Institutional Equity Research Earnings Update · Find CIBC research on Bloomberg, Reuters,...

23

Find CIBC research on Bloomberg, Reuters, firstcall.com CIBC World Markets Inc., P.O. Box 500, 161 Bay Street, Brookfield Place, Toronto, Canada M5J 2S8 (416) 594-7000 and ResearchCentral.cibcwm.com Institutional Equity Research Earnings Update December 5, 2011 Technology Hardware Wi-LAN Inc. A Good Buy, Below The NAV Wi-LAN's share price is attractive, trading below its signed deals + cash NAV of $6.11 (discounted 5%). Approximately 80% of WIN's contracts are fixed, meaning its outlook will be resistant to economic swings. Our research coverage is reinstated with a SO rating and price target of $10. 2012 catalysts would be signing new licenses. WIN has four active litigations with 14 defendants in areas such as wireless (CDMA, 3GPP, 4G) and its V-Chip, including some major players. License agreements are expected from both new OEMs and renewals for agreements set to expire. Our view is that present value of WIN's licensing pipeline is at least $6 per share (discounted 15%). The exact timing of future agreements is difficult to predict though. Deals that are likely to be signed sooner include 1) renewals with Nokia & RIM and 2) new wireless deals with HTC and others. Our SO rating and $10 PT are unchanged. WIN's price has pulled back on flat Q4 guidance and no recent signings. The shares should be bought now as there is no value being given to any future signings for 2012. Stock Price Performance Source: Re uters All figures in Canadian dollars, unless otherwise stated. 11-113255 © 2011 CIBC World Markets does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. See "Important Disclosures" section at the end of this report for important required disclosures, including potential conflicts of interest. See "Price Target Calculation" and "Key Risks to Price Target" sections at the end of this report, where applicable. Todd Coupland, CFA 1 (416) 956-6025 [email protected] Robin Manson-Hing 1 (416) 594-7232 [email protected] Stock Rating: Sector Outperformer Sector Weighting: Market Weight 12-18 mo. Price Target $10. 00 WIN-TSX (12/5/11) $5.51 Key Indices: NASDAQ, Toronto 3-5-Yr. EPS Gr. Rate (E) NM 52-week Range $4.18-$9.56 Shares Outstanding 123. 6M Float 123. 6M Shrs Av g. Daily Trading Vol. 1,113,005 Market Capitalization $681.0M Div idend/Div Yield $0.10 / 1.8% Fiscal Year Ends December Book Value $2.76 per Shr 2009 ROE (E) NM N et C ash $197.00M Preferred N il Common Equity $340.8M C onv ertible Av ailable No Earnings Per Share Prev Current 2010 $0.05A 2011 $0.62E $0.62E 2012 $0.79E $0.51E P/E 2010 NM 2011 8.9x 8.9x 2012 7.0x 10.8x Company Description Wi-LAN Inc. is an IP licensing firm focused on its core patent areas including V-C hip, C DMA, WiFi, DSL, WiMAX, Bluetooth and 3GPP technologies. www.wi-lan.com

Transcript of Institutional Equity Research Earnings Update · Find CIBC research on Bloomberg, Reuters,...

Find CIBC research on Bloomberg, Reuters, firstcall.com CIBC World Markets Inc., P.O. Box 500, 161 Bay Street, Brookfield Place, Toronto, Canada M5J 2S8 (416) 594-7000

and ResearchCentral.cibcwm.com

Institutional Equity Research

Earnings Update

December 5, 2011 Technology Hardware

Wi-LAN Inc. A Good Buy, Below The NAV

Wi-LAN's share price is attractive, trading below its signed deals + cash NAV

of $6.11 (discounted 5%). Approximately 80% of WIN's contracts are fixed,

meaning its outlook will be resistant to economic swings. Our research

coverage is reinstated with a SO rating and price target of $10.

2012 catalysts would be signing new licenses. WIN has four active

litigations with 14 defendants in areas such as wireless (CDMA, 3GPP, 4G)

and its V-Chip, including some major players. License agreements are

expected from both new OEMs and renewals for agreements set to expire.

Our view is that present value of WIN's licensing pipeline is at least $6 per

share (discounted 15%). The exact timing of future agreements is difficult

to predict though. Deals that are likely to be signed sooner include 1)

renewals with Nokia & RIM and 2) new wireless deals with HTC and others.

Our SO rating and $10 PT are unchanged. WIN's price has pulled back on

flat Q4 guidance and no recent signings. The shares should be bought now

as there is no value being given to any future signings for 2012.

Stock Price Performance

Source: Reuters All figures in Canadian dollars, unless otherwise stated. 11-113255 © 2011

CIBC World Markets does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may

have a conflict of interest that could affect the objectivity of this report.

Investors should consider this report as only a single factor in making their

investment decision.

See "Important Disclosures" section at the end of this report for important

required disclosures, including potential conflicts of interest.

See "Price Target Calculation" and "Key Risks to Price Target" sections at the

end of this report, where applicable.

Todd Coupland, CFA 1 (416) 956-6025 [email protected]

Robin Manson-Hing 1 (416) 594-7232 [email protected]

Stock Rating:

Sector Outperformer

Sector Weighting:

Market Weight 12-18 mo. Price Target $10.00

WIN-TSX (12/5/11) $5.51

Key Indices: NASDAQ, Toronto

3-5-Yr. EPS Gr. Rate (E) NM

52-week Range $4.18-$9.56 Shares Outstanding 123.6M

Float 123.6M Shrs

Avg. Daily Trading Vol. 1,113,005 Market Capitalization $681.0M

Div idend/Div Yield $0.10 / 1.8%

Fiscal Year Ends December Book Value $2.76 per Shr

2009 ROE (E) NM

Net Cash $197.00M Preferred Nil

Common Equity $340.8M

Convertible Available No Earnings Per Share Prev Current

2010 $0.05A 2011 $0.62E $0.62E

2012 $0.79E $0.51E

P/E 2010 NM 2011 8.9x 8.9x 2012 7.0x 10.8x

Company Description Wi-LAN Inc. is an IP licensing firm focused on its core patent areas including V-Chip, CDMA, WiFi, DSL, WiMAX, Bluetooth and 3GPP technologies.

www.wi-lan.com

A Good Buy, Below The NAV - December 05, 2011

2

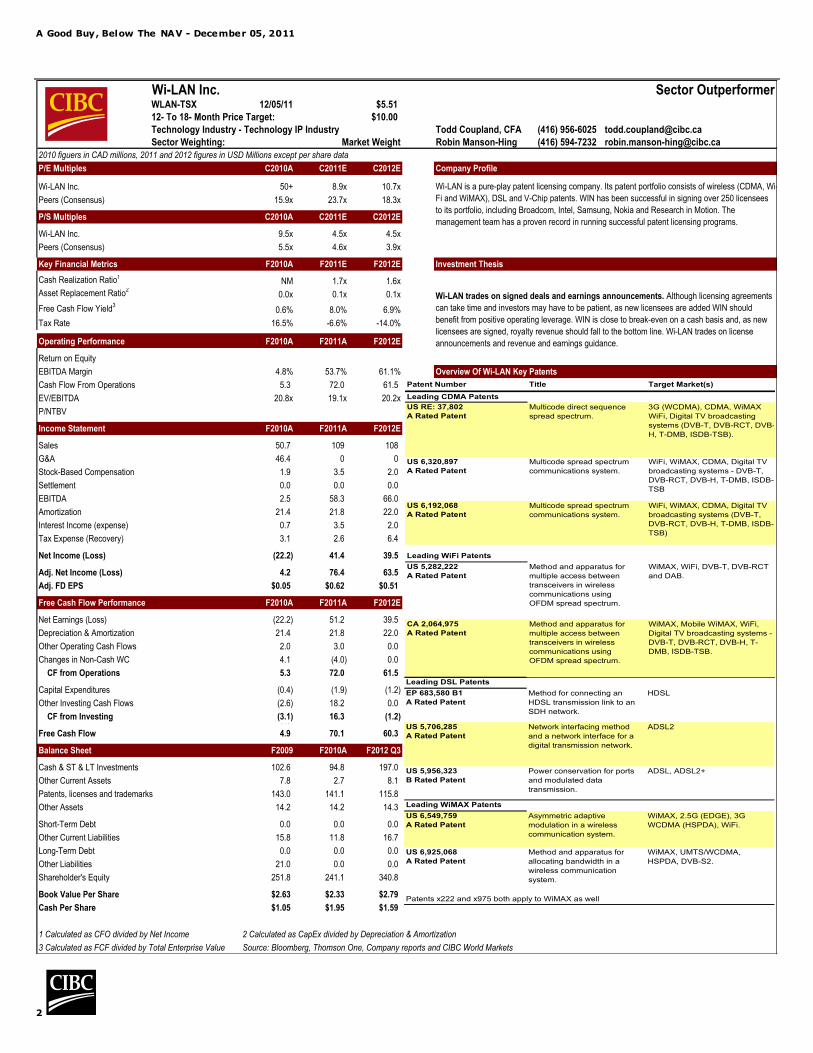

Wi-LAN Inc. Sector OutperformerWLAN-TSX 12/05/11 $5.51

12- To 18- Month Price Target: $10.00

Technology Industry - Technology IP Industry Todd Coupland, CFA (416) 956-6025 [email protected]

Sector Weighting: Market Weight Robin Manson-Hing (416) 594-7232 [email protected]

2010 figuers in CAD millions, 2011 and 2012 figures in USD Millions except per share data

P/E Multiples C2010A C2011E C2012E

Wi-LAN Inc. 50+ 8.9x 10.7x

Peers (Consensus) 15.9x 23.7x 18.3x

P/S Multiples C2010A C2011E C2012E

Wi-LAN Inc. 9.5x 4.5x 4.5x

Peers (Consensus) 5.5x 4.6x 3.9xTraditional CDN Energy Utilities (Consensus)18.1x 18.1x 18.1x 18.1x 18.1x 15.6x

Key Financial Metrics F2010A F2011E F2012E Investment Thesis

Cash Realization Ratio1NM 1.7x 1.6x

Asset Replacement Ratio2

0.0x 0.1x 0.1x

Free Cash Flow Yield3

0.6% 8.0% 6.9%

Tax Rate 16.5% -6.6% -14.0%

Operating Performance F2010A F2011A F2012E

Return on Equity

EBITDA Margin 4.8% 53.7% 61.1%

Cash Flow From Operations 5.3 72.0 61.5

EV/EBITDA 20.8x 19.1x 20.2x

P/NTBV 2.7x 2.8x 2.0x

Income Statement F2010A F2011A F2012E

Sales 50.7 109 108

G&A 46.4 0 0

Stock-Based Compensation 1.9 3.5 2.0

Settlement 0.0 0.0 0.0

EBITDA 2.5 58.3 66.0

Amortization 21.4 21.8 22.0

Interest Income (expense) 0.7 3.5 2.0

Tax Expense (Recovery) 3.1 2.6 6.4

Net Income (Loss) (22.2) 41.4 39.5

Adj. Net Income (Loss) 4.2 76.4 63.5

Adj. FD EPS $0.05 $0.62 $0.51

Free Cash Flow Performance F2010A F2011A F2012E

Net Earnings (Loss) (22.2) 51.2 39.5

Depreciation & Amortization 21.4 21.8 22.0

Other Operating Cash Flows 2.0 3.0 0.0

Changes in Non-Cash WC 4.1 (4.0) 0.0

CF from Operations 5.3 72.0 61.521.4

Capital Expenditures (0.4) (1.9) (1.2)

Other Investing Cash Flows (2.6) 18.2 0.0

CF from Investing (3.1) 16.3 (1.2)0.0

Free Cash Flow 4.9 70.1 60.3

Balance Sheet F2009 F2010A F2012 Q3

Cash & ST & LT Investments 102.6 94.8 197.0

Other Current Assets 7.8 2.7 8.1

Patents, licenses and trademarks 143.0 141.1 115.8

Other Assets 14.2 14.2 14.3

Short-Term Debt 0.0 0.0 0.0

Other Current Liabilities 15.8 11.8 16.7

Long-Term Debt 0.0 0.0 0.0

Other Liabilities 21.0 0.0 0.0

Shareholder's Equity 251.8 241.1 340.8

Book Value Per Share $2.63 $2.33 $2.79

Cash Per Share $1.05 $1.95 $1.59

1 Calculated as CFO divided by Net Income 2 Calculated as CapEx divided by Depreciation & Amortization

3 Calculated as FCF divided by Total Enterprise Value Source: Bloomberg, Thomson One, Company reports and CIBC World Markets

Wi-LAN trades on signed deals and earnings announcements. Although licensing agreements

can take time and investors may have to be patient, as new licensees are added WIN should

benefit from positive operating leverage. WIN is close to break-even on a cash basis and, as new

licensees are signed, royalty revenue should fall to the bottom line. Wi-LAN trades on license

announcements and revenue and earnings guidance.

Overview Of Wi-LAN Key Patents

Company Profile

Wi-LAN is a pure-play patent licensing company. Its patent portfolio consists of wireless (CDMA, Wi-

Fi and WiMAX), DSL and V-Chip patents. WIN has been successful in signing over 250 licensees

to its portfolio, including Broadcom, Intel, Samsung, Nokia and Research in Motion. The

management team has a proven record in running successful patent licensing programs.

Patent Number Title Target Market(s)

Leading CDMA Patents

US RE: 37,802

A Rated Patent

Multicode direct sequence

spread spectrum.

3G (WCDMA), CDMA, WiMAX

WiFi, Digital TV broadcasting

systems (DVB-T, DVB-RCT, DVB-

H, T-DMB, ISDB-TSB).

US 6,320,897

A Rated Patent

Multicode spread spectrum

communications system.

WiFi, WiMAX, CDMA, Digital TV

broadcasting systems - DVB-T,

DVB-RCT, DVB-H, T-DMB, ISDB-

TSB

US 6,192,068

A Rated Patent

Multicode spread spectrum

communications system.

WiFi, WiMAX, CDMA, Digital TV

broadcasting systems (DVB-T,

DVB-RCT, DVB-H, T-DMB, ISDB-

TSB)

Leading WiFi Patents

US 5,282,222

A Rated Patent

Method and apparatus for

multiple access between

transceivers in wireless

communications using

OFDM spread spectrum.

WiMAX, WiFi, DVB-T, DVB-RCT

and DAB.

CA 2,064,975

A Rated Patent

Method and apparatus for

multiple access between

transceivers in wireless

communications using

OFDM spread spectrum.

WiMAX, Mobile WiMAX, WiFi,

Digital TV broadcasting systems -

DVB-T, DVB-RCT, DVB-H, T-

DMB, ISDB-TSB.

Leading DSL Patents

EP 683,580 B1

A Rated Patent

Method for connecting an

HDSL transmission link to an

SDH network.

HDSL

US 5,706,285

A Rated Patent

Network interfacing method

and a network interface for a

digital transmission network.

ADSL2

US 5,956,323

B Rated Patent

Power conservation for ports

and modulated data

transmission.

ADSL, ADSL2+

Leading WiMAX Patents

US 6,549,759

A Rated Patent

Asymmetric adaptive

modulation in a wireless

communication system.

WiMAX, 2.5G (EDGE), 3G

WCDMA (HSPDA), WiFi.

US 6,925,068

A Rated Patent

Method and apparatus for

allocating bandwidth in a

wireless communication

system.

WiMAX, UMTS/WCDMA,

HSPDA, DVB-S2.

Patents x222 and x975 both apply to WiMAX as well

A Good Buy, Below The NAV - December 05, 2011

3

Our View in Summary

Once again we reinforce our view that Wi-LAN (WIN-SO) should trade at least at its signed deals plus net cash value and that the share price will track any

significant future signings. With the MOSAID acquisition attempt behind them, Wi-LAN can now turn its full attention to the dozens of other parties potentially

infringing one of their 40 patent families containing over 1,400 patents.

Recent events whilst we were restricted included Wi-LAN reporting an in-line Q3

but lowering its 2011 guidance range by $5 million to $105MM - $110MM in

revenue and adjusted earnings to $70MM - $75MM. This did not come as a surprise to us as WIN has not signed a major licensing deal since our last note in

August and previous expectations of coming to a settlement with LG on V-Chip have been pushed back. Our updated forecast now reflects the current run rate

of Wi-LAN‟s business. Any future signings would be upside to our 2012 forecast.

Our SO recommendation and price target of $10 remain unchanged and we believe the shares should be bought.

2012 Catalysts, Renewals and New Deals For 2012, specific timing on when agreements will be inked is difficult to predict.

In spite of that, there are a number of catalysts that investors should keep in

mind. For the expiring agreements, we know the dates. For current litigation we

know to focus on events which in the past have led parties on either side to

come to the table and sign licensing agreements. We believe investors should

focus on both during 2012. Exhibit 1 shows the upcoming litigation schedule.

Renewal Opportunities - Nokia‟s license is coming due at the end of

December 2011. We expect a significantly larger renewal than the $15 million in

cash they received from Nokia in 2006. Other material renewal dates include

RIM (est. August 2013 for major patents) and Samsung (est. 2014). In each

case, these agreements are expected to be substantially larger than the original

deals. In the past, these OEMs signed very narrow agreements. Our rational for

a larger agreement is that Wi-LAN‟s patent portfolio has grown from 146 just

after the Nokia signing in 2006 to 370 patents in July of 2009 to over 1400

patents currently issued or pending. Many of these acquired patents cover

technologies dealing with various 2G, 3G (general GSM patents, EDGE,

CDMA2000, HSPA) and 4G (LTE and WiMAX) technologies as well as in areas

such as Bluetooth, mobile messaging and wireless data transmission that all

read on mobile devices. It is our understanding that Wi-LAN will focus on

bringing a number of technologies into these renegotiations that should

ultimately yield higher royalty rates.

Legal Activity for 2012 - The 3GPP Markman hearing (a pre-trial hearing on

the appropriate meanings of relevant keywords used in a patent claim

determined by the Judge) in April will give us a better idea as to the strength of

Wi-LAN‟s case. The 3GPP case refers to patents covering wireless communication

products that are compliant with 3GPP standards, including mobile handsets and

base stations. The complaint named Alcatel-Lucent and Ericsson base stations

involving GSM/EDGE, WCDMA/HSPA and LTE (ex: ALU‟s 9926 Distributed Base

Station, Ericsson‟s RBS 3000 and RBS 6000 as well as Sony Ericsson phones

such as the Xperia X10 and Vivaz). Generally speaking, once the Markman

hearing has passed, the Judge‟s written ruling can take about six weeks to

complete implying a mid-May verdict. Following the ruling either side will assess

their respective positions and then decide if it makes sense to settle or push on

towards the trial.

A Good Buy, Below The NAV - December 05, 2011

4

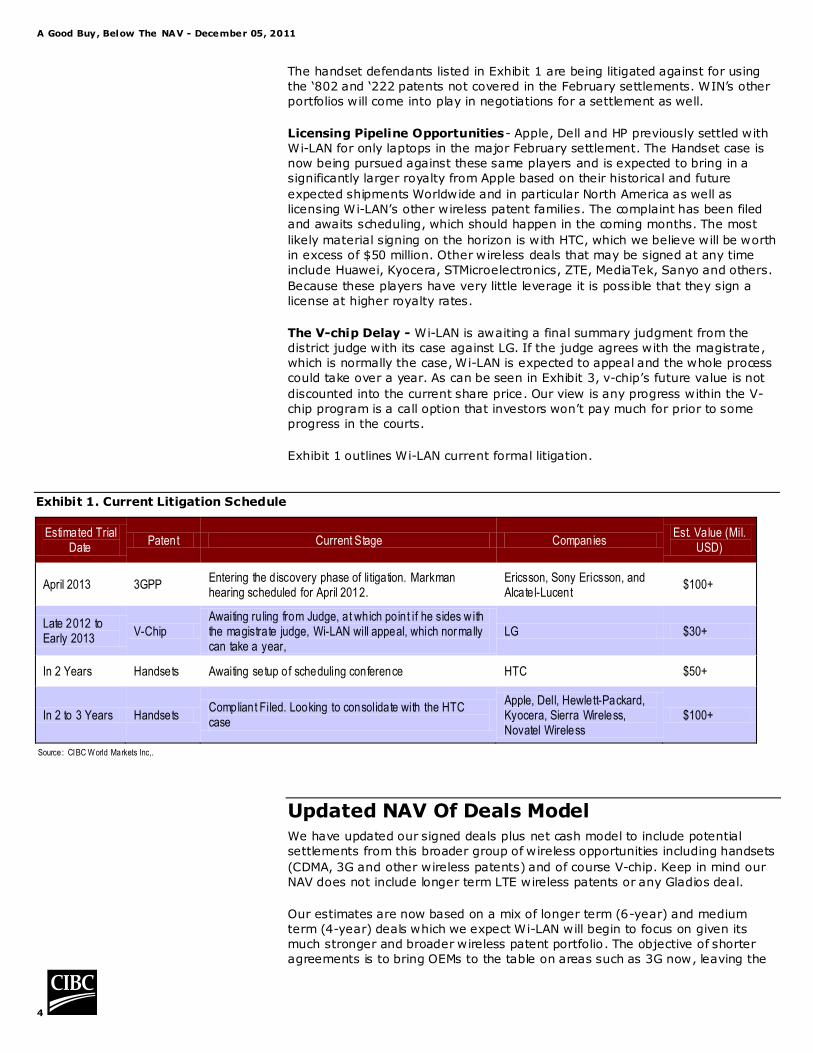

The handset defendants listed in Exhibit 1 are being litigated against for using

the „802 and „222 patents not covered in the February settlements. WIN‟s other

portfolios will come into play in negotiations for a settlement as well.

Licensing Pipeline Opportunities- Apple, Dell and HP previously settled with

Wi-LAN for only laptops in the major February settlement. The Handset case is

now being pursued against these same players and is expected to bring in a

significantly larger royalty from Apple based on their historical and future

expected shipments Worldwide and in particular North America as well as

licensing Wi-LAN‟s other wireless patent families. The complaint has been filed

and awaits scheduling, which should happen in the coming months. The most

likely material signing on the horizon is with HTC, which we believe will be worth

in excess of $50 million. Other wireless deals that may be signed at any time

include Huawei, Kyocera, STMicroelectronics, ZTE, MediaTek, Sanyo and others.

Because these players have very little leverage it is possible that they sign a

license at higher royalty rates.

The V-chip Delay - Wi-LAN is awaiting a final summary judgment from the

district judge with its case against LG. If the judge agrees with the magistrate,

which is normally the case, Wi-LAN is expected to appeal and the whole process

could take over a year. As can be seen in Exhibit 3, v-chip‟s future value is not

discounted into the current share price. Our view is any progress within the V-

chip program is a call option that investors won‟t pay much for prior to some

progress in the courts.

Exhibit 1 outlines Wi-LAN current formal litigation.

Exhibit 1. Current Litigation Schedule

Estimated Trial Date

Patent Current Stage Companies Est. Value (Mil.

USD)

April 2013 3GPP Entering the discovery phase of litigation. Markman hearing scheduled for April 2012.

Ericsson, Sony Ericsson, and Alcatel-Lucent

$100+

Late 2012 to Early 2013

V-Chip Awaiting ruling from Judge, at which point if he sides w ith the magistrate judge, Wi-LAN will appeal, which normally can take a year,

LG $30+

In 2 Years Handsets Awaiting setup of scheduling conference HTC $50+

In 2 to 3 Years Handsets Compliant Filed. Looking to consolidate with the HTC case

Apple, Dell, Hewlett-Packard, Kyocera, Sierra Wireless, Novatel Wireless

$100+

Source : CIBC World Markets Inc,.

Updated NAV Of Deals Model We have updated our signed deals plus net cash model to include potential

settlements from this broader group of wireless opportunities including handsets

(CDMA, 3G and other wireless patents) and of course V-chip. Keep in mind our

NAV does not include longer term LTE wireless patents or any Gladios deal.

Our estimates are now based on a mix of longer term (6-year) and medium

term (4-year) deals which we expect Wi-LAN will begin to focus on given its

much stronger and broader wireless patent portfolio. The objective of shorter

agreements is to bring OEMs to the table on areas such as 3G now, leaving the

A Good Buy, Below The NAV - December 05, 2011

5

less mature 4G (or LTE) infringement to deal with in follow-on renewal

agreements. This shift by Wi-LAN has merit as it is clearly designed to

encourage deals sooner rather than getting stuck in protracted negotiations on

issues and market outlooks such as the 4G market that cannot be known at this

time.

Deducting Expenses: In Q3, Wi-LAN announced $28 million ($0.23/share) in

payments to McKool Smith lawyers for their contribution in the Wi-Fi case. Wi-

LAN will make roughly 20 equal quarterly payments. We are now deducting this

amount from our NAV as it is a specific and known expense related to the signed

Wi-Fi agreements of late 2010 and 2011.

The balance of Wi-LAN expenses we do not deduct from our NAV. Our issue in

doing this is determining which expenses should be deducted. Our NAV is based

on a finite number of four to six year agreements that excludes many

opportunities. We also assume no renewals or terminal value. By contrast, total

expenses cover all the opportunities both short and long term. For those

investors who still would like an idea on the impact we present the value of that

calculation here. The present value of five years of total operating expenses

(including McKool Smith) at the current run rate at an APR of 15% is $139

million or $1.12 per share.

A Good Buy, Below The NAV - December 05, 2011

6

Exhibit 2. NAV Of Signed And Potential Deals Plus Net Cash

Wi-LAN (WIN-TSX)

Avg. Revenue Per

Year

Value

Remaining

($Mil.)

Per ShareAvg. Revenue

Per Year

Value Expected

($Mil.)Per Share

Major Wireless Deals Signed in '802/'222 EDTX Case Major Unsigned Wireless Deals

Broadcom $20.00 $100.74 $0.82 STMicroelectronics $4.22 $25.36 $0.21

Atheros $13.52 $67.72 $0.55 MediaTek $1.80 $10.80 $0.09

Intel $13.02 $65.49 $0.53 ZTE $2.98 $17.92 $0.15

Marvell $7.55 $37.76 $0.31 Pantech $1.16 $6.99 $0.06

CSR $5.72 $29.42 $0.24 Sanyo $1.02 $6.12 $0.05

UTStarcom $0.60 $12.12 $0.10 Other Semis $5.84 $35.11 $0.28

Realtek $2.45 $12.31 $0.10 Total Value of Remaining of Unsigned Deals $17.03 $102.30 $0.83

Ralink $1.52 $7.58 $0.06 3GPP (Formal Litigation Began October 2010)

2Wire $0.78 $4.56 $0.04 Alcatel-Lucent $5.13 $30.79 $0.25

Netgear $0.98 $5.70 $0.05 Ericsson $7.80 $46.77 $0.38

Acer $0.99 $4.73 $0.04 SonyEricsson $3.02 $18.11 $0.15

Dell - Laptops only $0.37 $1.98 $0.02 Total Value of Remaining $15.95 $95.68 $0.77

Apple - Laptops only $1.33 $6.45 $0.05 Wireless (Formal Litigation Began September 2011)

Hewlett-Packard - Laptops only $0.93 $4.95 $0.04 Apple (4-Year, no LTE) $17.05 $68.20 $0.55

D-Link $0.59 $3.42 $0.03 Dell $0.63 $3.76 $0.03

Belkin $0.39 $2.28 $0.02 Hewlett-Packard $0.97 $5.84 $0.05

T.I. $8.80 $0.07 HTC (4-Year, no LTE) $11.60 $46.40 $0.38

Other Wireless Deals $0.40 $2.77 $0.02 Kyocera $3.18 $19.09 $0.15

Wireless Deals Signed $71.14 $378.77 $3.07 Novatel $0.91 $5.44 $0.04

Major Other Wireless / DSL Deals Signed Sierra $2.38 $14.25 $0.12

Motorola $5.84 $28.18 $0.23 Total Value of Remaining '802 & '222 $36.70 $162.97 $1.32

LG $4.80 $21.89 $0.18 Renewal Deals

Samsung $7.34 $14.60 $0.12 Nokia (4-Year Renewal, no LTE) $8.04 $32.15 $0.26

Cisco $2.39 $11.65 $0.09 Samsung (4-Year Renewal, no LTE) $17.41 $69.65 $0.56

Sharp $0.56 $4.19 $0.03 RIM (4-Year Renewal, no LTE) $12.53 $50.13 $0.41

RIM $0.68 $1.69 $0.01 Total Value of Major Upcoming Renewals $37.98 $151.93 $1.23

Asus $0.52 $0.99 $0.01 Est. Value of Unsigned Wireless Deals $107.66 $512.87 $4.15

Other Deals $2.28 $22.80 $0.18 Major Unsigned V-Chip

CDMA/Other Wireless Signed $24.41 $105.99 $0.86 Samsung (U.S. only) $12.08 $61.34 $0.50

V-Chip Signed Sony (U.S. only) $6.92 $35.11 $0.28

Funai $3.83 $26.82 $0.22 LG (North America) $5.20 $26.42 $0.21

AmTran $3.36 $22.62 $0.18 Panasonic (North America) $4.08 $20.71 $0.17

Sanyo V-chip $1.87 $16.84 $0.14 Toshiba (U.S. only) $4.17 $21.18 $0.17

Top Victory $1.37 $12.33 $0.10 Sharp (U.S. only) $2.72 $16.30 $0.13

Other v-Chip $2.47 $22.27 $0.18 Est. Value of V-Chip Market $35.17 $181.05 $1.47

V-Chip Signed $12.91 $100.88 $0.82 Signed And Unsigned Value Of The Opportunity

Cash & Short Term Investments $196.97 $1.59 Wireless $203 $998 $8.07

Value of Deals Signed + Cash $108 $782.61 $6.33 V-Chip $48 $282 $2.28

Less: McKool Smith Payments ($28.00) ($0.23) Cash & Short Term Investments $197 $1.59

Value of Deals Signed + Net Cash $108 $754.61 $6.11 Less: McKool Smith Payments ($28) ($0.23)

Value of Signed/Unsigned + Cash $251 $1,449 $11.72

Asset Value of Deals

Discounted at 5%

Value of Potential Deals

Discounted at 15%

Todd Coupland (416) 956-6025

Robin Manson-Hing (416) 594-7232

Source: Company reports and CIB C World Markets Inc.

Valuing Wi-LAN The Share Price Tracks the NAV: Exhibit 3 outlines the share performance

versus the NAV of signed deals plus net cash, showing that the share price has

indeed traded at or above its signed deals plus net cash value for most of the

past two years. Currently the share price has dropped below their signed deals

plus net cash value. We believe by entering the stock at these levels

investors will be positioned for future agreements and upside.

A Good Buy, Below The NAV - December 05, 2011

7

Exhibit 3. Share Price Versus NAV Of Signed Deals Plus Net Cash

Source: Company reports and CIB C World Markets Inc.

The V-Chip Delay Is Already Priced In: As mentioned previously, Assuming

LG prevails with its v-chip judgment, we fully expect Wi-LAN to file an appeal on

the merits that LG does in fact infringe in spite of its claim of its work around. It

will take a year or more for Wi-LAN to appeal any ruling in favor of LG. As result,

we see the v-chip opportunity pushed out as other major players who have not

signed a license are likely to take a wait and see approach. Note that in our

upside NAV, the remaining v-chip value is approximately $1.60 per share. This is

down from about $2 per share. The differences are a lower royalty rate

assumption and to a lesser extent lower TV sales. As can be seen from Exhibit 3,

investors have taken the v-chip opportunity out of their expectations and any

future signings of v-chip players listed in our NAV would be considered

upside.

Uses for the Cash

Wi-LAN continues to take a multi-pronged approach to patent acquisitions,

including:

1. Buy Patents: Direct purchases of patent portfolios as was done with

Motorola antenna and Glenayre wireless patents. It was mentioned last

quarter that they have signed partnerships in cloud computing, internet based technology and even medical patent opportunities.

A Good Buy, Below The NAV - December 05, 2011

8

2. Partner for Patents: The Gladios IP model is already making significant

inroads with two significant agreements with 01Communique and Poynt. It was said there are a number of other deals on the table and they are

now in the process of due diligence. We generally expect these

opportunities will take until 2013 or so to establish themselves as licensing programs.

3. Full M&A: Company acquisitions could also be on the horizon, to a

smaller extent than MOSAID. Recall the last significant acquisition made

by Wi-LAN was Tri-Vision (v-chip) for $108 million in 2007. Wi-LAN has stated that with their excess cash, M&A remains an option.

Q3 Results Revenue was aided by $1 million in brokerage revenue from the sale of patents

to one party. Perhaps the only surprise was the slightly lower-than-expected

litigation expense ($2.3MM vs. estimate of $3MM) that was countered by higher

R&D costs and G&A costs. The end result was an in-line quarter.

Exhibit 4. Q3 Results

Revenue ($Mil) Net Margin (%) Adjusted Net

Income ($Mil) Adj. EPS

Q3/11 Actual $27.8 81.8% $22.8 $0.18

Q3/10 - Year Ago $11.3 9.7% $1.1 $0.01

Y/Y Change 147% 7211 bps 1979%

Q2/11 - Quarter Ago $27.4 75.9% $20.8 $0.17

Q/Q Change 1% 591 bps 9%

Q4/11E - Consensus (7 estimates) $27.6 70.6% $19.5 $0.17

Actual Difference to Consensus 1% 1122 bps 17%

Q4/11E - Prior Estimate $28.0 75.4% $21.1 $0.17

Actual Difference to CIBC Est. -1% 646 bps 8%

Source : Thomson One and CIB C World Markets Inc.

A Good Buy, Below The NAV - December 05, 2011

9

Q4 Forecast The Q4 guidance implies no new business and slightly higher operating costs

which we have forecasted for.

Exhibit 5 Q4 Forecast

Revenue

($Mil) Net Margin

(%) Adjusted Net Income ($Mil)

Adj. EPS

Q4/11E Estimate $27.0 73.3% $19.8 $0.16

Q4/10 - Year Ago $11.2 -43.6% ($4.9) ($0.04)

Y/Y Change 141% 11690 bps -506%

Q3/11 - Quarter Ago $27.8 81.8% $22.8 $0.18

Q/Q Change -3% -854 bps -13%

Q4/11E - Consensus (7 estimates) $27.4 78.6% $21.5 $0.17

Difference to our Estimate -1% -526 bps -8%

Q4/11E - Implied Guidance Range $23.4 -

$28.4 47% - 79% $13.4 - $18.4 $0.11 - $0.15

Q4/11E - Implied Mid-Point $25.9 63.0% $15.9 $0.13

Difference to our Estimate 4% 16% 24%

Q4/11E - Prior Estimate $30.0 75.4% $22.6 $0.18

Actual Difference to CIBC Est. -10% -205 bps -12%

Consensus for Net Income and EPS is GAAP based.

2011 and 2012 Forecast We have lowered our 2012 forecast to take into account updated guidance, a

delayed v-chip opportunity, as well as payments to McKool Smith over the next

five years. Our 2012 forecast is conservative and is based on the current run

rate of Wi-LAN business. Any material signings would require us to move our

estimates higher.

Exhibit 6. F2011 and F2012 Forecast

Net

Revenue ($Mil)

Net Margin (%)

Adjusted Net Income ($Mil)

Adj. EPS

2010A $51 8.3% $4.2 $0.05

2011E

CIBC – new $109 70.4% $76.4 $0.62

Y/Y Change 114% 6213 bps 1726%

CIBC – prior $112 69.0% $78.4 $0.62

Change in Estimate -3% 138 bps -2%

Guidance Range $105 -

$110 61% - 71% $70 - $75 $0.57 - $0.61

Guidance Mid-Point $108 66.1% $72.5 $0.59

Prev ious Guidance Range $110 -

$115 65% - 73% $75 - $80 $0.61 - $0.66

Prev ious Guidance Mid-Point $113 69.0% $77.5 $0.64

In Comparison to our Estimate 4% -140 bps 1%

Consensus (7 Estimates) $105 71.1% $74.5 $0.58

Consensus vs. CIBC -4% 72 bps -3%

2012E

CIBC – new $108 58.8% $63.5 $0.51

Y/Y Change -1% -1155 bps -17%

CIBC – prior $134 74.0% $99 $0.79

Change in Estimate -19% -1522 bps -36%

Consensus (7 Estimates) $128 72.7% $92.7 $0.70

Consensus vs. CIBC -15% -1384 bps -31%

Source: Thomson One A nalytics and CIBC World Markets Inc.

A Good Buy, Below The NAV - December 05, 2011

10

Recommendation And Valuation

We maintain our Sector Outperformer rating and price target of $10.

Wi-LAN‟s share price is trading just below the value of its signed agreements

plus cash. The upside to our target is based on agreements that are highly likely

given the success that Wi-LAN has demonstrated to date in its key patent areas.

We have kept LG as a potential deal until an outcome has become clearer.

Price Target Calculation

Our price target of $10 is based on our portion of potential deals in the NAV that

can possibly be signed over the next 18 months plus pro forma cash per share

of $1.59 less McKool Smith payments and interest income of $0.01.

Another way to value Wi-LAN is to deduct the run rate of operating expenses

over the next five years ($1.12) off the PV of signed and unsigned deals plus

cash ($11.95) to come up with a price of $10.83.

Finally investors could look at peer comparison for valuation, for which 14x

F2012 EPS of $0.51 plus cash per share of $1.59 gives us $8.73. Peers are

trading at 18.3x C2012 EPS, although it should be noted that only about half of

WIN‟s 2012 EPS is taxed due to back losses carrying forward until H2/2012.

Again patent licensing peers trade at 23.7x and 18.3x 2011 and 2012 EPS. WIN

trades at 10.7x next year‟s EPS. Our view is Wi-LAN valuation will continue to

close in on its peer group given its growth in revenue and earnings, licensing

agreements and this management team‟s superior business execution. Also as

they sign new agreements, their NAV of signed deals plus cash will increase.

Key Risks To Price Target Ability To Sign Remaining Players In The Market: While the majority of

major wireless players are now signed by Wi-LAN, a number still remain

outstanding including Texas Instruments and HTC. Also there are a number of

other players that Wi-LAN has yet to go after including Pantech, ZTE, Kyocera

and potentially even Qualcomm or Apple. As well, there remain a number of

other significant players in v-chip and 3GPP that still exist.

Monetizing Future Patent Acquisitions: It tends to take over two years upon

patent acquisitions to monetize them. There is a risk in going to trial that the

patents are not deemed legitimate. If this were to happen with any of the major

significant remaining patent portfolios it would likely prove to be a negative

towards the stock price.

A Good Buy, Below The NAV - December 05, 2011

11

Exhibit 7. Forecast Model

Wi-LAN 2010A 2011E 2012E Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11 Q3/11 Q4/11E Q1/12E Q2/12E Q3/12E 0.15

FY End October 31 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12

Income Statement (CAD mlns up to 2010, USD mlns otherwise, except per share data)

Fixed revenue 22.0 23.0 22.3 23.0 23.0 23.0 23.0 23.0

Variable revenue 4.0 5.0 5.6 4.0 4.0 4.0 4.0 4.0

Top 10 Customers Revenue 35.2 12.4 9.8 9.5 22.4 21.7 21.5

# of Licensees Over 10% of Royalty Revenue 3 3 2 3 2 3 3

Royalties 46.9 13.9 10.5 11.3 11.2 26.3 27.4 26.8

Brokerage 3.8 2.5 1.3 0.0 1.0

Backlog

Revenue 50.7 108.6 108.0 16.5 11.8 11.3 11.2 26.3 27.4 27.8 27.0 27.0 27.0 27.0 27.0

Cash revenue

Non-cash revenue

Income Expenses

Patent Licencing 5.6 4.2 4.0 2.2 1.3 1.0 1.0 0.9 0.9 1.6 0.9 1.0 1.0 1.0 1.0

Litigation 29.8 17.9 12.0 4.0 6.8 7.0 12.0 11.4 2.3 1.2 3.0 3.0 3.0 3.0 3.0

McKool Smith Payments 0.0 6.0 1.5 1.5 1.5 1.5

Research and Development 3.8 6.1 8.0 0.9 0.8 0.8 1.2 1.3 1.5 1.9 1.5 2.0 2.0 2.0 2.0

G&A 7.2 10.0 10.0 1.8 1.9 1.6 2.0 2.3 2.7 2.7 2.3 2.5 2.5 2.5 2.5

Total operating expenses 46.4 38.2 40.0 8.9 10.8 10.4 16.2 15.8 7.4 7.3 7.7 10.0 10.0 10.0 10.0

Stock-based compensation 1.9 3.5 2.0 0.6 0.5 0.4 0.4 0.7 0.8 1.5 0.5 0.5 0.5 0.5 0.5

Realized FX loss (gain) (1.7)

Unrealized FX loss/(gain) 0.0 (0.2) 0.2 (0.1) 0.1 (2.1) (0.3) 12.7

EBITA 2.5 58.3 66.0 7.1 0.3 0.5 (5.5) 12.0 19.5 8.0 18.8 16.5 16.5 16.5 16.5

Amortization 21.4 21.8 22.0 5.3 5.4 5.4 5.4 5.1 5.5 5.7 5.5 5.5 5.5 5.5 5.5

EBIT (19.0) 36.5 44.0 1.8 (5.0) (4.9) (10.9) 6.9 14.0 2.3 13.3 11.0 11.0 11.0 11.0

Interest:

Interest income 0.7 3.5 2.0 0.2 0.1 0.2 0.2 0.3 0.5 2.2 0.5 0.5 0.5 0.5 0.5

Interest expense on long-term debt 0.8

Transaction costs 1.2

Accretion of debt discount 0.5

Unrealized gain on conversion feature (8.5)

Financing costs 3.6

Restructuring charges 0.8 0.8

Other interest expense

Earnings from continuing operations (19.0) 40.1 46.0 2.0 (4.9) (5.5) (10.7) 7.2 14.5 6.8 13.8 11.5 11.5 11.5 11.5

Deduct: Provision for future income tax recovery 0.0 0.0 0.9 (0.9) (13.6) 3.5

Deduct: Cumulative translation adjustment 9.8

Income Taxes 3.1 2.6 6.4 1.0 0.8 1.4 1.0 0.7 0.9 0.0 0.0 0.0 3.2 3.2

Deferred Taxes (1.4)

Net income (loss) (22.2) 41.4 39.5 1.1 (5.9) (6.2) (12.1) 10.0 10.3 7.317 13.8 11.5 11.5 8.3 8.3

Basic shares outstanding 103.3 121.4 123.0 102.1 102.8 103.3 103.4 117.1 122.3 123.4 123.0 123.0 123.0 123.0 123.0

Fully Diluted shares outstanding 103.3 123.5 123.6 103.6 102.8 103.3 103.4 119.9 124.8 125.6 123.6 123.6 123.6 123.6 123.6

Shares Outstanding End of Period 122.1 123.3 123.6

EPS - Basic ($0.21) $0.34 $0.32 $0.01 ($0.06) ($0.06) ($0.12) $0.09 $0.08 $0.06 $0.11 $0.09 $0.09 $0.07 $0.07

EPS - Fully Diluted ($0.21) $0.34 $0.32 $0.01 ($0.06) ($0.06) ($0.12) $0.08 $0.08 $0.06 $0.11 $0.09 $0.09 $0.07 $0.07

Adjusted Net Income

Net Income ($23.0) $41.4 $39.5 $1.1 ($5.9) ($6.2) ($12.1) $10.0 $10.3 $7.3 $13.8 $11.5 $11.5 $8.3 $8.3

Adjustment for discontinued Operations $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0

Net Income From Continuing Operations ($23.0) $41.4 $39.5 $1.1 ($5.9) ($6.2) ($12.1) $10.0 $10.3 $7.3 $13.8 $11.5 $11.5 $8.3 $8.3

EPS From Continuing Operations ($0.22) $0.34 $0.32 $0.01 ($0.06) ($0.06) ($0.12) $0.08 $0.08 $0.06 $0.11 $0.09 $0.09 $0.07 $0.07

Add: Amortization $21.42 $21.77 $22.00 5.3 5.4 5.4 5.4 5.1 $5.48 $5.7 $5.50 $5.50 $5.50 $5.50 $5.50

Add: Provision for future income tax recovery (13.6) $3.48 ($0.5)

Add: Cumulative translation adjustment 9.8 $0.00

Taxes $3.14 $1.72 $0.00 0.0 1.0 0.8 1.4 1.0 $0.72

Stock-based compensation $1.89 $3.55 $2.00 0.6 0.5 0.4 0.4 0.7 $0.85 $1.5 $0.50 $0.50 $0.50 $0.50 $0.50

Restructuring $0.76 $0.00 0.8 $0.3

Add: Unrealized FX loss $12.7

Add: Mosaid Transaction Costs ($4.2)

Other $0.00 $0.00

Adjusted Net Income 4.2 76.4 63.5 7.0 0.9 1.1 (4.9) 13.0 20.8 $22.8 19.8 17.5 17.5 14.3 14.3

Cash EPS 0.05 0.62 0.51 0.07 0.01 0.01 (0.04) 0.11 0.17 0.18 0.16 0.14 0.14 0.12 0.12

Effective tax rate (%) 16.5% -6.6% -14.0% 0.0% 19.5% 13.8% 13.3% 13.9% 4.9% 13.3% 0.0% 0.0% 0.0% 28.0% 28.0%

Net Margin (%) 8% 70% 59% 43% 8% 10% -44% 49% 76% 82% 73% 65% 65% 53% 53%

Source: Company reports and CIB C World Markets Inc.

A G

ood

Buy

, Belo

w T

he

NA

V - D

ecem

ber 0

5, 2

011

12

Exhibit 8. Comparables Table

Ticker Fiscal Price P/Net

Symbol YE Mkt. Cap. 12/5/2011 LTM FY0 FY1 FY2 C10E C11E C12E LTM FY0 FY1 FY2 C10 C11E C12E C10 C11E C12E Tang BV C10 C11E C12E C10 C11E C12E

Mosaid Technologies (C$) MSD-T Apr-12 #N/A $45.84 #N/A $2.89 $2.26 $2.65 $3.03 $2.50 $2.36 NA 15.8x 20.3x 17.3x 15.1x 18.4x 19.5x NA NA NA NA NA NA NA #N/A #N/A NA

Wi-LAN Inc. (C$) WIN-T Dec-11 681 $5.51 $0.34 $0.05 $0.62 $0.51 $0.05 $0.62 $0.51 16.4x 50+ 8.9x 10.7x 50+ 8.9x 10.7x 50+ 8.3x 7.3x 2.0x 9.5x 4.5x 4.5x $0.18 $0.53 $0.53#N/A

Acacia Research (US$) ACTG-O Dec-11 1,520 $35.45 1.29 1.39 1.24 1.87 1.39 1.24 1.87 27.5x 25.5x 28.6x 19.0x 25.5x 28.6x 19.0x 21.6x 18.1x 11.4x 25.7x 9.2x 5.8x 4.6x $1.46 NA NA

InterDigital Inc. (US$) IDCC-O Dec-11 1,977 $43.46 2.21 3.43 1.82 2.58 3.43 1.82 2.58 19.7x 12.7x 23.9x 16.8x 12.7x 23.9x 16.8x 6.8x 11.8x 7.3x 6.3x 4.5x 6.0x 4.8x NA NA NA

Qualcomm, Inc. (US$) QCOM-O Sep-11 91,598 $54.49 2.86 3.20 3.58 4.00 2.66 3.29 3.69 19.1x 17.0x 15.2x 13.6x 20.5x 16.6x 14.8x 16.4x 11.6x 10.8x 4.5x 7.5x 5.4x 4.5x $1.75 $3.84 $3.92

Rambus Inc. (US$) RMBS-O Dec-11 864 $7.86 0.07 1.30 (0.19) 0.05 1.30 (0.19) 0.05 50+ 6.0x NM 50+ 6.0x NM 50+ 3.1x NA NA 6.0x 2.6x 2.8x 2.7x NA NA NA

RPX (US$) RPXC-O Dec-11 774 $17.00 0.30 0.30 NA NA 0.30 NA NA 50+ 50+ NA NA 50+ NA NA 22.9x NA NA NA 6.5x NA NA $1.04 NA NA

Tessera Technologies Inc. (US$) TSRA-O Dec-11 884 $17.15 0.94 1.14 0.67 0.76 1.14 0.67 0.76 18.2x 15.0x 25.6x 22.6x 15.0x 25.6x 22.6x 7.1x NA 11.4x 1.5x 2.6x 3.1x 3.0x $2.10 NA $1.02

Group Average 21.1x 15.3x 23.3x 18.0x 15.9x 23.7x 18.3x 13.0x 13.8x 10.2x 8.8x 5.5x 4.6x 3.9x

Note: Estimates for all companies were taken from Firstcall, except Wi-LAN and Mosaid which are CIBC WM estimates.

Note: WIN and MSD are rated by CIBC World Markets, all other companies are not rated by CIBC World Markets.

Pricing and financial data converted to CDN using current exchange rate of: 1.01 C$/US$

Sources: CIBC World Markets, First Call Corp., Company Reports, Bloomberg.

See “Legal Disclaimer” section at the end of this report for important disclosures, including potential conflicts of interest.

CFPS

Fiscal Yr. Adjusted FD EPS

in local currency P/S less Net CashEV/EBITDA

Price to

Adjusted FD EPS Multiples

Source: Company reports and CIB C World Markets Inc.

A Good Buy, Below The NAV - December 05, 2011

13

Appendix Assumptions on NAV of Signed Deals - In modeling the backlog of royalty

payments, we assumed the weighted average life of their signed deals is

between 4 and 6 years. Wi-LAN has signed 255 licenses as of September 30.

The breakdown is in the range of 125 v-chip deals (12% of revenue), 120

wireless (85%+ of revenue) and 10 wireline agreements. We make estimates on

smaller unannounced deals based on quarterly royalty revenue reported, public

statements on license concentration and breakdowns, licensees publicly

announced and market share data.

80% of revenue from royalties from their top 10 customers in Q3 – Our

NAV model estimates this to be 78%. The $21.5 million in royalty revenue in Q3 from their top 10 licensees compares with $21.6 million last quarter and $22.4

million the prior quarter. This contribution can be expected to remain virtually

flat for the coming quarters as the large majority of licenses are fixed payments. This will only change when Wi-LAN adds material new licenses.

V-chip adjusted – In Q2, we noticed the unusually low v-chip sales number.

On the conference call it was re-confirmed that approximately 20% of Wi-LAN‟s

revenue is variable with a major source of that coming from V-Chip, said to about 12 to 13% of revenue. We are lowering our estimates on V-Chip, both

current revenue and future opportunity, to take into account these comments

and the lower expected volumes of TVs sold. A rough 15% decline in sales of digital TVs y/y was said to be a significant factor. We now estimate average

revenue per year from v-chip to be 12% (of revenue) on average, in-line with comments last quarter. We believe v-chip licensees Funai and AmTran (who

supplies more than half the TVs sold by Vizio) were 10% customers in the

quarter and resulted in the slightly lower revenue from their top 10 customers.

Keep in mind that our assumptions could be off based on timing of the payments

and revenue recognition as well as not having the exact numbers of each agreement. Again Exhibit 9 outlines our NAV analysis of both signed and

unsigned agreements by major licensees.

A Good Buy, Below The NAV - December 05, 2011

14

Exhibit 9. List Of Major Signed Deals

Licensee Patent Estimated Date Signed Estimated Effective DateEst. Original

Contract Size

Est.

LengthEst. Type Of Contract

Fully Diluted

Shares

Outstanding

(millions)

Per Share

Current

Value

Est. Expiry Date

Cisco (Original) All Wi-LAN patents at the time December 2, 2005 December 31, 2005 $10 MM 5Term License Running Royalty Upon

Meeting Minimum Volume45.8 $0.00 December 2, 2010

Fujitsu WiMAX 802.16d May 29, 2006 June 30, 2006 $0 MM 5Term License Running Royalty Upon

Meeting Minimum Volume49.0 $0.00 June 30, 2011

Nokia All Wi-LAN patents December 4, 2006 December 31, 2006 $15 MM 0 Lump Sum Payment 66.7 December 31, 2006

Tri-Vision V-Chip March 27, 2007 June 3, 2007 $128 MM 10 Term License Running Royalty 72.3 $0.47 December 31, 2016

March Networks All Wi-LAN patents "ELP" April 3, 2007 June 30, 2007 $0 MM 5 Term License Running Royalty 72.3 $0.00 June 30, 2012

Powerstar International "Certain IP" July 31, 2007 April 3, 2007 $0 MM 5 Term License Running Royalty 83.7 $0.00 July 30, 2012

Unannounced Company All Wi-LAN patents "ELP" June 28, 2007 June 30, 2007 $15 MM 5 Term License Running Royalty 83.7 $0.01 June 30, 2012

Fujitsu Remaining patents from Wi-LAN July 25, 2007 September 30, 2007 $4 MM 5 Term License Running Royalty 83.7 $0.01 September 30, 2012

AmTRAN V-Chip October 26, 2007 October 31, 2007 $30 MM 9 Term License Running Royalty 93.5 $0.12 November 1, 2016

Panasonic CDMA and Wi-Fi November 1, 2007 December 31, 2007 $0 MM 5 Term License Running Royalty 93.5 $0.00 December 31, 2012

Hyundai IT V-Chip November 20, 2007 December 31, 2007 $2 MM 9 Term License Running Royalty 93.5 $0.01 December 31, 2016

Acer Canada V-Chip December 6, 2007 December 31, 2007 $2 MM 9 Term License Running Royalty 93.5 $0.01 December 31, 2016

Hon Hai Precision V-Chip January 29, 2008 January 31, 2008 9 Term License Running Royalty 93.5 $0.00 December 31, 2016

Other Smaller V-Chip Licenses V-Chip Late 2007 to Early 2008 Late 2007 to Early 2008 $20 MM 9 Term License Running Royalty 93.5 $0.08 December 31, 2016

Four Unidentified Companies Wi-Fi March 6, 2008 March 31, 2008 $10 MM 5 Term License Running Royalty 93.5 $0.02 March 31, 2013

Zonet Wi-Fi March 27, 2008 March 31, 2008 $0 MM 6Term License Running Royalty + Past

Use93.5 $0.00 March 31, 2014

ASUS Wi-Fi May 22, 2008 June 30, 2008 $3 MM 5 Term License Running Royalty 93.5 $0.01 June 30, 2013

RIM All Wi-LAN patents August 11, 2008 September 30, 2008 $5 MM 5 Term License Running Royalty 93.5 $0.01 September 30, 2013

Samsung All Wi-LAN patents January 15, 2009 January 15, 2009 $37 MM 5 Term License Running Royalty 93.5 $0.12 January 15, 2014

Westinghouse V-Chip March 10, 2009 March 31, 2009 $6 MM 8 Term License Running Royalty 92.8 $0.03 December 31, 2016

Infineon Technologies Wireless LAN, xDSL, other patents May 7, 2009 June 30, 2009 $2 MM 5 Term License Running Royalty 94.4 $0.01 July 1, 2014

Casio CDMA, Wi-Fi, Bluetooth June 24, 2009 June 30, 2009 $1 MM 5 Term License Running Royalty 94.4 $0.00 July 1, 2014

Agilent Wi-Fi, CDMA, Bluetooth July 31, 2009 September 30, 2009 $1 MM 5 Term License Running Royalty 94.4 $0.00 October 1, 2014

Nikon Wi-Fi October 29, 2009 December 31, 2009 $1 MM 5 Term License Running Royalty 102.9 $0.00 January 1, 2015

NEC ADSL November 10, 2009 December 31, 2009 $5 MM 5 Term License Running Royalty 102.9 $0.02 January 1, 2015

Buffalo Certain wireless technology December 15, 2009 December 31, 2009 $5 MM 5 Term License Running Royalty 102.9 $0.02 January 1, 2015

Ricoh Wi-Fi December 16, 2009 December 31, 2009 $2 MM 5 Term License Running Royalty 102.9 $0.01 January 1, 2015

Sharp Wi-Fi June 17, 2010 June 30, 2010 $6 MM 6 Term License Running Royalty 102.8 $0.03 July 1, 2016

UTStarcom Wi-Fi, CDMA, Bluetooth August 11, 2010 September 30, 2010 $3 MM 5 Term License Running Royalty 103.3 $0.02 October 1, 2015

LG Wi-Fi, CDMA, Bluetooth December 22, 2010 December 31, 2010 $29 MM 6 Term License Running Royalty 103.4 $0.17 January 1, 2017

Intel Wi-Fi, CDMA, Bluetooth January 14, 2011 March 31, 2011 $78 MM 6 Term License Fixed Payments 122.1 $0.48 April 1, 2017

Atheros Wi-Fi, CDMA, Bluetooth January 18, 2011 June 30, 2011 $81 MM 6 Term License Fixed Payments 122.1 $0.52 July 1, 2017

Broadcom Wi-Fi, CDMA, Bluetooth January 19, 2011 March 31, 2011 $120 MM 6 Term License Fixed Payments 122.1 $0.74 April 1, 2017

Realtek Wi-Fi, CDMA, Bluetooth January 25, 2011 March 31, 2011 $15 MM 6 Term License Fixed Payments 122.1 $0.09 April 1, 2017

Acer Wi-Fi, CDMA, Bluetooth January 26, 2011 March 31, 2011 $6 MM 6 Term License Fixed Payments 122.1 $0.04 April 1, 2017

Motorola CDMA, Bluetooth January 27, 2011 March 31, 2011 $35 MM 6 Term License Fixed Payments 122.1 $0.22 April 1, 2017

Marvell Wi-Fi, CDMA, Bluetooth January 31, 2011 March 31, 2011 $45 MM 6 Term License Fixed Payments 122.1 $0.28 April 1, 2017

2Wire Wi-Fi January 31, 2011 March 31, 2011 $5 MM 7 Term License Fixed Payments 122.1 $0.03 April 1, 2018

Belkin Wi-Fi January 31, 2011 March 31, 2011 $3 MM 7 Term License Fixed Payments 122.1 $0.02 April 1, 2018

Netgear Wi-Fi January 31, 2011 March 31, 2011 $7 MM 7 Term License Fixed Payments 122.1 $0.04 April 1, 2018

Lenovo Wi-Fi January 31, 2011 March 31, 2011 $2 MM 6 Term License Fixed Payments 122.1 $0.01 April 1, 2017

Westell Wi-Fi January 31, 2011 March 31, 2011 $0 MM 6 Term License Fixed Payments 122.1 $0.00 April 1, 2017

Dell Laptops Wi-Fi Only January 31, 2011 March 31, 2011 $2 MM 6 Term License Fixed Payments 122.1 $0.01 April 1, 2017

D-Link Wi-Fi Only January 31, 2011 March 31, 2011 $4 MM 7 Term License Fixed Payments 122.1 $0.03 April 1, 2018

Hewlett-Packard Laptops Wi-Fi Only January 31, 2011 March 31, 2011 $6 MM 6 Term License Fixed Payments 122.1 $0.03 April 1, 2017

Apple Laptops Wi-Fi Only January 31, 2011 March 31, 2011 $8 MM 6 Term License Fixed Payments 122.1 $0.05 April 1, 2017

Sony Wi-Fi Only January 31, 2011 March 31, 2011 $1 MM 6 Term License Fixed Payments 122.1 $0.01 April 1, 2017

Toshiba Wi-Fi Only January 31, 2011 March 31, 2011 $3 MM 6 Term License Fixed Payments 122.1 $0.02 April 1, 2017

CSR Bluetooth, Wi-Fi February 18, 2011 March 31, 2011 $34 MM 6 Term License Fixed Payments 122.1 $0.21 April 1, 2017

Ralink All Wi-LAN patents February 23, 2011 March 31, 2011 $9 MM 6 Term License Fixed Payments 122.1 $0.06 April 1, 2017

Cisco Virtually All Wi-LAN patents April 15, 2011 December 31, 2010 $16 MM 6 Term License Fixed Payments 123.3 $0.09 January 1, 2017

T.I. Bluetooth Only July 4, 2011 June 30, 2011 $10 MM 1 Agreement 123.6 $0.04 June 29, 2012

Other Smaller V-Chip Licenses

Throught 2010 and 2011V-Chip July 28, 2011 2010 to 2011 $15 MM 5 Term License Running Royalty 123.6 $0.11 December 31, 2016

Ixia Wi-Fi October 5, 2011 December 31, 2011 $3 MM 5 Term License Fixed Payments 123.6 $0.02 December 31, 2016

Source: CIB C World Marke ts Inc.

A Good Buy, Below The NAV - December 05, 2011

15

Exhibit 10. Semiconductor Insights’ General Findings + ‘759 Validity Confirmed By USPTO In November 2011

Patent Number Title Target Market(s) Technical Strength Commercial Impact Ability To Detect Strength of Claims

Leading CDMA Patents

US RE: 37,802

A Rated Patent

Multicode direct sequence

spread spectrum.

3G (WCDMA), CDMA, WiMAX

WiFi, Digital TV broadcasting

systems (DVB-T, DVB-RCT, DVB-

H, T-DMB, ISDB-TSB).

4 - In a commercial context, the invention

is unique for CDMA and OFDM based

transceiver systems for wireless

applications.

4 - The patent is expected to

have high probability of current

and future use in the listed

target markets.

3 - Significant reverse engineering would be

needed to support the claims relating to DSP

domain as it is not easy to support or detect.

4 - 4 independent and 35 dependent claims. 1

independent claim is method, the others are

apparatus.

US 6,320,897

A Rated Patent

Multicode spread spectrum

communications system.

WiFi, WiMAX, CDMA, Digital TV

broadcasting systems - DVB-T,

DVB-RCT, DVB-H, T-DMB, ISDB-

TSB

4 - In a commercial context, the invention

is unique for CDMA and OFDM based

transceiver systems for wireless

applications.

4 - The patent is expected to

have high probability of current

and future use in the listed

target markets.

3 - Significant reverse engineering would be

needed to support the claims relating to DSP

domain as it is not easy to support or detect.

4 - 4 independent claims and 42 dependent

claims. Of the 4 independent claims 2 are

methods and 2 are apparatus. The claims cover

the possible uses of the invention well.

US 6,192,068

A Rated Patent

Multicode spread spectrum

communications system.

WiFi, WiMAX, CDMA, Digital TV

broadcasting systems (DVB-T,

DVB-RCT, DVB-H, T-DMB, ISDB-

TSB)

4 - The invention is unique for CDMA and

OFDM based transceiver systems for

wireless applications.

4 - The patent is expected to

have high probability of current

and future use in the listed

target markets.

3 - Significant reverse engineering would be

needed to support the claims relating to DSP

domain as it is not easy to support or detect.

4 - 4 independent claims and 7 dependent claims.

Of the 4 independent claims, 2 are method and 2

are apparatus. Claims cover the uses for the

invention very well.

Leading WiFi Patents

US 5,282,222

A Rated Patent

Method and apparatus for

multiple access between

transceivers in wireless

communications using

OFDM spread spectrum.

WiMAX, WiFi, DVB-T, DVB-RCT

and DAB.

4 - In a commercial context the invention is

unique for multi-carrier based transceiver

systems for wireless applications.

4 - The patent is expected to

have high probability of current

and future use in the listed

target markets.

3 - Part of the claims are easy to detect, others

will require reverse engineering.

3 - 2 independent and 10 dependent claims.

Some claims cover details in terms of carrier

spacing and speed limits between TX and Rx,

which could limit the scope of the patent.

CA 2,064,975

A Rated Patent

Method and apparatus for

multiple access between

transceivers in wireless

communications using

OFDM spread spectrum.

WiMAX, Mobile WiMAX, WiFi,

Digital TV broadcasting systems -

DVB-T, DVB-RCT, DVB-H, T-

DMB, ISDB-TSB.

4 - In a commercial context the invention is

unique for multi-carrier based transceiver

systems for wireless applications.

4 - The patent is expected to

have high probability of current

and future use in the listed

target markets.

3 - Part of the claims are easy to detect, others

will require reverse engineering.

3 - 5 independent claims and 25 dependent

claims. Some claims cover details in terms of

carrier spacing and speed limits between TX and

Rx, which could limit the scope of the patent.

Leading DSL Patents

EP 683,580 B1

A Rated Patent

Method for connecting an

HDSL transmission link to an

SDH network.

HDSL 3 - Offers an interesting solution by

performing both operations at the same

location.

3 - The patent filing date is prior

to standards (G.991.1) and may

have an impact if applicable.

4 - Easy to detect by looking at literature to

detect the claims.

3 - 1 independent claim and 2 dependent claims.

The independent claim is broad enough to cover

various mapping formats.

US 5,706,285

A Rated Patent

Network interfacing method

and a network interface for a

digital transmission network.

ADSL2 3 - Data rate adaptation based on

monitoring, buffering and multiplexing for

the time of the invention is quite unique.

3 - The method is promising and

likely to be used in the target

markets.

4 - Easy to detect looking at the literature.

Could use some reverse engineering to

support the claims.

3 - 4 independent claims and 18 dependent

claims. Fixed cell size is mentioned in the claims

and could limit them.

US 5,956,323

B Rated Patent

Power conservation for ports

and modulated data

transmission.

ADSL, ADSL2+ 3 - Offers a power consumption reduction

method by monitoring the loop. Other

methods typically increase the complexity,

and therefore this solution is superior.

3 - The method is promising and

likely to be used in the target

markets.

3 - Standards documentation and literature

review would increase the likelihood of

supporting claims. Some reverse engineering

would help.

3 - 4 independent claims and 3 dependent claims.

The independent claims capture the invention.

The claims cover central office and customer side

equipment.

Leading WiMAX Patents

US 6,549,759

A Rated Patent

Asymmetric adaptive

modulation in a wireless

communication system.

WiMAX, 2.5G (EDGE), 3G

WCDMA (HSPDA), WiFi.

4 - Excellent invention and appears to

have very few, if any, known alternative for

bi-directional point-multipoint wireless

networks.

4 - The patent is expected to

have high probability of current

and future use in the listed

target markets.

3 - Likely that the invention is implemented on

a programmable processor in the form of

software code. Depending on if the code is on

chip or off chip it may be easy or difficult to

support the claims.

4 - 6 independent claims and 21 dependent

claims. 1 independent claims is method while the

rest are apparatus. Claims are well written and

cover the possible uses of the invention very well.

US 6,925,068

A Rated Patent

Method and apparatus for

allocating bandwidth in a

wireless communication

system.

WiMAX, UMTS/WCDMA,

HSPDA, DVB-S2.

4 - The invention allows instantaneous

changes in traffic asymmetry by making

real-time adjustments to upstream and

downstream capacity and bursts by users.

4 - The patent is expected to

have high probability of current

and future use in the listed

target markets.

3 - Likely that the invention is implemented on

a programmable processor in the form of

software code. Depending on if the code is on

chip or off chip it may be easy or difficult to

support the claims.

4 - 5 independent claims and 29 dependent

claims. All independent claims are method claims.

Patents x222 and x975 both apply to WiMAX as well

Source: Company reports and CIB C World Markets Inc.

A Good Buy, Below The NAV - December 05, 2011

16

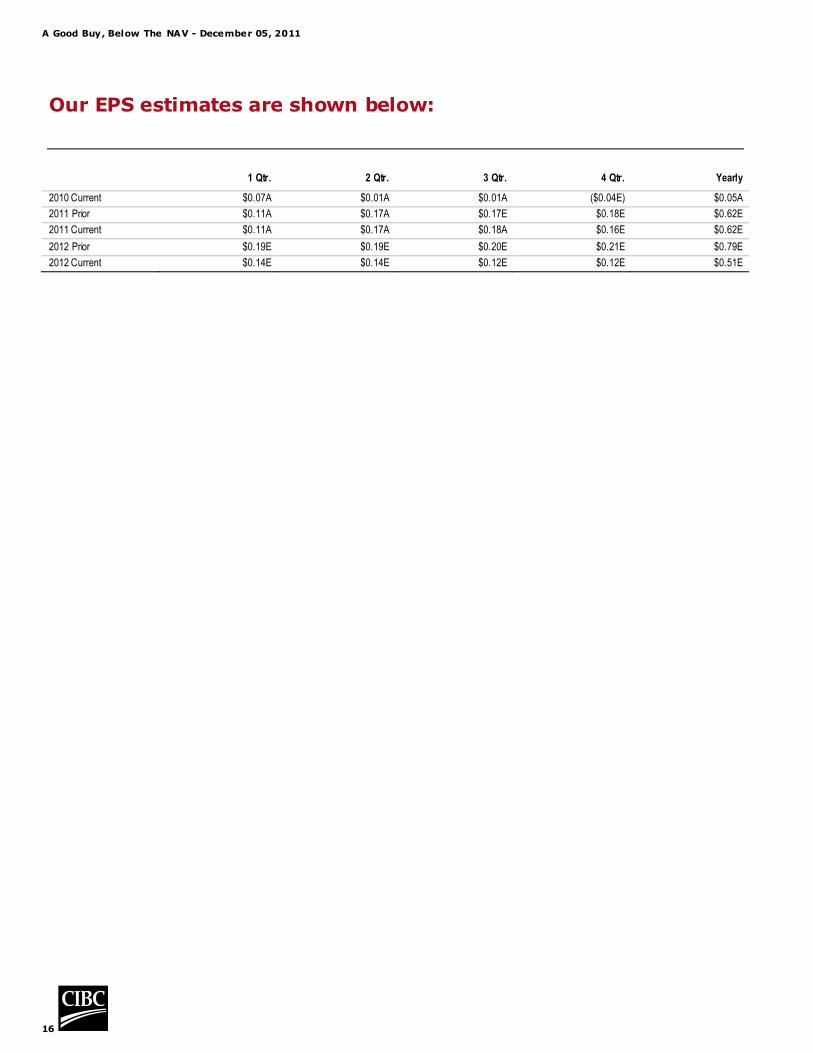

Our EPS estimates are shown below:

1 Qtr. 2 Qtr. 3 Qtr. 4 Qtr. Yearly

2010 Current $0.07A $0.01A $0.01A ($0.04E) $0.05A

2011 Prior $0.11A $0.17A $0.17E $0.18E $0.62E

2011 Current $0.11A $0.17A $0.18A $0.16E $0.62E

2012 Prior $0.19E $0.19E $0.20E $0.21E $0.79E

2012 Current $0.14E $0.14E $0.12E $0.12E $0.51E

A Good Buy, Below The NAV - December 05, 2011

17

IMPORTANT DISCLOSURES:

Analyst Certification: Each CIBC World Markets research analyst named on the front page of this research report, or

at the beginning of any subsection hereof, hereby certifies that (i) the recommendations and opinions expressed herein

accurately reflect such research analyst's personal views about the company and securities that are the subject of this

report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii)

no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific

recommendations or views expressed by such research analyst in this report.

Potential Conflicts of Interest: Equity research analysts employed by CIBC World Markets are compensated from

revenues generated by various CIBC World Markets businesses, including the CIBC World Markets Investment Banking

Department. Research analysts do not receive compensation based upon revenues from specific investment banking

transactions. CIBC World Markets generally prohibits any research analyst and any member of his or her household from

executing trades in the securities of a company that such research analyst covers. Additionally, CIBC World Markets

generally prohibits any research analyst from serving as an officer, director or advisory board member of a company that

such analyst covers.

In addition to 1% ownership positions in covered companies that are required to be specifically disclosed in this report,

CIBC World Markets may have a long position of less than 1% or a short position or deal as principal in the securities

discussed herein, related securities or in options, futures or other derivative instruments based thereon.

Recipients of this report are advised that any or all of the foregoing arrangements, as well as more specific disclosures

set forth below, may at times give rise to potential conflicts of interest.

Important Disclosure Footnotes for Wi-LAN Inc. (WIN)

2a Wi-LAN Inc. is a client for which a CIBC World Markets company has performed investment banking services

in the past 12 months.

2c CIBC World Markets Inc. has managed or co-managed a public offering of securities for Wi-LAN Inc. in the

past 12 months.

2e CIBC World Markets Inc. has received compensation for investment banking services from Wi-LAN Inc. in the

past 12 months.

2g CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking services

from Wi-LAN Inc. in the next 3 months.

A Good Buy, Below The NAV - December 05, 2011

18

Important Disclosure Footnotes for Companies Mentioned in this Report that Are Covered by CIBC World Markets Inc.:

Stock Prices as of 12/05/2011:

March Networks Corp. (2g) (MN-TSX, $4.63, Sector Outperformer)

MOSAID Technologies Incorporated (2g) (MSD-TSX, $45.84, Sector Outperformer)

Research In Motion Limited (2g, 7) (RIMM-NASDAQ, US$17.02, Sector Outperformer - Speculative)

Sierra Wireless Inc. (2g) (SWIR-NASDAQ, US$6.84, Sector Performer)

Wi-LAN Inc. (2a, 2c, 2e, 2g) (WIN-TSX, $5.51, Sector Outperformer)

Companies Mentioned in this Report that Are Not Covered by CIBC World Markets Inc.:

Stock Prices as of 12/05/2011:

01 Communique Labratory Inc. (ONE-TSX, $0.46, Not Rated)

Acacia Research (ACTG-OTC, US$35.45, Not Rated)

Acer Inc (2353-TW, [TWD]34.00, Not Rated)

Agilent Technologies (A-NYSE, US$37.06, Not Rated)

Alcatel-Lucent (ALU-NYSE, US$1.68, Not Rated)

Amtran Technologies Co. Ltd. (2489-TW, [TWD]16.85, Not Rated)

Apple Inc. (AAPL-NASDAQ, US$393.01, Not Rated)

Asustek (2357-TW, [TWD]199.00, Not Rated)

Atheros Communications Inc. (ATHR-NASDAQ, US$44.99, Not Rated)

Broadcom Corp. (BRCM-NASDAQ, US$30.42, Not Rated)

Cisco Systems (CSCO-NASDAQ, US$18.79, Not Rated)

Comcast (CMCSA-NASDAQ, US$23.15, Not Rated)

CSR plc (CSR-L, p172.75, Not Rated)

D-Link (2332-TW, [TWD]21.00, Not Rated)

Dell Computer Corp. (DELL-NASDAQ, US$15.93, Not Rated)

Fujitsu Ltd. (6702-T, ¥416.00, Not Rated)

Funai Electric Co (6839-T, ¥1671.00, Not Rated)

Google Inc. (GOOG-NASDAQ, US$625.65, Not Rated)

Hewlett-Packard (HPQ-NYSE, US$28.12, Not Rated)

Hitachi Ltd. (6501-T, ¥425.00, Not Rated)

Hon Hai Precision (2317-TW, [TWD]81.20, Not Rated)

HTC Corporation (2498-TW, [TWD]460.00, Not Rated)

Infineon (IFNNY-OTC, US$8.30, Not Rated)

Intel Corporation (INTC-NASDAQ, US$25.01, Not Rated)

InterDigital Communications Corp. (IDCC-NASDAQ, US$43.46, Not Rated)

Ixia (XXIA-OTC, US$11.65, Not Rated)

Kyocera Corp. (6971-T, ¥6790.00, Not Rated)

Lenovo Group Ltd. (992-HK, [HKD]5.49, Not Rated)

LG Electronics (066570-KS, [KRW]79800.00, Not Rated)

LM Ericsson AB (ERIC-NASDAQ, US$10.38, Not Rated)

Marvell Technology (MRVL-NASDAQ, US$13.78, Not Rated)

MediaTek Inc. (2454.TW-TW, [TWD]270.00, Not Rated)

Motorola, Inc. (MMI-NYSE, US$38.89, Not Rated)

NEC (6701-T, ¥171.00, Not Rated)

Netgear (NTGR-OTC, US$37.00, Not Rated)

Nokia Corporation (NOK-NYSE, US$5.37, Not Rated)

A Good Buy, Below The NAV - December 05, 2011

19

Companies Mentioned in this Report that Are Not Covered by CIBC World Markets Inc.: (Continued)

Stock Prices as of 12/05/2011:

Novatel Wireless Inc. (NVTL-NASDAQ, US$3.17, Not Rated)

Panasonic Corp. (6752-T, ¥717.00, Not Rated)

Pantech Co. (025930-KS, [KRW]1230.00, Not Rated)

Poynt Corporation (PYN-V, $0.13, Not Rated)

Qualcomm (QCOM-NASDAQ, US$54.49, Not Rated)

Ralink Technologies (3534-TW, [TWD]102.50, Not Rated)

Rambus (RMBS-OTC, US$7.86, Not Rated)

Realtek (2379.TW-TW, [TWD]44.70, Not Rated)

Ricoh Ltd. (RICOY-OTC, US$43.95, Not Rated)

RPX Corporation (RPXC-NASDAQ, US$23.57, Not Rated)

Samsung Corp. (000830-KS, [KRW]69100.00, Not Rated)

Sanyo Electric (1614-TW, [TWD]26.60, Not Rated)

Sharp Corp. (6753-T, ¥760.00, Not Rated)

Sony (SNE-NYSE, US$17.88, Not Rated)

STMicroelectronics N.V. (STM-NYSE, US$6.26, Not Rated)

Tessera Technologies, Inc. (TSRA-NASDAQ, US$17.15, Not Rated)

Texas Instruments (TXN-NYSE, US$30.23, Not Rated)

Toshiba Corp. (6502-T, ¥341.00, Not Rated)

UTStarcom Inc. (UTSI-OTC, US$1.39, Not Rated)

Westell (WSTL-OTC, US$2.10, Not Rated)

Zhongxing Teleco (ZTE) (000063-SZ, [CNY]17.14, Not Rated)

ZTE Corporation (ZTCOF-OTC, US$3.00, Not Rated)

Ztest Electronics (ZTE-V, $0.22, Not Rated)

Important disclosure footnotes that correspond to the footnotes in this table may be found in the "Key to

Important Disclosure Footnotes" section of this report.

A Good Buy, Below The NAV - December 05, 2011

20

Key to Important Disclosure Footnotes:

1 CIBC World Markets Corp. makes a market in the securities of this company.

2a This company is a client for which a CIBC World Markets company has performed investment banking services

in the past 12 months.

2b CIBC World Markets Corp. has managed or co-managed a public offering of securities for this company in the

past 12 months.

2c CIBC World Markets Inc. has managed or co-managed a public offering of securities for this company in the

past 12 months.

2d CIBC World Markets Corp. has received compensation for investment banking services from this company in

the past 12 months.

2e CIBC World Markets Inc. has received compensation for investment banking services from this company in the

past 12 months.

2f CIBC World Markets Corp. expects to receive or intends to seek compensation for investment banking services

from this company in the next 3 months.

2g CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking services

from this company in the next 3 months.

3a This company is a client for which a CIBC World Markets company has performed non-investment banking,

securities-related services in the past 12 months.

3b CIBC World Markets Corp. has received compensation for non-investment banking, securities-related services

from this company in the past 12 months.

3c CIBC World Markets Inc. has received compensation for non-investment banking, securities-related services

from this company in the past 12 months.

4a This company is a client for which a CIBC World Markets company has performed non-investment banking,

non-securities-related services in the past 12 months.

4b CIBC World Markets Corp. has received compensation for non-investment banking, non-securities-related

services from this company in the past 12 months.

4c CIBC World Markets Inc. has received compensation for non-investment banking, non-securities-related

services from this company in the past 12 months.

5a The CIBC World Markets Corp. analyst(s) who covers this company also has a long position in its common

equity securities.

5b A member of the household of a CIBC World Markets Corp. research analyst who covers this company has a

long position in the common equity securities of this company.

6a The CIBC World Markets Inc. fundamental analyst(s) who covers this company also has a long position in its

common equity securities.

6b A member of the household of a CIBC World Markets Inc. fundamental research analyst who covers this

company has a long position in the common equity securities of this company.

7 CIBC World Markets Corp., CIBC World Markets Inc., and their affiliates, in the aggregate, beneficially own 1%

or more of a class of equity securities issued by this company.

8 An executive of CIBC World Markets Inc. or any analyst involved in the preparation of this research report has

provided services to this company for remuneration in the past 12 months.

9 A senior executive member or director of Canadian Imperial Bank of Commerce ("CIBC"), the parent company

to CIBC World Markets Inc. and CIBC World Markets Corp., or a member of his/her household is an officer,

director or advisory board member of this company or one of its subsidiaries.

10 Canadian Imperial Bank of Commerce ("CIBC"), the parent company to CIBC World Markets Inc. and CIBC

World Markets Corp., has a significant credit relationship with this company.

11 The equity securities of this company are restricted voting shares.

12 The equity securities of this company are subordinate voting shares.

13 The equity securities of this company are non-voting shares.

14 The equity securities of this company are limited voting shares.

A Good Buy, Below The NAV - December 05, 2011

21

CIBC World Markets Inc. Price Chart

HISTORICAL PERFORMANCE OF CIBC WORLD MARKETS INC. RECOMMENDATIONS FOR WI-LAN INC. (WIN)

Date Change Type Closing Price Rating Price Target Coverage

01/15/2009 1.70 SO 6.00 Todd Coupland, CFA

06/25/2009 2.13 R - Todd Coupland, CFA

07/20/2009 2.15 SO 6.00 Todd Coupland, CFA

11/30/2010 4.48 R - Todd Coupland, CFA

12/20/2010 4.26 SO 6.00 Todd Coupland, CFA

01/16/2011 6.93 SO 10.00 Todd Coupland, CFA

01/18/2011 7.17 R - Todd Coupland, CFA

02/04/2011 6.40 SO 10.00 Todd Coupland, CFA

08/17/2011 7.09 R - Todd Coupland, CFA

11/16/2011 6.18 SO 10.00 Todd Coupland, CFA

A Good Buy, Below The NAV - December 05, 2011

22

CIBC World Markets Inc. Stock Rating System

Abbreviation Rating Description

Stock Ratings

SO Sector Outperformer Stock is expected to outperform the sector during the next 12-18 months.

SP Sector Performer Stock is expected to perform in line with the sector during the next 12-18 months.

SU Sector Underperformer Stock is expected to underperform the sector during the next 12-18 months.

NR Not Rated CIBC World Markets does not maintain an investment recommendation on the stock.

R Restricted CIBC World Markets is restricted*** from rating the stock.

Sector Weightings**

O Overweight Sector is expected to outperform the broader market averages.

M Market Weight Sector is expected to equal the performance of the broader market averages.

U Underweight Sector is expected to underperform the broader market averages.

NA None Sector rating is not applicable.

**Broader market averages refer to the S&P 500 in the U.S. and the S&P/TSX Composite in Canada.

"Speculative" indicates that an investment in this security involves a high amount of risk due to volatility and/or liquidity issues.

***Restricted due to a potential conflict of interest.

Ratings Distribution*: CIBC World Markets Inc. Coverage Universe

(as of 05 Dec 2011) Count Percent Inv. Banking Relationships Count Percent

Sector Outperformer (Buy) 164 46.6% Sector Outperformer (Buy) 164 100.0%

Sector Performer (Hold/Neutral) 150 42.6% Sector Performer (Hold/Neutral) 143 95.3%

Sector Underperformer (Sell) 28 8.0% Sector Underperformer (Sell) 25 89.3%

Restricted 9 2.6% Restricted 9 100.0%

Ratings Distribution: Technology Hardware Coverage Universe

(as of 05 Dec 2011) Count Percent Inv. Banking Relationships Count Percent

Sector Outperformer (Buy) 9 69.2% Sector Outperformer (Buy) 9 100.0%

Sector Performer (Hold/Neutral) 3 23.1% Sector Performer (Hold/Neutral) 3 100.0%

Sector Underperformer (Sell) 1 7.7% Sector Underperformer (Sell) 1 100.0%

Restricted 0 0.0% Restricted 0 0.0%

Technology Hardware Sector includes the following tickers: DWI, GND, MN, MSD, MT, RCM, RDL, RIMM, SMT, SVC, SWIR, VCM, WIN.

*Although the investment recommendations within the three-tiered, relative stock rating system utilized by CIBC World Markets Inc.

do not correlate to buy, hold and sell recommendations, for the purposes of complying with NYSE and NASD rules, CIBC World

Markets Inc. has assigned buy ratings to securities rated Sector Outperformer, hold ratings to securities rated Sector Performer, and

sell ratings to securities rated Sector Underperformer without taking into consideration the analyst's sector weighting.

Important disclosures required by IIROC Rule 3400, including potential conflicts of interest information, our system for

rating investment opportunities and our dissemination policy can be obtained by visiting CIBC World Markets on the web

at http://researchcentral.cibcwm.com under 'Quick Links' or by writing to CIBC World Markets Inc., Brookfield Place, 161 Bay Street, 4th Floor, Toronto, Ontario M5J 2S8, Attention: Research Disclosures Request.

A Good Buy, Below The NAV - December 05, 2011

23

Legal Disclaimer

This report is issued and approved for distribution by (a) in Canada, CIBC World Markets Inc., a member of the

Investment Industry Regulatory Organization of Canada (“IIROC”), the Toronto Stock Exchange, the TSX Venture

Exchange and a Member of the Canadian Investor Protection Fund, (b) in the United Kingdom, CIBC World Markets plc,

which is regulated by the Financial Services Authority ("FSA"), and (c) in Australia, CIBC Australia Limited, a member of

the Australian Stock Exchange and regulated by the ASIC (collectively, "CIBC World Markets") and (d) in the United

States either by (i) CIBC World Markets Inc. for distribution only to U.S. Major Institutional Investors (“MII”) (as such

term is defined in SEC Rule 15a-6) or (ii) CIBC World Markets Corp., a member of the Financial Industry Regulatory

Authority (“FINRA”). U.S. MIIs receiving this report from CIBC World Markets Inc. (the Canadian broker-dealer) are

required to effect transactions (other than negotiating their terms) in securities discussed in the report through CIBC

World Markets Corp. (the U.S. broker-dealer).

This report is provided, for informational purposes only, to institutional investor and retail clients of CIBC World

Markets in Canada, and does not constitute an offer or solicitation to buy or sell any securities discussed herein in any

jurisdiction where such offer or solicitation would be prohibited. This document and any of the products and information

contained herein are not intended for the use of private investors in the United Kingdom. Such investors will not be able

to enter into agreements or purchase products mentioned herein from CIBC World Markets plc. The comments and views

expressed in this document are meant for the general interests of wholesale clients of CIBC Australia Limited.

The securities mentioned in this report may not be suitable for all types of investors. This report does not take into

account the investment objectives, financial situation or specific needs of any particular client of CIBC World Markets.

Recipients should consider this report as only a single factor in making an investment decision and should not rely solely

on investment recommendations contained herein, if any, as a substitution for the exercise of independent judgment of

the merits and risks of investments. The analyst writing the report is not a person or company with actual, implied or

apparent authority to act on behalf of any issuer mentioned in the report. Before making an investment decision with

respect to any security recommended in this report, the recipient should consider whether such recommendation is

appropriate given the recipient's particular investment needs, objectives and financial circumstances. CIBC World

Markets suggests that, prior to acting on any of the recommendations herein, Canadian retail clients of CIBC World

Markets contact one of our client advisers in your jurisdiction to discuss your particular circumstances. Non-client

recipients of this report who are not institutional investor clients of CIBC World Markets should consult with an

independent financial advisor prior to making any investment decision based on this report or for any necessary

explanation of its contents. CIBC World Markets will not treat non-client recipients as its clients solely by virtue of their

receiving this report.

Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is

made regarding future performance of any security mentioned in this report. The price of the securities mentioned in

this report and the income they produce may fluctuate and/or be adversely affected by exchange rates, and investo rs

may realize losses on investments in such securities, including the loss of investment principal. CIBC World Markets

accepts no liability for any loss arising from the use of information contained in this report, except to the extent that

liability may arise under specific statutes or regulations applicable to CIBC World Markets.

Information, opinions and statistical data contained in this report were obtained or derived from sources believed to

be reliable, but CIBC World Markets does not represent that any such information, opinion or statistical data is accurate

or complete (with the exception of information contained in the Important Disclosures section of this report provided by

CIBC World Markets or individual research analysts), and they should not be relied upon as such. All estimates, opinions

and recommendations expressed herein constitute judgments as of the date of this report and are subject to change

without notice. Nothing in this report constitutes legal, accounting or tax advice. Since the levels and bases of taxation

can change, any reference in this report to the impact of taxation should not be construed as offering tax advice on the