INSTITUTIONAL EQUITY RESEARCH Parag Milk Foods (PARAG...

32

INSTITUTIONAL EQUITY RESEARCH Page | 1 | PHILLIPCAPITAL INDIA RESEARCH Parag Milk Foods (PARAG IN) Moo-ving fast in the high-growth value-added dairy space INDIA | DAIRY | Initiating Coverage 27 September 2016 We initiate coverage on PARAG with a Buy rating and target price of Rs 350. Parag Milk Foods (PARAG) is a play on the high-growth value-added dairy products space. It has tremendous capability to innovate and create industry leading brands – in a short span, its brands ‘Go’ and ‘Gowardhan’ have become household names. Its focus on consistent product innovation and mix improvement will lead to sustained better margins, which coupled with high revenue growth would translate into sharp earnings growth. It has delivered strong 25% PAT CAGR in FY12-16, and we expect growth momentum to continue in FY17-20 (we see 30% CAGR). With capex cycle almost at completion and with capital utilizations set to improve, we estimate the free cash flows to improve substantially from FY18 onwards. Our key investment arguments: (1) PARAG’s sales will grow in mid-teens in the medium term led by high-margin value added products, (2) mix improvement and operating leverage will enhance margins, (3) return ratios will improve (medium term) with better capacity utilization, (4) will start generating strong free cash flows from FY18, and (5) current market valuation does not factor in strong growth expected in the medium term. PARAG will benefit from strong growth in the Indian dairy industry: This industry is poised to grow to Rs 9.4tn by 2020 from Rs 4.1tn in 2014 (15% CAGR), as per IMARC. Within this, the organised segment (20% value share) could see faster 20% CAGR. PARAG dominates high-margin categories (cheese, flavoured and UHT milk, flavoured yoghurts and others), which are poised to see >25% CAGR. We expect PARAG to deliver 14% sales CAGR in the medium term led by 20%+ growth in key value-added products. Gross margins to improve 50bps annually; EBITDA margins to edge towards 11% by FY20: PARAG’s gross margins should improve to 30.4% in FY20 from 28.4% in FY16, majorly led by mix improvement. We expect the share of skimmed milk powder to fall by 480bps during FY16-20 and share of high-margin value-added products to make up this fall. This, along with introduction of premium variants, would lead to a ~50bps gross-margin expansion every year. While operating expenses would stay high (as the company expands), we still expect EBITDA margins to move to 10.8% in FY20 from 9% in FY16. Return ratios to improve on better capacity utilization: As sales expand for the company in the medium term, we expect capacity utilization levels for packaged milk, UHT, ghee, and butter to improve from sub-50% levels – which in turn would improve fixed-asset turnover over the medium term and lead to an improvement in return ratios. We see RoE improving to 12.9% in FY20 from 8.3% in FY16 – a modest improvement, limited by the company’s need to invest on distribution for growth. Free cash flows will turn positive from FY18, as capex intensity will reduce: We believe the company would have sufficient capacity after its FY17/18 capex cycle, and would not need major capex for the succeeding five years. Fall in capex and stabilization in working-capital days (as sales expand) would lead to better cash flows. We see free cash flows turning positive from FY18 and rising substantially thereafter. Valuations in dairy industry: The stock of Parag Milk Foods, after rallying almost 50% since listing in May 2016, now trades at 24x our FY18 earnings (29x our FY18 recurring earnings). In comparison, its peers, Hatsun Agro/Heritage Foods/Prabhat Dairy/Kwality Dairy trade at 39/22/18/15 times our FY18 earnings. On EV/EBITDA, PARAG trades at 14 times our FY18 EBITDA vs. 14/11/7/9 times our FY18 EBITDA for the same peer-set. The PC FMCG universe (ex ITC), in comparison, currently trades at 40x one-year forward earnings. Initiate with BUY rating: We expect PARAG to deliver strong PAT growth (30% CAGR) during FY17-20 and value the stock at Rs 24 times our September 2018 earnings (30x our FY18 adjusted earnings – 1 PEG) at Rs 350. We initiate coverage on the stock with a BUY rating. BUY CMP RS 295 TARGET RS 350 (+18%) COMPANY DATA O/S SHARES (MN) : 84 MARKET CAP (RSBN) : 24.8 MARKET CAP (USDBN) : 0.4 52 - WK HI/LO (RS) : 357 / 897 LIQUIDITY 3M (USDMN) : 1.7 PAR VALUE (RS) : 10 SHARE HOLDING PATTERN, % Jun 16 PROMOTERS : 47.5 FII / NRI : 27.0 FI / MF : 4.3 NON PRO : 19.9 PUBLIC & OTHERS : 1.4 PRICE PERFORMANCE, % 1MTH 3MTH ABS -4.8 13.7 REL TO BSE -6.7 6.5 PRICE VS. SENSEX Source: Phillip Capital India Research KEY FINANCIALS Rs mn FY17 FY18E FY19E Net Sales 17,535 20,291 23,612 EBIDTA 1,696 2,072 2,532 Net Profit 795 1,031 1,334 EPS, Rs 9.5 12.3 15.9 PER, x 31.2 24.1 18.6 P/BV, x 3.4 3.0 2.6 ROE, % 10.8 12.3 13.7 Debt/Equity (%) 40.8 35.8 30.9 Source: PhillipCapital India Research Est. Jubil Jain (+ 9122 6667 9766) [email protected] Naveen Kulkarni (+ 9122 6667 9947) [email protected] 80 100 120 140 160 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Parag BSE Sensex

Transcript of INSTITUTIONAL EQUITY RESEARCH Parag Milk Foods (PARAG...

INSTITUTIONAL EQUITY RESEARCH

Page | 1 | PHILLIPCAPITAL INDIA RESEARCH

Parag Milk Foods (PARAG IN)

Moo-ving fast in the high-growth value-added dairy space

INDIA | DAIRY | Initiating Coverage

27 September 2016

We initiate coverage on PARAG with a Buy rating and target price of Rs 350.

Parag Milk Foods (PARAG) is a play on the high-growth value-added dairy products space. It has tremendous capability to innovate and create industry leading brands – in a short span, its brands ‘Go’ and ‘Gowardhan’ have become household names. Its focus on consistent product innovation and mix improvement will lead to sustained better margins, which coupled with high revenue growth would translate into sharp earnings growth. It has delivered strong 25% PAT CAGR in FY12-16, and we expect growth momentum to continue in FY17-20 (we see 30% CAGR). With capex cycle almost at completion and with capital utilizations set to improve, we estimate the free cash flows to improve substantially from FY18 onwards.

Our key investment arguments: (1) PARAG’s sales will grow in mid-teens in the medium term led by high-margin value added products, (2) mix improvement and operating leverage will enhance margins, (3) return ratios will improve (medium term) with better capacity utilization, (4) will start generating strong free cash flows from FY18, and (5) current market valuation does not factor in strong growth expected in the medium term.

PARAG will benefit from strong growth in the Indian dairy industry: This industry is poised to grow to Rs 9.4tn by 2020 from Rs 4.1tn in 2014 (15% CAGR), as per IMARC. Within this, the organised segment (20% value share) could see faster 20% CAGR. PARAG dominates high-margin categories (cheese, flavoured and UHT milk, flavoured yoghurts and others), which are poised to see >25% CAGR. We expect PARAG to deliver 14% sales CAGR in the medium term led by 20%+ growth in key value-added products.

Gross margins to improve 50bps annually; EBITDA margins to edge towards 11% by FY20: PARAG’s gross margins should improve to 30.4% in FY20 from 28.4% in FY16, majorly led by mix improvement. We expect the share of skimmed milk powder to fall by 480bps during FY16-20 and share of high-margin value-added products to make up this fall. This, along with introduction of premium variants, would lead to a ~50bps gross-margin expansion every year. While operating expenses would stay high (as the company expands), we still expect EBITDA margins to move to 10.8% in FY20 from 9% in FY16.

Return ratios to improve on better capacity utilization: As sales expand for the company in the medium term, we expect capacity utilization levels for packaged milk, UHT, ghee, and butter to improve from sub-50% levels – which in turn would improve fixed-asset turnover over the medium term and lead to an improvement in return ratios. We see RoE improving to 12.9% in FY20 from 8.3% in FY16 – a modest improvement, limited by the company’s need to invest on distribution for growth.

Free cash flows will turn positive from FY18, as capex intensity will reduce: We believe the company would have sufficient capacity after its FY17/18 capex cycle, and would not need major capex for the succeeding five years. Fall in capex and stabilization in working-capital days (as sales expand) would lead to better cash flows. We see free cash flows turning positive from FY18 and rising substantially thereafter.

Valuations in dairy industry: The stock of Parag Milk Foods, after rallying almost 50% since listing in May 2016, now trades at 24x our FY18 earnings (29x our FY18 recurring earnings). In comparison, its peers, Hatsun Agro/Heritage Foods/Prabhat Dairy/Kwality Dairy trade at 39/22/18/15 times our FY18 earnings. On EV/EBITDA, PARAG trades at 14 times our FY18 EBITDA vs. 14/11/7/9 times our FY18 EBITDA for the same peer-set. The PC FMCG universe (ex ITC), in comparison, currently trades at 40x one-year forward earnings.

Initiate with BUY rating: We expect PARAG to deliver strong PAT growth (30% CAGR) during FY17-20 and value the stock at Rs 24 times our September 2018 earnings (30x our FY18 adjusted earnings – 1 PEG) at Rs 350. We initiate coverage on the stock with a BUY rating.

BUY CMP RS 295

TARGET RS 350 (+18%) COMPANY DATA

O/S SHARES (MN) : 84

MARKET CAP (RSBN) : 24.8

MARKET CAP (USDBN) : 0.4

52 - WK HI/LO (RS) : 357 / 897

LIQUIDITY 3M (USDMN) : 1.7

PAR VALUE (RS) : 10

SHARE HOLDING PATTERN, %

Jun 16

PROMOTERS : 47.5

FII / NRI : 27.0

FI / MF : 4.3

NON PRO : 19.9

PUBLIC & OTHERS : 1.4

PRICE PERFORMANCE, %

1MTH 3MTH

ABS -4.8 13.7

REL TO BSE -6.7 6.5

PRICE VS. SENSEX

Source: Phillip Capital India Research

KEY FINANCIALS

Rs mn FY17 FY18E FY19E

Net Sales 17,535 20,291 23,612

EBIDTA 1,696 2,072 2,532

Net Profit 795 1,031 1,334

EPS, Rs 9.5 12.3 15.9

PER, x 31.2 24.1 18.6

P/BV, x 3.4 3.0 2.6

ROE, % 10.8 12.3 13.7

Debt/Equity (%) 40.8 35.8 30.9

Source: PhillipCapital India Research Est.

Jubil Jain (+ 9122 6667 9766) [email protected] Naveen Kulkarni (+ 9122 6667 9947) [email protected]

80

100

120

140

160

May-16 Jun-16 Jul-16 Aug-16 Sep-16

Parag BSE Sensex

Page | 2 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Indian dairy poised to take off India is currently the largest producer and consumer of milk. In FY15, India produced 147mn tonnes and consumed 138mn tonnes of milk (~17% of global volumes). However, annual per capita consumption in India is just 97 litres as against more than 280 litres in US/Europe. We see this as a huge opportunity and we believe that with rising income levels and rising production, per capita milk consumption in India in the long term will rise and the gap with developed nations will reduce.

India’s milk production and consumption volumes have seen consistent growth in the last five years (Quantity in Tonnes)

Source: IMARC report, Company RHP

…however, India’s per-capita consumption of milk is far lower than in developed markets and even compared to its emerging market peers

Source: IMARC report, Company RHP

100

105

110

115

120

125

130

135

140

145

150

FY11 FY12 FY13 FY14 FY15

Production Consumption

0

50

100

150

200

250

300

US EU27 Russia Brazil India

Per capita consumption (L/yr)

While India is the largest producer and consumer of milk, annual per capita consumption in India is a fraction of that in developed world

Page | 3 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Indian dairy industry to see 15% CAGR in 2014-20 says IMARC Indian dairy industry is poised to grow to Rs 9.4tn by 2020 from Rs 4.1tn in 2014 (15% CAGR), as per a report by IMARC (International Market Analysis Research and Consulting Group). High-margin categories – cheese, flavoured and UHT milk, flavoured yoghurts and lassi – in which organised players like Parag have a dominant share, are poised to see >25% CAGR in 2014-20. Key growth drivers for the sector are rising middle class and urban population, changing dietary patterns, acceptance of milk as a perfect health food, and consumer shift towards packaged milk.

Indian dairy industry: Category-wise growth prospects

Industry size

in 2010 (Rs bn)

Industry size

in 2014 (Rs bn)

Industry size

in 2020E (Rs bn)

CAGR

2010-2014

CAGR

2014-2020E

Liquid milk 1501 2,621 6,068 15% 15%

Ghee 345 618 1,367 16% 14%

Paneer 164 293 654 16% 14%

Curd 124 216 493 15% 15%

Butter *96 168 382 15% 15%

Skimmed milk powder 28 50 113 15% 15%

UHT milk 10 26 104 27% 26%

Buttermilk 6 14 43 23% 21%

Cream 7 13 30 16% 15%

Flavoured milk 5 13 48 26% 25%

Lassi 5 12 39 26% 21%

Cheese 5 12 59 24% 31%

Whey (powder) *1.5 3 10 20% 21%

Flavoured & Frozen Yoghurt 1 2 12 23% 32%

Total 2,298 4,061 9,397 15% 15%

Source: IMARC report, Company RHP; * PC estimates

Organised players to grow faster than unorganised players In 2010-14, the unorganised segment saw 14% CAGR, while organised saw a faster 21% CAGR. In 2015-20, IMARC expects a higher organised-segment CAGR of about 20% vs. 13% for the unorganised segment. As a result, the share of the organised business in the Indian dairy industry has been continuously rising.

Value growth Value share

Source: IMARC report,

0%

5%

10%

15%

20%

25%

2010-14 CAGR 2015-20 CAGR

Unorganised Organised

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Value share (2014) Value share (2020)

Unorganised Organised

High-margin categories – cheese, flavored and UHT milk, flavored yoghurts, and lassi – in which organized players like Parag Milk Foods have dominant share, are poised to see >25% CAGR in 2014-20

Page | 4 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Co-operatives will continue to dominate the industry, but there is space for private players too While co-operatives dominate the fresh-milk space, private players have room to expand in the value-added products category Currently, co-operatives (with 55% organised-market volume share) dominate the organised sector due to their strong sourcing capabilities. While this dominance will continue in most states, private players have huge growth potential if they develop strong brands and expand their value-added products categories. Co-operatives, due to their mandate to procure all the milk offered by farmer members irrespective of demand and to maximise payment to farmer members, have the risk of being financially inefficient. An analysis of EBITDA margins for co-operative and listed players shows that on an average, co-operatives have lower profitability than private players, which can limit their ability to invest in capacity for value-added products.

Key metrics of select dairy players (Rs mn, unless specified otherwise) Gujarat

co-operative

Rajasthan

co-operative

PARAG Prabhat Dairy

Sales 207,504 4,299 16,451 11,705

Gross Profit 9,772 607 4,676 2,608

Gross margin (%) 4.7 14.1 28.4 22.3

Operating expenses 8,659 540 3,200 1,416

EBITDA 1,113 67 1,476 1,192

EBITDA margin (%) 0.5 1.6 9.0 10.2

Source: Company, PhillipCapital India Research Estimates

Co-operatives have lower profitability than private players, which can limit their ability to invest in capacity for value-added products

Page | 5 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

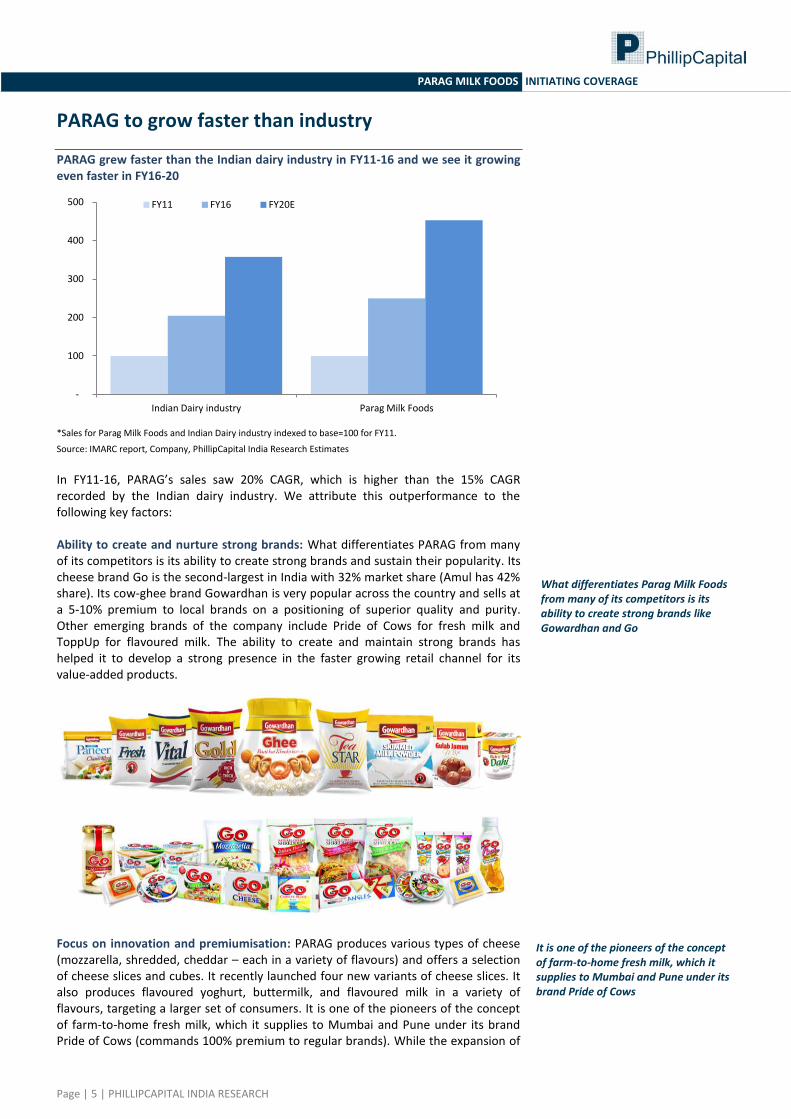

PARAG to grow faster than industry

PARAG grew faster than the Indian dairy industry in FY11-16 and we see it growing even faster in FY16-20

*Sales for Parag Milk Foods and Indian Dairy industry indexed to base=100 for FY11.

Source: IMARC report, Company, PhillipCapital India Research Estimates

In FY11-16, PARAG’s sales saw 20% CAGR, which is higher than the 15% CAGR recorded by the Indian dairy industry. We attribute this outperformance to the following key factors: Ability to create and nurture strong brands: What differentiates PARAG from many of its competitors is its ability to create strong brands and sustain their popularity. Its cheese brand Go is the second-largest in India with 32% market share (Amul has 42% share). Its cow-ghee brand Gowardhan is very popular across the country and sells at a 5-10% premium to local brands on a positioning of superior quality and purity. Other emerging brands of the company include Pride of Cows for fresh milk and ToppUp for flavoured milk. The ability to create and maintain strong brands has helped it to develop a strong presence in the faster growing retail channel for its value-added products.

Focus on innovation and premiumisation: PARAG produces various types of cheese (mozzarella, shredded, cheddar – each in a variety of flavours) and offers a selection of cheese slices and cubes. It recently launched four new variants of cheese slices. It also produces flavoured yoghurt, buttermilk, and flavoured milk in a variety of flavours, targeting a larger set of consumers. It is one of the pioneers of the concept of farm-to-home fresh milk, which it supplies to Mumbai and Pune under its brand Pride of Cows (commands 100% premium to regular brands). While the expansion of

-

100

200

300

400

500

Indian Dairy industry Parag Milk Foods

FY11 FY16 FY20E

What differentiates Parag Milk Foods from many of its competitors is its ability to create strong brands like Gowardhan and Go

It is one of the pioneers of the concept of farm-to-home fresh milk, which it supplies to Mumbai and Pune under its brand Pride of Cows

Page | 6 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Pride of Cows business is not in the company’s priority list, it showcases PARAG’s innovation and premiumisation capabilities. It plans to boost its whey-protein business by introducing premium products, which will help it move further up on the value chain. We believe these strategies will help the company to outperform peers and unbranded players on both growth and margins in the long term.

Strong sourcing chain and strong retail channel distribution network: Over the last two decades, PARAG has set up a strong sourcing and distribution network. It sources milk from 250,000 farmers in 3,400 villages across Maharashtra, Andhra Pradesh, Karnataka, and Tamil Nadu, and also procures milk indirectly through wholesalers. The quantity of milk sourced directly and indirectly varies based on the prevalent supply conditions of milk. It has a dairy farm near Pune with 2,000 cows of the Holstein breed, maintained mainly for R&D purposes. It is also among the few private dairy players with a pan-India presence. Currently, its distribution network consists of 16 depots and over 3,000 distributors across the country. It employs 560 people for distribution and marketing. We believe that the company has the right sourcing and distribution strategy and as its sales expand, its network will increase and aid growth.

It has a dairy farm near Pune with 2,000 cows of the Holstein breed

It produces flavored yoghurt, buttermilk, and flavored milk in a variety of flavors, targeting a larger set of consumers

Page | 7 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Key strategic initiatives of the company: PARAG has a holistic strategy for growth – it plans to focus on product portfolio, sourcing and distribution, promotion, and cost management.

Increase value-added product portfolio: Offer wider range of farm-to-home products under ‘Pride of Cows’ and sell whey directly to retail consumers in the form of branded health supplement foods and beverages.

Focus on health and nutrition: Introduce products such as milk-based high protein drinks (Topp Up, T-Star, Go), daily supplements, and high-protein low fat cheese products.

Grow product reach: Add six depots in FY17, introduce low unit price products in tier-3 cities, and identify geographies on which to focus sales efforts.

Increase milk procurement: Strengthen existing farmer relations and set up new collection centres, enter new districts for procurement, add 75 new bulk coolers, and 100 automated collection systems.

Focus on strengthening brands: Enhance brand recall through ad spends in diverse media such as television, newsprint, digital media, etc.

Increase operational efficiencies: Develop systems and processes, enhance customer service levels, and maintain strict operational controls.

We believe that the company has the right growth strategy and can achieve its growth objectives through right execution.

PARAG to grow in future led by value added categories: In FY16-20, we expect a sales CAGR of ~16%, primarily led by value-added categories like cheese, UHT, whey, and other high-margin products. We expect skimmed milk powder growth to slow down to 5% and its share in the portfolio to reduce below 10%.

Historical and projected sales for Parag Milk Foods (Rs mn)

Source: Company, PhillipCapital India Research Estimates

Category-wise projected growth rate from FY15-20

Sales in FY15

(RS mn)

Expected growth rate (%)

Products FY15 FY16 FY17 FY18 FY19 FY20

Fresh Milk 2,555 11 17 22 20 18 15

Ghee/Butter/Cream 2,629 27 35 8 10 13 14

Cheese/Paneer 2,670 32 25 20 20 20 20

UHT 468 87 50 20 20 20 20

Whey 225 1 80 20 20 25 25

Skimmed milk powder 3,010 48 (33) 5 5 5 5

Other manufactured products 1,788 155 10 20 20 20 20

Other Traded goods 492 -38 73 -71 0 0 0

Total Sales 13,836 33.2% 14.1% 16.2% 16.3% 15.9% 16.1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

-

5,000

10,000

15,000

20,000

25,000

30,000

FY12 FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

Sales (Rs mn) Sales growth (rhs)

In FY16-20, we expect sales CAGR of ~16%, primarily led by value-added categories like cheese, UHT, whey, and other high-margin products

Page | 8 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Source: Company, PhillipCapital India Research Estimates

Projected share in total revenue of key product categories

Source: Company, PhillipCapital India Research Estimates

0%

20%

40%

60%

80%

100%

FY16 FY17 FY18 FY19 FY20

Other operating income

Traded products

Other manufactured products

Skimmed milk powder

Whey

UHT

Cheese/Paneer

Ghee/Butter/Cream

Fresh Milk

Share of fresh milk and high margin value added products like cheese and UHT will improve gradually over the years

Page | 9 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

PARAG is well-placed vs. competition We ranked PARAG on three of the most crucial parameters needed to succeed in the dairy business – sourcing, branding, and retail distribution. Amul currently has the strongest operational metrics in the industry, being strong in sourcing, retail distribution, and branding. Similarly, Hatsun Agro and Heritage Foods have a very strong sourcing and retail distribution network, and their brand names are well-known in their respective markets. PARAG ranks in the middle with strong pan-India brands like Go and Gowardhan. Currently, as per our estimates, it procures 30-40% milk indirectly and its institutional business has a 40-50% sales share. However, we believe that it has acquired critical mass and can improve on both the parameters –direct milk procurement and retail distribution – if it maintains its current strategy.

Comparison with other key players across key parameters for ‘Right to Win’ 'Players Direct milk

procurement

Brand

strength

Share of retail

business

Score

Amul Strong Strong Strong 9

Hatsun Agro Strong Strong Strong 9

Heritage Strong Strong Strong 9

Parag Milk Foods Moderate Strong Moderate 7

Prabhat Dairy Moderate Moderate Weak 5

Kwality Dairy Moderate Weak Weak 4

Source: PhillipCapital India Research Estimates

Parag Milk Foods fares satisfactorily in comparison with peers on Right to Win. It has acquired critical mass and can improve on direct milk procurement and retail distribution

Page | 10 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Capacity utilization levels set to improve

Historical Capacity utilisation (%) _____________Manchar_____________ _____________Palamaner_____________

Product Units 2013 2014 2015 9MFY16 2013 2014 2015 9MFY16

Milk processing capacity (litres per day) 61 55 77 74 32 39 50 66

Milk powders (includes drying capacity for whey

powders and dairy whiteners) (metric tons per day)

68 62 79 65 19 55 67 86

Liquid milk in pouches (litres per day) 54 70 82 62 76 50 34 41

Flavoured milk (packs per day) 2 28 29 28 16

UHT Products* (litres per day) 9 18 18 33

Cheese/Paneer (metric tons per day) 44 47 67 81

Ghee (metric tons per day) 49 45 39 72 8 5 10 13

Butter (metric tons per day) 18 6 17 17 13 30 62 81

Curd (includes pouch curd, cup curd, fruit yoghurt

and shrikhand) (metric tons per day)

55 48 27 43 48 63 51 75

Source: Company, PhillipCapital India Research Estimates

PARAG has two manufacturing facilities in Manchar (near Pune, Maharashtra)/ Palamner (Andhra Pradesh) with milk-processing capacities of 1.2/0.8mn litres per day. In the Pune plant, its capacity utilisation levels are already high and with increase in milk procurement, we expect these levels to improve. In the Palamner plant, capacity utilisation levels are currently lower vs. Manchar, as the Palamner plant was commissioned only six years ago. However, with the company’s strategy to increase milk procurement from Andhra Pradesh, we expect these utilisation levels to increase. Capacity utilisation levels for its major product categories vary from 50% to 70% and there is room to meet demand for the next two years. However, by March 2019 it will increase capacities across major categories by using its IPO proceeds. This capacity addition will help it to meet demand for the next five years.

Capacity for different product categories

Product Units Manchar Palamaner

Current

Total

Proposed

expansion

Milk processing capacity (litres per day) 1,200,000 800,000 2,000,000 1,400,000

Milk powders (includes drying capacity for whey

powders and dairy whiteners) (metric tons per day)

70 40 110 -

Liquid milk in pouches (litres per day) 200,000 175,000 375,000 150,000

Flavoured milk (packs per day) 30,000 70000 100,000 30,000

UHT Products* (litres per day) 0 165,000 165,000 80,000

Cheese/Paneer (metric tons per day) 40 0 40 20 cheese +

20 paneer

Ghee (metric tons per day) 40 30 70 -

Butter (metric tons per day) 50 25 75

Curd (includes pouch curd, cup curd, fruit yoghurt

and shrikhand) (metric tons per day)

20 40 60 20

Whey Processing (litres per day) 400,000 0 400,000 600,000

*Includes lassi and buttermilk

Source: Company, PhillipCapital India Research Estimates

Capacity utilization will improve over the medium term; proposed expansion will help meet demand for the next five years

Page | 11 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Capacity utilisation – Historical and forecasted Capacity Utilisation (%)

Product Units FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

Milk processing capacity 49 49 66 71 79 89 **57 62

Milk powders (incl drying capacity for whey

powders and dairy whiteners)

50 59 75 73 76 80 84 88

Liquid milk in pouches 64 61 60 52 58 65 **51 56

Flavoured milk 2 28 29 65 76 89 **80 94

UHT Products* 9 18 18 33 39 45 **36 42

Cheese/Paneer 44 47 67 81 95 **55 65 76

Ghee 31 28 27 47 52 59 66 74

Butter 16 14 32 38 43 48 54 60

Curd (includes pouch curd, cup curd, fruit

yoghurt and shrikhand)

50 58 43 64 75 88 **77 90

*Includes lassi and buttermilk

** Assuming proposed expansion will be commissioned in the particular year

Source: Company, PhillipCapital India Research Estimates

With capacity in place for the next three years, capital investment will reduce from FY19 Through IPO proceeds, PARAG will complete major capex capital investment for medium term by FY18. For FY19-22, with capacity in place, the annual capital expenditure will fall to Rs 250mn from Rs 831mn in FY17. Since capacity utilisation levels will be low even in FY20 (for some activities like milk processing and butter/ghee/UHT milk/liquid milk manufacturing), we expect capital expenditure from FY21 to not be as high as it was in FY16-18. This will help the company to report strong free cash flows during FY19-24.

While current utilisation levels are high, proposed expansion will cover the next five years of growth

Reduction in capex intensity starting FY19 will help increase free cash flows substantially

Page | 12 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Operational parameters will see consistent improvement Milk prices are likely to see moderate inflation over the next few years; price hikes to offset input cost inflation After abnormally high inflation levels in FY15, milk prices stabilised in the latter half of FY16, led by oversupply in India and globally, and a global fall in skimmed milk powder prices. In the medium term, we expect milk prices in India to rise moderately because: (1) global milk prices continue to be subdued due to global oversupply and subdued Chinese demand, and (2) milk production in India is expected to grow at a robust pace. We do not expect milk price inflation to impact gross margins for PARAG in the medium term, as we believe the company will take proportionate price hikes across its product portfolio.

Skimmed milk powder inflation Milk price inflation

Source: Bloomberg, PhillipCapital India Research Estimates

Mix improvement will lead to ~50bps gross margin expansion every year Value-added products like UHT, whey, flavoured milk, and cheese have gross margins that are higher than 30% vs. just 5% for skimmed milk powder (SMP). We estimate the rise in share of value-added products in PARAG’s portfolio and fall in share of SMP to lead to a gross-margin improvement of 30-50 bps every year for the next few years. Also, due to its strategy introducing premium products in key categories like cheese, milk, and whey, it will see an improvement in mix even within categories – which will add to gross-margin expansion. We have built in 50bps annual improvement in gross margins in FY16-20.

Impact of mix change on gross margins

Estimated gross margin

(incl. manufacturing overheads)

Share in manufactured products sales

Products FY17 FY18 FY19 FY20

Fresh Milk 14% 20.0% 20.7% 21.0% 20.9%

Ghee/Butter/Cream 28% 21.0% 20.0% 19.4% 19.1%

Cheese/Paneer 33% 21.9% 22.8% 23.5% 24.3%

UHT 40% 4.6% 4.8% 4.9% 5.1%

Whey 60% 2.7% 2.8% 3.0% 3.2%

Skimmed milk powder 5% 11.6% 10.5% 9.5% 8.6%

Other manufactured products 40% 18.2% 18.4% 18.6% 18.9%

Others 20% 5.3% 5.0% 4.8% 4.6%

Total gross margin 26.2% 26.5% 26.9% 27.3%

Gross margin improvement due

to mix

31 bps 38 bps 44 bps

Source: PhillipCapital India Research Estimates

-60%

-40%

-20%

0%

20%

40%

60%

80%

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Skimmed milk powder inflation

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Milk price inflation

We expect mix improvement to add 30-50 bps to gross margins every year

Page | 13 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Gross margins to see gradual improvement Gross profits to see 17% CAGR in FY17-20

Source: Company, PhillipCapital India Research Estimates

EBITDA margins to improve due to operating leverage In FY15/16 EBITDA margins were at 7.4%/9.0% – these will see gradual improvement in FY17-20 and edge towards 11% majorly led by gross-margin improvement and operating leverage due to improving capacity utilisations. However, the need for the company to invest in sales-force and advertising will limit improvement in the medium term. We expect EBITDA to grow by 22% CAGR in FY17-20.

EBITDA margins to see gradual improvement EBITDA to see 22% CAGR in FY17-20

Source: Company, PhillipCapital India Research Estimates

PAT to register healthy growth as finance costs reduce with debt repayment and depreciation growth cools down will reduction in capex intensity The company has repaid Rs 1bn debt with its IPO proceeds, and as per our estimates, it would not need to take additional debt in FY17-20. As a result, finance costs will reduce from FY17, PAT margins will improve to 6% levels from ~3% in FY16 and we expect PAT to grow by 30% CAGR in FY17-20.

0%

5%

10%

15%

20%

25%

30%

35%

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

Gross margins

0%

10%

20%

30%

40%

50%

60%

FY12 FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

Gross profit growth

0%

2%

4%

6%

8%

10%

12%

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

EBITDA margins

-10%

0%

10%

20%

30%

40%

50%

60%

70%

FY12 FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

EBITDA growth

Page | 14 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

PAT margins to see gradual improvement to 6% PAT to see 30% CAGR in FY17-20

Source: Company, PhillipCapital India Research Estimates

Working capital will continue to remain high as it expands retail distribution PARAG is still in the initial high-growth phase as compared to major FMCG companies in India. Hence, we expect it to invest on expanding its distribution and reach in the medium term, which will require working capital investment. It plans to reduce the share of its institutional business and increase its retail business. However, this will not lead to a significant fall in receivable and inventory days because sales expansion of value-added products in retail requires high receivable days (~30). Also, cheddar cheese sold (majorly through the retail format) requires more ageing (~45-60 days) than mozzarella cheese sold to institutions (~15 days). We do not expect a significant decline in working capital/sales or working capital days in the medium term.

Working capital days will continue to stay high Working Capital/Sales will stabilise around 25% levels

Source: Company, PhillipCapital India Research Estimates

Free cash flows to improve; do not see further increase in debt From FY19, the medium-term capex intensity for PARAG would reduce, even as operating cash flows would maintain their double-digit growth trajectory. From FY19, we expect annual capex to reduce to Rs 250mn from an average of Rs 590mn during FY11-16. As a result, PARAG will deliver positive and strong free cash flows, starting FY18. Taking into account IPO proceeds and the fact that free cash flows would be sufficient to fund working capital and capex needs starting FY19, we do not see further increase in debt levels for the company.

-1%

0%

1%

2%

3%

4%

5%

6%

7%

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

PAT margin

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

PAT growth

-

10

20

30

40

50

60

70

80

90

Recievable Days Inventory days Payable Days

FY12

FY13

FY14

FY15

FY16E

FY17E

FY18E

FY19E

FY20E 0%

5%

10%

15%

20%

25%

30%

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E FY19E FY20E

Working Capital/Sales

Sales expansion of value-added products in retail channel requires high receivable days

Page | 15 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Operating cash flows will continue to improve Free cash flows to get a boost starting FY18 on lower capex

Source: Company, PhillipCapital India Research Estimates

With increasing capacity utilisations, return ratios will improve We expect an improvement in both key return ratios – RoE and RoCE; however, this improvement will be modest in the medium term because of investments in next few years on manufacturing and distribution. Ratios should improve faster once the company reaches a larger scale in terms of retail distribution and manufacturing.

Return on equity ratio will improve gradually Return on capital employed will improve gradually

Source: Company, PhillipCapital India Research Estimates

(1,000)

(500)

-

500

1,000

1,500

Operating cash flow Investing cash flow

FY11

FY12

FY13

FY14

FY15

FY16E

FY17E

FY18E

FY19E

FY20E (1,000)

(500)

-

500

1,000

1,500 Free cash flow

0%

10%

20%

30%

40%

50% RoE

0%

2%

4%

6%

8%

10%

12%

14%

16% RoCE

Page | 16 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

About Parag Milk Foods PARAG was founded in 1992. It is an integrated dairy company, one of the largest private dairy players, and has a milk-processing capacity of 2mn litres per day. It is present in over 17 dairy product categories and markets products under the brands Gowardhan, Go, Pride of Cows, and Topp-up.

Brand-wise product categories of PARAG Brands Categories Target

Gowardhan Ghee, milk, paneer, dahi, curd , butter,

dairy whitener and gulab jamun (an Indian

sweet) mix

Every-day dairy products, house hold

consumption used as cooking ingredients

Go Flavoured cheese, tubes, slices etc Children and youth, primarily for direct

consumption

Pride of Cows Farm-to- home, subscription model Consumer seeking premium quality

Topp- Up Flavored milk with extra proteins Youth and travelers

Source: Company, PhillipCapital India Research

Currently, the biggest contributors to its revenue (>20% each) are fresh milk, ghee/butter, and cheese/paneer. It intends to increase its dairy-based beverages portfolio under the ‘Go’ brand, introduce milk-based high-protein drinks, and a new variant of curd with higher protein and lower fat content. It also intends to set up a whey-proteins manufacturing facility and increase its presence in the premium health supplement space. Because of high proportion of sales from value-added products like cheese, UHT, flavoured milk, buttermilk and curd (~30%), and branding in the otherwise low-margin ghee business (~32%), Parag has consistently delivered gross margins of 22-25% in FY11-16.

Page | 17 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Management profile Mr Devendra Shah He founded the company in 1992 and is executive Chairman. He has 23 years of experience in the dairy industry. Apart from promoting India’s largest cow farm called Bhagyalaxmi Dairy farm, he also holds reputed positions in various ventures (Director - Bhimashankar Sahakari Sakhar Karkhana, Pargaon, Secretary of National Centre for Rural Development, Chairman - Sharad Sahakari Bank, and Director, NDRI). Mr Pritam Shah He is responsible for the company’s overall growth strategy and consolidating market presence. He is the Managing Director and has 23 years of experience in the industry. He has a strong understanding in procurement and distribution channels. Mr Bharat Kedia He has been the Chief Financial Officer since January 2, 2015. His experience spans Goodlass Nerolac Paints Private Limited, Farvane Overseas Consultants Limited, and Russian operations at Coca Cola Hellenic Bottling Company. He also served as the Chief Executive Officer at TLG India Private Limited. He is a qualified chartered accountant and company secretary. Mr Mahesh Israni He leads Global Sales and Marketing for Gowardhan and Go brands and handles the company’s overall marketing strategy, brand development, and RTM strategy. Mr Israni has worked with Pidilite and HUL in various roles and has over 25 years of experience in sales and customer marketing in FMCG sector. Mr BM Vyas Mr Vyas joined the company as a consultant and currently he is the director responsible for advising the top management in making efficient and effective growth strategies. He is closely involved with monitoring the entire gamut of the business processes and getting them streamlined and efficient. He advises the Chairman on various avenues to bring in internal and external development. Prior to this, Mr Vyas was MD of Gujarat Co-operative Milk Federation (GCMMF), which markets Amul. He has four decades of experience in the dairy industry.

Page | 18 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Shareholding structure Category of shareholder 16-Jun

Promoters 47.4

FII / NRI 27

FI / MF 4.3

PUBLIC & OTHERS 21.3

Source: Bloomberg, BSE India

Key investors Top shareholders June-2016

Institutions

Tata Balanced Fund 3.95

Nomura India Investment Fund Mother Fund 2.98

Macquarie Emerging Markets Asian Trading PTE. Ltd. 2.95

India Opportunities Growth Fund Ltd - Pinewood STR 2.21

Government Pension Fund Global 2.19

Abu Dhabi Investment Authority - Behave 2.1

Goldman Sachs India Fund Limited 1.94

Quantum (M) Limited 1.79

Copthall Mauritius Investment Limited 1.68

Morgan Stanley Mauritius Company Limited 1.67

Individuals & NBFCs

Ashish Kacholia 1.7

Narendra Kumar Agarwal 1.14

IDFC SPICE FUND 2.87

IDFC TRUSTEE CO. LTD A/C IDFC INFRASTRUCTURE FUND 6.98

Source: Bloomberg, BSE India

Page | 19 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Valuation matrix for Dairy

CMP

M Cap

(Rs. Bn)

Sales EBITDA PAT PER EV/EBITDA RoE RoE RoCE RoCE

Company FY16 FY16 FY16 FY17E FY18E FY17E FY18E FY15 FY16 FY15 FY16

Kwality Dairy* 135 31,650 57,242 3,514 1,442 18.1 14.8 10.7 9.1 28.0 20.9 16.1 13.2 Hatsun Agro 339 51,710 34,446 3,047 605 46.6 38.9 16.0 13.8 19.5 26.8 14.4 12.6 Prabhat Dairy 114 11,180 11,705 1,192 245 25.1 18.2 9.2 7.4 7.8 4.9 9.6 6.7 Parag Milk Foods 295 24,760 16,451 1,476 473 31.1 24.0 16.7 13.7 29.2 19.5 13.2 13.0 Heritage Foods 881 20,530 23,806 1,322 554 28.9 22.4 13.7 11.3 15.2 26.2 26.7 38.9

______Sales growth______ _____EBITDA growth_____ _____EBITDA margin_____ ______PAT growth______ 1 yr

return Company FY15 FY16 FY17E FY15 FY16 FY17E FY15 FY16 FY17E FY15 FY16 FY17E

Kwality Dairy* 15.1 8.6 9.0 17.4 9.7 17.2 6.1 6.1 6.6 11.3 2.3 21.3 81% Hatsun Agro 17.6 17.4 17.0 11.6 53.6 15.8 6.8 8.8 8.8 (52.1) 54.5 83.6 21% Prabhat Dairy 17.1 16.7 12.0 14.5 15.2 15.5 10.3 10.2 10.5 28.5 (5.7) 81.5 4% Parag Milk Foods 32.7 13.9 10.9 30.4 37.6 14.9 7.4 9.0 9.3 102.4 46.4 68.1 50%** Heritage Foods 20.4 14.8 18.0 (13.6) 57.9 16.8 4.0 5.6 5.5 (38.4) 101.3 25.1 127%

Source: Company, PhillipCapital India Research Estimates

*For Kwality Dairy only standalone numbers are considered

**For Parag Milk Foods, 1 yera return is calculated from its date of listing in May 2016.

Page | 20 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Appendix 1: Comparison of financial parameters with other listed dairy players

Historical sales (Rs mn) and sales CAGR

Gross margins

EBITDA margins

Source: Company, PhillipCapital India Research

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods (Only Dairy segment)

FY2012 FY2013 FY2014 FY2015 FY2016

0%

5%

10%

15%

20%

25%

30%

Kwality Dairy (adj.)

Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods (Only Dairy segment)

FY2012 FY2013 FY2014 FY2015 FY2016

0%

2%

4%

6%

8%

10%

12%

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods (Only Dairy segment)

FY2012 FY2013 FY2014 FY2015 FY2016

Sales growth has been strong for all Dairy players

Except Kwality Dairy, which sells more low-margin products, others have gross margins of 20-25%

EBITDA margins are lower for dairy players because of higher operating expenses

Page | 21 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Profit margins

Except Hatsun and Heritage, which have major portion of portfolio in retail, receivable days are very high for others. PARAG has high inventory days due to higher share of cheese in sales, which requires aging.

Receivables days

Inventory days

Source: Company, PhillipCapital India Research

0%

1%

1%

2%

2%

3%

3%

4%

4%

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods

FY2012 FY2013 FY2014 FY2015 FY2016

-

10

20

30

40

50

60

70

80

90

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods

FY2012 FY2013 FY2014 FY2015 FY2016

-

10

20

30

40

50

60

70

80

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods

FY2012 FY2013 FY2014 FY2015 FY2016

PAT margins of dairy players are lower than those of FMCG peers, because dairy requires higher capital expenditure and higher working capital

Except Hatsun and Heritage, which have major portion of portfolio in retail, receivable days are very high for others

PARAG has high inventory days due to higher share of cheese in sales, which requires aging

Page | 22 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Payables days

Free cash: Most worrisome aspect of the dairy industry is that free cash flow has been negative for most companies for many years because of capital investment and increase in receivables. We however, expect Parag Milk Foods to report substantial positive free cash flow starting FY18.

Free cash flow

Net debt/EBITDA

Source: Company, PhillipCapital India Research

-

5

10

15

20

25

30

35

40

45

50

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods

FY2012 FY2013 FY2014 FY2015 FY2016

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods

FY2012 FY2013 FY2014 FY2015 FY2016

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods

FY2012 FY2013 FY2014 FY2015 FY2016

Free cash flow has been negative for many dairy companies for many years because of capital investment and increase in receivables. We however, expect Parag Milk Foods to report substantial positive free cash flow starting FY18

Page | 23 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Total debt/Equity

RoE

RoCE

Source: Company, PhillipCapital India Research

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods

FY2012 FY2013 FY2014 FY2015 FY2016

0%

10%

20%

30%

40%

50%

60%

70%

80%

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods

FY2012 FY2013 FY2014 FY2015 FY2016

0%

10%

20%

30%

40%

50%

60%

70%

Kwality Dairy Hatsun Agro Prabhat Dairy Parag Milk Foods Heritage Foods (Only Dairy segment)

FY2012 FY2013 FY2014 FY2015 FY2016

Total debt/Equity for Parag Milk Foods has reduced substantially over the years

Return ratios are lower in Dairy industry vs. those in FMCG

Page | 24 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Appendix 2: Key product categories in Indian Dairy industry

Traditional categories Liquid Milk: Liquid milk is the largest dairy segment in India, valued at Rs 3tn in 2015. While 80% of liquid milk is sold through unorganised segment, the organised segment is growing faster. Currently, the organised segment is strongly dominated by local state co-operatives like Amul, Nandini, and others. However, some private players like Hatsun Agro, Tirumal, and PARAG have established a strong presence in specific geographies. As was pointed out in our March 2016 edition of Ground View, strong presence in the liquid milk segment is very important to succeed in the dairy business. This business helps to develop a strong sourcing and distribution network, to develop strong brands, and to expand retail business.

Indian Liquid milk market (Rs bn)

Ghee or clarified butter: India has traditionally had a larger ghee market than a butter or cheese one. The Indian ghee market saw 17% CAGR in 2007-14 to Rs 618bn. Currently, the market is dominated by the unorganised segment, which has 82% share. However, the organised segment is expected to see at 17% CAGR in 2014-20, faster than overall market, which is poised to grow at 14%. Cow ghee currently accounts for just 10% of the total ghee market, but it is growing faster than the overall ghee market. PARAG is currently the largest player in the cow ghee segment and competes with other major players like Amul, Nandini, and Dynamix.

Indian ghee market (Rs bn)

Source: IMARC Report

1259 1422 1619 1843 2102 2393 2722 3089 3500

3965 4475

242 284 348

428 519

629 760

918

1105

1329

1593

0

1000

2000

3000

4000

5000

6000

7000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

Organised Unorganised

291 339 390 446 508 578 657 746

846 957

1078

54 65

78 93

110 130

154 181

212

248

289

0

200

400

600

800

1000

1200

1400

1600

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

Organised Unorganised

Page | 25 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Cheese: Cheese is still a nascent category in India, valued at Rs 11.7bn in 2014 as against ghee, which was valued at Rs 618bn. However, it is among the fastest growing dairy categories in India and saw 27% CAGR in 2007-14. With improving consumption patterns, it is expected achieve 31% CAGR in 2015-20. Retail and institutional businesses account for 50% each of total cheese sales. Maharashtra accounts for 33% of total cheese consumption followed by Gujarat, Delhi, and Tamil Nadu at 16%, 7%, and 7%, respectively. Amul, PARAG, and Britannia are the largest players in cheese.

Indian cheese market (Rs bn)

Paneer: The Indian paneer market, valued at Rs 293bn in 2014, is strongly dominated by the unorganised segment (98% share). However, the organised segment is has been and is expected to grow faster (22% CAGR) than the unorganised segment (14%) in 2014-20. Given its large size and strong growth potential in the organised segment, it is a very important dairy category. Currently, 80% of demand is from institutional players and it is expected to increase significantly with growth in restaurant and cafeteria industries.

Indian paneer market (Rs bn)

Source: IMARC Report

5 6 8 9 12 15 20

27 35

46

59

0

10

20

30

40

50

60

70

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

161 190 216 249 286 328

375 429

489 556

631

0

100

200

300

400

500

600

700

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

Unorganised Organised

Page | 26 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Curd: Curd category, valued at Rs 217bn in 2014m is expected to grow to Rs 493bn in 2020 (15% CAGR). Institutional sales account for major portion of the category. However, the organised segment currently accounts for only 6% of the sales and is expected to grow faster than the category. Nandini, Torumala and AMul are the top three playters in the segment. PArag Milk Foods is an important player in the category in West and South India.

Indian Curd market (Rs bn)

Buttermilk: Buttermilk category, valued in 2014 at Rs 13.8bn, is expected to explode to Rs 43bn by 2020 (21% CAGR). The segment is currently dominated by cooperatives from Gujarat, Tamil Nadu and Karnatak. PARAG has a popular offering, called Go Buttermilk, in this space.

Indian Buttermilk market (Rs bn)

Source: IMARC Report

118 136 155 180 205 236 271

310 355

404 458

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

Unorganised Organised

6 8 9 11 14

17 21

25 30

36

43

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

Page | 27 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

New avenues for growth Whey: Whey is the by-product that is left after casein and milk-fat are separated from milk by coagulation, while manufacturing cheese. Only 35% of the produced volume, namely sweet whey, is edible. As per IMARC, the sweet whey powder market in India saw ~26% CAGR in 2007-14 to Rs 3bn and volumes were 29,500MT in 2014. Key players include Amul, PARAG, and Schreiber Dynamix. Highly concentrated solutions of whey powder have realisations of more than five-times that of unprocessed whey. However, there is no domestic manufacturer of concentrated whey powders and the entire demand is met with imports. PARAG aims to produce concentrated whey powder in India, which would help it improve realisations, margins, and expand in the fast-growing whey-protein category. UHT milk: UHT milk, valued in 2014 at Rs 26bn, accounts for less than 1% of the total milk market and 5% of the organised milk market. However, the category is expected to explode to Rs 104bn by 2020 (26% CAGR) due to urbanisation and changing consumer preferences. UHT milk sells at 30-40% premium to fresh milk and provides higher margins. The segment is currently dominated by cooperatives (more than 80% of sales). PARAG is the largest private player in this space.

Indian UHT milk market (Rs bn)

Flavoured milk: Flavoured milk market in India saw 26% CAGR during 2007-2014 to touch Rs 12.6bn in 2014; it is expected to grow to Rs 47.8bn in 2020 (25% CAGR). Currently, dairy co-operatives dominate the organised segment and Amul is the market leader with 33% market share. PARAG is present in the category through the ‘Topp Up’ brand. Compared to liquid milk, which sells at around Rs 40 per litre, flavoured milk sells at about Rs 125.

Indian flavoured milk market (Rs bn)

Source: IMARC Report

10 13 16 21 26 33 42

53 66

83

104

0

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

5 6 8 10 13 16 20

25 31

39

48

0

10

20

30

40

50

60

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

Page | 28 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Flavoured and frozen yoghurt: Flavoured and frozen yoghurt market in India saw 36% CAGR during 2011-2014 to touch Rs 2.3bn in 2014; it is expected to grow to Rs 12.1bn in 2020 (32% CAGR). Growth in the category has been driven primarily by increasing health consciousness among the urban middle class. He segment was pioneered by PArag Milk Foods in 2010 with the launch of Go Fruit and Dahi. Currently, Amul, Mother Dairy and Britannia are the market leaders in the category.

Indian flavoured and frozen yoghurt market (Rs bn)

Source: IMARC Report

1 1 2 2

3 4

5

7

9

12

0

2

4

6

8

10

12

14

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

(Rs

bn

)

Page | 29 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Financials

Income Statement Y/E Mar, Rs mn FY16 FY17e FY18e FY19e

Net sales 15,814 17,535 20,291 23,612

Growth, % 14 11 16 16

Total income 16,451 18,251 21,106 24,539

Raw material expenses -11,776 -12,972 -14,896 -17,197

Employee expenses -701 -794 -918 -1,067

Other Operating expenses -2,499 -2,789 -3,220 -3,743

EBITDA (Core) 1,476 1,696 2,072 2,532

Growth, % 37.6 14.9 22.2 22.2

Margin, % 9.3 9.7 10.2 10.7

Depreciation -334 -395 -446 -484

EBIT 1,142 1,301 1,626 2,048

Growth, % 43.2 13.9 25.0 25.9

Margin, % 7.2 7.4 8.0 8.7

Interest paid -490 -330 -330 -330

Pre-tax profit 668 1,105 1,431 1,852

Tax provided -195 -309 -401 -519

Net Profit 473 795 1,031 1,334

Growth, % 46.4 68.1 29.6 29.4

Non-recurring Items (post tax) 173 187 210 235

Net Profit (adjusted) 300 608 821 1,099

Unadj. shares (m) 84 84 84 84

Wtd avg shares (m) 84 84 84 84

Balance Sheet Y/E Mar, Rs mn FY16 FY17e FY18e FY19e

Cash & bank 77 1,910 1,958 2,527

Debtors 2,360 2,599 2,987 3,453

Inventory 2,724 3,156 3,652 4,250

Loans & advances 454 523 601 691

Other current assets 400 460 529 609

Total current assets 6,016 8,648 9,728 11,530

Investments 0 0 0 0

Gross fixed assets 5,224 6,055 6,682 6,951

Less: Depreciation -1,789 -2,184 -2,630 -3,114

Add: Capital WIP 290 290 290 290

Net fixed assets 3,725 4,161 4,342 4,127

Total assets 9,909 13,002 14,289 15,907

Current liabilities 4,704 4,062 4,319 4,603

Provisions 47 47 47 47

Total current liabilities 4,751 4,109 4,366 4,650

Non-current liabilities 1,539 1,539 1,539 1,539

Total liabilities 6,290 5,647 5,904 6,189

Paid-up capital 704 841 841 841

Reserves & surplus 2,915 6,513 7,544 8,877

Shareholders’ equity 3,619 7,354 8,385 9,718

Total equity & liabilities 9,909 13,002 14,289 15,907

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY16 FY17e FY18e FY19e

Pre-tax profit 668 1,105 1,431 1,852

Depreciation 334 395 446 484

Chg in working capital -425 -859 -802 -979

Total tax paid -195 -309 -401 -519

Other operating activities 545 196 195 195

Cash flow from operating activities 928 527 869 1,033

Capital expenditure -865 -831 -626 -269

Chg in investments 0 0 0 0

Other investing activities 16 134 135 135

Cash flow from investing activities -849 -698 -491 -135

Free cash flow 79 -170 379 898

Equity raised/(repaid) -43 2,940 0 0

Debt raised/(repaid) 478 -607 0 0

Other financing activities -490 -330 -330 -330

Cash flow from financing activities -55 2,003 -330 -330

Net chg in cash 24 1,833 49 568

Valuation Ratios

FY16 FY17e FY18e FY19e

Per Share data

EPS (INR) 5.6 9.5 12.3 15.9

Growth, % 46.4 68.1 29.6 29.4

Book NAV/share (INR) 43.0 87.4 99.7 115.5

FDEPS (INR) 5.6 9.5 12.3 15.9

CEPS (INR) 9.6 14.1 17.5 21.6

CFPS (INR) (12.0) 2.6 6.7 8.7

Return ratios Return on assets (%) 8.2 8.8 9.1 10.2

Return on equity (%) 13.1 10.8 12.3 13.7

Return on capital employed (%) 18.6 14.2 13.1 14.4

Turnover ratios Asset turnover (x) 2.7 2.3 2.3 2.4

Sales/Total assets (x) 1.7 1.5 1.5 1.6

Sales/Net FA (x) 4.6 4.4 4.8 5.6

Working capital/Sales (x) 8% 15% 17% 19%

Receivable days 54.5 54.1 53.7 53.4

Inventory days 62.9 65.7 65.7 65.7

Payable days 40.9 36.2 36.4 36.2

Working capital days 28.5 55.7 62.1 68.0

Liquidity ratios

Current ratio (x) 1.3 2.1 2.3 2.5

Quick ratio (x) 0.7 1.4 1.4 1.6

Interest cover (x) 2.3 3.9 4.9 6.2

Total debt/Equity (%) 99.7 40.8 35.8 30.9

Net debt/Equity (%) 97.5 14.8 12.4 4.9

Valuation

PER (x) 52.4 31.2 24.1 18.6

PEG (x) - y-o-y growth 1.1 0.5 0.8 0.6

Price/Book (x) 6.9 3.4 3.0 2.6

EV/Net sales (x) 1.8 1.5 1.3 1.1

EV/EBITDA (x) 19.2 15.3 12.5 10.0

EV/EBIT (x) 24.8 19.9 15.9 12.4

Page | 30 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Rating Methodology We rate stock on absolute return basis. Our target price for the stocks has an investment horizon of one year.

Rating Criteria Definition

BUY >= +15% Target price is equal to or more than 15% of current market price

NEUTRAL -15% > to < +15% Target price is less than +15% but more than -15%

SELL <= -15% Target price is less than or equal to -15%.

Contact Information (Regional Member Companies)

SINGAPORE: Phillip Securities Pte Ltd

250 North Bridge Road, #06-00 RafflesCityTower,

Singapore 179101

Tel : (65) 6533 6001 Fax: (65) 6535 3834

www.phillip.com.sg

MALAYSIA: Phillip Capital Management Sdn Bhd

B-3-6 Block B Level 3, Megan Avenue II,

No. 12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur

Tel (60) 3 2162 8841 Fax (60) 3 2166 5099

www.poems.com.my

HONG KONG: Phillip Securities (HK) Ltd

11/F United Centre 95 Queensway Hong Kong

Tel (852) 2277 6600 Fax: (852) 2868 5307

www.phillip.com.hk

JAPAN: Phillip Securities Japan, Ltd

4-2 Nihonbashi Kabutocho, Chuo-ku

Tokyo 103-0026

Tel: (81) 3 3666 2101 Fax: (81) 3 3664 0141

www.phillip.co.jp

INDONESIA: PT Phillip Securities Indonesia

ANZTower Level 23B, Jl Jend Sudirman Kav 33A,

Jakarta 10220, Indonesia

Tel (62) 21 5790 0800 Fax: (62) 21 5790 0809

www.phillip.co.id

CHINA: Phillip Financial Advisory (Shanghai) Co. Ltd.

No 550 Yan An East Road, OceanTower Unit 2318

Shanghai 200 001

Tel (86) 21 5169 9200 Fax: (86) 21 6351 2940

www.phillip.com.cn

THAILAND: Phillip Securities (Thailand) Public Co. Ltd.

15th Floor, VorawatBuilding, 849 Silom Road,

Silom, Bangrak, Bangkok 10500 Thailand

Tel (66) 2 2268 0999 Fax: (66) 2 2268 0921

www.phillip.co.th

FRANCE: King & Shaxson Capital Ltd.

3rd Floor, 35 Rue de la Bienfaisance

75008 Paris France

Tel (33) 1 4563 3100 Fax : (33) 1 4563 6017

www.kingandshaxson.com

UNITED KINGDOM: King & Shaxson Ltd.

6th Floor, Candlewick House, 120 Cannon Street

London, EC4N 6AS

Tel (44) 20 7929 5300 Fax: (44) 20 7283 6835

www.kingandshaxson.com

UNITED STATES: Phillip Futures Inc.

141 W Jackson Blvd Ste 3050

The Chicago Board of TradeBuilding

Chicago, IL 60604 USA

Tel (1) 312 356 9000 Fax: (1) 312 356 9005

AUSTRALIA: PhillipCapital Australia

Level 10, 330 Collins Street

Melbourne, VIC 3000, Australia

Tel: (61) 3 8633 9800 Fax: (61) 3 8633 9899

www.phillipcapital.com.au

SRI LANKA: Asha Phillip Securities Limited

Level 4, Millennium House, 46/58 Navam Mawatha,

Colombo 2, Sri Lanka

Tel: (94) 11 2429 100 Fax: (94) 11 2429 199

www.ashaphillip.net/home.htm

INDIA

PhillipCapital (India) Private Limited

No. 1, 18th Floor, Urmi Estate, 95 Ganpatrao Kadam Marg, Lower Parel West, Mumbai 400013

Tel: (9122) 2300 2999 Fax: (9122) 6667 9955 www.phillipcapital.in

Management(91 22) 2483 1919

Kinshuk Bharti Tiwari (Head – Institutional Equity) (91 22) 6667 9946

(91 22) 6667 9735

Research IT Services Pharma & Speciality Chem

Dhawal Doshi (9122) 6667 9769 Vibhor Singhal (9122) 6667 9949 Surya Patra (9122) 6667 9768

Nitesh Sharma, CFA (9122) 6667 9965 Shyamal Dhruve (9122) 6667 9992 Mehul Sheth (9122) 6667 9996

Banking, NBFCs Infrastructure Strategy

Manish Agarwalla (9122) 6667 9962 Vibhor Singhal (9122) 6667 9949 Naveen Kulkarni, CFA, FRM (9122) 6667 9947

Pradeep Agrawal (9122) 6667 9953 Deepak Agarwal (9122) 6667 9944 Telecom

Paresh Jain (9122) 6667 9948 Logistics, Transportation & Midcap Naveen Kulkarni, CFA, FRM (9122) 6667 9947

Consumer & Retail Vikram Suryavanshi (9122) 6667 9951 Manoj Behera (9122) 6667 9973

Naveen Kulkarni, CFA, FRM (9122) 6667 9947 Media Technicals

Jubil Jain (9122) 6667 9766 Manoj Behera (9122) 6667 9973 Subodh Gupta, CMT (9122) 6667 9762

Preeyam Tolia (9122) 6667 9950 Metals Production Manager

Cement Dhawal Doshi (9122) 6667 9769 Ganesh Deorukhkar (9122) 6667 9966

Vaibhav Agarwal (9122) 6667 9967 Yash Doshi (9122) 6667 9987 Editor

Economics Mid-Caps & Database Manager Roshan Sony 98199 72726

Anjali Verma (9122) 6667 9969 Deepak Agarwal (9122) 6667 9944 Sr. Manager – Equities Support

Engineering, Capital Goods Oil & Gas Rosie Ferns (9122) 6667 9971

Jonas Bhutta (9122) 6667 9759 Sabri Hazarika (9122) 6667 9756

Vikram Rawat (9122) 6667 9986

Sales & Distribution Ashvin Patil (9122) 6667 9991 Sales Trader Zarine Damania (9122) 6667 9976

Shubhangi Agrawal (9122) 6667 9964 Dilesh Doshi (9122) 6667 9747 Bharati Ponda (9122) 6667 9943

Kishor Binwal (9122) 6667 9989 Suniil Pandit (9122) 6667 9745

Bhavin Shah (9122) 6667 9974

Ashka Mehta Gulati (9122) 6667 9934 Execution

Archan Vyas (9122) 6667 9785 Mayur Shah (9122) 6667 9945

Corporate Communications

Vineet Bhatnagar (Managing Director)

Jignesh Shah (Head – Equity Derivatives)

Automobiles

Page | 31 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Disclosures and Disclaimers PhillipCapital (India) Pvt. Ltd. has three independent equity research groups: Institutional Equities, Institutional Equity Derivatives, and Private Client Group. This report has been prepared by Institutional Equities Group. The views and opinions expressed in this document may, may not match, or may be contrary at times with the views, estimates, rating, and target price of the other equity research groups of PhillipCapital (India) Pvt. Ltd.

This report is issued by PhillipCapital (India) Pvt. Ltd., which is regulated by the SEBI. PhillipCapital (India) Pvt. Ltd. is a subsidiary of Phillip (Mauritius) Pvt. Ltd. References to "PCIPL" in this report shall mean PhillipCapital (India) Pvt. Ltd unless otherwise stated. This report is prepared and distributed by PCIPL for information purposes only, and neither the information contained herein, nor any opinion expressed should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment, or derivatives. The information and opinions contained in the report were considered by PCIPL to be valid when published. The report also contains information provided to PCIPL by third parties. The source of such information will usually be disclosed in the report. Whilst PCIPL has taken all reasonable steps to ensure that this information is correct, PCIPL does not offer any warranty as to the accuracy or completeness of such information. Any person placing reliance on the report to undertake trading does so entirely at his or her own risk and PCIPL does not accept any liability as a result. Securities and Derivatives markets may be subject to rapid and unexpected price movements and past performance is not necessarily an indication of future performance.

This report does not regard the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors must undertake independent analysis with their own legal, tax, and financial advisors and reach their own conclusions regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realised. Under no circumstances can it be used or considered as an offer to sell or as a solicitation of any offer to buy or sell the securities mentioned within it. The information contained in the research reports may have been taken from trade and statistical services and other sources, which PCIL believe is reliable. PhillipCapital (India) Pvt. Ltd. or any of its group/associate/affiliate companies do not guarantee that such information is accurate or complete and it should not be relied upon as such. Any opinions expressed reflect judgments at this date and are subject to change without notice.

Important: These disclosures and disclaimers must be read in conjunction with the research report of which it forms part. Receipt and use of the research report is subject to all aspects of these disclosures and disclaimers. Additional information about the issuers and securities discussed in this research report is available on request.

Certifications: The research analyst(s) who prepared this research report hereby certifies that the views expressed in this research report accurately reflect the research analyst’s personal views about all of the subject issuers and/or securities, that the analyst(s) have no known conflict of interest and no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the specific views or recommendations contained in this research report.

Additional Disclosures of Interest: Unless specifically mentioned in Point No. 9 below: 1. The Research Analyst(s), PCIL, or its associates or relatives of the Research Analyst does not have any financial interest in the company(ies) covered in

this report. 2. The Research Analyst, PCIL or its associates or relatives of the Research Analyst affiliates collectively do not hold more than 1% of the securities of the

company (ies)covered in this report as of the end of the month immediately preceding the distribution of the research report. 3. The Research Analyst, his/her associate, his/her relative, and PCIL, do not have any other material conflict of interest at the time of publication of this

research report. 4. The Research Analyst, PCIL, and its associates have not received compensation for investment banking or merchant banking or brokerage services or for

any other products or services from the company(ies) covered in this report, in the past twelve months. 5. The Research Analyst, PCIL or its associates have not managed or co-managed in the previous twelve months, a private or public offering of securities for

the company (ies) covered in this report. 6. PCIL or its associates have not received compensation or other benefits from the company(ies) covered in this report or from any third party, in

connection with the research report. 7. The Research Analyst has not served as an Officer, Director, or employee of the company (ies) covered in the Research report. 8. The Research Analyst and PCIL has not been engaged in market making activity for the company(ies) covered in the Research report. 9. Details of PCIL, Research Analyst and its associates pertaining to the companies covered in the Research report:

Sr. no. Particulars Yes/No

1 Whether compensation has been received from the company(ies) covered in the Research report in the past 12 months for investment banking transaction by PCIL

No

2 Whether Research Analyst, PCIL or its associates or relatives of the Research Analyst affiliates collectively hold more than 1% of the company(ies) covered in the Research report

No

3 Whether compensation has been received by PCIL or its associates from the company(ies) covered in the Research report No

4 PCIL or its affiliates have managed or co-managed in the previous twelve months a private or public offering of securities for the company(ies) covered in the Research report

No

5 Research Analyst, his associate, PCIL or its associates have received compensation for investment banking or merchant banking or brokerage services or for any other products or services from the company(ies) covered in the Research report, in the last twelve months

No

Independence: PhillipCapital (India) Pvt. Ltd. has not had an investment banking relationship with, and has not received any compensation for investment banking services from, the subject issuers in the past twelve (12) months, and PhillipCapital (India) Pvt. Ltd does not anticipate receiving or intend to seek compensation for investment banking services from the subject issuers in the next three (3) months. PhillipCapital (India) Pvt. Ltd is not a market maker in the securities mentioned in this research report, although it, or its affiliates/employees, may have positions in, purchase or sell, or be materially interested in any of the securities covered in the report.

Suitability and Risks: This research report is for informational purposes only and is not tailored to the specific investment objectives, financial situation or particular requirements of any individual recipient hereof. Certain securities may give rise to substantial risks and may not be suitable for certain investors. Each investor must make its own determination as to the appropriateness of any securities referred to in this research report based upon the legal, tax and accounting considerations applicable to such investor and its own investment objectives or strategy, its financial situation and its investing experience. The value of any security may be positively or adversely affected by changes in foreign exchange or interest rates, as well as by other financial, economic, or political factors. Past performance is not necessarily indicative of future performance or results.

Page | 32 | PHILLIPCAPITAL INDIA RESEARCH

PARAG MILK FOODS INITIATING COVERAGE

Sources, Completeness and Accuracy: The material herein is based upon information obtained from sources that PCIPL and the research analyst believe to be reliable, but neither PCIPL nor the research analyst represents or guarantees that the information contained herein is accurate or complete and it should not be relied upon as such. Opinions expressed herein are current opinions as of the date appearing on this material, and are subject to change without notice. Furthermore, PCIPL is under no obligation to update or keep the information current. Without limiting any of the foregoing, in no event shall PCIL, any of its affiliates/employees or any third party involved in, or related to computing or compiling the information have any liability for any damages of any kind including but not limited to any direct or consequential loss or damage, however arising, from the use of this document.

Copyright: The copyright in this research report belongs exclusively to PCIPL. All rights are reserved. Any unauthorised use or disclosure is prohibited. No reprinting or reproduction, in whole or in part, is permitted without the PCIPL’s prior consent, except that a recipient may reprint it for internal circulation only and only if it is reprinted in its entirety.

Caution: Risk of loss in trading/investment can be substantial and even more than the amount / margin given by you. The recipient should carefully consider whether trading/investment is appropriate for the recipient in light of the recipient’s experience, objectives, financial resources and other relevant circumstances. PCIPL and any of its employees, directors, associates, group entities, or affiliates shall not be liable for losses, if any, incurred by the recipient. The recipient is further cautioned that trading/investments in financial markets are subject to market risks and are advised to seek trading/investment advice before investing. There is no guarantee/assurance as to returns or profits or capital protection or appreciation. PCIPL and any of its employees, directors, associates, group entities, affiliates are not inducing the recipient for trading/investing in the financial market(s). Trading/Investment decision is the sole responsibility of the recipient.