Why Families are Choosing Chicago IVF for Their Infertility Care

Infertility & IVF in the MENA Region - Opportunities and Challenges

Mansoor Ahmed – Director (MENA Region) Healthcare, Education, PPP

Colliers International MENA

Biography

Mansoor Ahmed

Director (MENA Region)

Healthcare, Education and PPP

[email protected] +971 4 453 7400 | Mobile +971 55 899 6091 P O Box 48817 | Dubai | UAE

http://www.colliers.com/en-gb/unitedarabemirates/services/healthcare

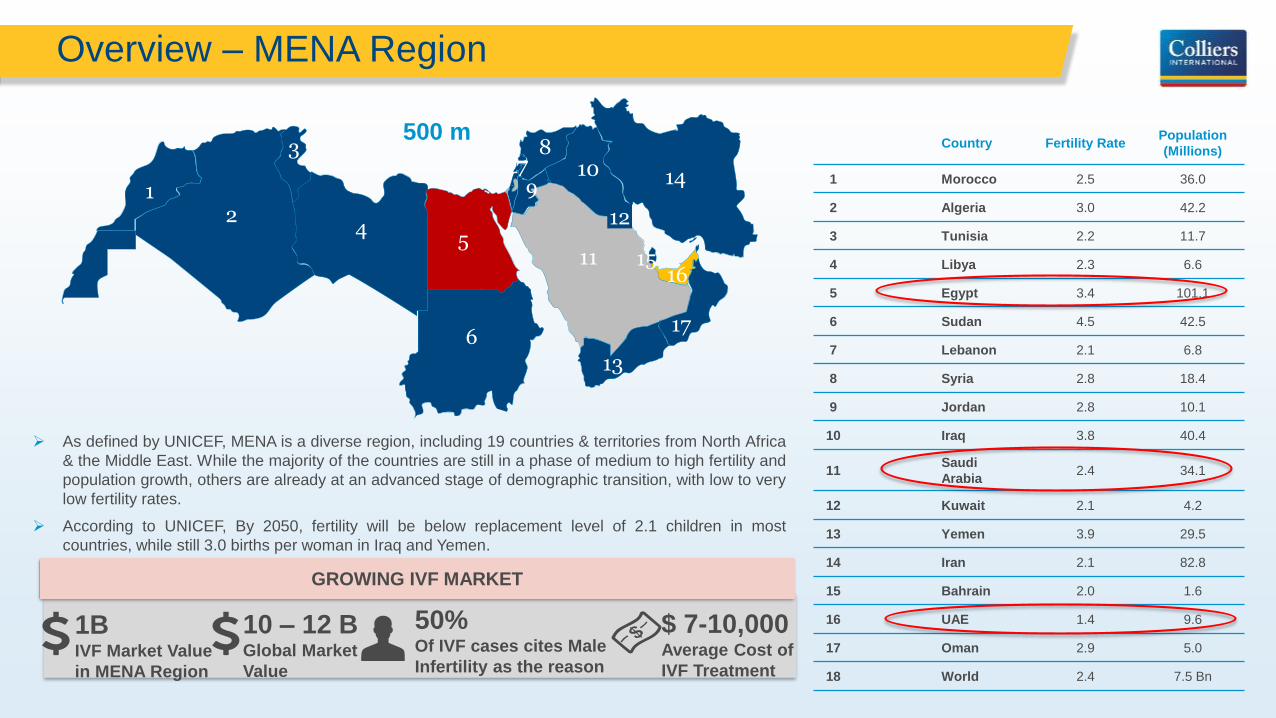

Overview – MENA Region

12

3

45

6

78

910

11

14

12

1516

17

13

Country Fertility RatePopulation

(Millions)

1 Morocco 2.5 36.0

2 Algeria 3.0 42.2

3 Tunisia 2.2 11.7

4 Libya 2.3 6.6

5 Egypt 3.4 101.1

6 Sudan 4.5 42.5

7 Lebanon 2.1 6.8

8 Syria 2.8 18.4

9 Jordan 2.8 10.1

10 Iraq 3.8 40.4

11Saudi

Arabia2.4 34.1

12 Kuwait 2.1 4.2

13 Yemen 3.9 29.5

14 Iran 2.1 82.8

15 Bahrain 2.0 1.6

16 UAE 1.4 9.6

17 Oman 2.9 5.0

18 World 2.4 7.5 Bn

➢ As defined by UNICEF, MENA is a diverse region, including 19 countries & territories from North Africa

& the Middle East. While the majority of the countries are still in a phase of medium to high fertility and

population growth, others are already at an advanced stage of demographic transition, with low to very

low fertility rates.

➢ According to UNICEF, By 2050, fertility will be below replacement level of 2.1 children in most

countries, while still 3.0 births per woman in Iraq and Yemen.

GROWING IVF MARKET

1BIVF Market Value

in MENA Region

10 – 12 BGlobal Market

Value

50%Of IVF cases cites Male

Infertility as the reason

$ 7-10,000 Average Cost of

IVF Treatment

500 m

Key healthcare indicators in the MENA Region has shown improvement

Life expectancy at birth, years

Mortality rate, infant (per 1,000 live birth)

Mortality rate, under 5 (per 1,000)

Mortality rate, adult (per 1,000 adults)

Fertility rate, total (births per woman)

2018

IND

ICA

TO

RS

Comparison

MENA region

1980

61.17 75.73

49.9 18.3

65.1 21.9

255 112

6.2 2.8

Improvement (+)

/decrease (-)

+24%

– 64%

– 67%

– 56%

– 55%

Despite falling fertility rates, the number of births in the

region will remain relatively stable until 2050 because

of the growing number of women of reproductive age

The number of under-five deaths in the region will

continue to decline over the coming decades

By 2030, half of the MENA countries will have total

fertility rates at or below replacement level

The Changing Population Composition – MENA Region

0-45-9

10-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79

80+

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80+

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80+

2018

484 m

2030

580 m1980

184 m

Life expectancy at birth, years

Fertility rate, total (births per woman)

1980 2018

75.7361.17

2.86.2

+24%

– 55%

The Changing Population Composition – Egypt

2018

97 m

2030

117 m

1980

43 m

0-45-9

10-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79

80+

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80+

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80+

Life expectancy at birth, years

Fertility rate, total (births per woman)

1980 2018

71.658.3

3.375.61

+24%

– 55%

The Changing Population Composition – Saudi Arabia

2018

33 m

2030

45 m

19809.7 m

00-04

05-09

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80+

00-0405-0910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7474-79

80+

00-04

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80+

Life expectancy at birth, years

Fertility rate, total (births per woman)

1980 2018

74.862.8

2.47.2

+18%

– 67%

The Changing Population Composition – UAE

2018

9.0 m

2030

10.9 m

1980

1.0 m

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80+

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80+

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80+

Life expectancy at birth, years

Fertility rate, total (births per woman)

1980 2018

77.668.2 +14%

– 75%2.47.2

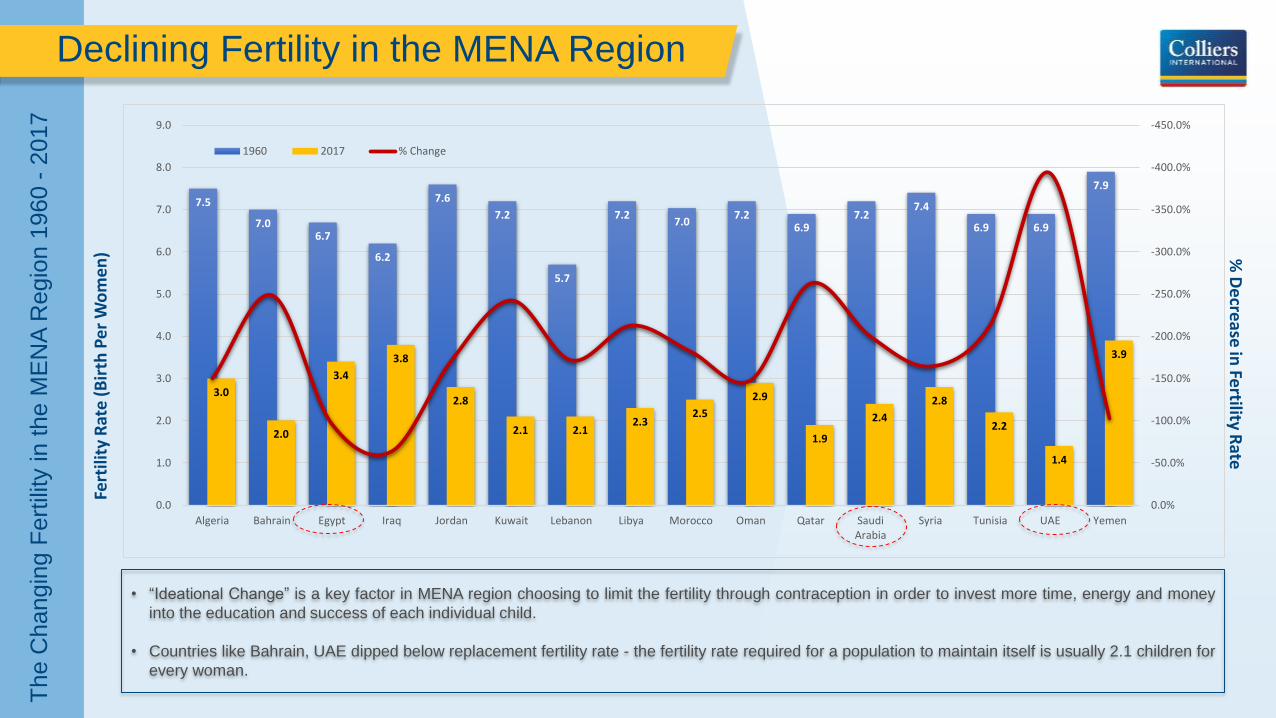

Declining Fertility in the MENA Region

Fert

ility

Rat

e (

Bir

th P

er

Wo

me

n) %

De

crease

in Fe

rtility Rate

Th

e C

hangin

g F

ert

ility

in t

he M

EN

A R

egio

n 1

960 -

2017

7.5

7.06.7

6.2

7.6

7.2

5.7

7.27.0

7.26.9

7.27.4

6.9 6.9

7.9

3.0

2.0

3.4

3.8

2.8

2.1 2.12.3

2.5

2.9

1.9

2.4

2.8

2.2

1.4

3.9

-450.0%

-400.0%

-350.0%

-300.0%

-250.0%

-200.0%

-150.0%

-100.0%

-50.0%

0.0%0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Algeria Bahrain Egypt Iraq Jordan Kuwait Lebanon Libya Morocco Oman Qatar SaudiArabia

Syria Tunisia UAE Yemen

1960 2017 % Change

• “Ideational Change” is a key factor in MENA region choosing to limit the fertility through contraception in order to invest more time, energy and money

into the education and success of each individual child.

• Countries like Bahrain, UAE dipped below replacement fertility rate - the fertility rate required for a population to maintain itself is usually 2.1 children for

every woman.

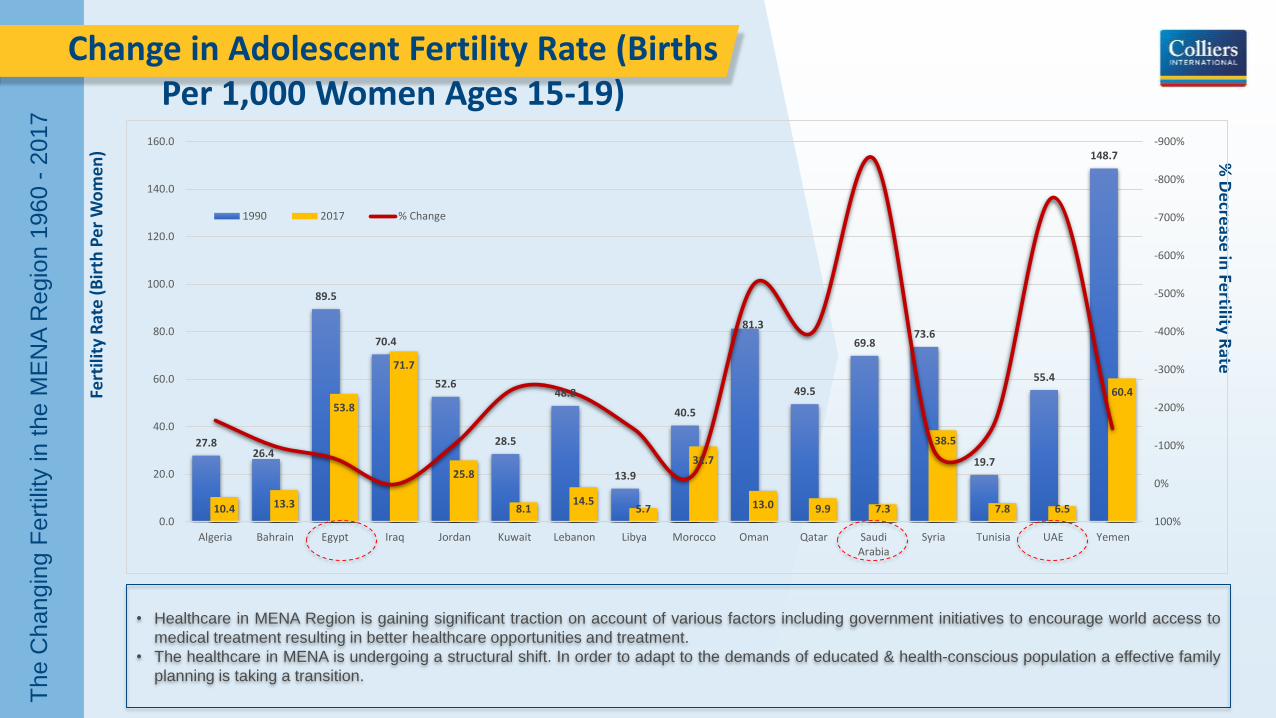

Change in Adolescent Fertility Rate (Births Per 1,000 Women Ages 15-19)

Fert

ility

Rat

e (

Bir

th P

er

Wo

me

n) %

De

crease

in Fe

rtility Rate

Th

e C

hangin

g F

ert

ility

in t

he M

EN

A R

egio

n 1

960 -

2017

27.826.4

89.5

70.4

52.6

28.5

48.8

13.9

40.5

81.3

49.5

69.873.6

19.7

55.4

148.7

10.4 13.3

53.8

71.7

25.8

8.114.5

5.7

31.7

13.0 9.9 7.3

38.5

7.8 6.5

60.4

-900%

-800%

-700%

-600%

-500%

-400%

-300%

-200%

-100%

0%

100%0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Algeria Bahrain Egypt Iraq Jordan Kuwait Lebanon Libya Morocco Oman Qatar SaudiArabia

Syria Tunisia UAE Yemen

1990 2017 % Change

• Healthcare in MENA Region is gaining significant traction on account of various factors including government initiatives to encourage world access to

medical treatment resulting in better healthcare opportunities and treatment.

• The healthcare in MENA is undergoing a structural shift. In order to adapt to the demands of educated & health-conscious population a effective family

planning is taking a transition.

Demand Drivers for IVF in MENA region

1

Literacy Rate

MENA region is turning page on Literacy by making

education as a key part to prepare for future. The overall

literacy rate for both men and women in the Arab World

has increased from just below 62% in 1978 to over 85%

in 2016, empowering women and this directly influences

their fertility behavior as they are included in the

household decision making, age of marriage and family

planning.

Gender Selection

Procedures like gender selection are getting more

reliable and consistent as the technology is developing.

Medical tourists from countries in which gender

selection is prohibited or individuals who wish to seek a

gender selection are willing to pay a price for it.

2

3

4

Late Marriages

Late marriage and infertility has an imperative

relationship. More and more women in the region are

focusing on building their career. Thus, delaying

marriage and putting off having a family due to work,

which is triggering infertility

5 Poor Lifestyle

Smoking, consuming too much alcohol, mental stress

and poor diet have a negative effect on both male and

female fertility. Male infertility identified as a growing

problem occurring in approximately 50% of the cases in

the GCC and Middle East, in addition to genetic

diseases.

6

Female Labor Force Participation

Overall female labor force participation rate in the Arab

World has increased from 20% in 1990 to over 22% in

2016. Most of the GCC countries made significant

improvement, such as in the UAE the ratio increased

from 32% to 42%, KSA (15% to 23%), Oman (21% to

32%), while the ratio in Egypt remains more or less

static increasing from 23% to 24%. The increase in

female participation in labor force and an aspiration for

economic freedom has a direct impact on marriage age

and fertility.

Multiple Embryo Transfer

Some countries in MENA region permits multiple

embryo transfer during any one cycle of IVF treatment

procedure resulting in twins, triplets babies. Patients

perceive a twin pregnancy as an attractive option

especially with IVF treatment being complicated and

expensive.

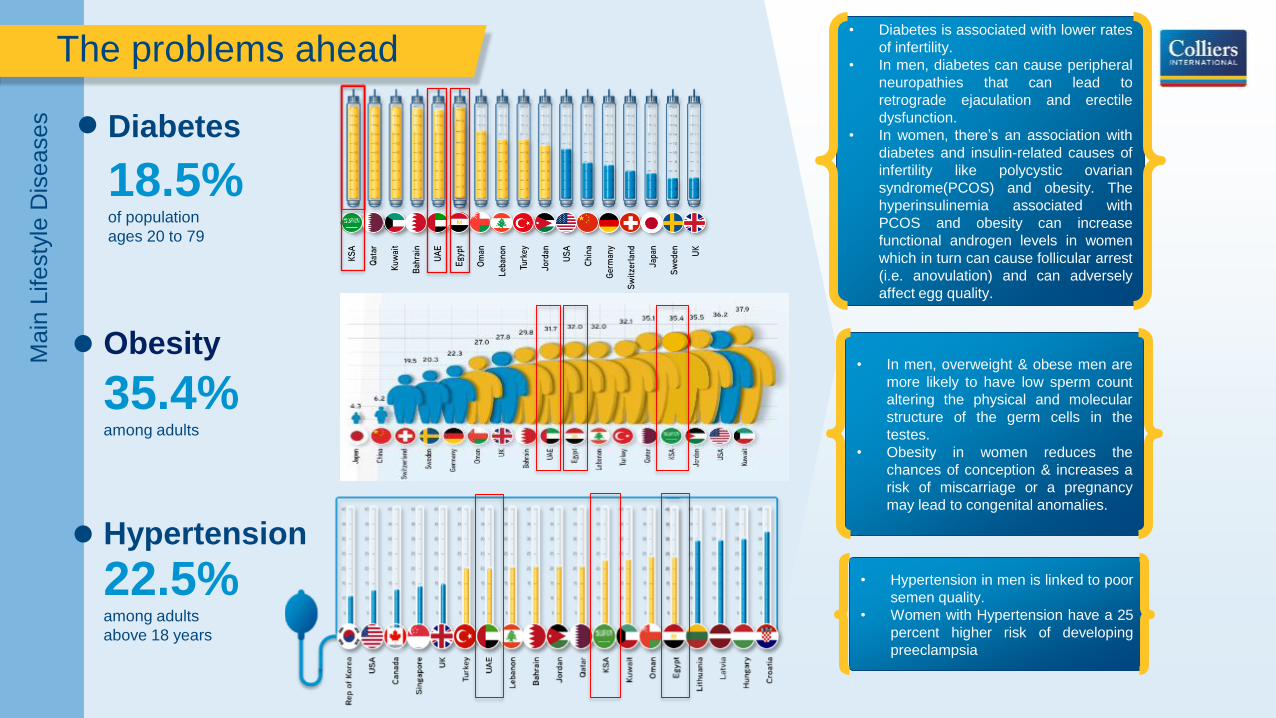

The problems aheadM

ain

Lifesty

le D

iseases

• Diabetes is associated with lower rates

of infertility.

• In men, diabetes can cause peripheral

neuropathies that can lead to

retrograde ejaculation and erectile

dysfunction.

• In women, there’s an association with

diabetes and insulin-related causes of

infertility like polycystic ovarian

syndrome(PCOS) and obesity. The

hyperinsulinemia associated with

PCOS and obesity can increase

functional androgen levels in women

which in turn can cause follicular arrest

(i.e. anovulation) and can adversely

affect egg quality.

Diabetes

18.5%of population

ages 20 to 79

Obesity

35.4%among adults

Hypertension

22.5%among adults

above 18 years

• In men, overweight & obese men are

more likely to have low sperm count

altering the physical and molecular

structure of the germ cells in the

testes.

• Obesity in women reduces the

chances of conception & increases a

risk of miscarriage or a pregnancy

may lead to congenital anomalies.

• Hypertension in men is linked to poor

semen quality.

• Women with Hypertension have a 25

percent higher risk of developing

preeclampsia

Cost of IVF Treatment

14

Saudi

Arabia

Spain

Czech

Republic

Russia

UK

Egypt

India

Turkey

United

Arab

Emirates

USA

IVF Cost: $ 3000 – 5000

Egg Donation: Not allowed

Sperm Donation: Not allowed

IVF Cost: $ 3000 – 5000

Egg Donation: Allowed

Sperm Donation: Allowed

IVF Cost: $ 3000 – 5000

Egg Donation: Allowed

Sperm Donation: Allowed

IVF Cost: $ 3000 – 5000

Egg Donation: Allowed

Sperm Donation: Allowed

IVF Cost: $ 7,000 – 10,000

Egg Donation: Not allowed

Sperm Donation: Not allowed

IVF Cost: $ 5,000 – 10,000

Egg Donation: Not allowed

Sperm Donation: Not allowed

IVF Cost: $ 5000 – 7,000

Egg Donation: Not Allowed

Sperm Donation: Not Allowed

IVF Cost: 5000 – 15000 $

Egg Donation: Allowed

Sperm Donation: Allowed

IVF Cost: $ 3000 - 5000

Egg Donation: Allowed

Sperm Donation: Allowed

IVF Cost: $ 3000 – 5000

Egg Donation: Allowed

Sperm Donation: Allowed

The cost of IVF treatment in UAE is most expensive in

the MENA Region followed by Saudi Arabia & Egypt. At

a high end facility in UAE the price of IVF treatment can

go up to $15,000.

Cost of IVF treatment in

MENA Region is at par

with Western Countries.

Egg & Sperm donation

is also not allowed.

THEN WHY CHOOSE

MENA?

Market Opportunities

• Most MENA countries are

experiencing rapid population growth

and providers of fertility treatments

operating in a individual or a hospital

set up lack affiliation from International

groups.

Large Population &

Lack of International

Affiliation

Egypt• Egypt’s healthcare system is improving both

quantitively and qualitatively to meet with the

existing and potential demand gap.

• Egypt has a strong reputation within the

region of having quality doctors,

infrastructure, and easier visa access when

compared to some of the regional

competitors.

Fragmented Market

• Despite increased interest and investments, the

fertility market in Middle East remains relatively

fragmented. The market is served mostly by

individual clinics and as hospitals unit.

UAE• The UAE is forecasted to command 5.5 %

of the global In-Vitro Fertilization market

by 2020.

• UAE has a strong health regulation

framework, which has helped ensure

quality healthcare, a catalyst for medical

tourism.

• Foreign investor can have a 100%

ownership.

Saudi Arabia

• In line with the government’s

Vision 2030 and the National

Transformation Program (NTP),

the Ministry of Health (MoH) is

expected to spend close to US$71

billion over five-years ending in

2020.

• Foreign investor can have a 100%

ownership.

Visa RestrictionsIn case of some MENA there is difficulty

in getting visas for the Western

Countries. Therefore, increasing the

healthcare market within the region.

Gender Selection/Family

Balancing

Shift from a Taboo to a Cultural AcceptabilityThe stigma of IVF treatment is fading and people are willingly

coming forward for fertility treatments.

Why UAE?

Most common nationalities seeking IVF treatmentin the UAE are Emiratis, GCC nationals,expatriates from sub-continent and Africa. Latelypatients have also started coming from China.

Top

Nationalities

Medical tourism accounts for 10% to 15% of the IVF patient volumes.

Medical

Tourism

The success rates in the UAE Region are quitehigh. Patients also come for gender selection, asUAE, is one of the few countries where genderselection is still permitted.

Why UAE?

Dubai being an attractive “tourism destination”offers several entertainment, cultural andshopping options which are “pull” factors formedical tourism beside quality of medial offering.

UAE: “The

Destination”

Factor

Approximately 15% to 30% parents opt for IVFtreatment to conceive second child, while 10%-15% return to IVF centres to have anothersuccessful treatment cycle to conceive theirsecond child using IVF treatment again.

The Second

Child

The reason for multiple pregnancies is due tomultiple embryos transferred. Some patientsperceive a twin pregnancy as an attractive optionespecially with IVF treatment being complicatedand expensive.

The Twin

Factor

The average cost of an IVF treatment rangesbetween USD 7,000 – 10,000, but it may varydepending upon the type of treatmentrecommended for each patient including the costof medications, stimulation protocols, proceduralcharges, blood tests e etc.

The IVF

Treatment

Cost

The key challenge is restriction on embryofreezing which results in repeat cycles of fulltreatment thereby increasing patients’ costs andmorbidity.

Key

Challenges

Major key challenge is a separate licensingrequirements across the different regions. Asingle, unified, licensing process can resolve thischallenge. Some MENA Countries still don’t allowembryo freezing whereas UAE recently brought areform by allowing embryo freezing in the region.

Regulatory

Challenges

In over 50% cases male infertility is the reason forseeking IVF treatment. The factors contributing tomale infertility include lifestyle, diabetes, obesity,hypertension and genetics.

Male

Infertility

Key Insights for Investors

Revenue Streams

Typical Charges for IVF in the region are:

• UAE: USD 10,000 to 15,000 per cycle

• KSA: USD 7,000 to 10,000 per cycle

• Egypt: USD 5,000 to 7,000 per cycle

Volume of patients

On average, a team comprising of a physician

(Fertility Consultant or Specialist), 2

embryologists and up to 4 nurses can manage

300-350 IVF cycles annually. Most clinics in the

region typically comprise of 2 to 4 such teams.

Set-up costs

Typical set-up cost of a mid-size premium facility

ranges from USD 2.5 million to USD 3.5 million

inclusive of medical equipment, furniture and fit-

outs but exclusive of premises construction.

Financial returns

The business offers attractive returns for

investors in the region. EBITDA margins for

efficiently run clinics at optimal capacity typically

range between 25% to 40%. Project investment

returns (IRR) typically ranges from 18% to 25%.

Case Study:

A successful premium IVF center in UAE

About the Facility

Services

Patient Profile

Key Reasons of

Infertility

The idea of IVF facility was conceived in 2009, and

the facility commenced operations in Q1 2011.

The facility performs annually:• IVF/ICSI: +3200

• IUI: +150

• Cryopreservation:

+2000

• Reproductive

Surgeries: +200

• Sperm extraction: +120

• Genetic testing: +550

• Age Group: 40% patients are aged less than 35

years, whereas 60% are aged over 35 years

• Payer group: 70% insured, 30% self pay

• Nationality: 64% Emiratis, 16% Middle Eastern,

8% Africans, 5% Asians, 2% Westerners, and

5% Other Nationalities

Most patients present with primary Infertility.

Tubal Factor – 0.3%, Ovulatory Dysfunction –

1.5%, Diminished Ovarian reserve – 0.0%,

Endometriosis – 0.1%, Uterine Factor - 1.2%,

Oligospermia – 17.9%, Male factor - 11.6%,

Other Factor - 5.2%, Unspecified - 61.1%

Key Players

JCI & CAP Accredited JCI Accredited

JCI & CAP Accredited

About Colliers’ International

Dubai

Abu Dhabi

Riyadh

Jeddah

Cairo

Regional

5Regional Offices

Over 20years

Regional and

Management

Experience

90+

Professionals

15Professionals

dedicated Healthcare,

Education & PPP team

Global

$ 3.3 BN

IN REVENUE

$127 BNTransaction Value

68COUNTRIES

6CONTINENTS

17,000PROFESSIONALS

About Colliers’ Healthcare & Wellness Advisory Services

Services Offered

• Strategic & Business Planning

• Economic Impact Studies

• Medical Planning

• Market & Competitive Studies

• Catchment Area Analysis

• Market & Financial Feasibility Studies

• Financial and Business Modelling

• Market & Commercial Due Diligence

• Land & Property Valuation

• Business & Brand Valuation

• Mergers & Acquisitions Assistance

• Buy Side Advisory / Sell Side Advisory

• Sale & Lease Back Advisory

• Public Private Partnership (PPP) & Privatisation

• Operator Search & Selection and Contract Negotiation

• Site Selection & Land / Property Acquisition

• Asset & Performance Management

• Performance Management & Industry Benchmark Surveys

Why Colliers

A Truly Regional Team with International

Experience

Colliers Advantage

Market Awareness

Creative Solutions

Offer a memorable experience

Access to Subject Matter Experts

Qualified and Experienced Staff (15)

Shared Knowledge

The Knowledge Hub

To download https://www2.colliers.com/en-AE/Services/Healthcare-Services

Colliers International

Al Shafar Tower 1, Suite 1204

Barsha Hieghts

P O Box 71591 | Dubai | United Arab Emirates

TEL +971 4 453 7400

MANSOOR AHMED

Director (MENA Region)

Development Solutions | Healthcare, Education & PPP

+ 971 55 899 6091 / + 971 50 66 88 239