INSIGHTS BIG DATA - equifax.com DATA INSIGHTS How to Turn Big Data into Profitable Insights Third...

12

How to Turn Big Data into Profitable Insights Third Party Data Turnpike Structured Data Street Attributes Ave Insights Interstate Decisions Drive REVENUE GROWTH REVENUE GROWTH

Transcript of INSIGHTS BIG DATA - equifax.com DATA INSIGHTS How to Turn Big Data into Profitable Insights Third...

BIG DATAINSIGHTS

How to Turn Big Data into Profitable Insights Third Party Data Turnpike

Structured Data Street

Attributes Ave

Insi

ghts

Inte

rsta

te

Decisions Drive

REVENUE GROWTHREVENUE GROWTH

The term ‘Big Data’ is used everywhere in today’s business world. Financial institutions have taken notice and are eager to take advantage of the unique growth and revenue opportunities made possible through the skilled analysis of Big Data.

But where do you begin? How do you transform Big Data into big customer insights? How do you effectively manage an immense and soaring volume of disparate data? How do you derive fresh, salient business intelligence that can lift your financial performance?

Through a diverse series of industry articles, interviews and use cases within this eBook, we give you a roadmap for navigating the Big Data Super Highway. You’ll see how to combine third-party data with your own diverse, multifaceted customer data to generate a dynamic source of concentrated market intelligence that creates fresh insights for more predictive decisions, and fuels everything from improved customer segmentation and risk mitigation to revenue growth.

If you’re ready to make sense of the vast data you’ve worked so hard to collect, we can show you how.

Strap on your seatbelt, because your journey begins now.

Navigating the Big Data Super HighwayHow to Turn Big Data into Profitable Insights

2 THINK YOU KNOW YOUR CUSTOMERS? THINK AGAIN

BIG DATAINSIGHTS

Third Party Data Turnpike

Structured Data Street

Attributes Ave

Insi

ghts

Inte

rsta

te

Decisions Drive

REVENUE GROWTHREVENUE GROWTH

CHECKING ACCOUNT GROWTH CONSUMER LOAN GROWTH

According to a 2012 Harvard Business Review article on big data, “data-driven decisions are better decisions—it’s as simple as that.”1 Aite Group’s experience suggests that many bank execs subscribe to this theory and strive to be more analytical in how they make marketing decisions. And from our research, we would conclude that a distinguishing characteristic of high-growth banks and credit unions is their superior marketing analytics capabilities.

BACKGROUNDIn February 2013, Aite Group and The Financial Brand surveyed 135 marketing executives from banks and credit unions. Based on the FI’s 2012 growth from 2011 number of checking account relationships and number of consumer loans issued, we slotted them into one of three buckets: High Growth, Moderate Growth, and Low Growth.

High Growth FIs accounted for one in five respondents, averaging 8.3% growth in both checking account relationships and consumer loans issued in 2012. Nearly half (44%) of the FIs surveyed were categorized as Moderate Growth FIs, and they averaged 4.6% and 5.8% growth in checking account and consumer loans issued, respectively. Low Growth FIs represented 35% of the sample, and these FIs grew checking account relationships by an average 2.7% and consumer loans by 3.9% (Figure 1).

Ron Shevlin, Senior Analyst, Retail Banking Aite Group

5Navigating the Big Data Super Highway

The Marketing Analytics Capabilities of High-Performing Financial Institutions

Figure 1: Average Growth in Checking Account Relationships and Consumer Loans, 2012

Average Percentage Growth, 2012 vs. 2011

Number of checking account relationships Number of consumer loans

Low Growth Fls (n=42) Moderate Growth Fls (n=53) High Growth Fls (n=26)

2.7%

4.6%

8.3%

3.9%5.8%

8.3%

Source: Aite Group survey of 135 financial services executives, February 2013

4 Navigating the Big Data Super Highway

6 Navigating the Big Data Super Highway

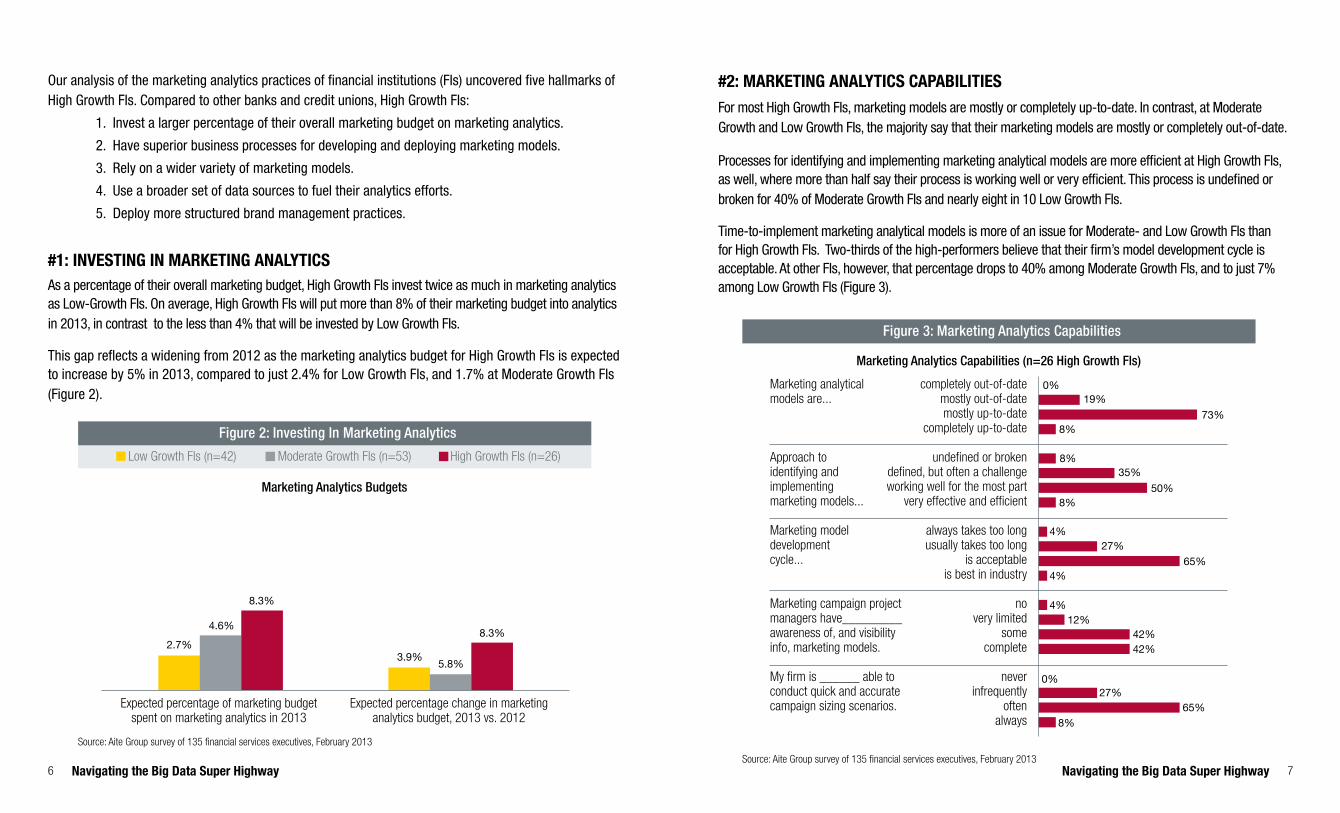

#2: MARKETING ANALYTICS CAPABILITIESFor most High Growth FIs, marketing models are mostly or completely up-to-date. In contrast, at Moderate Growth and Low Growth FIs, the majority say that their marketing models are mostly or completely out-of-date.

Processes for identifying and implementing marketing analytical models are more efficient at High Growth FIs, as well, where more than half say their process is working well or very efficient. This process is undefined or broken for 40% of Moderate Growth FIs and nearly eight in 10 Low Growth FIs.

Time-to-implement marketing analytical models is more of an issue for Moderate- and Low Growth FIs than for High Growth FIs. Two-thirds of the high-performers believe that their firm’s model development cycle is acceptable. At other FIs, however, that percentage drops to 40% among Moderate Growth FIs, and to just 7% among Low Growth FIs (Figure 3).

7Navigating the Big Data Super Highway

Our analysis of the marketing analytics practices of financial institutions (FIs) uncovered five hallmarks of High Growth FIs. Compared to other banks and credit unions, High Growth FIs:

1. Invest a larger percentage of their overall marketing budget on marketing analytics.

2. Have superior business processes for developing and deploying marketing models.

3. Rely on a wider variety of marketing models.

4. Use a broader set of data sources to fuel their analytics efforts.

5. Deploy more structured brand management practices.

#1: INVESTING IN MARKETING ANALYTICSAs a percentage of their overall marketing budget, High Growth FIs invest twice as much in marketing analytics as Low-Growth FIs. On average, High Growth FIs will put more than 8% of their marketing budget into analytics in 2013, in contrast to the less than 4% that will be invested by Low Growth FIs.

This gap reflects a widening from 2012 as the marketing analytics budget for High Growth FIs is expected to increase by 5% in 2013, compared to just 2.4% for Low Growth FIs, and 1.7% at Moderate Growth FIs (Figure 2).

Figure 2: Investing In Marketing Analytics

Marketing Analytics Budgets

Expected percentage of marketing budget Expected percentage change in marketing spent on marketing analytics in 2013 analytics budget, 2013 vs. 2012

Low Growth Fls (n=42) Moderate Growth Fls (n=53) High Growth Fls (n=26)

2.7%

4.6%

8.3%

3.9% 5.8%

8.3%

Source: Aite Group survey of 135 financial services executives, February 2013

Figure 3: Marketing Analytics Capabilities

Marketing Analytics Capabilities (n=26 High Growth Fls)

Source: Aite Group survey of 135 financial services executives, February 2013

Marketing analyticalmodels are...

Approach toidentifying andimplementingmarketing models...

Marketing modeldevelopmentcycle...

Marketing campaign project managers have_________awareness of, and visibilityinfo, marketing models.

My firm is ______ able toconduct quick and accuratecampaign sizing scenarios.

completely out-of-datemostly out-of-datemostly up-to-date

completely up-to-date

undefined or brokendefined, but often a challengeworking well for the most part

very effective and efficient

always takes too longusually takes too long

is acceptableis best in industry

novery limited

somecomplete

neverinfrequently

oftenalways

73%19%

8%

8%35%

50%8%

4%27%

65%4%

4%12%

42%42%

0%27%

65%8%

0%

8 Navigating the Big Data Super Highway

#3: MARKETING MODEL DEPLOYMENTWhen asked about eight different types of marketing models for credit, deposit, and investment products, High Growth FIs have deployed a significantly larger percentage of models than other FIs. Roughly four in 10 High Growth FIs have developed and deployed 11 or more types of marketing models, in contrast to just 13% of Moderate Growth FIs and 7% of Low Growth FIs. For credit products, customer segmentation, response, and next-best-product models are the most commonly deployed models, found in more than half of High Growth FIs (Figure 4).

#4: DATA SOURCESWhile many financial institutions rely on consumer demographics and credit data in their analytical models, High Growth FIs stand out in terms of their use of social media data and consumer purchase data (Figure 5). In fact, nearly two-thirds of High Growth FIs use five or more data sources in their models. Just one in five Low Growth FIs use five or more sources.

9Navigating the Big Data Super Highway

Figure 4: Marketing Model Deployment

Low Growth Fls (n=42) Moderate Growth Fls (n=53) High Growth Fls (n=26)

Q. Which of the following models have you deployed to supportthe marketing of credit products?

Customer segmentation

Response

Next best product

Customer life stage

Attrition

Contact cadence

Marketing spend optimization

Media mix

69%51%

31%

58%30%

14%

58%38%

26%

50%34%

17%

42%28%

14%

31%9%

2%

23%13%

7%

23%6%7%

Source: Aite Group survey of 135 financial services executives, February 2013

Figure 5: Data Sources Used for Marketing Analytics

Low Growth Fls (n=42) Moderate Growth Fls (n=53) High Growth Fls (n=26)

Q. Which of the following data types do you currently use in yourmarketing analytics efforts?

Social Media

Credit (e.g., Equifax, Experian)

Compiled demographics

Survey (attitudinal, lifestyle)

Behavioral (e.g., channel)

Consumer retail purchase (spending)

Psychographic (e.g., Claritas, Personix)

PFM (e.g., Yodlee)

88%53%

45%

83%74%

51%

79%87%

45%

71%60%

32%

67%62%

37%

63%40%

21%

38%32%

22%

25%15%

14%

Source: Aite Group survey of 135 financial services executives, February 2013

10 Navigating the Big Data Super Highway

#5: BRAND MANAGEMENTHigh Growth FIs don’t just have their analytics act together—they have their brand management act together as well. Nearly all of them have brand guidelines which they make available to employees. But so do many Moderate Growth FIs. What distinguishes the High Growth FIs is that most of them train new employees on the brand guidelines and provide on-going brand training to all employees, which many other FIs don’t do (Figure 6).

CONCLUSIONInvesting more in marketing analytics, deploying a wider set of models, or relying on a broader set of data sources won’t guarantee market growth. But Aite Group’s research does indicate that a robust set of marketing analytics capabilities is a distinguishing characteristic of high-growth banks and credit unions.

Brand Management Practices

Q. Which of the following do you have in place in your company?

Brand guidelinesmanual for employees

Design guidelines,brand standards

manual or style guide

New employeebrand orientation

training

On-going brand training for all employees

Low Growth Fls (n=42) Moderate Growth Fls (n=53) High Growth Fls (n=26)

17%

66%

92%

36%

81%

96%

5%

45%

96%

7%

25%

69%

Source: Aite Group survey of 135 financial services executives, February 2013

1 Source: “Getting Control of Big Data,” Harvard Business Review, October 2012.

Equifax white paper:

Retail Banking: The Future of Demand Deposit AccountsAlternative data offers fresh strategy and big opportunities

12 Navigating the Big Data Super Highway

The market for Demand Deposit Accounts (DDAs) is changing. Tight regulatory oversight is curtailing account fees and tough economic conditions mean fewer consumers are shopping around their financial services. The result is less profit potential for retail banks, and higher risk potential. To adjust for these shifting conditions, retail banks must rethink how they acquire and evaluate DDAs at the point of sale in order to create profitable household accounts and lasting customer relationships.

This brief white paper explores how the alternative data used in the Equifax Insight Score for Retail Banking can help banks more accurately assess DDA risk—and opportunity—in this new environment by offering a more comprehensive view of a consumer’s financial obligations.

Retail Banking: The Future of DemandDeposit Accounts Alternative data offers fresh strategy and big opportunities April 2013

Nancy ConnerSenior Director, Product Marketing, Financial [email protected]

For the full white paper, please visit: http://www.equifaxretailbanking.com

11Navigating the Big Data Super Highway

Big Data isn’t new.The application of Big Data for fighting fraud is not a new story. Financial institutions have long employed a variety of data sources to determine fraud risk, verify identities, control online access to bank accounts, and reveal suspicious activities.

When bank personnel or bank systems use a score, a reason code, or a flag in the course of fraud detection and prevention processes, they are likely already leveraging Big Data that came from a huge database with billions of records.

What continues to evolve is the sophisticated techniques fraudsters deploy, and the need for banks to access even more data sources to help identify suspicious activity.

Don’t just give me data - tell me what to do with it.Banking is complex enough as it is. Banks want to make an instantaneous decision on a potentially fraudulent request or application. The bank doesn’t want terabytes of data. The bank doesn’t care about all the monitoring, sifting, scrubbing, and modeling involved behind the scenes. The bank just wants to get insights, in milliseconds, in a simple-to-use form. Born from Big Data, banks want the scores and attributes that embody the predictive knowledge for reducing fraud.

Internal resources aren’t enough to win.Internal systems, by definition, focus on the bank’s own customer base, incident history, and products. Fraud prevention teams need both internal and external perspectives. External data sources are essential because they give a bank visibility into fraud attempts everywhere.

Fraud teams need more than outside data assets; they frequently seek outside expertise, too. Banks of all sizes often ask their outside data partners to develop data attributes, customized models, or analytical research for their specific anti-fraud applications.

When a known fraud threat has been identified by external resources, the bank needs to know before that threat comes knocking at the door.

12

1

2

3

13Navigating the Big Data Super Highway

“Big Data” is demonstrating its value across many industries. Public and private organizations are processing torrents of data—from terabytes to multiple “petabytes” (one petabyte is a million gigabytes). Examples we’ve seen in the news include predicting weather and airline delays, identifying treatments for premature babies, increasing operating margins, and reducing crime. For instance Google, by analyzing billions of search terms, can predict flu outbreaks more accurately than the Centers for Disease Control, according to a Wall Street Journal article.

Getting a “Big Data” view of anything is just a means to an end. For fraud fighters at banks, a major goal is reducing fraud losses. To do so, banks invest heavily in data, analytics and technology. They rely on internal IT resources and external parties to convert massive amounts of data into business intelligence—the predictive insights they need for better fraud prevention decisions.

These days, everyone seems to be jumping on the Big Data bandwagon. What are the implications of this trend for bank executives who are trying to control fraud losses? The hype on Big Data is almost as voluminous as the data—but at the risk of over-simplifying a complicated topic, let’s examine what the Big Data story means from a fraud control perspective.

To help you cut through the hype, here are our top 10 takeaways on how to leverage Big Data for fraud mitigation:

by Andrew Smith, Senior Vice President, Analytics and Gasan Awad, Vice President, Fraud and Identity Product Management

Navigating the Big Data Super Highway

Data is a raw material, not a finished product. Your bank should ask some probing questions about a Big Data provider’s volume, variety, velocity, and veracity.

• Find out what types of data are available and match them to your strategic objectives. Someproviders offer an extensive depth and breadth of services based on public and privatedatabases, such as utility payments, credit files, income and employment verification, cell phonenumbers, addresses, social security numbers, IP address, device location, and much more.

• Determine what applications need real-time decisions, and which data sources can meetthese high-velocity requirements.

• Ask if the data is structured or unstructured. Unstructured data, such as text, images, and videoextracted from social media, can deliver unique insights—but only if the data can be efficientlymined for relevant information and then converted into a form for predictive analysis.

• What is the Big Data provider’s track record in building data attributes, developing models,and delivering measurable results for other financial institutions.

Consortiums are the gold standard of Big Data.Some industries, including financial institutions, contribute valuable information to central repositories. Hosts of the repositories capture petabytes of data from consortium members and make the information available to authorized parties. As the host for several industry-leading consortiums, Equifax is in a privileged position to access deep, rich consortium data to help combat fraud.

New pattern detection tools add heavy firepower to the fraud fighter’s arsenal. Certain patterns of activity are indicative of fraud—and the patterns are hard for fraudsters to hide. For most banks, the ability to spot fraud patterns has been limited to what they can detect within their organizations. External velocity and behavioral pattern detection tools, which are getting much more sophisticated, can alert fraud teams to suspicious schemes that are in progress elsewhere.

5

15Navigating the Big Data Super Highway

Four variables drive your Big Data view.The “four V’s” of Big Data will determine the effectiveness of a data asset for fraud control:

• Volume—how much data is involved.

• Variety—the types of structured and unstructured data used by the application, such ascredit files, utility records, or even Facebook posts.

• Velocity—how fast and frequently the data will be processed by an application. You can’twaste time massaging or cleansing data that’s needed for time-sensitive, real-time processes.

• Veracity—the data’s accuracy. Can it be verified? Do you trust the data as an effective,predictive element of your fraud decisions?

The more experience a solutions’ provider has with the four V’s, the more you can trust the predictive power of their Big Data.

4

Equifax fraud management experts offer the following tips:1. Focus significant prevention measures on the first line of defense: account

opening processes. Use a multi-layered approach to detect fraud at accountopening and monitor volumes closely. Combining alerts can be essential forreal-time, multi-channel defenses to address a wide spectrum of fraud threats.

2. Use internal and external data and analytics to detect hidden patterns for new applications and withinexisting accounts. Tip-offs to fraud might include application anomalies, unusually high purchases ofpopular items, or multiple accounts being opened in a short period of time with data in common.

3. Leverage external consortium data with velocity and pattern detection to be alerted to suspiciousbehavior by an applicant at other organizations. With 3rd party velocity and pattern detection alerts, yourorganization will detect suspicious activity that would have otherwise been missed.

Equifax worked with a bank to help mitigate deposit account fraud. In this case, the existing false positive rate for the bank was 53:1. The Equifax fraud solution was used to isolate the most important attributes. The result was a reduction in the false positive rate from 53:1 to 15:1 or a 72% improvement. Based on industry averages and by including velocity and pattern detection alerts in their account opening processes, the bank is on track to save $700,000 dollars a year.

6

7

14 Navigating the Big Data Super Highway

Leveraging unstructured data to identify emerging threatsThe Equifax Compliance Data Center (CDC) proactively gathers structured and unstructured data from over 20,000 different sources including OFAC, global government compliance and law enforcement lists, interpol data, SEC and global regulatory lists, and news stories from worldwide media publications.

News information on individuals and businesses are stored in the CDC database as identities. The total database, with all inquiries and monitoring, contains over 300 million identities. New identity information is added and matched daily to confirm existing information in the database, and reduce false positives around negative information. When a known identity is flagged with new negative information, it is passed on to financial institutions that have a vested interest in those individuals or businesses. The CDC’s harnessing of Big Data helps with compliance around USA Patriot Act and the Bank Secrecy Act, but also allows Equifax customers to respond quickly to emerging threats.

16 Navigating the Big Data Super Highway

• Device identity tools that track phone settings, model information and location, serve asgood proxies for personal identifiers.

Big Data can do double-duty for banks.Tough regulatory requirements require lenders to perform many checks before issuing credit to any individual. These verification processes typically reside in account opening and other front-line sales systems. Consequently, banks have an opportunity to get “extra mileage” as they upgrade their regulatory processes to also improve their fraud prevention measures. A holistic view of the consumer helps improve regulatory compliance, reduce fraud and improve customer satisfaction.

SummaryFraudsters are continually developing new techniques to rob financial institutions of billions of dollars. Keeping up with criminals is a vast undertaking that puts Big Data concepts in the forefront of next-generation fraud management. When contemplating leveraging Big Data for fraud mitigation, be sure to look for a solutions’ provider that offers:

• Comprehensive data coverage from thousands of consortium members supplying millionsof records daily

• The ability to add meaningful context to vast amounts of data through sophisticated record-keying technology, analytics, scoring and attribute reporting

• The ability to deliver scores and attributes based on real-time data, reported timely byconsortium members

108

9

17Navigating the Big Data Super Highway

Discreet measures avoid friction with good customers.According to researchers, fraud managers spend more than half of their budgets on costly manual reviews of false positives. Used in conjunction with pattern detection tools, passive techniques can pull through good applications quickly with minimal false positives and revenue loss. Passive checks operate in the background, without negatively impacting the customer experience. A best practice is to waterfall between multiple passive checks before actively engaging with the consumer to verify if they are indeed who they say they are.

Fraud keeps changing—and so do the countermeasures. Banks need to constantly upgrade the tools they use to stop fraud without interfering with the flow of “good” account applications and transactions. Data providers are responding with new tools and techniques that combine Big Data concepts and mammoth computing power to fight fraud. Here are several examples:

• Proprietary keying technology is now being used to link and consolidate records fromhundreds of millions of consumers. Unique identifiers or “keys” to every consumer helpdiscern their true identity despite variations in the data. These solutions can dramaticallyreduce false positives.

• Voiceprints and other forms of biometrics are gaining traction as anti-fraud measures.

For white papers and case studies that highlight how your organization can effectively mitigate fraud, please visit the Related Resources section at: http://www.equifax.com/technology/account-opening/en_tas

12 Navigating the Big Data Super Highway

For more information on Equifax fraud solutions, please visit: www.equifaxfraudsolutions.com

How does Big Data play into actionable segmentation strategies?Marketing organizations across the Financial Services industry struggle with how to best size and pursue cross sell and new customer acquisition opportunities in order to add precious new revenue to their businesses. One key approach that relies on being able to gather and distill disparate data is segmentation. Many firms segment their existing customer bases as well as the markets in which they do business in some fashion today, but often find it a struggle to do so in a way that will be effective and actionable.

Example 1: Using Big Data to define segments

There are numerous ways to segment a population to reach specific goals and get the desired outcomes.

Depending on the objective, banks can segment existing customers by internal behavioral data. However, without a lens into the full client wallet and financial situation, banks will not fully understand the relationship potential that exists. For existing customers and prospects, banks can use estimated investable assets, income, credit, likely investment style, age, or other criteria. Households can be assigned to a segment based on anonymous, aggregated financial, behavioral, and demographic characteristics.

A goal might be to improve effectiveness of cross sell marketing efforts for single service credit card clients.

In this example, the bank can use aggregated spending behavioral data purchased from an external source to segment customers and identify optimal cross-sell opportunities. This data gives a sense for the full spending behavior of a household, not only what a customer does with a card issued by a single bank. As shown in the chart below, by matching cross-sell offers to customers’ interests, the relevancy of the offer increases.

In addition to defining customer segments for cross-selling, segmentation schemes can be used in the following valuable ways:

• Size markets and identify growth opportunities for key target segments

• Tailor online messaging by differentiating online visitors

• Improve CRM and loyalty efforts by delivering communications using the right channels and relevant messages

Example 2: Target services to the right consumer

The bank’s objective may be to grow revenue by applying Big Data that will improve its ability to identify high-value households.

By applying data provided by an external supplier in combination with the bank’s own internal knowledge of client behavior, preferences, etc., the bank can implement a segmentation scheme

18 Navigating the Big Data Super Highway 19Navigating the Big Data Super Highway

Greta Lovenheim Capps, Senior Vice President, Financial Services Leader Equifax – IXI Services

Turning Big Data into Big Revenue: Market segmentation tools for relevant customer-centric offers

The term “Big Data” has evolved to mean a variety of things over the past few years. To many, it is an overused buzzword and perhaps even a vague concept within the data landscape that

everyone has heard, but few really understand. Despite the confusion around exactly what it is, many would agree that Big Data has become a growing challenge for corporations that, if leveraged well, can become a substantial competitive advantage.

One example of how the industry defines the term comes from the McKinsey Global Institute. It defines Big Data as “datasets whose size is beyond the ability of typical database software tools to capture, store, manage, and analyze.” That definition captures the anxiety that many financial institutions feel about Big Data. They want the insights Big Data can provide, but are overwhelmed by its sheer volume and velocity.

The following definition from the Gartner Group represents a more holistic, actionable paradigm with which to consider Big Data. They define Big Data as “high volume, velocity and/or variety of information assets that demand cost effective, innovative forms of information processing that enable enhanced insight, decision making and process automation.” The reality is, as this definition suggests, to benefit from Big Data banks don’t have to drown in it. Financial institutions can turn to external resources in order to access vast amounts of rich, well-managed external data for better decision-making.

High spend in home repairs Offer Home Equity Line of Credit

High spend in travel Offer credit card with travel rewards program

High spend in online shopping Offer prepaid card and ID theft protection

CONSUMER’S SPENDING TRAIT CROSS-SELL OPPORTUNITY

21

Equifax TodayA global leader in information solutions, Equifax leverages one of the largest sources of consumer and commercial data, along with advanced analytics and proprietary technology, to create customized insights that enrich both the performance of businesses and the lives of consumers.

With a heritage dating back 114 years, customers have trusted Equifax to deliver innovative solutions with the highest level of integrity and reliability. Organizations of all sizes rely on us for consumer and business credit intelligence, portfolio management, fraud detection, decisioning technology, marketing tools and much more.

For more info visit www.equifaxretailbanking.com or call 1.800.879.1025.

Navigating the Big Data Super Highway

Empowering Financial InstitutionsIn today’s ever-changing consumer landscape, financial institutions need to more precisely measure risk and capture opportunity in order to grow profitable households and achieve organic growth.

Equifax leverages unmatched data, analytics and technology that empower financial institutions to acquire, expand and retain profitable households. Only Equifax has the tools to optimize household growth across all product types and at every stage of the household life cycle.

Our Retail Banking Solutions help financial institutions cross-sell additional products and services, increase wallet share, combat fraud and lower the cost of operations.

that best matches its target segments. Various tools exist that distill anonymous wealth data from millions of U.S. households such as estimates of their deposits, stocks, bonds, mutual funds, annuities, and other assets that may be held at other financial institutions.

With these and other insights, a financial institution can more effectively target its most profitable services to the most likely profitable buyers. It is no longer casting a wide net when launching a marketing campaign aimed at account acquisition or cross-sell. Banks can implement smart segmentation strategies for in-branch cross selling, call center dialogs, direct mail and digital marketing. This same segmentation can and should be used to make inbound call center, online banking and inbound branch traffic conversations more relevant to the customer and more effective and profitable to the bank.

Segmentation best practices—even more important for Big DataSegmentation best practices work for both traditional data sets and Big Data from internal or external sources. Following are five strategies to follow:

1. Begin with the end in mind. Get agreement on the business goal and then design a segmentation approach around that goal.

2. Build only what can be operationalized. Define the steps for turning segmentation data into insights and then into decisions. Make sure each step is feasible, affordable, and compliant with regulations.

3. Use data that replicates the customer’s view, not just the bank’s view. For example, a bank needs to look beyond a client’s accounts at the bank and consider the client’s total wallet and needs. Share the insights gained from segmentation. Often times, segment definitions can be applied without substantial changes by other core systems and customer-facing personnel.

4. Minimize expenses and optimize investment. Understand cost to serve for key segments and use this as guidance for fee refund decisions, rate offers and pricing, customer experience improvements, and other decisions involving expenses and investments in Big Data assets.

Ultimately, a bank that does not use available data assets for a broad, deep and timely view of its customers and prospects will lose business to its competitors. Now is the time to start thinking of Big Data as a big opportunity rather than a big effort.

20 Navigating the Big Data Super Highway

“Accelerating Revenue with Customer Centric Offers” This white paper addresses how banks can transform their cross-sell approach from a product-centric focus to a more customer-centric view in order to have more success.

“Top 20 Bank Increases Profits with Real-time Offers”This case study highlights how a top 20 bank grew wallet-share and profits by making the right offer to customers at the point-of-service.

For more info visit www.equifax.com

Equifax and EFX are registered trademarks of Equifax Inc. Inform > Enrich > Empower is a trademark of Equifax Inc. Copyright ©2013, Equifax Inc., Atlanta, Georgia. All rights reserved.

The roughly 60 million under-banked people with little to no credit represent a big growth opportunity in retail banking.

Profit potential is so immense and promising that banks of all sizes are scurrying for fresh insight into this under-served market.

At Equifax, we recommend you consider using alternative data. It helps you put minor credit inadequacies in context and recognize the true potential of an account by augmenting traditional credit data with alternative data, which includes payment history for non-credit related bills such as cable, phone and utilities.

It’s the expanded insight you need to:n Identify and serve more potentially profitable households,

including thin-file and no-file consumers

n Maximize account decisions in real-time at account opening and throughout the account lifecycle

Learn more about alternative data and other innovative ways to grow your household accounts in 2013 by contacting us at 1.800.879.1025, [email protected] or visit us at: www.equifaxretailbanking.com.

Retail bankers—this is your

big opportunity. Embrace unique alternative data NOW to grow your DDA accounts in 2013.

BIG DATAINSIGHTS

Equifax and EFX are registered trademarks of Equifax Inc. Inform > Enrich > Empower is a trademark of Equifax Inc.

Copyright ©2013, Equifax Inc., Atlanta, Georgia. All rights reserved.