Industry Solution Papers: Russian crude oil exports to the ... · 2 | SPECIAL REPORT: RUSSIAN CRUDE...

10

SPECIAL REPORT Russian crude oil exports to the Pacific Basin – an ESPO update February 2011 OIL

-

Upload

nguyenkhanh -

Category

Documents

-

view

219 -

download

2

Transcript of Industry Solution Papers: Russian crude oil exports to the ... · 2 | SPECIAL REPORT: RUSSIAN CRUDE...

S P E C I A L R E P O R T

Russian crude oil exports to the Pacifi c Basin – an ESPO update February 2011

OIL

2 |

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATESPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

ESPO PIPELINE DELIVERIES TO CHINA START

Russia’s Eastern Siberia Pipeline Oil made further inroads into the world oil market in early 2011 with the start of regular exports of the crude to China. The official start of flows to China has brought the total volume of ESPO exports to around 600,000 barrels/day, and marks the end of the first phase of the multi-billion dollar project.

Russian pipeline operator Transneft pumped the first test volume of ESPO crude to Daqing in China on November 1, 2010 and shipped a total of 250,000 mt (61,000 b/d) in November and 300,000 mt in December.

Commercial supplies through an offshoot of the ESPO pipeline were officially launched on January 1, 2011, with a total of 1.318 million mt (311,643 b/d) of oil delivered to China via the line in January 2011.

Russia’s state-owned, oil giant Rosneft has signed a 20-year contract with China’s CNPC for the delivery of 300,000 b/d of oil, and supplies could increase beyond this in the future. In return, China Development Bank agreed to provide Rosneft and Transneft with 20-year loans of $15 billion and $10 billion, respectively. The price at the Russia-China border, currently the end of

the operational ESPO pipeline in Russia, for deliveries into China is equal to the FOB-basis price at Kozmino on the Pacific coast, with no premiums or discounts being applied, according to sources involved in negotiations.

Russia’s deputy Prime Minister Igor Sechin estimated the contract signed between Rosneft and CNPC to be worth at least $100 billion. The contract envisages total oil deliveries of 300 million mt (close to 2.26 billion barrels) over 20 years. At current price levels the deliveries on an annualized basis would have an invoice price of about $10-billion. This would make the value of the project, if present trends continue, to be in excess of $200-billion.

PetroChina, the listed arm of Chinese oil giant CNPC, geared up for the arrival of ESPO by upgrading facilities at a few of its refineries to process the crude blend. In October, PetroChina announced that it had upgraded secondary units at its 10 million mt/year Liaoyang refinery in northeast China’s Liaoning province, and the 20.5 million mt/year Dalian refinery and 10 million mt/year Fushun refinery are also expected to process ESPO crude.

Sea ofOkhotsk

LakeBalkhash

LakeBaikal

Sea ofJapan

West Siberianoil & gas �elds

Kozmino

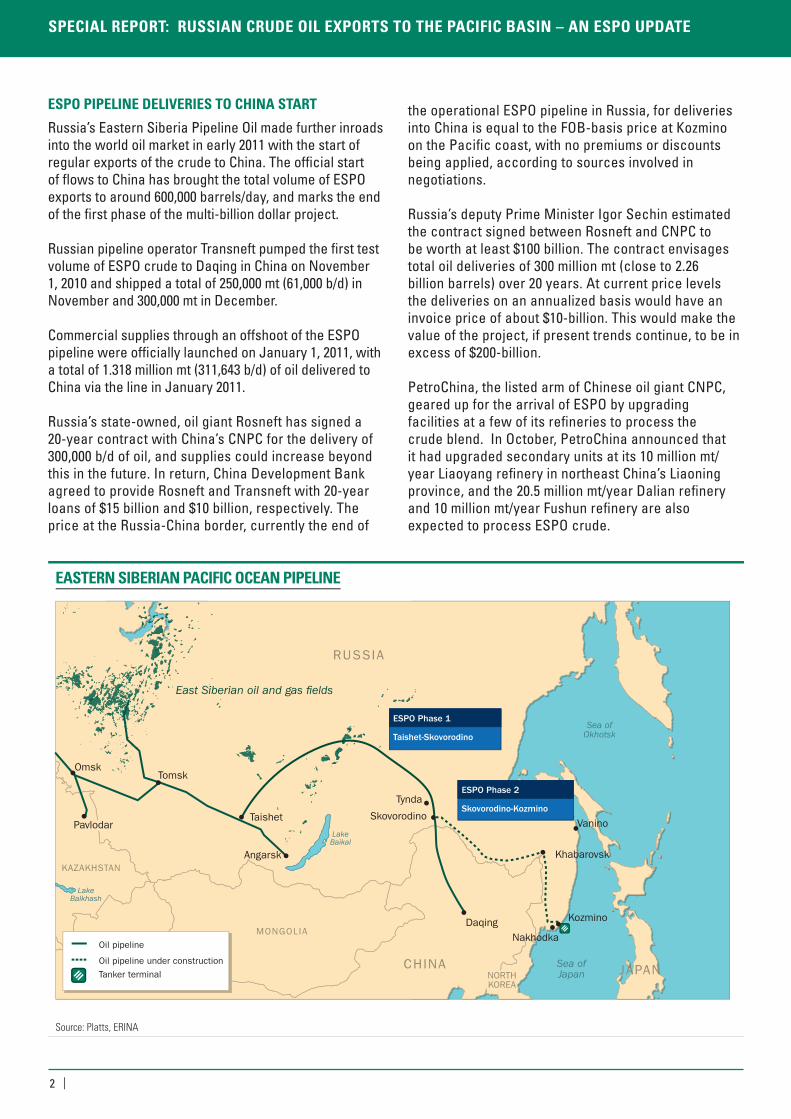

ESPO Phase 1

Taishet-Skovorodino

ESPO Phase 2

Skovorodino-Kozmino

East Siberian oil and gas fields

Omsk

Angarsk

Tomsk

PavlodarPavlodar

NakhodkaDaqing

Khabarovsk

VaninoTaishet Skovorodino

Tynda

JAPAN NORTHKOREANORTHKOREA

MONGOLIA

KAZAKHSTAN

RUSSIA

CHINA

Oil pipeline

Oil pipeline under construction

Tanker terminal

EASTERN SIBERIAN PACIFIC OCEAN PIPELINE

Source: Platts, ERINA

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

| 3

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

The 64-km Russian section of the pipeline which runs from Skovorodino to China’s northeastern frontier was completed in August 2010. The section from the frontier to Daqing in China, which was built by Chinese oil company CNPC, was completed a month later in September 2010.

ESPO is a relatively new export stream and the first pipeline emanating from Russia to target the growing demand for oil in the Asia-Pacific region. ESPO crude began flowing in December 2009 out of the Russian port of Kozmino, near Vladivostok in the Far East. Since then, this crude has been delivered on both sides of the Pacific Basin to refiners in Asia and the US, and exports have averaged around 300,000 b/d, with deliveries some months exceeding 330,000 b/d.

Platts, the energy information division of The McGraw-Hill Companies, launched crude oil price assessments for ESPO in December 2009. Platts consulted widely in the development of this new crude assessment with Russian producers and Pacific Basin consumers, as well as with Russian energy ministry officials. The launch was scheduled to ensure a numerical assessment basis to the contractual relationship between China and Russia.

The initial stage of the ESPO pipeline, which runs for 2,757 km from Taishet in east Siberia to Skovorodino in the Amur region of Russia’s Far East, near the border with China, has a capacity of 600,000 b/d. From Skovorodino, half of the crude is now being shipped to China through the spur pipeline to Daqing, and the other 300,000 b/d is being transported by rail to the dedicated ESPO export facilities at Kozmino on the Pacific Coast.

SELLERS AND BUYERS OF ESPO CRUDE

The first exports from Kozmino took place on December 28, 2009, when a 100,000 mt Rosneft cargo departed for Hong Kong. In 2010, Rosneft exported around 7.5 million mt of oil from Kozmino, with TNK-BP accounting for a further 2.2 million mt of ESPO exports, Surgutneftegaz more than 2.6 million mt and Gazprom Neft between 1.8 and 2 million mt.

Average loadings rose during early 2010, but since April 2010 the monthly loading volume has averaged around 1.4 million mt (14 cargoes of 100,000 mt). Through the end of 2010, some 84% of ESPO crude exports have gone to Asian countries, with Japan (30%) and South Korea (29%) being the top two recipients of this oil. At least 16% has moved to the US, as can be seen in the chart opposite.

The table on pages 8 to 10 displays the ESPO loading program from Kozmino and tracks the buyers, loading vessels, and prices where applicable. Platts has also published data in its publications regarding the destination of the shipments. The majority of shipments to the US have landed on the West Coast, but in May 2010 the first shipment landed in the US Gulf Coast as Valero received ESPO crude at its Corpus Christi refinery.

Vietnam joined the list of countries supplied with ESPO crude in November 2010. On September 20, 2010, TNK-BP signed a term contract with state-run PetroVietnam to supply ESPO crude blend over 12 months, with the first shipment of 100,000 mt due in November. In December 2010, Indonesian state-owned oil and gas company Pertamina bought its first ESPO cargo for delivery in February 2011.

End-users that have bought ESPO crude include South Korea’s GS Caltex and SK Energy, China’s Sinopec, Philippines’ Petron, US refiner Tesoro, ExxonMobil, which is taking it to its joint venture refinery with Japan’s TonenGeneral, PetroVietnam, Indonesia’s Pertamina and BP at its refinery in Carson, California.

ESPO PRICING – A FUTURE BENCHMARK?

As is often the case with a new export stream, it took some time for ESPO to find its value in the market, with refiners initially wary of paying full value for an unknown crude. But as the new blend has become more widely accepted by Asian and US refiners, its market value has risen.

Singapore (2%)

South Korea (29%)

Japan (30%)

United States (16%)

China (8%)

Thailand (11%)

Taiwan (1%)

ESPO CRUDE EXPORTS BY DESTINATION

Source: Platts

Philippines (3%)

4 |

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATESPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

ESPO initially traded at a discount to Middle East benchmark Dubai crude, but since August 2010 it has begun to trade at a premium to Dubai and the differential has increased steadily through the second half of 2010. Customers first discounted the crude based on their lack of familiarity with the quality specifications and initially perceived it to be inferior to Dubai. Over time, customers determined the quality and it has begun to compete with Middle Eastern premium grades such as Abu Dhabi’s Murban. The highest premium to Platts Dubai assessments achieved so far by ESPO was $3.62/barrel for a cargo loading in January 2011.

The ESPO premium to Dubai is attributed by market participants to several factors. Firstly, ESPO is a sweeter and lighter crude than Dubai. Secondly, ESPO has become widely accepted by Asian and US refiners due to the proximity of Kozmino to key Asian demand centers. And finally, according to many traders, a widening of the Brent/Dubai spread has encouraged end-users in Asia to buy more of this crude oil priced against Dubai rather than other grades that price against Dated Brent.

Prices for ESPO are assessed by Platts at the close of business in Singapore and again at the London close. ESPO barrels are currently priced as a differential to a commonly used benchmark — Platts Dubai — but due to its location, ample production levels and wide equity ownership, the ESPO crude stream has attributes that could, over time, lead to it becoming a major flat price indicator of spot oil volumes in Asia. The Asian markets are heavily dependent on imported oil and the role of Russian oil has been growing in recent years.

The Platts ESPO FOB Kozmino assessment is used for Rosneft term deliveries to China averaged over respective calendar months. The price basis FOB Kozmino is taken as being equivalent to that at the Russian-Chinese border due to deliveries through Transneft’s ESPO system being charged a flat fee.

CRUDE QUALITY AND YIELD

An ESPO crude assay became available in early February 2010. The assay came from the first cargo that loaded from Kozmino over December 27-29, 2009. The test, conducted by SGS, is based on a composite sample taken from the ship’s tanks after the cargo loaded.

The assay puts the sulfur content of the crude at 0.535% and its gravity at 34.7 API. The assay also shows the crude as having a total acid number of 0.05 mg KOH/g, water content of 0.35% and a pour point of minus 30 degrees Celsius.

Using a cut point of 10-148 for naphtha, 148-232 for kerosene, 232-343 for gasoil and 343 and above for residue, the crude grade is able to yield slightly over 15% of naphtha, over 13% of kerosene, slightly above 20% of gasoil and over 51% of residue. The diesel-rich crude appeals to most Asian refiners.

The most recent ESPO assay reviewed by Platts came in March 2010 and was sourced from multiple cargoes loading at Kozmino in February (see page 5). This test, conducted by Intertek Caleb Brett, is derived from a composite sample taken during the loading process. Information obtained from industry sources in early 2011 indicates that the quality parameters have remained steady through the past year.

The assay puts the sulfur content of the crude at 0.54% and its API gravity at 34.7 degrees, very similar in quality to the first cargo assay. The second assay also shows the crude having a total acid number of less than 0.05 mg KOH/mg and a pour point of less than minus 36 degrees Celsius. Again, this is similar in quality to the initial assay.

PLATTS ESPO CRUDE ASSESSMENTS ASIAN CLOSE

Source: Platts

($/barrel)

65

70

75

80

85

90

95

100

Jan-11Nov-10Sep-10Jul-10May-10Mar-10Jan-10

PLATTS ESPO VS DUBAI

Source: Platts

($/barrel)

-2

-1

0

1

2

3

4

Jan-11Nov-10Sep-10Jul-10May-10Mar-10Jan-10

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

| 5

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

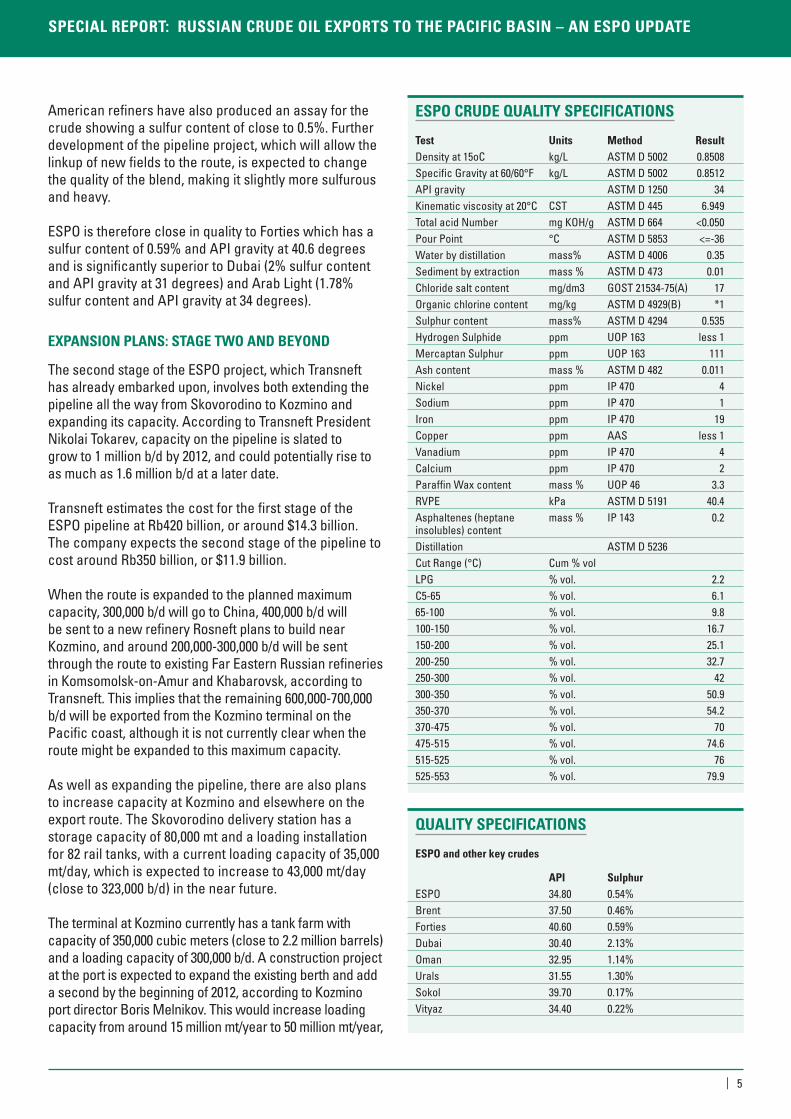

ESPO CRUDE QUALITY SPECIFICATIONS

Test Units Method ResultDensity at 15oC kg/L ASTM D 5002 0.8508Specific Gravity at 60/60°F kg/L ASTM D 5002 0.8512API gravity ASTM D 1250 34Kinematic viscosity at 20°C CST ASTM D 445 6.949Total acid Number mg KOH/g ASTM D 664 <0.050Pour Point °C ASTM D 5853 <=-36Water by distillation mass% ASTM D 4006 0.35Sediment by extraction mass % ASTM D 473 0.01Chloride salt content mg/dm3 GOST 21534-75(A) 17Organic chlorine content mg/kg ASTM D 4929(B) *1Sulphur content mass% ASTM D 4294 0.535Hydrogen Sulphide ppm UOP 163 less 1Mercaptan Sulphur ppm UOP 163 111Ash content mass % ASTM D 482 0.011Nickel ppm IP 470 4Sodium ppm IP 470 1Iron ppm IP 470 19Copper ppm AAS less 1Vanadium ppm IP 470 4Calcium ppm IP 470 2Paraffin Wax content mass % UOP 46 3.3RVPE kPa ASTM D 5191 40.4Asphaltenes (heptane mass % IP 143 0.2 insolubles) content Distillation ASTM D 5236 Cut Range (°C) Cum % vol LPG % vol. 2.2C5-65 % vol. 6.165-100 % vol. 9.8100-150 % vol. 16.7150-200 % vol. 25.1200-250 % vol. 32.7250-300 % vol. 42300-350 % vol. 50.9350-370 % vol. 54.2370-475 % vol. 70475-515 % vol. 74.6515-525 % vol. 76525-553 % vol. 79.9

American refiners have also produced an assay for the crude showing a sulfur content of close to 0.5%. Further development of the pipeline project, which will allow the linkup of new fields to the route, is expected to change the quality of the blend, making it slightly more sulfurous and heavy.

ESPO is therefore close in quality to Forties which has a sulfur content of 0.59% and API gravity at 40.6 degrees and is significantly superior to Dubai (2% sulfur content and API gravity at 31 degrees) and Arab Light (1.78% sulfur content and API gravity at 34 degrees).

EXPANSION PLANS: STAGE TWO AND BEYOND

The second stage of the ESPO project, which Transneft has already embarked upon, involves both extending the pipeline all the way from Skovorodino to Kozmino and expanding its capacity. According to Transneft President Nikolai Tokarev, capacity on the pipeline is slated to grow to 1 million b/d by 2012, and could potentially rise to as much as 1.6 million b/d at a later date.

Transneft estimates the cost for the first stage of the ESPO pipeline at Rb420 billion, or around $14.3 billion. The company expects the second stage of the pipeline to cost around Rb350 billion, or $11.9 billion.

When the route is expanded to the planned maximum capacity, 300,000 b/d will go to China, 400,000 b/d will be sent to a new refinery Rosneft plans to build near Kozmino, and around 200,000-300,000 b/d will be sent through the route to existing Far Eastern Russian refineries in Komsomolsk-on-Amur and Khabarovsk, according to Transneft. This implies that the remaining 600,000-700,000 b/d will be exported from the Kozmino terminal on the Pacific coast, although it is not currently clear when the route might be expanded to this maximum capacity.

As well as expanding the pipeline, there are also plans to increase capacity at Kozmino and elsewhere on the export route. The Skovorodino delivery station has a storage capacity of 80,000 mt and a loading installation for 82 rail tanks, with a current loading capacity of 35,000 mt/day, which is expected to increase to 43,000 mt/day (close to 323,000 b/d) in the near future.

The terminal at Kozmino currently has a tank farm with capacity of 350,000 cubic meters (close to 2.2 million barrels) and a loading capacity of 300,000 b/d. A construction project at the port is expected to expand the existing berth and add a second by the beginning of 2012, according to Kozmino port director Boris Melnikov. This would increase loading capacity from around 15 million mt/year to 50 million mt/year,

QUALITY SPECIFICATIONS

ESPO and other key crudes

API SulphurESPO 34.80 0.54%Brent 37.50 0.46%Forties 40.60 0.59%Dubai 30.40 2.13%Oman 32.95 1.14%Urals 31.55 1.30%Sokol 39.70 0.17%Vityaz 34.40 0.22%

6 |

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATESPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

or around 1 million b/d, which would be more than enough to handle expected future export levels.

Russia has not ruled out sending additional volumes of west Siberian crude to the ESPO pipeline if there is not enough crude produced in east Siberia to fill the line. Russia’s energy minister Sergei Shmatko, however, has said that he believes east Siberia will produce enough crude to fill the pipeline and account for all of the ESPO exports.

In addition to a crude supply deal, CNPC and Rosneft also signed an agreement in late September 2010 to conduct a front-end engineering design study for a refinery to be jointly built near Tianjin in northern China, and held a groundbreak-ing ceremony to mark the start of the construction. The 260,000 b/d refinery is scheduled for completion by 2015, with Rosneft to supply 70% of the crude feedstock to the refinery and CNPC to supply the remaining 30%.

In 2010, Transneft laid 1,150 km of pipeline as part of the second stage of the ESPO construction (out of a total of 2,046 km) and 300 km of the northern Purpe-Samotlor pipeline, which would allow the transportation of crude from northern east Siberia to the ESPO pipeline. The construction of the second stage of ESPO is to be finished in 2012, according to Transneft sources.

Transneft is also considering a possible expansion of the capacity of a planned pipeline from Zapolyarnoye to Purpe to transport crude from new fields in the northern Yamal Nenets Autonomous region and the north of the east Siberian Krasnoyarsk region. The pipeline was initially planned to have a capacity of 12 million mt/year but Transneft is considering increasing this to 45 million mt/year (900,000 b/d). The Zapolyarnoye-Purpe section is designed to link the new reserves to the national pipeline infrastructure for further shipments via ESPO. Transneft expects to build the 488-km pipeline in three stages.

The first stage is to be commissioned in December 2013, the second stage is due in December 2014 and the third stage in December 2015.

Transneft estimates the new pipeline to cost Rb120 billion ($87.2 billion) and plans to build it jointly with oil producers Lukoil, TNK-BP and Gazprom Neft, which have reserves in the area. The Zapolyarnoye-Purpe pipeline will extend to the Purpe-Samotlor line, which will shorten the route for feeding crude into ESPO.

RISING RUSSIAN PRODUCTION

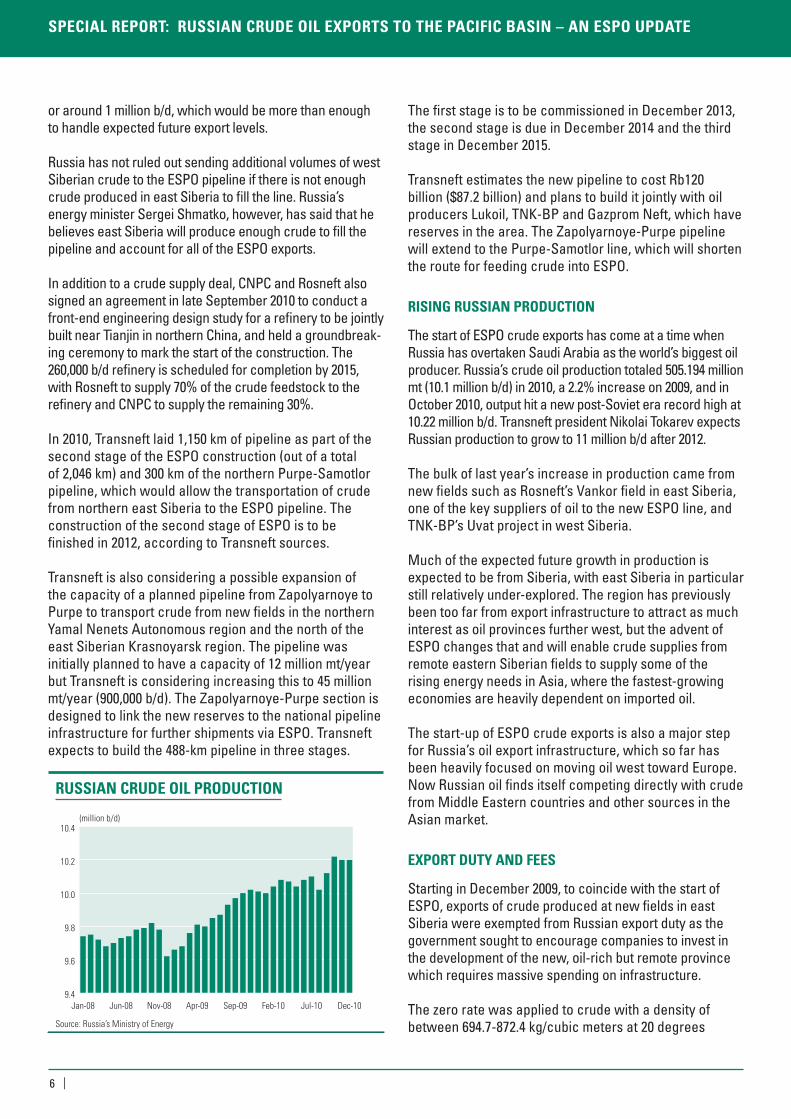

The start of ESPO crude exports has come at a time when Russia has overtaken Saudi Arabia as the world’s biggest oil producer. Russia’s crude oil production totaled 505.194 million mt (10.1 million b/d) in 2010, a 2.2% increase on 2009, and in October 2010, output hit a new post-Soviet era record high at 10.22 million b/d. Transneft president Nikolai Tokarev expects Russian production to grow to 11 million b/d after 2012.

The bulk of last year’s increase in production came from new fields such as Rosneft’s Vankor field in east Siberia, one of the key suppliers of oil to the new ESPO line, and TNK-BP’s Uvat project in west Siberia.

Much of the expected future growth in production is expected to be from Siberia, with east Siberia in particular still relatively under-explored. The region has previously been too far from export infrastructure to attract as much interest as oil provinces further west, but the advent of ESPO changes that and will enable crude supplies from remote eastern Siberian fields to supply some of the rising energy needs in Asia, where the fastest-growing economies are heavily dependent on imported oil.

The start-up of ESPO crude exports is also a major step for Russia’s oil export infrastructure, which so far has been heavily focused on moving oil west toward Europe. Now Russian oil finds itself competing directly with crude from Middle Eastern countries and other sources in the Asian market.

EXPORT DUTY AND FEES

Starting in December 2009, to coincide with the start of ESPO, exports of crude produced at new fields in east Siberia were exempted from Russian export duty as the government sought to encourage companies to invest in the development of the new, oil-rich but remote province which requires massive spending on infrastructure.

The zero rate was applied to crude with a density of between 694.7-872.4 kg/cubic meters at 20 degrees

(million b/d)

9.4

9.6

9.8

10.0

10.2

10.4

Dec-10Jul-10Feb-10Sep-09Apr-09Nov-08Jun-08Jan-08

RUSSIAN CRUDE OIL PRODUCTION

Source: Russia’s Ministry of Energy

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

| 7

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

RUSSIAN EXPORT DUTY

Source: Platts

($/mt)

50

100

150

200

250

300

350

Feb-11Dec-10Oct-10Aug-10Jun-10Apr-10Feb-10Dec-09

ESPO Urals

Celsius (equivalent approximately to API gravity of 30-70 at 15.5 degrees Celsius) and with a sulfur content of between 0.1% and 1%, according to the document signed by Russian Prime Minister Vladimir Putin, easily covering the typical specifications of ESPO blend.

A total of 22 separate fields in east Siberia were eligible for the zero rate, including Vankor, Yurubcheno-Tokhomskoye, Talakan (including the East Block), Alinskoye, Srednebotuobinskoye, Dulisminskoye, Verkhnechonskoye, Kuyumbinskoye, North Talakan, East Alinskoye, Verkhnepeleduyskoye, Pilyudinskoye, and Stanakhskoye. The fields, most of which are not currently in production, are owned by several entities including Rosneft, Surgutneftegaz, TNK-BP and Gazprom Neft, and all are destined to feed the ESPO pipeline. Currently only six of the fields are operational: Vankor (Rosneft), Verkhnechonskoye (TNK-BP and Rosneft), Dulisminskoye (TNK-BP), Alinskoye (Surgutneftegaz), Talakan (Surgutneftegaz) and Yaraktinskoe (Irkutsk Oil). Crude oil from these six currently constitutes the ESPO blend and determines the quality of the crude, which could change in the future as oil from other fields joins the system.

Russia’s finance ministry pushed the government to lift the tax exemption or at least impose a reduced export duty for east Siberian crude and an export duty of $69.90/mt or $9.50/b was introduced from July 1, 2010, equivalent at the time to 28% of the duty levied on Urals, Russia’s main export crude oil blend. Since then, the export duty for ESPO blend has been revised on a monthly basis and in February 2011 the ESPO duty was set at $137.60/mt or $18.72/b, equivalent to 40% of Urals duty. According to the latest finance ministry data, the ESPO export duty is likely to be fixed between $149/mt and $150/mt, or $20.41/b and $20.54/b in March 2011.

Over the next few years the export duty on eastern Siberian crude is expected to reflect normal Russian crude oil export duty levels although the timing of the eligibility for the reduced rate of export duty is expected to differ for each field.

On September 16, 2010, the finance ministry said the reduced rate of export duty paid on crude oil from Rosneft’s Vankor oil field (the largest field contributing to ESPO), which produced 12.7 million mt (255,000 b/d) in 2010 and is expected to produce around 15 million mt (300,000 b/d) in 2011, may be extended to 2014 following a request from Prime Minister Vladimir Putin. No declarative announcement has yet followed.

Russia’s Federal Tariffs Service, which sets the tariffs for crude transportation charged by Transneft, approved a

through transportation fee for crude deliveries via the new export oil pipeline across east Siberia towards the Pacific Ocean in December 2009. The fee was initially set at Rb 1,598/mt ($52.68/mt or $7.21/b). It was revised from August 1, 2010 to Rb 1,651/mt ($54.59/mt or $7.47/b) and again from December 1, 2010 to Rb 1,815/mt ($60.01/mt or $8.21/b).

The fee includes services for crude deliveries via the pipeline, by railroad, and for crude re-loading at terminals including at Kozmino for onward export. The same through transportation fee is fixed for crude deliveries via the ESPO pipeline to China.

CONCLUSION

Pipeline deliveries of ESPO to China commenced slightly ahead of schedule with the overall project exceeding expectations and schedules set at the onset of the project. The deliveries of oil triggered a set of changes in the pricing of crude oil in Asia. Subsequently, Middle Eastern producers now need to consider oil more readily available and geographically closer which can be delivered directly into Asia. The market viewed ESPO as a crude competing in the same supply space already filled by Middle Eastern producers and hence priced the crude relative to Dubai, the benchmark for the Middle East. The price of ESPO has established a clear footprint in the Pacific Basin and the price has improved on a relative basis to Dubai as the refiners have familiarized themselves with the crude’s quality and the producers have demonstrated an ability to maintain a consistent quality.

Production and deliveries of ESPO will continue to grow as more fields in eastern Siberia are brought on stream but the next exports will not rise as rapidly as initially anticipated due to the planned building of a refinery or maybe even more in the far east of Russia.

8 |

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATESPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

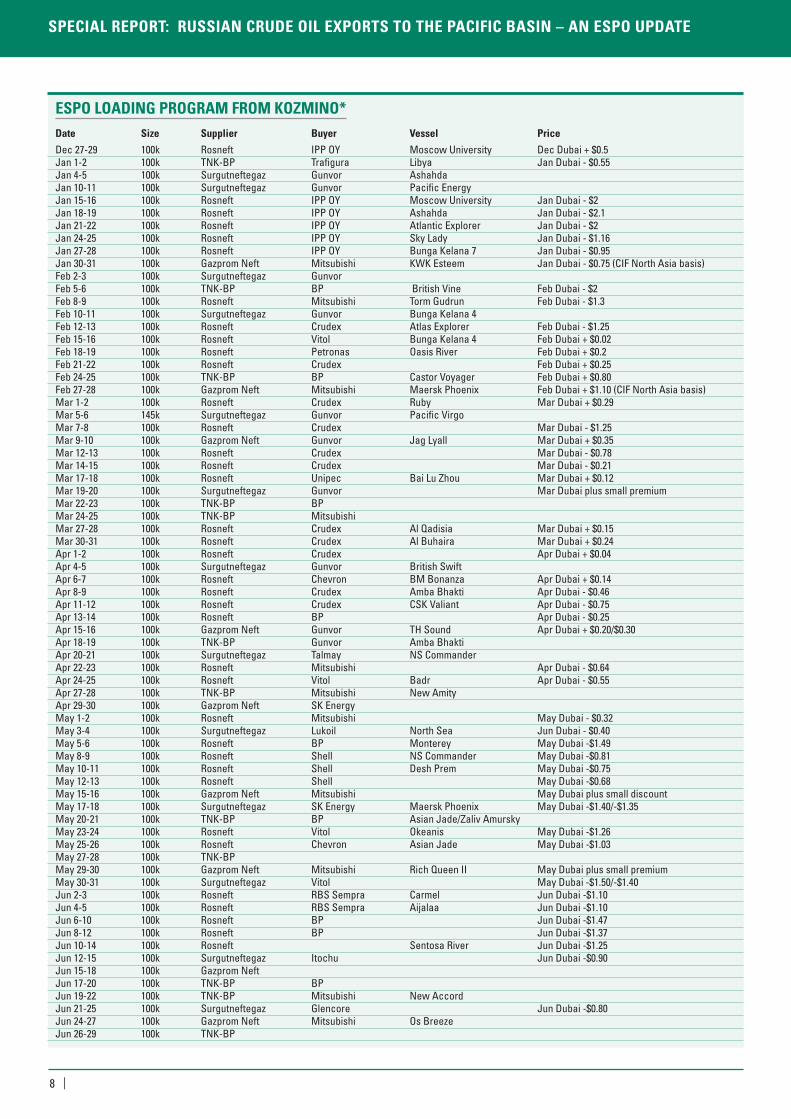

ESPO LOADING PROGRAM FROM KOzMINO*Date Size Supplier Buyer Vessel Price

Dec 27-29 100k Rosneft IPP OY Moscow University Dec Dubai + $0.5Jan 1-2 100k TNK-BP Trafigura Libya Jan Dubai - $0.55Jan 4-5 100k Surgutneftegaz Gunvor Ashahda Jan 10-11 100k Surgutneftegaz Gunvor Pacific Energy Jan 15-16 100k Rosneft IPP OY Moscow University Jan Dubai - $2Jan 18-19 100k Rosneft IPP OY Ashahda Jan Dubai - $2.1Jan 21-22 100k Rosneft IPP OY Atlantic Explorer Jan Dubai - $2Jan 24-25 100k Rosneft IPP OY Sky Lady Jan Dubai - $1.16Jan 27-28 100k Rosneft IPP OY Bunga Kelana 7 Jan Dubai - $0.95Jan 30-31 100k Gazprom Neft Mitsubishi KWK Esteem Jan Dubai - $0.75 (CIF North Asia basis)Feb 2-3 100k Surgutneftegaz Gunvor Feb 5-6 100k TNK-BP BP British Vine Feb Dubai - $2Feb 8-9 100k Rosneft Mitsubishi Torm Gudrun Feb Dubai - $1.3Feb 10-11 100k Surgutneftegaz Gunvor Bunga Kelana 4 Feb 12-13 100k Rosneft Crudex Atlas Explorer Feb Dubai - $1.25Feb 15-16 100k Rosneft Vitol Bunga Kelana 4 Feb Dubai + $0.02Feb 18-19 100k Rosneft Petronas Oasis River Feb Dubai + $0.2Feb 21-22 100k Rosneft Crudex Feb Dubai + $0.25Feb 24-25 100k TNK-BP BP Castor Voyager Feb Dubai + $0.80Feb 27-28 100k Gazprom Neft Mitsubishi Maersk Phoenix Feb Dubai + $1.10 (CIF North Asia basis)Mar 1-2 100k Rosneft Crudex Ruby Mar Dubai + $0.29Mar 5-6 145k Surgutneftegaz Gunvor Pacific Virgo Mar 7-8 100k Rosneft Crudex Mar Dubai - $1.25Mar 9-10 100k Gazprom Neft Gunvor Jag Lyall Mar Dubai + $0.35Mar 12-13 100k Rosneft Crudex Mar Dubai - $0.78Mar 14-15 100k Rosneft Crudex Mar Dubai - $0.21Mar 17-18 100k Rosneft Unipec Bai Lu Zhou Mar Dubai + $0.12Mar 19-20 100k Surgutneftegaz Gunvor Mar Dubai plus small premiumMar 22-23 100k TNK-BP BP Mar 24-25 100k TNK-BP Mitsubishi Mar 27-28 100k Rosneft Crudex Al Qadisia Mar Dubai + $0.15Mar 30-31 100k Rosneft Crudex Al Buhaira Mar Dubai + $0.24Apr 1-2 100k Rosneft Crudex Apr Dubai + $0.04Apr 4-5 100k Surgutneftegaz Gunvor British Swift Apr 6-7 100k Rosneft Chevron BM Bonanza Apr Dubai + $0.14Apr 8-9 100k Rosneft Crudex Amba Bhakti Apr Dubai - $0.46Apr 11-12 100k Rosneft Crudex CSK Valiant Apr Dubai - $0.75Apr 13-14 100k Rosneft BP Apr Dubai - $0.25Apr 15-16 100k Gazprom Neft Gunvor TH Sound Apr Dubai + $0.20/$0.30Apr 18-19 100k TNK-BP Gunvor Amba Bhakti Apr 20-21 100k Surgutneftegaz Talmay NS Commander Apr 22-23 100k Rosneft Mitsubishi Apr Dubai - $0.64Apr 24-25 100k Rosneft Vitol Badr Apr Dubai - $0.55Apr 27-28 100k TNK-BP Mitsubishi New Amity Apr 29-30 100k Gazprom Neft SK Energy May 1-2 100k Rosneft Mitsubishi May Dubai - $0.32May 3-4 100k Surgutneftegaz Lukoil North Sea Jun Dubai - $0.40May 5-6 100k Rosneft BP Monterey May Dubai -$1.49May 8-9 100k Rosneft Shell NS Commander May Dubai -$0.81May 10-11 100k Rosneft Shell Desh Prem May Dubai -$0.75May 12-13 100k Rosneft Shell May Dubai -$0.68May 15-16 100k Gazprom Neft Mitsubishi May Dubai plus small discountMay 17-18 100k Surgutneftegaz SK Energy Maersk Phoenix May Dubai -$1.40/-$1.35May 20-21 100k TNK-BP BP Asian Jade/Zaliv Amursky May 23-24 100k Rosneft Vitol Okeanis May Dubai -$1.26May 25-26 100k Rosneft Chevron Asian Jade May Dubai -$1.03May 27-28 100k TNK-BP May 29-30 100k Gazprom Neft Mitsubishi Rich Queen II May Dubai plus small premiumMay 30-31 100k Surgutneftegaz Vitol May Dubai -$1.50/-$1.40Jun 2-3 100k Rosneft RBS Sempra Carmel Jun Dubai -$1.10Jun 4-5 100k Rosneft RBS Sempra Aijalaa Jun Dubai -$1.10Jun 6-10 100k Rosneft BP Jun Dubai -$1.47Jun 8-12 100k Rosneft BP Jun Dubai -$1.37Jun 10-14 100k Rosneft Sentosa River Jun Dubai -$1.25Jun 12-15 100k Surgutneftegaz Itochu Jun Dubai -$0.90Jun 15-18 100k Gazprom Neft Jun 17-20 100k TNK-BP BP Jun 19-22 100k TNK-BP Mitsubishi New Accord Jun 21-25 100k Surgutneftegaz Glencore Jun Dubai -$0.80Jun 24-27 100k Gazprom Neft Mitsubishi Os Breeze Jun 26-29 100k TNK-BP

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

| 9

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

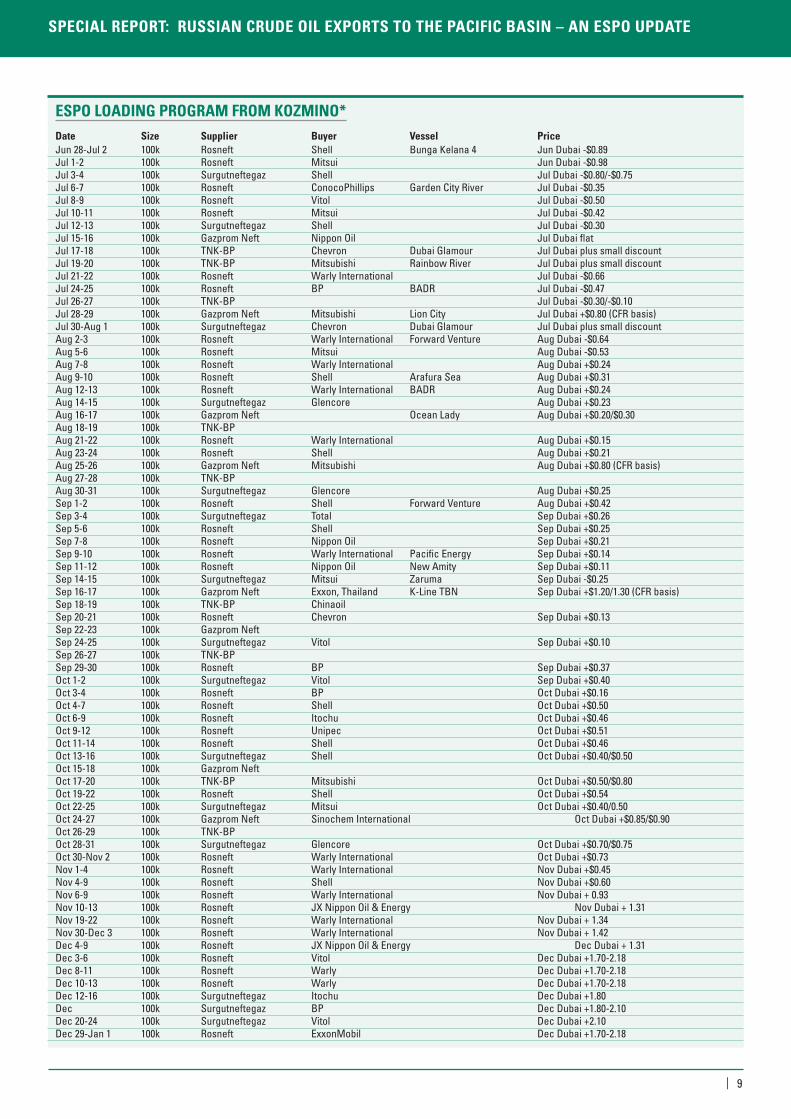

Jun 28-Jul 2 100k Rosneft Shell Bunga Kelana 4 Jun Dubai -$0.89Jul 1-2 100k Rosneft Mitsui Jun Dubai -$0.98Jul 3-4 100k Surgutneftegaz Shell Jul Dubai -$0.80/-$0.75Jul 6-7 100k Rosneft ConocoPhillips Garden City River Jul Dubai -$0.35Jul 8-9 100k Rosneft Vitol Jul Dubai -$0.50Jul 10-11 100k Rosneft Mitsui Jul Dubai -$0.42Jul 12-13 100k Surgutneftegaz Shell Jul Dubai -$0.30Jul 15-16 100k Gazprom Neft Nippon Oil Jul Dubai flatJul 17-18 100k TNK-BP Chevron Dubai Glamour Jul Dubai plus small discountJul 19-20 100k TNK-BP Mitsubishi Rainbow River Jul Dubai plus small discountJul 21-22 100k Rosneft Warly International Jul Dubai -$0.66Jul 24-25 100k Rosneft BP BADR Jul Dubai -$0.47Jul 26-27 100k TNK-BP Jul Dubai -$0.30/-$0.10Jul 28-29 100k Gazprom Neft Mitsubishi Lion City Jul Dubai +$0.80 (CFR basis)Jul 30-Aug 1 100k Surgutneftegaz Chevron Dubai Glamour Jul Dubai plus small discountAug 2-3 100k Rosneft Warly International Forward Venture Aug Dubai -$0.64Aug 5-6 100k Rosneft Mitsui Aug Dubai -$0.53Aug 7-8 100k Rosneft Warly International Aug Dubai +$0.24Aug 9-10 100k Rosneft Shell Arafura Sea Aug Dubai +$0.31Aug 12-13 100k Rosneft Warly International BADR Aug Dubai +$0.24Aug 14-15 100k Surgutneftegaz Glencore Aug Dubai +$0.23Aug 16-17 100k Gazprom Neft Ocean Lady Aug Dubai +$0.20/$0.30 Aug 18-19 100k TNK-BP Aug 21-22 100k Rosneft Warly International Aug Dubai +$0.15Aug 23-24 100k Rosneft Shell Aug Dubai +$0.21Aug 25-26 100k Gazprom Neft Mitsubishi Aug Dubai +$0.80 (CFR basis)Aug 27-28 100k TNK-BP Aug 30-31 100k Surgutneftegaz Glencore Aug Dubai +$0.25Sep 1-2 100k Rosneft Shell Forward Venture Aug Dubai +$0.42Sep 3-4 100k Surgutneftegaz Total Sep Dubai +$0.26Sep 5-6 100k Rosneft Shell Sep Dubai +$0.25Sep 7-8 100k Rosneft Nippon Oil Sep Dubai +$0.21Sep 9-10 100k Rosneft Warly International Pacific Energy Sep Dubai +$0.14Sep 11-12 100k Rosneft Nippon Oil New Amity Sep Dubai +$0.11Sep 14-15 100k Surgutneftegaz Mitsui Zaruma Sep Dubai -$0.25Sep 16-17 100k Gazprom Neft Exxon, Thailand K-Line TBN Sep Dubai +$1.20/1.30 (CFR basis)Sep 18-19 100k TNK-BP Chinaoil Sep 20-21 100k Rosneft Chevron Sep Dubai +$0.13Sep 22-23 100k Gazprom Neft Sep 24-25 100k Surgutneftegaz Vitol Sep Dubai +$0.10Sep 26-27 100k TNK-BP Sep 29-30 100k Rosneft BP Sep Dubai +$0.37Oct 1-2 100k Surgutneftegaz Vitol Sep Dubai +$0.40 Oct 3-4 100k Rosneft BP Oct Dubai +$0.16Oct 4-7 100k Rosneft Shell Oct Dubai +$0.50Oct 6-9 100k Rosneft Itochu Oct Dubai +$0.46Oct 9-12 100k Rosneft Unipec Oct Dubai +$0.51Oct 11-14 100k Rosneft Shell Oct Dubai +$0.46Oct 13-16 100k Surgutneftegaz Shell Oct Dubai +$0.40/$0.50Oct 15-18 100k Gazprom Neft Oct 17-20 100k TNK-BP Mitsubishi Oct Dubai +$0.50/$0.80Oct 19-22 100k Rosneft Shell Oct Dubai +$0.54Oct 22-25 100k Surgutneftegaz Mitsui Oct Dubai +$0.40/0.50Oct 24-27 100k Gazprom Neft Sinochem International Oct Dubai +$0.85/$0.90Oct 26-29 100k TNK-BP Oct 28-31 100k Surgutneftegaz Glencore Oct Dubai +$0.70/$0.75Oct 30-Nov 2 100k Rosneft Warly International Oct Dubai +$0.73Nov 1-4 100k Rosneft Warly International Nov Dubai +$0.45Nov 4-9 100k Rosneft Shell Nov Dubai +$0.60Nov 6-9 100k Rosneft Warly International Nov Dubai + 0.93Nov 10-13 100k Rosneft JX Nippon Oil & Energy Nov Dubai + 1.31Nov 19-22 100k Rosneft Warly International Nov Dubai + 1.34Nov 30-Dec 3 100k Rosneft Warly International Nov Dubai + 1.42Dec 4-9 100k Rosneft JX Nippon Oil & Energy Dec Dubai + 1.31Dec 3-6 100k Rosneft Vitol Dec Dubai +1.70-2.18Dec 8-11 100k Rosneft Warly Dec Dubai +1.70-2.18Dec 10-13 100k Rosneft Warly Dec Dubai +1.70-2.18Dec 12-16 100k Surgutneftegaz Itochu Dec Dubai +1.80Dec 100k Surgutneftegaz BP Dec Dubai +1.80-2.10Dec 20-24 100k Surgutneftegaz Vitol Dec Dubai +2.10Dec 29-Jan 1 100k Rosneft ExxonMobil Dec Dubai +1.70-2.18

ESPO LOADING PROGRAM FROM KOzMINO*Date Size Supplier Buyer Vessel Price

10 |

SPECIAL REPORT: RUSSIAN CRUDE OIL EXPORTS TO THE PACIFIC BASIN – AN ESPO UPDATE

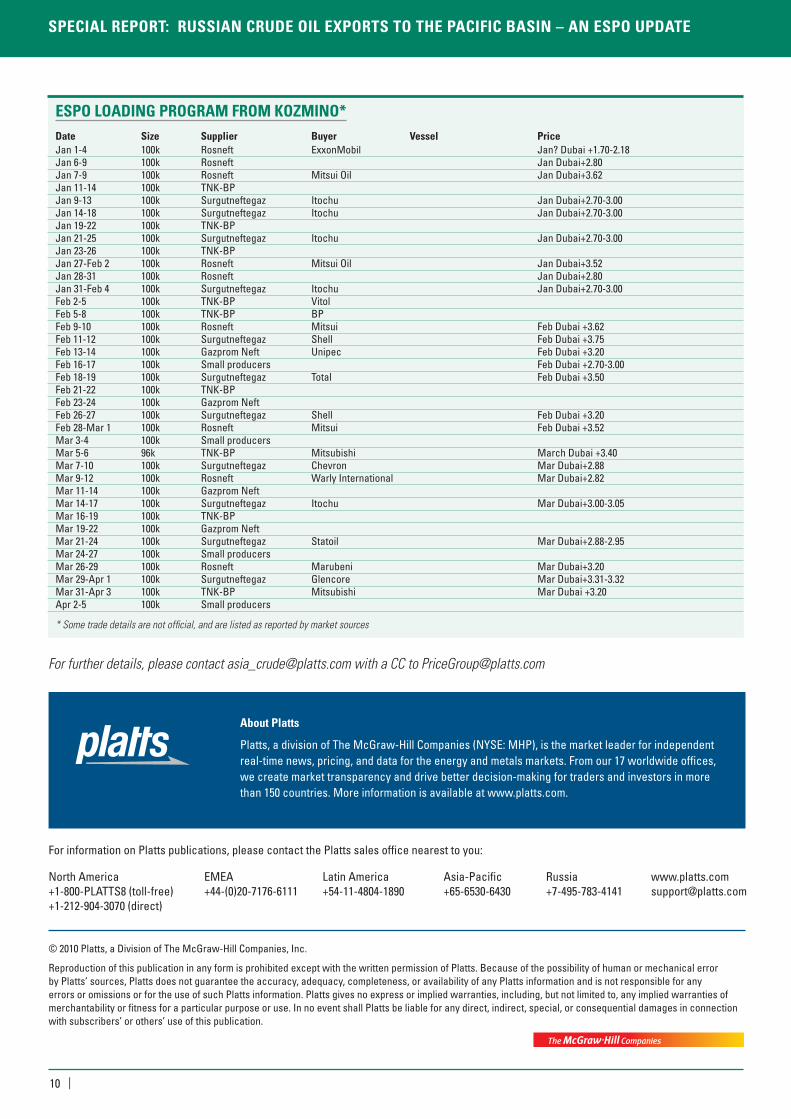

Jan 1-4 100k Rosneft ExxonMobil Jan? Dubai +1.70-2.18Jan 6-9 100k Rosneft Jan Dubai+2.80Jan 7-9 100k Rosneft Mitsui Oil Jan Dubai+3.62Jan 11-14 100k TNK-BP Jan 9-13 100k Surgutneftegaz Itochu Jan Dubai+2.70-3.00Jan 14-18 100k Surgutneftegaz Itochu Jan Dubai+2.70-3.00Jan 19-22 100k TNK-BP Jan 21-25 100k Surgutneftegaz Itochu Jan Dubai+2.70-3.00Jan 23-26 100k TNK-BP Jan 27-Feb 2 100k Rosneft Mitsui Oil Jan Dubai+3.52Jan 28-31 100k Rosneft Jan Dubai+2.80Jan 31-Feb 4 100k Surgutneftegaz Itochu Jan Dubai+2.70-3.00Feb 2-5 100k TNK-BP Vitol Feb 5-8 100k TNK-BP BP Feb 9-10 100k Rosneft Mitsui Feb Dubai +3.62Feb 11-12 100k Surgutneftegaz Shell Feb Dubai +3.75Feb 13-14 100k Gazprom Neft Unipec Feb Dubai +3.20Feb 16-17 100k Small producers Feb Dubai +2.70-3.00Feb 18-19 100k Surgutneftegaz Total Feb Dubai +3.50Feb 21-22 100k TNK-BP Feb 23-24 100k Gazprom Neft Feb 26-27 100k Surgutneftegaz Shell Feb Dubai +3.20Feb 28-Mar 1 100k Rosneft Mitsui Feb Dubai +3.52Mar 3-4 100k Small producers Mar 5-6 96k TNK-BP Mitsubishi March Dubai +3.40Mar 7-10 100k Surgutneftegaz Chevron Mar Dubai+2.88Mar 9-12 100k Rosneft Warly International Mar Dubai+2.82 Mar 11-14 100k Gazprom Neft Mar 14-17 100k Surgutneftegaz Itochu Mar Dubai+3.00-3.05Mar 16-19 100k TNK-BP Mar 19-22 100k Gazprom Neft Mar 21-24 100k Surgutneftegaz Statoil Mar Dubai+2.88-2.95Mar 24-27 100k Small producers Mar 26-29 100k Rosneft Marubeni Mar Dubai+3.20Mar 29-Apr 1 100k Surgutneftegaz Glencore Mar Dubai+3.31-3.32Mar 31-Apr 3 100k TNK-BP Mitsubishi Mar Dubai +3.20Apr 2-5 100k Small producers

* Some trade details are not official, and are listed as reported by market sources

ESPO LOADING PROGRAM FROM KOzMINO*Date Size Supplier Buyer Vessel Price

© 2010 Platts, a Division of The McGraw-Hill Companies, Inc.

Reproduction of this publication in any form is prohibited except with the written permission of Platts. Because of the possibility of human or mechanical error by Platts’ sources, Platts does not guarantee the accuracy, adequacy, completeness, or availability of any Platts information and is not responsible for any errors or omissions or for the use of such Platts information. Platts gives no express or implied warranties, including, but not limited to, any implied warranties of merchantability or fitness for a particular purpose or use. In no event shall Platts be liable for any direct, indirect, special, or consequential damages in connection with subscribers’ or others’ use of this publication.

About Platts

Platts, a division of The McGraw-Hill Companies (NYSE: MHP), is the market leader for independent real-time news, pricing, and data for the energy and metals markets. From our 17 worldwide offices, we create market transparency and drive better decision-making for traders and investors in more than 150 countries. More information is available at www.platts.com.

For information on Platts publications, please contact the Platts sales office nearest to you:

North America EMEA Latin America Asia-Pacific Russia www.platts.com +1-800-PLATTS8 (toll-free) +44-(0)20-7176-6111 +54-11-4804-1890 +65-6530-6430 +7-495-783-4141 [email protected] +1-212-904-3070 (direct)

For further details, please contact [email protected] with a CC to [email protected]