Informality: Engine of Structural Transformation ? The...

28

Informality: Engine of Structural Transformation ? The Case of Francophone Africa 1 By Nancy Claire Benjamin, World Bank ([email protected]) and Ahmadou Aly Mbaye, Université Cheikh Anta Diop de Dakar, ([email protected] ) 1 We are grateful to participants of a workshop organized by Development Policy Research Unit, at the University of Cape Town, in November 2015, for useful comments on an earlier draft of these results. The results presented in this paper are drawn from a bigger project on the informal sector in francophone Africa, sponsored by IDRC- Canada and the World Bank. In particular, insights from Pirella Paci and Flaubert Mbiekop in the design of the project are acknowledged. The usual disclaimer does apply.

Transcript of Informality: Engine of Structural Transformation ? The...

Informality:EngineofStructuralTransformation?TheCaseofFrancophone

Africa 1

By

Nancy Claire Benjamin, World Bank ([email protected])

and

Ahmadou Aly Mbaye, Université Cheikh Anta Diop de Dakar, ([email protected] )

1WearegratefultoparticipantsofaworkshoporganizedbyDevelopmentPolicyResearchUnit,attheUniversityofCapeTown,inNovember2015,forusefulcommentsonanearlierdraftoftheseresults.TheresultspresentedinthispaperaredrawnfromabiggerprojectontheinformalsectorinfrancophoneAfrica,sponsoredbyIDRC-CanadaandtheWorldBank.Inparticular,insightsfromPirellaPaciandFlaubertMbiekopinthedesignoftheprojectareacknowledged.Theusualdisclaimerdoesapply.

Informality:EngineofStructuralTransformation?TheCaseofFrancophoneAfrica

Introduction

Theinformalsectorhasamajorroleineconomy-widestructuraltransformation.First,becauseitisthelargestemployerinsub-SaharanAfrica.Second,becauseitproduceshalformoreoftotalvalueaddedinpoorAfricancountries.Andthird,becausethelowproductivityobservedininformalactivities--ascomparedtoformalactivitiesinthesamecountry–indicatethathigherreturnscouldbeearnedbythefactorsthereemployed.

Thischapterreviewsthefollowingquestions:CaninformalfirmsdriveAfrica’stransformation?Whatgivesrisetoinformalityandwhatkindofjobsdoesitcreate?Howdoesthelargeinformaleconomyinfluencestructuraltransformation?Howcanweimprovetheeconomicreturnstofactorsemployedintheinformalsector?

Themainmessagesincludethefollowing:RelativereturnstofactorsintheurbanandruralsectorsinAfricahavegivenrisetosubstantialrural-urbanmigration,whereemploymentopportunitiesformigrantsandnon-migrantsalikeareoverwhelminglyintheinformaleconomy.Thustheinformalsectorisalreadythedrawfortransformationaloutmigrationfromagriculture;themainchallengeisthemodernizationofinformaleconomicactivity.Theinformalsectorisquitediverse,withastrongmajorityofsmallsubsistencefirms,butalsoaninfluentiallayeroflarge,sophisticated,thoughstillinformalfirms.Theseinformalactorsrepresentalargecadreofclientsforbusinessservicesandsocialservices,butexperiencedifficultrelationswithGovernmentandweakinstitutionalsupport.Policyshouldfocusonwhatconstrainsfastermodernizationoftheinformaleconomyandthusinhibitsaccesstothebenefitsofmodernity,includinghigherproductivity.Inparticular,policiesthatconcentraterentsintoasmallnumberofhandsarelikelytoraisefactorcostsforformalfirmsandinturnreducetheincentivesformodern,internationalfirmstoprovideanengineofmodernizationfortheinformaleconomy.

MuchofthedatausedinthispaperisdrawnfromadatasetcompiledthroughextensivefirmsurveysinFrancophoneAfrica.Followinganapproachthattakestheheterogeneityofthesectorintoaccount,wedefinetheinformaleconomyasacontinuumandincludeinoursamplethedifferentsegmentsoftheinformalsectorspectrum.Wethenuseastratifiedsamplingstrategy,obtainedbycombiningthedifferentlevelsofinformality(smallinformal,largeinformal,formal)andthedifferentsectorsofactivity(commerce,otherservices,industry).Thebaseforthesamplingisthetotalpopulationoffirmscorrespondingtodifferenttaxregimes.Accordingtothetaxregimetowhichthecompanybelongs,wedistinguish:

a)thesubsetoffirmssubjecttoregulartaxation,b)thesubsetoffirmssubjecttothepresumptivelumpsumtaxplan,c) thesubsetofallotherfirmsthatareeitherunknowntotaxrecordsorarenotsubjecttoanyoftheaboveregimes.

Fromthesesubsets,wehavedrawnastratifiedsampleoffirmsintheindustry,tradeandservicessectors(seeMbayeetal.,2015formoredetails).ThisapproachhasbeenusedindifferentperiodsoftimetogatherinformationonformalandinformalfirmsinWestandCentreAfrica.AnarrowersampleoffirmswithsimilarcharacteristicswasdrawnineachofthecitiesofDakarandCotonou,andadministeredaversionofthequestionnairecenteredonvaluechainsandthepatternsandmagnitudesofinteractionsbetweensmallinformalandlargerformalfirms.

Theinformaleconomy

Ashasbeenwell-documentedinsub-SaharanAfrica,theinformaleconomyishighlydiverse(Chen2006,BenjaminandMbaye2012,Benjaminetal.2014).Itspansagreatvarietyofbusinessescoveringthefullspectrumfromsubsistence,self-employmentandhouseholdenterprisestoextensivenetworksofcross-bordertradersandlarge,sophisticatedfirmsthatare,nevertheless,informalinsomesignificantrespect.Thestrongheterogeneityamonginformalfirmsunderliesthedifficultyofprovidingasingledefinitionofinformality and the consequent approach of classifying firms according to a continuum ofcharacteristics.ResultsfromBenjaminandMbaye(2012)confirmtheimportanceofdistinguishingthelarge from the small informal firms indescribingbehaviorand identifyingobstacles in the investmentclimate.Whilethevastmajorityofinformalfirmsareverysmall,thelargeinformalfirmsplayamajorrole.Afirmthatchoosestobeinformalinacountrywithweakregulatoryenforcementcangrowquitelarge,andmayhavestrongincentivestodoso.

Firms—bothformaland informal—needrelationshipsoftrust inordertosecure inputs,getcreditandmarket theirproducts. When formal institutions fail toprovideeffectiveproperty rights, firmscan tosome extent internalize these relationships of trust if they are large enough. Sometimes, becoming‘largeenough’cantaketheformofinformalnetworks,suchasinformalreligiousandethnicnetworks.Thesecansubstituteforofficialinstitutionsthatshould(butoftenfailto)supportarms-lengthtradingintheformalsector(GolubandHansonMeyer,2012).

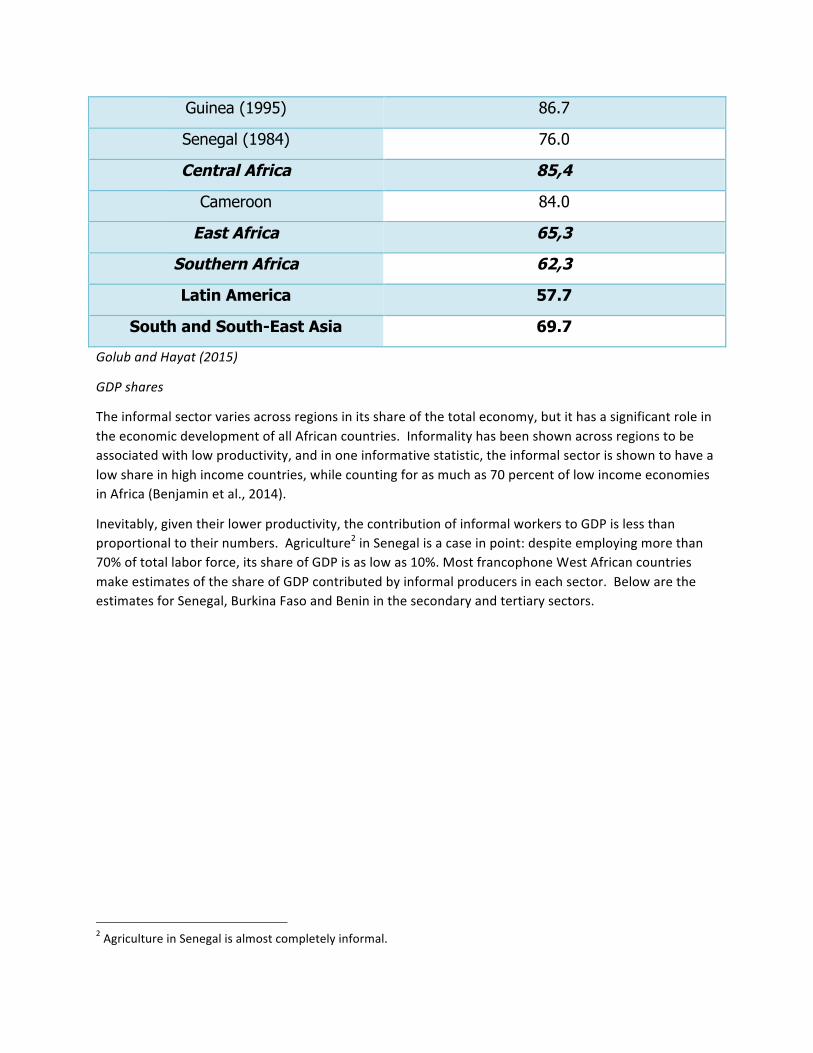

Employmentshares

Asawhole,theinformalsectoremploysoverhalfthetotalworkforceandbysomeestimatescreates90percentofnewjobs(Chen,2001).AsisapparentintheTablebelow,informalemploymentisanespeciallyimportantfactorinWestAfrica.Ofparticularsignificanceisthattheinformaleconomyemploysmostoftheworkersfromvulnerablegroups,includingwomenandyouth.Byandlarge,theinformalsectorallowsopenentryandbecomestheplaceofemploymentforthoseleavingtheagriculturesector–thecoremigrationunderlyingstructuraltransformation.Finally,thevastmajorityofsmallandmicroenterprisesoperateintheinformaleconomy.

Table 1 : Share of informal employment in total non agricultural employment (%)

Regions/Countries/Years 2000-10

North Africa 53.0

Sub-Saharan Africa 70.5

West Africa 73,6

Benin 96.3

Burkina Faso 90.5

Guinea (1995) 86.7

Senegal (1984) 76.0

Central Africa 85,4

Cameroon 84.0

East Africa 65,3

Southern Africa 62,3

Latin America 57.7

South and South-East Asia 69.7 GolubandHayat(2015)

GDPshares

Theinformalsectorvariesacrossregionsinitsshareofthetotaleconomy,butithasasignificantroleintheeconomicdevelopmentofallAfricancountries.Informalityhasbeenshownacrossregionstobeassociatedwithlowproductivity,andinoneinformativestatistic,theinformalsectorisshowntohavealowshareinhighincomecountries,whilecountingforasmuchas70percentoflowincomeeconomiesinAfrica(Benjaminetal.,2014).

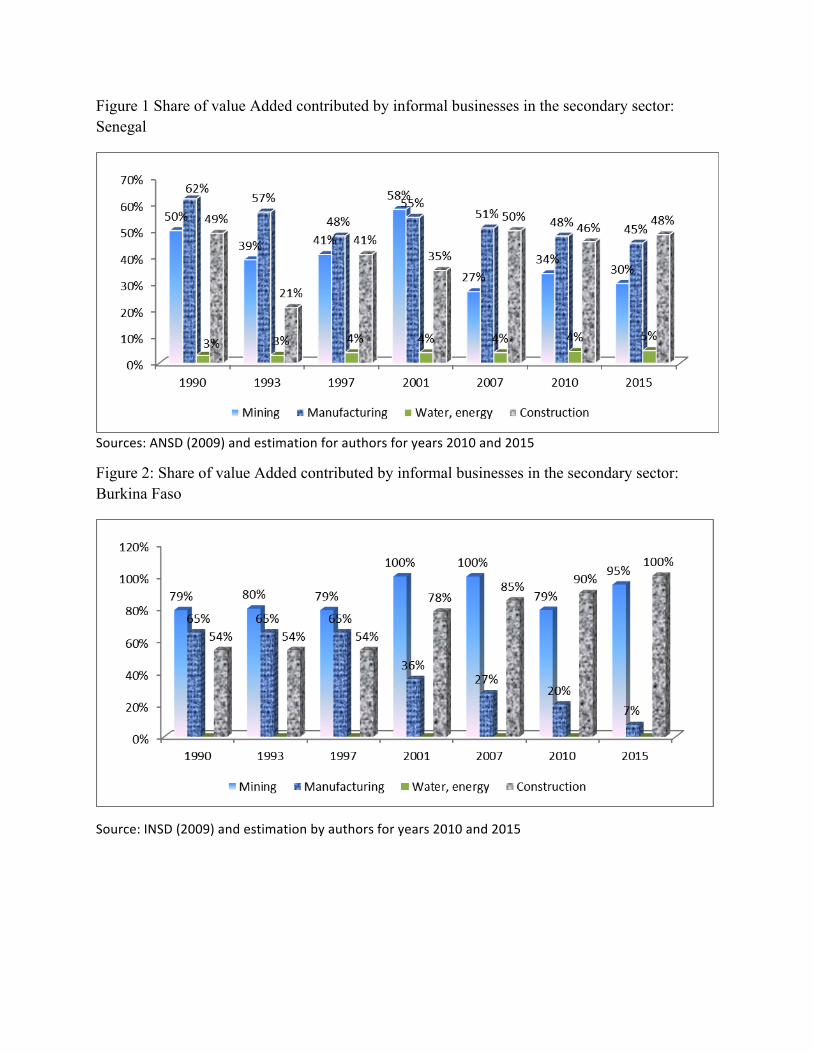

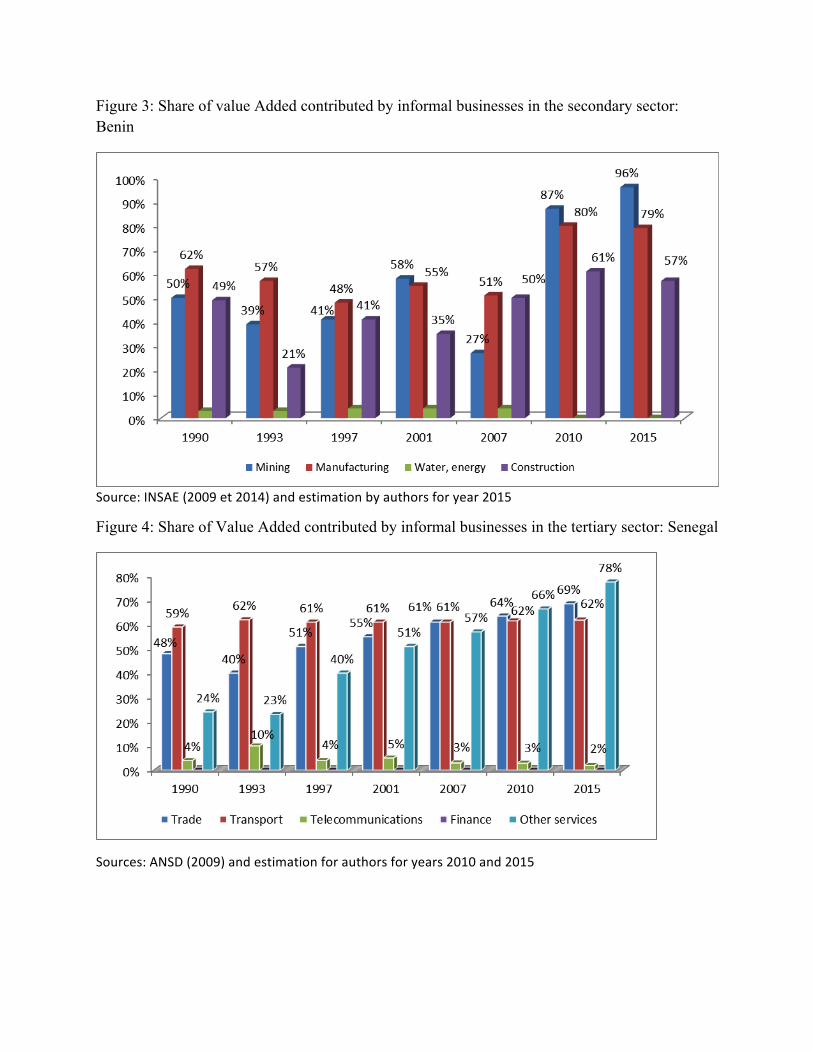

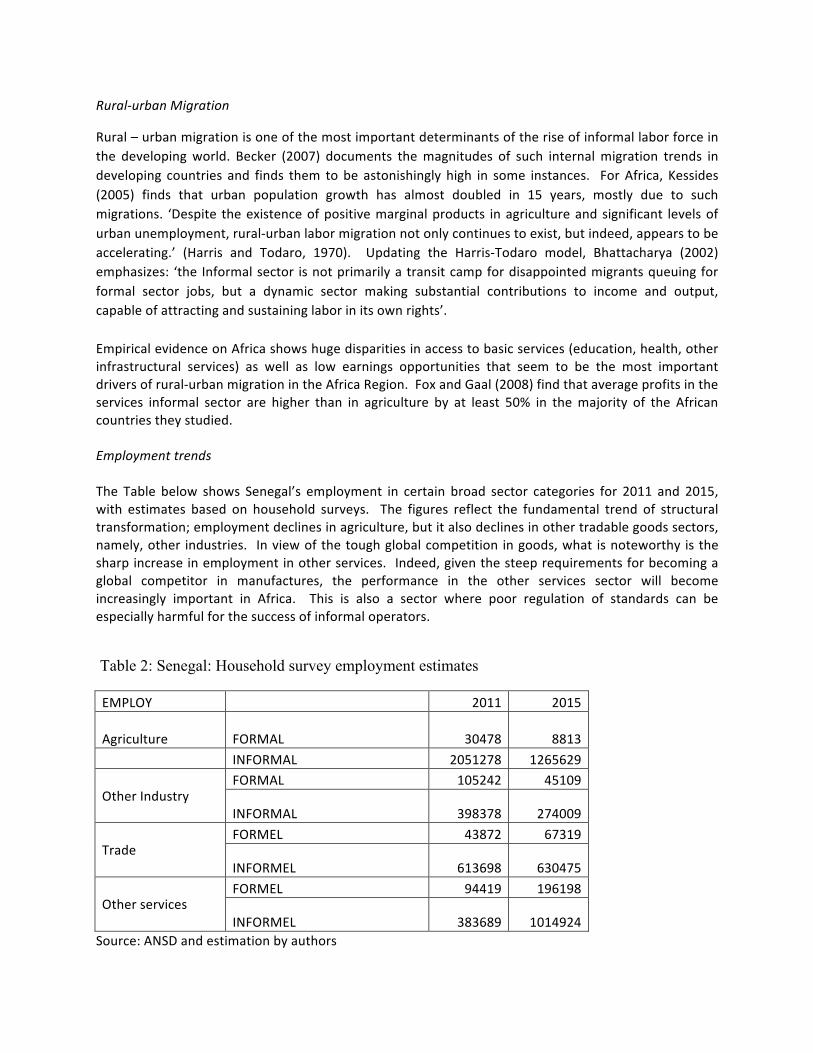

Inevitably,giventheirlowerproductivity,thecontributionofinformalworkerstoGDPislessthanproportionaltotheirnumbers.Agriculture2inSenegalisacaseinpoint:despiteemployingmorethan70%oftotallaborforce,itsshareofGDPisaslowas10%.MostfrancophoneWestAfricancountriesmakeestimatesoftheshareofGDPcontributedbyinformalproducersineachsector.BelowaretheestimatesforSenegal,BurkinaFasoandBenininthesecondaryandtertiarysectors.

2AgricultureinSenegalisalmostcompletelyinformal.

Figure 1 Share of value Added contributed by informal businesses in the secondary sector: Senegal

Sources:ANSD(2009)andestimationforauthorsforyears2010and2015

Figure 2: Share of value Added contributed by informal businesses in the secondary sector: Burkina Faso

Source:INSD(2009)andestimationbyauthorsforyears2010and2015

Figure 3: Share of value Added contributed by informal businesses in the secondary sector: Benin

Source:INSAE(2009et2014)andestimationbyauthorsforyear2015

Figure 4: Share of Value Added contributed by informal businesses in the tertiary sector: Senegal

Sources:ANSD(2009)andestimationforauthorsforyears2010and2015

Figure 5: Share of Value Added contributed by informal businesses in the tertiary sector: Burkina Faso

Source:INSD(2009)andestimationbyauthorsforyears2010and2015

Figure 6: Share of Value Added contributed by informal businesses in the tertiary sector: Benin

Source:INSAE(2009et2014)andestimationbyauthorsforyear2015

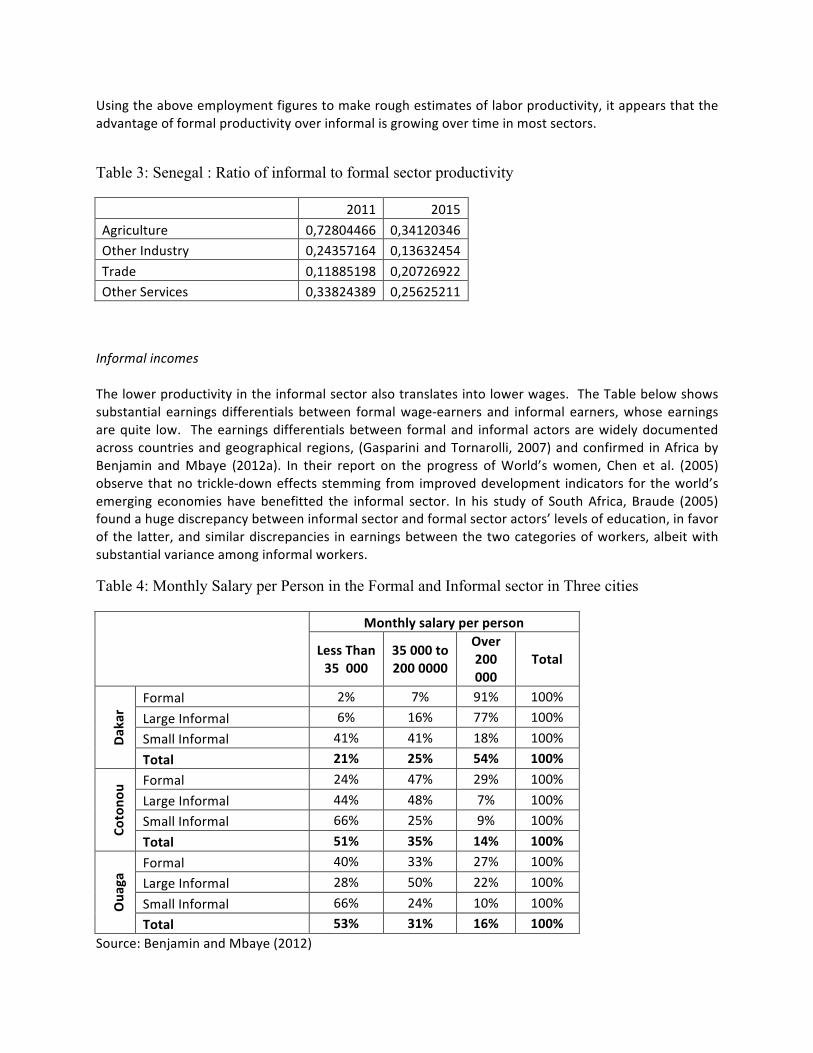

Rural-urbanMigration

Rural–urbanmigrationisoneofthemostimportantdeterminantsoftheriseofinformallaborforceinthe developingworld. Becker (2007) documents themagnitudes of such internalmigration trends indeveloping countries and finds them to be astonishingly high in some instances. ForAfrica, Kessides(2005) finds that urban population growth has almost doubled in 15 years, mostly due to suchmigrations. ‘Despite theexistenceofpositivemarginalproducts inagricultureandsignificant levelsofurbanunemployment,rural-urbanlabormigrationnotonlycontinuestoexist,butindeed,appearstobeaccelerating.’ (Harris and Todaro, 1970). Updating the Harris-Todaro model, Bhattacharya (2002)emphasizes: ‘the Informalsector isnotprimarilyatransitcampfordisappointedmigrantsqueuingforformal sector jobs, but a dynamic sector making substantial contributions to income and output,capableofattractingandsustaininglaborinitsownrights’.EmpiricalevidenceonAfricashowshugedisparitiesinaccesstobasicservices(education,health,otherinfrastructural services) as well as low earnings opportunities that seem to be the most importantdriversofrural-urbanmigrationintheAfricaRegion.FoxandGaal(2008)findthataverageprofitsintheservices informal sector are higher than in agriculture by at least 50% in themajority of the Africancountriestheystudied.EmploymenttrendsThe Table below shows Senegal’s employment in certain broad sector categories for 2011 and 2015,with estimates based on household surveys. The figures reflect the fundamental trend of structuraltransformation;employmentdeclinesinagriculture,butitalsodeclinesinothertradablegoodssectors,namely,other industries. Inviewofthetoughglobalcompetition ingoods,what isnoteworthy isthesharpincreaseinemploymentinotherservices.Indeed,giventhesteeprequirementsforbecomingaglobal competitor in manufactures, the performance in the other services sector will becomeincreasingly important in Africa. This is also a sector where poor regulation of standards can beespeciallyharmfulforthesuccessofinformaloperators.

Table 2: Senegal: Household survey employment estimates

EMPLOY 2011 2015Agriculture FORMAL 30478 8813 INFORMAL 2051278 1265629OtherIndustry

FORMAL 105242 45109

INFORMAL 398378 274009Trade

FORMEL 43872 67319

INFORMEL 613698 630475Otherservices

FORMEL 94419 196198

INFORMEL 383689 1014924Source:ANSDandestimationbyauthors

Usingtheaboveemploymentfigurestomakeroughestimatesoflaborproductivity,itappearsthattheadvantageofformalproductivityoverinformalisgrowingovertimeinmostsectors.

Table 3: Senegal : Ratio of informal to formal sector productivity

2011 2015

Agriculture 0,72804466 0,34120346OtherIndustry 0,24357164 0,13632454Trade 0,11885198 0,20726922OtherServices 0,33824389 0,25625211

InformalincomesThelowerproductivityintheinformalsectoralsotranslatesintolowerwages.TheTablebelowshowssubstantial earningsdifferentials between formalwage-earners and informal earners,whoseearningsarequite low. Theearningsdifferentialsbetween formaland informalactorsarewidelydocumentedacrosscountriesandgeographical regions, (GaspariniandTornarolli,2007)andconfirmed inAfricabyBenjamin andMbaye (2012a). In their report on the progress ofWorld’s women, Chen et al. (2005)observethatnotrickle-downeffectsstemming from improveddevelopment indicators for theworld’semerging economies have benefitted the informal sector. In his study of SouthAfrica, Braude (2005)foundahugediscrepancybetweeninformalsectorandformalsectoractors’levelsofeducation,infavorof the latter,andsimilardiscrepancies inearningsbetweenthetwocategoriesofworkers,albeitwithsubstantialvarianceamonginformalworkers.

Table 4: Monthly Salary per Person in the Formal and Informal sector in Three cities

Monthlysalaryperperson

LessThan35000

35000to2000000

Over200000

Total

Dakar

Formal 2% 7% 91% 100%LargeInformal 6% 16% 77% 100%SmallInformal 41% 41% 18% 100%Total 21% 25% 54% 100%

Cotono

u Formal 24% 47% 29% 100%LargeInformal 44% 48% 7% 100%SmallInformal 66% 25% 9% 100%Total 51% 35% 14% 100%

Oua

ga Formal 40% 33% 27% 100%

LargeInformal 28% 50% 22% 100%SmallInformal 66% 24% 10% 100%Total 53% 31% 16% 100%

Source:BenjaminandMbaye(2012)

Productivity

Productivity iscritical togrowthdynamics,anda large literatureshowsthatthere isastrongnegativecorrelation between informality and productivity of firms in developing countries. Factors explainingsuchadividearequitediverse. Gelbetal. (2009)emphasizethequalityof thebusinessenvironmentandtheenforcementof rules. Comparingcountries insouthernandeasternAfrica, theyconfirmthatformal sector firmsareonaveragemoreproductive than informalones,but thegapbetween formaland informal firms ismuch less for east African countries than for southern African countries. Theyconcludethattherelativeweaknessof thestate inEastAfricaunderminestheperformanceof formalfirmsandprovideslittleincentiveforstronginformalfirmstoformalize.

SteelandSnodgrass(2008)findthattheproductivitydifferentialbetweenformalandinformalfirmsisduemainlytounequalaccesstopublicservices.LaPortaandShleifer(2008),usingWorldBankinformalsectorsurveys,findthatoncetheycontrolforexpenditureoninputs,humancapitalofthetopmanagerand firm size, the factofbeingunregisteredhas little additional impactonproductivity. By contrast,Perry et al. (2007), find a residual negative impact of informality on productivity, even when othercharacteristicsarecontrolledfor.

Informalsectorstatusisahandicaptothefulldevelopmentofenterprises,forcingthemtooperatewithoutlegalprotection,andreducingtheiraccesstoawiderangeofancillarypublicandprivateservicessuchascredit,insurance,andgovernmentsupport.Thesefactorsmaycontributetotheproductivitydifferencesobservedbetweenformalandinformalfirmsandindicatethepotentialgainsfromstructuraltransformation.

Thelowerproductivityobservedforinformalfirmscomparedtoformaloneshasbeendocumentedinallregionsoftheworld,andwasconfirmedforWestAfricainBenjaminandMbaye,2012andinMbayeetal.2015.WhatisparticularabouttheresultsfromWestAfricaisthattheyreflectthelargeheterogeneityofproductivityacrosslargeandsmallinformalfirms.Informalfirmswereclassifiedaccordingtoacontinuumofcharacteristics,designatingthemas‘almostformal’,‘completelyinformal’,oroneofseveralstagesinbetween.Thusitwasfoundnotonlythatformalfirmshadhigherproductivitythaninformalones,butthatproductivitywascorrelatedwiththedegreeofinformality,wherethoseclosesttoformalityhadthehighestproductivityandthecompletelyinformalhadthelowest.

Thereissomeempiricalevidencetosuggestthatthiswiderangeofproductivityacrossfirmscancompoundthedifficultiesofprogramsdesignedtoraiseproductivitygrowth(Aghion,Bloom,Blundell,Griffith,andHowitt(2005).Somepoliciestrytofosterproductivitygrowthbyincreasingcompetitionasameanstopromoteefficiency.However,thisapproachmaynotbeeffectivewherethereisawidevarianceinfirms’attributesandproductivity.

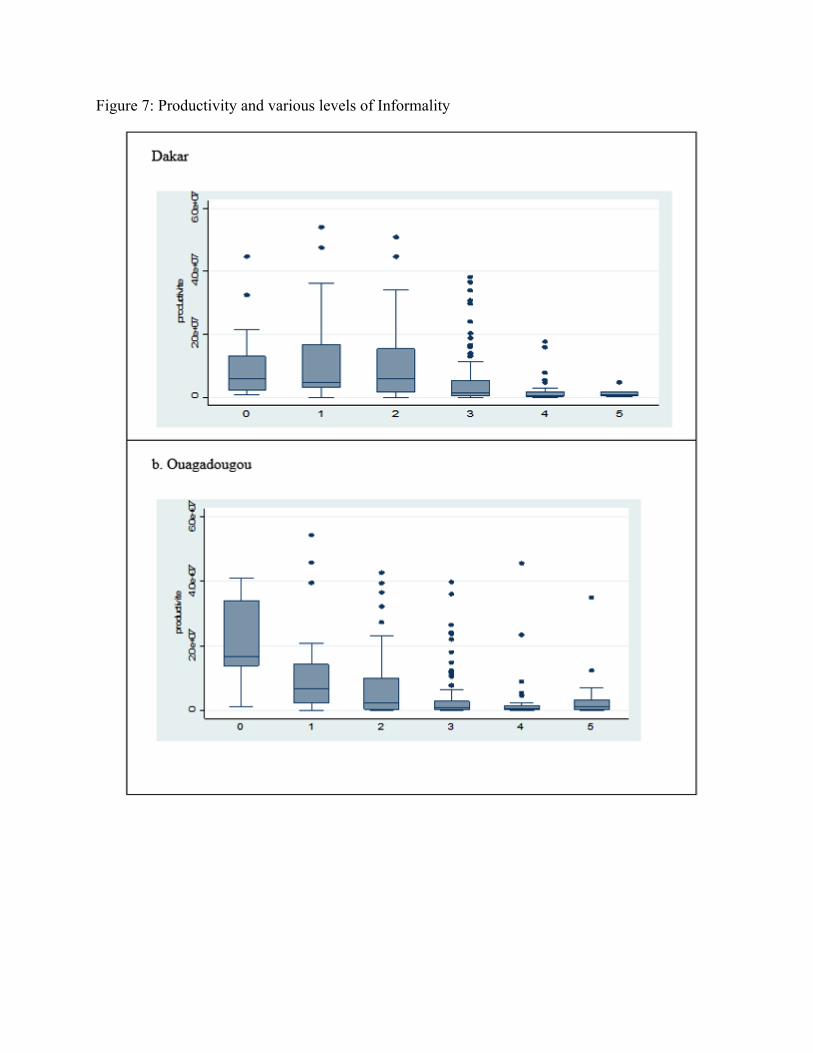

Mainstreamliteratureusesabinarydefinitionoftheinformalsector,classifyingfirmsaseitherbeingformalorinformal.BenjaminandMbaye(2012)arguethatthereisnosinglecriteriathatcanpersehighlightallthevariousandcomplexfeaturesofinformality.Instead,theyuseavarietyofcomplementarycriteriathatneedtobecombinedtocomeupwithacomprehensiveunderstandingofthephenomenon.Fiveofsuchcriteriaareconsideredintheanalysisrepresentedinthegraphsbelow:

thesizeofactivity,mobilityoftheworkplace,registration,taxation,andsincerityofaccounts.Combinationsofthesecriteriayieldseverallevelsofinformalityaccordingtothenumberofdefiningctiteriaagivenfirmfailstomeet.Atthebottomoftheladder,wehavefirmswhofailtomeetanyofthecriteriadefiningformality,andwhicharecompletelyinformal.Bycontrast,firmswhichmeetallcriteriadefiningformalityarecompletelyformal.Thissegmentationoftheinformalsectorhelpsusbetterunderstandtheconstraintsandchallengesattachedtoeachsegmentofinformalityanddesignmostappropriatepolicyresponsetoaddressthem.

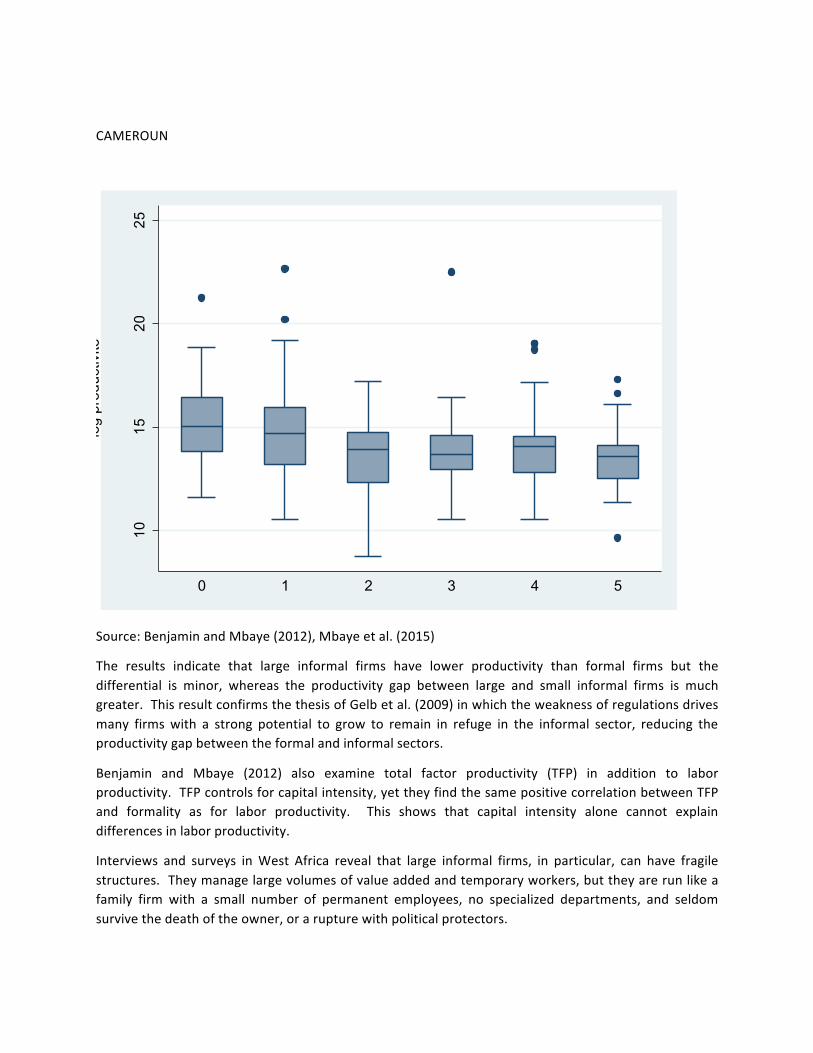

Weassumethatallinformalenterprisesexhibitatleastoneofthecharacteristicsabove.Adependentvariablecanthusbedefinedas0iftheenterpriseisformal,andthen1,2,3,4,or5accordingtothelevelofinformalityoftheenterprise.TheresultsindicatesignificantproductivitydifferentialsbetweenlargeandsmallinformalfirmsinWestAfrica.Figuresbelowdisplayboxplotsofthedistributionofproductivitylevelsfortheformalandinformalsectors,usingthecontinuousdefinitionofinformality.Thehorizontallinecrossingovereachrectangleismedianlaborproductivity.

Figure 7: Productivity and various levels of Informality

CAMEROUN

1015

2025

log

prod

uctiv

ité

0 1 2 3 4 5

Source:BenjaminandMbaye(2012),Mbayeetal.(2015)

The results indicate that large informal firms have lower productivity than formal firms but thedifferential is minor, whereas the productivity gap between large and small informal firms is muchgreater.ThisresultconfirmsthethesisofGelbetal.(2009)inwhichtheweaknessofregulationsdrivesmany firmswith a strong potential to grow to remain in refuge in the informal sector, reducing theproductivitygapbetweentheformalandinformalsectors.

Benjamin and Mbaye (2012) also examine total factor productivity (TFP) in addition to laborproductivity.TFPcontrolsforcapitalintensity,yettheyfindthesamepositivecorrelationbetweenTFPand formality as for labor productivity. This shows that capital intensity alone cannot explaindifferencesinlaborproductivity.

Interviews and surveys inWest Africa reveal that large informal firms, in particular, can have fragilestructures.Theymanagelargevolumesofvalueaddedandtemporaryworkers,buttheyarerunlikeafamily firm with a small number of permanent employees, no specialized departments, and seldomsurvivethedeathoftheowner,orarupturewithpoliticalprotectors.

The informal sector also relies on practices that hinder productivity growth. Their lower productivitymay be influenced by the fragility of management structures, lack of transparency of their ownaccounts, long-establishedtraditionsbasedonwell-entrenchedcontrolofterritoryandrents,andsub-optimalallocationofproductivefactors(includingrelianceonfamilysourcesforcredit).Informalityalsoprevents companies from acquiring modern management skills and worker training, limiting growthpotentialandaccesstotheworldmarket.Thustheinformalsectorcontributestoaninimicalinvestmentclimateforformalfirms,particularlyforeigninvestors.Further,theinformalsectoringeneralandlargeinformalfirmsinparticularareresponsibleforasubstantiallossoffiscalrevenuesandnarrowingofthetaxbase.

FactorcostsinWestAfrica

ThecostsofdoingbusinessinFrancophoneAfricaaresufficientlyhightoraisethequestionofhowfirmsintheformalsectormanagetosurvive.Indeed,withoutprotectionfromvariousprivilegesintheformoftaxorruleexemptionsorprotectedmarketpower,aformalbusinesswouldhardlysurvive.Apartfromtheinformalsector,themainsurvivingfirmsarethosecharacterizedbyahighlevelofprotectedrents.Below,weprovidesomedescriptionsoffactorcoststhatallcontributetomakeformalbusinessalmostimpossibletoupholdinfrancophoneAfrica.

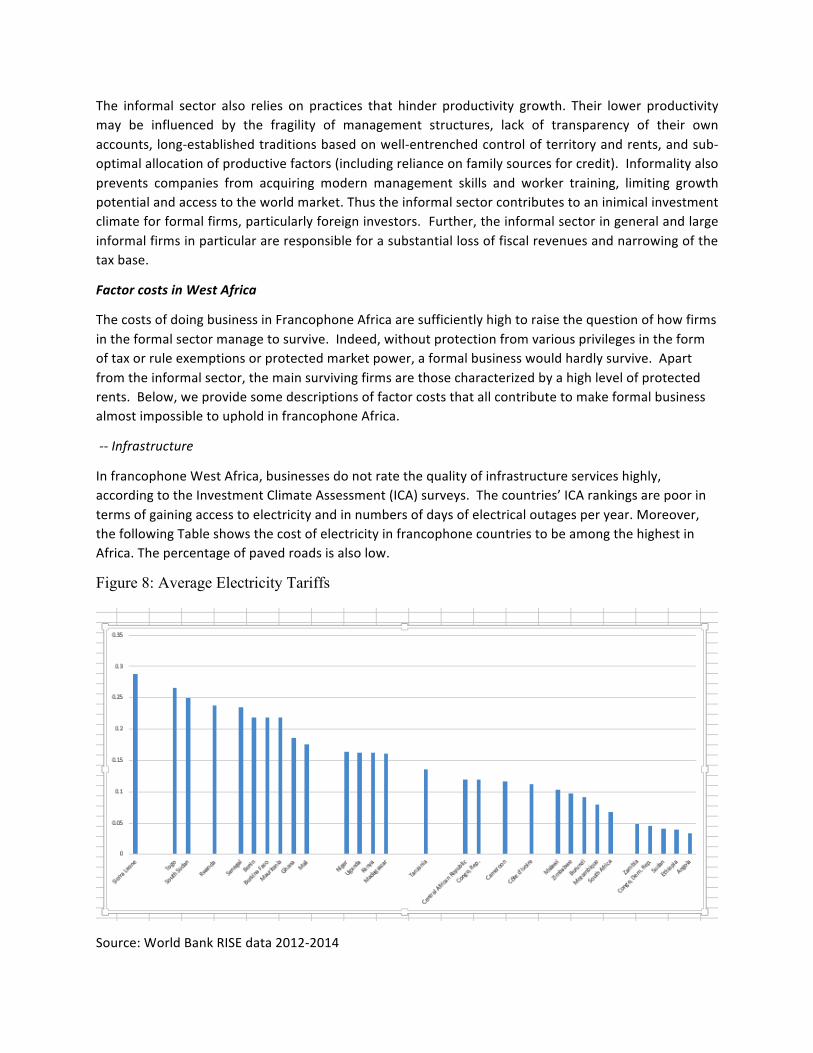

--Infrastructure

InfrancophoneWestAfrica,businessesdonotratethequalityofinfrastructureserviceshighly,accordingtotheInvestmentClimateAssessment(ICA)surveys.Thecountries’ICArankingsarepoorintermsofgainingaccesstoelectricityandinnumbersofdaysofelectricaloutagesperyear.Moreover,thefollowingTableshowsthecostofelectricityinfrancophonecountriestobeamongthehighestinAfrica.Thepercentageofpavedroadsisalsolow.

Figure 8: Average Electricity Tariffs

Source:WorldBankRISEdata2012-2014

FinancialCapital

WhilecommercialbanksinWestAfricaarefrequentlyseekingborrowers,potentialclientsintheinformaleconomyshowastrongpreferenceforothersourcesoffinancing.Resultsfromsurveysofinformalfirms(Mbayeetal,2015)indicateanoverwhelmingpreferenceforusingownsavings,retainedearnings,orloansfromfamilymembers.Eveninformalfirmsthatqualifyforbankloans,orthathavebankloansforsomefinancing,prefermorepersonalsourcesforthemajorityoffinancingneeds.

BankloansareexpensiveforallclientsinWestAfrica.Formalfirmsfrequentlypay15percentinterestwhileinformalfirmsreportpaying20percentormore.Further,mostfirmssurveyedreportdifficultyinrepayingloans,althoughthisismoreoftenthecaseforinformalfirms.

Labor

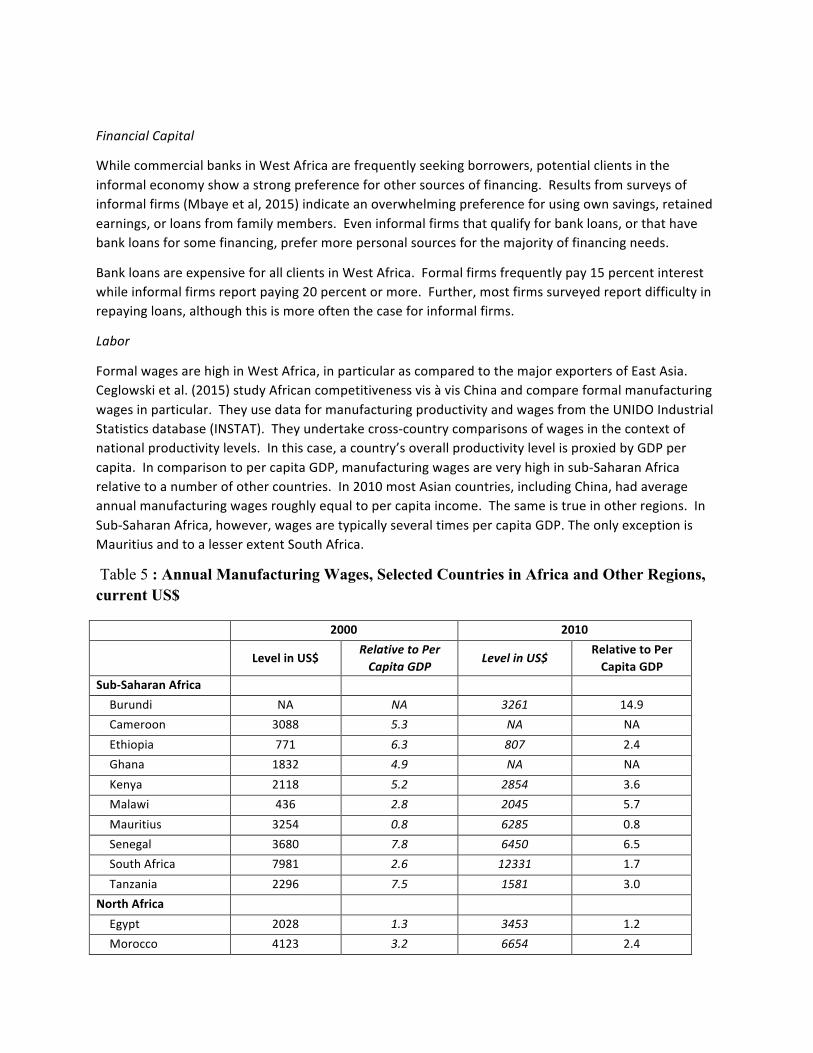

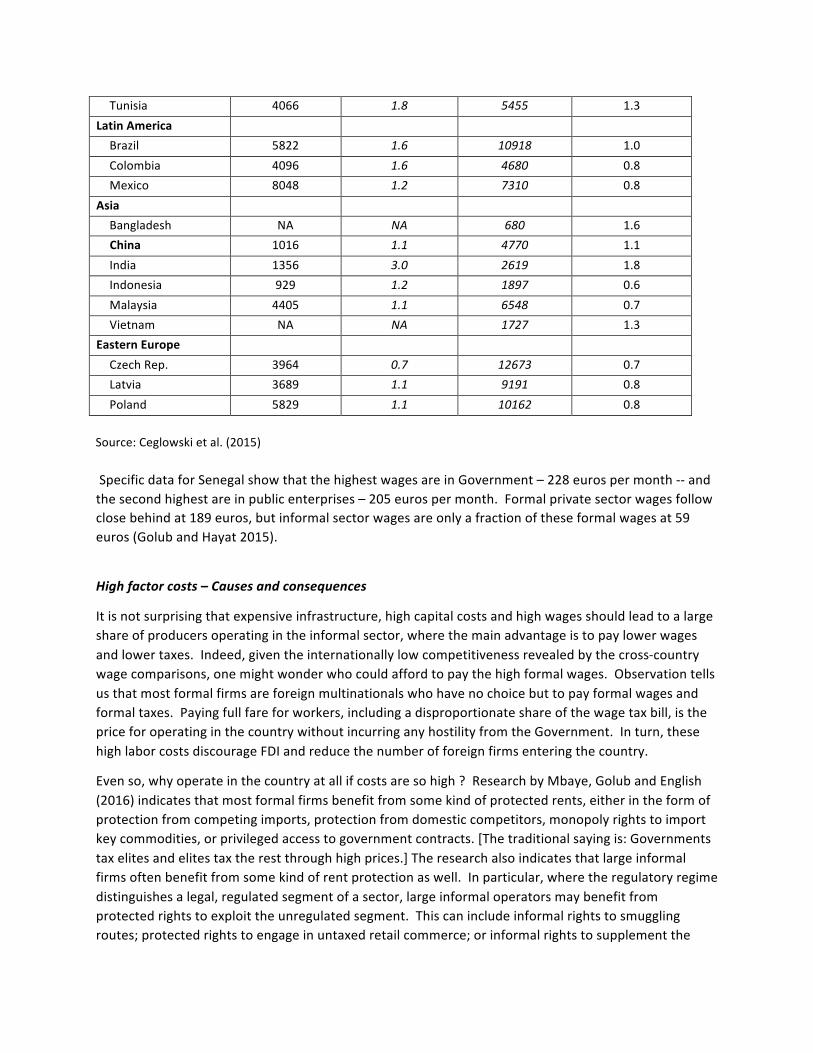

FormalwagesarehighinWestAfrica,inparticularascomparedtothemajorexportersofEastAsia.Ceglowskietal.(2015)studyAfricancompetitivenessvisàvisChinaandcompareformalmanufacturingwagesinparticular.TheyusedataformanufacturingproductivityandwagesfromtheUNIDOIndustrialStatisticsdatabase(INSTAT).Theyundertakecross-countrycomparisonsofwagesinthecontextofnationalproductivitylevels.Inthiscase,acountry’soverallproductivitylevelisproxiedbyGDPpercapita.IncomparisontopercapitaGDP,manufacturingwagesareveryhighinsub-SaharanAfricarelativetoanumberofothercountries.In2010mostAsiancountries,includingChina,hadaverageannualmanufacturingwagesroughlyequaltopercapitaincome.Thesameistrueinotherregions.InSub-SaharanAfrica,however,wagesaretypicallyseveraltimespercapitaGDP.TheonlyexceptionisMauritiusandtoalesserextentSouthAfrica.

Table 5 : Annual Manufacturing Wages, Selected Countries in Africa and Other Regions, current US$

2000 2010

LevelinUS$ RelativetoPerCapitaGDP LevelinUS$ RelativetoPer

CapitaGDPSub-SaharanAfrica Burundi NA NA 3261 14.9Cameroon 3088 5.3 NA NAEthiopia 771 6.3 807 2.4Ghana 1832 4.9 NA NAKenya 2118 5.2 2854 3.6Malawi 436 2.8 2045 5.7Mauritius 3254 0.8 6285 0.8Senegal 3680 7.8 6450 6.5SouthAfrica 7981 2.6 12331 1.7Tanzania 2296 7.5 1581 3.0

NorthAfrica Egypt 2028 1.3 3453 1.2Morocco 4123 3.2 6654 2.4

Tunisia 4066 1.8 5455 1.3LatinAmerica Brazil 5822 1.6 10918 1.0Colombia 4096 1.6 4680 0.8Mexico 8048 1.2 7310 0.8

Asia Bangladesh NA NA 680 1.6China 1016 1.1 4770 1.1India 1356 3.0 2619 1.8Indonesia 929 1.2 1897 0.6Malaysia 4405 1.1 6548 0.7Vietnam NA NA 1727 1.3

EasternEurope CzechRep. 3964 0.7 12673 0.7Latvia 3689 1.1 9191 0.8Poland 5829 1.1 10162 0.8

Source:Ceglowskietal.(2015)SpecificdataforSenegalshowthatthehighestwagesareinGovernment–228eurospermonth--andthesecondhighestareinpublicenterprises–205eurospermonth.Formalprivatesectorwagesfollowclosebehindat189euros,butinformalsectorwagesareonlyafractionoftheseformalwagesat59euros(GolubandHayat2015).

Highfactorcosts–Causesandconsequences

Itisnotsurprisingthatexpensiveinfrastructure,highcapitalcostsandhighwagesshouldleadtoalargeshareofproducersoperatingintheinformalsector,wherethemainadvantageistopaylowerwagesandlowertaxes.Indeed,giventheinternationallylowcompetitivenessrevealedbythecross-countrywagecomparisons,onemightwonderwhocouldaffordtopaythehighformalwages.Observationtellsusthatmostformalfirmsareforeignmultinationalswhohavenochoicebuttopayformalwagesandformaltaxes.Payingfullfareforworkers,includingadisproportionateshareofthewagetaxbill,isthepriceforoperatinginthecountrywithoutincurringanyhostilityfromtheGovernment.Inturn,thesehighlaborcostsdiscourageFDIandreducethenumberofforeignfirmsenteringthecountry.

Evenso,whyoperateinthecountryatallifcostsaresohigh?ResearchbyMbaye,GolubandEnglish(2016)indicatesthatmostformalfirmsbenefitfromsomekindofprotectedrents,eitherintheformofprotectionfromcompetingimports,protectionfromdomesticcompetitors,monopolyrightstoimportkeycommodities,orprivilegedaccesstogovernmentcontracts.[Thetraditionalsayingis:Governmentstaxelitesandelitestaxtherestthroughhighprices.]Theresearchalsoindicatesthatlargeinformalfirmsoftenbenefitfromsomekindofrentprotectionaswell.Inparticular,wheretheregulatoryregimedistinguishesalegal,regulatedsegmentofasector,largeinformaloperatorsmaybenefitfromprotectedrightstoexploittheunregulatedsegment.Thiscanincludeinformalrightstosmugglingroutes;protectedrightstoengageinuntaxedretailcommerce;orinformalrightstosupplementthe

rationedpublictransport(withvansormotorcycletaxis).Insomecases,theinformalparticipationofgovernmentofficialsinthebusinessmayhelpensurethisprotection.

Twothingsofnoteregardingtheseobservations:First,therentsassociatedwithtappingintotheaggregateconsumptionbundle,evenincountriesaspoorasthese,areworththeeffortsofformalfirmstocaptureaprotectedportionofthem.Second,whencertainfirmshavebeenallocatedaccesstoartificiallyhighrents,laborwillalwaysdemanditsshare(Azam,2001)).Thusthehighformalmanufacturingwagesmayreflectoverallprotectedrentsinthesector.

Thiskindofrentdistributionisnotunusualindevelopingcountries.Fornon-resourceexportingcountries,therentsderivefromaggregateconsumption.Whenacertainshareisallocatedtoasmallnumberofelitefirmsandtheirworkers,addinghighwagestotheotherexpensesofformaloperations,newentryofthesekindsofformalormodernenterprisescanbediscouragedandthemodernsectorcanstagnate.Aninterestingexamplecanbefoundintheliteraturede-bunkingthemyththattheDutchsufferedfromDutchdiseasefollowingtheexploitationofnaturalgasfieldsinthe1960sand70s.ThesubsequentstagnationofthetraditionalmanufacturingsectorintheNetherlandswasfoundnottoderivefromaforeignexchangewindfall,butratherfrompoliciesthatraisedsocialwelfarebenefits,leadingtohigherwagetaxesandaneconomy-wideincreaseinlaborcosts(seeKojo,2015andKremers,1986).WhiletheDutchpolicymayhaveinstigatedaneconomy-widelaborcostincrease,inWestAfrica,thehighwagesoccurinthepublicsectorandtheformalprivatesector.

Themessageforentrepreneursisclear:eithercultivateandcapturerentsoroperateintheinformalsector.Themessageformultinationalfirmsisalsoclear:donotcometothesecountriestomanufacturewithcheaplabor,becausetheformallaborisnotcheap.FromthelistinTable5above,onlyMauritius,withmanufacturingwagesclosetoGDP/capita,oroverallproductivity,hasastrongrecordasamanufacturingexporter,andEthiopiaonlyrecentlyso.ThemessageisalsoafamiliaroneinWestAfrica:controlofrentsismorelucrativethanraisingproductivity.

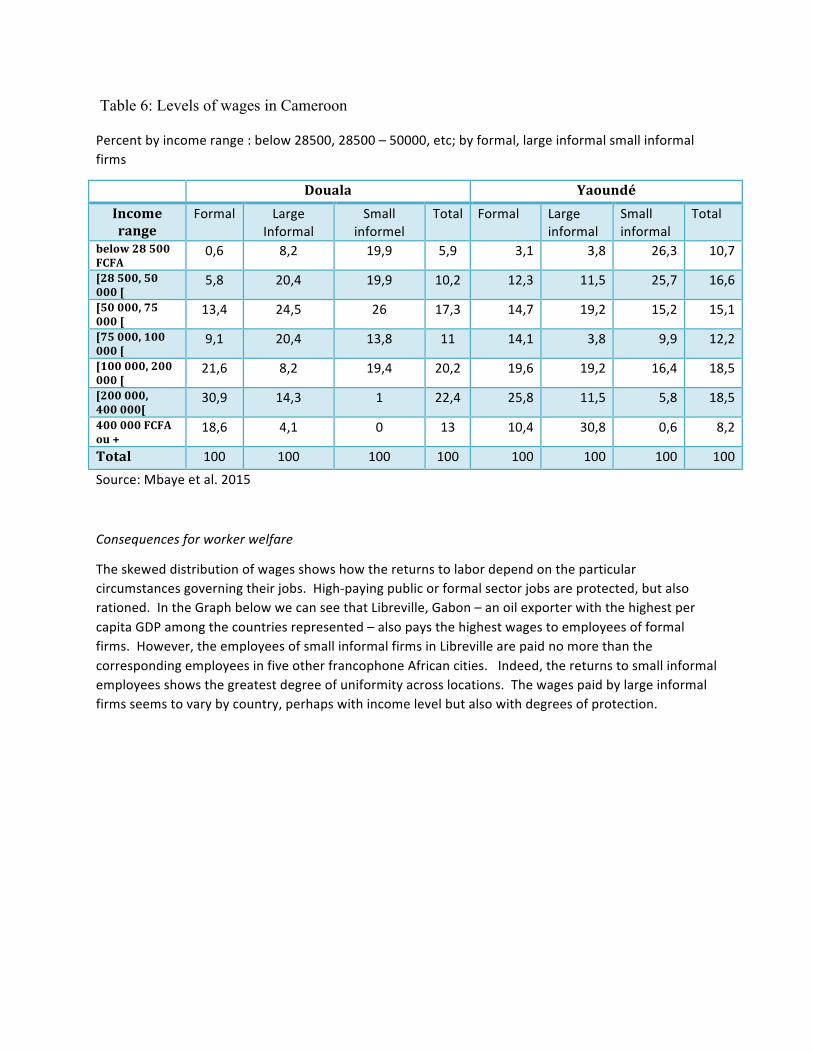

Giventhestrongadvantageofpayingthelower,informalwage,itisunderstandablethatformalfirmshirepeopleinformally–offthebooks–inadditiontotheirformallyregisteredworkers.Maintainingaformalveneermakesthecompanyeligibleforpubliccontracts,cheapercredit,morereliableinfrastructure,whileinformalhiringprovidesaccesstoworkersatalowerwage,andlowerwagetaxes.Thisoccursfrequentlyintheconstructionsectorwhereformalcompaniesbidonprojects,butinformalworkersprovidemuchofthelabor.LaborsurveysinNorthAfricaindicatethatamajorityofthepeoplewhoreportbeinginformallyemployedareinfactworkingforformalcompanies(Gattietal.2011).EvidencefromCentralWestAfricashowsthatformalfirmsarepayingimportantsharesoftheirworkersatlessthantheofficialminimumwage.(SeeTable6below):

Table 6: Levels of wages in Cameroon

Percentbyincomerange:below28500,28500–50000,etc;byformal,largeinformalsmallinformalfirms

Douala YaoundéIncomerange

Formal LargeInformal

Smallinformel

Total Formal Largeinformal

Smallinformal

Total

below28500FCFA

0,6 8,2 19,9 5,9 3,1 3,8 26,3 10,7

[28500,50000[

5,8 20,4 19,9 10,2 12,3 11,5 25,7 16,6

[50000,75000[

13,4 24,5 26 17,3 14,7 19,2 15,2 15,1

[75000,100000[

9,1 20,4 13,8 11 14,1 3,8 9,9 12,2

[100000,200000[

21,6 8,2 19,4 20,2 19,6 19,2 16,4 18,5

[200000,400000[

30,9 14,3 1 22,4 25,8 11,5 5,8 18,5

400000FCFAou+

18,6 4,1 0 13 10,4 30,8 0,6 8,2

Total 100 100 100 100 100 100 100 100Source:Mbayeetal.2015

Consequencesforworkerwelfare

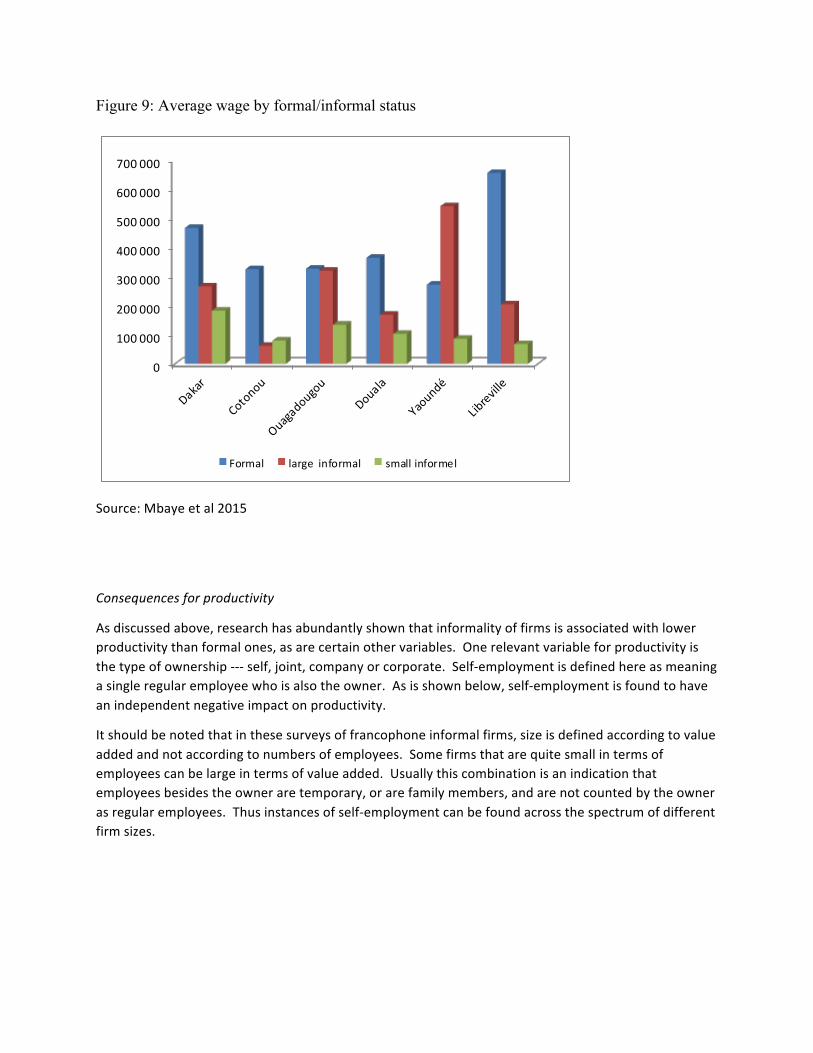

Theskeweddistributionofwagesshowshowthereturnstolabordependontheparticularcircumstancesgoverningtheirjobs.High-payingpublicorformalsectorjobsareprotected,butalsorationed.IntheGraphbelowwecanseethatLibreville,Gabon–anoilexporterwiththehighestpercapitaGDPamongthecountriesrepresented–alsopaysthehighestwagestoemployeesofformalfirms.However,theemployeesofsmallinformalfirmsinLibrevillearepaidnomorethanthecorrespondingemployeesinfiveotherfrancophoneAfricancities.Indeed,thereturnstosmallinformalemployeesshowsthegreatestdegreeofuniformityacrosslocations.Thewagespaidbylargeinformalfirmsseemstovarybycountry,perhapswithincomelevelbutalsowithdegreesofprotection.

Figure 9: Average wage by formal/informal status

0

100000

200000

300000

400000

500000

600000

700000

Formal largeinformal smallinformel

Source:Mbayeetal2015

Consequencesforproductivity

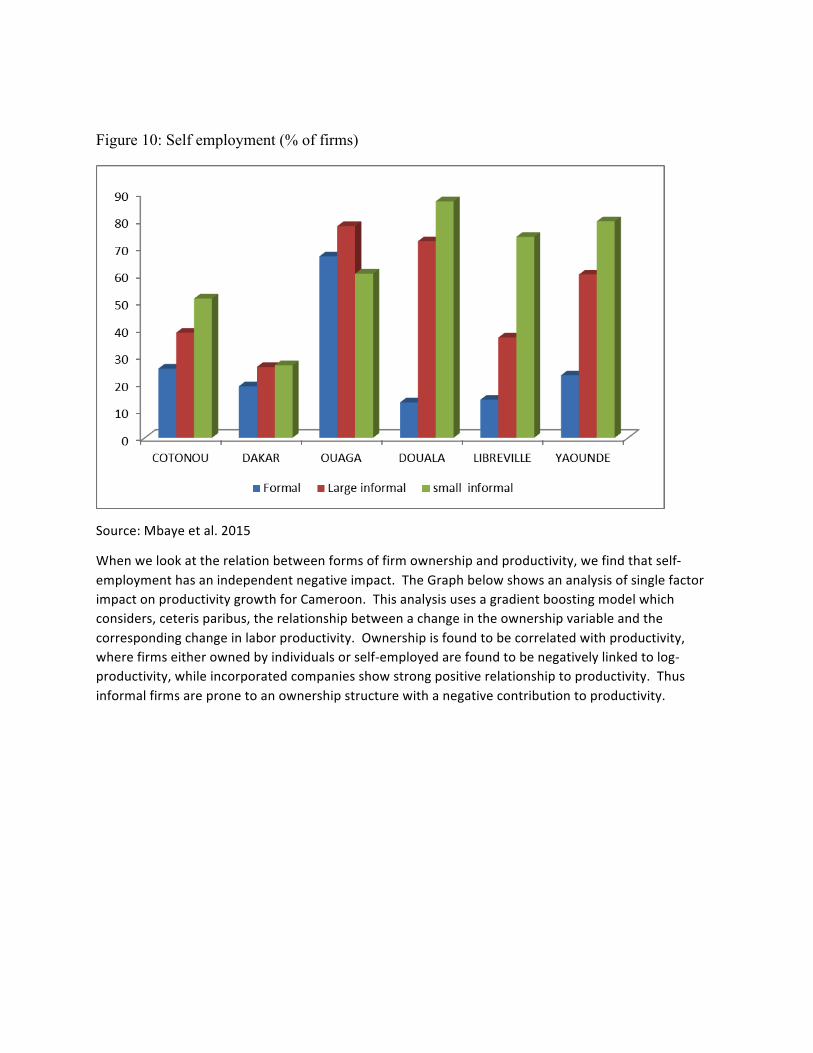

Asdiscussedabove,researchhasabundantlyshownthatinformalityoffirmsisassociatedwithlowerproductivitythanformalones,asarecertainothervariables.Onerelevantvariableforproductivityisthetypeofownership---self,joint,companyorcorporate.Self-employmentisdefinedhereasmeaningasingleregularemployeewhoisalsotheowner.Asisshownbelow,self-employmentisfoundtohaveanindependentnegativeimpactonproductivity.

Itshouldbenotedthatinthesesurveysoffrancophoneinformalfirms,sizeisdefinedaccordingtovalueaddedandnotaccordingtonumbersofemployees.Somefirmsthatarequitesmallintermsofemployeescanbelargeintermsofvalueadded.Usuallythiscombinationisanindicationthatemployeesbesidestheowneraretemporary,orarefamilymembers,andarenotcountedbytheownerasregularemployees.Thusinstancesofself-employmentcanbefoundacrossthespectrumofdifferentfirmsizes.

Figure 10: Self employment (% of firms)

Source:Mbayeetal.2015

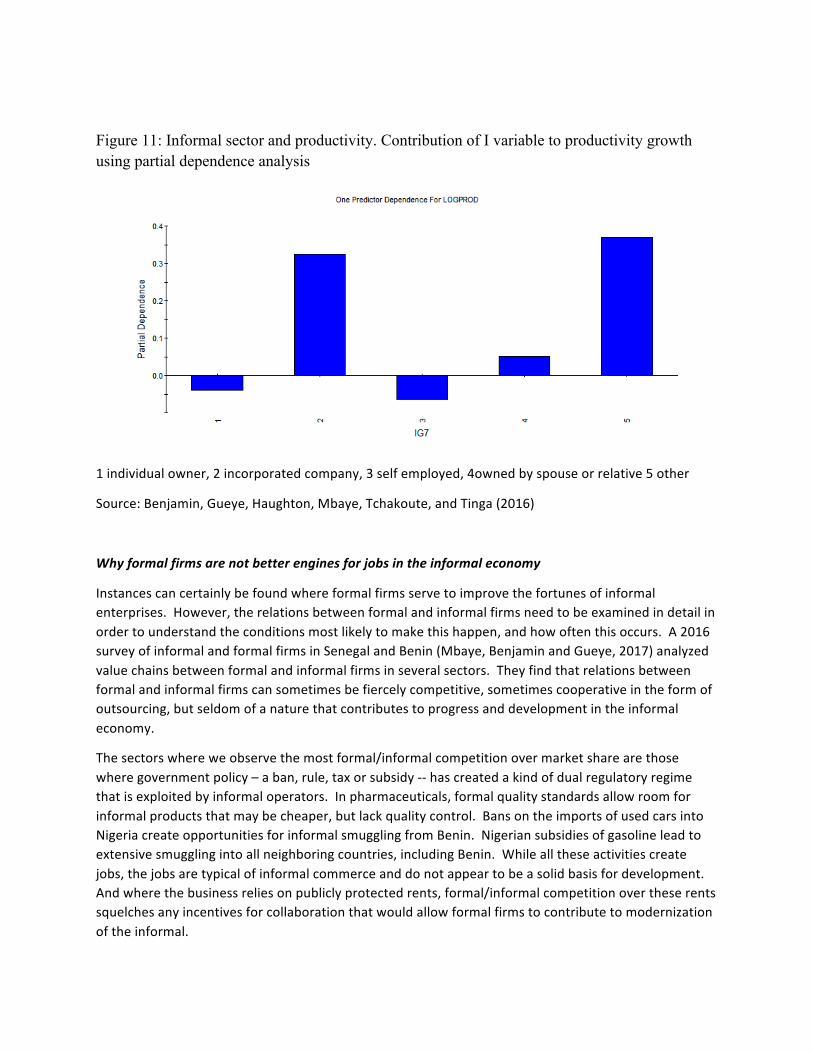

Whenwelookattherelationbetweenformsoffirmownershipandproductivity,wefindthatself-employmenthasanindependentnegativeimpact.TheGraphbelowshowsananalysisofsinglefactorimpactonproductivitygrowthforCameroon.Thisanalysisusesagradientboostingmodelwhichconsiders,ceterisparibus,therelationshipbetweenachangeintheownershipvariableandthecorrespondingchangeinlaborproductivity.Ownershipisfoundtobecorrelatedwithproductivity,wherefirmseitherownedbyindividualsorself-employedarefoundtobenegativelylinkedtolog-productivity,whileincorporatedcompaniesshowstrongpositiverelationshiptoproductivity.Thusinformalfirmsarepronetoanownershipstructurewithanegativecontributiontoproductivity.

Figure 11: Informal sector and productivity. Contribution of I variable to productivity growth using partial dependence analysis

1individualowner,2incorporatedcompany,3selfemployed,4ownedbyspouseorrelative5other

Source:Benjamin,Gueye,Haughton,Mbaye,Tchakoute,andTinga(2016)

Whyformalfirmsarenotbetterenginesforjobsintheinformaleconomy

Instancescancertainlybefoundwhereformalfirmsservetoimprovethefortunesofinformalenterprises.However,therelationsbetweenformalandinformalfirmsneedtobeexaminedindetailinordertounderstandtheconditionsmostlikelytomakethishappen,andhowoftenthisoccurs.A2016surveyofinformalandformalfirmsinSenegalandBenin(Mbaye,BenjaminandGueye,2017)analyzedvaluechainsbetweenformalandinformalfirmsinseveralsectors.Theyfindthatrelationsbetweenformalandinformalfirmscansometimesbefiercelycompetitive,sometimescooperativeintheformofoutsourcing,butseldomofanaturethatcontributestoprogressanddevelopmentintheinformaleconomy.

Thesectorswhereweobservethemostformal/informalcompetitionovermarketsharearethosewheregovernmentpolicy–aban,rule,taxorsubsidy--hascreatedakindofdualregulatoryregimethatisexploitedbyinformaloperators.Inpharmaceuticals,formalqualitystandardsallowroomforinformalproductsthatmaybecheaper,butlackqualitycontrol.BansontheimportsofusedcarsintoNigeriacreateopportunitiesforinformalsmugglingfromBenin.Nigeriansubsidiesofgasolineleadtoextensivesmugglingintoallneighboringcountries,includingBenin.Whilealltheseactivitiescreatejobs,thejobsaretypicalofinformalcommerceanddonotappeartobeasolidbasisfordevelopment.Andwherethebusinessreliesonpubliclyprotectedrents,formal/informalcompetitionovertheserentssquelchesanyincentivesforcollaborationthatwouldallowformalfirmstocontributetomodernizationoftheinformal.

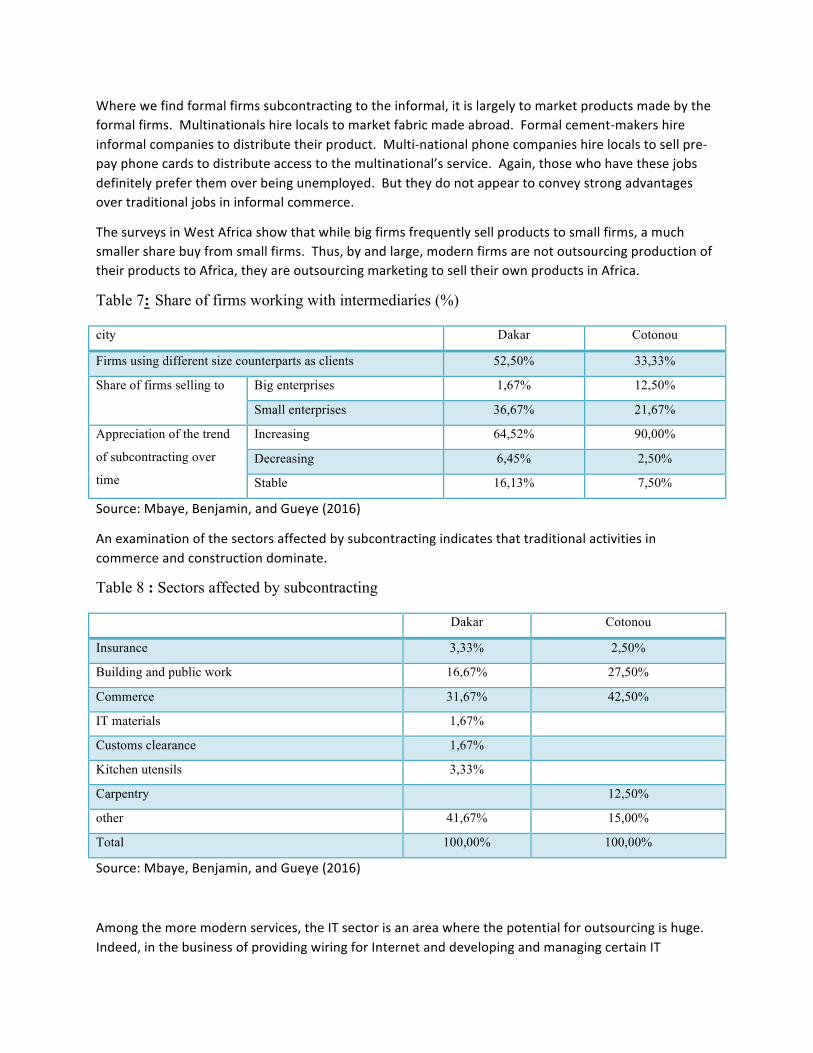

Wherewefindformalfirmssubcontractingtotheinformal,itislargelytomarketproductsmadebytheformalfirms.Multinationalshirelocalstomarketfabricmadeabroad.Formalcement-makershireinformalcompaniestodistributetheirproduct.Multi-nationalphonecompanieshirelocalstosellpre-payphonecardstodistributeaccesstothemultinational’sservice.Again,thosewhohavethesejobsdefinitelypreferthemoverbeingunemployed.Buttheydonotappeartoconveystrongadvantagesovertraditionaljobsininformalcommerce.

ThesurveysinWestAfricashowthatwhilebigfirmsfrequentlysellproductstosmallfirms,amuchsmallersharebuyfromsmallfirms.Thus,byandlarge,modernfirmsarenotoutsourcingproductionoftheirproductstoAfrica,theyareoutsourcingmarketingtoselltheirownproductsinAfrica.

Table 7: Share of firms working with intermediaries (%)

city Dakar Cotonou

Firms using different size counterparts as clients 52,50% 33,33%

Share of firms selling to Big enterprises 1,67% 12,50%

Small enterprises 36,67% 21,67%

Appreciation of the trend

of subcontracting over

time

Increasing 64,52% 90,00%

Decreasing 6,45% 2,50%

Stable 16,13% 7,50%

Source:Mbaye,Benjamin,andGueye(2016)

Anexaminationofthesectorsaffectedbysubcontractingindicatesthattraditionalactivitiesincommerceandconstructiondominate.

Table 8 : Sectors affected by subcontracting

Dakar Cotonou

Insurance 3,33% 2,50%

Building and public work 16,67% 27,50%

Commerce 31,67% 42,50%

IT materials 1,67%

Customs clearance 1,67%

Kitchen utensils 3,33%

Carpentry 12,50%

other 41,67% 15,00%

Total 100,00% 100,00%

Source:Mbaye,Benjamin,andGueye(2016)

Amongthemoremodernservices,theITsectorisanareawherethepotentialforoutsourcingishuge.Indeed,inthebusinessofprovidingwiringforInternetanddevelopingandmanagingcertainIT

applications,thereisroomformajoroperatorstosubcontracttosmallerones.Inthesub-region,mosttelephonecompaniesaremultinationalcorporationsthatcoexistwithanumberoflocalactorsintheITbusinesssubsector,mainlySME’s.Ingeneral,theseSMEsareinthebusinessofdevelopingsoftwareapplications,salesofcomputerhardware,computerwiring,computernetworkmanagement,etc.Theyoftencomplainthatlargeoperatorsdonotgivethemenoughwork.Instead,largeoperatorsprefertobringtechniciansonsitefromtheparentcompany.MostSMEITmanagersinterviewedinthecontextoffirmsurveysexpressedtheirfrustrationatnothavingaccesstothesecontracts.Accordingtothem,thereisaseriouscorruptionproblemwithbriberyinbothpublicandtheprivatesectorbids.Thiscanraisethemarketpricesbyupto30%.Theyalsonotethatpoliticiansquietlygetinvolvedinthesebusinessesandtakepersonaladvantage,byplayingtheirconnectionsinboththepublicandprivatesectors.Atthesametime,largetelecomoperatorsandsomeadministrativeofficialsblamethelowcapacityoflocalSMEstoproperlyexecutethetaskssuitableforsubcontracting.

Implicationsforstructuraltransformation

Structuraltransformationtrackstheevolutionofeconomiesasworkersmigrateoutofagriculture,manyatfirstintomanufacturing,andthen,asmanufacturingplateaus,systematicallyintoservices.Evidenceshows(SeeHerrendorf,RogersonandValentinyi,2013)thattheplateauinmanufacturingemploymentoccursataboutthesameLogofGDPpercapitaintoday’sdevelopingcountriesasitdidindevelopedeconomies.However,itdoesnotseemtobeoccurringatthesamerespectivedegreeofdevelopmentormodernization.Thelevellingoff,orevencontractionofmanufacturinginAfricaisoccurringatlowlevelsofproductivityandnationalincome.(SeeRodrik,‘PrematureDeindustrialization’,2015.)Theexodusfromagriculturecontinues,butthesemigratingworkerslargelyendupinlow-productivityinformalservicesandmanufacturing,andconnectionstothemodernsectorarenotstrong.Informalurbanincomesexceedthoseofsubsistenceagriculture,butarenotnecessarilycontributingtorisingproductivity.

Hendersonetal.(2016)havepointedoutthatdevelopedcountrieswhounderwentstructuraltransformationonehundredtotwohundredyearsago,didsoatatimewhentransportationcostswerestillhigh,andthuslocaldemandgaverisetolocalproduction.Atpresent,lowertransportcostsandglobalizedproductionhavelandedcheapconsumergoodsateveryone’sdoor,limitingtheneedforlocalproduction.AsFoxetal(2013)andothershaveobserved,currentdemographictrendsindicatethatthemodernsectorinAfricawillnotbeabletoabsorbthemigrationoutofagriculturefordecadestocome.Thusinformalityplaysanimportantroleinpresent-daystructuraltransformation,notonlyinabsorbingthebulkoftransitioningworkers,butalsoinprovidingcluesastowhymodernizationisnotkeepingpaceandwherepolicycanbemostconstructive.

Manyofthepertinentissuescomeunderthedomainofgovernanceandeconomicmanagement.WestAfricangovernmentshavenotbeensuccessfulinprovidingforreliableinfrastructureatreasonableprices.Thesagasofseveralnetworkutilitiesprovideabundantevidencethatrent-seekinginterfereswithservicedelivery.Inthecapitalmarkets,poorcontractenforcementleadstohighborrowingcosts.Similarly,Governmentactsasthegatekeepertoformal,legaloperationsoffirmsintheircountries,andthisleadstohighformalwagesandstagnationofformalmanufacturing.Italsoleadstoakindofdualregulatoryregimewhereformalfirmsfollowformalrulesandinformalfirms,unabletomeetthesestandards,areonlypartiallyregulated.Someinstitutionalarrangementsaredesignedspecificallytoaccommodateinformalfirms,suchasthepresumptivetaxregimethatispracticedinmostFrancophone

Africancountries.However,looseenforcementofaccountingstandardsandlaxcross-checkingacrossdifferentagenciesleadtoabundantabusesoftheseregimes(SeeBenjaminandMbaye,RDE2012).Inparticular,largeinformalfirmswithhighrevenuesfindwaystopayminimaltaxesunderthelowerpresumptivetaxregime.

Evenso,theinformaleconomystillhascollectiveneedsthatarenotservedbytheformalregime.Healthinsuranceandpensionsareparticularlylacking.Certificationofqualificationsforworkersisaproblem,especiallyinconstruction.Laggingcertificationofstandardsforservicesisalsoabarriertomodernization,asobservedintheITCsector.

Theinformaleconomycarriestheadvantagesofallowingopenentry,andprovidingopportunitiesforthosewithlittleeducationandnocapital.However,thisopenentrygenerateslargenumbersoffirmsoperatingatlowproductivity,withownershipormanagementstructuresthatresistmodernsystems.Eventhelargeandsophisticatedinformalfirms,closeinproductivitytoformalfirms,stilltendtooperatelikefamilyfirmsinwaysthatkeepthembelowtheefficiencylevelsoftheirformalcounterparts.

Recommendations

Whilethecharacteristicsoftheinformaleconomycanhelppointupsomeweaklinksinthemodernizationprocess,itcanalsoindicatepointsofentrywherepolicycanhelpraisethereturnstofactorsoperatinginthesector,thelargestemployerintheFrancophoneAfricaneconomies.Themostdirectapproachistoraisethecapacityofinformalworkers,includingbasiceducationandsomevocationaltraining.TraininginbusinessmanagementforSMEshasadecidedlymoremixedrecord,butincertaintargetedinstances,suchasITC,itcouldhelp.

Policyregardingformalizationshouldfocusratheronthelargeinformalfirms.Thesealreadyhavethecapacitytofunctionlikeformalfirms,andamorerule-basedregulatoryenforcementcouldbringthemintothebaseofformalfirmsandformaltax-payers.Itishighlydifficultforanygovernmenttoimplementasoliddevelopmentstrategywhenmostmajorplayersareallowedtooperateoutsidethesystem.Stricterrulesshouldalsoapplytogovernmentofficialsinvolvedinpublicorprivatebusinesses.

Betweenthelargeinformalfirmsthatcouldbeformalizedandthemicro-enterprisesthatneedbasicassistance,thereisalargesegmentoffirmsthatarenotclosetobeingabletofollowformalrules,butthatstillneedpublicgoodsandcollectiveservices.Importantaspectsofthesefirms’performance--productivity,profitability,employment,longevity--canbeimprovedalongtheinformalityspectrum,withoutrestrictingeitherpolicyorresultstoasimpleformal-informaldichotomy.Whilealloftheseaspectsoffirmperformanceareimportant,theissuesofproductivityandemploymenthavethegreatestsocialimpact.Forthesefirms,policyshouldfocuslessonregistrationandtaxesandmoreonwhatinhibitsmodernizationandaccesstothebenefitsofmodernity.

Whenpresentedwiththeoptionofbeingformalorinformal,thesesemi-informalfirmshardlyhaveachoice.Andyetsurveysandinterviewstellusthattherearemanyintermediatebargainstheywouldbewillingtomake.Whilefirmswantbettergovernanceandbetterpublicservices,governmentswantbettertaxcompliance(asdocomplianttax-payingfirms).Apublic-privatebargaincanenhancebothpublicperformanceandprivateparticipationintheformalregulatoryregime,includingcontributionstopublicfinances.Thedialogueonthismutualneedforreformmustincludebroadparticipationfromtheinformaleconomyandnotbeconfinedtoconstituentsfocusedondefendingthestatusquo.

Mostinformalfirmswouldbewillingtopayalittlemoreinpubliccontributionsiftheycouldbeguaranteedanincreaseinpublicservices.Wheretrustinthepublicsectorislow,Governmentmayneedtomakethefirstmove.Thespecificservicesthatsmallinformalbusinessesrequestvaryacrosslocationsandacrosssectors,sothereremainsanimportanttaskoflearningaboutthetypeofpublicserviceimprovementsmostsoughtbyinformalfirmsandworkers.

Morocco,forexample,haslaunchedapublicprogramthatsubsidizessocialinsuranceforinformalworkers.WhileGovernmentendsupwiththebillforthesocialinsurance,itencouragesinformalworkerstoformallyregister,soatleasttheGovernmentknowsaboutthem.

Inthecapitalmarkets,itisimportanttorecognizethatmostformalcreditinstrumentsdonotmatchthehigh-risknatureofinformalbusinesses,hencetheweakresponsetomicro-creditprogramsandthestrongerpreferenceformorepersonalsourcesoffinancing.Thehigh-riskcharacterofinformalbusinessincomeandtheirinabilitytoforfeitcollateralneedtobetakenintoaccountwhenfindingwaystoincreaseaccesstocredit.

Finally,governmentsneedtore-examinethestructureofprotectedrentsandwages.Therelativeincentivesofproductivitygrowthversusrentcaptureneedtoberebalanced.Structuraltransformationinthecurrentglobalizedeconomyrequiresanewviewofhowdevelopingcountriescanprovideawelcomeenvironmentformodernizingforceswhileensuringthewelfareofitsinformalworkers.

Prospects

Theinformaleconomyhas,andwillcontinuetohaveasubstantialroleinstructuraltransformationinAfrica.Butwhileitcontinuestoabsorbworkersmigratingoutoflow-productivityagriculture,itwillalsolimitthepotentialforgrowthandproductivityuntilmodernizingforcesexertmoreinfluence.Thelargeorsophisticatedfirmscanbeexpectedtoformalizeasgovernmentsaremoresystematicinensuringthebenefitstothosethatdoso.FormalwagesmaycontinuetodeclinetowardpercapitaGDP,andthismightmakemoreAfricanlocationscompetitiveforinternationalgrademanufactures.Butregardless,governmentsshouldfocusonimprovingtheregulatoryenvironmentfornon-retailservices,includingITC,asthesesectorscanmakeimportantcontributionstomodernization.Experienceinprovidingpublicservicestothemiddlelayerofinformalbusinessesandtheirworkersshouldimprovetheircivicparticipationandgenerateefficienciesfromextendingthecoverageoftheregulatoryframework.However,institutionsthatrestrictallocationsofrentswillneedtobecheckedtoavoidcounteractingmodernization.

References

Aghion,P.,N.Bloom,R.Blundell,R.Griffith,andP.Howitt.(2005)“CompetitionandInnovation:AnInverted-URelationship.”TheQuarterlyJournalofEconomics.

Azam,J-P,andRis,C.(2001).“Rent-sharing,hold-up,andmanufacturingwagesinCoted'Ivoire,”WashingtonDC:WorldBank.

Becker,KristinaF.(2004).TheInformalEconomy.Stockholm:SIDAPublications.

Benjamin,N.andMbaye,A.A.(2012).TheInformalSectorinFrancophoneAfrica:FirmSize,ProductivityandInstitutions,WashingtonDC:WorldBank.

Benjamin,N.andMbaye,A.A.(2012).«Informality,Productivity,andEnforcementinWestAfrica:AFirm-LevelAnalysis,”ReviewofDevelopmentEconomics.Benjamin,N.,Gueye,F.,Haughton,D.,Mbaye,A.A.,Tchakoute,R.,andTinga,M.,(2016).«TheInformalSectorinCameroon:PracticesandProductivity,”WorldBank.Benjamin,N.,Golub,S.S.andMbaye,A.A(2014).“Informality,RegionalIntegrationandSmugglinginWestAfrica,”JournalofBorderlandStudies.

Bhattacharya, P.C., (2002). “Rural-to-urban migration in LDCS: a test of two rival models, Journal ofInternationalDevelopment,JohnWiley&Sons,Ltd?Vol.14(7à,pages951-972.

Braude, W. (2005); «South Africa: bringing informal workers into the regulated sphere,overcomingApartheid’slegacy»,inAvirganetal.(Eds.)Ceglowski,J., Golub, S., Mbaye, A.A., Prasad, A., (2016) “Can Africa Compete with China inManufacturing?TheRoleofRelativeUnitLaborCosts,”DPRUWorkingPaper.

Chen,M.(2006)“TheInformalEconomy.”TheInternationalEncyclopediaofOrganizationStudies,

Chen,M.A.(2001).«WomenintheInformalSector:aGlobalPicture,theGlobalMovement».SAISReview,Winter-Spring.

Chen,M.,J.Vanek,F.Lund,J.Heintz,R.Jhabvala,andC.Bonner(2005).‘ProgressoftheWorld’sWomen2005:Women,WorkandPoverty’.NewYork:UnitedNationsDevelopmentFundforWomen.

Chen,M.A.(2006).RethinkingtheInformalEconomy:LinkageswiththeFormalEconomyandtheFormalRegulatoryEnvironment.InB.Guha-Khasnobis,R.Kanbur,E.Ostrom(eds),LinkingtheFormalandInformalEconomy–ConceptsandPolicies.Oxford:OxfordUniversityPress,pp.75-92.

Fox, L., and M. Gaal, (2008). WorkingOutofPoverty:JobCreationandtheQualityofGrowthinAfrica,WorldBank.

Fox,L.,A.Thomas,C.HainesandJ.Huerta(2013)Africa’sGotWorktoDo:EmploymentProspectsintheNewCentury.WorldBankandIMFGasparini,L.,andL.Tornarolli(2007).‘LaborInformalityinLatinAmericaandtheCaribbean:PatternsandTrendsfromHouseholdSurveyMicrodata’.CEDLASWorkingPaper0046.LaPlata:CentrodeEstudiosDistributivos,LaboralesySociales.

Gelb, A., Mengistae, T., Ramachandran, V., and Shah, M.K. (2009) “To Formalize or Not toFormalize?ComparisonsofMicroenterprisedatafromSouthernandEastAfrica,”CGDWorkingPaper.Harris, J.R. and Todaro, M.P., (1970). “Migration, Unemployment and Development: A two-sectorAnalysis,”AmericanEconomicReview.Henderson,H.,Squires,T.,Storeygard,A.,Weil,D.(March2016).“TheGlobalSpatialDistributionofEconomicActivity:Nature,History,andtheRoleofTrade.”Herrendorf,B.,Rogerson,R.,Valentinyi,A.,(2015).“GrowthandStructuralTransformation,”WorkingPaper18996,NBER.Kessides,C.,(2005).TheUrbanTransitioninSub-SaharanAfrica:ImplicationsforEconomicGrowthandPovertyReduction.AfricaRegionWorkingPaperSeries97,WashingtonDC,WorldBank.LaPorta,R.andShleifer,A.,(2008).“TheUnofficialEconomyandEconomicdevelopment”,BrookingsPapersonEconomicActivityMbaye,Aly,StephenGolubandPhilipEnglish(2016),“Protection,EmploymentandPovertyReductioninSenegal:TheSugar,EdibleOil,andFlourIndustries,”WorldBankWorkingPaper,forthcoming.Mbaye,A.AandBenjamin,N., (2015) Informality,GrowthandDevelopment inAfrica,” inHandbookofAfricaandEconomics,EditedbyJustinLinandCelestinMonga.

Mbaye,A.AandBenjamin,N.,Gueye,F.,(2017).“TheinterplaybetweenformalandinformalfirmsanditsimplicationsonjobsinfrancophoneAfrica:casestudiesofSenegalandBenin,”forthcominginTheInformalEconomyinGlobalPerspective,”Palgrave. Mbaye,A.AandBenjamin,N.,Golub,S.,Ekomie,J-J.(2014)“TheUrbanInformalSectorinFrancophoneAfrica:LargeVersusSmallEnterprisesinBenin,BurkinaFasoandSenegal,”DPRUWorkingPaper.

Perry G. E., W.F. Maloney, O.S. Arias, P. Fajnzyblber, A. Mason, J. Saavedra-Chanduvi, (2007),Informality:ExitandExclusion,TheWorldBank,WashingtonDC.

Rodrik,D.,‘PrematureDeindustrialization’,2015

Steel,W.andD.Snodgrass,(2008).“RaisingProductivityandReducingRisksofHouseholdEnterprises”:DiagnoticMethodologyFramework,WorldBank.

WorldBank(2009),MonitoringPerformanceofElectricUtilities:IndicatorsandBenchmarkinginSub-SaharanAfrica.