INSTITUTIONAL PRESENTATION 2Q21

120

1 INSTITUTIONAL PRESENTATION 2Q21

Transcript of INSTITUTIONAL PRESENTATION 2Q21

1

INSTITUTIONALPRESENTATION

2Q21

22

Disclaimer

This presentation may contain forward-looking statements. Such statements are not

statements of historical facts and reflect the beliefs and expectations of the company's

management. The words "anticipates”, "believes”, "estimates”, "expects”, "forecasts”,

"plans”, "predicts”, "projects”, "targets" and all similar words are intended to identify these

statements, which necessarily involve both known and unknown risks and uncertainties.

Known risks include uncertainties, which are not limited to the impact of competitive

services and pricing, market acceptance of services, service transactions by the company and

its competitors, regulatory approval, currency fluctuations, changes in the service mix

offered, and other risks described in the company’s reports. Forward-looking statements

speak only in terms of the date they are made and Banco Bradesco does not assume any

obligation to update them in light of new information and/or future developments.

33

4-13

Corporate Profile

Results 90-105

Corporate Strategy

14-20

21-26

ESG 27-46

Our Businesses 47-89

106-119

Macroeconomic Information

Attachments

4

MacroeconomicInformation

5

69.865.5

73.7 75.3 74.3

88.8

82.1 83.1

2015 2016 2017 2018 2019 2020 2021 2022

GDP should show important growth in 2021

Economic growth has accelerated with progress in the COVID-19 vaccination process, companies’ low indebtedness, and good global conditions.

The formal labor market has experienced strong expansion, favoring credit and keeping delinquency rates low.

Inflation has accelerated in the context of greater demand and shocks related to food and energy prices.

Fiscal risks have diminished in light of GDP growth, and contributed to currency appreciation. Along with Selic hikes, we expect lower inflationary pressures ahead.

The global context remains favorable for commodity prices, contributing significantly to various sectors in Brazil.

Formal Employment with a Broad Recovery(Index Feb. 2020 =100)

Projections for Public-Sector Debt Have ImprovedGross Debt / GDP

Macro Context

95.7*96.7*

* Greater projection observed in Fiscal Prism report (Oct. 2020)

103.7

106.8

104.3

102.6

104.7105.1

90

92

94

96

98

100

102

104

106

108

Feb-20 Apr-20 Jun-20 Aug-20 Oct-20 Dec-20 Feb-21 Apr-21

Brazil North

Northeast Southeast

South Midwest

6

BRL vs EmergingAccumulated variation of the Real against median and emerging percentiles

Source: Bloomberg, Bradesco

3.913.83

4.08

5.20

3.5

4.0

4.5

5.0

5.5

jan/2019 mai/2019 set/2019 jan/2020 mai/2020 set/2020 jan/2021 mai/2021 set/2021

75%

25%

mediana

BRL

Jan-2019 May-2019 Sep-2019 Jan-2020 May-2020 Sep-2020 Jan-2021 May-2021 Sep-2021

Average

7

IPCA*Core Average

Source: IBGE, Bradesco* Desasonalized and annualized – 3ma, 6ma e 12 months

8.60%

6.86%

6.13%

-5%

0%

5%

10%

15%

20%

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

3ma 6ma 12m

8

IPCA Expectations 2022Focus Expectations, Median and top5

Source: BCB, Bradesco

Average Last 5 days Top 5

.

.

4.2

3.9

4

3.8

3.7

3.6

3.5

3.4

3.3

99

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Jan

-18

Fe

b-1

8

Ma

r-18

Ap

r-18

Ma

y-1

8

Jun

-18

Jul-

18

Au

g-1

8

Se

p-1

8

Oc

t-18

No

v-1

8

De

c-1

8

Jan

-19

Fe

b-1

9

Ma

r-19

Ap

r-19

Ma

y-1

9

Jun

-19

Jul-

19

Au

g-1

9

Se

p-1

9

Oc

t-19

No

v-1

9

De

c-1

9

Jan

-20

Fe

b-2

0

Ma

r-2

0

Ap

r-2

0

Ma

y-2

0

Jun

-20

Jul-

20

Au

g-2

0

Se

p-2

0

Oc

t-2

0

No

v-2

0

De

c-2

0

Jan

-21

Fe

b-2

1

Ma

r-2

1

Ap

r-2

1

Ma

y-2

1

Jun

-21

Jul-

21

Au

g-2

1

SELIC (5.25%) DI 2022 (6.35%) DI 2023 (7.88%) DI 2024 (8.50%) DI 2025 (8.78%) DI 2027 (9.10%) DI 2030 (9.41%)

*Through 8/4/2021 | Source: Eikon

Fixed x Floating Rate (DI) Swap

10

CDI and COPOM Implied EstimateSelic Expected in the Market Curve

Source: Bloomberg, Bradesco

5,3

6,7

8,1

9,19,6 9,8 9,9 10,0 10,1 10,3 10,4 10,6

3,5

4,5

5,5

6,5

7,5

8,5

9,5

10,5

11,5

ago-21 set-21 out-21 dez-21 jan-22 mar-22 abr-22 jun-22 jul-22 set-22 out-22 dez-22

11.5

10.5

9.5

8.5

7.5

6.5

5.5

4.5

3.5

5.3

6.7

8.1

9.19.6 9.8 9.9 10.0 10.1 19.3 10.4 10.6

Aug-21 Sep-21 Oct-21 Dec-21 Jan-22 Mar-22 Apr-22 Jun-22 Jul-22 Sep-22 Oct-22 Dec-22

11

Median of GDP Projections – 2022 e 2023Projections Begin to Reflect High Interest Rates

Source: BCB, Bradesco

1.93

2.35

1.8

1.9

2

2.1

2.2

2.3

2.4

2.5

2.6

Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21

2022

2023

12

90.0

92.0

94.0

96.0

98.0

100.0

102.0

104.0

106.0

4T16 1T17 2T17 3T17 4T17 1T18 2T18 3T18 4T18 1T19 2T19 3T19 4T19 1T20 2T20 3T20 4T20 1T21 2T21

PIB x Mercado de Trabalho4T16=100, dessazonalizado

PIB Emprego

4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21

GDP and JobBase 100 = 4Q16

Source: Bradesco

GDP Job

1313

Economic ScenarioProjections Table

2019 2020 2021 2022

GDP (% p.a.) 1.4 -4.1 5.2 1.8

Extended Consumer Price Index IPCA (% p.a.) 4.31 4.52 7.8 3.3

General Market Price Index IGP-M FGV (%) 7.3 23.1 18.6 4.0

Selic (% p.a.) year-end 4.50 2.00 7.50 7.50

USD - Commercial Rate (R$/US$) year-end 4.03 5.20 5.00 5.50

Industrial production (% p.a.) -1.1 -4.5 5.4 1.5

Expanded Retail Sales (% p.a.) 3.9 -1.5 6.0 3.6

Jobs created (in thousands) 1,816 -8,373 5,601 2,753

Unemployment rate (% p.a. year average) 11.9 13.2 13.8 12.4

Credit Stock (%p.a.) 6.5 15.6 12.0 9.3

Balance of Trade (BCB) (US$ billion) 40.5 43.2 71.4 83.0

Current Account Balance (US$ billion) -50.7 -12.5 9.0 10.9

Public Sector Primary Result (R$ billion) -61.9 -703.0 -110.1 -102.2

Gross Debt (% GDP) 74.3 88.8 81.5 83.2

Depec’s economic projections are reassessed every month. In times of greater volatility, the degree of uncertainty and the margin of

error increase, especially between review periods. The projections reflect the premise that the necessary adjustments to the economy will be made in the coming years. If the adjustments are not confirmed, or are even better than expected, there may be a major change in the scenario projections. Last scenario update: 09/01/2021

14

CorporateProfile

1515

ROE(accumulated)

1H21

18.2%

BankingCorrespondents

41,584Branches +

PAs/PAEs + UNs

8,720Tier 1

Capital

14.1%

R$ 288

(34.2 million account holders)

Million Clients

71.2

Recurring Net Income 1H21

Billion

R$ 12.8

BillionPremiums and Contributions

1H21

R$23.2R$ 342Total

Assets

Billion

INSURANCE OPERATIONS

Total Assets

Trillion

R$ 1.7Billion

R$ 726Expanded Loan

Portfolio

Net Income1H21

R$ 2.3Billion Billion

Technical Provisions

Financial Highlights- 2Q21One of the largest financial groups in Latin America

CONSOLIDATED GROUP

1616

1997• Credireal• Itabanco• BCN• Companhia União

de Seguros Gerais

• BCR1998

1999• Banep• Continental

• Banco BoaVistaInteratlântico

• Banco das Nações2000

2001• Banque

Banespa International Luxemburg

• Banco Postal/Correios

• Banco Cidade• BES (3%)• BEA• Banco Mercantil• Deutsche Bank

DTMV S.A.2002

2003• Banco Zogbi S.A.• BBVA• Gestão de Recursos de

Terceiros do JP Morgan S.A.

• B.E.M2004

2005• BEC

• Amex2006

2007• BMC

• Ágora Corretora• Medservice2008

2009• IBI• Odontoprev

• Baloise - Atlântica Cia Brasileira de Seguros

1996

Founding of Banco Brasileiro

de Descontos(Bradesco)

Creation of

Fundação

Bradesco

Formation

of group

Bradesco

Seguros

Our HistoryPioneering, innovation, and expansion

First company in

Latin America

to buy a computer

Bradesco Card

First Brazilian

credit card

First “cash

dispenser” installed,

SOS Bradesco,

predecessor of the

current ATM

Branch nº 1,000

opened in Chuí, far

south of Brazil

First Mobile

Banking in

Latin America

First credit card

made from

recycled plastic

1943 1956 1962 1968 1970 1995

First Internet

banking in Latin

America

2000

2007 2010

First branch on a boat

(Voyager III). It runs

about 1,600 km

between Manaus and

Tabatinga (Amazonas)

2013

1983

2014 2020

MAIN ACQUISITIONS:

2017 2018

• HSBC Brasil2016

Biometrics

End of

Password

2021

New Information technology center,

part of the IT

improvement project, started in

2003

Self-service

without card

BIA

2008

2005

Joined the UN Global Compact

2006

Included in the Dow Jones

Sustainability Indexes

Included in ISE

Joined the CDP

2011

Joined UNEP-FI

First Brazilian bank to

commit toNet-Zero

Yearbook S&P 2021 –

Only Brazilian in the

category

Relaunch of Ágora

2019• BAC Florida

2009

1717

An Ecosystem EvolvingCustomer service for all of your needs

Bradesco Leasing

Losango

Bitz

Bradesco Financiamentos

BBI

next

Ágora

Bradesco Internacional

BAC

BRAM

Bradesco Cards

Bradesco Consórcios(Consortia)

Initiatives

Bradesco

Target AudiencesInvested

Bradesco Seguros

Bradesco Auto/Re

(Vehicle/P&C)

Orizon, OdontoPrev,

EuropAssistance, Fleury, IRB

Brasil RE, andSwiss Re

Bradesco Vida e Previdência

(Life and PensionPlan)

Bradesco Saúde

(Health)Bradesco

Capitalização(Capitalization)

Bradesco BSPEmpreendimentos

Livelo, Veloe, andCartão DIN (DIN Card)

Elopar, Digio, Alelo,

and Elo

Quod Credit Manageme

nt and Recovery

(RCB)

Market PlaceBradesco

Autoline

Shopfácil(Shop Easy)

MEI Portal

BIA

Inovabra

Bradesco Agronegócios(Agribusiness)

Corporate

Bradesco Expresso(Bradesco Express)

Private

Bradesco Public

Authority

Prime

Institutional Non-accountholder

Retail

Cielo

1818

46,85150,006

43,560

38,340 38,70839,100

39,100 39,10040,920 41,584

2013 2014 2015 2016 2017 2018 2019 2020 1Q21 2Q21

Service ChannelsServing customers how they desire

Digital Channels

Internet Banking Bradesco Apps

Fone Fácil ATMs

Physical Channels

Branches + Service Points (PAs + PAEs) + BUs (UNs)

Bradesco Expresso

4,674 4,659 4,507 5,314 4,749 4,617 4,478 3,395 3,312 3,168

57708 766 877

4,766 4,631 4,2474,834 4,827 4,731 4,871 4,737 4,709 4,675

9,440 9,290 8,7549,576 9,348 9,406 8,840 8,787 8,720

2013 2014 2015 2016 2017 2018 2019 2020 1Q21 2Q21

Branches UNs PAs + PAEs

10,148

98% of

transactions are made

through digital channels

91% are

concentrated in mobile

and the internet

19

Physical PresenceProximity and speed to serve customers

Exchange Services

New York

Mexico City

Cayman Islands

Buenos Aires

London

Luxemburg

Hong Kong

São Paulo

Miami Commercial/ Private bank

BBI/Securities

3,168Branches

5,552Customer

Service Points

41,584Expresso

% Network Distribution % Market ShareD M

D

M

22.5%

23.9%

D

M

7.2%

21.9%

D

M

7.9%

16.9%

D

M

14.2%

13.5%

D

M48.2 %

17.4%

20

1 – Asset management, pension funds, and securities brokers2 – Individual clients or corporate client consumers of Bradesco’s products that do not have a bank account

Large Corporate

≥ R$4 bn

Corporate

R$ 500 mn to R$ 4 bn

CorporateOne

R$ 30 mn to R$ 500 mn

Co

mp

an

ies a

nd

Bu

sin

ess

Up to R$ 30 mn

≤ R$4,000

Classic

≥ R$40,000 to R$ 149,999.99

Exclusive

R$4,000 to R$14,999.99

≥ R$5 mn

Private Bank

Pri

me

≥ R$150,000

≥ R$15,000

Non-account holders2

IND

IVID

UA

LS

InvestmentMonthly Income Annual Revenue

CO

MP

AN

IES

Multis & institutional1

Customer Segmentation A bank for everyone

21

CorporateStrategy

22

Clientsour inspiration

Digital transformationhow we do it

Sustainabilitymade to last

Peopleour team

“Create opportunities for people’s fulfillment and

the sustainable development of

companies and society

”

• Client-centered• Contextualized offers• Journeys of excellence• Digital service evolution• Customer empowerment

• Efficiency• Agility• Security• Improvement• Innovation

• Entrepreneurial attitude• High performance

• Transformational skills• Ethics, transparency, and respect

• Innovative, challenging, and diverse environment

Corporate StrategyOn four pillars, which guide our trajectory towards longevity

• Capital strength and liquidity• Integrated view of risks

• Diversity•Environmental ethics and responsibility

• Corporate governance

23

Business as a Service

Third parties developing new lines of business, reaching new segments

Portal MEI – Solutions for individual micro entrepreneurs

3. Open Banking

R$ 6 billion Invested in technology per year

R$ 2 billion

Invested in innovation

Focus on customer experience

New products and technologies (Digital Wallet)

BIA – leading bank in AI

Millennials and hyperconnected people

Construction of journeys

Without fees, with “special gifts”

2. Native Platforms

Present in the Bradesco and Next apps

Advice for clients through investment specialists

Digital wallet created with a complete ecosystem

20-25% market share in 3 years

Acquisition of Didin

Cybersecurity and SecurityPrograms

Digital StrategyThree fronts focused on digital acceleration

1. Digital Transformation

Development in Agile Methodology and teams organized in villages

24

104.5

348.0

733.1

24.045.9

1H19 1H20 1H21

233%

111%

91%

PF

PJ

Digital Account HoldersIn millions

MobileFinancial Transactions | In millions

14% 13%

+ AUTONOMY + EXPERIENCE

Ind

ivid

ua

ls

Total Sales| R$

+80%1H21 x 1H20

Number of ItensDistributed

+62%1H21 x 1H20

Mobile Sales | R$

+164%1H21 x 1H20

Internet Banking Sales| R$

+63%1H21 x 1H20

App Downloads

8MN1H21

Health Reimbursements

94%1H21

77%1H21

Private Pension Plan Sales

91%1H21

Bradesco Insurance

Digital Channels Expansion in the use and generation of financial transactions

17.520.0

22.5

Jun-19 Jun-20 Jun-21

214.6315.0

599.6

1H19 1H20 1H21

Opening of Accounts by AppIn thousands

Clients can handle everything without leaving home

98% of transactions were made via digital channels in 1H21

Investments | R$

+59%1H21 x 1H20

+51%1H21 x 1H20

Loan Operations | R$

Personal Loan and Payroll-Deductible Loans

Discount of Trade Bills

Advances to Suppliers

Granting of Loans

+21%1H21 x 1H20

PIX

+63%2Q21 x 1Q21

+108%2Q21 x 1Q21

COMPANIESINDIVIDUALS

INDIVIDUALS

COMPANIES

INDIVIDUALS

Issuing Credit Cards

+3.9MN1H21

Payments | R$

+30%1H21 x 1H20

Requests for Credit Cards

+270%1H21 x 1H20

Consortium | R$

+62%1H21 x 1H20

Light and Heavy Vehicles and Real Estate

COMPANIES

Claims Inspections of Autos

Taxes, Collections and Consumer

25

Technologies

Artificial

Intelligence

algorithms

Blockchain APIBiometricsBig

Data

CENTERS

RESEARCH

VENTURES

STARTUPS

LAB

HUB

HABITAT

INTERNATIONAL

Open innovation

AI and other

technologies

Investments

in startups

Open innovation

Space for co-innovation

NY & London

Open innovation

portal

Prototyping,

PoCs and certification

Innovation Ecosystem

inovabra.com.br

Awards

Valor Inovação Brasil 2019: 1st place in the banking category

(3rd consecutive year)

Efma Innovation of the Month: Sole Proprietorship Portal case study

Efma Innovation Awards 2019 • Digital Marketing: Vagalume case study

Gartner Eye on Innovation: Entrepreneur Sole Proprietorship Portal case study

FELABAN CLAB 2019: BIA case study

Whow! Award: Banking Category

Bank Reporting Award: Blockchain-Ripple case study

Bank Reporting Recognition: Move Caronas app

Learning & Performance Brazil 2019/2020:

BIA, in the Best in Brazil category

Most Innovative Bank in Latin America: The Banker

2020 and 2021

InnovationComplete innovation ecosystem

26

New!

8.5 million income statements

for individuals delivered by BIA Mobile

(through June 2021)

New!

1.3 million interactions

BIA on Bradesco Portal(from April 2021 to June 2021)

93Products and Services

Multi-PlatformBradesco app, Fone Fácil (Electronic

Service), WhatsApp, Google Assistant,

Amazon Alexa, Apple Business Chat,

and Bradesco Portal

100%of requests fulfilled in first call to

Fone Fácil (Electronic Service)

BIA Against HarassmentInspired by UNESCO’s “Hey Update My Voice” movement we changed BIA’s

answers so that it can react fairly and firmly against harassment

BIA, our artificial intelligence, is constantly evolving and improving its

communication skills in order to offer an experience that is even more

pleasant, intelligent, and intuitive. Bradesco is the pioneering bank in artificial

intelligence, assisting clients, and employees.

Digital Advances Centered on Clients Personalized interactions and offers

83.4 millioninteractions on WhatsApp

(from Jan. to June 2021)

Total InteractionsIn millions

61.9

192.7

275.1

1H19 1H20 1H21

43%

211%

New Features to Check

on WhatsApp

Credit Card Limits

195.9 thousand (from Jan. to June 2021)

27

ESG

28

Reference date: June 20211In thousands.2Excludes 5,402 ON and 3,845 PN shares held in treasury

53.70% COMMON

26.07% TOTAL47.93% COMMON

47.93% TOTAL

17.08% COMMON

8.56% TOTAL

28.81% COMMON

97.73% PREFERRED63.19% TOTAL

16.63% COMMON

16.63% TOTAL45.67% COMMON

0.02% PREFERRED

22.90% TOTAL

25.13% COMMON

100.00% PREFERRED

60.41% TOTAL

8.44% COMMON

2.25% PREFERRED

5.35% TOTAL

74.72% COMMON

39.51% TOTAL

0.15% COMMON

0.08% TOTAL

46.30% COMMON

100.00% PREFERRED

73.93% TOTAL

35.44% COMMON

35.44% TOTAL

# Shares June 2021 %

ON1,2 4,865,177 50.11%

PN1,2 4,844,655 49.89%

Total 9,709,832

Shareholder Structure

2929

10 members, of which 7 are

external and 3 independent

Body instated every year since 2002,

becoming permanent from 2015,

currently comprising 5 members, 2 of

which are elected by minority

shareholders.

*As of March 2021.

COMMITTEES POLICIES

BOARD OF DIRECTORS*

FISCAL COUNCILListed shares on the Brazilian Stock

Exchange, just 3 years after its

foundation

1946

Level 1 ADRs – Preferred Shares

1997

Level 2 ADRs and Latibex – Preferred Shares

2001

Level 2 ADRs – Common Shares

2012

Instrument of Policies on Disclosure and Use of

Information on Material Acts or Events and Trading

of Securities issued by Banco Bradesco S.A.;

Anti-Corruption Corporate Policy;

Internal Controls Policy;

Risk Management Policies;

Corporate Sustainability Policy;

Related-Party Transactions Policy;

Corporate Governance Policy;

Nomination and Succession of Officers Policy;

Diversity and Inclusion Policy;

Human Resources Management Policy;

Independent Auditors Hiring Policy;

Corporate Information Security and Cyber Policy;

others.

Seven Board of Director committees (Audit;

Compensation; Integrity and Ethical Conduct;

Integrated Risks Management and Capital

Allocation; Nomination and Succession; Risks;

Sustainability and Diversity) and various

executive committees

VOLUNTARY MEMBERSHIPIn 2001, joined Level 1 of Corporate

Governance at B3 S.A. – Brasil, Bolsa, Balcão

TAG-ALONG100% Common

80% Preferred

FREE FLOATCommon: 28.86%

Preferred: 97.73%

TOTAL63.22%

ETHICSCode of Corporate Ethical Conduct and various

sector codes for ethical conduct:

- For professional purchasing

- For financial and capital market professionals

- For Bradesco Seguros Group and BSP

- For internal auditors and inspectors

Corporate GovernanceRobust, transparent, and sound governance

3030*As of: March 2021.

Governance Structure

The highest governance body, responsible for

deciding on our business and electing the

members of the Board of Directors

SHAREHOLDERS’ MEETING

Ten members, 7 external and 3 independent;

responsible for establishing corporate strategy

and reviewing business plans and policies, in

addition to supervising and monitoring the

strategies assigned to the Executive Board

BOARD OF DIRECTORS*

Responsible for drawing up and monitoring

the execution of the strategic guidance

established by the Board of Directors,

managing and representing the company

BOARD OF EXECUTIVEOFFICERS

Oversight body installed

every year since 2002,

becoming permanent as of

2015, currently consisting of 5

members, 2 of which elected

by minority shareholders

FISCAL COUNCIL

Independent body, evaluating

areas and activities regarding

risk management, adequacy

of governance, and internal

controls

INTERNAL AUDIT

Audit: Monitoring of accounting practices adopted for

preparing the financial statements and the effectiveness of the

independent auditor

Compensation: Handling of the management compensation

policy

Integrity and Ethical Conduct: Disseminating and ensuring

compliance with the Bradesco oganization’s Codes of Ethical

Conduct and corporate policies

Risk Management and Capital Allocation: Management and

control of risks and capital (consolidated economic and

financial)

Nomination and Succession: Conducting succession policy and

appointing directors

Risk: Risk and capital management

Sustainability and Diversity: ESG performance evaluation,

establishing of initiatives and action strategies

COMMITTEES

Assist in the activities of the Executive Board, all regulated by

their own regulations

EXECUTIVE COMMITTEES

31

SUSTAINABILITY EVERYDAY BUSINESS

Sustainability management at

Bradesco is based on 5 core actions:

Sustainability at Bradesco

Diversity and

inclusion

High-level governance

bodies

Sustainability

governance

Policies, standards,

and manuals

Sustainability

guidelines

Integration of ESG factors into decision-making

ESG risks &

opportunities

Performance

management

Improvement of practices and

indicators

Culture and

engagement

With internal and external stakeholders

For more information about our sustainability strategy, practices and

results, visit: BradescoSustentabilidade.com.br

Sustainability Strategyand its connection with Bradesco´sprioritized SDG

Diversity and Inclusion

3232

Sustainability at Bradesco | Highlights Reinforcing our commitment to Sustainable Development

WASTE

MANAGEMENT

BIOFUELS LOW-CARBON

AGRICULTURE

HEALTH

AND SOCIALSECURITY

EDUCATION,

CULTURE ANDSPORTS

RENEWABLE

ENERGY

SANITATION

AND WATER

FOREST

MANAGEMENT

Industry group

SUSTAINABLE

BUSINESS

Credit and

capital market

advisory for

positive impact

sectors

Financial

solutions with

ESG focus

New goal: Deploy R$ 250 billion for sustainable financing by 2025

Rated Silver for the 3rd consecutive year

Only Brazilian bank among the top 5% in the sector

The only Brazilian bank to participate in the construction of the Principles for Banking Responsibility, together with the financial arm of the United Nations Environment Program (UNEP FI)

33

Sustainability at BradescoReinforcing our commitment to sustainable development

33

to commit to

*their credit and investment portfolios

*net emissions equal to zero

Forth place in the 2020 Corporate

Governance and Responsibility Ranking

Ninth among the most responsible companies

during the pandemic, in special ranking

3434

SIGNED

COMMITMENTS

DIVERSITY IS EMBODIED IN OUR:

DIVERSITY MANAGEMENT AREA:

DIVERSITY AND INCLUSION GOVERNANCE:

Code of Ethical Conduct

Human Resources Management Policy

Bradesco Organization’s Diversity and Inclusion Policy

Inserted in the Human Resources Department

Objective: To engage and strengthen diversity and inclusion within

Bradesco

Sustainability and Diversity Committee

Working Group on Diversity and Inclusion

Affinity Groups: on Gender, Sexual Orientation and Gender Identity, Accessibility, and Ethnicity

Diversity and Inclusion Commitment to diversity and representativeness

2,052interns

87,362employees

27%are black

51%are woman

4,224employees with

disabilities

3535

Human ResourcesAcknowledgments from the market (2021)

LINKEDIN TOP COMPANIES Brazil

Bradesco appears in the ranking’s top 3.

TOP EMPLOYER Certification

Excellence in people management &

employer branding.

Career of Dreams – Cia de Talentos

2nd most desirable company, being 1st

among banks.

WEPS Brazil

Silver recognition in the large corporate

category.

Best Practices in WORK AND FAMILY

BALANCE

1st place in the large corporate category

CIEE - BEST INTERNSHIP PROGRAM

1st place in the Financial and Insurance

Services category.

Best Companies GPTW WOMAN

5th place in the thematic ranking.

Best Companies GPTW LGBTQI+

Among the 10 best companies.

3636

Actions During the PandemicEthics and respect in all activities and relationships

SUPPORTING OUR CLIENTS

COMMITMENT TO SOCIETY

HEALTH AND WELL-BEINGOF OUR PEOPLE

Implementation of health and

prevention protocols to cope with

Covid-19

Opening of the new unit of Meu

Doutor Novamed, at the Head

Office Cidade de Deus

More than 79 thousand doses of

vaccines against H1N1 influenza

given to interns, employees, and

dependents

With the incentive of the

Bradesco Volunteer Program,

employees and interns donated

220 tons of food, which benefited

63 thousand people

New resources with special

conditions for personal loans

with a grace period of up to 90

days

Participation in government programs

Extension of installment

payment of loans and financing

Donation of medical supplies and

medicines to the Santa Casa

Acquisition of oxygen

concentrators for the “Oxigênio

para Todos Program” (Oxygen

for All), of the Ministry of Health

Construction of field hospital (RJ)

Installation of hospital tent in Salvador

Donations to fight the pandemic

Support in the production of low-cost respirators

3737

Under the management of human resources, the Bradesco Corporate University, Unibrad, has as its mission: promotingeducation for professional excellence and social mobility, and becoming a reference in skills training and leadership, strengthening the brand’s value and social commitment for the continuity of Bradesco’s business.

• Present in in-person hubs in the country

• Online platform with more than 2 thousand learning solutions

• Recognized nationally and internationally - Global CCU, Cubic Awards, and Micropower

• People Office area with a fundamental role to redesign and improve employee experience, collaborating for a personalized experience

NEW LEARNING SOLUTIONS

+ 184 thousand views* on the UniBrad website, which offers free educational content.

+ 545 thousand* participations in learning

solutions.

UnibradEducation, inclusion, and democratization of knowledge

• Solutions focused on Mental Health – lectures, courses, live streams to share tips and experiences related to behavior, signs and symptoms of mental illness, quality of sleep, healthy eating, and physical activity.

• InvestFlix Companies and Business – to enhance and deepen strategic and technical knowledge about investments and financial markets.

• Diversity Growing in Differences – raising awareness, educating, and showing the power of diversity and its impact on people, in business, and in the community, encouraging an environment of living together better with differences.

• Onboarding – learning pathway for new employees, with customized solutions for integration and presentation of the Bradesco culture.

* In 1H21

3838

Based on the belief in education as a key factor for life improvement, Fundação Bradesco has been operating for 64 years

COMMITMENT TO THE FUTURE

in investments planned for 2021

R$ 798.9 MN

students to benefit, of which about 90% come from local

communities

+ 83k

young people have benefited from the Jovem Aprendiz program since

2004

+ 4k

distance learning students expected through Escola Virtual (Virtual School)

+ 3.5 MN

basic education students – including high school-level technical vocational education

+ 41k

??

??

We strive for comprehensive education of students to provide opportunities for

a better future, encouraging the realization of dreams and the ability to

write their own life story.

40schools throughout Brazil

Fundação BradescoThe largest private socio-educational program in the country

39

Sustainability at BradescoRated mostly above average in major ESG indices and ratings

Average performance

0

A+C+CDD-

AA AAABBBCCC AAA

2.9 3.2 50 5

40+ 24.330+ 0

0 6344 56 100

10075 92

0 10039 87 89

D AA- AC

As Sustainalytics refers to a risk score, the closer to 0, the better.

Benchmark

Ref. June 2021

40

Added value to society

14.4%

27.1%

23.7%

32.9%

1.9%

Governmentcontribution

Return on third-party capital (rentals)

Profit reinvestment

Work compensation

Dividends / IoC(paid / provisioned)

R$16.6Billion

distributed in 2Q21

41

Guidance

DisclosedGuidance

2021

Actual1H21

ReviewedGuidance

2021

Expanded Loan Portfolio 9% to 13% 9.9% 9% to 13%

Client Portion 2% to 6% 2.2% 2% to 6%

Fee and Commission income 1% to 5% 3.6% 1% to 5%

Operating Expenses(Personnel + Administrative + Others)

-5% to -1% -4.4% -5% to -1%

Income from Insurance, Pension Plans and Capitalization Bond (includes operating financial income)1 2% to 6% -29.8% -15% to -20%

Expanded ALL - R$ Billion R$ 14.0 to R$ 17.0 R$ 7.4 R$ 14.0 to R$ 17.0

1- Billing projections with growth between 8% and 10%.

42

12.6 12.613.1

1.00.7 0.3

(0.5)

1.113.6 14.1

Mar-21 Net Income

2Q21

Prudential Adjustments

Effects

Interest on

Shareholders' Equity

Jun-21

Common Equity Additional Capital

116.1%

%

8.625 Tier I

7.125 CommonEquity

Limits 20211

Variation %

Capital and Liquidity

Basel Ratio%

Regulatory Capital and RWA

Changes in Tier I Ratio in the Quarter

Liquidity CoverageRatio (LCR)

Net Stable Funding Ratio (NSFR)

1-Refer to the required minimums, in accordance with Resolution No. 4,193/13, added to the additional capital contributions established by Circulars No. 3,768/15 and No. 3,769/15.

R$ million Jun/21Jun/21 x

Mar/21

Jun/21 x

Jun/20

Regulatory Capital 141,108 4.1 7.2

RWA 884,639 0.3 1.1

Credit Risk 799,070 0.2 1.6

Operational Risk 66,908 0.0 5.0

Market Risk 18,661 6.3 (25.3)

156.0%

11.5 11.8 12.7 12.6 13.1

15.0 15.1 15.8 15.4 16.0

12.5 12.9 13.8 13.6 14.1

1.1 1.11.1 1.0 1.1

Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

Total Ratio Common Equity Additional Capital (Level I)

43

In 2020, net payout was limited to 30% as per

Central Bank Resolution nº 4,820/20.

Dividends and Interest on Shareholders’ EquityR$ Million

In 2021, a share buyback program of up to 1% of total outstanding shares

was instituted.

Gross Payout | Dividends and Interest on EquityHistorical distributions above the minimum established in the bylaws

(1) In 12M19, it considers R$8 billion of extraordinary dividends paid on October 23, 2019; and (2) Calculated on the basis of the book net income after adjustment on legal reserves. Note: In July 2021, the payment was made of interest on shareholders’ equity to intermediaries, related to the first half of 2021, to the sum of R$5.0 billion.

5,0556,035

6,976 7,204 7,299

15,863

5,548 5,992

35.3%37.0%

48.7%51.7%

40.3%

73.9%

34.8%

52.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

-

5,000

10,000

15,000

20,000

25,000

30,000

2014 2015 2016 2017 2018 2019 2020 2Q21

Dividends/Interest on Shareholders' Equity (1) Gross Payout (2)

44

1Reference date: June 20212Cidade de Deus, NCF, Nova Cidade de Deus, and Fundação Bradesco3Brazilian Investors

Average Daily Trading Volume*R$ Million

Shareholders’ Profile¹

Investors and TradingGrowing volume of trades

Shareholder

Base

% of Total

Shareholders

% of

Common

Shares

% of

Preferred

Shares

% of Total

Shares

- Controlling Shareholders2 4 0.0% 71.1% 2.3% 36.8%

- Minority Shareholders 741,530 100.0% 28.9% 97.7% 63.2%

- Individuals3 704,229 95.0% 11.0% 27.7% 19.3%

- Institutional3 35,956 4.8% 6.9% 9.1% 8.0%

- Foreign Investors 1,345 0.2% 11.0% 60.9% 35.9%

Total 741,534 100.0% 100.0% 100.0% 100.0%RECOMMENDATION OF

MARKET ANALYSTS

BBDC4

100%

Buy

CONSENSUS

(R$ million) 2021

Bloomberg 25,795

Refinitiv Eikon 26,355

Sell Side 26,114

Buy Side 26,873

155 193 233 292 326 320 352 354 522734 1,089 1,240

315 312 278 239 296 327 352330

406489

497693470 505 511 531 622 647 704

684928

1,223

1,5861,933

-1000

0

1000

2000

3000

0

500

1000

1500

2000

2500

3000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 1Q21 2Q21

Brazil U.S.A Total*Source: Economática

45

111.6 107.2132.2 128.4

146.0

100.4

161.4

201.3

243.6

283.2

227.7212.1

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Last*

+90%Ibov variation: +76%

*Last: 8/4/2021. Source: Refinitiv Eikon.

Market CapR$ Billion

MULTIPLE P/BV

2.3x 1.9x 1.9x 1.8x 1.8x 1.1x 1.6x 1.8x 2.0x 2.1x 1.6x 1.4x

MULTIPLE P/E

11.2x 9.6x 11.4x 10.5x 9.5x 5.6X 9.4x 10.5x 11.3x 10.4x 11.7x 8.6x

ROE (%)

22.2 21.3 19.2 18.0 20.1 20.5 17.6 18.1 19.0 20.6 14.8 17.6

Market Cap & MultiplexA company of value and high profitability over time

46

FITCH RATINGS

International Scale National Scale

Viability Support Domestic Currency Foreign Currency Domestic Currency

bb 4Long-term Short-term Long-term Short-term Long-term Short-term

BB B BB B AAA(bra) F1+(bra)

MOODY'S INVESTORS SERVICE(1)

Global Scale National Scale

Domestic Currency

Counterparty

Foreign Currency

Counterparty

Deposits -

Domestic Currency

Foreign Currency

DepositDomestic Currency

Long-term Short-term Long-term Short-term Long-term Short-term Long-term Short-term Long-term Short-term

Ba1 NP Ba1 NP Ba2 NP Ba2 NP AAA.br ML A-1.br

S&P GLOBAL(1) AUSTIN RATING

Global Scale - Issuer Credit Rating National Scale National Scale

Foreign Currency Domestic Currency Issuer Credit Rating

Long-term Short-term Long-term Short-term Long-term Short-term Long-term Short-term

BB- B BB- B brAAA brA-1+ brAAA brA-1

Main Credit RatingsSoundness and reliability

(1) Due to the change in methodology in June 2021, the national scale ratings were changed from "Aa1.br" and "BR-1" to "AAA.br"and "ML A-1.br".

47

Our Business

4848

BRADESCO SEGUROS

Main segments and businesses

48

BRAM

REAL ESTATE

CARDS

VEHICLES

PAYROLL-DEDUCTIBLE LOAN

ÁGORA

NEXT

BITZ

BBI

49

12th

largest economy in the world

18th

largest insurance market

in the world¹

0.9%share of global

premiums¹

²PREMIUMS EARNED / NOMINAL GDP

1.3 1.3 1.4 1.3

2.1 2.12.7

4.44.8 5.0

5.4 5.5 5.76.1

6.4 6.5 6.4 6.6 6.7

90 91 92 93 94 97 2000 2005 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Brazilian Insurance MarketGrowing revenue volume and share of GDP

¹ Source: Swiss Re / ² Source: Cnseg (R$ in premiums divided by GDP)

BRADESCO SEGUROS

50

¹ Percent of economically active population² Percent of total Active age population³ Percent of total population

INSURANCE PENETRATIONMillion

HEALTH PLAN

BENEFICIARIES

ADDITIONAL PENSION

PLAN CONTRACTS

25%3

48.1

18%2

30.0PARTICIPANTS

IN LIFE

15%

11.0INSURED

HOMES

14%3

27.7DENTAL PLAN

BENEFICIARIES

17%¹

17.8

31%

18.0INSURED

VEHICLES

Brazilian Insurance MarketOpportunities to enhance penetration

BRADESCO SEGUROS

51

Ranking 2021 Premiums Earned (R$ million) Share (%)

1st 32,595 22.9

2nd 23,773 16.7

3rd 15,842 11.1

4th 9,628 6.8

5th 7,258 5.1

6th 6,901 4.9

7th 6,812 4.8

8th 4,077 2.9

Others 35,328 24.8

Total 142,214 100,0

May 2021

Brazilian Insurance MarketLeading group in the Brazilian market

BRADESCO SEGUROS

52

50.01%

40.0%

22.5%

50.0%

100.0%

Insurance Group Structure Coverage of the main lines and groups

*IBR Brasil RE: Discontinued company. Last matchin March 2020BRADESCO SEGUROS

53

*Market share by Revenue** considering Insurers and OperatorsSource: Susep/ANS Reference date: May 2021

Market Share* Prominent position in the main lines and groups

BRADESCO SEGUROS

Market Share Ranking

Pension Plans 21.0%3rd

Life 19.0%1st

Health** 12.5% 1st

Capitalization 23.1% 1st

Bonds

Auto 11.9% 3nd

Total 22.9% 1st

54

Insurance Group - Selected dataResumption of Written Premiums

BRADESCO SEGUROS

(1)Premiums Earned from Insurance, Pension Plan Contribution and Capitalization Bond Income- In the first half of 2020, additional provisions were made in the sum of R$1,108 million, which were classified as supplementary provisions in the line of Other Income/Operating

R$ million

Variation%

2Q21 1H212Q21x1Q

21

2Q21x

2Q20

1H21x

1H20

Written Premiuns

Life and Pension Plans 9,171 18,365 (0.3) 28.3 13.3

Health 7,784 15,396 2.3 13.3 9.8

Auto / P&C 1,540 2,924 11.3 24.0 15.1

Capitalization Bonds 1,379 2,718 3.0 14.4 2.0

Total 19,874 39,403 1.8 20.7 11.2

Premiums Earned 1 11,642 23,235 0.4 12.7 6.9

Selected data

Total Assets 341,613 341,613 1.0 4.4 1.0

Financial Assets 321,125 321,125 1.0 4.0 1.0

Technical Provisions 288,364 288,364 1.1 4.9 1.1

Shareholders` Equity 36,486 36,486 1.0 (7.8) 1.0

55

Income from Insurance, Pension Plans and Capitalization BondsImpacted by events related to the pandemic

BRADESCO SEGUROS

2,065 2,034 2,347 2,1842,947

2,122

838 1,720

887

361

782

701

1,129

1,848

1,529 1,4391,533

747

831 1,009

1,443

1,417

687

3,594 3,4733,900

2,931

4,1393,913

2,982

4,266

3,422

2Q19 3Q 4Q 1Q20 2Q 3Q 4Q 1Q21 2Q

Operating Income Sinistros Avisados Covid-19 Financial Result (*) Com Efeito Covid-19

R$ million

3,778(*)3,131(*)

2,281(*)

3,137(*)

1,574(*)

Claims Reported - Covid-19 (*) With the Effect of Covid-19

56

Insurance Consolidated Income StatementResumption in Premiums and Claims impacted by the pandemic

(1) In the first half of 2020, additional provisions were made to the amount of R$1,108 million, which were classified as supplementary provisions in the line of Other Income/Operating Expenses.

Variation%

R$ million 2Q21 1H212Q21

x 1Q21

2Q21

x 2Q20

1H21

x 1H20

Premiums Earned from Insurance, Pension Plan Contribution and Capitalization

Bond Income (1)11,642 23,235 0.4 12.7 6.9

Retained Claims (8,722) (16,630) 10.3 58.1 31.4

Capitalization Bond Withdrawals and Redemptions (1,225) (2,419) 2.6 13.3 1.5

Selling Expenses (808) (1,580) 4.7 3.3 1.5

Financial Results 687 2,104 (51.5) (17.3) 33.4

Income from Insurance, Pension Plans and Capitalization Bonds 1,574 4,711 (49,8) (58.3) (29.8)

Fee and Commission Income 441 883 (0.2) (2.0) (4.6)

Personnel Expenses (398) (808) (2.9) 7.0 4.8

Other Administrative Expenses (354) (682) 8.0 (0.2) (5.1)

Others(1) (184) (351) 10.4 (84.5) (81.2)

Operating Income 1,078 3,752 (59.7) (53.4) (12.3)

Non-Operating Income / Income Tax / Social Contribution / Non-controlling

interests in subsidiaries(423) (1,468) (59.6) (55.5) (16.6)

Recurring Net Income 655 2,284 (59.8) (51.8) (9.3)

BRADESCO SEGUROS

57

Technical Provision

Adjusted Net Income and ROER$ Million

Written Premiums

Technical Provision and Selected DataHealth, Life and Pension Plans impacted by Covid-19

Net Income

4,4065,289 5,551 5,534

6,3897,451

5,120

1,629655

23.7% 24.2% 23.0%

19.4%20.0%

23.5%

14.3%19.6%

7.8%

2014 2015 2016 2017 2018 2019 2020 1Q21 2Q21

Adjusted Net Income ROE

46%

8%7%

39% Life And Pension Plans

Auto/P&C/Others

Savings Bonds

Health

Variation %

R$ million 2Q21 1Q21 2Q202Q21

x 1Q21

2Q21

x 2Q20

Life and Pension Plans 260,483 257,899 250,168 1.0 4.1

Health 14,556 14,026 11,325 3.8 28.5

Auto / P&C 4,837 4,734 4,391 2.2 10.2

Capitalization Bonds 8,488 8,504 8,755 (0.2) (3.0)

Total 288,364 285,163 274,861 1.1 4.9

BRADESCO SEGUROS

R$ million

583 627

-161

341580

544

78

108

117

359

314

155

1,361

1,629

655

2Q20 1Q21 2Q21

Auto/P&C/Others Savings Bonds Health Total

58

¹Financial Assets and Technical Reserves. ²Does not consider DPVAT segment.

Other Information¹ – Bradesco SegurosHealth, Life and Pension Plans provisions are the Highlights

R$ Billion

Financial Assets

308.8318.0 321.1

Jun-20 Mar-21 Jun-21

BRADESCO SEGUROS

Technical Provision

274.9285.2 288.4

Jun-20 Mar-21 Jun-21

Health

11.3

14.0 14.6

Jun-20 Mar-21 Jun-21

Pension Plans and Life/VGBL

250.2 257.9 260.5

Jun-20 Mar-21 Jun-21

4.4 4.7 4.8

Jun-20 Mar-21 Jun-21

Auto/P&C² Capitalization Bonds

8.8 8.5 8.5

Jun-20 Mar-21 Jun-21

5959

BRADESCO SEGUROS

59

NEXT

BRAM

CARDS

VEHICLES

PAYROLL-DEDUCTIBLE LOAN

ÁGORA

BITZ

BBI

REAL ESTATE

Main segments and businesses

6060

100

72 69

2Q20 1Q21 2Q21

Cost of Serving (CTS)(Base 100)

100

192218

2Q20 1Q21 2Q21

Cards(Base 100)

100

210263

2Q20 1Q21 2Q21

Total Transaction

Volume(Base 100)

2.7

4.45.4

2Q20 1Q21 2Q21

Total Accounts (in million)

429

689

1,016

2Q20 1Q21 2Q21

Open Accounts (in thousands)

nextThe native digital bank

77%were not Bradesco

account holders

+137% +99%

68%between 18 and 34

years old

HIGHLIGHTS

MAIN INDICATORS

The total volume transacted grew 163% YoY -

demonstrating greater customer engagement

with the platform

The amount of cards transacted

increased 118% YoY – important

business indicator for next

The 31% YoY reduction

demonstrates efficiency gains in

our operation

ACCOUNTS

Member Get Member (MGM): We launched

INDICA Y INDICA, a program that offers

rewards to those who bring new customers,

boosting the base's growth and helping to

improve the platform’s satisfaction rate.

Jornada de Adesão: We made

improvements that simplified the account

opening process. Today, more than 70%

of accounts are opened within 24 hours

ShopFácil: We completed the integration

of ShopFácil, adding to next an important

source of revenue and a new vertical of

non-financial business.

Mimos: We closed the quarter with more

than 300 partner brands and over 1,000

offers. Large promotions intensified

engagement with the hub, such as the

Valentine's Day action and with the gamer

audience.

5.4 million customers, with more than

1 million new accounts in 2Q21

NEXT

6161

BRADESCO SEGUROS

61

BRAM

ÁGORA

NEXT

BITZ

BBI

CARDS

VEHICLES

PAYROLL-DEDUCTIBLE LOAN

REAL ESTATE

Main segments and businesses

6262

ACCUMULATED DOWNLOADS

Pix releaseGenerating 41% jump in the number of users with a balance in the wallet.42% of users have at least one registered Pix key.

Free payment account with a balance that yields 100% of the CDI rate and cashback

mechanics to encourage usage. Created for the more than 40 million unbanked

Brazilians.

Main growth drivers in the period:

BITZ

ACCUMULATED ACCOUNTS

1st advertising campaignNationwide dissemination via digital, merchandising, and film for broadcast TV and local radio.

Reality show sponsorshipTwo nationwide reality shows on Record TV from May to July:• Power Couple Brasil 5• Canta Comigo

Accounts created81% increase in number of clients in the quarter.

TPV (Total Payment Value)43.5% increase in volume transacted.

NPS12.8% increase reaching the NPS of 44.

Operational results

BitzThe digital wallet created with a comprehensive ecosystem

7218

592

1,067

1,418

3QT20 4Q20 1Q21 2Q21 Aug21*

+33%

10332

853

1,546

2,051

3Q20 4Q20 1Q21 2Q21 Aug21*

+33%

In thousands

In thousands

* In Aug 11th, 2021

6363

BRADESCO SEGUROS

63

BRAM

ÁGORA

NEXT

BITZ

BBI

CARDS

VEHICLES

PAYROLL-DEDUCTIBLE LOAN

REAL ESTATE

Main segments and businesses

6464

JUN 2020

MAR 2021

JUN 2021

CLIENT BASEFUNDING

Vision: Volume under custody - billion

449 kclients

632 kclients

673 kclients

+49.9% y/y

+6.5% q/q

R$50.6

R$63.3

R$72.2

+42.7% y/y

+14.1% q/q

64

Open platform of investment products for account holders and non-account holders

Present in Bradesco and

next Apps

Advice to clients through investment specialists

ÁGORA

ÁgoraComplete and digital experience, with exclusive products and services

NETFUNDINGR$ Million

3,828

6,930

1H20 1H21

+81%

6565

BRADESCO SEGUROS

65

BRAM

ÁGORA

NEXT

BITZ

BBI

CARDS

VEHICLES

PAYROLL-DEDUCTIBLE LOAN

REAL ESTATE

Main segments and businesses

6666

Highest international credit risk classification

Moody’s Investors Service

Highest international risk classification

Standard & Poor’s

Incorporation of environmental, social and

governance issues into the decision-making process

Excellent Rating Highest international rating in investment

management

06/30/2021

INSTITUTIONAMOUNT¹

(R$ Million)

1 BB 1,283,840

2 ITAÚ-UNIBANCO 779,290

3 BRADESCO 541,768

4 CAIXA 421,715

5 SANTANDER 297,288

6 BTG PACTUAL 211,796

7 BRL DTVM 141,842

8 XP ASSET MANAGEMENT 119,472

9 CREDIT SUISSE 107,667

10 SAFRA 107,084

R$ 541.77 BILLION (US$ 108.31 BILLION2)

in assets under management

Note: (1) Domestic Market, ANBIMA Ranking of Management;(2) R$5.0022: US$ 1.00 on 06/30/2021 (Source: Brazilian Central Bank).

BRAM – Bradesco Asset Management Offering complete solutions

BRAM

6767

BRADESCO SEGUROS

67

BRAM

ÁGORA

NEXT

BITZ

BBI

CARDS

VEHICLES

PAYROLL-DEDUCTIBLE LOAN

REAL ESTATE

Main segments and businesses

68

# of transactions US$ million

ECM1 ECM1

US$ millionInternational DCM3

M&A2

US$ millionLocaL DCM4

# of transactionsProject Finance5

31

37 37

BBI BTG Pactual Itaú BBA

16,659

12,00010,350

BBI Santander Itaú BBA

30,359 30,881

15,922

BBI Itaú BBA BTG

82

48

28

Santander BBI Sumitomo

3,052 2,997

2,728

BBI Itaú BBA Morgan Stanley

22,00424,731

18,904

BBI BTG Pactual JP Morgan

BBI

Bradesco BBIOutstanding performance and presence in major transactions

US$ million

Source: Thomson Reuters; Dealogic; ANBIMA. Note: (1) Volume and number of transactions as of Dec. 2020 (2) Official Mergermarket ranking of M&A announced transactions, 2020

(3) Transaction volume as of 2019(4) Transaction volume (origination) YTD as of Nov. 2020(5) Number of transactions as of 2019

6969

BRADESCO SEGUROS

69

BRAM

PAYROLL-DEDUCTIBLE LOAN

ÁGORA

NEXT

BITZ

BBI

CARDS

VEHICLES

REAL ESTATE

Main segments and businesses

70

22.0% 20.8% 20.8% 21.3% 22.7% 21.8%23.9% 23.9%4.5% 5.1% 6.2%

7.9%9.7%

10.9%

10.7% 10.7%

16.3% 16.6% 15.5%14.3%

13.8%12.8%

12.5% 12.4%

21.3%21.8% 22.2%

20.7%17.7%

16.5%

15.9% 15.7%

12.0%12.7%

13.5%14.2%

15.1%

16.6%

15.8% 16.1%

23.8%

23.0%21.8%

21.7%

21.1%

21.4%

21.2%21.3%

247.8

273.0 287.8

310.7

337.4

379.2

440.6 452.9

Dec-14 Dec-15 Dec-16 Dec-17 Dec-18 Dec-19 Dec-20 Mar-21

Others Bank I Bank II Bank III BRADESCO Bank IV

PAYROLL-DEDUCTIBLE LOAN

Payroll-Deductible Loans / GDP Market Share – BalanceR$ Billion

Source: IF Data - BCBReference date : June 2021Source: DEPEC (Bradesco)

Payroll-Deductible Loan – BrazilSteady market growth

Dec-10 Dec-20

3.6%

6.0%

71

Bradesco – Portfolio¹ Market – Portfolio²Bradesco – Distribution¹

Market share3

20.3%

13.3%

14.1%

INSS

Private Sector

Public Sector

16.4%

Total

11.5 MILLION

RETIREES PAID THROUGH BRADESCO

¹ Source: Bradesco / In June 2021² Source: BCB / In June 2021³ Base date: June 2021

Correspondent

Banks / Others

14%

Branch

Network

86%

Payroll-Deductible Loans - PortfolioStrong positioning in retirees and pensioners

PAYROLL-DEDUCTIBLE LOAN

Social

Security

39%

Public

Sector

55%

Private

Sector

6%

Social Security

48%

Public

Sector 47%

Private

Sector 5%

7272

BRADESCO SEGUROS

72

BRAM

PAYROLL-DEDUCTIBLE LOAN

ÁGORA

NEXT

BITZ

BBI

CARDS

VEHICLES

REAL ESTATE

Main segments and businesses

73

1.5 1.8 2.23.0

4.05.2

6.37.6

9.0 9.5 9.7 9.5 9.2 9.29.8 10.2

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021*

Brazil%

World

%

REAL ESTATE

Real Estate | Financing and Mortgages/GDPExpansion opportunities

Sources: United Kingdom, Portugal, Poland, Hungary, Czech Republic, Bulgaria, Turkey, Russia 2014; Argentina 2015; USA, Spain, France, Germany, South Africa, Chile, Italy, Mexico, Colombia2016; Brazil 2020. Sources: European Mortgage Federation, Bacen, Hypostat, Febraban, HFN, Abecip and Ecowin.*Depec estimates

75.0 77.0

59.248.0

42.0 36.0 30.0 24.022.0 20.0 16.6 16.6

11.0 9.8 8.3 6.5 6.0 1.9

UK

US

A

Po

rtu

ga

l

Sp

ain

Fra

nc

e

Ge

rma

ny

So

uth

Afr

ica

Ch

ile

Ita

ly

Po

lan

d

Hu

ng

ary

Cz

ec

h R

ep

.

Me

xic

o

Bra

zil

Bu

lga

ria

Tu

rke

y

Co

lom

bia

Arg

en

tin

a

74

HOUSING DEFICIT: 7.7 MILLION HOMES

Source: ABECIP

ANNUAL ORIGINATIONR$ Million

109,178 112,854

75,578

46,610 43,149

57,387

78,702

123,974

97,047

2013 2014 2015 2016 2017 2018 2019 2020 Jul-21

REAL ESTATE

Real Estate – BrazilRobust growth in originations

75

7.8% 8.6% 8.9% 8.6% 8.5% 7.8% 6.6% 6.2% 6.0%6.3% 6.4% 6.0% 5.6% 5.7% 5.9% 6.2% 6.4% 6.5%7.9%

8.0% 8.0% 7.7% 7.5% 7.5% 8.1% 8.8% 9.5%9.0%9.4% 10.0% 9.6% 9.4% 9.1%

10.5% 10.8% 10.9%

68.3%

67.2%67.0% 69.1% 68.9% 69.2%

68.9%68.3%

67.4%

0.7%

0.4%

0.1%0.4%

497,847

572,313605,736

624,834645,355

672,073

741,479759,339

786,121

Dec14 Dec15 Dec16 Dec17 Dec18 Dec19 Dec20 Mar21 Jun21

Bank I Bank II Bank III Bradesco Bank IV Others

Source – BCB, banks’ balance sheets, and ABECIP

BalanceR$ Millions

REAL ESTATE

Mortgage - Brazil Market share growth

76

ORIGINATION

Individuals

AVERAGE TERM:321 MONTHS

AVERAGE TICKET:

PROPERTY ASSESSMENT

R$ 522 Thousand

FINANCING

R$ 315 Thousand

LOAN TO VALUE

60.4 %

LOAN TO VALUE

(INVENTORY)

50.8 %Reference date: June 2021

REAL ESTATE

Mortgage – Retail | BradescoGreater safety margins in originations

77

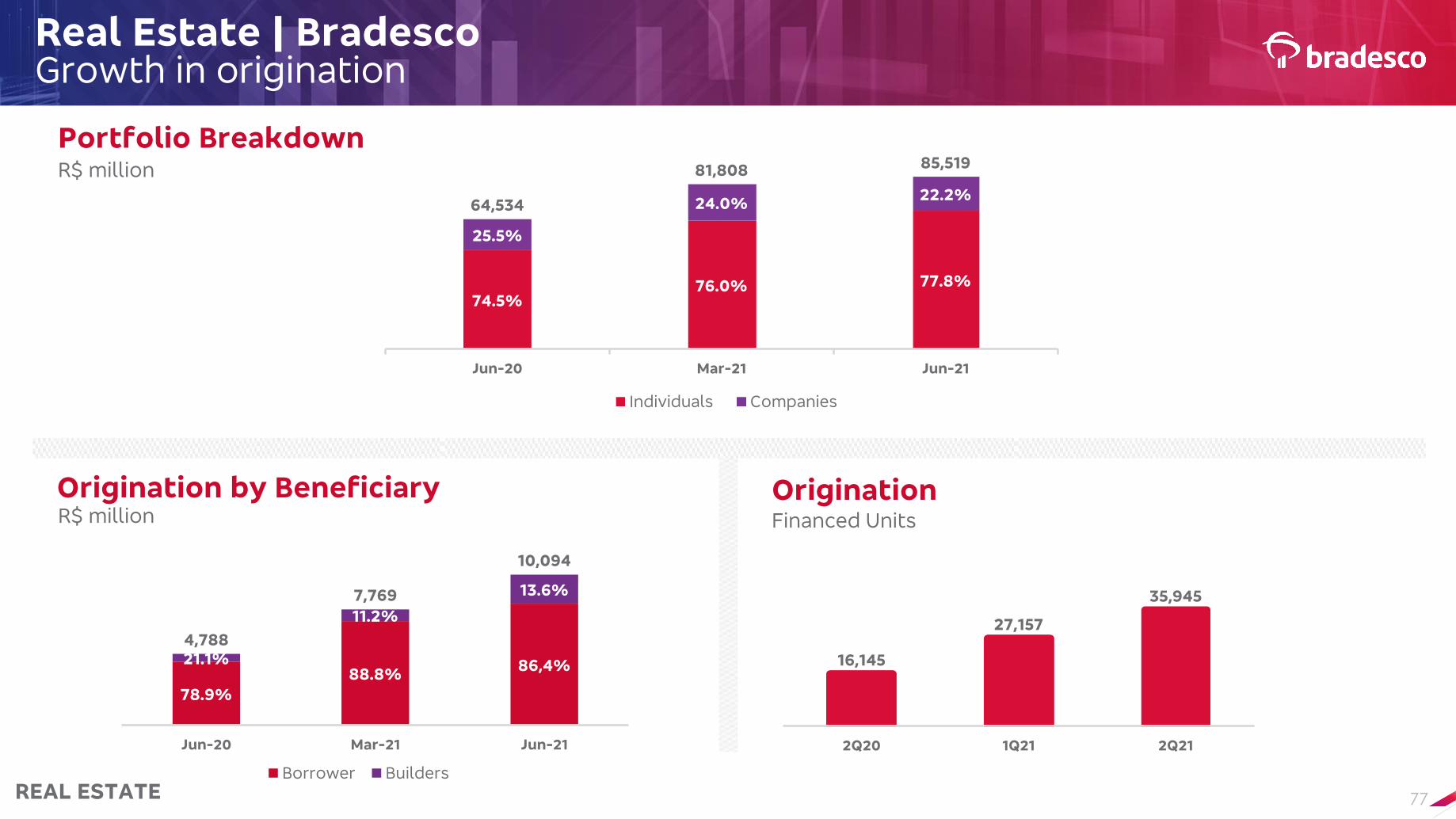

Portfolio Breakdown

Origination by Beneficiary Origination

R$ million

R$ million Financed Units

REAL ESTATE

Real Estate | Bradesco Growth in origination

74.5%76.0% 77.8%

25.5%

24.0%22.2%

64,534

81,808 85,519

Jun-20 Mar-21 Jun-21

Individuals Companies

78.9%

88.8%86,4%21.1%

11.2%

13.6%

4,788

7,769

10,094

-

2,000

4,000

6,000

8,000

10,000

12,000

Jun-20 Mar-21 Jun-21

Borrower Builders

16,145

27,157

35,945

2Q20 1Q21 2Q21

7878

BRADESCO SEGUROS

78

BRAM

PAYROLL-DEDUCTIBLE LOAN

ÁGORA

NEXT

BITZ

BBI

CARDS

VEHICLES

REAL ESTATE

Main segments and businesses

79

Evolution of billed in means ofpayment – Credit and Debit

(2Q21 X 1Q21)

Cards Market | Transaction VolumeEvolutionary resumption in billing

VOLUME BILLED IN MEANS OF PAYMENT – CREDIT AND DEBIT

Source: Abecs

CARDS

400.7

506.3

609.6558.3

609.2

2Q20 3Q20 4Q20 1Q21 2Q21

R$ Billion

+9.1%

+52.0%

9.1%

7.1 billion of transactions carried outwith cards in the 2Q21

Source: AbecsIn Aug/21

R$ 2.5

trillion

R$523

billion

R$ 2.0

trillion

2000 2021E2010

80

BRAND

LOYALTY

ACQUIRER

FOOD VOUCHER

PAYMENT TAG

ISSUER

CLIENT(Tolls, parking and others)

CARDS

Bradesco Cards PositioningOperating throughout the value chain

CLIENT

81

Distribution channelsWide distribution capacity - ominichannel

Digital Channels – App and Web 20% of total sales

Greatest Market Capillarity:+ 30 physical and digital channels with national presence+ 25 thousand points of sales and branches network

Bradesco channels synergy: Ágora, Losango, Bradesco Financiamentos, Seguros

Experience for the Customers:Card available for use immediately after

approval, no need to wait the physical card to arrive home

Integration Technology with Retail Partnerships:

best experience according to each customer's profile

Bradesco Partner Channels:Bradescard and Bradesco Expresso

banking correspondents

CARDS

82

Products portfolioC

OM

PA

NIE

S

IND

IVID

UA

LS

Complete and for everyone

BNDES TRANSPORTS PURCHASES VIRTUAL PAYROLL RETAILERS ACADEMIC COBRANDED

NIC

HE

S

Classic

Exclusive

Private Bank

Pri

me

Non-account holders

Large Corporate

Corporate

CorporateOne C

om

pa

nie

s a

nd

B

usin

ess

Multis & institutional

CARDS

83

Innovation and Services

P2P and P2M

AppBradesco

Virtual Card

BIAServices

QR Code

App BradescoCards

All forms of payment

Digital experience

CardTech - area dedicated to technological innovation entirely in agile methodology

Development of digital

applications, products and

services focused on the

better customer

experience

Focused on winning partnerships and projects for better value delivery to customers

Disney+ STAR+ with relevant

differential and integrated journey in

the bank's digital channels, with the

best payment experience in the market

Special offers in installment payments and

discounts with Apple when purchasing any

product

Complete self-service solution

Complete line of payments solutions with innovative products

CARDS

848484

Main segments and businesses

BRADESCO SEGUROS

BRAM

VEHICLES

ÁGORA

NEXT

BITZ

BBI

CARDS

PAYROLL-DEDUCTIBLE LOAN

REAL ESTATE

85

Inhabitants per Vehicle

Market Delinquency – Over 90 Days%

1Source: Brazilian Central Bank; 2 Considering only credit products with market interest rates; 3 Auto Loan (CDC) + Leasing

Credit in the Financial System (1)R$ Billion

Vehicle Financing – BrazilSlight portfolio growth and stable delinquency

Source: ANFAVEA (2021)

VEHICLES

4.9

3.53.2

1.7 1.7 1.61.2

4.8

3.4 3.2

1.7 1.7 1.61.2

Brazil Mexico Argentina Germany UK Japan USA

2014 2015

6.7 6.9

5.7 5.36.2 6.1

5.2 4.8 5.04.16.2

6.7

5.4

4.0 4.3 4.63.8

3.3 3.4 3.4

2011 2012 2013 2014 2015 2016 2017 2018 2019 jun-20

Total Credit - Individuals Auto Loan (CDC) & Leasing - Individuals

2,3682,711

3,017 3,230 3,118 3,105 3,265 3,4774,021 4,214

211 201 187 163 145 151 171 204 221 229

690 742 781 805 811 855 9541,112

1,232 1,320

2012 2013 2014 2015 2016 2017 2018 2019 2020 Jun21

Total Credit Outstanding Vehicles Financing - Individuals (3) Total Credit Individuals (2)

86

Loan book origination details

Source: Bradesco (Departamento de Empréstimos e Financiamentos1 – Customers portfolio – Jun’212 – Production R$ – Apr’21 – Jun’213 – Consider Individuals and Companies4 – Average

Indicators – 2Q21

CUSTOMERS¹ AVERAGE TERM²

AVERAGE TICKET²

AVERAGE PRODUCTION²

LOANBOOK3

392Thousand

47Months

~R$87 Thousand

~1,267 Million

Bradesco(Bank operation) ~23,584

Million

999 Thousand

44Months

~R$46Thousand

~1,430 Million

Bradesco Financiamentos (Dealer operation) ~25,439

Million

34%

36%

DOWNPAYMENT4

87

Main Indicators

Vehicle Financing - Bradesco Growth in the average loan and term

Average Term(Months)

Average Loan(R$ Thousand)

Considers CDC/Leasing (new cars, used cars, motorcycles and heavy vehicles)Source: Bradesco

VEHICLES

37.1 37.1 37.1 37.1 34.8 38.749.7

57.160.5

80.8

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

41 41 40 39 38 40 42 45 46 47

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

88

Main Indicators

Considers CDC/Leasing (new cars, used cars, motorcycles and heavy vehicles)Source: Bradesco Financiamentos

VEHICLES

Average Loan(R$ Thousand)

Average Term(Months)

Vehicle Financing - Bradesco FinanciamentosGrowth in average loan and term

43

4039 39

3839

40

42

4344

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

20.4 21.923.9 24.6 24.1

26.4 28.531.9 34.6

43.5

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

89

HIGHLIGHTS OF THE OPERATION

FINANCED ASSETS

Vehicles

Motorcycles

FINANCING OF VEHICLESthrough the branch network, digital

channels, or network of banking correspondents (14+ thousand)

Trucks & Road Implements

MachineryAgricultural

Civil ConstructionImplements

Boosted FinancingFinancing of Accessories and Services included in the vehicle installment.

Bradesco SegurosLargest insurer in Brazil and in Latin America.

LiveloLargest and most complete market place platform in the rewards sector.

VeloeInstant payments at toll booths, malls and parking lots.

Specialist inTransportation and AgricultureCustomer service structure dedicated

to the segment of heavy-duty vehicles (trucks, machinery and implements).

MAIN PARTNERS

White Label

In addition to Jeep brand vehicles, the Jeep Bank program also covers the brands Dodge, Chrysler, and RAM.

We are the financing providers for world-class automakers.

VEHICLES

Vehicle Financing Diversified offers

90

2nd QUARTER RESULTS 2021

91

Tier I Capital

1.6 p.p. y/y0.5 p.p. q/q

ROAEAccumulated

6.4 p.p. y/y-0.5 p.p. q/q

9.9% y/y3.0% q/q

Expanded Loan Portfolio

Financial Highlights 2Q21

Operating Efficiency Ratio (ER)

-2.1 p.p. y/y0.4 p.p. q/q

Recurring Net Income

63.2% y/y-3.0% q/q

(accumulated 12 months)

Interest on Shareholders’ Equity

Payout in 1H21 of 52%

92

Operational Evolution

3.6% 1H21/1H20

Fee and Commission Income

-4.4%1H21/1H20

Operating Expenses

Variation %

-52.6%1H21/1H20

Expanded ALL

R$ million 2Q21 1H212Q21

x 1Q21

2Q21

x 2Q20

1H21

x 1H20

Net Interest Income 15,738 31,316 1.0 (5.7) 0.4

Expanded ALL (3,487) (7,394) (10.7) (60.8) (52.6)

Gross Income from Financial Intermediation 12,251 23,922 5.0 57.2 53.5

Income from Insurance, Pension Plans and

Capitalization Bonds 1,574 4,711 (49.8) (58.3) (29.8)

Fee and Commission Income 8,412 16,479 4.3 10.3 3.6

Operating Expenses (10,990) (22,194) (1.9) (4.1) (4.4)

Tax Expenses+ Earnings (losses) in unconsolidated

subsidiaries(1,728) (3,631) (9.2) (15.1) (6.6)

Operating Income 9,519 19,287 (2.5) 66.9 73.7

Non-Operating Income + Income Tax + Non-

controlling interests in subsidiaries + Others(3,200) (6,453) (1.6) 74.8 85.7

Recurring Net Income 6,319 12,834 (3.0) 63.2 68.3

Income Origin(Financial and Insurance Areas)

72%

65%

75%90%

28%

35%

25% 10%

6,462

3,873

6,5156,319

2Q19 2Q20 1Q21 2Q21

Financial Insurance

Comparison 1H21 x 1H19

R$ million 1H19 1H211H21

x 1H19

Total Revenues 67,080 71,030 5.9%

Total Expenses 23,932 22,194 (7.3)%

Efficiency Ratio 49.4% 45.7% (3.7) p.p.

EBT 17,196 19,287 7.7%

93

R$35.0 bn4.5% y/y

Client Funds1

Total Funding and Loan/FundingR$ Million

Funding & Loans

4.1% y/y

Total Funding

Growth of Bacen

Portfolio + Debentures in

1H21

1- Client Funds Net of Reserve Requirements.

559.2 581.6 584.4

135.6 133.7 138.8

694.8 715.3 723.2

83.3%87.5% 89.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

2Q20 1Q21 2Q21

Borrowing, Onlending and Other obligations Client Funds Net of Reserve Requirements Loan/Funding

94

R$ million Jun/21Jun/21

x Mar/21

Jun/21

x Jun/20Jun/21

Companies 440,833 1.4 3.7 60.7

Large corporates 292,995 (0.2) (5.6) 40.3

Micro, Small and Medium-Sized Enterprises 147,838 4.6 28.7 20.4

Individuals 285,620 5.7 21.0 39.3

Payroll-deductible Loans 78,425 7.7 19.8 10.8

Real Estate Financing 68,668 7.7 40.0 9.5

Credit Cards 43,170 6.5 23.1 5.9

CDC/Vehicles Financing 30,102 1.9 6.4 4.1

Personal Loans 31,767 2.9 8.9 4.4

Other Products 33,488 2.4 15.6 4.6

Total Expanded Loan Portfolio 726,453 3.0 9.9 100.0

Without exchange variation 4.0 10.6

30% y/y

Individuals

??

28.7% y/y

SMEs

25% y/y

38% y/y

Variation % Total %

Expanded Loan Portfolio

40.0% y/y

Real Estate Financing

19.8% y/y

Payroll-deductible Loans

Loan Originationper business day

100106

130

2Q20 1Q21 2Q21

100 99

125

2Q20 1Q21 2Q21

100

119

138

2Q20 1Q21 2Q21

Companies

Total

95

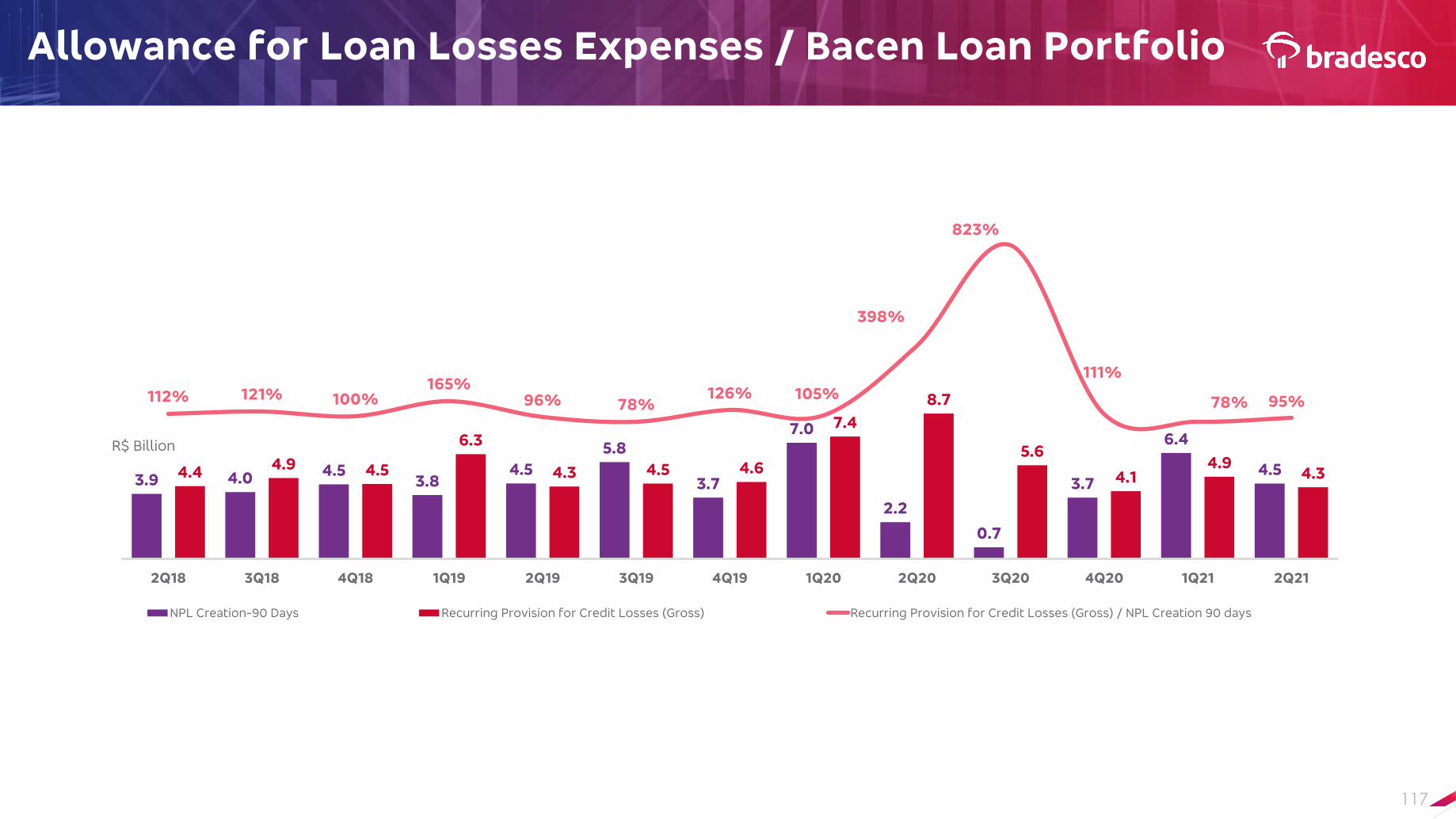

Coverage Ratio – Over 90 days

Coverage Ratio – over 90 days + reneg.

Provision for Credit Risk

Expanded ALL (Expenses)R$ Billion

Allowance For Loan Losses*R$ Billion

*ALL balance includes Specific, Generic and Complementary portions.

36.9 36.1 36.840.5 43.2 44.9 45.3 46.0 44.4

8.6% 8.2% 8.1% 8.5%9.0% 9.2% 8.9% 8.7%

8.1%

2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21

ALL Balance ALL Balance / Bacen Portfolio

267%

226%245%

228%

299%

398% 403%

350%325%

Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

122% 116% 120% 121% 124% 121% 118% 120% 117%

Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

3.5 3.3 4.0

6.7

8.9

5.64.6 3.9 3.5

2.4% 2.2% 2.6%

4.1%

5.4%

3.4%2.7%

2.2% 1.9%

2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21

Expanded ALL Expanded ALL / Expanded Portfolio - Annualized Rate

95

96

15 to 90 Days%

Gross ALL Expenses X NPL Creation >90 DaysR$ billion

Delinquency Ratio

Over 90 Days%

2.7

4.8

3.43.9

4.2 4.14.5

6.0

8.6

6.6

4.2 3.7

1.9

2.6 2.6

6.1

7.4

5.56.1 6.2

5.0 4.75.5

6.9

5.54.4 4.4

3.13.5 3.4

0.50.9

0.4 0.4 0.3 0.6 0.8 0.51.2

1.91.5

0.8

0.70.4 0.4

3.4

4.9

3.6 3.9

4.13.5 3.5

4.1

5.5

4.7

3.53.3 2.2

2.5 2.5

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Dec-18 Dec-19 Dec-20 Mar-21 Jun-21

Micro, Small and Medium-Sized Enterprises Individuals Large Corporates Total

4.0 4.13.3

4.1 4.1 4.3 4.3

6.0 5.9 6.1

4.3 4.23.0

3.3

2.3

8.8

7.7

6.3 6.3 6.25.6

5.2

5.7 5.85.1

4.8 4.84.0

4.63.8

0.3 0.2 0.2 0.3 0.5 0.2 0.4 0.4

2.2

0.6 0.9 0.70.2 0.3 0.1

4.9 4.63.8

4.1 4.0 3.7 3.64.1

4.64.0

3.5 3.62.8

3.22.6

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Dec-18 Dec-19 Dec-20 Mar-21 Jun-21

Micro, Small and Medium-Sized Enterprises Individuals Large Corporates Total

4.5

2.2

6.4

4.54.3

8.7

4.94.3

96%

398%

78% 95%

2Q19 2Q20 1Q21 2Q21

NPL Creation - 90 days

Gross ALL Expense – Recurrent

Gross ALL Expense - Recurrent / NPL Creation 90 days

97

92% 91%Rating AA to C

R$ billionThe R$41.3 billion balance in June 2021 includes the following components:

On time – R$33.4 billion

In arrears – R$3.5 billion

Grace period – R$4.3 billion

68% 13 years

Extended Loan Portfolio

No delay history inthe 12 months prior to the pandemic

With real collateral

Average relationship time

Extensions Accounting Balance(Net of Amortizations)

* Delinquency ratio above 30 days calculated considering the balance of the expanded loan portfolio.

13.2 13.3 10.5 10.3 8.9

42.8 42.037.5

33.8 32.4

56.0 55.348.0

44.1 41.3

0.1

0.0%

1.1

0.2%

2.9

0.6%

3.9

0.7%3.5

0.6%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

Wholesale Mass Market Product In Arreas (over 30 days)

98

66%

Renegotiated Portfolio

of renegotiations in the quarter were less than 90 days in arrears

Allowance for Loan Losses/

Renegotiated Portfolio

Delinquency Ratio Over 90 Days

Renegotiated Portfolio/ Bacen Portfolio

R$ billionEvolution of Portfolio Balance

Large Corporate

16%

SMEs

32%

Individuals

52%

12.3 13.0 13.6 14.118.5

22.8 24.5 24.0 23.5

7.3 5.8 5.4 5.5

5.0

4.74.9 5.4 5.0

19.6 18.8 19.0 19.6

23.5

27.529.4 29.4 28.5

Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

Originated from portfolio in write-off Originated from active portfolio

66.4% 66.9% 66.8% 68.2% 61.7% 61.5% 63.8% 61.9%

Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

19.0% 17.4%20.8%

11.5%

5.9% 7.4%

14.4% 14.6%

Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

4.2% 4.2% 4.1%4.8%

5.6% 5.8% 5.6% 5.2%

Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21

99

Net Interest Income

1.0% q/q

Net Interest Income

1.9% q/q

Client NII2.5% q/q

Average Balance

R$ million

Total Net Interest Income

NII Clients Variation

R$ million

1- Relates to the result of operations made with assets (loans and other) and liabilities sensitive to spreads. The calculation of the result for assets sensitive to spreads considers the original rate of the deducted operations from the internal funding cost and the result for liabilities represents the difference between the cost of raising funds and the internal transfer rate of these funds; and 2- Composed of Asset and Liability Management (ALM), Trading and Working Capital.

R$ million 2Q21 1H212Q21

x 1Q21

2Q21

x 2Q20

1H21

x 1H20

%Total

2Q21

Net Interest Income 15,738 31,316 1.0 (5.7) 0.4 100.0

Client NII1 13,471 26,696 1.9 2.3 2.2 85.6

Average Balance 624,710 617,144 2.5 9.1 10.9

Average Rate 8.9% 8.9% (0.2) p.p. (0.6) p.p. (0.7) p.p.

Market NII2 2,267 4,620 (3.7) (35.6) (8.6) 14.4

Variation %

328

(484)

256145 13,471

13,225

13,163 13,225 13,471

3,521 2,353 2,267

16,68415,578 15,738

6.9%

6.0% 6.0%

9.5%9.1% 8.9%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

11.0%

2Q20 1Q21 2Q21

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Client NII Market NII NIM Total NIM Clients

100

3.6% 1H21/1H20 6.6% 1H21/1H20 1.1% 1H21/1H20

Variation %

Fee and Commission Income

Total Fee Income Card IncomeChecking Account

Total Clients OrganizationIn million

Other clients of the organizationIn million

R$ million 2Q21 1H212Q21

x 1Q21

2Q21

x 2Q20

1H21

x 1H20

% Total

2Q21

Card Income 2,744 5,383 4.0 16.7 6.6 32.6

Checking Account 2,000 3,943 2.9 4.1 1.1 23.8

Asset Management 828 1,625 3.9 1.7 (5.9) 9.8

Loan Operations 662 1,296 4.4 0.8 (6.0) 7.9

Collections and Payments 594 1,209 (3.4) (4.3) (5.5) 7.1

Consortium Management 540 1,053 5.3 23.0 13.3 6.4

Underwriting / Financial Advisory

Services390 645 52.9 68.1 52.1 4.6

Custody and Brokerage Services 351 709 (2.0) 15.8 9.2 4.2

Other 303 616 (3.2) 5.6 8.3 3.6

Total 8,412 16,479 4.3 10.3 3.6 100.0

Business Days 62 123 1 1 0

Bradesco Checking Account HoldersIn million

30.131.4 31.8

2Q20 1Q21 2Q21

39.4 39.3 39.4

2Q20 1Q21 2Q21

69.570.7 71.2

2Q20 1Q21 2Q21

101

40,835 40,920 41,584

2Q20 1Q21 2Q21

-4.4% 1H21/1H20 -2.2% 1H21/1H20 0.3% 1H21/1H20

Variation %