Innovative Finance to increase Agricultural Technology Adoption Anna Yalouris J-PAL Africa...

47

Innovative Finance to increase Agricultural Technology Adoption Anna Yalouris J-PAL Africa University of Cape Town

-

Upload

gervase-mckinney -

Category

Documents

-

view

216 -

download

3

Transcript of Innovative Finance to increase Agricultural Technology Adoption Anna Yalouris J-PAL Africa...

Innovative Finance to increase Agricultural Technology Adoption

Anna YalourisJ-PAL AfricaUniversity of Cape Town

WHO IS J-PAL?

500+ ongoing and completed evaluations

Randomized Evaluations (REs)

• Identify an eligible population

• Before the program starts, randomly assign individuals (or villages, schools, etc.) to different groups• Treatment: receives intervention• Comparison: status quo

• Groups are statistically equivalent due to randomization

• Any difference in outcomes can be attributed to the intervention

Agricultural Technology Adoption Initiative

Credit market projects

How might credit market constraints affect technology adoption?

• Farmers don’t have cash to cover the upfront costs of adoption

• Farmers don’t have collateral to back a loan

• Farmers don’t have financial literacy needed to use credit

• There is no credit available

• Farmers struggle to save income from one harvest to the next

How might improving access to

credit help?• Access to financial products can

affect agricultural activity• Switching to higher-value crops • Investing in long-lasting inputs• crop-related expenditures • fertilizer use

Ashraf et al. 2009; Crepon et al. 2013; Tarozzi et al. 2013; Beaman et al. 2014; Karlan et al. 2013; Carter et al. 2013

Challenge of agricultural lending

• Clients often lack adequate collateral

• Lenders cannot schedule frequent repayments

• All farmers need cash at the same time (planting season)

• Joint liability may be ineffective if individual production shocks are correlated with weather

• Lenders have limited information on profitability of customers

When does credit work?

1. Flexible collateral arrangements• Asset collateralized loans for dairy farmers

2. Improved information about borrowers to improve credit markets

• Fingerprinting to reduce risky borrowing

3. The most successful credit interventions account for seasonal distribution of farmer income

• Harvest time storage loans• Incentives to prepay for inputs• Credit with repayment deferred until harvest

Flexible Collateral Arrangements

1. Asset collateralized lending

Flexible collateral arrangements

• Researchers evaluate alternative credit contracts to facilitate purchase of new agricultural technology

• Population: Kenyan smallholding dairy farmers• Problem: Insufficient water supply; under-watering cows

affects milk productivity• Asset: 5,000 liter rainwater harvesting tank

• The technology is expensive!• Use to smooth water consumption through the dry seasons (also

used for providing livestock water) • Cost: 24,000 KSh = $320 ~ 20% of HH consumption

Unsurprisingly, very low adoption ratesDe Laat, Joost, William Jack, Michael Kremer and Tavneet Suri. 2014. “Encouraging adoption of rainwater harvesting tanks through collateralized loans in Kenya.” Working paper.

The players

• Dairy cooperative:• Receives milk delivered by farmers

every day• Tests, cools, stores, and transports milk

to processing plant• Pays farmers• Potentially facilitates debt collection

• Savings and Credit Cooperative (SACCO):• Holds savings of members (and some

non members)• Makes loans to members for livestock

services as well as non-farm needs• Requires 100% cash collateralization

De Laat et al., 2014

Testing innovative credit contracts

i. 100% cash collateralized joint-liability loan• Borrowers required to make deposit equivalent to 1/3 loan value • Three guarantors required to insure 2/3 loan value through savings with

cooperative• Contract resembled standard loan contract typically used by the cooperative

ii. 4% deposit, asset collateralized loan • Small (Ksh 1,000) deposit required at signing (4% of loan value)

iii. 25% deposit, asset collateralized loan • Larger (Ksh 6,000) deposit required at signing (25% of loan value)

iv. 25% guarantor, asset collateralized loan • Small (Ksh 1,000) deposit required at signing (4% of loan value) • Single guarantor required to pledge Ksh 5,000 (21% of loan value)

Critical to design: Repayments automatically deducted from monthly milk sales at the cooperativeDe Laat et al., 2014

Loan offer take up (%)

01020304050

2.4

44.3

27.6 23.5

Perc

en

t of

Hou

seh

old

s

De Laat et al., 2014

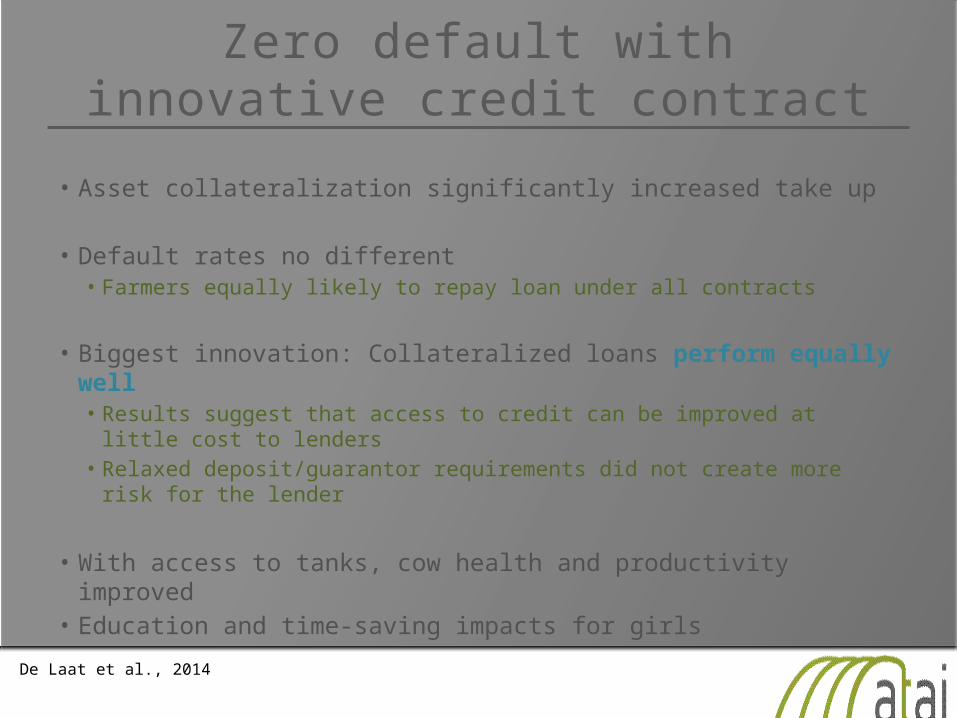

Zero default with innovative credit contract

• Asset collateralization significantly increased take up

• Default rates no different• Farmers equally likely to repay loan under all contracts

• Biggest innovation: Collateralized loans perform equally well• Results suggest that access to credit can be improved at little

cost to lenders• Relaxed deposit/guarantor requirements did not create more risk

for the lender

• With access to tanks, cow health and productivity improved• Education and time-saving impacts for girls

De Laat et al., 2014

Policy lessons

• Many people who want to borrow prevented from doing so by heavy deposit or guarantor requirements • Farmers vastly preferred asset collateralization to joint-liability ⇒

asset collateralization means banks could extend many more loans

• Extending more loans didn’t create more risk for lender• Automatic repayment structure facilitated simplified repayments

(farmers don’t need to figure out where to get cash to repay their loans)

• Asset collateralization successful in this context: could it work more broadly? • Must be careful of the asset – can’t be small, movable or easy to hide• Tanks large visible asset, difficult to hide• Farmers valued the benefit of the tank, keen to not have the tank

repossessedDe Laat et al., 2014

Harvest Time Credit Schedules

1. Harvest time storage loans 2. Incentives to prepay for inputs

3. Credit with deferred repayment

Accounting for seasonal distribution of farming income

• Large and regular seasonal fluctuations in grain prices• Increases of 50-100% between post-harvest lows and pre-

harvest peaks are common

• Farmers face difficulty using storage to save grain for sale at times of high prices• Due in part to limited borrowing opportunities

• Farmers often sell grain at post-harvest low prices to meet urgent cash needs

• To meet consumption needs later in the year, farmers may end up buying back grain a few months after selling it Maize market functions as high-interest lender of last resort

Burke, Marshall. 2014. “Selling low and buying high: An arbitrage puzzle in Kenyan villages.”Working paper, March 20, 2014.

Monthly average maize prices (1994-2001)

Burke, 2014

Buy low and sell high?

Fact 1: Maize prices double over seasonal price fluctuations

Fact 2: Farmers have ability to store maize for sale at later date

So store maize and sell when prices rise later in year? Find the opposite:

Farmers sell low and buy high!

Q: Why do you sell at harvest instead of later, when prices are higher?

A: I need the cashBurke, 2014

With OAF, offered a storage loan

• In partnership with agricultural microfinance NGO, One Acre Fund

• Researchers offered cash loan (~$100) at harvest time to randomly selected OAF smallholder maize farmers

• Treatment 1: Loan given at harvest • Treatment 2: Loan given 3 months after harvest

• Stored maize as collateral• 10% interest, repay flexibly

• Take up was very high: >70%Burke, 2014

Overall price rise was exceptionally small in this year

Burke, 2014

Results at the farmer level

Burke, 2014

Results at the farmer level

Burke, 2014

Results at the farmer level

• Even with low price rise: 20% return on investment after loan repayment for farmers offered the loan at harvest

Burke, 2014

Policy lessons

• Access to well-timed credit can help improve the profitability of small farmers

• Absence of credit markets spills over into other markets that matter for the poor• Missing credit market exacerbate seasonal price swings

• When is this type of loan relevant?• Markets with high seasonal price fluctuations• Crops with storage potential

Burke, 2014

Timing is crucial for adoption

• Low adoption of profitable farming inputs such as fertilizer

• Policy response in many countries ⇒ heavy fertilizer subsidies

Even with subsidies, fertilizer is expensive and adoption is low.

Unaffordability is only part of the problem:• Timing for input purchase• Universal tendency of procrastination may also be important

Duflo, Esther, Michael Kremer, and Jonathan Robinson. 2011. “Nudging Farmers to Use Fertilizer: Theory and Experimental Evidence from Kenya.” American Economic Review.

Nudging farmers to prepay for inputs

• Researchers evaluate whether small, time-limited incentives for advanced fertilizer purchase can increase adoption?

Intervention: • Farmers visited directly after harvest time and

offered chance to prepay for fertilizer voucher• Fertilizer offered at full price, but included small

incentive of free delivery • Compared to 50% discount on fertilizer offered at

application time

Duflo et al. 2011

Prepayment increased fertilizer adoption

• Offering option to purchase full-price fertilizer at harvest time led to the same take-up as offering a 50% discount on the fertilizer at planting time

Duflo et al. 2011

Policy lessons

• Can be implemented as a small subsidy for early purchase

• Small commitment devices can nudge people to overcome savings problems and procrastination• Commitment savings devices have also been highly

successful at increasing investment in agricultural technologies

• A small “nudge” at the appropriate time was as powerful as a heavy subsidy—and may be a better policy

Duflo et al. 2011

Credit with deferred repayment

• Several studies find that offering loans with repayment delayed until harvest can increase technology adoption • In Mali – input use increased and rice

output increased by 31%• In Uganda – similar impacts on maize

production

TOMOYA MATSUMOTO, TAKASHI YAMANO, AND DICK SSERUNKUUMA. “Technology Adoption and Dissemination in Agriculture: Evidence from Sequential Intervention in Maize Production in Uganda”

Lori Beaman, Dean Karlan, Bram Thuysbaert, and Christopher Udry. 2013. “Profitability of Fertilizer: Experimental Evidence from Female Rice Farmers in Mali” American Economic Review

Improved Information About Borrowers

1. Fingerprinting to reduce risky borrowing

Improved information about borrowers

• Addressing other sources of risk for lender: Positive identification of borrowers• Lenders use “dynamic incentives” to elicit timely repayment and

lower lending costs• Without dynamic incentives, lenders may limit supply of credit

• Biometric technology: methods for identifying people based on unique physical or behavioral traits • Unique to each person - cannot be lost, forgotten or stolen

• Fingerprinting can make the idea of future credit denial more than a threat. Financial institutions can: • Withhold new loans from past defaulters • Reward responsible past borrowers with increased credit• Store borrower repayment behavior year to year (credit bureaus)

Gine, Xavier, Jessica Goldberg, and Dean Yang. 2012. "Credit Market Consequences of Improved Personal Identification: Field Experimental Evidence from Malawi." American Economic Review

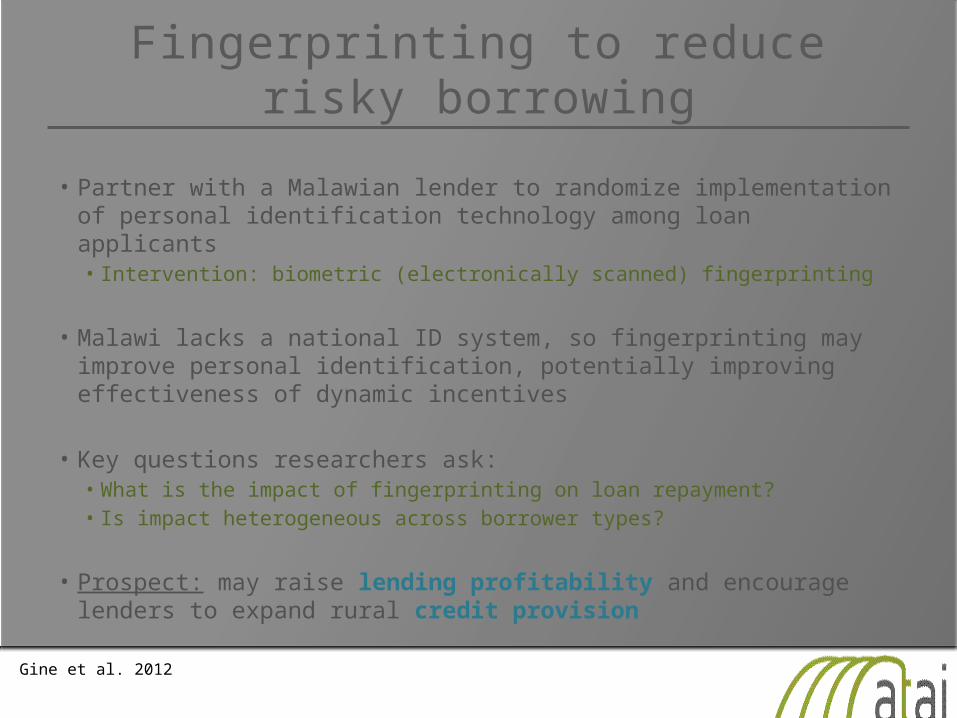

Fingerprinting to reduce risky borrowing

• Partner with a Malawian lender to randomize implementation of personal identification technology among loan applicants • Intervention: biometric (electronically scanned) fingerprinting

• Malawi lacks a national ID system, so fingerprinting may improve personal identification, potentially improving effectiveness of dynamic incentives

• Key questions researchers ask: • What is the impact of fingerprinting on loan repayment? • Is impact heterogeneous across borrower types?

• Prospect: may raise lending profitability and encourage lenders to expand rural credit provision

Gine et al. 2012

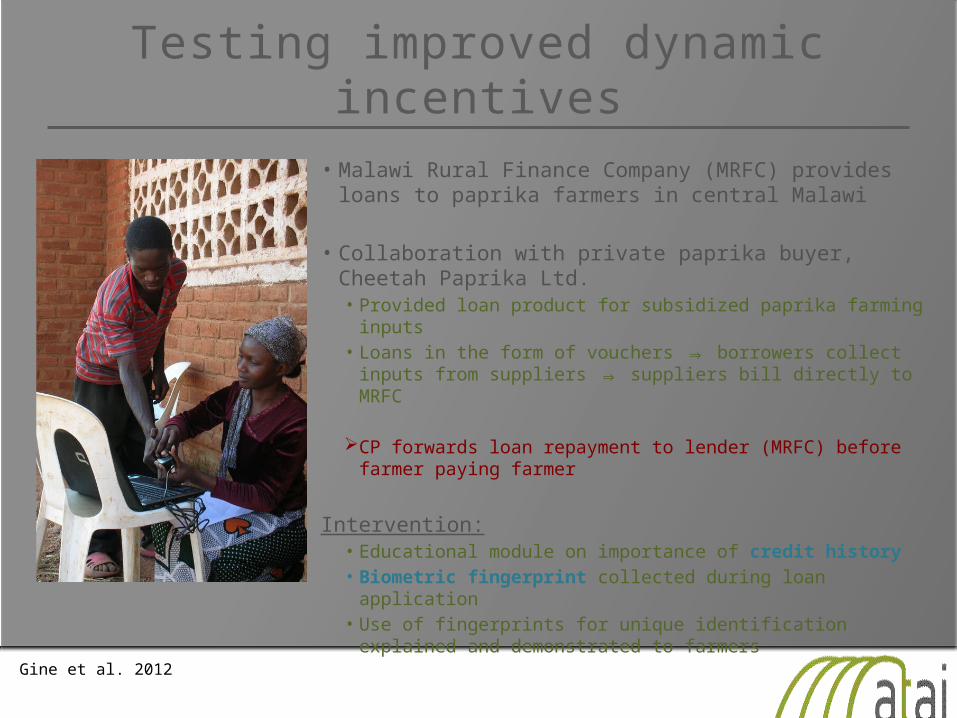

Testing improved dynamic incentives

• Malawi Rural Finance Company (MRFC) provides loans to paprika farmers in central Malawi

• Collaboration with private paprika buyer, Cheetah Paprika Ltd.

• Provided loan product for subsidized paprika farming inputs

• Loans in the form of vouchers ⇒ borrowers collect inputs from suppliers ⇒ suppliers bill directly to MRFC

CP forwards loan repayment to lender (MRFC) before

farmer paying farmer

Intervention:• Educational module on importance of credit history • Biometric fingerprint collected during loan

application • Use of fingerprints for unique identification explained

and demonstrated to farmersGine et al. 2012

Results: Loan repayment behavior

Gine et al. 2012

• Fingerprinting improved loan repayment, particularly for riskiest borrowers

• Fingerprinting allows the lender to more effectively use dynamic repayment incentives: • Withholding future loans from past defaulters • Rewarding good borrowers with better loan conditions

• Personal identification improved repayment rates, particularly for riskiest borrowers

• Borrowers not deterred from seeking credit, rather • Risky borrowers took out smaller loans• Less fertilizer diverted away from paprika crop

Policy lessons

Gine et al. 2012

Policy lessons

• Using biometric technology to identify borrowers had a high rate of return for the lender• Benefit‐cost ratio is 2.27• $3.36 benefit vs. $1.48 cost per individual

fingerprinted

• Improved identification may address one barrier to providing credit in rural areas

• Borrower responses to personal identification systems offer lessons for establishing credit bureaus

Gine et al. 2012

Conclusions & recap

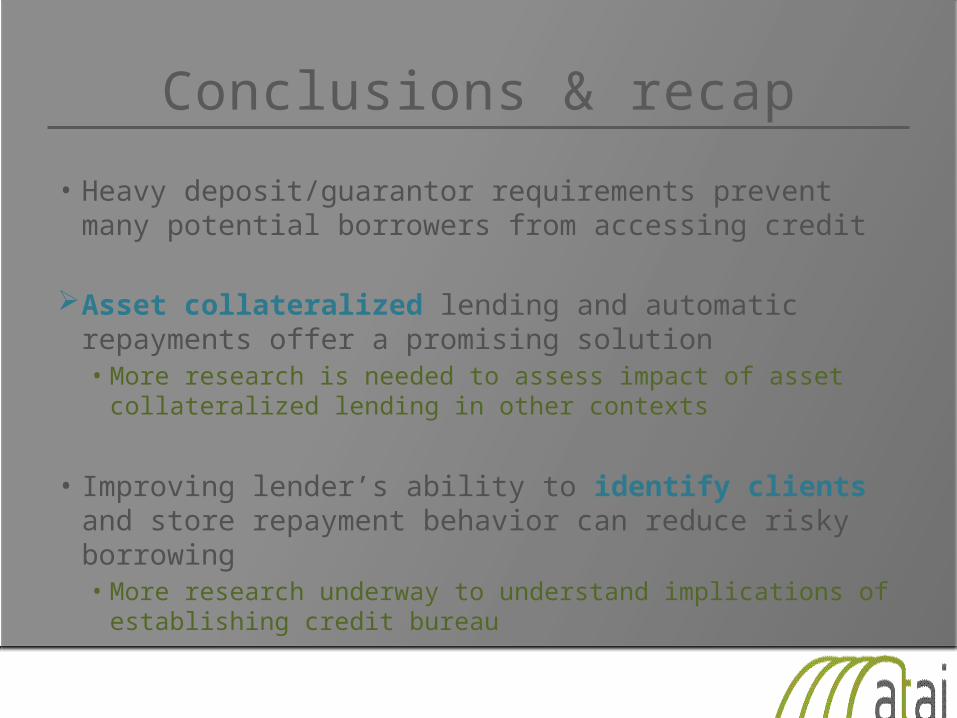

• Heavy deposit/guarantor requirements prevent many potential borrowers from accessing credit

Asset collateralized lending and automatic repayments offer a promising solution• More research is needed to assess impact of asset

collateralized lending in other contexts

• Improving lender’s ability to identify clients and store repayment behavior can reduce risky borrowing• More research underway to understand implications of

establishing credit bureau

Conclusions & recap

• Harvest-time credit allowed farmers to buy maize at low prices and sell stored maize at high prices later, increasing profits

• Evidence suggests that policies that help farmers commit to save or prepay for inputs can increase investment in technology

• Credit products with payment deferred until harvest can increase use of inputs

Resources atai-research.org

cega.berkeley.edu

povertyactionlab.org

Accounting for seasonal distribution of farmer

income

Monthly average maize prices (1994-2001)