Insurance Tax Update Presented by: Brandon Lagarde, CPA, JD, LLM.

33

Insurance Tax Update Presented by: Brandon Lagarde, CPA, JD, LLM

-

Upload

lacey-standring -

Category

Documents

-

view

219 -

download

5

Transcript of Insurance Tax Update Presented by: Brandon Lagarde, CPA, JD, LLM.

Insurance Tax UpdatePresented by:

Brandon Lagarde, CPA, JD, LLM

IntroductionJudicial and administrative updates

2013 Tax Changes

Capitalization Regulations

Affordable Care Act Reporting

Foreign Asset Reporting

F.W. Services v. Commissioner5th Circuit – ruled that premium payments that were held by

an insurer as a deposit against future deductibles that were to be refunded to a business at the end of the term of the policy are not deductible as an insurance premium.

The holding is related to risk shifting. Since any excess premium would have been refunded and if there had been a need for more, then an additional payment would have been made.

State Farm v. CommissionerCourt found that the standards used in the NAIC Annual

Statement governed the tax treatment.

Under NAIC guidance, compensatory damages for bad faith awards are taken into consideration for calculating unpaid loss reserves, not punitive damages.

PLR 201224018The IRS ruled that a foreign captive insurance company qualified

as a domestic insurance company for income tax purposes, and that reinsurance premiums paid to the reinsurance pool are deductible.o The insurance is offered to 6 related insured corporations and other

entities;o To try to achieve risk distribution, the Company takes part in a

reinsurance pool with 14 other non-related insurers;o The Company cedes its risk to the pool and then through another

reinsurance agreement assumes a quota share back from the pool;o The IRS ruled that none of the companies is paying a significant

portion of their own risk and therefore there is risk shifting and distribution.

TAM 201149021The IRS ruled that a policy of insurance that insures against a

market decline is not insurance.o The risks under the contract were related to investment risk as

opposed to insurance risk.o Second, the IRS concluded that the risk was one of a universal

nature (a market decline) as opposed to one in a group of large numbers that might fortuitously happen to one insured rather than to all. Therefore, they concluded there was no way to have risk distribution.

Acuity Mutual Insurance Co. v. Commissioner, T.C. Memo 2013-209Actuity used in-house actuary to compute total loss reserves for 2006

o 900 pages of analysiso 8 separate methodso $660 million

Acuity also used an outside consulting actuary to independently review loss reserves each yearo Narrow range of reasonable reserveso $577 million to $661 million

Loss reserves within range, so independent actuary signed a statement of actuarial opinion stating so.

Filed Annual Statement showing loss reserves of $660M.

Acuity Mutual Insurance Co. v. Commissioner, T.C. Memo 2013-209

IRS issued deficiency notice stating that Acuity’s loss reserves were overstated by $96M.o Argued that the annual statement controls only what is

includable in the loss reserves, not the amount of the reserve itself

o Tax Court relied on the Seventh Circuit case law to the effect that the NAIC-approved annual statement is the starting point for computing unpaid losses

o Court disagreed with IRS argument, holding that the annual statement should be the source of unpaid losses for federal tax purposes

o IRS did not produce persuasive evidence to the contrary

Acuity Mutual Insurance Co. v. Commissioner, T.C. Memo 2013-209

IRS issued deficiency notice stating that Acuity’s loss reserves were overstated by $96M.o Argued that the annual statement controls only what is

includable in the loss reserves, not the amount of the reserve itself

o Tax Court relied on the Seventh Circuit case law to the effect that the NAIC-approved annual statement is the starting point for computing unpaid losses

o Court disagreed with IRS argument, holding that the annual statement should be the source of unpaid losses for federal tax purposes

o IRS did not produce persuasive evidence to the contrary

Rent-A-Center v. Commissioner, 142 T.C. No. 1 (Jan. 14, 2014)Captive case

Held that payments to a Bermuda captive on behalf of approximately 15 subsidiaries were deductible insurance expenses.

IRS took issue with the arrangement based on 4 facts:o The parent corporation was the listed policyholder and paid dividends

on behalf of its subsidiarieso The parent guaranteed the liquidity of the captive insurer’s deferred

tax assetso The captive invested in non-dividend paying treasury stock of its

parento Risks were concentrated in small number of sibling corporations.

Rent-A-Center v. Commissioner, 142 T.C. No. 1 (Jan. 14, 2014)

Court disagreed with IRS o Captive was established for a non-tax reason.

Supported by absence of circular flow of fundsPremium to surplus ratios that were commercially reasonableOperation as a bona fide insurance company

o Court found that there was appropriate risk shifting and risk distribution.

Massachusetts Mutual Life Insurance Co. v. United States, 103 Fed. Cl. 111 (Fed. Cl. 2012)

IRS is appealing a Court of Federal Claims case that allowed a deduction for policyholder dividends paid within 8 ½ months after the end of the year.

On the other hand, New York Life is appealing its case out of the 2nd Circuit. The court disallowed the Company’s deduction for policyholder dividends paid after year end. New York Life Insurance Co. v. United States, 724 F. 3d 256.

Split in the circuits

2013 Tax Rate Changes

Top individual rate: 39.6% (up from 35% in 2012)

Maximum capital gains rate: 20% (up from 15% in 2012)

Medicare contribution tax: .9% on earned income (new for 2013)

Net Investment income tax: 3.8% on net investment income (new for 2013)

Top rate as high as 43.4%

No change in C corporation income tax rates (yet)

Capitalization Regulations

Final regulations issued September 2013o Simplify and refine some of the temporary regulations and

create new safe harborso Move away from facts and circumstances and subjective nature

of current standardso Taxpayer friendly

Effective for years beginning on or after January 1, 2014o Option to apply to 2012 or 2013

Capitalization Regulations

Code Section 263o Capitalization of amounts paid to acquire, produce or improve

tangible property

Code Section 162o Deduction for all ordinary and necessary business expenses,

including certain supplies, repairs and maintenance

New Regulationso General framework for distinguishing capital expenses v.

deductible supply, repair and maintenance costs

De Minimis Capitalization

Final regulationso Safe harbor at the invoice or item level

$5,000 per invoice or item, if applicable financial statement$500 per invoice or item, if no applicable financial statement

Applicable financial statemento Certified audited financial statement

Not a review or compilationo Financial statements required to be submitted to a federal or

state agencyIncludes insurance company Annual Statements

De Minimis Capitalization

Accounting Policyo To take advantage of the $5,000 de minimis rule, taxpayers

must have written book policies in place at the start of the tax year that specify a per-item dollar amount (up to $5,000) that will be expensed for financial accounting purposes.The policy can set different thresholds for each asset class.

Routine Maintenance

Cost of certain routine maintenance need not be capitalizedo Recurring activitieso More than once during the life of the propertyo Expect to perform to keep property in ordinarily efficient

operation conditiono Final regulations now include buildings and structural

componentso More than once over a 10 year periodo No need to consider treatment of costs on financial statements

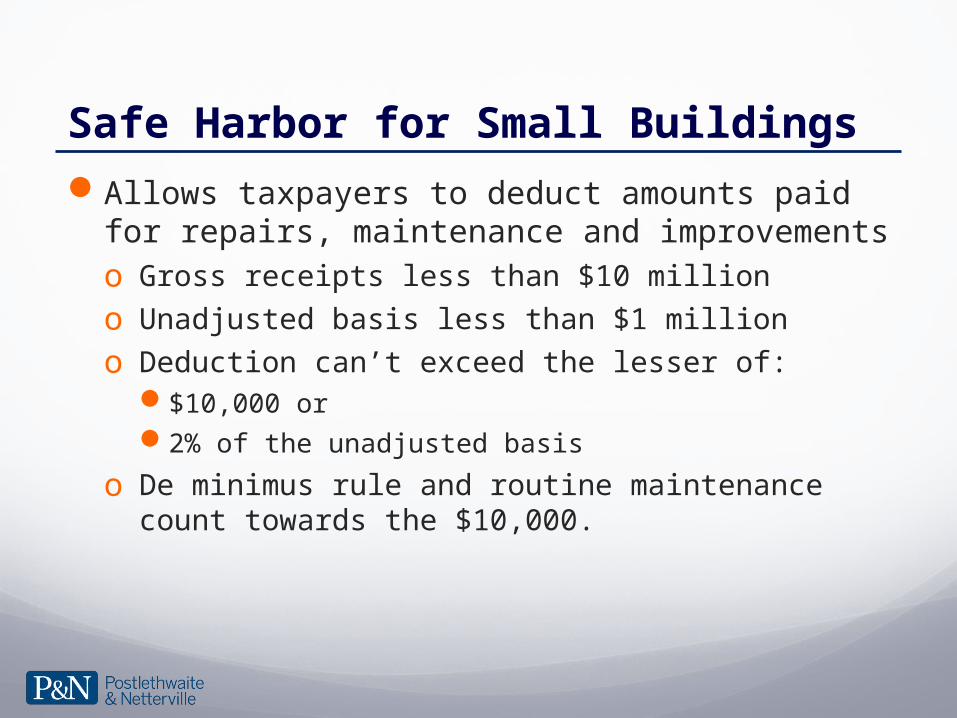

Safe Harbor for Small Buildings

Allows taxpayers to deduct amounts paid for repairs, maintenance and improvementso Gross receipts less than $10 milliono Unadjusted basis less than $1 milliono Deduction can’t exceed the lesser of:

$10,000 or2% of the unadjusted basis

o De minimus rule and routine maintenance count towards the $10,000.

Election to Capitalize Repair and Maintenance Costs

Annual election to opt out of expensing repair and maintenance costso Must be capitalized on books and records as wello Depreciate expenses

Dispositions

Released final regulations on August 14, 2014.

Taxpayer can recover the basis of “ghost assets” that may still be on the books from years past.

Limited time to clean up the books.

Must make the “late partial disposition election” by January 1, 2015.

Affordable Care Act

2014 – Individual Mandate enforced

2015 – Large Employer Mandate (offer minimum affordable coverage or pay penalty)o Transitional relief for employers with 50-100 employees.o Reporting of information begins in 2016 with information from

2015.o 1094-B, 1094-C, 1095-B and 1095-C

Report of Foreign Bank and Financial Accounts

FBARo Not a tax returno Fin Cen Form 114o Filed by United States Persons with a financial interest in or

signature authority over a foreign financial accountAggregate value of accounts must exceed $10,000 at any time

during a calendar year

Report of Foreign Bank and Financial Accounts

FBARo Financial interest – US person is owner of record or has legal

titleo Owner or legal title holder is defined as:

Person acting as agent for US personCorporation with 50% of vote or value owned by US personPartnership with 50% of profits or capital owned by US personTrust

US person is grantor and has ownership interest, or Greater than 50% in assets of trust, or US person has appointed protector subject to US persons instruction

Report of Foreign Bank and Financial Accounts

FBARo Signature Authority

Authority of an individual to control the disposition of money, funds or other assets held in financial account by direct communication

Authority can be alone or in conjunction with another individualo Personal financial managers often have such authority

Report of Foreign Bank and Financial Accounts

FBARo Filings

Must be received by June 30Mailbox rule does not apply

o PenaltiesUp to 50% of account value for each failure to fileCriminal penalties may include prison

Report of Foreign Bank and Financial Accounts

Form 8938o Required by section 6038Do Tax form filed with annual income tax returno Filed by “Specified Individuals” with an interest in “Specified

Foreign Financial Assets”o Until further guidance is issued, only individuals need to file

this form.

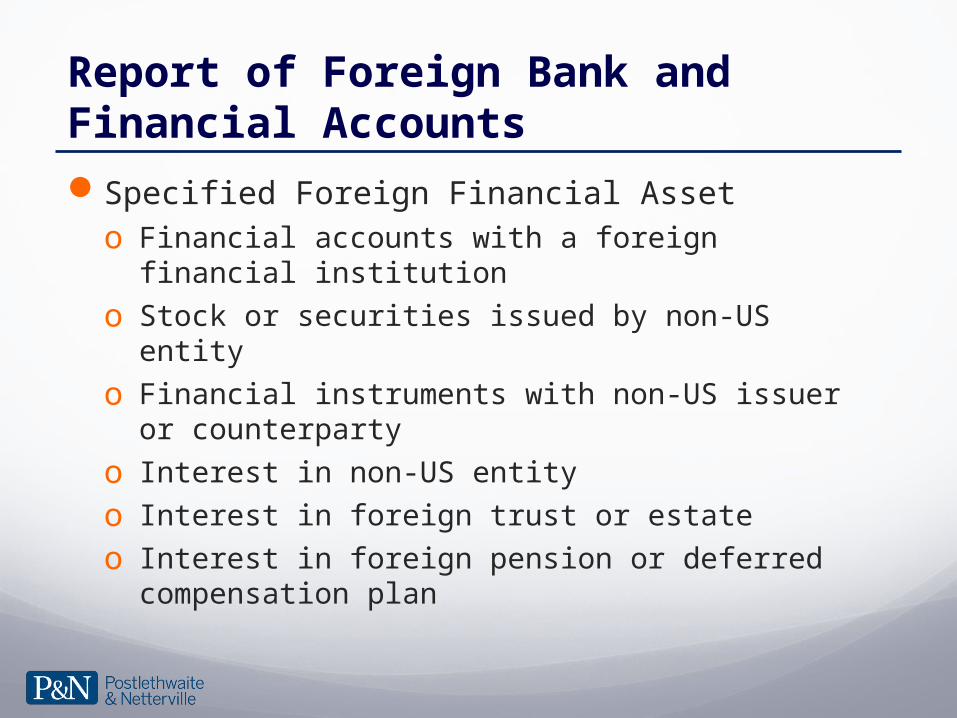

Report of Foreign Bank and Financial Accounts

Specified Foreign Financial Asseto Financial accounts with a foreign financial institutiono Stock or securities issued by non-US entityo Financial instruments with non-US issuer or counterpartyo Interest in non-US entityo Interest in foreign trust or estateo Interest in foreign pension or deferred compensation plan

Report of Foreign Bank and Financial Accounts

Specified Foreign Financial Asset (exceptions)o Assets held through US or foreign custody account

Foreign custody account must be reportedo Assets held by non-disregarded entities

Interest in entity may be reportableLook through applies to disregarded entities

o Real estate if not held through foreign entityo Foreign social securityo Assets reported on certain other forms

Foreign Account Tax Compliance Act (“FATCA”) FATCA was enacted in 2010.

Regulations were enacted in January 17, 2013 to implement FATCA and took effect on July 1, 2014.

Purpose is the uncover and deter US individuals hiding unreported financial accounts outside the US

To accomplish goal, the US needs information from financial institution outside the U.S. for these accounts to ensure the US residents/citizens are reporting their financial accounts.

To “incentivize” foreign financial institutions (“FFI”) to enter into agreements with the IRS, FATCA requires withholding agents making “withholdable payments” to non-participating FFI to withhold 30% on such payments.

Foreign Account Tax Compliance Act (“FATCA”) FATCA was enacted in 2010.

Regulations were enacted in January 17, 2013 to implement FATCA and took effect on July 1, 2014.

Purpose is the uncover and deter US individuals hiding unreported financial accounts outside the US

To accomplish goal, the US needs information from financial institution outside the U.S. for these accounts to ensure the US residents/citizens are reporting their financial accounts.

To “incentivize” foreign financial institutions (“FFI”) to enter into agreements with the IRS, FATCA requires withholding agents making “withholdable payments” to non-participating FFI to withhold 30% on such payments.

Foreign Account Tax Compliance Act (“FATCA”) FATCA

o Withholding agents include US entities making a withholding payment under FATCA

o If withholding agent fails to withhold, they are liable for the 30% withholding plus interest and penalties.

FATCA withholding is required when:o A withholding agent;o Has control, receipt, custody or disposal of income that is a type identified

as “withholdable” under FATCAo Makes a payment of this “withholdable” income to a foreign recipient; ando That foreign recipient has not provided information attesting to its

compliance with FATCA.

Foreign Account Tax Compliance Act (“FATCA”) A US entity will only be a US withholding agent under FATCA if the payments it makes

are withholdable payments under FATCA

In generalo US source FDAP (“fixed, determinable, annual, periodic”) income.o Gross proceeds from the sale or other disposition of property of a type that can produce US

source interest or dividends

More specifically for FATCA-o Payments in connection with a lending transactiono Payments in connection with a forward, futures, option or notional principal contract or

similar financial instrumentso Premiums for insurance contractso Amounts paid under cash surrender insurance or annuity contractso Dividendso Interesto Investment advisory, custodial, bank and brokerage fees