Interaction of Debt Agency Problems and Optimal … of Debt Agency Problems and Optimal Capital...

26

JOURNAL OF RNANCIAL AND QUANTITATIVE ANALYSIS VOL 38, NO. Z JUNE 2003 COPYRIGKT 2003, SCHOOL OF BUSINESS AOMINISmATION, UNIVERSFTY OF WASHINGTON. SEATTLE, WA 9B195 Interaction of Debt Agency Problems and Optimal Capital Structure: Theory and Evidence Connie X. Mao* Abstract E>oeg more leverage always wcfsen tbe debt ageocy problem? This paper ptesents a unified analysis that acconntB for both risk-shifting and nixler-iiivestiiient ddbt agency problems. Forfirmswith positive marginal volatility of investment (defined as the change in cash flow volatility cone^ponding to a change of itwestment scale), equity holders' risk-shifting in- centive will midgate the under-investment problem. This inqdies that, cotUrary to ccmven- tional views, the total agency cost of debt does not unifcsmly increase with leverage. This model fiiither predicts tbat, for Mg^ growthfirmsin which the under-investment problem is severe, the optimal debt ratio is positivelyrelatedto the marginal volatility of investmenL Empirical results suppmt this prediction. I. Introduction Two principal debt agency problems have been identified in the literature. One is the risk-shifting or asset substitution problem,firstidentified by Jensen and Meckling (1976). In their views, equity can be seen as a call option on the firm and call values increase with the volatility of the underlying asseL This creates an incentive for equity holders to shift thefirm'sinvestments into high risk projects. The other is the under-investment incentive. Myeis (1977) argues that, when a firm's leverage increases, equity holdeis have an incentive to under-invest in positive net present value (NPV) projects. This occurs because equity bolders bear the costs of investment but capture only part of the net benefit, and the rest accrues to bond holders. Rational (tebt holders arc aware of the equity holders' incentives to shift risk and under-invest, thereby pricing the debt accordingly and demanding a higher rate of retum. ITius, the adverse consequences of debt agency problems *Mao, nxxn1nie9sbm.ten9le.edu. Fox Scbool of Business and Management, Iteiple Univetsity, Ptiiladelphia, PA 19122. I diank Robert Jarrow, Wanen Bailey, Haitao U , Jaime Zender, Micbael Alderson, and seminar participants at Cornell University, Univenity of Arizona, University of Iowa, Univnsity of Pittsbuigb, Tkilane Univexsity, Temple University, University of Massachusetts, Amhent, Baruch College, the 1999 Financial Management Association mw^ngn, and tiie 1999 Soudietn Fi- nance Associadon meetings for belpful comments and discussions. I also tbanlc Jooatban Karpoff (tbe editor) and TiKHnas Cbemmanur (tbe rcfoee) for their insigirtfnl comments and suggestiuis. All errors are solely mine. 399

Transcript of Interaction of Debt Agency Problems and Optimal … of Debt Agency Problems and Optimal Capital...

JOURNAL OF RNANCIAL AND QUANTITATIVE ANALYSIS VOL 38, NO. Z JUNE 2003COPYRIGKT 2003, SCHOOL OF BUSINESS AOMINISmATION, UNIVERSFTY OF WASHINGTON. SEATTLE, WA 9B195

Interaction of Debt Agency Problems andOptimal Capital Structure: Theory andEvidence

Connie X. Mao*

Abstract

E>oeg more leverage always wcfsen tbe debt ageocy problem? This paper ptesents a unifiedanalysis that acconntB for both risk-shifting and nixler-iiivestiiient ddbt agency problems.For firms with positive marginal volatility of investment (defined as the change in cash flowvolatility cone^ponding to a change of itwestment scale), equity holders' risk-shifting in-centive will midgate the under-investment problem. This inqdies that, cotUrary to ccmven-tional views, the total agency cost of debt does not unifcsmly increase with leverage. Thismodel fiiither predicts tbat, for Mg^ growth firms in which the under-investment problemis severe, the optimal debt ratio is positively related to the marginal volatility of investmenLEmpirical results suppmt this prediction.

I. Introduction

Two principal debt agency problems have been identified in the literature.One is the risk-shifting or asset substitution problem, first identified by Jensen andMeckling (1976). In their views, equity can be seen as a call option on the firmand call values increase with the volatility of the underlying asseL This creates anincentive for equity holders to shift the firm's investments into high risk projects.The other is the under-investment incentive. Myeis (1977) argues that, whena firm's leverage increases, equity holdeis have an incentive to under-invest inpositive net present value (NPV) projects. This occurs because equity bolders bearthe costs of investment but capture only part of the net benefit, and the rest accruesto bond holders. Rational (tebt holders arc aware of the equity holders' incentivesto shift risk and under-invest, thereby pricing the debt accordingly and demandinga higher rate of retum. ITius, the adverse consequences of debt agency problems

*Mao, nxxn1nie9sbm.ten9le.edu. Fox Scbool of Business and Management, Iteiple Univetsity,Ptiiladelphia, PA 19122. I diank Robert Jarrow, Wanen Bailey, Haitao U, Jaime Zender, MicbaelAlderson, and seminar participants at Cornell University, Univenity of Arizona, University of Iowa,Univnsity of Pittsbuigb, Tkilane Univexsity, Temple University, University of Massachusetts, Amhent,Baruch College, the 1999 Financial Management Association mw^ngn, and tiie 1999 Soudietn Fi-nance Associadon meetings for belpful comments and discussions. I also tbanlc Jooatban Karpoff(tbe editor) and TiKHnas Cbemmanur (tbe rcfoee) for their insigirtfnl comments and suggestiuis. Allerrors are solely mine.

399

400 Joumai of Financial and Quantitative Anaiysis

are entirely bome by the equity holders themselves dnough the increased cost ofdebt financing.

The implications of debt agency problems for an optimal c^tal structurehave been widely studied in the litraature. In their seminal p^)er, Jensen andMeckling (1976) propose that a firm's optimal debt-equity ratio is achieved byequating the marginal agency cost of debt and the marginal agency cost of equity.This theory assumes that the agency cost of debt increases monotonically withthe amount of leverage the firm employs.' The relationship between die leverageratio and debt agency cost has been explored by several studies, but previousresearch typically focuses on only one type of the debt agesacy ixoblem, either therisk-shifting or the under-investment problem. Gavish and Kalay (1983) adopt avery simple one-period model to examine the relationship between leverage andthe severity of the risk-shifting problem. They argue that equity holders' risk-shifting incentive is not an increasing function of the leverage ratio. Green andTalmor (1986) restate the problem in a similar model context, and find that Gavishand Kalay's original conclusion is a misinterpretation of the result. Their studysuggests diat more debt aggravates shareholders' incentive to take risk. This isconsistent with the original conjecture of Jensen and Meckling. Similarly, Myers(1977) also demonstrates a positive relationship between leverage and the agencycost of under-investmenL

Given the properties of the risk-shifting and under-investment problems ex-amined in isolation, it is often asserted that mare levraage exacerbates the debtagency problem. Such an assertion assumes that the two debt agency problemsdrive firms' investment decisions in the same direction, and n^lects the potentialinteraction between the two. Suppose that the volatility of a firm's cash fiowsincreases with investment scale, or that a firm faces a potential project with cashfiows positively correlated with the cash fiows from its existing assets. In thiscase, increasing the scale of investment would increase the total volatility of thefirm's cash flows, in a leveraged firm, equity holders would increase investment toincrease firm risk, while their under-investment incentives discourage them frominvesting. Therefore, the two incentive problems will affect the firm's investmentand debt policy in different directions.

The potential interaction between the under-investment problem and the risk-shifting incentive has not been completely ignored. Myers (1977) points out that,if investment increases the variance of project return, equity holders' incentiveto shift risk wiU mitigate the under-investment problem. He concludes: "Theimpact of risky debt on the market value of the firm is less for firms holdinginvestment options on assets that are risky relative to the firms' present assets. Inthis sense we may observe risky firms borrowing more than safe ones" (Myers(1977), p. 167). Myers' argument suggests a positive relationship between theoptimal debt level and business risk. Despite several attempts to test this idea,however, the empirical evidence is ambiguous (e.g., see Long and Malitz (1985),Bradley, Jarrell, and Kim (1984), and Titman and Wessels (1988)). I argue that

'As Jensen and Meckling comment. "We are fairly confident of our arguments regarding the signsof the first derivatives of the functions . . . " (Jensen and Meckling (1976), p. 3A6). Here "the func-tions" refer to the debt agency cost function and the equity agency cost function.

Mao 401

this is because the interaction between the two debt agency problems has not beenfully understood.

To address this lack, I develop a simple model that captures both the dsk-shifting and the under-investment problems. In the model, a firm faces a dis-cretionary investment decision, and the terminal firm value is a random variablewhose mean and volatility both depend on the size of the irrvestmenL Thus therisk-shifting and under-investment incentives will affect the investment decisionof a leverage firm in the same or different direction, and the total agency cost ofdebt will depend on the tradeoff between the two incentive problems.

A key result of the model is that, if the volatility of project cash flows in-creases with investment scale, risk-shifting by equity holders will mitigate theunder-investment problem. This implies that, contrary to the conventional wis-dom, the total agency cost of debt is not monotonically increasing with leverage.Furthermore, the model predicts a unique relationship between the optimal debtlevel and the marginal volatility of investment (MVI), which I define as die changeof cash fiow volatility corresponding to a change of iavestment scale. For highgrowth firms, the optijnal level of debt increases with the magnitude of MVI whenMVI is positive, but declines with the magnitude of MVI when MVI is negative. Itsuggests a positive relationship between the optimal debt level and MVI. For lowgrowth firms, the optimal level of debt decreases with the magnitude of MVI forbotii positive and negative MVI firms. It suggests a negative relationship betweenthe optimal debt level and MVI when MVI is positive, and a positive relationshipbetween the optimal debt level and MVI when MVI is negative.

I test the model's predictions using cross-sectional data from Compustat(1976-1995). Empirical findings support these predictions. For high growthfirms, I find a significant positive relationship between leverage and MVL Forlow growth firms, I observe a significandy negative relationship between leverageand MVI when MVI is positive, and a weakly positive relationship between thetwo when MVI is negative.

The paper is organized as follows. Section n presents a one-period discrete-time model that captures both the risk-shifting and under-investment problems.Section ni reviews and interprets empirical tests and results. Section IV concludesthe paper.

IL The Model

I examine the effects of leverage on a firm's investment decision in a one-period discrete-time model. Ib higjilight the central canfiicts of interest betweenequity holders and bond holders, I abstract from many important influences onfinancial decisions, such as risk aversion, dividend policy, taxes, agency costsof equity, and deadweight costs of bankruptcy. The model, which allows fora simultaneous analysis of the Hsk-shifting and under-investment pn^lems, isdescribed by the following assumptions:

402 Journai of Financial and Quantitative Analysis

i) Equity holders control the firm, and the managerial objective is to maximizethe value of equity.

ii) lliere are no taxes or bankmptcy costs, and there is no infonnation asymme-try between insiders and outside investors.

iii) Investment policy cannot be established (or specified) contractually ex arrte,

iv) All economic agents are risk neutral, and the risk-fiee rate is zero.

v) Investment decisions are made at time 0, and the firm liquidates at time 1,

Consider a firm with a single investment prqjecL Let

(1) * i =

is the end-of-periodcash flow at time 1, which is also the terminal valueof the firm; Jko measures the investment scale and is chosen by equity holders attime 0; £i is a random variable that represents the state of nature at time 1 resultingfiom randomness in technology, in the prices of inputs and outputs, and in thedemand fodng the firm, I assume that ei is a random variable with continuousdensity function/(£i), a mean of zero, and a variance of one. Given equation (1),the terminal firm value, j^i, is a random variable whose mean and volatility bothdepend on the initial investment, ito-1^ ensure limited liability for equity holders,I assume that . i = (ifco) + <T(ko)ei > 0 fbr all £i and ko. This implies that

where £* is the low bound of £i.I assume that the mean function of the firm's cash fiows, ju(iko)> is a twice

continuously differentiable function with ii'(ko) > 0 and ii"{ko) < 0. TUs isconsistent with many types of technologies, such as a Cobb-Douglas productionfunction. I assume that (T{ko) is once differentiable in ito, a°d I call its first deriva-tive [o''(Jto)] the marginal volatility of investment (MVI). The sign on a'(ito) isunrestricted, since it may differ across firms or industries. In fact, the relationshipbetween the volatility of cash fiows and the investment scale may dqwnd on afirm's investment opportunity set and the stochastic driving forces of cash fiows.

I assume that, before time 0, the firm issues equity and debt to raise capitalfor investment in the project Suppose it issues zero-coupon bonds that have a totalface value of D and mature at time 1. As I have assumed above, monitoring andbonding costs exclude die possibility of contracting equity holders to a particularito ex ante. Therefore, at time 0, for a given level of debt, D, equity holders wouldinvest ito units of capital so as to maximize the net present value of their claims.

an important assumption to cast tbe cooflicts of interest between equity holders and debtholders. In feet, managers may pursue their own interests instead of those of eqtiity holders. Thereare numerous studies of the agency costs of managerial discretion, e.g., Stulz (1990). Along anotherline of the research on optimal capital stmcttire under asymmetric infbrmaticn, Dj nvig and Zender(1991) argue that the optimal choice cf managerial compensation contract may resolve the ctnflicts ofinterest among different classes of stakeholders of firm. These are interesting issues, hut beyond thescope of hJK study.

^As in Myers (1977), Long and Malitz (1985), Brander and Lewis (1986), and Kim and Malcsi-movic (1990), the debt level is [nedetermiiied cr exo^nously given at the time the investment decision

Mao 403

Required capital outlay is [noportional to the size of investment, Coko, where Cois the unit cost of c^tal.*^ If the proceeds from the sale of securities in the firstplace are less than the required capital outlay, the firm could issue more equity attime 0. On the contrary, if the proceeds are larger than the costs of investment,the firm could pay out the diffeience as a dividend at time 0.

A. Debt Agency Problems and Investment Policy

To demonstrate how debt agency problems influence investment policy, Ievaluate the investment decision, i o. fiist for an all-equity firm, and then for aleveraged firm.

1. All-Equity Firm

I denote the net present value of an all-equity firm at time 0 as NPV(/ko).where

(3) NPV(Ab) =

At time 0, an all-equity firm would choose an investment policy, k^, to maximizenet present value. Then k^ must satisfy the following.

(4, »SM = ,.(^)-C. = 0.

Equation (4) suggests that optimal investment is achieved at the point where themarginal retum on investment equals its marginal cosL Given that /x"(Ab) < 0,there is a unique value of itg that maximizes the NPV of the firm.

2. Leveraged Rrm

In a leveraged firm, the objective of equity holders is to select an invest-ment policy, k^, that will maximize the net present value of their equity claims,ENPV(io),

(5) ENPV(*o) = J

D -where h =

is made. Thus, my study chancterizes the effect of leverage on the film's subsequent investment de-cisions. Knowing how the debt level will lead to a sub(q)timal fiiture investment dedsico, tbe fiimwould choose an ex ante optimal capital stiucttire that ensures equity holdois muTiinim the fiim valueat time 0.

^The dependence of investment cost on the capital scale allows the modd to incarponte the under-investment problem. Green and lUmor (1986) focus only on the risk-shifting problem. In tbeirmodel, there is no under-investment incentive since they implicitly assume that the cost of investmentis independent of scale.

404 Journal of Rnancial and Quantitative Analysis

The first-order condition leads to an investment policy in a levraaged firm,which is detennined by the following.

(6) ^ ^ ^ * ^ ^ = Jifi'iko) + cT'iko)ei)f{ei)de,-Co = 0.

Tb determine how the level of debt in a firm affects equity holders' invest-ment policy, I totally differentiate equation (6) and get

(7)

Assuming that the second-order condition fbr an interior optimum is satisfied, thedenominator on the right-hand side of (7) is negative. Thus, the sign of dk^/dDis the same as the sign of the cross-partial derivative in the numerator. Tkldngd«ivatives on both sides of equation (6) with respect to D evaluated at k^, I have

(do) -(8) sign 5 ^ = signV dk^dD J

A detailed derivation is shown in Appendix A.The joint effect of the risk-shifting and the under-investment incentives on

a firm's investment policy is clearly illustrated in equation (8). The first termon the right-hand side is related to the risk-shifting incentive, which increaseswith er' iko). This term contributes to a positive relationship between leverage andinvestment policy if the marginal voladlity of investoKnt, o-'(ko), is positive, buta negative relationship if cr'iko) is negative. The second term is associated withthe under-investment incentive, which is proportional to the unit cost of ci^tal,Q). This tenn creates a negative relation between leverage and investment policy.All else equal, the higher is Co, the stronger is the under-investment incentive.This is because when Co is high, the increasing debt level, D, will reduce moreinvestment in jfeg. As a result, the sign of idk^)/idD) wUl depend on the tradeoffbetween the two incentive problems.

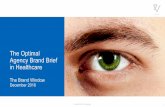

I first consider that the volatility of project cash flows increases with in-vestment scale, (r'ik^) > 0. As Appendix B proves and Figure 1 depicts, therisk-shifting incentive is dominant at a low level of debL Increases in leveragewill initially lead the firm to over-invest, k^ > Ag. As the debt level rises, tbeunder-investment incentive becomes more and more significant, and countervailsthe dsk-shifting problem, llius, the firm becomes less and less over-invested.At some high level of debt, tbe under-investment incentive dominates the firm'sdsk-shifting decision, and a leveraged firm under-invests at a level k^ that is lessthan &g. If the value function of project cash fiows is well bdiaved, thne exists a

Mao 405

positive level of debt, D*, at which these two incentives offset each other, and anoptimal investment decision is achieved, Jbg=k . Hie optimal level of debt, D*, atwhich neither an over-investment nor under-investment incentive is induced, canbe determined by the following equation.

/

+= 0,

where = Co.

FIGURE 1

The Eflect of Leverage on Irrvestrrarrt Decision and Debt Agency Coet

DeULBvel

Investment

K

Agency Cost(AC)

Detit Level

Debt Level

Figure 1 shows the effect of leverage on the marginal retum of a bond [S'(kg)]. investment dectakxi (kg), and tha agencyccet of debt (AC) when <r'(kg) > 0. At a kw dabt level. Increases In levsr^je lead tha fVm to ovarlnvesL kg > kg. Theagency cost of debt increases with levsrags. Aa the Isval c( dabt Incraaaaa beyond ZT*. msncy coat dedinaa and reacheszaro at CT. at which an optimal Invaatment policy Is achlevad. kg = kg. As Ihe debt lavel exceada ZT. a Isvsragad ftrmundar-lnvasts. kg < kg. and tha agency cost rt9es wHh debt level once nmxa.

Alternatively, if the volatility of cash flows declines or does not change withinvestment scale, eT'{k^) < 0, the risk-shifting incentive encourages a leveraged

406 Journai of Rnanciai and Quantitative Analysis

firm to under-invest (see Appendix B). Thus, b (^ the risk-shifting and the under-investment problems influence the investment decision in the same way. Thehigho- the debt level, the more the firm under-invests.

B. Agency Cost of Debt

In an efBcient capital market, the adverse consequences of debt agency areborne entirely by equity holders through the increased cost of debt financing. Anydeviations from firm value-maximizing policies will be reflected in a decline inthe value of firm. Following the literature, the agency cost of debt (AC) is definedas the difference between the net present value of an all-equity firm and that of aleveraged firm. Thus,

(10) AC =

where /i'(Ao) = CQ. The change in the agency cost corresponding to a change indebt £> is

Look first at the volatility of project cash fiows increasing with investmentscale, cr'(Ao) > 0. As Appendix B proves and Figure 1 depicts, at a low debtlevel, {dk^)l{dD) > 0. Because the risk-shifting incentive is dominant, the firmover-invests, and /i'(io) < Q-^ Thus, the agency cost of debt rises with thedebt level, dAC/dD > 0. As the level of debt increases beyond a positive levelof D", the total agency cost declines with leverage, dAC/dD < 0. At the opti-noal debt level, D*, the two debt agency problems offset each other, and a value-maximizing investment policy is adopted, Jtg = k^. Thas, the agency cost dropsto zero. For a debt level higher than D*, equity holders' under-investment incen-tive becomes dominant, and a leveraged firm tends to invest less than the optimal.Hence, dAC/dD > 0, and the agency cost again becomes positive and rises withleverage.

Figure 1 shows that this dynamic effect of leverage on agency cost is coinci-dent with its influences on investment policy and the marginal retum of the bond.Unlike Jensen and Meckling (1976), Myers (1977), and Green and TUmor (1986),my study indicates that, for firms with positive marginal volatility of investment,a'ik^) > 0, the total agency cost of debt does not uniformly increase with theamount of leverage.

Appendix B also shows that firms with zero or negative marginal volatility ofinvestment, tr'ik^) < 0, experience an under-investment problem at any positivelevel of debt. Hence, dAC/dD is positive, and the agency cost of debt increasesmonotonically with leverage.

'The over-investment problem here aiises fiom eqtnty bolden' risk-shifting incentive. This isdifferent fiom the over-investment incentive discussed by (Stulz (1990) and I i and I i (1996)), whichresults from the agency costs of managerial discretion given that the manageis' perqtiisites increasewith the size of investment

Mao 407

C. Marginal Volatility of Investment and Det>t Policy

The above analysis suggests a countervailing interaction between the twodebt agency problems. This potential interaction has not gone unnoticed. Myers(1977) points out that, if investment raises the variance of project return, equityholders' incentive to shift risk will mitigate the under-investment problem. Heconcludes: " . . . we may observe hsky firms borrowing more than safe ones"(Myers (1977), p. 167). While Myers' argument suggests a positive relationshipbetween the optimal debt level and business risk, the empirical evidence is am-biguous. Long and Malitz (1985) find that a firm's debt level and the riskiness ofcash flows are positively related. Bradley, et al. (1984) and Titman and Wessels(1988), however, find a negative and an insignificant relationship, respectively.Empirical tests in Kale, Noe, and Ramirez (1991) support a U-shaped relation-ship between optimal leverage and business risk.

My simultaneous analysis of the risk-shifting and under-investment prob-lems suggests that it is the mar;ginal volatility of investment (MVI), not the volatil-ity itself, that alleviates the agency problem of under-investmenL Although risk-shifting firms may have high volatility in project cash flows, firms with highvolatility need not have a high risk-shifting incentive. Simulation analysis in Par-rino and Weisbach (1999) suggests that a firm with high cash fiow volatility hasa low risk-shifting incentive. This is because, if a firm has assets generating cashflows with high volatility, there are not many additional projects that will increasethis volatility so as to shift risk. Thus, I expect a close relationship between theoptimal debt level and the marginal volatility, rather than the volatility level.

To investigate this relationship, I assume that the volatility of project cashflow is a linear function of investment scale, a'(Ao) = oAg + b.^ Then marginalvolatility. <7'(i^), is equal to the constant, a. I first consider a positive marginalvolatility of investment (« > 0). From equation (9), I can derive dD*Ida, anddetennine its signs.

Proposition I. For firms with positive marginal volatility of investment and highunit cost of capital, Co, the optimal debt level increases with the mnrginal volatil-ity of investment. In contrast, when Co is low, the optimal debt level decreaseswith the marginal volatility of investmenL

Proof. See Appendix C.

In this model, the unit cost of coital, Co, represents the magnitude of theunder-investment problem. As shown above, the higher is Co, the more likely afirm is to under-invesL This is because when Co is high, raising the debt level,D, will reduce more investment in k^. Proposition 1 implies that, for firms with asevere under-investment problem, the risk-shifting incentive alleviates the under-investment problem, thereby reducing the total agency cost of debt financing.

^Tbis is tbe simplest form of a volatility flinction, which differentiates itself fiom many previousstudies tbat bave only examined tbe efTect of exogenous business riiik on corporate capital structure(Castanias (1983). Bradley. Jarrell. and Kim (1984). Kale. Noe, and Ramirez (1991)). It basicallydecomposes the riskincM of a project cash flow into two parts. One is tbe endogenous risk, wbichis proportional to tbe investment decision, i : tiie other part represents exogenous risk due to marketfluctuation that is unrelated to tbe investment decision.

406 Journal of Rnancial and Quantitative Analysis

Thus, such firms can toleiate more debt in their capital structure. For firms withfew under-investment problems, however, the dominance of the risk-shifting in-centive pushes the optimal capital structure to a comer solution, and the agencycost of debt uniformly rises with debt level. In such a scenario, the optimal debtlevel would be negatively related to the marginal volatility of investment

Proposition 1 applies only to firms with positive marginal volatility of in-vestment (MVI). As shown above, if MVI is negative or zero, the risk-shiftingincentive leads equity holders to under-invest, and the agency cost of debt in-creases with the magnitude of MVI. Since the agency cost of debt and the optimaldebt level move in opposite directions, the optimal debt level decreases with tbemagnitude of MVI.

Implication I. For firms with negative Tnnrginnl volatility of investment, the opti-mal debt level decreases with the magnitude of MVI.

III. Empirical Analysis

The above analysis suggests a unique empirical predicticm on the relation-ship of the optimal leverage and the marginal volatility of investment (MVI). Thisrelationship depends on whether the under-investment problem is severe. In theagmcy literature, it has been well established that the higher is a firm's growth po-tential, the mare likely it is to under-invest. Therefore, I use a measure of growthpotential to proxy for the degree of under-investmenL Based on Proposition 1 andImplication 1,1 propose the following testable hypothesis.

HI. For high growth firms, the optimal level of debt increases with the magnitudeof MVI when MVI is positive, hut declines with the magnitude of MVI whenMVI is negative. It suggests a positive relationship between the optimal debtlevel and MVI. For low growth firms, the optimal level of debt decreases withthe magnitude of MVI fbr both positive and n^ative MVI firms. It suggestsa negative relationship between the optimal debt level and MVI when MVI ispositive, and a positive relationship between the optimal debt level and MVI whenMVI is negative.

For high growth firms with a significant under-investment problem, the modelsuggests that the agency cost of debt will decrease with the magnitude of MVI ifthe MVI is positive, but increase with the magnitude of MVI if the MVI is n^a-tive. This is because the under-investment and risk-shifting incentives offiset eachother in the farrstsx case. For low growth firms where under-investment is likely tobe insignificant, the agency cost of debt will increase with the magnitude of MVIfor both positive and negative MVI firms, since the risk-shifting problem is thedominant agency problem generated by debt in this case. Since the agency cost ofdebt and the optimal dd)t level move in opposite directions, for high growth firms,the optimal debt level will rise with the magnitude of MVI when MVI is positive,but decline with the magnitude of MVI when MVI is negative. For low growthfirms, the optimal debt level will decrease with the magnitude of MVI when MVIis positive or negative.

Mao 409

A. Empirical Method

To test the above hypothesis, I first develop an econometric method to esti-mate the marginal volatility of investment. Second, I test HI by cross-sectionallyrelating those estimates of MVI to firms' leverage ratios.

1. Estimation of Marginal Volatlltty of Investment (MVI)

In a multi-period setting, equation (1) can be rewritten as

(12) *,+, =

where the cash fiow in the next period, . M-I. is a random variable whose meanand volatility both depend on current investment k,. Equation (12) is very gen-eral in the sense that the error term, £,.^\, could be heteroskedastic and autocor-related.^ To be consistent with the theoretical model above, I assume a simplelinear relationship between the volatility of cash fiows and the investment scale,cr(it,) =ait/ +b, where a and b are constants. In addition, I assume a Cobb-Douglasproduction function for the mean cash fiow, /i(iti) = ck}. where c and d are con-stants.

I estimate the parameters (a, b, c, and d) of this model using the GeneralizedMethod of Moments (GMM) technique. There are several advantages of apply-ing this technique in estimating equation (12). First, the GMM approach does notrequire that the distribution of cash fiow be nonnal. Second, the GMM estimatorsand their standard errors are consistent even if the disturbance, e,,^\, is both het-eroskedastic and autocorrelated. Based on equation (12), lagged investment scaleit, is a natural candidate for an instrumental variable, since it is highly correlatedwith the true value of investment scale, it,, but is unlikely to be related to the errortemi, £|+|. As a result, the following population moments implied by the modelexactly identify the parameter vector 0 = {a, b,c,d).

(13) = 0.

I use earnings before interest, depreciation, and taxes (EBEDT) as a measurefor cash fiows, .^^.i, and c^tal expenditure adjusted for depreciation (CAPXAD)for investment scale, it,. Both EBIDT and CAPXAD are normalized by the bookvalue of assets.

^This would be consistent with product markets, for example, in which good sales this period maylikely be followed by good sales next period because the product is superior, or has been inarketedsuccessfully.

' A firm's real investment expenditures also include advertising and R&D expenses, however, datafor advertising and R&D expenses are missing fw 80% of the sample. I tise an accounting measureof eamings because it is mne directly related to investment decisions than stock price. Stock pricereflectsthepresemvalueof all the expected future cash flows, and its volatility would be much noisierthan the volatility of cash flows. Moreover, stock prices are directly inSuenced by the financingdecision, which may induce spurious correlation between leverage ratio and MVI in the regressionanalysis.

410 Journal of Rnanciai and Quantitative Anaiysis

Ideally, one would like to obtain estimates of the parameter vector fi forindividual firms. In the GMM analysis, I estimate four parameters by fitting anonlinear mean function and a linear volatility function as described above. Fornonlinear models, the individual f-test for each parameter is only asymptoticallyvalid. Tiius, it requires a large number of data points to get reliable estimates, butthe amount of individual firm data is insufBcient for this task.

Tb circumvent this data problem, I pool firms into industry groups based ondieir SIC codes. This method of grouping is reasonable for diree reasons. First,firms in the same industry are likely to have similar cash fiow dynamics becausethey tend to have similar technologies. Second, firms in the same industry aresubject to similar economic shocks that may affect the risk-return structure ofthe investments. Third, investment opportunity sets are similar for firms withindie same industry. If a rislqr project with positive NPV appears in a particularindustry, all firms in the industry are able to invest in the projea and shift risk.Hence, the marginal volatility of investment is likely similar for firms within thesame industry.

2. Other Factors Affecting Rnandng Policies

The primary focus of the empirical analysis is to examine the model's pre-diction on how the optimal capital structure is related to the marginal volatilityof investment. It is important, howevo', to control for competing explanations ofdebt policy. Omitting odier detnminants of capital structure from the specifica-tion would bias the estimates. In addition, without controlling for those factors, itis possible that the estimates of MVI would not really test the model but insteadproxy for other explanatory variables for capital structure, such as a firm's busi-ness risk. Furthermore, including control variables allows determination of therelative contribution of the MVI variable to the firm's debt policy.

The previous literature provides useful precedents for selecting proxy vari-ables. According to Harris and Raviv (1991), it has been well documented diatleverage increases with tangibility of assets and firm size. Leverage decreaseswith non-debt tax shields, volatility, growth opportunities, and the probability ofbankruptcy. I include a number of such variables in the cross-sectional regres-sions.

B. Data

My data consists of Compustat firms (including those from the researehtapes) and covers the years 1976 through 1995. I exclude all financial and realestate firms from die sample (two-digit SIC codes between 60 and 68).

Using the GMM technique, I obtain estimates of marginal volatility of invest-ment, MVI, for different two-digit SIC coded industries from panel data for 1976-1995. Ib yield reliable estimates without losing too many industries, I select in-dustries in which at least 100 panel data points of bodi EBIDT and CAPXAD areavailable for GMM estimation. There are 54 industries satisfying this restriction.

'Many finns in Ihe financial services industry do not have information availahle on earnings be-fore interest depredation, and taxes (EBIDT), because such earnings are not meaningful for thesecompanies.

fwiao 411

I conduct cross-sectional regression analysis for firms included in the GMManalysis. Independent variables, including firm size (logsize), growth opportuni-ties (market-to-book), tangibility of assets (TANG), non-debt tax shields (ITC),and book leverage ratios, are averages over the 20-year sample period 1976-1995.Eamings volatility (VAR) is calculated as the standard deviation of the first dif-ference in armual EBIDT over the 20-year poiod divided by the average value oftotal assets over the same time period. The sample is further restricted to onlythose firms that have at least three firm-year non-missing time-series values forlogsize, market-to-book, TANG, ITC, and book leverage as well as at least threedifferenced EBIDTs for computing VAR. Table 1 reports the descriptive statisticsfor all these variables.

TABLE 1

Descrlpthn Statistics of Lsverage Ratio and Other Firm Charactartetic Vailables

Logsl^eMarfcel-tc-boakTANGrrcVAHBookleverBga

N

345234523452345234523452

kitoan

4.68641.46930.36960.00380.06970.1968

Std. DGV.

194840.61220.20640.00420.07180.1348

MIn.

- 0 . 0C870.58870.0133O.COOO0.CO100.0000

KllBX.

10.07129.43210.92230.03631.18440.7666

Table 1 reports deecrlpttve slatMJcc cn firm characteristic variables fbr a sample ot 3452 finns Included In the analysis.Theee firms have at least three flmvyear non-mlsaing time-sertee vslues for bgsize, markat-to-bock, TANG, fTC, and bookleverage rato as well es al least three dfferenced EBIDTs for oaksuleting VAR during tha sample pedod 1976-1995. Allvariables except VAR are aveiages overihe sample period.

Logsize: logerithm of book value of assets.

Merke!-io-bcok' ratio of market value of assets (book value of assets - book value of equity + market value o(equHy] over book value of aseeis.

TANG' plarrt and equipment es a percentage ol book vBlue of assets.

ITC: Investrrent tax credits over nei sales.

VAR: standard Oevlalkxi of the fkst difference h annual eamings before Interest depredation, and tax(EBIDT] over ihe 20-yeer period divided by the average value of total assets over the same dmeperkxj.

Book leverage ratio: ratk) of kxigmsrm debt over txxM value of assets.

C. Empirical Results

1. Parameter Estimates from GMM Analysis

There are 54 two-digit SIC industries that meet the sample restrictions, andall parameter estimates converge successfully in the estimation procedure. Table2 presents descriptive statistifs for the GMM estimates. Widiout any restrictionon the estimation procedure, I obtain reasonable estimates of the Cobb-Douglasmean function of cash fiows. The coefficients of mean cash fiows, c, are pos-itive for aU 54 industries, with a mean of 14.6. The exponent coefficients ofinvestment in the mean function, J, are all positive with a minimum of 0.33 and amaximum of 1.12. Furthennore, 52 estimates of d aie between zero and one. Thisfact accords well with die parameter restrictions on the Cobb-Douglas productionfunction, and validates my theoretical assumption that the mean cash fiow is anincreasing and concave function of investment scale.

For the linear volatility fiuiction, the intercept, b, measures the exogenouspan of the volatility of cash fiows unrelated to investment scale. Hie finding that

412 Journal of Rnancial and Quantitative Anaiysis

TABLE 2

Descriptive SlBtistte of GMM Pararnater EsUmales for 54 IVro-DlgK SIC Coded

EBtlmalB No. al Oba. Mean StdDgv. MIn. Max. Rar<ia

Unearcoamdent of the volatility function 54 -0 .02 1.71 -3 .88 3.B4 7.52of cash flowa (d)

IntarcaptofthevQlalllHyfinctlonofcaah 54 107.71 I i a 2 3 a51 684.14 645.63flmw(b)

Coemdentofthemeantmstkinolcash 54 14.60 27.69 1.62 21039 209.27f lm«(c)

Exponent coifflclent of the mean funcOon 54 0.74 0.14 C.33 1.12 0.79of cash flowB ((0

Table 2 presente Bunmery alatladcs of parerneter eeUiielee of the rnean and volBtlllty function of cash flows for 54 tvvo.<fgltSIC coded Indualiies. EMIirates of parairater vector p = (s, b,c.d) toe each two-ckit SIC Muatry are obtained fionpenel data for 1976-1995 using QMM analysis. The BtochaBlk:procee8C( cash fknn^^i Is modeled as X^+i =fi(Ait) +< r M > V i <*'><"<» f ' ( ' 4 ) = ' ^ Slid ff('4)=a'ir+b Cashftam, J^+1. are prcoded tiyearnlnas before Irrterest depreclBllcn,end taxes (EBIDT), and Investments, k,, are proxled by capital expendfturee ed)ijsted for depreciation (CAPXAD). BothEBIDT snd CAPXAO are ncrmaBzed by the book vsiue of assats. The sample Is leetricted to the hdurtrlea that heve atleast 100 pensi deta points of boDi EBIDT snd CAPXAO fbr QkM esdmaUxi. Hsnge statlsBcs sre the difference betweenthe maxknum and minhun.

the estimates of Z> are all positive is thus sensible. The matginai volatility of in-vestment, a, however, is not restricted to either positive or negative. The minimumestimate of a is -3.88, and the maximum is 3.64. Of 54 estimates of a, 32 arepositive. Based on their associated r-statistics, 30 of them have posidve marginalvolatility of investment significant at the level of 1%. This result indicates thatthe volatility of a firm's cash flows, for some industries, increases with the size ofinvestment Therefore, a positive marginal volatility of investment is theoreticallyand empirically relevant. °

2. Chatacteristic Differences between Positive and Negative MVI Rrms

Given these estimates, I divide firms into two groups. Those from industrieswith positive marginal volatility of investment are categorized as positive MVIfirms, the rest are negative MVI firms. First of all, I compare firm characteristicsbetween the two groups. Ibble 3 reports the means (in panel A) and medians (inpanel B) of the logsize (proxy for firm size), market-to-book (proxy for growthopportunities), ITC (proxy for non-debt tax shields), TANG (proxy for assets tan-gibility), VAR (proxy for eamings volatility), and book leverage ratios, f-testsand Wilcoxon signed-rank tests are used to examine the difference of means andmedians between the two groups respectively.

The logsize and market-to-book ratios of tbese two groups are not signifi-cantly different. Positive MVI firms, bowever, are systematically different fromnegative MVI firms in other respects. Positive MVI firms have significantly highereamings volatility (at the 1% level), but significantly fewer tangible assets andnon-debt tax shields (at the 1% level), and significantly lower book leverage ra-tios (at the 1% level). The lower proportions of tangible assets in positive MVIfirms is consistent with the fact that tangible assets can serve as collateral, therebyreducing the firm's risk-shifting incentive as measured by MVI. Because of therisk-shifdng incentive, positive MVI firms have, as expected, higher levels ofbusiness risk than negative MVI firms. The differences between the two groups

'"Additional tests (» heterogeneity of MVI eatimaies across firms and industries will be preseiuedaod discussed in Section m.C.S.

Mao 413

TABLE 3

Characteristic DlflerBnces between Positive and NegaUve MVI Rrms

Logsiza Martet-toflook FTC TANG VAR Book Lavarage Ratk)

Panel A Sample UtansolCharactertslx:\Mat>leect Positive and Negative KM nmia(p-valuea am mporM Inparontheses for teets of equality ol Ihe two sampleetiaaadcnt-leelsasatxning unequal variancea)

VN\>0 4.6154 1.4752 0.C034 0.3202 0.0732 01812M V I < 0 4.7077 1.6280 0.CO42 0.4457 0.0639 0.2231Maendiff. -0.0923 -O0528 -O0008— -01255*** O0093— -O0419*-*

(01619) (0.1744) (O0001) (0.0000) (0.0001) (0.0001)

PanelB.SanvieUddbnsoftt>eaiaracmiBtk:VbrlablasofPoeltiveandNegatlvaliMF^nna(p-valuesammporladlnparanlheaeelorlesbcf equally al the madlanBcf tie NIG eaifjluu baaed on Wlkx3xonelif)Bd^tnltlaels)WN\>0 4.3905 1.2376 0.0022 O2950 O0531 O1720MVI < U 4.5196 1.1851 O0030 0.4248 0.0439 0.2223Med. dW -0.1293 0X1525 -0 .0006*" -0.1296~* 0.C093*** - 0 .0503" '

.'0.1094) (O8420) (O0001) (O0001) (0.0001) (O0001)

TaUa 3 reports charactartatk: JllfeiBncee of samples dasalfled into poeltiva and negative MVI Urms accoidng to theirmarginal volatlinyodrrveetmsnt (MVI) aadmatBd from QMM analysis, t- ests and Wncoxon sKried^iank testB are UBed toexamino the dflerence of means and madians between Iha two groups, reepsctlvaly.Logsiza: bgartthm c( book value of assats.Mart(et-x>.bool(. ralki of markat value of assets (book -/akja of assets - book value of equity + markat value of

equity) over book value of assets.TANG: plant and equipment as a percentaga of book value of aaaala.rrC: Investment tax cradts over net sales.VAR: standard deviation of tha fkst difference In annual eamlnga balore Interest, dspreolatkxi, and tax

(EBIDT) over tha 2O.yaar perkxl dvkted by the average valua of total assets ovsr the same timaperkxl.

Bock leverage rat»: ratki of nng-tarm debt over book valua olaseeta.-.". "-Bignlhcart at the 10%, 5%. and 1% levels, respectlvaiyL

suggest that it is important to control for these variables in order to examine therelationship between leverage and MVI.

3. Regression Analysis

Hypothesis HI suggests a differential relationship between leverage and themarginal volatility of investment conditional on firms' growth opportunities, i btest HI, I partition the sample into high and low growth firms. I follow Lang,Ofek, and Stulz (19%) and use the growth rate of capital expenditures as a growthmeasure.'' The three-year growth rate of capital expenditures is defined as theratio of capital expenditures in year +3 to the capital expenditures in year 0, mi-nus one. Firms are ranked according to their average three-year growth ratesof capital expenditures over the sample period. One-third of the firms with thehighest growth rate of capital expenditures is categorized as "high growth," andone-third with the lowest growth rate of capital expenditures is categorized as"low growth."'^

By construction, the differences in the three-year growth rate of capital ex-penditures between the high and low growth samples are dramatic. As Tkble 4shows, the average three-year growth rate of capital expenditures is 2.6737 forthe high growth sample and -0.2366 for the low growth sample, and the differ-

McConnell and Servaes (1995). I avoid using the book-to-maricct ratio as a grosvthmeasure for dividing the sample into high and low giowth firms. Sampling on book-to-maricet ratiobefore Ktimating the regression with the seme variable violates the assumption of OLS r^ressions.

'' Results cf tests using the top and bottom quaitiles of the giowth classification are more supponiveof Hypothesis HI than the three-group resulLs.

414 Journal of Rnanciai and Quantitative Anaiysis

ence is highly significant, I also constmct three altemative growth measures ofLang, Ofek, and Stulz (1996); the one-year growth rate of c^tal expenditures(CAPXl), and one-year and three-year growth rate of employment (EMPl andEMP3). These measures are all significantiy higher for the high growth sam-ple. In contrast, the high growth sample has a significantiy lower proportion oftangible assets (TANG), which accords well with the negative relation of assettangibility and growth opportunities. In addition, the risk-shifting incentive asmeasured by the MVI is significantiy higher for the high growth sample than forthe low growth sample. This finding is consistent with the idea that firms with lowgrowth potential and high levels of tangible assets are less likely to shift risk. Tiiisis because risk-shifting is more easily monitored by debt holders in these firms.

TABLE 4

Characteristic Differences between High and Low (afowth Rrms

CAPX3 CAPX1 EbP3 EhP1 lANQ hM

PanelASanvletJeanaofarowlhavmclerlstlc\lMableeofHiatiandLowamvitt>FlnTa(p^valueear^parenlheeee for laatacl equally ol the means cf Ihe two aamplee based on t-leaaaaaumlna unequal variances)

High growth 2.B737 0.6823 1.1253 0.1453 0.3320 0.1749Lowgnwth -0.2386 0.0805 aO484 0.0190 0.3898 0.1397Maandlfr. 2.9103— 0.5828*** 1.0789*" 0.1283— -0.0578"* 0.0352""

(0.0001) (0.0001) (0.0001) (0.0001) (0.0X1) (0.0075)

pamntheessfortsstsotsquaHtyot Ihe medisnaoHhehmaairvlsstisasd on WBcoxonaloneitfank tests)

HIghgnwth 1.4599 0.4381 0.3556 0.0944 0.2859 a4556Lowgrowth -0.1850 0.0295 -0.084S - a 0 0 9 8 0.3389 0.3305Med.din. 1.6249— 0.4088*- 0/4407" 0.1040-** -0.0610-** a i25(r*

(0.0001) (0.0001) (0.0001) (0.0001) (0.0001) (0.0253)

TsOe 4 rsportB charactarWIc dWerencaa tiatwesn Bamplra daBtifled hto high and low gnmth flrms according to thefollowing growth maaauras. Hssts and WllcGxon slgned^ank tests are used to examlna tha dinarenco cf means andmsdena tMtvveen the t«n groups raapectlvely.

CAPX3: three-year gniwth rate of capital axpendltures, which l8 the ratio c( capital axpendbjrse in yaar+3 to the capitalexpsrKlbjrsa in year 0. minus cna.

CAPX1: one-year gniwlh rats cf capital expendltms. which la the ratic cl caplal expendturss In year 4-1 to the capitalexpendlturee In year 0. minua era.

EMP3: threo yoar growth rate cf employment, which la the ratio cf employment fri year +3 to the emptoymant In year 0,minus one.

Bff>l: one-year growth rate ot employment, which Is the radc of emptcyment in year+1tc the anploymerrt In yevO,

minus one.

TANQ: plant and equipment as a percentage cf book value of aaeets.

MVI: industry esthalBscf the marghalvoMlitycflnveatmenL

*.**,—slgnlflBsnt et the 10%, 5%. and 1% levels, respectively.

I estimate separate cross-sectional regressions for the high and low growthsamples. To control for the characteristic differences between positive and nega-tive MVI firms that are known to explain debt policy, I include logsize, market-to-book, TANG, rrc, and VAR in a regression of the book leverage ratios onestimated MVI. All tests are conducted using a heteroskedasticity-consistent co-variance matrix (see White (1980)).

Tiible 5 reports the results of cross-sectional regressions using the time-seriesmean of each variable by firm. ' To identify the relative contribution of the risk-

' Running the regression in a single cross-section eliminates the problem of serially correlatederms. The cross-secdonal r^ression preserves the dispersion across firms, but does not exploit anytime-series variation in the observations.

Mao 415

shifting variable (MVI) to the firm's debt policy, for each sample regressions arecarried out without or with the MVI variable. All regressions are highly signifi-cant, and have adjusted R^ of about 30%. For high growth firms, the coefficient forlogsize is positive and significant This result suggests that larger firms are morediversified and have lower probability of bankruptcy, thereby adopting more debtin their capital structure. Consistent with the theory of agency cost of debt, thecoefficient on the market-to-book ratio is negative and highly significant In ad-dition, asset tangibility (TANG) has a significant efEect with the predicted sign,suggesting that a high fraction of plant and equipment (tangible assets) in the as-set base makes high debt level more desirable. However, in contrast to prediction,the coefficient of non-debt tax shields (FFC) is positive and significant at the 1%level.'** The coefficient of earnings volatility (VAR) is negative but insignificant.In the regression including MVI, the risk-shifting variable barely changes the co-efficients of those control variables. Most important, as the model predicts, thecoefficient on MVI is significandy positive. The magnitude of the coefficientsindicates that the leverage efFiEct is also economically consequential. Ilie 25thpercentile of the MVI is -1.70, and the 75th percentile is 1.04. According to theregression, an increase in MVI from the 25th to the 75th percentile is associatedwith an increase in leverage ratio of 2%.

For the low growth sample, HI suggests that the optimal leverage decreaseswith the absolute value of MVI. To account for the change of the slope term inthe linear regression, I estimate the following model.

(]4) (Leverage),- = QI+a2D/ +/3i (Logsize),-i-/32(Market-to-book)/

+ A(TANG), + ^4(rrc), + A(VAR),- + Ai(MVI),-

where Di is a dummy variable that equals one for negative MVI firms and zerootherwise, ai and 0q represent the difference in intercept and MVI fector loadingbetween negative and positive MVI firms, respectively. The coefficient of MVIfor positive MVI firms is 0f, while the coefficient for negative MVI firms is ^6 +^ . Table 5 shows that the coefficients of logsize, market-to-book, and TANGare significant and are comparable in magnitude and sign to those observed forthe high growth sanqile. However, ITC has a negative effect on the leverageratio significant at the level of 5% in the low growth sample. ' Interestingly,the coefficient of MVI is negative and significant for positive MVI firms. Fornegative MVI firms, the coefficient becomes positive and marginally significantat the 10% level. Consistent with HI, this result suggests that for low growthfirms, die leverage ratio is negatively related to the absolute value of MVI.

'*This is because investment tax credits (ITC) tend to be Mgh when a firm's vahie depends substan-tially OD tangible assets-in-place. The correlation coefficient of ITC and TANG is 0.27 and significantat the 0.01% level. While the tax theory predicts a n^ative effect of ITC on debt use, the agencyiheor>' predicts a positive coefficient for ITC. Thus, the sign of ITC would depend on the tradeoffbetween these two oppoute effects. A positive coefficient of ITC has been previously documented byBradley, Janell, and Kim (1984) and MacKie-Mason (1990).

' Thiii is becatue the n^ative effect of non-debt tax shields on debt policy would be observed onlyfor firms near tax exhaustion so as to affect firms' marginal tax rale. Firms in the low growth sainplemay be more likely near tax exhaustion than those in the high growth sample.

416 Journal of Financial and Quantitative Analysis

TABLE 5

Cross-Seobonal Regressions Classified by CAPX3

CAPX3

Independent Wriabte

Intercept

Logaize

Mar1(el-to-book

TANG

ITC

VAR

MVI

D

High Growth

0.1026"*(aOGGO)

0.0106-**(0.CO00)

-0 .0341*"(0.0000)

0.2690"*(O.OOX)

2.9023*"(0.0014)

-0.0247(0.6543)

0.323116

1172

0.0967***(0.0000)

0.0099***(0.0000)

—0.0323***

(aoooo)a3085***(0.C000)

2.6547"*(0.0032)

-0.0368(0.5104)

0.0077*"(00021)

0.339100

1172

ai220"*(0.0000)

0.0055"*(0.0017)

-0.0288***(0.0000)

0.2815*"lOXXXXi)

-Z0324**(aO346)

-0 .1213"(aO263)

0.26394

1139

LowGiowth

aii5e***(0.0000)

0.0062*"(0.0005)

—0.0270"*(0.0000)

0.2854"*(0.0000)

-ZO74a"(0.0446)

-0.1148"(0.0356)

—o.cxso**(0.0358)

0.0320(0.1878)

0.0048*(0.0893)

0.29880

1139

Table 5 pr nts eeotlonal analysis d leverage ratio on marginal votadllty of investment (MVI) and control varlablasfor samplea daasffled Into high and kw (^owth fkms according to their three-year gRwth rats of capital axpendturee(CAPX3). pvakjas, using the heteroskedastk%.«xislstentstanderd enors (White (1980)), we In paremheees below thecoefficients.

logarithm o( book valua of assets.

ratk) of market value of easels (book value of assets — bock value of equity + market value of

Logsize:Market-to-bcok:

equity) over book value of e

ptanlandequipmerrtasapercerrtageofbookvalueofa

Investment tax credts over net sales.standard devtaUon of the fkst difference h annual eamings befcre Interest depreclafion, end tax(EBIDT) over the 20-year perkxl dvkied by the average value of k)tal asests over the same tkneparkxJ.

a durmiy variable that equals one tor negattvs MVI fkme and zero othenwlae.

ratio of kmg-tarm debt over bock value c4 assets.

three-yaar growth rate of capilal expendltues, which Is the ratk) of capital axpenditursa In year+3to the capital axpendbjree in year 0. minus one.

,'**slgnincam atthe 10%, 5%. and 1% levels, respectively.

ITC:

VAR:

Book leverage retio:

CAPX3:

4. Tests for Robustness

The empirical results above support the theoretical prediction of the model.However, these results may depend on the specific classification scheme and thevariable definitions employed. A particular concern here is whether the three-year growth rate of capital expenditure is a reasonable proxy for the firm's futureinvestment growth opportunities. To shed light on this question, I try alternativemeasures of growth oi portunities, CAPXl, EMP3, andEMPl. Again, I subdividethe sample by top and bottom thirds according to these growth measures, and thenestimate regression models separately for the high and low growth firms. Theresults in Ibble 6 confirm the earlier findings. For high growth firms, the relationbetween leverage and MVI is positive and significant; for low growth firms, therelation is significantiy negative when MVI is positive and weakly positive whenMVI is negative. Furthermore, for bodi the high and low growth samples, the

Mao 417

coefficients of MVI are comparable in size to those using CAPX3 as a growthmeasure as in Table S.

TABLE 6

Cross-Sectional Regressions Classlfled by CAPX1, EMP3,

IndeperxientVaneble

intareept

Logsize

Uarket-tc-book

TW4G

ITC

VAR

W l

D

MVl4.D*IVIVI

Adl.fi'PNo.of3bs.

CAPX1

High

0.0766'"(0.0000)

0.0160*-*(0.0000)

- 0 . 0 2 9 9 —(0.0000)

0.3091**'(0.0000)

1.8424"(0.0229)

—0.0363(0.4426)

0.0079"'(0.0011)

0.338107

1243

Low

0.1379-'*(O.OOOC)

0.0042(01032)

- 0 . 0 3 1 3 " '(0.0000)

0.2817"*(0.0000)

-1 .0346(C.3546)

- 0 . 1 5 4 6 —(0.0023)

- 0 . 0 0 5 7 - '(0.0433)

0.0345(0.3786)

0.C051*(0.0698)

0.31294

1207

Hi j i

(0.0000)

0.0134"(0.0000)

-0.0354-(0.0000)

0.277(]*'(0.0000)

2.3493"(0.0007)

-0.0719(0.1455)

0.0067"(0.01161

0.367108

1155

EMP3

Growth

Low

0.1483'"(0.0000)

0.0033(ai230)

-0.0378'*'(aoooo)

" 0.Z719**-(0.0000)

-1.1576(0.3278)

-0.0296*(0.0896)

-0.0073*-(0.0064)

0.0478(0.1345)

0.0058'*(0.0356)

0.23856

1121

andEMPI

EMP1

Hfah

01005'"(0.0000)

0.0143*-(0.0000)

— 0.0395"*(0.0000)

03031*"(0.0000)

2.8887"'(0.0006)

-0.050410.3784)

0.0059*-(0.0318)

0.397136

1232

Low

0.1396"*

(aoooo)0.0023'(0.0643)

-0.0328"*(0.0000)

0.2874"*(0.0000)

—2.87B3"(0.0334)

—0.0662(0.3713)

-0.0038'(0.0742)

0.0302(0.4596)

a0045*(0.0953)

0.24862

1197

Tabie 6 presents cross-sectlcnal analysis of leversgs ratio on marglnel votatUHy of Invsetment (MVI) and control vart-sblea for samples classified Imo high and low growth firms according to one-year growth rate c( csipltal expenditures(CAPX1). ;hree.year and one-year growth rale of employment ( E M ^ snd EM>1, respectively), ^values, ushg thehstsToskedastidiy-conslsmnt standard efiDTB (White (1980)). sre h parentheses below the coefflolents.

LogtJza: logoftttim cf booK value of ssests.

Market-io-book: ratio of market valje of aseets (aook value of assetB — book value of equity + market value ofequity) over book value of seests.

TANG: plant and equlpnent ass percentage of book vslue of assets.

rrC' Investment tax credits over net sales.

V/>P: standard devisUon of ihe first difference in snnual earnings belore interesL oepreclaticn, snd tex(EBIDT) over the 20-year period dMded by the average value of total assets over the ssme tkneperiod.

3ook leverage ratio: ratio cf long-term debt over book value of assets.

CAPX1: one-year growth rote of capital expenditures, whk:h Is the ratio of capital expendtures In year 4.1 tothe capital expendRurss in year 0, mInuE one.

EMP3: three-year ffowthraiedempkiyrrent.whrch is the ratio o( employments year 4.3 to the employmentIn year 0. mkus one.

EMP1: one-year growth rate of ernplcyment, which Is the ratio otempk)yment in year 4.1 to the empk)ymentin year 0 minus cne.

- ".-"slgnificam ai the 10%, 5%. and 1% levels, rospectively.

I perform an additional sensitivity test by dividing the sample into threegroups according to the firm's price-to-eamings ratio (P/E). The results (notshown) are also consistent with those based upon other classification schemes.Thus, the empirical results appear robust to the choice of a growth measure.

418 Journal of Rnancial and Quantitative Analysis

5. Tests for Heterogeneity of GMM Estimates across Rrms and Industries

Although I have argued above that firms in the same industry are more likelyto have similar MVIs than firms in different industries, it is important to ensurethat there is no significant heterogeneity of MVI across firms in a given industry.I have attempted to address this issue in the following ways.

First, I estimate equation (13) on the firm level, but &il to obtain parameterestimates. For reasons of data limitations, all estimates Ml to converge in theestimation procedure. At most, there are only 20 time-series observations foreach firm, not enough to get reliable GNfM estimates.

Second, I estimate equation (13) for each four-digit SIC industry. Thereare 240 four-digit SIC industries satisfying my sample restriction criteria, butonly 194 of them survive the estimation procedure (parameter estimates of 46industries Mi to converge). This creates a significant problem of sample bias.

Third, I estimate equation (13) for each three-digit SIC industry. There are18S industries that meet sample restrictions, and 179 of them survive the esti-mation procedure. I group these parameter estimates according to their two-digitSIC codes, yielding 33 two-digit SIC industries that have more than one estimateat the three-digit level. Ib measure the heterogeneity of these estimates withina two-digit SIC industry, I compute their standard deviation and range statistics(defined as the maximum minus the minimum) within the same two-digit SICgroup. Ilible 7 presents summary statistics on these 33 variability measures. Theaverage standard deviation of the three-digit estimates of MVI within each two-digit SIC industry is 0.61, about one-third the standard deviation of 1.71 acrossthe two-digit SIC industry (see Ikble 2). Average standard deviation of the otherthree parameter estimates within the tWD-digit SIC industry are one-half or one-third of those across the two-digit SIC industry. Tba average range statistics ofthe MVI estimates at the three-digit level is 2.S2, whereas the range statistics ofMVIs across the two-digit industry is 7.S2. Hie average range statistics of theother GMM estimates within the two-digit SIC industry are also less than half ofthose across the two-digit SIC industry. These results suggest that there is muchless heterogeneity of MVI estimates within the two-digit SIC industry than acrossthe industry, which justifies the use of the estimates at the two-digit SIC level.

IV. Conclusions

By endogenizing a firm's risk policy as part of the investment decision, thispaper unifies the analysis of the two debt agency {nnblems, risk-shifting andunder-investment. A key finding is that, if the volatility of project cash flowsincreases with investment scale, risk-shifdng by equity holders will mitigate theunder-investment problem. Thus, contrary to conventional views, the total agencycost of debt is not monotonically increasing with leverage. Furthermore, the studysuggests a unique relationship between the optimal debt level and the marginalvolatility of investment (MVI), which I define as the change of cash flow volatil-ity corresponding to a change of investment scale. For high growth firms, theoptimal level of debt increases with the magnitude of MVI when MVI is positive,but declines with the magnitude of MVI when MVI is negative. For low growth

Mao 419

TABLE 7

Summary Statistics on Vartablltty of TTiree-Oiglt SIC Industry Estimates

VBriaUe hki.cfObt.

No. cf three-digit SIC industries within a two-digit SIC industry 33

Sic. dev, olsslmats(•)ib)

id)Range slaHsllcs ot esttmaiela)

IC)

W

33333333

33333333

Mear

4.21

0.6141.9610.410.05

2.52140.3618.920.36

Mm.

2

0.115.612.540.01

0.373.700.780.03

Mex.

9

1.2053.0414.290.11

8.80472.12

81.750.S9

Table 7 reports surrmary statistics cn the vartabtity ot the three-digit SIC Industry esdmatee within the same two-digit SICr.lL.._I..A i.r .jAri_i.l.i. a l A r.i. _ _ • . ! . ll Imt Om :.iH.._l..i _ . . • nhtnlrwiH 1.n.Ti n iJ I I nnnk..ila

Standard deviation and range stattstlcs cf theee eethnates within each two-dlgK SIC code group are ccnvxited to measureIhe disperskxi cf theae estknsles si the three^iglt level. Flar«e stab'stjcs Is computed as the difference between Ihemaximum and mlnknum There are 33 two-digit SIC industrlea wHh mors than era three-digit eedmate so that standarddeviation ana range statistics can be computed.

firms, the optimal level of debt decreases with the magnitude of MVI for bothpositive and negative MVI firms.

I test the model's predictions using cross-sectional data firom Compustat(1976-1995), Empirical findings suj^r t these predictions. For high growthfirms, I find a significant positive relationship between leverage and MVI. Forlow growth firms, I observe a significantly negative relationship between leverageand MVI when MVI is positive, and a weakly positive relationship between thetwo when MVI is negative.

Despite these positive empirical results, there are several limitations to thisstudy. Pirst. because of the data limitation, I estimate MVI based on the two-digitSIC industry data instead of firm level data. Although it appears that estimatesof MVI are more homogeneous within the same industry t h ^ across industries,MVI could be firm specific like the other control variables used in the regressions.Second, because of die dynamic properties of a firm's investment opportunity set,MVI could be time varying instead of constant over the sample period as I haveassumed. Tliird, while I attempt to control for some of the previously identifiedexplanatory variables, it is possible that the estimates of the marginal volatility ofim'estment are proxying for some other unidentified fiactors that are related to theleverage ratio in the same way as 1 observed.

Appendix

A. Proof of Equation (8)

Given that the investment policy in a leveraged firm, k^ is determined by thefollowing equation,

| ^ i i - C o = 0,

where h -where h -

420 Journal of Financial and Quantitative Analysis

rearranging (A-1) yields

Taking derivatives with respect to Jtg on both sides of equation (A-1), I have

f{h)Co

The second equality follows 6om equation (A-2).

B. Proof of the Dynamic Effect of Leverage (D) on a Firm's InvestmentPolicy (k^)

Ib dissect the effect of leverage on a firm's investment policy, I define dietotal value of debt at time 0 as B(Jt ),

CB-1) B {4) = n Df{ei)dEi + f {fi{ki)+(T {ki) £,)/(£,)&,.

The change in the bond value consequent to a change in iko is

(B-2)

where F(*) is the cumulative distribution function of e i. Thus,

Mao 421

DefineX = Co

Case 1. a'[ko) > 0.

dX _ TdD -

So X is a monotonicaUy increasing function of D. As D = 0, fi'ik^) = Co, and)At a low level of debt, A = (D — liik^))/i(TikQ)) is negative and very small,

then X < 0. Based on (B-3), (5^B(*g))/(5*^50) < 0. Hence, B'(*g) < 0, andk^> k^. This suggests that a levered firm ov«'-invests.

As the debt level increases, A = (!) — A'(^))/(<^(^)) becomes larger andeven positive. Since AT is a uniformly rising function of D, there exists a level ofdebt, D\ at which X = 0. D' is determined by the following equation,

roc ^+oo

f{£i)dei-(T'{k^) ei/(e,)£/e, = 0.Jh

At this debt level, D", i8i^Bi1(^))l{dk^dD) = 0. Then as debt increases more,

Co + a' (Jkg) h r°fisi)dei - a" (*g) [ ^ eif{ei)dei > 0,Jh Jh

Jh

id'^Bik^)) I idk^dD) switches sign and becomes positive. If the function of S' (is well behaved, there exists a positive debt level D*, at which ffik^) = 0, andi^ = i^. It implies that, in the presence of debt level D*, a levered firm wouldadopt an optimal investment policy as an all-equity firm. And D* is determinedby

= 0,

where /i'(*^) = Q, .

When d ie level o f debt is even bigher than £>' , s ince ( ( g ) ) / ( g )0, then B'{k^) > 0 , and i o < ^^ indicating that a leveraged firm under-iirvests.

Case2.eT'{ko) < 0.

As shown above in (B-3),

Since £[£, |ei > A] - A > 0, it is always true that iB^Bik^)) j[dk^dD) > 0. AsD = Q,B'{k^)= 0. Fbr any positive level of debt D, B' (*g) > 0, and then ifeg < *g.^ ( J ^ ) is uniformly increasing with D.

422 Journal of Financiai and Quantitative Anaiysis

C. Proof of Proposition 1

Assuming that (/fco) =ak^+b, the marginal volatility of investment (T'{k^) =a. Since the optimal debt level, D* must satisfy the following equation,

= 0,

where |i'(ft^)=Co, and/t=(D -/i(ik^))/((7 (*^)), in order to detmnine the relationbetween D* and the marginal volatility of investment a, I totally differentiate(C-1) with respect to a, which yields

da

Giventhat ^ ^ ^ > 0 at D',

I have

(C-2) si

As shown in Appendix subsection A, at the optimal debt level D",> 0. Thus,

)

{Co+ah)f{h) ^ Qk^ b

In addition, J^°° £]/(£] )dei > 0, thus the sign of flD*/aa will depend on thesign of A = (D - Ai(i^))/(o'(i^)), which is dependent on the optimal investmentscale, k^, which is in turn related to the unit cost of c^tal, Co. Given that fi'{k) =Co, dk/dCo = l/(p"{k)) < 0. Hence, k^isa decreasing function of Co. When Cois high, ifcg will be low. Since /i(/^) is an increasing function of kg, ii{k^) wouldbe low, and then h = {D- A*(* ))/(<y(*o)) '* positive. Therefore dD'/da > 0, Incontrast, when Co is low, Ag and fi{k^) will be high, so A < 0. Thus, a negative

Mao 423

ReferencesBradley. M.; C. JancU; and E. Kim. "On the Existence of an Optimal Capital Structure: Theory and

Evidence.- Journal of Finance, 39 (1984), 857-878.Brander, J., and X Lewis. "Xiligopoly and Financial Structure: the limited Liability Effect" American

Economic Review. 76 (1986), 956-971.Castariios. R. "Bankruptcy Risk and Optimal Capital Structure" Joiimai cf Finance, 38 (1983),

1617-1635.Dybvig, P. H., and J. E Zender. "C^)ital Structure and Dividend Irrelevance with Asymmetric Infor-

mation.'' Review cf Financial Studies, 4 (1991), 201-219.Gavish, B.. and A. Kalay. "On the Asset Substitution Problem." Journal of Financial and Quantitative

Analysis, 26 (1983), 21-30.Green. R.. and E. Tatmoc. "Asset Snbstitution and the Agency Costs of Debt Fmancing." Journal cf

Banking and Fuwnce. 10 (1986). 391-399.Harris. M.. and A. Raviv. "The Theixy of Capital Structure." Journal cf Finance. 46 (1991), 297-355.Jensen, M.. and W. Meckling. "Theoiy of the Firm: Managerial Behavior, Agency Costs, and Owner-

ship Structure." Journal of Financial Economics. 2 (1976), 305-360.Kale. J. R.; T. H. Noe; and G. G. Ramirez. The Effect of Business Risk on Coiponte Capital

Stricture: The(»y and Evidence." Journal cf Finance, 46 (1991), 1693-1715.Kim. M., and V. Maksimovic. "DKhnology, Debt and the Exploitation of Growth Options." Journal

of Banking and Finance, 14(1990), 1113-1131.Lang, L.; E. Ofek: and R. M. Stulz. "Leverage, Investment, and IHrm Growth." Journal of Financial

Economics. 40 (1996), 3-29.Li. D.. and S. U. "A Theory of Corporate Scope and Financial Structure." Journal cf Finance, 51

(1996), 691-709.Long. M. S., and L B. Malitz. "Investment Patterns and Financial Leverage." In Corporate Capital

Structures in the United States. B. M. Friedman, ed. Chicago. IL: Univ. of Chicago Press (1985).MflcKie-Mason, J. K. "Do l ^ e s AfTect Corpoiate Fmaricing Decisionsr Journal cf Finance, 45

(1990), 1471-1493.McConnell, J. J., and H. Servaes. "Equity Ownership and the Two Faces of DebL** Journal cf Finan-

cial Economics. 39 (1995), 131-157.My-ers, S. "Determinants of Corporate Borrowing." Journal (^Financial Economics. 5 (1977), 147-

175.Parrino. R., and M. S. Weisbach. "Measuring Investment Distortions Arising ftom Stockholdei-

Bondholder Conflicts." Journal of Financial Economics, 53 (1999), 3-42.Stulz. R. M. "Managerial Discretion and Optimal Financing Policies." Journal cf Financial Eco-

noTOV..«. 26 (1990), 3-27.Titmac. S.. and R. Wessels. "The Determinants of Capital Structure Choice." Journal of Finance, 43

(1988). 1-19.