Intel European Investor Meeting -...

27

INVESTOR MEETING 2011 Intel European Investor Meeting Christian Morales Vice President - Sales & Marketing, GM EMEA

-

Upload

dinhnguyet -

Category

Documents

-

view

215 -

download

1

Transcript of Intel European Investor Meeting -...

INVESTOR MEETING 2011

Intel European Investor Meeting

Christian Morales

Vice President - Sales & Marketing, GM EMEA

INVESTOR MEETING 2011

Reinventing the PC Again

The Attributes of a Tablet, the Performance of a PC. All Day, Every Day.

> 10 Hours Battery Life*

Ultra Secure Ultra Thin

Ultra Responsive

7X Graphics Improvement*

* Projections based on 2013 platforms. Actual results may vary due to OEM/ODM designs and system configurations.

INVESTOR MEETING 2011

2011 2012 2013 2014 2015

Revolutionizing Power & Performance for Low Power Devices

Intel Tablet GFX Performance*

Pe

rfo

rma

nce

(F

PS

)

Pe

rfo

rma

nce

*Projections for Atom based tablets, starting with 2011 (2nd generation tablets) as baseline SPEC2000int_rate

2011 2012 2013 2014 2015

Intel Tablet CPU Performance*

Intel Architecture in Competitive Phone and Tablet Form Factors

10X+

10X+

INVESTOR MEETING 2011

We Know How To Transform Experiences

1995 2003 2012/2013

Ultra Thin Ultra Secure

Ultra Responsive

22 nm Process Technology

Intel µ-architecture

(Haswell)

Ivy Bridge

130 nm Process Technology

Intel® µ-architecture (Pentium®M)

Banias

Multi-media

Instructions

Dadi: Do you want to use this slide as lead in?

Intel µ-architecture (Sandy Bridge)

Haswell

INVESTOR MEETING 2011

Translating Technology Leadership into

New Compelling Product Roadmaps

40W

20W

10W

5W

<1W

60W+

Power

New Notebook Design Target

Notebook Design Target

The result: A full spectrum of

products from milliwatts to

teraflops New

Expanded Range

Source: Intel Roadmap

SOC Design Target

INVESTOR MEETING 2011

Delivering the Next Exponential Increase in Visuals Graphics, Media, Imaging

Expect Another

12X Improvement in Processor Graphics

by 2015*

* Projecting 12X graphics improvement from 2011 to 2015 in the ‘new notebook design target’ power envelope.

INVESTOR MEETING 2011

The “No Compromise” Consumer PC Experience

Sleek, Cool, Super Responsive and a Full PC

• Thin and light at mainstream price points

• Best in class CPU and graphics performance

• Great visual and media experience

• Instant On and Always On /Always Connected

• World-class battery life

• Full keyboard − convertible to full touch

• Sensors

Other brands and names may be claimed as the property of others

INVESTOR MEETING 2011

Transition Begins Today

2011 2013 2012

Fast Flash Standby

Turbo

Always On /

Always Connected

Stylish Designs

Context Aware -

Sensors

Near Field

Communication

Touch User

Interface

Security for Online

Gaming and Media

Sharing

Sensor Based Sync

& Media Sharing

Mobile Gaming

and Video

Conferencing

World-class

Battery Life

DEMO: FFS, AO/AC and PC Synch

Thunderbolt

Other brands and names may be claimed as the property of others

INVESTOR MEETING 2011

Delivering Extraordinary Devices and Experiences

INVESTOR MEETING 2011

> 50% reduction

0.1

1

Low

er

Act

ive P

ow

er

Act

ive

Po

we

r p

er

Tra

nsi

sto

r (n

orm

alize

d)

22 Nm Tri-gate Transistors Increase The Benefit From A New Technology Generation

65nm

Planar

45nm

Planar

32nm

Planar

22nm

Tri-Gate

Constant Performance

Energy-Efficient Performance Built on Moore’s Law

Source: Intel

32nm 45nm 1x

0.1x

0.01x

0.001x

65nm 22nm

Low

er

Tra

nsi

stor

Leakage

Higher Transistor Performance (Switching Speed)

* Projected

14nm*

Source: Intel

22 nm Benefits Smallest Handhelds to Powerful Cloud-based Servers

INVESTOR MEETING 2011

Taking Full Advantage of Our Process Technology in New Markets

Silvermont

22nm

Low Power Microarchitecture

Optimized Power Performance

Microarchitecture

Saltwell

32nm

Bonnell

45nm

14nm Future Product

14nm

Airmont

*All products, computer systems, dates, and figures specified are preliminary based on current expectations, and are subject to

change without notice. Intel product plans in this presentation do not constitute Intel plan of record product roadmaps. Please

contact your Intel representative to obtain Intel‟s current plan of record product roadmaps

Accelerating the Atom™ SoC Roadmap

Sandy Bridge Westmere Future Product Ivy Bridge 32nm 22nm

2011-2012

2013 2014

INVESTOR MEETING 2011

A Systems Approach to Low Power

INTEL CPU GFX VIDEO DISPLAY

INTEL‟S INTERCONNECT FABRIC

BRIDGE to

EXT FABRIC

EXTERNAL ECOSYSTEM FABRIC

MEM CTRL

MEMORY INTERCONNECT

IOs 3rd PARTY

IPs ACCELERATOR

IPs

3rd PARTY IPs

System On a Chip Across All Devices

Not Just CPU & Graphics, but All the Assets to Deliver Complete Solutions

INVESTOR MEETING 2011

SoC Ecosystem for Devices in the Continuum

SOC Chassis

Base SoC

SoC Modularity Enables Reuse Across Devices

Handheld

Embedded Digital Home

Tablet

Micro Server

INVESTOR MEETING 2011

Consistency Across Platforms

INVESTOR MEETING 2011

Redefining Connectivity

3G 10G

• Not just connecting to the Internet, but moving data/images and content seamlessly between devices

• Wi-Fi, Bluetooth, Near Field Communications, etc to share content consistently across a continuum of devices.

• Wi-Di demonstrates Intel‟s ability to deliver completeness of the solution

Other brands and names may be claimed as the property of others

INVESTOR MEETING 2011

Data Center Group

CHARTER

Servers Storage Networking (Wired)

Software & System Building Blocks

INVESTOR MEETING 2011

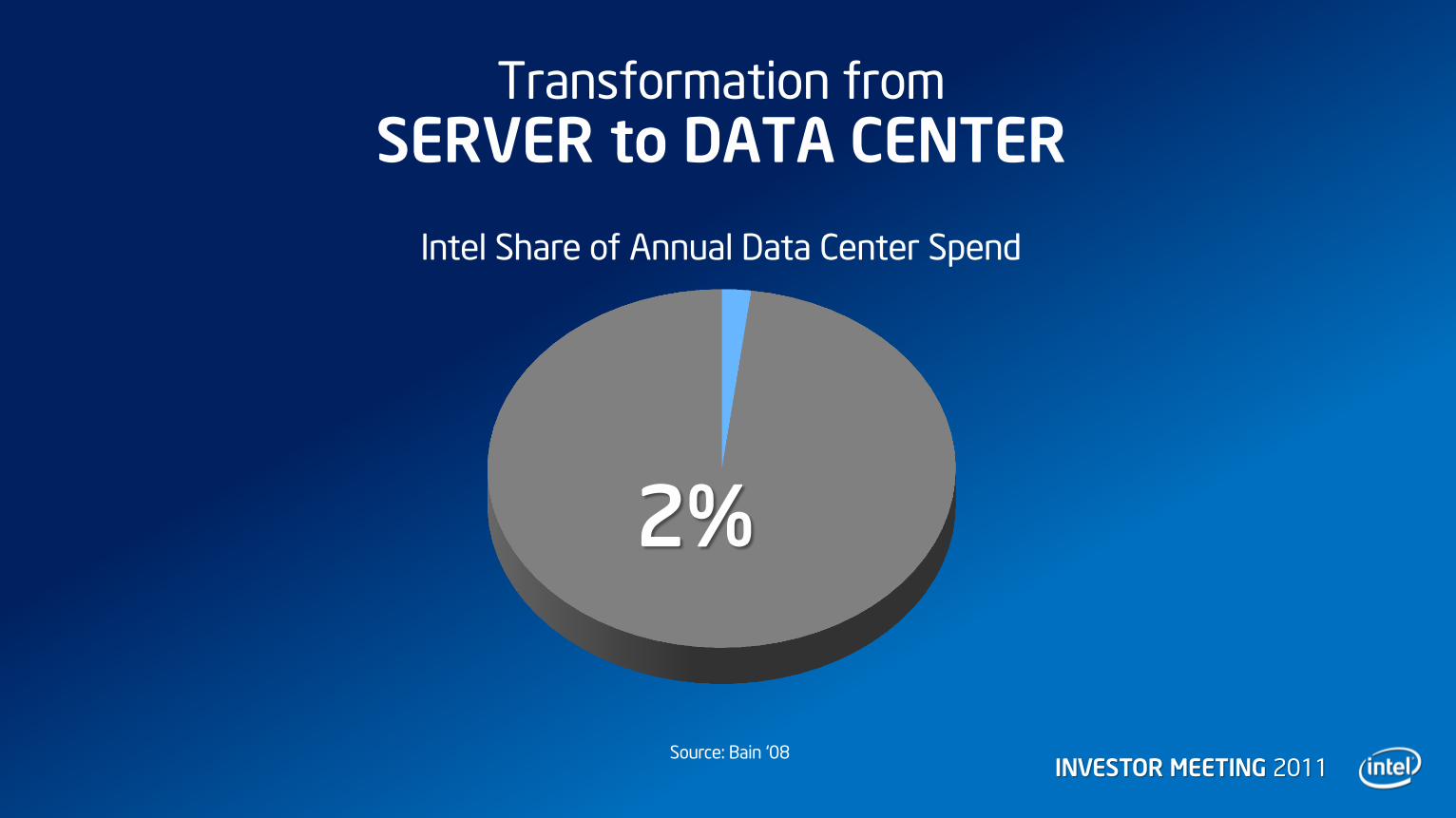

Transformation from

SERVER to DATA CENTER

Source: Bain „08

Intel Share of Annual Data Center Spend

2%

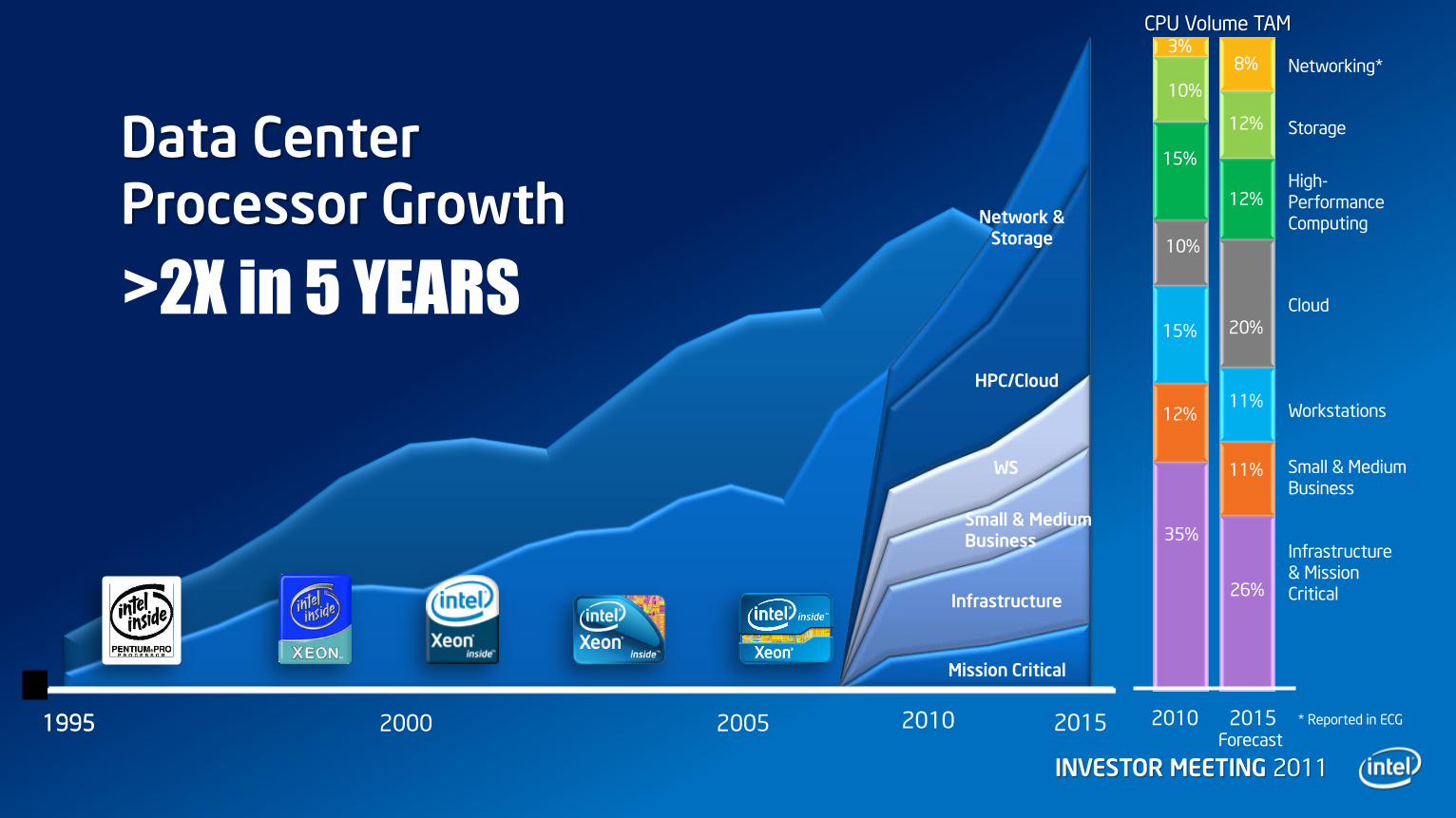

INVESTOR MEETING 2011

2010 2015

Mission Critical

Infrastructure

Small & Medium Business

WS

HPC/Cloud

Network & Storage

1995 1995 2000 2005

CPU Volume TAM

2010 2015

Networking*

Storage

High-Performance Computing

Cloud

Small & Medium Business

Infrastructure & Mission Critical

Workstations

3%

10%

15%

35%

10%

15%

12%

8%

12%

12%

20%

26%

11%

11%

Forecast

Data Center Processor Growth

>2X in 5 YEARS

* Reported in ECG

INVESTOR MEETING 2011

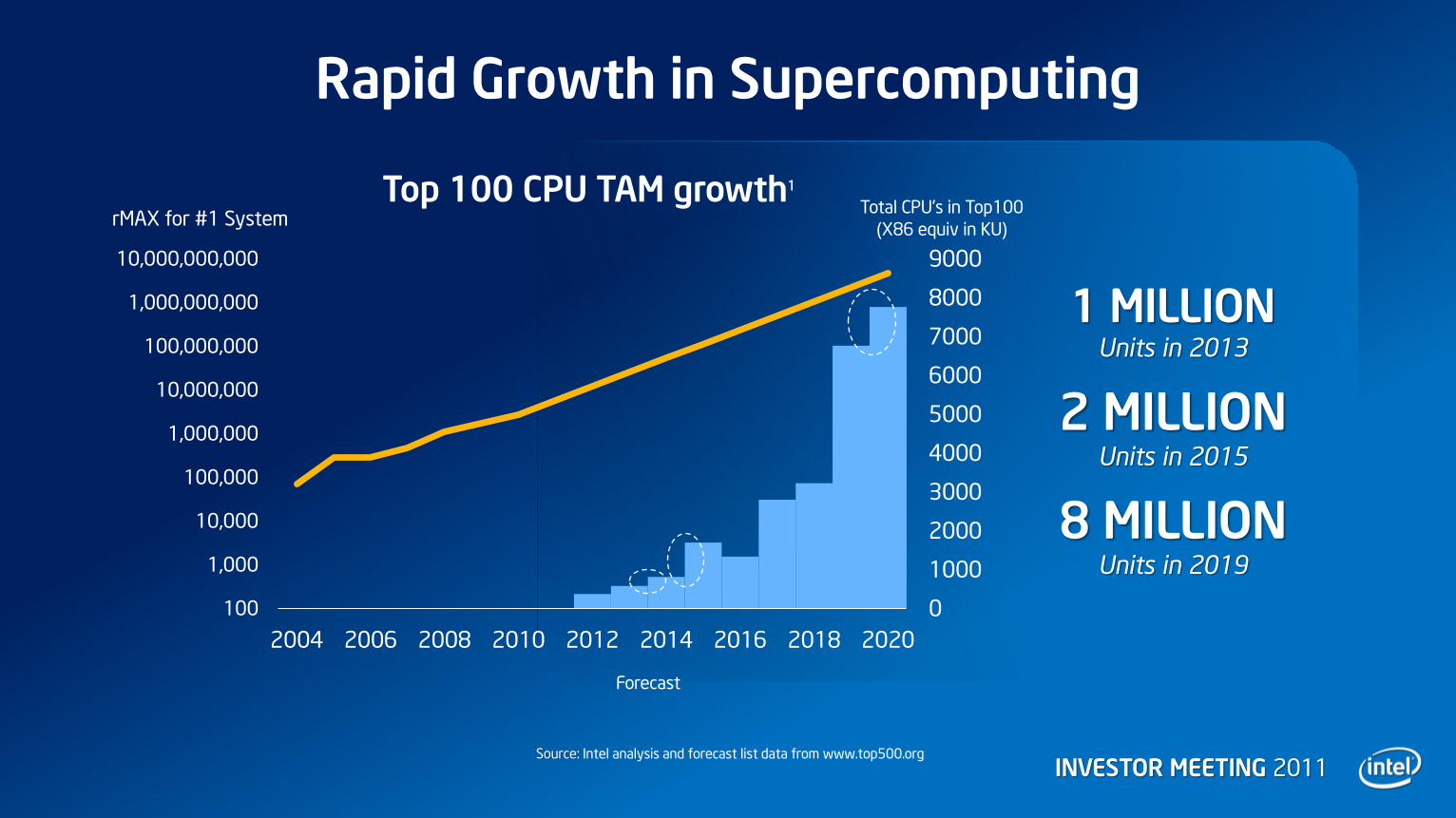

Rapid Growth in Supercomputing

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

100

1,000

10,000

100,000

1,000,000

10,000,000

100,000,000

1,000,000,000

10,000,000,000

2004 2006 2008 2010 2012 2014 2016 2018 2020

Total CPU's in Top100

(X86 equiv in KU) rMAX for #1 System

Top 100 CPU TAM growth1

1 MILLION Units in 2013

2 MILLION Units in 2015

8 MILLION Units in 2019

Forecast

Source: Intel analysis and forecast list data from www.top500.org

INVESTOR MEETING 2011

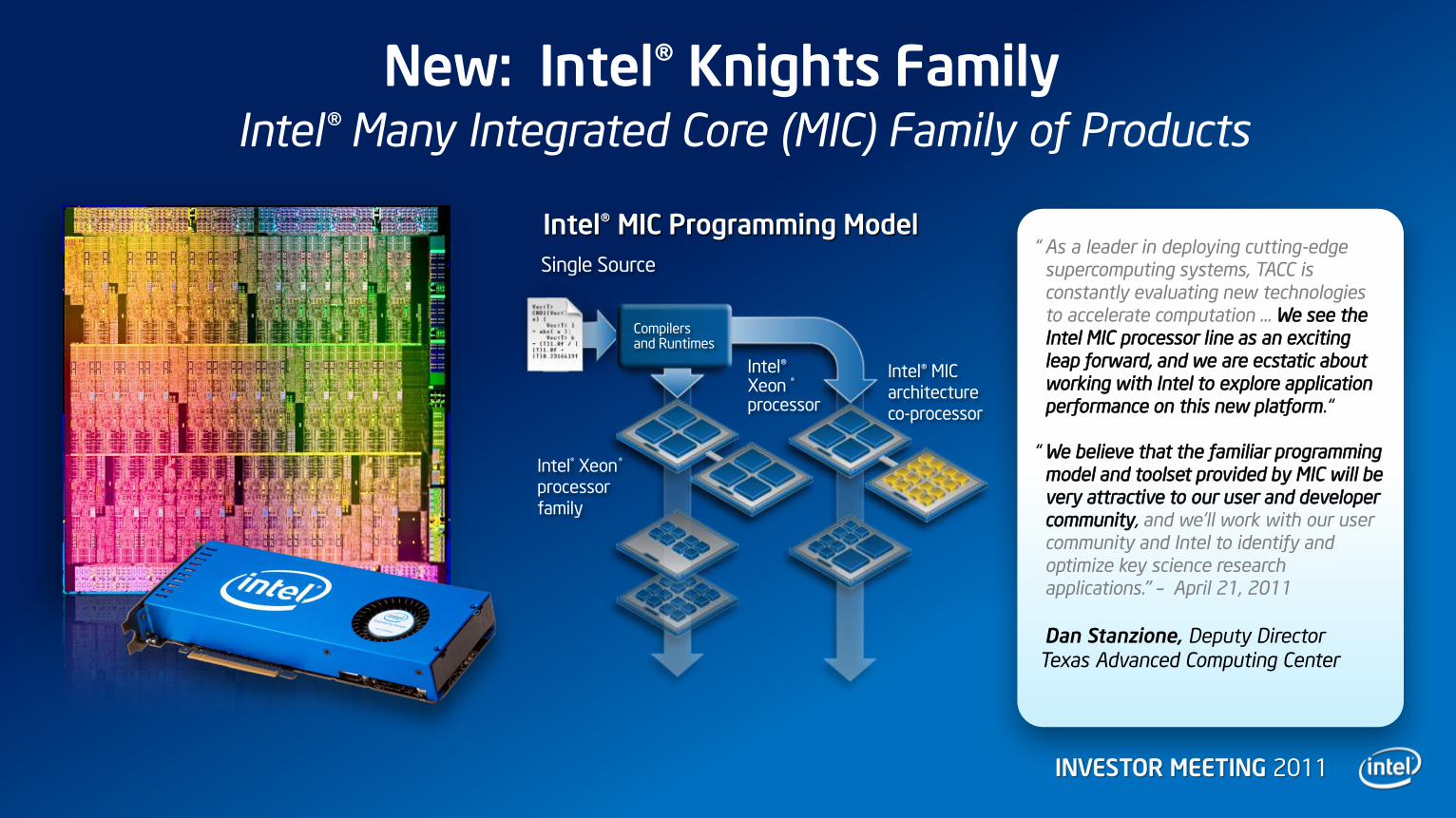

New: Intel® Knights Family Intel® Many Integrated Core (MIC) Family of Products

Intel® MIC Programming Model

Intel® Xeon® processor family

Intel® Xeon ® processor

Intel® MIC architecture co-processor

Single Source

Compilers and Runtimes

“ As a leader in deploying cutting-edge

supercomputing systems, TACC is

constantly evaluating new technologies

to accelerate computation … We see the

Intel MIC processor line as an exciting

leap forward, and we are ecstatic about

working with Intel to explore application

performance on this new platform.“

“ We believe that the familiar programming

model and toolset provided by MIC will be

very attractive to our user and developer

community, and we'll work with our user

community and Intel to identify and

optimize key science research

applications." – April 21, 2011

Dan Stanzione, Deputy Director

Texas Advanced Computing Center

INVESTOR MEETING 2011

Forecast Forecast

Cloud 2015 More users, more devices, more data, more storage, more traffic …

1. IDC “The Internet Reaches Late Adolescence” Dec 2009, extrapolation by Intel for 2015

2. ECG “Worldwide Device Estimates Year 2020 - Intel One Smart Network Work” forecast

3. IDC

4. Source: http://www.cisco.com/assets/cdc_content_elements/networking_solutions/service_provider/visual_networking_ip_traffic_chart.html,

http://www.cisco.com/en/US/solutions/collateral/ns341/ns525/ns537/ns705/ns827/white_paper_c11-481360_ns827_Networking_Solutions_White_Paper.html extrapolated to 2015

0

200

400

600

800

1000

1200

2009 2010 2011 2012 2013 2014 2015

15B

>1000 >1B NEW NETIZENS

CONNECTED DEVICES

EXABYTES OF TRAFFIC

0

20

40

60

80

100

2009 2010 2011 2012 2013 2014

670% GROWTH IN STORAGE

CAPACITY SHIPPED

Exabytes Exabytes

INVESTOR MEETING 2011

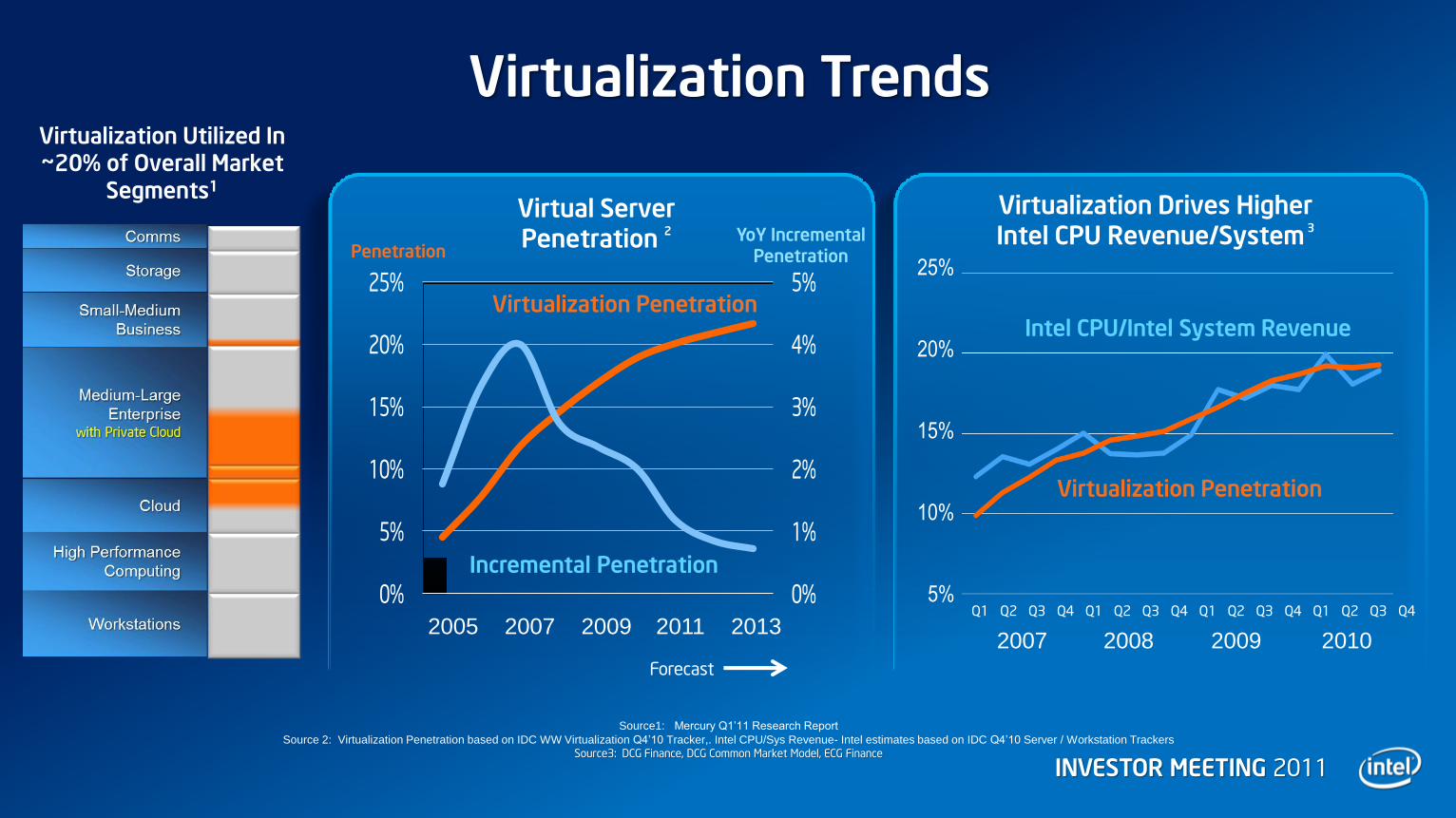

Virtualization Trends

Source1: Mercury Q1’11 Research Report

Source 2: Virtualization Penetration based on IDC WW Virtualization Q4’10 Tracker,. Intel CPU/Sys Revenue- Intel estimates based on IDC Q4’10 Server / Workstation Trackers

Source3: DCG Finance, DCG Common Market Model, ECG Finance

Virtualization Utilized In ~20% of Overall Market

Segments1

Virtualization Drives Higher Intel CPU Revenue/System

3

Intel CPU/Intel System Revenue

Virtualization Penetration

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2008 2009 2010

5%

10%

15%

20%

25%

Forecast

Intel CPU/System Revenue Share and Virtualization Penetration3

0%

5%

10%

15%

20%

25%

Q1

'07

Q2

'07

Q3

'07

Q4

'07

Q1

'08

Q2

'08

Q3

'08

Q4

'08

Q1

'09

Q2

'09

Q3

'09

Q4

'09

Intel CPU/ Intel System Revenue

Virtualization Penetration

Pe

ne

tra

tio

n

Yo

YIn

cre

me

nta

l P

en

etr

atio

n

Forecast

0%

1%

2%

3%

4%

5%

0%

5%

10%

15%

20%

25%

Virtual Server Penetration2

Virtualization Penetration

Incremental Penetration

Virtual Server Penetration

2

Virtualization Penetration

Incremental Penetration

2005 2007 2009 2011 2013

Penetration YoY Incremental

Penetration

INVESTOR MEETING 2011

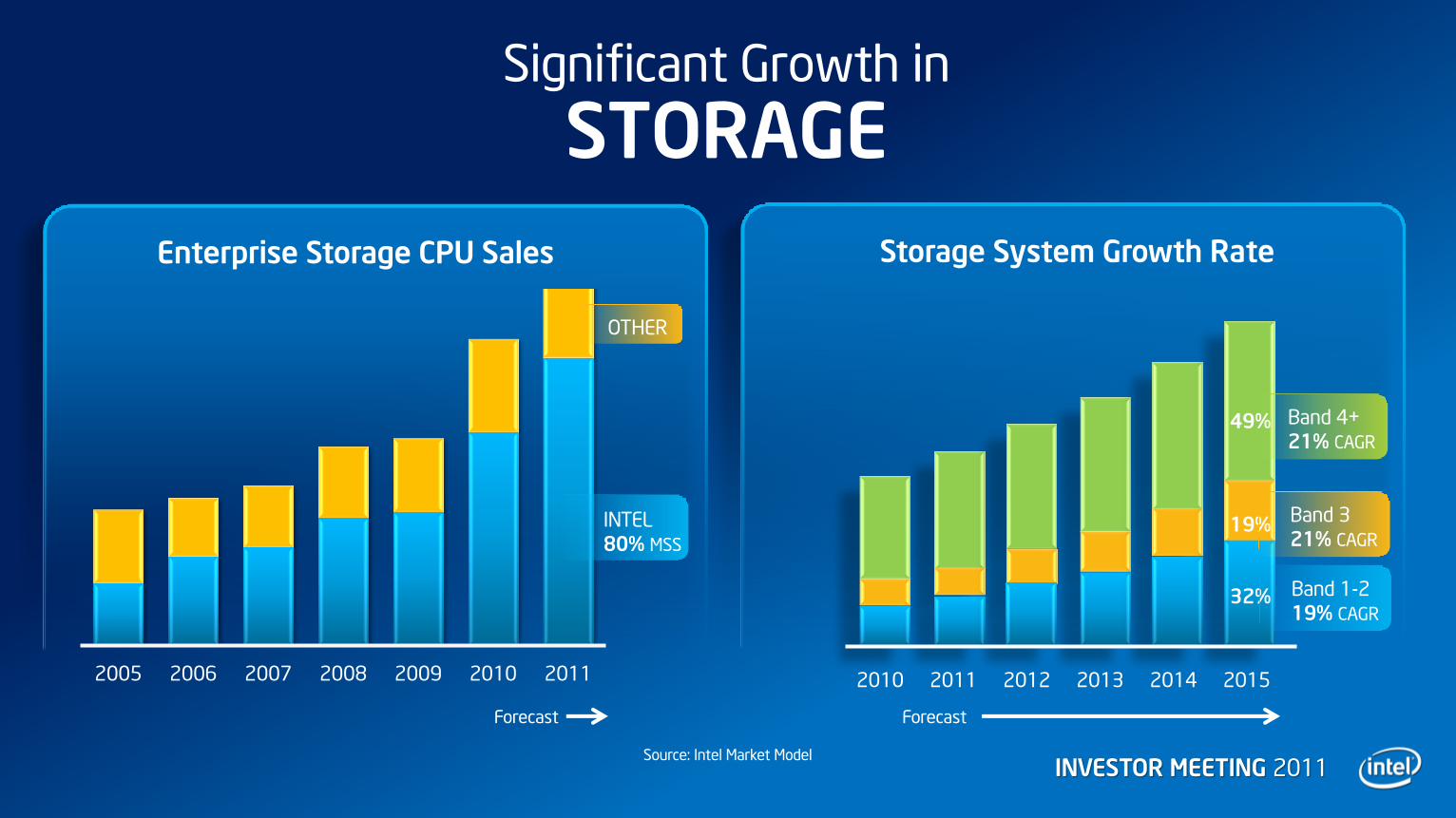

Significant Growth in

STORAGE

2010 2011 2012 2013 2014 2015

49%

19%

32% Band 1-2

19% CAGR

Band 3

21% CAGR

Band 4+

21% CAGR

Storage System Growth Rate

2005 2006 2007 2008 2009 2010 2011

Enterprise Storage CPU Sales

INTEL

80% MSS

OTHER

Forecast Forecast

Source: Intel Market Model

INVESTOR MEETING 2011

Networking Transformation

2008 2010

>60% INCREASE

IN

VOLUME

Sources:

Dell‟Oro Q4‟10 Ethernet Report

Intel shipments

Top 10 MNC Networking OEM Intel CPU Shipments

Intel® 10Gbe Adapter: #1 MSS

$100M ramp in < 1 Year

INVESTOR MEETING 2011

2010*

RISC MIGRATION Transition from Proprietary to Standards-Based Computing

Source: IDC World Wide Server Tracker Q4‟10, system revenue

RISC/

Mainframes

$30B

RISC/

Mainframes

$15B Intel x86

$19.2B Intel x86

$30.5B AMD

$2.8B

AMD $330M

$102M $4B

2002

Intel® Itanium® Intel® Itanium®

INVESTOR MEETING 2011 26

Risk Factors

The above statements and any others in this document that refer to plans and expectations for the second quarter, the year and the future are forward-looking statements that involve a number of risks and uncertainties. Words such as “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “may,” “will,” “should,” and their variations identify forward-looking statements. Statements that refer to or are based on projections, uncertain events or assumptions also identify forward-looking statements. Many factors could affect Intel‟s actual results, and variances from Intel‟s current expectations regarding such factors could cause actual results to differ materially from those expressed in these forward-looking statements. Intel presently considers the following to be the important factors that could cause actual results to differ materially from the company‟s expectations. Demand could be different from Intel's expectations due to factors including changes in business and economic conditions, including supply constraints and other disruptions affecting customers; customer acceptance of Intel‟s and competitors‟ products; changes in customer order patterns including order cancellations; and changes in the level of inventory at customers. Potential disruptions in the high technology supply chain resulting from the recent disaster in Japan could cause customer demand to be different from Intel‟s expectations. Intel operates in intensely competitive industries that are characterized by a high percentage of costs that are fixed or difficult to reduce in the short term and product demand that is highly variable and difficult to forecast. Revenue and the gross margin percentage are affected by the timing of Intel product introductions and the demand for and market acceptance of Intel's products; actions taken by Intel's competitors, including product offerings and introductions, marketing programs and pricing pressures and Intel‟s response to such actions; and Intel‟s ability to respond quickly to technological developments and to incorporate new features into its products. The gross margin percentage could vary significantly from expectations based on capacity utilization; variations in inventory valuation, including variations related to the timing of qualifying products for sale; changes in revenue levels; product mix and pricing; the timing and execution of the manufacturing ramp and associated costs; start-up costs; excess or obsolete inventory; changes in unit costs; defects or disruptions in the supply of materials or resources; product manufacturing quality/yields; and impairments of long-lived assets, including manufacturing, assembly/test and intangible assets. Expenses, particularly certain marketing and compensation expenses, as well as restructuring and asset impairment charges, vary depending on the level of demand for Intel's products and the level of revenue and profits. The tax rate expectation is based on current tax law and current expected income. The tax rate may be affected by the jurisdictions in which profits are determined to be earned and taxed; changes in the estimates of credits, benefits and deductions; the resolution of issues arising from tax audits with various tax authorities, including payment of interest and penalties; and the ability to realize deferred tax assets. Gains or losses from equity securities and interest and other could vary from expectations depending on gains or losses on the sale, exchange, change in the fair value or impairments of debt and equity investments; interest rates; cash balances; and changes in fair value of derivative instruments. The majority of Intel‟s non-marketable equity investment portfolio balance is concentrated in companies in the flash memory market segment, and declines in this market segment or changes in management‟s plans with respect to Intel‟s investments in this market segment could result in significant impairment charges, impacting restructuring charges as well as gains/losses on equity investments and interest and other. Intel's results could be affected by adverse economic, social, political and physical/infrastructure conditions in countries where Intel, its customers or its suppliers operate, including military conflict and other security risks, natural disasters, infrastructure disruptions, health concerns and fluctuations in currency exchange rates. Intel‟s results could be affected by the timing of closing of acquisitions and divestitures. Intel's results could be affected by adverse effects associated with product defects and errata (deviations from published specifications), and by litigation or regulatory matters involving intellectual property, stockholder, consumer, antitrust and other issues, such as the litigation and regulatory matters described in Intel's SEC reports. An unfavorable ruling could include monetary damages or an injunction prohibiting us from manufacturing or selling one or more products, precluding particular business practices, impacting Intel‟s ability to design its products, or requiring other remedies such as compulsory licensing of intellectual property. A detailed discussion of these and other factors that could affect Intel‟s results is included in Intel‟s SEC filings, including the report on Form 10-Q for the quarter ended April 2, 2011.

Rev. 5/9/11