Insurance Regulatory Framework update 2016 11 14 Insurance Regulatory... · Insurance Regulatory...

22

Insurance Regulatory Framework update 2016 November 2016 Presentation for: 2016 Insurance Regulatory Framework Seminar By: Jo-Ann Ferreira

Transcript of Insurance Regulatory Framework update 2016 11 14 Insurance Regulatory... · Insurance Regulatory...

Insurance

Regulatory

Framework

update 2016

November 2016

Presentation for:

2016 Insurance Regulatory

Framework Seminar

By: Jo-Ann Ferreira

Financial

Services

Board

Slide 2

Agenda

• Legislative reforms

−Primary Legislation

−Subordinate Legislation

• Demarcation regulations

• Other regulatory initiatives

Financial

Services

Board

Slide 5

Primary Legislation

Insurance Bill

Where we are:

− Bill tabled in Parliament on 27 January 2016

− To be published for comment by Parliament soon

− Parliament process to commence early in 2017

− Envisaged commencement date: 2nd half of 2017

Includes:

− Consequential amendments to the LTIA & STIA through Schedule 1

to align the LTIA & STIA to the Insurance Bill

Financial

Services

Board

Slide 6

Primary Legislation

Insurance Bill

Overview:

− Bill has a “prudential” focus (insurance “conduct of business” provisions

will in the interim be dealt with through LTIA & STIA and finally in CoFI Bill)

− Consolidates long-term (life) and short-term (non-life) prudential regulatory

framework

− Proportionality principle applies throughout

− Framework legislation - technical requirements in subordinate legislation

i.e. prudential standards

− Complements broader financial sector reforms

− Repeals prudential sections of the LTIA & STIA

Financial

Services

Board

Slide 7

Primary Legislation

Conduct of Financial Institutions (CoFI) Bill

Overview:

− Phase 2 of Twin Peaks

− Phase 1: FSR Bill will build on existing market conduct framework (serve as

an overlay)

− Phase 2: Existing sectoral legislation to be reviewed, amended and

ultimately replaced with CoFI Bill, to ensure a comprehensive, consistent

and complete approach to governing the conduct of financial institutions

across the financial sector

− NT has established a working group, with FSB & SARB representatives, to

develop the CoFI Bill

− Aim to table in Parliament in 2018

Financial

Services

Board

Slide 8

Subordinate Legislation

Regulations

Policyholder Protection Rules (PPRs)

Conduct of

Business

Standards

Prudential

Financial

Services

Board

Slide 9

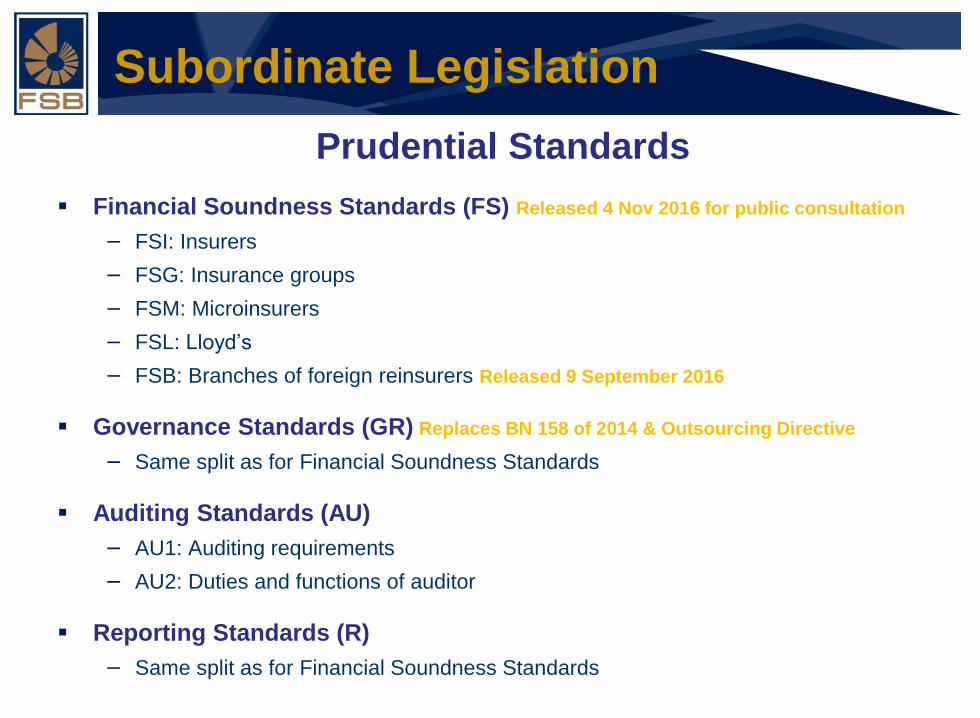

Subordinate Legislation

Prudential Standards

Financial Soundness Standards (FS) Released 4 Nov 2016 for public consultation

− FSI: Insurers

− FSG: Insurance groups

− FSM: Microinsurers

− FSL: Lloyd’s

− FSB: Branches of foreign reinsurers Released 9 September 2016

Governance Standards (GR) Replaces BN 158 of 2014 & Outsourcing Directive

− Same split as for Financial Soundness Standards

Auditing Standards (AU)

− AU1: Auditing requirements

− AU2: Duties and functions of auditor

Reporting Standards (R)

− Same split as for Financial Soundness Standards

Financial

Services

Board

Slide 10

Subordinate Legislation

Prudential Standards

General Standards (G) Issued for comment on 9 September 2016

− G1: Microinsurance business thresholds

− G2: Insurance business excluded from or included in the application of Bill

− G3: Registration of shares in name of nominee

− G4: Reinsurance Arrangements

Fit & Proper Standards (FP) Replaces BN 158 of 2015

− FP1: Fit & Proper framework

− FP2: Directors, senior managers, heads of a control functions and auditors

− FP3: Trustees of trusts of Lloyd’s or a branch of a foreign reinsurer

− FP4: Significant owners

Financial

Services

Board

Slide 11

Subordinate Legislation

Conduct of Business

• Conduct of business reforms to be given effect to through Regulations and

PPRs under the LTIA & STIA.

• To be given effect to in two tranches during the course of 2016 / 2017

• Separate presentation on these reforms

PRUDENTIAL MARKET CONDUCT

PRIMARY SECONDARY PRIMARY SECONDARY

CURRENT LTIA

STIA

Board Notices

Insurance Notices

PPRs

Regulations

LTIA

STIA

Board Notices

Insurance Notices

PPRs

Regulations

TWIN PEAKS

PHASE 1 Insurance Act Prudential Standards

LTIA

STIA

Insurance Notices

PPRs

Regulations

TWIN PEAKS

PHASE 2 Insurance Act Prudential Standards CoFI Act Conduct Standards

Financial

Services

Board

Slide 13

Demarcation Regulations

Status:

− Regulations were tabled in Parliament on 28 October 2016 with planned

effective date of 1 April 2017

− 3rd revised draft (1st draft - March 2012, 2nd draft - April 2014)

Purpose:

− Demarcates responsibility for supervision of medical schemes and health

insurance products

− Aims to ensure that health insurance products do not undermine the medical

scheme environment

− Specifies which types of contracts are regulated under the LTIA & STIA as

health policies and accident & health policies, and are accordingly excluded from

regulation under the Medical Schemes Act (MSA), despite meeting the definition

of “business of a medical scheme”

Financial

Services

Board

Slide 14

Demarcation Regulations

COVER TYPE

Not deemed to be

business of

medical scheme

(written under

LTIA/STIA; MSA

does not apply)

Deemed to be business of medical

scheme, but exempted from MSA

through the regulations

Deemed to be

business of

medical scheme,

not exempted from

MSA through

regulations

Can be written

under LTIA

Can be written

under STIA

Non-impacted products,

e.g. dread disease X

Medical expense shortfall X

Non-medical expense cover

as a result of hospitalisation X X

HIV, Aids, tuberculosis and

malaria testing & treatment X X

Medical emergency

evacuation or transport X X

Frail care X

International travel

insurance X

Primary health insurance X

Financial

Services

Board

Slide 15

Demarcation Regulations

Primary Health Insurance Products:

− Not allowed to be offered by insurers i.t.o. LTIA/STIA; has to be offered in

accordance with MSA

− 2 year exemption period will be facilitated by CMS to allow development of a

Low Cost Benefit Framework led by Department of Health

Definition of a “business of a medical scheme”:

− Amended by FSLGA Act 45 of 2013 (effective 28 February 2014)

− To come into effect at the same time as the Regulations are finalised

− Aimed for 1 April 2017

Financial

Services

Board

Slide 16

Demarcation Regulations

Transitional periods:

− Existing health policies (LTIA) expected to be aligned as and when varied or

renewed after the Regulations come into operation

− Existing accident and health policies (STIA) expected to be aligned by 1 January

2018

Financial

Services

Board

Slide 17

Demarcation Regulations

Products subject to prescribed requirements:

− Marketing, disclosure and reporting requirements

− Maximum commission levels and maximum policy benefits

− Policy and underwriting limitations, including:

Gap cover, hospital plans, cover for HIV/Aids, TB, malaria testing & treatment

- must be underwritten on a group and non-discriminatory basis

- limitation on waiting periods

- requirements for variation and termination

All (except gap cover)

- may not require medical scheme membership

Hospital plans

- prohibition on policy benefits that fully or partially indemnify against medical

expenses

Financial

Services

Board

Slide 19

Other Regulatory Initiatives

• Third-party Cell Captive Insurance position paper

− To be published before the end of 2016

• Information Request 3 of 2016 (LT&ST&LL)

− Info request on binder functions and binder fees

− Issued on 12 September 2016 due by 14 October 2016

• Information Letter 4 of 2016

− Standing approval under s.24 LTIA and s.23 STIA for the issuance of shares

by or a change in capital structure of cell captive insurers, issued on 13

September 2016, including additional notification and reporting requirements

• Information Request 5 of 2016

− Info request on new and existing third-party cell captive insurance business

− Issued on 12 September 2016 due by 31 October 2016

− Information collected will form the basis for ongoing supervision, including a

planned thematic review in 2017

Financial

Services

Board

Slide 20

Other Regulatory Initiatives

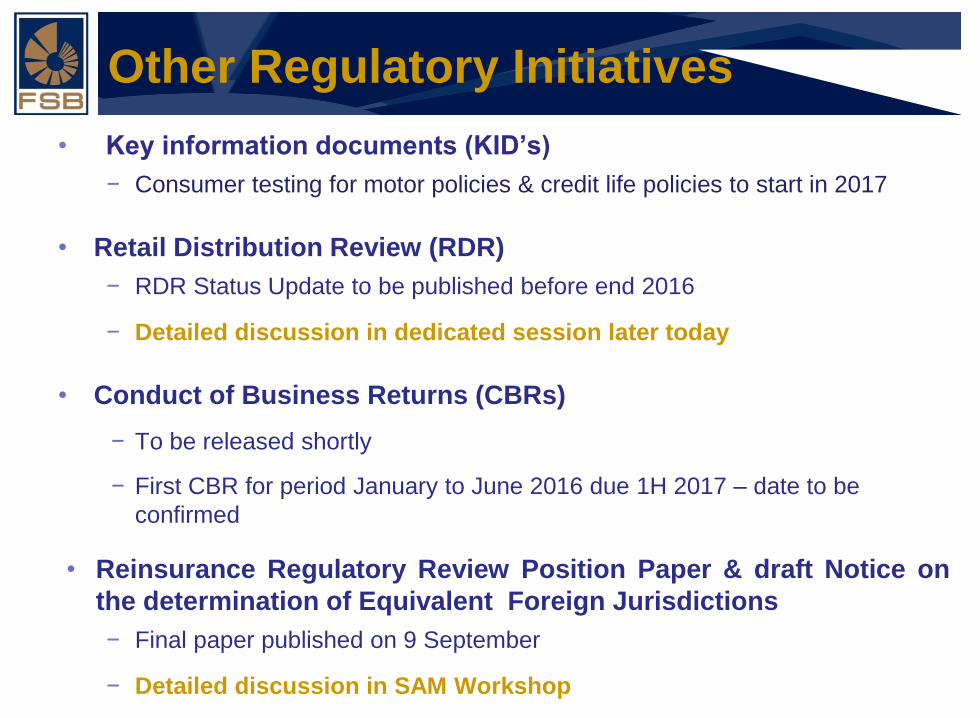

• Key information documents (KID’s)

− Consumer testing for motor policies & credit life policies to start in 2017

• Retail Distribution Review (RDR)

− RDR Status Update to be published before end 2016

− Detailed discussion in dedicated session later today

• Conduct of Business Returns (CBRs)

− To be released shortly

− First CBR for period January to June 2016 due 1H 2017 – date to be

confirmed

• Reinsurance Regulatory Review Position Paper & draft Notice on

the determination of Equivalent Foreign Jurisdictions

− Final paper published on 9 September

− Detailed discussion in SAM Workshop

Financial

Services

Board

Slide 21

Other Regulatory Initiatives

• Consumer credit insurance − As said, amendments to the Regulations and PPRs will facilitate alignment with dti

regulations on credit life insurance and give effect to certain regulatory reforms

proposed in the Technical Report

− Responses on the CCI Information Request (IR 3/2015 (LT&ST)) issued in December

2015 due mid-March 2016 analysed

− Report summarising key trends emerging from the responses being finalised

− Will inform possible supervisory interventions relating to CCI going forward

• Inclusive insurance market − Microinsurance paper will be published soon

− Update on the proposed regulation and supervision of an “inclusive insurance

market” including setting out regulatory options for funeral parlours

− Overview of the work undertaken since NT’s Microinsurance Policy Document

in July 2011, as well as the roadmap for implementing the framework

(including the proposed timelines) and interim arrangements

Qu

esti

on

s?