Initiation: steering towards a better...

26

See important disclosures, including any required research certifications, beginning on page 25 Hong Kong Consumer Discretionary Investment case: Increased adoption to drive earnings growth. Nexteer is a leading global power steering provider that we think stands to benefit from the industry conversion to more fuel-efficient electric power steering from traditional energy-consuming hydraulic power steering (HPS). We forecast electric power steering penetration to rise to 74% by 2017 from 60% in 2014, driven by strengthening fuel efficiency standards across the globe. Nexteer should benefit, given that electric power steering occupies a big portion of its revenue mix and has higher margins than traditional HPS. Good earnings visibility. With the largest market share of 30%+ in the US, and supported by its well-established relationships with General Motors (GM), Fiat Chrysler Automobiles (FCA) and Ford, Nexteer enjoys steady earnings growth in the US. High technical entry barriers to the steering industry, the high cost to OEMs of changing steering suppliers during a model life cycle, and long lead times of 2-2.5 years for each model programme provide good earnings visibility for the company, in our view. Large exposure to China’s outperforming SUV market. Based on our observations, Nexteer aims to be one of the top-3 steering suppliers in China by 2020, from its current <5% market share and 20% revenue contribution in China. About 90% of its revenue in China is from SUVs, MPVs and minivans, the sub-segments whose sales volumes we estimate will significantly outperform the overall China PV market in 2016-17E. A large proportion of Nexteer’s products are for small size engines (<1.6L), which augurs well for the company given China’s recent reduction in the purchase tax from 10% to 5%. Catalysts: Nexteer’s ultimate controlling shareholder, AVIC, is a Chinese SOE engaged in (among other things) local steering industry. Nexteer has indicated its interest to expand its China business through forming alliances or acquiring automotive and direction motion businesses. As such, the announcement of an acquisition or new programme secured by leveraging on AVIC’s SOE status to secure orders from other auto OEMs with SOE backgrounds, would boost its share price, in our view. Valuation: We initiate coverage with a Buy (1) rating and 12-month TP of HKD9.70, based on a 2016E PER of 13x, at the high end of its global steering peers’ range. In our view, this premium is justified by Nexteer’s leading position in the steering business, and reflects our strong earnings CAGR forecast of 15%+ for 2015-17 and high ROE of 25% for 2015-16E. Risks: High concentration is the main risk, as Nexteer’s top-3 customers accounted for 79% of its revenue in 1H15. 3 November 2015 Initiation: steering towards a better future Electric power steering adoption set to rise on fuel efficiency demand Rising share in China’s electric power steering market, especially SUVs Initiate with a Buy (1) rating and TP of HK9.7 based on 13x 2016E PER Source: FactSet, Daiwa forecasts Nexteer Automotive Group (1316 HK) Target price: HKD9.70 Share price (2 Nov): HKD8.28 | Up/downside: +17.1% Brian Lam (852) 2532 4341 [email protected] Kelvin Lau (852) 2848 4467 [email protected] 80 95 110 125 140 5.5 6.6 7.8 8.9 10.0 Nov-14 Feb-15 May-15 Aug-15 Share price performance NAG (LHS) Relative to HSI (RHS) (HKD) (%) 12-month range 5.97-9.82 Market cap (USDbn) 2.66 3m avg daily turnover (USDm) 3.30 Shares outstanding (m) 2,498 Major shareholder Pacific Century Motor (67.0%) Financial summary (USD) Year to 31 Dec 15E 16E 17E Revenue (m) 3,338 3,745 4,185 Operating profit (m) 298 341 386 Net profit (m) 202 236 269 Core EPS (fully-diluted) 0.081 0.094 0.108 EPS change (%) 25.1 16.8 14.0 Daiwa vs Cons. EPS (%) 0.1 (3.7) (4.0) PER (x) 13.2 11.3 9.9 Dividend yield (%) 1.5 1.8 2.0 DPS 0.016 0.019 0.022 PBR (x) 3.1 2.5 2.1 EV/EBITDA (x) 6.8 5.7 4.8 ROE (%) 26.3 24.8 23.2

Transcript of Initiation: steering towards a better...

See important disclosures, including any required research certifications, beginning on page 25

Hong Kong Consumer Discretionary

Investment case: Increased adoption to drive earnings growth.

Nexteer is a leading global power steering provider that we think stands to

benefit from the industry conversion to more fuel-efficient electric power

steering from traditional energy-consuming hydraulic power steering (HPS).

We forecast electric power steering penetration to rise to 74% by 2017 from

60% in 2014, driven by strengthening fuel efficiency standards across the

globe. Nexteer should benefit, given that electric power steering occupies a

big portion of its revenue mix and has higher margins than traditional HPS.

Good earnings visibility. With the largest market share of 30%+ in the

US, and supported by its well-established relationships with General

Motors (GM), Fiat Chrysler Automobiles (FCA) and Ford, Nexteer enjoys

steady earnings growth in the US. High technical entry barriers to the

steering industry, the high cost to OEMs of changing steering suppliers

during a model life cycle, and long lead times of 2-2.5 years for each model

programme provide good earnings visibility for the company, in our view.

Large exposure to China’s outperforming SUV market. Based on our

observations, Nexteer aims to be one of the top-3 steering suppliers in

China by 2020, from its current <5% market share and 20% revenue

contribution in China. About 90% of its revenue in China is from SUVs,

MPVs and minivans, the sub-segments whose sales volumes we estimate

will significantly outperform the overall China PV market in 2016-17E. A

large proportion of Nexteer’s products are for small size engines (<1.6L),

which augurs well for the company given China’s recent reduction in the

purchase tax from 10% to 5%.

Catalysts: Nexteer’s ultimate controlling shareholder, AVIC, is a Chinese

SOE engaged in (among other things) local steering industry. Nexteer has

indicated its interest to expand its China business through forming alliances

or acquiring automotive and direction motion businesses. As such, the

announcement of an acquisition or new programme secured by leveraging

on AVIC’s SOE status to secure orders from other auto OEMs with SOE

backgrounds, would boost its share price, in our view.

Valuation: We initiate coverage with a Buy (1) rating and 12-month TP of

HKD9.70, based on a 2016E PER of 13x, at the high end of its global

steering peers’ range. In our view, this premium is justified by Nexteer’s

leading position in the steering business, and reflects our strong earnings

CAGR forecast of 15%+ for 2015-17 and high ROE of 25% for 2015-16E.

Risks: High concentration is the main risk, as Nexteer’s top-3 customers

accounted for 79% of its revenue in 1H15.

3 November 2015

Nexteer Automoti ve Group

Initiation: steering towards a better future

Electric power steering adoption set to rise on fuel efficiency demand

Rising share in China’s electric power steering market, especially SUVs

Initiate with a Buy (1) rating and TP of HK9.7 based on 13x 2016E PER

Source: FactSet, Daiwa forecasts

Nexteer Automotive Group (1316 HK)

Target price: HKD9.70

Share price (2 Nov): HKD8.28 | Up/downside: +17.1%

Brian Lam(852) 2532 4341

Kelvin Lau(852) 2848 4467

80

95

110

125

140

5.5

6.6

7.8

8.9

10.0

Nov-14 Feb-15 May-15 Aug-15

Share price performance

NAG (LHS) Relative to HSI (RHS)

(HKD) (%)

12-month range 5.97-9.82

Market cap (USDbn) 2.66

3m avg daily turnover (USDm) 3.30

Shares outstanding (m) 2,498

Major shareholder Pacific Century Motor (67.0%)

Financial summary (USD)

Year to 31 Dec 15E 16E 17E

Revenue (m) 3,338 3,745 4,185

Operating profit (m) 298 341 386

Net profit (m) 202 236 269

Core EPS (fully-diluted) 0.081 0.094 0.108

EPS change (%) 25.1 16.8 14.0

Daiwa vs Cons. EPS (%) 0.1 (3.7) (4.0)

PER (x) 13.2 11.3 9.9

Dividend yield (%) 1.5 1.8 2.0

DPS 0.016 0.019 0.022

PBR (x) 3.1 2.5 2.1

EV/EBITDA (x) 6.8 5.7 4.8

ROE (%) 26.3 24.8 23.2

2

Nexteer Automotive Group (1316 HK): 3 November 2015

Table of contents

Investment thesis 6

Technology conversion from hydraulic power steering to electric power steering ..........................6

Global trend of strengthening fuel efficiency standards to drive electric power steering growth .....7

Long lead times and high earnings visibility ...................................................................................8

Global auto demand still strong despite China slowdown ..............................................................8

AVIC as a controlling shareholder ............................................................................................... 10

Competitive landscape ................................................................................................................ 10

A leading steering manufacturer 12

Rich backlog, extensive electric power steering exposure ........................................................... 12

New programmes focussed on SUVs and MPVs ......................................................................... 12

Financial forecasts ...................................................................................................................... 13

Valuation and recommendation ................................................................................................... 15

Risks to our call ........................................................................................................................... 17

Company background 18

Company history ......................................................................................................................... 18

Products ...................................................................................................................................... 19

3

Nexteer Automotive Group (1316 HK): 3 November 2015

How do we justify our view?

Growth outlook Valuation Earnings revisions

Growth outlook Nexteer: net-profit forecasts

Nexteer reported net-profit growth of 48% YoY to

USD161m for 2014, driven by the conversion of steering

systems from hydraulic power steering to electric power

steering, especially in emerging countries like China. From

a high earnings base in 2014, the company still stands to

record solid net profit growth of 25%/17% YoY for 2015-

2016, based on our forecasts, supported by market-share

gains in China’s SUV market and Nexteer’s rich order

backlog coverage of 3.0x for 2016E.

Source: Company, Daiwa forecasts

Valuation Nexteer: 1-year forward PER (x)

Nexteer is trading currently at PERs of 13x for 2015E and

11x for 2016E, based on our EPS forecasts, compared with

its average trading PER of 10x since listing in October

2013. We set our target price at HKD9.7, based on a

2016E 13x PER, in line with global auto part peers’

average of 13.1x, but at the high end of its steering peers’

valuation range, justified in our view by Nexteer’s higher-

than-peer profit growth and ROE for the next 3 years.

Source: Company, Daiwa forecasts

Earnings revisions Nexteer: revisions to the Bloomberg-consensus EPS forecasts

Our earnings forecasts are largely in line with the

Bloomberg consensus. However, on the operational front,

we are more bullish than the market on Nexteer securing

more orders in the China market, by leveraging on AVIC’s

strong SOE background and network.

Source: Bloomberg

(20%)

0%

20%

40%

60%

80%

100%

0

50

100

150

200

250

300

2012 2013 2014 2015E 2016E 2017E

Net Profit (LHS) YoY Growth (RHS)

(USDm)

4

6

8

10

12

14

16

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Trading PER Average + 1SD -1 SD

(PER)

-1 SD

Avg

+1 SD

0.00

0.02

0.04

0.06

0.08

0.10

0.12

Jan-

14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

(USD)

2015E 2016E

4

Nexteer Automotive Group (1316 HK): 3 November 2015

Financial summary

Key assumptions

Profit and loss (USDm)

Cash flow (USDm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017E

Revenue growth (%) - U.S. 0.0 13.3 4.5 10.4 20.3 10.0 10.0 8.0

Revenue growth (%) - China 0.0 14.3 8.2 43.6 78.8 40.0 25.0 25.0

EBITDAR margin (%) - U.S. 2.5 4.6 4.7 10.9 11.4 14.0 14.0 14.0

EBITDAR margin (%) - China 13.2 (2.5) 11.0 8.6 15.5 16.0 16.5 17.0

Year to 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017E

North America 1,298 1,470 1,536 1,697 2,042 2,246 2,471 2,668

China 147 168 182 262 468 655 819 1,024

Other Revenue 607 609 449 428 468 437 455 493

Total Revenue 2,052 2,248 2,168 2,387 2,978 3,338 3,745 4,185

Other income (7) 9 (3) (2) (5) (13) (15) (17)

COGS (1,793) (1,970) (1,896) (2,047) (2,558) (2,830) (3,167) (3,536)

SG&A (225) (197) (180) (163) (178) (197) (221) (247)

Other op.expenses 0 0 0 0 0 0 0 0

Operating profit 27 90 89 175 238 298 341 386

Net-interest inc./(exp.) (6) (16) (22) (22) (22) (24) (24) (24)

Assoc/forex/extraord./others 1 (1) (5) (2) (1) (2) (2) (2)

Pre-tax profit 22 73 62 151 215 272 315 360

Tax (11) (5) (4) (40) (51) (65) (75) (86)

Min. int./pref. div./others (2) (1) (2) (2) (2) (5) (4) (5)

Net profit (reported) 9 67 57 109 161 202 236 269

Net profit (adjusted) 9 67 57 109 161 202 236 269

EPS (reported)(USD) 9.416 66.686 57.096 0.058 0.065 0.081 0.094 0.108

EPS (adjusted)(USD) 9.416 66.686 57.096 0.058 0.065 0.081 0.094 0.108

EPS (adjusted fully-diluted)(USD) 9.416 66.686 57.096 0.058 0.065 0.081 0.094 0.108

DPS (USD) 0.000 33.600 0.000 0.009 0.013 0.016 0.019 0.022

EBIT 27 90 89 175 238 298 341 386

EBITDA 57 144 146 248 356 447 523 602

Year to 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017E

Profit before tax 22 73 62 151 215 272 315 360

Depreciation and amortisation 30 54 58 74 119 149 181 216

Tax paid (8) (8) (6) (7) (51) (65) (75) (86)

Change in working capital 25 (39) (8) (27) (109) (35) (37) (40)

Other operational CF items 7 17 54 32 78 28 28 28

Cash flow from operations 76 98 160 223 251 349 413 478

Capex (61) (137) (276) (287) (279) (287) (293) (304)

Net (acquisitions)/disposals (318) 3 4 13 0 3 4 6

Other investing CF items (0) 1 (0) (4) 3 0 0 0

Cash flow from investing (379) (133) (273) (277) (276) (284) (288) (298)

Change in debt 299 15 133 47 (107) 0 0 0

Net share issues/(repurchases) 0 0 0 295 0 0 0 0

Dividends paid (34) 0 0 0 (22) (32) (40) (47)

Other financing CF items 92 (15) (34) (38) 219 (26) (26) (26)

Cash flow from financing 357 0 99 305 91 (58) (67) (73)

Forex effect/others 0 0 0 0 0 0 0 0

Change in cash 53 (35) (14) 250 66 6 58 107

Free cash flow 14 (39) (116) (65) (28) 62 120 174

5

Nexteer Automotive Group (1316 HK): 3 November 2015

Financial summary continued …

Balance sheet (USDm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

As at 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017E

Cash & short-term investment 113 78 64 314 380 387 444 552

Inventory 152 157 174 185 226 250 280 312

Accounts receivable 308 316 324 364 525 589 660 738

Other current assets 50 45 65 76 94 105 118 132

Total current assets 624 596 628 939 1,226 1,331 1,503 1,734

Fixed assets 271 290 434 563 626 699 760 807

Goodwill & intangibles 6 76 180 272 345 399 438 465

Other non-current assets 12 12 17 31 46 52 57 63

Total assets 912 973 1,259 1,805 2,242 2,481 2,758 3,069

Short-term debt 365 405 99 130 97 97 97 97

Accounts payable 255 260 296 336 439 486 544 607

Other current liabilities 139 103 112 125 146 163 183 204

Total current liabilities 758 767 507 592 682 746 823 908

Long-term debt 26 2 442 458 634 634 634 634

Other non-current liabilities 53 82 118 165 218 218 218 218

Total liabilities 837 850 1,067 1,214 1,534 1,598 1,675 1,760

Share capital 54 111 171 568 684 684 684 684

Reserves/R.E./others 0 0 0 0 0 170 365 587

Shareholders' equity 54 111 171 568 684 853 1,049 1,270

Minority interests 21 12 21 23 24 30 34 39

Total equity & liabilities 912 973 1,259 1,805 2,242 2,481 2,758 3,069

EV 2,966 3,009 3,166 2,966 3,038 3,031 2,972 2,864

Net debt/(cash) 277 328 477 274 351 344 287 179

BVPS (USD) 54.339 110.828 170.931 0.227 0.274 0.342 0.420 0.509

Year to 31 Dec 2010 2011 2012 2013 2014 2015E 2016E 2017E

Sales (YoY) n.a. 9.5 (3.6) 10.1 24.8 12.1 12.2 11.8

EBITDA (YoY) n.a. 154.4 1.7 69.6 43.6 25.4 17.0 15.1

Operating profit (YoY) n.a. 232.5 (1.7) 97.2 36.1 25.5 14.5 12.9

Net profit (YoY) n.a. 608.2 (14.4) 91.2 47.8 25.1 16.8 14.0

Core EPS (fully-diluted) (YoY) n.a. 608.2 (14.4) (99.9) 10.5 25.1 16.8 14.0

Gross-profit margin 12.6 12.4 12.5 14.2 14.1 15.2 15.4 15.5

EBITDA margin 2.8 6.4 6.8 10.4 12.0 13.4 14.0 14.4

Operating-profit margin 1.3 4.0 4.1 7.3 8.0 8.9 9.1 9.2

Net profit margin 0.5 3.0 2.6 4.6 5.4 6.1 6.3 6.4

ROAE 34.7 80.7 40.5 29.6 25.8 26.3 24.8 23.2

ROAA 2.1 7.1 5.1 7.1 8.0 8.6 9.0 9.2

ROCE 11.6 18.1 14.0 18.3 18.2 19.5 19.9 20.0

ROIC 4.0 20.8 14.9 16.7 18.8 19.8 20.0 20.5

Net debt to equity 509.7 296.3 278.8 48.2 51.3 40.4 27.3 14.1

Effective tax rate 48.3 7.4 5.7 26.7 23.9 23.9 23.9 23.9

Accounts receivable (days) 27.4 50.7 53.9 52.6 54.5 60.9 60.9 61.0

Current ratio (x) 0.8 0.8 1.2 1.6 1.8 1.8 1.8 1.9

Net interest cover (x) 4.8 5.7 4.1 8.0 11.0 12.4 14.2 16.2

Net dividend payout 0.0 50.4 0.0 15.0 20.0 20.0 20.0 20.0

Free cash flow yield 0.5 n.a. n.a. n.a. n.a. 2.3 4.5 6.5

Company profile

Listed on the Hong Kong Stock Exchange in 2013, Nexteer is a leading global steering and driveline

manufacturer, solely dedicated to electric and hydraulic steering systems, steering columns and

driveline products for original equipment manufacturers. Its customers include General Motors, Fiat

Chrysler, Ford, Toyota and PSA Peugeot Citroen, as well as automakers in India, China and South

America.

6

Nexteer Automotive Group (1316 HK): 3 November 2015

Investment thesis

Technology conversion from hydraulic power steering to electric power steering

Power steering

Power steering is a system that helps drivers steer the wheels of vehicles using a source

of power other than the driver’s own power. Depending on the origins of the power,

steering systems can be further categorised into: 1) electric power steering, which uses

electrical components to generate power and control steering, and 2) hydraulic power

steering, which uses fluid pressure to control the steering.

Advantages of electric power steering over hydraulic power steering

Nexteer’s technology edge is in electronic power steering, a comparatively new

technology. Electric power steering involves a less complicated build and mechanism

which takes up less space in a vehicle’s engine, while hydraulic power steering is a

primitive technology that has been around for decades. Due to the advantages listed below

of electric power steering over hydraulic power steering, there has been increasing

conversion from hydraulic power steering to electric power steering over the past 5 years:

i) Electric power steering is about 5% more energy efficient than hydraulic power

steering, as hydraulic power steering extracts power from the engine, while electric

power steering consumes power from the battery.

ii) Electric power steering needs less maintenance compared to hydraulic power

steering, since hydraulic power steering uses hydraulic fluids for operation, whereas

there is no such fluid needed for electric power steering.

iii) Electric power steering is not connected to the engine by a belt (as is hydraulic

steering), and is therefore engine-independent. It can still run when the engine is off,

as it depends on the car’s electrical systems.

iv) Electric power steering gives a better response at different speeds compared to

hydraulic power steering.

v) Electric power steering is less prone to problems and faults and its components are

more durable.

vi) Hydraulic power steering is more complicated and usually weighs more than electric

power steering.

Rising electric power steering penetration for the auto industry

Benefiting from the rising trend of fuel-efficient vehicle development, electric power

steering is likely to see an acceleration in adoption globally. In 2015, we forecast the global

automotive steering system market size to reach USD31bn (from USD23bn in 2007), while

electric power steering dominates the steering system market, with a market share of over

60%.

Electric power steering, hydraulic power steering and Others revenue split in global steering market

Source: Company, IPSOS, Daiwa forecasts

22,878 23,948

20,697

24,661 26,339 27,045 28,162 29,436 30,945

32,673 34,654

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 E 2016 E 2017 E

(USDm)(USDm)

Electric Power Steering Hydraulic Power Steering Others

Electric power steering

is more fuel efficient,

requires less

maintenance, and is

more durable than

hydraulic power steering

7

Nexteer Automotive Group (1316 HK): 3 November 2015

Adoption of electric power steering in emerging markets still lags that in the US and Europe In 2014, China’s automotive steering system market size reached 23.89m units, from only

21m units in 2013, of which the demand for passenger car steering systems rose to 19.9m

units. In emerging markets like China, mainstream companies’ electric power steering

technology has been maturing over the past 5 years, and replacing hydraulic power

steering to take the main role in the automotive steering system market in China. However,

the adoption rate in China, at about 52%, is still behind that in the US (70%+) and

Europe/Japan (80%+).

Global trend of strengthening fuel efficiency standards to drive electric power steering growth

Electric power steering market share to increase to 74% by 2017E on greater demand for fuel efficiency Due to increasingly stringent government fuel efficiency, emissions and safety regulations

across the globe, OEMs have as a result seen increased demand for electric power

steering to replace conventional hydraulic power steering for its better fuel efficiency.

According to a recent IPSOS Report, the market share of electric power steering increased

from 44.6% in 2007 to 58.8% of the total steering industry in 2012 in terms of sales

revenue, and is expected to rise to 74.0% of the total steering industry by 2017E.

China to strengthen fuel efficiency standards by 35% in next 5 years China’s new fuel consumption standards, targeted to be implemented for passenger

vehicles (PVs) by end-2015, call for vehicle fuel consumption to be reduced to 5.0L/km (or

21.3km/litre) by 2020, from 6.9L/km (or 15.7km/litre) currently. This is lower than current

US standards and close to Japan’s (see table). Meanwhile, China has also announced that

it plans to cut CO2 emissions by 27% by 2020.

China’s fuel-consumption target is calculated by taking the weighted average number of

vehicles sold and then determining the corresponding fuel consumption per OEM. Thus,

we think the OEMs are likely to develop more electric vehicles (EVs) in the coming years,

as doing so would allow them to reduce their blended fuel consumption figures. We see

increasing demand for electric power steering in China, especially for SUV OEMs, as they

will need to develop more fuel-efficient models, given that SUVs typically consume a lot of

fuel.

Nexteer’s advanced technology is complemented by its strong technical expertise in the

field of electric power steering, which is widely considered a pioneering and industry-

leading technology. In our view, the company is poised to benefit from higher electric

power steering adoption in China.

Summary of fuel-efficiency targets: major markets in terms of car manufacturing or exports

km/l (mpg) US EU Japan China S. Korea

2005 12.4 (29.0) 15.8 (37.2) 16.7 (39.3) 11.0 (25.9) 12.3 (28.9)

2010 13.9 (33.0) 18.0 (42.3) 19.6 (46.1) 14.4 (33.9) 14.8 (34.8)

2015 15.4 (36.0) 19.7 (46.3) 21.0 (49.4) 15.7 (36.9) 16.7 (39.3)

2020 19.9 (47.0) 25.8 (60.7) 23.4 (55.0) 21.3 (50.1) 16.7 (39.3)

2025 23.9 (56.0) 30.8 (72.4) ~ 35.0 (82.3) 23.4 (55.0) 21.3 (50.1) 16.7 (39.3)

5-YOY (%) US EU Japan China S. Korea

2010 12.1% 13.9% 17.4% 30.9% 20.3%

2015 10.8% 9.4% 7.1% 9.0% 12.8%

2020 29.2% 31.0% 11.4% 35.7% 0.0%

2025 20.1% 19.4%~35.7% 0.0% 0.0% 0.0%

Improvement (%) US EU Japan China S. Korea

2010-25 71.9% 71.1%~94.4% 19.4% 47.9% 12.8%

2015-25 55.2% 56.3%~77.7% 11.4% 35.7% 0.0%

Source: ICCT

Note: No official guidance on fuel efficiency has been provided by Korea (beyond 2015), Japan (beyond 2020), or China (beyond 2020)

Higher fuel efficiency

standards and

environmental

regulations should

accelerate the adoption

of electric power

steering

8

Nexteer Automotive Group (1316 HK): 3 November 2015

CO2 emissions targets: major car markets

Year (g/km) US EU Japan China S. Korea

2005 212 162 153 n.a. 325

2010 188 140 128 180 175

2015 167 130 110 161 153

2020 126 95 105 117 153

2025 103 68~78 105 117 153

5-YoY (%) US EU Japan China S. Korea

2010 -11.3% -13.6% -16.3% n.a. -46.2%

2015 -11.2% -7.1% -14.1% -10.6% -12.6%

2020 -24.6% -26.9% -4.5% -27.3% 0.0%

2025 -18.3% -17.9~-28.4% 0.0% 0.0% 0.0%

Improvement (%) US EU Japan China S. Korea

2010-25 -45.2% -44%~-51% -18.0% -35.0% -12.6%

2015-25 -38.3% -39%~-48% -4.5% -27.3% 0.0%

Source: The International Council on Clean Transportation (ICCT)

Note: No official guidance on emissions has been provided by Korea (beyond 2015), Japan ( beyond 2020), or China (beyond 2020)

Long lead times and high earnings visibility

Barriers for OEMs to switch steering suppliers

Steering systems and driveline suppliers have to get involved in the early stage of new

automobile model design, usually 2-2.5 years (longer for some luxury brands) ahead of the

official launch of the models. Moreover, the steering suppliers typically enter into business

contracts with auto OEMs that last the whole life cycle (usually 4-7 years) of a vehicle’s

programme. Once a steering systems supplier has secured the contract for a new

programme, it is likely to predict the visible revenue contribution from that programme. It is

therefore unlikely that OEMs would switch suppliers during the course of a vehicle

programme.

Barriers to entry to the steering systems market

One of the main barriers to entry to the global driveline system market is the competitive

nature of the market, which is dominated by a few key manufacturers, including Nexteer,

JTEKT Corporation (6473 JP, JPY2,102, Outperform [2]), Germany’s ZF Lenksysteme, and

the US’s TRW Automotive, which all have typically established long-term relationships with

auto OEMs.

Other barriers include limited access to relevant technology, and the capital-intensive

nature of the industry. High investment is needed for continuous testing of new products

and development. Steering systems suppliers must have strong technical and engineering

capabilities in vehicle integration and software development. New entrants lacking

sufficient capital and technical capability will face difficulties meeting the stringent

requirements of world-class automotive manufacturers.

New business opportunities typically arise only when new models of vehicles are

developed or existing models undergo a design enhancement. OEMs conduct a global

supplier search to source the next generation of such vehicle programmes, which may or

may not include the incumbent supplier. Each new vehicle programme includes new

requirements for suppliers, including new design specifications.

Global auto demand still strong despite China slowdown

Enjoys the largest market share in the US

During the conference call for the company’s 3Q update, Nexteer management said the

company’s automobile sales in North America had maintained solid momentum and

continued to be strong. According to Wards, year-to-September overall US automobile

sales were up 5%, largely driven by 11% growth in the light trucks segment. Nexteer had

the largest market share of more than 30% in terms of sales revenue from steering

systems in 2014, by our estimate, and is therefore well positioned to gain from the steady

growth of the US automobile market.

High entry barriers given

technology and capital

requirements, plus long

lead times, provide good

earnings visibility

9

Nexteer Automotive Group (1316 HK): 3 November 2015

US: light vehicle sales volume and growth US: truck vehicle sales volume and growth

Source: Wards Source: Wards

Recovering EU automobile market

Light vehicle sales in the EU market have recovered to 9% YoY growth in the YTD to end-

September 2015, from 6% YoY growth for 2014. Management noted that auto sales for

3Q15 picked up and that the 4Q15 number could see a further improvement. The company

targets for its EU operation to enjoy a natural hedge by increasing localisation in the region

by next year.

EU: passenger vehicle sales volume and growth EU: commercial vehicle sales volume and growth

Source: ACEA Source: ACEA

Considerable exposure to China’s SUV market According to management, about 90% of Nexteer’s revenue in China is derived from

steering and driveline systems for SUVs, MPVs and minivans, sub-segments that tend to

significantly outperform the overall automobile market in China. For instance, in the YTD to

September, the SUV and MPV sales volumes grew by 50% and 11%, respectively, while

the overall passenger vehicles market edged up by 3% only. A large proportion of

Nexteer’s products are for PVs with small engines (<1.6L), which should also benefit from

China’s reduction in September of its purchase tax cut to 5% (previously 10%).

China: passenger vehicle sales volume and growth China: SUV sales volume and growth

Source: CAAM Source: CAAM

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

2011 2012 2013 2014 2015 YTDSep

(YoY %)(Units)

US Light vehicle sales YoY % (RHS)

0%

2%

4%

6%

8%

10%

12%

14%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

2011 2012 2013 2014 2015 YTD Sep

(YoY %) (Units)

US Light trucks YoY % (RHS)

(10%)

(5%)

0%

5%

10%

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

2011 2012 2013 2014 2015 YTDSep

(YoY %)(Units)

EU PV YoY % (RHS)

(15%)

(10%)

(5%)

0%

5%

10%

15%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2011 2012 2013 2014 2015 YTDSep

(YoY %)(Units)

EU <= 3.5t YoY % (RHS)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

5,000,000

10,000,000

15,000,000

20,000,000

2011 2012 2013 2014 2015 YTDSep

(YoY %)(Units)

China PV sales YoY % (RHS)

0%

10%

20%

30%

40%

50%

60%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2011 2012 2013 2014 2015 YTDSep

(YoY %)(Units)

China SUV salse YoY % (RHS)

Stable US auto market,

recovering EU market,

and gaining market

share in China, with

focus on outperforming

SUV segment

10

Nexteer Automotive Group (1316 HK): 3 November 2015

AVIC as a controlling shareholder

China market share likely to increase, benefiting from AVIC’s SOE background

AVIC, Nexteer’s controlling shareholder (through Pacific Century Motor [PCM], of which

AVIC owns 51%), is a China SOE conglomerate with businesses spanning several

segments, including defence, helicopters, avionic systems, general aviation, asset

management, financial services and automobiles. PCM, a subsidiary of Beijing E-Town, an

investment arm of the Beijing Government, bought a 100% stake in Nexteer from GM in

2010. AVIC then purchased a 51% stake in PCM in 2011, becoming Nexteer’s largest

shareholder.

Following the AVIC acquisition, we believe Nexteer will gradually start competing more

aggressively in China, taking advantage of parent AVIC’s SOE background. For example,

two of the auto-related companies controlled by AVIC, namely Zhuzhou Yilida Electrical

Mechanical (Yilida) and Yubei Steering System (Yubei Steering), are engaged in the

steering business. Both are not listed and their technology lags that of Nexteer. It is

therefore possible, in our view, that Nexteer will leverage on its parent AVIC to expand its

own steering business in China. Nexteer has also indicated its interest in expanding the

China business through acquisitions and alliances in both the automotive and direction

motion businesses, to achieve greater autonomous functionality in the longer term.

Competitive landscape

With the expansion of the global automotive market, demand for steering systems has

showed steady growth. In 2014, the size of the global automotive steering system market

exceeded 90m units, with revenue of USD31.1bn. Electric power steering has a dominant

position in the steering system market, with a share of more than 60%.

The size of China’s automotive steering system market increased to 23.89m units in 2014

from 21m units in 2013, of which the demand for passenger car steering systems rose to

19.92m units. In China, the electric power steering technology of the mainstream

manufacturing companies has become more mature over the past 5 years, with product

demand growing rapidly, and electric power steering replacing hydraulic power steering as

the main role in the automotive steering system market.

The global automotive steering system market is highly concentrated, with only 6 big

producers, namely, JTEKT Corporation, ZF Lenksysteme, TRW, NSK (6471 JP,

JPY1,442, , Hold [3]) , Korea’s Mando (204320 KS, KRW146,500, Underperform [4]), and

Nexteer. In 2014, a 100% stake of the world's second-largest steering system

manufacturer in terms of revenue and volume, ZF Lenksysteme, was acquired by Bosch,

while ZF Lenksysteme acquired the third-ranked TRW Automotive in 2014.

In China, JTEKT and other foreign manufacturers still hold dominant positions. At the same

time, local China enterprises, such as China Automotive Systems (CAAS), Zhejiang

Shibao, FAWER Automotive Parts and AVIC-Xihang Yubei have been increasing their

market shares. As China's largest steering system group, CAAS operates its business

through 8 subsidiaries. In China, CAAS serves mainly Geely (175 HK, HKD4.09, Buy [1],

Great Wall Motors (2333 HK, HKD9.50, Underperform [4]), Brilliance Jinbei, BYD (1211

HK, HKD47.7, Outperform [2]), Beiqi Foton, Dongfeng Motor, FAW Group and Chery.

Leveraging AVIC’s

network in china

automobile industry,

Nexteer looks set to gain

market share in China

Electric power steering

is a competitive but

growing industry

11

Nexteer Automotive Group (1316 HK): 3 November 2015

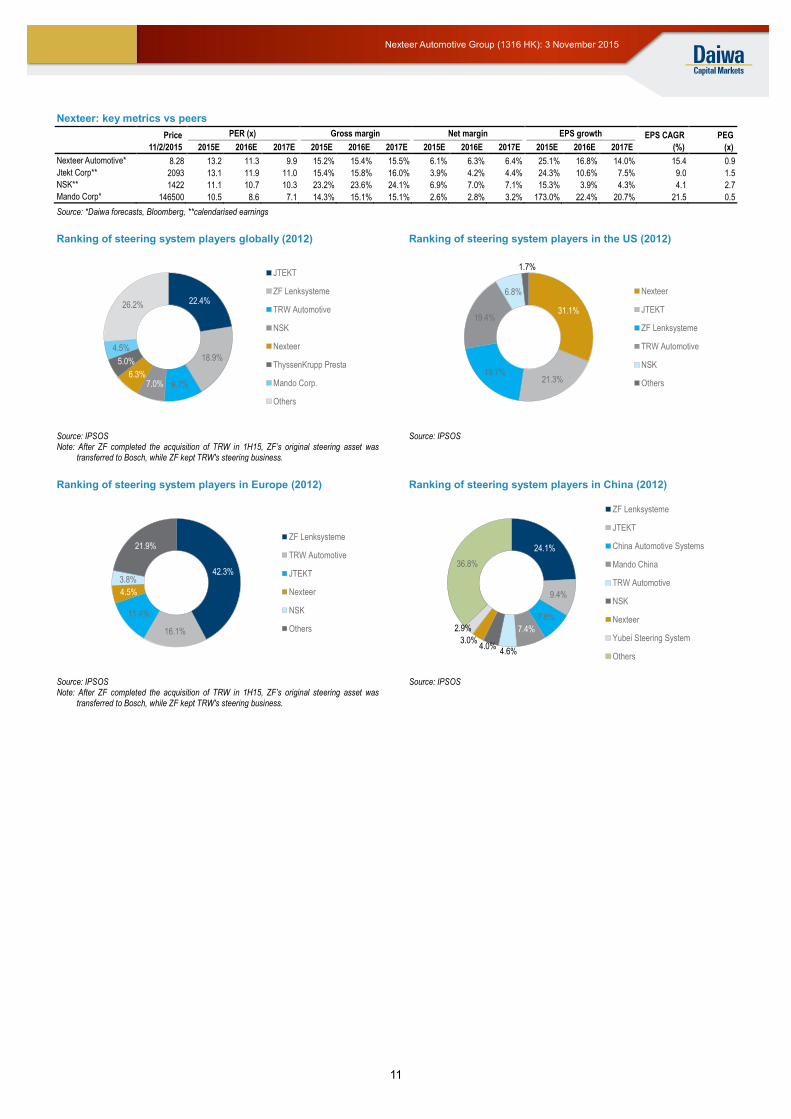

Nexteer: key metrics vs peers

Price PER (x) Gross margin Net margin EPS growth EPS CAGR PEG

11/2/2015 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E (%) (x)

Nexteer Automotive* 8.28 13.2 11.3 9.9 15.2% 15.4% 15.5% 6.1% 6.3% 6.4% 25.1% 16.8% 14.0% 15.4 0.9

Jtekt Corp** 2093 13.1 11.9 11.0 15.4% 15.8% 16.0% 3.9% 4.2% 4.4% 24.3% 10.6% 7.5% 9.0 1.5

NSK** 1422 11.1 10.7 10.3 23.2% 23.6% 24.1% 6.9% 7.0% 7.1% 15.3% 3.9% 4.3% 4.1 2.7

Mando Corp* 146500 10.5 8.6 7.1 14.3% 15.1% 15.1% 2.6% 2.8% 3.2% 173.0% 22.4% 20.7% 21.5 0.5

Source: *Daiwa forecasts, Bloomberg, **calendarised earnings

Ranking of steering system players globally (2012) Ranking of steering system players in the US (2012)

Source: IPSOS Note: After ZF completed the acquisition of TRW in 1H15, ZF’s original steering asset was

transferred to Bosch, while ZF kept TRW's steering business.

Source: IPSOS

Ranking of steering system players in Europe (2012) Ranking of steering system players in China (2012)

Source: IPSOS Note: After ZF completed the acquisition of TRW in 1H15, ZF’s original steering asset was

transferred to Bosch, while ZF kept TRW's steering business.

Source: IPSOS

22.4%

18.9%

9.7%7.0%6.3%

5.0%

4.5%

26.2%

JTEKT

ZF Lenksysteme

TRW Automotive

NSK

Nexteer

ThyssenKrupp Presta

Mando Corp.

Others

31.1%

21.3%19.7%

19.4%

6.8%

1.7%

Nexteer

JTEKT

ZF Lenksysteme

TRW Automotive

NSK

Others

42.3%

16.1%

11.4%

4.5%

3.8%

21.9%ZF Lenksysteme

TRW Automotive

JTEKT

Nexteer

NSK

Others

24.1%

9.4%

7.8%

7.4%

4.6%4.0%

3.0%

2.9%

36.8%

ZF Lenksysteme

JTEKT

China Automotive Systems

Mando China

TRW Automotive

NSK

Nexteer

Yubei Steering System

Others

12

Nexteer Automotive Group (1316 HK): 3 November 2015

A leading steering manufacturer

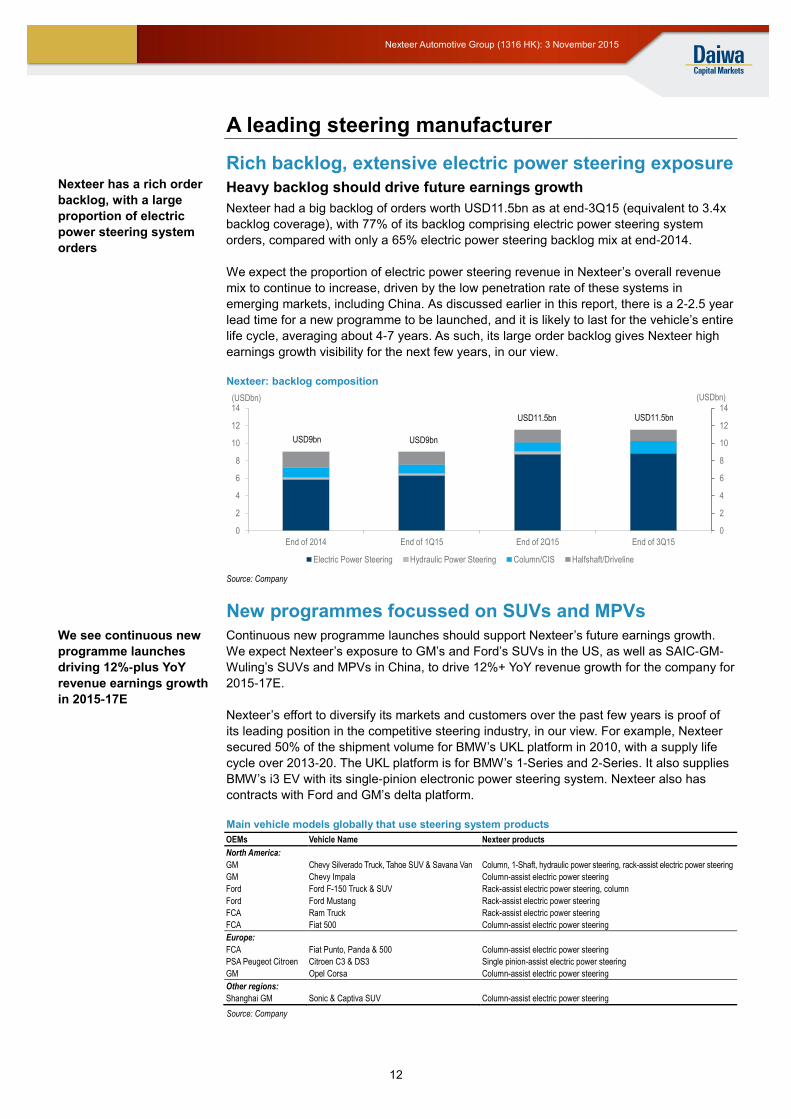

Rich backlog, extensive electric power steering exposure

Heavy backlog should drive future earnings growth

Nexteer had a big backlog of orders worth USD11.5bn as at end-3Q15 (equivalent to 3.4x

backlog coverage), with 77% of its backlog comprising electric power steering system

orders, compared with only a 65% electric power steering backlog mix at end-2014.

We expect the proportion of electric power steering revenue in Nexteer’s overall revenue

mix to continue to increase, driven by the low penetration rate of these systems in

emerging markets, including China. As discussed earlier in this report, there is a 2-2.5 year

lead time for a new programme to be launched, and it is likely to last for the vehicle’s entire

life cycle, averaging about 4-7 years. As such, its large order backlog gives Nexteer high

earnings growth visibility for the next few years, in our view.

Nexteer: backlog composition

Source: Company

New programmes focussed on SUVs and MPVs

Continuous new programme launches should support Nexteer’s future earnings growth.

We expect Nexteer’s exposure to GM’s and Ford’s SUVs in the US, as well as SAIC-GM-

Wuling’s SUVs and MPVs in China, to drive 12%+ YoY revenue growth for the company for

2015-17E.

Nexteer’s effort to diversify its markets and customers over the past few years is proof of

its leading position in the competitive steering industry, in our view. For example, Nexteer

secured 50% of the shipment volume for BMW’s UKL platform in 2010, with a supply life

cycle over 2013-20. The UKL platform is for BMW’s 1-Series and 2-Series. It also supplies

BMW’s i3 EV with its single-pinion electronic power steering system. Nexteer also has

contracts with Ford and GM’s delta platform.

Main vehicle models globally that use steering system products

OEMs Vehicle Name Nexteer products

North America:

GM Chevy Silverado Truck, Tahoe SUV & Savana Van Column, 1-Shaft, hydraulic power steering, rack-assist electric power steering

GM Chevy Impala Column-assist electric power steering

Ford Ford F-150 Truck & SUV Rack-assist electric power steering, column

Ford Ford Mustang Rack-assist electric power steering

FCA Ram Truck Rack-assist electric power steering

FCA Fiat 500 Column-assist electric power steering

Europe:

FCA Fiat Punto, Panda & 500 Column-assist electric power steering

PSA Peugeot Citroen Citroen C3 & DS3 Single pinion-assist electric power steering

GM Opel Corsa Column-assist electric power steering

Other regions:

Shanghai GM Sonic & Captiva SUV Column-assist electric power steering

Source: Company

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

End of 2014 End of 1Q15 End of 2Q15 End of 3Q15

(USDbn)(USDbn)

Electric Power Steering Hydraulic Power Steering Column/CIS Halfshaft/Driveline

USD11.5bn USD11.5bn

USD9bn USD9bn

Nexteer has a rich order

backlog, with a large

proportion of electric

power steering system

orders

We see continuous new

programme launches

driving 12%-plus YoY

revenue earnings growth

in 2015-17E

13

Nexteer Automotive Group (1316 HK): 3 November 2015

Main vehicle models globally that use driveline system products

OEMs Vehicle Name Nexteer products

North America:

GM Silverado, Tahoe, Malibu, Lacross, Regal, Cruze, Impala, Camaro & ATS Halfshafts

GM Equinox, Terrain, Traverse & Enclave Halfshafts, Intermediate Drive Shafts

Chrysler Ram Truck, 300 & Liberty Halfshafts

Chrysler Mini Van Halfshafts, Intermediate Drive Shafts

Other regions:

PSA Peugeot Citroen Brazil Various models Halfshafts

Chinese local OEMs Various models Halfshafts

Indian local OEMs Various models Halfshafts

Source: Company

Product programmes launched by various OEMs in 2015

OEMs Vehicle Name Nexteer products Launch time

North America:

GM Equinox, Terrain Halfshafts 1Q15

Ford F550, F650, F750 Column 2Q15

GM Chevy Volt Halfshafts 3Q15

GM Heavy duty Chevy Silverado, GM Sierras Hydraulic power steering 3Q15

China:

Ford Ranger, Everest Hydraulic power steering 2Q15

SAIC-GM-Wuling Bao Jun 560 Rack-assist electric power steering 2Q15

SAIC-GM-Wuling Hong Guang S1 Brush column-assist electric power steering 2Q15

FCA Fiat 225 E6 Brush column-assist electric power steering 2Q15

Changan CS75 Halfshafts 3Q15

Other regions:

Renault Clio, Kangoo Hydraulic power steering 1Q15

Suzuki Every & Every Wagon Column 1Q15

Renault Logan, Sandero, Hydraulic power steering 2Q15

Mahindra Jeeto Halfshafts 2Q15

Eicher Polaris Multix Halfshafts 2Q15

Ford Mustang Electric power steering 3Q15

Renault Kwind Halfshafts 3Q15

Tata Indica Halfshafts 3Q15

Maruti-Suzuki Swift Halfshafts 3Q15

Source: Company

Financial forecasts

Nexteer’s 15%+ earnings CAGR driven by increasing electric power steering adoption in China coupled with its existing strong US presence

We forecast the revenue generated from the China market to account for 20% of Nexteer’s

total revenue in 2015, and further increase to 24% by 2017E, from 16% in 2014. For the

US market, which is largest revenue contributor, Nexteer should see strong momentum in

SUV and pick-up truck sales, while we think Europe should see signs of recovery by the

end of this year. We forecast 40%/10%/0% YoY revenue growth for Nexteer from China/the

US/Europe, respectively, for 2015.

Nexteer’s increasing portion of electric power steering in its revenue mix (from 56% in

2014 to 66% by 2017E) should stand the company in good stead amid the ongoing shift

from hydraulic power steering to electric power steering, especially in emerging markets

like China. Such a high level of electric power steering revenue suggests further margin

expansion for the company over the next 3 years, as electric power steering products

usually carry ASPs that are more than 2x higher than those for hydraulic power steering,

as well as higher margins.

As a result, we forecast Nexteer’s overall revenue to increase by 12% per year for 2015-

17E, backed by market-share gains in China, while its net profit rises by 25%/17%/14%

YoY for 2015-17E, outperforming top-line growth as a result of a strong 2.4pp rise in the

EBITDA margin to 14.4% by 2017E from 12% in 2014.

Increasing revenue

contribution from China

despite slowing China

auto market

Revenue growth backed

by China market-share

gains

14

Nexteer Automotive Group (1316 HK): 3 November 2015

Nexteer: revenue projection by region Nexteer: revenue mix by region

Source: Company, Daiwa forecasts Source: Company, Daiwa forecasts

Nexteer: revenue projection by product Nexteer: revenue mix by product

Source: Company, Daiwa forecasts Source: Company, Daiwa forecasts

Improving cash flow and gearing

Net of maintenance capex of USD287m, we forecast the company’s free cash flow to turn

positive in 2015, and enable it to reduce its net gearing to 40% in 2015E from 51% in 2014.

We look for ROE of 26% for 2015E, but see this figure gradually falling to 23% by 2017E

on further deleveraging. We assume a dividend payout ratio of 20%. The current share

price suggests 1.5%/1.8% dividend yields for 15E/16E. In our view, Nexteer’s healthy

balance sheet will enable it to expand its existing business and seize any new businesses

opportunities.

Nexteer: FCF and debt/equity ratio

Source: Company, Daiwa forecasts

Raw-material costs a large proportion of cost of sales

The company’s raw-material costs accounted for the largest proportion, at 67%, of

Nexteer’s cost of sales in 2014, while manufacturing expenses comprised 30%. Its raw

materials, which are mostly used in castings, machine parts, motors, and bearings, etc.,

are affected by commodities prices, including steel, rare earth magnet materials, aluminium

and copper. The company’s practice is to negotiate certain contracts that permit it to fully

1,697 2,042 2,246 2,471 2,668

303 363

363 381

419

262

468 655

819 1,024

125

105

73 73

73

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2013 2014 2015E 2016E 2017E

(USDm)(USDm)

North America Europe China RoW

71% 69% 67% 66% 64%

13% 12% 11% 10% 10%

11% 16% 20% 22% 24%

5% 4% 2% 2% 2%

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

2013 2014 2015E 2016E 2017E

(Mix %)(Mix %)

North America Europe China RoW

1,085 1,668

2,002 2,402

2,883 320

183 146

117

94

513

583 630

680

735

470

544 560

545

474

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2013 2014 2015E 2016E 2017E

(USDm)(USDm)

Electric Power Steering Hydraulic Power Steering Column Driveline

45%56% 60% 64% 69%

13%6% 4%

3%2%21% 20% 19% 18%18%

20% 18% 17% 15% 11%

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

2013 2014 2015E 2016E 2017E

(Mix %)(Mix %)

Electric Power Steering Hydraulic Power Steering Column Driveline

0%

10%

20%

30%

40%

50%

60%

(150)

(100)

(50)

0

50

100

150

200

2013 2014 2015E 2016E 2017 E

(Net debt / equity ratio,%)(USDm)

Free Cash Flow (LHS) Net debt/ equity ratio (RHS)

We look for net gearing

to decline to 38% this

year

15

Nexteer Automotive Group (1316 HK): 3 November 2015

or partially pass on certain raw-material price increases, particularly price increases related

to steel, to mitigate the impact on its margins.

Nexteer: cost of sales breakdown (2014)

Source: Company

Nexteer: income statement

(In USDm except otherwise indicated) 2013 2014 2015E 2016E 2017E

Revenue 2,387 2,978 3,338 3,745 4,185

YoY growth (RHS) 10% 25% 12% 12% 12%

Rev by region:

North America 1,697 2,042 2,246 2,471 2,668

Europe 303 363 363 381 419

China 262 468 655 819 1,024

RoW 125 105 73 73 73

Rev Mix by regions

North America 71% 69% 67% 66% 64%

Europe 13% 12% 11% 10% 10%

China 11% 16% 20% 22% 24%

RoW 5% 4% 2% 2% 2%

Rev by product:

Steering – electric power steering 1,085 1,668 2,002 2,402 2,883

Steering - hydraulic power steering 320 183 146 117 94

Column 513 583 630 680 735

Driveline 470 544 560 545 474

Rev Mix by product:

Steering - electric power steering 45% 56% 60% 64% 69%

Steering - hydraulic power steering 13% 6% 4% 3% 2%

Column 21% 20% 19% 18% 18%

Driveline 20% 18% 17% 15% 11%

Gross profit 339 420 508 577 649

YoY growth 25% 24% 21% 14% 12%

Gross margin 14.2% 14.1% 15.2% 15.4% 15.5%

EBITDA 248 356 447 523 602

YoY growth 70% 44% 25% 17% 15%

EBITDA margin 10.4% 12.0% 13.4% 14.0% 14.4%

EBIT 175 238 298 341 386

YoY growth 97% 36% 26% 15% 13%

EBIT margin 7.3% 8.0% 8.9% 9.1% 9.2%

Net income, post-exceptionals 109 161 202 236 269

YoY growth 91% 48% 25% 17% 14%

Net margin 4.6% 5.4% 6.1% 6.3% 6.4%

ROE 29.6% 25.8% 26.3% 24.8% 23.2%

ROA 7.1% 8.0% 8.6% 9.0% 9.2%

SG&A/revenue -6.8% -6.0% -5.9% -5.9% -5.9%

Source: Company, Daiwa forecasts

Valuation and recommendation

We initiate coverage of Nexteer with a Buy (1) rating and 12-month target price of

HKD9.70, based on a 2016E PER of 13x, representing 17% upside potential from the

current share price level. We believe Nexteer’s leading position in the steering business,

potentially stronger-than-peer earnings CAGR (which we forecast at 15%+ over 2015-17E)

and ROE (c25%+ for 2015-16E) and increasing exposure to the SUV segment

outperforming the China market, justify the stock trading at a valuation premium to its

peers. Nexteer’s global automotive parts peers are trading currently at weighted average

2016F PER of 13.1x, based on the Bloomberg-consensus forecasts. Our target multiple for

Raw material67%

Manufacturing expense30%

Other expenses2%

We believe Nexteer

should trade at the high

end of its peers’ range,

backed by its higher

ROE and earnings

growth, especially in

China SUV market

16

Nexteer Automotive Group (1316 HK): 3 November 2015

Nexteer represents the average of the global auto parts players’ valuation, but is at a high

end of its steering peers’ range – a premium we believe is well deserved.

Auto fuel efficiency standards are currently being strengthened across the globe, which is

resulting in an acceleration in the shift to electric power steering from hydraulic power

steering. Nexteer, as one of the world’s leading steering systems manufacturers, should

benefit from its substantial electric power steering revenue portion, leading to higher

margins and earnings growth for the company.

By 2020, the company targets to have become a top-3 steering supplier in China, the

largest auto market in the world. About 90% of Nexteer’s revenue in China is derived from

SUVs, MPVs and minivans, the sub-segments that since this year have significantly

outperformed (in terms of volume) the overall automobile market in China. New vehicle

programmes from OEMs also provide good delivery visibility and sold earnings growth.

Nexteer: PER bands Nexteer: PBR bands

Source: Bloomberg, Daiwa forecasts Source: Bloomberg, Daiwa forecasts

Auto parts: valuation comparisons

Name

Bloomberg Trading

Share price

Market cap Rating PER (x) PBR (x) EV/EBITDA(x) Div yield (%) ROE (%)

code currency USDm

FY15E FY16E FY15E FY16E FY15E FY16E FY15E FY16E FY15E FY16E

China H-share listed

Nexteer Automotive * 1316 HK HKD 8.28 2669 Buy 13.2 11.3 3.1 2.5 6.8 5.7 1.5 1.8 26.3 24.8

Minth Group

425 HK HKD 16.04 2290 NR 11.6 9.9 1.5 1.4 9.0 7.7 3.3 3.7 14.2 14.8

Johnson Electric Holdings ** 179 HK HKD 27.90 3170 NR 14.2 13.2 1.5 1.4 7.4 6.9 1.9 2.1 11.3 11.3

Japan

Jtekt Corp *,** 6473 JP JPY 2093.00 5956 NR 13.1 11.9 1.4 1.3 5.9 5.6 1.9 2.1 11.0 11.3

Nsk Ltd *, ** 6471 JP JPY 1422.00 6498 Neutral 11.1 10.7 1.5 1.4 6.3 6.1 2.4 2.6 14.2 13.1

Ntn Corp ** 6472 JP JPY 552.00 2437 NR 9.1 8.6 1.1 1.0 6.0 6.0 1.9 2.6 12.2 11.2

Denso Corp *, ** 6902 JP JPY 5546.00 40645 Outperform 15.4 13.8 1.3 1.2 6.5 6.1 2.2 2.4 8.5 8.9

Aisin Seiki *, ** 7259 JP JPY 4820.00 11774 Outperform 14.3 12.6 1.1 1.0 4.4 4.0 2.1 2.4 7.9 8.5

S.Korea

Hyundai Mobis * 012330 KS KRW 240000.00 20543 Buy 7.1 6.2 0.9 0.8 4.2 3.4 1.5 1.7 13.2 13.6

Mando Corp * 204320 KS KRW 146500.00 1210 Underperform 10.5 8.6 1.0 0.8 5.7 5.7 3.3 3.7 10.5 10.9

Halla Holdings Corp

060980 KS KRW 56500.00 537 NR 3.1 2.7 0.4 0.4 1.8 1.5 1.8 1.8 15.1 15.2

US

Dana Holding Corp

DAN US USD 16.80 2569 NR 9.3 9.2 2.7 2.3 4.9 4.8 1.3 1.3 27.5 27.1

Johnson Controls Inc *** JCI US USD 45.18 29551 NR 13.3 11.8 2.6 2.5 9.3 8.6 2.3 2.4 19.3 21.1

Delphi Automotive Plc

DLPH US USD 83.19 23301 NR 16.1 13.4 9.4 7.0 10.7 9.2 1.2 1.3 56.0 59.4

Autoliv Inc

ALV US USD 121.24 10679 NR 19.1 16.6 3.0 2.8 9.3 8.4 1.9 2.1 14.9 17.2

Visteon Corp

VC US USD 109.07 4410 NR 55.6 36.8 1.7 2.3 8.4 7.2 n.a. n.a. 4.0 5.2

Others

Motherson Sumi Systems ** MSS IN INR 245.05 4938 NR 23.1 16.2 7.8 6.1 7.3 5.8 1.5 2.0 35.9 39.6

Tong Yang Industry

1319 TT TWD 36.45 663 NR 16.0 13.2 1.2 1.2 7.2 6.7 2.7 3.5 7.5 8.9

Valeo Sa

FR FP EUR 142.35 12461 NR 15.8 14.1 3.4 2.9 6.8 6.2 1.9 2.2 22.3 21.7

Magna International Inc

MG CN CAD 68.96 21330 NR 11.5 9.7 1.8 1.9 6.7 5.7 1.6 1.8 22.2 24.3

Total

Weighted average

14.7 13.1 2.8 2.4 7.2 6.5 1.9 2.1 19.8 21.0

High

55.6 36.8 9.4 7.0 10.7 9.2 3.3 3.7 56.0 59.4

Low

3.1 2.7 0.4 0.4 1.8 1.5 1.2 1.3 4.0 5.2

Median

13.2 11.8 1.5 1.4 6.7 6.0 1.9 2.1 14.2 14.2

Source: Bloomberg, *Daiwa forecasts Note: **Mar year-end, *** Sep year-end, Japan companies are based on calendarised earnings Pricing as of 2 November 2015 for Asia stocks, and 30 October 2015 for North America and Europe stocks

2

3

4

5

6

7

8

9

10

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

(HKD)

Historical Avg PER: 10.3x

13x

12x

11x

10x

9x8x

2

3

4

5

6

7

8

9

10

11

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb

-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

(HKD)

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

Historical Avg PBR: 2.4x

17

Nexteer Automotive Group (1316 HK): 3 November 2015

Risks to our call

Main risk: high customer concentration

Nexteer’s top-3 customers (including GM, FCA and Ford) accounted for 79% of its revenue

in 1H15. Its largest customer, GM, accounted for 49% of Nexteer’s global sales, with the

next 2 largest customers making up a further 19% and 12%, respectively. The loss of any

one of these customers could have a material adverse effect on the company’s financial

condition.

Worse-than-expected automobile sales

The steering business is directly related to automotive sales and production, which are

highly cyclical and depend on general economic conditions and consumer spending.

Slower-than-expected auto sales in the US (Nexteer’s largest market) and China

(increasing exposure) would have a negative impact on the company’s financial

performance.

Foreign-exchange risk

Since Nexteer reports in USD, a strong USD, especially against the Euro and CNY, can

lead to translation losses, even though the company targets to limit its currency exposure

through natural hedges in Europe by 2016.

18

Nexteer Automotive Group (1316 HK): 3 November 2015

Company background

Listed on the Stock Exchange of Hong Kong, Nexteer is a global manufacturer of steering

and driveline products, with more than 10,000 employees and 20 manufacturing plants

worldwide, as well as 14 local customer support centres and 5 regional engineering and

test centres. The company is the fourth-largest steering-parts supplier by market share. It

has more than 60 customers globally, including BMW, GM, Ford, Chrysler, Fiat, Toyota,

PSA Peugeot Citroen, and other manufacturers in North America, Europe, China and

South America.

Nexteeer: revenue breakdown by product type (2014)

Source: Company

Company history Nexteer: development milestones

Year Event

1906 Founded as Jackson, Church & Wilcox Co. in the US

1909 Acquired by GM’s Buick

1917 Separated from Buick and became Jackson, Church, Wilcox Division, the first automotive parts manufacturing division of GM

1950s Saginaw Safety Power Steering was made available to the market

1968 Introduced anti-theft steering column to the market. Energy-absorbing steering column is a critical element of governmental safety legislation in developed markets such as the US and Europe, while anti-theft functionality is a critical technical requirement

1976 Rack and pinion (R&P) steering system was introduced to the market on the AMC Pacer. This system provides a more direct steer ing connection with greater road feedback to the driver

1995 Expanded into the China market by establishing Nexteer Zhuozhou, a joint venture, in China to produce halfshafts

1995 Advanced systems centre opened in Saginaw, Michigan

1995 Delphi EPS system was made available to the market

1995 Vehicle evaluation test track commenced construction in Saginaw, Michigan, to facilitate faster development of steering and driveline products

1996 Expanded into the India market by constructing a manufacturing facility in Bangalore to produce halfshafts

1998 Launched EPS business with Volkswagen

1998 Expanded into Poland market by commencing construction of a manufacturing facility in Tychy, Poland to produce axle shafts

1998 Organized as a division of Delphi Corporation, which was created by GM

1999 Became a division of an independent publicly held corporation after Delphi Corporation was spun off from GM

1999 Received Pace Award for E-STEER electronic power steering from Automotive News. The Automotive News Pace Awards honour superior innovation, technological advancement and business performance among automotive suppliers

1999 Launched the driveline business with Volkswagen

2000 Received Shingo Prize for Excellence Award from The Shingo Prize for Operational Excellence, which is awarded to organisations demonstrating the sound application of improvement techniques across an enterprise

2000 International Organization for Standardization 140001 certification obtained for the manufacturing site in the US

2003 Introduced Delphi EPS on the Fiat Panda, the European Car of the Year in 2004

2006 100-year anniversary

2006 Introduced Driver Protection Module and One Touch Adjustable Column to the market

2007 Launched the electronic power steering product with Ford

2009 Acquired by GM and renamed Nexteer Automotive

2010 Acquired by PCM China from GM

2010 High Output 12 Volt Rack EPS debuts on Ford Mustang and Ford F-150 Truck

2011 AVIC Auto acquired a 51% interest in PCM China from Beijing E-Town

2012 Expanded product portfolio by securing contract for entry-level CEPS products

2012 Grew high-output REPS business by contracting with an additional global OEM customer

2012 Contracted for the first global business with Volkswagen

2013 Listed on the Hong Kong Stock Exchange

Source: Company

USD1,668m;rev mix 56%

USD183m;6%

USD 583m;20%

USD 544m; 18% Electric Power Steering

Hydraulic Power Steering

Column

Driveline

19

Nexteer Automotive Group (1316 HK): 3 November 2015

Nexteer: shareholding structure

Source: Company

Products

What is power steering?

Power steering is a system that helps to steer a vehicle’s wheels using a source of power

other than the driver’s manual force. Nexteer is mainly engaged in the manufacturing of: 1)

steering systems that include electronic power steering, hydraulic power steering, and

steering columns, and 2) driveline systems including halfshafts, intermediate drive shafts

and propeller shaft joints. Its products are used on a broad range of vehicles, from small

passenger cars to full-size trucks.

Electronic power steering

Electronic power steering uses an electric motor to assist the driver in steering. Depending

on the type of electric power steering system, a computer module applies assistive power

via an electric motor coupled directly to either the steering gear or steering column.

1) Column-assist electric power steering integrates the system electronics (motor,

controller and sensor) and assists mechanism with the steering column. Auto OEMs

that use Nexteer’s column-assist electric power steering products include GM in small

cars, such as the Aveo, Shanghai GM in the Sonic and Captiva sports utility vehicles,

and Fiat Chrysler in small cars such as the Fiat 500. In China, the company has

introduced a new entry-level brush motor column-assist electric power steering (brush

column-assist electric power steering) specifically tailored for developing markets.

OEMs that use Nexteer’s Brush column-assist electric power steering include SAIC-

GM-Wuling Automobile for the Wuling Hongguang S micro van and Zheng Cheng.

2) Rack-assist electric power steering integrates the electric assist mechanism with

the steering rack, and they are contained under the hood/bonnet in the engine

compartment. Nexteer’s rack-assist electric power steering customers include Ford for

the F-150 pickup truck and Mustang, Fiat Chrysler in the Ram pickup truck, and GM in

AVIC Automobile Industry Holding Co., Ltd

(China)

100%

Pacific Century Motors, Inc.

(China)

49% 51%

Nexteer Automotive (Hong Kong) Holding Limited

(Hong Kong) Other Shareholders

Nexteer Automotive Group Limited

(1316 HK)

67% 33%

Beijing E-Town International Investment & Development Co.,

Ltd.

(China)

20

Nexteer Automotive Group (1316 HK): 3 November 2015

various half-ton trucks and SUVs. The company also supplies rack-assist electric

power steering for performance vehicles including the Ford Mustang, Dodge Charger

and Dodge Challenger.

3) Single pinion-assist electric power steering integrates the electric assist

mechanism with the steering gear pinion shaft. The company’s single pinion-assist

electric power steering customers include PSA Peugeot Citroën in the Citroën C3 and

DS3, Dongfeng Peugeot Citroën in the Citroën C-Elysée and Peugeot 2008, and BMW

in the 1-series, the i3 and the Mini Cooper line.

Hydraulic power steering

HPS uses high pressure fluids to assist driver steering, where an engine-driven power

steering pump creates system pressure. When the driver turns the steering wheel, it opens

up the flow of pressurised fluid, turning the wheels in the required direction. Nexteer’s OEM

customers that use steering gears include GM in its three-quarter-ton trucks and large

vans, and Fiat Chrysler in various light commercial vehicles. OEM customers that use

steering pumps include Fiat Chrysler, GM and PSA Peugeot Citroën.

Column-assist electric power steering Rack-assist electric power steering

Source: Company Source: Company

Single pinion-assist electric power steering Hydraulic power steering

Source: Company Source: Company

Steering columns and intermediate shafts

Steering columns and intermediate shafts connect the steering wheel to the steering

mechanism and control steering by transferring the driver’s input torque from the steering

wheel. The company designs these products for small cars, SUVs and trucks. OEM

customers for steering columns include GM for various full-size trucks, large vans and the

Chevy Impala, and Ford in the F-150 pickup truck.

21

Nexteer Automotive Group (1316 HK): 3 November 2015

Steering column

Source: Company

Driveline systems

Halfshafts are designed for a variety of vehicles and are custom engineered to meet

specific vehicle requirements. OEM customers that use the company’s halfshafts include:

Fiat Chrysler, GM, PSA Peugeot Citroën, Volkswagen and a number of China and India

OEMs. Intermediate drive shafts work in conjunction with the halfshafts to improve vehicle

handling and eliminate driveline disturbance issues on front wheel drive vehicles with

unequal length axles, higher torque and running angles. OEM customers that use

Nexteer’s intermediate drive shafts include GM in various crossover utility vehicles.

Propeller shaft joints are designed for high-speed use in vehicles employing a front

engine/rear drive powertrain configuration. OEM customers that use the company’s

propeller shaft joints include Ford in the Taurus, Flex and Fusion.

Driveline systems

Source: Company

22

Nexteer Automotive Group (1316 HK): 3 November 2015

Nexteer: management profile

Management Profile

ZHAO, Guibin Mr Zhao has been the CEO since June 2012, and was appointed as executive director and chairman of the board in June 2013. He is primarily responsible for setting the strategic vision, direction and goals, and overseeing the overall execution of the group's strategy. Mr Zhao held managerial positions at subsidiaries of AVIC since 2003, including chairman of the board and general manager of AVIC Auto, Chairman of the Board of AVIC Heavy Machinery Co. Ltd, and General Manager of Sichuan Lingfeng Aeronautics Hydraulic. Mr Zhao has 17 years of experience in the automotive industry.

RICHARDSON, Michael Paul Mr Richardson was appointed as executive director in June 2013. He has been senior vice president, chief technology and strategy officer, as well as chairman of both the China division and the driveline business unit of Nexteer Automotive since June 2012. Mr Richardson has over 40 years of experience in the automotive industry. He is now responsible for all of the group's technology planning, information technology and strategy planning , as well as M&A.

FAN, Yi Mr Fan was appointed as joint company secretary in January 2013, and then executive director in June 2013, as well as vice president in November 2013. With approximately 16 years of experience in the automotive industry, he is now responsible for the management of the operations and handling of company secretarial duties.

LU, Daen Mr Lu was appointed as non-executive director in August 2013, and is mainly responsible for participating in the group's strategic and key operational decision-making processes and advising on strategies and policies. Mr Lu has 19 years of relevant experience in the automotive industry, and formerly served as a director and general manager of AVIC Auto and a director of PCM China.

WANG, Xiaobao Mr Wang was appointed as non-executive director in August 2013, and is responsible for participating in the group's strategic and key operational decision-making processes and advising on strategies and policies. He has approximately 3 years of experience in the automotive industry.

BRESSON, Laurent Robert Mr Bresson was appointed as global chief operating officer in May 2012, and then president in June 2012. He is responsible for reporting to the chairman of the board and overseeing the group's global functions including sales, engineering, operation, human resources, finance and global supply management, and is in charge of overseeing the group's product lines. He is concurrently leading the Nexteer Strategy Counsel (NSC), the top strategy and policy-making body in the group. Mr Bresson has 19 years of experience in the automotive industry.

PERKINS, Joseph Michael Mr Perkins was appointed as senior vice president and chief financial officer in December 2012. He is responsible for the group's investor relations, treasury, capital funding and structure, M&A support, accounting and financial reporting, financial planning and analysis, program finance, risk management, financial controls and taxation. Mr Perkins is also a member of the NSC. He has 24 years of automotive sector experience.

CORBEIL, James Martin Mr Corbeil was appointed as vice president and chief procurement officer in November 2012. He is responsible for purchasing, supplier development, production control, global logistics as well as suppler launch management functions. Mr Corbeil has 25 years of global, progressive and multi-functional experience in both the defence and

automotive industries.

LUBISCHER, Frank Peter Josef Mr Lubischer was appointed a chief operating officer (Europe), and vice president of global engineering in December 2012. He is responsible for the group's global engineering, and customer application. He has 20 years of automotive managerial expertise and is also a member of the NSC.

HOEG, Dennis Steven Mr Hoeg was appointed as vice president of enterprise systems, manufacturing engineering and capital in December 2012. He is responsible for the group's global manufacturing engineering (focusing primarily on launch of products), capital plan, and enterprise system improvements. He has 37 years automotive experience and is also a member of the NSC.

FRIES, Diane Marthey Ms. Fries was appointed as vice president of quality in February 2012. She is responsible for the establishment and improvement of the group's quality culture and quality system, representing the group's quality systems to customers and third parties, and managing corporate responsibilities for warranty, audit, problem solving, advanced product quality planning and metrics. She is also a member of the NSC. Ms. Fries has 18 years of quality system expertise in the automotive industry.

OWENBY, Douglas E. Mr Owenby was appointed as vice president, chief operating officer of the Saginaw division in August 2013. He is responsible for developing and executing the business plan of the Saginaw division, negotiating commitments from the business lines, leveraging corporate functions to meet the business plan and the overall financial position of the Saginaw division. He has approximately 27 years of relevant experience in the automotive industry. He is also a member of the NSC.

LIU, Tao Mr Liu was appointed as vice president and chief operating officer of the China division in August 2013. He is responsible for the business plan, the overall financial position and advising on strategic direction of the China division of the group. Mr Liu has approximately 17 years of relevant experience in the automotive industry.

DECKER, Mark P. Mr Decker was appointed as president and chief human resources officer in September 213. He is responsible for all global human resources activities. Mr Decker has approximately 22 years of experience in the automotive industry.

Source: Company

23

Nexteer Automotive Group (1316 HK): 3 November 2015

Daiwa’s Asia Pacific Research Directory

HONG KONG

Takashi FUJIKURA (852) 2848 4051 [email protected]

Regional Research Head

Kosuke MIZUNO (852) 2848 4949 / (852) 2773 8273

Regional Research Co-head

John HETHERINGTON (852) 2773 8787 [email protected]

Regional Deputy Head of Asia Pacific Research

Rohan DALZIELL (852) 2848 4938 [email protected]

Regional Head of Product Management

Kevin LAI (852) 2848 4926 [email protected]

Chief Economist for Asia ex-Japan; Macro Economics (Regional)

Christie CHIEN (852) 2848 4482 [email protected]

Macro Economics (Regional); Banking; Insurance (Taiwan)

Junjie TANG (852) 2773 8736 [email protected]

Macro Economics (China)

Jonas KAN (852) 2848 4439 [email protected]

Head of Hong Kong and China Property

Cynthia CHAN (852) 2773 8243 [email protected]

Property (China)

Leon QI (852) 2532 4381 [email protected]

Banking (Hong Kong/China); Broker (China); Insurance (China)

Anson CHAN (852) 2532 4350 [email protected]

Consumer (Hong Kong/China)

Jamie SOO (852) 2773 8529 [email protected]

Gaming and Leisure (Hong Kong/China)

Dennis IP (852) 2848 4068 [email protected]

Power; Utilities; Renewables and Environment (Hong Kong/China)

John CHOI (852) 2773 8730 [email protected]

Head of Hong Kong and China Internet; Regional Head of Small/Mid Cap

Kelvin LAU (852) 2848 4467 [email protected]

Head of Automobiles; Transportation and Industrial (Hong Kong/China)

Brian LAM (852) 2532 4341 [email protected]

Transportation – Railway; Construction and Engineering (China)

Jibo MA (852) 2848 4489 [email protected]

Head of Custom Products Group

Thomas HO (852) 2773 8716 [email protected]

Custom Products Group

PHILIPPINES

Bianca SOLEMA (63) 2 737 3023 [email protected]

Utilities and Energy

SOUTH KOREA

Sung Yop CHUNG (82) 2 787 9157 [email protected]

Pan-Asia Co-head/Regional Head of Automobiles and Components; Automobiles; Shipbuilding; Steel

Mike OH (82) 2 787 9179 [email protected]

Banking; Capital Goods (Construction and Machinery)