Innovation inspired by future scenarios, collaboration and metrics.

1

GN Store Nord Investor Presentation March 2022

2

Safe Harbor Statement

The forward-looking statements in this report reflect the management's current expectations of certain future events and

financial results. Statements regarding the future are, naturally, subject to risks and uncertainties, which may result in

considerable deviations from the outlook set forth. Furthermore, some of these expectations are based on assumptions

regarding future events, which may prove incorrect.

Factors that may cause actual results to deviate materially from expectations include – but are not limited to – general

economic developments and developments in the financial markets, technological developments, changes and

amendments to legislation and regulations governing GN’s markets, changes in the demand for GN's products,

competition, fluctuations in sub-contractor supplies and developments in ongoing litigation (including but not limited to class

action and patent infringement litigation in the United States).

This presentation should not be considered an offer to sell or buy securities in GN Store Nord.

3

Agenda

GN at a glance

GN Hearing

GN Audio

Financials

GN’s investment case

Clear strategy underpinned by deep technology expertise and

strategic global partnerships

Strong cash conversion and asset light business model

Focused growth model, dedicated developer, manufacturer and

distributor, refraining from vertical integration

Profitability in line with or better than peers

Focused innovation within sound and video processing in selected market

segments

Leading positions in attractive markets with high entry barriers

4

Revenue & organic growth

(DKK million & %)GN Hearing GN Audio

GN at a glance

Global leader in intelligent audio solutions Global reach, local presence

• Founded in 1869 and listed on Nasdaq Copenhagen

• Technology-driven company primarily developing and manufacturing

hearing aids (GN Hearing) and headsets, speakers and video (GN Audio)

• Innovation leader with expertise in the human ear, sound and wireless

technology under one roof

• Unique portfolio of medical, professional and consumer audio solutions and

deep R&D expertise (total R&D spend of DKK 1.4 billion per year)

• Strong track record of strategic partnerships with leading channels,

customers and adjacent industry technology leaders

• Access to attractive and growing gaming gear market through the

acquisition of SteelSeries

Financial summaryBusiness areas and brands

EBITA & EBITA margin

(DKK million & %)

Countries with GN offices

Countries with GN distributors

FCF & cash conversion*

(DKK million & %)

*FCF: Free cash-flow excluding M&A, cash conversion: FCF / EBITA

10,607

12,57413,449

15,775

2021

13%

20%

2018

15%

2019

9%

2020

1,956

2,321

1,866

2,619

2020

18.4%

2018

16.6%

2021

18.5%

2019

13.9%

1,110

1,296

1,865

-100

-50

0

50

100

150

200

57%

20192018 2021

56%

27%

2020

100%

702

5

GN builds on innovation and ecosystem leadership

6

20031st to introduce an

open mini BTE

20141st Made-for-

iPhone

hearing aids

20121st to introduce

2.4 GHz e2e

technology

20201st to introduce All

Access Directionality

& M&RIE

20081st to introduce

Asymmetric

directionality

Definitions: DSP: Digital Signal Processing; e2e: Ear to Ear

20001st Bluetooth®

headset

20041st digital amplifier

with DSP

20141st wireless earbuds

with built-in heart rate

monitor

20131st BT Stereo

headphones with

Dolby

1st smart panoramic -

4k-pixel plug-and-play

video solution

20111st Bluetooth

headset with ANC

1st all-in-one

hearable,

Jabra Enhance Plus

In 2021 the R&D spend was DKK 1.4 bn, corresponding to an R&D to revenue ratio of 9%

20181st company to introduce direct

streaming from Android devices

using Bluetooth Low Energy

2015Smart Hearing

Alliance with

Cochlear

20171st headset officially meeting

Open Office Microsoft

Skype for Business

requirements

2.4 GHz

GN’s engineering capabilities in hardware and software for audio and video deliver unique and individualzied customer experiences.

To enhance our impact, we partner with leading channels, ecosystems, scientists, and other industry leaders to leverage technology

and market acess

7

Agenda

GN at a glance

GN Hearing

GN Audio

Financials

8

GN Hearing at a glance

Brands, products and partnerships

Financial Performance

Revenue & organic growth

(DKK million & %)

EBITA & EBITA margin

(DKK million & %)

FCF & cash conversion1

(DKK million & %)

Note 1: FCF: Free cash-flow excluding M&A, cash conversion: FCF / EBITA

Strategic Focus

Individualized customer experience: We will obsess about

customer experience for users of hearing aids and business support

for hearing care professionals

Innovation leadership: We will continue to lead in innovation – in

individualized hearing experience, in overall user experience, in

connectivity, and in customer care

Commercial & ecosystem excellence: We will build more and

stronger relationships with hearing care professionals and

ecosystem partners

5,8336,351

4,7255,332

7%

2020

-24%

7%

20192018 2021

16%

1,1941,284

41

643

2018 2020

21%

1%

20%

2019 2021

12%

574

672

127

198

310%

48%

20192018 2020

52%

2021

31%

Living with untreated hearing loss increases the risk of health problems

9

• The incidence of dementia is greater in people with hearing loss1, and early studies show that wearing hearing aids may have a postive effect on cognitive function2

• People with mild hearing loss were nearly three times more likely to have a history of falling than those with no hearing loss3. One study shows that wearing hearing aids may improve balance4

• Wearing hearing aids reduce the risk of depression5

• Untreated hearing loss reduces quality of life6

References: 1 Lin FR, Metter EJ, O'Brien RJ, Resnick SM, Zonderman A, Ferrucci L. Hearing loss and incident dementia. Arch Neurol. 2011 Feb;68(2):214-202 Lancet Commission on Dementia Prevention: Intervention and Care Reference, August 2019 3 Lin F. & Ferrucci, L. (2012) Hearing Loss and Falls Among Older People in the United States. Arch Intern Med. 2012;172(4):369-3714 Hullar, T: The effect of hearing aids on postural stability. Laryngoscope, 2014.5 Hearing Industries Association: MT10:MarkeTrak, March 27, 20196 Kochkin, S. MarkeTrak VIII: Patients report improved quality of life with hearing aid usage, Hearing Journal, Vol. 64 (6), June 2011.

0301

02 04

10

Multiple attractive megatrends driving market growth~4-6% expected unit CAGR in coming years1

Room for penetration growth High barriers to entry to the market

Penetration still low,

especially for less

severe hearing loss

• 65+ population expected to grow significantly in the years to come

• Baby boomers generation reaching retirement age

• Increasing noise pollution drives prevalence of hearing loss

• Increasing wealth among larger middle class

1) ASP decline of 1-2%. Based on company estimates, industry association EHIMA 2) World bank

Profound

Severe

Moderately severe

Moderate

Mild

Source: MarkeTrak, EuroTrak, GN estimates

Global hearing aids market growth1

(unit growth)

GDP growth (annual %)2 0% GDP growth

The hearing aid market remains very attractive and robust in the mid to long term

’02 ’08’05’03 ’07’04 ’06 ’09 ’17’10 ’11 ’12 ’13 ’14 ’15 ’16 ’18 ’19 ’20 ’21 ’22E

~4-6%

Degree of penetration

• Users of hearing aids tend to

choose hearing aids based

on inputs from their hearing

care professional

• Sticky distribution as hearing

care professionals tend to

partner with same

manufactures

• 75+ years of knowhow in the

hearing aid space

• Significant investments

required into R&D

• Extensive intellectual

property rights in the hearing

aid space

• FDA regulations (Medical

Class II devices)

• Increasing requirements

from the EU Medical Device

Regulation

• Extensive investments

needed into quality

management systems

DistributionTechnologyRegulations

Key trends and drivers

impacting

GN Hearing’s business

Over the past few years, we have seen an acceleration of existing

trends as well as an emergence of new ones. The trends GN Hearing

continue to benefit from are:

11

GN Hearing strategy update

Individualized

customer experience

Innovation leadership

Commercial &

ecosystem excellence

To realize our ambition, GN Hearing will continue building on the strong existing foundation of

the business and retain the three strategic pillars laid out in the ‘2020 and beyond’ strategy:

Digitalization and data

Regulatory shifts

expanding the market

Changing competitive

landscape

ConsumerizationAging populations with

low adoption rates

Sustainability drives design

and manufacturing decisons

Digitize and simplify the way we work

Core business

12

GN Hearing strategy update

➢ Modernize hearing care by building new ways of connecting hearing care professionals, consumers and partners

➢ Digitize, simplify and automate the supply chain

➢ Simplify the way we work and reduce complexity

➢ Accelerate through M&A and partnerships

• Participate in new channels and hearing solution adjacencies

• Build on the combined competencies of GN to reach new customer groups

with lifestyle hearing products including Jabra Enhance Plus

• Deliver customer-centric products and experiences with organic

hearing including multiple new product launches in 2022

• Be a trusted and innovative partner for our hearing care

professionals in key markets

Emerging business

Simplify to growUnlocking the potential of the hearing solutions market

Current focus areas

Making hearing sound natural, feel natural and enabling people to connect naturally

again through Organic Hearing

ReSound ONE

Advanced

Essential

Premium

ReSound LiNX Quattro ReSound ENZO Q ReSound Key

ReSound

SmartFit

ReSound

Assist

ReSound

Assist Live

ReSound Smart 3D

iOS and AndroidTM

5 models

10 models 2 models

10 models

Announced August 2018 Announced February 2020RIEs announced August 2020, BTEs announced February 2022 Announced February 2021

Wireless

Accessories

13

Worldwide: 80% of people with a hearing loss currently live without hearing aids

14

Do not want a traditional hearing aid

Interested in tech but want an

easy solution

Source: MarkeTrak, EuroTrak, GN estimates

Recognized hearing difficulty

Want a consumerized

approach

All in One

Penetrated20%

Not penetrated80%

Penetration of hearing aids What are the 80% non-users looking for?

• Lifestyle consumer proposition

• All-in-one solution; hearing enhancement, great call and music quality

• Small, discreet and stylish design – 50% smaller than Jabra Elite 75t

• 10 hours battery life on a single charge and 30 hours included

with charging case

• Available exclusively through licensed HCP’s

Building on years of research, innovation and

engineering GN introduces Jabra Enhance Plus

15

Lively 2021 financial highlights

The acquisition of Lively - new business opportunities emerging

16

Lively - a leader in online hearing care

• Leader in online hearing care and digital marketing platform,

enabling consumers to receive hearing care from licensed hearing

care professionals in the U.S. all from the comfort of their home

• Online market is estimated to account for ~4% of the U.S.

hearing care market and is expected to continue to grow at a

much faster pace than other segments

• Customers are almost ten years younger than users seen in

hearing care clinics providing the opportunity to expand the market

• Significant lead generation opportunity for GN’s Beltone and

ReSound partners as the unserved two-thirds of Lively’s consumer

inquiries now can be helped

EBITA (DKK)

-171m

Revenue (DKK)

114m+143% organic growth

16

17

The most focused hearing instruments manufacturer in the world

Cochlear implants

Hearing instruments

(Retail)

Bone anchored hearing systems

Hearing diagnostics

Hearing instruments

(Wholesale)

Size (market value)

5% Profitability 30%

0%

G

row

th 1

5%

• Five main manufacturers

of hearing instruments

• Competing for market

access

Profit pool (margin)

(20-25%)

• Consolidated market

with two main

component suppliers

(Sonion and Knowles)

Profit pool (margin)

(20-30%)

• Top buying groups

include Audigy, Elite,

and AHAA

• Many distributors across

the world – highly

fragmented

Profit pool (margin)

(10-15%)

• Traditional hearing

instrument dispensers,

ENTs and online

retailers

• Largest retail player is

Amplifon, but

manufacturers are

catching-up

Profit pool (margin)

(5-15%)

USD

~5bn

Focus on core capabilities within hearing instruments… …and strategic partnerships in the distribution channel

Wholesale

hearing instruments

USD

~5bn

Component

manufacturersManufacturers

Distributors /

buying groups Retailers

• Maintain high margins

• Ensure channel access

Competitors

• Retail networks add complexity, limits agility and are investment/cost heavy

• Verticals (Implants) divert attention (few synergies)

GN refrains from

vertical integration

18

GN uniquely positioned for future growth with its distribution approach

Focus on

independent retail

markets

▪ +85% of the global market is not locked by hearing aid manufacturers

▪ GN has significant room to grow its global market share

Note: Selected countries with indication of unit share of market not locked by manufacturers (GN Hearing estimates)

The vast majority of the retail market is not locked by manufacturers

65-75% >75%

Innovation

excellenceStrategic

partnerships

Efficient use

of capital

Focus on

core

competencies

No

competition

with

customers

Strategic

agility

Driving growth through strategic collaboration

Partnering up with

tech giants

Exposure to fast-growing

cochlear market

19

Refraining from

vertical integration

20

Agenda

GN at a glance

GN Hearing

GN Audio

Financials

21

GN Audio at a glance

Brands and products

Revenue & organic growth

(DKK million & %)

Adj. EBITA & Adj. EBITA Margin

(DKK million & %)

FCF & cash conversion1

(DKK million & %)

Strategic Focus

Individualized customer experience: We will offer customers

best-in-class experiences as we transform from strict product focus

to a more segment- and experience driven approach

Ecosystem-led innovation: We will lead in innovation and develop

world-class and highly relevant audio and video products and

solutions together with leading ecosystem partners

Sustainable commercial & operational excellence: We will excel

in go-to-market execution in enterprise, retail and online channels

and support our high growth with agile, sustainable and scalable

operations

4,774

6,223

8,724

10,443

26%21%

2018 2019 2020

42%

22%

2021

905

1,244

1,888

2,209

2018

20%19%

20202019

22%

2021

21%

798 849

1,729

1,288

86%

20202018

88%

2019

71%

2021

60%

Note 1: FCF: Free cash-flow excluding M&A, cash conversion: FCF / EBITA

Financial Performance

22

Strong demand and estimated market growth across business segments

Target users Market characteristics Market share Market size (USD) Market growth

OfficeOffice-based

knowledge workers

From desk-phone telephony in private

offices to UC&C in open offices

~2.1bn ~10%

Contact center “Calls for a living“From desk-phones using on-premise

infrastructure to laptop-based cloud calling

Collaboration Plug-and-play collaborationFrom built-in legacy equipment to UC&C-

enabled plug-and-play solutions ~2.5bn ~20%

ConsumerPreference for great calls,

music and an active lifestyle

From corded headbands to True Wireless

as the preferred form factor ~24bn ~10%

GamingPremium software-enabled

gaming gear

Growing base of gamers and low

penetration of purpose-built gaming gear ~5.5bn ~7-8%

Hearing protectionTactical hearing protection for

defense and security

Hearing protection systems is a growing

political need ~0.6bn ~10%

Sources: MarkeTrak, EuroTrak, GN estimates, NewZoo, The NPD Group Inc.

23

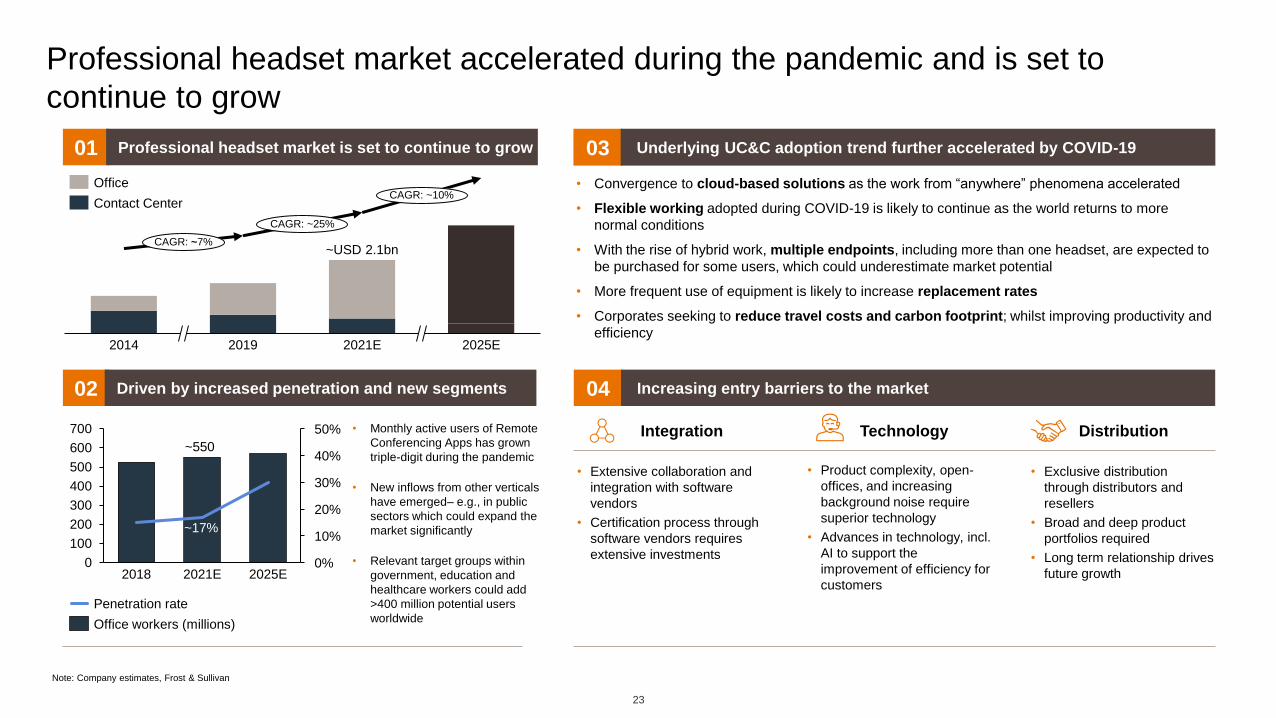

Professional headset market accelerated during the pandemic and is set to

continue to grow

0301

02 04

• Exclusive distribution

through distributors and

resellers

• Broad and deep product

portfolios required

• Long term relationship drives

future growth

• Product complexity, open-

offices, and increasing

background noise require

superior technology

• Advances in technology, incl.

AI to support the

improvement of efficiency for

customers

Underlying UC&C adoption trend further accelerated by COVID-19Professional headset market is set to continue to grow

Driven by increased penetration and new segments Increasing entry barriers to the market

• Extensive collaboration and

integration with software

vendors

• Certification process through

software vendors requires

extensive investments

DistributionTechnologyIntegration• Monthly active users of Remote

Conferencing Apps has grown

triple-digit during the pandemic

• New inflows from other verticals

have emerged– e.g., in public

sectors which could expand the

market significantly

• Relevant target groups within

government, education and

healthcare workers could add

>400 million potential users

worldwide

Note: Company estimates, Frost & Sullivan

2014 2019 2021E 2025E

~USD 2.1bnCAGR: ~7%

CAGR: ~25%

CAGR: ~10%

0

100

200

300

400

500

600

700

20%

0%

10%

50%

30%

40%

2018 2021E 2025E

Penetration rate

Office workers (millions)

~17%

~550

Office

Contact Center

• Convergence to cloud-based solutions as the work from “anywhere” phenomena accelerated

• Flexible working adopted during COVID-19 is likely to continue as the world returns to more

normal conditions

• With the rise of hybrid work, multiple endpoints, including more than one headset, are expected to

be purchased for some users, which could underestimate market potential

• More frequent use of equipment is likely to increase replacement rates

• Corporates seeking to reduce travel costs and carbon footprint; whilst improving productivity and

efficiency

24

UC platform growth has significantly outpaced the professional headset market

“Teams usage has never been higher. We have nearly 250

million monthly active users as people use Teams each day to

communicate, collaborate, and co-author content across work,

life, and learning”

- Satya Nadella, Chairman and CEO of Microsoft. July 27, 2021

6x Up ~6x in daily

active users

30x Up ~30x in daily

active participants

“In a recent survey we conducted, 80% of US respondents

agreed that all interactions will continue to have a virtual

element post-pandemic, and that figure was even higher in

many of the other markets we surveyed”

- Eric Yuan, President and CEO of Zoom. June 1, 2021

Unified communication platforms have experienced massive growth* Professional headset market accelerated during the pandemic

Office workers

~550 million

Government

workers~150 million

Established segment

New opportunities: Public sector

With ~17% penetration

Low penetration

* In 2020 accelerated by COVID-19

Source: Public Information, Frost & Sullivan and GN estimates

Education and

healthcare personas~260 million

Low penetration

25

GN Audio strategy update

UC moves beyond office

Gaming goes mainstream

Products and channels

become more consumerized

Audio, video and data

replaces audio-only

Work-life becomes hybrid

Sustainability drives design

and manufacturing decisons

Key trends and drivers

impacting GN Audio’s business

Over the past few years, we have seen an acceleration of existing

trends as well as an emergence of new ones. The trends GN Audio

continue to benefit from are:

Individualized

customer experience

Ecosystem led innovation

Sustainable commercial &

operational excellence

To realize our ambition, GN Audio will continue building on the strong existing foundation of

the business and retain the three strategic pillars laid out in the ‘2020 and beyond’ strategy:

GN Audio strategy update

Simplify to grow

Industry solutions*

Enable through M&A

*) Targeting more than two billion "deskless workers" (teachers, doctors, retail staff, logistics personnel, first responders, and many other key roles)

ConsumerContact center

Take share in maturing market;

Explore adjacent opportunities Win high-growth markets

Office Collaboration Gaming

Simplify the way we work

➢ Transforming from an audio-only business to an audio, video, and gaming business

➢ Prioritize resources in Office, Collaboration, and Gaming while taking share in Consumer and Contact Center

➢ Broaden the scope of the Office business unit beyond office headsets

➢ Accelerate through M&A and drive simpler ways of working

Continue to take market share

by expanding propositions and

delivering innovative products

to every professional

Scale existing business and

continue portfolio expansionLead the market for premium

and software-led gaming

peripherals

Convert installed base and

gain market share with

digital solutions

Continue growth of the true

wireless portfolio

Expand propositions

towards non-office workers

Current focus areas

26

27

New ways of working calls for superior technology

In the office Jabra Evolve2 85

• Background noise

• Different UC platforms

• Interruptions

• Need for collaboration

• Busy environment

Working from home

“On the go”

• Plug into a new set-up

• Background noise from kids,

dog, etc.

• Limited privacy

• Concentration issues

• More than one device Intelligent 10-microphone

technology and new improved signal

processing algorithms delivering

outstanding call performance,

everywhere

Bigger speakers: Powerful leak-

tolerant 40mm. Factor in advanced

digital chipset and the latest AAC

codec driving superior sound quality

for both calls and music

Busylight visible from any direction.

Red light automatically activated

when in call or in a meeting

Discrete hidden boom arm:

Retractable boom arm allows for a

more casual look without

compromising on call quality

Noise isolating design and ANC:

Enhanced noise isolating design and

powerful digital hybrid ANC

Soft memory headband: New ergonomic

headband designed from hundred of head

scans, for comfortable all-day wear

Superior

battery: Up to

37 hours

battery life - 8

hours of

battery life

charged in 15

minutes

• No charging options

• Background noise

• Changing environments

• Move from office to “on the go”

• Preference for music listening

and smarter design

Use case:

Use case:

Use case:

Panacast 50

Panacast 20

• The world’s first new-normal-ready intelligent video bar

• Three 13-megapixel cameras mounted in a high-precision multi-camera

array creating an immersive 180° field of view covering the full room

• Architecture enables the intelligent video bar to carry out real-time

integration of audio, video and data allowing for Intelligent Zoom feature

• Safety Capacity, Room Usage and People Count generating anonymous

room occupancy data

• Plug-and-play solution with an advanced security layer integrating up

against all leading UC vendors

28

Intelligent camera line up for insight driven collaboration in the hybrid working spaceIntroducing Jabra PanaCast 50 & 20

• Jabra’s first intelligent personal camera

• 4K Ultra HD Video as well as personalized Intelligent Zoom and

automatic lighting correction

• Built-in presentation features like the new Picture-in-Picture mode

• All the experiences are powered on the device itself, significantly

minimizing the risk of security breaches,

maximizing speed, accuracy, and quality

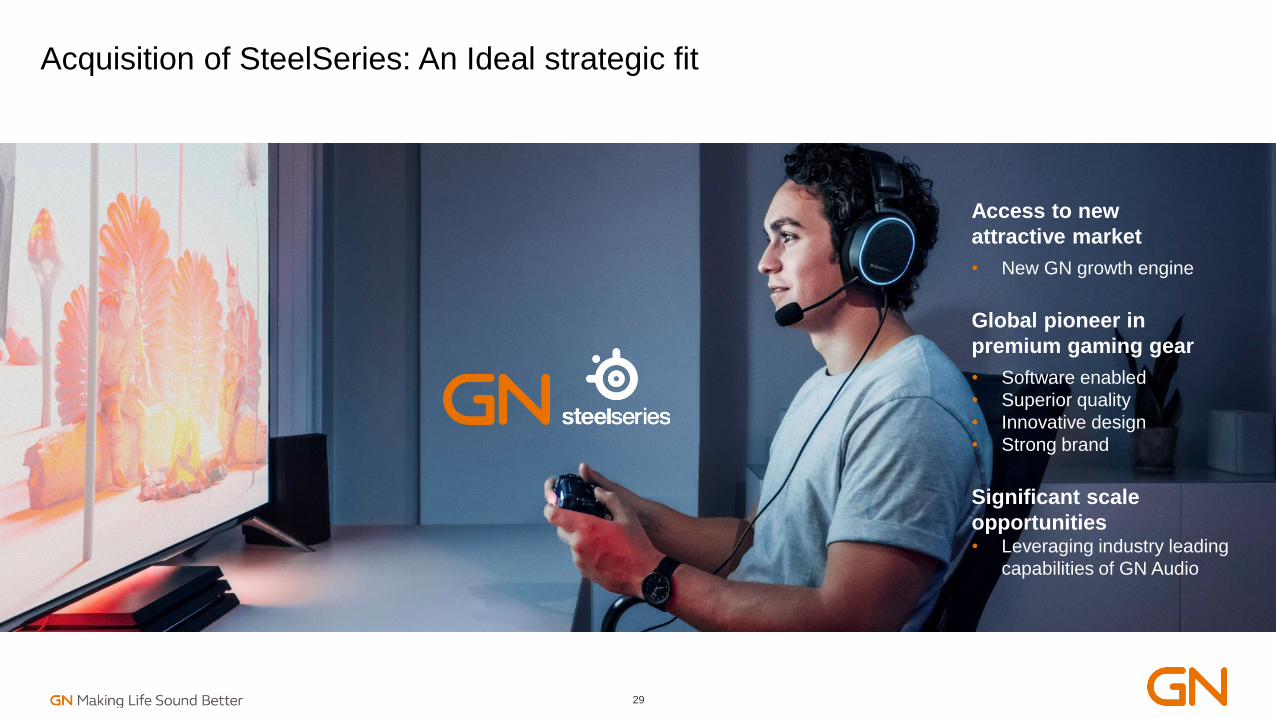

Acquisition of SteelSeries: An Ideal strategic fit

29

Global pioneer in

premium gaming gear

• Software enabled

• Superior quality

• Innovative design

• Strong brand

Significant scale

opportunities• Leveraging industry leading

capabilities of GN Audio

Access to new

attractive market

• New GN growth engine

30

SteelSeries continued their growth journey in 2021Transaction closed January 12, 2022

SteelSeries 2021 performance Synergies and costs

(Revenue, DKK million)

Growth engine and Integration Strategy

• SteelSeries added as a new growth engine to GN and will function as a business unit within GN Audio. Integration will focus on supply chain

Synergies

• Annual run-rate operational synergies of DKK ~150 million expected by end of 2022

Transaction costs

• Estimated to DKK ~ -150 million (with DKK -45 million already booked in 2021)

Integration costs

• Estimated to DKK ~ -100 million

Accounting impact

• PPA effect of DKK ~ -200 million in COGS primarily in Q1 2022, as well as yearly step-up amortizations of DKK ~ -250 million

731

970

1,244

2,020

2,697

0

1,000

2,000

3,000

2017 2018 2019 2020 2021

... and with an adj. EBITA margin of 13.6% in 2021

Evolve2 40 & PanaCast 20 Speak 710Evolve2 75 Evolve2 85 Elite 7 Pro Evolve 75e

Broad product portfolio, two-tier distribution model and long-term relationships

driving commercial excellence

Road warriorExecutive nomadFlexible hub workerRemote workerCorridor warriorDesk worker

HIGH MOBILITYLOW MOBILITY

Meeting room

PanaCast 3 & PanaCast 50

Broad and deep product portfolio required

31

Go-to-market strategy drives the commercial execution

Enterprise high-touch sales

Medium/ large enterprise

Small/ medium enterprise

GN Audio sales organization

Distribution sales

Distributors

B2B channel sales

Reseller

Reseller

Reseller

32

Driving scalability with very efficient outsourced supply chain setup

Outsourced but fully controlled process with GN driving sourcing

Component

suppliersRegional

distribution

centers

R&D and

product

development

In-house process

Contract

manufacturers

Dual sourcing strategy

throughout value chainScalability and agility

Unmatched distribution

networkKey strengths

North America

distributors and

customers

Europe

distributors and

customers

Rest of World

distributors and

customers

33

Agenda

GN at a glance

GN Hearing

GN Audio

Financials

GN - 10 years of relentless growth...

5.86.2

6.8

7.88.7

9.6

10.6

12.613.4

15.8

’12 ’13 ’19’14 ’16’15 ’18’17 ’20 ’21

CAGR: 12%

0.8

1.21.3

1.4

1.61.7

2.0

2.4

1.8

2.7

’14’12 ’13 ’15 ’17’16 ’18 ’19 ’20 ’21

CAGR: 14%

2.6

4.75.3

5.8

7.98.9

10.2

13.2

10.5

15.3

’18’14’12 ’19’16’13 ’15 ’17 ’20 ’21

CAGR: 22%

Revenue development (DKKbn) EBITA* development (DKKbn) Adj. EPS development (DKK)

* Excluding one-offs

R&D

~25%

M&A

~15%

35

Strict focus on capital allocation

• Organic Investments

• Synergistic M&A

• Annual Dividend

• Share Buy Back

GN capital allocation over the past 3 years

Share buy back

~40%

CAPEX

~10%

Dividend

~10%

Target leverage

1-2x

Creating shareholder value through efficient capital structure

36

Shareholder distribution• GN distributed DKK 1,354 million to shareholders in

2021 before pausing the share buyback program in

October 2021 following the acquisition of SteelSeries

• GN expects its financial leverage to increase short term as

a consequence of the SteelSeries and Lively acquisitions

• Due to the expected strong cash flow generation across

the business, it is expected that GN will quickly de-

leverage

• Long term leverage target of 1-2x NIBD/EBITDA is

confirmed, with de-leverage within a couple of years

• Annual General Meeting on March 9, 2022:

• GN will propose a dividend of DKK 1.55 per share in

respect of the fiscal year 2021, total DKK 214 million

• Proposal to cancel 982,604 treasury shares

Q4

2022

NIBD/

EBITDA

Capital

structure

policy

target

Expected development of leverage ratio

Q1

202220202017 2018 2019 Q4

2021Couple of years

1.0x

2.0x

0

500

1,000

1,500

2017

1,443

2019 20202018

1,1681,392

356

2021

1,354

Share buyback Dividends

Financial guidance 2022

37

Organic revenue

growth

Adjusted

EBITA margin4)Non-recurring items

(DKK million)5)

Growth in

adjusted EPS6)

GN Hearing

- Core business organic 5 - 10% ~14% ~ -150

- Emerging Business1) (DKK million) ~ -190

GN Audio2) 3) ~20% ~ -400

- GN Audio organic >5%

- SteelSeries >10%

Other (DKK million) ~ -190

GN Store Nord >10%

Note 1) Emerging Business mainly includes the Lively acquisition

Note 2) The SteelSeries organic revenue growth will be reported as M&A growth for GN Audio

Note 3) GN Audio and SteelSeries organic revenue growth constrained by the current global supply chain situation

Note 4) Excluding non-recurring items

Note 5) Non-recurring items in GN Hearing primarily related to supply chain investments (DKK ~ -150m) and in GN Audio related to transaction (DKK ~ -100m) and integration costs (DKK ~ -100m) as

well as non-cash PPAs (DKK ~ -200m), associated with SteelSeries

Note 6) Compared to 2021 adjusted EPS (excluding non-recurring items and amortization and impairment of acquired intangible assets) of DKK 15.29

Based on foreign exchange rates as of February 10, 2022

Full year 2022 guidance based on a challenging Q1 2022 and an assumption of a

strong H2 2022 performance across the business

38

The GN Hearing financial guidance is based on the following assumptions:

• Revenue in core hearing aid business: Q1 2022 organic revenue growth to be low-single digit. H2 2022 organic revenue

growth to be high-single digit following key product launches with extension of the ReSound ONE platform in H1 2022 and a

new platform launch in Q3 2022

• EBITA in core hearing aid business: Q1 2022 EBITA margin to be low-single digit (excluding non-recurring items) with a

gradual improvement in the three remaining quarters towards 20% by Q4 2022

• Non-recurring items: DKK ~ -150 million in EBITA investments primarily in the supply chain

The GN Audio financial guidance is based on the following assumptions:

• Revenue: Q1 2022 organic revenue growth of ~ -25% (in GN Audio organic and SteelSeries) due to supply chain constraints.

H2 2022 to return to double-digit growth rates as the supply situation is expected to ease

• EBITA: Q1 2022 EBITA margin to be in the mid-teens (excluding non-recurring items) with a gradual improvement in the three

remaining quarters resulting in an EBITA margin of ~20% for 2022 (excluding non-recurring items)

• Non-recurring items: Transaction related costs of DKK ~ -100 million and non-cash PPAs of DKK ~ -200 million following the

SteelSeries acquisition to be booked primarily in Q1 2022. Integration costs of DKK ~ -100 million

Based on foreign exchange rates as of February 10, 2022

Ambitious mid-term targets

1) In the mid-term, GN Hearing expects the global hearing aid market to continue to grow at ~4 - 6% in units with an ASP decline of ~1 - 2% annually

2) In the mid-term, GN Audio expects its markets to continue to grow at ~10% annually

Organic revenue growth EBITA margin Growth in EPS

GN Hearing(Excl. Emerging Business)

>market growth1 >20%

GN Audio(Incl. SteelSeries)

>market growth2 >20%

GN Store Nord >10% >10%

• Moreover, GN Store Nord expects to maintain a conservative capital structure policy of net interest-bearing debt to EBITDA of 1.0 - 2.0x, where

excess liquidity will be distributed to shareholders through share buybacks and dividends

39

41

➢ Climate neutral in company activities (scope 1+2)

➢ Halve the carbon footprint of company air travel

➢ Reduce our carbon footprint in our distribution and manufacturing

➢ Report to CDP and TCFD in our 2021 Sustainability | ESG Report

2025 Sustainability Goals

➢ 50% sustainable material in new products

➢ 100% sustainable packaging (minimal plastic, small size, FSC)

➢ Use sustainable product development requirements

➢ Expand take-back schemes to relevant products and regions

➢ Give more products a second life through repair or refurb

➢ Help 10 million+ people with hearing loss to Hear More, Do More and Be More

➢ Create awareness of hearing loss and break down stigmas

➢ New health functionalities in our products

➢ Support unmet hearing health needs through donations and capacity-building

Protecting our planet Truly sustainable products

and packaging

Improving health and

wellbeing

42

GN commits to Science Based Targets initiative

GN commits to Science Based Targets initiative to limit global warming to 1.5C and being net-zero by 2050

▪ Climate goals will be independently certified to be aligned with the scientific consensus

▪ GN joins the Business Ambition for 1.5 C coalition

▪ Required additional goals will be prepared in collaboration with the Science Based Target initiative

▪ Progress will be reported in the annual reports