Input Tax Credit and Composition Levy 23122016IGST IGST CGST SGST CGST CGST IGST SGST SGST IGST....

40

WORKSHOP ON GST

Transcript of Input Tax Credit and Composition Levy 23122016IGST IGST CGST SGST CGST CGST IGST SGST SGST IGST....

WORKSHOP ON GST

The full right to deduct input tax through thesupply chain, except by the final consumer,ensures the neutrality of the tax, whatever thenature of the product, the structure of thedistribution chain and the technical meansused for its delivery (retail stores, physicaldelivery, Internet).

Destination basedconsumption tax allowsseamlessflow of ITCB2B Transactions Tax shouldnever be added.B2C Transactions Tax formspart of the cost of goods and / orservices wherein they are finallyconsumed.

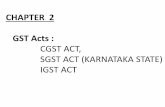

A-Vadodara

B-Mumbai

C-Karnataka

IGST

IGST

CGST

SGST

CGST

CGST

IGST

SGST

SGST

IGST

Important Definitions under Revised GST Model Law

Section 2(52): Input means any goods other thanCapital Goods used or intended to be used by aSupplier in the course or furtherance of business.Section 2(53): Input Services means any service usedor intended to be used by a Supplier in the course orfurtherance of business.Section 2(19): Capital Goods means Goods, the valueof which is capitalized in the books of accounts of theperson claiming the credit and which are used orintended to be used in the course or furtherance ofbusiness.

Section 2(55): Input Tax" in relation to ataxable person, means the IGST, including thaton import of goods, CGST and SGST chargedon any supply of goods or services to him andincludes the tax payable under sub-section (3)of section 8, but does not include the tax paidunder section 9.Section 2(56): Input Tax Credit means creditof Input Tax asdefined in Sub-Section 55.

Present Regime

In or in relation tobeing used in CENVATCredit Rules, 2004 andfor the purpose of

making Sale beingused in the VATLaws.

Proposed revised Model GST Law

Used or Intended to be used in the course or furtherance of business.

Tax Invoice, Debit Note or other to be prescribed Tax

Paying Document

Receipt of Goods / Services (Goods received on Lots / Installments against an Invoice last receipt)

Tax charged must have been paid to the account of

Appropriate Government

Return must have been furnished by him u/s. 34

ITC

Motor Vehicles and other conveyances except when they are used for:

Further Supply of suchVehicles orConveyances

Transportation ofPassengers

Imparting Training onDriving, Flying,navigating such vehiclesor conveyances

Transportation ofGoods

No ITC on Inward Supply of Goods and Services

Food and BeveragesOutdoor CateringBeauty TreatmentHealth ServicesCosmetic and Plastic Surgery

Club MembershipMembership of Health

and Fitness CentreRent-A-CabLife InsuranceHealth Insurance except

obligation by Governmenton employers to provide toits employees.Travel Benefits extended

to employees on vacationsuch as leave or HomeTravel Concession.

ITC in Works Contract and Construction

Works Contract Servicewhen supplied forconstruction of ImmovableProperty, other than Plantand Machinery, exceptwhen it is an Input Servicefor further supply of WorksContract Service.

Goods or Services receivedby a taxable person forconstruction of animmovable property on hisown account, other thanPlant and Machinery, evenwhen used in course orfurtherance of business.

Goods / Services on which Tax has been paidunder Section 9.Goods / Services used for personalconsumption.Goods lost, stolen, destroyed, written off ordisposed of by way of gift or free samples.Any tax paid in termsof Section 67, 89 or 90.

Restriction on ITC when Goods / Services areused by Registered Taxable Person partly forBusinessand partly for other purpose.In case of Goods / Services being used foreffecting both - Taxable Supplies includingZero-Rated Supplies and for effecting exemptsupplies, the ITCshall be available only for theGoods / Services used for Taxable Suppliesincluding Zero-Rated Supplies.

What about RCM???A Banking Co, a Financial Institution and NBFCshall have the option to follow the above or avail50% of eligible ITC on Inputs, Capital Goods andInput Services in every month. The option onceexercised shall not be withdrawn during the year.Manner shall be prescribed for aboveapportionments. So again Rule 6 of CENVATCredit Rules, 2004????

Provisional Acceptance of ITC and it s Utilization

Section 36 Sub-Section (1) and (2):ITC (as self assessed in his Return) to becredited in Electronic Credit Ledger on aprovisional basis.Provisional ITC Credit can be utilized only forthe payment of self-assessed output taxliability asper the Return.

Matching, Reversal and Reclaim of ITC

With corresponding details of outward Supply furnished

With the Additional Duty of Customs paid

For Duplication of Claims

Matching, Reversal and Reclaim of Reduction in Output Tax Liability

With corresponding in Claim for ITC

For Duplication of Claims

If any person claims that he is eligible forInput Tax Credit, the burden of proving suchclaim or claimsshall lie on him.

Will there be any time bar on usage of ITC???

Section 44 a simple Section but Sub-Section(4) needsto be pondered upon.The Amount available in the electronic Credit

Ledger may be used for making any paymenttowards Output Tax payable under theprovisions of the Act or the Rules made thereunder in such manner and subject to suchconditions and within such time as may beprescribed.

The recipient of service is required to makepayment of invoice amount along with taxthereon to the supplier of service within a periodof 3 months from the date of issue of invoice, thefailure of which will result in the addition inoutput tax liability.No ITCafter filing of Return u/s. 34 for the monthof September or filing of Annual Return,whichever isearlier. No direct reference.

ITC- A boon for Telecom Companies

CENVAT Credit on Telecommunication Towers denied in the present regime.ITC on Pipelines and Telecommunication Towers including foundation and structural support thereto shall be available in installments.

Tax to be deducted at source at the rate of 1% by theRecipient from the payment to be made or credited tothe supplier of Taxable Goods / Services to be notifiedby the CG or a SG on the recommendations of theCouncil, where the total value of such supply, under acontract, exceedsRs. 5,00,000/-.Value to be taken inclusive of tax or exclusive of tax???TDSto be deposited within 10 days from the end of themonth along with a Return to be furnished in GSTR-7.

Certificate to be furnished within 5 days, otherwise beready for penalty Rs. 100/- per day subject to amaximum of Rs. 5,000/-.The deductor to furnish TDS Return by 10th of nextmonth and the said amount shall be available as creditin Electronic Cash Ledger in the manner as may beprescribed.Refund to the deductor or deductee, arising on accountof excess or erroneous deduction shall be governed bySection 48. No Refund to deductor if amount of TDScredited to Electronic Ledger of the deductee.

1% of Net Taxable Value of Supplies madethrough E-Commerce Operator shall becollected as TCS by the Operator where theconsideration with respect to such supplies isto be collected by the Operator.The Operator to deposit the collected amountand file a Return within 10 days after the endof the month.Credit to be claimed in Electronic Cash Ledger.

No ITC if registered taxable person hasclaimed depreciation on the tax component ofthe cost of capital goodsunder the provisionsof the Income Tax Act, 1961. Section 16(3).What about Input Services capitalized in thebooks of accounts of a registered taxableperson???

Section 15 (3)(b)(ii) of the Model CGSTAct:Reversal of ITCby the recipient of supply as isattributable to the discount on the basis ofdocument issued by the supplier.

Present RegimeMoney Changing Agent, Air Travelling Agent,Life Insurance Business and Lottery Agentsunder Finance Act, 1994 and specified WorksContractors and Builders and assesses havingTurnover below the prescribed limit underState VATLaws.

Composition Levy GST perspective

Overriding Provision over other provisions butsubject to RCM Section 8(3).Council s recommendationConditionsand Restrictionsto be prescribed.Permission shall be granted to a registeredTaxable Person by the proper officer of theCentral or the State Government.

ARegistered Taxable PersonAggregate Turnover in the preceding

financial year did not exceed Rs. 50 Lakhs.Permission to get automatically withdrawnfrom the day on which aggregate turnover inthe present FYexceedsRs. 50 Lakhs.

All India basis same PAN

Taxable Supplies

Export of Goods / Services

Inter State Supplies of a person

having the same PAN

RCMValue of Inward

Supplies

Not Taxable + Nil Rate + Exemption u/s.11

Not lessthan 2.50%in case of a manufacturerand 1%in any other case of the Turnover in aState duringthe year.

Supplier of ServiceAny Supply of Goodswhich are not leviable to taxunder GSTInter-State Outward SuppliesSupply of Goods through E-Commerce Operatorwho isrequired to collect tax at sourceManufacturer of such goods as may be notifiedon the recommendation of the Council.

ITC not availableTax paid by supplier cannot be claimed as ITCby the recipient as the Tax cannot be collectedfrom the recipient.Transitional Provisions to be taken intoconsideration at the time of shifting fromComposition to Normal Taxability and vice aversa.

If Return not furnished for 3 consecutive taxperiods, the proper officer may cancel theregistration. (Different criteria for others)Instead of Tax Invoice, a Bill of Supply needs to beissued.Return to be furnished quarterly in GSTR-4 by18th of the month following the end of thequarter.Section 166(7) and proviso there to dealing withMigration of Existing Tax Payers to GST to betaken into consideration.

Multiple Registrations State Wise as well as vertical wise within the state???Optional or Mandatory??Mixed Supply??Composite Supply???