

2.1 ASSIGNMENTS UNDERTAKEN DURING THE INTERNSHIP

2.1.1 IntroductionTreasury Department: As an intern, for the first three weeks of my internship I was

placed in the treasury department. In treasury department I was assigned various tasks

related to lending and borrowing of currencies, buying and selling of foreign currencies,

making CRR reports, entries of other transactions.

2.1.2 Procedure of Activity/ FunctionLending and borrowing deals:

At first the treasury department needs to find out the fund position of the bank by

preparation of the fund statement every day. After that if the fund is short then borrowing

of currencies and if the currencies are long then lending currencies should be undertaken

by the bank. Generally the lending and borrowing of currencies is done through telephone

conversation by front office. Here banks either borrow or lend funds at the interbank

interest rate. Such rate will differ depending upon the type of bank.

After making deal the responsibility of a back office person is to type and print a letter

with reference to the finalized deal. After printing a deal letter bank will be responsible to

send a copy of that letter to another bank. Usually these letters were sent though fax.

After receiving fax from the counter bank the bank needs to fill the deal slip form. After

filling the form, the entries of transaction would be recorded manually as well as in the

system. Lastly letters of banks, manual entries and deal form will be filed and stored.

Buying and Selling of Foreign currencies: Generally the source of foreign currency for

any bank is export and inward remittance and the uses of foreign currencies are import

and outward remittance. In a daily basis banks will be dealing with various transactions

related to sources and uses of foreign funds and the proper management of these funds is

15

another function of treasury department. In order to mange foreign currencies banks

involve themselves in buying and selling of foreign currencies.

At first banks needs to find out their foreign currency position and then their foreign

currency requirement. After knowing the requirement banks involve themselves in

buying and selling of foreign currency. Basically the process of buying and selling

currency is similar to borrowing and lending activities. The banks would make deals

though the telephone conversation and here the exchange rate will be the major factor.

After making deals the letter should be typed, printed and then sent to the counter bank

for reference. The counter bank will also send a fax of that deal letter. After receiving

such deal the foreign currency deal slip together with manual transaction form would be

filled and transaction would be entered in the system. Lastly the transaction, deal slip

would be filed and stored manually.

Making CRR reports:

Generally CRR reports were prepared in the excel sheets in the computer. These sheets

were in build sheets in the system. While making these reports the total local currency

deposit for the first week is calculated and then the 5.5% balance has to be maintained in

the third week.

Entries of other transaction:

The entry of other transactions includes IBT and IDT transactions. The IBT transactions

are inter branch ticket and IDT transactions are inter department transactions as the other

departments and branch were required to go through the treasury department whenever

the transaction would touch the NOSTRO accounts. For example the transaction related

to issue of NRB cheque. Generally the manual general entries and the computerized

entries of these transactions would be made in the system by using pumori plus.

2.1.3 My Role in the Activity/ FunctionLending and borrowing deals:

As an intern my task in lending and borrowing deals would be to type, save and print

letter of deal agreement. The format of such letter was already available in the system and

16

my task as an intern was to make modification on that letter and save it. After printing

deal I was responsible to send copy of deal or contract to counter banks. Also, after

receiving the fax from counter bank I was responsible to fill the deal slip. Finally I was

responsible to make manual entry of the transaction.

Buying and selling of foreign currencies:

As an intern my task in lending and borrowing deals would be to type, save and print

letter of FCY deal agreement. After printing deal I was responsible to send copy of FCY

deal letter or contract to counter banks. After receiving the fax from counter bank I was

responsible to fill the FCY deal slip together with the manual entry of the transaction.

Making CRR Reports:

While making CRR Reports I was only required to make calculations in excel sheet.

While calculating I would need balance at NRB and banks deposits other than margin

account and FCY balance. So while making CRR reports I took the input from the

consolidated balance sheet as this would contain deposit other than margin and FCY

balance. Similarly balance at NRB would be taken from the NRB website.

Entries of other transaction:

In case of entries related to other transaction I was assigned to make the manual general

entries of these transactions.

2.1.4 Outcome of Activity/ FunctionThe major outcome of my assignment at treasury department was proper management of

funds. Apart from this outcome particular outcome is as follows:

Prepared one CRR report in a week

Manually made journal entries of about ten transactions per day

Handled about four to five deals related to lending and borrowing funds in a day

Handled about three to four purchase and sell of foreign currency in a day

17

2.1.5 Conclusion and RecommendationObservation

When I was in treasury department I observed that this department didn’t have direct

contact with the customers but their function would indirectly affect the customers. For

instance whenever customer would come for issue of NRB cheque for custom clearance

then the customers would visit remittance department and the staffs from remittance

department would visit treasury department for issuance of NRB cheque. Further staffs

from the remittance would use exchange rate actually published by treasury department.

Further staffs of remittance department were required to ask for exchange rate when there

would be involvement of funds above USD 2000. Moreover treasury department would

perform work related to reporting to NRB, maintaining liquidity position of the bank,

managing foreign currency and so on. So this department would be dealing with other

banks including NRB, staffs of other department and branches rather than general

customers.

Experience

Working in treasury department was entirely new experience for me. As function of

treasury department was very wide and getting knowledge regarding every aspect of

treasury was almost impossible in the limited time frame of three weeks so I concentrate

myself only in lending and borrowing deals, buying and selling of foreign currencies,

making CRR reports. Except this, I was also involved in making manual entries of

transactions.

Suggestion

While I was working in treasury department I found that the space allocated for this

department was quite congested due to which people from all levels were placed by the

organization in the same room. So in my opinion this department should be placed where

there are more space.

18

In treasury department there was no separate scan machine and staffs were frequently

required to visit another department and disturb staffs of another department for the

purpose of scanning. So I think organization should provide separate scanning machine to

this department.

2.1.6. Learning from the Activity/ FunctionApart from the activity itself I learned following things at Treasury Department

In professional world we should complete our work within deadlines

We work in teams and the overall outcome is considered of more importance

We should be punctual, disciplined and polite with others

We should be informative

We should have learning nature as environment changing frequently outside in

working environment

2.2. INTRODCTIONRemittance Department: As an intern, I spend about 5 weeks of my internship period in

remittance department. In the remittance department I was directly or indirectly involved

in activities related to purchase and sell of foreign currencies, making drafts, making

swift transfers and purchase and sell of traveler’s cheque.

2.2.1 Procedure of Activity/ Function:A. Draft

Bank Draft is a Cheque drawn by a bank on one of its own branch or correspondent

banks authorizing the latter to pay a specific amount to the individual named in the draft.

At the paying bank, it is treated as any other cheque and processed through local clearing

system. There are various types of bank draft. They are INR draft and FCY draft. Both

INR and FCY draft are of personal, advance payment and bill payment.

19

1. Procedure of personal draft

Providing the application form

Verification of application form, personal identity cards and supporting

documents if document is necessary

Making calculations by converting INR or FCY amount to LCY amount and

adding commission to it

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

Make and print draft

Get the draft signed by two authorized person of the bank

Get two photocopies of signed draft

Provide one photocopy and original draft to the customer

Ask the customer to sign in photocopy of draft upon the receipt

Make necessary journal entries in the system about the transaction

Take the entries for approval

After approval filing the transaction

Sending Confirmation to NOSTRO Bank

a. NRB Regulation of INR Personal Draft

Upto INR 25,000 with citizenship or passport.

For draft over INR 25,000 supporting documents like Performa Invoice is needed

Draft Application & INR purchase form should be filled

Apply draft issuance commission as per bank

Apply selling rate to convert into equivalent LCY

Current available Nostro are SCB & ICICI

b. NRB Regulation of FCY Personal Draft

Upto USD 1,000 on following documents

Copy of Citizenship or Passport

20

Documents supporting purpose of payment like bill/invoice/ letter/ filled college

forms etc

Documents must clearly show the exact amount and name of beneficiary for

whom the draft is being prepared

Beneficiary must be an institution (not an individual)

Draft must be account Payee

2. Procedure of Advance Payment Draft

Providing the application form

Verification of application form

Verification of proforma invoice

Filling B.B.N 4(Ga) in 3 copies in case of INR draft and B.B.N. 3 (Ka) in case of

FCY draft

Making calculations by converting INR amount to LCY amount and adding

commission to it

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

Make and print draft

Get the draft signed by two authorized person of the bank

Get two photocopies of signed draft and one photocopy of proforma invoice

Provide one photocopy and original draft to together with first and second copy of

B.B.N 4(Ga)and B.B.N. 3 (Ka) to customer incase of INR draft FCY draft

respectively

Ask the customer to sign in photocopy of draft upon the receipt

Make necessary journal entries in the system about the transaction

Take the entries for approval

After approval filing the transaction

Sending confirmation to NOSTRO Bank

a. NRB Regulation of INR Advance Payment Draft

21

Where payment is done to the exporter before the arrival of goods

No supporting documents required upto INR 16,000

For Draft over INR 16,000

Performa Invoice (only upto Performa invoice value)

Draft Application & INR purchase form should be filled

B.B.N 4(Ga) should be filled by us in 3 copies (First & Second copy is handed

over to the customer & third copy for our record)

After arrival of goods, applicant must bring one certified copy of B.B.N 4 (Ga)

along with “Pragyapan Patra”

b. NRB Regulation of Advance Payment USD Draft

For FCY draft over USD 30,000, NRB approval must be taken

Both applicant & beneficiary must be firm (not individual)

Documents required

o Firm Registration Certificate

o Income Tax Clearance Certificate

o Performa Invoice stating the type, quantity, price of goods duly signed and

stamped by the beneficiary

B.B.N. 3 (Ka) and Draft Application form

Prepare the draft/ SWIFT message/ TT

Hold 10% margin

After arrival of goods:

o Fill up B.B.N. 4 (Ka) in triplicate

o Prepare account payee NRB Cheque equivalent to 10% margin held

previously in favor of respective custom office

o Hand over two copies of B.B.N 4(Ka) to the customer along with NRB

Cheque

o Customer must return certified copy of B.B.N. 4(Ka) along with

pragyapan Patra within 90 days of issuance

o Report to NRB if not done so

22

Procedure of INR Bill Payment Draft

Providing the application form

Verification of application form

Verification of documents such as invoice, Pragyapan Patra, custom clearance

bill, airway bill

Filling INR purchase form

Making calculations by converting INR amount to LCY amount and adding

commission to it

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

Make and print draft

Get the draft signed by two authorized person of the bank

Get two photocopies of signed draft

Provide one photocopy and original draft to the customer

Ask the customer to sign in photocopy of draft upon the receipt

Make necessary journal entries in the system about the transaction

Take the entries for approval

After approval filing the transaction

Sending confirmation to NOSTRO Bank

NRB Regulation of INR Bill Payment Draft

Where payment is done to the exporter after the arrival of goods in Nepal

Documents required

Invoice

Pragyapan Patra

Custom Clearance Receipt

Airway Bill (If by air)

B. SWIFT Transfers

23

The Society for Worldwide Interbank Financial Telecommunication ("SWIFT") operates

a worldwide financial messaging network. It is a cooperative society which was founded

in Brussels in 1973, supported by 239 banks in 15 countries. It started to establish

common standards for financial transactions and a shared data processing system and

worldwide communications network. The majority of international interbank messages

use the SWIFT network. SWIFT is solely a carrier of messages. It does not hold funds

nor does it manage accounts on behalf of customers, nor does it store financial

information on an on-going basis. As a data carrier, SWIFT transports messages between

two financial institutions. This activity involves the secure exchange of proprietary data

while ensuring its confidentiality and integrity.

Procedure of SWIFT Transfers

Swift transfers can be personal, advance payment and bill payment. While transferring

funds for customers through SWIFT, all the preliminary steps and regulations are exactly

similar to issuance of a draft. Instead of preparing a draft, banks prepare MT103.

C. Travelers Cheque

Travelers cheque is a preprinted, fixed-amount cheque designed to allow the person

signing it to make an unconditional payment to someone else as a result of having paid

the issuer for that privilege.

At the time of purchase, purchaser has to sign on the cheque at the prescribed place. At

the time of encashment, he has to countersign at the encashing place and fill in the

relevant data. He might also present photo identification to encash the travelers’ cheque.

Procedure of issuing Travelers cheque against passport and Air ticket

Asking customers to fill the application form

Verification of passport and air ticket

Making calculations by converting FCY amount to LCY amount and adding

commission to it

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

24

Making endorsement in air ticket and passport

Make photocopy of endorsed documents

Ask customer to fill form of travel cheque issuing company together with

necessary signature

Filling necessary details related to issued travel cheque in the form

Asking customer to sign in the travel cheque

Providing travel cheque to the customer

Making record of the transaction

Procedure of selling of FCY Cash

Asking customers to fill the application form

Verification of passport and air ticket

Making calculations by converting FCY amount to LCY amount

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

Making endorsement in air ticket and passport

Make photocopy of endorsed documents

Providing FCY cash to the customer

Making record of the transaction

Procedure of buying FCY Cash

Asking customers to fill the application form

Verification of passport

Asking customer to provide FCY cash

Making calculations by converting FCY amount to LCY amount

Filling the cash deposit slip and asking customers to sign the slip

Make photocopy of passport

Providing LCY cash to the customer

Making record of the transaction

My Role in the Activity/ Function

25

Personal Draft

Providing the application form

Verification of application form, personal identity cards and supporting

documents if document is necessary

Making calculations by converting INR or FCY amount to LCY amount and

adding commission to it

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

Make and print draft

Get the draft signed by two authorized person of the bank

Get two photocopies of signed draft

Provide one photocopy and original draft to the customer

Ask the customer to sign in photocopy of draft upon the receipt

Advance Payment Draft

Filling B.B.N 4(Ga) in 3 copies in case of INR draft and B.B.N. 3 (Ka) in case of

FCY draft

Making calculations by converting INR amount to FCY amount and adding

commission to it

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

Make and print draft

Get the draft signed by two authorized person of the bank

Get two photocopies of signed draft and one photocopy of proforma invoice

Provide one photocopy and original draft to together with first and second copy of

B.B.N 4(Ga)and B.B.N. 3 (Ka) to customer incase of INR draft and FCY draft

respectively

Ask the customer to sign in photocopy of draft upon the receipt

26

SWIFT Transfers:

All the activities assigned to me in swift transfer was same as that of draft except I was

not required to make and print draft as message as we would send message using SWIFT

and I didn’t carry out the function of writing swift message.

Travel Cheque

Asking customers to fill the application form

Verification of passport and air ticket

Making calculations by converting FCY amount to LCY amount and adding

commission to it

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

Making endorsement in air ticket and passport

Make photocopy of endorsed documents

Selling FCY Cash

Asking customers to fill the application form

Verification of passport and air ticket

Making calculations by converting FCY amount to LCY amount

Asking customer to make payment

Filling the cash deposit slip and asking customers to sign the slip

Making endorsement in air ticket and passport

Make photocopy of endorsed documents

Providing FCY cash to the customer

Buying FCY Cash

Asking customers to fill the application form

Verification of passport

Asking customer to provide FCY cash

Making calculations by converting FCY amount to LCY amount

Filling the cash deposit slip and asking customers to sign the slip

27

Make photocopy of passport

Providing LCY cash to the customer

2.2.2 Outcome of the AssignmentThe major outcome of the assignment was satisfied customers. Apart from this the other

outcomes are:

Preparation of five draft on an average on daily basis

Dealing with five customers on an average related to sell of Travelers' cheque and

foreign cash on daily basis

Bills purchase related transaction occurred twice during five week time frame.

Dealing with five customers in a weeks

2.2.3. Conclusion and RecommendationObservation:

In remittance department I observed that staffs of this department were really busy and I

also found that some staffs in this department were really motivated to work whereas

some were not that motivated to work. I also observed that staffs of this department

would have direct interaction with customers. I also found that staffs of this department

were involved in making payments related to IME and Himal Remit, purchase and sell of

foreign currency and travel cheque, making draft and swift transfer. I also observed that

staffs of this department had to work on noisy environment. Further I also observed that

people who are emotionally stable would fit in this type of jobs.

Experience

In Remittance department I could gain experience regarding preparation of draft, swift

transfers, buying and selling of FCY cash and Travelers cheque of American Express,

payment of IME and Himal Remit. Apart from these experiences I could also experience

that in the actual working environment we should always listen to customers even though

28

they are wrong. I also experience that we should be polite with customers and focus on

quality of work more than our speed while working.

Suggestion

In Remittance department I found that photocopy machine and printer was damaged but

the administrative department was not replacing that machine due to which we were

compelled to visit other departments frequently for the photocopy and printing and this

was reducing the efficiency of the staffs.

I also found that there was not adequate filing cabinet in this department due to which

files were placed in the floor randomly so I think that the administrative department

should provide one filing cabinet for this department.

Learning from the Activity

Apart from the activity itself I learned that

The various departments and units of banks were interrelated as studied in books.

While dealing with customers we should be careful as they are the people who

will influence others decision either by good word of mouth or bad.

When we are new to particular place, sometime even easy thing can be difficult to

us because we are nervous, unaware and so on.

It becomes a challenge for us when we have assignments without resources and

much authority in achieving that task.

CHAPTER THREE

3. PROGRAM AND WORKPLACE RELATIONSHIP

MBA program is partially theory and partially practical based program. During MBA we

are given to carry out different types of research and project works in teams and also we

undergo eight week internship designed by the Prokhara University and we can

29

categories it as gaining of practical knowledge. During my internship through

observation, experience and analysis I came to know that there were many similarities

between the working environment that we talk in the book and real world. Further I also

found that many of the topics that we have learned during our MBA program are useful

in the practical world. During the internship period I found the significant use of

following theoretical knowledge. They are

Financial Institution and Market

When I was in treasury department I found that the knowledge that we had gained in the

subject was applicable in this department as we had gained theoretical knowledge about

the asset liability management and management of various types of risk by the banks and

practically I found that the basic function treasury department was of managing asset and

liability as well as various risk of the bank.

Financial Management

While working in treasury department I also found that banks also carry out fundamental

analysis before making any type of investment decision. For instance they calculate

intrinsic value of bond, share etc before making investments.

Emerging concepts of Management

While I was in treasury department I also found that banks also evaluate another firm by

conducting SWOT and PESTLE analysis of another firm before making investment

decisions because these factors were considered as major factor that would influence

banks investment decision.

The internship program has provided practical knowledge regarding working culture,

environmental influence to organization, and organization structure and so on and I was

able to observe this particularly because we had learned the theories and concept related

to these terms in many courses including emerging concepts of management. In fact

30

internship helped me to gather knowledge regarding relevance of this theories in actual

world.

Financial Accounting

During my internship I found in both treasury and remittance department that the

transactions were entered using basic accounting principle which we had learned in

financial accounting. I had learned that according to accounting principle owners and

organization was treated separately. Further in reality I found that departments as well as

branches were treated as separate while recording transaction.

In treasury department I was in fact using consolidated trial balance for the preparation of

CRR reports and I think we learned preparation of trail balance in financial accounts and

the outcome of trial balance was used further in treasury department to produce other

reports.

Managing Information System

While working in bank, in both the departments I found that there was proper

management of information. For instance the transactions were recorded manually, filed

and stored and these records were retrieved whenever such information would be needed

in the organization. While I was in remittance department whenever the customer would

come for the tuition fee payment for at least second time then before sending the amount

for tuition payment we were required to check the previously stored documents before

sending the amount.

Business Development Plan

In case of any corporate world business development plan that we studied in MBA has

great significance. I found its relevance while I was working in treasury department.

During my working period one person from Manakamana Remit visited treasury

department so as to convince the management to have business tie ups with his new

Remit office that was yet to be established and with my great surprise my supervisor of

31

treasury department was asking that person to bring concrete business plan with easy to

understand financial projections. This incident helped me to understand the significance

of business plan in the corporate world.

Managerial Communication

In both the department of organization I found great significance of managerial

communication as this subject taught us about the oral or verbal communication and

written communication. I basically found that managing our body language, gestures,

attitude, voice, tone, emotions etc is very much necessary while dealing with customers

of the organizations. If we fail to convey appropriate verbal and non verbal signals to our

customers our customers may get irritated and resulting into bad mouthing of the

organization so lessons we have learned in managerial communication is of great

significance. Similarly in case of written communication also things we have learned like

writing short and to the point, avoiding grammatical and spelling mistakes were taken

care in real world. So I found this particular course vary much useful in the practical

world.

Principles of Marketing

In the course principle of marketing we had basically learned about various types of

promotional activities that organizations use so as to attract their customers and in real

world also I found that organizations were using concepts of marketing especially in

promoting their product and services. While working, I found the significance of

marketing in Remittance department. As DCBL Bank was one of the agents of IME and

during Dashain festival I found that in order to promote their remittance service IME had

come up with promotional activities and under these activities the firm was providing key

ring, dairy, booklet of IME and so on.

Human Resource Management

In our subject Human resource management we learned about how organizations can

motivate their staffs. While working in bank I could sense that at DCBL Bank there was

good human resource management. As I found that staffs were well motivated and I also

32

felt that the major source of motivation for them was good pay, good relationship with co

worker and higher level staffs, timely promotion on the basis of performance and so on.

In our books also we have read same factors as sources of motivation and in practical

world also I found same factors as motivating factors.

Organizational Behavior

In organizational behavior we learned theories on organizational culture, leadership

styles, group behavior and individual behavior and while comparing these theories in

practice I found their relevance. For instance I found in Remittance department there

were some employees who were free riders. I also found that in professional world we

work in the team and the effort of team is considered than effort of single person. I also

found that heads of different department had different leadership styles. For instance I

found that head of treasury department very much democratic and participative.

Service Sector Management

In Service Sector Management we learned about overall management of service sector. In

this course we have basically learned that employees should be motivated as they are the

front line people dealing directly with customers and delivering quality services totally

dependent upon the these staffs so we learned that these staffs should be properly trained

and motivated. While I was working in the organization I found that banks often

organized trainings to their front line staffs, make them share profits in the form of bonus

and this had really motivated them to deliver quality services.

In my internship program I could achieve more than I expected. Internship experience

gave me knowledge regarding the work, working procedure etc. This practical knowledge

has helped me to develop confidence, build social relationship, and enhance interpersonal

communication skills and so on. Moreover this internship program has helped me to

bridges the gap between theoretical and work knowledge by making me aware about real

life situation.

33

34

CHAPTER FOUR

4. CONCLUSION

During the period of internship I leant a lot about the practical working environment.

Particularly I learned about banking operations and this helped me to enhance my skills

and knowledge in the banking field. I think that the eight week of internship period will

definitely help me in the future career as it has helped me gain basic knowledge about

banking and increased my confidence in carrying out functions of bank.

Basically I learn about basic operations of banking though experience and observation as

I was given only some of the task as my assignment. By doing the assigned tasks in the

Bank I was able to learn about the working procedure of that task. However I learned

many things through observation. So both the observation and experience has helped me

in enhancing my knowledge about banking. Especially in treasury department every day I

would get new information regarding the market and these information were particularly

related to banking rules, regulations and NRB circulars. Whereas in Remittance

department staffs rarely discussed about these matters as we would be busy in handling

the flood of customers.

Apart from these I could learn the corporate culture, working environment of the

organization especially working environment in Bank. During my internship my overall

experience was very good because the staffs were really helpful and they were ready to

help me whenever I would face difficulties in carrying out my functions or assignment.

Further they never became rude at my mistakes. The staffs also provided me conceptual

knowledge about their respective department. They were friendly with everyone. During

my whole internship period I found them happy, cheerful motivated towards their

assigned job. Even though I was only intern they made me feel I was the part of the

organization. They even organized farewell party for me at the last day of my internship

which really inspired me. In this way my overall learning at DCBL bank was above what

I expected.

35

36

APPENDIX

CAPITAL STRUCTURE

Authorized Capital Rs. 2,000,000,000

Issued Capital Rs. 1,661,184,000

Paid-up Capital Rs. 1,655,288,900

BRANCHES

DCBL Bank LimitedKathmandu Plaza, First Floor, Kamaladi GPO Box: 7716, Kathmandu, Nepal Tel no: 4168605, 4168606, 4168607, 4168608 4168610, 4168612, 4168613, 4168615 Fax: 977-1-4168609 Swift : DCBNNPKA E-mail: [email protected]

New Road BranchMeera Home, Khichapokhari, Kathmandu, NepalTel: 4233119, 4233120Fax: 4233124E-mail: [email protected]

Lalitpur BranchGabahal, Ward No. 18, Lalitpur BranchTel: 5522881, 5522876, 5522892E-mail: [email protected]

Pokhara BranchNew Road, Pokhara, NepalTel: 061-525252, 522827Fax: 061-522827Teku BranchTeku

Banepa BranchPanauti Road, Ward No. 10, Banepa, KavreTel: 011-660844, 660845E-mail: [email protected]

Bhairahawa BranchMilan Chowk, Bhairahawa, NepalTel:071-527450Fax: 071-527620Email: [email protected]

Bhotahity BranchBhotahity, KathmanduTel:4250445Fax: 4250602Email: [email protected]

NarayanGarh BranchShaidchowk, ChitwanTel:056-522736Fax: 056-522738Email: [email protected]

Itahari BranchDharanRoad, Itahari

37

Tel:4250806Fax: 4250603Email: [email protected] BranchSanepaTel:5544639Fax: 5544640Email: [email protected]

Tel:025-587278 Fax: 025-587275 Email: [email protected]

Dharan BranchCollageRoad, DharanTel:025-525004Fax: 025-530908Email: [email protected]

38

![Curs Pentru - Control Intern Si Audit Intern[1]](https://static.fdocuments.net/doc/165x107/5571f3b749795947648e7a21/curs-pentru-control-intern-si-audit-intern1.jpg)