INITIATING COVERAGE HDFC IN EQUITY February 21,...

32

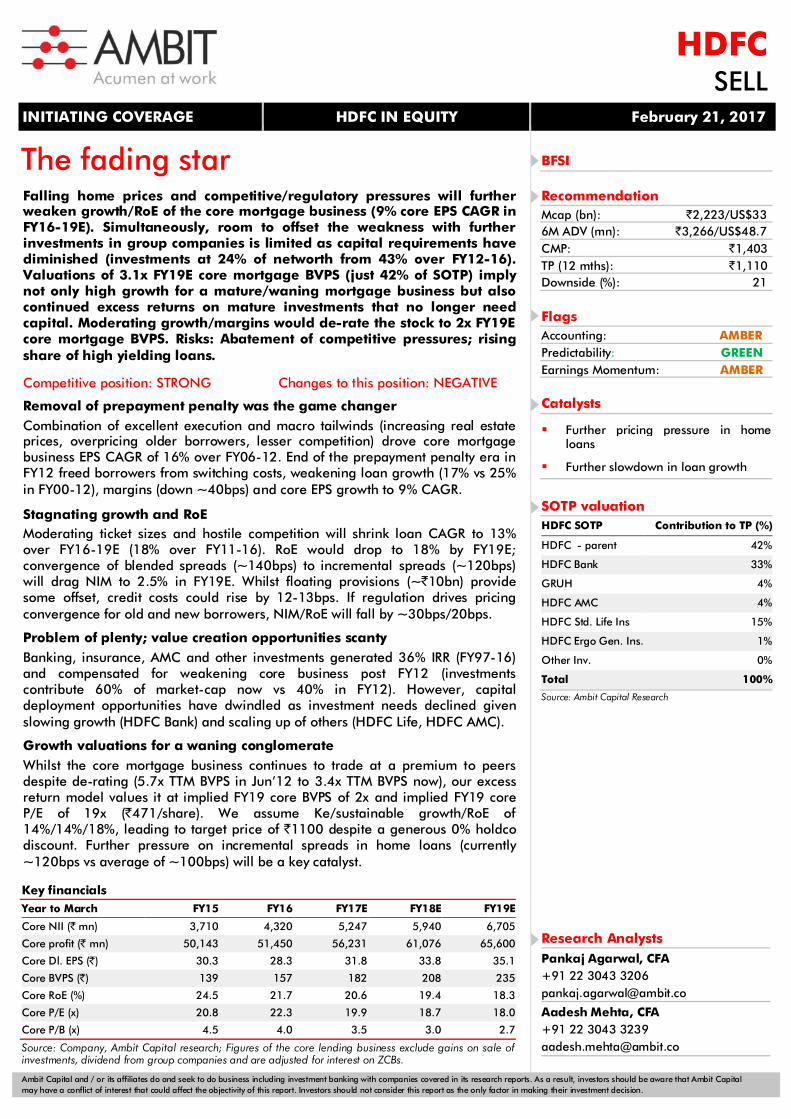

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision. The fading star Falling home prices and competitive/regulatory pressures will further weaken growth/RoE of the core mortgage business (9% core EPS CAGR in FY16-19E). Simultaneously, room to offset the weakness with further investments in group companies is limited as capital requirements have diminished (investments at 24% of networth from 43% over FY12-16). Valuations of 3.1x FY19E core mortgage BVPS (just 42% of SOTP) imply not only high growth for a mature/waning mortgage business but also continued excess returns on mature investments that no longer need capital. Moderating growth/margins would de-rate the stock to 2x FY19E core mortgage BVPS. Risks: Abatement of competitive pressures; rising share of high yielding loans. Competitive position: STRONG Changes to this position: NEGATIVE Removal of prepayment penalty was the game changer Combination of excellent execution and macro tailwinds (increasing real estate prices, overpricing older borrowers, lesser competition) drove core mortgage business EPS CAGR of 16% over FY06-12. End of the prepayment penalty era in FY12 freed borrowers from switching costs, weakening loan growth (17% vs 25% in FY00-12), margins (down ~40bps) and core EPS growth to 9% CAGR. Stagnating growth and RoE Moderating ticket sizes and hostile competition will shrink loan CAGR to 13% over FY16-19E (18% over FY11-16). RoE would drop to 18% by FY19E; convergence of blended spreads (~140bps) to incremental spreads (~120bps) will drag NIM to 2.5% in FY19E. Whilst floating provisions (~`10bn) provide some offset, credit costs could rise by 12-13bps. If regulation drives pricing convergence for old and new borrowers, NIM/RoE will fall by ~30bps/20bps. Problem of plenty; value creation opportunities scanty Banking, insurance, AMC and other investments generated 36% IRR (FY97-16) and compensated for weakening core business post FY12 (investments contribute 60% of market-cap now vs 40% in FY12). However, capital deployment opportunities have dwindled as investment needs declined given slowing growth (HDFC Bank) and scaling up of others (HDFC Life, HDFC AMC). Growth valuations for a waning conglomerate Whilst the core mortgage business continues to trade at a premium to peers despite de-rating (5.7x TTM BVPS in Jun’12 to 3.4x TTM BVPS now), our excess return model values it at implied FY19 core BVPS of 2x and implied FY19 core P/E of 19x (`471/share). We assume Ke/sustainable growth/RoE of 14%/14%/18%, leading to target price of `1100 despite a generous 0% holdco discount. Further pressure on incremental spreads in home loans (currently ~120bps vs average of ~100bps) will be a key catalyst. INITIATING COVERAGE HDFC IN EQUITY February 21, 2017 HDFC SELL BFSI Recommendation Mcap (bn): `2,223/US$33 6M ADV (mn): `3,266/US$48.7 CMP: `1,403 TP (12 mths): `1,110 Downside (%): 21 Flags Accounting: AMBER Predictability: GREEN Earnings Momentum: AMBER Catalysts Further pricing pressure in home loans Further slowdown in loan growth SOTP valuation HDFC SOTP Contribution to TP (%) HDFC - parent 42% HDFC Bank 33% GRUH 4% HDFC AMC 4% HDFC Std. Life Ins 15% HDFC Ergo Gen. Ins. 1% Other Inv. 0% Total 100% Source: Ambit Capital Research Research Analysts Pankaj Agarwal, CFA +91 22 3043 3206 [email protected] Aadesh Mehta, CFA +91 22 3043 3239 [email protected] Key financials Year to March FY15 FY16 FY17E FY18E FY19E Core NII (` mn) 3,710 4,320 5,247 5,940 6,705 Core profit (` mn) 50,143 51,450 56,231 61,076 65,600 Core Dl. EPS (`) 30.3 28.3 31.8 33.8 35.1 Core BVPS (`) 139 157 182 208 235 Core RoE (%) 24.5 21.7 20.6 19.4 18.3 Core P/E (x) 20.8 22.3 19.9 18.7 18.0 Core P/B (x) 4.5 4.0 3.5 3.0 2.7 Source: Company, Ambit Capital research; Figures of the core lending business exclude gains on sale of investments, dividend from group companies and are adjusted for interest on ZCBs.

Transcript of INITIATING COVERAGE HDFC IN EQUITY February 21,...

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

The fading star

Falling home prices and competitive/regulatory pressures will further weaken growth/RoE of the core mortgage business (9% core EPS CAGR in FY16-19E). Simultaneously, room to offset the weakness with further investments in group companies is limited as capital requirements have diminished (investments at 24% of networth from 43% over FY12-16). Valuations of 3.1x FY19E core mortgage BVPS (just 42% of SOTP) imply not only high growth for a mature/waning mortgage business but also continued excess returns on mature investments that no longer need capital. Moderating growth/margins would de-rate the stock to 2x FY19E core mortgage BVPS. Risks: Abatement of competitive pressures; rising share of high yielding loans.

Competitive position: STRONG Changes to this position: NEGATIVE Removal of prepayment penalty was the game changer Combination of excellent execution and macro tailwinds (increasing real estate prices, overpricing older borrowers, lesser competition) drove core mortgage business EPS CAGR of 16% over FY06-12. End of the prepayment penalty era in FY12 freed borrowers from switching costs, weakening loan growth (17% vs 25% in FY00-12), margins (down ~40bps) and core EPS growth to 9% CAGR. Stagnating growth and RoE Moderating ticket sizes and hostile competition will shrink loan CAGR to 13% over FY16-19E (18% over FY11-16). RoE would drop to 18% by FY19E; convergence of blended spreads (~140bps) to incremental spreads (~120bps) will drag NIM to 2.5% in FY19E. Whilst floating provisions (~`10bn) provide some offset, credit costs could rise by 12-13bps. If regulation drives pricing convergence for old and new borrowers, NIM/RoE will fall by ~30bps/20bps. Problem of plenty; value creation opportunities scanty Banking, insurance, AMC and other investments generated 36% IRR (FY97-16) and compensated for weakening core business post FY12 (investments contribute 60% of market-cap now vs 40% in FY12). However, capital deployment opportunities have dwindled as investment needs declined given slowing growth (HDFC Bank) and scaling up of others (HDFC Life, HDFC AMC).

Growth valuations for a waning conglomerate Whilst the core mortgage business continues to trade at a premium to peers despite de-rating (5.7x TTM BVPS in Jun’12 to 3.4x TTM BVPS now), our excess return model values it at implied FY19 core BVPS of 2x and implied FY19 core P/E of 19x (`471/share). We assume Ke/sustainable growth/RoE of 14%/14%/18%, leading to target price of `1100 despite a generous 0% holdco discount. Further pressure on incremental spreads in home loans (currently ~120bps vs average of ~100bps) will be a key catalyst.

INITIATING COVERAGE HDFC IN EQUITY February 21, 2017

HDFCSELL

BFSI

Recommendation Mcap (bn): `2,223/US$33 6M ADV (mn): `3,266/US$48.7 CMP: `1,403 TP (12 mths): `1,110 Downside (%): 21

Flags Accounting: AMBER Predictability: GREEN Earnings Momentum: AMBER

Catalysts

Further pricing pressure in home loans

Further slowdown in loan growth

SOTP valuation HDFC SOTP Contribution to TP (%)

HDFC - parent 42%

HDFC Bank 33%

GRUH 4%

HDFC AMC 4%

HDFC Std. Life Ins 15%

HDFC Ergo Gen. Ins. 1%

Other Inv. 0%

Total 100%

Source: Ambit Capital Research

Research Analysts Pankaj Agarwal, CFA +91 22 3043 3206 [email protected]

Aadesh Mehta, CFA +91 22 3043 3239 [email protected]

Key financials Year to March FY15 FY16 FY17E FY18E FY19E

Core NII (` mn) 3,710 4,320 5,247 5,940 6,705

Core profit (` mn) 50,143 51,450 56,231 61,076 65,600

Core Dl. EPS (`) 30.3 28.3 31.8 33.8 35.1

Core BVPS (`) 139 157 182 208 235

Core RoE (%) 24.5 21.7 20.6 19.4 18.3

Core P/E (x) 20.8 22.3 19.9 18.7 18.0

Core P/B (x) 4.5 4.0 3.5 3.0 2.7

Source: Company, Ambit Capital research; Figures of the core lending business exclude gains on sale of investments, dividend from group companies and are adjusted for interest on ZCBs.

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 2

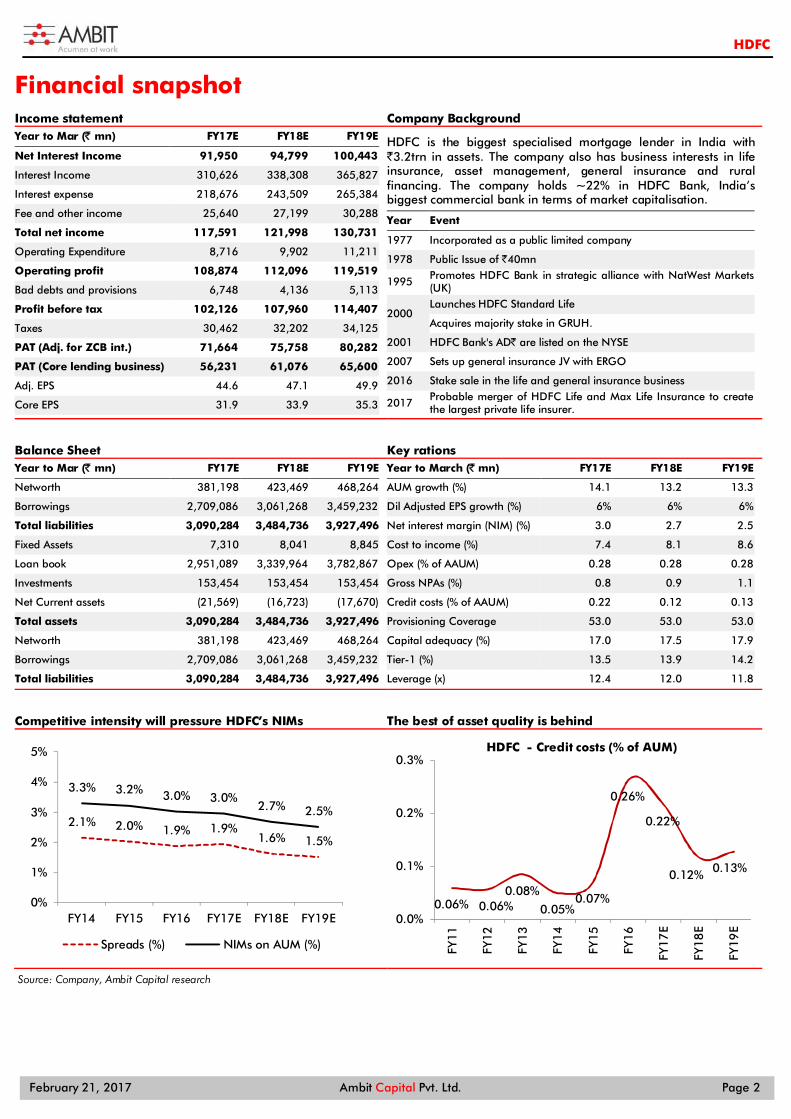

Financial snapshot Income statement Company Background Year to Mar (̀ mn) FY17E FY18E FY19E

Net Interest Income 91,950 94,799 100,443

Interest Income 310,626 338,308 365,827

Interest expense 218,676 243,509 265,384

Fee and other income 25,640 27,199 30,288

Total net income 117,591 121,998 130,731

Operating Expenditure 8,716 9,902 11,211

Operating profit 108,874 112,096 119,519

Bad debts and provisions 6,748 4,136 5,113

Profit before tax 102,126 107,960 114,407

Taxes 30,462 32,202 34,125

PAT (Adj. for ZCB int.) 71,664 75,758 80,282

PAT (Core lending business) 56,231 61,076 65,600

Adj. EPS 44.6 47.1 49.9

Core EPS 31.9 33.9 35.3

HDFC is the biggest specialised mortgage lender in India with `3.2trn in assets. The company also has business interests in life insurance, asset management, general insurance and rural financing. The company holds ~22% in HDFC Bank, India’s biggest commercial bank in terms of market capitalisation.

Year Event

1977 Incorporated as a public limited company

1978 Public Issue of `40mn

1995 Promotes HDFC Bank in strategic alliance with NatWest Markets (UK)

2000 Launches HDFC Standard Life

Acquires majority stake in GRUH.

2001 HDFC Bank's AD` are listed on the NYSE

2007 Sets up general insurance JV with ERGO

2016 Stake sale in the life and general insurance business

2017 Probable merger of HDFC Life and Max Life Insurance to create the largest private life insurer.

Balance Sheet Key rations Year to Mar (̀ mn) FY17E FY18E FY19E

Networth 381,198 423,469 468,264

Borrowings 2,709,086 3,061,268 3,459,232

Total liabilities 3,090,284 3,484,736 3,927,496

Fixed Assets 7,310 8,041 8,845

Loan book 2,951,089 3,339,964 3,782,867

Investments 153,454 153,454 153,454

Net Current assets (21,569) (16,723) (17,670)

Total assets 3,090,284 3,484,736 3,927,496

Networth 381,198 423,469 468,264

Borrowings 2,709,086 3,061,268 3,459,232

Total liabilities 3,090,284 3,484,736 3,927,496

Year to March (̀ mn) FY17E FY18E FY19E

AUM growth (%) 14.1 13.2 13.3

Dil Adjusted EPS growth (%) 6% 6% 6%

Net interest margin (NIM) (%) 3.0 2.7 2.5

Cost to income (%) 7.4 8.1 8.6

Opex (% of AAUM) 0.28 0.28 0.28

Gross NPAs (%) 0.8 0.9 1.1

Credit costs (% of AAUM) 0.22 0.12 0.13

Provisioning Coverage 53.0 53.0 53.0

Capital adequacy (%) 17.0 17.5 17.9

Tier-1 (%) 13.5 13.9 14.2

Leverage (x) 12.4 12.0 11.8

Competitive intensity will pressure HDFC’s NIMs The best of asset quality is behind

Source: Company, Ambit Capital research

2.1% 2.0% 1.9% 1.9%1.6% 1.5%

3.3% 3.2% 3.0% 3.0%2.7% 2.5%

0%

1%

2%

3%

4%

5%

FY14 FY15 FY16 FY17E FY18E FY19E

Spreads (%) NIMs on AUM (%)

0.06% 0.06%0.08%

0.05%0.07%

0.26%

0.22%

0.12% 0.13%

0.0%

0.1%

0.2%

0.3%

FY11

FY12

FY13

FY14

FY15

FY16

FY17

E

FY18

E

FY19

EHDFC - Credit costs (% of AUM)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 3

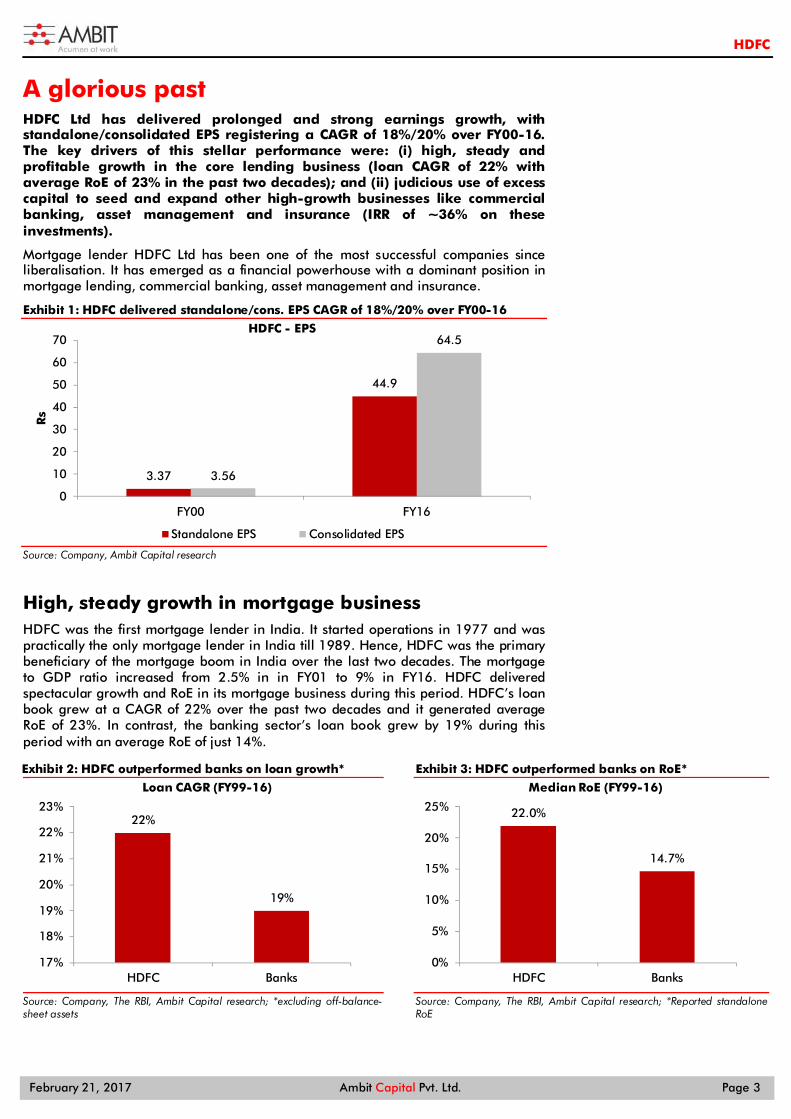

A glorious past HDFC Ltd has delivered prolonged and strong earnings growth, with standalone/consolidated EPS registering a CAGR of 18%/20% over FY00-16. The key drivers of this stellar performance were: (i) high, steady and profitable growth in the core lending business (loan CAGR of 22% with average RoE of 23% in the past two decades); and (ii) judicious use of excess capital to seed and expand other high-growth businesses like commercial banking, asset management and insurance (IRR of ~36% on these investments).

Mortgage lender HDFC Ltd has been one of the most successful companies since liberalisation. It has emerged as a financial powerhouse with a dominant position in mortgage lending, commercial banking, asset management and insurance.

Exhibit 1: HDFC delivered standalone/cons. EPS CAGR of 18%/20% over FY00-16

Source: Company, Ambit Capital research

High, steady growth in mortgage business HDFC was the first mortgage lender in India. It started operations in 1977 and was practically the only mortgage lender in India till 1989. Hence, HDFC was the primary beneficiary of the mortgage boom in India over the last two decades. The mortgage to GDP ratio increased from 2.5% in in FY01 to 9% in FY16. HDFC delivered spectacular growth and RoE in its mortgage business during this period. HDFC’s loan book grew at a CAGR of 22% over the past two decades and it generated average RoE of 23%. In contrast, the banking sector’s loan book grew by 19% during this period with an average RoE of just 14%.

Exhibit 2: HDFC outperformed banks on loan growth*

Source: Company, The RBI, Ambit Capital research; *excluding off-balance-sheet assets

Exhibit 3: HDFC outperformed banks on RoE*

Source: Company, The RBI, Ambit Capital research; *Reported standalone RoE

3.37

44.9

3.56

64.5

0

10

20

30

40

50

60

70

FY00 FY16

Rs

HDFC - EPS

Standalone EPS Consolidated EPS

22%

19%

17%

18%

19%

20%

21%

22%

23%

HDFC Banks

Loan CAGR (FY99-16)

22.0%

14.7%

0%

5%

10%

15%

20%

25%

HDFC Banks

Median RoE (FY99-16)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 4

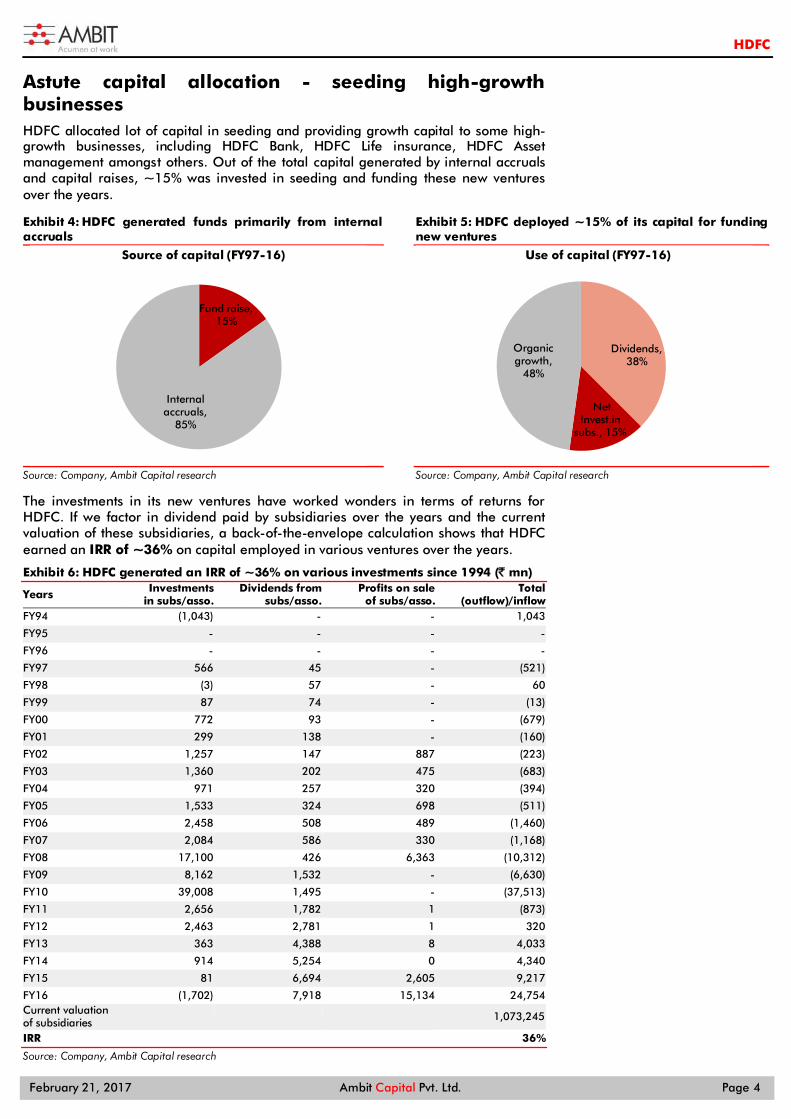

Astute capital allocation - seeding high-growth businesses HDFC allocated lot of capital in seeding and providing growth capital to some high-growth businesses, including HDFC Bank, HDFC Life insurance, HDFC Asset management amongst others. Out of the total capital generated by internal accruals and capital raises, ~15% was invested in seeding and funding these new ventures over the years.

Exhibit 4: HDFC generated funds primarily from internal accruals

Source: Company, Ambit Capital research

Exhibit 5: HDFC deployed ~15% of its capital for funding new ventures

Source: Company, Ambit Capital research

The investments in its new ventures have worked wonders in terms of returns for HDFC. If we factor in dividend paid by subsidiaries over the years and the current valuation of these subsidiaries, a back-of-the-envelope calculation shows that HDFC earned an IRR of ~36% on capital employed in various ventures over the years.

Exhibit 6: HDFC generated an IRR of ~36% on various investments since 1994 (` mn)

Years Investments in subs/asso.

Dividends from subs/asso.

Profits on sale of subs/asso.

Total (outflow)/inflow

FY94 (1,043) - - 1,043

FY95 - - - -

FY96 - - - -

FY97 566 45 - (521)

FY98 (3) 57 - 60

FY99 87 74 - (13)

FY00 772 93 - (679)

FY01 299 138 - (160)

FY02 1,257 147 887 (223)

FY03 1,360 202 475 (683)

FY04 971 257 320 (394)

FY05 1,533 324 698 (511)

FY06 2,458 508 489 (1,460)

FY07 2,084 586 330 (1,168)

FY08 17,100 426 6,363 (10,312)

FY09 8,162 1,532 - (6,630)

FY10 39,008 1,495 - (37,513)

FY11 2,656 1,782 1 (873)

FY12 2,463 2,781 1 320

FY13 363 4,388 8 4,033

FY14 914 5,254 0 4,340

FY15 81 6,694 2,605 9,217

FY16 (1,702) 7,918 15,134 24,754 Current valuation of subsidiaries 1,073,245

IRR 36%

Source: Company, Ambit Capital research

Fund raise, 15%

Internal accruals,

85%

Source of capital (FY97-16)

Dividends, 38%

Net Invest.in

subs., 15%

Organic growth,

48%

Use of capital (FY97-16)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 5

Exhibit 7: HDFC is the strongest large HFC on our IBAS framework

Particulars GRUH HDFC LICHF REPCO CNFIN DHFL PNBHF Comments

Innovation

Innovation in terms of ability to appraise a non-salaried borrower is the key to gain penetration in the under-served low-income segment. HDFC is mediocre on this metric owing to its lower exposure to self-employed borrowers.

Brand

Brand for a home loan borrower will depend on the perceived customer service and the perceived project financing abilities by the lender. HDFC enjoys the best brand amongst the HFCs due to superior perception on the above metrics.

Architecture

A robust branch network with decentralised decision making is the key to gain penetration in small-ticket housing finance. HDFC with ~400 branches and a decentralised decision making has one of the best architectures amongst peers, closely followed by DHFL and GRUH.

Strategic asset

Tie up with associate HDFC Bank, strong credit rating and a granular retail deposit franchise are the key strategic assets for HDFC.

Overall rank

HDFC comes out as one the strongest HFCs versus its peers due to its strengths in brand, architecture and strategic assets.

Source: Company, Ambit Capital research; Note: - Strong; - Relatively Strong; - Average; - Relatively weak.

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 6

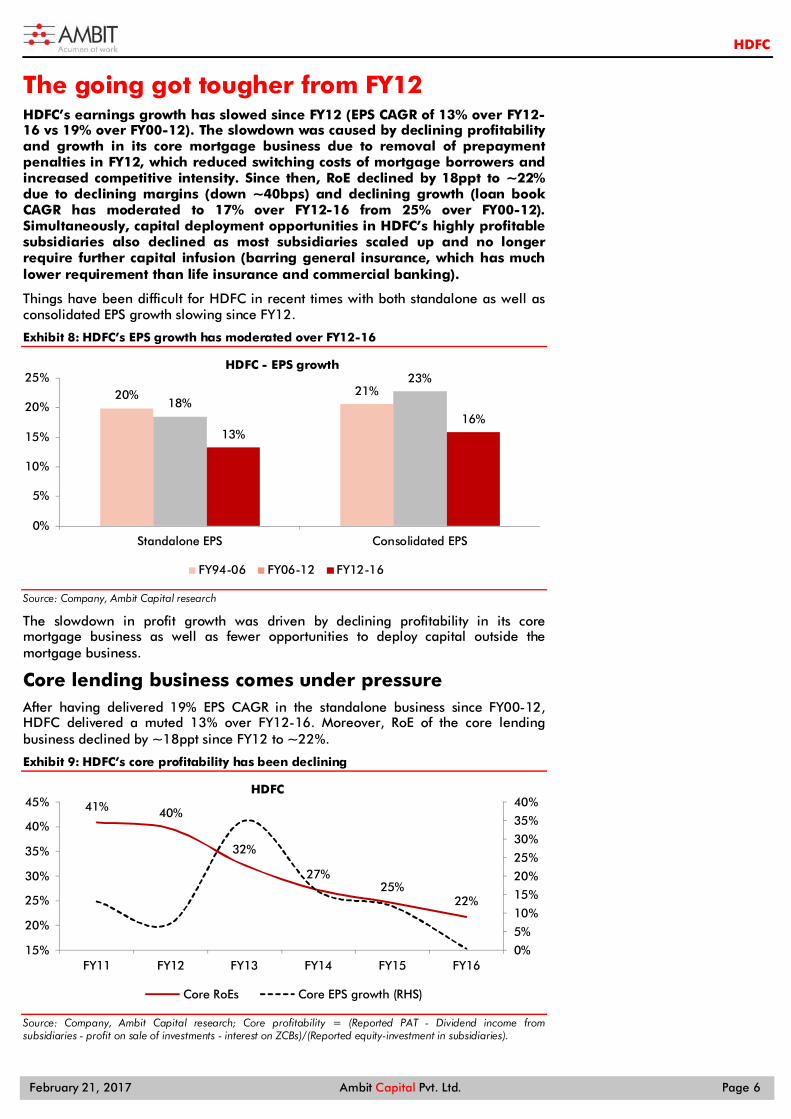

The going got tougher from FY12 HDFC’s earnings growth has slowed since FY12 (EPS CAGR of 13% over FY12-16 vs 19% over FY00-12). The slowdown was caused by declining profitability and growth in its core mortgage business due to removal of prepayment penalties in FY12, which reduced switching costs of mortgage borrowers and increased competitive intensity. Since then, RoE declined by 18ppt to ~22% due to declining margins (down ~40bps) and declining growth (loan book CAGR has moderated to 17% over FY12-16 from 25% over FY00-12). Simultaneously, capital deployment opportunities in HDFC’s highly profitable subsidiaries also declined as most subsidiaries scaled up and no longer require further capital infusion (barring general insurance, which has much lower requirement than life insurance and commercial banking).

Things have been difficult for HDFC in recent times with both standalone as well as consolidated EPS growth slowing since FY12.

Exhibit 8: HDFC’s EPS growth has moderated over FY12-16

Source: Company, Ambit Capital research

The slowdown in profit growth was driven by declining profitability in its core mortgage business as well as fewer opportunities to deploy capital outside the mortgage business.

Core lending business comes under pressure After having delivered 19% EPS CAGR in the standalone business since FY00-12, HDFC delivered a muted 13% over FY12-16. Moreover, RoE of the core lending business declined by ~18ppt since FY12 to ~22%.

Exhibit 9: HDFC’s core profitability has been declining

Source: Company, Ambit Capital research; Core profitability = (Reported PAT - Dividend income from subsidiaries - profit on sale of investments - interest on ZCBs)/(Reported equity-investment in subsidiaries).

20% 21%18%

23%

13%16%

0%

5%

10%

15%

20%

25%

Standalone EPS Consolidated EPS

HDFC - EPS growth

FY94-06 FY06-12 FY12-16

41% 40%

32%

27%25%

22%

0%

5%

10%

15%

20%

25%

30%

35%

40%

15%

20%

25%

30%

35%

40%

45%

FY11 FY12 FY13 FY14 FY15 FY16

HDFC

Core RoEs Core EPS growth (RHS)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 7

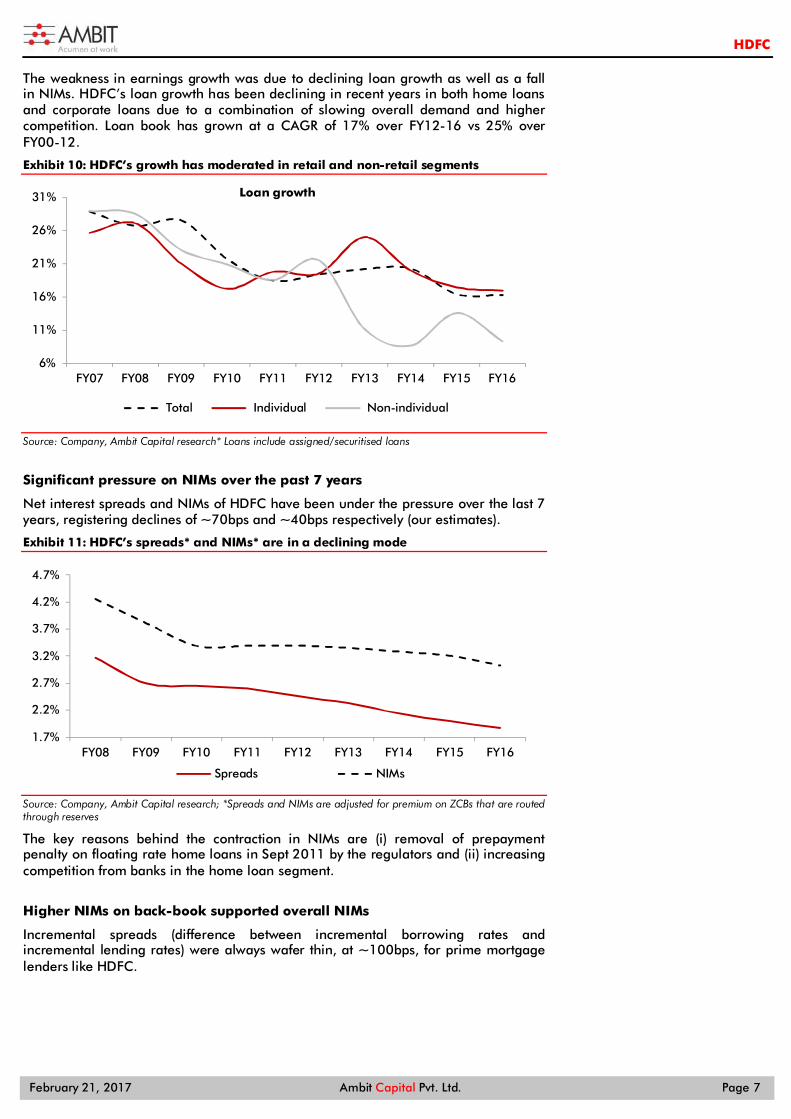

The weakness in earnings growth was due to declining loan growth as well as a fall in NIMs. HDFC’s loan growth has been declining in recent years in both home loans and corporate loans due to a combination of slowing overall demand and higher competition. Loan book has grown at a CAGR of 17% over FY12-16 vs 25% over FY00-12.

Exhibit 10: HDFC’s growth has moderated in retail and non-retail segments

Source: Company, Ambit Capital research* Loans include assigned/securitised loans

Significant pressure on NIMs over the past 7 years

Net interest spreads and NIMs of HDFC have been under the pressure over the last 7 years, registering declines of ~70bps and ~40bps respectively (our estimates).

Exhibit 11: HDFC’s spreads* and NIMs* are in a declining mode

Source: Company, Ambit Capital research; *Spreads and NIMs are adjusted for premium on ZCBs that are routed through reserves

The key reasons behind the contraction in NIMs are (i) removal of prepayment penalty on floating rate home loans in Sept 2011 by the regulators and (ii) increasing competition from banks in the home loan segment.

Higher NIMs on back-book supported overall NIMs

Incremental spreads (difference between incremental borrowing rates and incremental lending rates) were always wafer thin, at ~100bps, for prime mortgage lenders like HDFC.

6%

11%

16%

21%

26%

31%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Loan growth

Total Individual Non-individual

1.7%

2.2%

2.7%

3.2%

3.7%

4.2%

4.7%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Spreads NIMs

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 8

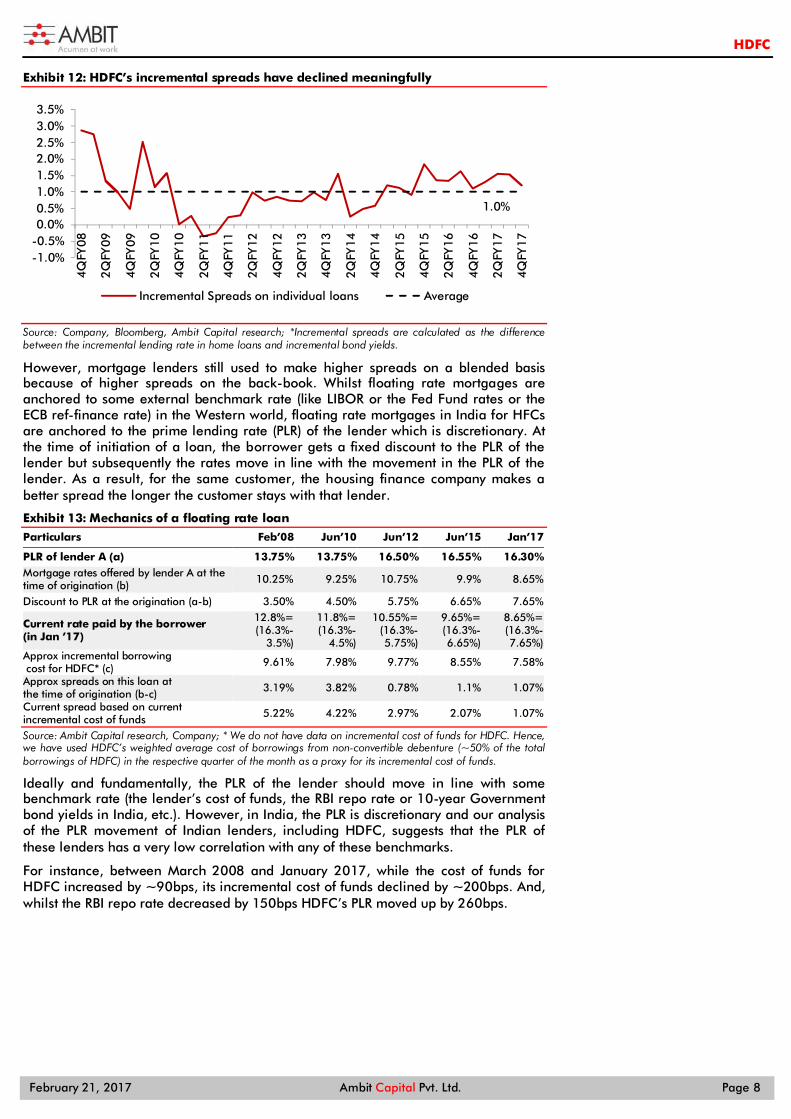

Exhibit 12: HDFC’s incremental spreads have declined meaningfully

Source: Company, Bloomberg, Ambit Capital research; *Incremental spreads are calculated as the difference between the incremental lending rate in home loans and incremental bond yields.

However, mortgage lenders still used to make higher spreads on a blended basis because of higher spreads on the back-book. Whilst floating rate mortgages are anchored to some external benchmark rate (like LIBOR or the Fed Fund rates or the ECB ref-finance rate) in the Western world, floating rate mortgages in India for HFCs are anchored to the prime lending rate (PLR) of the lender which is discretionary. At the time of initiation of a loan, the borrower gets a fixed discount to the PLR of the lender but subsequently the rates move in line with the movement in the PLR of the lender. As a result, for the same customer, the housing finance company makes a better spread the longer the customer stays with that lender.

Exhibit 13: Mechanics of a floating rate loan

Particulars Feb’08 Jun’10 Jun’12 Jun’15 Jan’17

PLR of lender A (a) 13.75% 13.75% 16.50% 16.55% 16.30% Mortgage rates offered by lender A at the time of origination (b) 10.25% 9.25% 10.75% 9.9% 8.65%

Discount to PLR at the origination (a-b) 3.50% 4.50% 5.75% 6.65% 7.65%

Current rate paid by the borrower (in Jan ’17)

12.8%= (16.3%-

3.5%)

11.8%= (16.3%-

4.5%)

10.55%= (16.3%-5.75%)

9.65%= (16.3%-6.65%)

8.65%= (16.3%-7.65%)

Approx incremental borrowing cost for HDFC* (c) 9.61% 7.98% 9.77% 8.55% 7.58%

Approx spreads on this loan at the time of origination (b-c) 3.19% 3.82% 0.78% 1.1% 1.07%

Current spread based on current incremental cost of funds 5.22% 4.22% 2.97% 2.07% 1.07%

Source: Ambit Capital research, Company; * We do not have data on incremental cost of funds for HDFC. Hence, we have used HDFC’s weighted average cost of borrowings from non-convertible debenture (~50% of the total borrowings of HDFC) in the respective quarter of the month as a proxy for its incremental cost of funds.

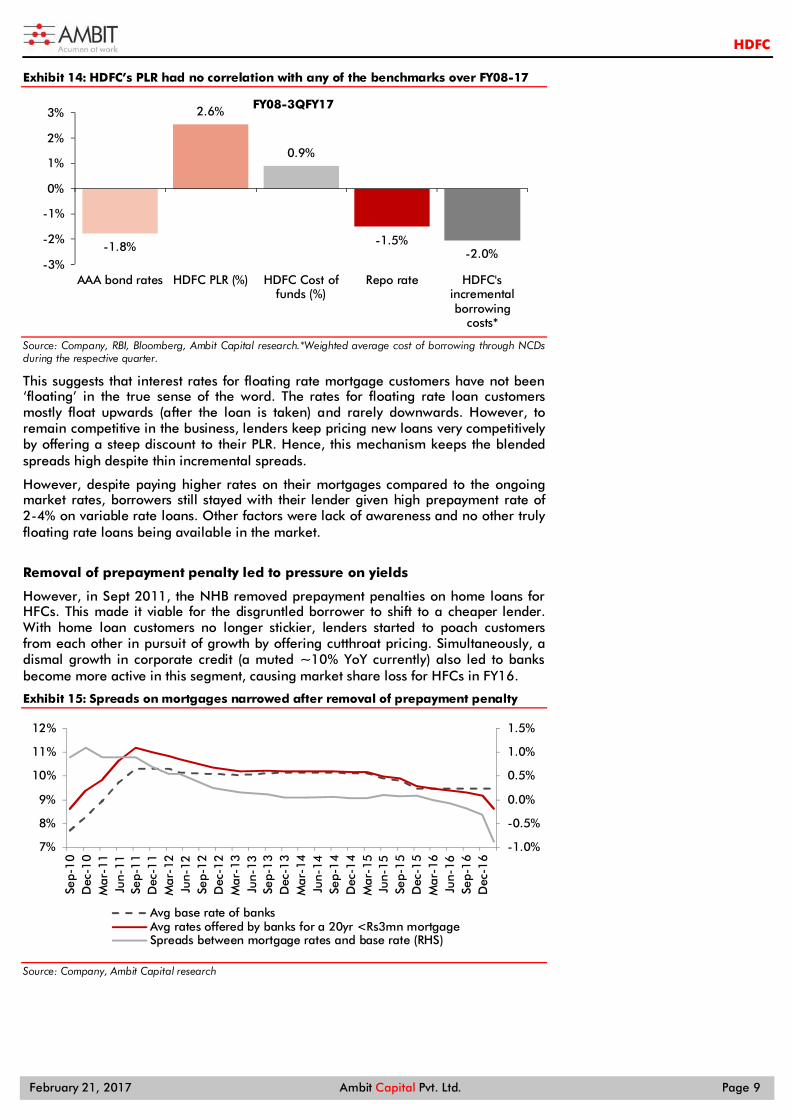

Ideally and fundamentally, the PLR of the lender should move in line with some benchmark rate (the lender’s cost of funds, the RBI repo rate or 10-year Government bond yields in India, etc.). However, in India, the PLR is discretionary and our analysis of the PLR movement of Indian lenders, including HDFC, suggests that the PLR of these lenders has a very low correlation with any of these benchmarks.

For instance, between March 2008 and January 2017, while the cost of funds for HDFC increased by ~90bps, its incremental cost of funds declined by ~200bps. And, whilst the RBI repo rate decreased by 150bps HDFC’s PLR moved up by 260bps.

1.0%

-1.0%-0.5%0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%

4QFY

08

2QFY

09

4QFY

09

2QFY

10

4QFY

10

2QFY

11

4QFY

11

2QFY

12

4QFY

12

2QFY

13

4QFY

13

2QFY

14

4QFY

14

2QFY

15

4QFY

15

2QFY

16

4QFY

16

2QFY

17

4QFY

17

Incremental Spreads on individual loans Average

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 9

Exhibit 14: HDFC’s PLR had no correlation with any of the benchmarks over FY08-17

Source: Company, RBI, Bloomberg, Ambit Capital research.*Weighted average cost of borrowing through NCDs during the respective quarter.

This suggests that interest rates for floating rate mortgage customers have not been ‘floating’ in the true sense of the word. The rates for floating rate loan customers mostly float upwards (after the loan is taken) and rarely downwards. However, to remain competitive in the business, lenders keep pricing new loans very competitively by offering a steep discount to their PLR. Hence, this mechanism keeps the blended spreads high despite thin incremental spreads.

However, despite paying higher rates on their mortgages compared to the ongoing market rates, borrowers still stayed with their lender given high prepayment rate of 2-4% on variable rate loans. Other factors were lack of awareness and no other truly floating rate loans being available in the market.

Removal of prepayment penalty led to pressure on yields

However, in Sept 2011, the NHB removed prepayment penalties on home loans for HFCs. This made it viable for the disgruntled borrower to shift to a cheaper lender. With home loan customers no longer stickier, lenders started to poach customers from each other in pursuit of growth by offering cutthroat pricing. Simultaneously, a dismal growth in corporate credit (a muted ~10% YoY currently) also led to banks become more active in this segment, causing market share loss for HFCs in FY16.

Exhibit 15: Spreads on mortgages narrowed after removal of prepayment penalty

Source: Company, Ambit Capital research

-1.8%

2.6%

0.9%

-1.5%-2.0%

-3%

-2%

-1%

0%

1%

2%

3%

AAA bond rates HDFC PLR (%) HDFC Cost offunds (%)

Repo rate HDFC'sincrementalborrowing

costs*

FY08-3QFY17

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

7%

8%

9%

10%

11%

12%

Sep-

10

Dec

-10

Mar

-11

Jun-

11Se

p-1

1D

ec-1

1M

ar-1

2Ju

n-12

Sep-

12

Dec

-12

Mar

-13

Jun-

13Se

p-1

3D

ec-1

3M

ar-1

4Ju

n-14

Sep-

14

Dec

-14

Mar

-15

Jun-

15Se

p-1

5D

ec-1

5M

ar-1

6Ju

n-16

Sep-

16

Dec

-16

Avg base rate of banksAvg rates offered by banks for a 20yr <Rs3mn mortgageSpreads between mortgage rates and base rate (RHS)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 10

Exhibit 16: Banks growth rate has picked up in home loans in recent years with growth rate slowing down for HDFC

Source: RBI, Company, Ambit Capital research

The increased competition resulted in not only lower yields for HDFC but also increased prepayments. So, loan growth and margins have declined meaningfully since FY11.

Exhibit 17: HDFC’s repayment rates have structurally risen due to increasing competition

Source: Company, Ambit Capital research; *for overall book (including developer loans). *Repayment rate is calculated as ((Loan book year 1 – Loan book year 2 + disbursements)/ Loan book year 1).

Reinvestment opportunities have declined Declining growth and profitability in HDFC’s core mortgage business has also coincided with declining opportunities of capital deployment in its highly profitable subsidiaries. This is because its subsidiaries barring the general insurance business have scaled up and are profitable now and no longer require further capital infusion from HDFC. In general insurance, too, the requirement seems to be lower than for businesses like life insurance and commercial banking.

Exhibit 18: HDFC’s subsidiaries are now profitable and don’t need external capital infusion

RoE FY14 FY15 FY16 Capital infusion requirement

HDFC Bank 21.3% 19.4% 18.3% Its TTM loan book growth has slowed down to 21%, broadly in line with RoE. It can sustain growth through internal accruals.

GRUH Fin Ltd. 32.2% 30.9% 31.5% Its TTM loan book growth has slowed down to 22%, lower than RoE. It can sustain growth through internal accruals.

HDFC Std Life Ins. 44.7% 35.1% 28.7% Its solvency ratio is at 209% versus the regulatory requirement of 150%. It can sustain growth through internal accruals.

HDFC ERGO Gen Ins Co. 24.4% 11.1% 14.6% Its solvency ratio is at 152% versus the regulatory requirement of 150%. It needs capital.

HDFC AMC 44.6% 41.1% 42.1% It is a cash rich business and it doesn’t require capital.

Source: Company, Ambit Capital research

0%

5%

10%

15%

20%

25%

30%

35%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

YoY growth - Retail home loans

Banks

HDFC

0%5%

10%15%20%25%30%35%40%45%50%

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

Repayment rate* (HDFC)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 11

The decrease in investment opportunities outside the mortgage business is also reflected in the decline in investments in associates/subsidiaries as a percentage of shareholder equity in recent times.

Exhibit 19: HDFC’s declining investments

Source: Company, Ambit Capital research

20%23% 22% 25%

29%

50%46%

43%

33%30%

27%24%

0%

10%

20%

30%

40%

50%

60%

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Investments in asso./subs (% of networth)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 12

RoE/growth of mortgage business waning HDFC’s growth would moderate to 14% CAGR over FY16-19E from 19% over FY11-16, given: (i) slowing of ticket size growth (contributing 60% of total growth) as real estate prices moderate and (ii) increasing competition not only in home loans but also in construction financing and lease rental discounting (challengers like Indiabulls Housing Finance, Piramal Enterprises and PNBHF). Profitability faces challenges from a further decline in NIMs (down ~50bps over FY16-19E) as well as deterioration in asset quality (credit costs to remain elevated at 12-13bps over FY16-19E vs ~6bps over FY11-15). NIMs face risks of structural decline as blended spreads on individual loans (~140bps) converge towards incremental spreads (~120bps), lack of room to increase cheaper bond borrowings (~56% now) and tightening of loose regulations (introduction of base rates etc.) on loan pricing. Notwithstanding prudent underwriting, asset quality could worsen from peak levels given increasing risks of low borrower equity and a high proportion of under-construction homes.

Though NIMs and growth in the lending business have been declining since FY11, we expect further pressure on growth and NIMs, resulting in a decline in core mortgage business RoE to 18% by FY19 from 22% in FY16.

Growth to remain muted HDFC’s AUM growth would remain muted. We expect it to decline to 14% CAGR over FY16-19E from 19% over FY12-16 driven by following factors:

1. Declining growth in ticket size

Increasing real estate price has been a major driver of high growth in the mortgage segment over the last 7-8 years with ticket sizes contributing as much as 50-60% of growth of the lenders.

Exhibit 20: Increasing real estate prices have driven loan growth

CAGR

Loans No. of Customers

Avg. Ticket size

Time period

HDFC 19% 7% 11% FY08-16

LICHF 21% 8% 13% FY08-16

Source: Company, Ambit Capital research

However, demonetisation is expected to bring down real estate prices as real estate has been a safe haven for black money (cash transactions account for 30-40% of transactions). With the system being short of cash than earlier levels, liquidity in the real estate market is expected to be sucked out and prices are expected to decline. Moreover, the Government’s crusade against black money is not going to halt just at demonetisation. With the amendments to the Benami Property law expected to be operational soon, there are expectations that real estate holdings of individuals in the country would also be digitised to identify ‘Benami properties’ bought against unexplained income. This would not only lead to a further decline in real estate prices but also in lower transactions, resulting in declining growth for mortgage lenders both in terms of number of customers and average ticket sizes.

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 13

2. Declining investor demand

A rapid increase in real estate prices since 2006 led to increased investor participation in home purchase for quick gains. This was evident in the rising number of vacant homes, which accounted for 20% of the incremental housing stock over FY01-11 versus 10% in FY91-01. However, investor participation is expected to decline as:

Real estate has delivered lacklustre returns of late versus other asset classes. This has resulted in dwindling interest amongst investors.

There is less demand to hide black money with most of it sucked out of the system owing to the demonetisation. Hence, the “safe haven” demand for real estate has deteriorated.

One of the key reasons of real estate’s popularity as an investment tool was tax savings as interest on home loans could be fully expensed if the home is classified as a let-out property. The budget has proposed to restrict the loss from let-out house property to `200,000 (versus no limit earlier). This could increase the interest burden (net of tax shield) and cost of holding of the investors by up to 33%, especially for home loans where ticket sizes are over `2mn. Consequently, investor demand is expected to further dwindle for larger-ticket homes (>`2.5mn). With ~50% of HFC disbursements for loans exceeding `2.5mn and HDFC being a market leader amongst HFCs, loan book growth should be affected by the potential decline investor demand.

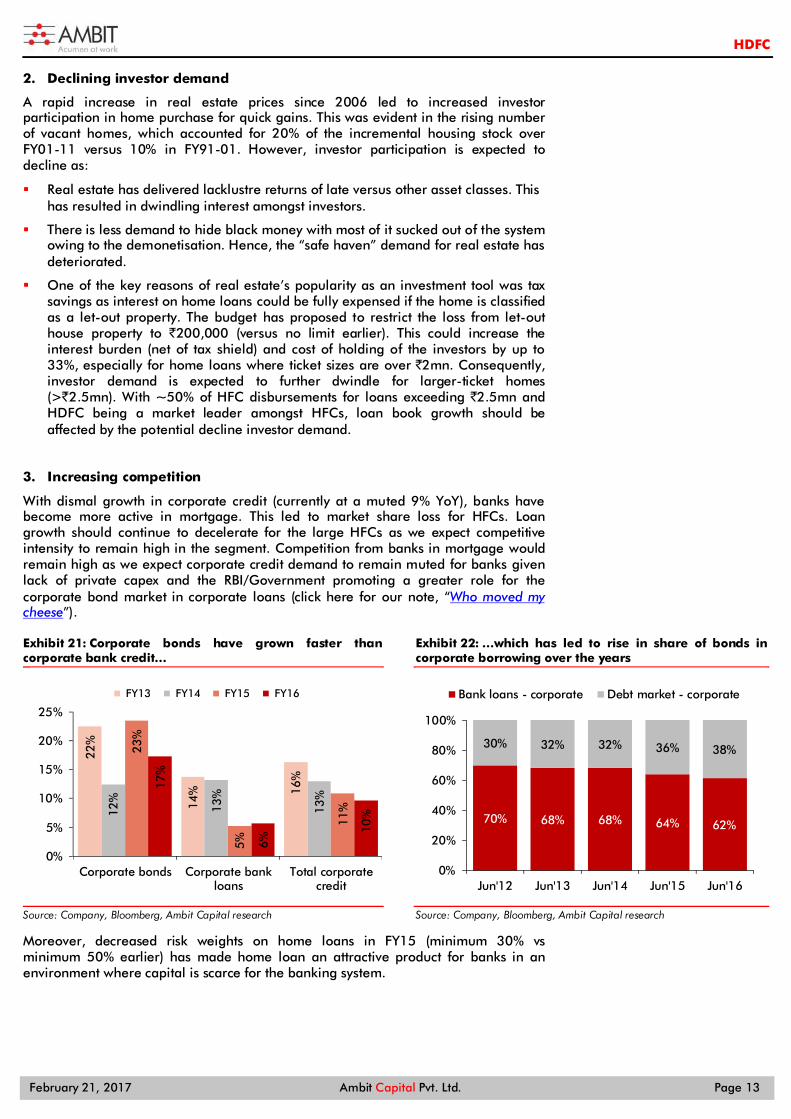

3. Increasing competition

With dismal growth in corporate credit (currently at a muted 9% YoY), banks have become more active in mortgage. This led to market share loss for HFCs. Loan growth should continue to decelerate for the large HFCs as we expect competitive intensity to remain high in the segment. Competition from banks in mortgage would remain high as we expect corporate credit demand to remain muted for banks given lack of private capex and the RBI/Government promoting a greater role for the corporate bond market in corporate loans (click here for our note, “Who moved my cheese”).

Exhibit 21: Corporate bonds have grown faster than corporate bank credit…

Source: Company, Bloomberg, Ambit Capital research

Exhibit 22: …which has led to rise in share of bonds in corporate borrowing over the years

Source: Company, Bloomberg, Ambit Capital research

Moreover, decreased risk weights on home loans in FY15 (minimum 30% vs minimum 50% earlier) has made home loan an attractive product for banks in an environment where capital is scarce for the banking system.

22%

14% 16

%

12%

13%

13%

23%

5%

11%

17%

6%

10%

0%

5%

10%

15%

20%

25%

Corporate bonds Corporate bankloans

Total corporatecredit

FY13 FY14 FY15 FY16

70% 68% 68% 64% 62%

30% 32% 32% 36% 38%

0%

20%

40%

60%

80%

100%

Jun'12 Jun'13 Jun'14 Jun'15 Jun'16

Bank loans - corporate Debt market - corporate

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 14

Exhibit 23: Home loans provide higher profitability for banks due to higher leverage

FY16 Bank – Corp. loans

Bank – Home loans

HFC – Home loans

Yield on loans 9.0% 9.0% 9.7%

Cost of funds 5.4% 5.7% 6.9%

- Liability cost 5.0% 5.3% 6.9%

- Regulatory cost 0.38% 0.40% 0.02%

NIM 3.6% 3.3% 2.7%

Other income 0.6% 0.5% 0.1%

Total income 4.2% 3.8% 2.9%

Opex 1.0% 1.3% 0.3%

PPOP 3.2% 2.5% 2.6%

Credit costs 1.0% 0.5% 0.2%

PBT 2.2% 2.0% 2.4%

Tax 0.7% 0.7% 0.8%

RoA 1.5% 1.3% 1.6%

Leverage 11 27 12.7

RoE 16% 36% 20%

Cost of liabilities FDs 7.0% 7.0% 7.5%

CASA 3.0% 3.0% NA

Bonds 7.5% 7.5% 7.5%

Incremental liability mix FDs 48.3% 48.3% 30.0%

CASA 38.7% 38.7% NA

Bonds 13.0% 13.0% 70.0%

Regulatory cost* 0.42% 0.42% 0.02%

Source: Ambit Capital research; * Regulatory cost includes cost of CRR/SLR and PSL carry.

Moreover, even within HFCs, competition is increasing with many new players like CANFIN Homes, PNB Housing Finance and Indiabulls emerging as competitors for HDFC (apart from LIC Housing). Increasing regulatory thrust on housing finance has meant that NHB has also been giving out more licenses. For e.g., the number of HFCs operating in affordable housing finance is up from 43 in 2009 to 71 in 2016.

Exhibit 24: Competition has grown faster than HDFC in core home loans segment

Source: Company, Ambit Capital research; * We have used overall loan book growth as proxy of growth in non-retail loan book for PNBHF due to lack of data availability.

4. No more the sole tapper of bond markets

Historically, HDFC’s key competitive advantage over other HFCs was its ability to source low-cost funds by tapping the bond markets. However, with more HFCs now able to source funds from bond markets due to regulatory relaxations, smaller HFCs ability to compete with HDFC in its core salary home loan market has significantly increased.

0%

10%

20%

30%

40%

50%

60%

70%

80%

HDFC LICHF IBULL PNBHF DEWAN REPCO CANFIN

FY12

FY13

FY14

FY15

FY16

3Q17

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 15

Exhibit 25: Other HFCs have scaled up non-bank borrowings more rapidly than HDFC

Source: Company, Ambit Capital research

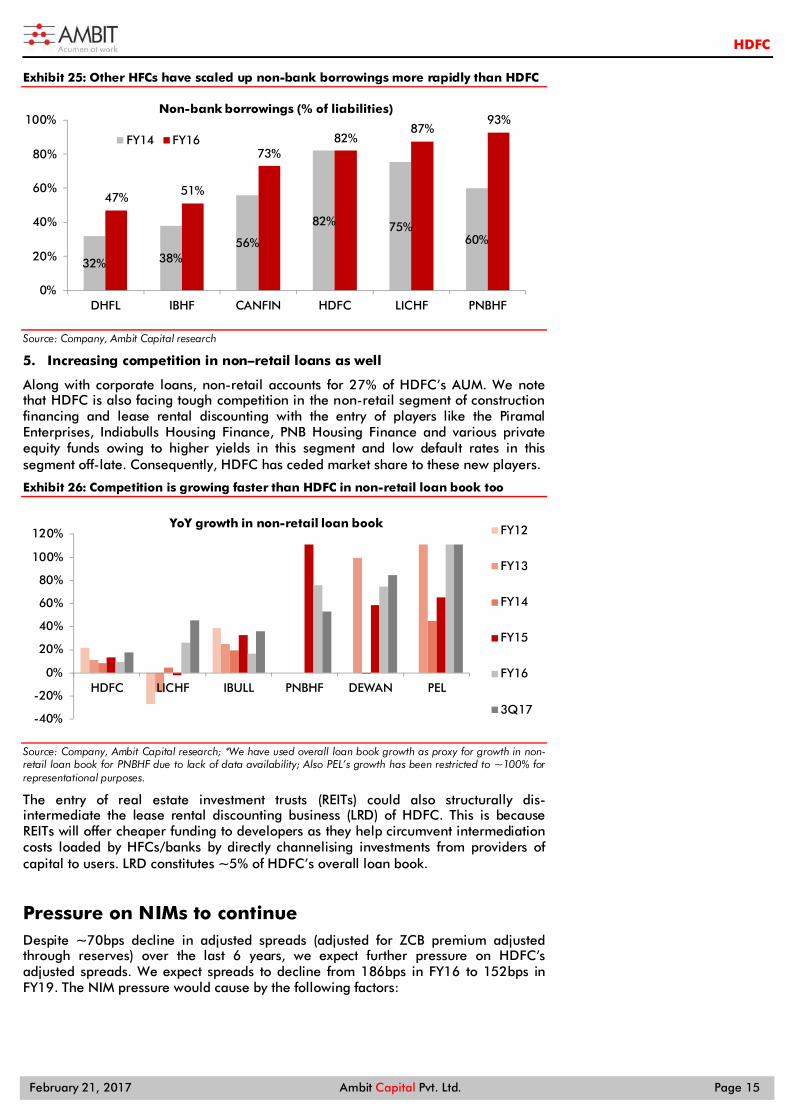

5. Increasing competition in non–retail loans as well

Along with corporate loans, non-retail accounts for 27% of HDFC’s AUM. We note that HDFC is also facing tough competition in the non-retail segment of construction financing and lease rental discounting with the entry of players like the Piramal Enterprises, Indiabulls Housing Finance, PNB Housing Finance and various private equity funds owing to higher yields in this segment and low default rates in this segment off-late. Consequently, HDFC has ceded market share to these new players.

Exhibit 26: Competition is growing faster than HDFC in non-retail loan book too

Source: Company, Ambit Capital research; *We have used overall loan book growth as proxy for growth in non-retail loan book for PNBHF due to lack of data availability; Also PEL’s growth has been restricted to ~100% for representational purposes.

The entry of real estate investment trusts (REITs) could also structurally dis-intermediate the lease rental discounting business (LRD) of HDFC. This is because REITs will offer cheaper funding to developers as they help circumvent intermediation costs loaded by HFCs/banks by directly channelising investments from providers of capital to users. LRD constitutes ~5% of HDFC’s overall loan book.

Pressure on NIMs to continue Despite ~70bps decline in adjusted spreads (adjusted for ZCB premium adjusted through reserves) over the last 6 years, we expect further pressure on HDFC’s adjusted spreads. We expect spreads to decline from 186bps in FY16 to 152bps in FY19. The NIM pressure would cause by the following factors:

32% 38%56%

82% 75%60%

47% 51%

73%82%

87%93%

0%

20%

40%

60%

80%

100%

DHFL IBHF CANFIN HDFC LICHF PNBHF

Non-bank borrowings (% of liabilities)

FY14 FY16

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

HDFC LICHF IBULL PNBHF DEWAN PEL

YoY growth in non-retail loan book FY12

FY13

FY14

FY15

FY16

3Q17

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 16

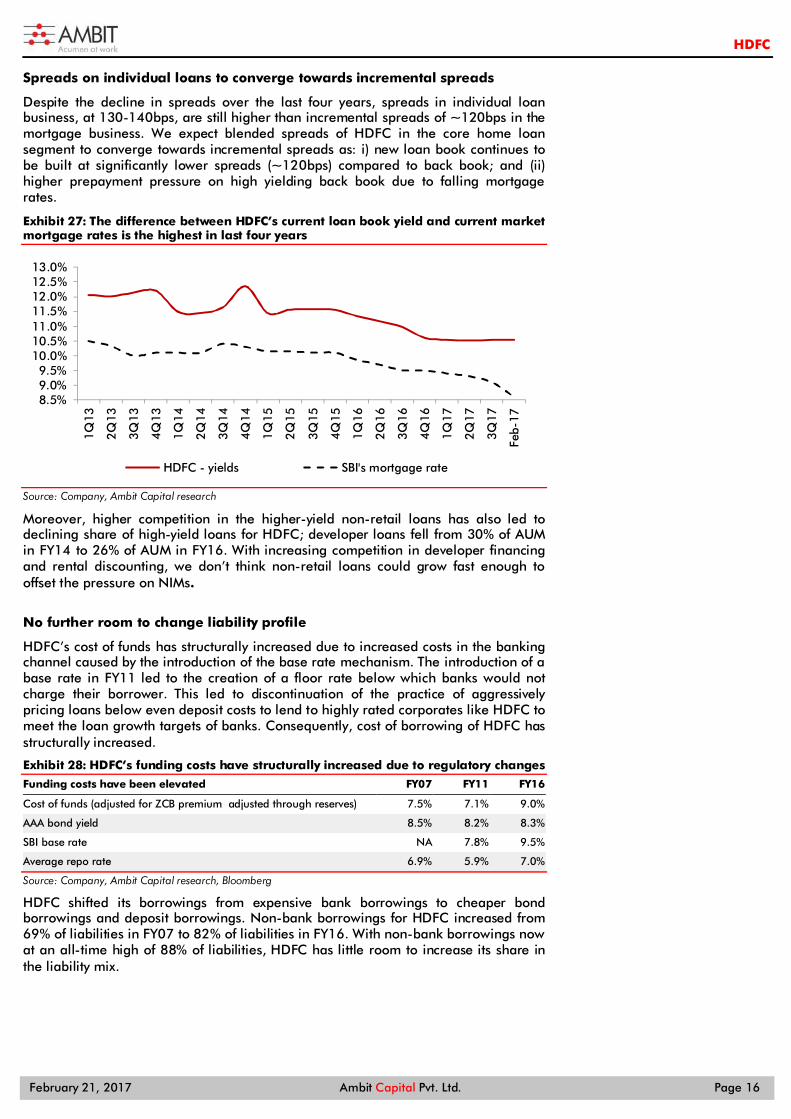

Spreads on individual loans to converge towards incremental spreads

Despite the decline in spreads over the last four years, spreads in individual loan business, at 130-140bps, are still higher than incremental spreads of ~120bps in the mortgage business. We expect blended spreads of HDFC in the core home loan segment to converge towards incremental spreads as: i) new loan book continues to be built at significantly lower spreads (~120bps) compared to back book; and (ii) higher prepayment pressure on high yielding back book due to falling mortgage rates.

Exhibit 27: The difference between HDFC’s current loan book yield and current market mortgage rates is the highest in last four years

Source: Company, Ambit Capital research

Moreover, higher competition in the higher-yield non-retail loans has also led to declining share of high-yield loans for HDFC; developer loans fell from 30% of AUM in FY14 to 26% of AUM in FY16. With increasing competition in developer financing and rental discounting, we don’t think non-retail loans could grow fast enough to offset the pressure on NIMs.

No further room to change liability profile

HDFC’s cost of funds has structurally increased due to increased costs in the banking channel caused by the introduction of the base rate mechanism. The introduction of a base rate in FY11 led to the creation of a floor rate below which banks would not charge their borrower. This led to discontinuation of the practice of aggressively pricing loans below even deposit costs to lend to highly rated corporates like HDFC to meet the loan growth targets of banks. Consequently, cost of borrowing of HDFC has structurally increased.

Exhibit 28: HDFC’s funding costs have structurally increased due to regulatory changes

Funding costs have been elevated FY07 FY11 FY16

Cost of funds (adjusted for ZCB premium adjusted through reserves) 7.5% 7.1% 9.0%

AAA bond yield 8.5% 8.2% 8.3%

SBI base rate NA 7.8% 9.5%

Average repo rate 6.9% 5.9% 7.0%

Source: Company, Ambit Capital research, Bloomberg

HDFC shifted its borrowings from expensive bank borrowings to cheaper bond borrowings and deposit borrowings. Non-bank borrowings for HDFC increased from 69% of liabilities in FY07 to 82% of liabilities in FY16. With non-bank borrowings now at an all-time high of 88% of liabilities, HDFC has little room to increase its share in the liability mix.

8.5%9.0%9.5%

10.0%10.5%11.0%11.5%12.0%12.5%13.0%

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

Feb-

17

HDFC - yields SBI's mortgage rate

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 17

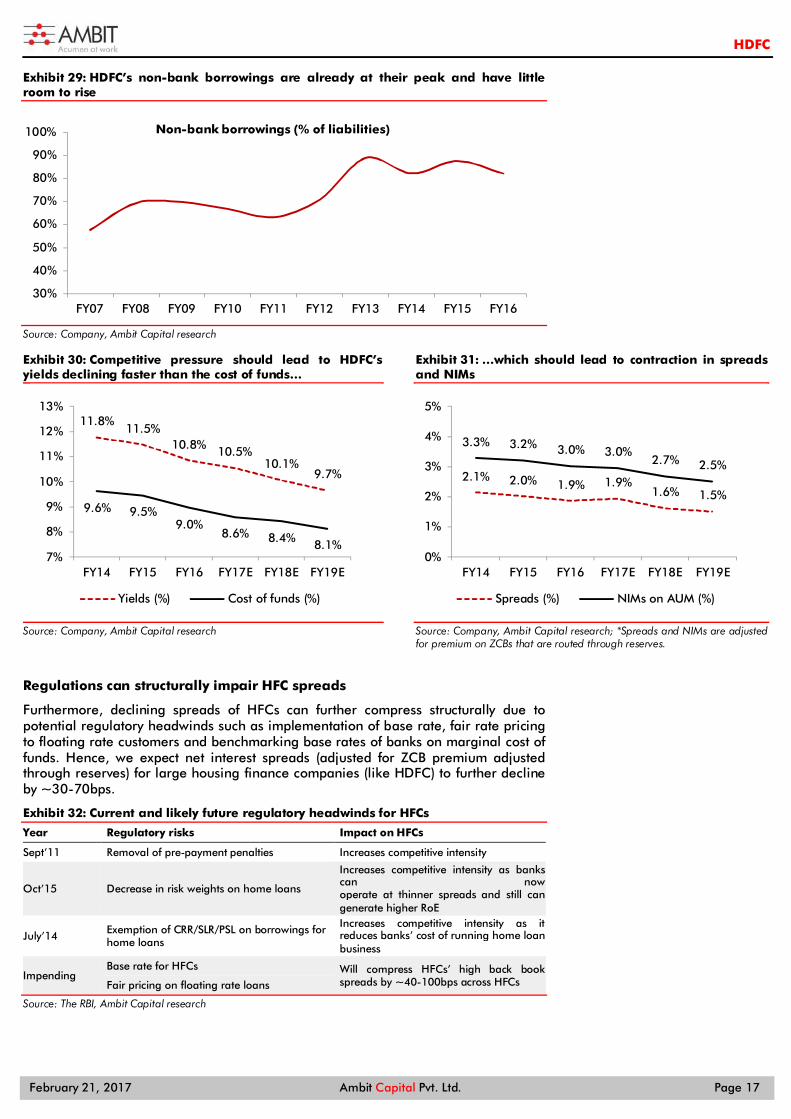

Exhibit 29: HDFC’s non-bank borrowings are already at their peak and have little room to rise

Source: Company, Ambit Capital research

Exhibit 30: Competitive pressure should lead to HDFC’s yields declining faster than the cost of funds…

Source: Company, Ambit Capital research

Exhibit 31: …which should lead to contraction in spreads and NIMs

Source: Company, Ambit Capital research; *Spreads and NIMs are adjusted for premium on ZCBs that are routed through reserves.

Regulations can structurally impair HFC spreads

Furthermore, declining spreads of HFCs can further compress structurally due to potential regulatory headwinds such as implementation of base rate, fair rate pricing to floating rate customers and benchmarking base rates of banks on marginal cost of funds. Hence, we expect net interest spreads (adjusted for ZCB premium adjusted through reserves) for large housing finance companies (like HDFC) to further decline by ~30-70bps.

Exhibit 32: Current and likely future regulatory headwinds for HFCs

Year Regulatory risks Impact on HFCs

Sept’11 Removal of pre-payment penalties Increases competitive intensity

Oct’15 Decrease in risk weights on home loans

Increases competitive intensity as banks can now operate at thinner spreads and still can generate higher RoE

July’14 Exemption of CRR/SLR/PSL on borrowings for home loans

Increases competitive intensity as it reduces banks’ cost of running home loan business

Impending Base rate for HFCs Will compress HFCs’ high back book

spreads by ~40-100bps across HFCs Fair pricing on floating rate loans

Source: The RBI, Ambit Capital research

30%

40%

50%

60%

70%

80%

90%

100%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Non-bank borrowings (% of liabilities)

11.8%11.5%

10.8% 10.5%10.1%

9.7%

9.6% 9.5%9.0%

8.6% 8.4% 8.1%7%

8%

9%

10%

11%

12%

13%

FY14 FY15 FY16 FY17E FY18E FY19E

Yields (%) Cost of funds (%)

2.1% 2.0% 1.9% 1.9%1.6% 1.5%

3.3% 3.2% 3.0% 3.0%2.7% 2.5%

0%

1%

2%

3%

4%

5%

FY14 FY15 FY16 FY17E FY18E FY19E

Spreads (%) NIMs on AUM (%)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 18

Asset quality pressure could emerge As highlighted in our thematic note dated 18th January (HFCs: Past perfect, Future tense, click here for the link), HFCs face increasing risks in their loan books due to lower borrower equity and higher borrower risk profile in an environment of declining real estate prices. We assess risks in the loan book of HFCs based on: i) high share of builder loans; ii) high share of LAP, especially the high-ticket segments; iii) high share of under-construction homes (excluding self-construction); iv) low seasoning of the book; v) low provisioning coverage; and vi) high share of non-salaried borrowers. Our assessment indicates that HDFC stands in the middle rung in the framework owing to:

A very high share of builder and corporate loans, at 27% of loan book;

Undisclosed share of under-construction loans in its book; which could be high. This is because of 72% of disbursements of HFCs are for acquisition/construction of new homes and HDFC is the market leader amongst HFCs;

Relatively high share of recent disbursements in loan book (72% of AUM).

Exhibit 33: HDFC’s high share of builder loans, undisclosed share of under-construction homes and recent disbursements are a cause of worry Particulars HDFC LICHF IBULL PNBHF DHFL GRUH REPCO CNFIN

Builder/corp. loans (% of AUM) 27% 3% 29% 9% 8% 3% 0% 0%

LAP loans (% of AUM) 4% 9% 37% 26% 16% 11% 20% 6%

LAP (ATS, ` mn) NA 1.9 7.3 5.6 2.5 0.8 2.3 1.3

Under-construction (% of HL) NA 65% 35% 37% 12% 2% 15% 4%

Recent disb (% of AUM) 74% 53% 76% 88% 63% 63% 65% 68%

Provisioning coverage (%) 74% 47% 71% 36% 41% 71% 64% 100%

Non-sal. borrowers (% of HL) 15% 16% 30% 39% 45% 36% 49% 16%

Source: Company, Ambit capital research

Exhibit 34: HDFC is placed in the middle rung in terms of asset quality

Metrics HDFC LICHF IBULL PNBHF DEWAN GRUH REPCO CANFIN

Builder loans

LAP

Under-construction

Recent disb (% of AUM)

Provisioning coverage (%)

Non-salaried borrowers

Aggregate

Source: Company, Ambit capital research. Note: - Strong; - Relatively Strong; - Average;

- Relatively weak

The increasing risks for HDFC are also reflected in its increasing NPAs and credit costs. Consequently, the best in asset quality for HDFC is definitely behind. We expect gross NPAs for HDFC to increase by ~38bps and credit costs to remain elevated at 12-13bps over FY18-19E. Note that HDFC is carrying excess provisions of ~`10bn on its balance sheet, which can be used to provide for increasing gross NPAs. Should HDFC decide to use such provisions, its credit costs may not rise proportionately with gross NPAs over FY18-19E.

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 19

Exhibit 35: HDFC’s gross NPA growth YoY is showing an uptrend

Source: Company, Ambit capital research

Exhibit 36: HDFC’s credit cost has increased from lows and should remain elevated

Source: Company, Ambit capital research

-40%

-20%

0%

20%

40%

60%

80%

100%

HDFC LICHF REPCO GRUH CANFIN IBULLS DEWAN PNBHF

FY12

FY13

FY14

FY15

FY16

0.06% 0.06%0.08%

0.05%0.07%

0.26%

0.22%

0.12% 0.13%

0.00%

0.10%

0.20%

0.30%

0.40%

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

HDFC credit costs (% of AUM)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 20

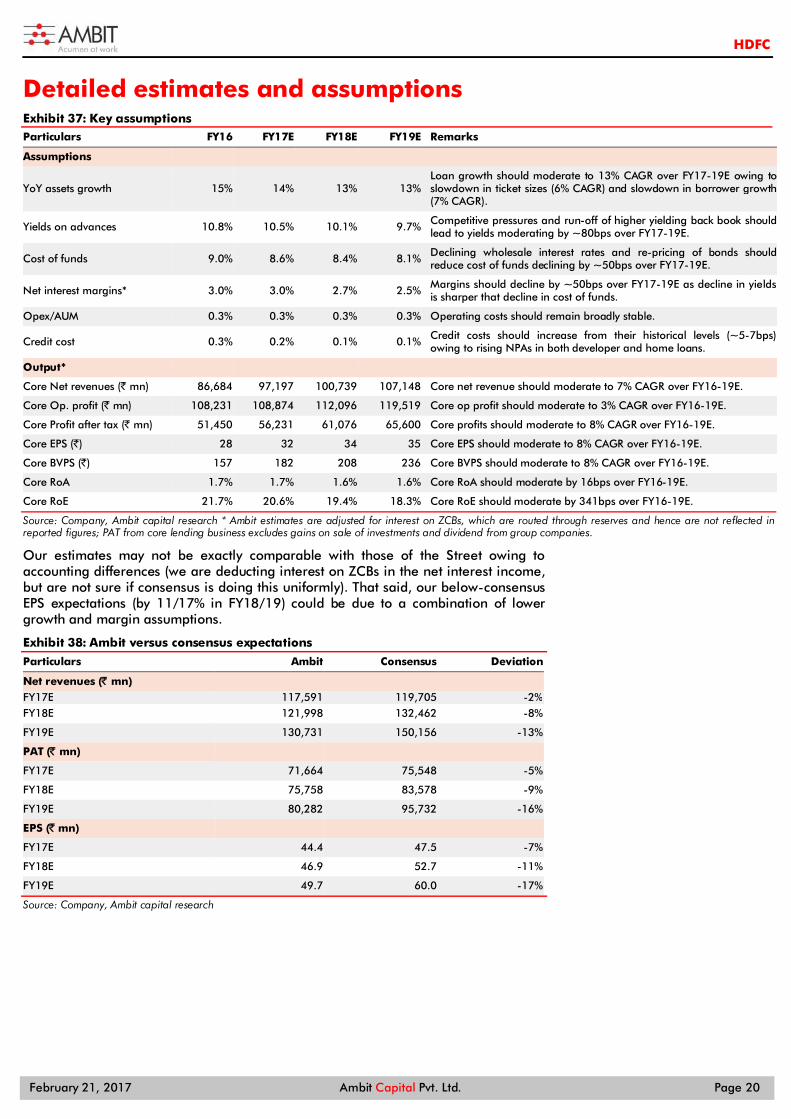

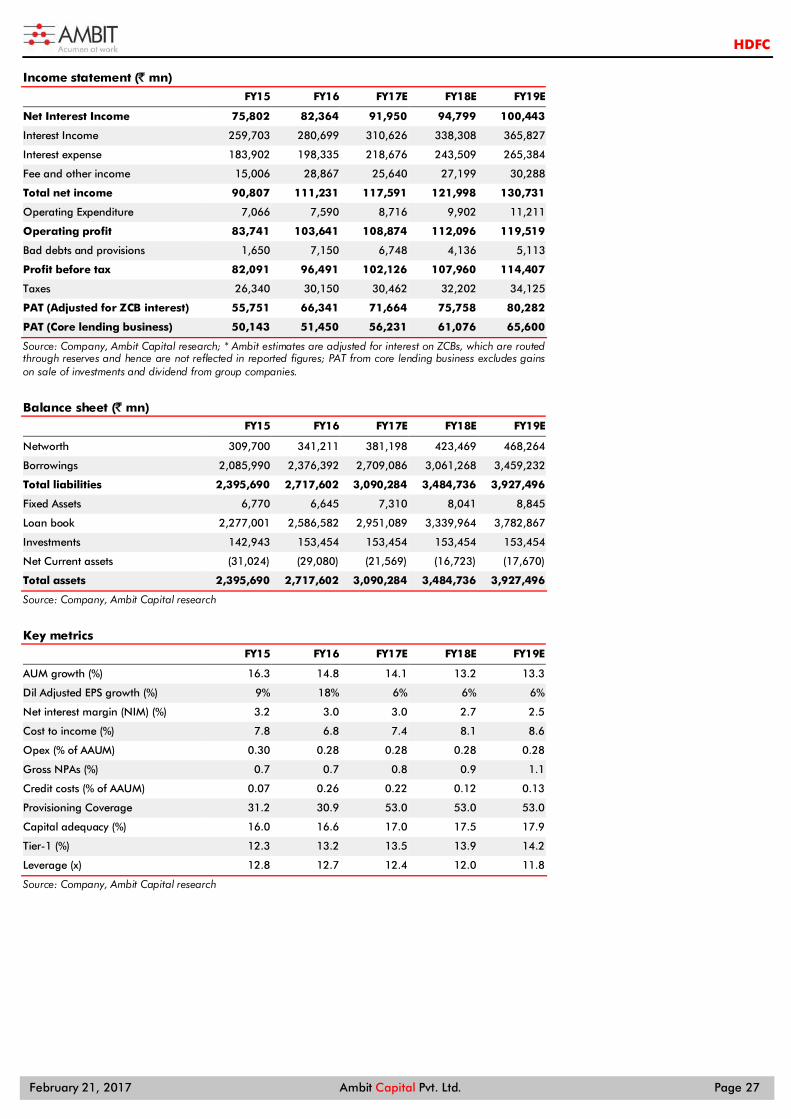

Detailed estimates and assumptions Exhibit 37: Key assumptions Particulars FY16 FY17E FY18E FY19E Remarks

Assumptions

YoY assets growth 15% 14% 13% 13% Loan growth should moderate to 13% CAGR over FY17-19E owing to slowdown in ticket sizes (6% CAGR) and slowdown in borrower growth (7% CAGR).

Yields on advances 10.8% 10.5% 10.1% 9.7% Competitive pressures and run-off of higher yielding back book should lead to yields moderating by ~80bps over FY17-19E.

Cost of funds 9.0% 8.6% 8.4% 8.1% Declining wholesale interest rates and re-pricing of bonds should reduce cost of funds declining by ~50bps over FY17-19E.

Net interest margins* 3.0% 3.0% 2.7% 2.5% Margins should decline by ~50bps over FY17-19E as decline in yields is sharper that decline in cost of funds.

Opex/AUM 0.3% 0.3% 0.3% 0.3% Operating costs should remain broadly stable.

Credit cost 0.3% 0.2% 0.1% 0.1% Credit costs should increase from their historical levels (~5-7bps) owing to rising NPAs in both developer and home loans.

Output*

Core Net revenues (` mn) 86,684 97,197 100,739 107,148 Core net revenue should moderate to 7% CAGR over FY16-19E.

Core Op. profit (` mn) 108,231 108,874 112,096 119,519 Core op profit should moderate to 3% CAGR over FY16-19E.

Core Profit after tax (` mn) 51,450 56,231 61,076 65,600 Core profits should moderate to 8% CAGR over FY16-19E.

Core EPS (`) 28 32 34 35 Core EPS should moderate to 8% CAGR over FY16-19E.

Core BVPS (`) 157 182 208 236 Core BVPS should moderate to 8% CAGR over FY16-19E.

Core RoA 1.7% 1.7% 1.6% 1.6% Core RoA should moderate by 16bps over FY16-19E.

Core RoE 21.7% 20.6% 19.4% 18.3% Core RoE should moderate by 341bps over FY16-19E.

Source: Company, Ambit capital research * Ambit estimates are adjusted for interest on ZCBs, which are routed through reserves and hence are not reflected in reported figures; PAT from core lending business excludes gains on sale of investments and dividend from group companies.

Our estimates may not be exactly comparable with those of the Street owing to accounting differences (we are deducting interest on ZCBs in the net interest income, but are not sure if consensus is doing this uniformly). That said, our below-consensus EPS expectations (by 11/17% in FY18/19) could be due to a combination of lower growth and margin assumptions.

Exhibit 38: Ambit versus consensus expectations

Particulars Ambit Consensus Deviation

Net revenues (̀ mn) FY17E 117,591 119,705 -2% FY18E 121,998 132,462 -8%

FY19E 130,731 150,156 -13%

PAT (̀ mn) FY17E 71,664 75,548 -5%

FY18E 75,758 83,578 -9%

FY19E 80,282 95,732 -16%

EPS (̀ mn) FY17E 44.4 47.5 -7%

FY18E 46.9 52.7 -11%

FY19E 49.7 60.0 -17%

Source: Company, Ambit capital research

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 21

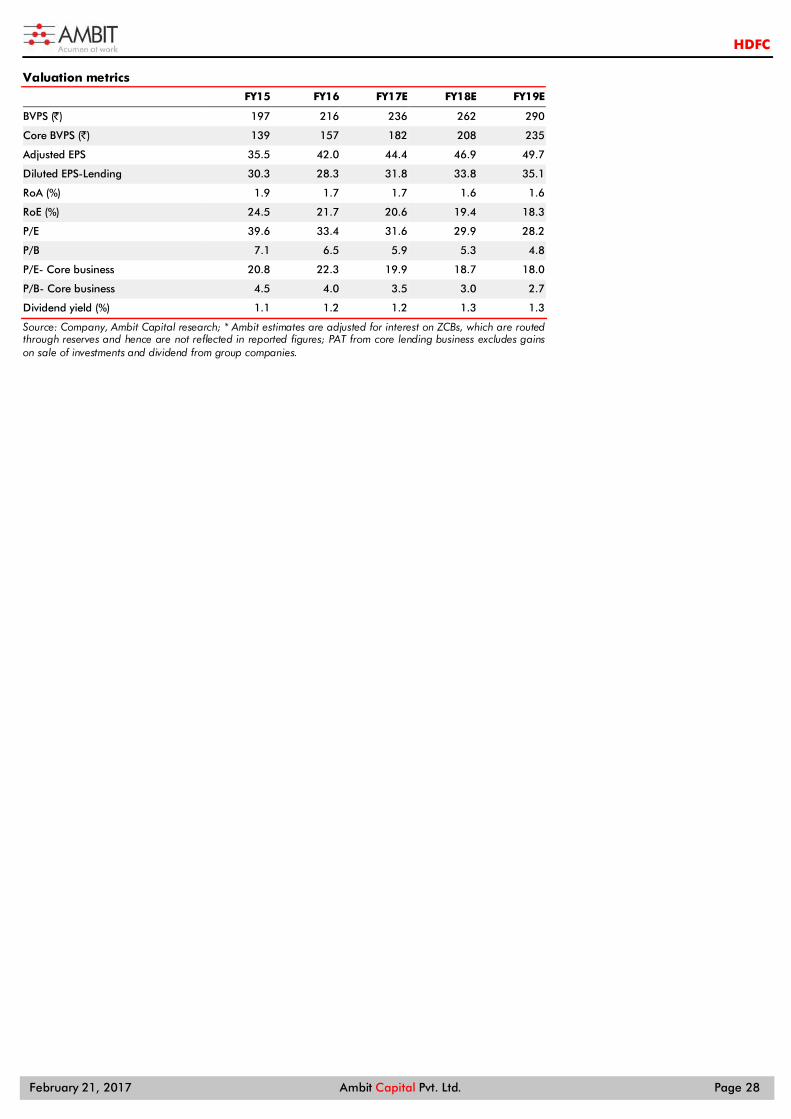

Valuations expensive despite de-rating Whilst the core mortgage business continues to trade at a premium despite de-rating (5.7x TTM BVPS in Jun’12 to 3.4x TTM BVPS now), our excess return model values it at implied FY19 core BVPS of 2x and implied FY19 core P/E of 19x (`471/share) . We assume Ke/sustainable growth/RoE of 14%/14%/18%, leading to a target price of `1100 despite a generous 0% holdco discount. Whilst increasing the dividend payouts could be a natural step in a scenario of diminished growth opportunities, signaling lower sustainable growth could de-rate valuations. However, use of unconventional structures to raise equity capital (low priced warrants with low/zero coupon bonds) has helped the company sustain respectable growth whilst simultaneously increasing the dividend payouts. Further pricing pressure in home loans and continued slowdown in earnings are the key catalysts for a de-rating. Abatement of competitive pressures; rising share of high yielding loans are the key risks.

Falling earnings growth over the last 5 years resulted in the stock returning just 15% CAGR vs an average 33% for the NBFC sector.

Exhibit 39: HDFC has massively underperformed the Bankex and NBFC indices

Source: Bloomberg, Ambit capital research

Core lending business: De-rating to continue To understand the valuation the market assigns to the standalone lending business, we have deducted the valuations of HDFC’s investment in its associates and subsidiaries from the valuation of the listed company. Based on such a calculation, the implied valuation assigned by the market to the standalone lending business is ~`631/share (Implied valuation of 3.4x TTM BVPS and 20x TTM EPS).

Exhibit 40: Implied valuations of HDFC’s core mortgage business

` bn Valuation (̀ bn) Methodology HDFC's stake in the co.(%)

HDFC's stake in the co. (̀ bn)

Valuation per share (̀ )

HDFC con. listed entity 2,223 Current Stock Price 100.0% 2,223

Less: HDFC Bank 3,516 Current Market price 21.6% 758 452

Less: Gruh Finance 137 Current Stock Price 58.6% 81 49

Less: HDFC AMC 111 5x AUM of Dec'16 59.9% 66 41

Less: Life Insurance 379 Assigning peer valn of 3.7x P/EV 70.7% 267 166

Less: General Insurance 50 Latest transaction value 50.7% 25 16

Less: Other investments 3 1 time current book value 100.0% 3 2 Implied valuation for HDFC's lending business 1,022 631

Source: Ambit capital research

We observe that the core mortgage business has de-rated over the last 4 years from 5.7x trailing BVPS in FY13 to 3.4x trailing BVPS in FY17.

0

100

200

300

400

500

Feb-

12

May

-12

Aug

-12

Nov

-12

Feb-

13

May

-13

Aug

-13

Nov

-13

Feb-

14

May

-14

Aug

-14

Nov

-14

Feb-

15

May

-15

Aug

-15

Nov

-15

Feb-

16

May

-16

Aug

-16

Nov

-16

NBFC Index HDFC BANKEX INDEX

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 22

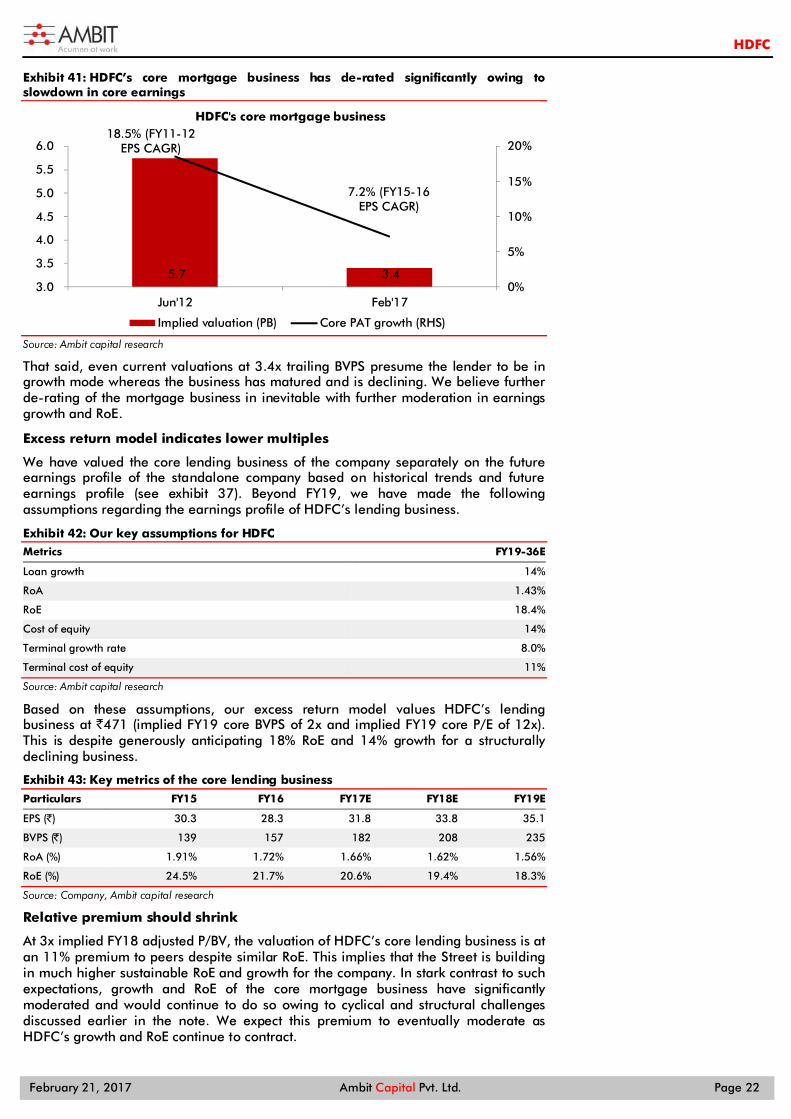

Exhibit 41: HDFC’s core mortgage business has de-rated significantly owing to slowdown in core earnings

Source: Ambit capital research

That said, even current valuations at 3.4x trailing BVPS presume the lender to be in growth mode whereas the business has matured and is declining. We believe further de-rating of the mortgage business in inevitable with further moderation in earnings growth and RoE.

Excess return model indicates lower multiples

We have valued the core lending business of the company separately on the future earnings profile of the standalone company based on historical trends and future earnings profile (see exhibit 37). Beyond FY19, we have made the following assumptions regarding the earnings profile of HDFC’s lending business.

Exhibit 42: Our key assumptions for HDFC Metrics FY19-36E

Loan growth 14%

RoA 1.43%

RoE 18.4%

Cost of equity 14%

Terminal growth rate 8.0%

Terminal cost of equity 11%

Source: Ambit capital research

Based on these assumptions, our excess return model values HDFC’s lending business at `471 (implied FY19 core BVPS of 2x and implied FY19 core P/E of 12x). This is despite generously anticipating 18% RoE and 14% growth for a structurally declining business.

Exhibit 43: Key metrics of the core lending business

Particulars FY15 FY16 FY17E FY18E FY19E

EPS (`) 30.3 28.3 31.8 33.8 35.1

BVPS (̀ ) 139 157 182 208 235

RoA (%) 1.91% 1.72% 1.66% 1.62% 1.56%

RoE (%) 24.5% 21.7% 20.6% 19.4% 18.3%

Source: Company, Ambit capital research

Relative premium should shrink

At 3x implied FY18 adjusted P/BV, the valuation of HDFC’s core lending business is at an 11% premium to peers despite similar RoE. This implies that the Street is building in much higher sustainable RoE and growth for the company. In stark contrast to such expectations, growth and RoE of the core mortgage business have significantly moderated and would continue to do so owing to cyclical and structural challenges discussed earlier in the note. We expect this premium to eventually moderate as HDFC’s growth and RoE continue to contract.

5.7 3.4

18.5% (FY11-12 EPS CAGR)

7.2% (FY15-16 EPS CAGR)

0%

5%

10%

15%

20%

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Jun'12 Feb'17

HDFC's core mortgage business

Implied valuation (PB) Core PAT growth (RHS)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 23

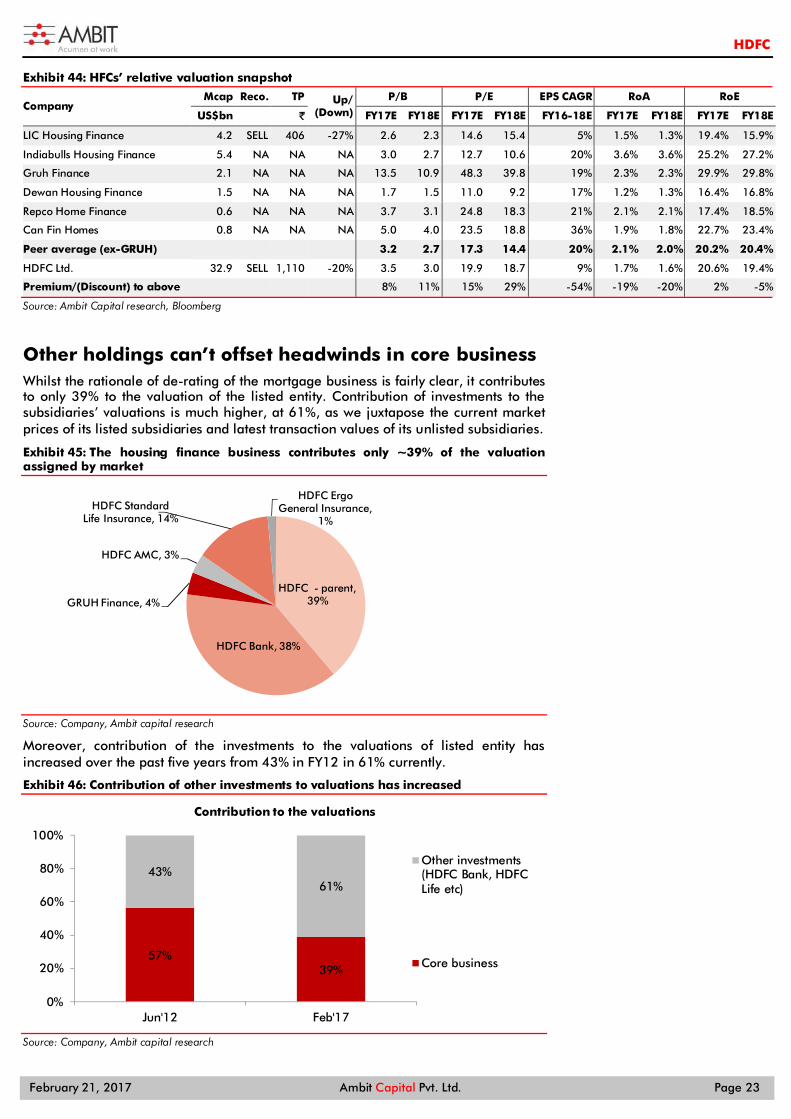

Exhibit 44: HFCs’ relative valuation snapshot

Company Mcap Reco. TP Up/

(Down) P/B P/E EPS CAGR RoA RoE

US$bn ` FY17E FY18E FY17E FY18E FY16-18E FY17E FY18E FY17E FY18E

LIC Housing Finance 4.2 SELL 406 -27% 2.6 2.3 14.6 15.4 5% 1.5% 1.3% 19.4% 15.9%

Indiabulls Housing Finance 5.4 NA NA NA 3.0 2.7 12.7 10.6 20% 3.6% 3.6% 25.2% 27.2%

Gruh Finance 2.1 NA NA NA 13.5 10.9 48.3 39.8 19% 2.3% 2.3% 29.9% 29.8%

Dewan Housing Finance 1.5 NA NA NA 1.7 1.5 11.0 9.2 17% 1.2% 1.3% 16.4% 16.8%

Repco Home Finance 0.6 NA NA NA 3.7 3.1 24.8 18.3 21% 2.1% 2.1% 17.4% 18.5%

Can Fin Homes 0.8 NA NA NA 5.0 4.0 23.5 18.8 36% 1.9% 1.8% 22.7% 23.4%

Peer average (ex-GRUH) 3.2 2.7 17.3 14.4 20% 2.1% 2.0% 20.2% 20.4%

HDFC Ltd. 32.9 SELL 1,110 -20% 3.5 3.0 19.9 18.7 9% 1.7% 1.6% 20.6% 19.4%

Premium/(Discount) to above 8% 11% 15% 29% -54% -19% -20% 2% -5%

Source: Ambit Capital research, Bloomberg

Other holdings can’t offset headwinds in core business Whilst the rationale of de-rating of the mortgage business is fairly clear, it contributes to only 39% to the valuation of the listed entity. Contribution of investments to the subsidiaries’ valuations is much higher, at 61%, as we juxtapose the current market prices of its listed subsidiaries and latest transaction values of its unlisted subsidiaries.

Exhibit 45: The housing finance business contributes only ~39% of the valuation assigned by market

Source: Company, Ambit capital research

Moreover, contribution of the investments to the valuations of listed entity has increased over the past five years from 43% in FY12 in 61% currently.

Exhibit 46: Contribution of other investments to valuations has increased

Source: Company, Ambit capital research

HDFC - parent, 39%

HDFC Bank, 38%

GRUH Finance, 4%

HDFC AMC, 3%

HDFC Standard Life Insurance, 14%

HDFC Ergo General Insurance,

1%

57%39%

43%61%

0%

20%

40%

60%

80%

100%

Jun'12 Feb'17

Contribution to the valuations

Other investments(HDFC Bank, HDFCLife etc)

Core business

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 24

With the rising contribution of investments to the valuation of the listed entity, the ability of HDFC to deploy the additional capital with high IRR could be a key antidote to the imminent de-rating of the mortgage business. However, as discussed in the earlier section of the note, we believe that the ability of these investments to add further value hereon is limited as:

Other business don’t need further capital: As discussed in the earlier sections of the note, other subsidiaries/associates in banking, asset management and insurance have scaled up, are highly profitable and require little capital support from HDFC (barring general insurance where capital requirement is modest). Moreover, these businesses are now paying healthy dividends to the parent.

Key businesses (HDFC bank) also faces earnings slowdown: Apart from the core housing finance business, HDFC’s investment in HDFC Bank (33% of SOTP) would struggle to add further value to overall valuations. With high competitive intensity in both retail and corporate loans, we expect growth to moderate to 19% CAGR over FY18-19E (vs ~24% over FY12-16) as operating profitability would remain under pressure (14% CAGR in operating profits over FY18-19E vs ~23% between FY12-FY16). Hence, EPS growth should settle at the FY16-17 run-rate of ~15% versus ~30% during most part of the last decade. The current valuation multiples of 23x FY18E P/E and 3.7x FY18E P/B, at a ~40% premium to peers, largely capture superior earnings growth of the bank in the medium term (even including subsidiaries) and leave little margin of safety for investors. We are SELLers of HDFC Bank with a Dec’2017 target price of `1,079 (17.7x FY18E EPS and 2.9x FY18E BVPS).

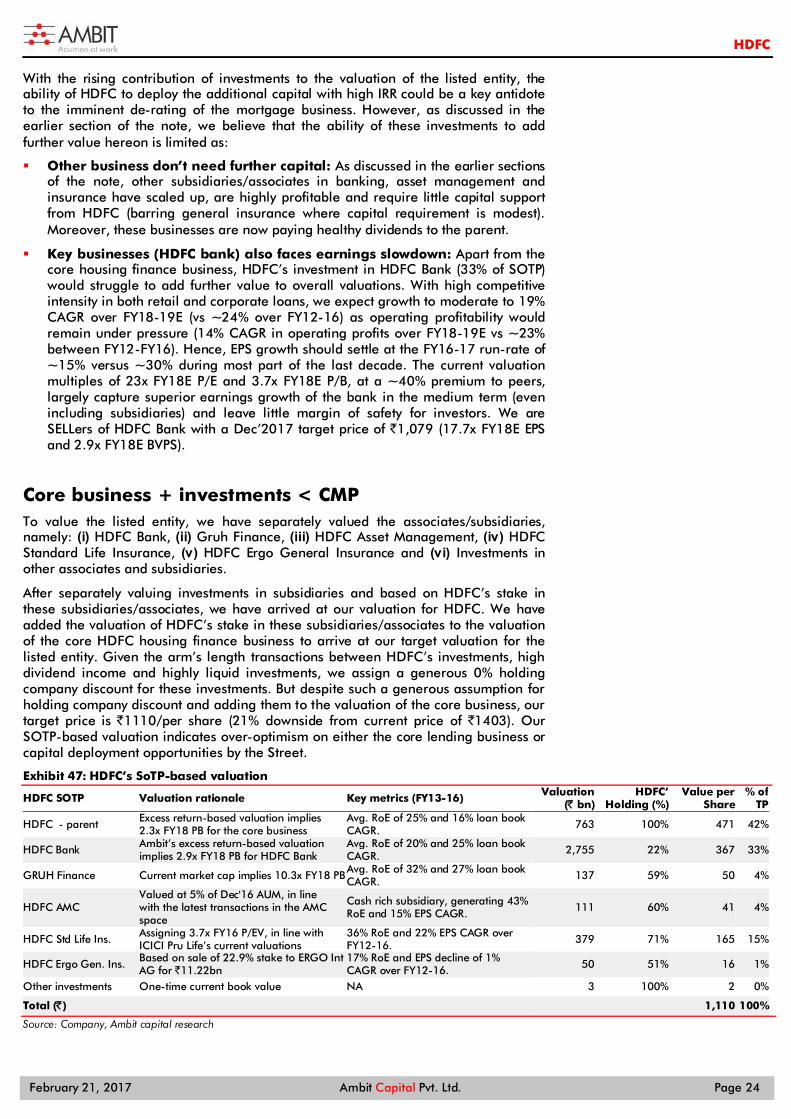

Core business + investments < CMP To value the listed entity, we have separately valued the associates/subsidiaries, namely: (i) HDFC Bank, (ii) Gruh Finance, (iii) HDFC Asset Management, (iv) HDFC Standard Life Insurance, (v) HDFC Ergo General Insurance and (vi) Investments in other associates and subsidiaries.

After separately valuing investments in subsidiaries and based on HDFC’s stake in these subsidiaries/associates, we have arrived at our valuation for HDFC. We have added the valuation of HDFC’s stake in these subsidiaries/associates to the valuation of the core HDFC housing finance business to arrive at our target valuation for the listed entity. Given the arm’s length transactions between HDFC’s investments, high dividend income and highly liquid investments, we assign a generous 0% holding company discount for these investments. But despite such a generous assumption for holding company discount and adding them to the valuation of the core business, our target price is `1110/per share (21% downside from current price of `1403). Our SOTP-based valuation indicates over-optimism on either the core lending business or capital deployment opportunities by the Street.

Exhibit 47: HDFC’s SoTP-based valuation

HDFC SOTP Valuation rationale Key metrics (FY13-16) Valuation (̀ bn)

HDFC’ Holding (%)

Value per Share

% of TP

HDFC - parent Excess return-based valuation implies 2.3x FY18 PB for the core business

Avg. RoE of 25% and 16% loan book CAGR. 763 100% 471 42%

HDFC Bank Ambit’s excess return-based valuation implies 2.9x FY18 PB for HDFC Bank

Avg. RoE of 20% and 25% loan book CAGR. 2,755 22% 367 33%

GRUH Finance Current market cap implies 10.3x FY18 PB Avg. RoE of 32% and 27% loan book CAGR. 137 59% 50 4%

HDFC AMC Valued at 5% of Dec'16 AUM, in line with the latest transactions in the AMC space

Cash rich subsidiary, generating 43% RoE and 15% EPS CAGR. 111 60% 41 4%

HDFC Std Life Ins. Assigning 3.7x FY16 P/EV, in line with ICICI Pru Life’s current valuations

36% RoE and 22% EPS CAGR over FY12-16. 379 71% 165 15%

HDFC Ergo Gen. Ins. Based on sale of 22.9% stake to ERGO Int AG for `11.22bn

17% RoE and EPS decline of 1% CAGR over FY12-16. 50 51% 16 1%

Other investments One-time current book value NA 3 100% 2 0%

Total (̀ ) 1,110 100%

Source: Company, Ambit capital research

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 25

Returning cash also won’t help With business having scaled up and growth of the core business moderating, returning excess cash either through increasing dividend payout is the best way to maximise shareholder value. In fact, HDFC’s dividend payout ratio has doubled from ~20% in FY94 to ~44% in FY16.

Exhibit 48: HDFC’s dividend payout has increased over FY94-16

Source: Company, Ambit capital research; Note: Dividend payout for HDFC is high in FY00 and FY02 owing to special one-time dividend.

Further increasing dividend payout will lower sustainable growth…

However, increasing the payout ratio and thus lower retained profits imply lower future networth for HDFC, which in turn would lower sustainable growth. In our excess return model, we believe an average 36% payout ratio is reasonable to achieve 14% loan growth without capital raise. However, increasing the payout ratio implies lower sustainable growth and thus lower valuation multiples unless HDFC raises capital at a much lower cost of equity.

..unless future capital raises are at favourable valuations

That said, HDFC has been successful in raising capital at favorable valuations (high implied multiples) to compensate for the increased payout ratio. This is despite growth and profitability moderating. One key reason for such success is the innovative structures through which HDFC has raised capital – low/zero-coupon NCDs along with share warrants in Oct’15 and Aug’09, which not only prevent immediate and bulky dilution but also lower the cost of equity by giving increased flexibility to the investor and underwriting minimum return of the instrument. In this regard, it’s worthwhile to ponder if the company is raising capital from new investors to return capital to the older investors?

Exhibit 49: HDFC’s increasing dividend payout has coincided with capital raises that largely compensate for dividends

Source: Company, Ambit capital research; Note: Rs134bn capital raised includes Rs50.51bn of simultaneous issue of NCDs with warrants in Oct'15. Dividends paid and payout ratio include dividend tax.

0%

10%

20%

30%

40%

50%

60%

70%

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

Dividend payout ratio

0

134

(23)

(183)35%

44%

30%

32%34%

36%38%

40%42%

44%46%

(200)

(150)

(100)

(50)

-

50

100

150

FY94-05 FY06-16

Capital raised (Rs bn) Dividends paid (Rs bn) Median dividend payout (RHS)

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 26

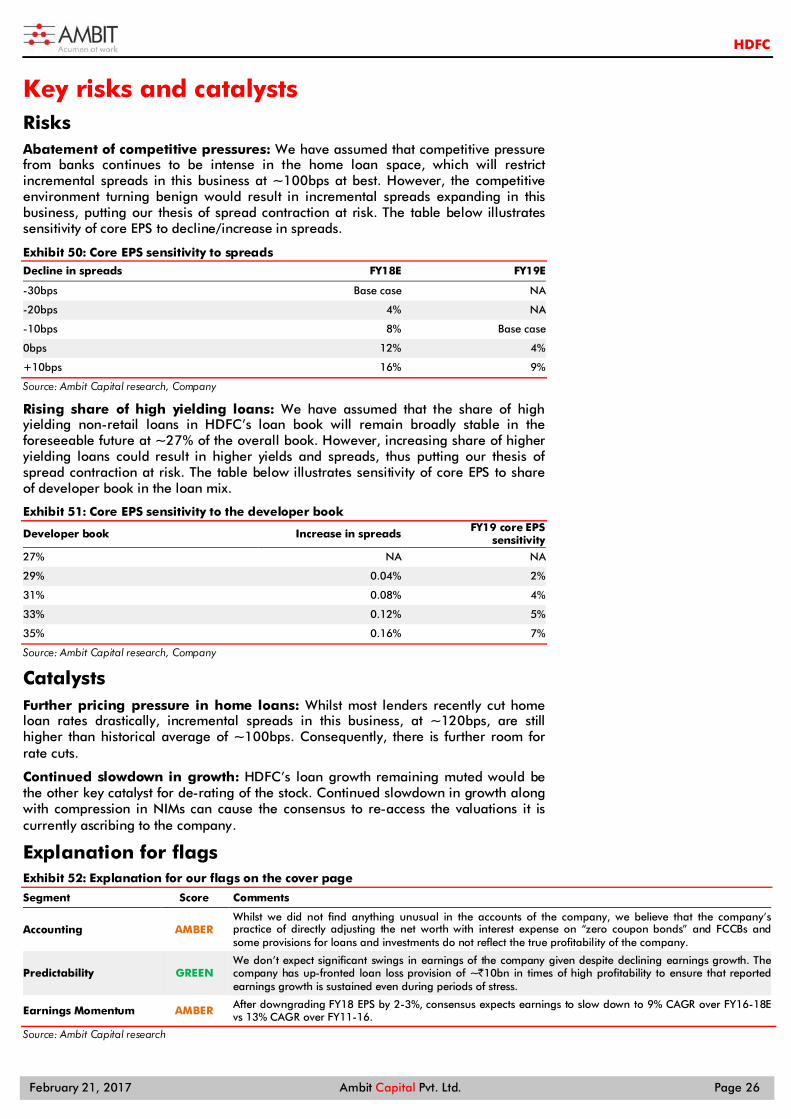

Key risks and catalysts Risks Abatement of competitive pressures: We have assumed that competitive pressure from banks continues to be intense in the home loan space, which will restrict incremental spreads in this business at ~100bps at best. However, the competitive environment turning benign would result in incremental spreads expanding in this business, putting our thesis of spread contraction at risk. The table below illustrates sensitivity of core EPS to decline/increase in spreads.

Exhibit 50: Core EPS sensitivity to spreads Decline in spreads FY18E FY19E

-30bps Base case NA

-20bps 4% NA

-10bps 8% Base case

0bps 12% 4%

+10bps 16% 9%

Source: Ambit Capital research, Company

Rising share of high yielding loans: We have assumed that the share of high yielding non-retail loans in HDFC’s loan book will remain broadly stable in the foreseeable future at ~27% of the overall book. However, increasing share of higher yielding loans could result in higher yields and spreads, thus putting our thesis of spread contraction at risk. The table below illustrates sensitivity of core EPS to share of developer book in the loan mix.

Exhibit 51: Core EPS sensitivity to the developer book

Developer book Increase in spreads FY19 core EPS sensitivity

27% NA NA

29% 0.04% 2%

31% 0.08% 4%

33% 0.12% 5%

35% 0.16% 7%

Source: Ambit Capital research, Company

Catalysts Further pricing pressure in home loans: Whilst most lenders recently cut home loan rates drastically, incremental spreads in this business, at ~120bps, are still higher than historical average of ~100bps. Consequently, there is further room for rate cuts.

Continued slowdown in growth: HDFC’s loan growth remaining muted would be the other key catalyst for de-rating of the stock. Continued slowdown in growth along with compression in NIMs can cause the consensus to re-access the valuations it is currently ascribing to the company.

Explanation for flags Exhibit 52: Explanation for our flags on the cover page

Segment Score Comments

Accounting AMBER Whilst we did not find anything unusual in the accounts of the company, we believe that the company’s practice of directly adjusting the net worth with interest expense on “zero coupon bonds” and FCCBs and some provisions for loans and investments do not reflect the true profitability of the company.

Predictability GREEN We don’t expect significant swings in earnings of the company given despite declining earnings growth. The company has up-fronted loan loss provision of ~`10bn in times of high profitability to ensure that reported earnings growth is sustained even during periods of stress.

Earnings Momentum AMBER After downgrading FY18 EPS by 2-3%, consensus expects earnings to slow down to 9% CAGR over FY16-18E vs 13% CAGR over FY11-16.

Source: Ambit Capital research

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 27

Income statement (` mn)

FY15 FY16 FY17E FY18E FY19E

Net Interest Income 75,802 82,364 91,950 94,799 100,443

Interest Income 259,703 280,699 310,626 338,308 365,827

Interest expense 183,902 198,335 218,676 243,509 265,384

Fee and other income 15,006 28,867 25,640 27,199 30,288

Total net income 90,807 111,231 117,591 121,998 130,731

Operating Expenditure 7,066 7,590 8,716 9,902 11,211

Operating profit 83,741 103,641 108,874 112,096 119,519

Bad debts and provisions 1,650 7,150 6,748 4,136 5,113

Profit before tax 82,091 96,491 102,126 107,960 114,407

Taxes 26,340 30,150 30,462 32,202 34,125

PAT (Adjusted for ZCB interest) 55,751 66,341 71,664 75,758 80,282

PAT (Core lending business) 50,143 51,450 56,231 61,076 65,600

Source: Company, Ambit Capital research; * Ambit estimates are adjusted for interest on ZCBs, which are routed through reserves and hence are not reflected in reported figures; PAT from core lending business excludes gains on sale of investments and dividend from group companies.

Balance sheet (` mn) FY15 FY16 FY17E FY18E FY19E

Networth 309,700 341,211 381,198 423,469 468,264

Borrowings 2,085,990 2,376,392 2,709,086 3,061,268 3,459,232

Total liabilities 2,395,690 2,717,602 3,090,284 3,484,736 3,927,496

Fixed Assets 6,770 6,645 7,310 8,041 8,845

Loan book 2,277,001 2,586,582 2,951,089 3,339,964 3,782,867

Investments 142,943 153,454 153,454 153,454 153,454

Net Current assets (31,024) (29,080) (21,569) (16,723) (17,670)

Total assets 2,395,690 2,717,602 3,090,284 3,484,736 3,927,496

Source: Company, Ambit Capital research

Key metrics FY15 FY16 FY17E FY18E FY19E

AUM growth (%) 16.3 14.8 14.1 13.2 13.3

Dil Adjusted EPS growth (%) 9% 18% 6% 6% 6%

Net interest margin (NIM) (%) 3.2 3.0 3.0 2.7 2.5

Cost to income (%) 7.8 6.8 7.4 8.1 8.6

Opex (% of AAUM) 0.30 0.28 0.28 0.28 0.28

Gross NPAs (%) 0.7 0.7 0.8 0.9 1.1

Credit costs (% of AAUM) 0.07 0.26 0.22 0.12 0.13

Provisioning Coverage 31.2 30.9 53.0 53.0 53.0

Capital adequacy (%) 16.0 16.6 17.0 17.5 17.9

Tier-1 (%) 12.3 13.2 13.5 13.9 14.2

Leverage (x) 12.8 12.7 12.4 12.0 11.8

Source: Company, Ambit Capital research

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 28

Valuation metrics

FY15 FY16 FY17E FY18E FY19E

BVPS (̀ ) 197 216 236 262 290

Core BVPS (`) 139 157 182 208 235

Adjusted EPS 35.5 42.0 44.4 46.9 49.7

Diluted EPS-Lending 30.3 28.3 31.8 33.8 35.1

RoA (%) 1.9 1.7 1.7 1.6 1.6

RoE (%) 24.5 21.7 20.6 19.4 18.3

P/E 39.6 33.4 31.6 29.9 28.2

P/B 7.1 6.5 5.9 5.3 4.8

P/E- Core business 20.8 22.3 19.9 18.7 18.0

P/B- Core business 4.5 4.0 3.5 3.0 2.7

Dividend yield (%) 1.1 1.2 1.2 1.3 1.3

Source: Company, Ambit Capital research; * Ambit estimates are adjusted for interest on ZCBs, which are routed through reserves and hence are not reflected in reported figures; PAT from core lending business excludes gains on sale of investments and dividend from group companies.

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 29

Institutional Equities Team Saurabh Mukherjea, CFA CEO, Ambit Capital Private Limited (022) 30433174 [email protected] Pramod Gubbi, CFA Head of Equities (022) 30433124 [email protected]

Research Analysts

Name Industry Sectors Desk-Phone E-mail

Nitin Bhasin - Head of Research E&C / Infra / Cement / Home Building (022) 30433241 [email protected] Aadesh Mehta, CFA Banking / Financial Services (022) 30433239 [email protected] Abhishek Ranganathan, CFA Retail / Consumer Discretionary (022) 30433085 [email protected] Anuj Bansal Consumer (022) 30433122 [email protected] Aditi Singh Economy / Strategy (022) 30433284 [email protected] Ashvin Shetty, CFA Automobiles / Auto Ancillaries (022) 30433285 [email protected] Bhargav Buddhadev Power Utilities / Capital Goods (022) 30433252 [email protected] Deepesh Agarwal, CFA Power Utilities / Capital Goods (022) 30433275 [email protected] Dhiraj Mistry, CFA Consumer (022) 30433264 [email protected] Gaurav Khandelwal, CFA Automobiles / Auto Ancillaries (022) 30433132 [email protected] Girisha Saraf Home Building (022) 30433211 [email protected] Karan Khanna, CFA Strategy (022) 30433251 [email protected] Mayank Porwal Retail / Consumer Discretionary (022) 30433214 [email protected] Pankaj Agarwal, CFA Banking / Financial Services (022) 30433206 [email protected] Paresh Dave, CFA Healthcare (022) 30433212 [email protected] Parita Ashar, CFA Cement / Metals / Aviation (022) 30433223 [email protected] Prashant Mittal, CFA Strategy / Derivatives (022) 30433218 [email protected] Rahil Shah Banking / Financial Services (022) 30433217 [email protected] Ravi Singh Banking / Financial Services (022) 30433181 [email protected] Ritesh Gupta, CFA Oil & Gas / Chemicals / Agri Inputs (022) 30433242 [email protected] Ritesh Vaidya, CFA Consumer (022) 30433246 [email protected] Ritika Mankar Mukherjee, CFA Economy / Strategy (022) 30433175 [email protected] Sagar Rastogi Technology (022) 30433291 [email protected] Sudheer Guntupalli Technology (022) 30433203 [email protected] Sumit Shekhar Economy / Strategy (022) 30433229 [email protected] Utsav Mehta, CFA E&C / Infrastructure (022) 30433209 [email protected] Vivekanand Subbaraman, CFA Media / Telecom (022) 30433261 [email protected]

Sales

Name Regions Desk-Phone E-mail

Sarojini Ramachandran - Head of Sales UK +44 (0) 20 7886 2740 [email protected] Dharmen Shah India / Asia (022) 30433289 [email protected] Dipti Mehta India (022) 30433053 [email protected] Krishnan V India / Asia (022) 30433295 [email protected] Nityam Shah, CFA Europe (022) 30433259 [email protected] Punitraj Mehra, CFA India / Asia (022) 30433198 [email protected] Shaleen Silori India (022) 30433256 [email protected]

Singapore

Praveena Pattabiraman Singapore +65 6536 0481 [email protected] Shashank Abhisheik Singapore +65 6536 1935 [email protected]

USA / Canada

Ravilochan Pola – CEO Americas +1(646) 793 6001 [email protected] Hitakshi Mehra Americas +1(646) 793 6002 [email protected] Achint Bhagat, CFA Americas +1(646) 793 6752 [email protected]

Production

Sajid Merchant Production (022) 30433247 [email protected] Sharoz G Hussain Production (022) 30433183 [email protected] Jestin George Editor (022) 30433272 [email protected] Richard Mugutmal Editor (022) 30433273 [email protected] Nikhil Pillai Database (022) 30433265 [email protected]

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 30

Housing Development Finance (HDFC IN, SELL)

Source: Bloomberg, Ambit Capital research

0200400600800

1,0001,2001,4001,600

Feb-

14

Apr

-14

Jun-

14

Aug

-14

Oct

-14

Dec

-14

Feb-

15

Apr

-15

Jun-

15

Aug

-15

Oct

-15

Dec

-15

Feb-

16

Apr

-16

Jun-

16

Aug

-16

Oct

-16

Dec

-16

Feb-

17

Housing Development Finance Corp Ltd

HDFC

February 21, 2017 Ambit Capital Pvt. Ltd. Page 31

Explanation of Investment Rating

Investment Rating Expected return (over 12-month)

BUY >10%

SELL <10%

NO STANCE We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation