INPUT TAX CREDIT UNDER GST - ctconline.org Shah_Input Tax Credit_27... · ITC framework under the...

63

© Economic Laws Practice 2017 INPUT TAX CREDIT UNDER GST Harsh Shah 27 April 2017

Transcript of INPUT TAX CREDIT UNDER GST - ctconline.org Shah_Input Tax Credit_27... · ITC framework under the...

© E

co

no

mic

La

ws

Pra

cti

ce

20

17

INPUT TAX CREDIT UNDER GST

Harsh Shah

27 April 2017

© Economic Laws Practice 2017© Economic Laws Practice 2017

Agenda

I. Input tax credit framework under the GST regime

II. Transitional provisions concerning Input tax credit

III. Documentation

2

© Economic Laws Practice 2017© Economic Laws Practice 2017 3

© Economic Laws Practice 2017© Economic Laws Practice 2017

ITC framework under the GST

regime

4

Sr. No. Concept Section under the CGST Act

Draft Rule

1 Scope and conditions for availment of ITC 16(1), (2) 1, 2

2 Non-eligibility of credit to the extent of depreciation claimed under IT Act

16(3)

3 Time limit for availment of credit 16(4)

4 Availment and reversal of credit for goods and services used for taxable as well as exempted supplies

17(1), (2), (3) 7, 8

5 Special provisions for banking and financial services sector 17(4) 3

6 Blocked credits 17(5)

7 Availment of credit in special circumstances (such as upon obtaining registration, composition, etc.)

18(1), (2), (4), (5) 5, 9

8 Credit upon change in constitution of business 18(3) 6

9 Supply of CG and P&M on which credit is availed 18(6)

10 Credit in respect of goods sent for job work 19 10

11 Distribution of credit by ISD and conditions for the same 20, 21 4

© Economic Laws Practice 2017

SOME KEY DEFINITIONS

5

© Economic Laws Practice 2017

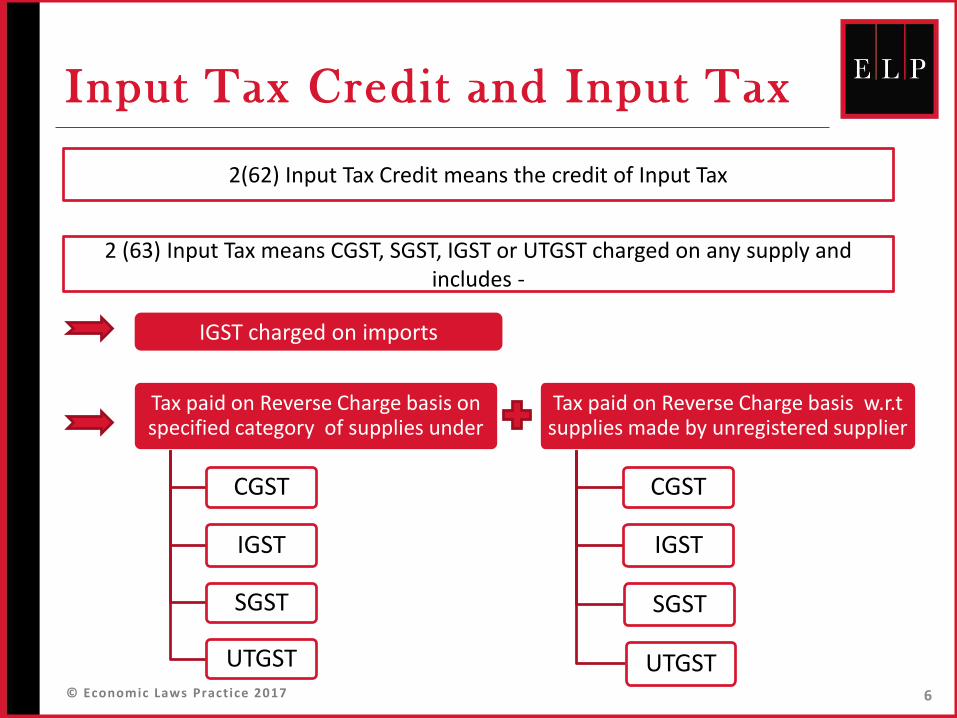

Input Tax Credit and Input Tax

6

Tax paid on Reverse Charge basis on specified category of supplies under

CGST

IGST

SGST

UTGST

Tax paid on Reverse Charge basis w.r.t supplies made by unregistered supplier

CGST

IGST

SGST

UTGST

2 (63) Input Tax means CGST, SGST, IGST or UTGST charged on any supply and includes -

IGST charged on imports

2(62) Input Tax Credit means the credit of Input Tax

© Economic Laws Practice 2017

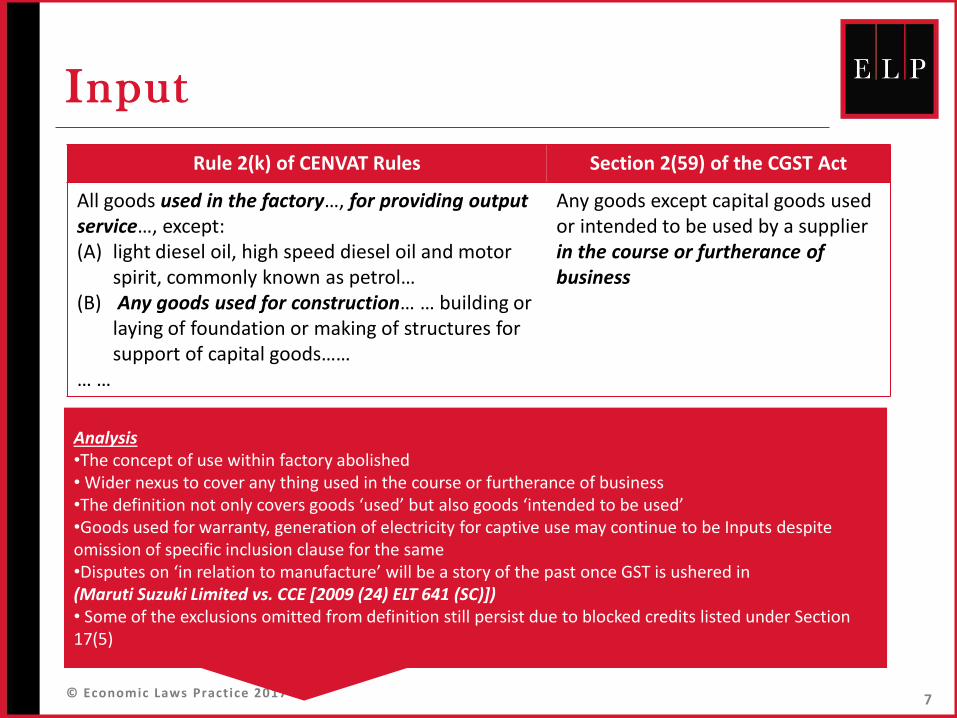

Input

7

Rule 2(k) of CENVAT Rules Section 2(59) of the CGST Act

All goods used in the factory…, for providing output service…, except:(A) light diesel oil, high speed diesel oil and motor

spirit, commonly known as petrol…(B) Any goods used for construction… … building or

laying of foundation or making of structures for support of capital goods……

… …

Any goods except capital goods used or intended to be used by a supplier in the course or furtherance of business

Analysis•The concept of use within factory abolished• Wider nexus to cover any thing used in the course or furtherance of business•The definition not only covers goods ‘used’ but also goods ‘intended to be used’•Goods used for warranty, generation of electricity for captive use may continue to be Inputs despite omission of specific inclusion clause for the same•Disputes on ‘in relation to manufacture’ will be a story of the past once GST is ushered in(Maruti Suzuki Limited vs. CCE [2009 (24) ELT 641 (SC)])• Some of the exclusions omitted from definition still persist due to blocked credits listed under Section 17(5)

© Economic Laws Practice 2017

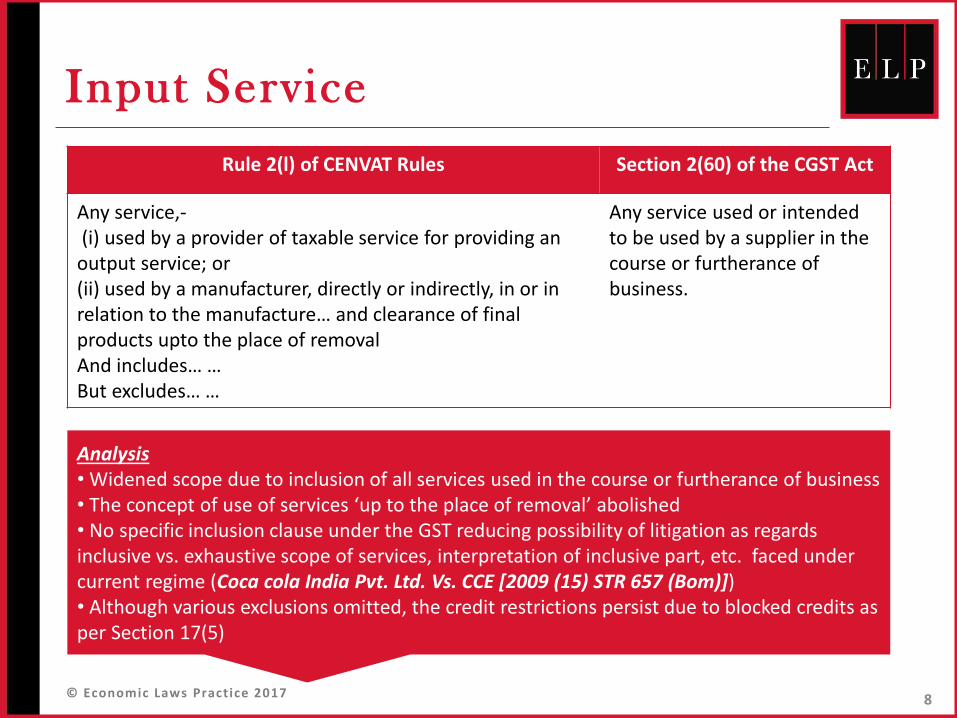

Input Service

8

Rule 2(l) of CENVAT Rules Section 2(60) of the CGST Act

Any service,-(i) used by a provider of taxable service for providing an output service; or(ii) used by a manufacturer, directly or indirectly, in or in relation to the manufacture… and clearance of final products upto the place of removalAnd includes… …But excludes… …

Any service used or intended to be used by a supplier in the course or furtherance of business.

Analysis• Widened scope due to inclusion of all services used in the course or furtherance of business• The concept of use of services ‘up to the place of removal’ abolished• No specific inclusion clause under the GST reducing possibility of litigation as regards inclusive vs. exhaustive scope of services, interpretation of inclusive part, etc. faced under current regime (Coca cola India Pvt. Ltd. Vs. CCE [2009 (15) STR 657 (Bom)])• Although various exclusions omitted, the credit restrictions persist due to blocked credits as per Section 17(5)

© Economic Laws Practice 2017

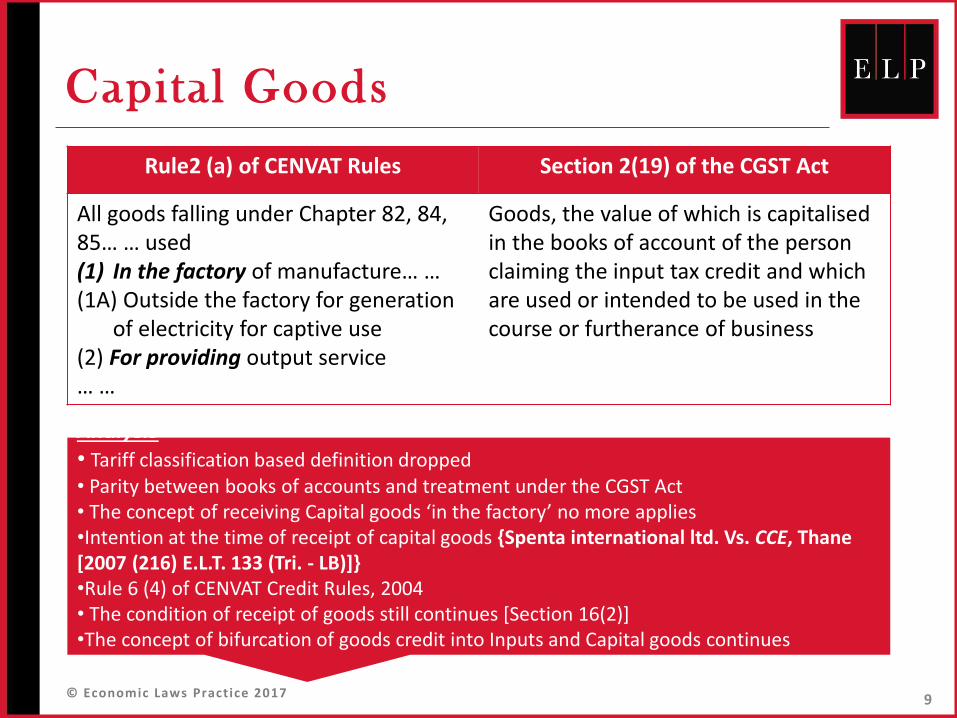

Capital Goods

9

Rule2 (a) of CENVAT Rules Section 2(19) of the CGST Act

All goods falling under Chapter 82, 84, 85… … used(1) In the factory of manufacture… …(1A) Outside the factory for generation

of electricity for captive use (2) For providing output service… …

Goods, the value of which is capitalised in the books of account of the person claiming the input tax credit and which are used or intended to be used in the course or furtherance of business

Analysis• Tariff classification based definition dropped• Parity between books of accounts and treatment under the CGST Act• The concept of receiving Capital goods ‘in the factory’ no more applies•Intention at the time of receipt of capital goods {Spenta international ltd. Vs. CCE, Thane [2007 (216) E.L.T. 133 (Tri. - LB)]}•Rule 6 (4) of CENVAT Credit Rules, 2004• The condition of receipt of goods still continues [Section 16(2)]•The concept of bifurcation of goods credit into Inputs and Capital goods continues

© Economic Laws Practice 2017

AVAILMENT OF CREDIT AND

CONDITIONS

Section 16 read with Rule 1, 2

10

© Economic Laws Practice 2017

Eligibil i ty and conditions for

taking input tax credit

S. 16(1) Every registered person shall, subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of his business and the said amount shall be credited to the electronic credit ledger of such person.

Analysis

•Registration a pre-requisite for availment of credit(Imagination Technologies India P. Ltd. Vs. Commr. of C. Ex., Pune-III [2011 (023) STR 0661 Tri.-Bom], Well Known Polyesters Ltd. Vs. Commissioner of C. Ex., Vapi [2012 (025) STR 0411 Tri.-Ahmd.])• Uniform criteria for availment of credit on Inputs, Input services and Capital goods• Credit availment through electronic credit ledger

11

© Economic Laws Practice 2017

Conditions for Availing Credit [S. 16(2)]

12

Possession of Tax Invoice or Debit Note or other documents

(such as BOE, document issued by ISD, etc. as per Rule 1)

Receipt of goods or services or both

Tax has been actually paid to the Government

Return has been furnished

© Economic Laws Practice 2017

Important to examine

Taxable supplies only

Definitions under GST

Inputs, input services and

capital goods?

13

© Economic Laws Practice 2017

Conditions – payment by supplier

Credit eligible only after payment of tax by supplier

Practical difficulties

Validity of granting credit only after payment by other person upheld by theBombay High Court in Mahalaxmi Cotton Ginning Pressing and Oil Industries vs.State of Maharashtra [2012 (051) VST 0001 BOM] Similar view adopted by various High Courts

Against the long established concepts under the CENVAT and erstwhile MODVATregime that credit is an inherent right and is indefeasible Collector of Central Excise vs. Dai Ichi Karkaria Ltd. [1999 (112) ELT 353 (SC)] Eicher Motors Ltd. vs. Union of India [1999 (106) ELT 3(SC)]

Latin maxim - Nemo punitur pro alieno delicto (no one is punished for the crime ofanother)

Onerous condition can be read down Bhavya Apparels Pvt. Ltd. vs. Union of India [2007 (SC3) GJX 0858 SC]

14

© Economic Laws Practice 2017

Conditions – receipt of goods or

services both

Explanation I to Section 12(1) and 13(1) of the CGST Act

Supply deemed to have been made to the extent it is covered by invoice or payment

Receipt of goods or services vs. Supply deemed to have been made

While time of supply arises upon receipt of advance, credit eligibility crystallisedonly upon receipt of goods or services

While liability to pay tax arises in April 2017, whether credit will be eligible inApril or in June

Will it result into credit mismatch?

15

Example

Date of booking order 25 April 2017

Date of payment / receipt of advance/ date of invoice 27 April 2017

Date of dispatch of goods 29 April 2017

Date of receipt of goods 1 June 2017

© Economic Laws Practice 2017

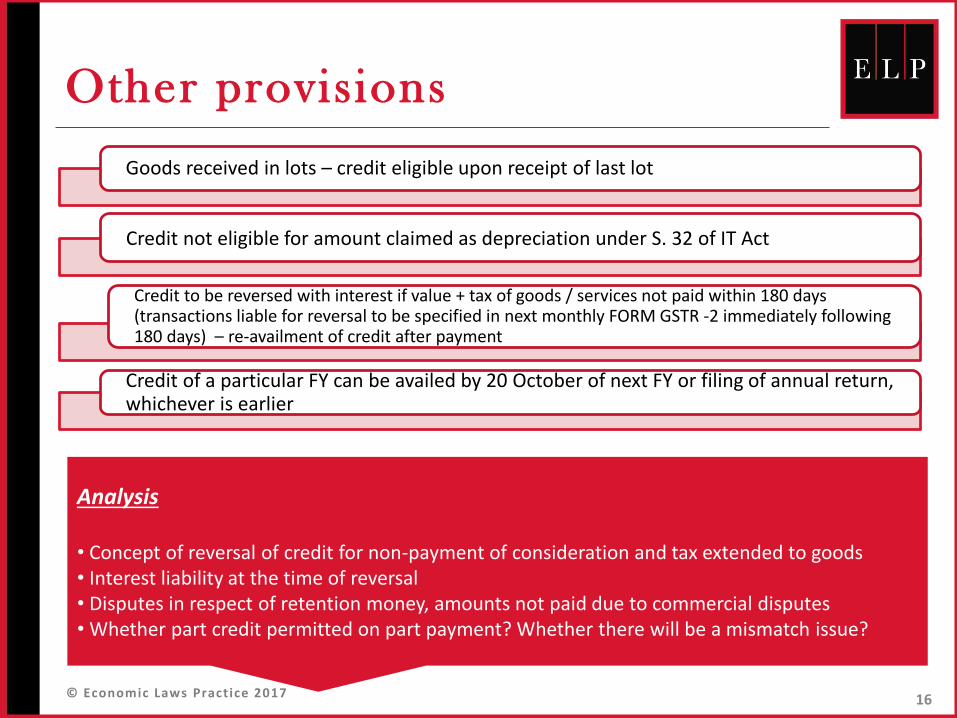

Other provisions

16

Goods received in lots – credit eligible upon receipt of last lot

Credit not eligible for amount claimed as depreciation under S. 32 of IT Act

Credit to be reversed with interest if value + tax of goods / services not paid within 180 days (transactions liable for reversal to be specified in next monthly FORM GSTR -2 immediately following 180 days) – re-availment of credit after payment

Credit of a particular FY can be availed by 20 October of next FY or filing of annual return, whichever is earlier

Analysis

• Concept of reversal of credit for non-payment of consideration and tax extended to goods• Interest liability at the time of reversal• Disputes in respect of retention money, amounts not paid due to commercial disputes• Whether part credit permitted on part payment? Whether there will be a mismatch issue?

© Economic Laws Practice 2017

APPORTIONMENT OF CREDIT

AND BLOCKED CREDITS

Section 17 read with Rule 7, 8

17

© Economic Laws Practice 2017

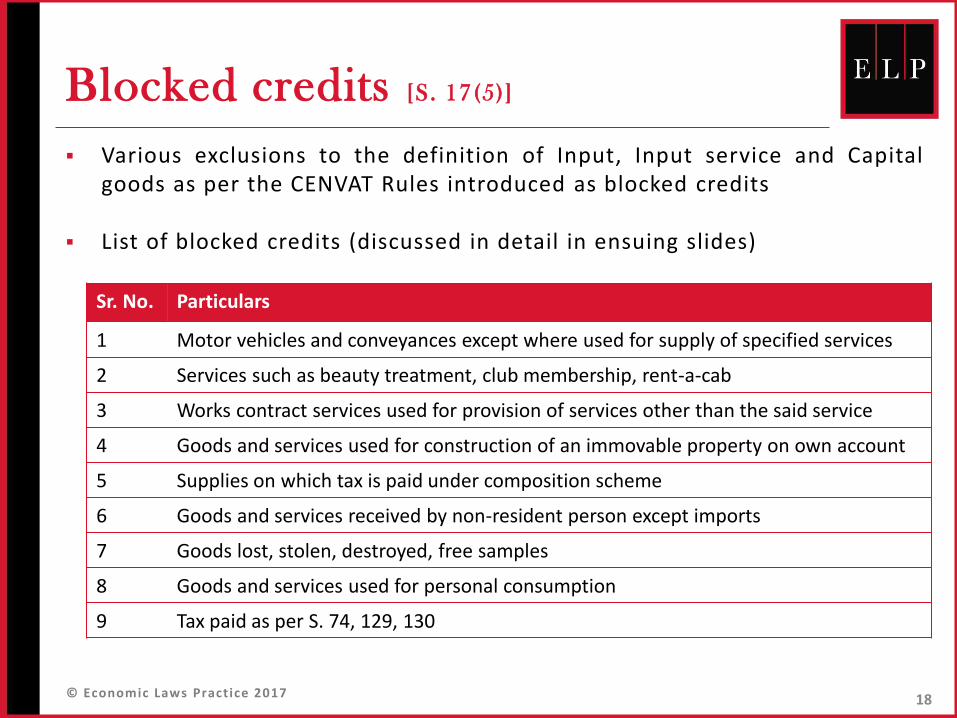

Blocked credits [S. 17(5)]

Various exclusions to the definition of Input, Input service and Capitalgoods as per the CENVAT Rules introduced as blocked credits

List of blocked credits (discussed in detail in ensuing slides)

Sr. No. Particulars

1 Motor vehicles and conveyances except where used for supply of specified services

2 Services such as beauty treatment, club membership, rent-a-cab

3 Works contract services used for provision of services other than the said service

4 Goods and services used for construction of an immovable property on own account

5 Supplies on which tax is paid under composition scheme

6 Goods and services received by non-resident person except imports

7 Goods lost, stolen, destroyed, free samples

8 Goods and services used for personal consumption

9 Tax paid as per S. 74, 129, 130

18

© Economic Laws Practice 2017

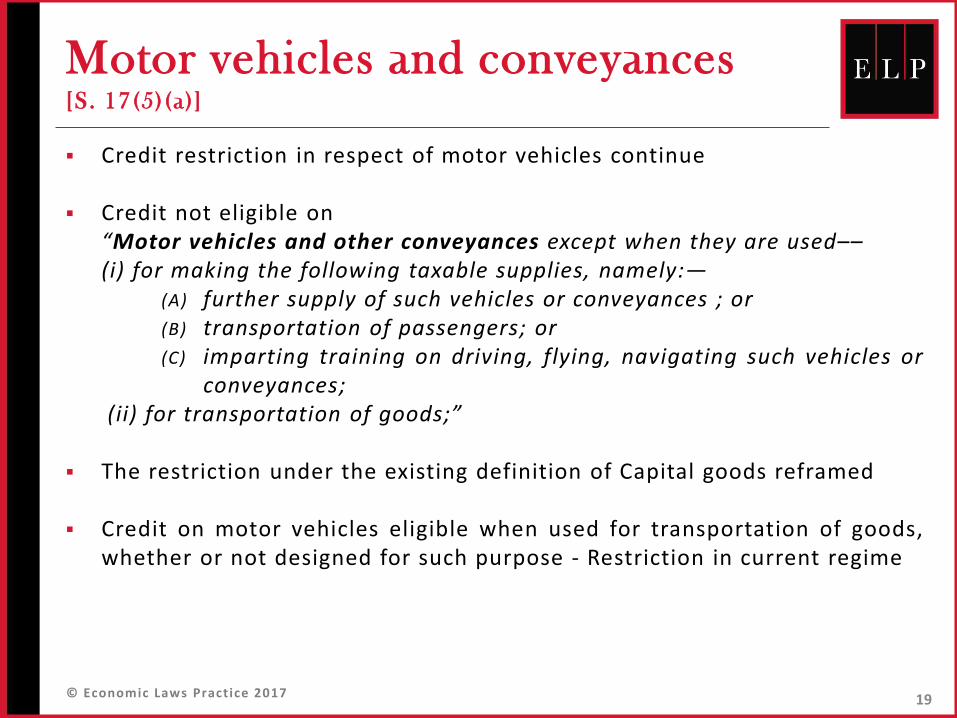

Motor vehicles and conveyances[S. 17(5)(a)]

Credit restriction in respect of motor vehicles continue

Credit not eligible on“Motor vehicles and other conveyances except when they are used––(i) for making the following taxable supplies, namely:—

(A) further supply of such vehicles or conveyances ; or(B) transportation of passengers; or(C) imparting training on driving, flying, navigating such vehicles or

conveyances;(ii) for transportation of goods;”

The restriction under the existing definition of Capital goods reframed

Credit on motor vehicles eligible when used for transportation of goods,whether or not designed for such purpose - Restriction in current regime

19

© Economic Laws Practice 2017

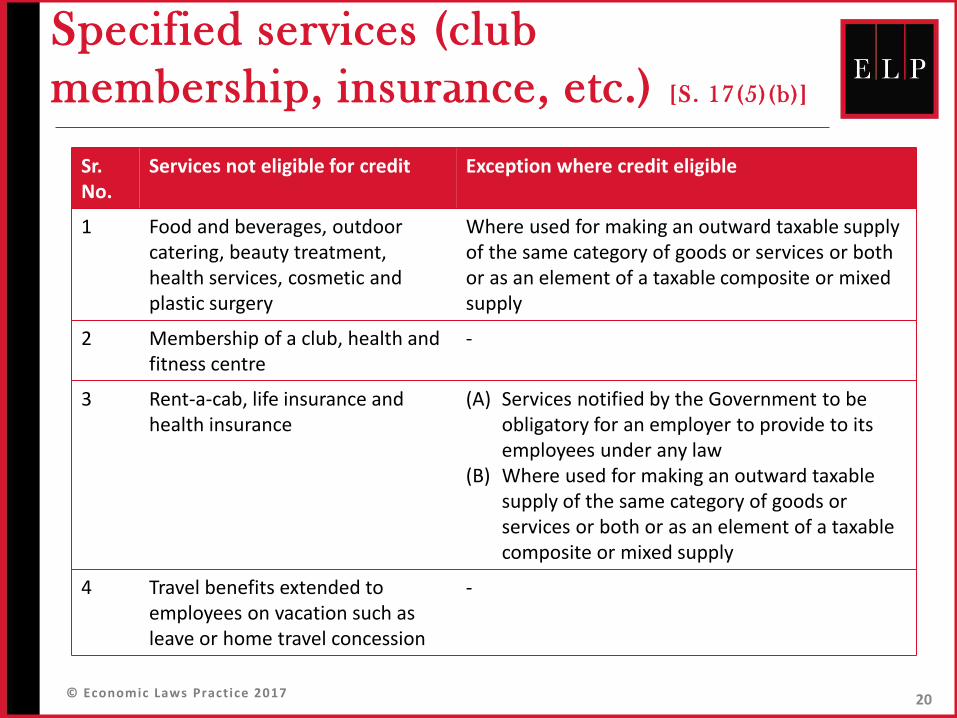

Specified services (club

membership, insurance, etc.) [S. 17(5)(b)]

Sr. No.

Services not eligible for credit Exception where credit eligible

1 Food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery

Where used for making an outward taxable supply of the same category of goods or services or both or as an element of a taxable composite or mixed supply

2 Membership of a club, health and fitness centre

-

3 Rent-a-cab, life insurance and health insurance

(A) Services notified by the Government to be obligatory for an employer to provide to its employees under any law

(B) Where used for making an outward taxable supply of the same category of goods or services or both or as an element of a taxable composite or mixed supply

4 Travel benefits extended to employees on vacation such as leave or home travel concession

-

20

© Economic Laws Practice 2017

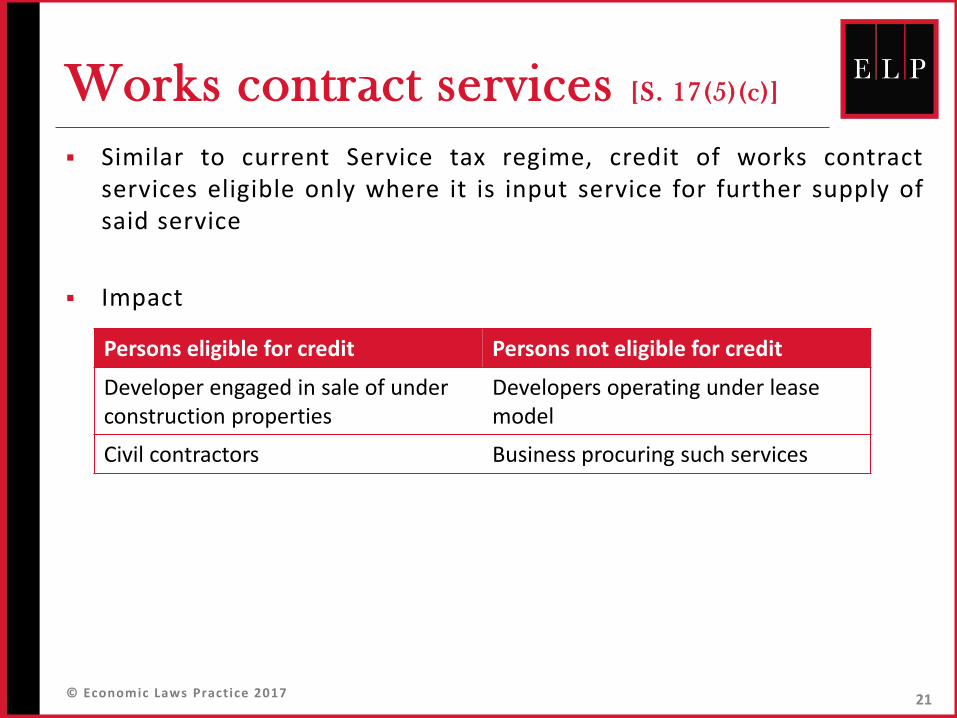

Works contract services [S. 17(5)(c)]

Similar to current Service tax regime, credit of works contractservices eligible only where it is input service for further supply ofsaid service

Impact

Persons eligible for credit Persons not eligible for credit

Developer engaged in sale of underconstruction properties

Developers operating under lease model

Civil contractors Business procuring such services

21

© Economic Laws Practice 2017

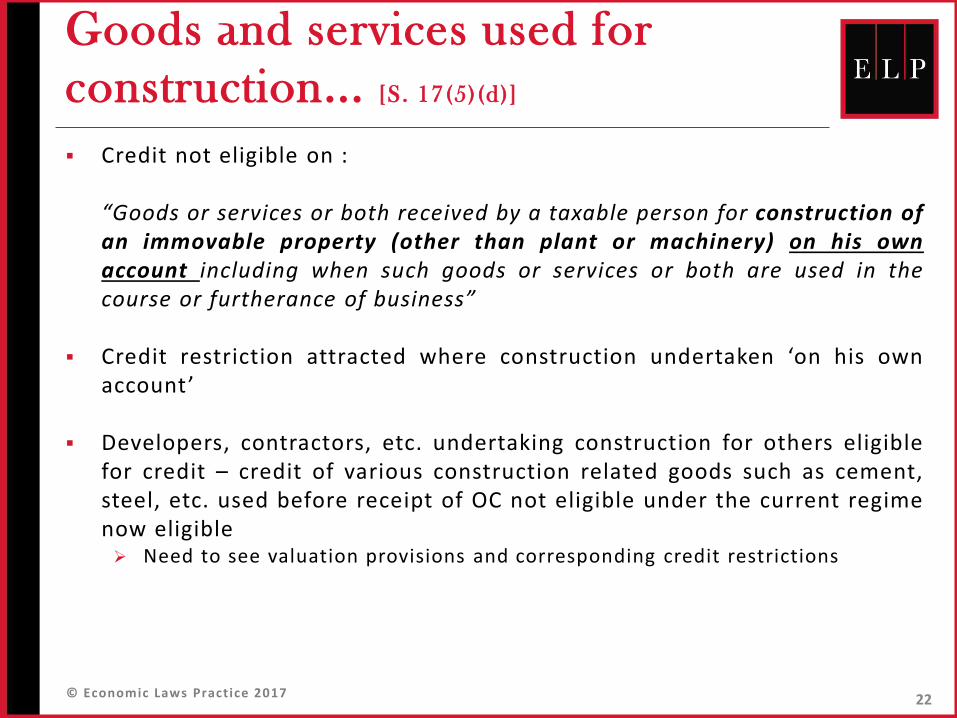

Goods and services used for

construction... [S. 17(5)(d)]

Credit not eligible on :

“Goods or services or both received by a taxable person for construction ofan immovable property (other than plant or machinery) on his ownaccount including when such goods or services or both are used in thecourse or furtherance of business”

Credit restriction attracted where construction undertaken ‘on his ownaccount’

Developers, contractors, etc. undertaking construction for others eligiblefor credit – credit of various construction related goods such as cement,steel, etc. used before receipt of OC not eligible under the current regimenow eligible Need to see valuation provisions and corresponding credit restrictions

22

© Economic Laws Practice 2017

...Goods and services used for

construction [S. 17(5)(d)]

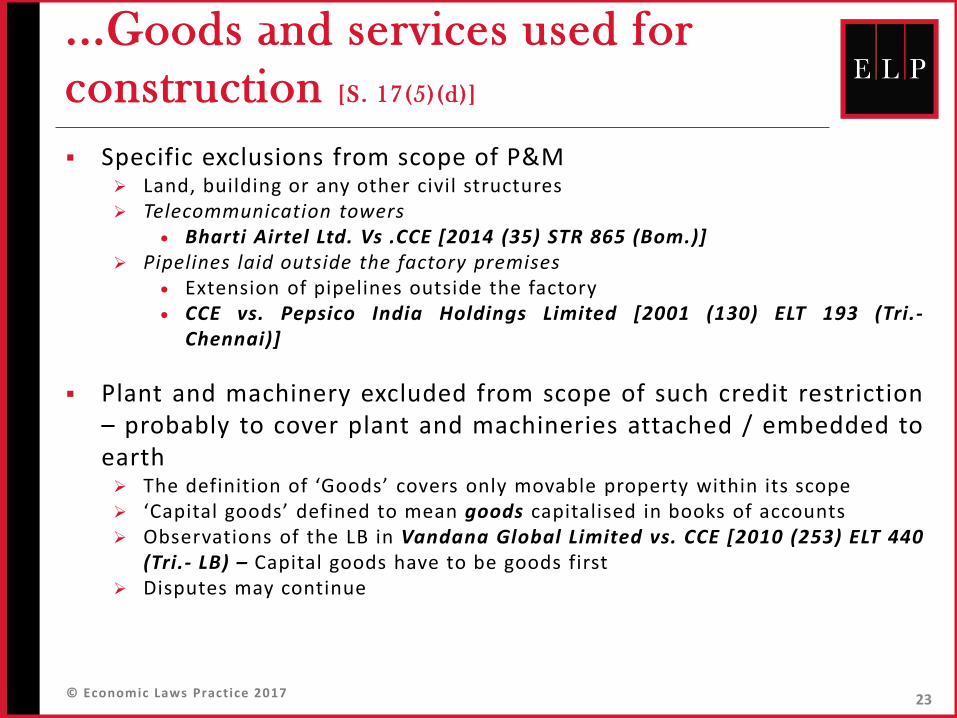

Specific exclusions from scope of P&M Land, building or any other civil structures Telecommunication towers

Bharti Airtel Ltd. Vs .CCE [2014 (35) STR 865 (Bom.)] Pipelines laid outside the factory premises

Extension of pipelines outside the factory CCE vs. Pepsico India Holdings Limited [2001 (130) ELT 193 (Tri.-

Chennai)]

Plant and machinery excluded from scope of such credit restriction– probably to cover plant and machineries attached / embedded toearth The definition of ‘Goods’ covers only movable property within its scope ‘Capital goods’ defined to mean goods capitalised in books of accounts Observations of the LB in Vandana Global Limited vs. CCE [2010 (253) ELT 440

(Tri.- LB) – Capital goods have to be goods first Disputes may continue

23

© Economic Laws Practice 2017

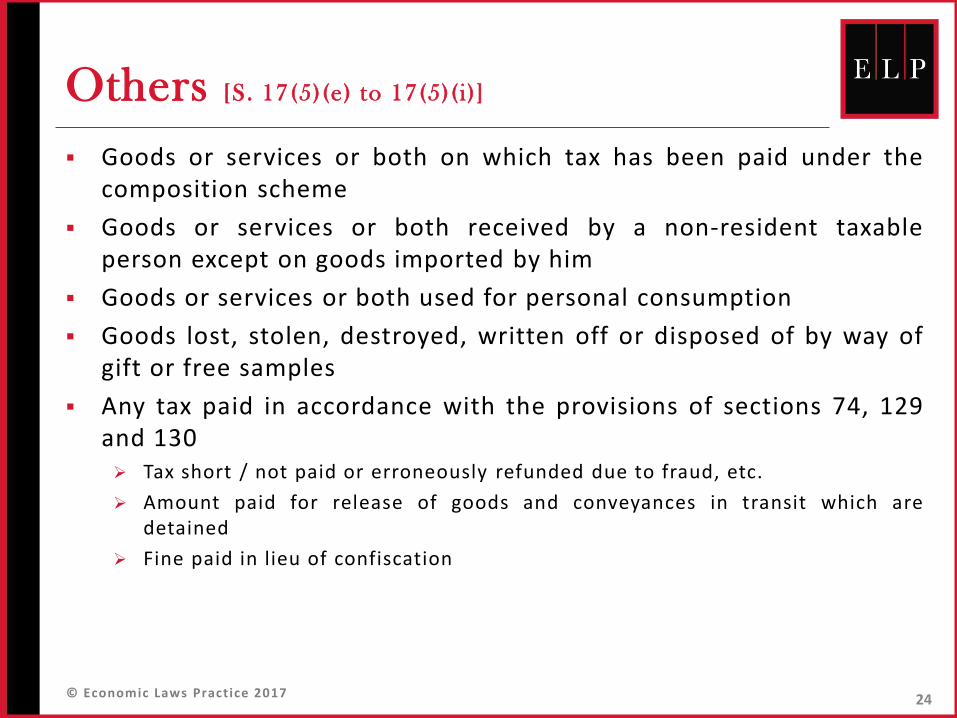

Others [S. 17(5)(e) to 17(5)( i)]

Goods or services or both on which tax has been paid under thecomposition scheme

Goods or services or both received by a non-resident taxableperson except on goods imported by him

Goods or services or both used for personal consumption

Goods lost, stolen, destroyed, written off or disposed of by way ofgift or free samples

Any tax paid in accordance with the provisions of sections 74, 129and 130 Tax short / not paid or erroneously refunded due to fraud, etc.

Amount paid for release of goods and conveyances in transit which aredetained

Fine paid in lieu of confiscation

24

© Economic Laws Practice 2017© Economic Laws Practice 2017

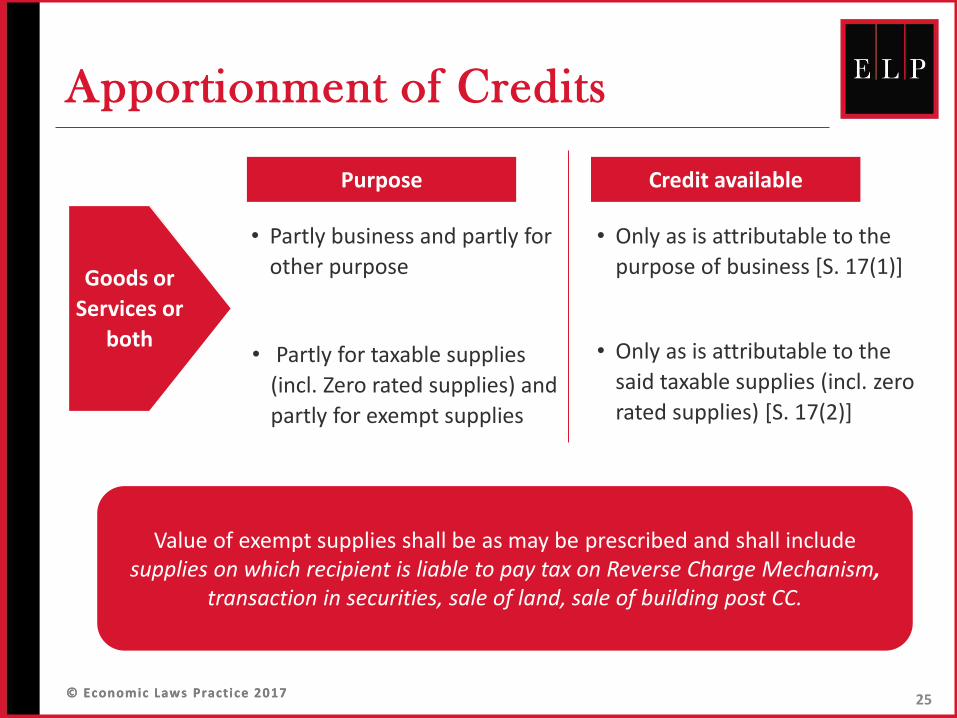

Apportionment of Credits

Goods or

Services or

both

• Partly business and partly for

other purpose

• Partly for taxable supplies

(incl. Zero rated supplies) and

partly for exempt supplies

• Only as is attributable to the

purpose of business [S. 17(1)]

• Only as is attributable to the

said taxable supplies (incl. zero

rated supplies) [S. 17(2)]

Purpose Credit available

Value of exempt supplies shall be as may be prescribed and shall include supplies on which recipient is liable to pay tax on Reverse Charge Mechanism,

transaction in securities, sale of land, sale of building post CC.

25

© Economic Laws Practice 2017

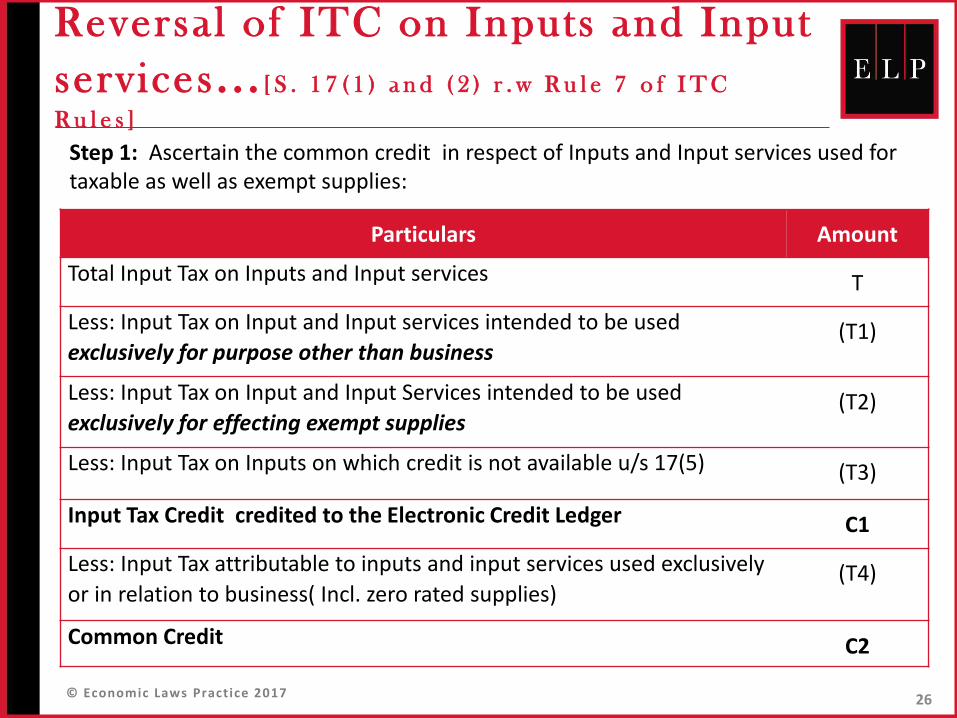

Reversal of ITC on Inputs and Input

services . . . [ S . 1 7 ( 1 ) a n d ( 2 ) r . w R u l e 7 o f I T C

R u l e s ]

26

Particulars Amount

Total Input Tax on Inputs and Input services T

Less: Input Tax on Input and Input services intended to be used

exclusively for purpose other than business(T1)

Less: Input Tax on Input and Input Services intended to be used

exclusively for effecting exempt supplies(T2)

Less: Input Tax on Inputs on which credit is not available u/s 17(5) (T3)

Input Tax Credit credited to the Electronic Credit Ledger C1

Less: Input Tax attributable to inputs and input services used exclusively

or in relation to business( Incl. zero rated supplies)(T4)

Common Credit C2

Step 1: Ascertain the common credit in respect of Inputs and Input services used for taxable as well as exempt supplies:

© Economic Laws Practice 2017

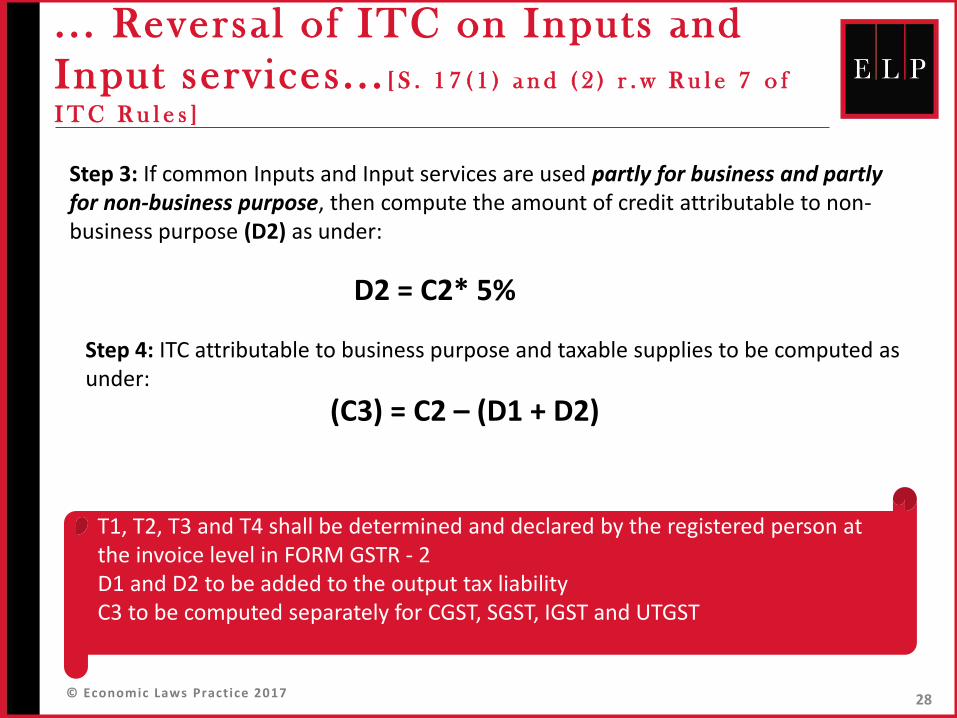

. . .Reversal of ITC on Inputs and

Input services. . . [ S . 1 7 ( 1 ) a n d ( 2 ) r . w R u l e 7 o f

I T C R u l e s ]

27

Step 2: Amount of ITC attributable to exempted supplies (D1) shall be calculated as follows:

D1 = (E/F)*C2

Where,

E is the aggregate of exempt supplies i.e. all supplies other than taxable and zero rated supplies during the tax period, andF is the total turnover of the registered person during the tax period

Value of exempt supplies include:(i) Supplies on which tax payable on reverse charge basis(ii) Value of land and building as adopted for the purpose of payment of Stamp

duty(iii) 1% of the sale of security as the value of securities

© Economic Laws Practice 2017

. . . Reversal of ITC on Inputs and

Input services. . . [ S . 1 7 ( 1 ) a n d ( 2 ) r . w R u l e 7 o f

I T C R u l e s ]

28

T1, T2, T3 and T4 shall be determined and declared by the registered person at the invoice level in FORM GSTR - 2D1 and D2 to be added to the output tax liabilityC3 to be computed separately for CGST, SGST, IGST and UTGST

Step 3: If common Inputs and Input services are used partly for business and partly for non-business purpose, then compute the amount of credit attributable to non-business purpose (D2) as under:

D2 = C2* 5%

Step 4: ITC attributable to business purpose and taxable supplies to be computed as under:

(C3) = C2 – (D1 + D2)

© Economic Laws Practice 2017

. . . Reversal of ITC on Inputs and

Input services. . . [ S . 1 7 ( 1 ) a n d ( 2 ) r . w R u l e 7 o f

I T C R u l e s ]

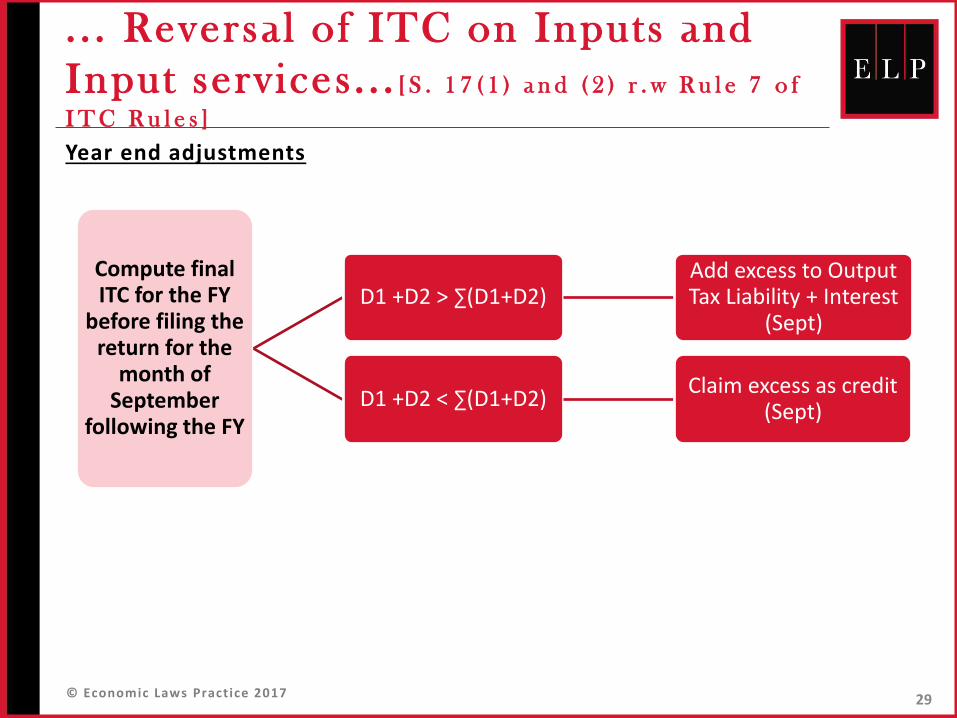

Year end adjustments

29

Compute final ITC for the FY

before filing the return for the

month of September

following the FY

D1 +D2 > ∑(D1+D2)Add excess to Output Tax Liability + Interest

(Sept)

D1 +D2 < ∑(D1+D2)Claim excess as credit

(Sept)

© Economic Laws Practice 2017

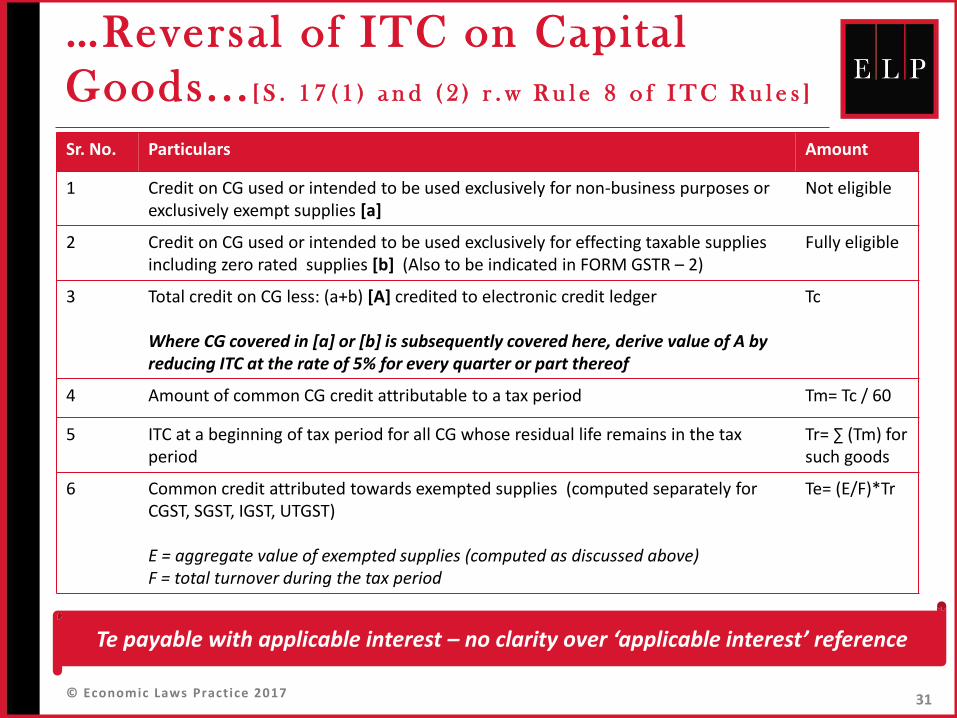

Reversal of ITC on Capital

Goods. . . [ S . 1 7 ( 1 ) a n d ( 2 ) r . w R u l e 8 o f I T C R u l e s ]

Unlike the current CENVAT Rules, the GST regime stipulates reversalof credit for Capital goods partly used for non-business purpose /exempt supplies

Exempted turnover for computation of reversal

30

Includes Excludes

(i) Supplies on which tax payable on reverse charge basis

(ii) Value of land and building as adopted for the purpose of payment of Stamp duty

(iii) 1% of the sale of security as the value of securities

(i) Excise duty levied under Entry 84 of List I

(ii) State Excise duty levied under Entry 51 of List II

(iii) Sales tax levied under Entry 54 of List II

© Economic Laws Practice 2017

…Reversal of ITC on Capital

Goods. . . [ S . 1 7 ( 1 ) a n d ( 2 ) r . w R u l e 8 o f I T C R u l e s ]

Sr. No. Particulars Amount

1 Credit on CG used or intended to be used exclusively for non-business purposes or exclusively exempt supplies [a]

Not eligible

2 Credit on CG used or intended to be used exclusively for effecting taxable supplies including zero rated supplies [b] (Also to be indicated in FORM GSTR – 2)

Fully eligible

3 Total credit on CG less: (a+b) [A] credited to electronic credit ledger

Where CG covered in [a] or [b] is subsequently covered here, derive value of A by reducing ITC at the rate of 5% for every quarter or part thereof

Tc

4 Amount of common CG credit attributable to a tax period Tm= Tc / 60

5 ITC at a beginning of tax period for all CG whose residual life remains in the tax period

Tr= ∑ (Tm) for such goods

6 Common credit attributed towards exempted supplies (computed separately for CGST, SGST, IGST, UTGST)

E = aggregate value of exempted supplies (computed as discussed above)F = total turnover during the tax period

Te= (E/F)*Tr

31

Te payable with applicable interest – no clarity over ‘applicable interest’ reference

© Economic Laws Practice 2017

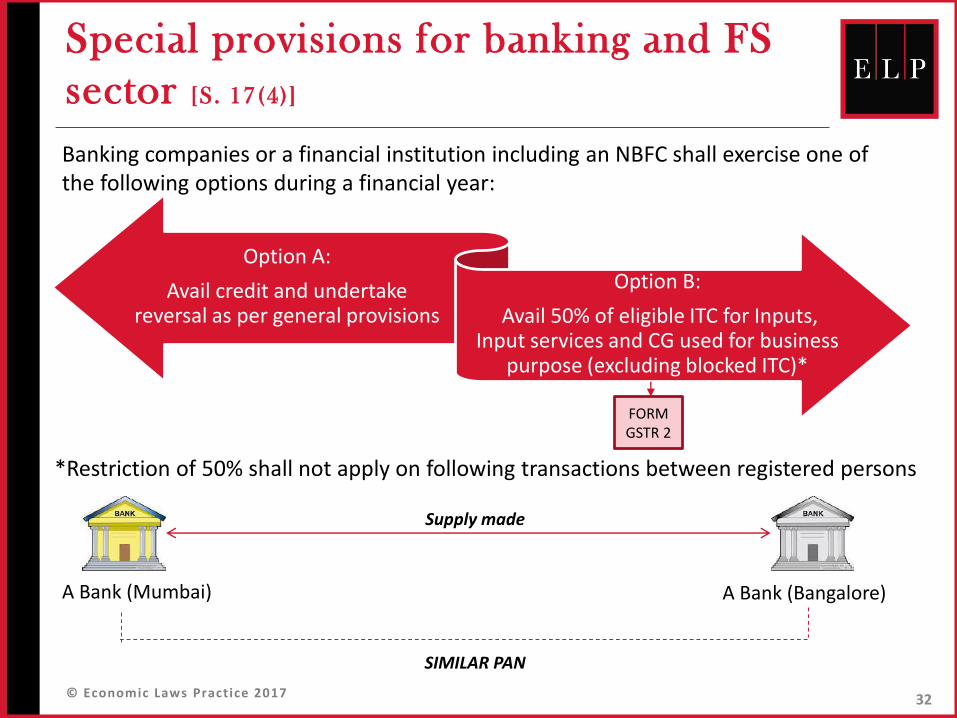

Special provisions for banking and FS

sector [S. 17(4)]

32

Supply made

A Bank (Mumbai) A Bank (Bangalore)

SIMILAR PAN

Banking companies or a financial institution including an NBFC shall exercise one of the following options during a financial year:

Option A:

Avail credit and undertake reversal as per general provisions

Option B:

Avail 50% of eligible ITC for Inputs, Input services and CG used for business

purpose (excluding blocked ITC)*

*Restriction of 50% shall not apply on following transactions between registered persons

FORM GSTR 2

© Economic Laws Practice 2017

AVAILMENT OF CREDIT IN

SPECIAL CIRCUMSTANCES

Section 18 read with Rule 5, 6, 9

33

© Economic Laws Practice 2017

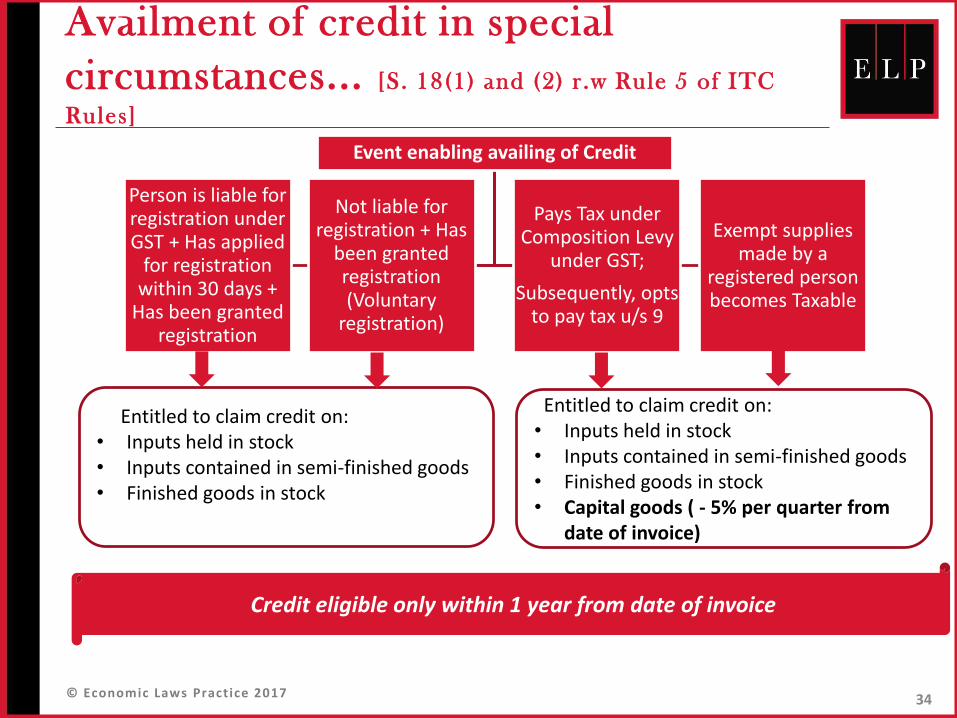

Availment of credit in special

circumstances... [S. 18(1) and (2) r .w Rule 5 of ITC

Rules]

34

Event enabling availing of Credit

Not liable for registration + Has

been granted registration (Voluntary

registration)

Pays Tax under Composition Levy

under GST;

Subsequently, opts to pay tax u/s 9

Person is liable for registration under GST + Has applied

for registration within 30 days +

Has been granted registration

Exempt supplies made by a

registered person becomes Taxable

Entitled to claim credit on:• Inputs held in stock• Inputs contained in semi-finished goods• Finished goods in stock

Entitled to claim credit on:• Inputs held in stock• Inputs contained in semi-finished goods• Finished goods in stock• Capital goods ( - 5% per quarter from

date of invoice)

Credit eligible only within 1 year from date of invoice

© Economic Laws Practice 2017

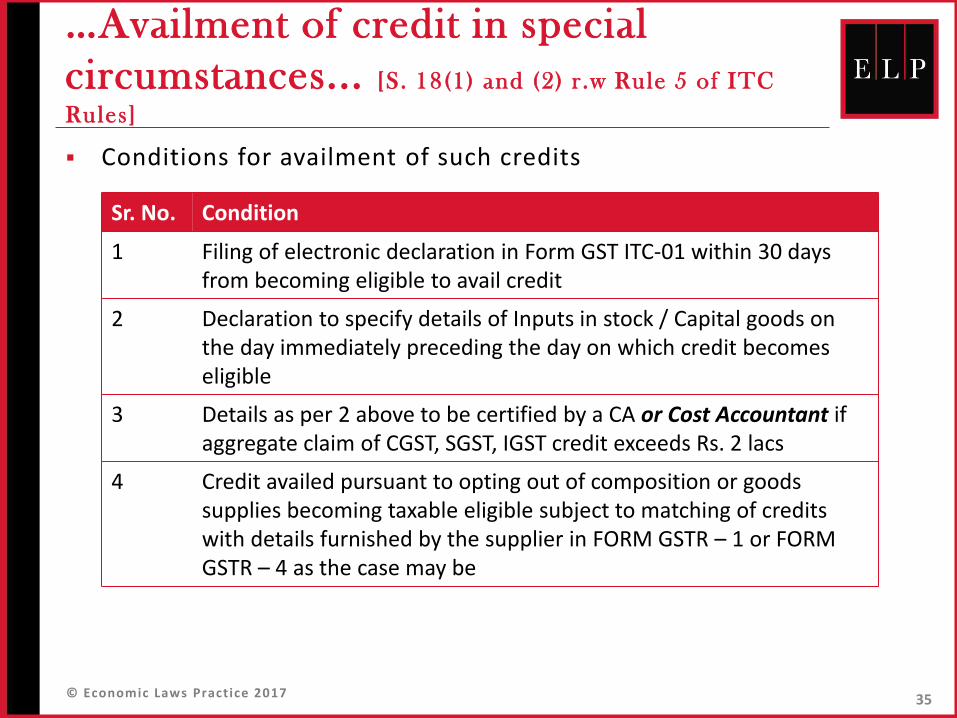

…Availment of credit in special

circumstances... [S. 18(1) and (2) r .w Rule 5 of ITC

Rules]

Conditions for availment of such credits

35

Sr. No. Condition

1 Filing of electronic declaration in Form GST ITC-01 within 30 days from becoming eligible to avail credit

2 Declaration to specify details of Inputs in stock / Capital goods on the day immediately preceding the day on which credit becomes eligible

3 Details as per 2 above to be certified by a CA or Cost Accountant if aggregate claim of CGST, SGST, IGST credit exceeds Rs. 2 lacs

4 Credit availed pursuant to opting out of composition or goods supplies becoming taxable eligible subject to matching of credits with details furnished by the supplier in FORM GSTR – 1 or FORM GSTR – 4 as the case may be

© Economic Laws Practice 2017

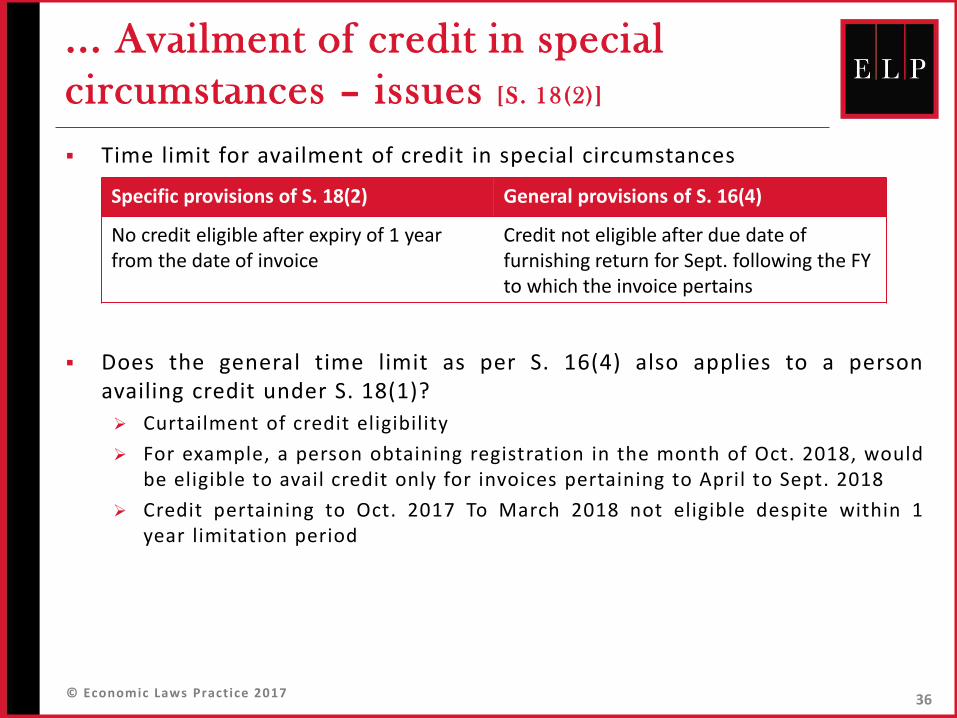

... Availment of credit in special

circumstances – issues [S. 18(2)]

Time limit for availment of credit in special circumstances

Does the general time limit as per S. 16(4) also applies to a personavailing credit under S. 18(1)?

Curtailment of credit eligibility

For example, a person obtaining registration in the month of Oct. 2018, wouldbe eligible to avail credit only for invoices pertaining to April to Sept. 2018

Credit pertaining to Oct. 2017 To March 2018 not eligible despite within 1year limitation period

36

Specific provisions of S. 18(2) General provisions of S. 16(4)

No credit eligible after expiry of 1 year from the date of invoice

Credit not eligible after due date of furnishing return for Sept. following the FY to which the invoice pertains

© Economic Laws Practice 2017

Reversal of credit in certain

circumstances... [S. 18(4), (6) r .w Rule 9 of ITC Rules]

37

Sr. No. Scenario Credit reversal

1 A registered person who has availed ITC opts to pay tax under composition

Pay amount equal to:(i) Credit on Inputs held in stock(ii) Credit of Inputs contained in semi-finished / finished goods

stock(iii) Credit on Capital goods ( - 5% per quarter)The balance of ITC after such reversal /payment shall lapse [S. 18(4)]

2 Where supplies of a registered person become fully exempt

3 Where registration is cancelled

Pay amount equal to :(i) Credit on Inputs held in stock(ii) Credit of Inputs contained in semi-finished / finished good stock(iii) Credit on Capital goods or P&M (- 5% per quarter)Or output tax payable on such goods, whichever is higher [S. 29(5)]

4 Supply of CG or P&M on which ITC has been taken (except specified goods)

Pay amount equal to higher of the following:(i) Credit on Capital goods or P&M (- 5% per quarter)(ii) Transaction value [S. 18(6)]

5 Supply of refractory bricks, moulds, dies jigs, fixtures

Pay amount equal to tax on transaction value [Proviso to S. 18(6)]

© Economic Laws Practice 2017

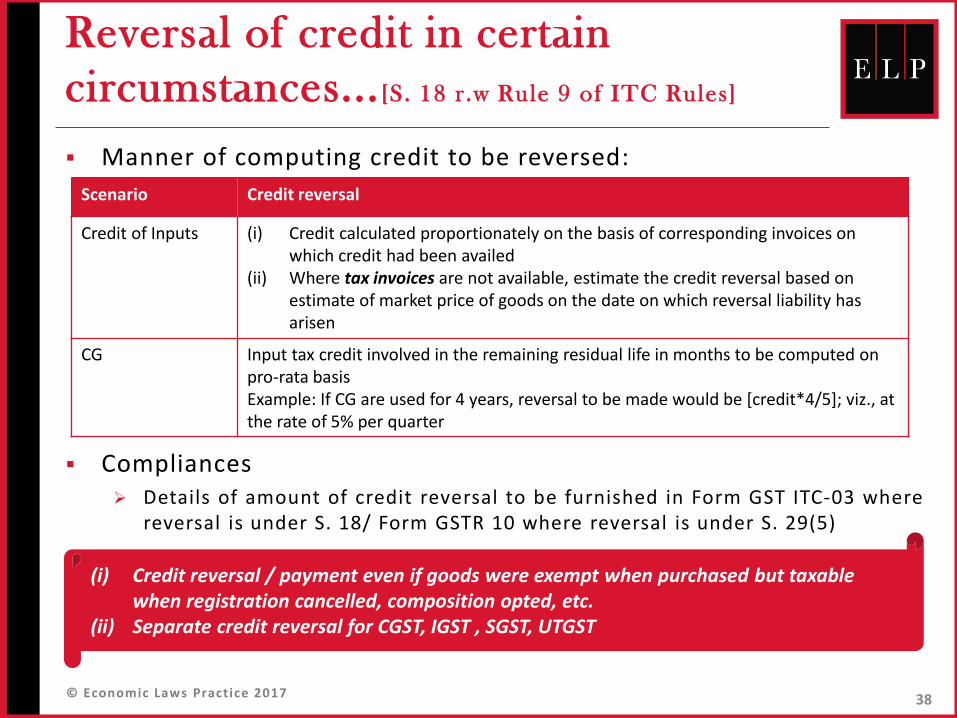

Reversal of credit in certain

circumstances... [S. 18 r .w Rule 9 of ITC Rules]

Manner of computing credit to be reversed:

Compliances Details of amount of credit reversal to be furnished in Form GST ITC-03 where

reversal is under S. 18/ Form GSTR 10 where reversal is under S. 29(5)

38

Scenario Credit reversal

Credit of Inputs (i) Credit calculated proportionately on the basis of corresponding invoices on which credit had been availed

(ii) Where tax invoices are not available, estimate the credit reversal based on estimate of market price of goods on the date on which reversal liability has arisen

CG Input tax credit involved in the remaining residual life in months to be computed on pro-rata basisExample: If CG are used for 4 years, reversal to be made would be [credit*4/5]; viz., at the rate of 5% per quarter

(i) Credit reversal / payment even if goods were exempt when purchased but taxable when registration cancelled, composition opted, etc.

(ii) Separate credit reversal for CGST, IGST , SGST, UTGST

© Economic Laws Practice 2017

Credit upon change in constitution of

business [S. 18(3) r .w Rule 6 of ITC Rules]

ITC permitted to be transferred upon change in constitution of a personon account of sale, merger, amalgamation, lease or transfer of businesswith transfer of liabilities

In case of demerger, ITC to be apportioned in the ratio of value of assetsof new unit as per the demerger scheme

The inputs and capital goods transferred shall be duly accounted for bythe transferee in his books of accounts

Procedure

39

Furnish details of change in constitution in FORM GSTR ITC-02 along with request to transfer ITC

Submit a copy of certificate issued by CA or Cost Accountant certifying that the change in constitution has

been done with the specific provisions for transfer of liabilities

Transferee shall accept the details so furnished by the transferor on the Common

Portal

© Economic Laws Practice 2017

DISTRIBUTION OF CREDIT

S. 20, 21 read with Rule 4

40

© Economic Laws Practice 2017

Credit distributed as [S. 19 r .w. Rule 4 of ITC

Rules]

41

ISDSame PAN

RecipientSame PAN

State A State A

IGST

CGST

SGST

IGST

CGST

SGST

ISDSame PAN

RecipientSame PAN

State A State B

IGST

CGST

SGST

IGST

IGST

IGST

© Economic Laws Practice 2017

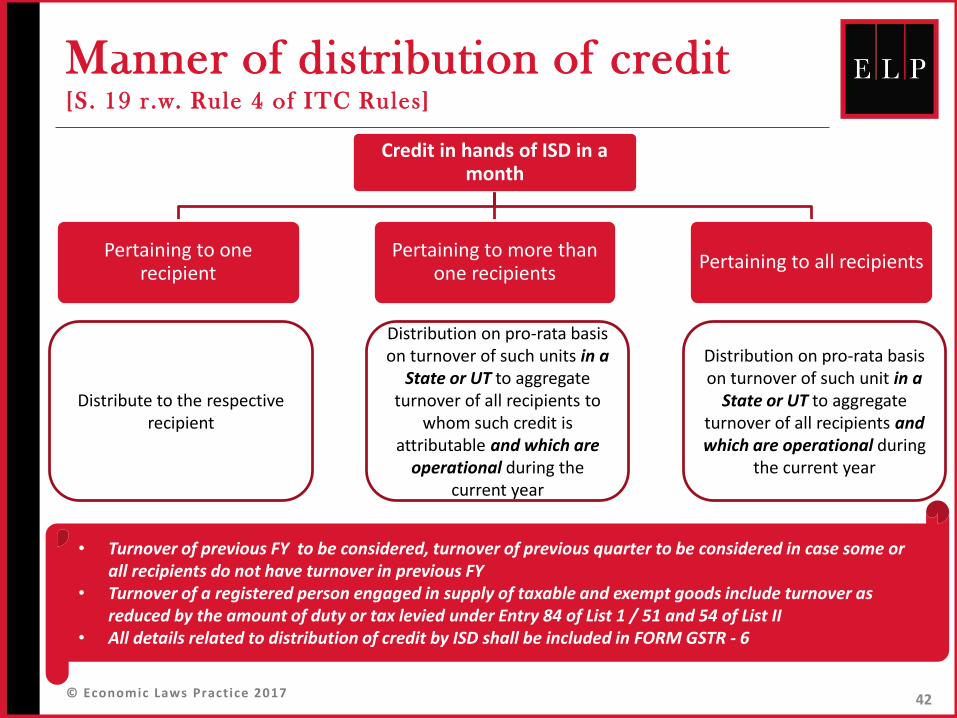

Manner of distribution of credit [S. 19 r .w. Rule 4 of ITC Rules]

42

Credit in hands of ISD in a month

Pertaining to one recipient

Pertaining to more than one recipients

Pertaining to all recipients

Distribute to the respective recipient

Distribution on pro-rata basis on turnover of such units in a

State or UT to aggregate turnover of all recipients to

whom such credit is attributable and which are

operational during the current year

Distribution on pro-rata basis on turnover of such unit in a

State or UT to aggregate turnover of all recipients and which are operational during

the current year

• Turnover of previous FY to be considered, turnover of previous quarter to be considered in case some or all recipients do not have turnover in previous FY

• Turnover of a registered person engaged in supply of taxable and exempt goods include turnover as reduced by the amount of duty or tax levied under Entry 84 of List 1 / 51 and 54 of List II

• All details related to distribution of credit by ISD shall be included in FORM GSTR - 6

© Economic Laws Practice 2017

ISD invoice

Credit to be distributed under cover of ISD invoice containing thefollowing details [Rule 7 of Draft Invoice Rules]

Details of ISD invoices to be furnished in monthly ISD return FormGSTR 6

43

Sr. No. Particulars

1 Name, address and GSTIN of the ISD

2 Consecutive serial number

3 Date of issue

4 Name, address and GSTIN of the recipient

5 Amount of credit distributed

6 Signature or digital signature of the ISD

© Economic Laws Practice 2017

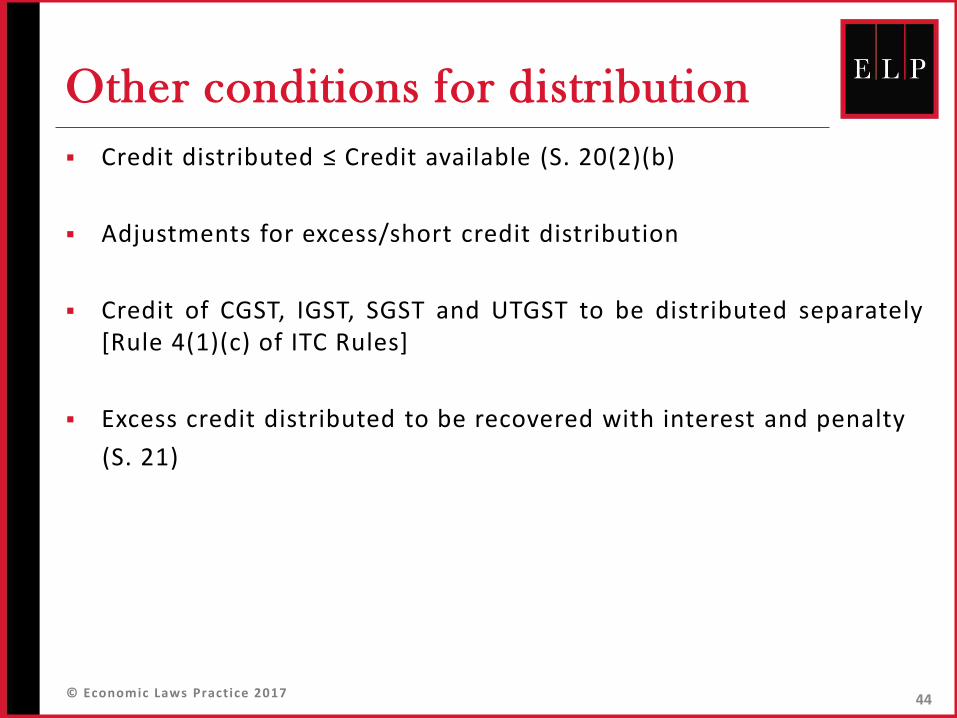

Other conditions for distribution

Credit distributed ≤ Credit available (S. 20(2)(b)

Adjustments for excess/short credit distribution

Credit of CGST, IGST, SGST and UTGST to be distributed separately[Rule 4(1)(c) of ITC Rules]

Excess credit distributed to be recovered with interest and penalty

(S. 21)

44

© Economic Laws Practice 2017

TRANSITIONAL PROVISIONS

FOR ITC

Section 140 of the CGST Act read with Rule 1 of the DraftTransition Rules

45

© Economic Laws Practice 2017

Specific definitions under CGST

Act

‘Capital goods’, ‘First stage dealer’, ‘Second stage dealer’,‘manufacture’ to have meaning as per CEA, 1944 [Explanation inChapter ‘Transitional Provisions’]

Eligible duties and taxes[S. 140(10)]

46

Eligible duties Eligible tax

Basic Excise Duty Service tax as per Section 66B of the Finance Act

CVD

SAD

Special Excise Duty, Additional Duty of Excise (GSI), etc.

Carry forward of Cess???

© Economic Laws Practice 2017

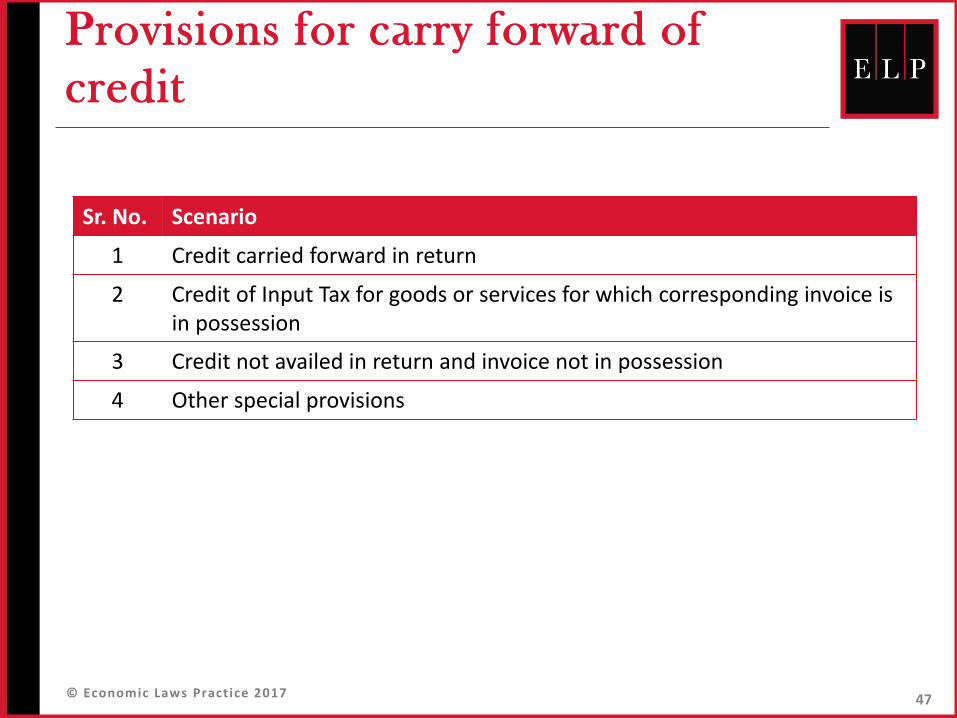

Provisions for carry forward of

credit

47

Sr. No. Scenario

1 Credit carried forward in return

2 Credit of Input Tax for goods or services for which corresponding invoice is in possession

3 Credit not availed in return and invoice not in possession

4 Other special provisions

© Economic Laws Practice 2017

General procedure for all credit claims [Rule

1(1) of Transitional Provision Rules]

48

Submit application electronically in Form

GST TRAN-1

Specify the amount of duty / tax of which credit

is entitled under transitional provisions

Submit the application within 60 days from the

appointed day

© Economic Laws Practice 2017 49

Credit carried forward in the return

© Economic Laws Practice 2017

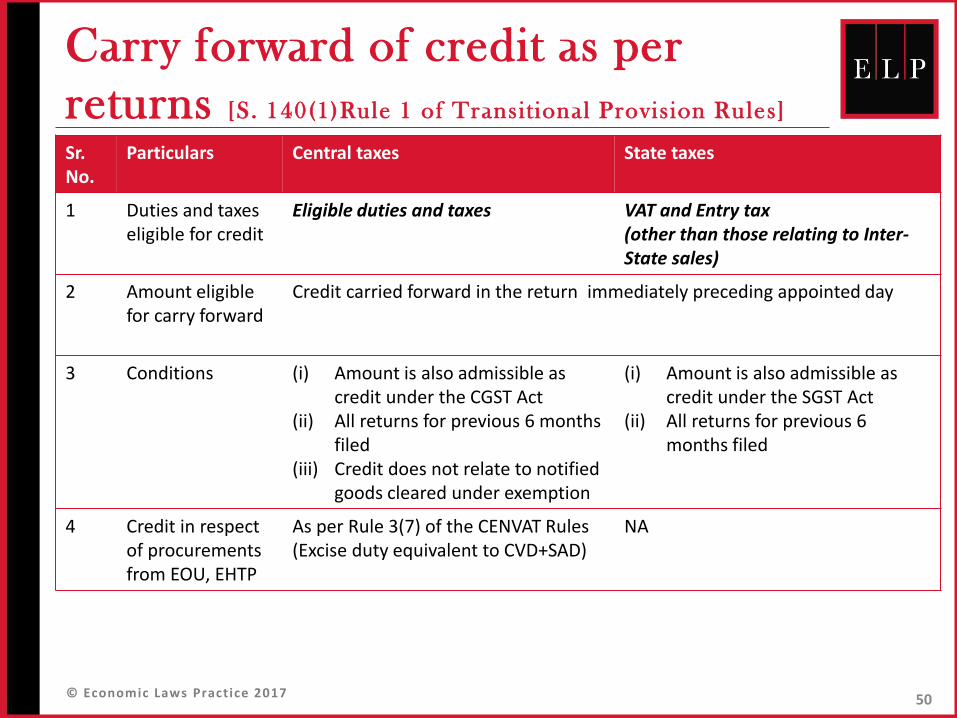

Carry forward of credit as per

returns [S. 140(1)Rule 1 of Transitional Provision Rules]

50

Sr. No.

Particulars Central taxes State taxes

1 Duties and taxes eligible for credit

Eligible duties and taxes VAT and Entry tax(other than those relating to Inter-State sales)

2 Amount eligible for carry forward

Credit carried forward in the return immediately preceding appointed day

3 Conditions (i) Amount is also admissible as credit under the CGST Act

(ii) All returns for previous 6 months filed

(iii) Credit does not relate to notified goods cleared under exemption

(i) Amount is also admissible as credit under the SGST Act

(ii) All returns for previous 6 months filed

4 Credit in respect of procurements from EOU, EHTP

As per Rule 3(7) of the CENVAT Rules(Excise duty equivalent to CVD+SAD)

NA

© Economic Laws Practice 2017 51

Credit not carried forward in return (documents available)

© Economic Laws Practice 2017

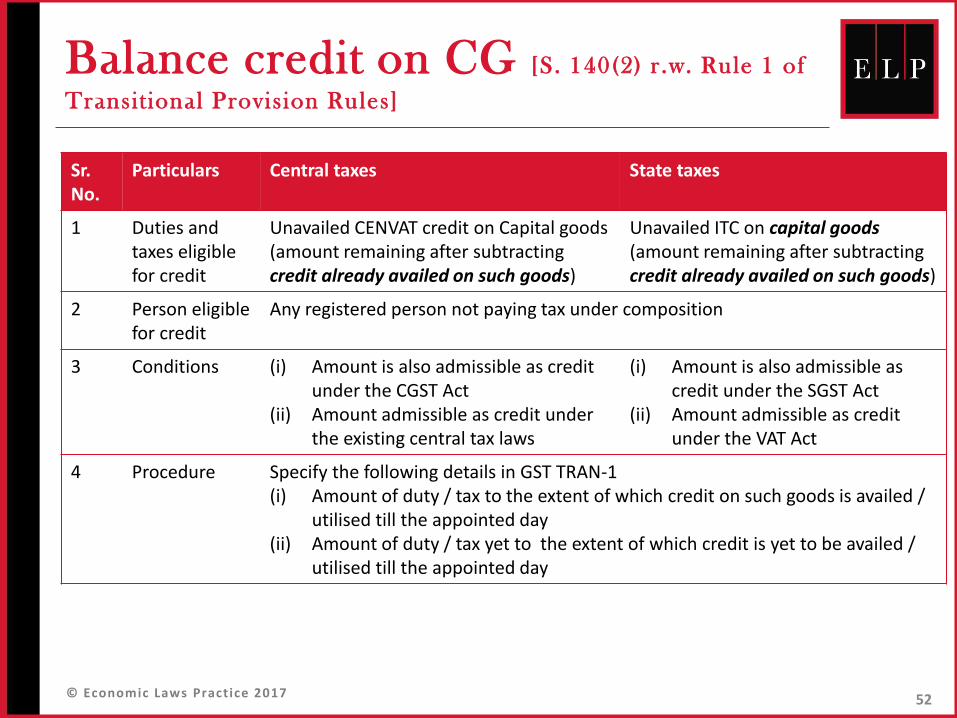

Balance credit on CG [S. 140(2) r .w. Rule 1 of

Transit ional Provision Rules]

52

Sr. No.

Particulars Central taxes State taxes

1 Duties and taxes eligible for credit

Unavailed CENVAT credit on Capital goods (amount remaining after subtracting credit already availed on such goods)

Unavailed ITC on capital goods (amount remaining after subtracting credit already availed on such goods)

2 Person eligible for credit

Any registered person not paying tax under composition

3 Conditions (i) Amount is also admissible as credit under the CGST Act

(ii) Amount admissible as credit under the existing central tax laws

(i) Amount is also admissible as credit under the SGST Act

(ii) Amount admissible as credit under the VAT Act

4 Procedure Specify the following details in GST TRAN-1(i) Amount of duty / tax to the extent of which credit on such goods is availed /

utilised till the appointed day(ii) Amount of duty / tax yet to the extent of which credit is yet to be availed /

utilised till the appointed day

© Economic Laws Practice 2017

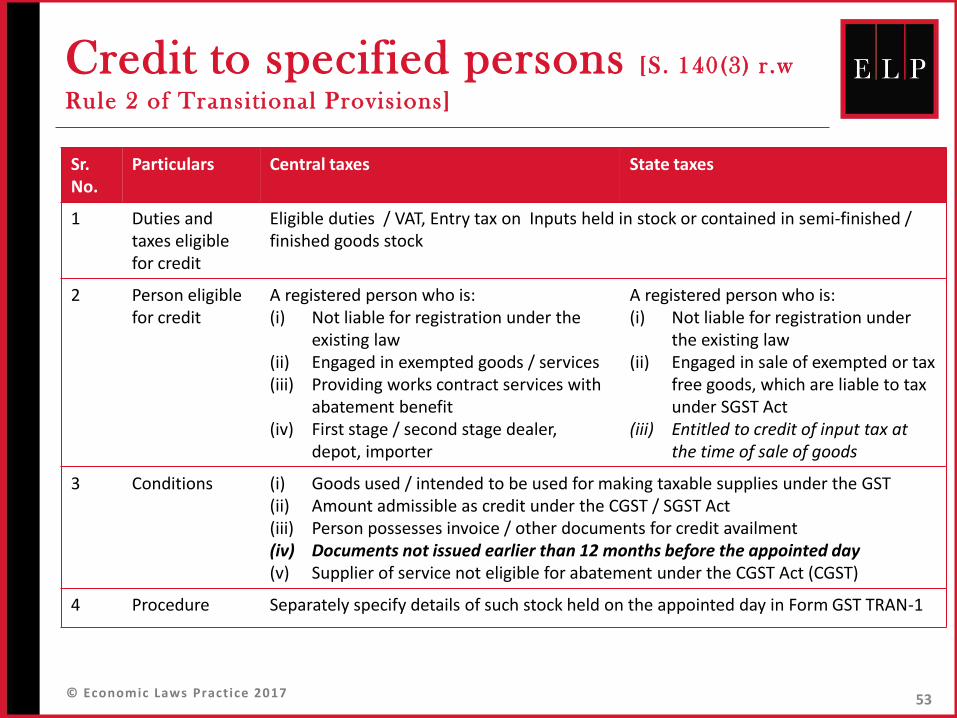

Credit to specified persons [S. 140(3) r .w

Rule 2 of Transitional Provisions]

53

Sr. No.

Particulars Central taxes State taxes

1 Duties and taxes eligible for credit

Eligible duties / VAT, Entry tax on Inputs held in stock or contained in semi-finished / finished goods stock

2 Person eligible for credit

A registered person who is:(i) Not liable for registration under the

existing law(ii) Engaged in exempted goods / services(iii) Providing works contract services with

abatement benefit(iv) First stage / second stage dealer,

depot, importer

A registered person who is:(i) Not liable for registration under

the existing law(ii) Engaged in sale of exempted or tax

free goods, which are liable to tax under SGST Act

(iii) Entitled to credit of input tax at the time of sale of goods

3 Conditions (i) Goods used / intended to be used for making taxable supplies under the GST (ii) Amount admissible as credit under the CGST / SGST Act(iii) Person possesses invoice / other documents for credit availment(iv) Documents not issued earlier than 12 months before the appointed day(v) Supplier of service not eligible for abatement under the CGST Act (CGST)

4 Procedure Separately specify details of such stock held on the appointed day in Form GST TRAN-1

© Economic Laws Practice 2017

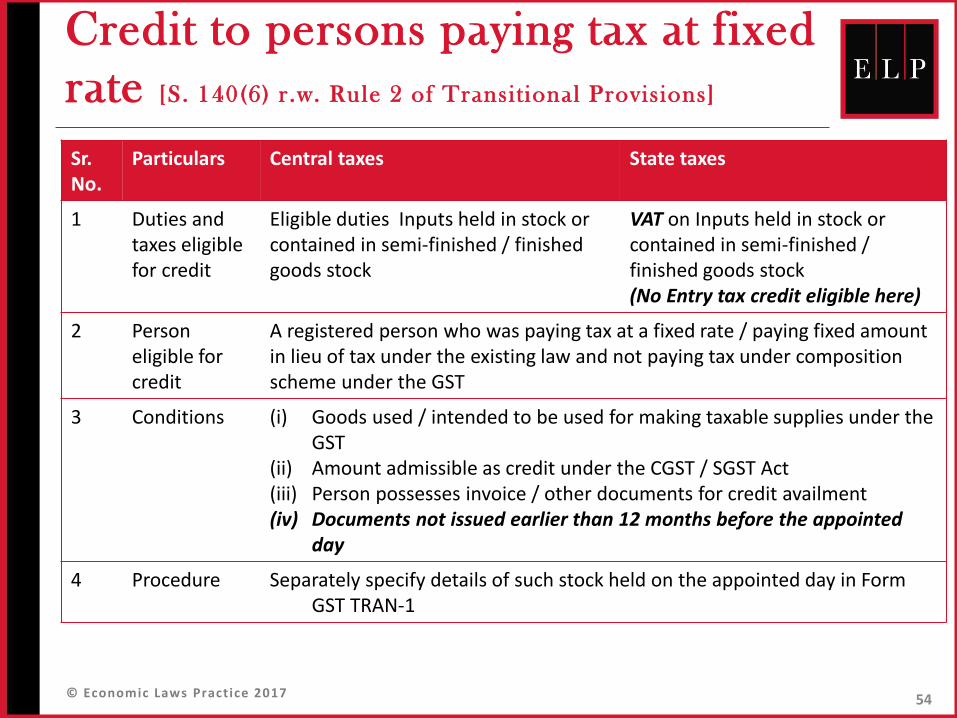

Credit to persons paying tax at fixed

rate [S. 140(6) r .w. Rule 2 of Transitional Provisions]

54

Sr. No.

Particulars Central taxes State taxes

1 Duties and taxes eligible for credit

Eligible duties Inputs held in stock or contained in semi-finished / finished goods stock

VAT on Inputs held in stock or contained in semi-finished / finished goods stock(No Entry tax credit eligible here)

2 Person eligible for credit

A registered person who was paying tax at a fixed rate / paying fixed amount in lieu of tax under the existing law and not paying tax under composition scheme under the GST

3 Conditions (i) Goods used / intended to be used for making taxable supplies under the GST

(ii) Amount admissible as credit under the CGST / SGST Act(iii) Person possesses invoice / other documents for credit availment(iv) Documents not issued earlier than 12 months before the appointed

day

4 Procedure Separately specify details of such stock held on the appointed day in Form GST TRAN-1

© Economic Laws Practice 2017

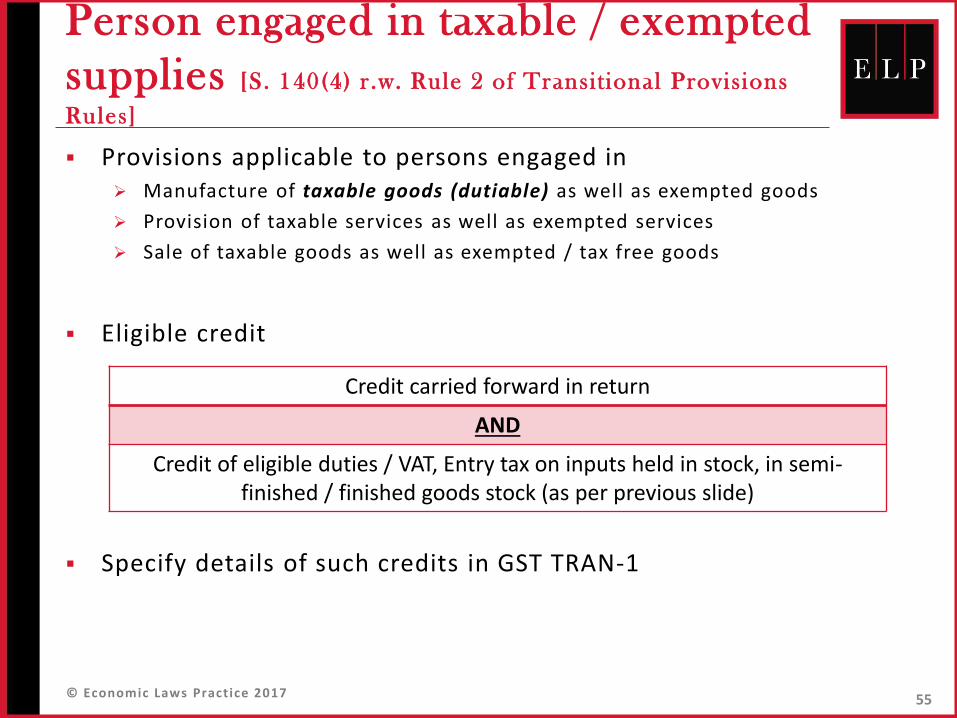

Person engaged in taxable / exempted

supplies [S. 140(4) r .w. Rule 2 of Transitional Provisions

Rules]

Provisions applicable to persons engaged in Manufacture of taxable goods (dutiable) as well as exempted goods

Provision of taxable services as well as exempted services

Sale of taxable goods as well as exempted / tax free goods

Eligible credit

Specify details of such credits in GST TRAN-1

55

Credit carried forward in return

AND

Credit of eligible duties / VAT, Entry tax on inputs held in stock, in semi-finished / finished goods stock (as per previous slide)

© Economic Laws Practice 2017

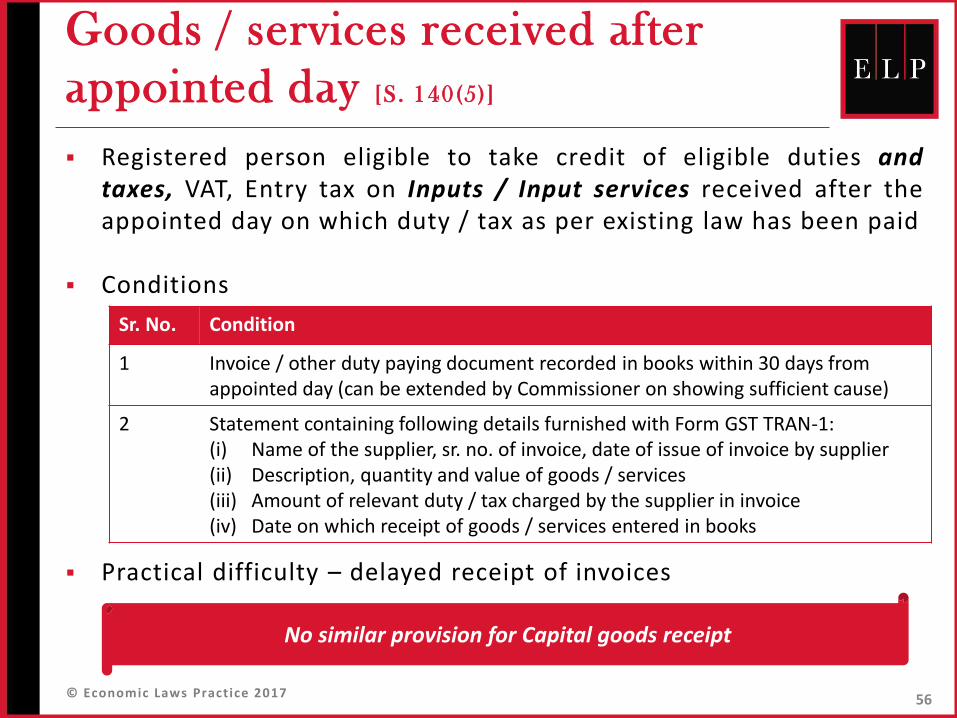

Goods / services received after

appointed day [S. 140(5)]

Registered person eligible to take credit of eligible duties andtaxes, VAT, Entry tax on Inputs / Input services received after theappointed day on which duty / tax as per existing law has been paid

Conditions

Practical difficulty – delayed receipt of invoices

56

Sr. No. Condition

1 Invoice / other duty paying document recorded in books within 30 days from appointed day (can be extended by Commissioner on showing sufficient cause)

2 Statement containing following details furnished with Form GST TRAN-1:(i) Name of the supplier, sr. no. of invoice, date of issue of invoice by supplier(ii) Description, quantity and value of goods / services(iii) Amount of relevant duty / tax charged by the supplier in invoice(iv) Date on which receipt of goods / services entered in books

No similar provision for Capital goods receipt

© Economic Laws Practice 2017 57

Credit for which invoices are not in possession

© Economic Laws Practice 2017

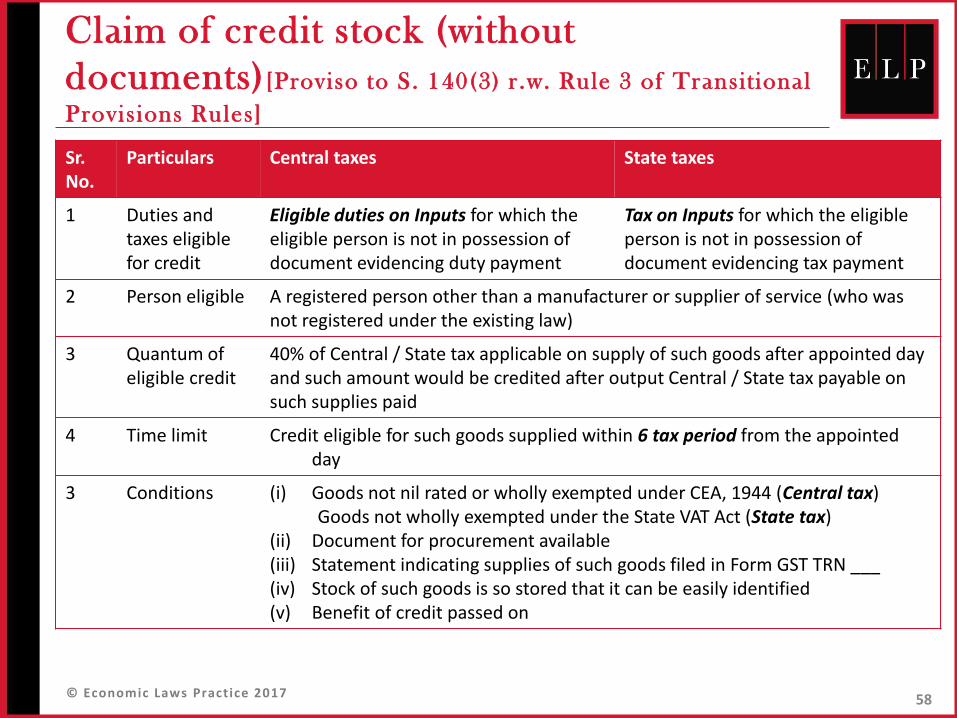

Claim of credit stock (without

documents) [Proviso to S. 140(3) r .w. Rule 3 of Transitional

Provisions Rules]

58

Sr. No.

Particulars Central taxes State taxes

1 Duties and taxes eligible for credit

Eligible duties on Inputs for which the eligible person is not in possession of document evidencing duty payment

Tax on Inputs for which the eligible person is not in possession of document evidencing tax payment

2 Person eligible A registered person other than a manufacturer or supplier of service (who was not registered under the existing law)

3 Quantum of eligible credit

40% of Central / State tax applicable on supply of such goods after appointed day and such amount would be credited after output Central / State tax payable on such supplies paid

4 Time limit Credit eligible for such goods supplied within 6 tax period from the appointed day

3 Conditions (i) Goods not nil rated or wholly exempted under CEA, 1944 (Central tax)Goods not wholly exempted under the State VAT Act (State tax)

(ii) Document for procurement available(iii) Statement indicating supplies of such goods filed in Form GST TRN ___(iv) Stock of such goods is so stored that it can be easily identified(v) Benefit of credit passed on

© Economic Laws Practice 2017 59

Other special provisions for CGST Act

© Economic Laws Practice 2017

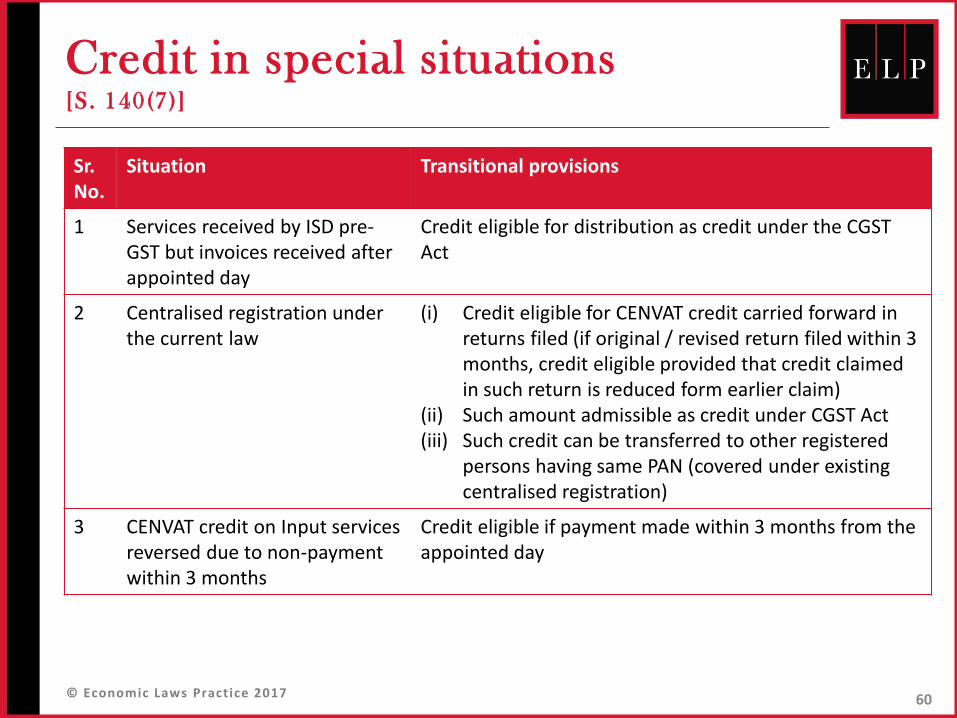

Credit in special situations[S. 140(7)]

60

Sr. No.

Situation Transitional provisions

1 Services received by ISD pre-GST but invoices received after appointed day

Credit eligible for distribution as credit under the CGST Act

2 Centralised registration under the current law

(i) Credit eligible for CENVAT credit carried forward in returns filed (if original / revised return filed within 3 months, credit eligible provided that credit claimed in such return is reduced form earlier claim)

(ii) Such amount admissible as credit under CGST Act(iii) Such credit can be transferred to other registered

persons having same PAN (covered under existing centralised registration)

3 CENVAT credit on Input services reversed due to non-payment within 3 months

Credit eligible if payment made within 3 months from the appointed day

© Economic Laws Practice 2017

Don’t Count The Days…. Make The Days Count

61

© Economic Laws Practice 2017© Economic Laws Practice 2017 62

MUMBAI

109 A, 1st FloorDalamal TowersFree Press Journal RoadNariman PointMumbai 400 021T: +91 22 6636 7000F: +91 22 6636 7172E: [email protected]

NEW DELHI

801 A, 8th FloorKonnectus TowerBhavbhuti MargOpp. Ajmeri Gate Railway StationNr. Minto BridgeNew Delhi 110 002T: +91 11 4354 8400F: +91 11 4353 8436E: [email protected]

PUNE

701, 7th FloorSuyog Fusion197 Dhole Patil RoadNr. Ruby Hall ClinicPune 411 001T: +91 20 4146 7400F: +91 20 4146 7402E: [email protected]

AHMEDABAD

801, 8th FloorAbhijeet IIIMithakali Six RoadEllisbridgeAhmedabad 380 006T: +91 79 6605 4480/1F: +91 79 6605 4482E: [email protected]

BENGALURU

6th FloorRockline Centre54, Richmond RoadBangalore 560 025T: +91 80 4168 5530/1E: [email protected]

CHENNAI

No. 6, 4th LaneNungambakkam High RoadChennai 600 034T: +91 44 4210 4863E: [email protected]

© E

co

no

mic

La

ws

Pra

cti

ce

20

17

Disclaimer: The information provided in this presentation is intended for informational purposes only and does notconstitute legal opinion or advice. Readers are requested to seek formal legal advice prior to acting upon any of theinformation provided herein. This presentation is not intended to address the circumstances of any particular individual orcorporate body. There can be no assurance that the judicial/ quasi judicial authorities may not take a position contrary tothe views mentioned herein.