Integris Credit Union - Integris - Banking, Insurance, and ... · Integris Credit Union March 2,...

56

Consolidated Financial statements of Integris Credit Union December 31, 2016

Transcript of Integris Credit Union - Integris - Banking, Insurance, and ... · Integris Credit Union March 2,...

Consolidated Financial statements of

Integris Credit Union

December 31, 2016

Integris Credit Union December 31, 2016 Table of contents Independent Auditor’s Report ................................................................................... 1-2

Consolidated Statement of Financial Position .............................................................. 3

Consolidated Statement of Comprehensive Income .................................................... 4

Consolidated Statement of Changes in Members’ Equity ............................................ 5

Consolidated Statement of Cash Flows ....................................................................... 6

Notes to the Consolidated Financial Statements .................................................... 7-53

Consolidated Continuity of Property and Equipment ................................................. 54

Deloitte LLP 500-299 Victoria Street Prince George BC V2L 5B8 Canada Tel: 250-564-1111 Fax: 250-562-4950 www.deloitte.ca

INDEPENDENT AUDITOR’S REPORT To the Members of Integris Credit Union We have audited the accompanying consolidated financial statements of Integris Credit Union, which comprise the consolidated statement of financial position as at December 31, 2016, and the consolidated statement of comprehensive income, consolidated statement of changes in members’ equity and consolidated statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information. Management’s Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

1

Integris Credit Union March 2, 2017 Page 2

Opinion In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of Integris Credit Union as at December 31, 2016, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards.

Chartered Professional Accountants

Prince George, BC March 2, 2017

2

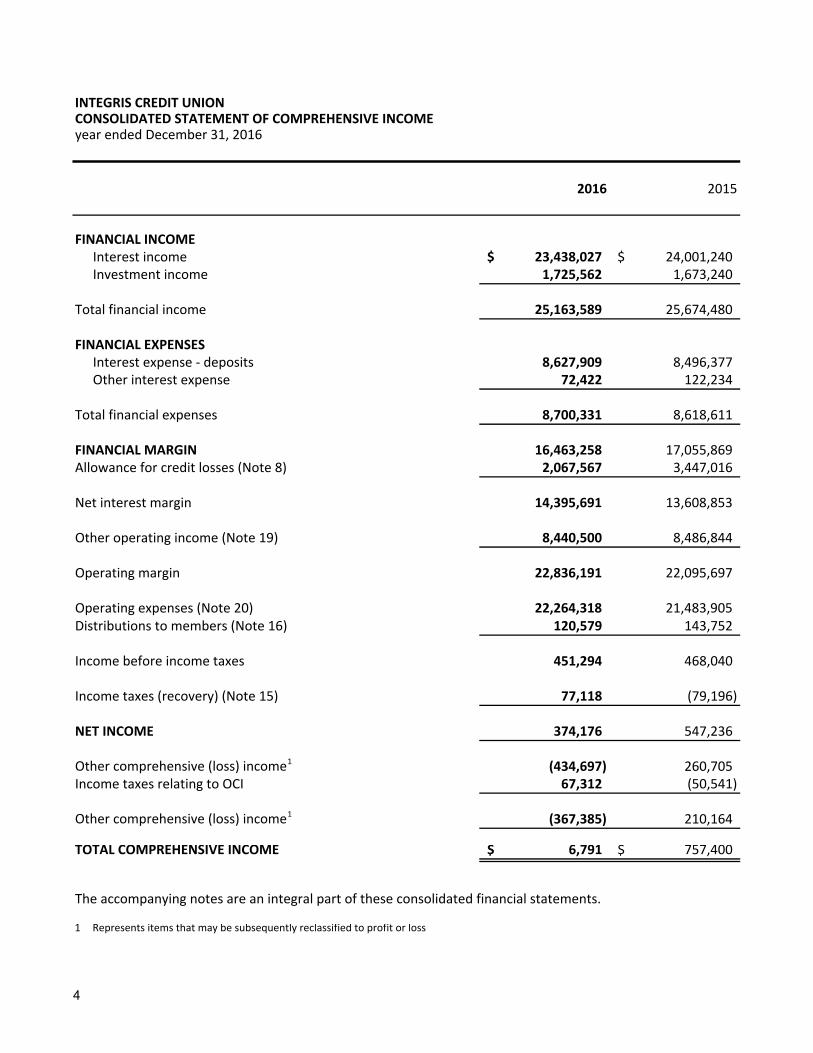

INTEGRIS CREDIT UNION CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOMEyear ended December 31, 2016

2016 2015

FINANCIAL INCOMEInterest income $ 23,438,027 $ 24,001,240 Investment income 1,725,562 1,673,240

Total financial income 25,163,589 25,674,480

FINANCIAL EXPENSESInterest expense ‐ deposits 8,627,909 8,496,377 Other interest expense 72,422 122,234

Total financial expenses 8,700,331 8,618,611

FINANCIAL MARGIN 16,463,258 17,055,869 Allowance for credit losses (Note 8) 2,067,567 3,447,016

Net interest margin 14,395,691 13,608,853

Other operating income (Note 19) 8,440,500 8,486,844

Operating margin 22,836,191 22,095,697

Operating expenses (Note 20) 22,264,318 21,483,905 Distributions to members (Note 16) 120,579 143,752

Income before income taxes 451,294 468,040

Income taxes (recovery) (Note 15) 77,118 (79,196)

NET INCOME 374,176 547,236

Other comprehensive (loss) income1 (434,697) 260,705 Income taxes relating to OCI 67,312 (50,541)

Other comprehensive (loss) income1 (367,385) 210,164

TOTAL COMPREHENSIVE INCOME $ 6,791 $ 757,400

The accompanying notes are an integral part of these consolidated financial statements.

1 Represents items that may be subsequently reclassified to profit or loss

4

INTEGRIS CREDIT UNIONCONSOLIDATED STATEMENT OF CHANGES IN MEMBERS' EQUITYyear ended December 31, 2016

Accumulatedother

Contributed comprehensiveMember Equity Retained incomeshares (Note 17) earnings (Note 18) Total

As at December 31, 2014 $ 6,156,802 $ 6,953,743 $ 18,518,091 $ 588,499 $ 32,217,135

Total comprehensive income ‐ ‐ 547,236 210,164 757,400

Issued membership shares 2,453,608 ‐ ‐ ‐ 2,453,608 Redeemed membership shares (147,033) ‐ ‐ ‐ (147,033) Dividends on investment shares 290,603 ‐ (243,525) ‐ 47,078

As at December 31, 2015 $ 8,753,980 $ 6,953,743 $ 18,821,802 $ 798,663 $ 35,328,188 Total comprehensive income ‐ ‐ 374,176 (367,385) 6,791 Issued membership shares 1,409,305 ‐ ‐ ‐ 1,409,305 Redeemed membership shares (215,063) ‐ ‐ ‐ (215,063) Dividends on investment shares 261,072 ‐ (217,050) ‐ 44,022

As at December 31, 2016$ 10,209,294 $ 6,953,743 $ 18,978,928 $ 431,278 $ 36,573,243

The accompanying notes are an integral part of these consolidated financial statements.

5

INTEGRIS CREDIT UNION

CONSOLIDATED STATEMENT OF CASH FLOWS

year ended December 31, 2016

2016 2015

Operating activitiesNet income $ 374,176 $ 547,236 Adjustments forAllowance for credit losses 2,067,567 3,447,016 Interest income (24,562,332) (24,942,826) Interest expense 8,700,331 8,618,611 Depreciation 1,590,754 1,427,951 Net loss on financial assets designated at fair value through profit or loss 8,875 31,252

(Gain) loss on sale of property and equipment ‐ (204,564) Income tax (recovery) expense 77,118 (79,196) Interest received 24,506,599 24,539,050 Interest paid (8,657,743) (8,121,450) Income tax paid 193,976 (394,222) Non‐cash distributions to members 120,579 143,752 Net unrealized foreign exchange gain (7,093) (6,102)

4,412,807 5,006,508

Changes in operating assets/liabilities:Loans to members, net of repayments (9,694,310) (36,066,378) Deposits from members, net of withdrawals 28,873,775 55,373,787 Other operating assets (571,295) (520,617) Other operating liabilities 355,766 (359,745)

23,376,743 23,433,555

Investing activitiesPurchase of equity investments (309,973) (320,434) Purchase of term deposits (29,650,000) (4,850,000) Purchase of intangible assets (2,876,518) (1,377,613) Purchase of property and equipment (911,342) (5,039,745) Proceeds from sale of property and equipment ‐ 213,367

(33,747,833) (11,374,425)

Financing activitiesProceeds from issuance of membership share capital 2,482,486 498,106 Redemption of membership share capital (2,575,314) (588,241) Proceeds from issuance of investment shares 2,077,298 3,377,551 Redemption of investment shares (592,862) (494,333) Repayment of loan securitization borrowings (187,601) (1,014,792) Proceeds from credit facility borrowings ‐ 39,000,000 Repayment of credit facility borrowings ‐ (39,000,000)

1,204,007 1,778,291

Net change in cash and cash equivalents (9,167,083) 13,837,421

Cash and cash equivalents, beginning of year 26,727,022 12,314,809

Effects of exchange rate changes on the balance of cash held in foreign currencies (304,223) 574,792

Cash and cash equivalents, end of year $ 17,255,716 $ 26,727,022

The accompanying notes are an integral part of these consolidated financial statements.

6

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

7

1. NATURE OF OPERATIONS AND BASIS OF PRESENTATION

Reporting entity

Integris Credit Union (the “Credit Union”) is incorporated under the Credit Union Incorporation Act of

British Columbia and is a member of Central 1 Credit Union Limited (“Central 1”). The Credit Union

operates as one operating segment in the loans and deposit taking industry in British Columbia.

Products and services offered to its members include mortgages, personal, and commercial loans ,

chequing and savings accounts, term deposits, RRSPs, RRIFs, TFSA’s, mutual funds, automated banking

machines, debit and credit cards and internet banking, financial planning services, and operates an

insurance agency. The Credit Union head office is located at 1598 6th Avenue, Prince George, British

Columbia.

These consolidated financial statements (the “financial statements”) have been authorized for issue

by the Board of Directors on March 2, 2017.

Basis of presentation

These financial statements have been prepared in accordance with International Financial Reporting

Standards (“IFRS”) as issued by the International Accounting Standards Board (the “IASB”).

These financial statements were prepared under the historical cost convention, as modified by the

revaluation of available‐for‐sale financial assets and derivative financial instruments measured at fair

value.

The Credit Union’s functional and presentation currency is the Canadian dollar.

The preparation of financial statements, in compliance with IFRS, requires management to make

certain critical accounting estimates. It also requires management to exercise judgment in applying

the Credit Union’s accounting policies. The areas involving a higher degree of judgment or complexity,

or areas where assumptions and estimates are significant to the financial statements are disclosed in

Notes 2 and 3.

Basis of consolidation

The consolidated financial statements incorporate the financial statements of the Credit Union and its wholly owned subsidiaries Integris Insurance Services Ltd., Integris Financial Planning Services Ltd. and 608538 BC Ltd., as well as its 20% interest in a joint operation in Northline Management Ltd. Control is achieved when the Credit Union:

has power over the investee;

is exposed, or has rights, to variable returns from its involvement with the investee; and

has the ability to use its power to affect its returns.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

8

1. NATURE OF OPERATIONS AND BASIS OF PRESENTATION (continued)

Basis of consolidation (continued)

The Credit Union reassesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control listed above.

When the Credit Union has less than a majority of the voting rights of an investee, it has power over the investee when the voting rights are sufficient to give it the practical ability to direct the relevant activities of the investee unilaterally. The Credit Union considers all relevant facts and circumstances in assessing whether or not the Credit Union's voting rights in an investee are sufficient to give it power, including:

the size of the Credit Union’s holding of voting rights relative to the size and dispersion of holdings of the other vote holders;

potential voting rights held by the Credit Union, other vote holders or other parties;

rights arising from other contractual arrangements; and

any additional facts and circumstances that indicate that the Credit Union has, or does not have, the current ability to direct the relevant activities at the time that decisions need to be made, including voting patterns at previous shareholders' meetings.

When necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with the Credit Union's accounting policies.

All intragroup assets and liabilities, equity, income, expenses and cash flows relating to transactions between the Credit Union and its investees are eliminated in full on consolidation.

Interests in joint operations

A joint operation is a joint arrangement whereby the parties that have joint control of the arrangement have rights to the assets, and obligations for the liabilities, relating to the arrangement. Joint control is the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require unanimous consent of the parties sharing control.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

9

1. NATURE OF OPERATIONS AND BASIS OF PRESENTATION (continued)

Interests in joint operations (continued)

When a group entity undertakes its activities under joint operations, the Credit Union as a joint operator recognizes in relation to its interest in a joint operation:

its assets, including its share of any assets held jointly;

its liabilities, including its share of any liabilities incurred jointly;

its share of the revenue from the sale of the output by the joint operation; and

its expenses, including its share of any expenses incurred jointly.

The Credit Union accounts for the assets, liabilities, revenues and expenses relating to its interest in a

joint operation in accordance with the IFRSs applicable to the particular assets, liabilities, revenues

and expenses.

When a group entity transacts with a joint operation in which a group entity is a joint operator (such as a sale or contribution of assets), the Credit Union is considered to be conducting the transaction with the other parties to the joint operation, and gains and losses resulting from the transactions are recognized in the Credit Union’s financial statements only to the extent of other parties' interests in the joint operation.

When a group entity transacts with a joint operation in which a group entity is a joint operator (such as a purchase of assets), the Credit Union does not recognize its share of the gains and losses until it resells those assets to a third party.

2. SIGNIFICANT ACCOUNTING POLICIES

The accounting policies set out below have been applied consistently by the Credit Union to all periods presented in these financial statements.

Business combinations

The Credit Union accounts for acquisitions using the acquisition method as at the acquisition date,

which is the date on which control is acquired by the Credit Union. Control is the power to govern,

the financial and operating policies of an entity so as to obtain benefits from its activities. In

assessing control, the Credit Union takes into consideration potential voting rights that are currently

exercisable or de facto control which is the ability to control because no other party has the power

to govern.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

10

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Business combinations (continued)

The Credit Union elects for each acquisition whether to measure non‐controlling interest at fair

value or at its proportionate share of the recognized amount of the identifiable net assets at the

acquisition date.

Transaction costs incurred with the acquisition, other than those associated with the issue of debt or

equity securities, are expensed as incurred.

Financial instruments

Financial assets and financial liabilities are recognized when the Credit Union becomes a party to the

contractual provisions of the instrument.

Financial assets and financial liabilities are initially recognized at fair value and their subsequent

measurement is dependent on their classification as described below. Their classification depends

on the purpose for which the financial instruments were acquired or issued, their characteristics and

the Credit Union’s designation of such instruments. Settlement date accounting is used.

The Credit Union is required to classify all financial assets either as fair value through profit or loss,

available‐for‐sale, held‐to‐maturity, or loans and receivables. Financial liabilities are classified as

either fair value through profit or loss, or other liabilities.

The standards require that all financial assets and financial liabilities, including all derivatives, be

subsequently measured at fair value with the exception of loans and receivables, debt securities

classified as held‐to‐maturity, available‐for‐sale financial assets that do not have quoted market

prices in an active market and whose fair value cannot be reliably estimated, and other liabilities.

a) Fair value through profit or loss (“FVTPL”) Financial assets and liabilities are classified as FVTPL when the financial asset or financial liability

is either held for trading or it is designated as at FVTPL.

A financial asset or financial liability is classified as held for trading if:

it has been acquired principally for the purpose of selling it in the near term; or

on initial recognition it is part of a portfolio of identified financial instruments that the Credit Union manages together and has a recent pattern of short‐term profit‐taking; or

it is a derivative that is not designated and effective as a hedging instrument.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

11

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Financial instruments (continued)

a) Fair value through profit or loss (continued)

A financial asset and financial liability other than a financial asset or financial liability held for trading may be designated as at FVTPL upon initial recognition if:

such designation eliminates or significantly reduces a measurement or recognition inconsistency that would otherwise arise; or

the financial asset/liability forms part of a group of financial assets or financial liabilities or both, which is managed and its performance is evaluated on a fair value basis, in accordance with the Credit Union’s documented risk management or investment strategy, and information about the grouping is provided internally on that basis; or

it forms part of a contract containing one or more embedded derivatives, and IAS 39 permits the entire combined contract (asset or liability) to be designated as at FVTPL.

Financial assets and financial liabilities at FVTPL are stated at fair value, with any gains or losses arising on re‐measurement recognized in profit or loss. The net gain or loss recognized in profit or loss incorporates any dividend or interest earned/paid on the financial asset/liability and is included in other operating income.

As at December 31, 2016, the Credit Union’s financial assets and financial liabilities classified as FVTPL include derivative instruments, unless they are designated and effective as hedging instruments in a hedge accounting relationship, and embedded derivatives.

b) Held‐to‐maturity

Held‐to‐maturity investments are non‐derivative financial assets with fixed or determinable payments and fixed maturity dates that the Credit Union has the positive intent and ability to hold to maturity, other than those that the entity upon initial recognition designates as fair value through profit or loss or as available for sale.

Subsequent to initial recognition, held‐to‐maturity financial assets are measured at amortized cost using the effective interest method, net of impairment losses.

As at December 31, 2016, the Credit Union’s held‐to‐maturity investments consist of liquidity deposits held with Central 1.

c) Available‐ for‐ sale financial assets

Available‐for‐sale financial assets are non‐derivative financial assets that are either designated as available‐for‐sale or are not classified as (a) loans and receivables, (b) held‐to‐maturity investments or (c) financial assets at fair value through profit or loss.

Shares held by the Credit Union that are not traded in an active market are classified as available‐for‐sale.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

12

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Financial instruments (continued)

c) Available‐ for‐ sale financial assets (continued)

Available‐for‐sale equity investments that do not have a quoted market price in an active market and whose fair value cannot be reliably measured are measured at cost less any identified impairment losses at the end of each reporting period.

Subsequent to initial recognition, available‐for‐sale financial assets that trade on an active market are measured at fair value, and the gains and losses on such assets are recorded in other comprehensive income until the investment is derecognized or until the investment is identified as being subject to impairment.

As at December 31, 2016, the Credit Union’s available‐for‐sale financial assets consist of equity investments.

d) Loans and receivables

Loans and receivables are non‐derivative financial assets with fixed or determinable payments that are not quoted in an active market and which the Credit Union does not intend to sell immediately or in the near term.

As at December 31, 2016, the Credit Union’s loans and receivables consist of loans to members, accrued interest on loans, accrued interest on investments, and accounts receivable, and are measured at amortized cost using the effective interest method, net of impairment losses.

Interest income is recognized by applying the effective interest rate.

e) Effective interest method The effective interest method is a method of calculating the amortized cost of a financial asset or financial liability and of allocating interest income/ expense over the relevant period. The effective interest rate is the rate that exactly discounts the estimated future cash payments and receipts through the expected life of the financial asset or liability (or, where appropriate, a shorter period) to the carrying amount of the financial asset or liability.

f) Impairment of financial assets Financial assets, other than those at fair value through profit or loss, are assessed for indicators of impairment at each period end date. Financial assets are impaired where there is objective evidence that, as a result of one or more events that occurred after the initial recognition of the financial asset, the estimated future cash flows of the asset have been affected. For financial assets carried at amortized cost and available‐for‐sale debt securities, the amount of the impairment is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the financial asset’s original effective interest rate.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

13

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Financial instruments (continued)

f) Impairment of financial assets (continued) The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets with the exception of loans to members, where the carrying amount is reduced through the use of an allowance account. When a loan to a member is considered uncollectible, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited against the allowance account. Changes in the carrying amount of the allowance account are recognized in profit or loss.

The impairment loss on financial assets is based on a review of all outstanding amounts at period end. The Credit Union has established percentages for the allowance for doubtful accounts which are based on historical collection trends for each payer type and age of the receivables. Accounts that are considered to be uncollectible are reserved for in the allowance until they are written off or collected.

When an available‐for‐sale financial asset is considered to be impaired, cumulative gains or losses previously recognized in other comprehensive income are reclassified to profit or loss in the period.

For financial assets other than available‐for‐sale equity securities, if, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, the previously recognized impairment loss is reversed through profit or loss to the extent that the carrying amount of the investment at the date the impairment is reversed does not exceed what the amortized cost would have been had the impairment not been recognized.

g) Derecognition of financial assets The Credit Union derecognizes a financial asset only when the contractual rights to the cash flows from the asset expire, or when it transfers the financial asset and substantially all the risks and rewards of ownership of the asset to another entity. If the Credit Union neither transfers nor retains substantially all the risks and rewards of ownership and continues to control the transferred asset, the Credit Union continues to recognize the transferred asset to the extent of the Credit Union’s continuing involvement in that asset. If the Credit Union retains substantially all the risks and rewards of ownership of a transferred asset, the Credit Union continues to recognize the financial asset and also recognizes a collateralized borrowing for the proceeds received.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

14

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Financial instruments (continued)

g) Derecognition of financial assets (continued) On derecognition of a financial asset in its entirety, the difference between the asset’s carrying value and the sum of the consideration received/ receivable and any cumulative gain or loss that had been recognized in other comprehensive income and accumulated comprehensive income is recognized in profit or loss.

h) Other financial liabilities

Other financial liabilities (including member deposits and borrowings) are subsequently measured at amortized cost using the effective interest method.

i) Derecognition of financial liabilities

The Credit Union derecognizes financial liabilities when, and only when, the Credit Union’s obligations are discharged, cancelled or they expire.

j) Transaction costs

Transaction costs related to financial assets and liabilities at fair value through profit and loss are expensed as incurred. Transaction costs include fees and commissions paid to agents, advisors, broker and dealers related to available‐for‐sale financial assets, held‐to‐maturity financial assets, other liabilities and loans and receivables are included in the carrying value of the asset or liability and are amortized over the expected life of the instrument using the effective interest method. Transaction costs do not include debt premiums or discounts, financing costs or internal administrative costs.

k) Derivative instruments

The Credit Union enters into a variety of derivative financial instruments to manage its exposure to market risk, including interest rate, foreign currencies and equity indices. Further details of derivative financial instruments are disclosed in Note 6. Derivatives are initially recognized at fair value at the date the derivative contract is entered into and are subsequently re‐measured to their fair value at the end of each reporting period. The resulting gain or loss is recognized in profit or loss immediately unless the derivative is designated and effective as a cash flow hedging instrument, in which event the effective portion of the gain or loss is recognized in other comprehensive income while the ineffective portion is recognized in profit or loss.

A derivative with a positive fair value is recognized as a financial asset. A derivative with a negative fair value is recognized as a financial liability.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

15

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Financial instruments (continued)

l) Embedded derivatives

Derivatives embedded in non‐derivative host contracts are treated as separate derivatives when their risks and characteristics are not closely related to those of the host contracts and the host contracts are not measured at FVTPL. As at December 31, 2016 and December 31, 2015, the Credit Union has embedded derivatives as described in other non‐hedge derivatives on page 17.

Cash and cash equivalents

Cash and cash equivalents includes cash on hand, deposits with Central 1, other short‐term highly

liquid investments with original maturities of three months or less; and for the purpose of the

statement of cash flows, bank overdrafts that are repayable on demand.

Cash and cash equivalents are classified as held for trading and are carried at fair value.

Investments

a) Central 1 deposits

These deposit instruments are classified as held to maturity and are initially measured at fair value

plus transaction costs that are directly attributable to their acquisition. Subsequently they are

carried at amortized cost, which approximates fair value.

b) Equity investments

These investments, consisting primarily of shares held in Central 1, are classified as available‐for‐

sale and are initially recognized at fair value plus transaction costs that are directly attributable

to their acquisition. Subsequently they would be carried at fair value, except that they do not

have a quoted market price in an active market and fair value is not reliably determinable

therefore they are carried at cost.

Changes in fair value are recognized as a separate component of other comprehensive income.

Where there is a significant or prolonged decline in the fair value of an equity investment (which

constitutes objective evidence of impairment), the full amount of the impairment, including any

amount previously recognized in other comprehensive income, is recognized in profit or loss.

Purchases and sales of equity investments are recognized on settlement date with any change in

fair value between trade date and settlement date being recognized in accumulated other

comprehensive income.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

16

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Investments (continued)

b) Equity investments (continued)

On sale, the amount held in accumulated other comprehensive income associated with that

instrument is recognized in profit or loss.

Derivative financial instruments and hedging

a) Hedges

The Credit Union, in accordance with its risk management strategies, enters into various

derivative financial instruments to protect itself against the risk of fluctuations in interest rates.

The Credit Union manages interest rate risk through interest rate swaps.

Hedge accounting is applied to derivative financial instruments only where all of the following

criteria are met:

at the inception of the hedge there is formal designation and documentation of the hedging relationship and the Credit Union’s risk management objective and strategy for undertaking the hedge;

for cash flow hedges, the hedged item in a forecast transaction is highly probable and presents an exposure to variations in cash flows that could ultimately affect profit or loss;

the effectiveness of the hedge can be reliably measured; and

the hedge is expected to be highly effective at inception and remains highly effective on each date it is tested. The Credit Union has chosen to test the effectiveness of its hedge on a quarterly basis.

The interest rate swap contracts can be designated as fair value hedge instruments or cash flow

hedge instruments. The Credit Union has not entered into any fair value hedges at this time.

Cash flow hedges modify exposure to variability in cash flows for variable rate interest bearing

instruments or the forecasted issuance of fixed rate liabilities. The Credit Union’s cash flow

hedges are primarily hedges of floating rate commercial and personal loans.

If the Credit Union closes out its hedge position early, the cumulative gains and losses recognized

in other comprehensive income are reclassified to profit or loss over the remaining term of the

original hedging relationship.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

17

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Derivative financial instruments and hedging (continued)

b) Other non‐hedge derivatives

The Credit Union designates certain financial assets upon initial recognition as at fair value

through profit or loss (fair value option). Financial instruments included in this category are the

embedded derivatives and derivatives related to index linked term deposits.

These instruments are measured at fair value, both initially and subsequently. The related

transaction costs are expensed. Gains and losses arising from changes in fair value of these

instruments are recorded in profit or loss.

Joint operation

The Credit Union has a joint operation, Northline Management Ltd. The Credit Union has a 20%

interest in the operation which is a credit union service organization that manages and maintains the

banking software for its investees. The operation is based in Williams Lake, BC.

Member loans

All member loans are non‐derivative financial assets with fixed or determinable payments that are

not quoted in an active market and have been classified as loans and receivables.

Member loans are initially measured at fair value, net of loan origination fees and inclusive of

transaction costs incurred. Member loans are subsequently measured at amortized cost, using the

effective interest rate method, less any impairment losses.

Loans to members are reported at their recoverable amount representing the aggregate amount of

principal, less any allowance or provision for impaired loans plus accrued interest. Interest is

accounted for on the accrual basis for all loans.

If there is objective evidence that an impairment loss on member loans carried at amortized cost has

been incurred, the amount of the loss is measured as the difference between the loans carrying

amount and the present value of expected cash flows discounted at the loans original effective

interest rate. Short‐ term balances are not discounted.

The Credit Union first assesses whether objective evidence of impairment exists individually for

financial assets that are individually significant.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

18

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Member loans (continued) If it is determined that no objective evidence of impairment exists for an individually assessed financial

asset, whether significant or not, the asset is included in a group of financial assets with similar credit

risk characteristics and that group of financial assets is collectively assessed for impairment. Assets

that are individually assessed for impairment and for which an impairment loss is or continues to be

recognized are not included in a collective assessment of impairment.

The expected future cash outflows for a group of financial assets with similar credit risk characteristics

are estimated based on historical loss experience.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be

related objectively to an event occurring after the impairment was recognized, the previously

recognized impairment loss is reversed. Any subsequent reversal of an impairment loss is recognized

in profit or loss.

Syndication

The Credit Union syndicates groups of assets with various other financial institutions primarily to

create liquidity and manage regulatory capital for the Credit Union. Syndicated loans transfer

substantially all the risks and rewards related to the transferred financial assets and are derecognized

from the Credit Union’s Consolidated Statement of Financial Position. All loans syndicated by the

Credit Union have been on a fully serviced basis. The Credit Union receives fee income for services

provided in the servicing of the transferred financial assets. Fee income is recognized in other income

on an accrual basis in relation to the reporting period in which the costs of providing the services are

incurred.

Bad debts written off

Bad debts are written off from time to time as determined by management and approved by the

Investment and Lending Committee when is it reasonable to expect that the recovery of the debt is

unlikely. Bad debts are written off against the provisions for impairment, if a provision for impairment

had previously been recognized. If no provision had been recognized, the write offs are recognized

as expenses in profit or loss.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

19

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Property and equipment

Property and equipment is initially recorded at cost and subsequently measured at cost less

accumulated depreciation and any accumulated impairment losses, with the exception of land which

is not depreciated.

Depreciation is recognized in profit or loss and is provided on a straight‐line basis over the estimated

useful life of the assets as follows:

Buildings 15‐40 years Furniture and equipment 5‐20 years Computer software 2‐7 years

Leasehold improvements Lease term plus one renewal period Vehicles 5 years

Parking lots 12 years

Depreciation methods, useful lives and residual values are reviewed annually and adjusted if

necessary.

Computer software which is not integral to the computer hardware owned by the Credit Union is

separately classified in property and equipment. Software is initially recorded at cost and

subsequently measured at cost less accumulated amortization and any accumulated impairment

losses. Software is amortized on a straight‐line basis over its estimated useful life of 2 years. Major

banking system software is amortized over a useful life of 7 years.

Intangible assets

Indefinite life intangible assets are carried at cost less accumulated impairment losses. Cost of

intangible assets includes expenditures directly attributable to the acquisition of the asset and

required to establish the asset in working condition given its intended use as well as borrowing costs.

Subsequent expenditures are capitalized only when they increase the future economic benefits

embodied in the asset.

Goodwill Goodwill arising on acquisition of a subsidiary or jointly controlled entity represents the excess of the

cost of acquisition over the Credit Union’s interest in the fair value of net identifiable assets, liabilities

and contingent liabilities of the subsidiary or jointly controlled entity recognized at the date of

acquisition. Goodwill is initially recognized as an asset at cost, and is subsequently measured at cost

less any accumulated impairment losses.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

20

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Goodwill (continued)

For the purpose of impairment testing, goodwill is allocated to each of the Credit Union’s cash‐

generating units expected to benefit from the synergies of the acquisition. Cash‐generating units to

which goodwill has been allocated are tested for impairment annually, or more frequently when there

is an indication that the unit may be impaired. If the recoverable amount of the cash‐generating unit

is less than the carrying amount of the unit, the impairment loss is allocated first to reduce the carrying

amount of any goodwill allocated to the unit and then to the other assets of the unit pro‐rata on the

basis of the carrying amount of each asset in the unit. An impairment loss recognized for goodwill is

not reversed in a subsequent period.

On disposal of a subsidiary, the attributable amount of goodwill is included in the determination of

the profit or loss on disposal.

Impairment of non‐financial assets (other than goodwill)

Non‐financial assets are subject to impairment tests whenever events or changes in circumstances

indicate that their carrying amount may not be recoverable. Intangible assets with indefinite useful

lives are tested for impairment at least annually, and whenever there is an indication that the asset

may be impaired. Where the carrying value of an asset exceeds its recoverable amount, which is the

higher of value in use and fair value less costs to sell, the asset is written down accordingly.

Where it is not possible to estimate the recoverable amount of an individual asset, the impairment

test is carried out on the asset’s cash‐generating unit, which is the lowest group of assets in which the

asset belongs for which there are separately identifiable cash flows.

Income taxes

Income tax expense comprises current and deferred tax. Current tax and deferred tax are recognized

in profit or loss except to the extent that it relates to a business combination, or items recognized

directly in equity or in other comprehensive income. Current income taxes are recognized for the

estimated income taxes payable or receivable on taxable income or loss for the current year and any

adjustment to income taxes payable in respect of previous years. Current income taxes are measured

at the amount expected to be recovered from or paid to the taxation authorities. This amount is

determined using tax laws that have been enacted or substantively enacted by the reporting date.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

21

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Income taxes (continued)

Deferred tax assets and liabilities are recognized where the carrying amount of an asset or liability

differs from its tax base, except for taxable temporary differences arising on the initial recognition of

goodwill and temporary differences arising on the initial recognition of an asset or liability in a

transaction which is not a business combination and at the time of the transaction affects neither

accounting or taxable profit or loss.

Recognition of deferred tax assets for unused tax losses, tax credits and deductible temporary

differences is restricted to those instances where it is probable that future taxable profit will be

available which allow the deferred tax asset to be utilized. Deferred tax assets are reviewed at each

reporting date and are reduced to the extent that it is no longer probable that the related tax benefit

will be realized.

The amount of the deferred tax asset or liability is measured at the amount expected to be recovered

from or paid to the taxation authorities. This amount is determined using tax rates and tax laws that

have been enacted or substantively enacted by the reporting date and are expected to apply when

the liabilities/ assets are settled/ recovered.

Member deposits

All member deposits are initially measured at fair value, net of any transaction costs directly

attributable to the issuance of the instrument. Member deposits are subsequently measured at

amortized cost, using the effective interest rate method.

Employee benefits

a) Pension Plan

The Credit Union participates in a defined contribution pension plan. The amounts payable to the

plan is in proportion to the services rendered to the Credit Union by the employees and are

expensed in the year which they relate. Unpaid contributions are recorded as a liability.

b) Termination benefits

Termination benefits are recognized as an expense when the Credit Union is committed without

realistic probability of withdrawal to a formal detailed plan either to terminate employment

before the normal retirement date or to provide termination benefits. If benefits are payable

more than 12 months after the reporting period, they are recorded at their discounted present

value.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

22

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Accounts payable and other payables

Liabilities for trade creditors and other payables are classified as other financial liabilities and initially

measured at fair value net of any transaction costs directly attributable to the issuance of the

instrument and subsequently carried at amortized cost using the effective interest rate method.

Provisions

Provisions are recognized when the Credit Union has a present legal or constructive obligation as a

result of a past event, it is probable that the Credit Union will be required to settle the obligation, and

a reliable estimate can be made of the amount of the obligation.

The amount recognized as a provision is the best estimate of the consideration required to settle the

present obligation at the end of the reporting period, taking into account the risks and uncertainties

surrounding the obligation. When a provision is measured using the cash flows estimated to settle the

present obligation, its carrying amount is the present value of those cash flows (when the effect of

the time value of money is material).

Members’ shares

Members’ shares issued by the Credit Union are classified as equity only to the extent that they do

not meet the definition of a financial liability.

Shares that contain redemption features subject to the Credit Union maintaining adequate regulatory

capital are accounted for using the partial treatment requirements of IFRIC 2 Members’ Shares in Co‐

operative Entities and Similar Instruments.

Distribution to members

Dividends on shares classified as liabilities are charged against earnings. Dividends on equity shares

classified as equity, less related income tax reductions, are charged against retained earnings in the

year in which they are declared. Dividends are recorded when declared by the Board of Directors.

Revenue recognition

Revenue from the provision of services to members is recognized when earned, specifically when

amounts are fixed or can be determined and the ability to collect is reasonably assured. Dividend

income is recognized in profit or loss when the Credit Union’s right to receive the dividends is

established. Interest income is recognized in income using the effective interest method. Foreign

exchange gains or losses on debt securities are recognized immediately in profit or loss and is included

in other operating income.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

23

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

Foreign currency translation

Foreign currency accounts are translated into Canadian dollars as follows:

At the transaction date, each asset, liability, revenue and expense denominated in a foreign currency

is translated into Canadian dollars by the use of the exchange rate in effect at that date. At the year‐

end date, unsettled monetary assets and liabilities are translated into Canadian dollars by using the

exchange rate in effect at the year‐end date and the related translation differences are recognized in

profit or loss.

Exchange gains and losses arising on the retranslation of monetary available‐for‐sale financial assets

are treated as a separate component of the change in fair value and are recognized in profit or loss.

Wealth management services

The Credit Union offers members access to a wide variety of investments though Integris Financial

Planning Ltd. Assets under administration are recorded separately from the Credit Union’s assets and

are not included in the Consolidated Statement of Financial Position. At December 31, 2016 assets

under management totalled $166,028,377 (December 31, 2015 ‐ $180,846,817).

New standards and interpretations not yet adopted

At December 31, 2016 a number of standards and interpretations, and amendments thereto have

been issued by the IASB, which are not effective for these consolidated financial statements, and have

not been applied in preparing these financial statements. Those which could have an impact on

Integris Credit Union’s consolidated financial statements are discussed below.

a) Acquisitions of interests in joint operations

The amendments to IFRS 11, Joint Arrangements (“IFRS 11”) provide guidance on how to account

for the acquisition of a joint operation that constitutes a business as defined in IFRS 3, Business

Combinations. The amendments to IFRS 11 are not effective until annual periods beginning on or

after January 1, 2017. Integris Credit Union does not anticipate that the amendments to IFRS 11

would have significant impact to its consolidated financial statements.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

24

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

New standards and interpretations not yet adopted (continued)

b) Financial instruments

On July 24, 2014 the IASB issued the final version of IFRS 9, Financial Instruments (“IFRS 9”). IFRS

9 is effective for annual periods beginning on or after January 1, 2018.

Key requirements of IFRS 9:

All recognized financial assets that are within the scope of IAS 39 are to be subsequently measured

at amortized cost or fair value. Specifically, debt investments that are held within a business

model whose objective is to collect the contractual cash flows, and that have contractual cash

flows that are solely payments of principal and interest on the principal outstanding are generally

measured at amortized cost at the end of subsequent accounting periods. Debt instruments that

are held within a business model whose objective is achieved both by collecting contractual cash

flows and selling financial assets, and that have contractual terms that give rise on specified dates

to cash flows that are solely of principal and interest on the principal amount outstanding, are

generally measured at fair value through OCI (FVTOCI). All other debt investments and equity

investments are measured at their fair value at the end of subsequent accounting periods.

In addition, under IFRS 9, entities may make an irrevocable election to present subsequent

changes in the fair value of an equity instrument (that is not held‐for‐trading) in OCI, with only

dividend income generally recognized in profit or loss.

With regard to the measurement of financial liabilities designated as at FVTPL, IFRS 9 requires

that the amount of change in the fair value of the financial liability, that is attributable to changes

in the credit risk of that liability, is presented in OCI, unless the recognition of the effects of

changes in the liability’s credit risk in OCI would create or enlarge an accounting mis‐match in

profit or loss. Changes in the fair value attributable to a financial liability’s credit risk are not

subsequently reclassified to profit or loss. Under IAS 39, the entire amount of the change in the

fair value of the financial liability designated as FVTPL is presented in profit or loss.

In relation to the impairment of financial assets, IFRS 9 requires an expected credit loss model, as

opposed to an incurred credit loss model under IAS 39. The expected credit loss model requires

an entity to account for expected credit losses and changes in those expected credit losses at each

reporting date to reflect changes in credit risk since initial recognition. In other words, it is no

longer necessary for a credit event to have occurred before credit losses are recognized.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

25

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

New standards and interpretations not yet adopted (continued)

b) Financial instruments (continued)

The Credit Union anticipates that the application of IFRS 9 in the future may have a significant

impact on amounts reported in respect to the Credit Union’s financial assets and financial

liabilities. However, it is not practicable to provide a reasonable estimate of the effect of IFRS 9

until a detailed review has been completed.

c) Revenue from contracts with customers

IFRS 15, Revenue from Contracts with Customers (IFRS 15), specifies how an entity will recognize

revenue from contracts with customers as well as additional disclosure requirements. It provides

a five‐step process for revenue recognition and is effective for periods beginning on or after

January 1, 2018. Early adoption of this standard is permitted but would be subject to regulatory

approval by FICOM. The standard does not apply to financial instruments as these currently fall

under IAS 39 and in the future under IFRS 9 above. Since the majority of the Credit Union’s

revenue is earned from financial instrument contracts, this standard is not expected to have a

material impact on the consolidated financial statements.

d) Leases

IFRS 16, Leases, specifies how the entity will recognize, measure, present and disclose leases. The

standard provides a single lessee accounting model, requiring lessees to recognize assets and

liabilities for all leases unless the term is twelve months or less or the underlying asset has a low

value. Lessors continue to classify leases as operating or finance, with IFRS 16’s approach to lessor

accounting substantially unchanged from its predecessor IAS 17. IFRS 16 is effective for periods

beginning on or after January 1, 2019. The Credit Union is currently evaluating the impact of the

new standard on its consolidated financial statements.Leases prescribes the accounting policies and disclosures applicable to leases, both for lessees and lessors. Leases are required to be classified as either finance leases (which transfer substantially all the risks and rewards of ownership, and give rise to asset and liability recognition by the lessee and a receivable by the lessor) and operating leases (which result in expense recognition by the lessee, with the asset remaining

AS 17 was reissued in December 2003 and applies to annual periods beginning on or after 1 January 2005. IAS 17 will be superseded by IFRS 16 Leases as of 1 January 2019

Integris Credit Union did not early adopt any new or amended standards in 2016.

3. CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS

The Credit Union makes estimates and assumptions about the future that affect the reported amounts

of assets, liabilities, revenues and expenses. Estimates and judgments are continually evaluated

based on historical experience and other factors, including expectations of future events that are

believed to be reasonable under the circumstances. In the future, actual experiences may differ from

these estimates and assumptions. The effect of a change in an accounting estimate is recognized

prospectively by including it in the financial statements in the period of the change, if the change

affects that period only; or in the period of the change and future periods, if the changes affects both.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

26

3. CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS (continued)

The estimates and assumptions that have a significant risk of causing material adjustment to the

carrying amounts of assets and liabilities within the next financial year are discussed below.

Fair value of financial instruments

The Credit Union determines the fair value of financial instruments that are not quoted in an active

market, using valuation techniques. Those techniques are significantly affected by the assumptions

used including discount rates and estimates of future cash flows. In that regard, the derived fair value

estimates cannot always be substantiated by comparison with independent markets and, in many

cases, may not be capable of being realized immediately. The methods and assumptions applies, and

the valuation techniques used, for financial instruments that are not quoted in an active market are

disclosed in Note 5 and Note 23.

Member loan loss provision

In determining whether an impairment loss should be recorded, the Credit Union makes judgements

on whether objective evidence of impairment exists individually for financial assets that are

individually significant.

Where this does not exist the Credit Union uses its judgement to group member loans with similar

credit risk characteristics to allow a collective assessment of the group to determine any impairment

loss. In determining the collective loan loss provision Management uses estimates based on historical

loss experience for assets with similar credit risk characteristics and objective evidence of impairment.

Further details on the estimates used to determine the allowance for impaired loans collective

provision are provided in Note 8.

Income tax

The Credit Union periodically assesses its liabilities and contingencies related to income taxes for all

years open to audit based on the latest information available. For matters where it is probable that

an adjustment will be made, the Credit Union records its best estimate of the tax liability including

the related interest and penalties in the current tax provision.

4. CASH AND CASH EQUIVALENTS

The Credit Union’s cash is held in current accounts with Central 1 except for cash on hand totaling

$3,955,624 as of December 31, 2016 ($3,612,810 – December 31, 2015). The average yield on cash

held with Central 1 at December 31, 2016 is 0.9% (2015 ‐ 0.9%).

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

27

5. INVESTMENTS

Central 1 deposits

Under requirements of the Act, the Credit Union must maintain liquidity reserves with Central 1 at 8% of total deposits at December 31 each year. The deposits can be withdrawn only if there is a sufficient reduction in the Credit Union’s total deposits or upon withdrawal of membership from Central 1. The liquidity reserves are due within one year. At maturity, these deposits are reinvested at market rates for various terms. The yield on the accounts at December 31, 2016 is between 0.59% and 2.23%. Equity investments

The shares in Central 1 are required as a condition of membership and are redeemable upon

withdrawal of membership or at the discretion of the Board of Directors of Central 1. In addition, the

member credit unions are subject to additional capital calls at the discretion of the Board of Directors

of Central 1.

Class A Central 1 shares are subject to an annual rebalancing mechanism and are issued and

redeemable at par value. There is no separately quoted market value for these shares; however, fair

value is determined to be equivalent to the par value due to the fact that transactions occur at par

value on a regular and recurring basis.

Class E Central 1 shares are issued with a par value of $0.01 each, however are redeemable at $1 each,

or a total of $20,727, at the option of Central 1. There is no separately quoted market value for these

shares and the fair value could not be measured reliably. Fair value cannot be measured reliably as

the timing of redemption of these shares cannot be determined, therefore, the range of reasonable

fair value estimates is significant and the probabilities of the various estimates cannot be reasonably

assessed. Therefore, they are recorded at cost.

The following tables provide information on the investments by type of security and issuer. The

maximum exposure to credit risk is limited to the amount recorded in the consolidated statement of

financial position.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

28

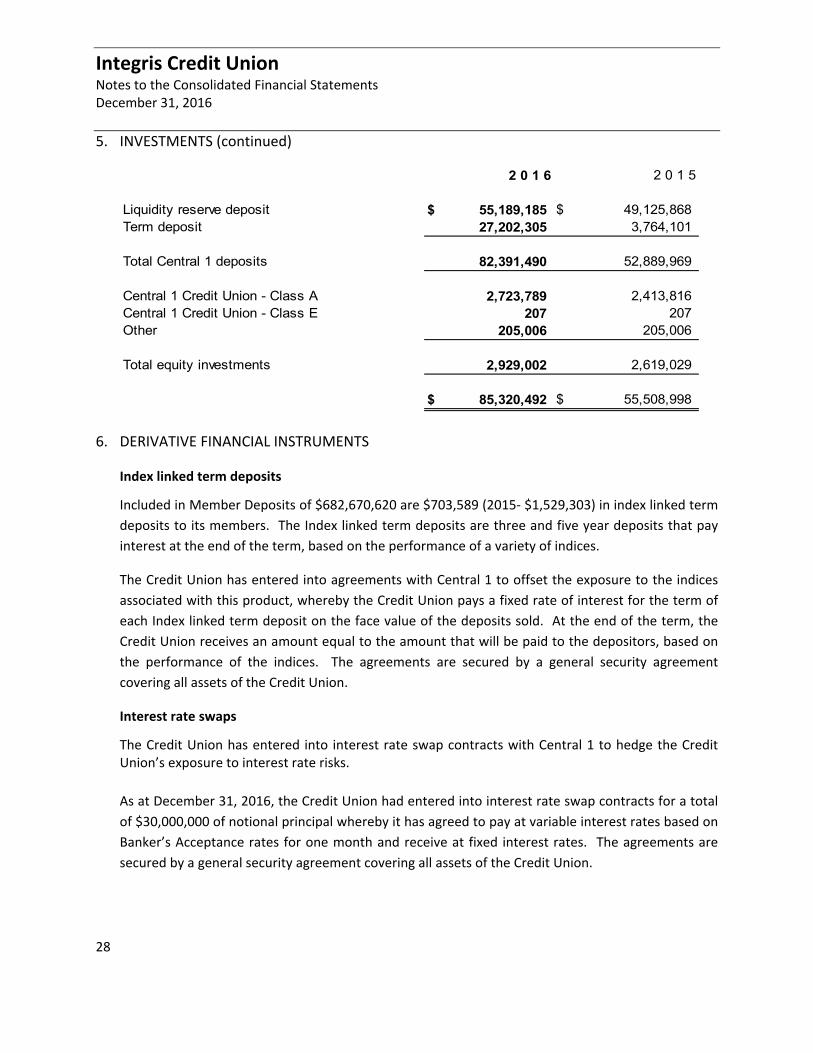

5. INVESTMENTS (continued)

2 0 1 6 2 0 1 5

Liquidity reserve deposit $ 55,189,185 $ 49,125,868Term deposit 27,202,305 3,764,101

Total Central 1 deposits 82,391,490 52,889,969

Central 1 Credit Union - Class A 2,723,789 2,413,816Central 1 Credit Union - Class E 207 207Other 205,006 205,006

Total equity investments 2,929,002 2,619,029

$ 85,320,492 $ 55,508,998

6. DERIVATIVE FINANCIAL INSTRUMENTS

Index linked term deposits

Included in Member Deposits of $682,670,620 are $703,589 (2015‐ $1,529,303) in index linked term

deposits to its members. The Index linked term deposits are three and five year deposits that pay

interest at the end of the term, based on the performance of a variety of indices.

The Credit Union has entered into agreements with Central 1 to offset the exposure to the indices

associated with this product, whereby the Credit Union pays a fixed rate of interest for the term of

each Index linked term deposit on the face value of the deposits sold. At the end of the term, the

Credit Union receives an amount equal to the amount that will be paid to the depositors, based on

the performance of the indices. The agreements are secured by a general security agreement

covering all assets of the Credit Union.

Interest rate swaps

The Credit Union has entered into interest rate swap contracts with Central 1 to hedge the Credit Union’s exposure to interest rate risks.

As at December 31, 2016, the Credit Union had entered into interest rate swap contracts for a total

of $30,000,000 of notional principal whereby it has agreed to pay at variable interest rates based on

Banker’s Acceptance rates for one month and receive at fixed interest rates. The agreements are

secured by a general security agreement covering all assets of the Credit Union.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

29

6. DERIVATIVE FINANCIAL INSTRUMENTS (continued)

2016Notional Maturity Paying Fair

Counterparty Amount Date Variable Receiving Value

Central 1 10,000,000 12‐May‐18 0.90% 2.015% 134,421 Central 1 10,000,000 12‐Jul‐18 0.80% 2.040% 150,962 Central 1 10,000,000 5‐Sep‐18 0.90% 2.500% 238,811

$ 30,000,000 $ 524,194

2015

Notional Maturity Paying FairCounterparty Amount Date Variable Receiving Value

Central 1 10,000,000 12‐May‐18 0.82% 2.015% 267,726 Central 1 10,000,000 12‐Jul‐18 0.80% 2.040% 287,612 Central 1 10,000,000 5‐Sep‐18 0.84% 2.500% 421,687

$ 30,000,000 $ 977,025

The Credit Union’s exposure under derivative contracts is closely monitored as part of the overall

management of the Credit Union’s market risk.

7. MEMBER LOANS

2 0 1 6 2 0 1 5

Residential mortgages $ 386,203,803 $ 354,316,652

Personal loans 49,862,863 50,919,702

Commercial loans 154,206,333 177,239,939

590,272,999 582,476,293

Accrued interest receivable 1,453,780 1,398,048

591,726,779 583,874,341

Allowance for impaired loans (Note 8) (2,731,679) (2,561,717)

Total member loans $ 588,995,100 $ 581,312,624

Terms and conditions

Member loans can have either a variable or fixed rate of interest and have maturities ranging from

one to ten years.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

30

7. MEMBER LOANS (continued)

Terms and conditions (continued)

Variable rate loans are based on a prime rate formula, ranging from prime minus 1.30% to prime plus

15%. The rate is determined by the type of security offered and the member’s credit worthiness. The

Credit Union’s prime rate at December 31, 2016 was unchanged from 2015 at 3.30%.

The interest rate offered on fixed rate loans being advanced at December 31, 2016 ranges from 2% to

21%. The rate offered to a member varies with the type of security offered and the member’s credit

worthiness.

Residential mortgages are loans and lines of credit secured by residential property and are generally

repayable monthly with either blended payments of principal and interest or interest only.

Personal loans consist of term loans and lines of credit that are non‐real estate secured and, as such,

have various repayment terms. Some of the personal loans are secured by chattels and personal

property or investments, and others are unsecured.

Commercial loans consist of term loans, operating lines of credit and mortgages to individuals,

partnerships and corporations, and have various repayment terms. They are secured by various types

of collateral, including mortgages on real property, general security agreements, charges on specific

equipment, investments, and personal guarantees.

Credit quality of loans

A breakdown of the portfolio based on type of security held is as follows:

2 0 1 6 2 0 1 5

Unsecured loans $ 28,324,414 $ 26,872,310 Loans secured by chattels 42,146,299 50,629,071 Loans guaranteed by government 1,033,254 2,323,929 Residential mortgages insured by government 162,081,107 147,423,592 Residential mortgages uninsured 224,122,694 206,893,059 Commercial mortgages uninsured 130,471,300 145,082,749 Fully secured 2,093,931 3,251,583

$ 590,272,999 $ 582,476,293

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

31

7. MEMBER LOANS (continued)

Terms and conditions (continued)

Concentration of credit risk

Concentration of credit risk exists if a number of borrowers are engaged in similar economic activities

or are located in the same geographic region, and indicate the relative sensitivity of the Credit Union’s

performance to developments affecting a particular segment of borrowers or geographic region.

Geographic credit risk exists for the credit union due to its primary service area being Prince George

and its surrounding areas. To reduce the impact of the credit risk, the credit union has 42.0% (2015 –

41.6%) of its residential mortgages insured against credit loss.

8. ALLOWANCE FOR IMPAIRED LOANS

Total allowance for impaired loan provision comprises:

2 0 1 6 2 0 1 5

Collective allowance $ 1,212,204 $ 1,188,862 Specific allowance 1,519,475 1,372,855

$ 2,731,679 $ 2,561,717

Movement in individual specific provision and collective allowance for impairment:

Write‐offs Ending

Beginning net of Balance

Balance Provision recoveries 2 0 1 6

Personal LoansMortgages $ 439,140 $ (53,939) 4,380 $ 380,821 Other 469,671 375,657 433,513 411,815

Commercial loansMortgages 658,475 1,499,286 755,718 1,402,043Other 994,431 246,563 703,994 537,000

$ 2,561,717 $ 2,067,567 $ 1,897,605 $ 2,731,679

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

32

8. ALLOWANCE FOR IMPAIRED LOANS (continued)

Write‐offs Ending Beginning net of Balance

Balance Provision recoveries 2 0 1 5

Personal LoansMortgages $ 366,731 $ 119,222 46,813 $ 439,140 Other 443,964 154,004 128,297 469,671

Commercial loansMortgages 130,184 588,001 59,710 658,475 Other 383,981 2,585,789 1,975,339 994,431

$ 1,324,860 $ 3,447,016 $ 2,210,159 $ 2,561,717

Analysis of individual loans that are impaired based on repayments outstanding:

Loan SpecificBalance Allowance 2 0 1 6

Personal LoansMortgages $ ‐ $ ‐ $ ‐ Other 165,957 36,475 129,482

Commercial loansMortgages 4,497,515 1,304,000 3,193,515 Other 436,373 179,000 257,373

$ 5,099,845 $ 1,519,475 $ 3,580,370

Carrying amount

Loan SpecificBalance Allowance 2 0 1 5

Personal LoansMortgages $ 75,273 $ 45,450 $ 29,823 Other 269,778 192,405 77,373

Commercial loansMortgages 4,016,101 1,079,000 2,937,101 Other 100,794 56,000 44,794

$ 4,461,946 $ 1,372,855 $ 3,089,091

Carrying amount

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

33

8. ALLOWANCE FOR IMPAIRED LOANS (continued)

Key assumptions in determining the allowance for impaired loans collective provision

The Credit Union has determined the likely impairment loss on loans which have not maintained the

loan repayments in accordance with the loan contract, or where there is other evidence of potential

impairment such as industrial restructuring, job losses or economic circumstances.

In identifying the impairment likely from these events the Credit Union estimates the potential

impairment using the loan type, industry, geographic location, type of loan security, the length of time

the loans are past due and the historical loss experience. The circumstances may vary for each loan

over time, resulting in higher or lower impairment losses. The methodology and assumptions used

for estimating future cash flows are reviewed regularly by the Credit Union to reduce any differences

between loss estimates and actual loss experience. For purposes of the collective provision loans are

classified into separate groups with similar risk characteristics, based on the type of product and type

of security.

Loans with repayments past due but not regarded as individually impaired and considered in

determining the collective provision:

Residential 2 0 1 6Mortgage Personal Commercial Total

30 to 90 days $ 202,253 $ 150,307 $ 30,283 $ 382,843 Over 90 days 154,653 257,760 4,527,689 4,940,102

Balance at December 31, 2016 $ 356,906 $ 408,067 $ 4,557,972 $ 5,322,945

Residential 2 0 1 5 Mortgage Personal Commercial Total

30 to 90 days $ 853,741 $ 122,590 $ 364,971 $ 1,341,302 Over 90 days 1,846,338 15,523 3,233,167 5,095,028

Balance at December 31, 2015 $ 2,700,079 $ 138,113 $ 3,598,138 $ 6,436,330

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

34

9. INTANGIBLE ASSETS

2 0 1 6 2 0 1 5

Indefinite useful life intangible assets:Licenses $ 3,377,677 $ 3,377,677 Goodwill 365,000 365,000

3,742,677 3,742,677

Limited life intangible assets:Book of business 484,686 ‐ Accumulated amortization (19,003) ‐

465,683 ‐

Banking platform 4,728,301 2,317,443 Accumulated amortization (996,732) (807,723)

3,731,569 1,509,720

$ 7,939,929 $ 5,252,397

10. OTHER ASSETS 2 0 1 6 2 0 1 5

Receivables, prepaids and other $ 3,143,116 $ 2,554,035

Derivative financial instrument (Note 6) 524,194 977,025

Income taxes receivable 129,797 276,813

Deferred income taxes (Note 15) 107,504 120,248

$ 3,904,611 $ 3,928,121

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

35

11. MEMBER DEPOSITS

2 0 1 6 2 0 1 5

Chequing $ 144,778,653 $ 152,378,953

Demand 131,822,637 120,948,032

Term 257,284,597 240,486,828

Registered savings plans 74,479,189 73,247,319

Registered retirement income funds 23,619,987 21,947,230

Tax free savings accounts 41,168,476 35,731,198

Members' shares (Note 16) 5,815,207 5,488,735

678,968,746 650,228,295

Accrued interest payable 3,701,874 3,659,285

$ 682,670,620 $ 653,887,580

Terms and conditions

Chequing deposits are due on demand and bear interest at a variable rates ranging from 0% up to

prime (3.30% at December 31, 2016).

Demand deposits are due on demand and bear interest at a variable rates ranging from 0% up to

prime (3.30% at December 31, 2016).

Term deposits bear fixed rates of interest for terms of up to five years. Interest can be paid annually,

semi‐annually, monthly or upon maturity. The interest rates on term deposits issued at December

31, 2016 range from 0.10% to 6.75%.

The registered retirement savings plans (“RRSP”) accounts can be fixed or variable rate. The fixed rate

RRSPs have terms and rates similar to the term deposit accounts described above. The variable rate

RRSPs bear interest at demand account rates up to 1.8% at December 31, 2016.

Registered retirement income funds (“RRIFs”) consist of both fixed and variable rate products with

terms and conditions similar to those of the RRSPs described above. Members may make withdrawals

from a RRIF account on a monthly, semiannual or annual basis. The regular withdrawal amounts vary

according to individual needs and statutory requirements.

The tax‐free savings accounts can be fixed or variable rate with terms and conditions similar to those

of the RRSPs described above.

Included in chequing deposits is an amount of $5,393,261 (2015 ‐ $6,670,787) denominated in US

dollars.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

36

11. MEMBER DEPOSITS (continued)

Terms and conditions (continued)

Concentration of risk

The Credit Union potentially has an exposure to groupings of individual deposits which concentrate

risk and create exposure to particular segments. The Credit Union mitigates this concentration risk

by limiting deposits by any one member or related group of members to no more than 2.5% of total

deposits. The Board of Directors may approve on exception a deposit outside of this policy. At

December 31, 2016 there were no members that were in exception to the 2.5% limit.

12. OTHER LIABILITIES 2 0 1 6 2 0 1 5

Accounts payable and accrued liabilities $ 2,410,905 $ 1,804,567 Post retirement benefits obligation (Note 14) 293,278 543,850

$ 2,704,183 $ 2,348,417

13. LOAN SECURITIZATION FINANCING

Loan securitization financing represents the carrying value of mortgage pools which have been

transferred to other financial institutions for which the Credit Union retains substantially all of the risk

and rewards relating to the transferred financial assets. The Credit Union may be required to

repurchase any maturing mortgages in any of the mortgage pools where the terms and conditions of

the loan cannot be agreed upon with that financial institution. These contracts have terms of

repayment between 1 to 6 years and bear interest at various rates ranging from 2.78% to 4.70%.

These assets were transferred to other institutions between 2004 and 2007. The value of the assets

transferred matched the corresponding liability incurred in the amount of $22,389,536. In the current

year, the Credit Union has recognized $3,484 of management fees.

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

37

14. PENSION PLAN

The Credit Union makes contributions to a pension plan, which is a multi‐employer defined

contribution plan, on behalf of members of its staff. The amount contributed to the plan for 2016

was $505,032 (2015‐$561,002). The contributions were made for current service and these have been

recognized in profit or loss. In accordance with the terms of specific employment contracts, certain

employees (and retired employees) are entitled to benefits after retirement. These benefits are

accrued as they are earned, and reversed as they are paid to the individual.

15. INCOME TAXES

The significant components of tax expense included in profit or loss are composed of:

2016 2015

Current tax

Current tax expense in respect of

current year $ 75,366 $ 74,418

Non‐deductible expenses (recoveries) 5,909 (25,141)

Other (16,901) 23,601

Reassesssment of 2005 taxes ‐ (77,987)

64,374 (5,109)

Deferred tax

Deferred tax expense (recovery) in the

current year 12,744 (74,087)

$ 77,118 $ (79,196)

Reasons for the difference between tax expense for the year and the expected income taxes based

on the statutory tax rate of 16.7% (2015‐ 15.9%) are as follows:

Integris Credit Union Notes to the Consolidated Financial Statements December 31, 2016

38

15. INCOME TAXES (continued)

2016 2015

Net income before tax $ 451,294 $ 468,040

Income tax expense based on statutory rate 75,366 74,418